Form N-CSR ALLIANCEBERNSTEIN GLOBAL For: Mar 31

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07732

ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas,

New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: March 31, 2023

Date of reporting period: March 31, 2023

ITEM 1. REPORTS TO STOCKHOLDERS.

MAR 03.31.23

ANNUAL REPORT

ALLIANCEBERNSTEIN

GLOBAL HIGH INCOME FUND

(NYSE: AWF)

| Investment Products Offered | • Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed | |

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AB’s website at www.abfunds.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227 4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Fund’s Form N-PORT reports are available on the Commission’s website at www.sec.gov. AB publishes full portfolio holdings for the Fund monthly at www.abfunds.com.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the Adviser of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

| FROM THE PRESIDENT |

|

Dear Shareholder,

We’re pleased to provide this report for AllianceBernstein Global High Income Fund, Inc. (the “Fund”). Please review the discussion of Fund performance, the market conditions during the reporting period and the Fund’s investment strategy.

At AB, we’re striving to help our clients achieve better outcomes by:

| + | Fostering diverse perspectives that give us a distinctive approach to navigating global capital markets |

| + | Applying differentiated investment insights through a connected global research network |

| + | Embracing innovation to design better ways to invest and leading-edge mutual-fund solutions |

Whether you’re an individual investor or a multibillion-dollar institution, we’re putting our knowledge and experience to work for you every day.

For more information about AB’s comprehensive range of products and shareholder resources, please log on to www.abfunds.com.

Thank you for your investment in AB mutual funds—and for placing your trust in our firm.

Sincerely,

Onur Erzan

President and Chief Executive Officer, AB Mutual Funds

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 1 | |

ANNUAL REPORT

May 8, 2023

This report provides management’s discussion of fund performance for AllianceBernstein Global High Income Fund, Inc. for the annual reporting period ended March 31, 2023. The Fund is a closed-end fund and its shares of common stock trade on the New York Stock Exchange.

The Fund seeks high current income and, secondarily, capital appreciation.

RETURNS AS OF MARCH 31, 2023 (unaudited)

| 6 Months | 12 Months | |||||||

| ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND (NAV)1 | 9.43% | -4.09% | ||||||

| Primary Benchmark: Bloomberg Global High Yield Index (USD hedged) |

9.45% | -3.45% | ||||||

| Blended Benchmark: 33% JPM GBI-EM / 33% JPM EMBI Global / 33% Bloomberg US Corporate HY 2% Issuer Capped Index |

8.78% | -3.93% | ||||||

| 1 | The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the Financial Highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

The Fund’s market price per share on March 31, 2023, was $9.72. The Fund’s NAV per share on March 31, 2023, was $10.56. For additional financial highlights, please see pages 117-118.

INVESTMENT RESULTS

The table above shows the Fund’s performance compared with its primary benchmark, the Bloomberg Global High Yield Index (USD hedged), as well as its blended benchmark for the six- and 12-month periods ended March 31, 2023. The blended benchmark is composed of equal weightings of the JPMorgan Government Bond Index-Emerging Markets (“JPM GBI-EM”) (local currency-denominated), the JPMorgan Emerging Markets Bond Index Global (“JPM EMBI Global”) and the Bloomberg US Corporate High Yield (“HY”) 2% Issuer Capped Index.

During the 12-month period, the Fund underperformed its primary and blended benchmarks. Security selection was the main detractor, relative to the primary benchmark, due to selections within US and eurozone high-yield corporate bonds, along with emerging-market sovereign and corporate bonds, which were partially offset by gains from selection within commercial mortgage-backed securities (“CMBS”) and US investment-grade corporate bonds. Yield-curve positioning was the largest contributor. Sector allocation also contributed, mostly from off-benchmark exposure to agency risk-sharing transactions and emerging-market sovereign bonds that added more to performance than losses from off-benchmark exposure to bank loans and emerging-market corporate

| 2 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

bonds. An underweight to the eurozone contributed from a country perspective. Currency decisions were a minor contributor, from a short in the euro.

Over the six-month period, the Fund underperformed its primary benchmark and outperformed its blended benchmark. Security selection detracted from performance, mainly from selections within US high-yield corporate bonds and CMBS that were partially offset by gains from selection within eurozone high-yield corporates and emerging-market corporate bonds. Sector allocation was the largest contributor to performance, mostly from the utilization of credit default swaps in the eurozone, off-benchmark exposure to collateralized loan obligations and an overweight to US high-yield corporate bonds. Losses from underweights to emerging-market sovereign and corporate bonds, and off-benchmark exposure to CMBS, US Treasuries, bank loans and US investment-grade corporate bonds partially offset gains. Yield-curve positioning added to performance, mostly from an overweight on the six-month part of the curve in the US, offset by a loss on the two-year part of the US curve from an underweight. An underweight to the eurozone contributed at the country level. A currency long position in the euro was a minor contributor to performance.

During both periods, the Fund used interest rate swaps and futures to manage and hedge duration risk and/or to take active yield-curve positioning. Currency forwards were used to hedge foreign currency exposure and/or to take active currency risk. Interest rate swaptions were used to take active yield-curve positioning. Credit default swaps were used to effectively obtain high-yield credit/sector exposure. Total return swaps were used to take active credit risk. During the 12-month period, written options were used to generate income.

During the 12-month period, the utilization of leverage on behalf of the Fund detracted from performance, relative to the benchmark. As the benchmark generated negative returns in excess of the Fund’s borrowing rates, the utilization of leverage detracted from the Fund’s absolute returns. During the six-month period, the utilization of leverage on behalf of the Fund contributed to outperformance, relative to the benchmark. As the benchmark generated positive returns in excess of the Fund’s borrowing rates, the utilization of leverage contributed to the Fund’s absolute returns.

MARKET REVIEW AND INVESTMENT STRATEGY

During the 12-month period ended March 31, 2023, fixed-income government bond market yields rose sharply, and bond prices fell in all major developed markets, except in Japan and Australia, as most central banks raised interest rates significantly to combat persistent inflation. Developed-market top-line inflation peaked in October, causing bond markets to rally until February, when investors realized that sticky core inflation would be

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 3 | |

more difficult to contain. Stress in the global banking sector led treasury markets to rally on growth concerns. Global investment-grade corporate bonds, which typically have longer maturities and are more sensitive to changes in yields than high-yield corporates, underperformed global treasuries—trailing US Treasury bonds in the US, while outperforming eurozone treasuries in the euro bloc. Developed-market high-yield corporate bonds also fell, but they significantly outperformed global treasuries, and outperformed respective treasury markets in the US and eurozone. Emerging-market hard-currency sovereign bonds trailed global developed-market treasuries as the US dollar rose against most developed- and emerging-market currencies. Emerging-market hard-currency corporate bonds outperformed developed-market treasuries by a wide margin, with high yield posting a small positive return. Emerging-market local-currency bonds also outperformed developed-market treasuries and led risk assets. Brent crude oil prices fell significantly on reduced demand and economic growth concerns.

The Fund’s Investment Management Team (the “Team”) seeks to generate high current income and, secondarily, capital appreciation. The Fund is a globally diversified portfolio that takes full advantage of the Team’s best research ideas by pursuing high-income opportunities across all fixed-income sectors. The Fund invests primarily (and without limit) in corporate debt securities from US and non-US issuers, as well as government bonds from both developing and developed countries, including the US. Under normal market conditions, the Fund invests substantially in lower-rated bonds, but may also invest in investment-grade and unrated debt securities.

INVESTMENT POLICIES

The Fund invests without limit in securities denominated in non-US currencies as well as those denominated in the US dollar. The Fund may also invest, without limit, in sovereign debt securities issued by emerging and developed nations and in debt securities of US and non-US corporate issuers. For more information regarding the Fund’s risks, please see “Disclosures and Risks” on pages 5-8 and “Note E—Risks Involved in Investing in the Fund” of the Notes to Financial Statements on pages 110-114.

| 4 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

AllianceBernstein Global High Income Fund Shareholder Information

Weekly comparative net asset value (“NAV”) and market price information about the Fund is published each Saturday in Barron’s and in other newspapers in a table called “Closed-End Funds.” Daily NAV and market price information, and additional information regarding the Fund, is available at www.abfunds.com and www.nyse.com. For additional shareholder information regarding this Fund, please see pages 122-123.

Benchmark Disclosure

All indices are unmanaged and do not reflect fees and expenses associated with the active management of a fund portfolio. The Bloomberg Global High Yield Index (USD hedged) represents non-investment grade fixed-income securities of companies in the US, and developed and emerging markets, hedged to the US dollar. The JPM® GBI-EM represents the performance of local currency government bonds issued by emerging markets. The JPM EMBI Global (market-capitalization weighted) represents the performance of US dollar-denominated Brady bonds, Eurobonds and trade loans issued by sovereign and quasi-sovereign entities. The Bloomberg US Corporate HY 2% Issuer Capped Index is the 2% Issuer Capped component of the US Corporate High Yield Index, which represents the performance of fixed-income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million and at least one year to maturity. An investor cannot invest directly in an index, and its results are not indicative of the performance of any specific investment, including the Fund.

A Word About Risk

Market Risk: The market value of a security may move up or down, sometimes rapidly and unpredictably. These fluctuations may cause a security to be worth less than the price originally paid for it, or less than it was worth at an earlier time. Market risk may affect a single issuer, industry, sector of the economy or the market as a whole. Global economies and financial markets are increasingly interconnected, which increases the probabilities that conditions in one country or region might adversely impact issuers in a different country or region. Conditions affecting the general economy, including political, social, or economic instability at the local, regional, or global level may also affect the market value of a security. Health crises, such as pandemic and epidemic diseases, as well as other incidents that interrupt the expected course of events, such as natural disasters, including fires, earthquakes and flooding, war or civil disturbance, acts of terrorism, power outages and other unforeseeable and external events, and the public response to or fear of such diseases or events, have had, and may in the future have, an adverse effect on the

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 5 | |

DISCLOSURES AND RISKS (continued)

Fund’s investments and net asset value and can lead to increased market volatility. For example, the diseases or events themselves or any preventative or protective actions that governments may take in respect of such diseases or events may result in periods of business disruption, inability to obtain raw materials, supplies and component parts, and reduced or disrupted operations for the Fund’s portfolio companies. The occurrence and pendency of such diseases or events could adversely affect the economies and financial markets either in specific countries or worldwide.

