Form 485BPOS AB INSTITUTIONAL FUNDS

Tweet

Tweet Share

Share

| THE SECURITIES ACT OF 1933 | ☐ | |||

| Pre-Effective Amendment No. | ☐ |

| Post-Effective Amendment No. 43 | ☒ |

| Amendment No. 44 | ☒ |

| ☐ |

immediately upon filing pursuant to paragraph (b)

|

| ☒ |

on

|

| ☐ |

60 days after filing pursuant to paragraph (a)

|

| ☐ |

on (date) pursuant to paragraph (a)

|

| ☐ |

75 days after filing pursuant to paragraph (a)(2)

|

| ☐ |

on (date) pursuant to paragraph (a)(2) of Rule 485.

|

| ☐ |

This post-effective amendment designates a new effective date for a previously filed post-effective amendment.

|

|

AB Global Real Estate Investment Fund II

(Class I–ARIIX)

|

|

Ø Are Not FDIC Insured

|

|

Ø May Lose Value

|

|

Ø Are Not Bank Guaranteed

|

| Class I | ||||

|

Management Fees

|

||||

|

Distribution and/or Service (12b‑1) Fees

|

||||

|

Other Expenses:

|

||||

|

Transfer Agent

|

||||

|

Other Expenses

|

||||

|

|

|

|||

|

Total Other Expenses

|

||||

|

|

|

|||

|

Total Annual Fund Operating Expenses

|

||||

|

|

|

|||

| Class I | ||||

|

After 1 Year

|

$ | |||

|

After 3 Years

|

$ | |||

|

After 5 Years

|

$ | |||

|

After 10 Years

|

$ | |||

| • |

Market Risk: The value of the Fund’s assets will fluctuate as the stock or bond market fluctuates. The value of its investments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events, including public health crises (including the occurrence of a contagious disease or illness) and regional and global conflicts, that affect large portions of the market.

|

| • |

Real Estate Risk: The Fund’s investments in real estate securities have many of the same risks as direct ownership of real estate, including the risk that the value of real estate could decline due to a variety of factors affecting the real estate market generally. Investments in REITs may have additional risks. REITs are dependent on the capability of their managers, may have limited diversification, and could be significantly affected by changes in taxes. Some REITs may utilize leverage, which increases investment risk and may potentially increase the Fund’s losses.

|

| • |

Foreign (Non‑U.S.) Risk: Investment in securities of non‑U.S. issuers may involve more risk than those of U.S. issuers. These securities may fluctuate more widely in price and may be more difficult to trade due to adverse market, economic, political, regulatory or other factors.

|

| • |

Interest Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of existing investments in fixed-income securities tends to fall, and this decrease in value may not be offset by higher income from new investments. Interest rate risk is generally greater for fixed-income securities with longer maturities or durations. The Fund may be subject to a greater risk of rising interest rates than would normally be the case due to the recent end of a period of historically low rates and the effect of potential central bank monetary policy, and government fiscal policy, initiatives and resulting market reactions to those initiatives.

|

| • |

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security and accrued interest. The degree of risk for a particular security may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security. Investments in fixed-income securities with lower ratings tend to have a higher probability that an issuer will default or fail to meet its payment obligations.

|

| • |

Currency Risk: Fluctuations in currency exchange rates may negatively affect the value of the Fund’s investments or reduce its returns.

|

| • |

Mortgage-Related and/or Other Asset-Backed Securities Risk: Investments in mortgage-related and other asset-backed securities are subject to certain additional risks. The value of these securities may be particularly sensitive to changes in interest rates. These risks include “extension risk”, which is the risk that, in periods of rising interest rates, issuers may delay the payment of principal, and “prepayment risk”, which is the risk that in periods of falling interest rates, issuers may pay principal sooner than expected, exposing the Fund to a lower rate of return upon reinvestment of principal. Mortgage-backed securities offered by non‑governmental issuers and other asset-backed securities may be subject to other risks, such as higher rates of default in the mortgages or assets backing the securities or risks associated with the nature and servicing of mortgages or assets backing the securities.

|

| • |

Derivatives Risk: Derivatives may be difficult to price or unwind and leveraged so that small changes may produce disproportionate losses for the Fund. A short position in a derivative instrument involves the risk of a theoretically unlimited increase in the value of the underlying asset, which could cause the Fund to suffer a potentially unlimited loss. Derivatives, especially over‑the‑counter derivatives, are also subject to counterparty risk, which is the risk that the counterparty (the party on the other side of the transaction) on a derivative transaction will be unable or unwilling to honor its contractual obligations to the Fund.

|

| • |

Leverage Risk: When the Fund borrows money or otherwise leverages its portfolio, it may be more volatile because leverage tends to exaggerate the effect of any increase or decrease in the value of the Fund’s investments. The Fund may create leverage through the use of reverse repurchase agreements or forward commitments, or by borrowing money.

|

| • |

Management Risk: The Fund is subject to management risk because it is an actively-managed investment fund. The Adviser will apply its investment techniques and risk analyses in making investment decisions, but there is no guarantee that its techniques will produce the desired results. Some of these techniques may incorporate, or rely upon, quantitative models, but there is no guarantee that these models will generate accurate forecasts, reduce risk or otherwise perform as expected.

|

| • |

|

| • |

|

| 1 Year | 5 Years | 10 Years | ||||||||||||||

| Class I* | Return Before Taxes | - |

||||||||||||||

|

|

|

|||||||||||||||

| Return After Taxes on Distributions** | - |

- |

||||||||||||||

|

|

|

|||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares** | - |

|||||||||||||||

| S&P 500 Index | - |

|||||||||||||||

|

FTSE EPRA/NAREIT Developed Real Estate Index (net)***

(reflects no deduction for fees, expenses, or taxes except the reinvestment of dividends net of non‑U.S. withholding taxes)

|

- |

- |

||||||||||||||

|

MSCI World Index (net)***

(reflects no deduction for fees, expenses or taxes except the reinvestment of dividends net of non‑U.S. withholding taxes)

|

- |

|||||||||||||||

|

FTSE NAREIT Equity REIT Index***

(reflects no deduction for fees, expenses, or taxes)

|

- |

|||||||||||||||

| * |

|

|

|

|

| ** | After‑tax returns are based on information available to the Fund as of the date of this Prospectus. |

| *** |

| Employee | Length of Service | Title | ||

| Eric J. Franco | Since 2012 | Senior Vice President of the Adviser |

| Initial | Subsequent | |||

| Class I Shares | $10,000* | None |

| * |

Applies to shares purchased through a Bernstein advisor. Otherwise, a $2,000,000 initial purchase minimum applies.

|

| • |

Forward Contracts. A forward contract is an agreement that obligates one party to buy, and the other party to sell, a specific quantity of an underlying commodity or other tangible asset for an agreed-upon price at a future date. A forward contract generally is settled by physical delivery of the commodity or tangible asset to an agreed-upon location (rather than settled by cash), or is rolled forward into a new forward contract or, in the case of a non‑deliverable forward, by a cash payment at maturity. The Fund’s investments in forward contracts may include the following:

|

| – |

Forward Currency Exchange Contracts. The Fund may purchase or sell forward currency exchange contracts for hedging purposes to minimize the risk from adverse changes in the relationship between the U.S. Dollar and other currencies or for non‑hedging purposes as a means

|

|

of making direct investments in foreign currencies, as described below under “Currency Transactions”. The Fund, for example, may enter into a forward contract as a transaction hedge (to “lock in” the U.S. Dollar price of a non‑U.S. Dollar security), as a position hedge (to protect the value of securities the Fund owns that are denominated in a foreign currency against substantial changes in the value of the foreign currency) or as a cross-hedge (to protect the value of securities the Fund owns that are denominated in a foreign currency against substantial changes in the value of that foreign currency by entering into a forward contract for a different foreign currency that is expected to change in the same direction as the currency in which the securities are denominated).

