Form 485BPOS ETF Series Solutions

Tweet

Tweet Share

ShareFiled with the U.S. Securities and Exchange Commission on November 28, 2022

1933 Act Registration File No. 333-179562

1940 Act File No. 811-22668

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | [X] | ||||||||||

| Pre-Effective Amendment No. | [ ] | ||||||||||

| Post-Effective Amendment No. | 838 | [X] | |||||||||

and

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | [X] | ||||||||||

| Amendment No. | 839 | [X] | |||||||||

(Check appropriate box or boxes.)

(Exact Name of Registrant as Specified in Charter)

615 East Michigan Street, Milwaukee, Wisconsin 53202

(Address of Principal Executive Offices)

(Registrant’s Telephone Number, including Area Code): (414) 516-1645

Kristina R. Nelson, President

ETF Series Solutions

c/o U.S. Bank Global Fund Services

777 East Wisconsin Avenue, 10th Floor

Milwaukee, Wisconsin 53202

(Name and Address of Agent for Service)

Copy to:

Christopher D. Menconi

Morgan, Lewis & Bockius LLP

1111 Pennsylvania Avenue, NW

Washington, DC 20004-2541

As soon as practical after the effective date of this Registration Statement

(Approximate Date of Proposed Public Offering)

It is proposed that this filing will become effective

| ¨ | immediately upon filing pursuant to paragraph (b) | ||||

| x | on November 30, 2022 pursuant to paragraph (b) | ||||

| ¨ | 60 days after filing pursuant to paragraph (a)(1) | ||||

| ¨ | on ______________ pursuant to paragraph (a)(1) | ||||

| ¨ | 75 days after filing pursuant to paragraph (a)(2) | ||||

| ¨ | on pursuant to paragraph (a)(2) of Rule 485. | ||||

If appropriate, check the following box

[ ] this post-effective amendment designates a new effective date for a previously filed post-effective amendment.

(VEGN )

Listed on NYSE Arca, Inc.

PROSPECTUS

The U.S. Securities and Exchange Commission (“SEC”) has not approved or disapproved of these securities or passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

US Vegan Climate ETF

TABLE OF CONTENTS

US Vegan Climate ETF - Fund Summary | |||||

US VEGAN CLIMATE ETF - FUND SUMMARY

Management Fees | |||||

Distribution and/or Service (12b-1) Fees | |||||

Other Expenses | |||||

Total Annual Fund Operating Expenses | |||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||||

| $ | $ | $ | $ | ||||||||

The Fund uses a “passive management” (or indexing) approach to track the performance, before fees and expenses, of the Index. The Index was developed in 2018 by Beyond Advisors IC (the “Index Provider”), the index provider and parent to the Fund’s investment adviser, Beyond Investing LLC (the “Adviser”), and is designed to implement a set of rules that seek to address the concerns of vegans, animal lovers, and environmentalists by avoiding investments in companies whose activities directly contribute to animal suffering, destruction of the natural environment, and climate change.

Beyond Investing US Vegan Climate Index

The Index’s construction begins with the constituents of the Solactive US Large Cap Index, consisting of approximately 500 of the largest U.S.-listed companies (the “Large Cap Equity Universe”). From the Large Cap Equity Universe, companies are excluded from the Index if they derive more than a de minimis proportion (i.e., more than 2%, generally) of their total revenue from products and services directly related to one or more of the following areas of concern (the “Prohibited Activities”):

2

Animals | • Animal testing • Animal-derived products, animal farming, and other exploitation activities • Animals in sport and entertainment • Research, development, and use of genetically engineered animals | ||||

| Planet | • Extraction or refining, or services principally related to the extraction or refining, of fossil fuels • Burning of fossil fuels for energy production • Other activities having a significant negative environmental impact (e.g., high carbon intensity activities, high climate change impact, habitat destruction), unless the applicable company undertakes positive initiatives that effectively counteract those impacts (e.g., having publicly announced and undertaken policies upon which the company provides regular reporting that enables the public to measure the degree to which the environmental impact has been reduced) | ||||

People | • Production of tobacco products • Armaments and products specifically designed for military and defense uses • Contributions to the abuse of human rights or lack of robust, detailed, and independently published policies covering human rights and child/forced labor | ||||

If a company’s primary business line implicates one or more Prohibited Activities, such company will automatically be excluded from the Index. If a company is engaged in multiple business lines, the identification of Prohibited Activities will be based on the company’s published materials, regulatory filings, websites, and product catalogues. If such additional sources do not objectively determine whether a company is engaged in Prohibited Activities, the company will be asked directly about its engagement in Prohibited Activities. Additionally, financial firms, accounting firms, and business service providers that provide services to companies excluded from the Index due to participation in Prohibited Activities are excluded from the Index if a disproportionately high portion of such service provider’s total revenue or business activities (as compared to the portion of revenue or business activities of other service providers) is from such excluded companies or if such service provider’s services are specifically targeted at companies involved in Prohibited Activities.

The remaining companies in the Large Cap Equity Universe (the “Large Cap Constituents”) are initially market capitalization weighted. All Large Cap Constituents with an initial market capitalization weight greater than 1.5% will have their weight adjusted to ensure that no company’s weight exceeds 5% at the time of each semi-annual reconstitution of the Index and to reallocate excess weight to such companies with weights above 1.5% but below the 5% threshold.

If after weighting the Large Cap Constituents as described above, the weight of any industry group in the Index would be more than 2% below the weight of the corresponding industry group of the Solactive US Large Cap Index, the Index will add the next largest securities from that industry group in the Solactive US Large & Mid Cap Index that are not engaged in Prohibited Activities (based on the same rules applicable to the Large Cap Constituents), one by one, and weight them based on their market capitalization until the weight of the applicable industry group in the Index is within 0.5% of the weight of the corresponding industry group of the Solactive US Large Cap Index.

As of October 31, 2022, there were 250 companies in the Index and a significant portion of the Index was comprised of companies in the communications services, financial, and information technology sectors.

The Index is reconstituted based on the above-described methodology on the first Wednesday of each June and December, based on data as of ten business days prior to each reconstitution.

The Fund’s Investment Strategy

The Fund will generally use a “replication” strategy to achieve its investment objective, meaning it generally will invest in all of the component securities of the Index in approximately the same proportion as in the Index. However, the Fund may use a “representative sampling” strategy, meaning it may invest in a sample of the securities in the Index whose risk, return and other characteristics closely resemble the risk, return and other characteristics of the Index as a whole, when the Fund’s sub-adviser believes it is in the best interests of the Fund (e.g., when replicating the Index involves practical difficulties or substantial costs, an Index constituent becomes temporarily illiquid, unavailable, or less liquid, or as a result of legal restrictions or limitations that apply to the Fund but not to the Index).

The Fund generally may invest in securities or other investments not included in the Index, but which the Fund’s sub-adviser believes will help the Fund track the Index and that do not derive more than a de minimis proportion of their total revenue from Prohibited Activities. For example, the Fund may invest in securities that are not components of the Index to reflect various corporate actions and other changes to the Index (such as reconstitutions, additions, and deletions).

3

The principal risks of investing in the Fund are summarized below. The principal risks are presented in alphabetical order to facilitate finding particular risks and comparing them with other funds. Each risk summarized below is considered a “principal risk” of investing in the Fund, regardless of the order in which it appears. As with any investment, there is a risk that you could lose all or a portion of your investment in the Fund. Some or all of these risks may adversely affect the Fund’s net asset value per share (“NAV”), trading price, yield, total return and/or ability to meet its objectives. For more information about the risks of investing in the Fund, see the section in the Fund’s Prospectus titled “Additional Information About the Fund.”

