Form 497 Short Term Investment

Tweet

Tweet Share

Share

| |

| PROSPECTUS |

| |

| |

| 1 | ||||

| 8 | ||||

| 8 | ||||

| 8 | ||||

| 9 | ||||

| 9 | ||||

| 10 | ||||

| 14 | ||||

| 17 | ||||

| 17 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 20 | ||||

| 20 | ||||

| 21 | ||||

| 21 | ||||

| 21 | ||||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 25 | ||||

| 26 | ||||

| 27 | ||||

| 27 | ||||

| 27 | ||||

| 27 | ||||

| 28 | ||||

| 28 |

| Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||

| Management Fee |

||

| Distribution and/or Service (12b‑1) Fees |

||

| Other Expenses(1) |

||

| Administration |

||

| Miscellaneous |

||

| Total Annual Fund Operating Expenses(2) |

||

| Less Fee Waivers and/or Expense Reimbursements(1) |

||

| Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursements(2) |

|

| 1 year | 3 years* | 5 years* | 10 years* | |||

| $ |

$ |

$ |

$ |

Average Annual Total Returns |

1 Year | 5 Years | 10 Years | |||

| Short Term Investment Fund for Puerto Rico Residents, Inc. |

||||||

| Return Before Taxes |

||||||

| Return After Taxes on Distributions |

||||||

| Return After Taxes on Distributions and Sales of Shares |

||||||

| ICE BofA US 3‑Month Treasury Bill Index |

| Name | Managed the Fund Since | Title | ||

| Leslie Highley, Jr. | 2003 | Managing Director of UBS Trust Company of Puerto Rico | ||

| Javier Rodriguez | 2007 | Director of UBS Trust Company of Puerto Rico | ||

| Heydi Cuadrado | 2008 | Director of UBS Trust Company of Puerto Rico |

| Fund Shares | ||

| Minimum Initial and Subsequent Investment Amounts |

There is no minimum investment for UBS brokerage accounts. There is a $10,000 minimum for initial and additional investments for purchases made through other UBS account or other financial intermediaries. |

You may redeem for cash all full and fractional Shares one each day that the New York Stock Exchange is open for trading and the Federal Reserve Bank of New York and banks in Puerto Rico are open for business at the price equal to the next calculated net asset value per Share after your order is received in “good form” meeting the requirements set forth under “Redemption Procedure” below. Redemption orders received on a redemption date after the calculation of the Fund’s net asset value on that date, will be effected on the next occurring redemption date at the Share price calculated on that date. Payment will generally be made within seven days after request are received in “good form,” but in any event, within seven days.

| FINANCIAL HIGHLIGHTS | ||||||||||||||||||||||

| For the period from July 1, 2021 to December 31, 2021 (Unaudited) |

For the fiscal year ended June 30, 2021 |

|||||||||||||||||||||

| Increase in Net Asset Value: |

||||||||||||||||||||||

| Per Share Operating |

Net asset value, beginning of period | $ | 1.00 | $ | 1.00 | |||||||||||||||||

| Performance: |

Net investment income (a) |

0.00 | * | * | 0.00 | * | * | |||||||||||||||

| Total from investment operations | 0.00 | 0.00 | ||||||||||||||||||||

| Less: Distributions from net investment income | (0.00 | ) | * | * | (0.00 | ) | * | * | ||||||||||||||

| Net asset value, end of period | $ | 1.00 | $ | 1.00 | ||||||||||||||||||

| Total Investment |

||||||||||||||||||||||

| Return: |

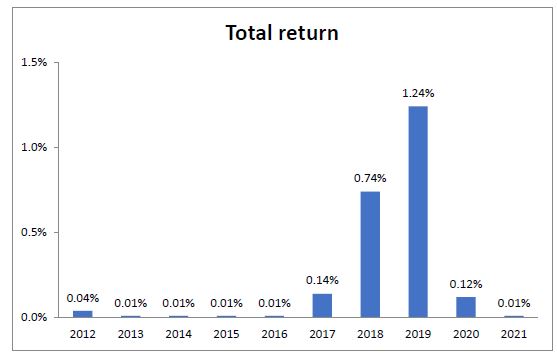

(b) | Based on net asset value per share | 0.01 | % | 0.02 | % | ||||||||||||||||

| Ratios: |

(c) (d) | Net expenses to average net assets - net of waived and/or reimbursed expenses | 0.01 | % | 0.06 | % | ||||||||||||||||

| (c) (d) | Gross expenses to average net assets | 0.88 | % | 0.81 | % | |||||||||||||||||

| (c) (d) | Net investment income to average net assets - net of waived and/or reimbursed expenses | 0.01 | % | 0.01 | % | |||||||||||||||||

| Net assets, end of period (in thousands) | $ | 231,028 | $ | 304,412 | ||||||||||||||||||

| Supplemental |

||||||||||||||||||||||

| Data: |

(e) | Portfolio turnover | - | - | ||||||||||||||||||

| ** | Net investment income and distributions from net investment income for the period from July 1, 2021 to December 31, 2021 and for the fiscal year ended June 30, 2021 were $0.0001 and $0.0001 per share, respectively. |

| (a) | Based on average outstanding common shares of 264,864,171 and 339,608,192 for the period from July 1, 2021 to December 31, 2021 and for the fiscal year ended June 30, 2021, respectively. |

| (b) | Dividends are assumed to be reinvested at the per share net asset value on the date dividends are paid. Investment return is not annualized for the period from July 1, 2021 to December 31, 2021. |

| (c) | Based on average net assets applicable to common shareholders of $265,131,064 and $339,608,192 for the period from July 1, 2021 to December 31, 2021 and for the fiscal year ended June 30, 2021, respectively. Ratios for the period from July 1, 2021 to December 31, 2021 were annualized using a 365 day base. |

| (d) | The effect of the expenses waived/reimbursed for the period from July 1, 2021 to December 31, 2021 and for the fiscal year ended June 30, 2021 was to decrease the expense ratios, thus increasing the net investment income ratio to average net assets by 0.87% and 0.75%, respectively |

| • | Investor applications and other forms, |

| • | Written and electronic correspondence, |

| • | Telephone contacts, |

| • | Account history (including information about Fund transactions and balances in your accounts with the Distributor or our affiliates, other fund holdings in the UBS family of funds, and any affiliation with the Distributor and its affiliates), |

| • | Website visits, |

| • | Consumer reporting agencies |

STATEMENT OF ADDITIONAL INFORMATION

SHORT TERM INVESTMENT FUND FOR PUERTO RICO RESIDENTS, INC.

250 Muñoz Rivera Avenue, Tenth Floor, San Juan, Puerto Rico 00918 • (787) 250-3600

This Statement of Additional Information (“SAI”) of the Short Term Investment Fund for Puerto Rico Residents, Inc. (the “Fund”) is not a prospectus and should be read in conjunction with the Prospectus of the Fund, dated May 16, 2022, as it may be amended or supplemented from time to time (the “Prospectus”), which has been filed with the Securities and Exchange Commission (the “Commission” or the “SEC”) and can be obtained, without charge, by writing or calling the Fund at the address or telephone number printed above, or on the Fund’s website at www.ubs.com/prfunds. The Prospectus is incorporated by reference into this SAI, and this SAI has been incorporated by reference into the Fund’s Prospectus. Only Puerto Rico Residents will receive the tax benefits of an investment in the Fund. See the section “Puerto Rico Taxation” for a description of such tax benefits. In addition, the Fund does not intend to qualify as a “RIC” under Subchapter M of the U.S. Internal Revenue Code of 1986, as amended, and consequently an investor that is not a Puerto Rico Resident will not receive the tax benefits (such as “RIC” tax treatment) of an investment in typical U.S. mutual fund registered under the Investment Company Act of 1940, as amended (the “1940 Act”) and may have adverse tax consequences for US federal income tax purposes. This SAI does not include all information that a prospective investor should consider before investing in the Fund. Investors should obtain and read the Prospectus prior to purchasing shares of the Fund. In addition, the Fund’s audited financial statements and the auditor’s report included in the Fund’s annual report for the fiscal year ended June 30, 2021 are incorporated by reference herein. The Fund’s unaudited financials included in the Fund’s semi-annual report for the period ended December 31, 2021 are incorporated by reference herein. Such reports include presentations and disclosures in accordance with guidance set forth by Regulation S-X. You may also obtain a copy of the prospectus on the SEC’s website (http://www.sec.gov). Capitalized terms used but not defined in this SAI have the meanings ascribed to them in the Prospectus.

