Form 497 NORTHERN LIGHTS FUND

Tweet

Tweet Share

Share

Pinnacle Sherman Multi-Strategy Core Fund

Class A Shares APSHX

Class C Shares CPSHX

Class I Shares IPSHX

PROSPECTUS

February 1, 2023

| Adviser: | |

| Pinnacle Family Advisors, LLC | |

| 620 W. Republic Road, Suite 104 | |

| Springfield, MO 65807 |

| www.pinnacledynamicfunds.com | 1-888-985-9830 |

This Prospectus provides important information about the Fund that you should know before investing. Please read it carefully and keep it for future reference.

These securities have not been approved or disapproved by the Securities and Exchange Commission nor has the Securities and Exchange Commission passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

Table of Contents

| FUND SUMMARY | 1 | |

| Investment Objective | 1 | |

| Fees and Expenses of the Fund | 1 | |

| Principal Investment Strategies | 2 | |

| Principal Investment Risks | 2 | |

| Performance | 4 | |

| Investment Adviser | 5 | |

| Portfolio Managers | 5 | |

| Purchase and Sale of Fund Shares | 5 | |

| Tax Information | 5 | |

| Payments to Broker-Dealers and Other Financial Intermediaries | 5 | |

| ADDITIONAL INFORMATION ABOUT PRINCIPAL INVESTMENT STRATEGIES AND RELATED RISKS | 6 | |

| Investment Objective | 6 | |

| Principal Investment Strategies | 6 | |

| Principal Investment Risks | 7 | |

| Temporary Investments | 10 | |

| Portfolio Holdings Disclosure | 10 | |

| Cybersecurity | 10 | |

| MANAGEMENT | 11 | |

| Investment Adviser | 11 | |

| Portfolio Managers | 11 | |

| HOW SHARES ARE PRICED | 12 | |

| HOW TO PURCHASE SHARES | 13 | |

| HOW TO REDEEM SHARES | 18 | |

| FREQUENT PURCHASES AND REDEMPTIONS OF FUND SHARES | 20 | |

| TAX STATUS, DIVIDENDS AND DISTRIBUTIONS | 21 | |

| DISTRIBUTION OF SHARES | 22 | |

| Distributor | 22 | |

| Distribution Fees | 22 | |

| Additional Compensation to Financial Intermediaries | 22 | |

| Householding | 22 | |

| FINANCIAL HIGHLIGHTS | 23 | |

| PRIVACY NOTICE | 26 |

i

FUND SUMMARY

Investment Objective:

The Fund seeks high total return with reasonable risk.

Fees and Expenses of the Fund:

This table describes the fees and expenses that you may pay if you buy, hold and sell shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the table and example below. You may qualify for sales charge discounts on purchases of Class A shares if you and your family invest, or agree to invest in the future, at least $25,000 in the Fund. More information about these and other discounts is available from your financial professional and in How to Purchase Shares on page 13 of this Prospectus.

Shareholder Fees |

Class A | Class C | Class I |

| Maximum

Sales Charge (Load) Imposed on purchases (as a percentage of offering price) |

5.75% | None | None |

| Maximum

Deferred Sales Charge (Load) (as a percentage of purchase price) |

None | None | None |

| Redemption

Fee (as a % of amount redeemed if held less than 60 days) |

1.00% | 1.00% | 1.00% |

Annual Fund Operating Expenses | |||

| Management Fees | 1.00% | 1.00% | 1.00% |

| Distribution and Service (12b-1) Fees | 0.25% | 1.00% | None |

| Other Expenses | 0.59% | 0.60% | 0.56% |

| Acquired Fund Fees and Expenses(1) | 0.18% | 0.18% | 0.18% |

| Total Annual Fund Operating Expenses | 2.02% | 2.78% | 1.74% |

| Fee Waiver and Expense Reimbursement(2) | (0.35)% | (0.36)% | (0.32)% |

| Total Annual Fund Operating Expenses After Fee Waiver | 1.67% | 2.42% | 1.42% |

| (1) | Acquired Fund Fees and Expenses are the estimated indirect costs of investing in other investment companies. The operating expenses in this fee table will not correlate to the expense ratio in the Fund’s financial highlights because the financial statements include only the direct operating expenses incurred by the Fund. | |

| (2) | The Fund’s adviser, Pinnacle Family Advisors, LLC, (the “Adviser”) has contractually agreed to waive management fees and to make payments to limit Fund expenses until August 1, 2024 so that the Total Annual Operating Expenses After Fee Waiver and Reimbursement (excluding: (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions; (iii) acquired fund fees and expenses; (iv) borrowing costs (such as interest and dividend expense on securities sold short); (v) taxes; and (vi) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees, contractual indemnification of Fund service providers (other than the Adviser))) do not exceed 1.49%, 2.24% and 1.24% of average daily net assets attributable to Class A, C and I shares, respectively. These fee waivers and expense reimbursements are subject to possible recoupment from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved, within the foregoing expense limits. This agreement may be terminated only by the Board of Trustees on 60 days’ written notice to the Adviser. |

Example:

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based upon these assumptions your costs would be:

| Class | 1 Year | 3 Years | 5 Years | 10 Years |

| A | $735 | $1,140 | $1,570 | $2,762 |

| C | $245 | $828 | $1,437 | $3,083 |

| I | $145 | $517 | $914 | $2,025 |

Portfolio Turnover:

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its

portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when Fund shares are held

in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Fund’s

performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 1,127% of the average value of its portfolio.

1

Principal Investment Strategies:

The Fund seeks to meet its investment objective by investing, under normal market conditions, in all major asset classes including, but not limited to, foreign and domestic (i) equity securities of all market capitalizations, (ii) fixed income securities of any credit quality, and (iii) cash and cash equivalents. The Fund intends to generally invest in a mix of asset classes. The Fund may invest in individual securities or in exchange traded funds (“ETFs”), and may invest in emerging markets. The Fund actively trades its portfolio investments.

The Adviser uses signals that come from W.E. Sherman & Co. to determine the Fund’s equity, fixed income, and/or cash allocations. W.E. Sherman & Co. publishes “The Sherman Sheet,” a financial research newsletter and website for licensed financial professionals that provides model portfolios along with the supporting research, analysis and data for those portfolios under various market conditions. The Adviser analyzes several models on The Sherman Sheet to determine the Fund’s allocations.

The process for each model is similar: (1) the expected market trend for equity securities over a period is examined; (2) if equities are trending upward for the applicable period based on the market indicator, the assets allocated to the applicable model are invested in equities based on the relative strength rankings of a limited number of asset classes and sectors; and (3) if equities are trending downward based on the market indicator, the assets allocated to the applicable model are primarily invested in fixed income securities or cash as dictated by the applicable model. The Fund actively trades its portfolio investments.

