Form 497 ADVISORS SERIES TRUST

Tweet

Tweet Share

Share

TABLE OF CONTENTS

SUMMARY SECTION

Class A | Class C | Class F | Institutional Class | |||||||||||

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | ||||||||||||||

Maximum Deferred Sales Charge (Load) (as a percentage of original purchase price or redemption price, whichever is less) | ||||||||||||||

Redemption Fee (as a percentage of amount redeemed on shares held for 30 days or less) | ||||||||||||||

| Management Fees | % | |||||||||||||||||||

| Distribution and Service (Rule 12b-1) Fees | % | |||||||||||||||||||

| Other Expenses (includes Shareholder Servicing Plan Fee) | % | (1) | (1) | |||||||||||||||||

| Shareholder Servicing Plan Fee | ||||||||||||||||||||

Total Annual Fund Operating Expenses(2) | % | |||||||||||||||||||

Less: Fee Waiver(3) | - | % | - | - | - | |||||||||||||||

| Total Annual Fund Operating Expenses After Fee Waiver | % | |||||||||||||||||||

(1)Other expenses are based on estimated amounts for the current fiscal year.

(2)Total Annual Fund Operating Expenses reflect the maximum Rule 12b-1 fee and/or Shareholder Servicing Plan fee allowed while the Expense Ratios in the Financial Highlights reflect actual expenses.

(3)Shenkman Capital Management, Inc. (the “Advisor”) has contractually agreed to waive a portion or all of its management fees and pay Floating Rate Fund expenses in order to limit Total Annual Fund Operating Expenses (excluding AFFE, taxes, interest expense, dividends on securities sold short, extraordinary expenses, Rule 12b-1 fees, shareholder servicing fees and any other class-specific expenses) to 0.54% of average daily net assets of the Fund (the “Expense Cap”). The Expense Cap

1

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||

Class A | $ | $ | $ | $ | ||||||||||

Class C (if you redeem your shares at the end of the period) | $ | $ | $ | $ | ||||||||||

Class F (if you redeem your shares at the end of the period) | $ | $ | $ | $ | ||||||||||

Institutional Class (if you redeem your shares at the end of the period) | $ | $ | $ | $ | ||||||||||

Class C | $ | $ | $ | $ | ||||||||||

Under normal market conditions, the Floating Rate Fund invests at least 80% of its net assets (plus any borrowings for investment purposes) in a diversified portfolio of senior secured and unsecured floating rate bank loans and other floating rate instruments. The Fund seeks to provide a high level of current income through comprehensive fundamental analysis and compounding interest income. The Fund also seeks to preserve capital by avoiding defaults and minimizing both interest rate volatility and credit risk.

The loans and other instruments in which the Floating Rate Fund invests include bank loans (i.e., loan assignments and participations) to corporate borrowers, traditional corporate bonds, notes, debentures, zero-coupon bonds, collateralized loan obligations (“CLOs”) and other corporate debt instruments, and obligations of the U.S. Government and government-sponsored entities. A substantial portion of the Floating Rate Fund’s net assets may be comprised of covenant lite loans. The Fund may invest in corporate fixed-income instruments and loans of any maturity or credit quality. The Fund may invest without limit in loans, bonds or other debt obligations rated lower than Baa by Moody’s Investors Service, Inc. (“Moody’s”) or BBB by S&P Global Ratings (“S&P”) (i.e., “junk” bonds and loans), and may also invest without limit in Rule 144A and restricted fixed-income securities; provided, however, that the Floating Rate Fund may only invest up to 20% of its total assets in fixed-income instruments. The Fund generally invests in high yield instruments rated Caa or better by Moody’s or CCC or better by S&P, but retains the discretion to invest in even lower-rated instruments.

2

•General Market Risk. Economies and financial markets throughout the world are becoming increasingly interconnected, which increases the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions. Securities in the Fund’s portfolio may underperform in comparison to securities in general financial markets, a particular financial market or other asset classes due to a number of factors, including: inflation (or expectations for inflation); interest rates; global demand for particular products or resources; natural disasters or events; pandemic diseases; terrorism; regulatory events; and government controls. U.S. and international markets have experienced significant periods of volatility in recent years and months due to a number of economic, political and global macro factors including the impact of COVID-19 as a global pandemic, which has resulted in a public health crisis, disruptions to business operations and supply chains, stress on the global healthcare system, growth concerns in the U.S. and overseas, staffing shortages and the inability to meet consumer demand, and widespread concern and uncertainty. The global recovery from COVID-19 is proceeding at slower than expected rates due to the emergence of variant strains and may last for an extended period of time. Continuing uncertainties regarding interest rates, rising inflation, political events, rising government debt in the U.S. and trade tensions also contribute to market volatility. As a result of continuing political tensions and armed conflicts, including the war between Ukraine and Russia, the U.S. and the European Union imposed sanctions on certain Russian individuals and companies, including certain financial institutions, and have limited certain exports and imports to and from Russia. The war has contributed to recent market volatility and may continue to do so.

•Bank Loan Risk. The Floating Rate Fund’s investments in secured and unsecured assignments of (or participations in) bank loans may create substantial risk. In making investments in bank loans, which are made by banks or other financial intermediaries to borrowers, the Fund will depend primarily upon the creditworthiness of the borrower, whose financial condition may be troubled or highly leveraged, for payment of principal and interest. When the Fund is a participant in a loan, the Fund has no direct claim on the loan and would be a creditor of the lender, and not the borrower, in the event of a borrower’s insolvency or default. Transactions involving floating rate loans have significantly longer settlement periods (e.g., longer than seven days) than more traditional investments and, as a result, sale proceeds related to the sale of loans may not be available to make additional investments or to meet the Fund’s redemption obligations until potentially a substantial

3

period after the sale of the loans. In addition, loans are not registered under the federal securities laws like stocks and bonds, so investors in loans have less protection against improper practices than investors in registered securities.

•Covenant Lite Loan Risk. Some covenant lite loans tend to have fewer or no financial maintenance covenants and restrictions. A covenant lite loan typically contains fewer clauses which allow an investor to proactively enforce financial covenants or prevent undesired actions by the borrower/issuer. Covenant lite loans also generally provide fewer investor protections if certain criteria are breached. The Fund may experience losses or delays in enforcing its rights on its holdings of covenant lite loans.

•LIBOR Risk. The Floating Rate Fund invests in certain debt securities or other financial instruments that utilize the London Inter-bank Offered Rate, or “LIBOR,” as a “benchmark” or “reference rate” for variable interest rate calculations. The United Kingdom’s Financial Conduct Authority, which regulates LIBOR, announced a desire to phase out the use of LIBOR by the end of 2021. On November 30, 2020, the administrator of LIBOR announced a delay in the phase out of a majority of the U.S. dollar LIBOR publications until June 30, 2023, with the remainder of LIBOR publications already phased out at the end of 2021. Although financial regulators and industry working groups have suggested alternative reference rates, global consensus is lacking and the process for amending existing contracts or instruments to transition away from LIBOR remains unclear. Uncertainty and risk also remain regarding the willingness and ability of issuers and lenders to include enhanced provisions in new and existing contracts or instruments. Consequently, the transition away from LIBOR may lead to increased volatility and illiquidity in markets that are tied to LIBOR, decreased values of LIBOR-related investments or investments in issuers that utilize LIBOR, increased difficulty in borrowing or refinancing and diminished effectiveness of hedging strategies, adversely affecting the Fund’s performance or net asset value. Uncertainty and volatility arising from the transition may result in a reduction in the value of certain LIBOR-based instruments held by the Fund or reduce the effectiveness of related transactions. Any such effects of the transition away from LIBOR, as well as other unforeseen effects, could result in losses to the Fund and may adversely affect the Fund’s performance or net asset value.