|

| • |

Futures Contracts and Options on Futures Contracts. A futures contract is a standardized, exchange-traded agreement that obligates the buyer to buy and the seller to sell a specified quantity of an underlying asset (or settle for cash the value of a contract based on an underlying asset, rate or index) at a specific price on the contract maturity date. Options on futures contracts are options that call for the delivery of futures contracts upon exercise. The Fund may purchase or sell futures contracts and options thereon to hedge against changes in interest rates, securities (through index futures or options) or currencies. The Fund may also purchase or sell futures contracts for foreign currencies or options thereon for non‑hedging purposes as a means of making direct investments in foreign currencies, as described below under “Other Derivatives and Strategies—Currency Transactions”.

|

| • |

Options. An option is an agreement that, for a premium payment or fee, gives the option holder (the buyer) the right but not the obligation to buy (a “call option”) or sell (a “put option”) the underlying asset (or settle for cash an amount based on an underlying asset, rate or index) at a specified price (the exercise price) during a period of time or on a specified date. Investments in options are considered speculative. The Fund may lose the premium paid for them if the price of the underlying security or other asset decreased or remained the same (in the case of a call option) or increased or remained the same (in the case of a put option). If a put or call option purchased by the Fund were permitted to expire without being sold or exercised, its premium would represent a loss to the Fund. The Fund’s investments in options include the following:

|

| – |

Options on Foreign Currencies. The Fund may invest in options on foreign currencies that are privately-negotiated or traded on U.S. or foreign exchanges for hedging purposes to protect against declines in the U.S. Dollar value of foreign currency denominated securities held by the Fund and against increases in the U.S. Dollar cost of securities to be acquired. The purchase of an option on a foreign currency may constitute an effective hedge against fluctuations in exchange rates, although if rates move adversely, the Fund may forfeit the entire amount of the premium plus related transaction costs. The Fund may also invest in options on foreign currencies for non‑hedging purposes as a means of making direct investments in foreign currencies, as described below under “Other Derivatives and Strategies—Currency Transactions”.

|

| – |

Options on Securities. The Fund may purchase or write a put or call option on securities. The Fund will only exercise an option it purchased if the price of the security was less (in the case of a put option) or more (in the case of a call option) than the exercise price. If the Fund does not exercise an option, the premium it paid for the option will be lost. The Fund may write covered options, which means writing an option for securities the Fund owns, and uncovered options. The Fund may also enter into options on the yield “spread” or yield differential between two securities. In contrast to other types of options, this option is based on the difference between the yields of designated securities, futures or other instruments. In addition, the Fund may write covered straddles. A straddle is a combination of a call and a put written on the same underlying security. In purchasing an option on securities, the Fund would be in a position to realize a gain if, during the option period, the price of the underlying securities increased (in the case of a call) or decreased (in the case of a put) by an amount in excess of the premium paid; otherwise the Fund would experience a loss not greater than the premium paid for the option. Thus, the Fund would realize a loss if the price of the underlying security declined or remained the same (in the case of a call) or increased or remained the same (in the case of a put) or otherwise did not increase (in the case of a put) or decrease (in the case of a call) by more than the amount of the premium. If a put or call option purchased by the Fund were permitted to expire without being sold or exercised, its premium would represent a loss to the Fund.

|

| – |

Options on Securities Indices. An option on a securities index is similar to an option on a security except that, rather than taking or making delivery of a security at a specified price, an option on a securities index gives the holder the right to receive, upon exercise of the option, an amount of cash if the closing level of the chosen index is greater than (in the case of a call) or less than (in the case of a put) the exercise price of the option.

|

| – |

Other Option Strategies. In an effort to earn extra income, to adjust exposure to individual securities or markets, or to protect all or a portion of its portfolio from a decline in value, sometimes within certain ranges, the Fund may use option strategies such as the concurrent purchase of a call or put option, including on individual

|

|

securities and stock indices, futures contracts (including on individual securities and stock indices) or shares of ETFs at one strike price and the writing of a call or put option on an individual security, the same stock index, futures contract or ETF at a higher strike price in the case of a call option or at a lower strike price in the case of a put option. The maximum profit from this strategy would result for the call options from an increase in the value of an individual security, the stock index, futures contract or ETF above the higher strike price or, for the put options, from the decline in the value of the individual security, stock index, futures contract or ETF below the lower strike price. If the price of the individual security, stock index, futures contract or ETF declines in the case of the call option or increases in the case of the put option, the Fund has the risk of losing the entire amount paid for the call or put options.

|

| • |

Swap Transactions—A swap is an agreement that obligates two parties to exchange a series of cash flows at specified intervals (payment dates) based upon or calculated by reference to changes in specified prices or rates (e.g., interest rates in the case of interest rate swaps or currency exchange rates in the case of currency swaps) for a specified amount of an underlying asset (the “notional” principal amount). Most swaps are entered into on a net basis (i.e., the two payment streams are netted out, with the Fund receiving or paying, as the case may be, only the net amount of the two payments). Generally, the notional principal amount is used solely to calculate the payment stream, but is not exchanged. Certain standardized swaps, including certain interest rate swaps and credit default swaps, are subject to mandatory central clearing and are required to be executed through a regulated swap execution facility. Cleared swaps are transacted through futures commission merchants (“FCMs”) that are members of central clearinghouses with the clearinghouse serving as central counterparty, similar to transactions in futures contracts. Portfolios post initial and variation margin to support their obligations under cleared swaps by making payments to their clearing member FCMs. Central clearing is intended to reduce counterparty credit risks and increase liquidity, but central clearing does not make swap transactions risk free. The Securities and Exchange Commission (the “Commission”) may adopt similar clearing and execution requirements in respect of certain security-based swaps under its jurisdiction. Privately negotiated swap agreements are two‑party contracts entered into primarily by institutional investors and are not cleared through a third party, nor are these required to be executed on a regulated swap execution facility.

|

| – |

Currency Swaps. The Fund may invest in currency swaps for hedging purposes in an attempt to protect against adverse changes in exchange rates between the U.S. Dollar and other currencies or for non‑hedging purposes as a means of making direct investments in foreign currencies, as described below under “Other Derivatives and Strategies—Currency Transactions”. Currency swaps involve the exchange by the Fund with another party of a series of payments in specified currencies. Currency swaps may involve the exchange of actual principal amounts of currencies by the counterparties at the initiation and again upon the termination of the transaction. Currency swaps may be bilateral and privately negotiated, with the Fund expecting to achieve an acceptable degree of correlation between its portfolio investments and its currency swap positions. The Fund will not enter into any currency swap unless the credit quality of the unsecured senior debt or the claims-paying ability of the counterparty thereto is rated in the highest short-term rating category of at least one nationally recognized statistical rating organization (“NRSRO”) at the time of entering into the transaction.