References to the 1940 Act or other applicable law, will include any rules promulgated thereunder and any guidance, interpretations or modifications by the Commission, Commission staff or other authority with appropriate jurisdiction, including court interpretations, and exemptive, no-action or other relief or permission from the Commission, Commission staff or other authority.

| Share Class |

Ticker Symbol | |

|

|

| |

| Shares Of Beneficial Interest |

PRALX |

UBS Asset Managers of Puerto Rico — Investment Adviser

UBS Financial Services Inc. — Distributor

The date of this Statement of Additional Information is May 16, 2022.

TABLE OF CONTENTS

| 1 | ||||

| 1 | ||||

| 1 | ||||

| Description of Certain Investments, Investment Techniques and Investment Risks |

3 | |||

| 3 | ||||

| 5 | ||||

| 8 | ||||

| 8 | ||||

| 8 | ||||

| 9 | ||||

| 9 | ||||

| 10 | ||||

| Leadership Structure and Oversight Responsibilities of the Board |

12 | |||

| 12 | ||||

| 13 | ||||

| Beneficial Ownership of Equity Securities in the Fund and Affiliated Funds by Each Director |

13 | |||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

| 16 | ||||

| 17 | ||||

| 17 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 23 | ||||

| 23 | ||||

| 23 | ||||

| 23 | ||||

| A-1 | ||||

| B-1 |

History of the Fund

The Fund is registered as an open-end management investment company under the 1940 Act. The Fund was incorporated under the laws of the Commonwealth of Puerto Rico on July 26, 2002 and started operations on December 8, 2006. Prior to May 14, 2021, the Fund was registered as an investment company under the Puerto Rico Investment Companies Act of 1954, as amended and operated as such under the laws of Puerto Rico. In 2018, the Economic Growth, Regulatory Relief, and Consumer Protection Act was signed into law in the United States and effectively requires investment companies organized under the laws of Puerto Rico to register as investment companies under the 1940 Act. As a result, the Fund has been registered under the 1940 Act since May 14, 2021.

As of the date of this SAI, the Fund is authorized to issue 2,000,000,000 shares of beneficial interest (the “Shares”) with a par value of $0.001 per share, which may be divided into different series and classes. The Fund currently has only one class of shares outstanding.

Investment Objectives, Policies and Restrictions

Please see the Prospectus for more information about the Fund’s investment objective and policies. Additional information regarding the Fund’s investment objective and policies is included below.

The Fund is classified as non-diversified under the 1940 Act.

The Fund’s investment objective and certain investment policies that are fundamental policies may not be changed unless authorized by a majority (which for this purpose and under the 1940 Act, means the lesser of (i) 67% of the shares represented at a meeting at which more than 50% of the outstanding shares are represented or (ii) more than 50% of the outstanding shares) and in some cases, a supermajority of the Fund’s outstanding voting securities (it being understood that, respect to these voting requirements or standards, the Fund will take no-action that is at that time inconsistent with the 1940 Act). However, subject to Puerto Rico law, all other investment policies and limitations may be changed by the Board of Directors (the “Board”) without shareholder approval.

Investment Policies and Restrictions

The Fund is subject to the following investment restrictions, all of which are fundamental policies. The Fund may not:

(a) issue preferred shares or debt securities, or borrow money from banks or other entities, provided, that, the Fund may borrow up to an additional 5% of the Fund’s total assets (including the amount borrowed) from banks or other financial institutions for temporary or emergency purposes, including to finance redemptions; or

(b) issue senior securities to the extent such issuance would violate the 1940 Act.

Notations Regarding the Funds’ Fundamental Investment Restrictions

The following notations are not considered to be part of the Fund’s fundamental investment restrictions and are subject to change without shareholder approval.

With respect to the fundamental policy relating to borrowing money set forth in (a) above, the Fund has restricted borrowing to 5% of the Fund’s total assets, which is more restrictive than the limitation imposed by the 1940 Act, which permits a fund to borrow money in amounts of up to one-third of the Fund’s total assets from banks for any purpose, and to borrow up to 5% of the Fund’s total assets from banks or other lenders for temporary or emergency purposes, including to finance redemptions. (A fund’s total assets include the amounts being borrowed.) To limit the risks attendant to borrowing, the 1940 Act requires the Fund to maintain at all times an “asset coverage” of at least 300% of the amount of its borrowings. Asset coverage means the ratio that the value of a fund’s total assets (including amounts borrowed), minus liabilities other than borrowings, bears to the aggregate amount of all borrowings. Borrowing money to increase portfolio holdings is known as “leveraging.” Certain trading practices and investments, such as reverse repurchase agreements, may be considered to be borrowings or involve leverage and thus are subject to the 1940 Act restrictions. In accordance with Commission staff guidance and interpretations prior to the compliance date of new Rule 18f-4 under the 1940 Act (“Rule 18f-4”), when a fund engages in

SAI-1

such transactions, instead of maintaining asset coverage of at least 300%, the fund may segregate or earmark liquid assets, or enter into an offsetting position, in an amount at least equal to the fund’s exposure, on a mark-to-market basis, to the transaction (as calculated pursuant to requirements of the Commission). On and after the compliance date of Rule 18f-4, borrowing through reverse repurchase agreements and dollar rolls will also be subject to the 300% asset coverage requirement.

The policy in (a) above (restricting the Fund’s borrowings to 5% of the Fund’s total assets for purposes of redeeming Shares) will be interpreted to otherwise permit the Fund to engage in trading practices and investments that may be considered to be borrowing or to involve leverage to the extent permitted by the 1940 Act and to otherwise permit the fund to segregate or earmark liquid assets or enter into offsetting positions in accordance with the 1940 Act, in each case subject to the policy. Short-term credits necessary for the settlement of securities transactions and arrangements with respect to securities lending will not be considered to be borrowings under the policy. Practices and investments that may involve leverage but are not considered to be borrowings (e.g., collateral arrangements with respect to options, forward currency and futures transactions and other derivative instruments, as well as delays in the settlement of securities transactions) are not subject to the policy.

In addition, the Fund may not change (1) the restrictions in (iii), (v), (vii), (viii) and (ix) below without the approval of a majority of the shareholders (as defined in the 1940 Act and as described above), and (2) any other restriction described below without the approval of a majority of the Board and prior written notice to shareholders of the Fund.

The Fund may not:

(i) purchase the securities of any one issuer if after such purchase it would own more than 25% of the voting securities of such issuer, provided that securities issued or guaranteed by the Commonwealth of Puerto Rico, United States government, or any of their respective agencies or instrumentalities (including GNMA, FNMA and FHLMC mortgage-backed securities) are not subject to this limitation;

(ii) make investments for the purpose of exercising control or management;

(iii) make an investment in any one industry if, at the time of purchase, the investment would cause the aggregate value of the Fund’s investments in such industry to equal 25% or more of the Fund’s total assets, provided that this limitation shall not apply to (i) investments made for temporary or defensive purposes; (ii) investments in high quality, short-term securities issued by Puerto Rico investment companies, (iii) investments in securities issued or guaranteed by the United States government, its agencies or instrumentalities, and (iv) tax-exempt Puerto Rico municipal obligations, other than those backed only by the assets or revenues of a non-governmental entity. For purposes of this restriction, the intended or designated use of real estate shall determine its industry, domestic and foreign banking will be considered separate industries, and mortgage-backed and asset-backed securities not issued or guaranteed by an agency or instrumentality of the United States government will be grouped in industries based on their underlying assets and not treated as a single, separate industry;

(iv) purchase securities on margin, except for short term credits necessary for clearance of portfolio transactions;

(v) engage in the business of underwriting securities of other issuers, except to the extent that, in connection with the acquisition or disposition of portfolio securities, the Fund may be deemed an underwriter under U.S. securities laws and except that the Fund may write options;

(vi) make short sales of securities or maintain a short position, except that the Fund may sell short “against the box.” A short sale “against the box” occurs when the Fund owns an equal amount of the securities sold or owns securities convertible into or exchangeable for, without payment of any further consideration, securities of the same issue as, and equal in amount to, the securities sold short;

(vii) purchase or sell real estate (including real estate limited partnership interests), provided that the Fund may invest in securities secured by real estate or interests therein or issued by entities that invest in real estate or interests therein (including mortgage-backed securities), and provided further that the Fund may exercise rights under agreements relating to such securities, including the right to enforce security interests and to liquidate real estate acquired as a result of such enforcement, provided, however, that such securities and any such real estate securing a security acquired by the Fund shall not be a “U.S. real property interest” within the meaning of Section 897 of the U.S. Code;

(viii) purchase or sell commodities or commodity contracts;

SAI-2

(ix) make loans, except through reverse repurchase agreements, provided that for purposes of this restriction the acquisition of bonds, debentures or other debt or similar instruments or interests therein, including investment in government obligations, shall not be deemed to be the making of a loan; or

(x) lend portfolio securities, except to the extent that such loans, if and when made, do not exceed 331⁄3% of the total assets of the Fund taken at market value.

