Form 485APOS VanEck ETF Trust

Tweet

Tweet Share

ShareAs filed with the Securities and Exchange Commission on September 28, 2021

| Securities Act File No. 333-123257 | ||

| Investment Company Act File No. 811-10325 | ||

United States Securities and Exchange Commission

Washington, D.C. 20549

FORM N-1A

Registration Statement Under the Securities Act of 1933 | x | |||||||

Pre-Effective Amendment No. | o | |||||||

Post Effective Amendment No. 2,742 | x | |||||||

and/or | ||||||||

Registration Statement Under the Investment Company Act of 1940 | x | |||||||

Amendment No. 2,746 | x | |||||||

VANECK ETF TRUST

(Exact Name of Registrant as Specified in its Charter)

| 666 Third Avenue, 9th Floor | ||

| New York, New York 10017 | ||

| (Address of Principal Executive Offices) | ||

| (212) 293-2000 | ||

| Registrant’s Telephone Number | ||

| Jonathan R. Simon, Esq. | ||

| Senior Vice President and General Counsel | ||

| Van Eck Associates Corporation | ||

| 666 Third Avenue, 9th Floor | ||

| New York, New York 10017 | ||

| (Name and Address of Agent for Service) | ||

| Copy to: | ||

| Allison M. Fumai, Esq. | ||

| Dechert LLP | ||

| 1095 Avenue of the Americas | ||

| New York, New York 10036 | ||

Approximate Date of Proposed Public Offering: As soon as practicable after the effective date of this registration statement.

IT IS PROPOSED THAT THIS FILING WILL BECOME EFFECTIVE (CHECK APPROPRIATE BOX)

| Immediately upon filing pursuant to paragraph (b) | |||||

| On [date] pursuant to paragraph (b) | |||||

| 60 days after filing pursuant to paragraph (a)(1) | |||||

| X | On December 10, 2021 pursuant to paragraph (a)(1) | ||||

| 75 days after filing pursuant to paragraph (a)(2) | |||||

| On [date] pursuant to paragraph (a)(2) of rule 485 | |||||

The information in this Prospectus is not complete and may be changed. The Trust may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This Prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated September 28, 2021

| PROSPECTUS | |||||||

| [ ] | ||||||||

VANECK

ChiNext ETF CNXT

Principal U.S. Listing Exchange for the Fund: NYSE Arca, Inc. | ||

The U.S. Securities and Exchange Commission ("SEC") has not approved or disapproved these securities or passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense. | ||

TABLE OF CONTENTS | |||||

| Summary Information | |||||

VANECK® CHINEXT ETF | ||

SUMMARY INFORMATION

INVESTMENT OBJECTIVE

VanEck® ChiNext ETF1 (the “Fund”) seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the ChiNext Index (the "ChiNext Index”).

FUND FEES AND EXPENSES

The following tables describe the fees and expenses that you may pay if you buy, hold and sell shares of the Fund (“Shares”). You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

Shareholder Fees (fees paid directly from your investment) | None | ||||

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

[TO BE UPDATED]

| Management Fee | 0.50 | % | |||||||||

Other Expenses | 0.65 | % | |||||||||

Total Annual Fund Operating Expenses(a) | 1.15 | % | |||||||||

Fee Waivers and Expense Reimbursement | -0.50 | % | |||||||||

Total Annual Fund Operating Expenses After Fee Waivers and Expense Reimbursement(a) | 0.65 | % | |||||||||

(a) Van Eck Associates Corporation (the “Adviser”) has agreed to waive fees and/or pay Fund expenses to the extent necessary to prevent the operating expenses of the Fund (excluding acquired fund fees and expenses, trading expenses, taxes and extraordinary expenses) from exceeding [ ]% of the Fund’s average daily net assets per year until at least [ ]. During such time, the expense limitation is expected to continue until the Fund’s Board of Trustees acts to discontinue all or a portion of such expense limitation.

EXPENSE EXAMPLE

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other funds. This example does not take into account brokerage commissions that you pay when purchasing or selling Shares of the Fund.

The example assumes that you invest $10,000 in the Fund for the time periods indicated and then sell or hold all of your Shares at the end of those periods. The example also assumes that your investment has a 5% annual return and that the Fund’s operating expenses remain the same (except that the example incorporates the fee waivers and/or expense reimbursement arrangement for only the first year). Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

[TO BE UPDATED]

| YEAR | EXPENSES | ||||||||||

| 1 | $66 | ||||||||||

| 3 | $316 | ||||||||||

| 5 | $585 | ||||||||||

| 10 | $1,353 | ||||||||||

PORTFOLIO TURNOVER

The Fund will pay transaction costs, such as commissions, when it purchases and sells securities (or “turns over” its portfolio). A higher portfolio turnover will cause the Fund to incur additional transaction costs and may result in higher taxes when Fund Shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, may affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was [96]% of the average value of its portfolio.

1 Prior to December 10, 2021, the Fund's name was VanEck Vectors® ChinaAMC SME-ChiNext ETF.

3 | ||

PRINCIPAL INVESTMENT STRATEGIES

The Fund normally invests at least 80% of its total assets in securities that comprise the Fund’s benchmark index. The ChiNext Index is a free-float adjusted index intended to track the performance of the 100 largest and most liquid stocks listed and trading on the ChiNext Market of the Shenzhen Stock Exchange. The ChiNext Index is comprised of China A-shares (“A-shares”).

As of August 2, 2021 the ChiNext Index included 100 securities of companies with a market capitalization range of between approximately $1.66 billion and $198.95 billion and a weighted average market capitalization of $51.95 billion. The Fund’s 80% investment policy is non-fundamental and may be changed without shareholder approval upon 60 days’ prior written notice to shareholders.

The Fund, using a “passive” or indexing investment approach, attempts to approximate the investment performance of the ChiNext Index by investing in a portfolio of securities that generally replicates the ChiNext Index. Unlike many investment companies that try to “beat” the performance of a benchmark index, the Fund does not try to “beat” the ChiNext Index and does not seek temporary defensive positions that are inconsistent with its investment objective of seeking to replicate the ChiNext Index.

The Fund will seek to achieve its investment objective by primarily investing directly in A-shares. A-shares are issued by companies incorporated in the People’s Republic of China (“China” or the “PRC”). A-shares are traded in renminbi (“RMB”) on the Shenzhen or Shanghai Stock Exchanges. The A-share market in China is made available to domestic PRC investors and foreign investors through the Shanghai-Hong Kong Stock Connect Program and the Shenzhen-Hong Kong Stock Connect Program (together, “Stock Connect”), and through licenses obtained under the Renminbi Qualified Foreign Institutional Investor (“RQFII”) or a Qualified Foreign Institutional Investor (“QFII”) programs. After obtaining a RQFII or QFII license, the RQFII or QFII would register itself with China’s State Administration of Foreign Exchange (“SAFE”). Investment companies are not currently within the types of entities that are eligible for a RQFII or QFII license. Because the Fund does not satisfy the criteria to qualify as a RQFII or QFII itself, the Fund intends to invest directly in A-shares via Stock Connect, as described below, or via the license granted to the Fund’s sub-adviser, China Asset Management (Hong Kong) Limited (the “Sub-Adviser”), by CSRC ("RQFII license"). The Sub-Adviser has obtained RQFII status, which the Sub-Adviser will use to invest in A-shares. The Fund may also invest in A-shares listed and traded on the Shanghai and Shenzhen Stock Exchanges through Stock Connect. Stock Connect is a securities trading and clearing program between the Shanghai and Shenzhen Stock Exchanges, the Stock Exchange of Hong Kong Limited, China Securities Depository and Clearing Corporation Limited (“CSDCC”) and Hong Kong Securities Clearing Company Limited (“HKSCC”) designed to permit mutual stock market access between mainland China and Hong Kong by allowing investors to trade and settle shares on each market via their local exchanges. Other exchanges in China may participate in Stock Connect in the future. Trading through Stock Connect is subject to daily quotas that limit the maximum daily net purchases on any particular day. Accordingly, the Fund’s direct investments in A-shares will be limited by the daily quotas that limit total purchases and/or sales through Stock Connect.

