Form N-CSR DWS MUNICIPAL INCOME For: Nov 30

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM N-CSR

Investment Company Act file number: 811-05655

DWS Municipal Income Trust

(Exact Name of Registrant as Specified in Charter)

875 Third Avenue

New York, NY 10022-6225

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (212) 454-4500

Diane Kenneally

100 Summer Street

Boston, MA 02110

(Name and Address of Agent for Service)

| Date of fiscal year end: | 11/30 |

| Date of reporting period: | 11/30/2022 |

| ITEM 1. | REPORT TO STOCKHOLDERS |

| (a) |

Contents

| 4 |

|

| 9 |

|

| 12 |

|

| 14 |

|

| 32 |

|

| 33 |

|

| 34 |

|

| 35 |

|

| 36 |

|

| 38 |

|

| 46 |

|

| 48 |

|

| 49 |

|

| 50 |

|

| 53 |

|

| 57 |

|

| 71 |

|

| 76 |

NOT FDIC/NCUA INSURED NO BANK GUARANTEE MAY LOSE VALUE

NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

| 2 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

3 |

| 4 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

5 |

| 6 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

7 |

| 8 |

| |

DWS Municipal Income Trust |

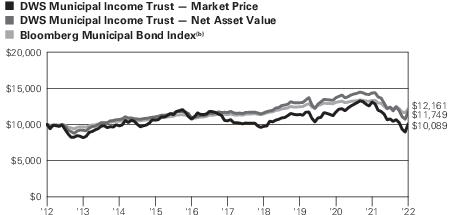

| Average Annual Total Returns as of 11/30/22 | |||

| DWS Municipal Income Trust |

1-Year |

5-Year |

10-Year |

| Based on Net Asset

Value(a) |

–18.12% |

0.19% |

1.62% |

| Based on Market

Price(a) |

–22.95% |

–0.80% |

0.09% |

| Bloomberg Municipal Bond Index(b) |

–8.64% |

1.40% |

1.98% |

| Morningstar Closed-End Municipal National Long Funds Category(c) |

–17.08% |

0.59% |

2.33% |

| DWS

Municipal Income Trust |

| |

9 |

| (a) |

Total return based on net asset value reflects changes in the Fund’s net asset value during each period. Total return based on market price reflects changes in market price. Each figure assumes that dividend and capital gain distributions, if any, were reinvested. These figures will differ depending upon the level of any discount from or premium to net asset value at which the Fund’s shares traded during the period. Expenses of the Fund include management fee, interest expense and other fund expenses. Total returns shown take into account these fees and expenses. The expense ratio of the Fund for the year ended November 30, 2022 was 2.11% (0.91% excluding interest expense). |

| (b) |

The unmanaged, unleveraged Bloomberg Municipal Bond Index covers the U.S. dollar-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and pre-refunded bonds. Index returns do not reflect any fees or expenses and it is not possible to invest directly into an index. |

| (c) |

Morningstar’s Closed-End Municipal National Long Funds category represents muni national long portfolios that invest in municipal bonds. Such bonds are issued by various state and local governments to fund public projects and are free from federal taxes. To lower risk, these funds spread their assets across many states and sectors. They focus on bonds with durations of seven years or more. This makes them more sensitive to interest rates, and thus riskier, than muni funds that focus on bonds with shorter maturities. Morningstar figures represent the average of the total returns based on net asset value reported by all of the closed-end funds designated by Morningstar, Inc. as falling into the Closed-End Municipal National Long Funds category. Category returns assume reinvestment of all distributions. It is not possible to invest directly in a Morningstar category. |

| Net Asset Value and Market Price |

|

|

| |

As of 11/30/22 |

As of 11/30/21 |

| Net Asset Value |

$ 9.96 |

$ 12.70 |

| Market Price |

$ 8.93 |

$ 12.10 |

| Premium (discount) |

(10.34%) |

(4.72%) |

| 10 |

| |

DWS Municipal Income Trust |

| Distribution Information |

|

| Twelve Months as of 11/30/22: Income Dividends (common shareholders) |

$ .42

|

| November Income Dividend (common shareholders) |

$ .028 |

| Current Annualized Distribution Rate (based on Net Asset Value) as of 11/30/22†

|

3.37% |

| Current Annualized Distribution Rate (based on Market Price) as of 11/30/22†

|

3.76% |

| Tax Equivalent Distribution Rate (based on Net Asset Value) as of 11/30/22†

|

5.70% |

| Tax Equivalent Distribution Rate (based on Market Price) as of 11/30/22†

|

6.36% |

| † |

Current annualized distribution rate is the latest monthly dividend shown as an annualized percentage of net asset value/market price on November 30, 2022. Distribution rate simply measures the level of dividends and is not a complete measure of performance. Tax equivalent distribution rate is based on the Fund’s distribution rate and a marginal income tax rate of 40.8%. Distribution rates are historical, not guaranteed and will fluctuate. Distributions do not include return of capital or other non-income sources. |

| DWS

Municipal Income Trust |

| |

11 |

| Asset Allocation (As a % of Investment Portfolio excluding Open-End Investment Companies) |

11/30/22 |

11/30/21 |

| Revenue Bonds |

77% |

78% |

| Lease Obligations |

9% |

9% |

| Escrow to Maturity/Prerefunded Bonds |

8% |

6% |

| General Obligation Bonds |

6% |

7% |

| Variable Rate Demand Notes |

0% |

0% |

| |

100% |

100% |

| Quality (As a % of Investment Portfolio excluding Open-End Investment Companies) |

11/30/22 |

11/30/21 |

| AAA |

2% |

2% |

| AA |

28% |

32% |

| A |

50% |

47% |

| BBB |

18% |

18% |

| BB |

— |

0% |

| Not Rated |

2% |

1% |

| |

100% |

100% |

| Top Five State/Territory Allocations (As a % of

Investment Portfolio excluding Open-End Investment

Companies) |

11/30/22 |

11/30/21 |

| Texas |

13% |

13% |

| New York |

11% |

12% |

| Florida |

9% |

9% |

| California |

8% |

9% |

| Illinois |

7% |

6% |

| 12 |

| |

DWS Municipal Income Trust |

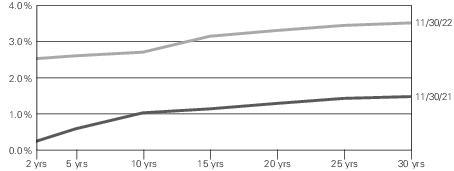

| Interest Rate Sensitivity |

11/30/22 |

11/30/21 |

| Effective Maturity |

10.7 years |

5.9 years |

| Modified Duration |

7.6 years |

5.4 years |

| Leverage (As a % of Total Assets) |

11/30/22 |

11/30/21 |

| |

38.88% |

33.36% |

| DWS

Municipal Income Trust |

| |

13 |

| |

Principal

Amount ($) |

Value ($) | |

| Municipal Investments 142.6% |

| ||

| Alabama 0.4% |

| ||

| Alabama, UAB Medicine Finance Authority Revenue, Series B2, 5.0%, 9/1/2041 |

|

1,625,000 |

1,666,555 |

| Alaska 1.7% |

| ||

| Alaska, Industrial Development & Export Authority, Tanana Chiefs Conference Project, 4.0%, 10/1/2044 |

|

5,410,000 |

4,963,019 |

| Alaska, Northern Tobacco Securitization Corp., Tobacco Settlement Revenue, “1” , Series A, 4.0%, 6/1/2050 |

|

2,250,000 |

1,918,718

|

| |

|

|

6,881,737 |

| Arizona 2.8% |

| ||

| Arizona, Salt Verde Financial Corp., Gas Revenue: |

|

|

|

| 5.0%, 12/1/2037, GTY: Citigroup Global Markets |

|

1,050,000 |

1,086,760 |

| 5.5%, 12/1/2029, GTY: Citigroup Global Markets |

|

1,400,000 |

1,506,578 |

| Arizona, State University, Green Bond, Series A, 5.0%, 7/1/2043 |

|

5,900,000 |

6,321,793 |

| Maricopa County, AZ, Industrial Development Authority, Hospital Revenue, Series A, 5.0%, 9/1/2042 |

|

1,000,000 |

1,025,553 |

| Phoenix, AZ, Civic Improvement Corp., Rental Car Facility Revenue, Series A, 4.0%, 7/1/2045 |

|

1,000,000 |

895,991 |

| |

|

|

10,836,675 |

| California 13.5% |

| ||

| California, Golden State Tobacco Securitization Corp., Tobacco Settlement: |

|

|

|

| Series A-1, Prerefunded, 5.0%, 6/1/2034 |

|

2,500,000 |

2,815,037 |

| Series A-1, Prerefunded, 5.0%, 6/1/2035 |

|

2,500,000 |

2,815,037 |

| California, Housing Finance Agency, Municipal Certificates, “A” , Series 2021-1, 3.5%, 11/20/2035 |

|

1,089,661 |

983,365 |

| California, Morongo Band of Mission Indians Revenue, Series B, 144A, 5.0%, 10/1/2042 |

|

345,000 |

346,031 |

| California, M-S-R Energy Authority, Series A, 7.0%, 11/1/2034, GTY: Citigroup Global Markets |

|

3,180,000 |

3,934,976 |

| California, State General Obligation, 5.0%, 11/1/2043 |

|

5,000,000 |

5,076,180 |

| California, State Municipal Finance Authority Revenue, LAX Integrated Express Solutions LLC, LINXS Apartment Project: |

