Form DEFA14A Hilton Grand Vacations

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of Earliest Event Reported): May 17, 2021

Hilton Grand Vacations Inc.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 001-37794 | 81-2545345 | ||

| (State or Other Jurisdiction of Incorporation) |

(Commission File Number) |

(IRS Employer Identification No.) |

| 6355 MetroWest Boulevard, Suite 180 Orlando, Florida |

32835 | |

| (Address of principal executive offices) | (Zip Code) |

(407) 613-3100

(Registrant’s Telephone Number, Including Area Code)

Not Applicable

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☐ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☒ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

| Common Stock, $0.01 par value per share | HGV | New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 7.01 | Regulation FD Disclosure. |

On May 17, 2021, Hilton Grand Vacations Borrower Escrow LLC and Hilton Grand Vacations Borrower Escrow Inc., each wholly-owned subsidiaries of Hilton Grand Vacations Inc. (the “Company”), commenced an offering (the “Offering”) of $675 million in aggregate principal amount of senior notes due 2029 in a private placement exempt from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”). The Company intends to use the proceeds from the Offering to finance the repayment of certain indebtedness in connection with the Company’s previously announced proposed acquisition (the “Merger”) of Dakota Holdings, Inc. (“Diamond”), pursuant to the Agreement and Plan of Merger, dated March 10, 2021, by and among the Company, Hilton Grand Vacations Borrower LLC, Diamond and certain stockholders of Diamond (the “Merger Agreement”).

In connection with the Offering, the Company disclosed certain information relating to the Company, Diamond and the Merger to prospective investors in a preliminary offering memorandum, dated May 17, 2021 (the “Preliminary Offering Memorandum”), excerpts of which are furnished herewith pursuant to Regulation FD, in the general form presented in the Preliminary Offering Memorandum, as Exhibit 99.1 to this Current Report on Form 8-K and is incorporated herein by reference.

The information furnished under this Item 7.01 of this Current Report on Form 8-K, including Exhibit 99.1, shall not be deemed to be “filed” for the purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference in any filing made by the Company under the Securities Act, or the Exchange Act, except as shall be expressly set forth by specific reference in such a filing.

| Item 8.01 | Other Events. |

On May 17, 2021, the Company issued a press release regarding the Offering in accordance with Rule 135c under the Securities Act. A copy of the press release is attached hereto as Exhibit 99.2 to this Current Report on Form 8-K and is incorporated herein by reference.

| Item 9.01 | Financial Statements and Exhibits. |

(d) Exhibits.

| Exhibit No. | Description | |

| Exhibit 99.1 | Excerpts from preliminary offering memorandum of the Company, dated May 17, 2021. | |

| Exhibit 99.2 | Press Release, dated May 17, 2021. | |

| Exhibit 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document). | |

Forward Looking Statements

This communication contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Exchange Act. Forward-looking statements convey management’s expectations as to the Company’s future, and are based on management’s beliefs, expectations, assumptions and such plans, estimates, projections and other information available to management at the time the Company makes such statements. Forward-looking statements include all statements that are not historical facts, including those related to the proposed Merger and the Company’s revenues, earnings, cash flow and operations, and may be identified by terminology such as the words “outlook,” “believe,” “expect,” “potential,” “goal,” “continues,” “may,” “will,” “should,” “could,” “seeks,” “approximately,” “projects,” predicts,” “intends,” “plans,” “estimates,” “anticipates” “future,” “guidance,” “target,” or the negative version of these words or other comparable words.

The Company cautions you that forward-looking statements involve known and unknown risks, uncertainties and other factors, including those that are beyond the Company’s control, that may cause its actual results, performance or achievements to be materially different from the future results. Factors that could cause the Company’s actual results to differ materially from those contemplated by its forward-looking statements include: the occurrence of any event, change or other circumstances that could give rise to the termination of the Merger Agreement; the inability to complete the proposed Merger due to the failure to obtain stockholder approval for the proposed Merger or the failure to satisfy other conditions to completion of the proposed Merger, including that a governmental entity may prohibit, delay or refuse to grant approval for the consummation of the transaction; risks related to disruption of management’s attention from the Company’s ongoing business operations due to the transaction; the effect of the announcement of the proposed Merger on the Company’s relationships, operating results and business generally; the risk that the proposed Merger will not be consummated in a timely manner; exceeding the expected costs of the Merger; the material impact of the COVID-19 pandemic on the Company’s business, operating results, and financial condition; the extent and duration of the impact of the COVID-19 pandemic on global economic conditions; the Company’s ability to meet its liquidity needs; risks related to the Company’s indebtedness; inherent business risks, market trends and competition within the timeshare and hospitality industries; the Company’s ability to successfully source inventory and market, sell and finance VOIs; default rates on the Company’s financing receivables; the reputation of and the Company’s ability to access Hilton Worldwide Holdings Inc.’s (“Hilton”) brands and programs, including the risk of a breach or termination of the Company’s license agreement with Hilton; compliance with and changes to United States and global laws and regulations, including those related to anti-corruption and privacy; risks related to the Company’s acquisitions, joint ventures, and other partnerships; the Company’s dependence on third-party development activities to secure just-in-time inventory; the performance of the Company’s information technology systems and its ability to maintain data security; regulatory proceedings or litigation; adequacy of the Company’s workforce to meet its business and operation needs; the Company’s ability to attract and retain key executives and employees with skills and capacity to meet its needs; and natural disasters or adverse geo-political conditions. Any one or more of the foregoing factors could adversely impact the Company’s operations, revenue, operating margins, financial condition and/or credit rating.

For a more detailed discussion of these factors, see the information under the captions “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in the Company’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 1, 2021, and its Quarterly Report on Form 10-Q for the Quarter Ended March 31, 2021, and filed with the SEC on April 29, 2021, which may be updated from time to time in the Company’s annual reports, quarterly reports, current reports and other filings the Company makes with the SEC.

The Company’s forward-looking statements speak only as of the date of this communication or as of the date they are made. The Company disclaims any intent or obligation to update any “forward looking statement” made in this communication to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time.

Additional Information about the Proposed Transaction and Where to Find It

This communication may be deemed solicitation material in respect of the proposed Merger. In connection with the proposed Merger transaction, the Company has filed with the SEC a preliminary proxy statement and other documents regarding the proposed Merger, and plans to file with the SEC a definitive proxy statement as well as other documents regarding the proposed Merger. This communication does not constitute a solicitation of any vote or approval. Stockholders are urged to read the preliminary proxy statement, the definitive proxy statement when it becomes available and any other documents to be filed with the SEC in connection with the proposed Merger or incorporated by reference in the proxy statement because they will contain important information about the proposed Merger.

Investors may obtain free of charge the preliminary proxy statement, definitive proxy statement when it becomes available, and other documents filed with the SEC at the SEC’s website at https://www.sec.gov. In addition, the proxy statement and the Company’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnish pursuant to Section 13(a) or 15(d) of the Exchange Act are available free of charge through the Company’s website at https://investors.hgv.com/ as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC.