The Fund may become non-diversified as defined under the Investment Company Act of 1940, as amended, solely as a result of a change in relative market capitalization or index weighting of one or more constituents of the ChiNext Index. This means that the Fund may invest a greater percentage of its assets in a limited number of issuers than would be the case if the Fund were always managed as a diversified management investment company. The Fund intends to be diversified in approximately the same proportion as the ChiNext Index. Shareholder approval will not be sought when the Fund crosses from diversified to non-diversified status due solely to a change in the relative market capitalization or index weighting of one or more constituents of the ChiNext Index.

The Fund may concentrate its investments in a particular industry or group of industries to the extent that the ChiNext Index concentrates in an industry or group of industries. As of August 2, 2021, each of the industrials, health care and information technology sectors represented a significant portion of the ChiNext Index.

PRINCIPAL RISKS OF INVESTING IN THE FUND

Investors in the Fund should be willing to accept a high degree of volatility in the price of the Fund’s Shares and the possibility of significant losses. An investment in the Fund involves a substantial degree of risk. An investment in the Fund is not a deposit with a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Therefore, you should consider carefully the following risks before investing in the Fund, each of which could significantly and adversely affect the value of an investment in the Fund.

Risk of the RQFII Regime and the Fund’s Principal Investment Strategy. The ChiNext Index is comprised of A-shares. In seeking to replicate the ChiNext Index, the Fund intends to invest directly in A-shares through the Sub-Adviser’s RQFII license and Stock Connect and in other shares directly. Because the Fund will not be able to invest directly in A-shares beyond the limits that may be imposed by Stock Connect, the size of the Fund’s direct investment in A-shares may be limited. In addition, the RQFII license of the Sub-Adviser may be revoked by the Chinese regulators if, among other things, the Sub-Adviser fails to observe SAFE and other applicable Chinese regulations. There can be no assurance the Fund could retain a replacement sub-adviser with an RQFII license or other means of investing in A-shares if that became necessary or appropriate for any reason.

The Fund cannot predict what would occur if the RQFII of the Sub-Adviser generally were eliminated, although such an occurrence would likely have a material adverse effect on the Fund, including the requirement that the Sub-Adviser on behalf of the Fund dispose of certain or all of its A-shares holdings. Therefore, any elimination may have a material adverse effect on the ability of the

Fund to achieve its investment objective. If the Fund is unable to obtain sufficient exposure to the performance of the ChiNext Index due to the limited availability of investments that provide exposure to the performance of A-shares, the Fund could, subject to any necessary regulatory relief, among other things, as a defensive measure limit or suspend creations until the Adviser and/or the Sub-Adviser determine that the requisite exposure to the ChiNext Index is obtainable. If any of the above events were to occur, the Fund could trade at a significant premium or discount to its net asset value (“NAV”) and could experience substantial redemptions and the Fund could, among other things, change its investment objective by, for example, seeking to track an alternative index focused on Chinese-related stocks other than A-shares or other appropriate investments, or decide to liquidate.

The A-share market is volatile with a risk of suspension of trading in a particular security or government intervention. Securities on the A-share market, including securities in the ChiNext Index, may be suspended from trading without an indication of how long the suspension will last, which may impair the liquidity of such securities.

Specific rules governing taxes on capital gains derived by RQFIIs and QFIIs from the trading of PRC securities have yet to be announced. In the absence of specific rules, the tax treatment of the Fund’s investments in A-shares through the Sub-Adviser’s RQFII quota should be governed by the general PRC tax provisions and provisions applicable to RQFIIs. Under these provisions, a non-PRC tax resident enterprise without permanent establishment in the PRC, such as the Fund, is generally subject to a tax of 10% on any PRC sourced income (including cash dividends, distributions, interest and capital gains) derived by it from an investment in PRC securities. In addition, a nonresident enterprise is subject to withholding tax at a rate of 10% on its capital gains. Withholding taxes on dividends, interest and capital gains may be taxed at a reduced rate under an applicable tax treaty, but the application of such treaties for an RQFII acting on behalf of a foreign investor (i.e., the Sub-Adviser acting on behalf of the Fund) is also uncertain. It is also unclear how China’s business tax may apply to activities of an RQFII such as the Sub-Adviser and how such application may be affected by tax treaty provisions. While it is unclear whether this tax will be applied to investments by an RQFII, such as the Sub-Adviser, or what the methodology for calculating or collecting the tax will be, the PRC’s Ministry of Finance announced that, effective November 17, 2014, PRC-sourced gains on disposal of shares and other equity investments (including A-shares) derived by QFIIs or RQFIIs (without an establishment or place of business in the PRC or having an establishment or place of business in the PRC but the income so derived in the PRC is not effectively connected with such establishment or place) would be temporarily exempt from PRC corporate income tax. The current PRC tax laws and regulations and interpretations thereof may be revised or amended in the future, including with respect to the possible liability of the Fund for obligations of the Sub-Adviser. Any revision or amendment in tax laws and regulations may adversely affect the Fund. The Fund, prior to December 22, 2014, reserved 10% of its realized and unrealized gains from its A-share investments to apply towards withholding tax liability with respect to realized and unrealized gains from the Fund’s investments in A-shares of “land-rich” enterprises, which are companies that have greater than 50% of their assets in land or real properties in the PRC. The tax reserve was reflected in the Fund’s daily NAV calculations as a deduction from the Fund’s NAV. During 2015, revenue authorities in the PRC made arrangements for the collection of capital gains taxes for investments realized between November 17, 2009 and November 16, 2014. The Fund could be subject to tax liability for any tax payments for which reserves have not been made or that were not previously withheld. The impact of any such tax liability on the Fund’s return could be substantial. The Fund may also be liable to the Sub-Adviser for any tax that is imposed on the Sub-Adviser by the PRC with respect to the Fund’s investments. The Fund may also potentially be subject to PRC value-added tax at the rate of 6% on capital gains derived from trading of A-shares.

If the Fund’s direct investments in A-shares through the Sub-Adviser’s RQFII license become subject to repatriation restrictions, the Fund may be unable to satisfy distribution requirements applicable to regulated investment companies (“RICs”) under the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), and be subject to income and excise tax at the Fund level. In addition, the Fund could be required to recognize unrealized gains, pay taxes and make distributions before re- qualifying for taxation as a RIC. See the prospectus under “Shareholder Information—Tax Information—Taxes on Distributions” for more information. The Fund may elect, for U.S. federal income tax purposes, to treat Chinese taxes (including withholding taxes) paid by the Fund as paid by its shareholders. Even if the Fund is qualified to make that election and does so, this treatment will not apply with respect to amounts the Fund reserves in anticipation of the imposition of withholding taxes not currently in effect (as discussed above). If these amounts are used to pay any tax liability of the Fund in a later year, they will be treated as paid by the shareholders in such later year, even if they are imposed with respect to income of an earlier year. See the section of this prospectus entitled “Shareholder Information—Tax Information” for a further description of this risk. There is no guarantee that the temporary tax exemption or non-taxable treatment with respect to assets traded via QFIIs and RQFIIs described above will continue to apply.