•Concentration Risk. The Fund’s investments will be concentrated in an industry or group of industries to the extent that the Index is so concentrated. In such event, the value of the Shares may rise and fall more than the value of shares of a fund that invests in securities of companies in a broader range of industries.

•Equity Market Risk. The equity securities held in the Fund’s portfolio may experience sudden, unpredictable drops in value or long periods of decline in value. This may occur because of factors that affect securities markets generally or factors affecting specific issuers, industries, or sectors in which the Fund invests. Common stocks are generally exposed to greater risk than other types of securities, such as preferred stock and debt obligations, because common stockholders generally have inferior rights to receive payment from issuers. In addition, local, regional or global events such as war, including Russia’s invasion of Ukraine, acts of terrorism, spread of infectious diseases or other public health issues, recessions, rising inflation, or other events could have a significant negative impact on the Fund and its investments. For example, the global pandemic caused by COVID-19, a novel coronavirus, and the aggressive responses taken by many governments, including closing borders, restricting international and domestic travel, and the imposition of prolonged quarantines or similar restrictions, has had negative impacts, and in many cases severe impacts, on markets worldwide. The COVID-19 pandemic has caused prolonged disruptions to the normal business operations of companies around the world and the impact of such disruptions is hard to predict. Such events may affect certain geographic regions, countries, sectors and industries more significantly than others. Such events could adversely affect the prices and liquidity of the Fund’s portfolio securities or other instruments and could result in disruptions in the trading markets.

•ETF Risks. The Fund is an ETF, and, as a result of an ETF’s structure, it is exposed to the following risks:

•Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk. The Fund has a limited number of financial institutions that may act as Authorized Participants (“APs”). In addition, there may be a limited number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events occur, Shares may trade at a material discount to NAV and possibly face delisting: (i) APs exit the business or otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business activities and no other entities step forward to perform their functions.

•Costs of Buying or Selling Shares. Due to the costs of buying or selling Shares, including brokerage commissions imposed by brokers and bid-ask spreads, frequent trading of Shares may significantly reduce investment results and an investment in Shares may not be advisable for investors who anticipate regularly making small investments.

•Shares May Trade at Prices Other Than NAV. As with all ETFs, Shares may be bought and sold in the secondary market at market prices. Although it is expected that the market price of Shares will approximate the Fund’s NAV, there may be times when the market price of Shares is more than the NAV intra-day (premium) or less than the NAV intra-day (discount) due to supply and demand of Shares or during periods of market volatility. This risk is heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading activity for Shares in the secondary market, in which case such premiums or discounts may be significant.

•Trading. Although Shares are listed for trading on NYSE Arca, Inc. (the “Exchange”) and may be traded on U.S. exchanges other than the Exchange, there can be no assurance that Shares will trade with any volume, or at all, on any stock exchange. In stressed market conditions, the liquidity of Shares may begin to mirror the liquidity of the Fund’s underlying portfolio holdings, which can be significantly less liquid than Shares, and this could lead to differences between the market price of the Shares and the underlying value of those Shares.

•Index Risk. Because the methodology of the Index selects securities of issuers for non-financial reasons, the Fund may underperform the broader equity market or other funds that do not utilize such criteria when selecting investments. Although the Index is designed to avoid investing in companies whose primary business line implicates one or more Prohibited Activities, there is no assurance that the Index or Fund will be able to avoid such securities at all times or that companies that have historically met the Index’s criteria will continue to exhibit such characteristics in the future.

•Large-Capitalization Companies Risk. The securities of large-capitalization companies may be relatively mature compared to smaller companies and therefore subject to slower growth during times of economic expansion.

•Mid-Capitalization Companies Risk. The securities of mid-capitalization companies may be more vulnerable to adverse issuer, market, political, or economic developments than securities of large-capitalization companies. The securities of mid-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than large capitalization stocks or the stock market as a whole.

•Passive Investment Risk. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets. As a result, the Fund’s performance may be adversely affected by a general decline in the market segments relating to its Index.

•Sector Risk. To the extent the Fund invests more heavily in particular sectors of the economy, its performance will be especially sensitive to developments that significantly affect those sectors.

•Communications Services Sector Risk. Communications services companies are subject to extensive government regulation. The costs of complying with governmental regulations, delays or failure to receive required regulatory approvals, or the enactment of new adverse regulatory requirements may adversely affect the business of such companies. Companies in the communications services sector can also be significantly affected by intense competition, including competition with alternative technologies such as wireless communications (including 5G and other technologies), product compatibility, consumer preferences, rapid product obsolescence, and research and development of new products.

•Financial Sector Risk. This sector can be significantly affected by changes in interest rates, government regulation, the rate of defaults on corporate, consumer and government debt, the availability and cost of capital, and fallout from the housing and sub-prime mortgage crisis. Insurance companies, in particular, may be significantly affected by changes in interest rates, catastrophic events, price and market competition, the imposition of premium rate caps, or other changes in government regulation or tax law and/or rate regulation, which may have an adverse impact on their profitability. This sector has experienced significant losses in the recent past, and the impact of more stringent capital requirements and of recent or future regulation on any individual financial company or on the sector as a whole cannot be predicted. In recent years, cyber attacks and technology malfunctions and failures have become increasingly frequent in this sector and have caused significant losses.

•Information Technology Sector Risk. Market or economic factors impacting information technology companies and companies that rely heavily on technological advances could have a significant effect on the value of the Fund’s investments. The value of stocks of information technology companies and companies that rely heavily on technology is particularly vulnerable to rapid changes in technology product cycles, rapid product obsolescence, government regulation and competition, both domestically and internationally, including competition from foreign competitors with lower production costs. Stocks of information technology companies and companies that rely heavily on technology, especially those of smaller, less-seasoned companies, tend to be more volatile than the overall market. Information technology companies are heavily dependent on patent and intellectual property rights, the loss or impairment of which may adversely affect profitability.

5

| US Vegan Climate ETF | 1 Year | Since Inception ( | ||||||

S&P 500® Index | ||||||||

Management

Adviser | Beyond Investing LLC (“Beyond” or the “Adviser”) | ||||

| Sub-Adviser | Penserra Capital Management, LLC (“Penserra” or the “Sub-Adviser”) | ||||

| Portfolio Managers | Dustin Lewellyn, CFA, Managing Director of Penserra; Ernesto Tong, CFA, Managing Director of Penserra; and Anand Desai, Associate of Penserra have been portfolio managers of the Fund since its inception in 2019. | ||||

6

Purchase and Sale of Shares

Shares are listed on the Exchange, and individual Shares may only be bought and sold in the secondary market through brokers at market prices, rather than NAV. Because Shares trade at market prices rather than NAV, Shares may trade at a price greater than NAV (premium) or less than NAV (discount).

The Fund issues and redeems Shares at NAV only in large blocks known as “Creation Units,” which only APs (typically, broker-dealers) may purchase or redeem. The Fund generally issues and redeems Creation Units in exchange for a portfolio of securities and/or a designated amount of U.S. cash.

Investors may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase Shares (bid) and the lowest price a seller is willing to accept for Shares (ask) when buying or selling Shares in the secondary market (the “bid-ask spread”). Recent information about the Fund, including its NAV, market price, premiums and discounts, and bid-ask spreads is available on the Fund’s website at www.veganetf.com.

Tax Information

Fund distributions are generally taxable as ordinary income, qualified dividend income, or capital gains (or a combination), unless your investment is in an individual retirement account (“IRA”) or other tax-advantaged account. Distributions on investments made through tax-deferred arrangements may be taxed later upon withdrawal of assets from those accounts.