The directors, executive officers and certain other members of management and employees of the Company may be deemed “participants” in the solicitation of proxies from stockholders of the Company in favor of the proposed Merger. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of the stockholders of the Company in connection with the proposed Merger can be found in the preliminary proxy statement and the other relevant documents that will be filed with the SEC. You can find information about the Company’s executive officers and directors in its Annual Report on Form 10-K for the fiscal year ended December 31, 2020 and in its definitive proxy statement for the 2021 annual meeting of stockholders filed with the SEC on Schedule 14A on March 26, 2021.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| HILTON GRAND VACATIONS INC. | ||

| By: | /s/ Charles R. Corbin | |

| Charles R. Corbin | ||

| Executive Vice President, General Counsel and Secretary | ||

Date: May 17, 2021

Exhibit 99.1

EXCERPTS FROM THE PRELIMINARY OFFERING MEMORANDUM, DATED MAY 17, 2021

CERTAIN DEFINITIONS

As used in this offering memorandum, unless otherwise specified or the context otherwise requires, references to:

| • | “contract sales” represents the total amount of VOI products under purchase agreements signed during the period where we have received a down payment of at least 10 percent of the contract price. Contract sales is not a recognized term under U.S. GAAP, and should not be considered in isolation or as an alternative to timeshare sales, net, or any other comparable operating measure derived in accordance with U.S. GAAP. For a reconciliation of contract sales to sales of VOIs, net, which we believe is the most closely comparable U.S. GAAP financial measure, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—Real Estate”; |

| • | “developed” refers to VOI inventory sourced from projects developed by HGV; |

| • | “fee-for-service” refers to VOI inventory we sell and manage on behalf of third-party developers; |

| • | “Hilton” refers to Hilton Worldwide Holdings Inc. and its consolidated subsidiaries, and references to “Hilton Parent” or “Parent” refer only to Hilton Worldwide Holdings Inc., exclusive of its subsidiaries; |

| • | “Hilton Grand Vacations,” “HGV,” “we,” “our,” “us,” “the Company” and “our company” refer to Hilton Grand Vacations Inc. and its consolidated subsidiaries; |

| • | “just-in-time” refers to VOI inventory sourced in transactions that are designed to closely correlate the timing of the acquisition with our sale of that inventory to purchasers; |

| • | “owned inventory” refers to our developed and just-in-time VOI inventory; |

| • | “Spin-Off” refers to the tax-free spin-off of HGV from Hilton completed on January 3, 2017; and |

| • | “VOI” refers to vacation ownership intervals. |

Summary

OUR COMPANY

Hilton Grand Vacations is a timeshare company that markets and sells vacation ownership intervals (“VOIs”), manages resorts in top leisure and urban destinations and operates a points-based vacation exchange program. As of March 31, 2021, we have 62 managed properties representing 499,616 VOIs, that are primarily located in vacation destinations such as Orlando, Las Vegas, the Hawaiian Islands, New York City, Washington D.C., South Carolina, Barbados and Mexico and feature spacious, condominium-style accommodations with superior amenities and quality service. As of March 31, 2021, we had approximately 328,000 Hilton Grand Vacations Club and Hilton Club (collectively the “HGV Club”) members. HGV Club members have the flexibility to exchange their VOIs for stays at other Hilton Grand Vacations resorts or properties in the Hilton system of 18 industry-leading brands across approximately 6,400 properties, as well as numerous experiential vacation options, such as cruises and guided tours.

Our compelling VOI product allows customers to advance purchase a lifetime of vacations. Because our VOI owners generally purchase only the vacation time they intend to use each year, they are able to efficiently split the full cost of owning and maintaining a vacation residence with other owners. Our customers also benefit from the high-quality amenities and service at our Hilton-branded resorts. Furthermore, our points-based reservation platform offers members tremendous flexibility, enabling us to more effectively adapt to their changing vacation needs over time. Building on the strength of that platform, we continuously seek new ways to add value to our HGV Club membership, including enhanced product offerings, greater geographic distribution, broader exchange networks and further technological innovation, all of which drive better, more personalized vacation experiences and guest satisfaction.

As innovators in the timeshare business, we continually seek to enhance our inventory strategy by developing an optimal inventory mix focused on developed properties as well as fee-for-service and just-in-time agreements to sell VOIs on behalf of or acquired from third-party developers.

We operate our business across two segments: (1) real estate sales and financing and (2) resort operations and club management. For more information regarding our segments, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations –HGV”, and Note 22: Business Segments in our audited consolidated financial statements and Note 18: Business Segments in our unaudited condensed consolidated financial statements, each included in this offering memorandum.

Our real estate sales and financing segment primarily generates revenue from:

| • | VOI Sales—We sell our owned inventory and, through our fee-for-service agreements, we sell VOIs on behalf of third-party developers using the Hilton Grand Vacations brand in exchange for sales, marketing and brand fees. Under these fee-for-service agreements, we earn commission fees based on a percentage of total interval sales. |

2

| • | Financing—We provide consumer financing, which includes interest income generated from the origination of consumer loans to members to finance their purchase of VOIs owned by us. We also generate fee revenue from servicing the loans provided by third-party developers to purchasers of their VOIs. |

Our resort operations and club management segment primarily generates revenue from:

| • | Resort Management—Our resort management services primarily consist of operating properties under management agreements for the benefit of homeowners’ association (“HOA”s) of VOI owners at both our resorts and those developed by third parties. Our management agreements with HOAs provide for a cost-plus management fee, which means we generally earn a fee equal to 10 percent to 15 percent of the costs to operate the applicable resort. |

| • | Club Management—We manage the HGV Club and receive activation fees, annual dues and transaction fees from member exchanges for other vacation products. |

| • | Rental of Available Inventory—We generate rental revenue from unit rentals of unsold inventory and inventory made available due to ownership exchanges through the HGV Club programs. This allows us to utilize otherwise unoccupied inventory to generate additional revenues. We also earn fee revenue from the rental of inventory owned by third parties as well as revenue from retail and spa outlets at our timeshare properties. |

Other than the United States, there were no countries that individually represented more than 10 percent of total revenues for the year ended December 31, 2020.

In the twelve months ended March 31, 2021 and the years ended December 31, 2020, 2019 and 2018, HGV had approximately 88,000, 127,000, 383,000 and 358,000 tours, respectively. In the twelve months ended March 31, 2021 and the years ended December 31, 2020, 2019 and 2018, HGV had approximately 328,000, 328,000, 326,000 and 309,000 owners, respectively. In the twelve months ended March 31, 2021 and the years ended December 31, 2020, 2019 and 2018, HGV had VPG of approximately $4,647, $3,889, $3,518 and $3,743, respectively. In the twelve months ended March 31, 2021 and the years ended December 31, 2020, 2019 and 2018, HGV had default rates of 6.6%, 6.3%, 5.1% and 4.7%, respectively.

Diamond Overview

Diamond Resorts International, Inc. and its subsidiaries, including Diamond Resorts Corporation, are a global leader in the hospitality industry and the largest, independent-branded vacation ownership company that markets and sells vacation ownership interests, manages resorts and multi-resort trusts (the “Diamond Collections”) in key vacation destinations, and operates points-based vacation clubs. Diamond’s portfolio consists of 110 properties it manages, or included in one of its Diamond Collections, representing approximately 14,198 units. In addition, Diamond’s global resort network includes 229 affiliated resorts and hotels (which Diamond does not manage and do not carry its brand, but are a part of Diamond’s exchange network). Through its innovative and extensive distribution network, Diamond sells a points-based VOI product, which allows its owners to travel to 339 vacation destinations located in 34 countries throughout the world, including key leisure destinations such as Orlando, Las Vegas, the Hawaiian Islands, Mexico, and Europe.

We believe Diamond is unique within the vacation ownership industry in its infusion of hospitality and experiences through the full life cycle of an owner or member’s relationship with Diamond and its properties. Diamond’s marketing has increasingly emphasized unique experiences to generate new customers and repeat business through Diamond’s innovative Events of a Lifetime, Diamond Resorts Concert Series, Diamond Dream Holidays, and related programs. These drive high quality leads to its hospitality focused sales processes.

3

Hospitality and unique experiences are offered during property stays, and Diamond continuously creates new and attractive offerings both pre- and post-stay for its members. Existing members are also offered additional unique experiences and the opportunity to enhance and upgrade their memberships. In this way Diamond is able to realize substantial lifetime value both from and for its members – often significantly in excess of their initial purchases.

Diamond’s flexible VOI product allows customers to purchase a lifetime of experiences. Diamond’s members receive an annual or biennial allotment of points and, depending on the number of points purchased, can use these points to stay at destinations within Diamond’s network of resort properties while maintaining flexibility relating to the location, season and duration of their vacation. Diamond’s points-based product also allows its owners to redeem their annual points for numerous alternative experiential vacation options, such as cruises or guided tours. Diamond seeks to continuously improve its value proposition to its existing owners or new customers by enhancing its product offerings, expanding the geographic diversity of its resort network, and providing best-in-class customer service.