Special Risk Considerations of Investing in China and A-shares. Investments in securities of Chinese issuers, including A-shares, involve risks and special considerations not typically associated with investments in the U.S. securities markets. These risks include, among others, (i) more frequent (and potentially widespread) trading suspensions and government interventions with respect to Chinese issuers, resulting in lack of liquidity and in price volatility, (ii) currency revaluations and other currency exchange rate fluctuations or blockage, (iii) the nature and extent of intervention by the Chinese government in the Chinese securities markets (including both direct and indirect market stabilization efforts, which may affect valuations of Chinese issuers), whether such intervention will continue and the impact of such intervention or its discontinuation, (iv) the risk of nationalization or expropriation of assets, (v) the risk that the Chinese government may decide not to continue to support economic reform programs, (vi) limitations on the use of brokers (or action by the Chinese government that discourages brokers from serving

international clients), (vii) higher rates of inflation, (viii) greater political, economic and social uncertainty, (ix) market volatility caused by any potential regional or territorial conflicts or natural or other disasters (x) the risk of increased trade tariffs, embargoes, sanctions, investment restrictions and other trade limitations, (xi) custody risks associated with investing via the Stock Connect Program or through a RQFII, where due to requirements regarding establishing a custody account in the joint names of the Fund and the Sub-Adviser the Fund’s assets may not be as well protected from the claims of the Sub-Adviser’s creditors than if the Fund had an account in its name only, (xii) both interim and permanent market regulations which may affect the ability of certain stockholders to sell Chinese securities when it would otherwise be advisable and (xiii) foreign ownership limits of any listed Chinese company.

The economy of China differs, often unfavorably, from the U.S. economy in such respects as structure, general development, government involvement, wealth distribution, rate of inflation, growth rate, interest rates, allocation of resources and capital reinvestment, among others. The Chinese central government has historically exercised substantial control over virtually every sector of the Chinese economy through administrative regulation and/or state ownership and actions of the Chinese central and local government authorities continue to have a substantial effect on economic conditions in China. In addition, the Chinese government has from time to time taken actions that influence the prices at which certain goods may be sold, encourage companies to invest or concentrate in particular industries, induce mergers between companies in certain industries and induce private companies to publicly offer their securities to increase or continue the rate of economic growth, control the rate of inflation or otherwise regulate economic expansion. It may do so in the future as well, potentially having a significant adverse effect on economic conditions in China.

The Sub-Adviser, as a licensed RQFII, is currently permitted to repatriate RMB daily and is not subject to RMB repatriation restrictions or prior approval, provided that final repatriation of capital and profits at the liquidation of the Fund will be subject to an audit report and tax filing. However, there is no assurance that RQFIIs may not be subject to restrictions or prior approval requirements in the future. Any additional restrictions imposed on the Sub-Adviser or RQFIIs generally may have an adverse effect on the Fund’s ability to invest directly in A-shares and its ability to meet redemption requests.

The Chinese securities markets are emerging markets characterized by greater price volatility relative to U.S. markets. Liquidity risks may be more pronounced for the A-share market than for Chinese securities markets generally because the A-share market is subject to greater government restrictions and control, including trading suspensions as discussed above. Price fluctuations of A-shares are limited per trading day. In addition, there is less regulation and monitoring of Chinese securities markets and the activities of investors, brokers and other participants than in the United States. Accounting, auditing and financial reporting standards in China are different from U.S. standards and, therefore, disclosure of certain material information may not be made. In addition, less information may be available to the Fund and other investors than would be the case if the Fund’s investments were restricted to securities of U.S. issuers. There is also generally less governmental regulation of the securities industry in China, and less enforcement of regulatory provisions relating thereto, than in the United States. Moreover, it may be more difficult to obtain a judgment in a court outside the United States.

The Chinese government strictly regulates the payment of foreign currency denominated obligations and sets monetary policy. In addition, the Chinese economy is export-driven and highly reliant on trade. Adverse changes to the economic conditions of its primary trading partners, such as the United States, Japan and South Korea, would adversely impact the Chinese economy and the Fund’s investments. Moreover, a slowdown in other significant economies of the world, such as the United States, the European Union and certain Asian countries, may adversely affect economic growth in China. An economic downturn in China would adversely impact the Fund’s investments.

Emerging markets such as China can experience high rates of inflation, deflation and currency devaluation. The value of the RMB may be subject to a high degree of fluctuation due to, among other things, changes in interest rates, the effects of monetary policies issued by the PRC, the United States, foreign governments, central banks or supranational entities, the imposition of currency controls or other national or global political or economic developments. The income received by the Fund for its investments denominated in RMB will principally be in RMB. The Fund’s exposure to the RMB and changes in value of the RMB versus the U.S. dollar may result in reduced returns for the Fund. Moreover, the Fund may incur costs in connection with conversions between U.S. dollars and RMB. The RMB is currently not a freely convertible currency. The Chinese government places strict regulation on RMB and sets the value of the RMB to levels dependent on the value of the U.S. dollar, but the Chinese government has been under pressure to manage the currency in a less restrictive fashion so that it is less correlated to the U.S. dollar. The Chinese government’s imposition of restrictions on the repatriation of RMB out of mainland China may limit the depth of the offshore RMB market and reduce the liquidity of the Fund’s investments. Under exceptional circumstances, payment of redemptions and/or dividend payment in RMB may be delayed due to the exchange controls and restrictions applicable to RMB. There may not be sufficient amounts of RMB for the Fund to be fully invested because the Fund has to convert U.S. dollars received from the purchase of Creation Units (defined herein) into RMB to purchase A-shares. As a result, these restrictions may adversely affect the Fund and its investments and may increase the risk of index tracking error.

Risks associated with the ChiNext Market. The Fund may, through the Shenzhen-Hong Kong Stock Connect, access securities listed on the ChiNext Market of the Shenzhen Stock Exchange. Listed companies on the ChiNext Market are usually of an emerging nature with smaller operating scale. They are subject to higher fluctuation in stock prices and liquidity and have higher

risks and turnover ratios than companies listed on the main board of the Shenzhen Stock Exchange. Securities listed on the ChiNext may be overvalued and such exceptionally high valuation may not be sustainable. Stock prices may be more susceptible to manipulation due to fewer circulating shares. It may be more common and faster for companies listed on ChiNext to delist. This may have an adverse impact on the Fund if the companies that they invest in are delisted. Also, the rules and regulations regarding companies listed on ChiNext Market are less stringent in terms of profitability and share capital than those on the main board. Investments in the ChiNext Market may result in significant losses for the Fund and its investors.

Risks of Investing through Stock Connect. The Fund may invest in A-shares listed and traded on the Shanghai Stock Exchange and the Shenzhen Stock Exchange through Stock Connect, or on such other stock exchanges in China which participate in Stock Connect from time to time or in the future. Trading through Stock Connect is subject to a number of restrictions that may affect the Fund’s investments and returns. For example, trading through Stock Connect is subject to daily quotas that limit the maximum daily net purchases on any particular day, which may restrict or preclude the Fund’s ability to invest in Stock Connect A-shares. In addition, investments made through Stock Connect are subject to trading, clearance and settlement procedures that are relatively untested in the PRC, which could pose risks to the Fund. Furthermore, securities purchased via Stock Connect will be held via a book entry omnibus account in the name of HKSCC, Hong Kong’s clearing entity, at the CSDCC. The Fund’s ownership interest in Stock Connect securities will not be reflected directly in book entry with CSDCC and will instead only be reflected on the books of its Hong Kong sub-custodian. The Fund may therefore depend on HKSCC’s ability or willingness as record-holder of Stock Connect securities to enforce the Fund’s shareholder rights. PRC law did not historically recognize the concept of beneficial ownership; while PRC regulations and the Hong Kong Stock Exchange have issued clarifications and guidance supporting the concept of beneficial ownership via Stock Connect, the interpretation of beneficial ownership in the PRC by regulators and courts may continue to evolve. Moreover, Stock Connect A-shares generally may not be sold, purchased or otherwise transferred other than through Stock Connect in accordance with applicable rules.