Financial Intermediary Compensation

If you purchase Shares through a broker-dealer or other financial intermediary (such as a bank) (an “Intermediary”), the Adviser or its affiliates may pay Intermediaries for certain activities related to the Fund, including participation in activities that are designed to make Intermediaries more knowledgeable about exchange traded products, including the Fund, or for other activities, such as marketing, educational training or other initiatives related to the sale or promotion of Shares. These payments may create a conflict of interest by influencing the Intermediary and your salesperson to recommend the Fund over another investment. Any such arrangements do not result in increased Fund expenses. Ask your salesperson or visit the Intermediary’s website for more information.

ADDITIONAL INFORMATION ABOUT THE FUND

Investment Objective. The Fund’s investment objective has been adopted as a non-fundamental investment policy and may be changed without shareholder approval upon written notice to shareholders.

Additional Information about the Index. Beyond Advisors IC (the “Index Provider”), the parent company to the Adviser, provides the Index to the Fund. The Index Provider created and is responsible for maintaining and applying the rules-based methodology of the Index. The Index is calculated by Solactive AG (the “Index Calculation Agent”), an independent third-party that is not affiliated with the Fund, the Index Provider, the Adviser, the Sub-Adviser, the Fund’s distributor, or any of their respective affiliates. The Index Calculation Agent provides information to the Fund about the Index constituents and does not provide investment advice with respect to the desirability of investing in, purchasing, or selling securities.

Additional Information About the Fund’s Principal Investment Strategies. The Fund has adopted the following policy to comply with Rule 35d-1 under the Investment Company Act of 1940 (the “1940 Act”). Such policy has been adopted as a non-fundamental investment policy and may be changed without shareholder approval upon 60 days’ written notice to shareholders. Under normal circumstances, at least 80% of the Fund’s net assets, plus borrowings for investment purposes, will be invested in securities that are traded principally in the United States.

Additional Information About the Principal Risks of Investing in the Fund. This section provides additional information regarding the principal risks described in the Fund Summary. As in the Fund Summary, the principal risks below are presented in alphabetical order to facilitate finding particular risks and comparing them with other funds. Each risk described below is considered a “principal risk” of investing in the Fund, regardless of the order in which it appears. Each of the factors below could have a negative impact on the Fund’s performance and trading prices.

•Concentration Risk. The Fund’s investments will be concentrated in an industry or group of industries to the extent that the Index is so concentrated. In such event, the value of the Shares may rise and fall more than the value of shares of a fund that invests in securities of companies in a broader range of industries.

7

•Equity Market Risk. Common stocks are susceptible to general stock market fluctuations and to volatile increases and decreases in value as market confidence in and perceptions of their issuers change. These investor perceptions are based on various and unpredictable factors including: expectations regarding government, economic, monetary and fiscal policies; inflation and interest rates; economic expansion or contraction; local, regional or global events such as acts of terrorism or war, including Russia’s invasion of Ukraine; and global or regional political, economic, public health, and banking crises. If you held common stock, or common stock equivalents, of any given issuer, you would generally be exposed to greater risk than if you held preferred stocks and debt obligations of the issuer because common stockholders, or holders of equivalent interests, generally have inferior rights to receive payments from issuers in comparison with the rights of preferred stockholders, bondholders, and other creditors of such issuers.

Beginning in the first quarter of 2020, financial markets in the United States and around the world experienced extreme and, in many cases, unprecedented volatility and severe losses due to the global pandemic caused by COVID-19, a novel coronavirus. The pandemic resulted in a wide range of social and economic disruptions, including closed borders, voluntary or compelled quarantines of large populations, stressed healthcare systems, reduced or prohibited domestic or international travel, and supply chain disruptions affecting the United States and many other countries. Some sectors of the economy and individual issuers have experienced particularly large losses as a result of these disruptions, and such disruptions may continue for an extended period of time or reoccur in the future to a similar or greater extent. In response, the U.S. government and the Federal Reserve have taken extraordinary actions to support the domestic economy and financial markets. Many countries, including the U.S., are subject to few restrictions related to the spread of COVID-19. It is unknown how long circumstances related to the pandemic will persist, whether they will reoccur in the future, whether efforts to support the economy and financial markets will be successful, and what additional implications may follow from the pandemic. The impact of these events and other epidemics or pandemics in the future could adversely affect Fund performance.

•ETF Risks. The Fund is an ETF, and, as a result of an ETF’s structure, it is exposed to the following risks:

•APs, Market Makers, and Liquidity Providers Concentration Risk. The Fund has a limited number of financial institutions that may act as APs. In addition, there may be a limited number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events occur, Shares may trade at a material discount to NAV and possibly face delisting: (i) APs exit the business or otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business activities and no other entities step forward to perform their functions.

•Costs of Buying or Selling Shares. Investors buying or selling Shares in the secondary market will pay brokerage commissions or other charges imposed by brokers, as determined by that broker. Brokerage commissions are often a fixed amount and may be a significant proportional cost for investors seeking to buy or sell relatively small amounts of Shares. In addition, secondary market investors will also incur the cost of the difference between the price at which an investor is willing to buy Shares (the “bid” price) and the price at which an investor is willing to sell Shares (the “ask” price). This difference in bid and ask prices is often referred to as the “spread” or “bid-ask spread.” The bid-ask spread varies over time for Shares based on trading volume and market liquidity, and the spread is generally lower if Shares have more trading volume and market liquidity and higher if Shares have little trading volume and market liquidity. Further, a relatively small investor base in the Fund, asset swings in the Fund, and/or increased market volatility may cause increased bid-ask spreads. Due to the costs of buying or selling Shares, including bid-ask spreads, frequent trading of Shares may significantly reduce investment results and an investment in Shares may not be advisable for investors who anticipate regularly making small investments.

•Shares May Trade at Prices Other Than NAV. As with all ETFs, Shares may be bought and sold in the secondary market at market prices. Although it is expected that the market price of Shares will approximate the Fund’s NAV, there may be times when the market price and the NAV vary significantly, including due to supply and demand of the Fund’s Shares and/or during periods of market volatility. Thus, you may pay more (or less) than NAV intra-day when you buy Shares in the secondary market, and you may receive more (or less) than NAV when you sell those Shares in the secondary market. This risk is heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading activity for Shares in the secondary market, in which case such premiums or discounts may be significant.

•Trading. Although Shares are listed for trading on the Exchange and may be listed or traded on U.S. and non-U.S. stock exchanges other than the Exchange, there can be no assurance that an active trading market for such Shares will develop or be maintained. Trading in Shares may be halted due to market conditions or for reasons that, in the

8

view of the Exchange, make trading in Shares inadvisable. In addition, trading in Shares on the Exchange is subject to trading halts caused by extraordinary market volatility pursuant to Exchange “circuit breaker” rules, which temporarily halt trading on the Exchange when a decline in the S&P 500® Index during a single day reaches certain thresholds (e.g., 7%, 13%, and 20%). Additional rules applicable to the Exchange may halt trading in Shares when extraordinary volatility causes sudden, significant swings in the market price of Shares. There can be no assurance that Shares will trade with any volume, or at all, on any stock exchange. In stressed market conditions, the liquidity of Shares may begin to mirror the liquidity of the Fund’s underlying portfolio holdings, which can be significantly less liquid than Shares, and this could lead to differences between the market price of the Shares and the underlying value of those Shares.

•Index Risk. Because the methodology of the Index selects securities of issuers for nonfinancial reasons, the Fund may underperform the broader equity market or other funds that do not utilize such criteria when selecting investments. Although the Index is designed to avoid investing in companies whose activities directly contribute to animal suffering, destruction of the natural environment, and climate change, there is no assurance that the Index or Fund will be able to avoid such securities at all times or that companies that have historically met the Index’s criteria will continue to exhibit such characteristics in the future. The Index relies on various sources of information regarding an issuer, including information that may be based on assumptions and estimates. Neither the Fund nor the Adviser can offer assurances that the Index’s calculation methodology or sources of information will provide an accurate assessment of the issuers of the securities included in the Index.