Diamond’s operations consist of two interrelated businesses: (i) Vacation interests sales and financing, which includes the marketing and sale of VOIs and consumer financing for purchasers of VOIs; and (ii) hospitality and management services, which includes management of resort properties and trusts, operation of the Diamond Clubs and resort amenities, and the provision of other hospitality and management services.

In the twelve months ended March 31, 2021 and the years ended December 31, 2020, 2019 and 2018, Diamond had approximately 93,000, 111,000, 280,000 and 269,000 tours, respectively. In the twelve months ended March 31, 2021 and the years ended December 31, 2020, 2019 and 2018, Diamond had approximately 383,000, 386,000, 399,000 and 413,000 owners, respectively. In the twelve months ended March 31, 2021 and the years ended December 31, 2020, 2019 and 2018, Diamond had VPG of approximately $4,687, $4,266, $3,331 and $3,162, respectively. In the twelve months ended March 31, 2021 and the years ended December 31, 2020, 2019 and 2018, Diamond had default rates of 16.0%, 22.1%, 18.0% and 17.6%, respectively.

Combined Company Business Segment Overview

We will operate the pro forma combined company business across two segments:

Real Estate Sales & Financing. Within this segment, we will:

| • | Market and sell fee-simple VOIs developed both by us or by third parties, and source VOIs through fee-for-service agreements with third-party developers. We will also sell points-based VOI, permitting members to maintain flexibility. |

| • | Provide consumer financing, which includes interest income generated from the origination of consumer loans to customers to finance their purchase of VOIs and revenue from servicing the loans. |

Resort Operations & Club Management. Within this segment, we will:

| • | Earn revenues from Club activation fees, annual dues and transaction fees from member exchanges. |

| • | Provide day-to-day management services, including housekeeping services, maintenance and certain accounting and administrative services for HOAs, for which we receive recurring management fees. |

| • | Rent unsold VOI inventory, third-party inventory and inventory made available due to ownership exchanges through Club programs. |

4

TRANSACTION OVERVIEW

On March 10, 2021, we announced the pending acquisition of Dakota Holdings, Inc. (“Diamond”), a Delaware corporation that is controlled by investment funds and vehicles managed by affiliates of Apollo Global Management Inc. (“Apollo”). Pursuant to an Agreement and Plan of Merger, dated as of March 10, 2021 (the “Merger Agreement”), by and among HGV Parent, the Issuer, Diamond, and certain stockholders of Diamond. Pursuant to the Merger Agreement, subject to customary closing conditions, Diamond, which indirectly owns all of the interests in Diamond Resorts International, Inc., will merge with and into the Issuer (the “Merger”) with the Issuer continuing as the surviving entity after the Merger and Apollo will receive common stock in HGV Parent equal to approximately 28% of HGV Parent’s outstanding common stock after giving effect to such transaction, subject to adjustments under the Merger Agreement (we refer to the transactions described in this sentence collectively as the “Acquisition”). In connection with the Acquisition, HGV’s Board of Directors will be expanded from 7 to 9 members, and Apollo will have the right to appoint two directors as long as their equity ownership remains at or above 15% of the outstanding stock at closing and one director as long as their equity ownership remains at or above 10% of the outstanding stock at closing.

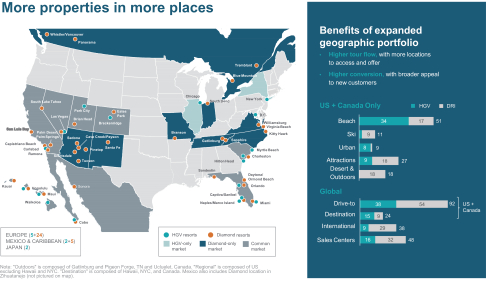

The Acquisition will combine the strength of HGV’s brand and culture with Diamond, the largest independent timeshare operator. Diamond’s 92 leisure resorts and nearly 400,000 owners uniquely complement HGV’s 62 upscale and luxury properties and nearly 330,000 owners. We believe the combination will create the premier vacation ownership company with a broad chain scale offering, encompassing 154 resort properties, 48 sales centers and over 720,000 owners. The Acquisition will expand and diversify our resort portfolio into over 20 new markets, adding additional drive-to destinations & sales centers while enhancing alignment with the Hilton network to widen customer reach.

We intend to use the net proceeds of this offering, together with cash on hand and the borrowing of $1,300 million under our Term Loan Facility (as defined below), to refinance certain of our and Diamond’s outstanding indebtedness in connection with the Acquisition. In this offering memorandum, we refer to the Acquisition, the entry into and borrowings under the Term Loan Facility, the amendment of our Revolving Credit Facility (as defined below) and the offering of notes contemplated hereby and the use of proceeds from the Term Loan Facility and the issuance of the Notes, together with the payment of fees and expenses in connection therewith, collectively, as the “Transactions.” See “—Transactions.”

On a pro forma combined basis after giving effect to the Transactions, our net loss for the twelve months ended March 31, 2021 would have been $(346) million and our Pro Forma Adjusted EBITDA would have been $433 million. For an explanation of how we calculate Pro Forma Adjusted EBITDA, see “—Summary Pro Forma Financial Information.”

5

STRATEGIC RATIONALE

We believe the Acquisition of Diamond presents a transformational opportunity for our Company and positions us to capitalize on anticipated leisure travel recovery. The Acquisition is expected to provide the following strategic benefits:

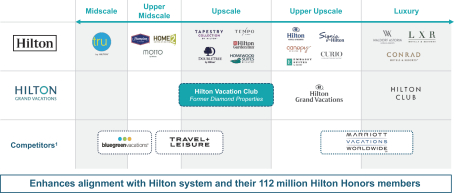

Enables significant value creation from scale. The combination of HGV and Diamond will create the largest independent timeshare company with HGV’s strong brand and culture, creating the premier vacation ownership company with a broad chain scale offering. The Acquisition will expand and diversify HGV’s resort portfolio into over 20 new markets and the combined company will have over 720,000 owners, 154 resorts and 48 sales centers.

Diversifies HGV’s portfolio. The Acquisition of Diamond doubles the number of vacation options for the combined owner base and adds additional drive-to destinations and allows HGV to leverage the Hilton network to widen customer reach. Diamond’s complementary footprint will bolster HGV’s strong network of beach, attraction-based, and urban markets, while adding new regional drive-to destinations in outdoor, desert and ski locations. The combined company will offer a broader range of pricing and product options which will widen our customer reach, enhancing alignment with the 112 million Hilton Honors members.

Broad chain scale offering

| 1) | Illustrative chain scale positioning. |

6

Accelerates launch of HGV-branded trust product offering. We expect to rebrand Diamond’s properties over time to drive revenue growth in a new customer segment. Combining HGV’s points-based deeded product with Diamond’s points-based trust structure will allow the combined company to cater to a wider audience, attract more new buyers and drive incremental growth in a capital-efficient manner. HGV’s deeded product provides premium pricing, inventory sourcing flexibility, and the ability to pre-sell projects to support strong project-level cash flow, while giving buyers and owners the value of guaranteed availability. We believe the introduction of a trust product will allow for lower barriers to ownership, reduced inventory delivery volatility and inventory recycling, enabling smoother sales and upgrades while providing buyers and owners network and pricing flexibility. We expect to integrate Diamond’s innovative Events of a Lifetime experiential sales and marketing platform that drives strong engagement and Volume Per Guest (“VPG”) premiums with HGV’s owner base.

Significant potential cost savings. We expect the Acquisition will result in approximately $125 million in potential annual run-rate cost savings by 24 months following consummation of the Acquisition. We also anticipate generating significant future revenue savings opportunities.