A primary feature of Stock Connect is the application of the home market’s laws and rules applicable to investors in A-shares. Therefore, the Fund’s investments in Stock Connect A-shares are generally subject to PRC securities regulations and listing rules, among other restrictions. Stock Connect is only available on days when markets in both the PRC and Hong Kong are open, which may limit the Fund’s ability to trade when it would be otherwise attractive to do so. Since the inception of Stock Connect, foreign investors (including the Fund) investing in A-shares through Stock Connect have been temporarily exempt from the PRC corporate income tax and value-added tax on the gains on disposal of such A-shares. Dividends are subject to PRC corporate income tax on a withholding basis at 10%, unless reduced under a double tax treaty with China upon application to and obtaining approval from the competent tax authority. Additionally, uncertainties in permanent PRC tax rules governing taxation of income and gains from investments in Stock Connect A-shares could result in unexpected tax liabilities for the Fund.

The Stock Connect program is a relatively new program and may be subject to further interpretation and guidance. There can be no assurance as to the program’s continued existence or whether future developments regarding the program may restrict or adversely affect the Fund’s investments or returns. In addition, the application and interpretation of the laws and regulations of Hong Kong and the PRC, and the rules, policies or guidelines published or applied by relevant regulators and exchanges in respect of the Stock Connect program are uncertain, and they may have a detrimental effect on the Fund’s investments and returns.

Risk of Investing in Foreign Securities. Investments in the securities of foreign issuers involve risks beyond those associated with investments in U.S. securities. These additional risks include greater market volatility, the availability of less reliable financial information, higher transactional and custody costs, taxation by foreign governments, decreased market liquidity and political instability. Because certain foreign securities markets may be limited in size, the activity of large traders may have an undue influence on the prices of securities that trade in such markets. The Fund invests in securities of issuers located in countries whose economies are heavily dependent upon trading with key partners. Any reduction in this trading may have an adverse impact on the Fund’s investments.

Risk of Investing in Emerging Market Issuers. Investments in securities of emerging market issuers are exposed to a number of risks that may make these investments volatile in price or difficult to trade. Emerging markets are more likely than developed markets to experience problems with the clearing and settling of trades, as well as the holding of securities by local banks, agents and depositories. Political risks may include unstable governments, nationalization, restrictions on foreign ownership, laws that prevent investors from getting their money out of a country and legal systems that do not protect property rights as well as the laws of the United States. Market risks may also include economies that concentrate in only a few industries, securities issues that are held by only a few investors, liquidity issues and limited trading capacity in local exchanges and the possibility that markets or issues may be manipulated by foreign nationals who have inside information. The frequency, availability and quality of financial information about investments in emerging markets varies. The Fund has limited rights and few practical remedies in emerging markets and the ability of U.S. authorities to bring enforcement actions in emerging markets may be limited, and the Fund's passive investment approach does not take account of these risks. All of these factors can make emerging market securities more volatile and potentially less liquid than securities issued in more developed markets.

Foreign Currency Risk. Because the Fund’s assets may be invested in securities denominated in foreign currencies, the proceeds received by the Fund from its investments and/or the revenues received by the issuer will generally be in foreign

currencies. The Fund’s exposure to foreign currencies and changes in the value of foreign currencies versus the U.S. dollar may result in reduced returns for the Fund, and the value of certain foreign currencies may be subject to a high degree of fluctuation. Moreover, the Fund may incur costs in connection with conversions between U.S. dollars and foreign currencies.

Risk of Investing in the Health Care Sector. The Fund will be sensitive to, and its performance will depend to a greater extent on, the overall condition of the health care sector. Companies in the health care sector may be affected by extensive government regulation, restrictions on government reimbursement for medical expenses, rising costs of medical products and services, pricing pressure, an increased emphasis on outpatient services, limited number of products, industry innovation, changes in technologies and other market developments. Many health care companies are heavily dependent on patent protection and are subject to extensive litigation based on product liability and similar claims.

Risk of Investing in the Industrials Sector. The Fund will be sensitive to, and its performance will depend to a greater extent on, the overall condition of the industrials sector. The industrials sector comprises companies who produce capital goods used in construction and manufacturing, such as companies that make and sell machinery, equipment and supplies that are used to produce other goods. Companies in the industrials sector may be adversely affected by changes in government regulation, world events and economic conditions. In addition, companies in the industrials sector may be adversely affected by environmental damages, product liability claims and exchange rates.

Risk of Investing in the Information Technology Sector. The Fund will be sensitive to, and its performance will depend to a greater extent on, the overall condition of the information technology sector. Information technology companies face intense competition, both domestically and internationally, which may have an adverse effect on profit margins. Information technology companies may have limited product lines, markets, financial resources or personnel. The products of information technology companies may face product obsolescence due to rapid technological developments and frequent new product introduction, unpredictable changes in growth rates and competition for the services of qualified personnel. Companies in the information technology sector are heavily dependent on patent protection and the expiration of patents may adversely affect the profitability of these companies.

Risk of Investing in Small- and Medium-Capitalization Companies. Small- and medium-capitalization companies may be more volatile and more likely than large-capitalization companies to have narrower product lines, fewer financial resources, less management depth and experience and less competitive strength. In addition, these companies often have greater price volatility, lower trading volume and less liquidity than larger more established companies. Returns on investments in securities of small- and medium-capitalization companies could trail the returns on investments in securities of large-capitalization companies.

Risk of Cash Transactions. Unlike other ETFs, the Fund expects to effect its creations and redemptions at least partially for cash, rather than wholly for in-kind securities. Therefore, it may be required to sell portfolio securities and subsequently incur brokerage costs and/or recognize gains or losses on such sales that the Fund might not have recognized if it were to distribute portfolio securities in kind. As such, investments in Shares may be less tax-efficient than an investment in a conventional ETF.

Equity Securities Risk. The value of the equity securities held by the Fund may fall due to general market and economic conditions, perceptions regarding the markets in which the issuers of securities held by the Fund participate, or factors relating to specific issuers in which the Fund invests. Equity securities are subordinated to preferred securities and debt in a company’s capital structure with respect to priority in right to a share of corporate income, and therefore will be subject to greater dividend risk than preferred securities or debt instruments. In addition, while broad market measures of equity securities have historically generated higher average returns than fixed income securities, equity securities have generally also experienced significantly more volatility in those returns, although under certain market conditions fixed income securities may have comparable or greater price volatility.

Market Risk. The prices of the securities in the Fund are subject to the risks associated with investing in the securities market, including general economic conditions, sudden and unpredictable drops in value, exchange trading suspensions and closures and public health risks. These risks may be magnified if certain social, political, economic and other conditions and events (such as natural disasters, epidemics and pandemics, terrorism, conflicts and social unrest) adversely interrupt the global economy; in these and other circumstances, such events or developments might affect companies world-wide. An investment in the Fund may lose money.

Operational Risk. The Fund is exposed to operational risk arising from a number of factors, including, but not limited to, human error, processing and communication errors, errors of the Fund’s service providers, counterparties or other third parties, failed or inadequate processes and technology or system failures.

High Portfolio Turnover Risk. The Fund will experience increased portfolio turnover in connection with the change in the Fund’s investment objective and benchmark index and the Fund’s repositioning, which will result in increased transaction costs to the Fund, including brokerage commissions, dealer mark-ups and other transaction costs on the sale of the securities and on

reinvestment in other securities. High portfolio turnover may also result in higher taxes when Fund Shares are held in a taxable account.