•Collateralized Loan Obligation Risk. The risks of an investment in a collateralized loan obligation depend largely on the type of the collateral securities and the class of the debt obligation in which the Fund invests. Collateralized loan obligations are generally subject to credit, interest rate, valuation, liquidity, prepayment and extension risks. These securities also are subject to risk of default on the underlying asset, particularly during periods of economic downturn. Collateralized loan obligations carry additional risks including, but not limited to, (i) the possibility that distributions from collateral securities will not be adequate to make interest or other payments, (ii) the collateral may decline in value or default, (iii) the Fund may invest in obligations that are subordinate to other classes, and (iv) the complex structure of the security may not be fully understood at the time of investment and produce disputes with the issuer or unexpected investment results.

•High Yield Risk. High yield debt obligations, including bonds and loans, rated below BBB by S&P or Baa by Moody’s (commonly referred to as “junk bonds”) typically carry higher coupon rates than investment grade securities, but also are described as speculative by both S&P and Moody’s and may be subject to greater market price fluctuations, less liquidity and greater risk of loss of income or principal including greater possibility of default and bankruptcy of the issuer of such instruments than more highly rated bonds and loans.

•Counterparty Risk. Counterparty risk arises upon entering into borrowing arrangements and is the risk from the potential inability of counterparties to meet the terms of their contracts.

•Credit Risk. The issuers of the bonds and other debt instruments held by the Floating Rate Fund may not be able to make interest or principal payments.

4

•Impairment of Collateral Risk. The value of any collateral securing a bond or loan can decline, and may be insufficient to meet the borrower’s obligations or difficult to liquidate. In addition, the Floating Rate Fund’s access to collateral may be limited by bankruptcy or other insolvency laws.

•Interest Rate Risk. The Fund’s investments in fixed-income instruments will change in value based on changes in interest rates. When interest rates decline, the value of a portfolio invested in fixed-rate obligations can be expected to rise. Conversely, when interest rates rise, the value of a portfolio investment in fixed-rate obligations can be expected to decline. Although the value of the Fund’s investments will vary, the Fund invests primarily in floating rate instruments, which should minimize fluctuations in value as a result of changes in market interest rates. However, because floating rates on loans and other instruments only reset periodically, changes in prevailing interest rates can still be expected to cause some fluctuation in the value of the Fund.

•Investment Risk. The Floating Rate Fund is not a complete investment program and you may lose money by investing in the Fund. The Fund invests primarily in high yield debt obligations issued by companies that may have significant risks as a result of business, financial, market or legal uncertainties. There can be no assurance that the Advisor will correctly evaluate the nature and magnitude of the various factors that could affect the value of, and return on, the Fund’s investments.

•Leverage Risk. Leverage can increase the investment returns of the Floating Rate Fund if the securities purchased increase in value in an amount exceeding the cost of the borrowing. However, if the securities decrease in value, the Fund will suffer a greater loss than would have resulted without the use of leverage.

•Liquidity Risk. Low or lack of trading volume may make it difficult to sell instruments held by the Fund at quoted market prices. The Floating Rate Fund’s investments may at any time consist of significant amounts of positions that are thinly traded or for which no market exists. For example, the investments held by the Fund may not be liquid in all circumstances so that, in volatile markets, the Advisor may not be able to close out a position without incurring a loss. The foregoing risks may be accentuated when the Fund is required to liquidate positions to meet withdrawal requests. Additionally, floating rate loans generally are subject to legal or contractual restrictions on resale, may trade infrequently, and their value may be impaired when the Fund needs to liquidate such loans. High yield bonds and loans generally trade only in the over-the-counter market rather than on an organized exchange and may be more difficult to purchase or sell at a fair price, which could have a negative impact on the Fund’s performance.

•Initial Public Offering (“IPO”) and Unseasoned Company Risk. The market value of IPO shares may fluctuate considerably due to factors such as the absence of a prior public market, unseasoned trading, the small number of shares available for trading and limited information about the issuer. Additionally, investments in unseasoned companies may involve greater risks, in part because they have limited product lines, markets and financial or managerial resources. In addition, less frequently-traded securities may be subject to more abrupt price movements than securities of larger capitalized companies.

•Convertible Bond Risk. Convertible bonds are hybrid securities that have characteristics of both bonds and common stocks and are therefore subject to both debt security risks and equity risk. Convertible bonds are subject to equity risk especially when their conversion value is greater than the interest and principal value of the bond. The prices of equity securities may rise or fall because of economic or political changes and may decline over short or extended periods of time.

•Foreign Instruments Risk. Investments in foreign instruments involve certain risks not associated with investments in U.S. companies. Foreign instruments in the Floating Rate Fund’s portfolio subject the Fund to the risks associated with investing in the particular country, including the political, regulatory, economic, social and other conditions or events occurring in the country, as well

5

as fluctuations in its currency, foreign currency exchange controls, foreign tax issues and the risks associated with less developed custody and settlement practices.

•Management Risk. The Floating Rate Fund is an actively managed portfolio. The Advisor’s management practices and investment strategies may not work to produce the desired results. The success of the Fund is largely dependent upon the ability of the Advisor to manage the Fund and implement the Fund’s investment program. If the Fund were to lose the services of the Advisor or its senior officers, the Fund may be adversely affected. Additionally, if the Fund or any of the other accounts managed by the Advisor were to incur substantial losses or were subject to an unusually high level of redemptions or withdrawals, the revenues of the Advisor may decline substantially. Such losses and/or withdrawals may impair the Advisor’s ability to retain employees and its ability to provide the same level of service to the Fund as it has in the past and continue operations.

•Preferred Stock Risk. Preferred stocks may be more volatile than fixed-income securities and are more correlated with the issuer’s underlying common stock than fixed-income securities. Additionally, the dividend on a preferred stock may be changed or omitted by the issuer.

•Rule 144A Securities Risk. The market for Rule 144A securities typically is less active than the market for publicly-traded securities. Rule 144A securities carry the risk that the liquidity of these securities may become impaired, making it more difficult for the Floating Rate Fund to sell these bonds.

•U.S. Government Obligations Risk. Certain U.S. government securities are supported by the full faith and credit of the United States; others are supported by the right of the issuer to borrow from the U.S. Treasury; others are supported by the discretionary authority of the U.S. government to purchase the agency’s obligations; and still others are supported only by the credit of the issuing agency, instrumentality, or enterprise. Although U.S. government-sponsored enterprises such as the Federal Home Loan Mortgage Corporation (Freddie Mac) and the Federal National Mortgage Association (Fannie Mae) may be chartered or sponsored by Congress, they are not funded by Congressional appropriations, and their securities are not issued by the U.S. Treasury, are not supported by the full faith and credit of the U.S. government, and involve increased credit risks.

•When-Issued Instruments Risk. The price or yield obtained in a when-issued transaction may be less favorable than the price or yield available in the market when the instruments’ delivery takes place. Additionally, failure of a party to a transaction to consummate the trade may result in a loss to the Floating Rate Fund or missing an opportunity to obtain a price considered advantageous.

•Yankee Bond Risk. Yankee bonds are subject to the same risks as other debt issues, notably credit risk, market risk, currency and liquidity risk. Other risks include adverse political and economic developments; the extent and quality of government regulations of financial markets and institutions; the imposition of foreign withholding taxes; and the expropriation or nationalization of foreign issuers.

