Form 497K AMERICAN CENTURY INVESTM

Tweet

Tweet Share

ShareSummary Prospectus May 19, 2022 American Century Investments® High Income Fund |  | ||||||||||

Investor Class: AHIVX I Class: AHIIX | Y Class: NPHIX A Class: AHIAX | R5 Class: AHIEX R6 Class: AHIDX | G Class: ACHFX | ||||||||

| Before you invest, you may want to review the fund’s prospectus, which contains more information about the fund and its risks. You can find the fund’s prospectus, reports to shareholders, and other information about the fund online at the web addresses listed below. You can also get this information at no cost by calling or sending an email request. The fund’s prospectus and other information are also available from financial intermediaries (such as banks and broker-dealers) through which shares of the fund may be purchased or sold. | |||||||||||

Retail Investors americancentury.com/docs 1-800-345-2021 or 816-531-5575 prospectus@americancentury.com | Financial Professionals americancentury.com/fadocs 1-800-345-6488 advisor_prospectus@americancentury.com | ||||||||||

This summary prospectus incorporates by reference the fund’s prospectus and statement of additional information (SAI), each dated May 19, 2022 (as supplemented at the time you receive this summary prospectus), as well as the Report of Independent Registered Public Accounting Firm and the financial statements included in the fund’s annual report to shareholders, dated March 31, 2021, and the financial statements (unaudited) included in the fund's semiannual report report to shareholders dated September 30, 2021. The fund’s SAI, annual report and semiannual report may be obtained, free of charge, in the same manner as the prospectus. | |||||||||||

Investment Objective

The fund seeks current yield and capital growth.

Fees and Expenses

The following table describes the fees and expenses you may pay if you buy, hold and sell shares of the fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in American Century Investments funds. More information about these and other discounts is available from your financial professional and in Calculation of Sales Charges on page 14 of the fund’s prospectus, Appendix A of the fund’s prospectus and Sales Charges in Appendix B of the statement of additional information.

Shareholder Fees (fees paid directly from your investment) | |||||||||||||||||||||||

| Investor | I | Y | A | R5 | R6 | G | |||||||||||||||||

| Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | None | None | None | 4.50% | None | None | None | ||||||||||||||||

| Maximum Deferred Sales Charge (Load) (as a percentage of the lower of the original offering price or redemption proceeds when redeemed within one year of purchase) | None | None | None | None¹ | None | None | None | ||||||||||||||||

| Maximum Annual Account Maintenance Fee (waived if eligible investments total at least $10,000) | $25 | None | None | None | None | None | None | ||||||||||||||||

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) | |||||||||||||||||||||||

| Investor | I | Y | A | R5 | R6 | G | |||||||||||||||||

| Management Fee | 0.78% | 0.68% | 0.58% | 0.78% | 0.58% | 0.53% | 0.53% | ||||||||||||||||

| Distribution and Service (12b-1) Fees | None | None | None | 0.25% | None | None | None | ||||||||||||||||

| Other Expenses | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | ||||||||||||||||

| Total Annual Fund Operating Expenses | 0.78% | 0.68% | 0.58% | 1.03% | 0.58% | 0.53% | 0.53% | ||||||||||||||||

| Fee Waiver | None | None | None | None | None | None | 0.53%² | ||||||||||||||||

| Total Annual Fund Operating Expenses After Fee Waiver | 0.78% | 0.68% | 0.58% | 1.03% | 0.58% | 0.53% | 0.00% | ||||||||||||||||

1 Purchases of $1 million or more may be subject to a contingent deferred sales charge of 1.00% if the shares are redeemed within one year of the date of the purchase.

2 The advisor has agreed to waive the G Class’s management fee in its entirety. The advisor expects the waiver to remain in effect permanently and cannot terminate it without the approval of the Board of Trustees.

Example

The example below is intended to help you compare the costs of investing in the fund with the costs of investing in other mutual funds. The example assumes that you invest $10,000 in the fund for the time periods indicated and then redeem all of your shares at the end of those periods and that you earn a 5% return each year. The example also assumes that the fund’s operating expenses remain the same, except that it reflects the rate and duration of any fee waivers noted in the table above. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

1 year | 3 years | 5 years | 10 years | |||||||||||

| Investor Class | $80 | $250 | $434 | $966 | ||||||||||

| I Class | $70 | $218 | $379 | $847 | ||||||||||

| Y Class | $59 | $186 | $324 | $726 | ||||||||||

| A Class | $551 | $764 | $994 | $1,653 | ||||||||||

| R5 Class | $59 | $186 | $324 | $726 | ||||||||||

| R6 Class | $54 | $170 | $297 | $665 | ||||||||||

| G Class | $0 | $0 | $0 | $0 | ||||||||||

Portfolio Turnover

The fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the fund’s performance. During the most recent fiscal year, the fund’s portfolio turnover rate was 49% of the average value of its portfolio.