Principal Investment Risks:

As with all mutual funds, there is a risk that you could lose money through your investment in the Fund. The Fund is not intended to be a complete investment program. Many factors affect the Fund’s net asset value (“NAV”) and performance. The following risks may apply to the Fund’s direct investments as well as the Fund’s indirect investments through ETFs.

| ● | Cash and Cash Equivalents Risk: When the Fund is out of the market and invests in cash and cash equivalents, there is a risk that the market will begin to rise rapidly, and the Fund will not be able to reinvest its cash positions into areas of the advancing market quickly enough to capture the initial returns of changing market conditions. | |

| ● | Credit Risk: Issuers may not make interest or principal payments on securities, resulting in losses to the Fund. In addition, the credit quality of securities held by the Fund may be lowered if an issuer’s financial condition changes. These risks are more pronounced for securities with lower credit quality, such as those rated below BBB- by Standard & Poor’s Ratings Group or another credit rating agency. | |

| ● | Derivatives Risk: The derivative instruments in which the Fund may invest either directly or through an underlying fund, may be more volatile than other instruments. The risks associated with investments in derivatives also include liquidity, interest rate, market, credit and management risks, mispricing or improper valuation. Changes in the market value of a derivative may not correlate perfectly with the underlying asset, rate or index, and the Fund could lose more than the principal amount invested. In addition, if a derivative is being used for hedging purposes there can be no assurance given that each derivative position will achieve a perfect correlation with the security or currency against which it is being hedged, or that a particular derivative position will be available when sought by the portfolio manager. | |

| ● | Emerging Market Risk: Investing in emerging markets involves not only the risks described below with respect to investing in foreign securities, but also other risks, including exposure to economic structures that are generally less diverse and mature, limited availability and reliability of information material to an investment decision, and exposure to political systems that can be expected to have less stability than those of developed countries. The market for the securities of issuers in emerging market typically is small, and a low or nonexistent trading volume in those securities may result in a lack of liquidity and price volatility. | |

| ● | Equity Risk: The NAV of the Fund will fluctuate based on changes in the value of the equity securities held by the underlying ETFs that invest in U.S. and/or foreign equity securities. Equity prices can fall rapidly in response to developments affecting a specific company or industry, or to changing economic, political or market conditions. | |

| ● | ETF Risk: ETFs are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. As a result, your cost of investing in the Fund will be higher than the cost of investing directly in ETFs and may be higher than other mutual funds that invest directly in securities. Each ETF is subject to specific risks, depending on its investments. | |

| ● | Fixed Income Risk: Typically, a rise in interest rates causes a decline in the value of fixed income securities. The value of fixed income securities typically falls when an issuer’s credit quality declines and may even become worthless if an issuer defaults. |

| ● | Foreign Currency Risk: Currency trading risks include market risk, credit risk and country risk. Market risk results from adverse changes in exchange rates in the currencies the Fund is long or short. Credit risk results because a currency-trade counterparty may default. Country risk arises because a government may interfere with transactions in its currency. |

2

| ● | Foreign Investment Risk: Foreign investing (including through American Depositary Receipts (“ADRs”), European Depositary Receipts (“EDRs”) and Global Depositary Receipts (“GDRs”)) involves risks not typically associated with U.S. investments, including adverse fluctuations in foreign currency values, adverse political, social and economic developments, less liquidity, greater volatility, less developed or less efficient trading markets, political instability and differing auditing and legal standards. Investing in emerging markets imposes different or greater risks than those associated with foreign developed countries. | |

| ● | High Yield (Junk) Bond Risk: Lower-quality fixed income securities, known as “high yield” or “junk” bonds, present greater risk than bonds of higher quality, including an increased risk of default. An economic downturn or period of rising interest rates could adversely affect the market for these bonds and reduce the Fund’s ability to sell its bonds. The lack of a liquid market for these bonds could decrease the Fund’s share price. |

| ○ | Defaulted Securities Risk: Repayment of defaulted securities and obligations of distressed issuers (including insolvent issuers or issuers in payment or covenant default, in workout or restructuring or in bankruptcy or in solvency proceedings) is subject to significant uncertainties. Investments in defaulted securities and obligations of distressed issuers are considered speculative. |

| ● | Issuer-Specific Risk: The value of securities of smaller issuers can be more volatile than those of larger issuers. The value of certain types of securities can be more volatile due to increased sensitivity to adverse issuer, political, regulatory, market, or economic developments. | |

| ● | Large Capitalization Risk: Large-capitalization companies may be less able than smaller capitalization companies to adapt to changing market conditions. Large-capitalization companies may be more mature and subject to more limited growth potential compared with smaller capitalization companies. During different market cycles, the performance of large capitalization companies has trailed the overall performance of the broader securities markets. | |

| ● | Management Risk: The Adviser’s judgment about the attractiveness, value and potential appreciation of particular asset classes and securities in which the Fund invests (long or short) may prove to be incorrect and may not produce the desired results. | |

| ● | Market and Geopolitical Risk: The increasing interconnectivity between global economies and financial markets increases the likelihood that events or conditions in one region or financial market may adversely impact issuers in a different country, region or financial market. Securities in the Fund’s portfolio may underperform due to inflation (or expectations for inflation), interest rates, global demand for particular products or resources, natural disasters, climate change and climate-related events, pandemics, epidemics, terrorism, international conflict, regulatory events and governmental or quasi-governmental actions. The occurrence of global events similar to those in recent years may result in market volatility and may have long term effects on both the U.S. and global financial markets. | |

| ● | Model Risk: Like all quantitative analysis, the investment model carries a risk that the model might be based on one or more incorrect assumptions or may not perform as expected. | |

| ● | Portfolio Turnover Risk: A higher portfolio turnover will result in higher transactional and brokerage costs. | |

| ● | Small and Medium Capitalization Risk: The value of small or medium capitalization companies may be subject to more abrupt or erratic market movements than those of larger, more established companies or the market averages in general. | |

| ● | Sovereign Debt Risk: The issuer of the foreign debt or the governmental authorities that control the repayment of the debt may be unable or unwilling to repay principal or interest when due, and the Fund may have limited recourse in the event of a default. The market prices of sovereign debt, and the Fund’s NAV, may be more volatile than prices of U.S. debt obligations and certain emerging markets may encounter difficulties in servicing their debt obligations. | |

| ● | U.S. Government Obligations Risk: U.S. Treasury obligations are backed by the “full faith and credit” of the U.S. government and generally have negligible credit risk. Securities issued or guaranteed by federal agencies or authorities and U.S. government-sponsored instrumentalities or enterprises may or may not be backed by the full faith and credit of the U.S. government. The Fund may be subject to such risk to the extent it invests in securities issued or guaranteed by federal agencies or authorities and U.S. government-sponsored instrumentalities or enterprises. |

3

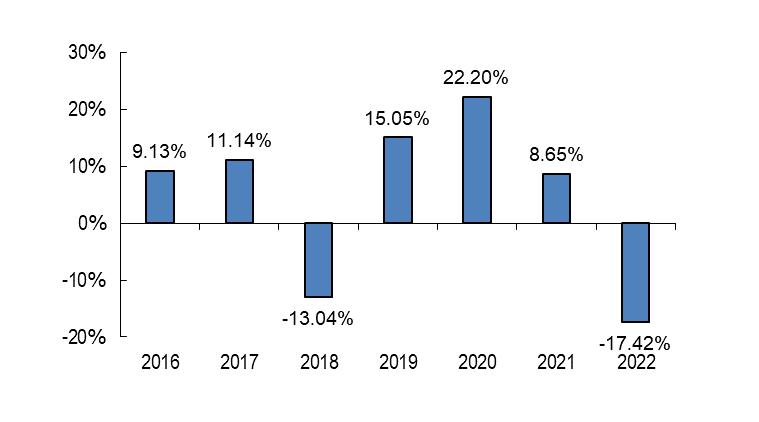

Performance:

The bar chart and performance table below show the variability of the Fund’s returns over time, which is some indication of the risks of investing in the Fund. The bar chart shows performance of the Fund’s Class I shares for each full calendar year since the Fund’s inception. The performance table compares the performance of the Fund’s shares over time to the performance of a broad-based market index. You should be aware that the Fund’s past performance (before and after taxes) may not be an indication of how the Fund will perform in the future. Although Class A and Class C shares have similar returns to Class I shares because the classes are invested in the same portfolio of securities, the returns for Class A and Class C shares are different from Class I shares because Class A and Class C shares have different expenses than Class I shares. Updated performance information is available at no cost by visiting www.pinnacledynamicfunds.com or by calling 1-888-985-9830.