Index Tracking Risk. The Fund’s return may not match the return of the ChiNext Index for a number of reasons. For example, the Fund incurs a number of operating expenses, including taxes, not applicable to the ChiNext Index and incurs costs associated with buying and selling securities and entering into derivatives transactions, especially when rebalancing the Fund’s securities holdings to reflect changes in the composition of the ChiNext Index, or (to the extent the Fund effects creations and redemptions for cash) raising cash to meet redemptions or deploying cash in connection with newly created Creation Units, which are not factored into the return of the ChiNext Index. Transaction costs, including brokerage costs, will decrease the Fund’s NAV to the extent not offset by the transaction fee payable by an Authorized Participant (“AP”). Market disruptions and regulatory restrictions could have an adverse effect on the Fund’s ability to adjust its exposure to the required levels in order to track the ChiNext Index. Errors in the ChiNext Index data, the ChiNext Index computations and/or the construction of the ChiNext Index in accordance with its methodology may occur from time to time and may not be identified and corrected by the ChiNext Index provider for a period of time or at all, which may have an adverse impact on the Fund and its shareholders. When the ChiNext Index is rebalanced and the Fund in turn rebalances its portfolio to attempt to increase the correlation between the Fund’s portfolio and the ChiNext Index, any transaction costs and market exposure arising from such portfolio rebalancing will be borne directly by the Fund and its shareholders. Shareholders should understand that any gains from the ChiNext Index provider's errors will be kept by the Fund and its shareholders and any losses or costs resulting from the ChiNext Index provider's errors will be borne by the Fund and its shareholders. Apart from scheduled rebalances, the ChiNext Index provider or its agents may carry out additional ad hoc rebalances to the ChiNext Index. Therefore, errors and additional ad hoc rebalances carried out by the ChiNext Index provider or its agents to the Fund’s Index may increase the costs to and the tracking error risk of the Fund. The Fund may not be fully invested at times either as a result of cash flows into the Fund or reserves of cash held by the Fund to meet redemptions or pay expenses. In addition, the Fund may not invest in certain securities included in the ChiNext Index, or invest in them in the exact proportions in which they are represented in the ChiNext Index. As discussed above, one or more securities included the ChiNext Index may be suspended from trading and such securities would be valued by the ChiNext Index at the last closing price. The Fund’s performance may also deviate from the return of the ChiNext Index due to legal restrictions or limitations imposed by the governments of certain countries, certain listing standards of the Fund’s listing exchange (the “Exchange”), a lack of liquidity on stock exchanges in which such securities trade, potential adverse tax consequences or other regulatory reasons (such as diversification requirements). The Fund may value certain of its investments, underlying currencies, and/or other assets based on fair value prices. To the extent the Fund calculates its NAV based on fair value prices and the value of the ChiNext Index is based on securities’ closing prices on local foreign markets (i.e., the value of the ChiNext Index is not based on fair value prices), the Fund’s ability to track the ChiNext Index may be adversely affected. In addition, any issues the Fund encounters with regard to currency convertibility (including the cost of borrowing funds, if any) and repatriation may also increase the index tracking risk. The Fund will be required to remit RMB to settle the purchase of A-shares and repatriate RMB to U.S. dollars to settle redemption orders. In the event such remittance is delayed or disrupted, the Fund will not be able to fully replicate the ChiNext Index by investing in the relevant A-shares, which may lead to increased tracking error, and may need to rely on borrowings to meet redemptions, which may lead to increased expenses. Because the ChiNext Index is priced in Chinese RMB and the Fund is priced in U.S. dollars, the ability of the Fund to track the ChiNext Index is in part subject to foreign exchange fluctuations as between the U.S. dollar and the RMB. The Fund’s performance may also deviate from the performance of the ChiNext Index due to the impact of withholding taxes, late announcements relating to changes to the ChiNext Index and high turnover of the ChiNext Index. When markets are volatile, the ability to sell securities at fair value prices may be adversely impacted and may result in additional trading costs and/or increase the index tracking risk. The Fund may underperform the ChiNext Index when the value of the U.S. dollar increases relative to the value of the RMB. The Fund may also need to rely on borrowings to meet redemptions, which may lead to increased expenses. For tax efficiency purposes, the Fund may sell certain securities, and such sale may cause the Fund to realize a loss and deviate from the performance of the ChiNext Index. In light of the factors discussed above, the Fund’s return may deviate significantly from the return of the ChiNext Index. Changes to the composition of the ChiNext Index in connection with a rebalancing or reconstitution of the ChiNext Index may cause the Fund to experience increased volatility, during which time the Fund’s index tracking risk may be heightened.

Authorized Participant Concentration Risk. The Fund may have a limited number of financial institutions that act as APs, none of which are obligated to engage in creation and/or redemption transactions. To the extent that those APs exit the business, or are unable to or choose not to process creation and/or redemption orders, and no other AP is able to step forward to create and redeem, there may be a significantly diminished trading market for Shares or Shares may trade like closed-end funds at a greater discount (or premium) to NAV and possibly face trading halts and/or de-listing. The AP concentration risk may be heightened in scenarios where APs have limited or diminished access to the capital required to post collateral.

No Guarantee of Active Trading Market. While Shares are listed on the Exchange, there can be no assurance that an active trading market for the Shares will be maintained. Further, secondary markets may be subject to irregular trading activity, wide bid/ask spreads and extended trade settlement periods in times of market stress because market makers and APs may step away from making a market in the Shares and in executing creation and redemption orders, which could cause a material deviation in the Fund’s market price from its NAV.

Trading Issues. Trading in Shares on the Exchange may be halted due to market conditions or for reasons that, in the view of the Exchange, make trading in Shares inadvisable. In addition, trading in Shares on the Exchange is subject to trading halts caused by extraordinary market volatility pursuant to the Exchange’s “circuit breaker” rules. There can be no assurance that the requirements of the Exchange necessary to maintain the listing of the Fund will continue to be met or will remain unchanged.

Passive Management Risk. An investment in the Fund involves risks similar to those of investing in any fund invested in equity securities traded on an exchange, such as market fluctuations caused by such factors as economic and political developments, changes in interest rates and perceived trends in security prices. However, because the Fund is not “actively” managed, unless a specific security is removed from the ChiNext Index, the Fund generally would not sell a security because the security’s issuer was in financial trouble. Additionally, unusual market conditions may cause the ChiNext Index provider to postpone a scheduled rebalance or reconstitution, which could cause the ChiNext Index to vary from its normal or expected composition. Therefore, the Fund’s performance could be lower than funds that may actively shift their portfolio assets to take advantage of market opportunities or to lessen the impact of a market decline or a decline in the value of one or more issuers.

Fund Shares Trading, Premium/Discount Risk and Liquidity of Fund Shares. The market price of the Shares may fluctuate in response to the Fund’s NAV, the intraday value of the Fund’s holdings and supply and demand for Shares. The Adviser cannot predict whether Shares will trade above, below, or at their most recent NAV. Disruptions to creations and redemptions, the existence of market volatility or potential lack of an active trading market for Shares (including through a trading halt), as well as other factors, may result in Shares trading at a significant premium or discount to NAV or to the intraday value of the Fund’s holdings. If a shareholder purchases Shares at a time when the market price is at a premium to the NAV or sells Shares at a time when the market price is at a discount to the NAV, the shareholder may pay significantly more or receive significantly less than the underlying value of the Shares that were bought or sold or the shareholder may be unable to sell his or her Shares. The securities held by the Fund may be traded in markets that close at a different time than the Exchange. Liquidity in those securities may be reduced after the applicable closing times. Accordingly, during the time when the Exchange is open but after the applicable market closing, fixing or settlement times, bid/ask spreads on the Exchange and the resulting premium or discount to the Shares’ NAV may widen. Additionally, in stressed market conditions, the market for the Fund’s Shares may become less liquid in response to deteriorating liquidity in the markets for the Fund’s underlying portfolio holdings. There are various methods by which investors can purchase and sell Shares. Investors should consult their financial intermediaries before purchasing or selling Shares of the Fund.

Non-Diversification Risk. The Fund may become classified as non-diversified under the Investment Company Act of1940, as amended, solely as a result of a change in relative market capitalization or index weighting of one or more constituents of the ChiNext Index. If the Fund becomes non-diversified, it may invest a greater portion of assets in securities of a smaller number of individual issuers than a diversified fund. As a result, changes in the market value of a single investment could cause greater fluctuations in share price than would occur in a more diversified fund.

Concentration Risk. The Fund’s assets may be concentrated in a particular sector or sectors or industry or group of industries to the extent the ChiNext Index concentrates in a particular sector or sectors or industry or group of industries. To the extent that the Fund is concentrated in a particular sector or sectors or industry or group of industries, the Fund will be subject to the risk that economic, political or other conditions that have a negative effect on those sectors and/or industries may negatively impact the Fund to a greater extent than if the Fund’s assets were invested in a wider variety of sectors or industries.