Principal Investment Strategies

Under normal market conditions, the fund invests primarily in high-yield corporate bonds and other debt instruments with an emphasis on those that are rated below investment-grade. A high-yield security, or junk bond, is one that has been rated below the four highest categories used by a nationally recognized statistical rating organization, or, if unrated, determined by the investment advisor to be of similar quality.

Types of high-yield securities the fund may invest in include: bank loans in the form of assignments or participations; payment-in-kind securities; deferred payment securities; and fixed, variable, and floating rate obligations. The fund may invest in new issuances of high yield securities, distressed securities, and restricted or illiquid securities, including Rule 144A securities.

Bank loans include senior secured and unsecured floating rate loans of corporations, partnerships, or other entities. Typically these loans hold a senior position in the borrower’s capital structure, they have interest rates that reset frequently, and they may be secured by the borrower’s assets or they may be unsecured. The fund may invest up to 20% of its net assets in bank loan investments.

Deferred payment securities are zero-coupon securities that convert on a specified date to interest bearing debt securities. On this date, the stated coupon rate becomes effective and interest is paid at regular intervals.

The fund may invest in fixed-income instruments of foreign issuers, including emerging market issuers. Generally, the fund invests in U.S. dollar denominated securities, however, the fund may invest in securities denominated in foreign currencies.

The fund has no average maturity limitations, but it typically invests in intermediate-term and long-term debt securities. The fund may also invest in short-term money market instruments and U.S. government securities.

To determine whether to buy or sell a security, the portfolio managers consider, among other things, various fund requirements and standards, along with economic conditions, alternative investments and interest rates.

Principal Risks

•Credit Risk – The inability or perceived inability of a security’s issuer to make interest and principal payments may cause the value of the security to decrease. As a result, the fund’s share price could also decrease. Changes in the credit rating of a debt security held by the fund could have a similar effect.

•High-Yield Risk – Issuers of high-yield securities are more vulnerable to real or perceived economic changes (such as an economic down turn or a prolonged period of rising interest rates), political changes or adverse developments specific to an issuer than issuers of investment grade debt securities. High-yield securities (junk bonds) are inherently speculative. These factors may be more likely to cause an issuer of high-yield bonds to default on its obligations.

•Liquidity Risk – The market for lower-quality debt securities is generally less liquid than the market for higher-quality securities. Changing regulatory and market conditions, including increases in interest rates and credit spreads may adversely affect the liquidity of the fund’s investments. During periods of market turbulence or unusually low trading activity, to meet redemptions it may be necessary for the fund to sell securities at prices that could have an adverse effect on the fund’s share price.

•Interest Rate Risk – Generally, the value of debt securities and the funds that hold them decline as interest rates rise. Because the fund typically invests in intermediate-term and long-term debt securities, the fund’s interest rate risk is generally higher than for funds with shorter-weighted average maturities, such as money market and short-term bond funds. A period of rising interest rates may negatively affect the fund’s performance.

•New Issue Risk – The market value of newly issued securities may fluctuate considerably due to factors such as the absence of a prior public market, unseasoned trading, the limited availability for trading, and limited information about the issuer.

•Bank Loans Risk – When purchasing participations, the fund generally has no rights to enforce borrower compliance with the terms of the loan agreement, nor any rights of set-off against the borrower, and the fund may not benefit directly from any collateral supporting the loan. This means the fund assumes the credit risk of both the borrower and the lender that sells the participation. Investments in unsecured bank loans are subject to greater risk than investment in loans secured by collateral. Bank loan transactions may take more than seven days to settle, meaning that proceeds would be unavailable to make additional purchases or meet redemptions. Finally, bank loans may not be considered “securities” under the federal securities laws. Therefore, the fund may not be able to rely on the anti-fraud provisions of those laws.