6

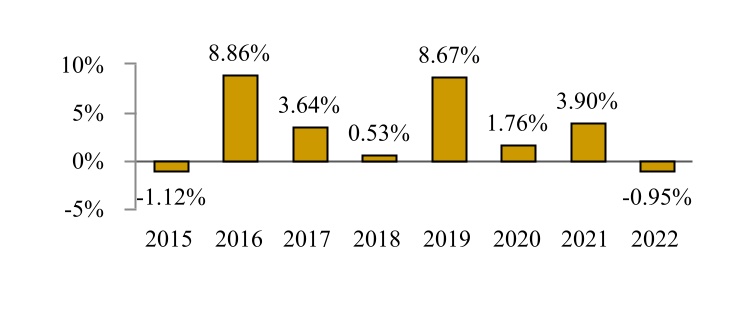

Average Annual Total Returns (for the periods ended December 31, 2022) | 1 Year | 5 Year | Since Inception (10/15/2014) | ||||||||

| Institutional Class | |||||||||||

| - | |||||||||||

| - | |||||||||||

| - | |||||||||||

Class F(1) | |||||||||||

| - | |||||||||||

(reflects no deduction for fees, expenses or taxes) | - | ||||||||||

(1) The Institutional Class incepted on October 15, 2014 March 1, 2017 . Class F performance for the period from October 15, 2014 to March 1, 2017 reflects the performance of the Institutional Class, adjusted to reflect Class F fees and expenses.

(2) On June 1, 2022, Morningstar, Inc. completed its acquisition of Leverage Commentary & Data from S&P Global. As a result of this acquisition, the S&P/LSTA Leveraged Loan Index has been renamed the Morningstar LSTA US Leveraged

7

Management

Investment Advisor. Shenkman Capital Management, Inc. is the Floating Rate Fund’s investment advisor.

Portfolio Managers. Mark R. Shenkman, Justin W. Slatky, David H. Lerner, Jeffrey Gallo, Jordan Barrow, Brian C. Goldberg and Eileen Spiro are the co-portfolio managers primarily responsible for the day-to-day management of the Floating Rate Fund. Mr. Shenkman is President and Founder of the Advisor and has managed the Fund since its inception in October 2014. Mr. Slatky is Executive Vice President, Chief Investment Officer and Senior Portfolio Manager of the Advisor and has managed the Fund since July 2016. Mr. Lerner is Senior Vice President and Head of Structured Credit of the Advisor and has managed the Fund since its inception. Mr. Gallo is Senior Vice President, Co-Head of Liquid Credit and Portfolio Manager of the Advisor and has managed the Fund since September 2015. Mr. Barrow is Senior Vice President, Co-Head of Liquid Credit and Portfolio Manager of the Advisor and has managed the Fund since July 2022. Mr. Goldberg is Senior Vice President, Head of Bank Loan & CLO Capital Markets and Portfolio Manager of the Advisor and has managed the Fund since September 2018. Ms. Spiro is Senior Vice President and Associate Portfolio Manager of the Advisor and has managed the Fund since July 2022.

Purchase and Sale of Fund Shares

You may purchase, exchange or redeem Floating Rate Fund shares on any business day by written request via mail (Shenkman Capital Floating Rate High Income Fund, c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, Wisconsin 53201-0701), by telephone at 1‑855-SHENKMAN (1-855-743-6562), or through a financial intermediary. You may also purchase or redeem Fund shares by wire transfer. Investors who wish to purchase, exchange or redeem Fund shares through a financial intermediary should contact the financial intermediary directly. The minimum initial and subsequent investment amounts are shown below.

| Type of Account | To Open Your Account | To Add to Your Account | ||||||

| Class A, Class C and Class F | ||||||||

| Regular Accounts | $1,000 | $100 | ||||||

| Retirement Accounts | $1,000 | $100 | ||||||

| Class F Only | ||||||||

| Merrill Lynch Private Bank Customers | $250 | None | ||||||

| Institutional Class | ||||||||

| All Accounts | $1 million | $100,000 | ||||||

8

Tax Information

The Floating Rate Fund’s distributions are taxable, and will be taxed as ordinary income or capital gains, unless you invest through a tax-deferred arrangement, such as a 401(k) plan or an IRA. Distributions on investments made through tax-deferred arrangements may be taxed later upon withdrawal of assets from those accounts.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase the Floating Rate Fund through a broker-dealer or other financial intermediary, the Fund and/or the Advisor may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

9

SUMMARY SECTION

Class A | Class C | Class F | Institutional Class | |||||||||||

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | ||||||||||||||

Maximum Deferred Sales Charge (Load) (as a percentage of original purchase price or redemption price, whichever is less) | ||||||||||||||

Redemption Fee (as a percentage of amount redeemed on shares held for 30 days or less) | ||||||||||||||

| Management Fees | ||||||||||||||

| Distribution and Service (Rule 12b-1) Fees | ||||||||||||||

| Other Expenses (includes Shareholder Servicing Plan Fee) | ||||||||||||||

| Shareholder Servicing Plan Fee | ||||||||||||||

Total Annual Fund Operating Expenses(1) | ||||||||||||||

Less: Fee Waiver(2) | - | - | - | - | ||||||||||

| Total Annual Fund Operating Expenses After Fee Waiver | ||||||||||||||

(1)Total Annual Fund Operating Expenses reflect the maximum Rule 12b-1 fee and/or Shareholder Servicing Plan fee allowed while the Expense Ratios in the Financial Highlights reflect actual expenses.

(2)Shenkman Capital Management, Inc. (the “Advisor”) has contractually agreed to waive a portion or all of its management fees and pay Short Duration Fund expenses in order to limit Total Annual Fund Operating Expenses (excluding AFFE, taxes, interest expense, dividends on securities sold short, extraordinary expenses, Rule 12b-1 fees, shareholder servicing fees, and any other class-specific expenses) to 0.65% of average daily net assets of the Fund (the “Expense Cap”). The Expense Cap will remain in effect through at least January 27, 2024 , and may be terminated only by the Trust’s Board of

10

1 Year | 3 Years | 5 Years | 10 Years | |||||||||||

Class A | $ | $ | $ | $ | ||||||||||

Class C (if you redeem your shares at the end of the period) | $ | $ | $ | $ | ||||||||||

Class F (if you redeem your shares at the end of the period) | $ | $ | $ | $ | ||||||||||

Institutional Class (if you redeem your shares at the end of the period) | $ | $ | $ | $ | ||||||||||

Class C | $ | $ | $ | $ | ||||||||||

Under normal market conditions, the Short Duration Fund will invest at least 80% of its net assets (plus any borrowings for investment purposes) in fixed-income securities, bank loans and other instruments issued by companies that are rated below investment grade (i.e., “junk” bonds and loans). The Fund considers below investment grade instruments to include instruments with ratings lower than BBB- by S&P Global Ratings (“S&P”) or Baa3 by Moody’s Investors Service, Inc. (“Moody’s”), or that are not rated or considered by the Advisor to be equivalent to high yield instruments. The Fund generally invests in high yield instruments rated CCC or better by S&P or Caa or better by Moody’s, but retains the discretion to invest in even lower rated instruments.

The fixed-income securities, bank loans and other instruments in which the Short Duration Fund invests include traditional corporate bonds, U.S. government obligations and bank loans to corporate borrowers, and may have fixed, floating or variable rates. The Fund typically focuses on instruments that have short durations (i.e., have an expected redemption through maturity, call or other corporate action within three years or less from the time of purchase). The Fund will seek to maintain a dollar-weighted average portfolio duration of approximately three years or less. Duration is a measure of a debt instrument’s price sensitivity to yield. Higher duration indicates debt instruments that are more sensitive to interest rate changes. Bonds with shorter duration are typically less sensitive to interest rate changes. Duration takes into account a debt instrument’s cash flows over time, including the possibility that a debt instrument

11

might be prepaid by the issuer or redeemed by the holder prior to its stated maturity date. In contrast, maturity measures only the time until final payment is due.

The Short Duration Fund may invest up to 20% of its total assets in foreign fixed-income instruments, including those denominated in U.S. dollars, such as Yankee bonds, or other currencies, and may also invest without limit in Rule 144A fixed-income securities. Additionally, the Fund may invest up to 15% of its total assets in convertible bonds, and up to 10% of its total assets in preferred stocks. The Fund may also utilize leverage of no more than 33% of the Fund’s total assets as part of the portfolio management process. Leverage is the practice of borrowing money to purchase investments, for instance, by borrowing money against a line of credit. The Fund may also create leverage by borrowing money against a margin account where the Fund’s portfolio holdings and cash serve as collateral for the loan. Additionally, the Fund may hold from time to time equity positions received as a result of a restructuring of a debt instrument held by the Fund.