•Market Capitalization Risk.

•Large-Capitalization Investing. The securities of large-capitalization companies may be relatively mature compared to smaller companies and therefore subject to slower growth during times of economic expansion. Large-capitalization companies may also be unable to respond quickly to new competitive challenges, such as changes in technology and consumer tastes.

•Mid-Capitalization Investing. The securities of mid-capitalization companies may be more vulnerable to adverse issuer, market, political, or economic developments than securities of large-capitalization companies, but they may also be subject to slower growth than small-capitalization companies during times of economic expansion. The securities of mid-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than large capitalization stocks or the stock market as a whole, but they may also be nimbler and more responsive to new challenges than large-capitalization companies. Some mid-capitalization companies have limited product lines, markets, financial resources, and management personnel and tend to concentrate on fewer geographical markets relative to large-capitalization companies.

•Passive Investment Risk. The Fund invests in the securities included in, or representative of, the Index regardless of their investment merit. The Fund does not attempt to outperform the Index or take defensive positions in declining markets. As a result, the Fund’s performance may be adversely affected by a general decline in the market segments relating to the Index. The returns from the types of securities in which the Fund invests may underperform returns from the various general securities markets or different asset classes. This may cause the Fund to underperform other investment vehicles that invest in different asset classes. Different types of securities (for example, large-, mid- and small-capitalization stocks) tend to go through cycles of doing better – or worse – than the general securities markets. In the past, these periods have lasted for as long as several years.

•Sector Risk. The Fund’s investing approach may result in an emphasis on certain sectors or sub-sectors of the market at any given time. To the extent the Fund invests more heavily in one sector or sub-sector of the market, it thereby presents a more concentrated risk and its performance will be especially sensitive to developments that significantly affect those sectors or sub-sectors. In addition, the value of Shares may change at different rates compared to the value of shares of a fund with investments in a more diversified mix of sectors and industries. An individual sector or sub-sector of the market may have above-average performance during particular periods, but it may also move up and down more than the broader market. The several industries that constitute a sector may all react in the same way to economic, political or regulatory events. The Fund’s performance could also be affected if the sectors or sub-sectors do not perform as expected. Alternatively, the lack of exposure to one or more sectors or sub-sectors may adversely affect performance.

•Communications Services Sector Risk. Communications services companies are subject to extensive government regulation. The costs of complying with governmental regulations, delays or failure to receive required regulatory approvals, or the enactment of new adverse regulatory requirements may adversely affect the business of such companies. Companies in the communications services sector can also be significantly affected by intense competition, including competition with alternative technologies such as wireless communications (including 5G

9

and other technologies), product compatibility, consumer preferences, rapid product obsolescence, and research and development of new products.

•Financial Sector Risk. Companies in the financial sector of an economy are often subject to extensive governmental regulation and intervention, which may adversely affect the scope of their activities, the prices they can charge and the amount of capital they must maintain. Governmental regulation may change frequently and may have significant adverse consequences for companies in the financial sector, including effects not intended by such regulation. The impact of recent or future regulation in various countries on any individual financial company or on the sector as a whole cannot be predicted.

Certain risks may impact the value of investments in the financial sector more severely than those of investments outside this sector, including the risks associated with companies that operate with substantial financial leverage. Companies in the financial sector may also be adversely affected by increases in interest rates and loan losses, decreases in the availability of money or asset valuations, credit rating downgrades and adverse conditions in other related markets.

Insurance companies, in particular, may be subject to severe price competition and/or rate regulation, which may have an adverse impact on their profitability. Insurance companies are subject to extensive government regulation in some countries and can be significantly affected by changes in interest rates, general economic conditions, price and marketing competition, the imposition of premium rate caps, or other changes in government regulation or tax law. Different segments of the insurance industry can be significantly affected by mortality and morbidity rates, environmental clean-up costs and catastrophic events such as earthquakes, hurricanes and terrorist acts.

The financial sector is also a target for cyber attacks and may experience technology malfunctions and disruptions. In recent years, cyber attacks and technology failures have become increasingly frequent and have caused significant losses.

•Information Technology Sector Risk. Market or economic factors impacting information technology companies and companies that rely heavily on technological advances could have a significant effect on the value of the Fund’s investments. The value of stocks of information technology companies and companies that rely heavily on technology is particularly vulnerable to rapid changes in technology product cycles, rapid product obsolescence, government regulation and competition, both domestically and internationally, including competition from foreign competitors with lower production costs. Stocks of information technology companies and companies that rely heavily on technology, especially those of smaller, less-seasoned companies, tend to be more volatile than the overall market. Information technology companies are heavily dependent on patent and intellectual property rights, the loss or impairment of which may adversely affect profitability. Additionally, companies in the technology sector may face dramatic and often unpredictable changes in growth rates and competition for the services of qualified personnel.

•Tracking Error Risk. As with all index funds, the performance of the Fund and the Index may differ from each other for a variety of reasons. For example, the Fund incurs operating expenses and portfolio transaction costs not incurred by the Index. In addition, the Fund may not be fully invested in the securities of the Index at all times or may hold securities not included in the Index.

PORTFOLIO HOLDINGS INFORMATION

Information about the Fund’s daily portfolio holdings is available at www.veganetf.com. A complete description of the Fund’s policies and procedures with respect to the disclosure of the Fund’s portfolio holdings is available in the Fund’s Statement of Additional Information (“SAI”).

MANAGEMENT

Adviser

Beyond Investing LLC serves as the investment adviser and has overall responsibility for the general management and administration of the Fund. The Adviser is a registered investment adviser with offices located at 14391 Spring Hill Drive, Suite 301, Spring Hill, Florida 34609. The Adviser also arranges for sub-advisory, transfer agency, custody, fund administration, and all other related services necessary for the Fund to operate. The Adviser is a subsidiary of Beyond Advisors IC.

The Adviser provides oversight of the Sub-Adviser, monitoring of the Sub-Adviser’s buying and selling of securities for the Fund, and review of the Sub-Adviser’s performance. For the services it provides to the Fund, the Fund pays the Adviser a

10

unified management fee, which is calculated daily and paid monthly, at an annual rate of 0.60% of the Fund’s average daily net assets.

Under the Investment Advisory Agreement, the Adviser has agreed to pay all expenses of the Fund except for interest charges on any borrowings, dividends and other expenses on securities sold short, taxes, brokerage commissions and other expenses incurred in placing orders for the purchase and sale of securities and other investment instruments, acquired fund fees and expenses, accrued deferred tax liability, extraordinary expenses, distribution fees and expenses paid by the Fund under any distribution plan adopted pursuant to Rule 12b-1 under the 1940 Act, and the unified management fee payable to the Adviser.

The basis for the Board’s approval of the Fund’s Investment Advisory Agreement is available in the Fund’s Annual Report to Shareholders dated July 31, 2022.

Sub-Adviser

The Adviser has retained Penserra Capital Management, LLC to serve as sub-adviser for the Fund. The Sub-Adviser is responsible for the day-to-day management of the Fund. The Sub-Adviser is a registered investment adviser and New York limited liability company whose principal office is located at 4 Orinda Way, Suite 100-A, Orinda, California 94563. The Sub-Adviser provides investment management services to investment companies and other investment advisers. The Sub-Adviser is responsible for trading portfolio securities for the Fund, including selecting broker-dealers to execute purchase and sale transactions or in connection with any rebalancing or reconstitution of the Index, subject to the supervision of the Adviser and the Board. For its services, the Sub-Adviser is paid a fee by the Adviser, which fee is calculated daily and paid monthly, at an annual rate of the Fund’s average daily net assets of 0.05% on the first $100 million; 0.04% on the next $150 million; 0.03% on the next $250 million; and 0.02% on net assets in excess of $500 million, subject to a minimum annual fee of $20,000.