Interest-Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of existing investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. Interest-rate risk is generally greater for fixed-income securities with longer maturities or durations. The Fund may be subject to a greater risk of rising interest rates than would normally be the case due to the recent end of a period of historically low rates and the effect of potential central bank monetary policy, and government fiscal policy, initiatives and resulting market reactions to those initiatives.

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security and accrued interest. The degree of risk for a particular security may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security.

Below Investment-Grade Securities Risk: Investments in fixed-income securities with lower ratings (commonly known as “junk bonds”) are subject to a higher probability that an issuer will default or fail to meet its payment obligations. These securities may be subject to greater price volatility due to such factors as specific corporate developments and negative perceptions of the junk bond market generally and may be more difficult to trade than other types of securities.

Duration Risk: Duration is a measure that relates the expected price volatility of a fixed-income security to changes in interest rates. The duration of a fixed-income security may be shorter than or equal to full maturity of a fixed-income security. Fixed-income securities with longer durations have more risk and will decrease in price as interest rates rise.

| 6 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

DISCLOSURES AND RISKS (continued)

Inflation Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Fund’s assets can decline as can the value of the Fund’s distributions. This risk is significantly greater for fixed-income securities with longer maturities.

Foreign (Non-US) Risk: Investments in securities of non-US issuers may involve more risk than those of US issuers. These securities may fluctuate more widely in price and may be more difficult to trade due to adverse market, economic, political, regulatory or other factors.

Emerging-Market Risk: Investments in emerging-market countries may have more risk because the markets are less developed and less liquid and are subject to increased economic, political, regulatory or other uncertainties.

Currency Risk: Fluctuations in currency exchange rates may negatively affect the value of the Fund’s investments or reduce its returns.

Leverage Risk: As a result of the Fund’s use of leveraging techniques, its NAV may be more volatile because leverage tends to exaggerate the effect of changes in interest rates and any increase or decrease in the value of the Fund’s investments.

Derivatives Risk: Investments in derivatives may be difficult to price or unwind and leveraged so that small changes may produce disproportionate losses for the Fund. A short position in a derivative instrument involves the risk of a theoretically unlimited increase in the value of the underlying asset, which could cause the Fund to suffer a potentially unlimited loss. Derivatives, especially over-the-counter derivatives, are also subject to counterparty risk, which is the risk that the counterparty (the party on the other side of the transaction) on a derivative transaction will be unable or unwilling to honor its contractual obligations to the Fund.

Illiquid Investments Risk: Illiquid investments risk exists when certain investments are or become difficult to purchase or sell. Difficulty in selling such investments may result in sales at disadvantageous prices affecting the value of your investment in the Fund. Causes of illiquid investments risk may include low trading volumes, large positions and heavy redemptions of Fund shares. Illiquid investments risk may be higher in a rising interest rate environment, when the value and liquidity of fixed-income securities generally decline.

Management Risk: The Fund is subject to management risk because it is an actively managed investment fund. The Adviser will apply its investment techniques and risk analyses in making investment decisions, but there is

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 7 | |

DISCLOSURES AND RISKS (continued)

no guarantee that its techniques will produce the intended results. Some of these techniques may incorporate, or rely upon, quantitative models, but there is no guarantee that these models will generate accurate forecasts, reduce risk or otherwise perform as expected.

Mortgage-Related and/or Other Asset-Backed Securities Risk: The Fund may invest in mortgage-backed and/or other asset-backed securities, including securities backed by mortgages and assets with an international or emerging-markets origination and securities backed by non-performing loans at the time of investment. Investments in mortgage-related and other asset-backed securities are subject to certain additional risks. The value of these securities may be particularly sensitive to changes in interest rates. These risks include “extension risk”, which is the risk that, in periods of rising interest rates, issuers may delay the payment of principal, and “prepayment risk”, which is the risk that, in periods of falling interest rates, issuers may pay principal sooner than expected, exposing the Fund to a lower rate of return upon reinvestment of principal. Mortgage-backed securities offered by nongovernmental issuers and other asset-backed securities may be subject to other risks, such as higher rates of default in the mortgages or assets backing the securities or risks associated with the nature and servicing of mortgages or assets backing the securities.

As with all investments, you may lose money by investing in the Fund.

An Important Note About Historical Performance

The performance shown in this report represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. All fees and expenses related to the operation of the Fund have been deducted. Performance assumes reinvestment of distributions and does not account for taxes. Historical performance does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the sale of fund shares and assumes the reinvestment of dividends and capital gains distributions at prices obtained pursuant to the Fund’s dividend reinvestment plan.

| 8 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

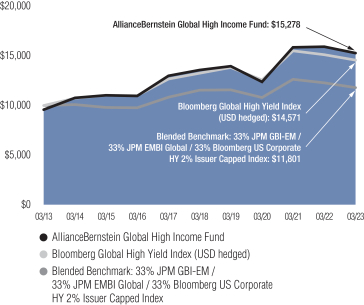

HISTORICAL PERFORMANCE

GROWTH OF A $10,000 INVESTMENT IN THE FUND (unaudited)

3/31/2013 TO 3/31/2023

This chart illustrates the total value of an assumed $10,000 investment in AllianceBernstein Global High Income Fund based on market prices (from 3/31/2013 to 3/31/2023) as compared with the performance of the Fund’s benchmarks. The chart assumes the reinvestment of dividends and capital gains distributions at prices obtained pursuant to the Fund’s dividend reinvestment plan.

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 9 | |

HISTORICAL PERFORMANCE (continued)

AVERAGE ANNUAL RETURNS AS OF MARCH 31, 2023 (unaudited)

| NAV Returns |

Market Price |

|||||||

| 1 Year | -4.09% | -5.00% | ||||||

| 5 Years | 2.41% | 3.41% | ||||||

| 10 Years | 4.33% | 3.06% | ||||||

AVERAGE ANNUAL RETURNS

AS OF THE MOST RECENT CALENDAR QUARTER-END

MARCH 31, 2023 (unaudited)

| NAV Returns |

Market Price |

|||||||

| 1 Year | -4.09% | -5.00% | ||||||

| 5 Years | 2.41% | 3.41% | ||||||

| 10 Years | 4.33% | 3.06% | ||||||

Performance assumes the reinvestment of dividends and capital gains distributions at prices obtained pursuant to the Fund’s dividend reinvestment plan.

| 10 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

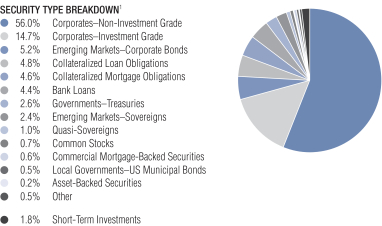

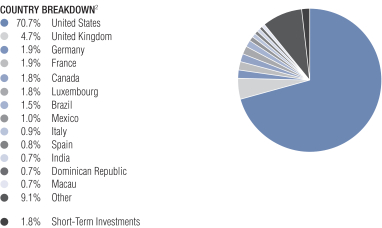

PORTFOLIO SUMMARY

March 31, 2023 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $910.9

| 1 | The Fund’s security type breakdown is expressed as a percentage of total investments and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Portfolio of Investments” section of the report for additional details). “Other” security type weightings represent 0.2% or less in the following: Governments–Sovereign Bonds, Inflation-Linked Securities, Preferred Stocks and Rights. |

| 2 | The Fund’s country breakdown is expressed as a percentage of total investments and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or other investment purposes (see “Portfolio of Investments” section of the report for additional details). “Other” country weightings represent 0.6% or less in the following: Angola, Argentina, Australia, Belgium, Cayman Islands, Chile, China, Colombia, Czech Republic, Ecuador, Egypt, El Salvador, Finland, Gabon, Ghana, Guatemala, Hong Kong, Indonesia, Ireland, Israel, Jamaica, Japan, Jersey (Channel Islands), Kazakhstan, Kuwait, Morocco, Netherlands, Nigeria, Norway, Panama, Peru, Slovenia, South Africa, South Korea, Sweden, Switzerland, Trinidad & Tobago, Turkey, Ukraine, Venezuela and Zambia. |

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 11 | |

PORTFOLIO OF INVESTMENTS

March 31, 2023

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| CORPORATES - NON-INVESTMENT GRADE – 55.3% |

||||||||||||

| Industrial – 48.9% |

||||||||||||

| Basic – 3.1% |

||||||||||||

| Advanced Drainage Systems, Inc.

|

U.S.$ | 140 | $ | 133,279 | ||||||||

| 6.375%, 06/15/2030(a) |

27 | 26,585 | ||||||||||

| Arconic Corp. |

83 | 81,833 | ||||||||||

| ASP Unifrax Holdings, Inc.

|

851 | 680,172 | ||||||||||

| 7.50%, 09/30/2029(a) |

1,244 | 843,751 | ||||||||||

| Baffinland Iron Mines Corp./Baffinland Iron Mines LP |

215 | 205,330 | ||||||||||

| Berry Global, Inc.

