Form N-CSR/A ETF Series Solutions For: Feb 28

Tweet

Tweet Share

ShareAs filed with the U.S. Securities and Exchange Commission on May 26, 2022

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22668

ETF Series Solutions

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Kristina R. Nelson

ETF Series Solutions

615 East Michigan Street

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 765-6076

Registrant's telephone number, including area code

Date of fiscal year end: February 28

Date of reporting period: February 28, 2022

Item 1. Reports to Stockholders.

(a)

Hoya Capital Housing ETF

Ticker: HOMZ

Hoya Capital High Dividend Yield ETF

Ticker: RIET

Annual Report

February 28, 2022

Hoya Capital ETFs

TABLE OF CONTENTS

Page |

|

Letter to Shareholders |

1 |

Performance Summary |

8 |

Portfolio Allocations |

10 |

Schedules of Investments |

16 |

Statements of Assets and Liabilities |

20 |

Statements of Operations |

21 |

Statements of Changes in Net Assets |

22 |

Financial Highlights |

24 |

Notes to Financial Statements |

26 |

Report of Independent Registered Public Accounting Firm |

36 |

Trustees and Officers |

38 |

Expense Examples |

41 |

Review of Liquidity Risk Management Program |

43 |

Approval of Advisory Agreement & Board Consideration |

44 |

Federal Tax Information |

50 |

Information About Portfolio Holdings |

50 |

Information About Proxy Voting |

51 |

Frequency Distribution of Premiums and Discounts |

51 |

Hoya Capital ETFs

Letter to Shareholders

(Unaudited)

Dear Shareholders,

On behalf of the entire Hoya Capital Real Estate team, we want to express our gratitude for the confidence you have placed in the Hoya Capital Housing ETF (“HOMZ” or the “Fund”). The following information pertains to the period from March 1, 2021 through February 28, 2022 (the “current fiscal period”).

HOMZ offers diversified exposure across the U.S. housing sector, one of the largest and most critical asset classes in the world. The Fund seeks to track the total return performance, before fees and expenses, of the Hoya Capital Housing 100TM Index (the “Index”). The Index is a rules-based index designed to track the 100 companies that collectively represent the performance of the U.S. Housing Industry including homebuilders, residential real estate investment trusts (“REITs”), home improvement companies, and real estate services and technology firms.

During this current fiscal period, the market value and net asset value (“NAV”) for HOMZ generated a cumulative total return of 14.16% and 14.60%, respectively, compared to a return of 7.98% on the S&P MidCap 400® Index and 16.39% on the S&P 500® Index. The Hoya Capital Housing 100TM Index increased 15.24% during the current fiscal period. Meanwhile, outstanding shares ended the current fiscal period at 1,600,000.

The U.S. Housing Industry emerged as a leader of the early post-pandemic economic recovery during the current fiscal period as key housing market indicators exhibited a sharp rebound in the back-half of 2020 and throughout 2021 following a slowdown at the outset of the coronavirus pandemic. During this period of significant uncertainty, consumers exhibited a propensity to prioritize housing-related investments and has reinforced the belief among many Americans that “there’s no place like home.”

During the current fiscal period, the Residential Real Estate Investment Trusts (“REITs”) and the Home Improvement Retailers sectors were the leading contributor to the Fund’s performance. For Residential REITs, demand for both apartments1 and single-family rental homes2 hit the highest level on record in 2021, resulting in the strongest pace of national rent growth and the lowest-level of vacancy rates on record. Rents rose in all 50 of the nation’s largest markets with the fastest annual rent growth observed across the Sunbelt.3

Meanwhile, the Home Improvement Retailers sector benefited from pandemic driven home-centric behavioral changes in which consumers – particularly those with work-from-home and remote-study arrangements - invested heavily in home improvement. Strong growth in personal incomes also drove accelerated spending on previously-deferred home repair and remodeling activity, a trend that we expect to continue given the aging of the American housing stock, a byproduct of low levels of new home construction activity in the 2010s.

1

Hoya Capital ETFs

Letter to Shareholders

(Unaudited) (Continued)

Leading detractors during the current fiscal period were the Real Estate Technology, Brokerage & Services and Home Furnishings & Home Goods sectors. For the Real Estate Technology, Brokerage & Services sector - which was among the leading contributors to performance in the prior annual period - performance was negatively impacted by multiple compression across many technology-related equities during the period and by company-specific operational challenges. Notably, Zillow closed its Zillow Offer home-buying business - citing operational challenges and high capital intensity of the iBuying strategy – and noted that it intends to focus on its core property technology business.

For the Home Furnishings & Home Goods sector, performance was negatively impacted by global supply chain disruptions resulting from the lingering effects of the coronavirus pandemic. Furniture, major appliances, mattresses, and cabinetry were among the products facing the most severe shortages, higher prices, and delivery delays, which prompted some consumers to defer these purchases. Despite these shortages and operational challenges, retail spending at Furniture and Home Furnishings Stores still rose 26.9% in 20214 – the highest on record.

More broadly, the current fiscal period saw a notable intensification of the housing shortage in the United States. Existing Home Sales data in February 2022 – the final month of the current fiscal period – showed that supply levels of homes for sale remained near historic lows with inventory down 15.5% from the prior year. Properties were on the market for just 18 days in February, on average, and 84% percent of homes sold were on the market for less than a month.5

Amid this intensifying housing shortage, demographic trends over the next decade are highly supportive of significant growth in housing demand, which we believe will necessitate significantly higher levels of new home construction activity. Additionally, we believe that home-centric behavioral changes resulting from the pandemic – and the increased value and attention that consumers dedicate towards their homes – will exhibit a high degree of persistence, resulting in higher sustained levels of investments on home improvement and physical space upgrades.

We continue to see a compelling long-term investment case for HOMZ over the next decade and beyond as the combination of historically low housing supply, the continued aging of the U.S. housing stock, and strong secular demand provide a favorable long-term macroeconomic backdrop for companies across the U.S. housing industry – tailwinds that will be enhanced by advancements in property technology which will significantly improve the efficiency, productivity, and margins of the housing industry at large.

2

Hoya Capital ETFs

Letter to Shareholders

(Unaudited) (Continued)

Further, HOMZ is the lowest-cost ETF out of five funds in its ETF Database (“ETFdb”) segment as of the end of the period,6 and given the ever-present uncertainty, we believe that capturing balanced and diversified exposure across the entire housing sector – homebuilders, rental operators, home improvement, and housing technology firms - is optimized to efficiently capture these thematic growth trends.

Thank you once again and we look forward to keeping you well informed.

Sincerely,

Alex Pettee, CFA

President & Director of Research and ETFs

Hoya Capital Real Estate, Adviser to the Fund

Must be preceded or accompanied by a prospectus.

Investing involves risks. Principal loss is possible. The Fund is not actively managed. The Fund’s investments will be concentrated in housing and real estate-related industries. Investments in real estate companies and the construction and housing industry involve unique risks. Real estate companies, including REITs, may have limited financial resources, may trade less frequently and in limited volume, and may be more volatile than other securities. Many factors may affect real estate values, including the availability of mortgages and changes in interest rates. Real estate companies are also subject to heavy cash flow dependency, defaults by borrowers, and self-liquidation. The construction and housing industry can be significantly affected by the real estate markets. Compared to large cap companies, small and mid- capitalizations companies may be less stable, and their securities may be more volatile and less liquid. As with all ETFs, Shares may be bought and sold in the secondary market at market prices and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. Although it is expected that the market price of Shares will approximate the Fund’s NAV, there may be times when the market price of Shares is more than the NAV intra-day (premium) or less than the NAV intra-day (discount) due to supply and demand of Shares or during periods of market volatility.

Short term performance, in particular, is not a good indication of the Fund’s future performance, and an investment should not be made based solely on returns.

The S&P 500® Index is a broad-based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. You cannot invest directly in an index.

The S&P Mid-Cap 400® Index, also known as the S&P 400 Index, is a broad-based unmanaged index of approximately 400 mid-capitalization stocks which is widely recognized as representative of the mid-cap segment of the U.S. equity market.

1 RealPage Analytics. “Apartment Demand Hit A Record in 2021.” January 10, 2022. https://www.realpage.comThen/analytics/apartment-demand-hits-a-record-in-2021/

2 CoreLogic Intelligence. “Single-Family Annual Rent Growth Finishes 2021 at New Record.” February 15, 2022. https://www.realpage.com/analytics/apartment-demand-hits-a-record-in-2021/

3 Zillow Research. “December 2021 Market Report.” January 20, 2022. https://www.zillow.com/research/december-2021-market-report-30530/

4 US Census Bureau, Advanced Retail Sales: Furniture & Home Furnishing Stores. March 16, 2022. https://fred.stlouisfed.org/series/RSFHFS

3

Hoya Capital ETFs

Letter to Shareholders

(Unaudited) (Continued)

5 Existing Home Inventory: National Association of Realtors, Existing Home Sales, February 2022 (Release Date: March 19, 2022). Inventory indicates the number of properties marked as active on the market. When a seller lists a property, it becomes counted as inventory. Inventory is calculated monthly by taking a count of the number of active listings on the last day of the month.