The basis for the Board’s approval of the Fund’s Investment Sub-Advisory Agreement is available in the Fund’s Annual Report to Shareholders dated July 31, 2022.

Portfolio Managers

Dustin Lewellyn, CFA, Managing Director of the Sub-Adviser, Ernesto Tong, CFA, Managing Director of the Sub-Adviser, and Anand Desai, Associate of the Sub-Adviser, are the Fund’s portfolio managers (the “Portfolio Managers”) and are jointly responsible for the day to day management of the Fund. The Portfolio Managers are responsible for various functions related to portfolio management, including, but not limited to, investing cash inflows, implementing investment strategy, researching and reviewing investment strategy, and overseeing members of their portfolio management team with more limited responsibilities.

Mr. Lewellyn has been a Managing Director with the Sub-Adviser since 2012. He was President and Founder of Golden Gate Investment Consulting LLC from 2011 through 2015. Prior to that, Mr. Lewellyn was a managing director at Charles Schwab Investment Management, Inc. (“CSIM”), which he joined in 2009, and head of portfolio management for Schwab ETFs. Prior to joining CSIM, he worked for two years as director of ETF product management and development at a major financial institution focused on asset and wealth management. Prior to that, he was a portfolio manager for institutional clients at a financial services firm for three years. In addition, he held roles in portfolio accounting and portfolio management at a large asset management firm for more than 6 years.

Mr. Tong has been a Managing Director with the Sub-Adviser since 2015. Prior to joining the Sub-Adviser, Mr. Tong spent seven years as a vice president at Blackrock, where he was a portfolio manager for a number of the iShares ETFs, and prior to that, he spent two years in the firm’s index research group.

Mr. Desai has been an Associate with the Sub-Adviser since 2015. Prior to joining the Sub-Adviser, Mr. Desai spent five years as a portfolio fund accountant at State Street.

The SAI provides additional information about the Portfolio Managers’ compensation structure, other accounts managed by the Portfolio Managers, and the Portfolio Managers’ ownership of Shares.

HOW TO BUY AND SELL SHARES

The Fund issues and redeems Shares at NAV only in Creation Units. Only APs may acquire Shares directly from the Fund, and only APs may tender their Shares for redemption directly to the Fund, at NAV. APs must be a member or participant of a clearing agency registered with the SEC and must execute a Participant Agreement that has been agreed to by the Distributor (defined below), and that has been accepted by the Fund’s transfer agent, with respect to purchases and redemptions of Creation Units. Once created, Shares trade in the secondary market in quantities less than a Creation Unit.

11

Most investors buy and sell Shares in secondary market transactions through brokers. Shares are listed for trading on the secondary market on the Exchange and can be bought and sold throughout the trading day like other publicly traded securities.

When buying or selling Shares through a broker, you will incur customary brokerage commissions and charges, and you may pay some or all of the bid-ask spread on your transactions. In addition, because secondary market transactions occur at market prices, you may pay more than NAV when you buy Shares and receive less than NAV when you sell those Shares.

Book-Entry

Shares are held in book-entry form, which means that no stock certificates are issued. The Depository Trust Company (“DTC”) or its nominee is the record owner of all outstanding Shares.

Investors owning Shares are beneficial owners as shown on the records of DTC or its participants. DTC serves as the securities depository for all Shares. DTC’s participants include securities brokers and dealers, banks, trust companies, clearing corporations and other institutions that directly or indirectly maintain a custodial relationship with DTC. As a beneficial owner of Shares, you are not entitled to receive physical delivery of stock certificates or to have Shares registered in your name, and you are not considered a registered owner of Shares. Therefore, to exercise any right as an owner of Shares, you must rely upon the procedures of DTC and its participants. These procedures are the same as those that apply to any other securities that you hold in book entry or “street name” through your brokerage account.

Frequent Purchases and Redemptions of Shares

The Fund imposes no restrictions on the frequency of purchases and redemptions of Shares. In determining not to approve a written, established policy, the Board evaluated the risks of market timing activities by Fund shareholders. Purchases and redemptions by APs, who are the only parties that may purchase or redeem Shares directly with the Fund, are an essential part of the ETF process and help keep Share trading prices in line with NAV. As such, the Fund accommodates frequent purchases and redemptions by APs. However, the Board has also determined that frequent purchases and redemptions for cash may increase tracking error and portfolio transaction costs and may lead to the realization of capital gains. To minimize these potential consequences of frequent purchases and redemptions, the Fund employs fair value pricing and may impose transaction fees on purchases and redemptions of Creation Units to cover the custodial and other costs incurred by the Fund in effecting trades. In addition, the Fund and the Adviser reserve the right to reject any purchase order at any time.

Determination of NAV

The Fund’s NAV is calculated as of the scheduled close of regular trading on the New York Stock Exchange (“NYSE”), generally 4:00 p.m. Eastern time, each day the NYSE is open for business. The NAV is calculated by dividing the Fund’s net assets by its Shares outstanding.

In calculating its NAV, the Fund generally values its assets on the basis of market quotations, last sale prices, or estimates of value furnished by a pricing service or brokers who make markets in such instruments. If such information is not available for a security held by the Fund or is determined to be unreliable, the security will be valued by the Adviser at fair value pursuant to procedures established by the Adviser and approved by the Board (as described below).

Fair Value Pricing

The Adviser has been designated by the Board as the valuation designee for the Fund pursuant to Rule 2a-5 under the 1940 Act. In its capacity as valuation designee, the Adviser has adopted procedures and methodologies to fair value Fund securities whose market prices are not “readily available” or are deemed to be unreliable. For example, such circumstances may arise when: (i) a security has been de-listed or has had its trading halted or suspended; (ii) a security’s primary pricing source is unable or unwilling to provide a price; (iii) a security’s primary trading market is closed during regular market hours; or (iv) a security’s value is materially affected by events occurring after the close of the security’s primary trading market. The Board has appointed the Adviser as the Fund’s valuation designee to perform all fair valuations of the Fund’s portfolio investments, subject to the Board’s oversight. Accordingly, the Adviser has established procedures for its fair valuation of the Fund’s portfolio investments. Generally, when fair valuing a security held by the Fund, the Adviser will take into account all reasonably available information that may be relevant to a particular valuation including, but not limited to, fundamental analytical data regarding the issuer, information relating to the issuer’s business, recent trades or offers of the security, general and/or specific market conditions and the specific facts giving rise to the need to fair value the security. Fair value determinations are made in good faith and in accordance with the fair value methodologies established by the Adviser. Due to the subjective and variable nature of determining the fair value of a security or other investment, there can be no assurance that the Adviser’s fair value will match or closely correlate to any market quotation that subsequently becomes available or

12

the price quoted or published by other sources. In addition, the Fund may not be able to obtain the fair value assigned to the security upon the sale of such security.

Investments by Registered Investment Companies

Section 12(d)(1) of the 1940 Act restricts investments by registered investment companies in the securities of other investment companies, including Shares. Registered investment companies are permitted to invest in the Fund beyond the limits set forth in section 12(d)(1) subject to certain terms and conditions set forth in Rule 12d1-4 under the 1940 Act, including that such investment companies enter into an agreement with the Fund.

