Form 424B2 BARCLAYS BANK PLC

Tweet

Tweet Share

Share|

Pricing Supplement dated September 24, 2021

(To the Prospectus dated August 1, 2019, the Prospectus Supplement dated August 1, 2019, the

Underlying Supplement dated August 1, 2019 and the Prospectus Supplement Addendum dated February 18, 2021) |

Filed Pursuant to Rule 424(b)(2)

Registration No. 333—232144

|

|

$560,000

Callable Contingent Coupon Notes due September 29, 2026

Linked to the Least Performing of the SPDR® S&P® Biotech ETF, the iShares® Global Clean Energy ETF and

the VanEck Semiconductor ETF Global Medium-Term Notes, Series A

|

Terms used in this pricing supplement, but not defined herein, shall have the meanings ascribed to them in the prospectus supplement.

|

Issuer:

|

Barclays Bank PLC

|

|

Denominations:

|

Minimum denomination of $1,000, and integral multiples of $1,000 in excess thereof

|

|

Initial Valuation Date:

|

September 24, 2021

|

|

Issue Date:

|

September 29, 2021

|

|

Final Valuation Date:*

|

September 24, 2026

|

|

Maturity Date:*

|

September 29, 2026

|

|

Reference Assets:

|

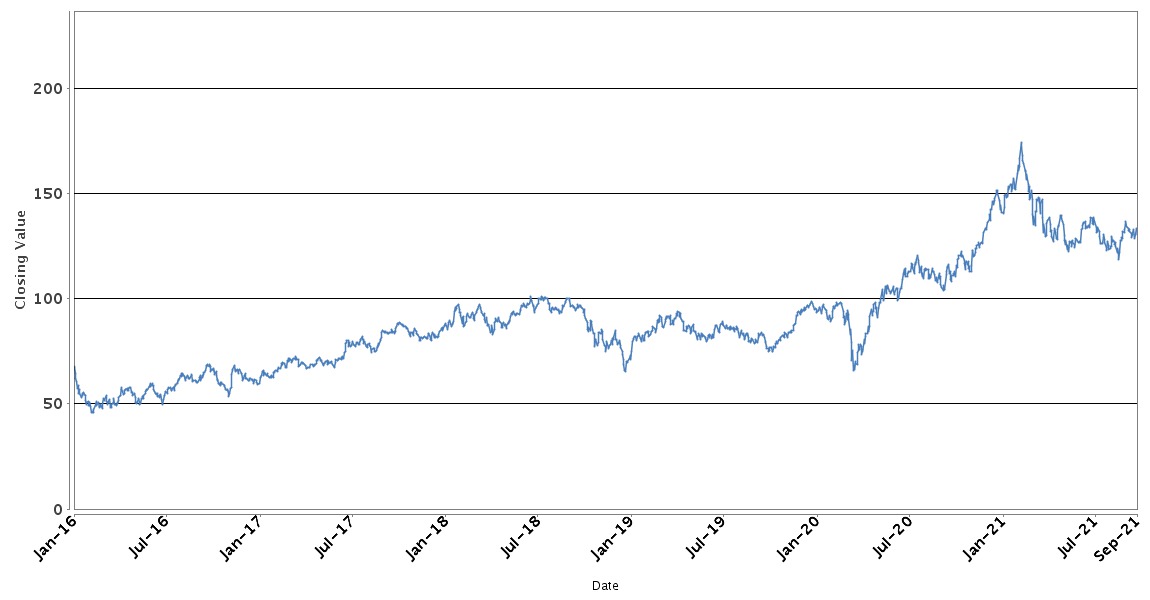

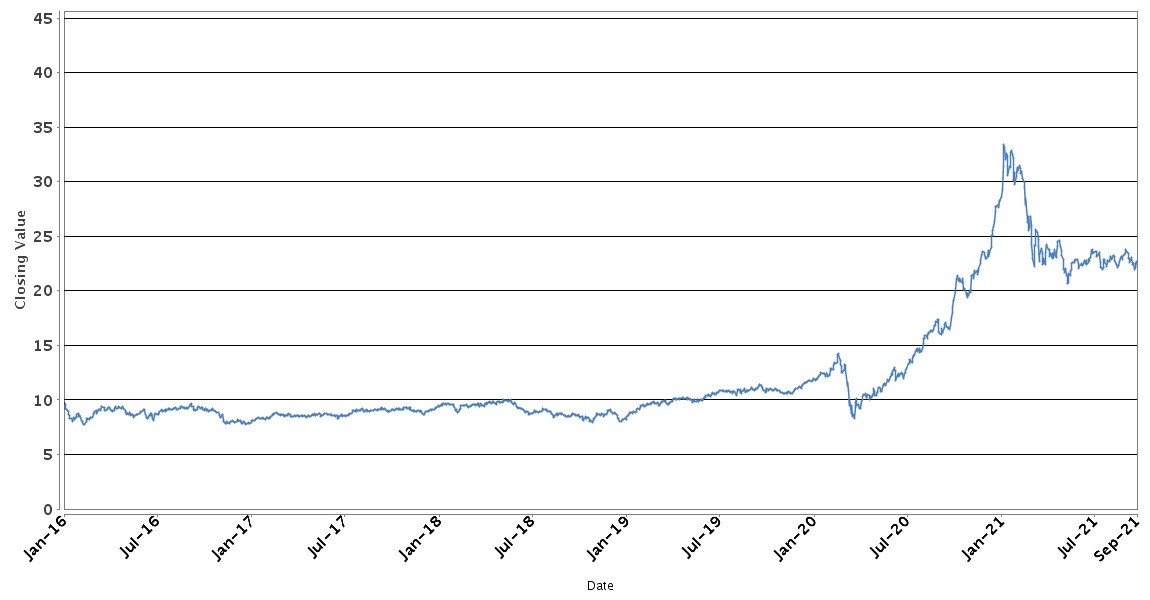

The SPDR® S&P® Biotech ETF (the “XBI Fund”), the iShares® Global Clean Energy ETF (the “ICLN Fund”) and the VanEck Semiconductor ETF (the “SMH Fund”), as set forth in the following table:

Reference Asset

Bloomberg Ticker

Initial Value

Coupon Barrier Value

Barrier Value

XBI Fund

XBI UP <Equity>

$130.37

$91.26

$91.26

ICLN Fund

ICLN US <Equity>

$22.25

$15.58

$15.58

SMH Fund

SMH US <Equity>

$272.39

$190.67

$190.67

The XBI Fund, the ICLN Fund and the SMH Fund are each referred to herein as a “Reference Asset” and, collectively, as the “Reference Assets.”

|

|

Payment at Maturity:

|

If the Notes are not redeemed prior to scheduled maturity, and if you hold the Notes to maturity, you will receive on the Maturity Date a cash payment per $1,000 principal amount Note that you hold (in each case, in addition to any Contingent Coupon that may be payable on such date) determined as follows:

■

If the Final Value of the Least Performing Reference Asset is greater than or equal to its Barrier Value, you will receive a payment of $1,000 per $1,000 principal amount Note.

■

If the Final Value of the Least Performing Reference Asset is less than its Barrier Value, you will receive an amount per $1,000 principal amount Note calculated as follows:

$1,000 + [$1,000 × Reference Asset Return of the Least Performing Reference Asset]