|

| – |

Credit Default Swaps. The “buyer” in a credit default swap contract is obligated to pay the “seller” a periodic stream of payments over the term of the contract in return for a contingent payment upon the occurrence of a credit event with respect to an underlying reference obligation. Generally, a credit event means bankruptcy, failure to pay, obligation acceleration or restructuring. The Fund may be either the buyer or seller in the transaction. If the Fund is a seller, the Fund receives a fixed rate of income throughout the term of the contract, which typically is between one month and ten years, provided that no credit event occurs. If a credit event occurs, the Fund, as seller, typically must pay the contingent payment to the buyer, which will be either: (i) the “par value” (face amount) of the reference obligation in which case the Fund will receive the reference obligation in return or (ii) an amount equal to the difference between the face amount and the current market value of the reference obligation. As a buyer, if a credit event occurs, the Fund would be the receiver of such contingent payments, either delivering the reference obligation in exchange for the full notional (face) value of a reference obligation that may have little or no value, or receiving a payment equal to the difference between the face amount and the current market value of the obligation. The current market value of the reference obligation is typically determined via an auction process sponsored by the International Swaps and Derivatives Association, Inc. The periodic payments received by the Fund, coupled with the value of any reference obligation received, may be less than the full amount it pays to the buyer, resulting in a loss to the Fund. If the Fund is a buyer and no credit event occurs, the Fund will lose its periodic stream of payments over the term of the contract. However, if a credit event occurs, the buyer typically receives full notional value for a reference obligation that may have little or no value.

|

| • |

Other Derivatives and Strategies

|

| – |

Currency Transactions. The Fund may invest in non‑U.S. Dollar-denominated securities on a currency hedged or unhedged basis. The Adviser may actively manage the Fund’s currency exposures and may seek investment opportunities by taking long or short positions in currencies through the use of currency-related derivatives, including forward currency exchange contracts, futures contracts and options on futures contracts, swaps and options. The Adviser may enter into transactions for investment opportunities when it anticipates that a foreign currency will appreciate or depreciate in value but securities denominated in that currency are not held by the Fund and do not present attractive investment opportunities. Such transactions may also be used when the Adviser believes that it may be more efficient than a direct investment in a foreign currency-denominated security. The Fund may also conduct currency exchange contracts on a spot basis (i.e., for cash at the spot rate prevailing in the currency exchange market for buying or selling currencies).

|

| – |

Synthetic Foreign Equity Securities. The Fund may invest in different types of derivatives generally referred to as synthetic foreign equity securities. These securities may include international warrants or local access products. International warrants are financial instruments issued by banks or other financial institutions, which may or may not be traded on a foreign exchange. International warrants are a form of derivative security that may give holders the right to buy or sell an underlying security or a basket of securities representing an index from or to the issuer of the warrant for a particular price or may entitle holders to receive a cash payment relating to the value of the underlying security or index, in each case upon exercise by the Fund. Local access products are similar to options in that they are exercisable by the holder for an underlying security or a cash payment based upon the value of that security, but are generally exercisable over a longer term than typical options. These types of instruments may be American style, which means that they can be exercised at any time on or before the expiration date of the international warrant, or European style, which means that they may be exercised only on the expiration date.

|

|

Argentina

Bangladesh

Belize

Brazil

Bulgaria

Chile

China

Colombia

Croatia

Czech Republic

Dominican Republic

Ecuador

Egypt

El Salvador

Gabon

Georgia

Ghana

Greece

|

Hungary

India

Indonesia

Iraq

Ivory Coast

Jamaica

Jordan

Kazakhstan

Kenya

Lebanon

Lithuania

Malaysia

Mexico

Mongolia

Nigeria

Pakistan

Panama

Peru

|

Philippines

Poland

Qatar

Saudi Arabia

Senegal

Serbia

South Africa

South Korea

Sri Lanka

Taiwan

Thailand

Turkey

Ukraine

United Arab Emirates

Uruguay

Venezuela

Vietnam

|

| • |

Are signed and dated by the person(s) authorized in accordance with the Fund’s policies and procedures to access the account and request transactions;

|

| • |

Include the fund and account number; and

|

| • |

Include the amount of the transaction (stated in dollars, shares, or percentage).

|

| • |

Medallion signature guarantees or notarized signatures, if required for the type of transaction. (Requirements are detailed on AllianceBernstein Investor Services, Inc., or ABIS, service forms; Please contact ABIS with any questions)

|

| • |

Any supporting documentation that may be required.

|

| Purchase Minimums: |

|

—Initial:

|

$ | 10,000 | * | |

|

—Subsequent:

|

None |

| * |

The minimum initial investment may be waived in the discretion of the Fund. The minimum purchase amount applies to shares purchased through a Bernstein advisor. Otherwise, a $2,000,000 initial purchase minimum applies. Investments made through fee‑based or wrap‑fee programs will satisfy the initial investment minimum requirement if the fee‑based or wrap‑fee program, as a whole, invests at least $2,000,000 in the Fund.

|

| • |

through accounts established under a fee‑based program sponsored and maintained by a registered broker-dealer or other financial intermediary and approved by the Fund’s principal underwriter, AllianceBernstein Investments, Inc., or ABI;

|

| • |

if you are an investment advisory client of, or are a certain other person associated with, the Adviser and its affiliate or the Fund; or

|

| • |

as an interest in a “qualified tuition program” within the meaning of Section 529 of the Code approved by ABI.

|

| - |

additional distribution support;

|

| - |

defrayal of costs for educational seminars and training; and

|

| - |

payments related to providing shareholder recordkeeping and/or transfer agency services.

|

| • |

Send a signed letter of instruction or stock power, along with certificates, to:

|

| • |

For certified or overnight deliveries, send to:

|

| • |

For your protection, a bank, a member firm of a national stock exchange, or other eligible guarantor institution, must guarantee signatures. Stock power forms are available from your financial intermediary, ABIS, and many commercial banks. Additional documentation is required for the sale of shares by corporations, intermediaries, fiduciaries, and surviving joint owners. If you have any questions about these procedures, contact ABIS.

|

| • |

You may redeem your shares for which no stock certificates have been issued by telephone request. Call ABIS at (800) 221‑5672 with instructions on how you wish to receive your sale proceeds.

|

| • |

ABIS must receive and confirm a telephone redemption request by the Fund Closing Time for you to receive that day’s NAV.

|

| • |

For your protection, ABIS will request personal or other information from you to verify your identity and will generally record the calls. Neither the Fund nor the Adviser, ABIS, ABI or other Fund agent will be liable for any loss, injury, damage or expense as a result of acting upon telephone instructions purporting to be on your behalf that ABIS reasonably believes to be genuine.

|

| • |

If you have selected electronic funds transfer in your Mutual Fund Application, the redemption proceeds may be sent directly to your bank. Otherwise, the proceeds will be mailed to you.

|

| • |

Redemption requests by electronic funds transfer or check may not exceed $100,000 per Fund account per day.

|

| • |

Telephone redemption is not available for shares held in nominee or “street name” accounts, retirement plan accounts, or shares held by a shareholder who has changed his or her address of record within the previous 30 calendar days.