Class I Performance Bar Chart For Calendar Years Ended December 31

| Best Quarter: | 12/31/20 | 11.74% |

| Worst Quarter: | 12/31/18 | (15.84)% |

Performance Table

Average Annual Total Returns

(For the periods ended December 31, 2022)

| One Year |

Five Years |

Since

Inception (10-1-15) | |

| Class I shares | |||

| Return before taxes | (17.42)% | 1.87% | 4.08% |

| Return after taxes on distributions | (17.42)% | 0.63% | 2.84% |

| Return after taxes on distributions and sale of Fund shares | (10.31)% | 1.17% | 2.84% |

| Class A shares | |||

| Return before taxes | (22.34)% | 0.44% | 2.97% |

| Class C shares | |||

| Return before taxes | (18.24)% | 0.85% | 3.03% |

| Dow

Jones Moderately Aggressive Portfolio Index(1) (reflects no deduction for fees, expenses or taxes) |

(15.59)% | 4.58% | 7.43% |

| (1) | Dow Jones Moderately Aggressive Portfolio Index® – A global benchmark that takes 80% of the risk of the global securities market. It is a total return index that is a time-varying weighted average of stocks, bonds, and cash. The Index is the efficient allocation of stocks, bonds, and cash in a portfolio with 80% of the risk of the Dow Jones Moderately Aggressive Portfolio Index. The Index is calculated on a total return basis with dividends reinvested. The Index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. |

After-tax returns were calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold shares of the Fund through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After tax returns for the share classes which are not presented will vary from the after-tax returns of Class I shares.

4

Investment Adviser: Pinnacle Family Advisors, LLC

Portfolio Managers: R. Sean McCurry is the Managing Member and President of the Adviser and Paul Carroll is the Chief Investment Officer and Chief Compliance Officer of the Adviser. Each has served the Fund as a portfolio manager since it commenced operations in October 2015.

Purchase and Sale of Fund Shares: You may purchase and redeem shares of the Fund on any day that the New York Stock Exchange is open for trading. The minimum initial investment is $2,000 for investors in Class A and Class C shares of the Fund and $1,000,000 for investors in Class I shares of the Fund. The minimum subsequent investment is $500 for Class A and Class C shares of the Fund and $5,000 for Class I shares of the Fund.

Tax Information: Dividends and capital gain distributions you receive from the Fund, whether you reinvest your distributions in additional Fund shares or receive them in cash, are taxable to you at either ordinary income or capital gains tax rates unless you are investing through a tax-deferred plan such as an IRA or 401(k) plan. However, these dividend and capital gain distributions may be taxable upon their eventual withdrawal from tax-deferred plans.

Payments to Broker-Dealers and Other Financial Intermediaries: If you purchase the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

5

ADDITIONAL INFORMATION ABOUT PRINCIPAL INVESTMENT STRATEGIES AND RELATED RISKS

Investment Objective:

The Fund seeks high total return with reasonable risk. The Fund’s investment objective may be changed by the Board of Trustees upon 60 days’ written notice to shareholders.

Principal Investment Strategies:

The Fund seeks to meet its investment objective by investing, under normal market conditions, in all major asset classes including, but not limited to, foreign and domestic (i) equity securities of all market capitalizations, (ii) fixed income securities of any credit quality, and (iii) cash and cash equivalents. The Fund intends to generally invest in a mix of asset classes. The Fund may invest in individual securities or in exchange traded funds (“ETFs”), and may invest in emerging markets. The Fund actively trades its portfolio investments.

The Adviser uses signals that come from W.E. Sherman & Co. to determine the Fund’s equity, fixed income, and/or cash allocations. W.E. Sherman & Co. publishes “The Sherman Sheet,” a financial research newsletter and website for licensed financial professionals that provides model portfolios along with the supporting research, analysis and data for those portfolios under various market conditions. The process for each model is similar and described in more detail below.

Simple Trend and Rank (STAR): On a daily basis the expected market trend for equities is examined using the Intermediate-Term Indicator. The Intermediate-Term Indicator is an algorithmic indicator that analyzes the closing prices of foreign and domestic equity securities to determine the trend in equity securities.

If the Intermediate-Term indicator status is showing that foreign and domestic equities are trending upward, OR if it is showing that either foreign or domestic equities is trending upward, the assets allocated to this model are invested in equities. If the Intermediate-Term indicator status is showing that foreign AND domestic equities are trending downward, the assets allocated to this model are invested in fixed income securities. This indicator may be applied on both a quarterly and/or daily basis.

Breakaway Stocks with Cash Directional Indicator: On a daily basis, the model examines the expected market trend for domestic equities using the Bull-Bear Indicator. The Bull-Bear Indicator is constructed from measurements of market analytics and is intended to reveal the relationship of supply and demand for a longer-term timeframe of typically 6 months or more under normal market conditions. The Bull-Bear Indicator uses market analytics such as up/down volume ratio (ratio of how much of an equity security’s trading volume for the day was during periods when the securities price was up versus when it was down); ratio of new 52-week highs to new 52-week lows; and advance/decline ratio (ratio of all equity securities that increased in value for the day to those that decreased in value).

As an added risk management tool, when the Bull-Bear Indicator is in Bull Status, the Fund may employ the Cash Directional Indicator to adjust the equity holdings determined above. The Cash Directional Indicator is driven by the relative strength of cash to certain equity asset classes and sectors.

If the Bull-Bear Indicator and the Cash Directional Indicator are positive (domestic equities are trending upward), at least 95% of the Fund’s assets are invested in individual equities and/or equity asset classes/sectors. If the Bull-Bear Indicator and Cash Directional Indicator are negative (domestic equities are trending downward), assets are invested in cash and/or cash equivalents. If the Bull-Bear Indicator and the Cash Directional Indicator are split, 0-50% of the Fund’s assets are invested in individual equities and/or equity asset classes/sectors, with the remaining assets invested in cash and/or cash alternatives. The Fund is invested in cash and/or cash alternatives when directed by the models except during periods that have historically shown a high probability of profit when invested in domestic equities based on the closing price of the S&P 500 over the history of the S&P 500, which are typically at the beginning and end of calendar months and shortly before holidays.

Long Cash: On a daily basis, the expected market trend for domestic equities is examined using the Short-Term Indicator. The Short-Term Indicator is constructed by examining sector analytics within 36 sub-sectors of the US market, and is intended to reveal the relationship of supply and demand for a short-term timeframe of typically 6 weeks to 6 months under normal market conditions. The Short-Term Indicator examines sector analytics, which includes looking at the number of sectors experiencing an uptrend in value versus those experiencing a downtrend in value as compared to the same ratio during the prior period.

If the Short-Term Indicator is positive (domestic equities are trending upward), then assets allocated to this model are invested in equity securities. If the Short-Term Indicator is negative (domestic equities are trending downward), and is confirmed by further price decline in the S&P 500, the assets allocated to this model are invested in cash and/or cash equivalents.

Buy/Replace with Cash Directional Indicator: On a daily basis the expected market trend for equity securities is examined using the Cash Directional Indicator. The Cash Directional Indicator is driven by the relative strength of cash as compared to the equity markets. If this indicator is positive, then assets allocated to this model are invested in equity securities. If this indicator is negative, then assets allocated to this model will be invested in cash and/or cash equivalents.