6 Lowest expense ratio out of 5 US-registered ETFs in the ETFdb Homebuilders ETF Segment as of 2/28/2022. Expense ratio data for other ETFs were obtained from the funds’ prospectuses, data pulled as of 2/28/2022. ETFs in the same ETFdb segment may track different indexes, have differences in holdings, and show different performance.

Past performance does not guarantee future results.

The Hoya Capital Housing 100TM Index is a rules-based index composed of the 100 companies that collectively represent the performance of the US Housing Industry. The index is designed to track total annual spending on housing and housing-related services across the United States. The Index is divided into four US Housing Industry Business Segments, weighted based on their relative contribution to GDP: 1) Home Ownership and Rental Operators; 2) Home Building and Construction; 3) Home Improvement and Furnishings; 4) Home Financing, Technology & Services.

Diversification does not assure a profit or protect against loss in a declining market.

Hoya Capital Real Estate, LLC is the advisor to HOMZ, which is distributed by Quasar Distributors, LLC.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice.

Fund holdings and sector allocations are subject to change and are not recommendations to buy or sell any security. Please refer to the Schedule of Investments in the report for a complete list of fund holdings.

4

Hoya Capital ETFs

Letter to Shareholders

(Unaudited) (Continued)

Dear Shareholders,

On behalf of the entire Hoya Capital Real Estate team, we want to express our gratitude for the confidence you have placed in the Hoya Capital High Dividend Yield ETF (“RIET” or the “Fund”). The following information pertains to the period from September 21, 2021 through February 28, 2022 (the “current fiscal period”).

RIET offers diversified exposure to select high-dividend yielding securities across the U.S. real estate sector. The Fund seeks to track the performance, before fees and expenses, of the Hoya Capital High Dividend Yield Index (“the Index”), a rules-based index that is designed to provide diversified exposure to 100 U.S. exchange-listed common and preferred securities that collectively provide income through high dividend yields.

The multi-factor selection process incorporates a quality screen to identify companies with lower leverage profiles and begins with the selection of “Dividend Champions.” Securities are then selected based principally on dividend yield across 14 property sectors and 3 market capitalization tiers. Real estate securities include exchange-listed common stocks, exchange-listed preferred stocks and other exchange-listed equity securities issued by U.S. real estate companies, including real estate investment trusts (“REITs”) and similar REIT-like entities.

During this current fiscal period, the market value and net asset value (“NAV”) for RIET generated a cumulative total return of -1.24% and -1.35%, respectively, compared to a return of -2.89% on the Dow Jones U.S. Real Estate Index (the “Benchmark”). The Hoya Capital High Dividend Yield Index (the “Index”) returned -2.28% during the current fiscal period. Meanwhile, outstanding shares ended the current fiscal period at 1,530,000.

During the current fiscal period, the Small-Cap REIT and Dividend Champion categories were the leading upside contributors to the fund’s performance. The Small-Cap REIT category benefited from merger and acquisitions (“M&A”) activity - which was a major theme across the U.S. real estate sector during the period - with Blackstone announcing acquisitions of two fund holdings during the period - Preferred Apartment Communities and Bluerock Residential Growth. Based on our research, there were 20 major M&A deals involving U.S. publicly-traded REITs during the fiscal period, one of the most active periods of REIT M&A in history.

The Dividend Champions category benefited from strong earnings growth and a historic wave of dividend increases across the U.S. real estate sector with more than half of all U.S. REITs raising their dividend rates in 2021, including six of the ten Dividend Champions in RIET. REIT earnings, measured by funds from operations (“FFO”) for all equity REITs, rose 24.6% from 2020 to 2021, according to NAREIT, which exceeded its pre-pandemic level. Total dividend distributions lagged FFO growth during the period, resulting in dividend payout ratios that are significantly below their historic average.1

5

Hoya Capital ETFs

Letter to Shareholders

(Unaudited) (Continued)

The leading detractors during the current fiscal period were Mid-Cap REITs and Large-Cap REITs. For Mid-Cap REITs, the rise in long-term interest rates and inflation expectations during the period resulted in underperformance among companies in the more “rate-sensitive” property sectors including Net Lease, Specialty, and Healthcare. These property sectors tend to utilize longer lease terms compared with other property sectors and thus, typically have a more limited ability to raise rents on individual leases to keep pace with inflation on a year-by-year basis. The underperformance from these property sectors was partially offset by stronger performance from companies in more “pro-cyclical” property sectors including office, retail, and commercial financing which tend to demonstrate a higher degree of inflation protection.

The Large-Cap REIT category, meanwhile, was negatively impacted by similar themes related to rising interest rates as the Mid-Cap REIT category, as well as underperformance from the companies in the Home Financing property sector resulting from elevated levels of interest rate volatility amid uncertainty over Federal Reserve monetary policy, geopolitical concerns, and the coronavirus global pandemic.

More broadly, a rotation from “growth-to-value” across the U.S. real estate sector in the period led to outperformance from more value-oriented property sectors and underperformance from several of the more growth-focused property sectors including technology and infrastructure, which also explained some of the Fund’s outperformance relative to the Benchmark during the period.

We continue to see a compelling long-term investment case for RIET, particularly for investors seeking diversified exposure to real, income-producing assets in the United States which provide the potential for reliable monthly income and inflation-hedging in an otherwise uncertain macroeconomic and geopolitical environment.

Further, the diligently researched rules-driven selection process of the Index reflects an “income-first” objective and is grounded in the core principals of balanced diversification and limited single-stock risk, which we believe provides both innovative and optimized exposure to high income-producing securities in a simple, accessible, and cost-effective package.

Thank you once again and we look forward to keeping you well informed.

Sincerely,

Alex Pettee, CFA

President & Director of Research and ETFs

Hoya Capital Real Estate, Adviser to the Fund

6

Hoya Capital ETFs

Letter to Shareholders

(Unaudited) (Continued)

Must be preceded or accompanied by a prospectus.

Investing involves risks. Principal loss is possible. The fund is passively managed and attempts to mirror the composition and performance of the Hoya Capital High Dividend Yield Index. The Fund’s returns may not match due to expenses incurred by the Fund or lack of precise correlation with the index and may at times not hold or be fully invested in the same securities as the index. The Fund’s investments will be concentrated in real estate-related industries. Investments in real estate companies involve unique risks. Real estate companies, including REITs, may have limited financial resources, may trade less frequently and in limited volume, and may be more volatile than other securities. Many factors may affect real estate values, including the availability of mortgages and changes in interest rates. Real estate companies are also subject to heavy cash flow dependency, defaults by borrowers, and self-liquidation. Preferred stocks may decline in price, fail to pay dividends, or be illiquid. Compared to large cap companies, small and mid-capitalizations companies may be less stable and their securities may be more volatile and less liquid. The Fund is new with no track record to evaluate. The fund seeks to maintain relatively consistent monthly distributions; however, because the amount of income earned by the Fund varies from month-to-month, the Fund’s distributions may be more or less than the actual amount of income earned in that period and may include income, return of capital, and capital gains. Distributions for funds investing in real estate investment trusts (REITs) may later be characterized as capital gains and/or a return of capital, depending on the character of the dividends reported to each fund after year-end by REITs held by a fund. The final tax treatment of these distributions will be reported to shareholders after the close of each fiscal year on form 1099-DIV.

Short term performance, in particular, is not a good indication of the Fund’s future performance, and an investment should not be made based solely on returns.

The Dow Jones U.S. Real Estate Index is designed to track the performance of real estate investment trusts (REIT) and other companies that invest directly or indirectly in real estate through development, management, or ownership, including property agencies.

1 NAREIT’s REIT Industry Update, March 4, 2022. Funds from operations (FFO) refers to the figure used by real estate investment trusts (REITs) to define the cash flow from their operations. Real estate companies use FFO as a measurement of operating performance.

Past performance does not guarantee future results.

The Hoya Capital High Dividend Yield Index seeks to provide diversified exposure to 100 of the highest dividend yielding real estate securities in the United States, utilizing a rules-based methodology to select U.S. exchange-listed real estate securities that collectively provide income through high dividend yields. Securities are selected to the Index through a multi-factor, tier-weighted process that selects components based principally on dividend yield, subject to diversification requirements across property sectors and market capitalizations, and subject to minimum liquidity requirements. Real estate securities include exchange-listed common stocks, exchange-listed preferred stocks and other exchange-listed equity securities issued by U.S. real estate companies, including real estate investment trusts (REITs) and similar REIT-like entities.

