Form 424B2 ROYAL BANK OF CANADA

Tweet

Tweet Share

Share

|

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-259205

|

||

|

Pricing Supplement

Dated May 13, 2022

To the Product Prospectus Supplement FIN-1 Dated September 14, 2021, and the Prospectus and Prospectus Supplement, each dated September 14, 2021

|

$2,152,000

Collared SOFR Floating Rate Notes, Due

May 19, 2025

Royal Bank of Canada

|

||

Royal Bank of Canada is offering the Collared SOFR Floating Rate Notes (the “Notes”) described in this document.

The CUSIP number for the Notes is 78014REN6.

The Notes will pay interest quarterly on the 19th day of each February, May, August and November, commencing on August 19, 2022, and ending on the Maturity Date.

The Notes will accrue interest at a per annum rate based on the Reference Rate during the term of the Notes. The “Reference Rate” is compounded SOFR, calculated as described in this document. In each

case, the interest rate on the Notes will be subject to a Coupon Cap of 5.00% and a Coupon Floor of 3.00%.

The Notes will not be listed on any securities exchange.

The Notes will be bail-inable notes (as defined in the accompanying prospectus supplement dated September 14, 2021) and subject to conversion in whole or in part – by means of a

transaction or series of transactions and in one or more steps – into common shares of the Bank or any of its affiliates under subsection 39.2(2.3) of the Canada Deposit Insurance Corporation Act (the “CDIC Act”) and to variation or

extinguishment in consequence, and subject to the application of the laws of the Province of Ontario and the federal laws of Canada applicable therein in respect of the operation of the CDIC Act with respect to the Notes.

Investing in the Notes involves a number of risks. See “Additional Risk Factors” on page P-6 of this pricing supplement, “Additional Risk Factors Specific to the Notes” beginning on page PS-5 of the

product prospectus supplement FIN-1 dated September 14, 2021 and “Risk Factors” on page S-2 of the prospectus supplement dated September 14, 2021.

The Notes will not constitute deposits insured by the Canada Deposit Insurance Corporation, the U.S. Federal Deposit Insurance Corporation or any other Canadian or U.S. government agency or

instrumentality.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or determined that this pricing supplement is truthful

or complete. Any representation to the contrary is a criminal offense.

We will deliver the Notes in book-entry only form through the facilities of The Depository Trust Company on May 19, 2022, against payment in immediately available funds.

|

Per Note

|

Total

|

||

|

Price to public(1)

|

100.00%

|

$2,152,000

|

|

|

Underwriting discounts and commissions(1)

|

1.00%

|

$21,520

|

|

|

Proceeds to Royal Bank of Canada

|

99.00%

|

$2,130,480

|

(1) UBS Financial Services Inc., which we refer to as UBS, will receive a commission of $10 per $1,000 principal amount of the Securities. See “Supplemental Plan of Distribution

(Conflicts of Interest)” below.

|

RBC Capital Markets, LLC

|

UBS Financial Services Inc.

|

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

The information in this “Summary” section is qualified by the more detailed information set forth in this pricing supplement, the product prospectus supplement FIN-1, the prospectus supplement, and the prospectus.

|

Issuer:

|

Royal Bank of Canada (“Royal Bank”)

|

|

Underwriter:

|

RBC Capital Markets, LLC

|

|

Currency:

|

U.S. Dollars

|

|

Minimum Investment:

|

$1,000 and minimum denominations of $1,000 in excess of $1,000

|

|

Pricing Date:

|

May 13, 2022

|

|

Issue Date:

|

May 19, 2022

|

|

Maturity Date:

|

May 19, 2025

|

|

Interest Rate:

|

The Notes will bear interest at a per annum rate based on the Reference Rate, subject to the Coupon Floor and the Coupon Cap.

|

|

Reference Rate:

|

The Reference Rate will be compounded SOFR, calculated as described in this document.

|

|

Coupon Floor:

|

3.00%

|

|

Coupon Cap:

|

5.00%

|

|

Day Count Fraction:

|

Interest will be calculated on a 30/360 basis.

|

|

Interest Payment

Dates:

|

Quarterly, on the 19th day of each February, May, August and November, commencing on August 19, 2022 and ending on the Maturity Date. If an Interest Payment Date falls on a day that is not

a business day in New York City, that Interest Payment Day will be postponed to the next day that is such a business day, with the same effect as if paid on the original due date. However, if the next such business day falls in the next

calendar month, then the Interest Payment Date will be advanced to the next preceding day that is a business day in New York City.

|

|

Interest Period:

|

Each period from, and including, an Interest Payment Date (or, for the first period, the issue date) to, but excluding, the next following Interest Payment Date.

|

|

Interest Determination

Dates:

|

Five U.S. Government Securities Business Days prior to the applicable Interest Payment Date. A “U.S. Government Securities Business Day” is any day except for a Saturday, a Sunday, or a day on which the

Securities Industry and Financial Markets Association (or any successor thereto) recommends that the fixed income departments of its members be closed for the entire day for purposes of trading in U.S. government securities.

|

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

|

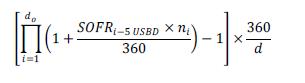

Compounded SOFR:

|

Interest on the Notes will be determined based on the daily compounding of interest, with the daily SOFR used for the calculation of interest.