If the Notes are not redeemed prior to scheduled maturity, and if the Final Value of the Least Performing Reference Asset is less than its Barrier Value, your Notes will be fully exposed to the decline of the Least Performing Reference Asset from its Initial Value. You may lose up to 100.00% of the principal amount of your Notes at maturity.

Any payment on the Notes, including any repayment of principal, is not guaranteed by any third party and is subject to (a) the creditworthiness of Barclays Bank PLC and (b) the risk of exercise of any U.K. Bail-in Power (as described on page PS-4 of this pricing supplement) by the relevant U.K. resolution authority. If Barclays Bank PLC were to default on its payment obligations or become subject to the exercise of any U.K. Bail-in Power (or any other resolution measure) by the relevant U.K. resolution authority, you might not receive any amounts owed to you under the Notes. See “Consent to U.K. Bail-in Power” and “Selected Risk Considerations” in this pricing supplement and “Risk Factors” in the accompanying prospectus supplement for more information.

|

|

Consent to U.K. Bail-in Power:

|

Notwithstanding and to the exclusion of any other term of the Notes or any other agreements, arrangements or understandings between Barclays Bank PLC and any holder or beneficial owner of the Notes, by acquiring the Notes, each holder and beneficial owner of the Notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority. See “Consent to U.K. Bail-in Power” on page PS-4 of this pricing supplement.

|

[Terms of the Notes Continue on the Next Page]

|

|

Initial Issue Price(1)

|

Price to Public

|

Agent’s Commission(2)

|

Proceeds to Barclays Bank PLC

|

|

Per Note

|

$1,000

|

100.00%

|

1.75%

|

98.25%

|

|

Total

|

$560,000

|

$560,000

|

$9,800

|

$550,200

|

|

(1)

|

Our estimated value of the Notes on the Initial Valuation Date, based on our internal pricing models, is $908.80 per Note. The estimated value is less than the initial issue price of the Notes. See “Additional Information Regarding Our Estimated Value of the Notes” on page PS—5 of this pricing supplement.

|

|

(2)

|

Barclays Capital Inc. will receive commissions from the Issuer of $17.50 per $1,000 principal amount Note. Barclays Capital Inc. will use these commissions to pay selling concessions or fees (including custodial or clearing fees) to other dealers.

|

Investing in the Notes involves a number of risks. See “Risk Factors” beginning on page S-7 of the prospectus supplement and “Selected Risk Considerations” beginning on page PS-12 of this pricing supplement.