Delivery of Shareholder Documents – Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents, please contact your broker-dealer. If you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

DIVIDENDS, DISTRIBUTIONS, AND TAXES

Dividends and Distributions

The Fund intends to pay out dividends, if any, quarterly and distribute any net realized capital gains, if any, to its shareholders at least annually. The Fund will declare and pay capital gain distributions, if any, in cash. Distributions in cash may be reinvested automatically in additional whole Shares only if the broker through whom you purchased Shares makes such option available. Your broker is responsible for distributing the income and capital gain distributions to you.

Taxes

The following discussion is a summary of some important U.S. federal income tax considerations generally applicable to investments in the Fund. Your investment in the Fund may have other tax implications. Please consult your tax advisor about the tax consequences of an investment in Shares, including the possible application of foreign, state, and local tax laws.

The Fund intends to elect and qualify each year for treatment as a regulated investment company (“RIC”) under the Code. If it meets certain minimum distribution requirements, a RIC is not subject to tax at the fund level on income and gains from investments that are timely distributed to shareholders. However, the Fund’s failure to qualify as a RIC or to meet minimum distribution requirements would result (if certain relief provisions were not available) in fund-level taxation and, consequently, a reduction in income available for distribution to shareholders.

Unless your investment in Shares is made through a tax-exempt entity or tax-advantaged account, such as an IRA, you need to be aware of the possible tax consequences when the Fund makes distributions, when you sell your Shares listed on the Exchange, and when you purchase or redeem Creation Units (APs only).

Taxes on Distributions. The Fund intends to distribute, at least annually, substantially all of its net investment income and net capital gains. For federal income tax purposes, distributions of investment income are generally taxable as ordinary income or qualified dividend income. Taxes on distributions of capital gains (if any) are determined by how long the Fund owned the investments that generated them, rather than how long a shareholder has owned his or her Shares. Sales of assets held by the Fund for more than one year generally result in long-term capital gains and losses, and sales of assets held by the Fund for one year or less generally result in short-term capital gains and losses. Distributions of the Fund’s net capital gain (the excess of net long-term capital gains over net short-term capital losses) that are reported by the Fund as capital gain dividends (“Capital Gain Dividends”) will be taxable as long-term capital gains, which for non-corporate shareholders are subject to tax at reduced rates of up to 20% (lower rates apply to individuals in lower tax brackets). Distributions of short-term capital gain will generally be taxable as ordinary income. Dividends and distributions are generally taxable to you whether you receive them in cash or reinvest them in additional Shares.

13

Distributions reported by the Fund as “qualified dividend income” are generally taxed to non-corporate shareholders at rates applicable to long-term capital gains, provided holding period and other requirements are met. “Qualified dividend income” generally is income derived from dividends paid by U.S. corporations or certain foreign corporations that are either incorporated in a U.S. possession or eligible for tax benefits under certain U.S. income tax treaties. In addition, dividends that the Fund received in respect of stock of certain foreign corporations may be qualified dividend income if that stock is readily tradable on an established U.S. securities market. Dividends received by the Fund from an ETF, a REIT, or an underlying fund taxable as a RIC may be treated as qualified dividend income generally only to the extent so reported by such ETF, REIT or underlying fund. Corporate shareholders may be entitled to a dividends received deduction for the portion of dividends they receive from the Fund that are attributable to dividends received by the Fund from U.S. corporations, subject to certain limitations.

Shortly after the close of each calendar year, you will be informed of the amount and character of any distributions received from the Fund.

U.S. individuals with income exceeding specified thresholds are subject to a 3.8% tax on all or a portion of their “net investment income,” which includes interest, dividends, and certain capital gains (generally including capital gains distributions and capital gains realized on the sale of Shares). This 3.8% tax also applies to all or a portion of the undistributed net investment income of certain shareholders that are estates and trusts.

In general, your distributions are subject to federal income tax for the year in which they are paid. Certain distributions paid in January, however, may be treated as paid on December 31 of the prior year. Distributions are generally taxable even if they are paid from income or gains earned by the Fund before your investment (and thus were included in the Shares’ NAV when you purchased your Shares).

You may wish to avoid investing in the Fund shortly before a dividend or other distribution, because such a distribution will generally be taxable even though it may economically represent a return of a portion of your investment.

If the Fund’s distributions exceed its earnings and profits, all or a portion of the distributions made for a taxable year may be recharacterized as a return of capital to shareholders. A return of capital distribution will generally not be taxable, but will reduce each shareholder’s cost basis in Shares and result in a higher capital gain or lower capital loss when the Shares are sold. After a shareholder’s basis in Shares has been reduced to zero, distributions in excess of earnings and profits in respect of those Shares will be treated as gain from the sale of the Shares.

If you are neither a resident nor a citizen of the United States or if you are a foreign entity, distributions (other than Capital Gain Dividends) paid to you by the Fund will generally be subject to a U.S. withholding tax at the rate of 30%, unless a lower treaty rate applies. Gains from the sale or other disposition of Shares by non-U.S. shareholders generally are not subject to U.S. taxation, unless you are a nonresident alien individual who is physically present in the U.S. for 183 days or more per year. The Fund may, under certain circumstances, report all or a portion of a dividend as an “interest-related dividend” or a “short-term capital gain dividend,” which would generally be exempt from this 30% U.S. withholding tax, provided certain other requirements are met. Different tax consequences may result if you are a foreign shareholder engaged in a trade or business within the United States or if a tax treaty applies.

The Fund (or a financial intermediary, such as a broker, through which a shareholder owns Shares) generally is required to withhold and remit to the U.S. Treasury a percentage of the taxable distributions and sale or redemption proceeds paid to any shareholder who fails to properly furnish a correct taxpayer identification number, who has underreported dividend or interest income, or who fails to certify that the shareholder is not subject to such withholding.

Taxes When Shares are Sold on the Exchange. Provided that a shareholder holds Shares as capital assets, any capital gain or loss realized upon a sale of Shares generally is treated as a long-term capital gain or loss if Shares have been held for more than one year and as a short-term capital gain or loss if Shares have been held for one year or less. However, any capital loss on a sale of Shares held for six months or less is treated as long-term capital loss to the extent of Capital Gain Dividends paid with respect to such Shares. Any loss realized on a sale will be disallowed to the extent Shares of the Fund are acquired, including through reinvestment of dividends, within a 61-day period beginning 30 days before and ending 30 days after the disposition of Shares. The ability to deduct capital losses may be limited.

The cost basis of Shares of the Fund acquired by purchase will generally be based on the amount paid for the Shares and then may be subsequently adjusted for other applicable transactions as required by the Code. The difference between the selling price and the cost basis of Shares generally determines the amount of the capital gain or loss realized on the sale or exchange of Shares. Contact the broker through whom you purchased your Shares to obtain information with respect to the available cost basis reporting methods and elections for your account.

14

Taxes on Purchases and Redemptions of Creation Units. An AP having the U.S. dollar as its functional currency for U.S. federal income tax purposes who exchanges securities for Creation Units generally recognizes a gain or a loss. The gain or loss will be equal to the difference between the value of the Creation Units at the time of the exchange and the exchanging AP’s aggregate basis in the securities delivered, plus the amount of any cash paid for the Creation Units. An AP who exchanges Creation Units for securities will generally recognize a gain or loss equal to the difference between the exchanging AP’s basis in the Creation Units and the aggregate U.S. dollar market value of the securities received, plus any cash received for such Creation Units. The Internal Revenue Service may assert, however, that a loss that is realized upon an exchange of securities for Creation Units may not be currently deducted under the rules governing “wash sales” (for an AP who does not mark-to-market its holdings), or on the basis that there has been no significant change in economic position. APs exchanging securities should consult their own tax advisor with respect to whether wash sales rules apply and when a loss might be deductible.