The interest payable on the Notes will be calculated by the Calculation Agent on each relevant Interest Determination Date occurring prior to the applicable Interest

Payment Date as follows. The resulting percentage will be rounded if necessary to the fifth decimal place, with 0.000005 being rounded upwards:

Where:

“d” is the number of calendar days in the relevant interest period;

“do” is the number of U.S. Government Securities Business Days in the relevant Observation Period;

“i” is a series of whole numbers from one to do, each representing the relevant U.S. Government Securities Business Day in chronological order from, and

including, the first U.S. Government Securities Business Day in the relevant Observation Period;

“ni”, for any U.S. Government Securities Business Day “i”, means the number of calendar days from, and including, such U.S. Government Securities Business

Day “i” up to, but excluding, the following U.S. Government Securities Business Day;

"Observation Period" means the period from, and including, the date falling five U.S. Government Securities Business Days prior to the first day of the relevant

interest period to (but excluding) the date falling five U.S. Government Securities Business Days prior to last day included in the relevant interest period;

“SOFR reference rate,” in respect of any U.S. Government Securities Business Day is a reference rate equal to the daily secured overnight financing (“SOFR”) rate for

that day, as provided by the Federal Reserve Bank of New York, as the administrator of such rate (or any successor administrator of such rate) on the website of the Federal Reserve Bank of New York currently at www.newyorkfed.org, or

any successor website of the Federal Reserve Bank of New York (in each case, on or about 5:00 p.m., New York City time, on the U.S. Government Securities Business Day immediately following that day); provided, however, if that rate is

not available at or around the indicated time on such date (and a Benchmark Transition Event and its related Benchmark Replacement Date (each as defined below) have not occurred), the SOFR reference rate for the applicable U.S.

Government Securities Business Day will be the SOFR rate in respect of the last U.S. Government Securities Business Day for which such rate was published on the Federal Reserve Bank of New York’s website; and

“SOFRi-5USBD” means, in respect of any U.S. Government Securities Business Day “i”, the SOFR reference rate for the U.S. Government Securities Business Day

falling five U.S. Government Securities Business Days prior to the relevant U.S. Government Securities Business Day “i”.

|

|

Redemption:

|

Not Applicable.

|

|

Survivor’s Option:

|

Not Applicable.

|

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

|

Calculation Agent:

|

RBC Capital Markets, LLC

|

|

Listing:

|

The Notes will not be listed on any securities exchange.

|

|

Clearance and

Settlement:

|

DTC global (including through its indirect participants Euroclear and Clearstream, Luxembourg as described under “Ownership and Book-Entry Issuance” in the prospectus dated September 14,

2021).

|

|

U.S. Tax Treatment:

|

In the opinion of our special U.S. tax counsel, Ashurst LLP, the Notes will be treated as variable rate debt instruments providing for stated interest at a single qualified floating rate.

Under this treatment, stated interest on the Notes will be taxable to a U.S. holder as ordinary interest income at the time it accrues or is received in accordance with the U.S. holder's method of tax accounting.

Please see the discussion in the accompanying prospectus dated September 14, 2021 under the section entitled “Tax Consequences—United States Taxation” and specifically the discussion under

“Tax Consequences—United States Taxation—Original Issue Discount—Variable Rate Debt Securities,” and in the product prospectus supplement FIN-1 dated September 14, 2021 (including the opinion of our special U.S. tax counsel) under

“Supplemental Discussion of U.S. Federal Income Tax Consequences” and specifically the discussion under “Supplemental Discussion of U.S. Federal Income Tax Consequences—Supplemental U.S. Tax Considerations—Where the term of your notes

will exceed one year—Fixed Rate Notes, Floating Rate Notes, Inverse Floating Rate Notes, Step Up Notes, Leveraged Notes, Range Accrual Notes, Dual Range Accrual Notes and Non-Inversion Range Accrual Notes,” and “Supplemental Discussion

of U.S. Federal Income Tax Consequences—Supplemental U.S. Tax Considerations—Where the term of your notes will exceed one year—Sale, Redemption or Maturity of Notes that Are Not Treated as Contingent Payment Debt Instruments,” which

apply to your Notes.

|

|

Terms Incorporated in

the Master Note: |

All of the terms appearing above the item captioned “Listing” on pages P-2 to P-4 of this pricing supplement, the sections below, "Agreement With Respect to the Exercise of Canadian Bail-In Powers" and

"Effect of Benchmark Transition Event on SOFR," and the applicable terms appearing under the caption “General Terms of the Notes” in the product prospectus supplement FIN-1, as modified by this pricing supplement.

|

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

ADDITIONAL TERMS OF YOUR NOTES

You should read this pricing supplement together with the prospectus dated September 14, 2021, as supplemented by the prospectus supplement dated September 14, 2021 and the product prospectus

supplement FIN-1 dated September 14, 2021, relating to our Senior Global Medium-Term Notes, Series I, of which these Notes are a part. Capitalized terms used but not defined in this pricing supplement will have the meanings given to them in the

product prospectus supplement FIN-1. In the event of any conflict, this pricing supplement will control. The Notes vary from the terms described in the product prospectus supplement FIN-1 in

several important ways. You should read this pricing supplement carefully.