|

| • |

Transaction Surveillance Procedures. The Fund, through its agents, ABI and ABIS, maintains surveillance procedures to detect excessive or short-term trading in Fund shares. This surveillance process involves several factors, which include scrutinizing transactions in Fund shares that exceed certain monetary thresholds or numerical limits within a specified period of time. Generally, more than two exchanges of Fund shares during any 60‑day period or purchases of shares followed by a sale within 60 days will be identified by these surveillance procedures. For purposes of these transaction surveillance procedures, the Fund may consider trading activity in multiple accounts under common ownership, control or influence. Trading activity identified by either, or a combination, of these factors, or as a result of any other information available at the time, will be evaluated to determine whether such activity might constitute excessive or short-term trading. With respect to managed or discretionary accounts for which the account owner gives his/her broker, investment adviser or other third party authority to buy and sell Fund shares, the Fund may consider trades initiated by the account owner, such as trades initiated in connection with bona fide cash management purposes, separately in their analysis. These surveillance procedures may be modified from time to time, as necessary or appropriate to improve the detection of excessive or short-term trading or to address specific circumstances.

|

| • |

Account Blocking Procedures. If the Fund determines, in its sole discretion, that a particular transaction or pattern of transactions identified by the transaction surveillance procedures described above is excessive or short-term trading in nature, the Fund will take remedial action that may include issuing a warning, revoking certain account-related privileges (such as the ability to place purchase, sale and exchange orders over the internet or by phone) or prohibiting or “blocking” future purchase or exchange activity. However, sales of Fund shares back to the Fund or redemptions will continue to be permitted in accordance with the terms of the Fund’s current Prospectus. As a result, unless the shareholder redeems his or her shares, which may have consequences if the shares have declined in value or adverse tax consequences may result, the shareholder may be “locked” into an unsuitable investment. A blocked account will generally remain blocked for 90 days. Subsequent detections of excessive or short-term trading may result in an indefinite account block or an account block until the account holder or the associated broker, dealer or other financial intermediary provides evidence or assurance acceptable to the Fund that the account holder did not or will not in the future engage in excessive or short-term trading.

|

| • |

Applications of Surveillance Procedures and Restrictions to Omnibus Accounts. Omnibus account arrangements are common forms of holding shares of the Fund, particularly among certain brokers, dealers and other financial intermediaries, including sponsors of retirement plans. The Fund applies its surveillance procedures to these omnibus account arrangements. As required by Commission rules, the Fund has entered into agreements with all of its financial intermediaries that require the financial intermediaries to provide the Fund, upon the request of the Fund or its agents, with individual account level information about their transactions. If the Fund detects excessive trading through its monitoring of omnibus accounts, including trading at the individual account level, the financial intermediaries will also execute instructions from the Fund to take actions to curtail the activity, which may include applying blocks to accounts to prohibit future purchases and exchanges of Fund shares. For certain retirement plan accounts, the Fund may request that the retirement plan or other intermediary revoke the relevant participant’s privilege to effect transactions in Fund shares via the internet or telephone, in which case the relevant participant must submit future transaction orders via the U.S. Postal Service (i.e., regular mail).

|

| Employee; Year; Title |

Principal Occupation(s) During

the Past Five (5) Years

|

|

| Eric J. Franco; since 2012; Senior Vice President of the Adviser | Senior Vice President of the Adviser, with which he has been associated in a substantially similar capacity to his current position since prior to 2018. |

| CLASS I | ||||||||||||||||||||

|

YEAR

ENDED

10/31/22 |

YEAR

ENDED

10/31/21 |

YEAR

ENDED

10/31/20 |

YEAR

ENDED

10/31/19 |

YEAR

ENDED

10/31/18 |

||||||||||||||||

|

Net asset value, beginning of period

|

$ | 12.89 | $ | 9.20 | $ | 12.38 | $ | 10.61 | $ | 11.04 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income From Investment Operations | ||||||||||||||||||||

|

Net investment income(a)(b)

|

.25 | .21 | .21 | .26 | .29 | |||||||||||||||

|

Net realized and unrealized gain (loss) on investment and foreign currency transactions

|

(3.45 | ) | 3.64 | (2.39 | ) | 1.95 | (.08 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Net increase (decrease) in net asset value from operations

|

(3.20 | ) | 3.85 | (2.18 | ) | 2.21 | .21 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Less: Dividends and Distributions | ||||||||||||||||||||

|

Dividends from net investment income

|

(.43 | ) | (.16 | ) | (.48 | ) | (.44 | ) | (.64 | ) | ||||||||||

|

Distributions from net realized gain on investment transactions

|

(.18 | ) | –0– | (.35 | ) | –0– | –0– | |||||||||||||

|

Return of capital

|

–0– | –0– | (.17 | ) | –0– | –0– | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Total dividends and distributions

|

(.61 | ) | (.16 | ) | (1.00 | ) | (.44 | ) | (.64 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Net asset value, end of period

|

$ | 9.08 | $ | 12.89 | $ | 9.20 | $ | 12.38 | $ | 10.61 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Return | ||||||||||||||||||||

|

Total investment return based on net asset value(c)*

|

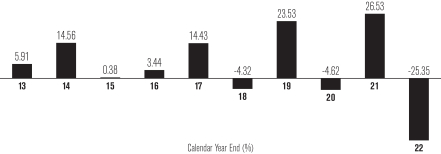

(25.88 | )% | 41.97 | % | (18.80 | )% | 21.50 | % | 1.82 | % | ||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

|

Net assets, end of period (000’s omitted)

|

$ | 175,306 | $ | 259,812 | $ | 215,548 | $ | 351,958 | $ | 287,905 | ||||||||||

|

Ratio to average net assets of:

|

||||||||||||||||||||

|

Expenses, net of waivers/reimbursements

|

.74 | % | .72 | % | .72 | % | .70 | % | .70 | % | ||||||||||

|

Expenses, before waivers/reimbursements

|

.74 | % | .72 | % | .72 | % | .70 | % | .70 | % | ||||||||||

|

Net investment income(b)

|

2.25 | % | 1.76 | % | 2.11 | % | 2.29 | % | 2.66 | % | ||||||||||

|

Portfolio turnover rate

|

53 | % | 46 | % | 48 | % | 64 | % | 70 | % | ||||||||||

| (a) |

Based on average shares outstanding.

|

| (b) |

Net of expenses waived/reimbursed by the Adviser.

|

| (c) |

Total investment return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, and redemption on the last day of the period. Total return does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Total investment return calculated for a period of less than one year is not annualized.

|

| * |

Includes the impact of proceeds received and credited to the Fund resulting from class action settlements, which enhanced the Fund’s performance for the year ended October 31, 2019 by .03%.

|

| Year |

Hypothetical

Investment

|

Hypothetical Performance Earnings |

Investment After Returns |

Hypothetical Expenses |

Hypothetical Ending Investment |

||||||||||||||||||||

|

1

|

$ | 10,000.00 | $ | 500.00 | $ | 10,500.00 | $ | 77.70 | $ | 10,422.30 | |||||||||||||||

|

2

|

10,422.30 | 521.12 | 10,943.42 | 80.98 | 10,862.44 | ||||||||||||||||||||

|

3

|

10,862.44 | 543.12 | 11,405.56 | 84.40 | 11,321.16 | ||||||||||||||||||||

|

4

|

11,321.16 | 566.06 | 11,887.22 | 87.97 | 11,799.25 | ||||||||||||||||||||

|

5

|

11,799.25 | 589.96 | 12,389.21 | 91.68 | 12,297.53 | ||||||||||||||||||||

|

6

|

12,297.53 | 614.88 | 12,912.41 | 95.55 | 12,816.86 | ||||||||||||||||||||

|

7

|

12,816.86 | 640.84 | 13,457.70 | 99.59 | 13,358.11 | ||||||||||||||||||||

|

8

|

13,358.11 | 667.91 | 14,026.02 | 103.79 | 13,922.23 | ||||||||||||||||||||

|

9

|

13,922.23 | 696.11 | 14,618.34 | 108.18 | 14,510.16 | ||||||||||||||||||||

|

10

|

14,510.16 | 725.51 | 15,235.67 | 112.74 | 15,122.93 | ||||||||||||||||||||

|

Cumulative

|

$ | 6,065.51 | $ | 942.58 | |||||||||||||||||||||

| • |

ANNUAL/SEMI-ANNUAL REPORTS TO SHAREHOLDERS

|

| • |

STATEMENT OF ADDITIONAL INFORMATION (SAI)

|

| By Mail: |

AllianceBernstein L.P.