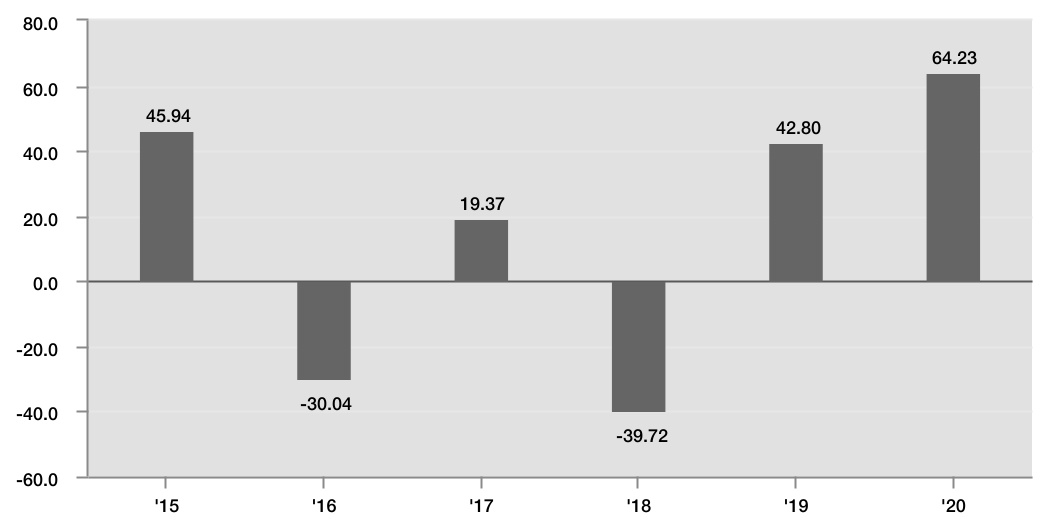

PERFORMANCE

The bar chart that follows shows how the Fund performed for the calendar years shown. The table below the bar chart shows the Fund’s average annual returns (before and after taxes). The bar chart and table provide an indication of the risks of investing in the Fund by comparing the Fund’s performance from year to year and by showing how the Fund’s average annual returns for the one year, five year, ten year and/or since inception periods, as applicable, compared with the Fund’s benchmark index and a broad measure of market performance. All returns assume reinvestment of dividends and distributions. The Fund’s past performance (before and after taxes) is not necessarily indicative of how the Fund will perform in the future. Updated performance information is available online at www.vaneck.com.

Annual Total Returns (%)—Calendar Years

[TO BE UPDATED]

| Best Quarter: | 49.51% | 1Q 2015 | ||||||

| Worst Quarter: | -29.80% | 3Q 2015 | ||||||

Average Annual Total Returns for the Periods Ended December 31, 2020

The after-tax returns presented in the table below are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Your actual after-tax returns will depend on your specific tax situation and may differ from those shown below. After-tax returns are not relevant to investors who hold Shares of the Fund through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

[TO BE UPDATED]

| Past One Year | Past Five Years | Since Inception (07/23/2014) | |||||||||||||||

| VanEck ChiNext ETF (return before taxes) | 64.23% | 3.37% | 11.33% | ||||||||||||||

| VanEck ChiNext ETF (return after taxes on distributions) | 64.22% | 3.37% | 11.33% | ||||||||||||||

| VanEck ChiNext ETF (return after taxes on distributions and sale of Fund Shares) | 38.02% | 2.63% | 9.18% | ||||||||||||||

| ChiNext Index (reflects no deduction for fees, expenses or taxes) | 71.71% | 6.15% | 14.35% | ||||||||||||||

S&P 500® Index (reflects no deduction for fees, expenses or taxes) | 18.40% | 15.22% | 12.64% | ||||||||||||||

See “License Agreements and Disclaimers” for important information.

PORTFOLIO MANAGEMENT

Investment Adviser. Van Eck Associates Corporation.

Investment Sub-Adviser. China Asset Management (Hong Kong) Limited.

Portfolio Managers. The following individuals are primarily and jointly responsible for the day-to-day management of the Fund’s portfolio:

| Name | Title with Sub-Adviser | Date Began Managing the Fund | ||||||||||||

| Max Lan | Portfolio Manager | March 2020 | ||||||||||||

| Name | Title with Adviser | Date Began Managing the Fund | ||||||||||||

| Peter H. Liao | Portfolio Manager | July 2014 | ||||||||||||

| Guo Hua (Jason) Jin | Portfolio Manager | March 2018 | ||||||||||||

PURCHASE AND SALE OF FUND SHARES

For important information about the purchase and sale of Fund Shares, tax information and payments to broker-dealers and other financial intermediaries, please turn to the “Summary Information About Purchases and Sales of Fund Shares, Taxes and Payments to Broker-Dealers and Other Financial Intermediaries” section of this Prospectus.

SUMMARY INFORMATION ABOUT PURCHASES AND SALES OF FUND SHARES, TAXES AND PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES | ||

PURCHASE AND SALE OF FUND SHARES

Individual Shares of the Fund may only be purchased and sold in secondary market transactions through a broker or dealer at a market price. Shares of the Fund are listed on the Exchange, and because Shares trade at market prices rather than NAV, Shares of the Fund may trade at a price greater than NAV (i.e., a "premium") or less than NAV (i.e., a "discount").

An investor may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase Shares of the Fund (bid) and the lowest price a seller is willing to accept for Shares (ask) when buying or selling Shares in the secondary market (the “bid/ask spread”).

Recent information, including information about the Fund’s NAV, market price, premiums and discounts, and bid/ask spreads, is included on the Fund’s website at www.vaneck.com.

TAX INFORMATION

The Fund’s distributions are taxable and will generally be taxed as ordinary income or capital gains.

PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

The Adviser and its related companies may pay broker-dealers or other financial intermediaries (such as a bank) for the sale of the Fund Shares and related services. These payments may create a conflict of interest by influencing your broker-dealer or other intermediary or its employees or associated persons to recommend the Fund over another investment. Ask your financial adviser or visit your financial intermediary’s website for more information.

ADDITIONAL INFORMATION ABOUT THE FUND'S INVESTMENT STRATEGIES AND RISKS | ||

PRINCIPAL INVESTMENT STRATEGIES

The Adviser and/or the Sub-Adviser anticipate that, generally, the portion of the Fund for which they are responsible will hold or gain exposure to all of the securities that comprise its benchmark index (the "Index") in proportion to their weightings in such Index. However, under various circumstances, it may not be possible or practicable to purchase all of those securities in those weightings. In these circumstances, the Fund may purchase a sample of securities in its Index. There also may be instances in which the Adviser and/or the Sub-Adviser may choose to underweight or overweight a security in the Fund’s Index, purchase securities not in the Fund’s Index that the Adviser and/or the Sub-Adviser believe are appropriate to substitute for certain securities in such Index or utilize various combinations of other available investment techniques in seeking to replicate as closely as possible, before fees and expenses, the price and yield performance of the Fund’s Index. The Fund may sell securities that are represented in its Index in anticipation of their removal from such Index or purchase securities not represented in its Index in anticipation of their addition to such Index. The Fund may also, in order to comply with the tax diversification requirements of the Internal Revenue Code, temporarily invest in securities not included in its Index that are expected to be highly correlated with the securities included in its Index.

The Fund’s assets will be primarily invested in A-shares. In addition, the Fund’s assets that are not allocated to the Sub-Adviser for investment will be managed by the Adviser for investment through Stock Connect, to the extent available.