•General Market Risk. Economies and financial markets throughout the world are becoming increasingly interconnected, which increases the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions. Securities in the Fund’s portfolio may underperform in comparison to securities in general financial markets, a particular financial market or other asset classes due to a number of factors, including: inflation (or expectations for inflation); interest rates; global demand for particular products or resources; natural disasters or events; pandemic diseases; terrorism; regulatory events; and government controls. U.S. and international markets have experienced significant periods of volatility in recent years and months due to a number of economic, political and global macro factors including the impact of COVID-19 as a global pandemic, which has resulted in a public health crisis, disruptions to business operations and supply chains, stress on the global healthcare system, growth concerns in the U.S. and overseas, staffing shortages and the inability to meet consumer demand, and widespread concern and uncertainty. The global recovery from COVID-19 is proceeding at slower than expected rates due to the emergence of variant strains and may last for an extended period of time. Continuing uncertainties regarding interest rates, rising inflation, political events, rising government debt in the U.S. and trade tensions also contribute to market volatility. As a result of continuing political tensions and armed conflicts, including the war between Ukraine and Russia, the U.S. and the European Union imposed sanctions on certain Russian individuals and companies, including certain financial institutions, and have limited certain exports and imports to and from Russia. The war has contributed to recent market volatility and may continue to do so.

•High Yield Risk. High yield debt obligations, including bonds and loans, rated below BBB by S&P or Baa by Moody’s (commonly referred to as “junk bonds”) typically carry higher coupon rates than investment grade securities, but also are described as speculative by both S&P and Moody’s and may be subject to greater market price fluctuations, less liquidity and greater risk of loss of income or principal including greater possibility of default and bankruptcy of the issuer of such instruments than more highly rated bonds and loans.

•Bank Loan Risk. The Short Duration Fund’s investments in secured and unsecured assignments of (or participations in) bank loans may create substantial risk. In making investments in such loans,

12

which are made by banks or other financial intermediaries to borrowers the Fund will depend primarily upon the creditworthiness of the borrower, whose financial condition may be troubled or highly leveraged for payment of principal and interest. When the Fund is a participant in a loan, the Fund has no direct claim on the loan and would be a creditor of the lender, and not the borrower, in the event of a borrower’s insolvency or default. Transactions involving floating rate loans have significantly longer settlement periods (e.g., longer than seven days) than more traditional investments and, as a result, sale proceeds related to the sale of loans may not be available to make additional investments or to meet the Fund’s redemption obligations until potentially a substantial period after the sale of the loans. In addition, loans are not registered under the federal securities laws like stocks and bonds, so investors in loans have less protection against improper practices than investors in registered securities.

•Counterparty Risk. Counterparty risk arises upon entering into borrowing arrangements or derivative transactions and is the risk from the potential inability of counterparties to meet the terms of their contracts.

•Credit Risk. The issuers of the bonds and other debt securities held by the Short Duration Fund may not be able to make interest or principal payments.

•Convertible Bond Risk. Convertible bonds are hybrid securities that have characteristics of both bonds and common stocks and are therefore subject to both debt security risks and equity risk. Convertible bonds are subject to equity risk especially when their conversion value is greater than the interest and principal value of the bond. The prices of equity securities may rise or fall because of economic or political changes and may decline over short or extended periods of time.

•Impairment of Collateral Risk. The value of any collateral securing a bond or loan can decline, and may be insufficient to meet the borrower’s obligations or difficult to liquidate. In addition, the Short Duration Fund’s access to collateral may be limited by bankruptcy or other insolvency laws.

•Interest Rate Risk. The Fund’s investments in fixed-income instruments will change in value based on changes in interest rates. When interest rates decline, the value of a portfolio invested in fixed-rate obligations can be expected to rise. Conversely, when interest rates rise, the value of a portfolio investment in fixed-rate obligations can be expected to decline. Although the value of the Fund’s investments will vary, the fluctuations in value of the Fund’s investments in floating rate instruments should be minimized as a result of changes in market interest rates. However, because floating rates on loans and other instruments only reset periodically, changes in prevailing interest rates can still be expected to cause some fluctuation in the value of the Fund.

•Investment Risk. The Short Duration Fund is not a complete investment program and you may lose money by investing in the Fund. The Fund invests primarily in high yield debt obligations issued by companies that may have significant risks as a result of business, financial, market or legal uncertainties. There can be no assurance that the Advisor will correctly evaluate the nature and magnitude of the various factors that could affect the value of, and return on, the Fund’s investments.

•Liquidity Risk. Low or lack of trading volume may make it difficult to sell instruments held by the Fund at quoted market prices. The Short Duration Fund’s investments may at any time consist of significant amounts of positions that are thinly traded or for which no market exists. For example, the investments held by the Fund may not be liquid in all circumstances so that, in volatile markets, the Advisor may not be able to close out a position without incurring a loss. The foregoing risks may be accentuated when the Fund is required to liquidate positions to meet withdrawal requests. Additionally, floating rate loans generally are subject to legal or contractual restrictions on resale, may trade infrequently, and their value may be impaired when the Fund needs to liquidate such loans. High yield bonds and loans generally trade only in the over-the-counter market rather than on an organized exchange and may be more difficult to purchase or sell at a fair price, which could have a negative impact on the Fund’s performance.

13

•Leverage Risk. Leverage can increase the investment returns of the Short Duration Fund if the securities purchased increase in value in an amount exceeding the cost of the borrowing. However, if the securities decrease in value, the Fund will suffer a greater loss than would have resulted without the use of leverage.

•Initial Public Offering (“IPO”) and Unseasoned Company Risk. The market value of IPO shares may fluctuate considerably due to factors such as the absence of a prior public market, unseasoned trading, the small number of shares available for trading and limited information about the issuer. Additionally, investments in unseasoned companies may involve greater risks, in part because they have limited product lines, markets and financial or managerial resources. In addition, less frequently-traded securities may be subject to more abrupt price movements than securities of larger capitalized companies.

•Foreign Instruments Risk. Investments in foreign instruments involve certain risks not associated with investments in U.S. companies. Foreign instruments in the Short Duration Fund’s portfolio subject the Fund to the risks associated with investing in the particular country, including the political, regulatory, economic, social and other conditions or events occurring in the country, as well as fluctuations in its currency, foreign currency exchange controls, foreign tax issues and the risks associated with less developed custody and settlement practices.

•Management Risk. The Short Duration Fund is an actively managed portfolio. The Advisor’s management practices and investment strategies might not work to produce the desired results. The success of the Fund is largely dependent upon the ability of the Advisor to manage the Fund and implement the Fund’s investment program. If the Fund were to lose the services of the Advisor or its senior officers, the Fund may be adversely affected. Additionally, if the Fund or any of the other accounts managed by the Advisor were to incur substantial losses or were subject to an unusually high level of redemptions or withdrawals, the revenues of the Advisor may decline substantially. Such losses and/or withdrawals may impair the Advisor’s ability to retain employees and its ability to provide the same level of service to the Fund as it has in the past and continue operations.

•Preferred Stock Risk. Preferred stocks may be more volatile than fixed-income securities and are more correlated with the issuer’s underlying common stock than fixed-income securities. Additionally, the dividend on a preferred stock may be changed or omitted by the issuer.

•Rule 144A Securities Risk. The market for Rule 144A securities typically is less active than the market for publicly-traded securities. Rule 144A securities carry the risk that the liquidity of these securities may become impaired, making it more difficult for the Short Duration Fund to sell these bonds.

•When-Issued Instruments Risk. The price or yield obtained in a when-issued transaction may be less favorable than the price or yield available in the market when the instruments’ delivery takes place. Additionally, failure of a party to a transaction to consummate the trade may result in a loss to the Floating Rate Fund or missing an opportunity to obtain a price considered advantageous.