We may use this pricing supplement in the initial sale of Notes. In addition, Barclays Capital Inc. or another of our affiliates may use this pricing supplement in market resale transactions in any Notes after their initial sale. Unless we or our agent informs you otherwise in the confirmation of sale, this pricing supplement is being used in a market resale transaction.

The Notes will not be listed on any U.S. securities exchange or quotation system. Neither the U.S. Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these Notes or determined that this pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The Notes constitute our unsecured and unsubordinated obligations. The Notes are not deposit liabilities of Barclays Bank PLC and are not covered by the U.K. Financial Services Compensation Scheme or insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency or deposit insurance agency of the United States, the United Kingdom or any other jurisdiction.

|

Terms of the Notes, Continued

|

|

|

Early Redemption at the Option of the Issuer:

|

The Notes cannot be redeemed for the first six months after the Issue Date. We may redeem the Notes (in whole but not in part) at our sole discretion without your consent at the Redemption Price set forth below on any Call Valuation Date. No further amounts will be payable on the Notes after they have been redeemed.

|

|

Contingent Coupon:

|

$21.25 per $1,000 principal amount Note, which is 2.125% of the principal amount per Note (rounded to six decimal places, as applicable) (based on 8.50% per annum rate)

If the Closing Value of each Reference Asset on an Observation Date is greater than or equal to its respective Coupon Barrier Value, you will receive a Contingent Coupon on the related Contingent Coupon Payment Date. If the Closing Value of any Reference Asset on an Observation Date is less than its Coupon Barrier Value, you will not receive a Contingent Coupon on the related Contingent Coupon Payment Date.

|

|

Observation Dates:*

|

December 27, 2021, March 24, 2022, June 24, 2022, September 26, 2022, December 27, 2022, March 24, 2023, June 26, 2023, September 25, 2023, December 26, 2023, March 25, 2024, June 24, 2024, September 24, 2024, December 24, 2024, March 24, 2025, June 24, 2025, September 24, 2025, December 24, 2025, March 24, 2026, June 24, 2026 and the Final Valuation Date

|

|

Contingent Coupon Payment Dates:*

|

December 30, 2021, March 29, 2022, June 29, 2022, September 29, 2022, December 30, 2022, March 29, 2023, June 29, 2023, September 28, 2023, December 29, 2023, March 28, 2024, June 27, 2024, September 27, 2024, December 30, 2024, March 27, 2025, June 27, 2025, September 29, 2025, December 30, 2025, March 27, 2026, June 29, 2026 and the Maturity Date

|

|

Call Valuation Dates:*

|

Each Observation Date during the term of the Notes, beginning in March 2022 and ending in and including June 2026. If we exercise our early redemption option on a Call Valuation Date, we will provide written notice to the trustee on such Call Valuation Date.

|

|

Call Settlement Date:*

|

The Contingent Coupon Payment Date following the Call Valuation Date on which we exercise our early redemption option

|

|

Initial Value:

|

With respect to each Reference Asset, the Closing Value on the Initial Valuation Date, as set forth in the table above

|

|

Coupon Barrier Value:

|

With respect to each Reference Asset, 70.00% of its Initial Value (rounded to two decimal places), as set forth in the table above

|

|

Barrier Value:

|

With respect to each Reference Asset, 70.00% of its Initial Value (rounded to two decimal places), as set forth in the table above

|

|

Final Value:

|

With respect to each Reference Asset, the Closing Value on the Final Valuation Date

|

|

Redemption Price:

|

$1,000 per $1,000 principal amount Note that you hold, plus the Contingent Coupon that will otherwise be payable on the Call Settlement Date

|

|

Reference Asset Return:

|

With respect to each Reference Asset, the performance of such Reference Asset from its Initial Value to its Final Value, calculated as follows:

Final Value — Initial Value

Initial Value |

|

Least Performing Reference Asset:

|

The Reference Asset with the lowest Reference Asset Return, as calculated in the manner set forth above

|

|

Closing Value:

|

The term “Closing Value” means the closing price of one share of the applicable Reference Asset, as further described under “Reference Assets—Exchange-Traded Funds—Special Calculation Provisions” in the prospectus supplement, rounded to two decimal places (if applicable).

|

|

Calculation Agent:

|

Barclays Bank PLC

|

|

CUSIP / ISIN:

|

06748WJX2 / US06748WJX20

|

* Subject to postponement, as described under “Additional Terms of the Notes” in this pricing supplement

|

PS—2

ADDITIONAL DOCUMENTS RELATED TO THE OFFERING OF THE NOTES

You should read this pricing supplement together with the prospectus dated August 1, 2019, as supplemented by the documents listed below, relating to our Global Medium-Term Notes, Series A, of which these Notes are a part. This pricing supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the prospectus supplement and “Selected Risk Considerations” in this pricing supplement, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes.