•Distressed Securities Risk – Distressed securities are speculative and involve substantial risk in addition to the risks of investing in high-yield bonds. Distressed securities frequently do not produce income while they are outstanding and may require the fund to bear certain extraordinary expenses to protect and recover its investment. Distressed securities are at high risk for default and may include securities that have already defaulted. The fund could lose its entire investment.

•Deferred Payment Securities Risk – During the time that interest payments are not being made on these securities, holders are deemed to receive income (phantom income) annually, even though cash is not received. Additionally, these securities may be subject to greater price fluctuations when interest rates change than securities that currently pay interest. Longer term zero-coupon bonds are more exposed to this risk than those with shorter terms.

•Foreign Securities Risk – Foreign securities are generally riskier than U.S. securities. Political events (such as civil unrest, national elections and imposition of exchange controls), social and economic events (such as labor strikes and rising inflation), natural disasters and public health emergencies occurring in a country where the fund invests could cause the fund’s investments in that country to experience losses. Securities of foreign issuers may be less liquid, more volatile and harder to value than U.S. securities.

•Emerging Market Risk – Investing in emerging market countries generally is also riskier than investing in foreign developed countries. Emerging market countries may have unstable governments and/or economies that are subject to sudden change, and significant volatility in their financial markets. These countries also may lack the legal, business and social framework to support securities markets.

•Restricted and Illiquid Securities Risk – The fund may invest in restricted or illiquid securities, including Rule 144A securities, which are securities that are not registered for sale to the general public under the Securities Act of 1933, as amended. These securities may be resold to certain institutional investors but, if at any time an insufficient number of qualified institutional buyers are interested in purchasing the securities, the fund may not have the ability to dispose of such securities promptly or at expected prices. As such, even if determined to be liquid, a fund’s investment in Rule 144A securities may subject the fund to enhanced liquidity risk and potentially increase the fund’s exposure to illiquid investments.

•Market Risk – The value of securities owned by the fund may go up and down, sometimes rapidly or unpredictably. Market risks, including political, regulatory, economic and social developments, can affect the value of the fund’s investments. Natural disasters, public health emergencies, war, terrorism and other unforeseeable events may lead to increased market volatility and may have adverse long-term effects on world economies and markets generally.

•Public Health Emergency Risk – A pandemic, caused by the infectious respiratory illness COVID-19, has caused market disruption and other economic impacts. Markets experienced volatility, reduced liquidity, and increased trading costs. The pandemic may continue to impact the fund and its underlying investments.

•Payment-in-Kind Securities Risk – Payment-in-kind securities carry additional risk as holders of these types of securities realize no cash until the cash payment date unless a portion of such securities is sold and, if the issuer defaults, the fund may obtain no return at all on its investment. The market price of payment-in-kind securities is affected by interest rate changes to a greater extent, and therefore tends to be more volatile, than that of securities which pay interest in cash.

•Redemption Risk – The fund may need to sell securities at times it would not otherwise do so to meet shareholder redemption requests. Selling securities to meet such redemptions may cause the fund to experience a loss, increase the fund’s transaction costs or have tax consequences. To the extent that a large shareholder (including a fund of funds or 529 college savings plan) invests in the fund, the fund may experience relatively large redemptions as such shareholder reallocates its assets.

•Principal Loss – At any given time your shares may be worth less than the price you paid for them. In other words, it is possible to lose money by investing in the fund.

An investment in the fund is not a bank deposit, and it is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency.