Compelling financial benefits. We believe the Acquisition will increase our recurring EBITDA streams and drive overall cash flow. We believe the combined company will generate strong steady-state adjusted free cash flow conversion of approximately 50-60%, driven by the realization of cost savings, significant inventory pipeline, acquired inventory and reduced long-term inventory spending. We believe the addition of new owners embeds additional value for the company over the life of their ownership. It is expected that Segment Adjusted EBITDA from recurring sources, including Club membership fees, property management fees and financing fees, will increase following the Acquisition, as compared to HGV on a standalone basis.

Compelling valuation and deal structure facilitate financial flexibility and deleveraging. Significant cash flow generation is expected to allow for deleveraging. After giving effect to the Transactions, on a pro forma basis as of March 31, 2021, our liquidity would have been approximately $976 million, comprised of $260 million in cash and cash equivalents and $456 million of borrowing capacity under our Revolving Credit Facility (after giving effect to approximately $1 million of outstanding letters of credit), as well as nearly $300 million of receivables eligible for securitization and the opportunity for capital market efficiencies from the increased scale of the combined company’s ABS platform.

7

VACATION OWNERSHIP INDUSTRY OVERVIEW

The vacation ownership industry enables customers to share ownership and use of fully furnished vacation accommodations. Typically, a purchaser acquires an interest (known as a “vacation ownership interest” or a “VOI”) that is either a real estate ownership interest (known as a “timeshare estate”) or a contractual right-to-use interest (known as a “timeshare license”) in a single resort or a collection of resort properties. In the United States, most vacation ownership products are sold as timeshare estates, which can be structured in a variety of ways, including, but not limited to, a deeded real estate interest in a specified accommodation unit, an undivided interest in a building or an entire resort, or a beneficial interest in a trust that owns one or more resort properties. For many purchasers, vacation ownership provides an attractive alternative to traditional lodging accommodations (such as hotels, resorts and condominium rentals). In addition to avoiding the volatility in room rates to which traditional lodging customers are subject, vacation ownership purchasers also enjoy accommodations that typically offer more spacious floor plans and residential features, such as living rooms, multiple bedrooms, in-unit washers and dryers, and fully equipped kitchens and dining areas. The weighted average timeshare unit size in North America in 2020 was approximately 1,030 square feet, and 61% of units had at least 2 bedrooms. Compared to traditional second-home ownership, the key advantages of vacation ownership products typically include a lower up-front acquisition cost and annual maintenance expenses, resort-style amenities such as swimming pools or fitness facilities, and the infrastructure to exchange annual usage rights to facilitate vacationing at different destinations.

The timeshare industry is one of the fastest growing segments of the global travel and tourism sector. VOI sales have grown 775% over the last 30 years, representing a compound annual growth rate of 7%, with approximately 9.9 million U.S. households owning one or more types of a VOI product at the end of 2019. We believe this growth has been driven by product innovation, geographic expansion, greater consumer awareness of the value proposition of vacation ownership, and the entrance of globally recognized lodging and entertainment companies into the vacation ownership industry. At inception, timeshare products were largely limited to a fixed or floating week, whereby a customer would purchase rights to use the same property each year, typically at the same time each year. The industry has since evolved to better meet consumer demands, offering more flexible products, such as membership in multi-property networks or clubs. Additionally, product locations have expanded beyond traditional resort markets to include urban and international destinations.

Positive macroeconomic trends including increased discretionary income, improving consumer confidence and increased leisure spending, have also fueled the industry’s growth. Total VOI sales in 2019 totaled $10.5 billion, approximating sales levels in 2007, demonstrating the continued opportunity for VOI sales growth.

The COVID-19 pandemic that started in early 2020 significantly negatively impacted the hospitality, travel and leisure industries due to various mandates and orders to close non-essential businesses, impose travel restrictions, require “stay-at-home” and/or self-quarantine, and require similar actions. Such restrictions and directives have resulted in cancellations and significant reductions in travel around the world and caused various other negative global economic conditions. With the anticipated continuation of the pandemic receding, as well as COVID-19 vaccinations becoming more widespread, such mandates and orders have continued to ease, resulting in consumer confidence increasing to resume normal activities, including travel and leisure, and more businesses to continue to resume operations. While we hope that conditions in the hospitality and travel industries continue to improve, there remains significant uncertainty as to the degree of continuing impact and duration of the conditions stemming from the ongoing pandemic on the timeshare industry. See “Risk Factors—Risks Related to Our Business and Industry—The COVID-19 pandemic and related events, including the various measures implemented or adopted to respond to the pandemic and the global economic downturn, have had, and will likely continue to have, a material adverse effect on our business, financial condition and results of operations for the foreseeable future.”

8

COMPETITIVE STRENGTHS OF THE PRO FORMA BUSINESS

Industry Leading Diverse Portfolio and Owner Network. The Acquisition will combine the largest independent timeshare company with HGV’s strong brand and culture, creating the premier vacation ownership company with a broad chain scale offering. HGV offers world-class hospitality with the strength of the trusted Hilton brand, with 62 upper upscale and luxury properties in premier resort destinations as well as a proven track record of net owner growth (“NOG”) and industry-leading VPG and margins. As the largest timeshare operator with no hotel brand affiliation, Diamond has an extensive network of 92 leisure resorts across the globe, with strong regional drive-to market exposure and complementary upscale range. The Acquisition will double the number of vacation options for the combined owner base and Diamond’s complementary footprint will bolster HGV’s strong network of beach, attraction-based, and urban markets, while adding new regional drive-to destinations in outdoor, desert and ski locations. The combined company will have over 720,000 owners, 154 resorts and 48 sales centers.

In addition to more properties in more places, combining HGV’s deeded product with Diamond’s points-based trust structure will allow the combined company to cater to a wider audience, attract more new buyers and drive incremental growth in a capital-efficient manner. HGV’s deeded product provides premium pricing, inventory sourcing flexibility, and the ability to pre-sell projects to support strong project-level cash flow, while giving buyers and owners the value of guaranteed availability. We believe the introduction of a trust product allows for lower barriers to ownership, reduced inventory delivery volatility and inventory recycling, enabling smoother sales and upgrades while providing buyers and owners network and pricing flexibility.

The combined company will also integrate Diamond’s innovative Events of a Lifetime experiential sales and marketing platform that drives strong engagement and VPG premiums with HGV’s owner base.

Diversified Earnings Profile. The combined company will have a diversified earnings profile with increased contribution from recurring and fee-based earnings. NOG generates several high margin, recurring revenue streams, including Club membership fees, property management fees and financing fees. New buyers and owner upgrades further grow these fee streams and create a multiplier effect. Despite COVID-19, owner upgrade sales continue to be a durable and predictable source of earnings. It is expected that Segment Adjusted EBITDA from recurring sources, including Club membership fees, property management fees and financing fees, will increase following the Acquisition, as compared to HGV on a standalone basis.

9

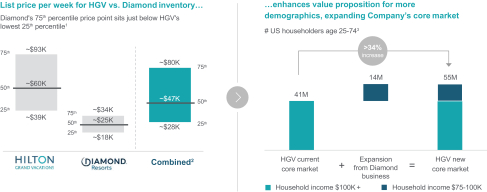

Broadened Addressable Market. The combined company will offer a broader range of pricing and product options, widening customer reach and enhancing alignment with the 112 million Hilton Honors members. Diamond’s 75th percentile price point of $34 thousand per week sits just below HGV’s 25th percentile price point of $39 thousand per week. We believe the wider range of available price points will enhance the value proposition for more demographics, expanding the combined company’s core market by approximately 34% as compared to HGV’s core market on a standalone basis, from approximately 41 million U.S. householders between the ages of 25 and 74 to 55 million, at a broader range of household income levels. Moreover, we believe the addition of Diamond’s points-based trust structure will cater to a wider audience, attract more new buyers by lowering barriers to ownership, while providing buyers and owners network and pricing flexibility.

| 1) | Figures unweighted by room type. |

| 2) | Represents the list prices for one week of vacation ownership for the 25th, 50th, and 75th percentiles of the pro forma combined portfolio. |

| 3) | Selected Characteristics of Households by Total Money Income in 2019. US Census Bureau, Current Population Survey, 2020 ASEC Supplement. |

Significant Potential Cost Savings from Strategic Combination. We believe the Acquisition is expected to unlock significant potential revenue and cost savings. We believe that more products (including the addition of a branded trust product, expanded chain scale, broader price coverage and more experiential offerings), more places (through the expansion of our regional network, high NOG and additional HGV owner sales) and more owners (through the activation of the Diamond owner base by the HGV brand, complimented by the activation of the HGV owner base by Diamond’s experiential platform) provide significant opportunities for revenue lift with respect to both new buyers and existing owners of both HGV and Diamond, as well as Diamond rental performance. In addition, we believe the Acquisition will result in approximately $125 million in potential annual run-rate cost savings from general and administrative, operational and financial efficiencies by 24 months following the consummation of the Acquisition. We also expect to realize incremental standalone cost reductions in HGV’s business.