You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

|

●

|

Prospectus dated August 1, 2019:

|

|

●

|

Prospectus Supplement dated August 1, 2019:

|

|

●

|

Underlying Supplement dated August 1, 2019:

|

|

●

|

Prospectus Supplement Addendum dated February 18, 2021:

|

Our SEC file number is 1—10257. As used in this pricing supplement, “we,” “us” or “our” refers to Barclays Bank PLC.

PS—3

Notwithstanding and to the exclusion of any other term of the Notes or any other agreements, arrangements or understandings between us and any holder or beneficial owner of the Notes, by acquiring the Notes, each holder and beneficial owner of the Notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority.

Under the U.K. Banking Act 2009, as amended, the relevant U.K. resolution authority may exercise a U.K. Bail-in Power in circumstances in which the relevant U.K. resolution authority is satisfied that the resolution conditions are met. These conditions include that a U.K. bank or investment firm is failing or is likely to fail to satisfy the Financial Services and Markets Act 2000 (the “FSMA”) threshold conditions for authorization to carry on certain regulated activities (within the meaning of section 55B FSMA) or, in the case of a U.K. banking group company that is a European Economic Area (“EEA”) or third country institution or investment firm, that the relevant EEA or third country relevant authority is satisfied that the resolution conditions are met in respect of that entity.

The U.K. Bail-in Power includes any write-down, conversion, transfer, modification and/or suspension power, which allows for (i) the reduction or cancellation of all, or a portion, of the principal amount of, interest on, or any other amounts payable on, the Notes; (ii) the conversion of all, or a portion, of the principal amount of, interest on, or any other amounts payable on, the Notes into shares or other securities or other obligations of Barclays Bank PLC or another person (and the issue to, or conferral on, the holder or beneficial owner of the Notes such shares, securities or obligations); (iii) the cancellation of the Notes and/or (iv) the amendment or alteration of the maturity of the Notes, or amendment of the amount of interest or any other amounts due on the Notes, or the dates on which interest or any other amounts become payable, including by suspending payment for a temporary period; which U.K. Bail-in Power may be exercised by means of a variation of the terms of the Notes solely to give effect to the exercise by the relevant U.K. resolution authority of such U.K. Bail-in Power. Each holder and beneficial owner of the Notes further acknowledges and agrees that the rights of the holders or beneficial owners of the Notes are subject to, and will be varied, if necessary, solely to give effect to, the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. For the avoidance of doubt, this consent and acknowledgment is not a waiver of any rights holders or beneficial owners of the Notes may have at law if and to the extent that any U.K. Bail-in Power is exercised by the relevant U.K. resolution authority in breach of laws applicable in England.

For more information, please see “Selected Risk Considerations—You May Lose Some or All of Your Investment If Any U.K. Bail-in Power Is Exercised by the Relevant U.K. Resolution Authority” in this pricing supplement as well as “U.K. Bail-in Power,” “Risk Factors—Risks Relating to the Securities Generally—Regulatory action in the event a bank or investment firm in the Group is failing or likely to fail could materially adversely affect the value of the securities” and “Risk Factors—Risks Relating to the Securities Generally—Under the terms of the securities, you have agreed to be bound by the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority” in the accompanying prospectus supplement.

The preceding discussion supersedes the discussion in the accompanying prospectus supplement to the extent it is inconsistent therewith.

PS—4

Our internal pricing models take into account a number of variables and are based on a number of subjective assumptions, which may or may not materialize, typically including volatility, interest rates, and our internal funding rates. Our internal funding rates (which are our internally published borrowing rates based on variables such as market benchmarks, our appetite for borrowing, and our existing obligations coming to maturity) may vary from the levels at which our benchmark debt securities trade in the secondary market. Our estimated value on the Initial Valuation Date is based on our internal funding rates. Our estimated value of the Notes may be lower if such valuation were based on the levels at which our benchmark debt securities trade in the secondary market.

Our estimated value of the Notes on the Initial Valuation Date is less than the initial issue price of the Notes. The difference between the initial issue price of the Notes and our estimated value of the Notes is a result of several factors, including any sales commissions to be paid to Barclays Capital Inc. or another affiliate of ours, any selling concessions, discounts, commissions or fees (including any structuring or other distribution related fees) to be allowed or paid to non-affiliated intermediaries, the estimated profit that we or any of our affiliates expect to earn in connection with structuring the Notes, the estimated cost which we may incur in hedging our obligations under the Notes, and estimated development and other costs which we may incur in connection with the Notes.