|

|

|

| Series A, AMT, 5.0%, 12/31/2043 |

|

1,825,000 |

1,845,909 |

| Series A, AMT, 5.0%, 6/1/2048 |

|

240,000 |

241,190 |

| California, Tobacco Securitization Authority, Tobacco Settlement Revenue, San Diego County Tobacco Asset Securitization Corp., Series A, 5.0%, 6/1/2048 |

|

700,000 |

714,910 |

| 14 |

| |

DWS Municipal Income Trust |

| |

Principal

Amount ($) |

Value ($) | |

| Long Beach, CA, Harbor Revenue, Series D, 5.0%, 5/15/2039 |

|

1,065,000 |

1,105,968 |

| Los Angeles, CA, Department of Airports Revenue: |

|

|

|

| Series C, AMT, 5.0%, 5/15/2044 |

|

3,750,000 |

3,845,730 |

| Series A, AMT, 5.0%, 5/15/2045 |

|

1,250,000 |

1,302,590 |

| Los Angeles, CA, Department of Airports Revenue, Los Angeles International Airport, Series A, AMT, 5.0%, 5/15/2044 |

|

6,430,000 |

6,608,840 |

| San Diego County, CA, Regional Airport Authority Revenue, Series B, AMT, Prerefunded, 5.0%, 7/1/2043 |

|

7,000,000 |

7,096,717 |

| San Diego, CA, Unified School District, Election 2012, Series C, Prerefunded, 5.0%, 7/1/2035 |

|

4,700,000 |

4,770,404 |

| San Diego, CA, Unified School District, Proposition Z Bonds, Series M2, 3.0%, 7/1/2050 |

|

2,000,000 |

1,564,413 |

| San Francisco City & County, CA, Airports Commission, International Airport Revenue, Series D, AMT, 5.0%, 5/1/2048 |

|

2,965,000 |

3,017,454 |

| San Francisco, CA, City & County Airports Commission, International Airport Revenue, Series E, 5.0%, 5/1/2045 |

|

5,000,000 |

5,123,860

|

| |

|

|

53,208,611 |

| Colorado 7.4% |

| ||

| Colorado, State Health Facilities Authority Revenue, School Health Systems, Series A, Prerefunded, 5.5%, 1/1/2035 |

|

5,450,000 |

5,614,807 |

| Colorado, State Health Facilities Authority, Hospital Revenue, CommonSpirit Health Obligation Group, Series A-1, 4.0%, 8/1/2044 |

|

9,960,000 |

8,650,915 |

| Colorado, State Health Facilities Authority, Hospital Revenue, Covenant Retirement Communities Obligated Group, Series A, 5.0%, 12/1/2048 |

|

1,305,000 |

1,301,983 |

| Denver, CO, City & County Airport Revenue: |

|

|

|

| Series A, AMT, 5.0%, 12/1/2048 |

|

10,110,000 |

10,258,459 |

| Series A, AMT, 5.25%, 11/15/2043 |

|

2,400,000 |

2,418,041 |

| Denver, CO, Health & Hospital Authority, Certificate of Participations, 5.0%, 12/1/2048 |

|

490,000 |

491,358 |

| Denver, CO, Health & Hospital Authority, Healthcare Revenue, Series A, 4.0%, 12/1/2040 |

|

450,000 |

393,671 |

| |

|

|

29,129,234 |

| Delaware 0.4% |

| ||

| Delaware, State Economic Development Authority, Retirement Communities Revenue, Acts Retirement Life Communities, Series B, 5.0%, 11/15/2048 |

|

1,750,000 |

1,695,561 |

| District of Columbia 2.1% |

| ||

| District of Columbia, International School Revenue, 5.0%, 7/1/2039 |

|

500,000 |

503,813 |

| DWS

Municipal Income Trust |

| |

15 |

| |

Principal

Amount ($) |

Value ($) | |

| District of Columbia, KIPP Project Revenue, 4.0%, 7/1/2049 |

|

2,405,000 |

2,072,247 |

| District of Columbia, Metropolitan Airport Authority Systems Revenue: |

|

|

|

| Series A, AMT, 5.0%, 10/1/2038 |

|

800,000 |

804,927 |

| Series A, AMT, 5.0%, 10/1/2043 |

|

3,400,000 |

3,413,968 |

| District of Columbia, Metropolitan Airport Authority, Dulles Toll Road Revenue, Dulles Metrorail & Capital Improvement Project, Series B, 4.0%, 10/1/2049 |

|

1,590,000 |

1,386,051

|

| |

|

|

8,181,006 |

| Florida 12.7% |

| ||

| Brevard County, FL, Health Facilities Authority, Hospital Revenue, Health First, Inc., Series A, 4.0%, 4/1/2052 |

|

2,500,000 |

2,205,194 |

| Broward County, FL, Airport Systems Revenue, Series A, AMT, 4.0%, 10/1/2049 |

|

345,000 |

310,787 |

| Clay County, FL, Sales Surtax Revenue, 4.0%, 10/1/2039 |

|

1,650,000 |

1,627,256 |

| Davie, FL, Educational Facilities Revenue, Nova Southeastern University Project, 5.0%, 4/1/2048 |

|

1,665,000 |

1,708,249 |

| Florida, Development Finance Corp., Educational Facilities Revenue, Mater Academy Projects: |

|

|

|

| Series A, 5.0%, 6/15/2047 |

|

900,000 |

900,405 |

| Series A, 5.0%, 6/15/2052 |

|

270,000 |

267,300 |

| Series A, 5.0%, 6/15/2056 |

|

440,000 |

429,127 |

| Florida, Development Finance Corp., Brightline Florida Passenger Rail Expansion Project, AMT, 2.9% (a), 12/1/2056 |

|

600,000 |

597,550 |

| Florida, Development Finance Corp., Educational Facilities Revenue, River City Science Academy Project: |

|

|

|

| Series A-1, 5.0%, 7/1/2042 |

|

60,000 |

60,137 |

| Series B, 5.0%, 7/1/2042 |

|

60,000 |

58,756 |

| Series A-1, 5.0%, 7/1/2051 |

|

55,000 |

54,017 |

| Series B, 5.0%, 7/1/2051 |

|

85,000 |

81,030 |

| Series A-1, 5.0%, 2/1/2057 |

|

80,000 |

77,135 |

| Series B, 5.0%, 7/1/2057 |

|

90,000 |

84,046 |

| Florida, State Atlantic University Finance Corp., Capital Improvements Revenue, Student Housing Project, Series B, 4.0%, 7/1/2044 |

|

2,525,000 |

2,370,651 |

| Florida, State Higher Educational Facilities Financial Authority Revenue, Florida Institute of Technology, Series A, 4.0%, 10/1/2044 |

|

1,000,000 |

860,838 |

| Greater Orlando, FL, Aviation Authority Airport Facilities Revenue: |

|

|

|

| Series A, AMT, 5.0%, 10/1/2042 |

|

1,490,000 |

1,516,155 |

| Series A, AMT, 5.0%, 10/1/2047 |

|

965,000 |

975,728 |

| 16 |

| |

DWS Municipal Income Trust |

| |

Principal

Amount ($) |

Value ($) | |

| Hillsborough County, FL, Aviation Authority, Tampa International Airport: |

|

|

|

| Series A, AMT, 4.0%, 10/1/2052 |

|

1,710,000 |

1,540,336 |

| Series A, AMT, 5.0%, 10/1/2048 |

|

2,500,000 |

2,535,664 |

| Miami-Dade County, FL, Aviation Revenue: |

|

|

|

| Series A, AMT, 5.0%, 10/1/2035 |

|

5,000,000 |

5,040,984 |

| Series B, AMT, 5.0%, 10/1/2040 |

|

2,360,000 |

2,407,471 |

| Miami-Dade County, FL, Expressway Authority, Toll Systems Revenue, Series A, 5.0%, 7/1/2035, INS: AGMC |

|

3,000,000 |

3,012,722 |

| Miami-Dade County, FL, Health Facilities Authority Hospital Revenue, Nicklaus Children’s Hospital, 5.0%, 8/1/2047 |

|

3,335,000 |

3,366,761 |

| Miami-Dade County, FL, Transit System, Series A, 4.0%, 7/1/2050 |

|

5,000,000 |

4,644,585 |

| Osceola County, FL, Transportation Revenue, Series A-1, 4.0%, 10/1/2054 |

|

3,000,000 |

2,512,308 |

| Palm Beach County, FL, Health Facilities Authority, Acts Retirement-Life Communities, Inc., Series A, 5.0%, 11/15/2045 |

|

3,100,000 |

3,033,645 |

| Palm Beach County, FL, Health Facilities Authority, Jupiter Medical Center, Series A, 5.0%, 11/1/2052 |

|

600,000 |

601,580 |

| Tallahassee, FL, Health Facilities Revenue, Memorial Healthcare, Inc. Project, Series A, 5.0%, 12/1/2055 |

|

2,045,000 |

2,053,714 |

| Tampa, FL, The University of Tampa Project, Series A, 4.0%, 4/1/2050 |

|

3,775,000 |

3,358,661 |

| Tampa, FL, Water & Waste Water System Revenue, Series A, 5.25%, 10/1/2057 |

|

1,500,000 |

1,656,798

|

| |

|

|

49,949,590 |

| Georgia 7.3% |

| ||

| Atlanta, GA, Airport Passenger Facility Charge Revenue, Series D, AMT, 4.0%, 7/1/2038 |

|

2,000,000 |

1,927,842 |

| Cobb County, GA, Kennestone Hospital Authority, Revenue Anticipation Certificates, Wellstar Health System, Inc. Project: |

|

|

|

| Series A, 4.0%, 4/1/2052 |

|

620,000 |

562,899 |

| Series A, 5.0%, 4/1/2047 |

|

875,000 |

881,771 |

| Fulton County, GA, Development Authority Hospital Revenue, Revenue Anticipation Certificates, Wellstar Health System, Series A, 5.0%, 4/1/2042 |