6

Principal Investment Risks:

The following section summarizes the principal risks of the Fund. These risks could adversely affect the NAV, total return and the value of the Fund and your investment. The risk descriptions below provide a more detailed explanation of the principal investment risks that correspond to the risks described in the “Fund Summary” section of this Prospectus.

| ● | Cash and Cash Equivalents Risk: When the Fund is out of the market and invests in cash and cash equivalents, there is a risk that the market will begin to rise rapidly, and the Fund will not be able to reinvest its cash positions into areas of the advancing market quickly enough to capture the initial returns of changing market conditions. | |

| ● | Credit Risk: There is a risk that issuers and counterparties will not make payments on securities and other investments held by the Fund, resulting in losses to the Fund. In addition, the credit quality of securities held by the Fund may be lowered if an issuer’s financial condition changes. Lower credit quality may lead to greater volatility in the price of a security and in shares of the Fund. Lower credit quality also may affect liquidity and make it difficult for the Fund to sell the security. Default, or the market’s perception that an issuer is likely to default, could reduce the value and liquidity of securities held by the Fund, thereby reducing the value of your investment in Fund shares. In addition, default may cause the Fund to incur expenses in seeking recovery of principal or interest on its portfolio holdings. Credit risk also exists whenever the Fund enters into a foreign exchange or derivative contract, because the counterparty may not be able or may choose not to perform under the contract. When the Fund invests in foreign currency contracts, or other over-the-counter derivative instruments (including options), it is assuming a credit risk with regard to the party with which it trades and also bears the risk of settlement default. These risks may differ materially from risks associated with transactions effected on an exchange, which generally are backed by clearing organization guarantees, daily mark-to-market and settlement, segregation and minimum capital requirements applicable to intermediaries. Transactions entered into directly between two counterparties generally do not benefit from such protections. Relying on a counterparty exposes the Fund to the risk that a counterparty will not settle a transaction in accordance with its terms and conditions because of a dispute over the terms of the contract (whether or not bona fide) or because of a credit or liquidity problem, thus causing the Fund to suffer a loss. If a counterparty defaults on its payment obligations to the Fund, this default will cause the value of an investment in the Fund to decrease. In addition, to the extent the Fund deals with a limited number of counterparties, it will be more susceptible to the credit risks associated with those counterparties. The Fund is neither restricted from dealing with any particular counterparty nor from concentrating any or all of its transactions with one counterparty. The ability of the Fund to transact business with any one or number of counterparties and the absence of a regulated market to facilitate settlement may increase the potential for losses by the Fund. | |

| ● | Derivatives Risk: The underlying ETFs’ use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments. These risks include (i) the risk that the counterparty to a derivative transaction may not fulfill its contractual obligations; (ii) risk of mispricing or improper valuation; and (iii) the risk that changes in the value of the derivative may not correlate perfectly with the underlying asset. Derivative prices are highly volatile and may fluctuate substantially during a short period of time. Such prices are influenced by numerous factors that affect the markets, including, but not limited to: changing supply and demand relationships; government programs and policies; national and international political and economic events, changes in interest rates, inflation and deflation and changes in supply and demand relationships. Trading derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities. Derivative contracts ordinarily have leverage inherent in their terms. The low margin deposits normally required in trading derivatives, including futures contracts, permit a high degree of leverage. Accordingly, a relatively small price movement may result in an immediate and substantial loss to the underlying ETF. The use of leverage may also cause the underlying ETF to liquidate portfolio positions when it would not be advantageous to do so in order to satisfy its obligations or to meet collateral segregation requirements. The use of leveraged derivatives can magnify the underlying ETFs’ potential for gain or loss and, therefore, amplify the effects of market volatility on share price. Because option premiums paid or received are small in relation to the market value of the investments underlying the options, buying and selling put and call options can be more speculative than investing directly in securities. |

7

| ● | Emerging Market Risk: The Fund may invest in countries with newly organized or less developed securities markets. Investments in emerging markets typically involves greater risks than investing in more developed markets. Generally, economic structures in these countries are less diverse and mature than those in developed countries and their political systems tend to be less stable. Emerging market countries may have different regulatory, accounting, auditing, and financial reporting and record keeping standards and may have material limitations on Public Company Accounting Oversight Board (“PCAOB”) inspection, investigation, and enforcement. Therefore, the availability and reliability of information, particularly financial information, material to an investment decision in emerging market companies may be limited in scope and reliability as compared to information provided by U.S. companies. Emerging market economies may be based on only a few industries. As a result, security issuers, including governments, may be more susceptible to economic weakness and more likely to default. Emerging market countries also may have relatively unstable governments, weaker economies, and less-developed legal systems with fewer security holder rights. Investments in emerging markets countries may be affected by government policies that restrict foreign investment in certain issuers or industries. The potentially smaller size of securities markets in emerging market countries and lower trading volumes can make investments relatively illiquid and potentially more volatile than investments in developed countries, and such securities may be subject to abrupt and severe price declines. Due to this relative lack of liquidity, the Fund may have to accept a lower price or may not be able to sell a portfolio security at all. An inability to sell a portfolio position can adversely affect the Fund’s value or prevent the Fund from being able to meet cash obligations or take advantage of other investment opportunities. |

| ● | Equity Risk: The NAV of the Fund will fluctuate based on changes in the value of the equity securities held by the Fund or underlying funds that invest in U.S. and/or foreign equity securities. Equity prices can fall rapidly in response to developments affecting a specific company or industry, or to changing economic, political or market conditions. | |

| ● | ETF Risk: ETFs are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. As a result, your cost of investing in the Fund will be higher than the cost of investing directly in ETFs and may be higher than other mutual funds that invest directly in stocks and bonds. ETFs are listed on national stock exchanges and are traded like stocks listed on an exchange. ETF shares may trade at a discount or a premium in market price if there is a limited market in such shares. ETFs are also subject to brokerage and other trading costs, which could result in greater expenses to the Fund. ETFs may employ leverage, which magnifies the changes in the value of the ETFs. Finally, because the value of ETF shares depends on the demand in the market, the adviser may not be able to liquidate the Fund’s holdings at the most optimal time, adversely affecting performance. |

You will indirectly bear fees and expenses charged by the ETFs in addition to the Fund’s direct fees and expenses. Additional risks of investing in ETFs are described below:

| ○ | Strategy Risk: Each ETF is subject to specific risks, depending on the nature of the ETF. These risks could include liquidity risk, sector risk as well as risks associated with fixed-income securities. | |

| ○ | NAV and Market Price Risk: The market value of the ETF shares may differ from their NAV. This difference in price may be due to the fact that the supply and demand in the market for ETF shares at any point in time is not always identical to the supply and demand in the market for the underlying basket of securities. Accordingly, there may be times when an ETF share trades at a premium or discount to its NAV. | |

| ○ | Tracking Risk: Investment in the Fund should be made with the understanding that the ETFs in which the Fund invests will not be able to replicate exactly the performance of the indices they track because the total return generated by the securities will be reduced by transaction costs incurred in adjusting the actual balance of the securities. In addition, the ETFs in which the Fund invests will incur expenses not incurred by their applicable indices. Certain securities comprising the indices tracked by the ETFs, from time to time, temporarily be unavailable, which may further impede the ability to track the applicable indices. |

| ● | Fixed Income Risk: When the Fund invests in fixed income securities, the value of your investment in the Fund will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of fixed income securities owned by the Fund. In general, the market price of debt securities with longer maturities will increase or decrease more in response to changes in interest rates than shorter-term securities. Convertible securities are hybrid securities that have characteristics of both fixed income securities and common stocks and are subject to risks associated with both debt securities and equity securities. Other risk factors include credit risk (the debtor may default) and prepayment risk (the debtor may pay its obligation early, reducing the amount of interest payments; or the debtor may pay its obligation later than expected, reducing the returns earned by an investment). These risks could affect the value of a particular investment by the Fund possibly causing the Fund’s share price and returns to be reduced and fluctuate more than other types of investments. |