Diversification does not assure a profit or protect against loss in a declining market.

Hoya Capital Real Estate, LLC is the advisor to RIET which is distributed by Quasar Distributors, LLC.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice.

Fund holdings and sector allocations are subject to change and are not recommendations to buy or sell any security. Please refer to the Schedule of Investments in the report for a complete list of fund holdings.

7

Hoya Capital Housing ETF

Performance Summary

(Unaudited)

Growth of $10,000

Average Annual Returns |

1 Year |

Since |

Hoya Capital Housing ETF - NAV |

14.60% |

19.51% |

Hoya Capital Housing ETF - Market |

14.16% |

19.48% |

Hoya Capital Housing 100TM Index |

15.24% |

20.09% |

S&P 500® Index |

16.39% |

17.87% |

This chart illustrates the performance of a hypothetical $10,000 investment made on March 19, 2019 and is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The chart assumes reinvestment of capital gains and dividends.

The performance data quoted represents past performance. Past performance does not guarantee future results. Returns for periods of less than one year are not annualized. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance current to most recent month end, please visit www.thehousingetf.com. Gross expense ratio as of the summary prospectus 06/30/21 was 0.30%.

8

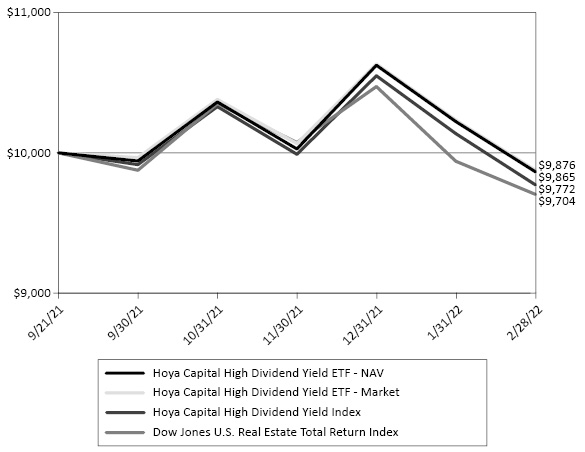

Hoya Capital High Dividend Yield ETF

Performance Summary

(Unaudited)

Growth of $10,000

Cumulative Returns |

Since |

Hoya Capital High Dividend Yield ETF - NAV |

-1.35% |

Hoya Capital High Dividend Yield ETF - Market |

-1.24% |

Hoya Capital High Dividend Yield Index |

-2.28% |

Dow Jones U.S. Real Estate Total Return Index |

-2.89% |

This chart illustrates the performance of a hypothetical $10,000 investment made on September 21, 2021 and is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The chart assumes reinvestment of capital gains and dividends.

The performance data quoted represents past performance. Past performance does not guarantee future results. Returns for periods of less than one year are not annualized. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance current to most recent month end, please visit www.TheIncomeETF.com/RIET. Gross expense ratio as of the summary prospectus 09/21/21 was 0.50%.

9

Hoya Capital ETFs

Portfolio Allocations

As of February 28, 2022 (Unaudited)

Hoya Capital Housing ETF |

|

Sector |

Percent of |

Residential REITs & Real Estate Operators (a) |

32.4% |

Home Building Products & Materials |

14.6 |

Homebuilders |

14.3 |

Home Furnishings & Home Goods |

12.4 |

Mortgage Lenders & Servicers |

10.6 |

Property, Title & Mortgage Insurance |

6.0 |

Home Improvement Retailers |

5.5 |

Real Estate Technology, Brokerage & Services |

3.5 |

Short-Term Investments |

0.6 |

Other Assets in Excess of Liabilities |

0.1 |

Total |

100.0% |

Hoya Capital High Dividend Yield ETF |

|

Sector |

Percent of |

Small-Cap REITs (b) |

30.0% |

Mid-Cap REITs (b) |

29.4 |

Large-Cap REITs |

15.0 |

Dividend Champions |

14.5 |

Preferred Stocks |

10.0 |

Short-Term Investments |

1.0 |

Other Assets in Excess of Liabilities |

0.1 |

Total |

100.0% |

(a) |

The Index, and consequently the Fund, is expected to concentrate its investments in the U.S. residential housing industry. The value of the Fund’s shares may rise and fall more than the value of shares of a fund that invests in securities of companies in a broader range of industries. See Note 7 in Notes to Financial Statements. |

(b) |

The Index, and consequently the Fund, is expected to concentrate its investments in real estate-related industries. The value of the Fund’s shares may rise and fall more than the value of shares of a fund that invests in securities of companies in a broader range of industries. See Note 7 in Notes to Financial Statements. |

10

Hoya Capital Housing ETF

Schedule of Investments

February 28, 2022

Shares |

Security Description |

Value |

||||||

COMMON STOCKS — 99.3% |

||||||||

Home Building Products & Materials — 14.6% |

||||||||

| 6,364 | A.O. Smith Corporation |

$ | 436,443 | |||||

| 4,615 | Armstrong World Industries, Inc. |

407,966 | ||||||

| 9,495 | Beacon Roofing Supply, Inc. (a) |

566,757 | ||||||

| 7,157 | Builders FirstSource, Inc. (a) |

532,624 | ||||||

| 9,561 | Carrier Global Corporation |

429,098 | ||||||

| 1,704 | Cavco Industries, Inc. (a) |

464,561 | ||||||

| 3,198 | Eagle Materials, Inc. |

437,582 | ||||||

| 12,190 | Leggett & Platt, Inc. |

452,005 | ||||||

| 1,634 | Lennox International, Inc. |

436,164 | ||||||

| 7,424 | Louisiana-Pacific Corporation |

534,157 | ||||||

| 7,690 | Masco Corporation |

430,948 | ||||||

| 2,895 | Mohawk Industries, Inc. (a) |

407,558 | ||||||

| 5,725 | Owens Corning |

533,513 | ||||||

| 9,266 | PotlatchDeltic Corporation |

508,703 | ||||||

| 3,269 | PPG Industries, Inc. |

436,248 | ||||||

| 4,354 | Simpson Manufacturing Company, Inc. |

515,992 | ||||||

| 1,875 | TopBuild Corporation (a) |

402,525 | ||||||

| 3,999 | Trex Company, Inc. (a) |

367,268 | ||||||

| 1,715 | Watsco, Inc. |

468,298 | ||||||

| 13,612 | Weyerhaeuser Company |

529,235 | ||||||

| 9,297,645 | ||||||||

Home Furnishings & Home Goods — 12.4% |

||||||||

| 155 | Amazon.com, Inc. (a) |

476,045 | ||||||

| 8,026 | American Woodmark Corporation (a) |

430,033 | ||||||

| 1,003 | Costco Wholesale Corporation |

520,808 | ||||||

| 4,166 | Floor & Decor Holdings, Inc. - Class A (a) |

398,353 | ||||||

| 5,135 | Fortune Brands Home & Security, Inc. |

446,231 | ||||||

| 6,625 | iRobot Corporation (a) |

411,810 | ||||||

| 15,165 | La-Z-Boy, Inc. |

442,515 | ||||||

| 2,950 | Middleby Corporation (a) |

523,979 | ||||||

| 12,967 | MillerKnoll, Inc. |

504,157 | ||||||

| 900 | RH (a) |

361,683 | ||||||

| 1,669 | Sherwin-Williams Company |

439,164 | ||||||

| 6,662 | Sleep Number Corporation (a) |

437,693 | ||||||

| 2,183 | Target Corporation |

436,098 | ||||||

| 12,393 | Tempur Sealy International, Inc. |

409,093 | ||||||

| 3,732 | Walmart, Inc. |

504,417 | ||||||

The accompanying notes are an integral part of these financial statements.