501 Commerce Street

Nashville, TN 37203

|

|

| By Phone: | (212) 486‑5800 | |

| On the Internet: | www.bernstein.com | |

AB INSTITUTIONAL FUNDS, INC.

- AB GLOBAL REAL ESTATE INVESTMENT FUND II

(Class I – ARIIX)

c/o AllianceBernstein Investor Services, Inc.

P.O. Box 786003, San Antonio, Texas 78278-6003

Toll Free (800) 221-5672

For Literature: Toll Free (800) 227-4618

STATEMENT OF ADDITIONAL INFORMATION

January 31, 2023

This Statement of Additional Information (“SAI”) is not a prospectus but supplements and should be read in conjunction with the current prospectus dated January 31, 2023, for AB Global Real Estate Investment Fund II (the “Fund”), a series of AB Institutional Funds, Inc. (the “Company”), that offers Class I shares of the Fund (the “Prospectus”). Financial statements for the Fund for the year ended October 31, 2022 are included in the annual report to shareholders and are incorporated into this SAI by reference. Copies of the Prospectus and annual report may be obtained by contacting AllianceBernstein Investor Services, Inc. (“ABIS”) at the address or the “For Literature” telephone number shown above or on the Internet at www.bernstein.com.

TABLE OF CONTENTS

Page

The [A/B] logo is a service mark of AllianceBernstein and AllianceBernstein® is a registered trademark used by permission of the owner, AllianceBernstein L.P.

Information About The Fund And Its Investments

The Fund is a series of the Company. The Company is an open-end investment company. The Fund is a separate pool of assets constituting, in effect, a separate open-end management investment company with its own investment objective and policies.

Except as otherwise indicated, the investment objective and policies of the Fund are not “fundamental policies” within the meaning of the Investment Company Act of 1940, as amended (the “1940 Act”), and may, therefore, be changed by the Company’s Board of Directors (the “Directors” or the “Board”) without a shareholder vote. However, the Fund will not change its investment objective without at least 60 days’ prior written notice to its shareholders. The Fund is a diversified fund as a matter of fundamental policy. There can be, of course, no assurance that the Fund will achieve its investment objective. Whenever any investment policy or practice, including any restriction, described in the Prospectus or herein states a maximum percentage of the Fund’s assets that may be invested in any security or other asset, it is intended that such maximum percentage limitation be determined immediately after and as a result of the Fund’s acquisition of such securities or other assets. Accordingly, except with respect to borrowing, any later increase or decrease in percentage beyond the specified limitation resulting from a change in values or net assets will not be considered a violation of any such maximum.

Additional Investment Policies and Practices

The following investment policies and practices supplements the information set forth in the Prospectus.

Convertible Securities

Convertible securities include bonds, debentures, corporate notes and preferred stocks that are convertible at a stated exchange rate into shares of the underlying common stock. Prior to their conversion, convertible securities have the same general characteristics as non-convertible debt securities, which provide a stable stream of income with generally higher yields than those of equity securities of the same or similar issuers. As with debt securities, the market value of convertible securities tends to decline as interest rates increase and, conversely, to increase as interest rates decline. While convertible securities generally offer lower interest or dividend yields than non-convertible debt securities of similar quality, they do enable investors to benefit from any increases in the market price of the underlying common stock.

When the market price of the common stock underlying a convertible security increases, the price of the convertible security increasingly reflects the value of the underlying common stock and may rise accordingly. As the market price of the underlying common stock declines, the convertible security tends to trade increasingly on a yield basis, and thus may not depreciate to the same extent as the underlying common stock. Convertible debt and preferred securities rank senior to common stock, and convertible debt securities rank senior to preferred stock, in an issuer’s capital structure. Convertible securities are consequently of higher quality and entail less risk than the issuer’s common stock, although the extent to which such risk is

| 1 |

reduced depends in large measure upon the degree to which the convertible security sells above its value as a fixed-income security.

Derivatives

The Fund may, but is not required to, use derivatives for hedging or other risk management purposes or as part of its investment strategies. Derivatives are financial contracts whose value depends on, or is derived from, the value of an underlying asset, reference rate or index. These assets, rates, and indices may include bonds, stocks, mortgages, commodities, interest rates, currency exchange rates, bond indices and stock indices.

There are four principal types of derivatives¾forwards, futures contracts, options, and swaps. These principal types of derivative instruments, as well as the ways they may be used by the Fund are described below. Derivatives include listed and cleared transactions where the Fund’s derivative trade counterparty is an exchange or clearinghouse, and non-cleared bilateral “over-the-counter” (“OTC”) transactions that are privately negotiated and where the Fund’s derivative trade counterparty is a financial institution. Exchange-traded or cleared derivatives transactions tend to be subject to less counterparty credit risk than those that are bilateral and privately negotiated. The Fund may use derivatives to earn income and enhance returns, to hedge or adjust the risk profile of a portfolio and either to replace more traditional direct investments or to obtain exposure to otherwise inaccessible markets.

Forward Contracts. A forward contract, which may be standardized and exchange-traded or customized and privately negotiated, is an agreement for one party to buy, and the other party to sell, a specific quantity of an underlying security, currency, commodity or other tangible asset for an agreed-upon price at a future date. A forward contract generally is settled by physical delivery of the security, commodity or other asset underlying the forward contract to an agreed-upon location at a future date (rather than settled by cash) or is rolled forward into a new forward contract. Non-deliverable forwards (“NDFs”) specify a cash payment upon maturity.

Futures Contracts and Options on Futures Contracts. A futures contract is an agreement that obligates the buyer to buy and the seller to sell a specified quantity of an underlying asset (or settle for cash the value of a contract based on an underlying asset, rate or index) at a specific price on the contract maturity date. Options on futures contracts are options that call for the delivery of futures contracts upon exercise. Futures contracts are standardized, exchange-traded instruments and are fungible (i.e., considered to be perfect substitutes for each other). This fungibility allows futures contracts to be readily offset or canceled through the acquisition of equal but opposite positions, which is the primary method by which futures contracts are liquidated. A cash-settled futures contract does not require physical delivery of the underlying asset but instead is settled for cash equal to the difference between the values of the contract on the date it is entered into and its maturity date.

Options. An option, which may be standardized and exchange-traded or customized and privately negotiated, is an agreement that, for a premium payment or fee, gives the option holder (the buyer) the right but not the obligation to buy (a “call”) or sell (a “put”) the underlying asset (or settle for cash an amount based on an underlying asset, rate or index) at a

| 2 |

specified price (the exercise price) during a period of time or on a specified date. Likewise, when an option is exercised the writer of the option is obligated to sell (in the case of a call option) or to purchase (in the case of a put option) the underlying asset (or settle for cash an amount based on an underlying asset, rate or index).