Description of Certain Investments, Investment Techniques and Investment Risks

Set forth below are descriptions of some of the types of investments and investment techniques that the Fund may utilize, as well as certain risks and other considerations associated with such investments and investment techniques. The information below supplements the information contained in the Fund’s Prospectus under “More Information About the Fund—Principal Investment Strategies of the Fund”, “More Information About the Fund—Other Investments”, “More Information About the Fund—Principal Risks” and “More Information About the Fund—Additional Risks”.

Types of Municipal Obligations and Associated Risks

The Fund may invest in a variety of municipal securities, as described below:

Municipal Bonds

Municipal bonds are debt obligations that are issued by states, municipalities, public authorities or other issuers and that pay interest that is exempt from federal income tax in the opinion of issuer’s counsel. The two principal classifications of municipal bonds are “general obligation” and “revenue” bonds. General obligation bonds are secured by the issuer’s pledge of its full faith, credit and taxing power for the payment of principal and interest. Revenue bonds are payable only from the revenues derived from a particular facility or class of facilities or, in some cases, from the proceeds of a special excise tax or other specific revenue source such as from the user of the facility being financed. The term “municipal bonds” also includes “moral obligation” issues, which are normally issued by special purpose authorities. In the case of such issues, an express or implied “moral obligation” of a related government share is pledged to the payment of the debt service, but is usually subject to annual budget appropriations. Custodial receipts that represent an ownership interest in one or more municipal bonds also are considered to be municipal obligations.

The Fund may invest in industrial development bonds (“IDBs”) and private activity bonds (“PABs”), which are municipal bonds issued by or on behalf of public authorities to finance various privately operated facilities, such as airports or pollution control facilities. IDBs and PABs are generally revenue bonds and thus are not payable from the unrestricted revenue of the issuer. The credit quality of IDBs and PABs is usually directly related to the credit standing of the user of the facilities being financed. The Fund may invest more than 25% of its assets in a single IDB or PAB.

The Fund may not presently concentrate its investments, e.g., invest a relatively high percentage of its assets in municipal obligations (e.g. revenue bonds) issued by entities which may pay their debt service obligations from the revenues derived from similar projects such as hospitals, multifamily housing, nursing homes, continuing care facilities, commercial facilities (including hotels), electric utility systems or industrial companies. This limitation may in the future be changed by a majority of the Fund’s outstanding voting securities. Any future determination to allow concentration of the Fund’s investments may make the Fund more susceptible to similar economic, political, or regulatory occurrences. As the similarity in issuers increases, the potential for fluctuation of the net asset value of shares of the Fund also increases. Also it is anticipated that a significant percentage of the municipal obligations in the Fund’s portfolio may be issued by entities or secured by facilities with a relatively short operating history.

Municipal Lease Obligations

Municipal lease obligations are municipal obligations that may take the form of leases, installment purchase contracts or conditional sales contracts, or certificates of participation with respect to such contracts or leases. Municipal lease obligations are issued by state and local governments and authorities to purchase land or various types of equipment and facilities. Although municipal lease obligations do not constitute general obligations of the municipality for which the municipality’s taxing power is pledged, they ordinarily are backed by the municipality’s covenant to budget for, appropriate and make the payments due under the lease obligation. The leases underlying certain municipal obligations, however, provide

SAI-3

that lease payments are subject to partial or full abatement if, because of material damage or destruction of the leased property, there is substantial interference with the lessee’s use or occupancy of such property. This “abatement risk” may be reduced by the existence of insurance covering the leased property, the maintenance by the lessee of reserve funds or the provision of credit enhancements such as letters of credit.

The liquidity of municipal lease obligations varies. Certain municipal lease obligations also contain “non-appropriation” clauses which provide that the municipality has no obligation to make lease or installment purchase payments in future years unless money is appropriated for such purpose on a yearly basis. Some municipal lease obligations of this type are insured as to timely payment of principal and interest, even in the event of a failure by the municipality to appropriate sufficient funds to make payments under the lease. However, in the case of an uninsured municipal lease obligation, the Fund’s ability to recover under the lease in the event of non-appropriation or default will be limited solely to the repossession of the leased property, without recourse to the general credit of the lessee, and disposition of the property in the event of foreclosure might prove difficult. The Fund does not intend to invest a significant portion of its assets in such uninsured “non-appropriation” municipal lease obligations. There is no limitation on the Fund’s ability to invest in other municipal lease obligations.

Zero Coupon Obligations

Zero coupon municipal obligations include “pure zero” obligations, which pay no interest for their entire life (either because they bear no stated rate of interest or because their stated rate of interest is not payable until maturity), and “zero/fixed” obligations, which pay no interest for an initial period and thereafter pay interest currently. Zero coupon obligations also include derivative instruments representing the principal-only components of municipal obligations from which the interest components have been stripped and sold separately by the holders of the underlying municipal obligations. Zero coupon obligations usually trade at a deep discount from their face or par value and will be subject to greater fluctuations in market value in response to changing interest rates than obligations of comparable maturities that make current distributions of interest.

Floating and Variable Rate Obligations

Floating and variable rate municipal notes and bonds frequently permit the holder to demand payment of principal at any time, or at specified intervals, and permit the issuer to prepay principal, plus accrued interest, at its discretion after a specified notice period. The issuer’s obligations under the demand feature of such notes and bonds generally are secured by bank letters of credit or other credit support arrangements. There frequently will be no secondary market for variable and floating rate obligations held by the Fund, although the Fund may be able to obtain payment of principal at face value by exercising the demand feature of the obligation.

Participation Interests

Participation interests in municipal bonds, including IDBs, PABs, and floating and variable rate securities give the Fund an undivided interest in a municipal bond owned by a bank. The Fund has the right to sell the instrument back to the bank. Such right is generally backed by the bank’s irrevocable letter of credit or guarantee and permits the Fund to draw on the letter of credit on demand, after specified notice, for all or any part of the principal amount of the Fund’s participation interest plus accrued interest. Generally, the Fund intends to exercise the demand under the letters of credit or other guarantees only upon a default under the terms of the underlying bond, or to maintain compliance with the investment objective and policies of the Fund. The ability of a bank to fulfill its obligations under a letter of credit or guarantee might be affected by possible financial difficulties of its borrowers, adverse interest rate or economic conditions, regulatory limitations or other factors. The Investment Adviser will monitor the pricing, quality and liquidity of the participation interests held by the Fund, and the credit standing of banks issuing letters of credit or guarantees supporting such participation interests on the basis of published financial information reports of rating services and bank analytical services.

Put Bonds

Put bonds are municipal bonds which give the holder an unconditional right to sell the bond back to the issuer or a remarketing agent at a specified price and exercise date, which is typically well in advance of the bond’s maturity date. If the put is a “one time only” put, the Fund ordinarily will sell the bond or put the bond, depending on the more favorable price. If the bond has a series of puts after the first put, the bond will be held as long as, in the respective Investment Adviser’s opinion, it is in the best interests of the Fund to do so. The obligation to purchase the bond on the exercise date of the put may be supported by a letter of credit or other credit support agreement from a bank, insurance company or other financial institution,

SAI-4

the credit standing of which affects the credit standing of the obligation. There is no assurance that an issuer or remarketing agent for a put bond will be able to repurchase the bond on the put exercise date if the Fund chooses to exercise its right to put the bond back to the issuer or remarketing agent.