11

Hoya Capital Housing ETF

Schedule OF INVESTMENTS

February 28, 2022 (Continued)

Shares |

Security Description |

Value |

||||||

COMMON STOCKS — 99.3% (Continued) |

||||||||

Home Furnishings & Home Goods — 12.4% (Continued) |

||||||||

| 2,099 | Wayfair, Inc. - Class A (a) |

$ | 295,686 | |||||

| 2,358 | Whirlpool Corporation |

474,595 | ||||||

| 2,573 | Williams-Sonoma, Inc. |

372,725 | ||||||

| 7,885,085 | ||||||||

Home Improvement Retailers — 5.5% |

||||||||

| 5,139 | Home Depot, Inc. |

1,623,050 | ||||||

| 8,328 | Lowe’s Companies, Inc. |

1,840,988 | ||||||

| 3,464,038 | ||||||||

Homebuilders — 14.3% |

||||||||

| 10,310 | DR Horton, Inc. |

880,474 | ||||||

| 23,861 | KB Home |

921,273 | ||||||

| 9,476 | Lennar Corporation - Class A |

851,703 | ||||||

| 20,306 | MDC Holdings, Inc. |

900,368 | ||||||

| 8,841 | Meritage Homes Corporation (a) |

871,546 | ||||||

| 197 | NVR, Inc. (a) |

976,813 | ||||||

| 19,836 | PulteGroup, Inc. |

985,056 | ||||||

| 31,323 | Taylor Morrison Home Corporation (a) |

924,028 | ||||||

| 15,873 | Toll Brothers, Inc. |

861,269 | ||||||

| 40,065 | Tri Pointe Homes, Inc. (a) |

896,254 | ||||||

| 9,068,784 | ||||||||

Mortgage Lenders & Servicers — 10.6% |

||||||||

| 29,098 | AGNC Investment Corporation |

375,655 | ||||||

| 55,298 | Annaly Capital Management, Inc. |

384,874 | ||||||

| 9,816 | Bank of America Corporation |

433,867 | ||||||

| 6,387 | Black Knight, Inc. (a) |

358,885 | ||||||

| 28,018 | Chimera Investment Corporation |

340,979 | ||||||

| 9,170 | Citizens Financial Group, Inc. |

480,692 | ||||||

| 2,131 | First Republic Bank |

369,217 | ||||||

| 28,421 | Huntington Bancshares, Inc. |

441,094 | ||||||

| 2,772 | JPMorgan Chase & Company |

393,070 | ||||||

| 2,888 | M&T Bank Corporation |

526,280 | ||||||

| 41,665 | New Residential Investment Corporation |

432,483 | ||||||

| 2,236 | PNC Financial Services Group, Inc. |

445,523 | ||||||

| 30,235 | Rocket Companies, Inc. - Class A |

390,334 | ||||||

| 7,416 | Truist Financial Corporation |

461,424 | ||||||

| 76,671 | Two Harbors Investment Corporation |

387,955 | ||||||

The accompanying notes are an integral part of these financial statements.

12

Hoya Capital Housing ETF

Schedule OF INVESTMENTS

February 28, 2022 (Continued)

Shares |

Security Description |

Value |

||||||

COMMON STOCKS — 99.3% (Continued) |

||||||||

Mortgage Lenders & Servicers — 10.6% (Continued) |

||||||||

| 9,074 | Wells Fargo & Company |

$ | 484,279 | |||||

| 6,706,611 | ||||||||

Property, Title & Mortgage Insurance — 6.0% |

||||||||

| 4,060 | Allstate Corporation |

496,781 | ||||||

| 8,893 | Fidelity National Financial, Inc. |

423,662 | ||||||

| 6,042 | First American Financial Corporation |

405,056 | ||||||

| 30,900 | MGIC Investment Corporation |

469,062 | ||||||

| 17,926 | Old Republic International Corporation |

472,350 | ||||||

| 4,933 | Progressive Corporation |

522,553 | ||||||

| 21,734 | Radian Group, Inc. |

519,443 | ||||||

| 2,912 | Travelers Companies, Inc. |

500,369 | ||||||

| 3,809,276 | ||||||||

Real Estate Technology, Brokerage & Services — 3.5% |

||||||||

| 5,816 | CoStar Group, Inc. (a) |

354,834 | ||||||

| 17,969 | Matterport, Inc. (a) |

133,150 | ||||||

| 16,215 | RE/MAX Holdings, Inc. - Class A |

480,613 | ||||||

| 29,048 | Realogy Holdings Corporation (a) |

528,093 | ||||||

| 11,264 | Redfin Corporation (a) |

243,640 | ||||||

| 8,578 | Zillow Group, Inc. - Class C (a) |

493,407 | ||||||

| 2,233,737 | ||||||||

Residential REITs & Real Estate Operators — 32.4% (b) |

||||||||

| 19,740 | American Campus Communities, Inc. |

1,062,209 | ||||||

| 25,854 | American Homes 4 Rent - Class A |

982,710 | ||||||

| 19,956 | Apartment Income REIT Corporation |

1,029,929 | ||||||

| 4,325 | AvalonBay Communities, Inc. |

1,031,902 | ||||||

| 6,266 | Camden Property Trust |

1,034,579 | ||||||

| 19,471 | CubeSmart |

938,697 | ||||||

| 12,479 | Equity LifeStyle Properties, Inc. |

931,183 | ||||||

| 12,103 | Equity Residential |

1,032,386 | ||||||

| 2,990 | Essex Property Trust, Inc. |

948,338 | ||||||

| 5,241 | Extra Space Storage, Inc. |

986,094 | ||||||

| 41,416 | Independence Realty Trust, Inc. |

1,046,582 | ||||||

| 25,491 | Invitation Homes, Inc. |

963,560 | ||||||

| 5,065 | Mid-America Apartment Communities, Inc. |

1,036,350 | ||||||

| 13,474 | NexPoint Residential Trust, Inc. |

1,144,886 | ||||||

| 3,180 | Public Storage |

1,128,964 | ||||||

The accompanying notes are an integral part of these financial statements.

13

Hoya Capital Housing ETF

Schedule OF INVESTMENTS

February 28, 2022 (Continued)

Shares |

Security Description |

Value |

||||||

COMMON STOCKS — 99.3% (Continued) |

||||||||

Residential REITs & Real Estate Operators — 32.4% (b) (Continued) |

||||||||

| 5,346 | Sun Communities, Inc. |

$ | 967,626 | |||||

| 74,707 | Tricon Residential, Inc. |

1,111,640 | ||||||

| 18,503 | UDR, Inc. |

1,015,260 | ||||||

| 20,548 | Ventas, Inc. |

1,109,592 | ||||||

| 12,227 | Welltower, Inc. |

1,018,387 | ||||||

| 20,520,874 | ||||||||

TOTAL COMMON STOCKS (Cost $58,788,761) |

62,986,050 | |||||||

SHORT-TERM INVESTMENTS — 0.6% |

||||||||

| 402,764 | First American Government Obligations Fund - Class X, 0.03% (c) |

402,764 | ||||||

TOTAL SHORT-TERM INVESTMENTS (Cost $402,764) |

402,764 | |||||||

TOTAL INVESTMENTS — 99.9% (Cost $59,191,525) |

63,388,814 | |||||||

Other Assets in Excess of Liabilities — 0.1% |

33,941 | |||||||

NET ASSETS — 100.0% |

$ | 63,422,755 | ||||||

Percentages are stated as a percent of net assets.

The Fund’s security classifications are defined by the Fund’s Adviser.

(a) |

Non-income producing security. |

(b) |

The Index, and consequently the Fund, is expected to concentrate its investments in the U.S. residential housing industry. The value of the Fund’s shares may rise and fall more than the value of shares of a fund that invests in securities of companies in a broader range of industries. See Note 7 in Notes to the Financial Statements. |

(c) |

Rate shown is the annualized seven-day yield as of February 28, 2022. |

REIT - Real Estate Investment Trust

The accompanying notes are an integral part of these financial statements.

14

Hoya Capital High Dividend Yield ETF

Schedule of Investments

February 28, 2022

Shares |

Security Description |

Value |

||||||

COMMON STOCKS — 88.9% |

||||||||

Dividend Champions — 14.5% |

||||||||

| 1,884 | Crown Castle International Corporation |

$ | 313,856 | |||||

| 2,081 | Digital Realty Trust, Inc. |

280,769 | ||||||

| 4,018 | Equity Residential |

342,735 | ||||||

| 1,728 | Extra Space Storage, Inc. |

325,123 | ||||||

| 1,305 | Innovative Industrial Properties, Inc. |

245,940 | ||||||

| 7,427 | Iron Mountain, Inc. |

365,260 | ||||||

| 2,053 | Simon Property Group, Inc. |

282,411 | ||||||

| 7,896 | Vornado Realty Trust |

341,739 | ||||||

| 4,047 | Welltower, Inc. |

337,075 | ||||||

| 4,486 | WP Carey, Inc. |

347,216 | ||||||

| 3,182,124 | ||||||||

Large-Cap REITs — 15.0% |

||||||||

| 21,781 | AGNC Investment Corporation |

281,193 | ||||||

| 41,400 | Annaly Capital Management, Inc. |

288,144 | ||||||

| 11,022 | Blackstone Mortgage Trust, Inc. - Class A |

350,279 | ||||||

| 7,536 | Gaming and Leisure Properties, Inc. |

342,210 | ||||||

| 16,290 | Medical Properties Trust, Inc. |

331,339 | ||||||

| 31,214 | New Residential Investment Corporation |

324,001 | ||||||

| 11,944 | Omega Healthcare Investors, Inc. |

336,462 | ||||||

| 7,519 | Spirit Realty Capital, Inc. |

348,656 | ||||||

| 13,325 | Starwood Property Trust, Inc. |

317,668 | ||||||

| 12,334 | VICI Properties, Inc. |

344,859 | ||||||

| 3,264,811 | ||||||||

Mid-Cap REITs — 29.4% |

||||||||

| 19,665 | Apollo Commercial Real Estate Finance, Inc. |

256,628 | ||||||

| 15,185 | Arbor Realty Trust, Inc. |

273,330 | ||||||

| 19,509 | Brandywine Realty Trust |

260,055 | ||||||

| 13,532 | CareTrust REIT, Inc. |

236,810 | ||||||

| 16,766 | Chimera Investment Corporation |

204,042 | ||||||

| 13,010 | Easterly Government Properties, Inc. |

270,868 | ||||||

| 5,548 | EPR Properties |

276,290 | ||||||

| 9,892 | Four Corners Property Trust, Inc. |

260,951 | ||||||

| 8,669 | Getty Realty Corporation |

238,831 | ||||||

| 18,667 | Global Net Lease, Inc. |

265,258 | ||||||

| 6,049 | Highwoods Properties, Inc. |

263,736 | ||||||

| 12,332 | Industrial Logistics Properties Trust |

275,867 | ||||||

The accompanying notes are an integral part of these financial statements.