|

166 | 163,475 | ||||||||||

| Big River Steel LLC/BRS Finance Corp. |

171 | 171,130 | ||||||||||

| Cerdia Finanz GmbH

|

419 | 384,377 | ||||||||||

| Chemours Co. (The) |

13 | 12,049 | ||||||||||

| 5.75%, 11/15/2028(a) |

232 | 208,428 | ||||||||||

| Cleveland-Cliffs, Inc.

|

107 | 108,863 | ||||||||||

| Commercial Metals Co. |

80 | 71,057 | ||||||||||

| 4.375%, 03/15/2032 |

80 | 69,364 | ||||||||||

| Constellium SE |

EUR | 1,109 | 974,527 | |||||||||

| Crown Americas LLC/Crown Americas Capital Corp. VI |

U.S.$ | 439 | 429,711 | |||||||||

| CVR Partners LP/CVR Nitrogen Finance Corp. |

370 | 328,219 | ||||||||||

| Domtar Corp. |

140 | 124,642 | ||||||||||

| Element Solutions, Inc.

|

1,279 | 1,121,166 | ||||||||||

| ERP Iron Ore, LLC

|

240 | 160,109 | ||||||||||

| FMG Resources (August 2006) Pty Ltd. |

2,191 | 1,892,327 | ||||||||||

| 4.50%, 09/15/2027(a) |

877 | 824,389 | ||||||||||

| 5.875%, 04/15/2030(a) |

76 | 72,840 | ||||||||||

| 6.125%, 04/15/2032(a) |

2,563 | 2,457,822 | ||||||||||

| 12 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Glatfelter Corp.

|

U.S.$ | 77 | $ | 51,339 | ||||||

| Graham Packaging Co., Inc.

|

420 | 364,915 | ||||||||

| Graphic Packaging International LLC

|

1,661 | 1,450,851 | ||||||||

| Hecla Mining Co. |

282 | 284,700 | ||||||||

| Hudbay Minerals, Inc.

|

215 | 199,995 | ||||||||

| 6.125%, 04/01/2029(a) |

174 | 164,461 | ||||||||

| INEOS Quattro Finance 1 PLC

|

EUR | 101 | 94,949 | |||||||

| INEOS Quattro Finance 2 PLC

|

U.S.$ | 426 | 389,670 | |||||||

| Ingevity Corp. |

643 | 555,753 | ||||||||

| Intelligent Packaging Holdco Issuer LP |

611 | 439,916 | ||||||||

| Intelligent Packaging Ltd. Finco, Inc./Intelligent Packaging Ltd.

Co-Issuer LLC |

603 | 518,460 | ||||||||

| Kaiser Aluminum Corp.

|

47 | 38,616 | ||||||||

| Kobe US Midco 2, Inc. |

1,300 | 949,251 | ||||||||

| LABL, Inc. |

222 | 214,240 | ||||||||

| Magnetation LLC/Mag Finance Corp.

|

2,857 | – 0 | – | |||||||

| Mercer International, Inc. |

969 | 830,043 | ||||||||

| Methanex Corp. |

16 | 14,955 | ||||||||

| Mineral Resources Ltd.

|

192 | 195,401 | ||||||||

| 8.125%, 05/01/2027(a) |

158 | 159,087 | ||||||||

| 8.50%, 05/01/2030(a) |

53 | 52,976 | ||||||||

| Novelis Corp. |

61 | 55,710 | ||||||||

| 3.875%, 08/15/2031(a) |

19 | 15,993 | ||||||||

| 4.75%, 01/30/2030(a) |

135 | 124,085 | ||||||||

| Olympus Water US Holding Corp.

|

237 | 193,795 | ||||||||

| 7.125%, 10/01/2027(a) |

755 | 708,325 | ||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 13 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Rain CII Carbon LLC/CII Carbon Corp. |

U.S.$ | 224 | $ | 214,788 | ||||||||

| Roller Bearing Co. of America, Inc. |

143 | 127,609 | ||||||||||

| SCIH Salt Holdings, Inc.

|

68 | 60,525 | ||||||||||

| SCIL IV LLC/SCIL USA Holdings LLC

|

EUR | 320 | 319,663 | |||||||||

| 5.375%, 11/01/2026(a) |

U.S.$ | 1,039 | 955,271 | |||||||||

| Sealed Air Corp. |

192 | 179,210 | ||||||||||

| 6.875%, 07/15/2033(a) |

726 | 739,126 | ||||||||||

| Sealed Air Corp./Sealed Air Corp. US |

546 | 552,492 | ||||||||||

| SPCM SA |

655 | 575,431 | ||||||||||

| 3.375%, 03/15/2030(a) |

951 | 787,353 | ||||||||||

| SunCoke Energy, Inc.

|

145 | 127,168 | ||||||||||

| Trinseo Materials Operating SCA/Trinseo Materials Finance, Inc. |

256 | 207,054 | ||||||||||

| Tronox, Inc. |

98 | 82,048 | ||||||||||

| United States Steel Corp. |

37 | 35,735 | ||||||||||

| 6.875%, 03/01/2029 |

110 | 109,994 | ||||||||||

| Vibrantz Technologies, Inc.

|

3,258 | 2,496,594 | ||||||||||

| WR Grace Holdings LLC

|

1,174 | 1,131,239 | ||||||||||

| 5.625%, 08/15/2029(a) |

61 | 51,750 | ||||||||||

|

|

|

|||||||||||

| 28,365,981 | ||||||||||||

|

|

|

|||||||||||

| Capital Goods – 3.6% |

||||||||||||

| ARD Finance SA |

EUR | 3,069 | 2,485,547 | |||||||||

| Ardagh Metal Packaging Finance USA LLC/Ardagh Metal Packaging Finance PLC |

U.S.$ | 985 | 772,279 | |||||||||

| 6.00%, 06/15/2027(a) |

684 | 676,237 | ||||||||||

| Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc. |

2,663 | 2,480,276 | ||||||||||

| 5.25%, 08/15/2027(a) |

235 | 184,288 | ||||||||||

| Artera Services LLC

|

133 | 114,558 | ||||||||||

| 14 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Ball Corp. |

U.S.$ | 103 | $ | 102,847 | ||||||

| 6.875%, 03/15/2028 |

159 | 164,544 | ||||||||

| Bombardier, Inc.

|

77 | 75,017 | ||||||||

| 7.125%, 06/15/2026(a) |

217 | 218,641 | ||||||||

| 7.50%, 02/01/2029(a) |

74 | 75,607 | ||||||||

| 7.875%, 04/15/2027(a) |

1,814 | 1,839,364 | ||||||||

| Camelot Return Merger Sub, Inc.

|

196 | 181,408 | ||||||||

| Clean Harbors, Inc.

|

69 | 66,959 | ||||||||

| 6.375%, 02/01/2031(a) |

11 | 11,224 | ||||||||

| Covanta Holding Corp.

|

66 | 58,314 | ||||||||

| Crown Americas LLC |

411 | 397,746 | ||||||||

| Eco Material Technologies, Inc.

|

2,614 | 2,488,533 | ||||||||

| Energizer Holdings, Inc.

|

348 | 315,181 | ||||||||

| EnerSys |

935 | 866,776 | ||||||||

| F-Brasile SpA/F-Brasile US

LLC |

957 | 793,848 | ||||||||

| GrafTech Finance, Inc.

|

65 | 54,839 | ||||||||

| Griffon Corp. |

603 | 558,856 | ||||||||

| Harsco Corp. |

1,384 | 1,083,913 | ||||||||

| JELD-WEN, Inc. |

128 | 119,416 | ||||||||

| Koppers, Inc. |

118 | 117,969 | ||||||||

| Madison IAQ LLC

|

359 | 275,880 | ||||||||

| Masonite International Corp.

|

166 | 158,530 | ||||||||

| MIWD Holdco II LLC/MIWD Finance Corp. |

84 | 70,864 | ||||||||

| Moog, Inc. |

171 | 160,428 | ||||||||

| Mueller Water Products, Inc.

|

291 | 261,762 | ||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 15 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| New Enterprise Stone & Lime Co., Inc. |

U.S.$ | 13 | $ | 11,571 | ||||||

| Oscar AcquisitionCo LLC/Oscar Finance, Inc. |

63 | 54,823 | ||||||||

| Owens-Brockway Glass Container, Inc. |

165 | 165,139 | ||||||||

| Renk AG/Frankfurt am Main

|

EUR | 1,560 | 1,653,144 | |||||||

| Rolls-Royce PLC

|

U.S.$ | 918 | 867,472 | |||||||

| Silgan Holdings, Inc. |

213 | 200,531 | ||||||||

| Smyrna Ready Mix Concrete LLC

|

53 | 49,724 | ||||||||

| Spirit AeroSystems, Inc. |

23 | 19,490 | ||||||||

| Stericycle, Inc.

|

764 | 673,669 | ||||||||

| Summit Materials LLC/Summit Materials Finance Corp. |

164 | 155,623 | ||||||||

| Terex Corp. |

86 | 79,927 | ||||||||

| Titan Holdings II BV

|

EUR | 649 | 541,568 | |||||||

| TK Elevator Holdco GmbH

|

U.S.$ | 465 | 403,816 | |||||||

| TK Elevator Midco GmbH

|

EUR | 885 | 869,118 | |||||||

| TK Elevator US Newco, Inc.

|

U.S.$ | 525 | 495,385 | |||||||

| TransDigm, Inc. |

491 | 436,161 | ||||||||

| 4.875%, 05/01/2029 |

2,049 | 1,813,685 | ||||||||

| 5.50%, 11/15/2027 |

175 | 165,030 | ||||||||

| 6.25%, 03/15/2026(a) |

332 | 332,261 | ||||||||

| 6.375%, 06/15/2026 |

165 | 162,186 | ||||||||

| 6.75%, 08/15/2028(a) |

2,508 | 2,533,070 | ||||||||

| Triumph Group, Inc. |

428 | 392,386 | ||||||||

| 9.00%, 03/15/2028(a) |

2,516 | 2,519,254 | ||||||||

| Trivium Packaging Finance BV

|

EUR | 100 | 100,090 | |||||||

| Tutor Perini Corp.