Tender Option Bonds

Tender option bonds are long-term municipal securities sold by a bank subject to a “tender option” that gives the purchaser the right to tender them to the bank at par plus accrued interest at designated times (the “tender option”). The tender option may be exercisable at intervals ranging from bi-weekly to semi-annually, and the interest rate on the bonds is typically reset at the end of the applicable interval in order to cause the bonds to have a market value that approximates their par value. The tender option generally would not be exercisable in the event of a default on, or significant downgrading of, the underlying municipal securities. Therefore, the Fund’s ability to exercise the tender option will be affected by the credit standing of both the bank involved and the issuer of the underlying securities.

Detachable Call Options and Embedded Caps

Detachable call options are sold by issuers of municipal obligations separately from the municipal obligations to which the call options relate and permit the purchasers of the call options to acquire the municipal obligations at the call price(s) and call date(s). In the event that interest rates drop, the purchaser could exercise the call option to acquire municipal obligations that yield above-market rates. The Fund expects to acquire detachable call options relating to municipal obligations that the Fund owns or will acquire in the immediate future and thereby, in effect, make such municipal obligations non-callable so long as the Fund continues to hold the detachable call option. Municipal obligations with embedded caps provide for additional tax-free payments for a stated period (generally a period that is shorter than the bond’s maturity) above the fixed-rated interest payable on the municipal obligations to the extent that the average level of a particular index exceeds a specified base level.

Mortgage-Backed Securities and Associated Risks

General

Mortgage-backed securities were introduced in the 1970s when the first pool of mortgage loans was converted into a mortgage pass-through security. Since the 1970s, the mortgage-backed securities market in general has vastly expanded and a variety of structures have been developed to meet investor needs.

New types of mortgage-backed securities are developed and marketed from time to time and, consistent with its investment limitations, the Fund expects to invest in those new types of mortgage-backed securities that the Investment Adviser believes may assist the Fund in achieving its investment objective. Not all of the types of securities described below are available in Puerto Rico.

Government National Mortgage Association (“GNMA”) Securities

GNMA is a wholly-owned corporate instrumentality of the United States within the Department of Housing and Urban Development. The National Housing Act of 1934, as amended (the “Housing Act”), authorizes GNMA to guarantee the timely payment of the principal of and interest on securities that are based on and backed by a pool of specified mortgage loans. To qualify such securities for a GNMA guarantee, the underlying mortgages must be insured by the Federal Housing Administration under the Housing Act, or Title V of the Housing Act of 1949 (“FHA Loans”), or be guaranteed by the Veterans’ Administration under the Servicemen’s Readjustment Act of 1944, as amended (“VA Loans”), or be pools of other eligible mortgage loans. The Housing Act provides that the full faith and credit of the United States Government is pledged to the payment of all amounts that may be required to be paid under any guarantee. In order to meet its obligations under such guarantee, GNMA is authorized to borrow from the United States Treasury with no limitations as to amount.

GNMA mortgage-backed securities include securities which are backed by mortgage loans insured by the Federal Housing Administration or guaranteed by the Veterans Administration, and which consist of mortgage-backed certificates with respect to pools of such mortgages guaranteed as to the timely payment of principal and interest by the Government National Mortgage Association. That guarantee is backed by the full faith and credit of the United States.

GNMA pass-through mortgage-backed securities may represent a pro rata interest in one or more pools of the following types of mortgage loans: (i) fixed rate level payment mortgage loans; (ii) fixed rate graduated payment mortgage

SAI-5

loans; (iii) fixed rate growing equity mortgage loans; (iv) fixed rate mortgage loans secured by manufactured (mobile) homes; (v) mortgage loans on multifamily residential properties under construction; (vi) mortgage loans on completed multifamily projects; (vii) fixed rate mortgage loans as to which escrowed funds are used to reduce the borrower’s monthly payments during the early years of the mortgage loans (“buydown” mortgage loans); (viii) mortgage loans that provide for adjustments in payments based on periodic changes in interest rates or in other payment terms of the mortgage loans; and (ix) mortgage-backed serial notes.

Federal National Mortgage Association (“FNMA”) Securities

FNMA is a federally chartered and privately owned corporation established under the Federal National Association Charter Act. FNMA was originally organized in 1938 as a United States Government agency to add greater liquidity to the mortgage market. FNMA was transformed into a private sector corporation by legislation enacted in 1968. FNMA provides funds to the mortgage market primarily by purchasing home mortgage loans from local lenders, thereby providing them with funds for additional lending. FNMA acquires funds to purchase such loans from investors that may not ordinarily invest in mortgage loans directly, thereby expanding the total amount of funds available for housing.

Each FNMA pass-through mortgage-backed security represents a pro rata interest in one or more pools of FHA Loans, VA Loans or conventional mortgage loans (i.e., mortgage loans that are not insured or guaranteed by any governmental agency). The loans contained in those pools consist of: (i) fixed rate level payment mortgage loans; (ii) fixed rate growing equity mortgage loans; (iii) fixed rate graduated payment mortgage loans; (iv) variable rate mortgage loans; (v) other adjustable rate mortgage loans; and (vi) fixed rate mortgage loans secured by multifamily projects. FNMA guarantees timely payment of principal and interest on FNMA mortgage-backed securities. The obligations of FNMA are not backed by the full faith and credit of the United States. Nevertheless, because of the relationship between FNMA and the United States, it is widely believed that FNMA Mortgage-Backed Securities present minimal credit risks.

Federal Home Loan Mortgage Corporation (“FHLMC”) Securities

FHLMC is a corporate instrumentality of the United States established by the Emergency Home Finance Act of 1970, as amended (the “FHLMC Act”). FHLMC was organized primarily for the purpose of increasing the availability of mortgage credit to finance needed housing. The operations of FHLMC currently consist primarily of the purchase of first lien, conventional, residential mortgage loans and participation interests in such mortgage loans and the resale of the mortgage loans so purchased in the form of mortgage-backed securities.

FHLMC mortgage-backed securities represent direct or indirect participations in, and are payable from, conventional residential mortgage loans. The mortgage loans underlying the FHLMC mortgage-backed securities typically consist of fixed rate or adjustable rate mortgage loans with original terms to maturity of between ten and thirty years, substantially all of which are secured by first liens on one- to four-family residential properties or multifamily projects. Each mortgage loan must meet the applicable standards set forth in the FHLMC Act. Mortgage loans underlying FHLMC mortgage-backed securities may include whole loans, participation interests in whole loans and undivided interests in whole loans and participations in another FHLMC mortgage-backed securities.

FHLMC guarantees: (i) the timely payment of interest on all FHLMC mortgage-backed securities; (ii) the ultimate collection of principal with respect to some FHLMC mortgage-backed securities; and (iii) the timely payment of principal with respect to other FHLMC mortgage-backed securities. The obligations of FHLMC are not backed by the full faith and credit of the United States, although they are generally considered to present minimal credit risks.

ARM and Floating Rate Mortgage-Backed Securities

Because the interest rates on ARM and Floating Rate mortgage-backed securities are reset in response to changes in a specified market index, the values of such securities tend to be less sensitive to interest rate fluctuations than the values of fixed-rate securities. ARM mortgage-backed securities represent a right to receive interest payments at a rate that is adjusted to reflect the interest earned on a pool of ARMs. ARMs generally provide that the borrower’s mortgage interest rate may not be adjusted above a specified lifetime maximum rate or, in some cases, below a minimum lifetime rate. In addition, certain ARMs provide for limitations on the maximum amount by which the mortgage interest rate may adjust for any single adjustment period. ARMs also may provide for limitations on changes in the maximum amount by which the borrower’s monthly payment may adjust for any single adjustment period. In the event that a monthly payment is not sufficient to pay the interest accruing on the ARM, any such excess interest is added to the mortgage loan (“negative amortization”), which is repaid through future

SAI-6

monthly payments. If the monthly payment exceeds the sum of the interest accrued at the applicable mortgage interest rate and the principal payment that would have been necessary to amortize the outstanding principal balance over the remaining term of the loan, the excess reduces the principal balance of the ARM. Borrowers under ARMs experiencing negative amortization may take longer to build up their equity in the underlying property and may be more likely to default.