15

Hoya Capital High Dividend Yield ETF

Schedule OF INVESTMENTS

February 28, 2022 (Continued)

Shares |

Security Description |

Value |

||||||

COMMON STOCKS — 88.9% (Continued) |

||||||||

Mid-Cap REITs — 29.4% (Continued) |

||||||||

| 13,088 | KKR Real Estate Finance Trust, Inc. |

$ | 280,999 | |||||

| 23,182 | Ladder Capital Corporation |

265,666 | ||||||

| 61,965 | MFA Financial, Inc. |

251,578 | ||||||

| 5,062 | National Health Investors, Inc. |

269,855 | ||||||

| 70,904 | New York Mortgage Trust, Inc. |

248,873 | ||||||

| 15,091 | PennyMac Mortgage Investment Trust |

235,420 | ||||||

| 15,385 | Physicians Realty Trust |

250,160 | ||||||

| 14,783 | Piedmont Office Realty Trust, Inc. |

251,902 | ||||||

| 20,119 | Redwood Trust, Inc. |

209,036 | ||||||

| 19,958 | Sabra Health Care REIT, Inc. |

268,036 | ||||||

| 3,836 | SL Green Realty Corporation |

305,039 | ||||||

| 45,935 | Two Harbors Investment Corporation |

232,431 | ||||||

| 20,260 | Uniti Group, Inc. |

262,772 | ||||||

| 6,414,433 | ||||||||

Small-Cap REITs — 30.0% |

||||||||

| 11,890 | AFC Gamma, Inc. |

234,827 | ||||||

| 1,002 | Alexander’s, Inc. |

253,927 | ||||||

| 15,508 | Alpine Income Property Trust, Inc. |

297,288 | ||||||

| 33,445 | American Finance Trust, Inc. |

235,453 | ||||||

| 18,011 | Ares Commercial Real Estate Corporation |

263,861 | ||||||

| 27,704 | ARMOUR Residential REIT, Inc. |

225,234 | ||||||

| 28,795 | BrightSpire Capital, Inc. |

255,124 | ||||||

| 28,474 | Broadmark Realty Capital, Inc. |

246,585 | ||||||

| 31,411 | Cherry Hill Mortgage Investment Corporation |

236,211 | ||||||

| 24,409 | Ellington Residential Mortgage REIT |

235,303 | ||||||

| 48,670 | Franklin Street Properties Corporation |

281,313 | ||||||

| 12,437 | Gladstone Commercial Corporation |

263,540 | ||||||

| 16,545 | Global Medical REIT, Inc. |

259,756 | ||||||

| 22,363 | Granite Point Mortgage Trust, Inc. |

250,913 | ||||||

| 90,165 | Invesco Mortgage Capital, Inc. |

196,560 | ||||||

| 8,319 | LTC Properties, Inc. |

281,432 | ||||||

| 13,075 | Nexpoint Real Estate Finance, Inc. |

274,706 | ||||||

| 10,935 | Office Properties Income Trust |

273,922 | ||||||

| 8,165 | One Liberty Properties, Inc. |

237,275 | ||||||

| 58,191 | Orchid Island Capital, Inc. |

191,448 | ||||||

| 15,949 | Postal Realty Trust, Inc. - Class A |

278,310 | ||||||

| 19,750 | Preferred Apartment Communities, Inc. |

498,885 | ||||||

The accompanying notes are an integral part of these financial statements.

16

Hoya Capital High Dividend Yield ETF

Schedule OF INVESTMENTS

February 28, 2022 (Continued)

Shares |

Security Description |

Value |

||||||

COMMON STOCKS — 88.9% (Continued) |

||||||||

Small-Cap REITs — 30.0% (Continued) |

||||||||

| 17,645 | Ready Capital Corporation |

$ | 262,028 | |||||

| 47,920 | Sachem Capital Corporation |

234,808 | ||||||

| 4,767 | Universal Health Realty Income Trust |

272,243 | ||||||

| 6,540,952 | ||||||||

TOTAL COMMON STOCKS (Cost $20,379,308) |

19,402,320 | |||||||

PREFERRED STOCKS — 10.0% |

||||||||

AG Mortgage Investment Trust, Inc. |

||||||||

| 3,011 | Series C, 8.000%, Perpetual (b) |

69,253 | ||||||

AGNC Investment Corporation |

||||||||

| 3,005 | Series C, 7.000%, Perpetual (b) |

73,112 | ||||||

| 3,011 | Series E, 6.500%, Perpetual (b) |

72,415 | ||||||

Annaly Capital Management, Inc. |

||||||||

| 3,002 | Series F, 6.950%, Perpetual (b) |

71,598 | ||||||

| 3,006 | Series G, 6.500%, Perpetual (b) |

68,356 | ||||||

| 2,942 | Series I, 6.7500%, Perpetual (b) |

71,373 | ||||||

ARMOUR Residential REIT, Inc. |

||||||||

| 2,994 | Series C, 7.000%, Perpetual |

72,904 | ||||||

Chimera Investment Corporation |

||||||||

| 2,992 | Series B, 8.000%, Perpetual (b) |

74,232 | ||||||

| 2,985 | Series C, 7.750%, Perpetual (b) |

73,431 | ||||||

| 2,970 | Series D, 8.000%, Perpetual (b) |

73,478 | ||||||

DigitalBridge Group, Inc. |

||||||||

| 3,086 | Series H, 7.125%, Perpetual |

76,132 | ||||||

| 3,089 | Series I, 7.150%, Perpetual |

76,298 | ||||||

| 3,003 | Series J, 7.125%, Perpetual |

74,444 | ||||||

Global Net Lease, Inc. |

||||||||

| 2,971 | Series A, 7.250%, Perpetual |

73,621 | ||||||

| 2,973 | Series B, 6.875%, Perpetual |

73,637 | ||||||

Hersha Hospitality Trust |

||||||||

| 3,264 | Series D, 6.500%, Perpetual |

71,090 | ||||||

| 3,229 | Series E, 6.500%, Perpetual |

70,222 | ||||||

Invesco Mortgage Capital, Inc. |

||||||||

| 3,083 | Series B, 7.750%, Perpetual (b) |

71,248 | ||||||

| 3,076 | Series C, 7.500%, Perpetual (b) |

74,531 | ||||||

The accompanying notes are an integral part of these financial statements.

17

Hoya Capital High Dividend Yield ETF

Schedule OF INVESTMENTS

February 28, 2022 (Continued)

Shares |

Security Description |

Value |

||||||

PREFERRED STOCKS — 10.0% (Continued) |

||||||||

KKR Real Estate Finance Trust, Inc. |

||||||||

| 2,984 | Series A, 6.500%, Perpetual |

$ | 72,988 | |||||

MFA Financial, Inc. |

||||||||

| 3,232 | Series C, 6.500%, Perpetual (b) |

73,851 | ||||||

Necessity Retail REIT, Inc. |

||||||||

| 2,934 | Series A, 7.500%, Perpetual |

74,817 | ||||||

New Residential Investment Corporation |

||||||||

| 3,086 | Series B, 7.125%, Perpetual (b) |

72,830 | ||||||

| 3,318 | Series C, 6.375%, Perpetual (b) |

72,200 | ||||||

New York Mortgage Trust, Inc. |

||||||||

| 3,006 | Series D, 8.000%, Perpetual (b) |

73,346 | ||||||

| 2,960 | Series E, 7.875%, Perpetual (b) |

69,826 | ||||||

RLJ Lodging Trust |

||||||||

| 2,684 | Series A, 1.950%, Perpetual (c) |

70,858 | ||||||

SITE Centers Corporation |

||||||||

| 3,067 | Series A, 6.375%, Perpetual |

75,908 | ||||||

Two Harbors Investment Corporation |

||||||||

| 3,065 | Series B, 7.625%, Perpetual (b) |

72,579 | ||||||

| 3,083 | Series C, 7.250%, Perpetual (b) |

71,711 | ||||||

TOTAL PREFERRED STOCKS (Cost $2,298,059) |

2,182,289 | |||||||

The accompanying notes are an integral part of these financial statements.