Our estimated value on the Initial Valuation Date is not a prediction of the price at which the Notes may trade in the secondary market, nor will it be the price at which Barclays Capital Inc. may buy or sell the Notes in the secondary market. Subject to normal market and funding conditions, Barclays Capital Inc. or another affiliate of ours intends to offer to purchase the Notes in the secondary market but it is not obligated to do so.

Assuming that all relevant factors remain constant after the Initial Valuation Date, the price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market, if any, and the value that we may initially use for customer account statements, if we provide any customer account statements at all, may exceed our estimated value on the Initial Valuation Date for a temporary period expected to be approximately three months after the Issue Date because, in our discretion, we may elect to effectively reimburse to investors a portion of the estimated cost of hedging our obligations under the Notes and other costs in connection with the Notes which we will no longer expect to incur over the term of the Notes. We made such discretionary election and determined this temporary reimbursement period on the basis of a number of factors, which may include the tenor of the Notes and/or any agreement we may have with the distributors of the Notes. The amount of our estimated costs which we effectively reimburse to investors in this way may not be allocated ratably throughout the reimbursement period, and we may discontinue such reimbursement at any time or revise the duration of the reimbursement period after the initial Issue Date of the Notes based on changes in market conditions and other factors that cannot be predicted.

We urge you to read the “Selected Risk Considerations” beginning on page PS-12 of this pricing supplement.

PS—5

SELECTED PURCHASE CONSIDERATIONS

The Notes are not suitable for all investors. The Notes may be a suitable investment for you if all of the following statements are true:

|

●

|

You do not seek an investment that produces fixed periodic interest or coupon payments or other non-contingent sources of current income, and you can tolerate receiving few or no Contingent Coupons over the term of the Notes in the event the Closing Value of any Reference Asset falls below its Coupon Barrier Value on one or more of the specified Observation Dates.

|

|

●

|

You understand and accept that you will not participate in any appreciation of any Reference Asset, which may be significant, and that your return potential on the Notes is limited to the Contingent Coupons, if any, paid on the Notes.

|

|

●

|

You can tolerate a loss of a significant portion or all of the principal amount of your Notes, and you are willing and able to make an investment that may have the full downside market risk of an investment in the Least Performing Reference Asset.

|

|

●

|

You do not anticipate that the Closing Value of any Reference Asset will fall below its Coupon Barrier Value on any Observation Date or below its Barrier Value on the Final Valuation Date.

|

|

●

|

You understand and accept that you will not be entitled to receive dividends or distributions that may be paid to holders of any Reference Asset or any securities to which any Reference Asset provides exposure, nor will you have any voting rights with respect to any Reference Asset or any securities to which any Reference Asset provides exposure.

|

|

●

|

You are willing and able to accept the individual market risk of each Reference Asset and understand that any decline in the value of one Reference Asset will not be offset or mitigated by a lesser decline or any potential increase in the value of any other Reference Asset.

|

|

●

|

You understand and accept the risks that (a) you will not receive a Contingent Coupon if the Closing Value of any Reference Asset is less than its Coupon Barrier Value on an Observation Date and (b) you will lose some or all of your principal at maturity if the Final Value of any Reference Asset is less than its Barrier Value.

|

|

●

|

You understand and accept the risk that, if the Notes are not redeemed prior to scheduled maturity, the payment at maturity, if any, will be based solely on the Reference Asset Return of the Least Performing Reference Asset.

|

|

●

|

You understand and are willing and able to accept the risks associated with an investment linked to the performance of the Reference Assets.

|

|

●

|

You are willing and able to accept the risk that the Notes may be redeemed prior to scheduled maturity and that you may not be able to reinvest your money in an alternative investment with comparable risk and yield.

|

|

●

|

You can tolerate fluctuations in the price of the Notes prior to scheduled maturity that may be similar to or exceed the downside fluctuations in the values of the Reference Assets.

|

|

●

|

You do not seek an investment for which there will be an active secondary market, and you are willing and able to hold the Notes to maturity if the Notes are not redeemed.

|

|

●

|

You are willing and able to assume our credit risk for all payments on the Notes.

|

|

●

|

You are willing and able to consent to the exercise of any U.K. Bail-in Power by any relevant U.K. resolution authority.

|

The Notes may not be a suitable investment for you if any of the following statements are true:

|

●

|

You seek an investment that produces fixed periodic interest or coupon payments or other non-contingent sources of current income, and/or you cannot tolerate receiving few or no Contingent Coupons over the term of the Notes in the event the Closing Value of any Reference Asset falls below its Coupon Barrier Value on one or more of the specified Observation Dates.

|

|

●

|

You seek an investment that participates in the full appreciation of any or all of the Reference Assets rather than an investment with a return that is limited to the Contingent Coupons, if any, paid on the Notes.