•Yankee Bond Risk. Yankee bonds are subject to the same risks as other debt issues, notably credit risk, market risk, currency and liquidity risk. Other risks include adverse political and economic developments; the extent and quality of government regulations of financial markets and institutions; the imposition of foreign withholding taxes; and the expropriation or nationalization of foreign issuers.

•U.S. Government Obligations Risk. Certain U.S. government securities are supported by the full faith and credit of the United States; others are supported by the right of the issuer to borrow from the U.S. Treasury; others are supported by the discretionary authority of the U.S. government to purchase the agency’s obligations; and still others are supported only by the credit of the issuing agency, instrumentality, or enterprise. Although U.S. government-sponsored enterprises such as the Federal

14

15

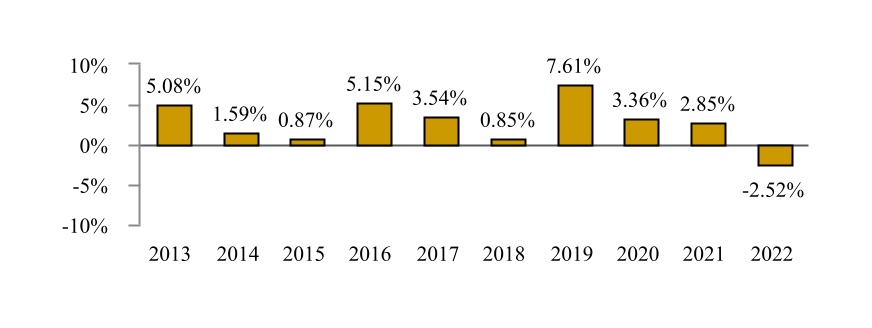

Average Annual Total Returns (for the periods ended December 31, 2022) | 1 Year | 5 Year | 10 Year | Since Inception (10/31/2012) | ||||||||||

| Institutional Class | ||||||||||||||

| - | ||||||||||||||

| - | ||||||||||||||

| - | ||||||||||||||

| Class A | ||||||||||||||

| - | ||||||||||||||

Class C(1) | ||||||||||||||

| - | ||||||||||||||

Class F(2) | ||||||||||||||

| - | ||||||||||||||

| - | ||||||||||||||

(reflects no deduction for fees, expenses or taxes) | - | |||||||||||||

(1) The Institutional Class incepted on October 31, 2012 January 28, 2014 . Class C performance for the period from October 31, 2012 to January 28, 2014, reflects the performance of the Institutional Class, adjusted to reflect Class C fees and expenses .

(2) The Institutional Class incepted on October 31, 2012, and Class F incepted on May 17, 2013 . Class F performance for the period from October 31, 2012 to May 17, 2013, reflects the performance of the Institutional Class, adjusted to reflect Class F fees and expenses.

(3) Please note in previous years, the Fund utilized the same benchmarks “without transaction costs”. Going forward, the Fund will compare its returns to the indices “with transaction costs”. Index returns include transaction costs, which may be higher or lower than the actual transaction costs incurred by the Fund.

Management

Investment Advisor. Shenkman Capital Management, Inc. is the Fund’s investment advisor.

Portfolio Managers. Mark R. Shenkman, Justin W. Slatky, Jordan Barrow, Jeffrey Gallo, Nicholas Sarchese and Neil Wechsler are the co-portfolio managers primarily responsible for the day-to-day management of the Short Duration Fund. Mr. Shenkman is President and Founder of the Advisor and has managed the Fund since its inception in October 2012. Mr. Slatky is Executive Vice President, Chief Investment Officer and Senior Portfolio Manager of the Advisor and has managed the Fund since July 2016. Mr. Barrow is Senior Vice President, Co-Head of Liquid Credit and Portfolio Manager of the Advisor and has managed the Fund since December 2016. Mr. Gallo is Senior Vice President, Co-Head

16

of Liquid Credit and Portfolio Manager of the Advisor and has managed the Fund since July 2022. Mr. Sarchese is Senior Vice President and Portfolio Manager of the Advisor and has managed the Fund since its inception. Mr. Wechsler is Senior Vice President, Credit Analyst and Portfolio Manager and has managed the Fund since July 2019.

Purchase and Sale of Fund Shares

You may purchase, redeem, or exchange Short Duration Fund shares on any business day by written request via mail (Shenkman Capital Short Duration High Income Fund, c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, Wisconsin 53201-0701), by telephone at 1‑855-SHENKMAN (1-855-743-6562), or through a financial intermediary. You may also purchase or redeem Fund shares by wire transfer. Investors who wish to purchase, redeem or exchange Fund shares through a financial intermediary should contact the financial intermediary directly.

The minimum initial and subsequent investment amounts are shown below.

| Type of Account | To Open Your Account | To Add to Your Account | ||||||

| Class A, Class C and Class F | ||||||||

| Regular Accounts | $1,000 | $100 | ||||||

| Retirement Accounts | $1,000 | $100 | ||||||

| Class F Only | ||||||||

| Merrill Lynch Private Bank Customers | $250 | None | ||||||

| Institutional Class | ||||||||

All Accounts | $1 million | $100,000 | ||||||

Tax Information

The Short Duration Fund’s distributions are taxable, and will be taxed as ordinary income or capital gains, unless you invest through a tax-deferred arrangement, such as a 401(k) plan or an IRA. Distributions on investments made through tax-deferred arrangements may be taxed later upon withdrawal of assets from those accounts.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase the Short Duration Fund through a broker-dealer or other financial intermediary, the Fund and/or the Advisor may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

17

PRINCIPAL INVESTMENT STRATEGIES AND RELATED RISKS

Floating Rate Fund

Under normal market conditions, the Floating Rate Fund invests at least 80% of its net assets (plus any borrowings for investment purposes) in a diversified portfolio of senior secured and unsecured floating rate bank loans and other floating rate instruments. This 80% investment policy may be changed upon at least 60 days’ prior written notice to shareholders. The Fund seeks to provide a high level of current income through comprehensive fundamental analysis and compounding interest income and to preserve capital by avoiding defaults and minimizing both interest rate volatility and credit risk.

The loans and other instruments in which the Floating Rate Fund invests include bank loans (i.e., loan assignments and participations) to corporate borrowers, traditional corporate bonds, notes, debentures, zero-coupon bonds, CLOs and other corporate debt securities, and obligations of the U.S. Government and government-sponsored entities. A substantial portion of the Floating Rate Fund’s net assets may be comprised of covenant lite loans. The Fund may invest in corporate fixed-income securities and loans of any maturity or credit quality. The Fund may invest without limit in loans, bonds or other debt obligations rated lower than Baa by Moody’s or BBB by S&P (i.e., “junk” bonds and loans), and may also invest without limit in Rule 144A and restricted fixed-income securities. The Fund generally invests in high yield instruments rated Caa or better by Moody’s or CCC or better by S&P, but retains the discretion to invest in even lower-rated instruments.

The Floating Rate Fund may invest up to 20% of its total assets in foreign fixed-income instruments, including those denominated in U.S. dollars, such as Yankee bonds, or other currencies, and may also invest up to 20% of its total assets in IPOs and other unseasoned companies. Additionally, the Fund may invest up to 15% of its total assets in convertible bonds, up to 15% of its total assets in other investment companies, including mutual funds and ETFs, up to 10% of its total assets in preferred stocks, and up to 10% of its total assets in when-issued securities. The Floating Rate Fund may also utilize leverage of no more than 33% of the Fund’s total assets as part of the portfolio management process. Leverage is the practice of borrowing money to purchase investments, for instance, by borrowing money against a line of credit. The Fund may also create leverage by borrowing money against a margin account where the Fund’s portfolio holdings and cash serve as collateral for the loan. The Fund may also hold equity positions, particularly equity positions received as a result of a restructuring of a debt instrument held by the Fund.