The rates of interest payable on certain ARMs, and therefore on certain ARM mortgage-backed securities, are based on indices, such as the one-year constant maturity Treasury Rate, that reflect changes in market interest rates. Others are based on indices, such as the 11th District Federal Home Loan Bank Cost of Funds index, that tend to lag behind changes in market interest rates. The values of ARM mortgage-backed securities supported by ARMs that adjust based on lagging indices tend to be somewhat more sensitive to interest rate fluctuations than those reflecting current interest rate levels, although the values of such ARM mortgage-backed securities still tend to be less sensitive to interest rate fluctuations than fixed-rate securities.

Floating rate mortgage-backed securities are classes of mortgage-backed securities that have been structured to represent the right to receive interest payments at rates that fluctuate in accordance with an index but that generally are supported by pools comprised of fixed-rate mortgage loans. As with ARM mortgage-backed securities, interest rate adjustments on floating rate mortgage-backed securities may be based on indices that lag behind market interest rates. Interest rates on floating rate mortgage-backed securities generally are adjusted monthly. Floating rate mortgage-backed securities are subject to lifetime interest rate caps, but they generally are not subject to limitations on monthly or other periodic changes in interest rates or monthly payments.

Specified Mortgage-Backed Securities

The Fund generally does not invest in derivatives but may invest in mortgage-backed securities that are derivatives such as interest only obligations (“IOs”) (other than IOs and principal only obligations (“POs”) that are PAC Bonds) or inverse floating rate obligations or other types of mortgage-backed securities that may be developed in the future and that are determined by the Investment Adviser to present types and levels of risk that are comparable to such IOs, POs and inverse floating rate obligations (collectively, “Specified Mortgage-Backed Securities”). The Fund will invest in Specified Mortgage-Backed Securities only when the Investment Adviser believes that such securities, when combined with the Fund’s other investments, would enable the Fund to achieve its investment objective and policies. In the opinion of the Investment Adviser, GNMA mortgage-backed securities issued under the GNMA I or GNMA II programs, securities with earlier maturities of mortgage-backed securities issued under the GNMA Serial Note program, mortgage pass-through certificates issued by FNMA and other types of substantially similar mortgage-backed pass-through or participation certificates (including collateralized mortgage obligations (“CMOs”)) are not considered derivative investments for purposes of the Fund’s investment policies, except as set forth below. The Investment Adviser also does not consider Private Label mortgage-backed securities (including CMOs) of any class that entitle the holder thereof to payments of principal and interest to be derivatives for that purpose (other than Private Label mortgage-backed securities the principal payments of which at the time of purchase by the Fund (i) are not limited by a schedule of principal distributions and (ii) support a schedule of principal distributions for another related class of Private Label mortgage-backed securities).

Stripped mortgage-backed securities (“SMBSs”) are classes of mortgage-backed securities that receive different proportions of the interest and principal distributions from the underlying pool of mortgage assets. SMBSs may be issued by agencies or instrumentalities of the United States government or by private mortgage lenders. A common type of SMBS will have one class that receives some of the interest and most of the principal from the mortgage assets, while the other class will receive most of the interest and the remainder of the principal.

An IO is an SMBS that is entitled to receive all or a portion of the interest, but none of the principal payments, on the underlying mortgage assets; a PO is an SMBS that is entitled to receive all or a portion of the principal payments, but none of the interest payments, on the underlying mortgage assets. The Investment Adviser believes that investments in POs may facilitate its ability to manage the price sensitivity of the Fund’s investments to interest rate changes. Generally, the yields to maturity on both IO and PO classes are extremely sensitive to the rate of principal payments (including prepayments) on the underlying mortgage assets. If the underlying mortgage assets of an IO class of mortgage-backed security held by the Fund experience greater than anticipated prepayments of principal, the Fund may fail to recoup fully its initial investment in such securities even though the securities are rated in the highest rating category. The Investment Adviser believes that, since principal amortization on PAC Bonds is designed to occur at a predictable rate, IOs and POs that are PAC Bonds generally are not as sensitive to principal prepayments as other IOs and POs.

SAI-7

Mortgage-backed securities that constitute inverse floating rate obligations are mortgage-backed securities on which the interest rates adjust or vary inversely to changes in market interest rates. Typically, an inverse floating rate mortgage-backed security is one of two components created from a pool of fixed rate mortgage loans. The other component is a variable rate mortgage-backed security, on which the amount of interest payable is adjusted directly in accordance with market interest rates. The inverse floating rate obligation receives the portion of the interest on the underlying fixed-rate mortgages that is allocable to the two components and that remains after subtracting the amount of interest payable on the variable rate component. The market value of an inverse floating rate obligation will be more volatile than that of a fixed-rate obligation and, like most debt obligations, will vary inversely with changes in interest rates. Certain of such inverse floating rate obligations have coupon rates that adjust to changes in market interest rates to a greater degree than the change in the market rate and accordingly have investment characteristics similar to investment leverage. As a result, the market value of such inverse floating rate obligations is subject to greater risk of fluctuation than other mortgage-backed securities, and such fluctuations could adversely affect the ability of the Fund to achieve its investment objectives and policies.

The yields on certain of the above mortgage-backed securities may be more sensitive to changes in interest rates than GNMA mortgage-backed securities. While the respective Investment Adviser will seek to limit the impact of these factors on the Fund, no assurance can be given that it will achieve this result.

Information on Directors and Executive Officers

The overall management of the business and affairs of the Fund is vested in the Board. The Board approves all significant agreements between the Fund and persons or companies furnishing services to it, including the Fund’s agreements with the Investment Adviser, Administrator, Distributor, Custodian and Transfer Agent. The day-to-day operations of the Fund have been delegated to UBS Trust Company of Puerto Rico (the “Administrator”), in its capacity as Administrator, subject to the Fund’s investment objective and policies and to general supervision by the Board.

The Board

The Board consists of seven Directors. Six of these are not “interested persons,” as defined in Section 2(a)(19) of the 1940 Act (the “Independent Directors”), and one is considered an “interested person” of the Fund as a result of his employment as an officer of the Fund, the Fund’s Investment Adviser or an affiliate thereof (the “Interested Director”). The number of members of the Fund’s Board may be changed by resolution of the Board.

Committees of the Board

The Board has three standing committees: the Audit Committee, the Dividend Committee and the Nominating Committee.

Audit Committee. The Board has adopted a written Audit Committee Charter, and the role of the Audit Committee is to oversee the Fund’s accounting and financial reporting policies and practices and to recommend to the Board any action to ensure that the Fund’s accounting and financial reporting are consistent with accepted accounting standards applicable to the mutual fund industry. The Audit Committee has three members, Messrs. Cabrer, León and Pellot, all of whom are Independent Directors. The Independent Directors who are Audit Committee members are represented by independent legal counsel in connection with their duties. Mr. León serves as an audit committee financial expert. The Audit Committee met nine (9) times during the fiscal year ended June 30, 2021.

Dividend Committee. The role of the Dividend Committee is to determine the amount, form, and record date of any dividends to be declared and paid by the Fund. The Dividend Committee has three members, two of whom are Independent Directors (Messrs. Cabrer, and Pellot) and one who is an Interested Director (Mr. Ubiñas). The Dividend Committee did not meet during the fiscal year ended June 30, 2021. The Dividend Committee sets dividends by Unanimous Consent.

Nominating Committee. Pursuant to the adoption of a written charter, the Fund has created a Nominating Committee. The principal responsibilities of the Nominating Committee are to identify individuals qualified to serve as Independent Directors and to recommend its nominees for consideration by the full Board. The Nominating Committee has three members, all of whom are Independent Directors (currently, Messrs. Cabrer, Nido and Pellot). The Independent Directors who are Nominating Committee members are represented by independent legal counsel in connection with their duties. While the

SAI-8

Nominating Committee is solely responsible for the selection and nomination of the Independent Directors, the Nominating Committee may consider nominations for the office of Director made by Fund shareholders as it deems appropriate. Shareholders who wish to recommend a nominee should send nominations to the Fund’s Secretary that include biographical information and set forth the qualifications of the proposed nominee. The Nominating Committee evaluates nominees from whatever source using the same standard. The Nominating Committee met three (3) time during the fiscal year ended June 30, 2021.