|

1,055,000 |

1,071,779 |

| Fulton County, GA, Development Authority Hospital Revenue, Wellstar Health System, Obligated Inc. Project, Series A, 4.0%, 4/1/2050 |

|

1,320,000 |

1,208,062 |

| George L Smith II, GA, Congress Center Authority, Convention Center Hotel First Tier, Series A, 4.0%, 1/1/2054 |

|

3,640,000 |

2,962,788 |

| DWS

Municipal Income Trust |

| |

17 |

| |

Principal

Amount ($) |

Value ($) | |

| Georgia, Glynn-Brunswick Memorial Hospital Authority, Anticipation Certificates, Southeast Georgia Health System Project, 5.0%, 8/1/2047 |

|

465,000 |

465,959 |

| Georgia, Main Street Natural Gas, Inc., Gas Project Revenue: |

|

|

|

| Series A, 5.5%, 9/15/2024, GTY: Merrill Lynch & Co. |

|

5,000,000 |

5,160,880 |

| Series A, 5.5%, 9/15/2028, GTY: Merrill Lynch & Co. |

|

10,000,000 |

10,796,863 |

| Georgia, Municipal Electric Authority Revenue, Project One: |

|

|

|

| Series A, 5.0%, 1/1/2035 |

|

1,010,000 |

1,033,579 |

| Series A, 5.0%, 1/1/2049 |

|

1,000,000 |

1,002,353 |

| Georgia, Private Colleges & Universities Authority Revenue, Mercer University Project, 4.0%, 10/1/2047 |

|

1,800,000 |

1,646,439

|

| |

|

|

28,721,214 |

| Hawaii 0.4% |

| ||

| Hawaii, State Airports Systems Revenue, Series A, AMT, 5.0%, 7/1/2041 |

|

1,490,000 |

1,501,313 |

| Illinois 11.0% |

| ||

| Chicago, IL, General Obligation: |

|

|

|

| Series A, 5.0%, 1/1/2044 |

|

800,000 |

785,631 |

| Series A, 5.5%, 1/1/2049 |

|

450,000 |

456,471 |

| Series A, 6.0%, 1/1/2038 |

|

405,000 |

421,123 |

| Chicago, IL, Metropolitan Pier & Exposition Authority, McCormick Place Expansion Project, Series B, Zero Coupon, 6/15/2044, INS: AGMC |

|

2,500,000 |

883,257 |

| Chicago, IL, O’Hare International Airport Revenue, Series A, AMT, 5.5%, 1/1/2055 |

|

1,355,000 |

1,426,591 |

| Chicago, IL, O’Hare International Airport Revenue, Senior Lien, Series D, AMT, 5.0%, 1/1/2047 |

|

6,785,000 |

6,847,417 |

| Chicago, IL, O’Hare International Airport, Special Facility Revenue, AMT, 5.0%, 7/1/2048 |

|

395,000 |

395,631 |

| Chicago, IL, Transit Authority, Sales Tax Receipts Revenue, Second Lien: |

|

|

|

| Series A, 4.0%, 12/1/2050 |

|

465,000 |

413,387 |

| Series A, 5.0%, 12/1/2052 |

|

3,000,000 |

3,068,619 |

| Illinois, Metropolitan Pier & Exposition Authority, Dedicated State Tax Revenue, Capital Appreciation-McCormick, Series A, Zero Coupon, 6/15/2036, INS: NATL |

|

3,500,000 |

1,869,783 |

| Illinois, State Finance Authority Revenue, Bradley University Project, Series A, 4.0%, 8/1/2051 |

|

3,000,000 |

2,486,088 |

| Illinois, State Finance Authority Revenue, OSF Healthcare Systems, Series A, 5.0%, 11/15/2045 |

|

1,745,000 |

1,758,774 |

| Illinois, State Finance Authority Revenue, University of Chicago, Series A, 5.0%, 10/1/2038 |

|

4,445,000 |

4,592,247 |

| 18 |

| |

DWS Municipal Income Trust |

| |

Principal

Amount ($) |

Value ($) | |

| Illinois, State General Obligation: |

|

|

|

| 4.0%, 6/1/2033 |

|

2,400,000 |

2,308,701 |

| Series C, 4.0%, 10/1/2037 |

|

2,500,000 |

2,316,500 |

| Series B, 5.0%, 10/1/2033 |

|

1,970,000 |

2,049,639 |

| Series A, 5.0%, 5/1/2034 |

|

3,500,000 |

3,614,138 |

| Series A, 5.0%, 5/1/2043 |

|

1,000,000 |

1,007,019 |

| Series A, 5.0%, 3/1/2046 |

|

335,000 |

336,219 |

| 5.5%, 5/1/2039 |

|

1,915,000 |

2,021,435 |

| 5.75%, 5/1/2045 |

|

735,000 |

774,995 |

| Illinois, State Toll Highway Authority, Series A, 5.0%, 1/1/2044 |

|

2,535,000 |

2,660,878 |

| Springfield, IL, Electric Revenue, Senior Lien, 5.0%, 3/1/2040, INS: AGMC |

|

970,000 |

1,004,219

|

| |

|

|

43,498,762 |

| Indiana 4.6% |

| ||

| Indiana, Finance Authority Revenue, DePauw University, Series A, 5.5%, 7/1/2052 |

|

4,000,000 |

4,280,889 |

| Indiana, State Finance Authority Revenue, BHI Senior Living Obligated Group, 5.0%, 11/15/2053 |

|

2,965,000 |

2,729,156 |

| Indiana, State Finance Authority, Health Facilities Revenue, Baptist Healthcare System, Series A, 5.0%, 8/15/2051 |

|

3,500,000 |

3,536,317 |

| Indiana, State Finance Authority, Hospital Revenue, Parkview Health System Obligated Group, Series A, 5.0%, 11/1/2043 |

|

7,000,000 |

7,174,990 |

| Indiana, State Housing & Community Development Authority, Single Family Mortgage Revenue, Series C-1, 5.0%, 7/1/2053 |

|

360,000 |

373,851 |

| |

|

|

18,095,203 |

| Iowa 0.3% |

| ||

| Iowa, Higher Education Loan Authority, Des Moines University Project, 5.375%, 10/1/2052 |

|

485,000 |

501,536 |

| Iowa, State Higher Education Loan Authority Revenue, Private College Facility, Des Moines University Project, 4.0%, 10/1/2045 |

|

885,000 |

789,700 |

| |

|

|

1,291,236 |

| Kentucky 0.9% |

| ||

| Kentucky, State Economic Development Finance Authority, Owensboro Health, Inc., Obligated Group: |

|

|

|

| Series A, 5.0%, 6/1/2045 |

|

320,000 |

321,282 |

| Series A, 5.25%, 6/1/2041 |

|

480,000 |

488,982 |

| DWS

Municipal Income Trust |

| |

19 |

| |

Principal

Amount ($) |

Value ($) | |

| Louisville & Jefferson County, KY, Metro Government Hospital Revenue, UOFL Health Project: |

|

|

|

| Series A, 5.0%, 5/15/2047 |

|

610,000 |

620,176 |

| Series A, 5.0%, 5/15/2052 |

|

1,960,000 |

1,981,218

|

| |

|

|

3,411,658 |

| Louisiana 2.5% |

| ||

| Louisiana, New Orleans Aviation Board, General Airport North Terminal, Series B, AMT, 5.0%, 1/1/2048 |

|

710,000 |

713,715 |

| Louisiana, Public Facilities Authority Revenue, Loyola University Project, 4.0%, 10/1/2051 |

|

850,000 |

705,128 |

| Louisiana, Public Facilities Authority Revenue, Ochsner Clinic Foundation Project, 5.0%, 5/15/2047 |

|

6,000,000 |

6,102,818 |

| New Orleans, LA, Aviation Board Special Facility Revenue, Parking Facilities Corp., Consol Garage System: |

|

|

|

| Series A, 5.0%, 10/1/2043, INS: AGMC |

|

1,020,000 |

1,066,430 |

| Series A, 5.0%, 10/1/2048, INS: AGMC |

|

1,140,000 |

1,185,112

|

| |

|

|

9,773,203 |

| Maryland 2.8% |

| ||

| Maryland, Stadium Authority Built To Learn Revenue, Series A, 4.0%, 6/1/2047 |

|

2,670,000 |

2,534,558 |

| Maryland, State Economic Development Corp., Student Housing Revenue, Morgan State University Project: |

|

|

|

| 5.0%, 7/1/2050 |

|

325,000 |

320,676 |

| 5.0%, 7/1/2056 |

|

2,550,000 |

2,493,070 |

| Series A, 5.75%, 7/1/2053 |

|

575,000 |

607,933 |

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Adventist Healthcare, Obligated Group, Series A, 5.5%, 1/1/2046 |

|

745,000 |

757,246 |

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Broadmead Inc.: |

|

|

|

| Series A, 5.0%, 7/1/2043 |

|

1,250,000 |

1,267,559 |

| Series A, 5.0%, 7/1/2048 |

|

3,000,000 |

3,026,028

|

| |

|

|

11,007,070 |

| Massachusetts 2.1% |

| ||

| Massachusetts, Educational Financing Authority, Issue M: |

|

|

|

| Series C, AMT, 3.0%, 7/1/2051 |

|

1,180,000 |

795,519 |

| Series B, AMT, 3.625%, 7/1/2038 |

|

1,365,000 |

1,256,688 |

| Series C, AMT, 4.125%, 7/1/2052 |

|

2,000,000 |

1,670,308 |

| Massachusetts, State Development Finance Agency Revenue, Northeastern University, Series A, 5.25%, 3/1/2037 |

|

2,500,000 |

2,533,304 |

| 20 |

| |

DWS Municipal Income Trust |

| |

Principal

Amount ($) |

Value ($) | |

| Massachusetts, State Development Finance Agency Revenue, Springfield College: |

|

|

|

| Series B, 4.0%, 6/1/2050 |

|

1,080,000 |

921,745 |

| Series A, 4.0%, 6/1/2056 |

|

1,295,000 |

1,069,985

|

| |

|

|

8,247,549 |

| Michigan 2.2% |

| ||

| Michigan, State Finance Authority Ltd. Obligation Revenue, Albion College: |

|

|

|

| 4.0%, 12/1/2046 |

|

410,000 |

353,174 |

| 4.0%, 12/1/2051 |

|

420,000 |

351,584 |

| Michigan, State Finance Authority Revenue, Series A, 4.0%, 2/15/2050 |

|

4,000,000 |

3,667,884 |

| Michigan, State Finance Authority Revenue, Michigan Finance Authority Tobacco Settlement Revenue, “1” , Series A, 4.0%,