|

U.S.$ | 90 | 63,497 | |||||||

| 16 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Waste Pro USA, Inc.

|

U.S.$ | 41 | $ | 37,721 | ||||||||

| WESCO Distribution, Inc.

|

20 | 20,336 | ||||||||||

| 7.25%, 06/15/2028(a) |

308 | 316,517 | ||||||||||

|

|

|

|||||||||||

| 32,364,845 | ||||||||||||

|

|

|

|||||||||||

| Communications - Media – 7.4% |

||||||||||||

| Advantage Sales & Marketing, Inc. |

393 | 298,172 | ||||||||||

| Allen Media LLC/Allen Media Co-Issuer, Inc.

|

42 | 22,997 | ||||||||||

| Altice Financing SA

|

1,456 | 1,173,134 | ||||||||||

| 5.75%, 08/15/2029(a) |

5,165 | 4,118,618 | ||||||||||

| AMC Networks, Inc. |

1,098 | 672,888 | ||||||||||

| 4.75%, 08/01/2025 |

914 | 807,069 | ||||||||||

| Arches Buyer, Inc.

|

605 | 501,314 | ||||||||||

| Banijay Entertainment SASU

|

EUR | 210 | 221,399 | |||||||||

| 5.375%, 03/01/2025(a) |

U.S.$ | 2,324 | 2,260,831 | |||||||||

| CCO Holdings LLC/CCO Holdings Capital Corp. |

163 | 126,256 | ||||||||||

| 4.50%, 08/15/2030(a) |

4,665 | 3,932,180 | ||||||||||

| 4.50%, 06/01/2033(a) |

2,998 | 2,390,728 | ||||||||||

| 4.75%, 02/01/2032(a) |

6,963 | 5,860,096 | ||||||||||

| 5.125%, 05/01/2027(a) |

327 | 308,867 | ||||||||||

| 6.375%, 09/01/2029(a) |

1,760 | 1,680,522 | ||||||||||

| 7.375%, 03/01/2031(a) |

2,762 | 2,722,304 | ||||||||||

| Clear Channel Outdoor Holdings, Inc. |

512 | 459,371 | ||||||||||

| CMG Media Corp.

|

158 | 119,496 | ||||||||||

| CSC Holdings LLC

|

981 | 702,515 | ||||||||||

| 4.625%, 12/01/2030(a) |

1,461 | 718,995 | ||||||||||

| 5.375%, 02/01/2028(a) |

1,278 | 1,049,584 | ||||||||||

| 5.75%, 01/15/2030(a) |

6,396 | 3,234,736 | ||||||||||

| 7.50%, 04/01/2028(a) |

1,150 | 732,460 | ||||||||||

| Deluxe Corp. |

17 | 12,409 | ||||||||||

| Diamond Sports Group LLC/Diamond Sports Finance Co. |

299 | 16,176 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 17 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| DISH DBS Corp. |

U.S.$ | 2,995 | $ | 1,580,405 | ||||||

| 5.25%, 12/01/2026(a) |

2,798 | 2,235,418 | ||||||||

| 5.75%, 12/01/2028(a) |

2,596 | 1,938,284 | ||||||||

| 5.875%, 11/15/2024 |

1,821 | 1,624,699 | ||||||||

| 7.375%, 07/01/2028 |

115 | 65,547 | ||||||||

| 7.75%, 07/01/2026 |

727 | 479,822 | ||||||||

| DISH Network Corp.

|

72 | 69,232 | ||||||||

| Gray Escrow II, Inc.

|

1,381 | 905,913 | ||||||||

| iHeartCommunications, Inc.

|

60 | 47,826 | ||||||||

| 5.25%, 08/15/2027(a) |

1,499 | 1,225,003 | ||||||||

| 8.375%, 05/01/2027 |

178 | 129,298 | ||||||||

| LCPR Senior Secured Financing DAC

|

2,910 | 2,459,861 | ||||||||

| 6.75%, 10/15/2027(a) |

200 | 184,032 | ||||||||

| Liberty Interactive LLC

|

870 | 134,438 | ||||||||

| McGraw-Hill Education, Inc.

|

1,123 | 977,010 | ||||||||

| National CineMedia LLC

|

623 | 192,995 | ||||||||

| Nexstar Media Inc.

|

172 | 152,910 | ||||||||

| Outfront Media Capital LLC/Outfront Media Capital Corp. |

391 | 324,148 | ||||||||

| 5.00%, 08/15/2027(a) |

113 | 102,899 | ||||||||

| Radiate Holdco LLC/Radiate Finance, Inc. |

1,331 | 1,040,699 | ||||||||

| 6.50%, 09/15/2028(a) |

124 | 51,130 | ||||||||

| Scripps Escrow II, Inc.

|

26 | 20,332 | ||||||||

| Sinclair Television Group, Inc.

|

1,613 | 1,302,205 | ||||||||

| 5.50%, 03/01/2030(a)(i) |

944 | 750,672 | ||||||||

| Sirius XM Radio, Inc.

|

6,132 | 5,270,947 | ||||||||

| 4.125%, 07/01/2030(a) |

204 | 166,761 | ||||||||

| 5.00%, 08/01/2027(a) |

982 | 912,735 | ||||||||

| 5.50%, 07/01/2029(a) |

186 | 169,122 | ||||||||

| Stagwell Global LLC

|

67 | 58,801 | ||||||||

| Summer BC Holdco B SARL

|

EUR | 1,395 | 1,318,197 | |||||||

| 18 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Summer BidCo BV |

EUR | 877 | $ | 735,053 | ||||||||

| TEGNA, Inc. |

U.S.$ | 333 | 288,035 | |||||||||

| Townsquare Media, Inc.

|

113 | 106,410 | ||||||||||

| Univision Communications, Inc.

|

1,593 | 1,513,347 | ||||||||||

| 7.375%, 06/30/2030(a) |

1,186 | 1,118,940 | ||||||||||

| Urban One, Inc.

|

2,221 | 2,015,773 | ||||||||||

| VZ Vendor Financing II BV

|

EUR | 885 | 764,201 | |||||||||

| Ziggo Bond Co. BV

|

U.S.$ | 1,124 | 903,845 | |||||||||

|

|

|

|||||||||||

| 67,480,062 | ||||||||||||

|

|

|

|||||||||||

| Communications - Telecommunications – 2.9% |

||||||||||||

| Altice France SA/France

|

EUR | 885 | 749,401 | |||||||||

| 5.125%, 07/15/2029(a) |

U.S.$ | 6,254 | 4,713,356 | |||||||||

| 5.50%, 10/15/2029(a) |

431 | 330,270 | ||||||||||

| 8.125%, 02/01/2027(a) |

224 | 205,827 | ||||||||||

| British Telecommunications PLC

|

214 | 185,866 | ||||||||||

| Connect Finco SARL/Connect US Finco LLC |

2,440 | 2,290,550 | ||||||||||

| Consolidated Communications, Inc.

|

795 | 540,116 | ||||||||||

| 6.50%, 10/01/2028(a) |

2,067 | 1,506,880 | ||||||||||

| Embarq Corp. |

2,128 | 891,989 | ||||||||||

| Frontier Communications Holdings LLC |

132 | 100,567 | ||||||||||

| 6.75%, 05/01/2029(a) |

524 | 415,270 | ||||||||||

| 8.625%, 03/15/2031(a) |

73 | 71,472 | ||||||||||

| 8.75%, 05/15/2030(a) |

893 | 888,993 | ||||||||||

| Hughes Satellite Systems Corp. |

465 | 439,181 | ||||||||||

| Iliad Holding SASU

|

719 | 687,691 | ||||||||||

| Intelsat Jackson Holdings SA

|

1,675 | – 0 | – | |||||||||

| Level 3 Financing, Inc.

|

64 | 35,324 | ||||||||||

| 3.75%, 07/15/2029(a) |

1,018 | 543,478 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 19 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| 4.25%, 07/01/2028(a) |

U.S.$ | 791 | $ | 445,749 | ||||||||

| 4.625%, 09/15/2027(a) |

1,691 | 1,015,801 | ||||||||||

| Lorca Telecom Bondco SA

|

EUR | 952 | 948,969 | |||||||||

| Lumen Technologies, Inc. |

U.S.$ | 73 | 27,919 | |||||||||

| Series U |

68 | 25,876 | ||||||||||

| Telecom Italia Capital SA |

50 | 42,711 | ||||||||||

| 7.20%, 07/18/2036 |

451 | 409,025 | ||||||||||

| 7.721%, 06/04/2038 |

1,596 | 1,480,143 | ||||||||||

| Telecom Italia SpA/Milano

|

403 | 394,844 | ||||||||||

| Telesat Canada/Telesat LLC

|

14 | 7,343 | ||||||||||

| 6.50%, 10/15/2027(a) |

132 | 39,898 | ||||||||||

| United Group BV

|

EUR | 237 | 183,228 | |||||||||

| 4.625%, 08/15/2028(a) |

481 | 384,880 | ||||||||||

| 7.357% (EURIBOR 3 Month + 4.88%), 02/01/2029(j) |

896 | 811,698 | ||||||||||

| Vmed O2 UK Financing I PLC

|

U.S.$ | 530 | 439,842 | |||||||||

| 4.75%, 07/15/2031(a) |

3,880 | 3,307,086 | ||||||||||

| Vodafone Group PLC |

208 | 162,240 | ||||||||||

| 5.125%, 06/04/2081 |

48 | 33,600 | ||||||||||

| Windstream Escrow LLC/Windstream Escrow Finance Corp. |

235 | 189,803 | ||||||||||

| Zayo Group Holdings, Inc.