18

Hoya Capital High Dividend Yield ETF

Schedule OF INVESTMENTS

February 28, 2022 (Continued)

Shares |

Security Description |

Value |

||||||

SHORT-TERM INVESTMENTS — 1.0% |

||||||||

| 210,767 | First American Government Obligations Fund - Class X, 0.03% (d) |

$ | 210,767 | |||||

TOTAL SHORT-TERM INVESTMENTS (Cost $210,767) |

210,767 | |||||||

TOTAL INVESTMENTS — 99.9% (Cost $22,888,134) |

21,795,376 | |||||||

Other Assets in Excess of Liabilities — 0.1% |

25,124 | |||||||

NET ASSETS — 100.0% |

$ | 21,820,500 | ||||||

Percentages are stated as a percent of net assets.

The Fund’s security classifications are defined by the Fund’s Adviser.

(a) |

The Index, and consequently the Fund, is expected to concentrate its investments in real estate-related industries. The value of the Fund’s shares may rise and fall more than the value of shares of a fund that invests in securities of companies in a broader range of industries. See Note 7 in Notes to Financial Statements. |

(b) |

Variable rate security based on a reference index and spread. Rate is fixed to variable and currently in the fixed phase. Rate disclosed is the rate in effect as of February 28, 2022. |

(c) |

Convertible security. |

(d) |

Rate shown is the annualized seven-day yield as of February 28, 2022. |

REIT - Real Estate Investment Trust

The accompanying notes are an integral part of these financial statements.

19

Hoya Capital ETFs

Statements of Assets and Liabilities

February 28, 2022

Hoya Capital |

Hoya Capital High |

|||||||

ASSETS |

||||||||

Investments in securities, at value* |

$ | 63,388,814 | $ | 21,795,376 | ||||

Dividends and interest receivable |

51,149 | 29,227 | ||||||

Total assets |

63,439,963 | 21,824,603 | ||||||

LIABILITIES |

||||||||

Management fees payable, net of waiver |

17,208 | 4,103 | ||||||

Total liabilities |

17,208 | 4,103 | ||||||

NET ASSETS |

$ | 63,422,755 | $ | 21,820,500 | ||||

Net Assets Consist of: |

||||||||

Paid-in capital |

$ | 59,771,603 | $ | 22,949,596 | ||||

Total distributable earnings (accumulated deficit) |

3,651,152 | (1,129,096 | ) | |||||

Net assets |

$ | 63,422,755 | $ | 21,820,500 | ||||

Net Asset Value: |

||||||||

Net Assets |

$ | 63,422,755 | $ | 21,820,500 | ||||

Shares outstanding^ |

1,600,000 | 1,530,000 | ||||||

Net asset value, offering and redemption price per share |

$ | 39.64 | $ | 14.26 | ||||

*Identified Cost: |

||||||||

Investments in Securities |

$ | 59,191,525 | $ | 22,888,134 | ||||

^ |

No par value, unlimited number of shares authorized. |

The accompanying notes are an integral part of these financial statements.

20

Hoya Capital ETFs

Statements of Operations

For the Year/Period Ended February 28, 2022

Hoya Capital |

Hoya Capital High |

|||||||

INCOME |

||||||||

Dividends+ |

$ | 986,396 | $ | 260,571 | ||||

Interest |

100 | 14 | ||||||

Total investment income |

986,496 | 260,585 | ||||||

EXPENSES |

||||||||

Management fees |

222,345 | 35,517 | ||||||

Total expenses before waiver |

222,345 | 35,517 | ||||||

Less management fees waived (see Note 3) |

— | (17,758 | ) | |||||

Net expenses |

222,345 | 17,759 | ||||||

Net investment income (loss) |

764,151 | 242,826 | ||||||

REALIZED & UNREALIZED GAIN (LOSS) ON INVESTMENTS |

||||||||

Net realized gain (loss) on investments |

10,822,631 | 70,441 | ||||||

Change in unrealized appreciation (depreciation) on investments |

(3,477,882 | ) | (1,092,758 | ) | ||||

Net realized and unrealized gain (loss) on investments |

7,344,749 | (1,022,317 | ) | |||||

Net increase (decrease) in net assets resulting from operations |

$ | 8,108,900 | $ | (779,491 | ) | |||

* |

The Fund commenced operations on September 21, 2021. The information presented is for the period from September 21, 2021 to February 28, 2022. |

+ |

Net of foreign taxes withheld of $751 and $0, respectively. |

The accompanying notes are an integral part of these financial statements.

21

Hoya Capital Housing ETF

Statements of Changes in Net Assets

Year Ended February 28, |

||||||||

2022 |

2021 |

|||||||

OPERATIONS |

||||||||

Net investment income (loss) |

$ | 764,151 | $ | 484,299 | ||||

Net realized gain (loss) on investments |

10,822,631 | 2,318,429 | ||||||

Change in unrealized appreciation (depreciation) of investments |

(3,477,882 | ) | 7,821,554 | |||||

Net increase (decrease) in net assets resulting from operations |

8,108,900 | 10,624,282 | ||||||

DISTRIBUTIONS TO SHAREHOLDERS |

||||||||

Net distributions to shareholders |

(783,934 | ) | (987,629 | ) | ||||

Tax return of capital to shareholders |

(233,770 | ) | (165,491 | ) | ||||

Total distributions to shareholders |

(1,017,704 | ) | (1,153,120 | ) | ||||

CAPITAL SHARE TRANSACTIONS |

||||||||

Proceeds from shares sold |

31,613,303 | 44,763,753 | ||||||

Payments for shares redeemed |

(34,906,983 | ) | (5,991,085 | ) | ||||

Net increase (decrease) in net assets derived from capital share transactions (a) |

(3,293,680 | ) | 38,772,668 | |||||

Net increase (decrease) in net assets |

$ | 3,797,516 | $ | 48,243,830 | ||||

NET ASSETS |

||||||||

Beginning of year |

$ | 59,625,239 | $ | 11,381,409 | ||||

End of year |

$ | 63,422,755 | $ | 59,625,239 | ||||

(a) |

A summary of capital shares transactions is as follows: |

Shares |

Shares |

|||||||

Shares sold |

775,000 | 1,475,000 | ||||||

Shares redeemed |

(875,000 | ) | (200,000 | ) | ||||

Net increase (decrease) |

(100,000 | ) | 1,275,000 | |||||

The accompanying notes are an integral part of these financial statements.

22

Hoya Capital High Dividend Yield ETF

Statement of Changes in Net Assets

Period Ended |

||||

OPERATIONS |

||||

Net investment income (loss) |

$ | 242,826 | ||

Net realized gain (loss) on investments |

70,441 | |||

Change in unrealized appreciation (depreciation) of investments |

(1,092,758 | ) | ||

Net increase (decrease) in net assets resulting from operations |

(779,491 | ) | ||

DISTRIBUTIONS TO SHAREHOLDERS |

||||

Net distributions to shareholders |

(349,605 | ) | ||

Tax return of capital to shareholders |

(200,959 | ) | ||

Total distributions to shareholders |

(550,564 | ) | ||

CAPITAL SHARE TRANSACTIONS |

||||

Proceeds from shares sold |

23,150,555 | |||

Payments for shares redeemed |

— | |||

Net increase (decrease) in net assets derived from capital share transactions (b) |

23,150,555 | |||

Net increase (decrease) in net assets |

$ | 21,820,500 | ||

NET ASSETS |

||||

Beginning of period |

$ | — | ||

End of period |

$ | 21,820,500 | ||

(a) |

The Fund commenced operations on September 21, 2021. The information presented is for the period from September 21, 2021 to February 28, 2022. |

(b) |

A summary of capital shares transactions is as follows: |

Shares |

||||

Shares sold |

1,530,000 | |||

Shares redeemed |

— | |||

Net increase (decrease) |

1,530,000 | |||

The accompanying notes are an integral part of these financial statements.