The Fund may include a payment of cash in addition to, or in place of, the delivery of a basket of securities upon the redemption of Creation Units. The Fund may sell portfolio securities to obtain the cash needed to distribute redemption proceeds. This may cause the Fund to recognize investment income and/or capital gains or losses that it might not have recognized if it had completely satisfied the redemption in-kind. As a result, the Fund may be less tax efficient if it includes such a cash payment in the proceeds paid upon the redemption of Creation Units.

The foregoing discussion summarizes some of the possible consequences under current federal tax law of an investment in the Fund. It is not a substitute for personal tax advice. You also may be subject to state and local tax on Fund distributions and sales of Shares. Consult your personal tax advisor about the potential tax consequences of an investment in Shares under all applicable tax laws. For more information, please see the section entitled “Federal Income Taxes” in the SAI.

DISTRIBUTION

The Distributor, Quasar Distributors, LLC, is a broker-dealer registered with the SEC. The Distributor distributes Creation Units for the Fund on an agency basis and does not maintain a secondary market in Shares. The Distributor has no role in determining the policies of the Fund or the securities that are purchased or sold by the Fund. The Distributor’s principal address is 111 East Kilbourn Avenue, Suite 2200, Milwaukee, Wisconsin 53202.

The Board has adopted a Distribution and Service Plan (the “Plan”) pursuant to Rule 12b-1 under the 1940 Act. In accordance with the Plan, the Fund is authorized to pay an amount up to 0.25% of its average daily net assets each year for certain distribution-related activities and shareholder services.

No Rule 12b-1 fees are currently paid by the Fund, and there are no plans to impose these fees. However, in the event Rule 12b-1 fees are charged in the future, because the fees are paid out of the Fund’s assets, over time these fees will increase the cost of your investment and may cost you more than certain other types of sales charges.

PREMIUM/DISCOUNT INFORMATION

Information regarding how often Shares traded on the Exchange at a price above (i.e., at a premium) or below (i.e., at a discount) the NAV per Share is available, free of charge, on the Fund’s website at www.veganetf.com.

ADDITIONAL NOTICES

Shares are not sponsored, endorsed, or promoted by the Exchange. The Exchange is not responsible for, nor has it participated in the determination of, the timing, prices, or quantities of Shares to be issued, nor in the determination or calculation of the equation by which Shares are redeemable. The Exchange has no obligation or liability to owners of Shares in connection with the administration, marketing, or trading of Shares.

Without limiting any of the foregoing, in no event shall the Exchange have any liability for any lost profits or indirect, punitive, special, or consequential damages even if notified of the possibility thereof.

The Adviser and the Fund make no representation or warranty, express or implied, to the owners of Shares or any member of the public regarding the advisability of investing in securities generally or in the Fund particularly.

15

FINANCIAL HIGHLIGHTS

The financial highlights table is intended to help you understand the Fund’s financial performance for the Fund’s five most recent fiscal years (or the life of the Fund, if shorter). Certain information reflects financial results for a single Fund share. The total returns in the table represent the rate that an investor would have earned or lost on an investment in the Fund (assuming reinvestment of all dividends and distributions). This information has been audited by Cohen & Company, Ltd., the Fund’s independent registered public accounting firm, whose report, along with the Fund’s financial statements, is included in the Fund’s annual report, which is available upon request.

US Vegan Climate ETF

FINANCIAL HIGHLIGHTS

For a capital share outstanding throughout the year/period

| Year Ended July 31, 2022 | Year Ended July 31, 2021 | Period Ended July 31, 2020(1) | ||||||||||||||||||

Net asset value, beginning of year/period | $ | 40.24 | $ | 28.93 | $ | 25.00 | ||||||||||||||

| INCOME (LOSS) FROM INVESTMENT OPERATIONS: | ||||||||||||||||||||

Net investment income (loss) (2) | 0.22 | 0.20 | 0.27 | |||||||||||||||||

| Net realized and unrealized gain (loss) on investments | (5.01) | 11.31 | 3.87 | |||||||||||||||||

| Total income (loss) from investment operations | (4.79) | 11.51 | 4.14 | |||||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||||||||||

| Distributions from: | ||||||||||||||||||||

| Net investment income | (0.19) | (0.20) | (0.21) | |||||||||||||||||

| Total distributions to shareholders | (0.19) | (0.20) | (0.21) | |||||||||||||||||

| Net asset value, end of year/period | $ | 35.26 | $ | 40.24 | $ | 28.93 | ||||||||||||||

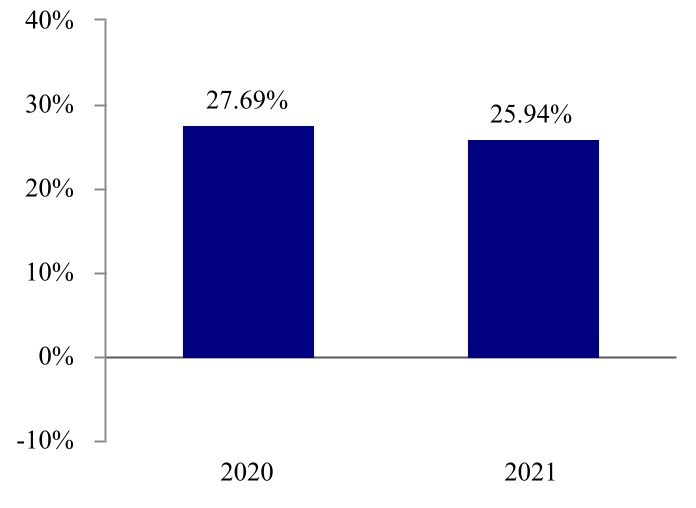

| Total return | -11.94 | % | 39.89 | % | 16.71 | % | (3) | |||||||||||||

| SUPPLEMENTAL DATA: | ||||||||||||||||||||

| Net assets at end of year/period (000’s) | $ | 67,876 | $ | 59,361 | $ | 22,424 | ||||||||||||||

| RATIOS TO AVERAGE NET ASSETS: | ||||||||||||||||||||

| Expenses to average net assets | 0.60 | % | 0.60 | % | 0.60 | % | (4) | |||||||||||||

| Net investment income (loss) to average net assets | 0.56 | % | 0.58 | % | 1.16 | % | (4) | |||||||||||||

Portfolio turnover rate (5) | 17 | % | 22 | % | 18 | % | (3) | |||||||||||||

(1)Commencement of operations on September 9, 2019.

(2)Calculated based on average shares outstanding during the period.

(3)Not annualized.

(4)Annualized.

(5)Excludes the impact of in-kind transactions.

16

US VEGAN CLIMATE ETF

Adviser | Beyond Investing LLC 14391 Spring Hill Drive, Suite 301 Spring Hill, Florida 34609 | Index Provider | Beyond Advisors IC Digital Hub Jersey, Block 3, Ground Floor Grenville Street St. Helier, Jersey JE2 4UF | ||||||||

Sub-Adviser | Penserra Capital Management, LLC 4 Orinda Way, Suite 100-A Orinda, California 94563 | Transfer Agent, Administrator, and Index Receipt Agent | U.S. Bancorp Fund Services, LLC d/b/a U.S. Bank Global Fund Services 615 East Michigan Street Milwaukee, Wisconsin 53202 | ||||||||

Custodian | U.S. Bank National Association 1555 N. Rivercenter Dr., Suite 302 Milwaukee, Wisconsin 53212 | Distributor | Quasar Distributors, LLC 111 East Kilbourn Avenue, Suite 2200 Milwaukee, Wisconsin 53202 | ||||||||

Legal Counsel | Morgan, Lewis & Bockius LLP 1111 Pennsylvania Avenue, NW Washington, DC 20004-2541 | Independent Registered Public Accounting Firm | Cohen & Company, Ltd. 342 North Water Street, Suite 830 Milwaukee, Wisconsin 53202 | ||||||||

Investors may find more information about the Fund in the following documents:

Statement of Additional Information: The Fund’s SAI provides additional details about the investments and techniques of the Fund and certain other additional information. A current SAI dated November 30, 2022, as supplemented from time to time, is on file with the SEC and is herein incorporated by reference into this Prospectus. It is legally considered a part of this Prospectus.