6/1/2049 |

|

260,000 |

215,396 |

| Michigan, Strategic Fund, 75 Improvement P3 Project, AMT, 5.0%, 6/30/2048 |

|

2,200,000 |

2,121,176 |

| Wayne County, MI, Airport Authority Revenue, Series F, AMT, 5.0%, 12/1/2034 |

|

2,000,000 |

2,052,870

|

| |

|

|

8,762,084 |

| Minnesota 3.3% |

| ||

| Duluth, MN, Economic Development Authority, Health Care Facilities Revenue, Essentia Health Obligated Group: |

|

|

|

| Series A, 5.0%, 2/15/2048 |

|

1,800,000 |

1,818,253 |

| Series A, 5.0%, 2/15/2053 |

|

5,060,000 |

5,085,969 |

| Minneapolis, MN, Health Care Systems Revenue, Fairview Health Services, Series A, 5.0%, 11/15/2049 |

|

1,220,000 |

1,246,382 |

| Rochester, MN, Health Care Facilities Revenue, Mayo Clinic, Series B, 5.0%, 11/15/2035 |

|

4,000,000 |

4,705,578

|

| |

|

|

12,856,182 |

| Missouri 0.2% |

| ||

| Missouri, State Health & Educational Facilities Authority Revenue, Medical Research, Lutheran Senior Services: |

|

|

|

| 4.0%, 2/1/2042 |

|

545,000 |

439,974 |

| Series A, 5.0%, 2/1/2046 |

|

335,000 |

314,019 |

| |

|

|

753,993 |

| Nebraska 0.3% |

| ||

| Douglas County, NE, Hospital Authority No.2, Health Facilities, Children’s Hospital Obligated Group, 5.0%, 11/15/2047 |

|

1,330,000 |

1,354,477 |

| DWS

Municipal Income Trust |

| |

21 |

| |

Principal

Amount ($) |

Value ($) | |

| New Hampshire 0.5% |

| ||

| New Hampshire, Business Finance Authority Revenue, Series 2022-2, 4.0%, 10/20/2036 |

|

2,245,503 |

2,070,740 |

| New Jersey 6.0% |

| ||

| Atlantic County, NJ, Improvement Authority Lease Revenue, Atlantic City Campus Phase II Project, Series A, 4.0%, 7/1/2047, INS: AGMC |

|

190,000 |

176,239 |

| Camden Country, NJ, Improvement Authority School Revenue, KIPP Cooper Norcross Obligated Group, 6.0%, 6/15/2062 |

|

1,400,000 |

1,454,561 |

| New Jersey, Economic Development Authority, Self Designated Social Bonds: |

|

|

|

| Series QQQ, 4.0%, 6/15/2046 |

|

115,000 |

104,875 |

| Series QQQ, 4.0%, 6/15/2050 |

|

115,000 |

103,740 |

| New Jersey, State Covid-19 General Obligation Emergency Bonds: |

|

|

|

| Series A, 4.0%, 6/1/2030 |

|

430,000 |

453,275 |

| Series A, 4.0%, 6/1/2031 |

|

635,000 |

673,033 |

| New Jersey, State Economic Development Authority Revenue, Series BBB, Prerefunded, 5.5%, 6/15/2030 |

|

2,690,000 |

2,989,880 |

| New Jersey, State Economic Development Authority Revenue, The Goethals Bridge Replacement Project, AMT, 5.125%, 7/1/2042, INS: AGMC |

|

1,250,000 |

1,251,310 |

| New Jersey, State Economic Development Authority, State Government Buildings Project: |

|

|

|

| Series A, 5.0%, 6/15/2042 |

|

345,000 |

352,390 |

| Series A, 5.0%, 6/15/2047 |

|

385,000 |

391,357 |

| New Jersey, State Educational Facilities Authority Revenue, Steven Institute of Technology, Series A, 4.0%, 7/1/2050 |

|

995,000 |

870,556 |

| New Jersey, State Educational Facilities Authority Revenue, Stockton University, Series A, 5.0%, 7/1/2041 |

|

685,000 |

693,641 |

| New Jersey, State Higher Education Assistance Authority, Student Loan Revenue, Series B, AMT, 2.5%, 12/1/2040 |

|

415,000 |

338,014 |

| New Jersey, State Transportation Trust Fund Authority, Series AA, 4.0%, 6/15/2045 |

|

435,000 |

397,941 |

| New Jersey, State Transportation Trust Fund Authority, Transportation Program, 5.0%, 6/15/2046 |

|

5,600,000 |

5,702,630 |

| New Jersey, State Transportation Trust Fund Authority, Transportation Systems: |

|

|

|

| Series AA, 4.0%, 6/15/2050 |

|

3,320,000 |

2,994,915 |

| Series A, 5.0%, 12/15/2034 |

|

1,855,000 |

1,970,200 |

| Series A, 5.0%, 12/15/2036 |

|

475,000 |

497,860 |

| New Jersey, State Turnpike Authority Revenue, Series B, 5.0%, 1/1/2040 |

|

65,000 |

69,126 |

| 22 |

| |

DWS Municipal Income Trust |

| |

Principal

Amount ($) |

Value ($) | |

| New Jersey, Tobacco Settlement Financing Corp., Series A, 5.25%, 6/1/2046 |

|

1,315,000 |

1,324,977 |

| South Jersey, NJ, Transportation Authority System Revenue, Series A, 5.25%, 11/1/2052 |

|

800,000 |

834,807 |

| |

|

|

23,645,327 |

| New York 12.3% |

| ||

| New York, Metropolitan Transportation Authority Revenue: |

|

|

|

| Series A-1, 4.0%, 11/15/2044 |

|

1,000,000 |

856,423 |

| Series A-1, 4.0%, 11/15/2045 |

|

1,000,000 |

851,685 |

| Series C, 5.0%, 11/15/2038 |

|

6,000,000 |

6,007,262 |

| Series D, 5.0%, 11/15/2038 |

|

1,090,000 |

1,092,826 |

| Series C, 5.0%, 11/15/2042 |

|

5,000,000 |

4,948,966 |

| Series A-1, 5.25%, 11/15/2039 |

|

4,000,000 |

4,017,588 |

| Series C-1, 5.25%, 11/15/2055 |

|

520,000 |

525,207 |

| New York, Metropolitan Transportation Authority Revenue, Green Bond, Series A-1, 5.0%, 11/15/2048 |

|

2,000,000 |

1,962,218 |

| New York, Port Authority of New York & New Jersey Consolidated, One Hundred Eighty-Fourth: |

|

|

|

| 5.0%, 9/1/2036 |

|

205,000 |

211,254 |

| 5.0%, 9/1/2039 |

|

510,000 |

523,543 |

| New York, State Dormitory Authority Revenues, Non-State Supported Debt, The New School: |

|

|

|

| Series A, 4.0%, 7/1/2047 |

|

150,000 |

130,499 |

| Series A, 4.0%, 7/1/2052 |

|

175,000 |

148,933 |

| New York, State Transportation Development Corp., Special Facilities Revenue, Delta Air Lines, Inc., LaGuardia Airport C&D Redevelopment, AMT, 5.0%, 1/1/2033 |

|

410,000 |

415,301 |

| New York, State Transportation Development Corp., Special Facilities Revenue, Terminal 4 John F. Kennedy, International Project, AMT, 5.0%, 12/1/2041 |

|

265,000 |

262,035 |

| New York, State Urban Development Corp. Revenue, Personal Income Tax, Series A, 4.0%, 3/15/2045 |

|

8,830,000 |

8,403,947 |

| New York, State Urban Development Corp. Revenue, State Personal Income Tax, Series C, 5.0%, 3/15/2047 |

|

3,500,000 |

3,732,392 |

| New York, State Urban Development Corp., Income Tax, 3.0%, 3/15/2050 |

|

2,000,000 |

1,523,442 |

| New York, State Urban Development Corp., State Personal Income Tax Revenue, Series C, 3.0%, 3/15/2048 |

|

3,475,000 |

2,685,738 |

| New York, TSASC, Inc., Series A, 5.0%, 6/1/2041 |

|

150,000 |

151,793 |

| New York City, NY, Housing Development Corp., Series C-1, 4.25%, 11/1/2052 |

|

3,000,000 |

2,728,042 |

| New York, NY, General Obligation: |

|

|

|

| Series 2, 1.96% (b), 12/1/2022 |

|

300,000 |

300,000 |

| Series 3, 2.1% (b), 12/1/2022 |

|

150,000 |

150,000 |

| DWS

Municipal Income Trust |

| |

23 |

| |

Principal

Amount ($) |

Value ($) | |

| Series A, 4.0%, 8/1/2040 |

|

3,500,000 |

3,472,153 |

| Series B-1, 5.25%, 10/1/2047 |

|

500,000 |

553,435 |

| Port Authority of New York & New Jersey, Series 207, AMT, 5.0%, 9/15/2048 |

|

1,875,000 |

1,912,708 |

| Port Authority of New York & New Jersey, One Hundred Ninety-Third, AMT, 5.0%, 10/15/2035 |