This pricing supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any other written

materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the

matters set forth in “Risk Factors” in the prospectus supplement dated September 14, 2021, “Additional Risk Factors Specific to the Notes” in the product prospectus supplement FIN-1 dated September 14, 2021 and “Additional Risk Factors” in this

pricing supplement, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. You may access these documents on

the SEC website at www.sec.gov as follows (or if that address has changed, by reviewing our filings for the relevant date on the SEC website):

Prospectus dated September 14, 2021:

Prospectus Supplement dated September 14, 2021:

Product Prospectus Supplement FIN-1 dated September 14, 2021:

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

ADDITIONAL RISK FACTORS

The Notes involve risks not associated with an investment in ordinary floating rate notes. This section describes the most significant risks relating to the terms of the Notes. For additional

information as to the risks related to an investment in the Notes, please see the accompanying product prospectus supplement FIN-1 and the prospectus supplement and prospectus, each dated September 14, 2021. You should carefully consider

whether the Notes are suited to your particular circumstances before you decide to purchase them. Accordingly, prospective investors should consult their financial and legal advisors as to the risks entailed by an investment in the Notes and

the suitability of the Notes in light of their particular circumstances.

Risks Relating to the Terms and Structure of the Notes

The Amount of Interest Payable on the Notes will Vary. The Notes differ from conventional fixed-rate debt securities in that the interest payable on the

Notes will vary based on the level of SOFR. The interest rate payable on the Notes may be as low as the Floor on each Interest Payment Date.

The Yield on the Notes May Be Lower Than the Yield on a Conventional Fixed-Rate Debt Security of Ours of Comparable Maturity. The interest rate applicable

to the Notes will vary based on the level of SOFR, and may be as low as the Floor on each Interest Payment Date. As a result, the effective yield on the Notes may be less than that which would be payable on a conventional fixed-rate,

non-callable debt security of ours of comparable maturity.

The Amount of Interest Payable on the Notes Is Capped. The interest rate on the Notes for each quarterly interest period is capped for that period at the

interest rate set forth on the cover of this pricing supplement. Thus, you will not benefit from the Reference Rate being greater than the Cap in any quarterly interest period.

Investors Are Subject to Our Credit Risk, and Our Credit Ratings and Credit Spreads May Adversely Affect the Market Value of the Notes. Investors are

dependent on our ability to pay all amounts due on the Notes on the Interest Payment Dates and at maturity, and, therefore, investors are subject to our credit risk and to changes in the market’s view of our creditworthiness. Any decrease in

our credit ratings or increase in the credit spreads charged by the market for taking our credit risk is likely to adversely affect the market value of the Notes. If we were to default on our obligations, you may not receive the amounts owed to

you under the terms of the Notes, and you could lose your entire initial investment.

Risks Relating to the Secondary Market for the Notes

There May Not Be an Active Trading Market for the Notes—Sales in the Secondary Market May Result in Significant Losses. There may be little or no secondary

market for the Notes. The Notes will not be listed on any securities exchange. RBCCM and our other affiliates intend to offer to purchase the Notes in the secondary market, but they are not required to do so. Because we do not expect that

other market makers will participate significantly in the secondary market for the Notes, the price at which you may be able to trade the Notes is likely to depend on the price, if any, at which RBCCM or one of our other affiliates is willing

to buy the Notes. RBCCM or any other affiliate of ours may stop any market-making activities at any time. Even if a secondary market for the Notes develops, it may not provide significant liquidity or trade at prices advantageous to you. We

expect that transaction costs in any secondary market would be high. As a result, the difference between bid and asked prices for the Notes in any secondary market could be substantial. If you sell the Notes before maturity, you may have to do

so at a substantial discount from the issue price, and as a result, you may suffer substantial losses.

The Price at Which You May Be Able to Sell Your Notes Prior to Maturity Will Depend on a Number of Factors, and May Be Substantially Less Than the Amount You Originally Invest. If

you attempt to sell the Notes prior to maturity, their market value may be lower than the price you paid for them. This is due to, among other things, changes in the level of the Reference Rate, our credit ratings and financial condition, the

borrowing rate we pay to issue securities of

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

this kind, and the inclusion in the price to the public of the underwriting discount and the estimated costs and profits relating to our hedging of the Notes. These factors, together with various

credit, market and economic factors over the term of the Notes, may reduce the price at which you may be able to sell the Notes in any secondary market and will affect the value of the Notes in complex and unpredictable ways. Assuming no

change in market conditions or any other relevant factors, the price, if any, at which you may be able to sell your Notes prior to maturity may be less than your original purchase price, as, for example, any such sale price would not be

expected to include the underwriting discount and the hedging costs relating to the Notes.

Risks Relating to SOFR

The Secured Overnight Financing Rate Is a Relatively New Reference Rate and its Composition and Characteristics Are Not

the Same as LIBOR. On June 22, 2017, the Alternative Reference Rates Committee (“ARRC”) convened by the Board of Governors of the Federal Reserve System and the Federal Reserve Bank of New York identified the Secured Overnight

Financing Rate (“SOFR”) as the rate that, in the consensus view of the ARRC, represented best practice for use in certain new U.S. dollar derivatives and other financial contracts. SOFR is a broad measure of the cost of borrowing cash overnight

collateralized by U.S. treasury securities, and has been published by the Federal Reserve Bank of New York since April 2018. The Federal Reserve Bank of New York has also begun publishing historical indicative Secured Overnight Financing Rates

from 2014. Investors should not rely on any historical changes or trends in SOFR as an indicator of future changes in SOFR.