|

1,515 | 1,149,111 | ||||||||||

| 6.125%, 03/01/2028(a) |

128 | 77,609 | ||||||||||

|

|

|

|||||||||||

| 26,173,606 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - Automotive – 4.0% |

||||||||||||

| Adient Global Holdings Ltd.

|

400 | 385,318 | ||||||||||

| Allison Transmission, Inc.

|

213 | 181,495 | ||||||||||

| 5.875%, 06/01/2029(a) |

1,163 | 1,132,434 | ||||||||||

| American Axle & Manufacturing, Inc. |

220 | 186,075 | ||||||||||

| Aston Martin Capital Holdings Ltd. |

1,028 | 1,099,052 | ||||||||||

| 20 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Clarios Global LP/Clarios US Finance Co. |

EUR | 210 | $ | 216,904 | ||||||

| Dana Financing Luxembourg SARL

|

U.S.$ | 109 | 107,701 | |||||||

| Dana, Inc. |

760 | 619,835 | ||||||||

| 5.375%, 11/15/2027 |

109 | 103,021 | ||||||||

| 5.625%, 06/15/2028 |

182 | 170,918 | ||||||||

| Dealer Tire LLC/DT Issuer LLC

|

1,116 | 1,002,947 | ||||||||

| Exide Technologies |

2,940 | – 0 | – | |||||||

| (First Lien) |

1,207 | – 0 | – | |||||||

| Ford Motor Co. |

3,020 | 2,364,403 | ||||||||

| 4.75%, 01/15/2043 |

107 | 81,455 | ||||||||

| 5.291%, 12/08/2046 |

249 | 201,996 | ||||||||

| 6.10%, 08/19/2032 |

4,663 | 4,504,965 | ||||||||

| Ford Motor Credit Co. LLC |

793 | 705,863 | ||||||||

| 3.664%, 09/08/2024 |

200 | 192,565 | ||||||||

| 4.271%, 01/09/2027 |

220 | 204,951 | ||||||||

| 4.95%, 05/28/2027 |

1,160 | 1,106,379 | ||||||||

| 7.35%, 11/04/2027 |

4,412 | 4,551,223 | ||||||||

| Series G |

200 | 189,727 | ||||||||

| Goodyear Tire & Rubber Co. (The) |

49 | 43,088 | ||||||||

| IHO Verwaltungs GmbH |

EUR | 284 | 306,951 | |||||||

| 3.75% (3.75% Cash or 4.50% PIK), 09/15/2026(a)(f) |

885 | 862,858 | ||||||||

| 3.875% (3.875% Cash or 4.625% PIK), 05/15/2027(a)(f) |

338 | 322,112 | ||||||||

| 4.75% (4.75% Cash or 5.50% PIK), 09/15/2026(a)(f) |

U.S.$ | 433 | 386,428 | |||||||

| 6.00% (6.00% Cash or 6.75% PIK), 05/15/2027(a)(f) |

1,984 | 1,823,562 | ||||||||

| 8.75% (8.75% Cash or 9.50% PIK), 05/15/2028(a)(f) |

EUR | 306 | 339,438 | |||||||

| Jaguar Land Rover Automotive PLC

|

U.S.$ | 1,490 | 1,168,278 | |||||||

| 5.875%, 01/15/2028(a) |

1,295 | 1,091,733 | ||||||||

| 7.75%, 10/15/2025(a) |

1,417 | 1,374,421 | ||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 21 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| JB Poindexter & Co., Inc.

|

U.S.$ | 146 | $ | 136,901 | ||||||||

| Mclaren Finance PLC

|

1,973 | 1,612,429 | ||||||||||

| PM General Purchaser LLC

|

1,339 | 1,229,722 | ||||||||||

| Real Hero Merger Sub 2, Inc.

|

1,777 | 1,318,005 | ||||||||||

| Titan International, Inc. |

1,465 | 1,319,856 | ||||||||||

| ZF Europe Finance BV

|

EUR | 200 | 197,138 | |||||||||

| ZF Finance GmbH |

200 | 186,728 | ||||||||||

| 2.75%, 05/25/2027(a) |

900 | 868,736 | ||||||||||

| ZF North America Capital, Inc.

|

U.S.$ | 2,528 | 2,484,957 | |||||||||

|

|

|

|||||||||||

| 36,382,568 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - Entertainment – 2.9% |

||||||||||||

| AMC Entertainment Holdings, Inc.

|

142 | 98,140 | ||||||||||

| Carnival Corp. |

1,739 | 1,492,279 | ||||||||||

| 5.75%, 03/01/2027(a) |

1,336 | 1,092,180 | ||||||||||

| 6.00%, 05/01/2029(a) |

43 | 34,185 | ||||||||||

| 7.625%, 03/01/2026(a) |

EUR | 311 | 300,128 | |||||||||

| 7.625%, 03/01/2026(a) |

U.S.$ | 246 | 224,475 | |||||||||

| 9.875%, 08/01/2027(a) |

437 | 448,917 | ||||||||||

| 10.125%, 02/01/2026(a) |

EUR | 310 | 353,127 | |||||||||

| 10.50%, 06/01/2030(a) |

U.S.$ | 212 | 203,520 | |||||||||

| Carnival Holdings Bermuda Ltd.

|

3,714 | 3,993,623 | ||||||||||

| Carnival PLC |

EUR | 202 | 111,371 | |||||||||

| Cedar Fair LP/Canada’s Wonderland Co./Magnum Management Corp./Millennium Op |

U.S.$ | 2,191 | 2,189,234 | |||||||||

| Cinemark USA, Inc.

|

521 | 452,179 | ||||||||||

| Lindblad Expeditions LLC

|

365 | 353,487 | ||||||||||

| Motion Bondco DAC

|

EUR | 670 | 641,078 | |||||||||

| NCL Corp., Ltd.

|

U.S.$ | 2,072 | 1,763,376 | |||||||||

| 22 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| 7.75%, 02/15/2029(a) |

U.S.$ | 93 | $ | 79,900 | ||||||||

| 8.375%, 02/01/2028(a) |

637 | 639,600 | ||||||||||

| NCL Finance Ltd.

|

39 | 31,639 | ||||||||||

| Royal Caribbean Cruises Ltd.

|

1,159 | 1,030,061 | ||||||||||

| 5.50%, 08/31/2026(a) |

1,118 | 1,045,945 | ||||||||||

| 5.50%, 04/01/2028(a) |

4,222 | 3,716,415 | ||||||||||

| 11.50%, 06/01/2025(a) |

1,409 | 1,502,403 | ||||||||||

| 11.625%, 08/15/2027(a) |

74 | 79,318 | ||||||||||

| Viking Cruises Ltd.

|

1,558 | 1,341,860 | ||||||||||

| 7.00%, 02/15/2029(a) |

1,837 | 1,575,601 | ||||||||||

| 13.00%, 05/15/2025(a) |

65 | 68,675 | ||||||||||

| VOC Escrow Ltd. |

1,822 | 1,614,751 | ||||||||||

|

|

|

|||||||||||

| 26,477,467 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - Other – 3.4% |

||||||||||||

| Adams Homes, Inc.

|

598 | 531,169 | ||||||||||

| Affinity Gaming

|

199 | 177,819 | ||||||||||

| Allwyn Entertainment Financing UK PLC |

EUR | 650 | 697,090 | |||||||||

| Beazer Homes USA, Inc. |

U.S.$ | 355 | 349,675 | |||||||||

| Brookfield Residential Properties, Inc./Brookfield Residential US LLC |

1,097 | 827,338 | ||||||||||

| 5.00%, 06/15/2029(a) |

167 | 127,751 | ||||||||||

| 6.25%, 09/15/2027(a) |

1,233 | 1,093,658 | ||||||||||

| Builders FirstSource, Inc.

|

244 | 210,958 | ||||||||||

| 6.375%, 06/15/2032(a) |

1,070 | 1,074,084 | ||||||||||

| Caesars Entertainment, Inc.

|

897 | 897,281 | ||||||||||

| 7.00%, 02/15/2030(a) |

1,275 | 1,297,064 | ||||||||||

| Castle UK Finco PLC |

GBP | 679 | 663,301 | |||||||||

| 7.904% (EURIBOR 3 Month + 5.25%), 05/15/2028(j) |

EUR | 514 | 463,930 | |||||||||

| Century Communities, Inc.

|

U.S.$ | 75 | 64,277 | |||||||||

| Churchill Downs, Inc.

|

520 | 486,910 | ||||||||||

| 5.50%, 04/01/2027(a) |

169 | 165,436 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 23 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| CP Atlas Buyer, Inc.

|

U.S.$ | 126 | $ | 93,484 | ||||||

| Everi Holdings, Inc.

|

240 | 215,208 | ||||||||

| Five Point Operating Co. LP/Five Point Capital Corp. |

1,969 | 1,765,922 | ||||||||

| Forestar Group, Inc.

|

385 | 349,139 | ||||||||

| Hilton Domestic Operating Co., Inc. |

1,728 | 1,456,778 | ||||||||

| 3.75%, 05/01/2029(a) |

62 | 55,489 | ||||||||

| 4.00%, 05/01/2031(a) |

54 | 47,279 | ||||||||

| 5.375%, 05/01/2025(a) |

229 | 228,497 | ||||||||

| 5.75%, 05/01/2028(a) |

450 | 449,707 | ||||||||

| Hilton Grand Vacations Borrower Escrow LLC/Hilton Grand Vacations Borrower Esc |

597 | 510,066 | ||||||||

| 5.00%, 06/01/2029(a) |

1,598 | 1,417,503 | ||||||||

| Installed Building Products, Inc.

|

291 | 269,350 | ||||||||

| Jacobs Entertainment, Inc.