|

800,000 |

817,521 |

| |

|

|

48,384,911 |

| Ohio 3.2% |

| ||

| Buckeye, OH, Tobacco Settlement Financing Authority, “1” , Series A, 4.0%, 6/1/2048 |

|

1,995,000 |

1,738,234 |

| Chillicothe, OH, Hospital Facilities Revenue, Adena Health System Obligated Group Project, 5.0%, 12/1/2047 |

|

1,785,000 |

1,808,739 |

| Franklin County, OH, Trinity Health Corp. Revenue, Series 2017, 5.0%, 12/1/2046 |

|

2,950,000 |

2,995,297 |

| Ohio, Akron, Bath & Copley Joint Township Hospital District Revenue, 5.25%, 11/15/2046 |

|

2,320,000 |

2,346,478 |

| Ohio, State Turnpike Commission, Junior Lien, Infrastructure Projects, Series A-1, 5.25%, 2/15/2039 |

|

3,520,000 |

3,540,030

|

| |

|

|

12,428,778 |

| Oregon 0.9% |

| ||

| Oregon, Portland Airport Revenue, Series 25B, AMT, 5.0%, 7/1/2049 |

|

3,335,000 |

3,404,112 |

| Pennsylvania 7.4% |

| ||

| Allegheny County, PA, Hospital Development Authority, Allegheny Health Network Obligated Group, Series A, 5.0%, 4/1/2047 |

|

3,090,000 |

3,128,955 |

| Pennsylvania, Certificate of Participations, Series A, 5.0%, 7/1/2043 |

|

460,000 |

484,901 |

| Pennsylvania, Commonwealth Financing Authority, Series A, 5.0%, 6/1/2035 |

|

1,560,000 |

1,623,036 |

| Pennsylvania, Commonwealth Financing Authority, Tobacco Master Settlement Payment Revenue Bonds: |

|

|

|

| 5.0%, 6/1/2034 |

|

750,000 |

810,109 |

| 5.0%, 6/1/2035 |

|

375,000 |

402,508 |

| Pennsylvania, Economic Development Financing Authority, Series A, 4.0%, 10/15/2051 |

|

3,000,000 |

2,674,729 |

| Pennsylvania, Geisinger Authority Health System Revenue, Series A-1, 5.0%, 2/15/2045 |

|

20,000 |

20,301 |

| Pennsylvania, State Higher Educational Facilities Authority Revenue, University of Pennsylvania Health System, 5.0%, 8/15/2049 |

|

5,000,000 |

5,198,564 |

| Pennsylvania, State Turnpike Commission Revenue: |

|

|

|

| Series B, 4.0%, 12/1/2051 |

|

2,655,000 |

2,540,896 |

| Series A, 5.0%, 12/1/2038 |

|

2,030,000 |

2,078,770 |

| 24 |

| |

DWS Municipal Income Trust |

| |

Principal

Amount ($) |

Value ($) | |

| Series B-1, 5.0%, 6/1/2042 |

|

2,000,000 |

2,060,055 |

| Series A, 5.0%, 12/1/2044 |

|

4,665,000 |

4,851,969 |

| Series B, 5.0%, 12/1/2051 |

|

665,000 |

697,383 |

| Philadelphia, PA, Airport Revenue, Series B, AMT, 5.0%, 7/1/2047 |

|

915,000 |

924,721 |

| Philadelphia, PA, School District, Series B, 5.0%, 9/1/2043 |

|

1,500,000 |

1,576,807

|

| |

|

|

29,073,704 |

| South Carolina 4.8% |

| ||

| Charleston County, SC, Airport District, Airport System Revenue, Series A, AMT, Prerefunded, 5.875%, 7/1/2032 |

|

6,560,000 |

6,680,416 |

| South Carolina, State Ports Authority Revenue, Series B, AMT, 4.0%, 7/1/2059 |

|

6,000,000 |

5,194,404 |

| South Carolina, State Public Service Authority Revenue, Series E, 5.25%, 12/1/2055 |

|

4,000,000 |

4,024,693 |

| South Carolina, State Public Service Authority Revenue, Santee Cooper, Series A, Prerefunded, 5.75%, 12/1/2043 |

|

3,000,000 |

3,092,817

|

| |

|

|

18,992,330 |

| South Dakota 0.2% |

| ||

| Lincon County, SD, Economic Development Revenue, Augustana College Association Project: |

|

|

|

| Series A, 4.0%, 8/1/2051 |

|

375,000 |

297,966 |

| Series A, 4.0%, 8/1/2056 |

|

250,000 |

191,982 |

| Series A, 4.0%, 8/1/2061 |

|

325,000 |

242,065 |

| |

|

|

732,013 |

| Tennessee 1.0% |

| ||

| Greeneville, TN, Health & Educational Facilities Board Hospital Revenue, Ballad Health Obligation Group: |

|

|

|

| Series A, 5.0%, 7/1/2036 |

|

1,040,000 |

1,074,811 |

| Series A, 5.0%, 7/1/2044 |

|

1,600,000 |

1,621,699 |

| Nashville & Davidson County, TN, Metropolitan Government Health & Educational Facilities Board Revenue, Blakeford At Green Hills Corp., Series A, 4.0%, 11/1/2045 |

|

1,500,000 |

1,210,528

|

| |

|

|

3,907,038 |

| Texas 18.9% |

| ||

| Central Texas, Regional Mobility Authority Revenue, Senior Lien: |

|

|

|

| Series A, Prerefunded, 5.0%, 1/1/2040 |

|

1,155,000 |

1,223,640 |

| Series E, 5.0%, 1/1/2045 |

|

300,000 |

313,444 |

| DWS

Municipal Income Trust |

| |

25 |

| |

Principal

Amount ($) |

Value ($) | |

| Clifton, TX, Higher Education Finance Corp., Idea Public Schools, Series T, 4.0%, 8/15/2042 |

|

400,000 |

400,765 |

| Houston, TX, Airport System Revenue, Series A, AMT, 5.0%, 7/1/2041 |

|

2,250,000 |

2,309,069 |

| Newark, TX, Higher Education Finance Corp., Texas Revenue, Abilene Christian University Project, Series A, 4.0%, 4/1/2057 |

|

3,000,000 |

2,556,250 |

| North Texas, Tollway Authority Revenue: |

|

|

|

| Series B, 5.0%, 1/1/2040 |

|

2,060,000 |

2,064,253 |

| 5.0%, 1/1/2048 |

|

4,710,000 |

4,838,103 |

| 5.0%, 1/1/2050 |

|

1,435,000 |

1,472,144 |

| San Antonio, TX, Education Facilities Corp. Revenue, University of the Incarnate Word Project: |

|

|

|

| Series A, 4.0%, 4/1/2046 |

|

1,520,000 |

1,252,157 |

| Series A, 4.0%, 4/1/2051 |

|

3,000,000 |

2,386,776 |

| Series A, 4.0%, 4/1/2054 |

|

790,000 |

614,300 |

| Tarrant County, TX, Cultural Education Facilities Finance Corp. Revenue, Christus Health Obligated Group: |

|

|

|

| Series B, 5.0%, 7/1/2034 |

|

3,000,000 |

3,202,309 |

| Series B, 5.0%, 7/1/2048 |

|

5,000,000 |

5,089,984 |

| Temple, TX, Tax Increment, Reinvestment Zone No. 1: |

|

|

|

| Series A, 4.0%, 8/1/2039, INS: BAM |

|

165,000 |

163,788 |

| Series A, 4.0%, 8/1/2041, INS: BAM |

|

200,000 |

193,142 |

| Texas, Dallas/Fort Worth International Airport Revenue, Series F, 5.25%, 11/1/2033 |

|

3,500,000 |

3,565,634 |

| Texas, Grand Parkway Transportation Corp., System Toll Revenue: |

|

|

|

| Series B, Prerefunded, 5.0%, 4/1/2053 |

|

3,500,000 |

3,570,751 |

| Series B, Prerefunded, 5.25%, 10/1/2051 |

|

5,000,000 |

5,111,274 |

| Texas, Lower Colorado River Authority, LCRA Transmission Services Corp., Project, 5.0%, 5/15/2048 |

|

6,250,000 |

6,443,351 |

| Texas, New Hope Cultural Education Facilities Finance Corp., Retirement Facilities Revenue, Westminster Project: |

|

|

|

| 4.0%, 11/1/2049 |

|

270,000 |

208,433 |

| 4.0%, 11/1/2055 |

|

305,000 |

226,170 |

| Texas, Private Activity Bond, Surface Transportation Corp. Revenue, Senior Lien, North Mobility Partners Segments LLC, AMT, 5.0%, 6/30/2058 |

|

3,000,000 |

2,980,119 |

| Texas, Regional Mobility Authority Revenue, Senior Lien, Series B, 4.0%, 1/1/2051 |

|

7,815,000 |

7,137,731 |

| Texas, SA Energy Acquisition Public Facility Corp., Gas Supply Revenue, 5.5%, 8/1/2025, GTY: Goldman Sachs Group, Inc. |