The composition and characteristics of SOFR are not the same as those of LIBOR, and SOFR is fundamentally different from LIBOR for two key reasons. First,

SOFR is a secured rate, while LIBOR is an unsecured rate. Second, SOFR is an overnight rate, while LIBOR is a forward-looking rate that represents interbank funding over different maturities (e.g., three months). As a result, there can be no

assurance that SOFR (including SOFR, compounded as described in this document) will perform in the same way as LIBOR would have at any time, including, without limitation, as a result of changes in interest and yield rates in the market, market

volatility or global or regional economic, financial, political, regulatory, judicial or other events.

SOFR May Be More Volatile Than Other Benchmark or Market Rates. Since the initial publication of SOFR, daily changes in SOFR

have, on occasion, been more volatile than daily changes in other benchmark or market rates, such as USD LIBOR. Although changes in SOFR, compounded as described in this document, generally are not expected to be as volatile as changes in daily

levels of SOFR, the return on and value of the Notes may fluctuate more than floating rate securities that are linked to less volatile rates. In addition, the volatility of SOFR has reflected the underlying volatility of the overnight U.S.

Treasury repo market. The Federal Reserve Bank of New York has at times conducted operations in the overnight U.S. Treasury repo market in order to help maintain the federal funds rate within a target range. There can be no assurance that the

Federal Reserve Bank of New York will continue to conduct such operations in the future, and the duration and extent of any such operations is inherently uncertain. The effect of any such operations, or of the cessation of such operations to

the extent they are commenced, is uncertain and could be materially adverse to investors in the Notes.

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

Any Failure of SOFR to Gain Market Acceptance Could Adversely Affect the Notes. According to the ARRC, SOFR was developed for use in

certain U.S. dollar derivatives and other financial contracts as an alternative to USD LIBOR in part because it is considered a good representation of general funding conditions in the overnight U.S. Treasury repurchase agreement market.

However, as a rate based on transactions secured by U.S. Treasury securities, it does not measure bank-specific credit risk and, as a result, is less likely to correlate with the unsecured short-term funding costs of banks. This may mean that

market participants would not consider SOFR a suitable replacement or successor for all of the purposes for which USD LIBOR historically has been used (including, without limitation, as a representation of the unsecured short-term funding costs

of banks), which may, in turn, lessen market acceptance of SOFR. Any failure of SOFR to gain market acceptance could adversely affect the return on and value of the Notes and the price at which investors can sell the Notes in any secondary

market.

In addition, if SOFR does not prove to be widely used as a benchmark in securities that are similar or comparable to the Notes, the trading price of the

Notes may be lower than those of securities that are linked to rates that are more widely used. Similarly, market terms for floating-rate debt securities linked to SOFR, such as the spread over the base rate reflected in interest rate

provisions or the manner of compounding the base rate, may evolve over time, and trading prices of the Notes may be lower than those of later-issued SOFR-based debt securities as a result. Investors in the Notes may not be able to sell the

Notes at all or may not be able to sell the Notes at prices that will provide them with a yield comparable to similar investments that have a developed secondary market, and may consequently suffer from increased pricing volatility and market

risk.

The Interest Rate on the Notes Is Based on a Compounded SOFR Rate, which is Relatively New in the Marketplace. The interest rate on

the Notes will be based on compounded SOFR, which is calculated using the SOFR published by the Federal Reserve Bank of New York, compounded according to the specific formula described above, and not the SOFR rate published on or in respect of

a particular date during an interest period or an arithmetic average of SOFR rates during that period. For this and other reasons, the interest rate on the Notes during any interest period will not necessarily be the same as the interest rate

on other SOFR-linked investments that use an alternative basis to determine the interest rate. Further, if the SOFR rate in respect of a particular date during an interest period is negative, its contribution to compounded SOFR will be less

than one, resulting in a reduction to the formula used to calculate the interest payable on the Notes on the Interest Payment Date for such interest period.

Limited market precedent exists for securities that use SOFR as the interest rate, and the method for calculating an interest rate based upon SOFR in

those precedents varies. Accordingly, the use of SOFR and/or the specific formula for compounded SOFR used in the Notes may not be widely adopted by other market participants, if at all. If the market adopts a different calculation method, that

would likely adversely affect the market value of the Notes.

The Reference Rate with Respect to a Particular Interest Period Will Only Be Capable of Being Determined Near the End of

the Relevant Interest Period. Compounded SOFR applicable to a particular interest period and, therefore, the amount of interest payable with respect to such interest period will be determined on the Interest Determination Date (as

defined above) for such interest period. Because each such date is near the end of such interest period, you will not know the amount of interest payable with respect to a particular interest period until shortly prior to the related Interest

Payment Date, and it may be difficult for you to reliably estimate the amount of interest that will be payable on each such Interest Payment Date. In addition, some investors may be unwilling or unable to trade the Notes without changes to

their information technology systems, both of which could adversely impact the liquidity and trading price of the Notes.