Attractive Free Cash Flow Profile. The Acquisition is expected to increase recurring EBITDA streams and drive overall cash flow. We believe the combined company will generate strong steady-state adjusted free cash flow conversion of approximately 50-60%, driven by realization of cost savings, significant inventory pipeline, acquired inventory and reduced long-term inventory spending. Adding new owners has the potential to embed additional value for the combined company over the life of their ownership.

Strong and Flexible Balance Sheet. The Acquisition is expected to result in a strong and flexible balance sheet to support the business. After giving effect to the Transactions, on a pro forma basis as of March 31, 2021, our liquidity would have been approximately $976 million, comprised of approximately $260 million in cash and cash equivalents and $456 million of borrowing capacity under our Revolving Credit Facility (after giving effect to approximately $1 million of outstanding letters of credit), as well as nearly $300 million of receivables eligible

10

for securitization and the opportunity for capital market efficiencies from the increased scale of the combined company’s ABS platform. We believe the combined business has the potential to generate significant cash flow generation is expected to allow for rapid deleveraging.

Experienced Management Team. Our experienced management team is headed by Mark D. Wang, our President and Chief Executive Officer, who has led Hilton’s global timeshare operations since 2008. Mr. Wang has over 35 years of experience in the timeshare industry. With this experience, our management team has created a lean and nimble organizational structure, which allows us to respond quickly and effectively to opportunities and dynamic market conditions. By fostering a culture with a strong focus on execution and operational effectiveness, management empowers our employees to respond to our members’ and guests’ needs and provide each of them with a unique and memorable experience.

STRATEGIES OF THE COMBINED BUSINESS

Following the closing of the Acquisition, we plan to execute on the following strategies:

Grow Vacation Sales. The combined company plans to continue growing contract sales by pursuing a balanced mix of sales to new and existing members. We expect to drive growth by enhancing the value of Club membership and expanding HGV’s highly effective sales distribution model, leveraging the complementary activation of the Diamond owner base by the HGV brand and activation of the HGV owner base by Diamond’s experiential platform, as well as tapping into Diamond’s four years of excess developed inventory available for sale. We believe HGV is well-positioned despite COVID-19 disruptions, due to factors including properties conducive to social distancing, low observed price elasticity, limited exposure to volatility in asset values, limited maintenance capital expenditures, minimal focus on rental income and dedicated focus on leisure travelers. As a result, we believe the combined company is well-positioned to capitalize on anticipated leisure travel recovery.

Grow Our Member Base. The combined company will continue to use HGV’s relationship with Hilton to target new, brand-loyal members, as well as leveraging a wider range of price points and product offerings to expand the demographics of our member base. Net owner growth supports strong future sales growth, as a significant portion of our member base buys additional VOI products, which expands our predictable, recurring fee-based resort and Club management business.

Continue to Enhance Member Experiences. We are continuously seeking new ways to add value to our Club membership, including expanding our vacation options and destinations, in-market and travel-related discounts, travel exchange partners and providing access to a growing network of new Hilton-branded hotels and resorts. The combined company will continue to build off of its expanded and diversified resort portfolio, and will integrate Diamond’s innovative Events of a Lifetime experiential sales and marketing platform. Our employees also are an important part of the vacation experiences of our members and will continue to enhance these experiences by providing HGV’s signature high-quality customer service. We believe the dedicated service of our employees, vacation experiences and Club value we offer our members foster loyalty and generate significant repeat business through our most cost-effective marketing channel.

Optimize Our Sales Mix of Capital-efficient Inventory. We believe that optimizing the combined company’s mix of capital-efficient and owned inventory sales will drive premium top line growth, cash flow generation and returns on invested capital. We also intend to take advantage of the combined company’s robust deal pipeline fueled by existing and new relationships with third-party developers for a full range of fee-for-service and just-in-time projects. We plan to maintain a disciplined approach to capital allocation, while strategically pursuing acquisitions and development of owned inventory in key markets.

11

Pursue Opportunistic Business Ventures. Despite recent consolidation, the timeshare industry remains fragmented. We will continue to evaluate market opportunities and consider additional strategic acquisitions in the future that meet our high product and service standards. This could include corporate and property acquisitions to expand our inventory options and distribution capabilities. We also intend to use our relationship with Hilton and third-party developers as well as our innovative platform and industry experience to create new products and additional efficiencies.

RECENT EVENTS RELATED TO THE COVID-19 PANDEMIC AND IMPACT ON OUR BUSINESS

In March 2020, a National Public Health Emergency was declared in response to the coronavirus, known as COVID-19. As a result, many local, county and state government officials have issued, and continue to issue or reinstate, various mandates and orders to close non-essential businesses, impose travel restrictions, and require “stay-at-home” and/or self-quarantine in certain cases, all in an effort to protect the health and safety of individuals and aimed at slowing and ultimately stopping the spread and transmission of the virus. Accordingly, commencing in March 2020, we and Diamond started to temporarily close substantially all properties and suspended U.S. sales operations and closed such sales offices. In the second quarter of 2020, we and Diamond each began a phased reopening of resorts and resumption of our business activities, but under new operating guidelines and with safety measures. With the anticipated gradual receding of the pandemic, as well as COVID-19 vaccinations becoming more widespread and various restrictions continuing to ease, consumers have started to resume normal activities, including travel and leisure, and more businesses have commenced resuming operations. We plan to continue to reopen our resorts and resume our normal business as conditions permit, but there can be no assurance that such positive trends will continue or that there will not be any increases of new infections or new variants that may impede or reverse recovery and such positive trends.

In response to the impact of the COVID-19 pandemic, we took a variety of actions to ensure the continuity of our business and operations and to secure our liquidity position to provide financial flexibility. These actions include amending certain financial covenant ratios through the third quarter of 2021, as may be needed due to the ongoing and uncertain future impact of the COVID-19 pandemic on our business and operations.

The temporary closure of resorts and sales centers, and the related suspensions of operations, as well as various travel and other restrictions, expectedly have had a materially adverse impact on our and Diamond’s revenues, net (loss) income and other operating results during the first quarter, as well as our and Diamond’s business and operations generally, as more fully discussed elsewhere in this offering memorandum and in the documents incorporated by reference herein. As discussed in further detail in the “Management’s Discussion and Analysis and Results of Operations” sections herein, substantially all of the unfavorable changes in our and Diamond’s operating results during the year ended December 31, 2020 and the quarter ended March 31, 2021 as compared to prior periods were a result of the ongoing impact of the COVID-19 pandemic on travel demand.

The COVID-19 pandemic has created an unprecedented and challenging time. Our current focus is on continuing to position the Company to be in a sound position from an operational, liquidity, credit access, and compliance perspective for a strong recovery when the impact of COVID-19 subsides. We have taken several steps to enhance our liquidity and provide financial flexibility. We will continue to assess the evolving COVID-19 pandemic, including the various restrictions on travel, leisure and other activities, and general business operations, and will take additional actions as appropriate.