|

7,250,000 |

7,511,568 |

| 26 |

| |

DWS Municipal Income Trust |

| |

Principal

Amount ($) |

Value ($) | |

| Texas, State Municipal Gas Acquisition & Supply Corp. I, Gas Supply Revenue, Series D, 6.25%, 12/15/2026, GTY: Merrill Lynch & Co. |

|

2,755,000 |

2,879,125 |

| Texas, State Transportation Commission, Turnpike Systems Revenue, Series C, 5.0%, 8/15/2034 |

|

1,235,000 |

1,259,709 |

| Texas, State Water Development Board Revenue, State Water Implementation Revenue Fund, Series A, 4.0%, 10/15/2049 |

|

2,815,000 |

2,724,549 |

| Texas, University of Texas Revenue, Series B, 5.0%, 8/15/2049 |

|

2,250,000 |

2,588,525

|

| |

|

|

74,287,063 |

| Utah 0.6% |

| ||

| Salt Lake City, UT, Airport Revenue: |

|

|

|

| Series A, AMT, 5.0%, 7/1/2043 |

|

960,000 |

979,485 |

| Series A, AMT, 5.0%, 7/1/2048 |

|

575,000 |

581,503 |

| Utah, Infrastructure Agency Telecommunications & Franchise Tax Revenue, Pleasant Gove City Project: |

|

|

|

| 4.0%, 10/15/2041 |

|

275,000 |

263,937 |

| 4.0%, 10/15/2048 |

|

680,000 |

618,365 |

| |

|

|

2,443,290 |

| Virginia 1.7% |

| ||

| Stafford County, VA, Economic Development Authority, Hospital Facilities Revenue, Mary Washington Healthcare: |

|

|

|

| 5.0%, 10/1/2042 |

|

140,000 |

148,136 |

| 5.0%, 10/1/2047 |

|

465,000 |

486,731 |

| 5.0%, 10/1/2052 |

|

600,000 |

622,353 |

| Virginia, Small Business Financing Authority Revenue, 95 Express Lanes LLC Project, AMT, 4.0%, 1/1/2048 |

|

560,000 |

468,064 |

| Virginia, Small Business Financing Authority, Elizabeth River Crossings OPCO LLC Project, AMT, 4.0%, 1/1/2039 |

|

575,000 |

531,604 |

| Virginia, Small Business Financing Authority, I-495 Hot Lanes Project: |

|

|

|

| AMT, 5.0%, 12/31/2052 |

|

625,000 |

642,143 |

| AMT, 5.0%, 12/31/2057 |

|

315,000 |

322,367 |

| Virginia, Small Business Financing Authority, Private Activity Revenue, Transform 66 P3 Project, AMT, 5.0%, 12/31/2052 |

|

3,435,000 |

3,429,547

|

| |

|

|

6,650,945 |

| Washington 2.7% |

| ||

| Washington, Port of Seattle Revenue: |

|

|

|

| Series A, AMT, 5.0%, 5/1/2043 |

|

1,935,000 |

1,968,830 |

| DWS

Municipal Income Trust |

| |

27 |

| |

Principal

Amount ($) |

Value ($) | |

| AMT, 5.0%, 4/1/2044 |

|

2,000,000 |

2,052,227 |

| Washington, State Convention Center Public Facilities District, 5.0%, 7/1/2043 |

|

6,000,000 |

5,959,439 |

| Washington, State Housing Finance Commission Municipal Certificates, “A” , Series A-1, 3.5%, 12/20/2035 |

|

601,728 |

539,775 |

| |

|

|

10,520,271 |

| West Virginia 1.0% |

| ||

| West Virginia, State Hospital Finance Authority, State University Health System Obligated Group: |

|

|

|

| Series A, 5.0%, 6/1/2042 |

|

2,015,000 |

2,048,288 |

| Series A, 5.0%, 6/1/2047 |

|

2,010,000 |

2,031,081 |

| |

|

|

4,079,369 |

| Wisconsin 2.4% |

| ||

| Wisconsin, Public Finance Authority, Eastern Michigan University, Series A-1, 5.625%, 7/1/2055, INS: BAM |

|

1,230,000 |

1,290,239 |

| Wisconsin, Public Finance Authority, Education Revenue, Triad Educational Services Ltd., Series 2021 A, 4.0%, 6/15/2061 |

|

5,200,000 |

3,933,372 |

| Wisconsin, Public Finance Authority, Fargo-Moorhead Metropolitan Area Flood Risk Management Project, AMT, 4.0%, 9/30/2051 |

|

1,590,000 |

1,258,693 |

| Wisconsin, Public Finance Authority, Hospital Revenue, Series A, 5.0%, 10/1/2044 |

|

2,925,000 |

2,975,598 |

| |

|

|

9,457,902 |

| Guam 0.1% |

| ||

| Guam, International Airport Authority Revenue: |

|

|

|

| Series C, AMT, 6.375%, 10/1/2043 |

|

255,000 |

261,801 |

| Series C, AMT, Prerefunded, 6.375%, 10/1/2043 |

|

280,000 |

287,468 |

| |

|

|

549,269 |

| Total Municipal Investments (Cost $580,785,595) |

561,449,975 | ||

| Underlying Municipal Bonds of Inverse Floaters (c) 19.2% |

| ||

| Florida 2.7% |

| ||

| Orange County, FL, School Board, Certificates of Participations, Series C, 5.0%, 8/1/2034 (d) |

|

10,000,000 |

10,555,608

|

| Trust: Florida, School Board, Series 2016-XM0182, 144A, 12.23%, 2/1/2024, Leverage Factor at purchase date: 4 to 1 |

|

|

|

| 28 |

| |

DWS Municipal Income Trust |

| |

Principal

Amount ($) |

Value ($) | |

| Massachusetts 2.8% |

| ||

| Massachusetts, State Development Finance Agency Revenue, Partners Healthcare System, Inc., Series Q, 5.0%, 7/1/2035 (d) |

|

10,425,000 |

10,955,033

|

| Trust: Massachusetts, State Development Finance Agency Revenue, Series 2016-XM0137, 144A, 12.306%, 1/1/2024, Leverage Factor at purchase date: 4 to 1 |

|

|

|

| New York 5.4% |

| ||

| New York, State Urban Development Corp. Revenue, Personal Income Tax, Series C-3, 5.0%, 3/15/2040 (d) |

|

10,000,000 |

10,569,281

|

| Trust: New York, State Urban Development Corp. Revenue, Personal Income Tax, Series 2018-XM0580, 144A, 12.755%, 9/15/2025, Leverage Factor at purchase date: 4 to 1 |

|

|

|

| New York City, NY, Transitional Finance Authority, Building AID Revenue, Series S-4A, 5.0%, 7/15/2034 (d) |

|

7,165,000 |

7,775,944

|

| Trust: New York, Transitional Finance Authority, Building AID Revenue, Series 2018-XM0620, 144A, 12.644%, 1/15/2026, Leverage Factor at purchase date: 4 to 1 |

|

|

|

| New York City, NY, Transitional Finance Authority, Building AID Revenue, Series S-3, 5.0%, 7/15/2038 (d) |

|

2,685,000 |

2,859,081

|

| Trust: New York, Transitional Finance Authority, Building AID Revenue, Series 2018-XM0620, 144A, 12.684%, 1/15/2026, Leverage Factor at purchase date: 4 to 1 |

|

|

|

| |

|

|

21,204,306 |

| Pennsylvania 2.8% |

| ||

| Pennsylvania, Southeastern Pennsylvania Transportation Authority, 5.25%, 6/1/2047 (d) |

|

10,000,000 |

10,987,515

|

| Trust: Pennsylvania, Southeastern Pennsylvania Transportation Authority, Series 2022-XM1057, 144A, 13.77%, 6/1/2030, Leverage Factor at purchase date: 4 to 1 |

|

|

|

| Texas 2.8% |

| ||

| Texas, State General Obligation, Series B, 5.0%, 2/1/2045 (d) |

|

10,000,000 |

11,017,448

|

| Trust: Texas, State General Obligation, Series 2022-XM1063, 12.83%, 2/1/2030, Leverage Factor at purchase date: 4 to 1 |

|

|

|

| DWS

Municipal Income Trust |

| |

29 |

| |

Principal

Amount ($) |

Value ($) | |

| Washington 2.7% |

| ||

| Washington, State General Obligation, Series D, 5.0%, 2/1/2035 (d) |

|

10,000,000 |

10,754,560

|

| Trust: Washington, State General Obligation, Series 2017-XM0477, 144A, 12.32%, 8/1/2024, Leverage Factor at purchase date: 4 to 1 |

|

|

|

| Total Underlying Municipal Bonds of Inverse Floaters (Cost

$75,747,867) |

75,474,470 | ||

| |

Shares |

Value ($) | |

| Open-End Investment Companies 0.2% |

| ||

| BlackRock Liquidity Funds MuniCash Portfolio, Institutional Shares, 1.8% (e) (Cost $679,062) |

|

678,722 |

678,790 |

| |

|

% of Net

Assets |

Value ($) |

| Total Investment Portfolio (Cost $657,212,524) |

162.0 |

637,603,235 | |

| Floating Rate Notes (c) |

(13.4) |

(52,700,000) | |

| Series 2020-1 VMTPS, net of deferred offering costs |

(50.5) |

(198,623,383) | |

| Other Assets and Liabilities, Net |

1.9 |

7,266,445 | |

| Net Assets Applicable to Common Shareholders |

100.0 |

393,546,297 | |

| (a) |

Variable or floating rate security. These securities are shown at their current rate as of November 30, 2022. For securities based on a published reference rate and spread, the reference rate and spread are indicated within the description above. Certain variable rate securities are not based on a published reference rate and spread but adjust periodically based on current market conditions, prepayment of underlying positions and/or other variables. Securities with a floor or ceiling feature are disclosed at the inherent rate, where applicable. |