SOFR May Be Modified or Discontinued and the Notes May Bear Interest by Reference to a Rate Other than SOFR, which Could Adversely

Affect the Value of the Notes. SOFR is published by the Federal Reserve Bank of New York based on data received by it from sources other than us, and we have no control over its methods of calculation, publication schedule, rate

revision practices or availability of SOFR at any time. There can be no guarantee, particularly given its relatively recent introduction, that SOFR will not be discontinued or fundamentally altered in a manner that is materially adverse to the

interests of investors in the Notes. If the manner in which SOFR is calculated, including the manner in which SOFR is calculated, is changed, that change may result in a reduction in the amount of interest payable

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

on the Notes and the trading prices of the Notes. In addition, the Federal Reserve Bank of New York may withdraw, modify or amend the published SOFR data

in its sole discretion and without notice. The interest rate for any interest period will not be adjusted for any modifications or amendments to SOFR data that the Federal Reserve Bank of New York may publish after the interest rate for that

interest period has been determined.

If the Calculation Agent determines that a Benchmark Transition Event and its related Benchmark Replacement Date have occurred in respect of SOFR, then

the interest rate on the Notes will no longer be determined by reference to SOFR, but instead will be determined by reference to a different rate, plus a spread adjustment, which we refer to as a “Benchmark Replacement,” as further described

below.

If a particular Benchmark Replacement or Benchmark Replacement Adjustment cannot be determined, then the next-available Benchmark Replacement or Benchmark

Replacement Adjustment will apply. These replacement rates and adjustments may be selected, recommended or formulated by (i) the Relevant Governmental Body (such as the ARRC), (ii) the International Swaps and Derivatives Association (“ISDA”) or

(iii) in certain circumstances, the Calculation Agent. In addition, the terms of the Notes expressly authorize the Calculation Agent to make Benchmark Replacement Conforming Changes with respect to, among other things, changes to the definition

of “interest period,” the methodology, timing and frequency of determining rates and making payments of interest and other administrative matters. The determination of a Benchmark Replacement, the calculation of the interest rate on the Notes

by reference to a Benchmark Replacement (including the application of a Benchmark Replacement Adjustment), any implementation of Benchmark Replacement Conforming Changes and any other determinations, decisions or elections that may be made

under the terms of the Notes in connection with a Benchmark Transition Event, could adversely affect the value of the Notes, the return on the Notes and the price at which you can sell such Notes.

In addition, (i) the composition and characteristics of the Benchmark Replacement will not be the same as those of SOFR, the Benchmark Replacement may not

be the economic equivalent of SOFR, there can be no assurance that the Benchmark Replacement will perform in the same way as SOFR would have at any time and there is no guarantee that the Benchmark Replacement will be a comparable substitute

for SOFR (each of which means that a Benchmark Transition Event could adversely affect the value of the Notes, the return on the Notes and the price at which you may sell the Notes), (ii) any failure of the Benchmark Replacement to gain market

acceptance could adversely affect the Notes, (iii) the Benchmark Replacement may have a very limited history and the future performance of the Benchmark Replacement may not be predicted based on historical performance, (iv) the secondary

trading market for Notes linked to the Benchmark Replacement may be limited and (v) the administrator of the Benchmark Replacement may make changes that could change the value of the Benchmark Replacement or discontinue the Benchmark

Replacement and has no obligation to consider your interests in doing so.

Additional Risks Relating to Conflicts of Interest

Trading Activities by Royal Bank or its Affiliates May Adversely Affect the Market Value of the Notes. As

described in the product prospectus supplement under the caption “Use of Proceeds and Hedging,” we or one or more affiliates may hedge our obligations under the Notes by purchasing securities, futures, options or other derivative instruments

with returns linked or related to changes in the level of the Reference Rate. We may adjust these hedges by, among other things, purchasing or selling these instruments at any time. It is possible that we or one or more of our affiliates could

receive substantial returns from these hedging activities while the market value of the Notes declines. We or one or more of our affiliates may also issue or underwrite other securities or financial or derivative instruments with returns

linked or related to changes in the performance of the Reference Rate. By introducing competing products into the marketplace in this manner, we or one or more of our affiliates could adversely affect the market value of the Notes.

We and our affiliates expect to engage in trading activities related to the Reference Rate that are not for the account of holders of the Notes or on their behalf.

These trading activities may present a conflict between the holders’ interest in the Notes and the interests we and our affiliates will have in their proprietary accounts, in facilitating transactions, including

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

options and other derivatives transactions, for their customers and in accounts under their management. These trading activities could be adverse to the

interests of the holders of the Notes.

There Are Potential Conflicts of Interest Between You and the Calculation Agent. The Calculation Agent will, among other

things, decide the amount of your payment for each Interest Payment Date. Our wholly-owned subsidiary, RBCCM, will serve as the Calculation Agent. We may change the Calculation Agent after the date of this document without notice to you. Since

the determinations by the Calculation Agent may affect payments on the Notes, the Calculation Agent may have a conflict of interest if it needs to make any such determination with respect to the Notes.

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

AGREEMENT WITH RESPECT TO THE EXERCISE OF CANADIAN BAIL-IN POWERS

By its acquisition of the Notes, each holder or beneficial owner is deemed to (i) agree to be bound, in respect of that Note, by the CDIC Act, including the conversion of

that Note, in whole or in part – by means of a transaction or series of transactions and in one or more steps – into common shares of the Bank or any of its affiliates under subsection 39.2(2.3) of the CDIC Act and the variation or

extinguishment of that Note in consequence, and by the application of the laws of the Province of Ontario and the federal laws of Canada applicable therein in respect of the operation of the CDIC Act with respect to that Note; (ii) attorn and

submit to the jurisdiction of the courts in the Province of Ontario with respect to the CDIC Act and those laws; and (iii) acknowledge and agree that the terms referred to in paragraphs (i) and (ii), above, are binding on that holder or

beneficial owner despite any provisions in the indenture or that Note, any other law that governs that Note and any other agreement, arrangement or understanding between that holder or beneficial owner and the Bank with respect to that Note.