As of March 31, 2021, approximately 80 percent of our resorts and nearly all of our sales centers are open and currently operating. However, some of our resorts and sales centers are operating in markets with capacity constraints and various safety measures, which are impacting consumer demand for resorts in those markets. Prior to reopening our resorts and sales centers, we introduced the HGV Enhanced Care Guidelines, designed to

12

provide owners, guests and team members with the highest level of cleaning protocols and safety standards recommended by the Center for Disease Control and Prevention and cleaning solutions approved by the Environmental Protection Agency in response to the COVID-19 pandemic. Since late May 2020, Diamond has re-opened the majority of its North American portfolio properties and onsite sales centers, albeit at reduced capacity levels and revenue has not returned to pre-COVID-19 levels. Diamond implemented and trained team members on the “Diamond Standard of Clean.”

While we plan to continue to reopen our resorts and resume our business as conditions and applicable rules and regulations permit, the pandemic continues to be unprecedented and rapidly changing, and has unknown duration and severity. Further, despite the recent receding of travel and other restrictions in regions and locations where we have a significant concentration of our properties and units and other positive trends with the pandemic, the pandemic continues to adversely impact consumer demand for our resorts in those areas and our business in general. Moreover, there can be no assurance those positive trends will continue.

Accordingly, there remains significant uncertainty as to the continuing degree of impact and duration of the conditions stemming from the ongoing pandemic on our and Diamond’s revenues, net income and other operating results, as well as our and Diamond’s business and operations generally.

TRANSACTIONS

The Acquisition

On March 10, 2021, the Issuer entered into the Merger Agreement with HGV Parent, Diamond, which indirectly owns all of the interests in Diamond Resorts International, Inc., and certain stockholders of Diamond. The Merger Agreement provides that we will acquire Diamond in a series of transactions. After the completion of the Acquisition, Diamond will cease to exist as a separate company and all of its assets and liabilities will be assumed by the Issuer, the surviving entity of the Merger, and the Issuer will continue to be a wholly-owned subsidiary of HGV Parent.

Upon consummation of the Acquisition, the Diamond stockholders are currently expected to receive an aggregate of approximately 34,630,532 shares (based on calculations as of May 13, 2021) of our common stock, par value $0.01 per share, or approximately 28% of our outstanding shares immediately following consummation of the Acquisition, subject to certain adjustments as a result of changes in certain liabilities and other items between signing and closing.

Each party’s obligation to consummate the Acquisition is subject to various customary closing conditions set forth in the Merger Agreement, including, (i) the accuracy of the representations and warranties of the other party contained in the Merger Agreement, subject to certain qualifications; (ii) the other party having performed in all material respects all obligations required to be performed by it under the Merger Agreement; (iii) the absence of a “material adverse effect” impacting the other party; (iv) the approval of the stock issuance proposal by the affirmative vote of a majority of the votes cast by holders of our common stock at a stockholders’ meeting duly called and held for such purpose; (v) the absence of any judgment, order, law or other legal restraint by a court or other governmental entity of competent jurisdiction that prevents the consummation of the Acquisition; (vi) the approval for listing by the New York Stock Exchange (“NYSE”) of the shares of our common stock issuable in the Acquisition; (vii) the termination or expiration of any applicable waiting period under the Hart-Scott-Rodino Antitrust Improvements Act (“HSR Act”); (viii) the receipt of all authorizations, consents, orders or approvals of, or declarations or filings with, or expirations of waiting periods imposed by, the Federal Economic Competition Commission (“COFECE”) under the Mexican Federal Economic Competition Law and the Federal Competition Authority under the Austrian Cartel Act and the Competition Act; (ix) certain ancillary agreements having been delivered and not having been rescinded or repudiated by certain parties; and (x) the

13

absence of defaults under Diamond’s Existing Unsecured Notes and absence of defaults and sufficient availability under Diamond’s warehouse facilities. We cannot assure you that the various closing conditions will be satisfied. We and our board of directors were named as defendants in lawsuits brought by alleged HGV stockholders challenging the adequacy of public disclosures related to the Acquisition and seeking, among other things, injunctive relief to enjoin us from completing the Acquisition. See “Risk Factors — Risks Related to the Acquisition” and “Business — Legal Proceedings” for more information.

The Merger Agreement contains certain termination rights for the parties thereto, including the right of each party to terminate the agreement if the Acquisition has not been consummated by September 10, 2021, subject to extension to December 9, 2021 under certain circumstances.

This offering is not conditioned upon the closing of the Acquisition. If the Acquisition is not consummated simultaneously with this offering, the gross proceeds of this offering will be funded into escrow and, upon release of the funds from escrow, the proceeds from this offering will be used to fund a portion of the Transactions as set forth below or, if applicable, will be used to fund the Special Mandatory Redemption as described herein. See “— Escrow.”

Financing Transactions

In connection with the consummation of the Acquisition, we have entered into or intend to enter into the following financing transactions:

| • | the borrowing of $1,300 million under a seven-year senior secured term loan facility (the “Term Loan Facility”); |

| • | an amendment to our revolving credit facility to permit the Transactions (the “Revolving Credit Facility”), which Revolving Credit Facility provides for aggregate borrowing capacity of $800 million; and |

| • | the issuance of $675 million aggregate principal amount of notes offered hereby. |

The proceeds from the Term Loan Facility and the notes offered hereby, together with cash on hand, will be used to (i) repay in full all $300 million of the Issuer’s outstanding 6.125% Senior Notes due 2024 (the “Existing HGV Notes”), whether through redemption or a tender offer, (ii) repay in full all outstanding indebtedness under Diamond’s existing senior secured credit facilities (the “Existing Diamond Credit Facilities”), (iii) repay in full all $500 million of Diamond’s outstanding 7.750% First-Priority Senior Secured Notes due 2023 (the “Existing Diamond Secured Notes”), whether through redemption or a tender offer, (iv) repay in full all outstanding indebtedness under our existing term loan (the “Existing HGV Term Loan”), (v) repay $316 million of outstanding indebtedness under our Revolving Credit Facility and (vi) pay related fees, costs, premiums and expenses in connection with these transactions. In connection with the Transactions, the Issuer will assume $617 million of Diamond’s outstanding indebtedness, including all obligations under Diamond’s $591 million outstanding aggregate principal amount of 10.750% Senior Notes due 2024 (the “Existing Diamond Unsecured Notes”) and $26 million in other Diamond indebtedness. Subject to market conditions and other factors, we may look to refinance the Existing Diamond Unsecured Notes in the near future with one or more notes offerings or other indebtedness. This offering memorandum does not constitute a notice of redemption or an offer to repurchase any existing securities of either HGV, the Issuers or Diamond.

See “Use of Proceeds” and “Description of Certain Other Indebtedness” for more information.

Hilton License Agreement Amendment

In connection with the Merger Agreement, HGV entered into an Amended and Restated License Agreement with Hilton on March 10, 2021 (the “A&R Hilton License Agreement”), which amends and restates in its entirety

14

the License Agreement, dated as of January 2, 2017, between HGV and Hilton (the “Original License Agreement”), and amended another related agreement (together with the A&R Hilton License Agreement, the “Hilton Agreements”). The A&R Hilton License Agreement amends the Original License Agreement to allow HGV to integrate the properties, assets and business of Diamond into its business subsequent to the Merger (the “Integration”), including:

| • | gradual ramp-up of royalty fee structure over the initial five (5) years following the closing of the Merger with respect to— |

| • | sales of interests or rights to use in a new exchange club or program (“New Club”) to be developed by HGV after the Merger as part of the Integration that may cover both HGV’s current properties and Diamond properties that will convert into HGV brand properties (“New Brand Properties”); and |

| • | various property-level revenues associated with New Brand Properties, such as transient rental revenues, and certain management fees; |

| • | extension of the Initial Noncompetition Term (as defined in the A&R Hilton License Agreement) by five (5) years to December 31, 2051; |

| • | amendment of certain provisions related to the parties’ obligations with respect to Hilton’s current co-branded credit card program; and |

| • | modification to certain marketing rights, marketing channel rights, and lead generation, hotel rate discount, employee participation in certain Hilton programs, and New Brand Properties and New Club branding and licensed mark provisions. |

In addition, as required by the Original License Agreement, HGV has obtained the consent of Hilton to HGV entering into the Merger Agreement and completing the Merger.