|

131 | 114,452 | ||||||||

| Marriott Ownership Resorts, Inc.

|

255 | 217,089 | ||||||||

| Mattamy Group Corp.

|

170 | 149,925 | ||||||||

| 5.25%, 12/15/2027(a) |

178 | 167,488 | ||||||||

| MGM Resorts International |

1,047 | 976,300 | ||||||||

| 5.50%, 04/15/2027 |

1,163 | 1,126,921 | ||||||||

| 5.75%, 06/15/2025 |

30 | 29,939 | ||||||||

| Mohegan Tribal Gaming Authority

|

223 | 204,045 | ||||||||

| New Home Co., Inc. (The)

|

211 | 195,203 | ||||||||

| Premier Entertainment Sub LLC/Premier Entertainment Finance Corp. |

69 | 51,046 | ||||||||

| 5.875%, 09/01/2031(a) |

39 | 28,025 | ||||||||

| Scientific Games Holdings LP/Scientific Games US FinCo, Inc. |

112 | 99,495 | ||||||||

| Scientific Games International, Inc. |

135 | 138,178 | ||||||||

| Shea Homes LP/Shea Homes Funding Corp. |

549 | 490,647 | ||||||||

| 4.75%, 04/01/2029 |

911 | 796,348 | ||||||||

| 24 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Standard Industries, Inc./NJ

|

U.S.$ | 929 | $ | 806,606 | ||||||||

| 4.75%, 01/15/2028(a) |

163 | 152,168 | ||||||||||

| Sugarhouse HSP Gaming Prop Mezz LP/Sugarhouse HSP Gaming Finance Corp. |

1,785 | 1,696,294 | ||||||||||

| Taylor Morrison Communities, Inc.

|

292 | 286,874 | ||||||||||

| Thor Industries, Inc.

|

230 | 190,002 | ||||||||||

| TopBuild Corp. |

69 | 58,516 | ||||||||||

| Travel + Leisure Co.

|

976 | 850,400 | ||||||||||

| 4.625%, 03/01/2030(a) |

2,415 | 2,078,237 | ||||||||||

| 6.00%, 04/01/2027 |

112 | 110,976 | ||||||||||

| 6.625%, 07/31/2026(a) |

637 | 639,527 | ||||||||||

| Universal Entertainment Corp.

|

410 | 381,833 | ||||||||||

| Wyndham Hotels & Resorts, Inc. |

727 | 670,009 | ||||||||||

| Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp. |

781 | 738,045 | ||||||||||

| Wynn Resorts Finance LLC/Wynn Resorts Capital Corp. |

1,988 | 1,804,303 | ||||||||||

|

|

|

|||||||||||

| 31,235,054 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - Restaurants – 0.5% |

||||||||||||

| 1011778 BC ULC/New Red Finance, Inc. |

1,524 | 1,417,939 | ||||||||||

| 4.375%, 01/15/2028(a) |

315 | 290,706 | ||||||||||

| CEC Entertainment LLC

|

210 | 199,389 | ||||||||||

| KFC Holding Co./Pizza Hut Holdings LLC/Taco Bell of America LLC |

168 | 164,629 | ||||||||||

| Stonegate Pub Co. Financing 2019 PLC |

GBP | 192 | 217,780 | |||||||||

| 8.25%, 07/31/2025(a) |

1,245 | 1,431,353 | ||||||||||

| Yum! Brands, Inc. |

U.S.$ | 49 | 42,981 | |||||||||

| 4.625%, 01/31/2032 |

1,114 | 1,035,116 | ||||||||||

| 4.75%, 01/15/2030(a) |

85 | 81,211 | ||||||||||

|

|

|

|||||||||||

| 4,881,104 | ||||||||||||

|

|

|

|||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 25 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Consumer Cyclical - Retailers – 2.5% |

||||||||||||

| Arko Corp. |

U.S.$ | 1,035 | $ | 864,592 | ||||||||

| Asbury Automotive Group, Inc.

|

852 | 762,333 | ||||||||||

| 5.00%, 02/15/2032(a) |

826 | 724,071 | ||||||||||

| At Home Group, Inc.

|

63 | 36,045 | ||||||||||

| Bath & Body Works, Inc.

|

1,916 | 1,866,639 | ||||||||||

| 6.75%, 07/01/2036 |

299 | 267,020 | ||||||||||

| 6.875%, 11/01/2035 |

587 | 530,880 | ||||||||||

| 7.50%, 06/15/2029 |

107 | 109,153 | ||||||||||

| 7.60%, 07/15/2037 |

261 | 226,368 | ||||||||||

| 9.375%, 07/01/2025(a) |

41 | 43,997 | ||||||||||

| BCPE Ulysses Intermediate, Inc. |

518 | 405,728 | ||||||||||

| Bed Bath & Beyond, Inc. |

58 | 3,108 | ||||||||||

| Carvana Co. |

415 | 185,620 | ||||||||||

| 5.875%, 10/01/2028(a) |

1,298 | 572,418 | ||||||||||

| eG Global Finance PLC

|

428 | 402,575 | ||||||||||

| 8.50%, 10/30/2025(a) |

408 | 378,973 | ||||||||||

| Foundation Building Materials, Inc.

|

246 | 195,584 | ||||||||||

| Gap, Inc. (The)

|

56 | 38,003 | ||||||||||

| Group 1 Automotive, Inc.

|

276 | 242,833 | ||||||||||

| Guitar Center, Inc.

|

145 | 127,201 | ||||||||||

| Kontoor Brands, Inc.

|

894 | 763,788 | ||||||||||

| LBM Acquisition LLC

|

81 | 62,261 | ||||||||||

| LCM Investments Holdings II LLC

|

52 | 43,469 | ||||||||||

| Levi Strauss & Co.

|

746 | 636,498 | ||||||||||

| Lithia Motors, Inc.

|

65 | 56,207 | ||||||||||

| 4.375%, 01/15/2031(a) |

60 | 51,737 | ||||||||||

| 26 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| LSF9 Atlantis Holdings LLC/Victra Finance Corp. |

U.S.$ | 154 | $ | 140,154 | ||||||||

| Michaels Cos, Inc. (The)

|

1,475 | 1,229,006 | ||||||||||

| 7.875%, 05/01/2029(a) |

1,378 | 964,282 | ||||||||||

| Murphy Oil USA, Inc.

|

246 | 207,315 | ||||||||||

| 4.75%, 09/15/2029 |

201 | 185,531 | ||||||||||

| 5.625%, 05/01/2027 |

69 | 66,927 | ||||||||||

| NMG Holding Co., Inc./Neiman Marcus Group LLC |

1,720 | 1,614,838 | ||||||||||

| Nordstrom, Inc. |

159 | 113,517 | ||||||||||

| 4.375%, 04/01/2030 |

47 | 36,059 | ||||||||||

| 5.00%, 01/15/2044 |

4 | 2,515 | ||||||||||

| Penske Automotive Group, Inc. |

1,029 | 887,726 | ||||||||||

| QVC, Inc. |

5 | 2,025 | ||||||||||

| 4.75%, 02/15/2027 |

213 | 89,393 | ||||||||||

| 4.85%, 04/01/2024 |

133 | 106,425 | ||||||||||

| Rite Aid Corp. |

992 | 593,524 | ||||||||||

| Sonic Automotive, Inc.

|

1,864 | 1,581,396 | ||||||||||

| 4.875%, 11/15/2031(a) |

221 | 180,926 | ||||||||||

| Specialty Building Products Holdings LLC/SBP Finance Corp. |

508 | 466,961 | ||||||||||

| Staples, Inc. |

2,323 | 2,035,037 | ||||||||||

| 10.75%, 04/15/2027(a) |

1,271 | 921,702 | ||||||||||

| TPro Acquisition Corp.

|

1,062 | 1,062,570 | ||||||||||

| Victoria’s Secret & Co. |

58 | 46,934 | ||||||||||

| White Cap Buyer LLC

|

226 | 196,357 | ||||||||||

| White Cap Parent LLC |

329 | 300,316 | ||||||||||

|

|

|

|||||||||||

| 22,628,537 | ||||||||||||

|

|

|

|||||||||||

| Consumer Non-Cyclical – 7.2% |

||||||||||||

| AdaptHealth LLC

|

288 | 263,759 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 27 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| AHP Health Partners, Inc.

|

U.S.$ | 988 | $ | 830,003 | ||||||

| Albertsons Cos., Inc./Safeway, Inc./New Albertsons LP/Albertsons LLC |

615 | 594,426 | ||||||||

| 4.875%, 02/15/2030(a) |

200 | 186,687 | ||||||||

| 6.50%, 02/15/2028(a) |

2,469 | 2,489,223 | ||||||||

| B&G Foods, Inc. |

193 | 179,577 | ||||||||

| Bausch Health Americas, Inc.

|

543 | 246,447 | ||||||||

| Bausch Health Cos., Inc.

|

2,835 | 1,684,730 | ||||||||

| 5.00%, 02/15/2029(a) |

1,338 | 520,917 | ||||||||

| 5.25%, 01/30/2030(a) |

8 | 2,978 | ||||||||

| 5.50%, 11/01/2025(a) |

196 | 163,472 | ||||||||

| 6.125%, 02/01/2027(a) |

303 | 196,319 | ||||||||

| 6.25%, 02/15/2029(a) |

911 | 362,211 | ||||||||

| 7.00%, 01/15/2028(a) |

204 | 81,920 | ||||||||

| 7.25%, 05/30/2029(a) |

254 | 97,893 | ||||||||

| 11.00%, 09/30/2028(a) |

236 | 173,569 | ||||||||

| Cab Selas |

EUR | 1,880 | 1,672,351 | |||||||

| CD&R Smokey Buyer, Inc.