Swaps. A swap is an agreement that obligates two parties to exchange a series of cash flows at specified intervals (payment dates) based upon or calculated by reference to changes in specified prices or rates (e.g., interest rates in the case of interest rate swaps, currency exchange rates in the case of currency swaps) for a specified amount of an underlying asset (the “notional” principal amount). Most swaps are entered into on a net basis (i.e., the two payment streams are netted out, with the Fund receiving or paying, as the case may be, only the net amount of the two payments). Generally, the notional principal amount is used solely to calculate the payment streams but is not exchanged. Certain standardized swaps, including certain interest rate swaps and credit default swaps, are subject to mandatory central clearing and are required to be executed through a regulated swap execution facility. Cleared swaps are transacted through futures commission merchants (“FCMs”) that are members of central clearinghouses with the clearinghouse serving as central counterparty, similar to transactions in futures contracts. Funds post initial and variation margin to support their obligations under cleared swaps by making payments to their clearing member FCMs. Central clearing is intended to reduce counterparty credit risks and increase liquidity, but central clearing does not make swap transactions risk free. The Securities and Exchange Commission (“Commission”) may adopt similar clearing and execution requirements in respect of certain security-based swaps under its jurisdiction. Privately negotiated swap agreements are two-party contracts entered into primarily by institutional investors and are not cleared through a third party, nor are these required to be executed on a regulated swap execution facility.

Risks of Derivatives and Other Regulatory Issues. Investment techniques employing such derivatives involve risks different from, and, in certain cases, greater than, the risks presented by more traditional investments. Following is a general discussion of important risk factors and issues concerning the use of derivatives.

-- Market Risk. This is the general risk attendant to all investments that the value of a particular investment will change in a way detrimental to the Fund’s interest.

-- Management Risk. Derivative products are highly specialized instruments that require investment techniques and risk analyses different from those associated with stocks and bonds. The use of a derivative requires an understanding not only of the underlying instrument but also of the derivative itself, without the benefit of observing the performance of the derivative under all possible market conditions. In particular, the use and complexity of derivatives require the maintenance of adequate controls to monitor the transactions entered into, the ability to assess the risk that a derivative adds to the Fund’s investment portfolio, and the ability to forecast price, interest rate or currency exchange rate movements correctly.

| 3 |

-- Credit Risk. This is the risk that a loss may be sustained by the Fund as a result of the failure of another party to a derivative (usually referred to as a “counterparty”) to comply with the terms of the derivative contract. The credit risk for derivatives traded on an exchange or through a clearinghouse is generally less than for uncleared OTC derivatives, since the performance of the exchange or clearinghouse, which is the issuer or counterparty to each derivative, is supported by all the members of such exchange or clearinghouse. The performance of an exchange or clearinghouse is further supported by a daily payment system (i.e., margin requirements) operated by the exchange or clearinghouse in order to reduce overall credit risk. There is no similar intermediary support for uncleared OTC derivatives. Therefore, the Fund will effect transactions in uncleared OTC derivatives only with investment dealers and other financial institutions (such as commercial banks) deemed creditworthy by AllianceBernstein L.P., the Fund’s adviser (the “Adviser”), and the Adviser has adopted procedures for monitoring the creditworthiness of such entities.

-- Counterparty Risk. The value of an OTC derivative will depend on the ability and willingness of the Fund’s counterparty to perform its obligations under the transaction. If the counterparty defaults, the Fund will have contractual remedies but may choose not to enforce them to avoid the cost and unpredictability of legal proceedings. In addition, if a counterparty fails to meet its contractual obligations, the Fund could miss investment opportunities or otherwise be required to retain investments it would prefer to sell, resulting in losses for the Fund. Participants in OTC derivatives markets generally are not subject to the same level of credit evaluation and regulatory oversight as are exchanges or clearinghouses. As a result, OTC derivatives generally expose the Fund to greater counterparty risk than derivatives traded on an exchange or through a clearinghouse.

Recent regulations affecting derivatives transactions require certain standardized derivatives, including many types of swaps, to be subject to mandatory central clearing. Under these requirements, a central clearing organization is substituted as the counterparty to each side of the derivatives transaction. Each party to derivatives transactions is required to maintain its positions with a clearing organization through one or more clearing brokers. Central clearing is intended to reduce, but not eliminate, counterparty risk. The Fund is subject to the risk that its clearing member or clearing organization will itself be unable to perform its obligations. The Fund may also face the indirect risk of the failure of another clearing member customer to meet its obligations to the clearing member, causing a default by the clearing member on its obligations to the clearinghouse.

-- Illiquid Investments Risk. Illiquid investments risk exists when a particular instrument is difficult to purchase, sell or otherwise liquidate. If a derivative transaction is particularly large or if the relevant market is illiquid (as is the case with many privately negotiated derivatives), it may not be possible to initiate a transaction or liquidate a position at an advantageous price.

| 4 |

-- Leverage Risk. Since many derivatives have a leverage component, adverse changes in the value or level of the underlying asset, rate or index can result in a loss substantially greater than the amount invested in the derivative itself. In the case of swaps, the risk of loss generally is related to a notional principal amount, even if the parties have not made any initial investment. Certain derivatives have the potential for unlimited loss, regardless of the size of the initial investment.

-- Regulatory Risk. Various U.S. Government entities, including the Commodity Futures Trading Commission (“CFTC”) and the Commission, are in the process of adopting and implementing additional regulations governing derivatives markets required by, among other things, the Dodd-Frank Act, including clearing as discussed above, margin, reporting and registration requirements. In addition, the Commission has adopted Rule 18f-4 under the 1940 Act, which governs the use of derivatives and certain other forms of leverage by registered investment companies. Rule 18f-4 requires certain funds, among other things, to adopt a comprehensive derivatives risk management program, appoint a derivatives risk manager and comply with a limit on fund leverage risk based on value-at-risk, or “VaR.” Funds that use derivatives in a limited amount are not subject to the full requirements of Rule 18f-4. In addition, Congress, various exchanges and regulatory and self-regulatory authorities have undertaken reviews of futures, options and swaps markets in light of market volatility. Among the actions that have been taken or proposed to be taken are new limits and reporting requirements for speculative positions, new or more stringent daily price fluctuation limits, and increased margin requirements for various types of futures. These regulations and actions may adversely affect the Fund’s ability to execute its investment strategy.

The CFTC has also issued rules requiring certain OTC derivatives transactions that fall within its jurisdiction to be executed through a regulated securities, futures or swap exchange or execution facility. Such requirements may make it more difficult or costly for the Fund to enter into highly tailored or customized transactions. They may also render certain strategies in which the Fund may otherwise engage impossible or so costly that they will not be economical to implement. If the Fund decides to become a direct member of one or more swap exchange or execution facilities, it will be subject to all of the rules of the exchange or execution facility.

European regulation of the derivatives market is also relevant to the extent the Fund engages in derivatives transactions with a counterparty that is subject to the European Market Infrastructure Regulation (“EMIR”). EMIR introduced uniform requirements in respect of OTC derivative contracts by requiring certain “eligible” OTC derivatives contracts to be submitted for clearing to regulated central clearing counterparties and by mandating the reporting of certain details of OTC derivatives contracts to trade repositories. In addition, EMIR imposes risk

| 5 |

mitigation requirements, including requiring appropriate procedures and arrangements to measure, monitor and mitigate operational and counterparty credit risk in respect of OTC derivatives contracts which are not subject to mandatory clearing. These risk mitigation requirements include the exchange, and potentially the segregation, of collateral by the parties, including by a Fund. While many of the obligations under EMIR have come into force, a number of other requirements have not yet come into force or are subject to phase-in periods, and certain key issues have not been resolved. It is therefore not yet fully clear how the OTC derivatives market will ultimately adapt to the new European regulatory regime for OTC derivatives.