Independent Directors

Certain biographical and other information relating to the Independent Directors is set forth below, including their ages and their principal occupations for at least five (5) years.

Messrs. Nido and Pellot and Mrs. Pérez are members of the boards of directors of all funds that have engaged UBS AMPR as their investment adviser (the “UBS Advised Funds”) or as their co-investment adviser (the “UBS Co-Advised Funds” and, together with the UBS Advised Funds, the “Affiliated Funds” or the “Fund Complex”). Messrs. Cabrer, León and Villamil are members solely of the board of directors of each of the UBS Advised Funds.

| Name (Age) and Address* |

Position (s) Held with the Fund |

Term of Office and Time Served** |

Principal Occupation(s) During Past Five Years |

Number of Affiliated Funds Overseen |

Public Directorships (other than the Affiliated Funds) | |||||

| Agustin Cabrer (72) | Director | Director since 2005 | President of Antonio Roig Sucesores (land holding enterprise with commercial properties) since 1995; President of Libra Government Building, Inc. (administration of court house building) since 1997; President of Cabrer Consulting (financial services business); President of CC Development, LLC (construction supervision and management consulting) for the last five years; President of CC Development, LLC (construction supervision and management consulting) since 2021; and Director of V. Suarez & Co. (food and beverage distribution company) since 2002. | 18 funds consisting of 29 portfolios | None | |||||

| Vicente León (82) | Director | Director since 2021 | Independent business consultant since 1999. | 18 funds consisting of 29 portfolios | None | |||||

| Carlos Nido (57) | Director | Director since 2007 | President of Green Isle Capital LLC (a Puerto Rico venture capital fund under law 185 investing primarily in feature films and healthcare) since 2016. | 25 funds consisting of 36 portfolios | None | |||||

| Luis M. Pellot (73) | Director | Director since 2005 | President of Pellot-González, Tax Attorneys & Counselors at Law, PSC (legal services business) since 1989. | 25 funds consisting of 36 portfolios | None | |||||

| Clotilde Pérez (69) | Director | Director since 2009 | Vice President Corporate Development Officer of V. Suarez & Co., Inc. (food and beverage wholesale distribution business) since 1999. | 25 funds consisting of 36 portfolios | None | |||||

| José J. Villamil (81) |

Director | Director since 2021 | Chairman of the Board and Chief Executive Officer of Estudios Técnicos, Inc. (consulting business) since 2005. | 18 funds consisting of 29 portfolios | None |

| * | The address of the Independent Directors is c/o UBS Trust Company of Puerto Rico — 250 Muñoz Rivera Avenue, Tenth Floor, San Juan, Puerto Rico 00918. |

| ** | Each Independent Director serves until his successor is elected and qualified, or until his death or resignation, or removal as provided in the Fund’s By-Laws or charter or by statute, or until December 31 of the year in which he turns 85. |

Interested Directors and Officers

Certain biographical and other information relating to the Interested Director(s) and to the officers of the Fund, is set forth below, including their ages, their principal occupations for at least the last five years, the length of time served, and the total number of Affiliated Funds overseen by them. These persons also serve as directors and officers of the UBS Advised Funds and, in some cases, of certain of the UBS Co-Advised Funds.

SAI-9

| Name (Age) and Address* |

Position(s) Held with the Fund |

Term of Office and Length of Time Served** |

Principal Occupation(s) During Past Five Years |

Number of Affiliated Funds Overseen |

Public Funds) | |||||

| Carlos V. Ubiñas (67) | Director, Chairman of the Board and President | President since 2015; Director and Chairman of the Board since 2005 | Managing Director, Head Asset Management and Investment Banking of UBS Financial Services Inc. since 2014; former Chief Operating Officer and Executive Vice President of UBS Financial Services Inc. from 1989 to 2005. | 18 funds consisting of 29 portfolios | None | |||||

| Leslie Highley, Jr. (74) | Senior Vice President and Treasurer | Senior Vice President since 2005 | Managing Director of UBS Trust PR; Senior Vice-President of UBS Financial Services Inc.; Senior Vice President of the Puerto Rico Investors Tax-Free Family of Funds; President of Dean Witter Puerto Rico, Inc. since 1989 and Executive Vice President of the Government Development Bank for Puerto Rico. | N/A | None | |||||

| Javier Rodriguez (48) | Assistant Vice President and Assistant Treasurer | Assistant Vice President and Assistant Treasurer since 2005 | Divisional Assistant Vice President, trader, and portfolio manager of UBS Trust PR since 2003; financial analyst with UBS Trust PR from 2002 to 2003; financial analyst with Popular Asset Management from 1998 to 2002. | N/A | None | |||||

| Liana Loyola (60) | Secretary | Secretary since 2014 | Attorney in private practice since 2009. Previously, she practiced law at a firm focusing on commercial litigation and corporate law and held various positions in the government and the private sectors. Ms. Loyola holds a B.A., magna cum laude, from the University of Puerto Rico - Mayagüez; M.A.L.D. from The Fletcher School of Law and Diplomacy, Tufts / Harvard Universities, and a J.D. from the University of Puerto Rico School of Law. Ms. Loyola is admitted to practice law in the Commonwealth of Puerto Rico, the U.S. District Court for the District of Puerto Rico, and the U.S. Court of Appeals for the First Circuit. | N/A | None | |||||

| Luz Colon (46) | Chief Compliance Officer | Chief Compliance Officer since 2013 | Mrs. Colon is an Executive Director and Chief Compliance Officer of UBS Asset Managers of Puerto Rico, and the Funds. Mrs. Colon served as Co-CCO for the Puerto Rico Investors Family of Funds which is co-managed by UBS Asset Managers of Puerto Rico and Banco Popular of Puerto Rico from 2013 to 2021. She began her career in the securities industry in 1997 with responsibilities that included supervisory and control and risk management roles. She earned her B.B.A. in Accounting from the University of Puerto Rico and her JD from the Inter American University of Puerto Rico, School of Law. She is admitted to practice law in the Commonwealth of Puerto Rico. Mrs. Colon received the Certified Regulatory and Compliance Professional (CRCP) designation from the FINRA Institute at Wharton School. | N/A | None | |||||

| Heydi Cuadrado (41) | Assistant Vice President | Assistant Vice President since 2019 | Director of UBS Trust Company since March 2012. Trader and Assistant Portfolio Manager for UBS Asset Managers since 2008. Joined UBS Trust Company in 2003. | N/A | None | |||||

| Gustavo Romañach (47) | Assistant Vice President | Assistant Vice President since 2019 | Director of UBS Asset Managers since 2013; Associate Director Portfolio analyst & trader of UBS Asset Managers since 2009; Assistant Vice-President of UBS Asset Managers since 2003. | N/A | None |

| * | The address of the Interested Director(s) and Officers of the Fund is c/o UBS Trust Company of Puerto Rico, American International Plaza - Tenth Floor, 250 Muñoz Rivera Avenue, San Juan, Puerto Rico 00918. |

| ** | Each Director serves until his successor is elected and qualified, or until his death or resignation, or removal as provided in the Fund’s by-laws or charter or by statute, or until December 31 of the year in which he or she turns 85. Each officer is elected by and serves at the pleasure of the Board. |

Board Diversification and Director Qualifications.