| (b) |

Variable rate demand notes are securities whose interest rates are reset periodically (usually daily mode or weekly mode) by remarketing agents based on current market levels, and are not directly set as a fixed spread to a reference rate. These securities may be redeemed at par by the holder through a put or tender feature, and are shown at their current rates as of November 30, 2022. Date shown reflects the earlier of demand date or stated maturity date. |

| (c) |

Securities represent the underlying municipal obligations of inverse floating rate obligations held by the Fund. The Floating Rate Notes represents leverage to the Fund and is the amount owed to the floating rate note holders. |

| (d) |

Security forms part of the below inverse floater. The Fund accounts for these inverse floaters as a form of secured borrowing, by reflecting the value of the underlying bond in the investments of the Fund and the amount owed to the floating rate note holder as a liability. |

| (e) |

Current yield; not a coupon rate. |

| 144A: Security exempt

from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in

transactions exempt from registration, normally to qualified institutional buyers. |

| 30 |

| |

DWS Municipal Income Trust |

| AGMC: Assured Guaranty Municipal Corp. |

| AMT: Subject to alternative minimum tax. |

| BAM: Build America Mutual |

| GTY: Guaranty Agreement |

| INS: Insured |

| NATL: National Public Finance Guarantee Corp. |

| Prerefunded: Bonds which are prerefunded are collateralized usually by U.S. Treasury

securities which are held in escrow and used to pay principal and interest on tax-exempt

issues and to retire the bonds in full at the earliest refunding date. |

| Assets |

Level 1 |

Level 2 |

Level 3 |

Total |

| Municipal Investments (a) |

$ — |

$636,924,445

|

$—

|

$636,924,445 |

| Open-End Investment Companies |

678,790 |

— |

— |

678,790 |

| Total |

$678,790 |

$636,924,445 |

$—

|

$637,603,235 |

| (a) |

See

Investment Portfolio for additional detailed categorizations. |

| DWS

Municipal Income Trust |

| |

31 |

| Assets |

|

| Investment in securities, at value (cost $657,212,524) |

$ 637,603,235 |

| Receivable for investments sold |

874,337 |

| Interest receivable |

8,331,903 |

| Other assets |

7,103 |

| Total assets |

646,816,578 |

| Liabilities |

|

| Payable for investments purchased |

1,020,833 |

| Payable for floating rate notes issued |

52,700,000 |

| Interest expense payable on preferred shares |

542,866 |

| Accrued management fee |

270,787 |

| Accrued Trustees' fees |

6,498 |

| Other accrued expenses and payables |

105,914 |

| Series 2020-1 VMTPS, net of deferred offering costs (liquidation value $198,750,000, see page 41 for more details) |

198,623,383 |

| Total liabilities |

253,270,281 |

| Net assets applicable to common shareholders, at value |

$393,546,297 |

| Net Assets Applicable to Common Shareholders Consist of |

|

| Distributable earnings (loss) |

(37,778,739) |

| Paid-in capital |

431,325,036 |

| Net assets applicable to common shareholders, at value |

$393,546,297 |

| Net Asset Value |

|

| Net Asset Value per common share

($393,546,297 ÷ 39,500,938 outstanding shares of beneficial interest,

$.01 par value, unlimited number of common shares authorized) |

$9.96 |

| 32 |

| |

DWS Municipal Income Trust |

| Investment Income |

|

| Income: |

|

| Interest |

$ 25,663,014 |

| Expenses: |

|

| Management fee |

3,453,129 |

| Services to shareholders |

29,074 |

| Custodian fee |

5,888 |

| Professional fees |

104,730 |

| Reports to shareholders |

62,997 |

| Trustees' fees and expenses |

26,725 |

| Interest expense and amortization of deferred cost on Series 2020-1 VMTPS |

4,404,435 |

| Interest expense on floating rate notes |

851,801 |

| Stock Exchange listing fees |

38,464 |

| Other |

59,158 |

| Total expenses |

9,036,401 |

| Net investment income |

16,626,613 |

| Realized and Unrealized Gain (Loss) |

|

| Net realized gain (loss) from investments |

(20,935,445) |

| Change in net unrealized appreciation (depreciation) on investments |

(87,050,307) |

| Net gain (loss) |

(107,985,752) |

| Net increase (decrease) in net assets resulting from operations |

$ (91,359,139)

|

| DWS

Municipal Income Trust |

| |

33 |

| Increase (Decrease) in Cash: Cash Flows from Operating Activities |

|

| Net increase (decrease) in net assets resulting from operations |

$(91,359,139) |

| Adjustments to reconcile net increase (decrease) in net assets resulting from operations to net cash provided by (used in) operating activities: |

|

| Purchases of long-term investments |

(378,318,452) |

| Net amortization of premium/(accretion of discount) |

4,810,772 |

| Proceeds from sales and maturities of long-term investments |

372,368,700 |

| Amortization of deferred offering cost on Series 2020-1 VMTPS |

132,543 |

| (Increase) decrease in interest receivable |

504,383 |

| (Increase) decrease in other assets |

2,283 |

| (Increase) decrease in receivable for investments sold |

(359,337) |

| Increase (decrease) in payable for investments purchased |

1,020,833 |

| Increase (decrease) in payable for investments purchased - when issued securities |

(409,040) |

| Increase (decrease) in other accrued expenses and payables |

(49,671) |

| Change in unrealized (appreciation) depreciation on investments |

87,050,307 |

| Net realized (gain) loss from investments |

20,935,445 |

| Cash provided by (used in) operating activities |

$16,329,627 |

| Cash Flows from Financing Activities |

|

| Distributions paid (net of reinvestment of distributions) |

(16,329,627) |

| Cash provided by (used in) financing activities |

(16,329,627) |

| Increase (decrease) in cash |

— |

| Cash at beginning of period |

— |

| Cash at end of period |

$— |

| Supplemental disclosure |

|

| Interest expense paid on preferred shares |

$(3,932,109) |

| Interest expense paid and fees on floating rate notes issued |

$(851,801) |

| 34 |

| |

DWS Municipal Income Trust |

| |

Years Ended November 30, | |

| Increase (Decrease) in Net Assets |

2022 |

2021 |

| Operations: |

|

|

| Net investment income |

$ 16,626,613 |

$ 18,747,384 |

| Net realized gain (loss) |

(20,935,445) |

645,624 |

| Change in net unrealized appreciation (depreciation) |

(87,050,307) |

2,526,215 |

| Net increase (decrease) in net assets applicable to common shareholders |

(91,359,139) |

21,919,223 |

| Distributions to common shareholders |

(16,669,410) |

(21,188,345) |

| Increase (decrease) in net assets |

(108,028,549) |

730,878 |

| Net assets at beginning of period applicable to common shareholders |

501,574,846 |

500,843,968 |

| Net assets at end of period applicable to common shareholders |

$393,546,297 |

$501,574,846

|

| Other Information: |

|

|

| Common shares outstanding at beginning of period |

39,500,938 |

39,500,938 |

| Common shares outstanding at end of period |

39,500,938 |

39,500,938 |

| DWS

Municipal Income Trust |

| |

35 |

| |

Years Ended November 30, | ||||

| |

2022 |

2021 |

2020 |

2019 |

2018 |

| Selected Per Share Data Applicable to Common Shareholders |

|||||

| Net asset value, beginning of period |

$12.70 |

$12.68 |

$12.58 |

$11.78 |

$12.50

|

| Income (loss) from investment operations: |

|

|

|

|

|

| Net investment incomea |

.42 |

.47 |

.51 |

.50 |

.56 |

| Net realized and unrealized gain (loss) |

(2.74) |

.08 |

.08 |

.85 |

(.66) |

| Total from investment operations |

(2.32) |

.55 |

.59 |

1.35 |

(.10) |

| Less distributions applicable to common shareholders from: |

|

|

|

|

|

| Net investment income |

(.42) |

(.50) |

(.47) |

(.52) |

(.61) |

| Net realized gains |

— |

(.03) |

(.02) |

(.03) |

(.01) |

| Total distributions |

(.42) |

(.53) |

(.49) |

(.55) |

(.62) |

| Net asset value, end of period |

$9.96 |

$12.70 |

$12.68 |

$12.58 |

$11.78

|

| Market price, end of period |

$8.93 |

$12.10 |

$11.34 |

$11.49 |

$10.34

|

| Total Return |

|

|

|

|

|

| Based on net asset value (%)b

|

(18.12) |

4.75 |

5.33c |

12.14 |

(.35) |

| Based on market price (%)b |

(22.95) |

11.60 |

3.14c |

16.69 |

(7.18) |

| Ratios to Average Net Assets Applicable to Common Shareholders and

Supplemental Data | |||||

| Net assets, end of period ($ millions) |

394 |

502 |

501 |

497 |

465 |

| Ratio of expenses before expense reductions (%) (including interest expense)d,e