-- Other Risks. Other risks in using derivatives include the risk of mispricing or improper valuation of derivatives and the inability of derivatives to correlate perfectly with underlying assets, rates and indices. Many derivatives, in particular privately negotiated derivatives, are complex and often valued subjectively. Improper valuations can result in increased cash payment requirements to counterparties or a loss of value to the Fund. Derivatives do not always perfectly or even highly correlate with or track the value of the assets, rates or indices they are designed to closely track. Consequently, the Fund’s use of derivatives may not always be an effective means of, and sometimes could be counterproductive to, furthering the Fund’s investment objective.

Other. The Fund may purchase and sell derivative instruments only to the extent that such activities are consistent with the requirements of the Commodity Exchange Act (“CEA”) and the rules adopted by the CFTC thereunder. Under CFTC rules, a registered investment company that conducts more than a certain amount of trading in futures contracts, commodity options, certain swaps and other commodity interests is a commodity pool and its adviser must register as a commodity pool operator (“CPO”). Under such rules, registered investment companies that are commodity pools are subject to additional recordkeeping, reporting and disclosure requirements. The Fund has claimed an exclusion from the definition of CPO under CFTC Rule 4.5 under the CEA based on the extent of the Fund’s derivatives use and is not currently subject to these recordkeeping, reporting and disclosure requirements.

Use of Options, Futures Contracts, Forwards and Swaps by the Fund

—Forward Currency Exchange Contracts. A forward currency exchange contract is an obligation by one party to buy, and the other party to sell, a specific amount of a currency for an agreed-upon price at a future date. A forward currency exchange contract may result in the delivery of the underlying asset upon maturity of the contract in return for the agreed-upon payment. NDFs specify a cash payment upon maturity. NDFs are normally used when the market for physical settlement of the currency is underdeveloped, heavily regulated or highly taxed.

The Fund may, for example, enter into forward currency exchange contracts to attempt to minimize the risk to the Fund from adverse changes in the relationship between the U.S. Dollar and other currencies. The Fund may purchase or sell forward currency exchange contracts for hedging purposes similar to those described below in connection with its

| 6 |

transactions in foreign currency futures contracts. The Fund may also purchase or sell forward currency exchange contracts for non-hedging purposes as a means of making direct investments in foreign currencies, as described below under “Currency Transactions”.

If a hedging transaction in forward currency exchange contracts is successful, the decline in the value of portfolio securities or the increase in the cost of securities to be acquired may be offset, at least in part, by profits on the forward currency exchange contract. Nevertheless, by entering into such forward currency exchange contracts, the Fund may be required to forgo all or a portion of the benefits which otherwise could have been obtained from favorable movements in exchange rates.

The Fund may use forward currency exchange contracts to seek to increase total return when the Adviser anticipates that a foreign currency will appreciate or depreciate in value but securities denominated in that currency are not held by the Fund and do not present attractive investment opportunities. For example, the Fund may enter into a foreign currency exchange contract to purchase a currency if the Adviser expects the currency to increase in value. The Fund would recognize a gain if the market value of the currency is more than the contract value of the currency at the time of settlement of the contract. Similarly, the Fund may enter into a foreign currency exchange contract to sell a currency if the Adviser expects the currency to decrease in value. The Fund would recognize a gain if the market value of the currency is less than the contract value of the currency at the time of settlement of the contract.

The cost of engaging in forward currency exchange contracts varies with such factors as the currencies involved, the length of the contract period and the market conditions then prevailing. Since transactions in foreign currencies are usually conducted on a principal basis, no fees or commissions are involved.

—Options on Securities. The Fund may write and purchase call and put options on securities. In purchasing an option on securities, the Fund would be in a position to realize a gain if, during the option period, the price of the underlying securities increased (in the case of a call) or decreased (in the case of a put) by an amount in excess of the premium paid; otherwise the Fund would experience a loss not greater than the premium paid for the option. Thus, the Fund would realize a loss if the price of the underlying security declined or remained the same (in the case of a call) or increased or remained the same (in the case of a put) or otherwise did not increase (in the case of a put) or decrease (in the case of a call) by more than the amount of the premium. If a put or call option purchased by the Fund were permitted to expire without being sold or exercised, its premium would represent a loss to the Fund.

The Fund may write a put or call option in return for a premium, which is retained by the Fund whether or not the option is exercised. The Fund may write covered options or uncovered options. A call option written by the Fund is “covered” if the Fund owns the underlying security, has an absolute and immediate right to acquire that security upon conversion or exchange of another security it holds, or holds a call option on the underlying security with an exercise price equal to or less than the exercise price of the call option it has written. A put option written by the Fund is covered if the Fund holds a put option on the underlying securities with an exercise price equal to or greater than the exercise price of the put option it has written. Uncovered options, or naked options, are riskier than covered options. For example, if the Fund

| 7 |

wrote a naked call option and the price of the underlying security increased, the Fund would have to purchase the underlying security for delivery to the call buyer and sustain a loss, which could be substantial, equal to the difference between the option price and the market price of the security.

The Fund may purchase put options to hedge against a decline in the value of portfolio securities. If such decline occurs, the put options will permit the Fund to sell the securities at the exercise price or to close out the options at a profit. By using put options in this way, the Fund will reduce any profit it might otherwise have realized on the underlying security by the amount of the premium paid for the put option and by transaction costs.

The Fund may purchase call options to hedge against an increase in the price of securities that the Fund anticipates purchasing in the future. If such increase occurs, the call option will permit the Fund to purchase the securities at the exercise price, or to close out the options at a profit. The premium paid for the call option plus any transaction costs will reduce the benefit, if any, realized by the Fund upon exercise of the option, and, unless the price of the underlying security rises sufficiently, the option may expire worthless to the Fund and the Fund will suffer a loss on the transaction to the extent of the premium paid.

The Fund may also, as an example, write combinations of put and call options on the same security, known as “straddles”, with the same exercise and expiration date. By writing a straddle, the Fund undertakes a simultaneous obligation to sell and purchase the same security in the event that one of the options is exercised. If the price of the security subsequently rises above the exercise price, the call will likely be exercised and the Fund will be required to sell the underlying security at or below market price. This loss may be offset, however, in whole or in part, by the premiums received on the writing of the two options. Conversely, if the price of the security declines by a sufficient amount, the put will likely be exercised. The writing of straddles will likely be effective, therefore, only where the price of the security remains stable and neither the call nor the put is exercised. In those instances where one of the options is exercised, the loss on the purchase or sale of the underlying security may exceed the amount of the premiums received.

By writing a call option, the Fund limits its opportunity to profit from any increase in the market value of the underlying security above the exercise price of the option. By writing a put option, the Fund assumes the risk that it may be required to purchase the underlying security for an exercise price above its then current market value, resulting in a capital loss unless the security subsequently appreciates in value. Where options are written for hedging purposes, such transactions constitute only a partial hedge against declines in the value of portfolio securities or against increases in the value of securities to be acquired, up to the amount of the premium.