23

Hoya Capital Housing ETF

Financial Highlights

For a capital share outstanding throughout the year/period

Year Ended February 28, |

Period Ended |

|||||||||||

2022 |

2021 |

|||||||||||

Net asset value, beginning of year/period |

$ | 35.07 | $ | 26.78 | $ | 25.00 | ||||||

INCOME (LOSS) FROM INVESTMENT OPERATIONS: |

||||||||||||

Net investment income (loss) (2) |

0.42 | 0.49 | 0.43 | |||||||||

Net realized and unrealized gain (loss) on investments (3) |

4.71 | 8.82 | 1.80 | |||||||||

Total from investment operations |

5.13 | 9.31 | 2.23 | |||||||||

DISTRIBUTIONS TO SHAREHOLDERS: |

||||||||||||

Distributions from: |

||||||||||||

Net investment income |

(0.42 | ) | (0.87 | ) | (0.45 | ) | ||||||

Net realized gains |

(0.01 | ) | — | — | ||||||||

Tax return of capital to shareholders |

(0.13 | ) | (0.15 | ) | — | |||||||

Total distributions to shareholders |

(0.56 | ) | (1.02 | ) | (0.45 | ) | ||||||

CAPITAL SHARE TRANSACTIONS: |

||||||||||||

Transaction fees (see Note 6) |

— | — | 0.00 | (4) | ||||||||

Net asset value, end of year/period |

$ | 39.64 | $ | 35.07 | $ | 26.78 | ||||||

Total return |

14.60 | % | 35.54 | % | 8.88 | %(5) | ||||||

SUPPLEMENTAL DATA: |

||||||||||||

Net assets at end of year/period (000’s) |

$ | 63,423 | $ | 59,625 | $ | 11,381 | ||||||

RATIOS TO AVERAGE NET ASSETS: |

||||||||||||

Expenses to average net assets |

0.30 | % | 0.33 | %(8) | 0.45 | %(6) | ||||||

Net investment income (loss) to average net assets |

1.03 | % | 1.67 | % | 1.60 | %(6) | ||||||

Portfolio turnover rate (7) |

13 | % | 19 | % | 11 | %(5) | ||||||

(1) |

Commencement of operations on March 19, 2019. |

(2) |

Calculated based on average shares outstanding during the period. |

(3) |

Realized and unrealized gains (losses) per share are balancing amounts necessary to reconcile the change in net asset value per share for the period and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions for the period. |

(4) |

Represents less than $0.005 per share. |

(5) |

Not annualized. |

(6) |

Annualized. |

(7) |

Excludes the impact of in-kind transactions. |

(8) |

Effective August 1, 2020, the management fee for the Fund was reduced from 0.45% to 0.30%. |

The accompanying notes are an integral part of these financial statements.

24

Hoya Capital High Dividend Yield ETF

Financial Highlights

For a capital share outstanding throughout the period

Period Ended |

||||

Net asset value, beginning of period |

$ | 14.92 | ||

INCOME (LOSS) FROM INVESTMENT OPERATIONS: |

||||

Net investment income (loss) (2) |

0.23 | |||

Net realized and unrealized gain (loss) on investments (3) |

(0.41 | ) | ||

Total from investment operations |

(0.18 | ) | ||

DISTRIBUTIONS TO SHAREHOLDERS: |

||||

Distributions from: |

||||

Net investment income |

(0.30 | ) | ||

Net realized gains |

(0.01 | ) | ||

Tax return of capital to shareholders |

(0.17 | ) | ||

Total distributions to shareholders |

(0.48 | ) | ||

Net asset value, end of period |

$ | 14.26 | ||

Total return |

-1.35 | %(4) | ||

SUPPLEMENTAL DATA: |

||||

Net assets at end of period (000’s) |

$ | 21,821 | ||

RATIOS TO AVERAGE NET ASSETS: |

||||

Expenses to average net assets (before management fees waived) |

0.50 | %(5) | ||

Expenses to average net assets (after management fees waived) |

0.25 | %(5) | ||

Net investment income (loss) to average net assets (before management fees waived) |

3.17 | %(5) | ||

Net investment income (loss) to average net assets (after management fees waived) |

3.42 | %(5) | ||

Portfolio turnover rate (6) |

7 | %(4) | ||

(1) |

Commencement of operations on September 21, 2021. |

(2) |

Calculated based on average shares outstanding during the period. |

(3) |

Realized and unrealized gains (losses) per share are balancing amounts necessary to reconcile the change in net asset value per share for the period and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions for the period. |

(4) |

Not annualized. |

(5) |

Annualized. |

(6) |

Excludes the impact of in-kind transactions. |

The accompanying notes are an integral part of these financial statements.

25

Hoya Capital ETFs

Notes to Financial Statements

February 28, 2022

NOTE 1 – ORGANIZATION

Hoya Capital Housing ETF and Hoya Capital High Dividend Yield ETF (individually each a “Fund” or collectively the “Funds”) are each a diversified series of ETF Series Solutions (“ESS” or the “Trust”), an open-end management investment company consisting of multiple investment series, organized as a Delaware statutory trust on February 9, 2012. The Trust is registered with the U.S. Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company and the offering of the Funds’ shares is registered under the Securities Act of 1933, as amended (the “Securities Act”). The investment objective of the Hoya Capital Housing ETF is to track the performance, before fees and expenses, of the Hoya Capital Housing 100™ Index (the “Index”). The investment objective of the Hoya Capital High Dividend Yield ETF is to track the performance, before fees and expenses, of the Hoya Capital High Dividend Yield Index (the “Index”). Hoya Capital Housing ETF commenced operations on March 19, 2019 and Hoya Capital High Dividend Yield ETF commenced operations on September 21, 2021.

The end of the reporting period for the Funds is February 28, 2022. The period covered by these Notes to Financial Statements for the Hoya Capital Housing ETF is the fiscal year ended February 28, 2022 (the “current fiscal period”). The period covered by these Notes to Financial Statements for the Hoya Capital High Dividend Yield ETF is the period from September 21, 2021 to February 28, 2022 (the “current fiscal period”).

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The Funds are investment companies and accordingly follow the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946 Financial Services-Investment Companies.

The following is a summary of significant accounting policies consistently followed by the Funds. These policies are in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”).

|

A. |

Security Valuation. All equity securities, including domestic and foreign common stocks, preferred stocks and exchange traded funds that are traded on a national securities exchange, except those listed on the Nasdaq Global Market®, Nasdaq Global Select Market® and the Nasdaq Capital Market® exchanges (collectively, “Nasdaq”) are valued at the last reported sale price on the exchange on which the security is principally traded. Securities traded on Nasdaq will be valued at the Nasdaq Official Closing Price (“NOCP”). If, on a particular day, an exchange-traded or Nasdaq security does not trade, then the mean between the most recent quoted bid and asked prices will be used. |

26

Hoya Capital ETFs

NOTES TO FINANCIAL STATEMENTS

February 28, 2022 (Continued)

All equity securities that are not traded on a listed exchange are valued at the last sale price in the over-the-counter market. If a non-exchange traded security does not trade on a particular day, then the mean between the last quoted closing bid and asked price will be used. Prices denominated in foreign currencies are converted to U.S. dollar equivalents at the current exchange rate, which approximates fair value.

Investments in mutual funds, including money market funds, are valued at their net asset value (“NAV”) per share.

Securities for which quotations are not readily available are valued at their respective fair values in accordance with pricing procedures adopted by the Fund’s Board of Trustees (the “Board”). When a security is “fair valued,” consideration is given to the facts and circumstances relevant to the particular situation, including a review of various factors set forth in the pricing procedures adopted by the Board. The use of fair value pricing by the Funds may cause the NAV of their shares to differ significantly from the NAV that would be calculated without regard to such considerations.

As described above, the Funds utilize various methods to measure the fair value of their investments on a recurring basis. U.S. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

|

Level 1 — |

Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

|

Level 2 — |

Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

|

Level 3 — |

Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available; representing the Funds’ own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that

27

Hoya Capital ETFs

NOTES TO FINANCIAL STATEMENTS

February 28, 2022 (Continued)

are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The following is a summary of the inputs used to value the Funds’ investments as of the end of the current fiscal period:

Hoya Capital Housing ETF |

||||||||||||||||

Assets^ |

Level 1 |

Level 2 |

Level 3 |

Total |

||||||||||||

Common Stocks |

$ | 62,986,050 | $ | — | $ | — | $ | 62,986,050 | ||||||||

Short-Term Investments |

402,764 | — | — | 402,764 | ||||||||||||

Total Investments in Securities |

$ | 63,388,814 | $ | — | $ | — | $ | 63,388,814 | ||||||||

Hoya Capital High Dividend Yield ETF |

||||||||||||||||

Assets^ |

Level 1 |

Level 2 |

Level 3 |

Total |

||||||||||||

Common Stocks |

$ | 19,402,320 | $ | — | $ | — | $ | 19,402,320 | ||||||||

Preferred Stocks |

2,182,289 | — | — | 2,182,289 | ||||||||||||

Short-Term Investments |

210,767 | — | — | 210,767 | ||||||||||||

Total Investments in Securities |

$ | 21,795,376 | $ | — | $ | — | $ | 21,795,376 | ||||||||

^ |

See Schedule of Investments for breakout of investments by sector classifications. |