Because the Fund does not satisfy the criteria to qualify as a RQFII or QFII themselves, the Fund intends to invest directly in A-shares via the Sub-Adviser’s RQFII license and may also invest through Stock Connect (to the extent available). In the event that the Sub-Adviser is unable to maintain its RQFII status or to seek to replicate the Fund’s Index through the other means described in this Prospectus, the Fund may retain one or more additional sub-advisers that maintain RQFII licenses and/or the Adviser may obtain a RQFII or QFII license and the Adviser or additional sub-adviser(s), on behalf of the Fund, may invest in A-shares and other permitted China securities listed on the Shenzhen and Shanghai Stock Exchanges.

FUNDAMENTAL AND NON-FUNDAMENTAL POLICIES

The Fund’s investment objective and each of its other investment policies are non-fundamental policies that may be changed by the Board of Trustees of the Trust (the “Board of Trustees”) without shareholder approval, except as noted in this Prospectus or the Statement of Additional Information (“SAI”) under the section entitled “Investment Policies and Restrictions—Investment Restrictions.”

RISKS OF INVESTING IN THE FUND

The following section provides additional information regarding the principal risks identified under “Principal Risks of Investing in the Fund” in the Fund’s “Summary Information” section followed by additional risk information. The risks listed below are applicable for the Fund unless otherwise noted.

Investors in the Fund should be willing to accept a high degree of volatility in the price of the Fund's Shares and the possibility of significant losses. An investment in the Fund involves a substantial degree of risk. An investment in the Fund is not a deposit with a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Therefore, you should consider carefully the following risks before investing in the Fund, each of which could significantly and adversely affect the value of an investment in the Fund.

Risk of the RQFII Regime and the Fund's Principal Investment Strategy. The ChiNext Index is comprised of A-shares. In seeking to replicate its Index, the Fund intends to invest directly in A-shares through the Sub-Adviser’s RQFII license and Stock Connect. Because the Fund will not be able to invest directly in A-shares beyond the limits that may be imposed by Stock Connect, the size of the Fund’s direct investment in A-shares may be limited. In addition, the RQFII license of the Sub-Adviser may be revoked by the Chinese regulators if, among other things, the Sub-Adviser fails to observe SAFE and other applicable Chinese regulations. There can be no assurance the Fund could retain a replacement sub-adviser with an RQFII license or other means of investing in A-shares if that became necessary or appropriate for any reason.

The Fund cannot predict what would occur if the RQFII license of the Sub-Adviser generally were eliminated, although such an occurrence would likely have a material adverse effect on the Fund, including the requirement that the Sub-Adviser on behalf of the Fund disposes of certain or all of its A-shares holdings, and may adversely affect the willingness and ability of potential swap counterparties to engage in swaps with the Fund linked to the performance of A-shares. These risks are compounded by the fact that, at present, there are only a limited number of firms and potential counterparties that have RQFII or QFII status or are willing and able to enter into swap transactions linked to the performance of A-shares. To the extent the Fund invests in swaps, there can be no guarantee that the Fund will be able to invest in appropriate swaps, and the PRC government may at times restrict the ability of firms regulated in the PRC to make such swaps available. Therefore, any such elimination may have a material adverse effect on the ability of the Fund to achieve its investment objective. If the Fund is unable to obtain sufficient exposure to the performance of its Index due to the limited availability of investments that provide exposure to the performance of A-shares, the Fund, subject to any necessary regulatory relief, could, among other things, as a defensive measure limit or suspend creations until the Adviser and/or the Sub-Adviser determine that the requisite exposure to the Index is obtainable. If any of the above events were to occur, the Fund could trade at a significant premium or discount to its net asset value (“NAV”) and could experience substantial redemptions and the Fund could, among other things, change its investment objective by, for example, seeking to

14 | ||

track an alternative index focused on Chinese-related stocks other than A-shares or other appropriate investments, or decide to liquidate the Fund.

On May 7, 2020, the People’s Bank of China (“PBOC”) and SAFE jointly issued the Regulations on Funds of Securities and Futures Investment by Foreign Institutional Investors (PBOC & SAFE Announcement [2020] No. 2, hereinafter referred to as the “FII Regulations”), which came into effect on 6 June 2020. The FII Regulations unify and supersede the rules applicable to QFII and RQFII regimes. One of the key changes of the FII Regulations is the removal of quota restrictions on investment.

The A-share market may be considered volatile with a risk of suspension of trading in a particular security or government intervention. Securities on the A-share market, including one or more securities in the Index, may be suspended from trading without an indication of how long the suspension will last, which may impair the liquidity of such securities.

Specific rules governing taxes on capital gains derived by RQFIIs and QFIIs from the trading of PRC securities have yet to be announced. In the absence of specific rules, the tax treatment of the Fund’s investments in A-shares through the Sub-Adviser’s RQFII quota should be governed by the general PRC tax provisions and provisions applicable to RQFIIs. Under these provisions, non-PRC tax resident enterprises without a permanent establishment in the PRC, such as the Fund, is generally subject to a tax of 10% on any PRC sourced income (including cash dividends, distributions, interest and capital gains) derived by it from an investment in PRC securities. Withholding taxes on dividends, interest and capital gains may be taxed at a reduced rate under an applicable tax treaty, but the application of such treaties for an RQFII acting on behalf of a foreign investor (i.e., the Sub-Adviser acting on behalf of the Fund) is also uncertain. It is also unclear how China’s business tax may apply to activities of an RQFII such as the Sub-Adviser and how such application may be affected by tax treaty provisions. While it is unclear whether this tax will be applied to investments by an RQFII, such as the Sub-Adviser, or what the methodology for calculating or collecting the tax will be, the PRC’s Ministry of Finance announced that, effective November 17, 2014, PRC-sourced gains on disposal of shares and other equity investments (including A-shares) derived by QFIIs or RQFIIs (without an establishment or place of business in the PRC or having an establishment or place of business in the PRC but the income so derived in the PRC is not effectively connected with such establishment or place) would be temporarily exempt from PRC corporate income tax. The current PRC tax laws and regulations and interpretations thereof may be revised or amended in the future, including with respect to the possible liability of the Fund for obligations of the Sub-Adviser. Any revision or amendment in tax laws and regulations may adversely affect the Fund. The Fund, prior to December 22, 2014, reserved 10% of its realized and unrealized gains from its A-share investments to apply towards withholding tax liability with respect to realized and unrealized gains from the Fund’s investments in A-shares of “land-rich” enterprises, which are companies that have greater than 50% of their assets in land or real properties in the PRC. The tax reserve was reflected in the Fund’s daily NAV calculations as a deduction from the Fund’s NAV. If the PRC begins applying tax rules regarding the taxation of capital gains from A-shares investment to RQFIIs, such as the Sub-Adviser, and/or begins collecting capital gains taxes on such investments, the Fund could be subject to withholding tax liability. The impact of any such tax liability on the Fund’s return could be substantial. The Fund may also potentially be subject to PRC value-added tax at the rate of 6% on capital gains derived from trading of A-shares. However, Caishui [2016] No. 36 and Caishui [2016] No. 70 provides a value-added tax exemption for QFIIs, as well as RQFIIs, in respect of their gains derived from the trading of PRC securities. In addition, urban maintenance and construction tax (currently at rates ranging from 1% to 7%), educational surcharge (currently at the rate of 3%) and local educational surcharge (currently at the rate of 2%) (collectively, the “Surtaxes”) are imposed based on value-added tax liabilities. Since QFIIs and RQFIIs are exempt from value-added tax, they are also exempt from the applicable Surtaxes. The Fund may also be liable to the Sub-Adviser for any tax that is imposed on the Sub-Adviser by the PRC with respect to the Fund’s investments.

The Sub-Adviser, as a licensed RQFII, is currently permitted to repatriate RMB daily and is not subject to RMB repatriation restrictions or prior approval, provided that final repatriation of capital and profits at the liquidation of the Fund will be subject to an audit report and tax filing. However, there is no assurance that RQFII may not be subject to restrictions or prior approval requirements in the future. Any additional restrictions imposed on the Sub-Adviser or RQFIIs generally may have adverse effect on the Fund’s ability to invest directly in A-shares and its ability to meet redemption requests.