Holders and beneficial owners of any Note will have no further rights in respect of that Note to the extent that Note is converted in a bail-in conversion, other than those

provided under the bail-in regime, and by its acquisition of an interest in any Note, each holder or beneficial owner of that Note is deemed to irrevocably consent to the converted portion of the principal amount of that Note and any accrued

and unpaid interest thereon being deemed paid in full by the Bank by the issuance of common shares of the Bank (or, if applicable, any of its affiliates) upon the occurrence of a bail-in conversion, which bail-in conversion will occur without

any further action on the part of that holder or beneficial owner or the trustee; provided that, for the avoidance of doubt, this consent will not limit or otherwise affect any rights that holders or beneficial owners may have under the bail-in

regime.

See “Description of Notes We May Offer―Special Provisions Related to Bail-inable Notes” in the accompanying prospectus supplement dated September 14, 2021 for a description of provisions

applicable to the Notes as a result of Canadian bail-in powers.

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

HISTORICAL INFORMATION

Historically, the Reference Rate has experienced significant fluctuations. Any historical upward or downward trend in the levels of the Reference Rate during any period shown below is not an

indication that the interest payable on the Notes is more or less likely to increase or decrease at any time during the term of the Notes.

The graph below sets forth the historical performance of SOFR from April 1, 2018 to May 13, 2022.

SOFR

Source: Bloomberg L.P. We have not independent verified the information provided by Bloomberg L.P.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

EFFECT OF BENCHMARK TRANSITION EVENT ON SOFR

(a) Benchmark Replacement. If the Calculation Agent determines that a Benchmark Transition Event and its related Benchmark Replacement Date have occurred

prior to the Reference Time in respect of any determination of the Benchmark on any date applicable to the payments on the Notes, the Benchmark Replacement will replace the then-current Benchmark for all purposes relating to the Notes in

respect of such determination on such date and all determinations on all subsequent dates.

(b) Benchmark Replacement Conforming Changes. In connection with the implementation of a Benchmark Replacement, the Calculation Agent will have the right

to make Benchmark Replacement Conforming Changes from time to time.

(c) Decisions and Determinations. Any determination, decision or election that may be made by the Calculation Agent or us pursuant to the benchmark

replacement provisions described herein, including any determination with respect to tenor, rate or adjustment or of the occurrence or non-occurrence of an event, circumstance or date and any decision to take or refrain from taking any action

or any selection:

| • |

will be conclusive and binding absent manifest error, may be made in the Calculation Agent’s sole discretion, notwithstanding anything to the contrary in this pricing supplement and the accompanying product

supplement, prospectus supplement and prospectus relating to the Notes;

|

| • |

if made by us, will be made in our sole discretion;

|

| • |

if made by the Calculation Agent, will be made after consultation with us, and the Calculation Agent will not make any such determination, decision or election to which we object; and

|

| • |

shall become effective without consent from any other party.

|

Any determination, decision or election pursuant to the benchmark replacement provisions not made by the Calculation Agent will be made by us on the basis as described above. The Calculation

Agent shall have no liability for not making any such determination, decision or election. In addition, we may designate an entity (which may be our affiliate) to make any determination, decision or election that we have the right to make in

connection with the benchmark replacement provisions set forth in this pricing supplement.

Certain Defined Terms

As used herein:

“Benchmark” means, initially, the SOFR reference rate, as such term is defined above; provided that if a Benchmark Transition Event and its related

Benchmark Replacement Date have occurred with respect to SOFR or the then-current Benchmark, then “Benchmark” means the applicable Benchmark Replacement.

“Benchmark Replacement” means the first alternative set forth in the order below that can be determined by the Calculation Agent as of the Benchmark

Replacement Date:

| (1) |

the sum of: (a) an alternate rate of interest that has been selected or recommended by the Relevant Governmental Body as the replacement for the then-current Benchmark for the applicable Corresponding Tenor

and (b) the Benchmark Replacement Adjustment;

|

| (2) |

the sum of: (a) the ISDA Fallback Rate and (b) the Benchmark Replacement Adjustment; and

|

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

| (3) |

provided that if (i) the Benchmark Replacement cannot be determined in accordance with clause (1) or (2) above as of the Benchmark Replacement Date or (ii) the Calculation Agent shall have determined that

the ISDA Fallback Rate determined in accordance with clause (2) above is not an industry-accepted rate of interest as a replacement for the then-current Benchmark for U.S. dollar-denominated floating rate notes at such time, then the

Benchmark Replacement shall be the sum of: (a) the alternate rate of interest that has been selected by the Calculation Agent as the replacement for the then-current Benchmark for the applicable Corresponding Tenor giving due

consideration to any industry-accepted rate of interest as a replacement for the then-current Benchmark for U.S. dollar denominated floating rate notes at such time and (b) the Benchmark Replacement Adjustment.