|

2.11 |

1.47 |

1.82 |

2.21 |

2.16 |

| Ratio of expenses after expense reductions (%) (including interest expense)d,f

|

2.11 |

1.47 |

1.64c |

2.21 |

2.16 |

| Ratio of expenses after expense reductions (%) (excluding interest expense)g

|

.91 |

.85 |

.71 |

.85 |

.86 |

| Ratio of net investment income (%) |

3.87 |

3.72 |

4.11 |

4.04 |

4.58 |

| Portfolio turnover rate (%) |

55 |

19 |

28 |

18 |

51 |

| Senior Securities |

|

|

|

|

|

| Preferred Shares information at period end, aggregate amount outstanding: |

|

|

|

|

|

| Series 2018 MTPS ($ millions) |

— |

— |

— |

199 |

199 |

| Series 2020-1 VMTPS ($ millions) |

199 |

199 |

199 |

— |

— |

| Asset coverage per share ($)h

|

149,005 |

176,182 |

175,998 |

17,503 |

16,705 |

| Liquidation and market price per share ($) |

50,000 |

50,000 |

50,000 |

5,000 |

5,000 |

| a |

Based on average common shares outstanding during the period. |

| 36 |

| |

DWS Municipal Income Trust |

| b |

Total return based on net asset value reflects changes in the Fund’s net asset value during each period. Total return based on market price reflects changes in market price. Each figure assumes that dividend and capital gain distributions, if any, were reinvested. These figures will differ depending upon the level of any discount from or premium to net asset value at which the Fund’s shares traded during the period. |

| c |

For the year ended November 30, 2020, the Advisor had agreed to voluntarily reduce its management fee. Total return would have been lower had expenses not been reduced. |

| d |

Interest expense represents interest and fees on short-term floating rate notes issued in conjunction with inverse floating rate securities and interest paid to shareholders of Series 2018 MTPS and Series 2020-1 VMTPS. |

| e |

The ratio of expenses before expense reductions (based on net assets of common and Preferred Shares, including interest expense) was 1.44%, 1.06%, 1.30%, 1.57% and 1.52% for the years ended November 30, 2022, 2021, 2020, 2019 and 2018, respectively. |

| f |

The ratio of expenses after expense reductions (based on net assets of common and Preferred Shares, including interest expense) was 1.44%, 1.06%, 1.17%, 1.57% and 1.52% for the years ended November 30, 2022, 2021, 2020, 2019 and 2018, respectively. |

| g |

The ratio of expenses after expense reductions (based on net assets of common and Preferred Shares, excluding interest expense) was 0.62%, 0.61%, 0.50%, 0.61% and 0.61% for the years ended November 30, 2022, 2021, 2020, 2019 and 2018, respectively. |

| h |

Asset coverage per share equals net assets of common shares plus the liquidation value of the Preferred Shares divided by the total number of Preferred Shares outstanding at the end of the period. |

| DWS

Municipal Income Trust |

| |

37 |

| 38 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

39 |

| 40 |

| |

DWS Municipal Income Trust |

| Undistributed tax-exempt income |

$ 364,500 |

| Capital loss carryforwards |

$ (21,823,000) |

| Net unrealized appreciation (depreciation) on investments |

$ (16,320,811)

|

| |

Years Ended November 30, | |

| |

2022 |

2021 |

| Distributions from tax-exempt income |

$

16,669,410 |

$ 19,908,510 |

| Distributions from ordinary income* |

$ — |

$

1,279,835 |

| * |

For tax purposes, short-term capital gain distributions are considered ordinary income distributions. |

| DWS

Municipal Income Trust |

| |

41 |

| 42 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

43 |

| 44 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

45 |

| 46 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

47 |

| 48 |

| |

DWS Municipal Income Trust |

| |

Number of Votes: | |

| |

For |

Withheld |

| Chad D. Perry |

29,021,143 |

3,650,700 |

| Catherine Schrand |

29,011,704 |

3,660,139 |

| |

Number of Votes: | |

| |

For |

Withheld |

| Dawn-Marie Driscoll |

3,975 |

0 |

| Keith R. Fox |

3,975 |

0 |

| DWS

Municipal Income Trust |

| |

49 |

| 50 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

51 |

| 52 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

53 |

| 54 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

55 |

| 56 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

57 |

| 58 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

59 |

| 60 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

61 |

| 62 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

63 |

| 64 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

65 |

| 66 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

67 |

| 68 |

| |

DWS Municipal Income Trust |

As described above, the Fund employs leverage through its issuance of preferred stock (the Series 2020-1 VMTPS) and its participation in tender option bond (TOB) transactions. The table below is furnished in response to requirements of the SEC. It is designed to illustrate the effects of leverage through the use of senior securities (such as the Fund’s Series 2020-1 VMTPS), as that term is defined under Section 18 of the 1940 Act, as well as certain other forms of leverage (such as the Fund’s participation in TOB transactions) on common share total return.

| Assumed Return on Portfolio (Net of Expenses) |

–10.00% |

–5.00% |

0.00% |

5.00% |

10.00% |

| Corresponding Return to Common Shareholders |

–20.46% |

–10.88% |

–1.30% |

8.28% |

17.85% |

| DWS

Municipal Income Trust |

| |

69 |

| 70 |

| |

DWS Municipal Income Trust |

| DWS

Municipal Income Trust |

| |

71 |

| Name, Year of Birth, Position with the Trust/ Corporation and Length of Time Served1

|

Business Experience and Directorships During the Past Five Years |

Number of Funds in DWS Fund Complex Overseen |

Other Directorships Held by Board Member |

| Keith R. Fox,

CFA (1954) Preferred Class Chairperson

since 2017, and Board Member

since 1996 |

Managing General Partner, Exeter Capital Partners (a series of private investment funds) (since 1986). Directorships: Progressive International Corporation (kitchen goods designer and distributor); former Chairman, National Association of Small Business Investment Companies; Former Directorships: ICI Mutual Insurance Company; BoxTop Media Inc. (advertising); Sun Capital Advisers Trust (mutual funds) |

69 |

— |

| John W.

Ballantine (1946) Class

III Board Member

since 1999 |

Retired; formerly, Executive Vice President

and Chief Risk Management Officer, First

Chicago NBD Corporation/The First National

Bank of Chicago (1996–1998); Executive Vice

President and Head of International Banking

(1995–1996); Not-for-Profit Directorships:

Window to the World Communications

(public media); Life Director of Harris Theater

for Music and Dance (Chicago); Life Director

of Hubbard Street Dance Chicago; Former

Directorships: Director and Chairman of the

Board, Healthways, Inc.2 (population

wellbeing and wellness services)

(2003–2014); Stockwell Capital Investments

PLC (private equity); Enron Corporation; FNB

Corporation; Tokheim Corporation; First Oak

Brook Bancshares, Inc.; Oak Brook Bank;

Portland General Electric2 (utility company

(2003–2021); and Prisma Energy

International; Former Not-for-Profit

Directorships: Public Radio International;

Palm Beach Civic Assn. |

69 |

— |

| Dawn-Marie

Driscoll (1946) Preferred Class Board Member

since 1987 |

Advisory Board and former Executive Fellow, Hoffman Center for Business Ethics, Bentley University; formerly: Partner, Palmer & Dodge (law firm) (1988–1990); Vice President of Corporate Affairs and General Counsel, Filene’s (retail) (1978–1988); Directorships: Trustee and former Chairman of the Board, Southwest Florida Community Foundation (charitable organization); Former Directorships: ICI Mutual Insurance Company (2007–2015); Sun Capital Advisers Trust (mutual funds) (2007–2012), Investment Company Institute (audit, executive, nominating committees) and Independent Directors Council (governance, executive committees) |

69 |

— |

| 72 |

| |

DWS Municipal Income Trust |

| Name, Year of Birth, Position with the Trust/ Corporation and Length of Time Served1

|

Business Experience and Directorships During the Past Five Years |

Number of Funds in DWS Fund Complex Overseen |

Other Directorships Held by Board Member |

| Richard J.

Herring (1946) Class I

Board Member since 1990 |

Jacob Safra Professor of International Banking and Professor of Finance, The Wharton School, University of Pennsylvania (since July 1972); formerly: Director, The Wharton Financial Institutions Center (1994–2020); Vice Dean and Director, Wharton Undergraduate Division (1995–2000) and Director, The Lauder Institute of International Management Studies (2000–2006); Member FDIC Systemic Risk Advisory Committee since 2011, member Systemic Risk Council since 2012 and member of the Advisory Board at the Yale Program on Financial Stability since 2013; Former Directorships: Co-Chair of the Shadow Financial Regulatory Committee (2003–2015), Executive Director of The Financial Economists Roundtable (2008–2015), Director of The Thai Capital Fund (2007–2013), Director of The Aberdeen Singapore Fund (2007–2018), Director, The Aberdeen Japan Fund (2007-2021) and Nonexecutive Director of Barclays Bank DE (2010–2018) |

69 |

— |

| Chad D. Perry

(1972) Class II

Board Member since 2021 |

Executive Vice President, General Counsel

and Secretary, Tanger Factory Outlet Centers,

Inc.2 (since 2011); formerly Executive Vice

President and Deputy General Counsel, LPL

Financial Holdings Inc.2 (2006–2011); Senior

Corporate Counsel, EMC Corporation

(2005–2006); Associate, Ropes & Gray

LLP (1997–2005) |

21 |

Director - Great

Elm Capital Corp. (business

development company) (since

2022) |

| Rebecca W.

Rimel (1951) Class III

Board Member since 1995 |

Director, The Bridgespan Group (nonprofit organization) (since October 2020); formerly: Executive Vice President, The Glenmede Trust Company (investment trust and wealth management) (1983–2004); Board Member, Investor Education (charitable organization) (2004–2005); Former Directorships: Trustee, Executive Committee, Philadelphia Chamber of Commerce (2001–2007); Director, Viasys Health Care2 (January 2007–June 2007); Trustee, Thomas Jefferson Foundation (charitable organization) (1994–2012); President, Chief Executive Officer and Director (1994–2020) and Senior Advisor (2020-2021), The Pew Charitable Trusts (charitable organization); Director, BioTelemetry Inc.2 (acquired by Royal Philips in 2021) (healthcare) (2009–2021); Director, Becton Dickinson and Company2 (medical technology company) (2012-2022) |