Escrow

If the Acquisition is not consummated simultaneously with this offering, concurrently with the closing of this offering, the Escrow Issuers will enter into an escrow agreement relating to the notes (the “Escrow Agreement”) with Wilmington Trust, National Association, as trustee for the notes and as escrow agent (in such capacity, the “Escrow Agent”), pursuant to which the Escrow Issuers will deposit (or cause to be deposited) an amount equal to the gross proceeds of the notes offered hereby into a segregated escrow account for the notes until the Escrow Release Conditions are satisfied. The property in the escrow account will be pledged as security for the benefit of the trustee and the holders of the notes. If, among other things, the Acquisition is not consummated on or prior to the by the Escrow End Date, the Escrow Issuers will redeem, on the Special Mandatory Redemption Date in accordance with the terms of the indenture that will govern the notes, all of the notes at the Special Mandatory Redemption Price.

Sources and Uses of Funds

The table below sets forth the estimated sources and uses of funds in connection with the Transactions (and after the gross proceeds from this offering are released from escrow, if applicable), assuming they occurred on March 31, 2021 and based on estimated amounts outstanding on that date. Actual amounts will vary from the estimated amounts shown below depending on several factors, including, among others, the amount of cash and cash equivalents balances, net working capital and any purchase price adjustments, indebtedness (including accrued interest on such indebtedness), in each case, of HGV or Diamond, changes made to the sources of the contemplated financings, the number of shares of capital stock and equity awards outstanding on the closing date of the Acquisition and differences from our estimated fees and expenses.

15

If the Acquisition is not consummated simultaneously with this offering, the gross proceeds of this offering will be funded into escrow and, upon release of the funds from escrow, the proceeds from this offering will be used to fund a portion of the Transactions as set forth below or, if applicable, will be used to fund the Special Mandatory Redemption as described herein. See “— Escrow.”

You should read the following together with the information included under the headings “— The Transactions,” “Capitalization” and “Unaudited Pro Forma Condensed Combined Financial Information of HGV and Diamond” included elsewhere in this offering memorandum.

| (in millions) |

(in millions) |

|||||||||

| Sources |

Amount | Uses |

Amount | |||||||

| Repayment of existing net debt: |

||||||||||

| Term Loan Facility(1) |

$ | 1,300 | Revolving Credit Facility(5) |

$ | 316 | |||||

| Notes offered hereby(2) |

675 | Existing Diamond Credit Facilities(6) |

863 | |||||||

| Diamond Debt Assumed(3) |

617 | Existing Diamond Secured Notes(6) |

500 | |||||||

| Cash on hand |

304 | Existing HGV Notes(6) |

300 | |||||||

| Equity issued to Diamond(4) |

1,392 | Existing HGV Term Loan(6) |

175 | |||||||

|

|

|

|||||||||

| Total sources |

$ | 4,288 | Diamond Debt Assumed(3) |

617 | ||||||

|

|

|

|||||||||

| Purchase of Diamond equity(4) |

1,392 | |||||||||

| Fees, costs and expenses(7) |

125 | |||||||||

|

|

|

|||||||||

| Total uses |

$ | 4,288 | ||||||||

|

|

|

|||||||||

| (1) | Represents the aggregate principal amount of the Term Loan Facility without giving effect to discounts or fees to be paid to the lenders. |

| (2) | Represents the aggregate principal amount of the notes offered hereby and does not reflect the initial purchasers’ discount or fees or any issue discount. |

| (3) | Includes $591 million outstanding principal amount of Existing Diamond Unsecured Notes and $26 million of other Diamond indebtedness consisting of notes payable including in connection with insurance policies. Excludes non-recourse, securitized timeshare debt of $611 million. |

| (4) | Assumes issuance of 34.5 million HGV common shares at $40.32 per share. |

| (5) | Our Revolving Credit Facility provides for $800 million of borrowing capacity, subject to customary borrowing conditions. As of March 31, 2021, we had $660 million outstanding under our Revolving Credit Facility (excluding $1 million of issued and undrawn letters of credit that we expect to be outstanding on the closing date of the Acquisition). In connection with the Transactions, we expect to repay $316 million of borrowings so that we have $344 million of borrowings outstanding following closing of the Transactions (after giving effect to $1 million of issued and undrawn letters of credit that we expect to be outstanding on the closing date of the Acquisition). |

| (6) | Excluding any prepayment premiums and accrued and unpaid interest. |

| (7) | Represents estimated fees, costs and expenses associated with the Transactions, including, without limitation, certain amounts payable under the Merger Agreement and any fees and expenses incurred in connection therewith, prepayment premiums on indebtedness being repaid, original issue discount on the Term Loan Facility, initial purchaser discounts and commissions, underwriting, placement and other financing fees, advisory fees, and other transactional costs and legal, accounting and other professional fees and expenses. |

16

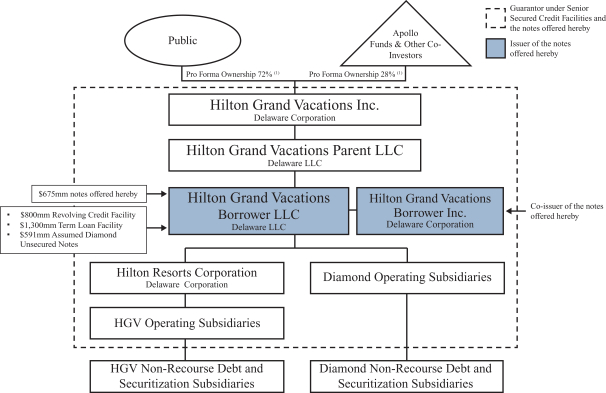

Organizational Structure

The following diagram illustrates our simplified organizational structure after giving effect to this offering and the Transactions. This diagram is provided for illustrative purposes only and does not show all legal entities or obligations of such entities:

| (1) | Subject to adjustments under the Merger Agreement |

Corporate Information

Hilton Grand Vacations Inc., a Delaware corporation, was incorporated under the laws of the state of Delaware on May 2, 2016. Hilton Grand Vacations Borrower LLC, a Delaware limited liability company, was formed under the laws of the state of Delaware on May 2, 2016. Hilton Grand Vacations Borrower Inc., a Delaware corporation, was formed under the laws of the state of Delaware on October 4, 2016. On January 3, 2017, Hilton completed a tax-free Spin-Off of HGV and Park Hotels & Resorts Inc. As a result of the Spin-Off, HGV became an independent publicly-traded company. Our principal executive office is located at 5323 Millenia Lakes Boulevard, Suite 120, Orlando, Florida, and our telephone number at that address is (407) 613-3100.

17

Unaudited Pro Forma Condensed Combined Financial Information Of HGV And Diamond

On March 10, 2021, HGV Parent, the Issuer, Diamond and certain stockholders of Diamond entered into the Merger Agreement, pursuant to which HGV will combine with Diamond through a series of business combinations. Following the Merger, Diamond will be an indirect, wholly-owned subsidiary of HGV.

The unaudited pro forma condensed combined financial information includes the unaudited pro forma condensed combined statement of operations and the unaudited pro forma condensed combined balance sheet. The unaudited pro forma condensed combined statement of operations of HGV and Diamond for the year ended December 31, 2020, three months ended March 31, 2021 and 2020 and the twelve months ended March 31, 2021 combine the historical consolidated statements of operations of HGV and Diamond, giving effect to the Transactions as if they had been completed on January 1, 2020. The unaudited pro forma condensed combined balance sheet as of March 31, 2021, combines the historical consolidated balance sheets of HGV and Diamond, giving effect to the Transactions as if they had been completed on March 31, 2021.