|

“Benchmark Replacement Adjustment” means the first alternative set forth in the order below that can be determined by the Calculation Agent as of the

Benchmark Replacement Date:

| (1) |

the spread adjustment (which may be a positive or negative value or zero), or method for calculating or determining such spread adjustment that has been selected or recommended by the Relevant Governmental

Body for the applicable Unadjusted Benchmark Replacement;

|

| (2) |

if the applicable Unadjusted Benchmark Replacement is equivalent to the ISDA Fallback Rate, then the ISDA Fallback Adjustment; and

|

| (3) |

the spread adjustment (which may be a positive or negative value or zero) that has been selected by the Calculation Agent giving due consideration to any industry-accepted spread adjustment, or method for

calculating or determining such spread adjustment, for the replacement of the then-current Benchmark with the applicable Unadjusted Benchmark Replacement for U.S. dollar denominated floating rate notes at such time.

|

“Benchmark Replacement Conforming Changes” means, with respect to any Benchmark Replacement, any technical, administrative or operational changes

(including changes to the definitions or interpretations of interest period, Observation Period, the methodology, timing and frequency of determining rates and making payments of interest, the rounding of amounts or tenors, and other

administrative matters) that the Calculation Agent decides may be appropriate to reflect the adoption of such Benchmark Replacement in a manner substantially consistent with market practice (or, if the Calculation Agent decides that adoption of

any portion of such market practice is not administratively feasible or if the Calculation Agent determines that no market practice for use of the Benchmark Replacement exists or that no market practice for such use is applicable to the Notes

offered hereby, in such other manner as the Calculation Agent determines is reasonably practicable).

“Benchmark Replacement Date” means the earliest to occur of the following events with respect to the then-current Benchmark:

| (1) |

in the case of clause (1) or (2) of the definition of “Benchmark Transition Event,” the later of (a) the date of the public statement or publication of information referenced therein and (b) the date on

which the administrator of the Benchmark permanently or indefinitely ceases to provide the Benchmark; or

|

| (2) |

in the case of clause (3) of the definition of “Benchmark Transition Event,” the date of the public statement or publication of information referenced therein.

|

For the avoidance of doubt, if the event giving rise to the Benchmark Replacement Date occurs on the same day as, but earlier than, the Reference Time in respect of any determination, the

Benchmark Replacement Date will be deemed to have occurred prior to the Reference Time for such determination.

For the avoidance of doubt, for purposes of the definitions of Benchmark Replacement Date and Benchmark Transition Event, references to Benchmark also include any reference rate underlying such Benchmark.

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

“Benchmark Transition Event” means the occurrence of one or more of the following events with respect to the then-current Benchmark:

| (1) |

a public statement or publication of information by or on behalf of the administrator of the Benchmark announcing that such administrator has ceased or will cease to provide the Benchmark, permanently or

indefinitely, provided that, at the time of such statement or publication, there is no successor administrator that will continue to provide the Benchmark;

|

| (2) |

a public statement or publication of information by the regulatory supervisor for the administrator of the Benchmark, the central bank for the currency of the Benchmark, an insolvency official with

jurisdiction over the administrator for the Benchmark, a resolution authority with jurisdiction over the administrator for the Benchmark or a court or an entity with similar insolvency or resolution authority over the administrator

for the Benchmark, which states that the administrator of the Benchmark has ceased or will cease to provide the Benchmark permanently or indefinitely, provided that, at the time of such statement or publication, there is no successor

administrator that will continue to provide the Benchmark; or

|

| (3) |

a public statement or publication of information by the regulatory supervisor for the administrator of the Benchmark announcing that the Benchmark is no longer representative.

|

“Corresponding Tenor” with respect to a Benchmark Replacement means a tenor (including overnight) having approximately the same length (disregarding

business day adjustment) as the applicable tenor for the then-current Benchmark.

“Federal Reserve Bank of New York’s Website” means the website of the Federal Reserve Bank of New York, currently

at http://www.newyorkfed.org, or any successor source.

“ISDA Definitions” means the 2006 ISDA Definitions published by the International Swaps and Derivatives Association, Inc. or any successor thereto, as

amended or supplemented from time to time, or any successor definitional booklet for interest rate derivatives published from time to time.

“ISDA Fallback Adjustment” means the spread adjustment (which may be a positive or negative value or zero) that would apply for derivatives transactions

referencing the ISDA Definitions to be determined upon the occurrence of an index cessation event with respect to the Benchmark for the applicable tenor.

“ISDA Fallback Rate” means the rate that would apply for derivatives transactions referencing the ISDA Definitions to be effective upon the occurrence of

an index cessation date with respect to the Benchmark for the applicable tenor excluding the applicable ISDA Fallback Adjustment.

“Reference Time” with respect to any determination of the Benchmark means (1) if the Benchmark is SOFR, the time determined as set forth above with

respect to SOFR, and (2) if the Benchmark is not SOFR, the time determined by the Calculation Agent in accordance with the Benchmark Replacement Conforming Changes.

“Relevant Governmental Body” means the Federal Reserve Board and/or the Federal Reserve Bank of New York, or a committee officially endorsed or convened

by the Federal Reserve Board and/or the Federal Reserve Bank of New York or any successor thereto.