Short Duration Fund

Under normal market conditions, the Short Duration Fund will invest at least 80% of its net assets (plus any borrowings for investment purposes) in fixed-income securities, bank loans and other instruments issued by companies that are rated below investment grade (i.e., “junk” bonds and loans). This 80% investment policy may be changed upon at least 60 days’ prior written notice to shareholders. The Fund considers below investment grade instruments to include instruments with ratings lower than BBB- by S&P or Baa3 by Moody’s, or that are not rated or considered by the Advisor to be equivalent to high yield instruments. The Fund generally invests in high yield instruments rated CCC or better by S&P or Caa or better by Moody’s but retains the discretion to invest in even lower rated instruments.

The fixed-income securities, loans and other instruments in which the Short Duration Fund expects to invest include traditional corporate bonds, U.S. Government obligations and bank loans to corporate borrowers, and may have fixed, floating or variable rates. The Fund typically focuses on instruments that have short durations (i.e., have an expected redemption through maturity, call or other corporate action within three years or less from the time of purchase). The Fund will seek to maintain a dollar-weighted average portfolio duration of approximately three years or less. The Fund may invest up to 20% of its total assets in foreign fixed-income instruments, including those denominated in U.S. dollars, such as Yankee bonds, or other currencies, and may also invest without limit in Rule 144A fixed-income securities. Additionally, the Fund may invest up to 15% of its total assets in convertible bonds, and up to 10% of its total assets in preferred stocks. The Fund may also utilize leverage of no more than 33% of the Fund’s total assets as part of the portfolio management process. Leverage is the practice of borrowing money to purchase investments, for instance, by borrowing money against a line of credit. The Fund may also create leverage by borrowing money against a margin account where the Fund’s portfolio holdings and cash serve as collateral for the loan. Additionally, the Fund may hold

18

from time to time hold equity positions particularly equity positions received as a result of a restructuring of a debt instrument held by the Fund.

Duration is a measure of a debt instrument’s price sensitivity to yield. Higher duration indicates debt instruments that are more sensitive to interest rate changes. Bonds with shorter duration are typically less sensitive to interest rate changes. For example, if a bond has a duration of 5 years, a 1% rise in interest rates would result in a 5% decline in value. If a bond has a duration of 10 years, a 1% rise in interest rates would result in a 10% decline in value. Duration takes into account a debt instrument’s cash flows over time including the possibility that a debt instrument might be prepaid by the issuer or redeemed by the holder prior to its stated maturity date. In contrast, maturity measures only the time until final payment is due. The following are examples of the relationship between a bond’s maturity and its duration. A 5% coupon bond having a ten-year maturity will have a duration of approximately 7.8 years. Similarly, a 5% coupon bond having a three-year maturity will have a duration of approximately 2.8 years.

Principal Investment Strategies Applicable to Both Funds

In selecting each Fund’s investments, the Advisor will employ a multi-faceted, “bottom up” investment approach that utilizes certain proprietary analytical tools. These tools include: (1) Quadrant Analysis, and (2) C.Scope®. The Advisor believes these tools are integral in assessing the potential risk of each investment. These tools also assist the Advisor in identifying companies that it believes are likely to have the ability to meet their interest and principal payments on their debt instruments.

The Advisor’s “Quadrant Analysis” is predicated on its belief that the high yield market is comprised of four distinct sectors (or “Quadrants”), each of which represents the degree of credit risk associated with an investment. The Advisor generally assigns a “Quadrant” to each investment based upon the amount of debt the company has outstanding and its ability to generate cash flow. The Advisor allocates investments among the four Quadrants based upon its outlook for risk in the economy and the high yield market. The C.Scope® tool is a numerical scoring system that ranks a proposed investment based on certain criteria, including the company’s financial condition, management and industry ranking. Investments made by the Advisor with respect to a Fund are categorized into a Quadrant and assigned a C.Scope® score.

The Advisor’s investment philosophy is predicated on the following principles:

•Drive performance through a combination of compounding interest income and maintaining a low default rate.

•Protect capital by minimizing losses when credit fundamentals deteriorate.

•Base investment decisions on in-depth, bottom-up fundamental credit analysis.

•Diversify portfolios by issuer and industry.

•Meet or communicate directly with the issuer’s senior management.

•Monitor credits on a systematic basis.

•Deliberate credit issues among the investment team.

•Avoid or de-emphasize industries with historically high default rates.

•Avoid or de-emphasize small, illiquid issues.

The Advisor believes that good investment ideas are the result of the careful collection and synthesis of information about each issuer and a disciplined investment process. Investment candidates are analyzed in depth at a variety of risk levels. Investments are not made on the basis of one single factor. Rather, investments are made based on the careful consideration of a variety of factors, including:

•Analyses of business risks (including leverage and technology risk) and macro risks (including interest rate trends, capital market conditions and default rates)

•Assessment of the industry’s attractiveness and competitiveness

19

•Evaluation of the business, including core strengths and competitive weaknesses

•Qualitative evaluation of the management team, including in-person meetings or conference calls with key managers

•Quantitative analyses of the company’s financial statements

The Advisor’s longstanding investment philosophy integrates environmental, social and governance (“ESG”) factors into its overall credit research process. As part of its investment process, the Advisor seeks to consider all meaningful risks or opportunities that may have an impact on a company’s future prospects, operating performance or valuation, including those related to ESG. Such risks and opportunities include the company’s ability to (i) effectively manage any potential environmental issues; (ii) operate with the highest levels of integrity and social responsibility, and (iii) exhibit good governance practices. Management engagement and capital markets dialogue are critical to the Advisor’s assessment. ESG factors are not stand-alone considerations in the Advisor’s investment process, but are instead woven into the process in the following ways:

•The Advisor’s proprietary management checklist is designed to evaluate governance and management integrity;

•The Advisor’s proprietary risk assessment checklist seeks to quantify both quantitative and qualitative risk factors;

•Key risk factors quantified by the Advisor’s analysts often include important ESG variables;

•The Advisor’s proprietary financial models seek to quantify the impact of many ESG risk factors;

•The Advisor’s proprietary C. Scope® score aims to assess all risk factors, including those related to ESG, that can impact credit quality; and

•The Advisor’s ESG checklist seeks to aggregate the various ESG factors in a single assessment.

If the Advisor believes one or more risk factors exist that may affect the investment thesis of a particular company, that company may be excluded from the Investment Manager’s list of approved issuers (i.e., generally would not be available for consideration for investment in a Fund). From time to time, if the Investment Manager believes an ESG factor or factors affect the investment thesis of a particular industry, the Investment Manager might exclude those companies in that industry from investment. These principles could preclude investments in companies: (i) in carbon intensive industries facing high compliance costs or environmental litigation; (ii) with increased regulatory, litigation or reputational risks; (iii) that lack appropriate financial reporting or investor communications; or (iv) with management that lacks integrity.

On a daily basis, the Advisor generally reviews each investment for unexpected changes such as with regards to its financial performance, news headlines, and potential downgrades, and monitors portfolio metrics such as price changes, industry and issuer exposures, using a variety of internally and externally developed systems. There are four red flags that require the Advisor to review an investment and may lead to an outright sale. The four red flags are: (i) Credit Drift, which is measured by specified declines in the Advisor’s proprietary C.Scope® score; (ii) Quadrant Drift, which occurs when a company is re-categorized into a lower proprietary Quadrant; (iii) Current Price Drift, which is measured by specified declines in the market price of a company’s bond and/or the issue has widened from its initial issue spread; and (iv) Management Drift, which occurs when the Advisor believes that the company’s management deviates from its stated strategic direction or fails to make good on its promises.