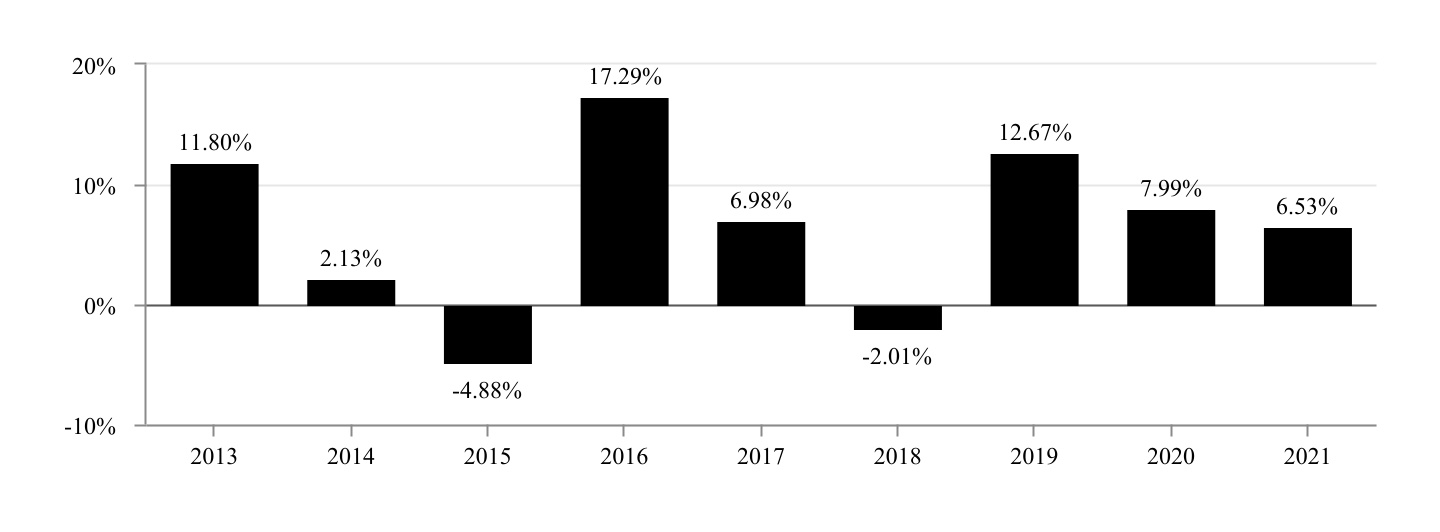

Fund Performance

The following bar chart and table provide some indication of the risks of investing in the fund. The bar chart shows changes in the fund’s performance from year to year for Y Class shares. The table shows how the fund’s average annual total returns for the periods shown compared with those of a broad measure of market performance. Because the G Class does not have investment performance for a full calendar year, it is not included. The fund’s past performance (before and after taxes) is not necessarily an indication of how the fund will perform in the future. For current performance information, including yields, please visit americancentury.com.

The fund acquired the assets and assumed the historical performance of the Nomura High Yield Fund, a series of The Advisors’ Inner Circle Fund III (the “Predecessor Fund”) on October 2, 2017 (the “Reorganization”). Accordingly, the performance shown for periods prior to October 2, 2017 represents the performance of Class I shares of the Predecessor Fund. In addition, the Predecessor Fund acquired the assets and assumed the historical performance of the High Yield Fund, a series of Nomura Partners Funds, Inc. (the “Prior Predecessor Fund,” and together with the Predecessor Fund, the “Predecessor Funds”) on December 8, 2014 (the “Prior Reorganization”). Accordingly, the performance shown for periods before December 8, 2014 represents the performance of Class I shares of the Prior Predecessor Fund. The Predecessor Funds’ returns in the bar chart and table have not been adjusted to reflect the fund’s expenses. If the Predecessor Funds’ performance information had been adjusted to reflect the fund’s expenses, the performance may have been higher or lower for a given period depending on the expenses incurred by the Predecessor Funds for that period.

Sales charges and account fees, if applicable, are not reflected in the bar chart. If those charges were included, returns would be less than those shown.

Calendar Year Total Returns

Highest Performance Quarter (2Q 2020): 9.19% Lowest Performance Quarter (1Q 2020): -12.50%

As of March 31, 2022, the most recent calendar quarter end, the fund’s Y Class year-to-date return was -4.20%.

Average Annual Total Returns For the calendar year ended December 31, 2021 | 1 year | 5 years | Since Inception | Inception Date | ||||||||||

Y Class Return Before Taxes | 6.53% | 6.32% | 6.27% | 12/27/2012 | ||||||||||

| Return After Taxes on Distributions | 3.94% | 3.81% | 3.42% | 12/27/2012 | ||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | 3.86% | 3.72% | 3.49% | 12/27/2012 | ||||||||||

Investor Class1 Return Before Taxes | 6.21% | — | 5.75% | 10/02/2017 | ||||||||||

I Class1 Return Before Taxes | 6.43% | 6.20% | 6.16% | 10/02/2017 | ||||||||||

A Class1 Return Before Taxes | 1.22% | 4.87% | 5.25% | 10/02/2017 | ||||||||||

R5 Class1 Return Before Taxes | 6.53% | 6.32% | 6.27% | 10/02/2017 | ||||||||||

R6 Class Return Before Taxes | 6.59% | — | 6.02% | 10/02/2017 | ||||||||||

ICE BofA U.S. High Yield Constrained Index (reflects no deduction for fees, expenses or taxes) | 5.35% | 6.07% | 5.76% | 12/27/2012 | ||||||||||

1Historical performance for the Investor, I, A and R5 Classes prior to their inception is based on the performance of the Predecessor Fund and Prior Predecessor Fund. Investor, I, A and R5 Class performance has been adjusted to reflect differences in sales charges, if applicable, and expenses between classes. Since inception performance is based on the inception date of the Predecessor Funds.