Annual/Semi-Annual Reports: Additional information about the Fund’s investments is available in the Fund’s annual and semi-annual reports to shareholders. In the annual report you will find a discussion of the market conditions and investment strategies that significantly affected the Fund’s performance.

You can obtain free copies of these documents, request other information or make general inquiries about the Fund by contacting the Fund at US Vegan Climate ETF, c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, Wisconsin 53201-0701 or calling 1-800-617-0004.

Shareholder reports and other information about the Fund are also available:

•Free of charge from the SEC’s EDGAR database on the SEC’s website at http://www.sec.gov; or

•Free of charge from the Fund’s Internet website at www.veganetf.com; or

•For a fee, by e-mail request to [email protected].

(SEC Investment Company Act File No. 811-22668)

17

US Vegan Climate ETF

(VEGN)

a series of ETF Series Solutions

Listed on NYSE Arca, Inc.

STATEMENT OF ADDITIONAL INFORMATION

November 30, 2022

This Statement of Additional Information (“SAI”) is not a prospectus and should be read in conjunction with the Prospectus for the US Vegan Climate ETF (the “Fund”), a series of ETF Series Solutions (the “Trust”), dated November 30, 2022, as may be supplemented from time to time (the “Prospectus”). Capitalized terms used in this SAI that are not defined have the same meaning as in the Prospectus, unless otherwise noted. A copy of the Prospectus may be obtained without charge, by calling the Fund at 800‑617‑0004, visiting www.veganetf.com, or writing to the Fund, c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, Wisconsin 53201-0701.

The Fund’s audited financial statements for the most recent fiscal year are incorporated into this SAI by reference to the Fund’s most recent Annual Report to Shareholders (File No. 811-22668). When available, you may obtain a copy of the Fund’s Annual Report at no charge by contacting the Fund at the address or phone number noted above.

TABLE OF CONTENTS

Appendix A – Proxy Voting Policies | A-1 | ||||

1

GENERAL INFORMATION ABOUT THE TRUST

The Trust is an open-end management investment company consisting of multiple investment series. This SAI relates to the Fund. The Trust was organized as a Delaware statutory trust on February 9, 2012. The Trust is registered with the U.S. Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940, as amended (together with the rules and regulations adopted thereunder, as amended, the “1940 Act”), as an open-end management investment company and the offering of the Fund’s shares (“Shares”) is registered under the Securities Act of 1933, as amended (the “Securities Act”). The Trust is governed by its Board of Trustees (the “Board”). Beyond Investing LLC (the “Adviser”) serves as investment adviser to the Fund, Beyond Advisors IC (the “Index Provider”) is the index provider to the Fund, and Penserra Capital Management, LLC (“Penserra” or the “Sub-Adviser”) serves as sub-adviser to the Fund. The investment objective of the Fund is to seek to track the performance, before fees and expenses, of its underlying Index.

The Fund offers and issues Shares at their net asset value (“NAV”) only in aggregations of a specified number of Shares (each, a “Creation Unit”). The Fund generally offers and issues Shares in exchange for a basket of securities included in its Index (“Deposit Securities”) together with the deposit of a specified cash payment (“Cash Component”). The Trust reserves the right to permit or require the substitution of a “cash in lieu” amount (“Deposit Cash”) to be added to the Cash Component to replace any Deposit Security. Shares are listed on the NYSE Arca, Inc. (the “Exchange”) and trade on the Exchange at market prices that may differ from the Shares’ NAV. Shares are also redeemable only in Creation Unit aggregations, primarily for a basket of Deposit Securities together with a Cash Component. A Creation Unit of the Fund generally consists of 25,000 Shares, though this may change from time to time. As a practical matter, only institutions or large investors purchase or redeem Creation Units. Except when aggregated in Creation Units, Shares are not redeemable securities.

Shares may be issued in advance of receipt of Deposit Securities subject to various conditions, including a requirement to maintain on deposit with the Trust cash at least equal to a specified percentage of the value of the missing Deposit Securities, as set forth in the Participant Agreement (as defined below). The Trust may impose a transaction fee for each creation or redemption. In all cases, such fees will be limited in accordance with the requirements of the SEC applicable to management investment companies offering redeemable securities. As in the case of other publicly traded securities, brokers’ commissions on transactions in the secondary market will be based on negotiated commission rates at customary levels.

ADDITIONAL INFORMATION ABOUT INVESTMENT OBJECTIVES, POLICIES, AND RELATED RISKS

The Fund’s investment objective and principal investment strategies are described in the Prospectus. The following information supplements, and should be read in conjunction with, the Prospectus. For a description of certain permitted investments, see “Description of Permitted Investments” in this SAI.

With respect to the Fund’s investments, unless otherwise noted, if a percentage limitation on investment is adhered to at the time of investment or contract, a subsequent increase or decrease as a result of market movement or redemption will not result in a violation of such investment limitation.

Diversification

The Fund is “diversified” within the meaning of the 1940 Act. Under applicable federal laws, to qualify as a diversified fund, the Fund, with respect to 75% of its total assets, may not invest greater than 5% of its total assets in any one issuer and may not hold greater than 10% of the securities of one issuer, other than investments in cash and cash items (including receivables), U.S. government securities, and securities of other investment companies. The remaining 25% of the Fund’s total assets do not need to be “diversified” and may be invested in securities of a single issuer, subject to other applicable laws. The diversification of the Fund’s holdings is measured at the time the Fund purchases a security. However, if the Fund purchases a security and holds it for a period of time, the security may become a larger percentage of the Fund’s total assets due to movements in the financial markets. If the market affects several securities held by the Fund, the Fund may have a greater percentage of its assets invested in securities of a single issuer or a small number of issuers. However, the Fund intends to satisfy the asset diversification requirements for qualification as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). See “Federal Income Taxes” below for details.

General Risks

The value of the Fund’s portfolio securities may fluctuate with changes in the financial condition of an issuer or counterparty, changes in specific economic or political conditions that affect a particular security or issuer and changes in general economic or political conditions. An investor in the Fund could lose money over short or long periods of time.

There can be no guarantee that a liquid market for the securities held by the Fund will be maintained. The existence of a liquid trading market for certain securities may depend on whether dealers will make a market in such securities. There can be no assurance that a market will be made or maintained or that any such market will be or remain liquid. The price at which securities

2

may be sold and the value of Shares will be adversely affected if trading markets for the Fund’s portfolio securities are limited or absent, or if bid-ask spreads are wide.

Cyber Security Risk. Investment companies, such as the Fund, and their service providers may be subject to operational and information security risks resulting from cyber attacks. Cyber attacks include, among other behaviors, stealing or corrupting data maintained online or digitally, denial of service attacks on websites, the unauthorized release of confidential information or various other forms of cyber security breaches. Cyber attacks affecting the Fund or the Adviser, Sub-Adviser, custodian, transfer agent, intermediaries and other third-party service providers may adversely impact the Fund. For instance, cyber attacks may interfere with the processing of shareholder transactions, impact the Fund’s ability to calculate its NAV, cause the release of private shareholder information or confidential company information, impede trading, subject the Fund to regulatory fines or financial losses, and cause reputational damage. The Fund may also incur additional costs for cyber security risk management purposes. Similar types of cyber security risks are also present for issuers of securities in which the Fund invests, which could result in material adverse consequences for such issuers, and may cause the Fund’s investments in such portfolio companies to lose value.