|

U.S.$ | 203 | 174,143 | |||||||

| Cheplapharm Arzneimittel GmbH

|

436 | 388,419 | ||||||||

| CHS/Community Health Systems, Inc.

|

493 | 364,607 | ||||||||

| 5.25%, 05/15/2030(a) |

66 | 51,435 | ||||||||

| 5.625%, 03/15/2027(a) |

416 | 360,926 | ||||||||

| 6.125%, 04/01/2030(a) |

3,702 | 2,230,486 | ||||||||

| 6.875%, 04/01/2028(a)(i) |

577 | 357,724 | ||||||||

| 6.875%, 04/15/2029(a) |

1,537 | 951,080 | ||||||||

| 8.00%, 03/15/2026(a) |

807 | 780,281 | ||||||||

| Coty, Inc. |

133 | 128,828 | ||||||||

| DaVita, Inc. |

687 | 541,328 | ||||||||

| 4.625%, 06/01/2030(a) |

3,556 | 3,034,337 | ||||||||

| Edgewell Personal Care Co.

|

164 | 145,137 | ||||||||

| 5.50%, 06/01/2028(a) |

81 | 77,563 | ||||||||

| Elanco Animal Health, Inc. |

1,416 | 1,336,442 | ||||||||

| Embecta Corp. |

2,581 | 2,222,002 | ||||||||

| 28 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Emergent BioSolutions, Inc.

|

U.S.$ | 1,516 | $ | 736,212 | ||||||

| Garden Spinco Corp.

|

883 | 954,841 | ||||||||

| Global Medical Response, Inc.

|

431 | 318,012 | ||||||||

| Grifols Escrow Issuer SA

|

EUR | 2,222 | 1,878,790 | |||||||

| Gruenenthal GmbH

|

885 | 901,183 | ||||||||

| 4.125%, 05/15/2028(a) |

1,141 | 1,122,954 | ||||||||

| Herbalife Nutrition Ltd./HLF Financing, Inc. |

U.S.$ | 59 | 55,165 | |||||||

| Hologic, Inc. |

246 | 218,963 | ||||||||

| IQVIA, Inc. |

EUR | 862 | 796,017 | |||||||

| Jazz Securities DAC

|

U.S.$ | 954 | 875,237 | |||||||

| Kronos Acquisition Holdings, Inc./KIK Custom Products, Inc. |

1,951 | 1,698,204 | ||||||||

| Lamb Weston Holdings, Inc.

|

1,209 | 1,106,791 | ||||||||

| 4.875%, 05/15/2028(a) |

204 | 198,496 | ||||||||

| Legacy LifePoint Health LLC

|

2,831 | 2,316,402 | ||||||||

| 6.75%, 04/15/2025(a) |

89 | 84,385 | ||||||||

| LifePoint Health, Inc.

|

41 | 25,066 | ||||||||

| Mallinckrodt International Finance SA/Mallinckrodt CB LLC |

109 | 63,421 | ||||||||

| 11.50%, 12/15/2028(a) |

201 | 164,457 | ||||||||

| Medline Borrower LP

|

1,738 | 1,507,973 | ||||||||

| 5.25%, 10/01/2029(a) |

3,373 | 2,926,386 | ||||||||

| Newell Brands, Inc. |

687 | 661,409 | ||||||||

| 4.875%, 06/01/2025 |

170 | 166,469 | ||||||||

| 5.875%, 04/01/2036 |

88 | 77,955 | ||||||||

| 6.00%, 04/01/2046 |

41 | 33,572 | ||||||||

| 6.375%, 09/15/2027 |

1,500 | 1,513,676 | ||||||||

| 6.625%, 09/15/2029 |

1,500 | 1,511,863 | ||||||||

| Organon & Co./Organon Foreign Debt Co-Issuer BV

|

EUR | 885 | 844,609 | |||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 29 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| 4.125%, 04/30/2028(a) |

U.S.$ | 1,837 | $ | 1,690,695 | ||||||

| 5.125%, 04/30/2031(a) |

420 | 372,819 | ||||||||

| Oriflame Investment Holding PLC

|

347 | 207,459 | ||||||||

| Owens & Minor, Inc.

|

47 | 37,304 | ||||||||

| 6.625%, 04/01/2030(a) |

19 | 16,313 | ||||||||

| Performance Food Group, Inc.

|

187 | 168,911 | ||||||||

| 5.50%, 10/15/2027(a) |

190 | 185,756 | ||||||||

| Perrigo Finance Unlimited Co. |

691 | 619,563 | ||||||||

| Post Holdings, Inc.

|

1,564 | 1,376,383 | ||||||||

| 4.625%, 04/15/2030(a) |

870 | 779,891 | ||||||||

| 5.50%, 12/15/2029(a) |

529 | 500,813 | ||||||||

| Prime Healthcare Services, Inc.

|

225 | 199,907 | ||||||||

| Primo Water Holdings, Inc.

|

1,227 | 1,077,699 | ||||||||

| Radiology Partners, Inc.

|

1,599 | 883,611 | ||||||||

| RegionalCare Hospital Partners Holdings, Inc./LifePoint Health, Inc. |

990 | 800,233 | ||||||||

| RP Escrow Issuer LLC

|

638 | 483,351 | ||||||||

| Simmons Foods Inc/Simmons Prepared Foods Inc/Simmons Pet Food Inc/Simmons Feed |

10 | 8,124 | ||||||||

| Spectrum Brands, Inc.

|

2,079 | 1,720,319 | ||||||||

| 4.00%, 10/01/2026(a) |

EUR | 530 | 537,320 | |||||||

| Tenet Healthcare Corp. |

U.S.$ | 2,307 | 2,071,123 | |||||||

| 6.125%, 10/01/2028 |

872 | 831,403 | ||||||||

| 6.125%, 06/15/2030(a) |

1,017 | 1,004,628 | ||||||||

| Triton Water Holdings, Inc.

|

884 | 696,694 | ||||||||

| United Natural Foods, Inc.

|

187 | 173,533 | ||||||||

| US Acute Care Solutions LLC

|

3,003 | 2,676,705 | ||||||||

| US Renal Care, Inc.

|

616 | 164,568 | ||||||||

| 30 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Vector Group Ltd.

|

U.S.$ | 188 | $ | 167,237 | ||||||||

| 10.50%, 11/01/2026(a) |

188 | 189,120 | ||||||||||

| Vista Outdoor, Inc.

|

202 | 162,904 | ||||||||||

|

|

|

|||||||||||

| 65,454,114 | ||||||||||||

|

|

|

|||||||||||

| Energy – 4.0% |

||||||||||||

| Aethon United BR LP/Aethon United Finance Corp. |

68 | 66,694 | ||||||||||

| Ascent Resources Utica Holdings LLC/ARU Finance Corp. |

18 | 17,394 | ||||||||||

| Berry Petroleum Co. LLC

|

245 | 229,482 | ||||||||||

| Blue Racer Midstream LLC/Blue Racer Finance Corp. |

421 | 417,852 | ||||||||||

| Buckeye Partners LP |

6 | 5,429 | ||||||||||

| 4.125%, 03/01/2025(a) |

171 | 162,744 | ||||||||||

| 4.125%, 12/01/2027 |

214 | 189,888 | ||||||||||

| 4.50%, 03/01/2028(a) |

17 | 15,336 | ||||||||||

| Callon Petroleum Co. |

301 | 299,748 | ||||||||||

| Calumet Specialty Products Partners LP/Calumet Finance Corp. |

33 | 33,956 | ||||||||||

| CGG SA |

422 | 356,988 | ||||||||||

| Chesapeake Energy Corp.

|

135 | 128,479 | ||||||||||

| 6.75%, 04/15/2029(a) |

158 | 156,729 | ||||||||||

| Citgo Holding, Inc.

|

478 | 479,107 | ||||||||||

| CITGO Petroleum Corp.

|

471 | 461,788 | ||||||||||

| 7.00%, 06/15/2025(a) |

1,781 | 1,761,312 | ||||||||||

| Civitas Resources, Inc.

|

682 | 643,357 | ||||||||||

| CNX Resources Corp.

|

423 | 397,515 | ||||||||||

| 7.375%, 01/15/2031(a) |

72 | 70,915 | ||||||||||

| Comstock Resources, Inc.

|

30 | 25,868 | ||||||||||

| 6.75%, 03/01/2029(a) |

294 | 267,674 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 31 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Crescent Energy Finance LLC

|

U.S.$ | 1,005 | $ | 944,724 | ||||||

| Crestwood Midstream Partners LP/Crestwood Midstream Finance Corp. |

182 | 175,415 | ||||||||

| 6.00%, 02/01/2029(a) |

54 | 51,286 | ||||||||

| 8.00%, 04/01/2029(a) |

101 | 102,958 | ||||||||

| CVR Energy, Inc.

|

223 | 215,127 | ||||||||

| Earthstone Energy Holdings LLC

|

151 | 148,134 | ||||||||

| Encino Acquisition Partners Holdings LLC |

1,352 | 1,181,992 | ||||||||

| Enerflex Ltd. |

174 | 169,236 | ||||||||

| EnLink Midstream Partners LP |

2,734 | 2,318,888 | ||||||||

| EQM Midstream Partners LP

|

811 | 689,560 | ||||||||

| 4.75%, 01/15/2031(a) |

859 | 713,296 | ||||||||

| 6.50%, 07/15/2048 |

137 | 105,645 | ||||||||

| FTAI Infra Escrow Holdings LLC

|

157 | 155,781 | ||||||||

| Genesis Energy LP/Genesis Energy Finance Corp. |

92 | 87,864 | ||||||||

| 6.50%, 10/01/2025 |

411 | 399,295 | ||||||||

| 7.75%, 02/01/2028 |

440 | 431,272 | ||||||||

| 8.00%, 01/15/2027 |

738 | 728,218 | ||||||||

| 8.875%, 04/15/2030 |

74 | 75,240 | ||||||||

| Global Partners LP/GLP Finance Corp. |

439 | 405,283 | ||||||||

| 7.00%, 08/01/2027 |

403 | 387,356 | ||||||||

| Gulfport Energy Corp.