During the current fiscal period, the Funds did not recognize any transfers to or from Level 3.

|

B. |

Federal Income Taxes. The Funds’ policy is to comply with the requirements of Subchapter M of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies and to distribute substantially all of their net investment income and net capital gains to shareholders. Therefore, no federal income tax provision is required. Each Fund plans to file U.S. Federal and applicable state and local tax returns. |

28

Hoya Capital ETFs

NOTES TO FINANCIAL STATEMENTS

February 28, 2022 (Continued)

Each Fund recognize the tax benefits of uncertain tax positions only when the position is more likely than not to be sustained. Management has analyzed each Fund’s uncertain tax positions and concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions. Management is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next 12 months. Income and capital gain distributions are determined in accordance with federal income tax regulations, which may differ from U.S. GAAP. The Funds recognize interest and penalties, if any, related to unrecognized tax benefits on uncertain tax positions as income tax expense in the Statement of Operations. During the current fiscal period, the Funds did not incur any interest or penalties.

|

C. |

Security Transactions and Investment Income. Investment securities transactions are accounted for on the trade date. Gains and losses realized on sales of securities are determined on a specific identification basis. Dividend income is recorded on the ex-dividend date. Non-cash dividends included in dividend income or separately disclosed, if any, are recorded at the fair value of the security received. Interest income is recorded on an accrual basis. Withholding taxes on foreign dividends, if any, have been provided for in accordance with the Funds’ understanding of the applicable tax rules and regulations. |

Distributions received from investments in Real Estate Investment Trusts (“REITs”) may be characterized as ordinary income, net capital gain, or a return of capital. The proper characterization of REIT distributions is generally not known until after the end of each calendar year. As such, the Funds must use estimates in reporting the character of income and distributions received during the current calendar year for financial statement purposes. The actual character of distributions to the Funds’ shareholders will be reflected on the Form 1099 received by shareholders after the end of the calendar year. Due to the nature of REIT investments, a portion of the distributions received by the Funds’ shareholders may represent a return of capital.

|

D. |

Distributions to Shareholders. Distributions to shareholders from net investment income, if any, are declared and paid monthly by the Funds. Distributions to shareholders from net realized gains on securities are declared and paid by the Funds on, at least, an annual basis. Distributions are recorded on the ex-dividend date. |

|

E. |

Use of Estimates. The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of |

29

Hoya Capital ETFs

NOTES TO FINANCIAL STATEMENTS

February 28, 2022 (Continued)

contingent assets and liabilities at the date of the financial statements, as well as the reported amounts of revenues and expenses during the current fiscal period. Actual results could differ from those estimates.

|

F. |

Share Valuation. The NAV per share of each Fund are calculated by dividing the sum of the value of the securities held by each Fund, plus cash and other assets, minus all liabilities (including estimated accrued expenses) by the total number of outstanding shares of each Fund, rounded to the nearest cent. The Funds’ shares will not be priced on the days on which the New York Stock Exchange (“NYSE”) is closed for trading. The offering and redemption price per share of each Fund is equal to each Fund’s NAV per share. |

|

G. |

Reclassifications of Capital Accounts. U.S. GAAP requires that certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. These reclassifications have no effect on net assets or NAV per share. |

These timing differences are primarily due to differing book and tax treatments for in-kind transactions.

For the current fiscal period, the following table shows the reclassifications made:

Distributable |

Paid-In Capital |

|||||||

Hoya Capital Housing ETF |

$ | (10,933,756 | ) | $ | 10,933,756 | |||

Hoya Capital High Dividend Yield ETF |

— | — | ||||||

During the current fiscal period the Hoya Capital Housing ETF realized $10,933,756 in net capital gains resulting from in-kind redemptions, in which shareholders exchanged Fund shares for securities held by the Fund rather than for cash. Because such gains are not taxable to the Fund, and are not distributed to shareholders, they have been reclassified from distributable earnings (accumulated deficit) to paid-in capital.

|

H. |

Guarantees and Indemnifications. In the normal course of business, the Funds enter into contracts with service providers that contain general indemnification clauses. The Funds’ maximum exposure under these arrangements is unknown as this would involve future claims that may be against the Funds that have not yet occurred. However, based on experience, the Funds expect the risk of loss to be remote. |

30

Hoya Capital ETFs

NOTES TO FINANCIAL STATEMENTS

February 28, 2022 (Continued)

|

I. |

Subsequent Events. In preparing these financial statements, management has evaluated events and transactions for potential recognition or disclosure through the date the financial statements were issued. There were no events or transactions that occurred during the period subsequent to the end of the current fiscal period that materially impacted the amounts or disclosures in the Funds’ financial statements. |

NOTE 3 – COMMITMENTS AND OTHER RELATED PARTY TRANSACTIONS

Hoya Capital Real Estate, LLC (the “Adviser”), serves as the investment adviser to the Funds. An affiliate of the Adviser, Hoya Capital Index Innovations (the “Index Provider”), serves as index provider to the Funds. Pursuant to an Investment Advisory Agreement (“Advisory Agreement”) between the Trust, on behalf of the Funds, and the Adviser, the Adviser provides investment advice to the Funds and oversees the day-to-day operations of the Funds, subject to the direction and control of the Board and the officers of the Trust. Under the Advisory Agreement, the Adviser is also responsible for arranging, in consultation with Penserra Capital Management, LLC, (the “Sub-Adviser”), transfer agency, custody, fund administration and accounting, and other non-distribution related services necessary for the Funds to operate. Under the Advisory Agreement, the Adviser has agreed to pay all expenses of the Funds, except for: the fee paid to the Adviser pursuant to the Advisory Agreement, interest charges on any borrowings, dividends and other expenses on securities sold short, taxes, brokerage commissions and other expenses incurred in placing orders for the purchase and sale of securities and other investment instruments, acquired fund fees and expenses, accrued deferred tax liability, extraordinary expenses and distribution (12b-1) fees and expenses. For the services it provides to the Funds, the Funds pay the Adviser a unified management fee, which is calculated daily and paid monthly, at the annual rates of each Fund’s average daily net assets listed below.

Hoya Capital Housing ETF |

0.30 | % | ||

Hoya Capital High Dividend Yield ETF |

0.50 | % |

The Adviser has agreed to waive 0.25% of its Advisor fees for the Hoya Capital High Dividend Yield ETF until at least September 30, 2022. This agreement may be terminated only by, or with the consent of, the Board. Fees waived under this waiver agreement are not subject to recoupment by the Adviser.

U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services (“Fund Services” or “Administrator”), acts as the Funds’ Administrator and, in that capacity, performs various administrative and accounting services for the Funds. The Administrator prepares various federal and state regulatory filings, reports and returns for the Funds, including regulatory compliance monitoring and financial reporting; prepares reports and materials to be supplied to the Board; monitors the activities of

31

Hoya Capital ETFs

NOTES TO FINANCIAL STATEMENTS

February 28, 2022 (Continued)

the Funds’ Custodian, transfer agent, and fund accountant. Fund Services also serves as the transfer agent and fund accountant to the Funds. U.S. Bank N.A. (the “Custodian”), an affiliate of Fund Services, serves as the Funds’ Custodian.

A Trustee and all officers of the Trust are affiliated with the Administrator and Custodian.

NOTE 4 – PURCHASES AND SALES OF SECURITIES

During the current fiscal period, purchases and sales of securities by the Funds, excluding short-term securities and in-kind transactions were as follow:

Purchases |

Sales |

|||||||

Hoya Capital Housing ETF |

$ | 12,713,749 | $ | 9,568,679 | ||||

Hoya Capital High Dividend Yield ETF |

$ | 1,092,175 | $ | 1,116,527 | ||||

During the current fiscal period, there were no purchases or sales of U.S. Government securities.

During the current fiscal period, in-kind transactions associated with creations and redemptions were as follow:

In-Kind |

In-Kind |

|||||||

Hoya Capital Housing ETF |

$ | 28,181,047 | $ | 34,538,138 | ||||

Hoya Capital High Dividend Yield ETF |

$ | 22,856,979 | — | |||||

NOTE 5 – INCOME TAX INFORMATION

The components of distributable earnings (accumulated deficit) and cost basis of investments for federal income tax purposes at February 28, 2022 were as follows:

Hoya Capital |

Hoya Capital |

|||||||

Tax cost of investments |

$ | 59,578,676 | $ | 22,924,472 | ||||

Gross tax unrealized appreciation |

$ | 8,347,536 | $ | 603,401 | ||||

Gross tax unrealized depreciation |

(4,537,398 | ) | (1,732,497 | ) | ||||

Net tax unrealized appreciation (depreciation) |