8

| ● | Foreign Currency Risk: Currency trading involves significant risks, including market risk, interest rate risk, country risk, counterparty credit risk and short sale risk. Market risk results from the price movement of foreign currency values in response to shifting market supply and demand. Since exchange rate changes can readily move in one direction, a currency position carried overnight or over a number of days may involve greater risk than one carried a few minutes or hours. Interest rate risk arises whenever a country changes its stated interest rate target associated with its currency. Country risk arises because virtually every country has interfered with international transactions in its currency. Interference has taken the form of regulation of the local exchange market, restrictions on foreign investment by residents or limits on inflows of investment funds from abroad. Restrictions on the exchange market or on international transactions are intended to affect the level or movement of the exchange rate. This risk could include the country issuing a new currency, effectively making the “old” currency worthless. The Fund may also take short positions, through derivatives, if the Adviser believes the value of a currency is likely to depreciate in value. A “short” position is, in effect, similar to a sale in which the Fund sells a currency it does not own but, has borrowed in anticipation that the market price of the currency will decline. The Fund must replace a short currency position by purchasing it at the market price at the time of replacement, which may be more or less than the price at which the Fund took a short position in the currency. |

| ● | Foreign Investment Risk: Foreign investing (including through ADRs, EDRs and GDRs) involves risks not typically associated with U.S. investments, including adverse fluctuations in foreign currency values, adverse political, social and economic developments, less liquidity, greater volatility, less developed or less efficient trading markets, political instability and differing auditing and legal standards. Investing in emerging markets imposes risks different from, or greater than, risks of investing in foreign developed countries. | |

| ● | High Yield (Junk) Bond Risk: Lower-quality fixed income securities, known as “high yield” or “junk” bonds, present a significant risk for loss of principal and interest. These bonds offer the potential for higher return, but also involve greater risk than bonds of higher quality, including an increased possibility that the bond’s issuer, obligor or guarantor may not be able to make its payments of interest and principal (credit quality risk). If that happens, the value of the bond may decrease, and the Fund’s share price may decrease and its income distribution may be reduced. An economic downturn or period of rising interest rates (interest rate risk) could adversely affect the market for these bonds and reduce the Fund’s ability to sell its bonds (liquidity risk). Such securities may also include “Rule 144A” securities, which are subject to resale restrictions. The lack of a liquid market for these bonds could decrease the Fund’s share price. |

| ○ | Defaulted Securities Risk: Defaulted securities risk refers to the uncertainty of repayment of defaulted securities and obligations of distressed issuers. Repayment of defaulted securities and obligations of distressed issuers (including insolvent issuers or issuers in payment or covenant default, in workout or restructuring or in bankruptcy or in solvency proceedings) is subject to significant uncertainties. Investments in defaulted securities and obligations of distressed issuers are considered speculative. |

| ● | Issuer-Specific Risk: The value of a specific security can be more volatile than the market as a whole and can perform differently from the value of the market as a whole. The value of securities of smaller issuers can be more volatile than those of larger issuers. The value of certain types of securities can be more volatile due to increased sensitivity to adverse issuer, political, regulatory, market, or economic developments. | |

| ● | Large Capitalization Risk: Large-capitalization companies may be less able than smaller capitalization companies to adapt to changing market conditions. Large-capitalization companies may be more mature and subject to more limited growth potential compared with smaller capitalization companies. During different market cycles, the performance of large capitalization companies has trailed the overall performance of the broader securities markets. | |

| ● | Management Risk: The NAV of the Fund changes daily based on the performance of the securities and derivatives in which it invests. The Adviser’s judgments about the attractiveness, value and potential appreciation of particular asset classes and securities in which the Fund invests (long or short) may prove to be incorrect and may not produce the desired results. | |

| ● | Market and Geopolitical Risk: The increasing interconnectivity between global economies and financial markets increases the likelihood that events or conditions in one region or financial market may adversely impact issuers in a different country, region or financial market. Securities in the Fund’s portfolio may underperform due to inflation (or expectations for inflation), interest rates, global demand for particular products or resources, natural disasters, climate change and climate-related events, pandemics, epidemics, terrorism, international conflicts, regulatory events and governmental or quasi-governmental actions. The occurrence of global events similar to those in recent years, such as terrorist attacks around the world, natural disasters, social and political discord or debt crises and downgrades, among others, may result in market volatility and may have long term effects on both the U.S. and global financial markets. It is difficult to predict when similar events affecting the U.S. or global financial markets may occur, the effects that such events may have and the duration of those effects. Any such event(s) could have a significant adverse impact on the value and risk profile of the Fund’s portfolio. The novel coronavirus (COVID-19) |

9

global pandemic and the aggressive responses taken by many governments, including closing borders, restricting international and domestic travel, and the imposition of prolonged quarantines or similar restrictions, as well as the forced or voluntary closure of, or operational changes to, many retail and other businesses, had negative impacts, and in many cases severe negative impacts, on markets worldwide. It is not known how long such impacts, or any future impacts of other significant events described above, will or would last, but there could be a prolonged period of global economic slowdown, which may impact your Fund investment. Therefore, the Fund could lose money over short periods due to short-term market movements and over longer periods during more prolonged market downturns. During a general market downturn, multiple asset classes may be negatively affected. Changes in market conditions and interest rates can have the same impact on all types of securities and instruments. In times of severe market disruptions you could lose your entire investment.

| ● | Model Risk: Like all quantitative analyses, the investment model carries a risk that the proprietary ranking system and valuation model used might be based on one or more incorrect assumptions or may not perform as expected. Rapidly changing and unforeseen market dynamics could also lead to a decrease in short term effectiveness of the model. | |

| ● | Portfolio Turnover Risk: A higher portfolio turnover will result in higher transactional and brokerage costs. | |

| ● | Small and Medium Capitalization Risk: Small or medium capitalization companies may have limited product lines, markets or financial resources, and they may be dependent on a limited management group. Securities of smaller companies may be subject to more abrupt or erratic market movements than those of larger, more established companies or the market averages in general. | |

| ● | Sovereign Debt Risk: The issuer of the foreign debt or the governmental authorities that control the repayment of the debt may be unable or unwilling to repay principal or interest when due, and the Fund may have limited recourse in the event of a default. The market prices of sovereign debt, and the Fund’s NAV, may be more volatile than prices of U.S. debt obligations and certain emerging markets may encounter difficulties in servicing their debt obligations. | |

| ● | U.S. Government Obligations Risk: U.S. Treasury obligations are backed by the “full faith and credit” of the U.S. government and generally have negligible credit risk. Securities issued or guaranteed by federal agencies or authorities and U.S. government-sponsored instrumentalities or enterprises may or may not be backed by the full faith and credit of the U.S. government. The Fund may be subject to such risk to the extent it invests in securities issued or guaranteed by federal agencies or authorities and U.S. government-sponsored instrumentalities or enterprises. |

Temporary Investments: To respond to adverse market, economic, political or other conditions, the Fund may invest 100% of its total assets, without limitation, in high-quality short-term debt securities and money market instruments. These short-term debt securities and money market instruments include: shares of money market mutual funds, commercial paper, certificates of deposit, bankers’ acceptances, U.S. government securities and repurchase agreements. While the Fund is in a defensive position, the opportunity to achieve its investment objective will be limited. Furthermore, to the extent that the Fund invests in money market mutual funds for cash positions, there will be some duplication of expenses because shareholders will pay the fees and expenses of the Fund and, indirectly, the fees and expenses of the underlying money market funds. The Fund may also invest a substantial portion of its assets in such instruments at any time to maintain liquidity or pending selection of investments in accordance with its policies.