|

589 | 371 | ||||||||

| 6.375%, 05/15/2025(c) |

1,547 | 975 | ||||||||

| 6.375%, 01/15/2026(c) |

1,710 | 1,077 | ||||||||

| 6.625%, 05/01/2023(c) |

161 | 101 | ||||||||

| 8.00%, 05/17/2026(a) |

610 | 603,871 | ||||||||

| Harbour Energy PLC

|

200 | 177,667 | ||||||||

| Harvest Midstream I LP

|

69 | 68,797 | ||||||||

| Hess Midstream Operations LP

|

481 | 475,555 | ||||||||

| 32 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Hilcorp Energy I LP/Hilcorp Finance Co. |

U.S.$ | 233 | $ | 216,773 | ||||||

| 6.00%, 02/01/2031(a) |

340 | 314,262 | ||||||||

| 6.25%, 04/15/2032(a) |

96 | 88,755 | ||||||||

| Ithaca Energy North Sea PLC

|

1,188 | 1,137,105 | ||||||||

| ITT Holdings LLC

|

2,299 | 1,939,185 | ||||||||

| KLX Energy Services Holdings, Inc.

|

64 | 60,160 | ||||||||

| MEG Energy Corp.

|

231 | 222,572 | ||||||||

| Moss Creek Resources Holdings, Inc.

|

713 | 661,396 | ||||||||

| 10.50%, 05/15/2027(a) |

202 | 192,225 | ||||||||

| Murphy Oil Corp. |

211 | 206,348 | ||||||||

| Nabors Industries Ltd.

|

403 | 384,279 | ||||||||

| 7.50%, 01/15/2028(a) |

2,085 | 1,915,563 | ||||||||

| Nabors Industries, Inc.

|

319 | 312,381 | ||||||||

| New Fortress Energy, Inc.

|

1,126 | 1,083,052 | ||||||||

| NGL Energy Operating LLC/NGL Energy Finance Corp. |

1,614 | 1,557,965 | ||||||||

| Northern Oil and Gas, Inc.

|

97 | 96,064 | ||||||||

| NuStar Logistics LP |

144 | 140,678 | ||||||||

| 6.375%, 10/01/2030 |

278 | 266,644 | ||||||||

| Parkland Corp. |

220 | 195,517 | ||||||||

| 4.625%, 05/01/2030(a) |

220 | 195,474 | ||||||||

| 5.875%, 07/15/2027(a) |

90 | 87,290 | ||||||||

| PBF Holding Co. LLC/PBF Finance Corp. |

216 | 207,686 | ||||||||

| 7.25%, 06/15/2025 |

212 | 211,140 | ||||||||

| PDC Energy, Inc. |

1,575 | 1,533,184 | ||||||||

| 6.125%, 09/15/2024 |

593 | 590,740 | ||||||||

| Permian Resources Operating LLC

|

42 | 39,779 | ||||||||

| Petrofac Ltd. |

200 | 149,284 | ||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 33 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Rockies Express Pipeline LLC

|

U.S.$ | 174 | $ | 163,551 | ||||||||

| 6.875%, 04/15/2040(a) |

77 | 64,662 | ||||||||||

| SM Energy Co. |

26 | 25,466 | ||||||||||

| Southwestern Energy Co. |

187 | 176,512 | ||||||||||

| 8.375%, 09/15/2028 |

120 | 126,175 | ||||||||||

| Strathcona Resources Ltd.

|

227 | 180,018 | ||||||||||

| Summit Midstream Holdings LLC/Summit Midstream Finance Corp. |

1,086 | 1,043,204 | ||||||||||

| Sunnova Energy Corp.

|

503 | 426,591 | ||||||||||

| Sunoco LP/Sunoco Finance Corp. |

114 | 104,456 | ||||||||||

| 5.875%, 03/15/2028 |

774 | 755,078 | ||||||||||

| 6.00%, 04/15/2027 |

192 | 190,268 | ||||||||||

| Tallgrass Energy Partners LP/Tallgrass Energy Finance Corp. |

9 | 8,560 | ||||||||||

| 6.00%, 12/31/2030(a) |

160 | 142,891 | ||||||||||

| 6.00%, 09/01/2031(a) |

151 | 133,635 | ||||||||||

| Topaz Solar Farms LLC

|

143 | 135,792 | ||||||||||

| Transocean Poseidon Ltd.

|

18 | 17,489 | ||||||||||

| Transocean, Inc.

|

82 | 83,640 | ||||||||||

| 11.50%, 01/30/2027(a) |

211 | 218,123 | ||||||||||

| USA Compression Partners LP/USA Compression Finance Corp. |

225 | 215,061 | ||||||||||

| Venture Global Calcasieu Pass LLC

|

890 | 781,525 | ||||||||||

| Weatherford International Ltd.

|

175 | 177,224 | ||||||||||

| 11.00%, 12/01/2024(a) |

9 | 9,243 | ||||||||||

|

|

|

|||||||||||

| 36,187,904 | ||||||||||||

|

|

|

|||||||||||

| Other Industrial – 0.2% |

||||||||||||

| AECOM |

221 | 216,764 | ||||||||||

| American Builders & Contractors Supply Co., Inc. |

100 | 91,339 | ||||||||||

| 34 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND |

abfunds.com | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Grand Canyon University |

U.S.$ | 207 | $ | 195,553 | ||||||||

| Ritchie Bros Holdings, Inc.

|

768 | 790,823 | ||||||||||

| 7.75%, 03/15/2031(a) |

703 | 736,649 | ||||||||||

|

|

|

|||||||||||

| 2,031,128 | ||||||||||||

|

|

|

|||||||||||

| Services – 3.5% |

||||||||||||

| ADT Security Corp. (The) |

11 | 10,958 | ||||||||||

| 4.875%, 07/15/2032(a) |

1,097 | 958,806 | ||||||||||

| Allied Universal Holdco LLC/Allied Universal Finance Corp. |

327 | 243,764 | ||||||||||

| 6.625%, 07/15/2026(a) |

312 | 299,655 | ||||||||||

| 9.75%, 07/15/2027(a) |

1,363 | 1,212,121 | ||||||||||

| Allied Universal Holdco LLC/Allied Universal Finance Corp./Atlas Luxco 4 SARL |

EUR | 255 | 226,775 | |||||||||

| 4.625%, 06/01/2028(a) |

U.S.$ | 1,727 | 1,450,099 | |||||||||

| 4.875%, 06/01/2028(a) |

GBP | 1,010 | 1,019,873 | |||||||||

| AMN Healthcare, Inc.

|

U.S.$ | 205 | 190,902 | |||||||||

| ANGI Group LLC |

2,420 | 1,893,326 | ||||||||||

| Aptim Corp. |

627 | 429,495 | ||||||||||

| APX Group, Inc. |

1,504 | 1,347,476 | ||||||||||

| 6.75%, 02/15/2027(a) |

676 | 672,245 | ||||||||||

| Aramark Services, Inc.

|

1,064 | 1,006,777 | ||||||||||

| Block, Inc. |

463 | 422,245 | ||||||||||

| 3.50%, 06/01/2031 |

1,474 | 1,209,531 | ||||||||||

| Brink’s Co. (The)

|

176 | 166,205 | ||||||||||

| Cars.com, Inc. |

830 | 784,635 | ||||||||||

| CoreLogic, Inc. |

119 | 92,212 | ||||||||||

| Garda World Security Corp.

|

102 | 92,553 | ||||||||||

| 6.00%, 06/01/2029(a) |

99 | 78,705 | ||||||||||

| 7.75%, 02/15/2028(a) |

1,355 | 1,335,643 | ||||||||||

| 9.50%, 11/01/2027(a) |

479 | 455,403 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 35 | |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Gartner, Inc. |

U.S.$ | 237 | $ | 211,695 | ||||||

| 4.50%, 07/01/2028(a) |

210 | 199,311 | ||||||||

| GrubHub Holdings, Inc.

|

234 | 176,241 | ||||||||

| IHS Markit Ltd. |

202 | 200,788 | ||||||||

| 4.75%, 08/01/2028 |

104 | 102,427 | ||||||||

| ION Trading Technologies SARL

|

1,067 | 854,558 | ||||||||

| Korn Ferry |

402 | 379,890 | ||||||||

| Millennium Escrow Corp.

|

1,828 | 1,187,064 | ||||||||

| Monitronics International, Inc.

|

958 | – 0 | – | |||||||

| MPH Acquisition Holdings

LLC |

1,922 | 1,548,460 | ||||||||

| 5.75%, 11/01/2028(a)(i) |

3,593 | 2,588,739 | ||||||||

| Neptune Bidco US, Inc.

|

2,157 | 1,999,062 | ||||||||

| Photo Holdings Merger Sub, Inc.

|

64 | 28,110 | ||||||||

| Prime Security Services Borrower LLC/Prime Finance, Inc. |

618 | 554,035 | ||||||||

| 5.25%, 04/15/2024(a) |

25 | 24,798 | ||||||||

| 6.25%, 01/15/2028(a) |

1,619 | 1,520,153 | ||||||||

| Q-Park Holding I BV |

EUR | 184 | 183,477 | |||||||

| 2.00%, 03/01/2027(a) |

579 | 521,798 | ||||||||

| Rakuten Group, Inc.

|

U.S.$ | 200 | 191,649 | |||||||

| Sabre GLBL, Inc.

|

378 | 355,918 | ||||||||

| 11.25%, 12/15/2027(a) |