|

|

●

|

You seek an investment that provides for the full repayment of principal at maturity, and/or you are unwilling or unable to accept the risk that you may lose some or all of the principal amount of the Notes in the event that the Final Value of the Least Performing Reference Asset falls below its Barrier Value.

|

|

●

|

You anticipate that the Closing Value of at least one Reference Asset will decline during the term of the Notes such that the Closing Value of at least one Reference Asset will fall below its Coupon Barrier Value on one or more Observation Dates and/or the Final Value of at least one Reference Asset will fall below its Barrier Value.

|

|

●

|

You are unwilling or unable to accept the individual market risk of each Reference Asset and/or do not understand that any decline in the value of one Reference Asset will not be offset or mitigated by a lesser decline or any potential increase in the value of any other Reference Asset.

|

|

●

|

You do not understand and/or are unwilling or unable to accept the risks associated with an investment linked to the performance of the Reference Assets.

|

|

●

|

You are unwilling or unable to accept the risk that the negative performance of only one Reference Asset may cause you to not receive Contingent Coupons and/or suffer a loss of principal at maturity, regardless of the performance of any other Reference Asset.

|

|

●

|

You are unwilling or unable to accept the risk that the Notes may be redeemed prior to scheduled maturity.

|

|

●

|

You seek an investment that entitles you to dividends or distributions on, or voting rights related to any Reference Asset or any securities to which any Reference Asset provides exposure.

|

PS—6

|

●

|

You cannot tolerate fluctuations in the price of the Notes prior to scheduled maturity that may be similar to or exceed the downside fluctuations in the values of the Reference Assets.

|

|

●

|

You seek an investment for which there will be an active secondary market, and/or you are unwilling or unable to hold the Notes to maturity if the Notes are not redeemed.

|

|

●

|

You prefer the lower risk, and therefore accept the potentially lower returns, of fixed income investments with comparable maturities and credit ratings.

|

|

●

|

You are unwilling or unable to assume our credit risk for all payments on the Notes.

|

|

●

|

You are unwilling or unable to consent to the exercise of any U.K. Bail-in Power by any relevant U.K. resolution authority.

|

You must rely on your own evaluation of the merits of an investment in the Notes. You should reach a decision whether to invest in the Notes after carefully considering, with your advisors, the suitability of the Notes in light of your investment objectives and the specific information set out in this pricing supplement and the documents referenced under “Additional Documents Related to the Offering of the Notes” in this pricing supplement. Neither the Issuer nor Barclays Capital Inc. makes any recommendation as to the suitability of the Notes for investment.

PS—7

ADDITIONAL TERMS OF THE NOTES

The Observation Dates (including the Final Valuation Date), the Contingent Coupon Payment Dates, any Call Settlement Date and the Maturity Date are subject to postponement in certain circumstances, as described under “Reference Assets—Exchange-Traded Funds—Market Disruption Events for Securities with an Exchange-Traded Fund that Holds Equity Securities as a Reference Asset,” “Reference Assets—Least or Best Performing Reference Asset—Scheduled Trading Days and Market Disruption Events for Securities Linked to the Reference Asset with the Lowest or Highest Return in a Group of Two or More Equity Securities, Exchange-Traded Funds and/or Indices of Equity Securities” and “Terms of the Notes—Payment Dates” in the accompanying prospectus supplement.

In addition, the Reference Assets and the Notes are subject to adjustment by the Calculation Agent under certain circumstances, as described under “Reference Assets—Exchange-Traded Funds—Adjustments Relating to Securities with an Exchange-Traded Fund as a Reference Asset” in the accompanying prospectus supplement.

PS—8

HYPOTHETICAL EXAMPLES OF AMOUNTS PAYABLE ON A SINGLE CONTINGENT COUPON PAYMENT DATE

The following examples demonstrate the circumstances under which you may receive a Contingent Coupon on a hypothetical Contingent Coupon Payment Date. The numbers appearing in these tables are purely hypothetical and are provided for illustrative purposes only. These examples do not take into account any tax consequences from investing in the Notes and make the following key assumptions:

|

■

|

Hypothetical Initial Value of each Reference Asset: 100.00*

|

|

■

|

Hypothetical Coupon Barrier Value for each Reference Asset: 70.00 (70.00% of the hypothetical Initial Value set forth above)*

|

* The hypothetical Initial Value of 100.00 and the hypothetical Coupon Barrier Value of 70.00 for each Reference Asset have been chosen for illustrative purposes only. The actual Initial Value and Coupon Barrier Value for each Reference Asset are as set forth on the cover of this pricing supplement.