“Unadjusted Benchmark Replacement” means the Benchmark Replacement excluding the Benchmark Replacement Adjustment.

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

SUPPLEMENTAL PLAN OF DISTRIBUTION (CONFLICTS OF INTEREST)

Delivery of the Notes will be made against payment for the Notes on May 19, 2022, which is the fourth business day following the Pricing Date (this settlement cycle being referred to as “T+4”).

See “Plan of Distribution” in the prospectus supplement dated September 14, 2021.

We will deliver the Notes on a date that is greater than two business days following the Pricing Date. Under Rule 15c6-1 of the Exchange Act, trades in the secondary market

generally are required to settle in two business days, unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade the Notes more than two business days prior to the original Issue Date will be

required to specify alternative arrangements to prevent a failed settlement.

We have agreed to indemnify UBS and RBCCM against liabilities under the Securities Act of 1933, as amended, or to contribute payments that UBS and RBCCM may be required to make

relating to these liabilities as described in the prospectus supplement and the prospectus. We have agreed that UBS may sell all or a part of the Notes that it will purchase from us to investors or its affiliates at the price indicated on the

cover page of this pricing supplement. UBS may allow a concession not in excess of the underwriting discount set forth on the cover of this pricing supplement to its affiliates for distribution of the Notes.

After the initial offering of the Notes, the price to the public may change.

The value of the Notes shown on your account statement may be based on RBCCM’s estimate of the value of the Notes if RBCCM or another of our affiliates were to make a market in the Notes (which

it is not obligated to do). That estimate will be based upon the price that RBCCM may pay for the Notes in light of then prevailing market conditions, our creditworthiness and transaction costs. For a period of up to approximately three

months after the issue date of the Notes, the value of the Notes that may be shown on your account statement is expected to be higher than RBCCM’s estimate of the value of the Notes at that time. This is because RBC's estimate of the value of

the Notes will not include the underwriting discount and our hedging costs and profits; however, the value of the Notes shown on your account statement during that period may initially be a higher amount, reflecting the addition of RBCCM’s

underwriting discount and our estimated costs and profits from hedging the Notes. This excess is expected to decrease over time until the end of this period. After this period, if RBCCM repurchases your Notes, it expects to do so at prices

that reflect RBCCM's estimate of their value.

We may use this pricing supplement in the initial sale of the Notes. In addition, RBCCM or another of our affiliates may use this pricing supplement in a market-making transaction in the Notes

after their initial sale. Unless we or our agent informs the purchaser otherwise in the confirmation of sale, this pricing supplement is being used in a market-making transaction.

VALIDITY OF THE NOTES

In the opinion of Norton Rose Fulbright Canada LLP, the issue and sale of the Notes has been duly authorized by all necessary corporate action of the Bank in conformity with the Indenture, and

when the Notes have been duly executed, authenticated and issued in accordance with the Indenture and delivered against payment therefor, the Notes will be validly issued and, to the extent validity of the Notes is a matter governed by the laws

of the Province of Ontario or Québec, or the laws of Canada applicable therein, will be valid obligations of the Bank, subject to equitable remedies which may only be granted at the discretion of a court of competent authority, subject to

applicable bankruptcy, to rights to indemnity and contribution under the Notes or the Indenture which may be limited by applicable law; to insolvency and other laws of general application affecting creditors’ rights, to limitations under

applicable limitations statutes, and to limitations as to the currency in which judgments in Canada may be rendered, as prescribed by the Currency Act (Canada). This opinion is given as of the date hereof and is limited to the laws of the

Provinces of Ontario and Québec

|

|

|

|

Collared SOFR Floating Rate Notes

Royal Bank of Canada

|

and the federal laws of Canada applicable thereto. In addition, this opinion is subject to customary assumptions about the Trustee’s authorization, execution and delivery of the

Indenture and the genuineness of signatures and certain factual matters, all as stated in the letter of such counsel dated September 14, 2021, which has been filed as Exhibit 5.3 to Royal Bank’s Form 6-K filed with the SEC dated September 14,

2021.

In the opinion of Ashurst LLP, when the Notes have been duly completed in accordance with the Indenture and issued and sold as contemplated by the prospectus supplement and the prospectus, the

Notes will be valid, binding and enforceable obligations of the Bank, entitled to the benefits of the Indenture, subject to applicable bankruptcy, insolvency, fraudulent transfer, reorganization, moratorium and similar laws of general

applicability relating to or affecting creditors' rights and subject to general principles of equity, public policy considerations and the discretion of the court before which any suit or proceeding may be brought. This opinion is given as of

the date hereof and is limited to the laws of the State of New York. This opinion is subject to customary assumptions about the Trustee’s authorization, execution and delivery of the Indenture and the genuineness of signatures and to such

counsel’s reliance on the Bank and other sources as to certain factual matters, all as stated in the legal opinion dated September 14, 2021, which has been filed as Exhibit 5.4 to the Bank’s Form 6-K dated September 14, 2021.

Exhibit 107.1

The pricing supplement to which this Exhibit is attached is a final prospectus for the related offering. The maximum aggregate offering price of the offering is

$2,152,000.

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Sobi Q1 2024 report: Strong sales reflecting the strength of the portfolio

- Form 8.5 (EPT/RI) - Accrol Group Holdings Plc

- Digitalist Group Plc’s Business Review, 1 January – 31 March 2024

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!