In determining that a particular director was qualified to serve on the Board, the Board has considered each director’s background, skills, experience and other attributes in light of the composition of the Board with no particular factor controlling. The Board believes that directors need to have the ability to critically review, evaluate, question and discuss information provided to them, and to interact effectively with Fund management, service providers and counsel, in order to exercise effective business judgment in the performance of their duties, and the Board believes each director satisfies this standard. An effective director may achieve this ability through his or her educational background; business, professional training or practice;

SAI-10

public service or academic positions; experience from service as a board member or executive of investment funds, public companies or significant private or not-for-profit entities or other organizations; and/or other life experiences. Accordingly, set forth below is a summary of the experiences, qualifications, attributes, and skills that led to the conclusion, as of the date of this document, that each director should continue to serve in that capacity. References to the experiences, qualifications, attributes and skills of directors are pursuant to requirements of the SEC, do not constitute holding out of the Board or any director as having any special expertise or experience and shall not impose any greater responsibility or liability on any such person or on the Board by reason thereof.

Luis M. Pellot. Mr. Pellot has been the President of Pellot-González, Tax Attorneys & Counselors at Law, PSC since 1989. He is also a member of the Puerto Rico Bar Association, Puerto Rico Manufacturers Association, Puerto Rico Chamber of Commerce, Puerto Rico General Contractors Association, Puerto Rico Hotel & Tourism Association and Hispanic National Bar Association and President of Tax Committee, Puerto Rico Chamber of Commerce from 1996 to 1997. He has been an Independent Director and member of the Audit Committee of the UBS Family of Funds since 2002.

Agustin Cabrer. Mr. Cabrer was the President of Starlight Development Group, Inc., a real estate development company, from 1995 to 2014. He is also the President of Antonio Roig Sucesores since 1995 (real estate development), a Partner of Desarrollos Roig since 1995, Desarrollos Agricolas del Este S.E. since 1995, and El Ejemplo, S.E. since 1995 (real estate development). He is also a Partner, Pennock Growers, Inc. since 1998, Partner and Managing Director of RERBAC Holdings, LLP since 2004 (real estate development), Director of V. Suarez & Co. since 2002, V. Suarez Investment Corporation since 2002, V. Suarez International Banking Entity, Inc. since 2002, Villa Pedres, Inc. since 2002, and Caparra Motor Service since 1998, Director of TC Management from 2002 to 2013, Officer of Candelero Holdings & Management, Inc. from 2001 to 2013, 100% owner, President and Registered Principal (Agent) of Starlight Securities Inc. since 1995 (registered broker-dealer), former Member of the Board of Trustees of the University of Puerto Rico, Partner and Officer of Grupo Enersol, LLC since 2013 (solar photovoltaic developer), President of Libra Government Building, Inc. since 1997, Partner of Cometa 74, LLC since 1998, Vice-President of Candelario Point Partners, Inc. since 1998 and Officer of Marbella Development, Corp. from 2001 to 2014.

Vicente J. León. Mr. León has been an Independent Director of the Funds from 2008 to 2019 and since 2021, he oversees 18 funds consisting of 29 portfolios. For the past five years, Mr. León is an independent business consultant and in 2020 and early 2021 was a consultant to the Audit Committee of the Funds. He is a former Member and Vice Chairman of the Board of Directors and Chairman and Financial Expert of the Audit Committee of Triple S Management Corp. (a Public Company) from 2000 to 2012, past president of the Puerto Rico Society of Certified Public Accountants and a former Partner at KPMG LLP.

Carlos Nido. Mr. Nido has been the President of Green Isle Capital LLC, a Puerto Rico Venture Capital Fund under law 185 investing primarily in feature films and healthcare, since 2015. He is also President and Executive Producer of Piñolywood Studios LLC. He also serves as a member of the Board of Grupo Ferré Rangel, GFR Media, LLC, the UBS Puerto Rico family of Mutual Funds, B. Fernández & Hnos. Inc., Puerto Rico Ambulatory Surgery Center, and the San Jorge Children’s Foundation; Member of the Advisory Board of Advent Morro Private Equity Funds. Former Senior Vice President of Sales of El Nuevo Día, President of Del Mar Events. He is the former President and founder of Virtual, Inc. and Zona Networks and General Manager of Editorial Primera Hora from 1997 until 1999.

Clotilde Pérez. Ms. Perez has been the Vice President Corporate Development Officer of V. Suarez & Co., Inc. since 1999; former Member of the Board of Trustee of the University of the Sacred Heart from 2005 to 2019; Member of the Board of Directors of Campofresco Corp. since 2012; former Member of the Board of Directors of Grupo Guayacan, Inc., EnterPrize, Inc. and Puerto Rico Venture Forum from 1999 to 2013; Vice President Venture Capital, PR Economic Development Bank from 1993-1996; and Associate Professor of Finance, University of Puerto Rico, Río Piedras Campus from 1987-1992.

Joaquin Villamil. Mr. Villamil is Chairman of the Board and Chief Executive Officer of Estudios Técnicos, Inc.; Member of the Board of Governors of United Way of Puerto Rico; Chairman of the Puerto Rico Manufacturer’s Association’s Committee on Competitiveness; Chairman of the Board of BBVA-PR from 1998 to 2012; founding Director of the Puerto Rico Community Foundation and the Aspen Institute’s Non-Profit Sector Research Fund; former Member of the New York Federal Reserve Bank’s Community Affairs Roundtable; former President of the Puerto Rico Chamber of Commerce, as well as former Chairman of its Economic Advisory Council; former President of the Inter-American Planning Society; former President of the Puerto Rico Economics Association; former Chairman of the Puerto Rico-2025 Commission (formerly, Alianza para el Desarrollo); former Chairman of the Commission on the Economic Future of Puerto Rico; former professor of the Economics Department of the University of Pennsylvania’s Wharton School and Graduate School of Arts and Sciences and former

SAI-11

Professor of Planning at the University of Puerto Rico. Mr. Villamil has served on numerous Boards such as, the Boards of the Ponce School of Medicine, St. John’s School and the Ana G. Méndez University System, the Board of the National Puerto Rican Coalition in Washington, and on the Board of Economists of Hispanic Business. In 2009, Mr. Villamil was appointed as a Member of the Economic Advisory Council as well as Chairman of the Strategic Planning Committee of the State Human Resources and Occupational Development Council; Director of UBS Family of Funds from 2013-2019.

Carlos V. Ubiñas. Mr. Ubiñas has been the Chief Executive Officer of UBS Financial Services Inc. since 2009. He has also been the President of UBS Financial Services Inc. since 2005 and the Managing Director, Head Asset Management and Investment Banking of UBS Financial Services Inc. since 2014. He is the former Chief Operating Officer and Executive Vice President of UBS Financial Services Inc. from 1989 to 2005.

Leadership Structure and Oversight Responsibilities of the Board

The Board is responsible for overseeing the Adviser’s management and operations of the Fund pursuant to the Advisory Agreement. Directors also have significant responsibilities under the federal securities laws. Among other things, they

| ● | oversee the performance of the Fund; |

| ● | monitor the quality of the advisory and shareholder services provided by the Investment Adviser; |

| ● | review annually the fees paid to the Investment Adviser for its services; |

| ● | monitor potential conflicts of interest between the Fund and the Investment Adviser; |

| ● | monitor distribution activities, custody of assets and the valuation of securities; and |

| ● | oversee the Fund’s compliance program. |

In performing their duties, Directors receive detailed information about the Fund and the Investment Adviser on a regular basis, and meet at least quarterly with management of the Investment Adviser to review reports relating to the Fund’s operations. The Directors’ role is to provide oversight and not to provide day-to-day management.

The Chairman of the Board is an interested person of the Fund as that term is defined under Section 2(a)(19) of the 1940 Act because of his affiliation with the Investment Adviser. The remaining Directors and their immediate family members have no affiliation or business connection with the Investment Adviser, the Fund’s principal underwriter or any of their affiliated persons and do not own any stock or other securities issued by the Investment Adviser or the Fund’s principal underwriter.

Mr. Ubiñas, the Chairman of the Board, is an Interested Director because of his affiliation with the Investment Adviser. The Independent Directors have not designated a lead Independent Director, but the Chairman of the Audit Committee, Agustin Cabrer, generally acts as chairman of meetings or executive sessions of the Independent Directors and, when appropriate, represents the views of the Independent Directors to management. The Board has determined that its leadership structure is appropriate for the Fund because it enables the Board to exercise informed and independent judgment over matters under its purview, allocates responsibility among committees in a manner that fosters effective oversight and allows the Board to devote appropriate resources to specific issues in a flexible manner as they arise. The Board periodically reviews its leadership structure as well as its overall structure, composition and functioning and may make changes in its discretion at any time.