Temporary Defensive Investment Strategies

For temporary defensive purposes in response to adverse market, economic, political or other conditions, the Advisor may invest up to 100% of a Fund’s total assets in high-quality, short-term debt securities and money market instruments. These short-term debt securities and money market instruments include shares of other mutual funds, commercial paper, certificates of deposit, bankers’ acceptances, U.S. Government securities and repurchase agreements. Taking a temporary defensive position may result in a Fund not achieving its investment objective. Furthermore, to the extent that a Fund invests in money market mutual funds for its cash position, there will be some duplication of expenses because the Fund would bear its pro rata portion of such money market funds’ management fees and operational expenses.

20

Principal Risks of Investing in a Fund

Each Fund’s investment objective described in the respective Summary Sections is non-fundamental and may be changed without shareholder approval upon 60 days’ written notice to shareholders. There is no assurance that a Fund’s investment objective will be achieved. Because prices of securities fluctuate, the value of an investment in a Fund will vary as the market value of its investment portfolio changes. The Funds, together or separately, are not a complete, balanced investment plan, and the risk exists that you could lose all or a portion of your investment in the Funds. A detailed description of the related risks of investing in a Fund that may adversely affect a Fund’s net asset value (“NAV”) or total return is discussed below.

General Market Risk. Economies and financial markets throughout the world are becoming increasingly interconnected, which increases the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions. Securities in a Fund’s portfolio may underperform in comparison to securities in general financial markets, a particular financial market or other asset classes due to a number of factors, including: inflation (or expectations for inflation); interest rates; global demand for particular products or resources; natural disasters or events; pandemic diseases; terrorism; regulatory events; and government controls. U.S. and international markets have experienced significant periods of volatility in recent years and months due to a number of economic, political and global macro factors including the impact of COVID-19 as a global pandemic, which has resulted in a public health crisis, disruptions to business operations and supply chains, stress on the global healthcare system, growth concerns in the U.S. and overseas, staffing shortages and the inability to meet consumer demand, and widespread concern and uncertainty. The global recovery from COVID-19 is proceeding at slower than expected rates due to the emergence of variant strains and may last for an extended period of time. Continuing uncertainties regarding interest rates, rising inflation, political events, rising government debt in the U.S. and trade tensions also contribute to market volatility. As a result of continuing political tensions and armed conflicts, including the war between Ukraine and Russia, the U.S. and the European Union imposed sanctions on certain Russian individuals and companies, including certain financial institutions, and have limited certain exports and imports to and from Russia. The war has contributed to recent market volatility and may continue to do so.

High Yield Risk. Bonds and loans rated below BBB by S&P or Baa by Moody’s (commonly referred to as “junk bonds or loans”) typically carry higher coupon rates than investment grade bonds, but also are described as speculative by both S&P and Moody’s and may be subject to greater market price fluctuations, less liquidity and greater risk of income or principal including greater possibility of default and bankruptcy of the issuer of such instruments than more highly rated bonds and loans. Lower-rated bonds and loans also are more likely to be sensitive to adverse economic or company developments and more subject to price fluctuations in response to changes in interest rates. The market for lower-rated debt issues generally is thinner and less active than that for higher quality instruments, which may limit a Fund’s ability to sell such instruments at fair value in response to changes in the economy or financial markets. During periods of economic downturn or rising interest rates, highly leveraged issuers of lower-rated instruments may experience financial stress which could adversely affect their ability to make payments of interest and principal and increase the possibility of default.

Bank Loan Risk. A Fund’s investments in assignments of secured and unsecured bank loans may create substantial risk. In making investments in such loans, which are made by banks or other financial intermediaries to borrowers, a Fund will depend primarily upon the creditworthiness of the borrower, whose financial condition may be troubled or highly leveraged, for payment of principal and interest. If a Fund does not receive scheduled interest or principal payments on such indebtedness, such Fund’s share price could be adversely affected. A Fund may invest in loans that are rated by a nationally recognized statistical rating organization or are unrated, and may invest in loans of any credit quality, including “distressed” companies with respect to which there is a substantial risk of losing the entire amount invested. In addition, certain bank loans in which a Fund may invest may be illiquid and, therefore, difficult to value and/or sell at a price that is beneficial to the Fund. A Fund, as a participant in a loan, has no direct claim on the loan and would be a creditor of the lender, and not the borrower, in the event of a borrower’s insolvency or default. Transactions in many loans settle on a delayed basis, and a Fund may not receive the proceeds from the sale of a loan for a substantial period after the sale (i.e., more than seven days after the sale). As a result, sale proceeds related to the sale of loans may not be available to make additional investments or to meet a Fund’s redemption obligations until potentially a substantial period after the sale of the loans. In addition, loans are not registered

21

under the federal securities laws like stocks and bonds, so investors in loans have less protection against improper practices than investors in registered securities.

Counterparty Risk. Each Fund may establish relationships to obtain financing and prime brokerage services that permit the Fund to trade in any variety of markets or asset classes over time. However, there can be no assurance that the Fund will be able to establish or maintain such relationships, which could prevent the Fund from trading at optimal rates and terms. Moreover, a disruption in the financing and prime brokerage services provided by any such relationships could have an impact on the Fund’s business due to the Master Fund’s reliance on such counterparties.

When a Fund enters into a contract directly with dealer counterparties, the Fund is exposed to the risk that a counterparty will not settle a transaction in accordance with its terms because of a solvency or liquidity problem with the counterparty. Delays in settlement may also result from disputes over the terms of the contract (whether or not bona fide). In addition, each Fund may have a concentrated risk in a particular counterparty, which may mean that if such counterparty were to become insolvent or have a liquidity problem, losses would be greater than if the Fund had entered into contracts with multiple counterparties. If there is a default by a counterparty, the Fund under most normal circumstances will have contractual remedies pursuant to the agreements related to the transaction. However, exercising such contractual rights may involve delays or costs which could result in the net asset value of the Fund being less than if the Fund had not entered into the transaction. Furthermore, there is a risk that any of such counterparties could become insolvent and/or the subject of insolvency proceedings. In such case, the recovery of the Fund’s collateral from such counterparty or the payment of claims therefor may be significantly delayed and the Fund may recover substantially less than the full value of the collateral entrusted to such counterparty. In addition, there are a number of proposed rules that, if they were to go into effect, may impact the laws that apply to insolvency proceeding and may impact whether the Fund may terminate its agreement with an insolvent counterparty.

Credit Risk. A company may not be able to repay its debt. The Funds invest primarily in “high yield” securities and loans (i.e., rated below Baa3 or BBB- by one or more nationally recognized statistical rating organizations or are unrated but are of comparable credit quality to obligations rated below investment-grade). High yield securities and loans have greater credit risk than more highly rated debt obligations and have a greater possibility that an adverse change in the financial condition of the issuer or the economy may impair the ability of the issuer to make payments of principal and interest. Bankruptcy and similar laws applicable to issuers of the high yield securities and loans may also limit the amount of a Fund’s recovery if the issuer becomes insolvent. High yield securities and loans have historically experienced greater default rates than has been the case for investment-grade securities.

Impairment of Collateral Risk. The value of any collateral securing a bond or loan can decline, and may be insufficient to meet the borrower’s obligations or difficult to liquidate. In addition, a Fund’s access to collateral may be limited by bankruptcy or other insolvency laws. Further, certain floating rate loans may not be fully collateralized and may decline in value.

Interest Rate Risk. Each Fund’s investments in fixed-income instruments will change in value based on changes in interest rates. When interest rates decline, the value of a portfolio invested in fixed-rate obligations can be expected to rise. Conversely, when interest rates rise, the value of a portfolio investment in fixed-rate obligations can be expected to decline. Although the value of each Fund’s investments will vary, the fluctuations in value of a Fund’s investments in floating rate instruments should be minimized as a result of changes in market interest rates. However, because floating rates on loans and other instruments only reset periodically, changes in prevailing interest rates can still be expected to cause some fluctuation in the value of a Fund.