Portfolio Holdings Disclosure: A description of the Fund’s policies regarding the release of portfolio holdings information is available in the Fund’s Statement of Additional Information (“SAI”).

Cybersecurity: The computer systems, networks and devices used by the Fund and its service providers to carry out routine business operations employ a variety of protections designed to prevent damage or interruption from computer viruses, network failures, computer and telecommunication failures, infiltration by unauthorized persons and security breaches. Despite the various protections utilized by the Fund and its service providers, systems, networks, or devices potentially can be breached. The Fund and its shareholders could be negatively impacted as a result of a cybersecurity breach.

Cybersecurity breaches can include unauthorized access to systems, networks, or devices; infection from computer viruses or other malicious software code; and attacks that shut down, disable, slow, or otherwise disrupt operations, business processes, or website access or functionality. Cybersecurity breaches may cause disruptions and impact the Fund’s business operations, potentially resulting in financial losses; interference with the Fund’s ability to calculate its NAV; impediments to trading; the inability of the Fund, the Adviser, and other service providers to transact business; violations of applicable privacy and other laws; regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, or additional compliance costs; as well as the inadvertent release of confidential information.

Similar adverse consequences could result from cybersecurity breaches affecting issuers of securities in which the Fund invests; counterparties with which the Fund engages in transactions; governmental and other regulatory authorities; exchange and other financial market operators, banks, brokers, dealers, insurance companies, and other financial institutions (including financial intermediaries and service providers for the Fund’s shareholders); and other parties. In addition, substantial costs may be incurred by these entities in order to prevent any cybersecurity breaches in the future.

10

MANAGEMENT

Investment Adviser: Pinnacle Family Advisors, LLC, 620 W. Republic Road, Suite 104, Springfield, MO 65807, serves as investment adviser to the Fund. Subject to the oversight of the Board of Trustees, the Adviser is responsible for management of the Fund’s investment portfolio. The Adviser is responsible for ensuring that investments are made according to the Fund’s investment objective, policies and restrictions. The Adviser was established in 2007 for the purpose of advising individuals and institutions. As of September 30, 2022, the Adviser had approximately $275 million in assets under management.

Pursuant to an investment advisory agreement with the Trust, on behalf of the Fund, the Adviser is entitled to receive, on a monthly basis, an annual advisory fee equal to 1.00% of the Fund’s average daily net assets. The Adviser has contractually agreed to waive management fees and to make payments to limit Fund expenses, at least until August 1, 2024, so the Total Annual Operating Expenses After Fee Waiver and Reimbursement (excluding: (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions; (iii) acquired fund fees and expenses; (iv) borrowing costs (such as interest and dividend expense on securities sold short); (v) taxes; and (vi) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees, contractual indemnification of Fund service providers (other than the Adviser))) of the Fund do not exceed 1.49% of average daily net assets attributable to Class A shares, 2.24% of average daily net assets attributable to Class C shares and 1.24% of average daily net assets attributable to Class I shares. These fee waivers and expense reimbursements are subject to possible recoupment from the Fund in future years on a rolling three-year basis (within the three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits. This agreement may be terminated only by the Board of Trustees on 60 days’ written notice to the Adviser. A discussion regarding the basis for the Board of Trustees’ renewal of the advisory agreement is available in the Fund’s September 30, 2022 Annual Report to Shareholders. During the fiscal year ended September 30, 2022, the Fund paid an aggregate of 0.66% of its average net assets in advisory fees to the Adviser (after fee waivers).

Portfolio Managers: The Fund is managed on a day to day basis by R. Sean McCurry and Paul Carroll. The SAI provides additional information about each Portfolio Manager’s compensation, other accounts managed by the Portfolio Managers, and the Portfolio Managers’ ownership in the Fund.

R. Sean McCurry has been the Managing Member and President of the Adviser since 2008. Mr. McCurry also previously served as a Financial Adviser and Branch Manager for Raymond James Financial Services from January 1999 to December 2007.

Paul Carroll has been the Chief Investment Officer and Chief Compliance Officer of the Adviser since 2008. Mr. Carroll also served as a Financial Adviser for Raymond James Financial Services from December 2005 to November 2008.

11

HOW SHARES ARE PRICED

Shares of the Fund are sold at NAV. The NAV of the Fund is determined at close of regular trading (normally 4:00 p.m. Eastern Time) on each day the New York Stock Exchange (“NYSE”) is open for business. NAV is computed by determining, on a per class basis, the aggregate market value of all assets of the Fund, less its liabilities, divided by the total number of shares outstanding ((assets-liabilities)/number of shares = NAV). The NYSE is closed on weekends and New Year’s Day, Martin Luther King, Jr. Day, Presidents’ Day, Good Friday, Memorial Day, Juneteenth, Independence Day, Labor Day, Thanksgiving Day and Christmas Day. The NAV takes into account, on a per class basis, the expenses and fees of the Fund, including management, administration, and distribution fees, which are accrued daily. The determination of NAV for a share class for a particular day is applicable to all applications for the purchase of shares, as well as all requests for the redemption of shares, received by the Fund (or an authorized broker or agent, or its authorized designee) before the close of trading on the NYSE on that day.

Generally, the Fund’s securities are valued each day at the last quoted sales price on each security’s primary exchange. Securities traded or dealt in upon one or more securities exchanges (whether domestic or foreign) for which market quotations are readily available and not subject to restrictions against resale shall be valued at the last quoted sales price on the primary exchange or, in the absence of a sale on the primary exchange, at the mean between the current bid ask prices on such exchanges. Securities primarily traded in the National Association of Securities Dealers’ Automated Quotation System (“NASDAQ”) National Market System for which market quotations are readily available shall be valued using the NASDAQ Official Closing Price. Securities that are not traded or dealt in any securities exchange (whether domestic or foreign) and for which over-the-counter market quotations are readily available generally shall be valued at the last sale price or, in the absence of a sale, at the mean between the current bid and ask price on such over-the-counter market. Debt securities not traded on an exchange may be valued at prices supplied by a pricing agent(s) based on broker or dealer supplied valuations or matrix pricing, a method of valuing securities by reference to the value of other securities with similar characteristics, such as rating, interest rate and maturity.

If market quotations are not readily available, securities will be valued at their fair market value as determined using the “fair value” procedures approved by the Board of Trustees. Fair value pricing involves subjective judgments and it is possible that the fair value determined for a security may be materially different from the value that could be realized upon the sale of that security. The fair value prices can differ from market prices when they become available or when a price becomes available. The Board of Trustees has delegated execution of these procedures to the Adviser, as the valuation designee. The Adviser may also enlist third party consultants such as an audit firm or financial officer of a security issuer on an as-needed basis to assist in determining a security-specific fair value. The Board of Trustees reviews and ratifies the execution of this process and the resultant fair value prices at least quarterly to assure the process produces reliable results.

The Fund may use independent pricing services to assist in calculating the value of the Fund’s securities. In addition, market prices for foreign securities are not determined at the same time of day as the NAV for the Fund. Because the Fund may invest in underlying ETFs which hold portfolio securities primarily listed on foreign exchanges, and these exchanges may trade on weekends or other days when the underlying ETFs do not price their shares, the value of some of the Fund’s portfolio securities may change on days when you may not be able to buy or sell Fund shares.