Risk Oversight by the Board

As mentioned above, the Board oversees the management of the Fund and meets at least quarterly with management of the Investment Adviser to review reports and receive information regarding the Fund’s operations. Risk oversight relating to the Fund is one component of the Board’s oversight and is undertaken in connection with the duties of the Board. As described above, the Board’s committees assist the Board in overseeing various types of risks relating to the Fund. The Board receives reports from committees regarding their areas of responsibility and, through those reports and its interactions with management of the Investment Adviser during and between meetings, analyzes, evaluates, and provides feedback on the Investment Adviser’s risk management process. In addition, the Board receives information regarding, and has discussions with senior management of the Investment Adviser about, the Investment Adviser’s risk management systems and strategies. The Fund’s Chief Compliance Officer (“CCO”) reports to the Board at least quarterly regarding compliance and legal risk concerns. In addition to quarterly reports, the CCO provides an annual report to the Board in accordance with the Fund’s compliance policies and procedures. The CCO regularly discusses relevant compliance and legal risk issues affecting the Fund

SAI-12

during meetings with the Independent Directors. The CCO updates the Board on the application of the Fund’s compliance policies and procedures and discusses how they mitigate risk. The CCO also is in charge of reporting to the Board regarding any problems associated with the Fund’s compliance policies and procedures that could expose the Funs to risk. There can be no assurance that all elements of risk, or even all elements of material risk, will be disclosed to or identified by the Board.

Compensation of Directors

Each Independent Director receives a stipend from the Fund of up to $1,000 plus expenses, for attendance at each meeting of the Board, and $500 plus expenses, for attendance at each meeting of a committee of the Board. The Independent Directors do not receive retirement or other benefits as part of their compensation. The following table sets forth the compensation earned by the Independent Directors from the Fund for the fiscal year ended June 30, 2021 and the total compensation paid to them by the Affiliated Funds for the calendar year ended December 31, 2021.

| Name of Independent Director |

Aggregate Compensation from Fund |

Retirement Benefits Accrued |

Annual Benefits Upon Retirement |

Total Compensation from Affiliated Funds Paid to Independent Directors | ||||

| Luis M. Pellot(1)(2) |

$6,722 | N/A | N/A | $152,031 | ||||

| Vicente J. León(3)(4)(5) |

$0 | N/A | N/A | $0 | ||||

| Agustin Cabrer(2)(3) |

$6,722 | N/A | N/A | $120,481 | ||||

| Carlos Nido(1) |

$4,194 | N/A | N/A | $105,596 | ||||

| Clotilde Pérez (1) |

$4,194 | N/A | N/A | $112,396 | ||||

| Joaquin J. Villamil(3)(4)(5) |

$0 | N/A | N/A | $0 |

| (1) | Independent Director who also serves on the boards of the twenty-five Affiliated Funds. |

| (2) | Independent Director who serves on the Audit Committee of each Affiliated Fund. |

| (3) | Independent Director who also serves on the boards of the eighteen UBS Advised Funds. |

| (4) | As provided in the Fund’s Bylaws as of that date, Director retired at the end of the calendar year upon reaching eighty (80) years of age. Fund bylaws have been amended to allow Directors to hold their positions until reaching eighty -five (85) years of age. |

| (5) | Messrs. Villamil and León were appointed to the Board of Directors on May 18, 2021 and May 13, 2021, respectively. |

Beneficial Ownership of Equity Securities in the Fund and Affiliated Funds by Each Director

The following table sets forth the dollar range of equity securities beneficially owned by each director as of December 31, 2021:

| Name of Director |

Dollar Range of Equity Securities in the Fund |

Aggregate Dollar Range of Equity Securities in All Registered Investment Companies Overseen by Director in Affiliated Funds (including funds in the Fund Complex) | ||

| Luis M. Pellot |

None | None | ||

| Vicente J. León |

$1–10,000 | $1–10,000 | ||

| Agustin Cabrer |

None | None | ||

| Clotilde Pérez |

None | None | ||

| Carlos Nido |

None | $10,001 –$50, 000 | ||

| Joaquin Villamil |

None | None | ||

| Carlos V. Ubiñas |

Over $100,000 | Over $100,000 |

As of April 12, 2022, the directors of the Fund as a group beneficially owned an aggregate of less than 1% of the Fund’s outstanding Shares. As of December 31, 2021, based on information provided by each of the Independent Directors, none of the Independent Directors or their immediate family members owned beneficially or of record any securities of the

SAI-13

Investment Adviser, the Fund’s principal underwriter or any person (other than a registered investment company) directly or indirectly controlling, controlled by or under common control with such entities.

None of the directors and officers of the Fund have entered into any material transactions with the Fund during the last two calendar years; provided, however, that certain of the directors and officers of the Fund are employees of entities which have entered into material agreements with the Fund, as described herein.

Indemnification of Directors and Officers

The Fund has obtained directors’ and officers’ liability insurance for its directors and officers. The Fund’s certificate of incorporation contains a provision that exempts directors from personal liability for monetary damages to the Fund or its shareholders for violations of the duty of care, to the fullest extent permitted by the Puerto Rico General Corporation Law. The Fund has also agreed to indemnify its directors and officers for certain liabilities to the fullest extent permitted by Puerto Rico law. Pursuant to Section 17(h) of the 1940 Act, such indemnification of the Directors would not protect a Director from liability to the Funds or their shareholders from liability that the Director would otherwise be subject to by reason of such Director’s own bad faith, willful misfeasance, gross negligence or reckless disregard of his or her duties as a Director.

Management, Advisory and Other Service Arrangements

Investment Advisory Arrangements

Subject to the oversight of the Board, investment advisory services are provided to the Fund by the Investment Adviser, UBS Asset Managers of Puerto Rico, a division of UBS Trust Company of Puerto Rico, pursuant to an investment advisory contract (the “Advisory Agreement”). As compensation for its investment advisory services and pursuant to the Advisory Agreement, the Fund pays the Investment Adviser an advisory fee at an annual rate of 0.50% of its average monthly net assets.

As of March 31, 2022, the Investment Adviser serves as investment adviser or co-investment adviser to funds with combined portfolio assets of approximately $2.0 billion. UBS Trust Company of Puerto Rico, an affiliate of the Fund and UBS Financial Services Inc., is a trust company organized and validly existing under the laws of Puerto Rico.

The following table sets forth the management fee paid by the Fund for the last three fiscal years:

| Management Fee Net of |

Expense Reimbursement | |||

| Fiscal year ended June 30, 2021 |

$ 1,698,281 | $ 2,563,486 | ||

| Fiscal year ended June 30, 2020 |

$ 1,082,985 | $ 0 | ||

| Fiscal year ended June 30, 2019 |

$ 1,114,807 | $ 360,081 |

Pursuant to the Advisory Agreement, the Investment Adviser is not liable for any loss, expense, cost, or liability arising out of any error in judgment or any action or omission, including any instruction given to the Fund’s custodian unless (i) such action or omission involved an officer, director, employee, or agent of the Investment Adviser, and (ii) such loss, expense, cost, or liability arises out of the Investment Adviser’s gross negligence, willful malfeasance, bad faith or reckless disregard of the Investment Adviser’s duties. The Investment Adviser may rely on any notice or communication (written or oral) reasonably believed by it to be genuine. These limitations shall not act to relieve the Investment Adviser from any responsibility or liability for any responsibility, obligation or duty that the Investment Adviser may have under state statutes, the laws of Puerto Rico, or any federal securities law which is not waivable.

Unless earlier terminated as described below, the Advisory Agreement is initially in effect for a period of two years from the date of execution and will remain in effect from year to year thereafter if approved annually by a vote of a majority of the Independent Directors. The Advisory Agreement provides that it will terminate automatically if assigned (as defined in the 1940 Act). The Advisory Agreement also provides that it may be terminated without penalty (i) at any time by a unanimous vote of the Independent Directors, (ii) on 60 days’ written notice by the Investment Adviser or (iii) on 60 days’ written notice to the Investment Adviser by the vote of a majority of the outstanding voting securities of the Fund.

SAI-14