Example 1: The Closing Value of each Reference Asset is greater than its Coupon Barrier Value on the relevant Observation Date.

|

Reference Asset

|

Closing Value on Relevant Observation Date

|

|

XBI Fund

|

$100.00

|

|

ICLN Fund

|

$75.00

|

|

SMH Fund

|

$80.00

|

Because the Closing Value of each Reference Asset is greater than its respective Coupon Barrier Value, you will receive a Contingent Coupon of $21.25 (2.125% of the principal amount per Note) on the related Contingent Coupon Payment Date.

Example 2: The Closing Value of one Reference Asset is greater than its Coupon Barrier Value on the relevant Observation Date and the Closing Value of at least one Reference Asset is less than its Coupon Barrier Value on the relevant Observation Date.

|

Reference Asset

|

Closing Value on Relevant Observation Date

|

|

XBI Fund

|

$80.00

|

|

ICLN Fund

|

$69.00

|

|

SMH Fund

|

$50.00

|

Because the Closing Value of at least one Reference Asset is less than its Coupon Barrier Value, you will not receive a Contingent Coupon on the related Contingent Coupon Payment Date.

Example 3: The Closing Value of each Reference Asset is less than its Coupon Barrier Value on the relevant Observation Date.

|

Reference Asset

|

Closing Value on Relevant Observation Date

|

|

XBI Fund

|

$68.00

|

|

ICLN Fund

|

$50.00

|

|

SMH Fund

|

$45.00

|

Because the Closing Value of at least one Reference Asset is less than its Coupon Barrier Value, you will not receive a Contingent Coupon on the related Contingent Coupon Payment Date.

Examples 2 and 3 demonstrate that you may not receive a Contingent Coupon on a Contingent Coupon Payment Date. If the Closing Value of any Reference Asset is below its Coupon Barrier Value on each Observation Date, you will not receive any Contingent Coupons during the term of the Notes.

PS—9

HYPOTHETICAL EXAMPLES OF AMOUNTS PAYABLE AT MATURITY

The following table illustrates the hypothetical payment at maturity under various circumstances. The examples set forth below are purely hypothetical and are provided for illustrative purposes only. The numbers appearing in the following table and examples have been rounded for ease of analysis. The hypothetical examples below do not take into account any tax consequences from investing in the Notes and make the following key assumptions:

|

■

|

Hypothetical Initial Value of each Reference Asset: 100.00*

|

|

■

|

Hypothetical Coupon Barrier Value for each Reference Asset: 70.00 (70.00% of the hypothetical Initial Value set forth above)*

|

|

■

|

Hypothetical Barrier Value for each Reference Asset: 70.00 (70.00% of the hypothetical Initial Value set forth above)*

|

|

■

|

You hold the Notes to maturity, and the Notes are NOT redeemed prior to scheduled maturity.

|

* The hypothetical Initial Value of 100.00, the hypothetical Coupon Barrier Value of 70.00 and the hypothetical Barrier Value of 70.00 for each Reference Asset have been chosen for illustrative purposes only. The actual Initial Value, Coupon Barrier Value and Barrier Value for each Reference Asset are as set forth on the cover of this pricing supplement.

|

Final Value

|

|

Reference Asset Return

|

|

|

|||||

|

XBI Fund

(Reference Asset A)

|

ICLN Fund

(Reference Asset B)

|

SMH Fund

(Reference Asset C)

|

|

XBI Fund

(Reference Asset A)

|

ICLN Fund

(Reference Asset B)

|

SMH Fund

(Reference Asset C)