The Fund may purchase or write options on securities of the types in which it is permitted to invest in privately negotiated (i.e., OTC) transactions. Options purchased or written in negotiated transactions may be illiquid and it may not be possible for the Fund to effect a closing transaction at a time when the Adviser believes it would be advantageous to do so.

| 8 |

—Options on Securities Indices. An option on a securities index is similar to an option on a security except that, rather than taking or making delivery of a security at a specified price, an option on a securities index gives the holder the right to receive, upon exercise of the option, an amount of cash if the closing level of the chosen index is greater than (in the case of a call) or less than (in the case of a put) the exercise price of the option.

The Fund may write (sell) call and put options and purchase call and put options on securities indices. If the Fund purchases put options on securities indices to hedge its investments against a decline in the value of portfolio securities, it will seek to offset a decline in the value of securities it owns through appreciation of the put option. If the value of the Fund’s investments does not decline as anticipated, or if the value of the option does not increase, the Fund’s loss will be limited to the premium paid for the option. The success of this strategy will largely depend on the accuracy of the correlation between the changes in value of the index and the changes in value of the Fund’s security holdings.

The Fund may also write put or call options on securities indices to, among other things, earn income. If the value of the chosen index declines below the exercise price of the put option, the Fund has the risk of loss of the amount of the difference between the exercise price and the closing level of the chosen index, which it would be required to pay to the buyer of the put option and which may not be offset by the premium it received upon sale of the put option. Similarly, if the value of the index is higher than the exercise price of the call option, the Fund has the risk of loss of the amount of the difference between the exercise price and the closing level of the chosen index, which may not be offset by the premium it received upon sale of the call option. If the value of the securities index is significantly below or above the exercise price of the written option, the Fund could experience a substantial loss.

The purchase of call options on securities indices may be used by the Fund to attempt to reduce the risk of missing a broad market advance, or an advance in an industry or market segment, at a time when the Fund holds uninvested cash or short-term debt securities awaiting investment. When purchasing call options for this purpose, the Fund will also bear the risk of losing all or a portion of the premium paid if the value of the index does not rise. The purchase of call options on stock indices when the Fund is substantially fully invested is a form of leverage, up to the amount of the premium and related transaction costs, and involves risks of loss and of increased volatility similar to those involved in purchasing call options on securities the Fund owns.

—Other Option Strategies. In an effort to earn extra income, to adjust exposure to individual securities or markets, or to protect all or a portion of its portfolio from a decline in value, sometimes within certain ranges, the Fund may use option strategies such as the concurrent purchase of a call or put option, including on individual securities, stock indices, futures contracts (including on individual securities and stock indices) or shares of exchange-traded funds (“ETFs”) at one strike price and the writing of a call or put option on the same individual security, stock index, futures contract or ETF at a higher strike price in the case of a call option or at a lower strike price in the case of a put option. The maximum profit from this strategy would result for the call options from an increase in the value of the individual security, stock index, futures contract or ETF above the higher strike price or for the put options the decline in the value of the individual security, stock index, futures contract or ETF below the

| 9 |

lower strike price. If the price of the individual security, stock index, futures contract or ETF declines in the case of the call option or increases in the case of the put option, the Fund has the risk of losing the entire amount paid for the call or put options.

—Options on Foreign Currencies. The Fund may purchase and write options on foreign currencies for hedging and non-hedging purposes. For example, a decline in the dollar value of a foreign currency in which portfolio securities are denominated will reduce the dollar value of such securities, even if their value in the foreign currency remains constant. In order to protect against such diminutions in the value of portfolio securities, the Fund may purchase put options on the foreign currency. If the value of the currency does decline, the Fund will have the right to sell such currency for a fixed amount in dollars and could thereby offset, in whole or in part, the adverse effect on its portfolio which otherwise would have resulted.

Conversely, where a rise in the dollar value of a currency in which securities to be acquired are denominated is projected, thereby increasing the cost of such securities, the Fund may purchase call options thereon. The purchase of such options could offset, at least partially, the effects of the adverse movements in exchange rates. As in the case of other types of options, however, the benefit to the Fund from purchases of foreign currency options will be reduced by the amount of the premium and related transaction costs. In addition, where currency exchange rates do not move in the direction or to the extent anticipated, the Fund could sustain losses on transactions in foreign currency options which would require it to forgo a portion or all of the benefits of advantageous changes in such rates.

The Fund may write options on foreign currencies for hedging purposes or in an effort to increase returns. For example, where the Fund anticipates a decline in the dollar value of non-U.S. Dollar-denominated securities due to adverse fluctuations in exchange rates it could, instead of purchasing a put option, write a call option on the relevant currency. If the expected decline occurs, the option will most likely not be exercised, and the diminution in value of portfolio securities could be offset by the amount of the premium received.

Similarly, instead of purchasing a call option to hedge against an anticipated increase in the dollar cost of securities to be acquired, the Fund could write a put option on the relevant currency, which, if rates move in the manner projected, will expire unexercised and allow the Fund to hedge such increased cost up to the amount of the premium. As in the case of other types of options, however, the writing of a foreign currency option will constitute only a partial hedge up to the amount of the premium, and only if rates move in the expected direction. If this does not occur, the option may be exercised and the Fund will be required to purchase or sell the underlying currency at a loss which may not be offset by the amount of the premium. Through the writing of options on foreign currencies, the Fund also may be required to forgo all or a portion of the benefits that might otherwise have been obtained from favorable movements in exchange rates.

In addition to using options for the hedging purposes described above, the Fund may also invest in options on foreign currencies for non-hedging purposes as a means of making direct investments in foreign currencies. The Fund may use options on currency to seek to increase total return when the Adviser anticipates that a foreign currency will appreciate or depreciate in value but securities denominated in that currency are not held by the Fund and do

| 10 |

not present attractive investment opportunities. For example, the Fund may purchase call options in anticipation of an increase in the market value of a currency. The Fund would ordinarily realize a gain if, during the option period, the value of such currency exceeded the sum of the exercise price, the premium paid and transaction costs. Otherwise, the Fund would realize no gain or loss on the purchase of the call option. Put options may be purchased by the Fund for the purpose of benefiting from a decline in the value of a currency that the Fund does not own. The Fund would normally realize a gain if, during the option period, the value of the underlying currency decreased below the exercise price sufficiently to more than cover the premium and transaction costs. Otherwise, the Fund would realize no gain or loss on the purchase of the put option. For additional information on the use of options on foreign currencies for non-hedging purposes, see “Currency Transactions” below.

Special Risks Associated with Options on Currencies. An exchange traded options position may be closed out only on an options exchange that provides a secondary market for an option of the same series. Although the Fund will generally purchase or sell options for which there appears to be an active secondary market, there is no assurance that a liquid secondary market on an exchange will exist for any particular option, or at any particular time. For some options, no secondary market on an exchange may exist. In such event, it might not be possible to effect closing transactions in particular options, with the result that the Fund would have to exercise its options in order to realize any profit and would incur transaction costs on the purchase or sale of the underlying currency.

—Futures Contracts and Options on Futures Contracts. Futures contracts that the Fund may buy and sell may include futures contracts on fixed-income or other securities, and contracts based on interest rates, foreign currencies or financial indices, including any index of U.S. Government securities. The Fund may, for example, purchase or sell futures contracts and options thereon to hedge against changes in interest rates, securities (through index futures or options) or currencies.