Over the past several years, the Federal Reserve has maintained the level of interest rates at or near historic lows. However, more recently, interest rates have begun to increase as a result of action that has been taken by the Federal Reserve, which has raised, and may continue to raise, interest rates. If interest rates rise, the Fund’s yield may not increase proportionately, and the maturities of fixed income securities that have the ability to be prepaid or called by the issuer may be extended. Changing interest rates may have unpredictable effects on the

22

markets and the Fund’s investments. A general rise in interest rates may cause investors to move out of fixed income securities on a large scale, which could adversely affect the price and liquidity of fixed income securities. The Fund may be exposed to heightened interest rate risk as interest rates rise from historically low levels. Fluctuations in interest rates may also affect the liquidity of fixed income securities and instruments held by the Fund.

Investment Risk. Neither Fund is a complete investment program and you may lose money by investing in the Funds. Each Fund invests primarily in debt obligations issued by non-investment grade companies that may have significant risks as a result of business, financial, market or legal uncertainties. There can be no assurance that the Advisor will correctly evaluate the nature and magnitude of the various factors that could affect the value of, and return on, a Fund’s investments. Prices of the investments held by the Funds may be volatile, and a variety of other factors that are inherently difficult to predict, such as domestic or international economic and political developments, may significantly affect the results of a Fund’s activities and the value of its investments.

Liquidity Risk. Low or lack of trading volume may make it difficult to sell instruments held by the Funds at quoted market prices. The Funds’ investments may at any time consist of significant amounts of positions that are thinly traded or for which no market exists. For example, the investments held by a Fund may not be liquid in all circumstances so that, in volatile markets, the Advisor may not be able to close out a position without incurring a loss. The foregoing risks may be accentuated when the Funds are required to liquidate positions to meet withdrawal requests. Additionally, floating rate loans generally are subject to legal or contractual restrictions on resale, may trade infrequently, and their value may be impaired when the Funds need to liquidate such loans. High yield bonds and loans generally trade only in the over-the-counter market rather than on an organized exchange and may be more difficult to purchase or sell at a fair price, which could have a negative impact on a Fund’s performance.

Convertible Bond Risk. Convertible bonds are hybrid securities that have characteristics of both bonds and common stocks and are therefore subject to both debt security risk and conversion value-related equity risk. Convertible bonds are similar to other fixed-income securities because they usually pay a fixed interest rate and are obligated to repay principal on a given date in the future. The market value of fixed-income securities tends to decline as interest rates increase. Convertible bonds are particularly sensitive to changes in interest rates when their conversion to equity feature is small relative to the interest and principal value of the bond. Convertible issuers may not be able to make principal and interest payments on the bond as they become due. Convertible bonds may also be subject to prepayment or redemption risk. If a convertible bond held by a Fund is called for redemption, the Fund will be required to surrender the security for redemption and convert it into the issuing company’s common stock or cash at a time that may be unfavorable to the Fund. Convertible securities have characteristics similar to common stocks especially when their conversion value is greater than the interest and principal value of the bond. The prices of equity securities may rise or fall because of economic or political changes. Stock prices in general may decline over short or even extended periods of time. Market prices of equity securities in broad market segments may be adversely affected by a prominent issuer having experienced losses or by the lack of earnings or such an issuer’s failure to meet the market’s expectations with respect to new products or services, or even by factors wholly unrelated to the value or condition of the issuer, such as changes in interest rates. When a convertible bond’s value is more closely tied to its conversion to stock feature, it is sensitive to the underlying stock’s price.

Foreign Instruments Risk. Foreign companies may differ from domestic companies in the same industry. Foreign companies or entities are frequently not subject to accounting and financial reporting standards applicable to U.S. companies, and there may be less information available about foreign issuers. Securities of foreign issuers are generally less liquid and more volatile than those of comparable domestic issuers. Investment in foreign issuers includes risks such as less social, political and economic stability; smaller securities markets and lower trading volume, which may result in less liquidity and greater price volatility; national policies that may restrict a Fund’s’ investment opportunities, including restrictions on investments in issuers or industries, or expropriation or confiscation of assets or property; less developed legal structures governing private or foreign investment; and the imposition of foreign exchange limitations (including currency blockage). The exchange rates between the U.S. dollar and foreign currencies might fluctuate, which could negatively affect the value of the Fund’s investments.

23

Management Risk. Each Fund is an actively managed portfolio The Advisor’s management practices and investment strategies might not work to produce the desired results. The success of a Fund is largely dependent upon the ability of the Advisor to manage the Fund and implement the Fund’s investment program. If a Fund were to lose the services of the Advisor or its senior officers, the Fund may be adversely affected. Additionally, if a Fund or any of the other accounts managed by the Advisor were to incur substantial losses or were subject to an unusually high level of redemptions or withdrawals, the revenues of the Advisor may decline substantially. Such losses and/or withdrawals may impair the Advisor’s ability to retain employees and its ability to provide the same level of service to a Fund as it has in the past and continue operations.

Market Risk. The prices of some or all of the instruments in which the Funds invest may decline for a number of reasons, including in response to economic developments and perceptions about the creditworthiness of individual issuers. The success of each Fund’s activities will be affected by general economic and market conditions, such as interest rates, availability of credit, credit defaults, inflation rates, commodity prices, economic uncertainty, changes in laws (including laws relating to taxation of each Fund’s investments), trade barriers, currency exchange controls, and national and international political circumstances (including wars, terrorist acts or security operations). These factors may affect the level and volatility of the prices and the liquidity of each Fund’s investments. Volatility or illiquidity could impair each Fund’s profitability or result in losses. The Funds may maintain substantial trading positions that can be adversely affected by the level of volatility in the financial markets. There can be no assurance that what is perceived as an investment opportunity will not, in fact, result in substantial losses. There is more risk that prices will go down for investors investing over short time horizons.

Leverage Risk. Any event that adversely affects the value of an investment, either directly or indirectly would be magnified to the extent that leverage is used. The cumulative effect of the use of leverage, directly or indirectly, in a market that moves adversely to the investments of the entity employing leverage could result in a loss to the Fund that would be greater than if leverage were not employed. Additionally, any leverage obtained, if terminated on short notice by the lender, could result in the Fund being forced to unwind positions quickly and at prices below what the Fund deems to be fair value for the positions.

Preferred Stock Risk. The value of preferred stocks may decline due to general market conditions which are not specifically related to a particular company or to factors affecting a particular industry or industries. Preferred stocks may be more volatile than fixed-income securities and are more correlated with the issuer’s underlying common stock than fixed-income securities. While most preferred stocks pay a dividend, the Funds may purchase preferred stock where the issuer has omitted, or is in danger of omitting, payment of its dividend.

Rule 144A Securities Risk. The market for Rule 144A securities typically is less active than the market for public securities. Rule 144A securities carry the risk that the trading market may not continue and the Funds might be unable to dispose of these securities promptly or at reasonable prices and might thereby experience difficulty satisfying redemption requirements.

U.S. Government Obligations Risk. Securities issued by U.S. government agencies or government-sponsored entities may not be guaranteed by the U.S. Treasury. The Government National Mortgage Association (“GNMA”), a wholly owned U.S. government corporation, is authorized to guarantee, with the full faith and credit of the U.S. government, the timely payment of principal and interest on securities issued by institutions approved by GNMA and backed by pools of mortgages insured by the Federal Housing Administration or the Department of Veterans Affairs. U.S. government agencies or government-sponsored entities (i.e., not backed by the full faith and credit of the U.S. government) include the Federal National Mortgage Association (“FNMA”) and the Federal Home Loan Mortgage Corporation (“FHLMC”). Pass-through securities issued by FNMA are guaranteed as to timely payment of principal and interest by FNMA but are not backed by the full faith and credit of the U.S. government. FHLMC guarantees the timely payment of interest and ultimate collection of principal, but its participation certificates are not backed by the full faith and credit of the U.S. government. If a government-sponsored entity is unable to meet its obligations, the performance of the Funds may be adversely impacted. U.S. government obligations are viewed as having minimal or no credit risk but are still subject to interest rate risk.

24