In computing the NAV, the Fund values foreign securities held by the Fund at the latest closing price on the exchange in which they are traded immediately prior to closing of the NYSE. Prices of foreign securities quoted in foreign currencies are translated into U.S. dollars at current rates. If events materially affecting the value of a security in the Fund’s portfolio, particularly foreign securities, occur after the close of trading on a foreign market but before the Fund prices its shares, the security may be priced using alternative market prices provided by a pricing service. For example, if trading in a portfolio security is halted and does not resume before the Fund calculates its NAV, alternative market prices may be used to value the security. Without a fair value price, short-term traders could take advantage of the arbitrage opportunity and dilute the NAV of long-term investors. Fair valuation of the Fund’s portfolio securities can serve to reduce arbitrage opportunities available to short-term traders, but there is no assurance that fair value pricing policies will prevent dilution of the Fund’s NAV by short term traders. The determination of fair value involves subjective judgments. As a result, using fair value to price a security may result in a price materially different from the prices used by other mutual funds to determine NAV, or from the price that may be realized upon the actual sale of the security.

With respect to any portion of the Fund’s assets that are invested in one or more open-end management investment companies registered under the Investment Company Act of 1940, as amended, the Fund’s NAV is calculated based upon the NAVs of those open-end management investment companies, and the prospectuses for these companies explain the circumstances under which those companies will use fair value pricing and the effects of using fair value pricing.

12

HOW TO PURCHASE SHARES

Share Classes

This Prospectus describes three classes of shares offered by the Fund: Class A, Class C and Class I. The Fund offers these three classes of shares so that you can choose the class that best suits your investment needs. Refer to the information below so that you can choose the class that best suits your investment needs. The main differences between each class are sales charges, ongoing fees and minimum investment. For information on ongoing distribution fees, see Distribution Fees on page 22 of this Prospectus. Each class of shares in the Fund represents interest in the same portfolio of investments within the Fund. There is no investment minimum on reinvested distributions and the Fund may change investment minimums at any time. The Fund reserves the right to waive sales charges, as described below. The Fund and the Adviser may each waive investment minimums at their individual discretion. Not all share classes may be available for purchase in all states.

Factors to Consider When Choosing a Share Class

When deciding which class of shares of the Fund to purchase, you should consider your investment goals, present and future amounts you may invest in the Fund, and the length of time you intend to hold your shares. To help you make a determination as to which class of shares to buy, please refer back to the examples of the Fund’s expenses over time in the Fees and Expenses of the Fund section in this Prospectus. You also may wish to consult with your financial adviser for advice with regard to which share class is most appropriate for you.

Class A Shares

Class A shares are offered at their public offering price, which is NAV plus the applicable sales charge and is subject to 12b-1 distribution fees of up to 0.25% of the average daily net assets of Class A shares. There are no sales charges on reinvested distributions. The minimum initial investment in Class A shares of the Fund is $2,000 for all accounts. The minimum subsequent investment in Class A shares of the Fund is $500 for all accounts.

| Amount Invested | Sales Charge as a % of Offering Price(1) | Sales Charge as a % of Amount Invested | Dealer Reallowance |

| Under $25,000 | 5.75% | 6.10% | 5.00% |

| $25,000 to $49,999 | 5.00% | 5.26% | 4.25% |

| $50,000 to $99,999 | 4.75% | 4.99% | 4.00% |

| $100,000 to $249,999 | 3.75% | 3.83% | 3.25% |

| $250,000 to $499,999 | 2.50% | 2.56% | 2.00% |

| $500,000 to $999,999 | 2.00% | 2.04% | 1.75% |

| $1,000,000 and above | 1.00% | 1.01% | 1.00% |

| (1) | Offering price includes the front-end sales load. The sales charge you pay may differ slightly from the amount set forth above because of rounding that occurs in the calculations used to determine your sales charge. |

How to Reduce Your Sales Charge - You may be eligible to purchase Class A shares at a reduced sales charge. To qualify for these reductions, you must notify the Fund’s distributor, Northern Lights Distributors, LLC (the “Distributor”), in writing and supply your account number at the time of purchase. You may combine your purchase with those of your “immediate family” (your spouse and your children under the age of 21) for purposes of determining eligibility. If applicable, you will need to provide the account numbers of your spouse and your minor children as well as the ages of your minor children.

Rights of Accumulation - To qualify for the lower sales charge rates that apply to larger purchases of Class A shares, you may combine your new purchases of Class A shares with Class A shares of the Fund that you already own. The applicable initial sales charge for the new purchase is based on the total of your current purchase and the current value of all other Class A shares that you own. The reduced sales charge will apply only to current purchases and must be requested in writing when you buy your shares.

Shares of the Fund held as follows cannot be combined with your current purchase for purposes of reduced sales charges:

| ● | Shares held indirectly through financial intermediaries other than your current purchase broker-dealer (for example, a different broker-dealer, a bank, a separate insurance company account or an investment adviser); | |

| ● | Shares held through an administrator or trustee/custodian of an Employer Sponsored Retirement Plan (for example, a 401(k) plan) other than employer-sponsored IRAs; and | |

| ● | Shares held directly in the Fund account on which the broker-dealer (financial adviser) of record is different than your current purchase broker-dealer. |

13

Letters of Intent - Under a Letter of Intent (“LOI”), you commit to purchase a specified dollar amount of Class A shares of the Fund, with a minimum of $25,000 during a 13-month period. The 13-month period begins upon the date of the LOI. At your written request, Class A shares purchases made during the 90 days prior to LOI may be included. The amount you agree to purchase determines the initial sales charge you pay. If the full-face amount of the LOI is not invested by the end of the 13-month period, your account will be adjusted to the higher initial sales charge level for the amount actually invested. You are not legally bound by the terms of your LOI to purchase the amount of your shares stated in the LOI. The LOI does, however, authorize the Fund to hold in escrow 5% of the total amount you intend to purchase. If you do not complete the total intended purchase at the end of the 13-month period, the Fund’s transfer agent will redeem the necessary portion of the escrowed shares to make up the difference between the reduced rate sales charge (based on the amount you intended to purchase) and the sales charge that would normally apply (based on the actual amount you purchased).

Repurchase of Class A Shares - If you have redeemed Class A shares of the Fund within the past 120 days, you may repurchase an equivalent amount of Class A shares of the Fund at NAV, without the normal front-end sales charge. In effect, this allows you to reacquire shares that you may have had to redeem, without repaying the front-end sales charge. You may exercise this privilege only once and must notify the Fund that you intend to do so in writing. The Fund must receive your purchase order within 120 days of your redemption. Note that if you reacquire shares through separate installments (e.g., through monthly or quarterly repurchases), the sales charge waiver will only apply to those portions of your repurchase order received within 120 days of your redemption. The redemption and repurchase of Fund shares may still result in a tax liability for federal income tax purposes.