If the Fund’s direct investments in A-shares through the Sub-Adviser’s RQFII license become subject to repatriation restrictions, the Fund may be unable to satisfy distribution requirements applicable to RICs under the Internal Revenue Code, and be subject to income and excise tax at the Fund level. In addition, the Fund could be required to recognize unrealized gains, pay taxes and make distributions before re-qualifying for taxation as a RIC. See below under “Shareholder Information—Tax Information—Taxes on Distributions” for more information. The Fund may elect, for U.S. federal income tax purposes, to treat Chinese taxes (including withholding taxes) paid by the Fund as paid by its shareholders. Even if the Fund is qualified to make that election and does so this treatment will not apply with respect to amounts the Fund reserves in anticipation of the imposition of withholding taxes not currently in effect (as discussed above). If these amounts are used to pay any tax liability of the Fund in a later year, they will be treated as paid by the shareholders in such later year, even if they are imposed with respect to income of an earlier year. See the section of this prospectus entitled “Shareholder Information—Tax Information” for a further description of this risk.

Special Risk Considerations of Investing in China. Investments in securities of Chinese issuers involve risks and special considerations not typically associated with investments in the U.S. securities markets, including the following:

Political and Economic Risk. The economy of China, which has been in a state of transition from a planned economy to a more market oriented economy, differs from the economies of most developed countries in many respects, including the level of government involvement, its state of development, its growth rate, control of foreign exchange, and allocation of resources. Although the majority of productive assets in China are still owned by the PRC government at various levels, in recent years, the PRC government has implemented economic reform measures emphasizing utilization of market forces in the development of the economy of China and a high level of management autonomy. The economy of China has experienced significant growth in the past 30 years, but growth has been uneven both geographically and among various sectors of the economy. Economic growth has also been accompanied by periods of high inflation. The PRC government has implemented various measures from time to time to control inflation and restrain the rate of economic growth.

For more than 30 years, the PRC government has carried out economic reforms to achieve decentralization and utilization of market forces to develop the economy of the PRC. These reforms have resulted in significant economic growth and social progress. There can, however, be no assurance that the PRC government will continue to pursue such economic policies or, if it does, that those policies will continue to be successful. Any such adjustment and modification of those economic policies may have an adverse impact on the securities market in the PRC as well as the underlying securities of the Fund’s Index. Further, the PRC government may from time to time adopt corrective measures to control the growth of the PRC economy which may also have an adverse impact on the capital growth and performance of the Fund.

Political changes, social instability and adverse diplomatic developments in the PRC could result in the imposition of additional government restrictions including expropriation of assets, confiscatory taxes or nationalization of some or all of the property held by the issuers of the Fund’s A-share investments or contained in the Fund’s Index.

Market volatility caused by potential regional or territorial conflicts or natural or other disasters, may have an adverse impact on the performance of the Fund.

The laws, regulations, including the investment regulations allowing RQFIIs (and QFIIs) to invest in A-shares, government policies and political and economic climate in China may change with little or no advance notice. Any such change could adversely affect market conditions and the performance of the Chinese economy and, thus, the value of the A-shares in the Fund’s portfolio.

Since 1949, the PRC has been a socialist state controlled by the Communist party. China has only recently opened up to foreign investment and has only begun to permit private economic activity. There is no guarantee that the Chinese government will not revert from its current open-market economy to the economic policy of central planning that it implemented prior to 1978.

Under the economic reforms implemented by the Chinese government, the Chinese economy has experienced tremendous growth, developing into one of the largest economies in the world. There is no assurance, however, that such growth will be sustained in the future.

The Chinese government continues to be an active participant in many economic sectors through ownership positions and regulation. The allocation of resources in China is subject to a high level of government control. The Chinese government strictly regulates the payment of foreign currency denominated obligations and sets monetary policy. Through its policies, the government may provide preferential treatment to particular industries or companies. The policies set by the government could have a substantial adverse effect on the Chinese economy and the Fund’s investments.

The Chinese economy is export-driven and highly reliant on trade, and much of China’s growth in recent years has been the result of focused investments in economic sectors intended to produce goods and services for export purposes. The performance of the Chinese economy may differ favorably or unfavorably from the U.S. economy in such respects as growth of gross domestic product, rate of inflation, currency revaluation, capital reinvestment, resource self-sufficiency and balance of payments position. Adverse changes to the economic conditions of its primary trading partners, such as the United States, Japan and South Korea, would adversely impact the Chinese economy and the Fund’s investments. International trade tensions involving China and its trading counterparties may arise from time to time which can result in trade tariffs, embargoes, sanctions, investment restrictions, trade limitations, trade wars and other negative consequences. Such actions and consequences may ultimately result in a significant reduction in international trade, an oversupply of certain manufactured goods, devaluations of existing inventories and potentially the failure of individual companies and/or large segments of China’s export industry with a potentially severe negative impact to the Fund.

Moreover, the current slowdown or any future recessions in other significant economies of the world, such as the United States, the European Union and certain Asian countries, may adversely affect economic growth in China. An economic downturn in China would adversely impact the Fund’s investments.

Inflation. Economic growth in China has also historically been accompanied by periods of high inflation. Beginning in 2004, the Chinese government commenced the implementation of various measures to control inflation, which included the tightening of the money supply, the raising of interest rates and more stringent control over certain industries. Rising inflation may, in the future, adversely affect the performance of the Chinese economy and the Fund’s investments.

Tax Changes. The Chinese system of taxation is not as well settled as that of the United States. China has implemented a number of tax reforms in recent years and may amend or revise its existing tax laws and/or procedures in the future, possibly with retroactive effect. Changes in applicable Chinese tax law, such as the cessation of tax exemptions in respect of investments in A-shares via RQFII and/or the Stock Connect, could reduce the after-tax profits of the Fund, directly or indirectly, including by reducing the after-tax profits of companies in China in which the Fund invests. Uncertainties in Chinese tax rules could result in unexpected tax liabilities for the Fund. Should legislation limit U.S. investors’ ability to invest in specific Chinese companies through A-shares or other share class listings that are part of the underlying holdings, these shares may be excluded from Fund holdings. In addition, changes in the Chinese tax system may have retroactive effects.

Nationalization and Expropriation. After the formation of the Chinese socialist state in 1949, the Chinese government renounced various debt obligations and nationalized private assets without providing any form of compensation. There can be no assurance that the Chinese government will not take similar actions in the future. Accordingly, an investment in the Fund involves a risk of a total loss.

Hong Kong Policy. As part of Hong Kong’s transition from British to Chinese sovereignty in 1997, China agreed to allow Hong Kong to maintain a high degree of autonomy with regard to its political, legal and economic systems for a period of at least 50 years. China controls matters that relate to defense and foreign affairs. Under the agreement, China does not tax Hong Kong, does not limit the exchange of the Hong Kong dollar for foreign currencies and does not place restrictions on free trade in Hong Kong. However, there is no guarantee that China will continue to honor the agreement, and China may change its policies regarding Hong Kong at any time. As of July 2020, the Chinese Standing Committee of the National People's Congress enacted the Law of the People's Republic of China on Safeguarding National Security in the Hong Kong Special Administrative Region. As of the same month, Hong Kong is no longer afforded preferential economic treatment by the United States under US law, and there is uncertainty as to how the economy of Hong Kong will be affected. Any further changes in PRC’s policies could adversely affect market conditions and the performance of the Hong Kong economy and, thus, the value of securities in the Fund’s portfolio.

Any such change could adversely affect market conditions and the performance of the Chinese economy and, thus, the value of securities in the Fund’s portfolio. Furthermore, as demonstrated by Hong Kong protests in recent years over political, economic, and legal freedoms, and the Chinese government's response to them, there continues to exist political uncertainty within Hong Kong.