After-tax returns are shown only for Y Class shares. After-tax returns for other share classes will vary. After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their fund shares through tax-deferred arrangements, such as 401(k) plans or IRAs.

Portfolio Management

Investment Advisor

American Century Investment Management, Inc.

Subadvisor

Nomura Corporate Research and Asset Management Inc. (NCRAM)

Portfolio Managers

David Crall, CFA, Chief Executive Officer, Chief Investment Officer and Managing Director of NCRAM, has managed the fund since its inception in 2017 and managed the Predecessor Funds since 2012.

Stephen Kotsen, CFA, Managing Director and Portfolio Manager of NCRAM, has managed the fund since its inception in 2017 and managed the Predecessor Funds since 2012.

Amy Yu Chang, CFA, Managing Director and Portfolio Manager of NCRAM, has managed the fund since 2019.

Derek Leung, CFA, Executive Director and Portfolio Manager of NCRAM, has managed the fund since 2019.

Purchase and Sale of Fund Shares

You may purchase or redeem shares of the fund on any business day through our website at americancentury.com, in person (at one of our Investor Centers), by mail (American Century Investments, P.O. Box 419200, Kansas City, MO 64141-6200), by telephone at 1-800-345-2021 (Investor Services Representative) or 1-800-345-3533 (Business, Not-For-Profit and Employer-Sponsored Retirement Plans), or through a financial intermediary. Shares may be purchased and redemption proceeds received by electronic bank transfer, by check or by wire.

Unless otherwise specified below, the minimum initial investment amount to open an account is $2,500 ($1,000 for Coverdell Education Savings Accounts and IRAs). However, American Century Investments will waive the fund minimum if you make an initial investment of at least $500 and continue to make automatic investments of at least $100 a month until reaching the fund minimum. Investors opening accounts through financial intermediaries may open an account with $250 for the Investor and A Classes, but the financial intermediaries may require their clients to meet different investment minimums. The minimum may be waived for broker-dealer sponsored wrap program accounts, fee based accounts, and accounts through bank/trust and wealth management advisory organizations.

The minimum initial investment amount for the I Class is generally $5 million ($3 million for endowments and foundations), but the minimum may be waived if you have an aggregate investment in the American Century family of funds of $10 million or more ($5 million for endowments and foundations). This includes accounts held directly with American Century and those held through a financial intermediary.

There is no minimum initial investment amount for Y, R5 or R6 Class shares.

For the Investor, A, R5 and R6 Classes, there is no minimum initial investment amount for certain employer-sponsored retirement plans, however, financial intermediaries or plan recordkeepers may require plans to meet different minimums. Employer-sponsored retirement plans are not eligible to purchase I or Y Class shares.

There is a $50 minimum for subsequent purchases, except that there is no subsequent purchase minimum for financial intermediaries or employer-sponsored retirement plans.

G Class shares are available for purchase only by funds advised by American Century Investments and other American Century advisory clients that are subject to a contractual fee for investment management services. G Class shares do not have a minimum purchase amount.

Tax Information

Fund distributions are generally taxable as ordinary income or capital gains, unless you are investing through a tax-deferred account such as a 401(k) or individual retirement account (in which case you may be taxed upon withdrawal of your investment from such account).

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase the fund through a broker-dealer or other financial intermediary (such as a bank, insurance company, plan sponsor or financial professional), the fund and its related companies may pay the intermediary for the sale of fund shares and related services for investments in all classes except the Y, R6 and G Classes. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

©2022 American Century Proprietary Holdings, Inc. All rights reserved.

CL-SUM-92495 2205

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Renesas Reports Financial Results for the First Quarter Ended March 31, 2024

- Helo Corp Announces Annual 2023 Results

- International Truck Integrates Allison Fully Automatic Transmissions with S13 Engine

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!