Sales Charge Waivers

The sales charge on purchases of Class A shares is waived for certain types of investors, including:

| ● | Current and retired directors and officers of the Fund sponsored by the Adviser or any of its subsidiaries, their immediate family members (i.e., spouse, children, mother or father) and any purchases referred through the Adviser. | |

| ● | Employees of the Adviser and their immediate family members, or any full-time employee or registered representative of the Distributor or of broker-dealers having dealer agreements with the Distributor (a “Selling Broker”) and their immediate family members (or any trust, pension, profit sharing or other benefit plan for the benefit of such persons). | |

| ● | Any full-time employee of a bank, savings and loan, credit union or other financial institution that utilizes a Selling Broker to clear purchases of the fund’s shares and their immediate family members. | |

| ● | Participants in certain “wrap-fee” or asset allocation programs or other fee-based arrangements sponsored by broker-dealers and other financial institutions that have entered into agreements with the Distributor. | |

| ● | Clients of financial intermediaries that have entered into arrangements with the Distributor providing for the shares to be used in particular investment products made available to such clients and for which such registered investment advisers may charge a separate fee. | |

| ● | Institutional investors (which may include bank trust departments and registered investment advisers). | |

| ● | Any accounts established on behalf of registered investment advisers or their clients by broker-dealers that charge a transaction fee and that have entered into agreements with the Distributor. | |

| ● | Separate accounts used to fund certain unregistered variable annuity contracts or Section 403(b) or 401(a) or (k) accounts. | |

| ● | Employer-sponsored retirement or benefit plans with total plan assets in excess of $5 million where the plan’s investments in the Fund are part of an omnibus account. A minimum initial investment of $1 million in the Fund is required. The Distributor in its sole discretion may waive these minimum dollar requirements. |

The Fund does not waive sales charges for the reinvestment of proceeds from the sale of shares of a different fund where those shares were subject to a front-end sales charge (sometimes called a “NAV transfer”). Whether a sales charge waiver is available for your retirement plan or charitable account depends upon the policies and procedures of your intermediary. Please consult your financial adviser for further information.

14

Class C Shares

Class C shares of the Fund are offered at their NAV without an initial sales charge. This means that 100% of your initial investment is placed into shares of the Fund. Class C shares pay up to 1.00% on an annualized basis of the average daily net assets as reimbursement or compensation for service and distribution-related activities with respect to the Fund and/or shareholder services. Over time, fees paid under this distribution and service plan will increase the cost of a Class C shareholder’s investment and may cost more than other types of sales charges. The minimum initial investment in the Class C shares is $2,000 and the minimum subsequent investment is $500.

Class I Shares

Class I shares of the Fund are sold at NAV without an initial sales charge and are not subject to 12b-1 distribution fees. This means that 100% of your initial investment is placed into shares of the Fund. Class I shares require a minimum initial investment of $1,000,000 and the minimum subsequent investment is $5,000.

Class I Shares may also be available on certain brokerage platforms. An investor transacting in Class I Shares through a broker acting as an agent for the investor may be required to pay a commission and/or other forms of compensation to the broker.

Class I shares are available to certain institutional investors, and directly to certain individual investors as set forth below:

| ● | Institutional Investors may include, but are not limited to, corporations, retirement plans, foundations/endowments and investors who purchase through a wrap account offered through a selling group member that enters into a wrap fee program agreement with the Distributor. | |

| ● | Individual Investors include trustees, officers and employees of the Trust and its affiliates, and immediate family members of all such persons. | |

| ● | Clients of the Adviser or purchases referred through the Adviser. | |

| ● | To investors on certain brokerage platforms. |

For accounts sold through financial intermediaries, it is the primary responsibility of the financial intermediary to ensure compliance with eligibility requirements such as investor type and investment minimums. An investor transacting through a broker acting as an agent for the investor may be required to pay a commission and/or other forms of compensation to the broker. The Fund may change investment minimums at any time. The Fund and the Adviser may each waive investment minimums at their individual discretion. Class I shares may not be available for purchase in all states.

Converting Shares

Shareholders of the Fund may elect on a voluntary basis to convert their shares in one class of the Fund into shares of a different class of the Fund, subject to satisfying the eligibility requirements for investment in the new share class.

Shares held through a financial intermediary offering different programs and fee structures that has an agreement with the Adviser or the Fund’s distributor may be converted by the financial intermediary, without notice, to another share class of the Fund, including share classes with a higher expense ratio than the original share class, if such conversion is consistent with the fee based or wrap fee program’s policies.

All permissible conversions will be made on the basis of the relevant NAVs of the two classes without the imposition of any front-end sales load. A share conversion within the Fund will not result in a capital gain or loss for federal income tax purposes. The Fund may change, suspend or terminate these conversion features at any time.

15

Purchasing Shares

You may purchase shares of the Fund by sending a completed application form to the following address:

Regular Mail Pinnacle Sherman Multi-Strategy Core Fund c/o Ultimus Fund Solutions, LLC P.O. Box 541150 Omaha, NE 68154 |

Express/Overnight Mail Pinnacle Sherman Multi-Strategy Core Fund c/o Ultimus Fund Solutions, LLC 4221 North 203rd Street, Suite 100 Elkhorn, NE 68022-3474 |

The USA PATRIOT Act requires financial institutions, including the Fund, to adopt certain policies and programs to prevent money-laundering activities, including procedures to verify the identity of customers opening new accounts. As requested on the application, you should supply your full name, date of birth, social security number and permanent street address. Mailing addresses containing a P.O. Box will not be accepted. This information will assist the Fund in verifying your identity. Until such verification is made, the Fund may temporarily limit additional share purchases. In addition, the Fund may limit additional share purchases or close an account if it is unable to verify a shareholder’s identity. As required by law, the Fund may employ various procedures, such as comparing the information to fraud databases or requesting additional information or documentation from you, to ensure that the information supplied by you is correct.

Purchase through Brokers: You may invest in the Fund through brokers or agents who have entered into selling agreements with the Distributor. The brokers and agents are authorized to receive purchase and redemption orders on behalf of the Fund. Such brokers are authorized to designate other intermediaries to receive purchase and redemption orders on the Fund’s behalf. The Fund will be deemed to have received a purchase or redemption order when an authorized broker or, if applicable, a brokers authorized designee receives the order. The broker or agent may set their own initial and subsequent investment minimums. You may be charged a fee if you use a broker or agent to buy or redeem shares of the Fund. Finally, various servicing agents use procedures and impose restrictions that may be in addition to, or different from those applicable to investors purchasing shares directly from the Fund. You should carefully read the program materials provided to you by your servicing agent.

Purchase by Wire: If you wish to wire money to make an investment in the Fund, please call the Fund at 1-888-985-9830 for wiring instructions and to notify the Fund that a wire transfer is coming. Any commercial bank can transfer same-day funds via wire. The Fund will normally accept wired funds for investment on the day received if they are received by the Fund’s designated bank before the close of regular trading on the NYSE. Your bank may charge you a fee for wiring same-day funds.

Automated Clearing House (ACH) Purchase: Current shareholders may purchase additional shares via Automated Clearing House (“ACH”). To have this option added to your account, please send a letter to the Fund requesting this option and supply a voided check for the bank account. Only bank accounts held at domestic institutions that are ACH members may be used for these transactions.

You may not use ACH transactions for your initial purchase of Fund shares. ACH purchases will be effective at the closing price per share on the business day after the order is placed. The Fund may alter, modify or terminate this purchase option at any time.

Shares purchased by ACH will not be available for redemption until the transactions have cleared. Shares purchased via ACH transfer may take up to 15 days to clear.

Transactions through www.pinnacledynamicfunds.com: You may purchase the Fund’s shares and redeem the Fund’s shares through the website www.pinnacledynamicfunds.com. To establish Internet transaction privileges, you must enroll through the website. You automatically have the ability to establish Internet transaction privileges unless you decline the privileges on your New Account Application or IRA Application. You will be required to enter into a user’s agreement through the website in order to enroll in these privileges. In order to conduct Internet transactions, you must have telephone transaction privileges. To purchase shares through the website you must also have ACH instructions on your account.

Redemption proceeds may be sent to you by check to the address of record, or if your account has existing bank information, by wire or ACH. Only bank accounts held at domestic financial institutions that are ACH members can be used for transactions through the website. Transactions through the website are subject to the same minimums as other transaction methods.

16