The historical consolidated financial statements of Diamond have been adjusted to reflect certain reclassifications in order to align financial statement presentation.

The unaudited pro forma adjustments are based upon currently available information, estimates and assumptions that HGV’s management believes are reasonable as of the date hereof. The unaudited pro forma condensed combined financial information should be read in conjunction with the accompanying notes. The unaudited pro forma condensed combined financial information is for informational purposes only, is not intended to represent or to be indicative of actual results of operations or financial position of HGV or Diamond had the Acquisition been completed on the dates assumed, and should not be taken as indicative of future consolidated results of operations or financial position. The actual results may differ significantly from those reflected in the pro forma statement of operations for a number of reasons, including, but not limited to, differences between the assumptions used to prepare the pro forma statements of operations and actual amounts.

In addition, the unaudited pro forma condensed combined financial information should be read in conjunction with:

| • | HGV’s audited consolidated financial statements and related notes as of and for the year ended December 31, 2020, and unaudited condensed consolidated financial statements and related notes as of and for the three months ended March 31, 2021, which are included in this offering memorandum; |

| • | Diamond’s audited consolidated financial statements and related notes as of and for the year ended December 31, 2020, and unaudited condensed consolidated financial statements and related notes as of and for the three months ended March 31, 2021, which are included in this offering memorandum; and |

| • | “Management’s Discussion and Analysis of Financial Condition and Results of Operations—HGV—Pro Forma Liquidity and Capital Resources.” |

The historical financial statements have been adjusted in the accompanying unaudited pro forma condensed combined financial information to give effect to pro forma events that are applicable to business combination accounting as required under generally accepted accounting principles in the United States (GAAP). The unaudited pro forma condensed combined financial information contained herein does not include integration costs or benefits from synergies that may result from the Acquisition.

The unaudited pro forma condensed combined financial information has been prepared using the acquisition method of accounting in accordance with GAAP, with HGV considered the acquirer of Diamond. Accordingly, consideration paid or exchanged by HGV to complete the Acquisition will generally be allocated to assets and liabilities of Diamond based on their estimated fair values as of the date of completion of the Acquisition. The

18

acquisition method of accounting is dependent upon certain valuation assumptions, including those related to the preliminary purchase price allocation of the assets acquired and liabilities assumed of Diamond based on management’s best estimates of fair value. The actual purchase price allocation may vary based on final analyses of the fair value of the acquired assets, assumed liabilities, and changes in the acquired balances from operations up to through the actual merger date. In addition, the value of the consideration paid or exchanged by HGV to complete the Acquisition will be determined based on the trading price of HGV common stock at the time of completion of the Acquisition. These changes may result in material adjustments.

Some amounts do not match the Diamond historical financial statements due to rounding (refer to Note 4 of the Unaudited Pro Forma Condensed Combined Financial Information).

19

UNAUDITED PRO FORMA CONDENSED COMBINED BALANCE SHEET

As of March 31, 2021

(in millions)

| HGV Historical |

Reclassified Diamond Historical Note 4 |

Transaction Accounting Adjustments Note 6 |

Financing Adjustments |

Pro Forma Combined |

||||||||||||||||||||

| ASSETS |

||||||||||||||||||||||||

| Cash and cash equivalents |

$ | 400 | $ | 197 | $ | (1,366 | ) | (a) | $ | 1,139 | (f) | $ | 260 | |||||||||||

| (105 | ) | (g) | ||||||||||||||||||||||

| (5 | ) | (j) | ||||||||||||||||||||||

| Restricted cash |

105 | 100 | 205 | |||||||||||||||||||||

| Accounts receivable, net of allowance for doubtful accounts |

111 | 75 | 186 | |||||||||||||||||||||

| Timeshare financing receivables, net |

940 | 590 | 70 | (c) | 1,600 | |||||||||||||||||||

| — | (e) | |||||||||||||||||||||||

| Inventory |

720 | 634 | 68 | (c) | 1,422 | |||||||||||||||||||

| Property and equipment, net |

501 | 355 | (33 | ) | (c) | 823 | ||||||||||||||||||

| Operating lease right-of-use assets, net |

48 | 19 | 67 | |||||||||||||||||||||

| Investments in unconsolidated affiliates |

53 | — | 53 | |||||||||||||||||||||

| Intangible assets, net |

80 | 992 | 883 | (c) | 1,955 | |||||||||||||||||||

| Goodwill |

— | 882 | (104 | ) | (c) | 992 | ||||||||||||||||||

| 214 | (h) | |||||||||||||||||||||||

| Land and infrastructure held for sale |

41 | — | 41 | |||||||||||||||||||||

| Other assets |

115 | 433 | (2 | ) | (c) | 546 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| TOTAL ASSETS |

$ | 3,114 | $ | 4,277 | $ | (380 | ) | $ | 1,139 | $ | 8,150 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| LIABILITIES AND EQUITY |

||||||||||||||||||||||||

| Accounts payable, accrued expenses and other |

$ | 260 | $ | 464 | $ | (3 | ) | (c) | $ | $ | 700 | |||||||||||||

| (16 | ) | (i) | ||||||||||||||||||||||

| (5 | ) | (j) | ||||||||||||||||||||||

| Advanced deposits |

114 | — | 114 | |||||||||||||||||||||

| Debt, net |

1,156 | 1,928 | 37 | (c) | 2,963 | |||||||||||||||||||

| (1,311 | ) | (d) | 1,153 | (f) | ||||||||||||||||||||

| Non-recourse debt, net |

698 | 559 | 26 | (c) | 1,283 | |||||||||||||||||||

| Operating lease liabilities |

63 | 21 | 84 | |||||||||||||||||||||

| Deferred revenues |

336 | 211 | 547 | |||||||||||||||||||||

| Deferred income tax liabilities |

118 | 378 | 214 | (h) | 710 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total liabilities |

2,745 | 3,561 | (1,058 | ) | 1,153 | 6,401 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Equity: |

||||||||||||||||||||||||

| Preferred Stock |

— | — | — | |||||||||||||||||||||

| Common stock |

1 | 1 | (1 | ) | (b) | 1 | ||||||||||||||||||

| Additional paid-in capital |

194 | 1,082 | 1,483 | (a) | 1,677 | |||||||||||||||||||

| (1,082 | ) | (b) | ||||||||||||||||||||||

| Accumulated retained earnings (loss) |

174 | (367 | ) | 367 | (b) | 71 | ||||||||||||||||||

| (14 | ) | (f) | ||||||||||||||||||||||

| — | (e) | |||||||||||||||||||||||

| (105 | ) | (g) | ||||||||||||||||||||||

| 16 | (i) | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total equity |

369 | 716 | 678 | (14 | ) | 1,749 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| TOTAL LIABILITIES AND EQUITY |

$ | 3,114 | $ | 4,277 | $ | (380 | ) | $ | 1,139 | $ | 8,150 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

See accompanying notes to unaudited pro forma financial information.

20

UNAUDITED PRO FORMA CONDENSED COMBINED STATEMENT OF OPERATIONS

For the Year Ended December 31, 2020

(in millions)

| HGV Historical |

Reclassified Diamond Historical Note 4 |

Transaction Accounting Adjustments Note 6 |

Financing Adjustments |

Pro Forma Combined |

||||||||||||||||||||

| Revenues |

||||||||||||||||||||||||

| Sales of VOIs, net |

$ | 108 | $ | 248 | $ | — | (ff) |

$ | $ | 356 | ||||||||||||||

| Sales, marketing, brand and other fees |

221 | 59 | 280 | |||||||||||||||||||||

| Financing |

165 | 126 | (21 | ) | (dd) | 270 | ||||||||||||||||||

| Resort and club management |

166 | 291 | 457 | |||||||||||||||||||||

| Rental and ancillary services |

97 | 151 | 248 | |||||||||||||||||||||

| Cost reimbursements |

137 | 89 | 226 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total revenues |

894 | 964 | (21 | ) | — | 1,837 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||