|

|

Reference Asset Return of the Least Performing Reference Asset

|

Payment at Maturity**

|

|

$140.00

|

$145.00

|

$150.00

|

|

40.00%

|

45.00%

|

50.00%

|

|

40.00%

|

$1,000.00

|

|

$135.00

|

$130.00

|

$140.00

|

|

35.00%

|

30.00%

|

40.00%

|

|

30.00%

|

$1,000.00

|

|

$120.00

|

$125.00

|

$122.00

|

|

20.00%

|

25.00%

|

22.00%

|

|

20.00%

|

$1,000.00

|

|

$112.00

|

$110.00

|

$115.00

|

|

12.00%

|

10.00%

|

15.00%

|

|

10.00%

|

$1,000.00

|

|

$100.00

|

$105.00

|

$120.00

|

|

0.00%

|

5.00%

|

20.00%

|

|

0.00%

|

$1,000.00

|

|

$140.00

|

$90.00

|

$105.00

|

|

40.00%

|

-10.00%

|

5.00%

|

|

-10.00%

|

$1,000.00

|

|

$80.00

|

$102.00

|

$105.00

|

|

-20.00%

|

2.00%

|

5.00%

|

|

-20.00%

|

$1,000.00

|

|

$80.00

|

$75.00

|

$70.00

|

|

-20.00%

|

-25.00%

|

-30.00%

|

|

-30.00%

|

$1,000.00

|

|

$60.00

|

$120.00

|

$100.00

|

|

-40.00%

|

20.00%

|

0.00%

|

|

-40.00%

|

$600.00

|

|

$135.00

|

$50.00

|

$110.00

|

|

35.00%

|

-50.00%

|

10.00%

|

|

-50.00%

|

$500.00

|

|

$150.00

|

$40.00

|

$100.00

|

|

50.00%

|

-60.00%

|

0.00%

|

|

-60.00%

|

$400.00

|

|

$40.00

|

$30.00

|

$90.00

|

|

-60.00%

|

-70.00%

|

-10.00%

|

|

-70.00%

|

$300.00

|

|

$20.00

|

$55.00

|

$50.00

|

|

-80.00%

|

-45.00%

|

-50.00%

|

|

-80.00%

|

$200.00

|

|

$50.00

|

$10.00

|

$55.00

|

|

-50.00%

|

-90.00%

|

-45.00%

|

|

-90.00%

|

$100.00

|

|

$0.00

|

$105.00

|

$80.00

|

|

-100.00%

|

5.00%

|

-20.00%

|

|

-100.00%

|

$0.00

|

** per $1,000 principal amount Note, excluding the final Contingent Coupon that may be payable on the Maturity Date.

The following examples illustrate how the payments at maturity set forth in the table above are calculated:

Example 1: The Final Value of Reference Asset A is $135.00, the Final Value of Reference Asset B is $130.00 and the Final Value of Reference Asset C is $140.00.

Because Reference Asset B has the lowest Reference Asset Return, Reference Asset B is the Least Performing Reference Asset. Because the Final Value of the Least Performing Reference Asset is greater than or equal to its Barrier Value, you will receive a payment at maturity of $1,000 per $1,000 principal amount Note that you hold (plus the Contingent Coupon that will otherwise be payable on the Maturity Date).

PS—10

Example 2: The Final Value of Reference Asset A is $140.00, the Final Value of Reference Asset B is $90.00 and the Final Value of Reference Asset C is $105.00.

Because Reference Asset B has the lowest Reference Asset Return, Reference Asset B is the Least Performing Reference Asset. Because the Final Value of the Least Performing Reference Asset is greater than or equal to its Barrier Value, you will receive a payment at maturity of $1,000 per $1,000 principal amount Note that you hold (plus the Contingent Coupon that will otherwise be payable on the Maturity Date).

Example 3: The Final Value of Reference Asset A is $60.00, the Final Value of Reference Asset B is $120.00 and the Final Value of Reference Asset C is $100.00.

Because Reference Asset A has the lowest Reference Asset Return, Reference Asset A is the Least Performing Reference Asset. Because the Final Value of the Least Performing Reference Asset is less than its Barrier Value, you will receive a payment at maturity of $600.00 per $1,000 principal amount Note that you hold, calculated as follows:

$1,000 + [$1,000 × Reference Asset Return of the Least Performing Reference Asset]

$1,000 + [$1,000 × -40.00%] = $600.00

In addition, because the Final Value of at least one Reference Asset is less than its Coupon Barrier Value, you will not receive a Contingent Coupon on the Maturity Date.

Example 3 demonstrates that if the Notes are not redeemed prior to scheduled maturity, and if the Final Value of the Least Performing Reference Asset is less than its Barrier Value, your investment in the Notes will be fully exposed to the decline of the Least Performing Reference Asset from its Initial Value. You will not benefit in any way from the Reference Asset Return of any other Reference Asset being higher than the Reference Asset Return of the Least Performing Reference Asset.

If the Notes are not redeemed prior to scheduled maturity, you may lose up to 100.00% of the principal amount of your Notes. Any payment on the Notes, including the repayment of principal, is subject to the credit risk of Barclays Bank PLC.

PS—11

An investment in the Notes involves significant risks. Investing in the Notes is not equivalent to investing directly in the Reference Assets or their components, if any. Some of the risks that apply to an investment in the Notes are summarized below, but we urge you to read the more detailed explanation of risks relating to the Notes generally in the “Risk Factors” section of the prospectus supplement. You should not purchase the Notes unless you understand and can bear the risks of investing in the Notes.

Risks Relating to the Notes Generally

|

●

|

Your Investment in the Notes May Result in a Significant Loss—The Notes differ from ordinary debt securities in that the Issuer will not necessarily repay the full principal amount of the Notes at maturity. If the Notes are not redeemed prior to scheduled maturity, and if the Final Value of the Least Performing Reference Asset is less than its Barrier Value, your Notes will be fully exposed to the decline of the Least Performing Reference Asset from its Initial Value. You may lose up to 100.00% of the principal amount of your Notes.

|

|

●

|

Potential Return is Limited to the Contingent Coupons, If Any, and You Will Not Participate in Any Appreciation of Any Reference Asset—The potential positive return on the Notes is limited to the Contingent Coupons, if any, that may be payable during the term of the Notes. You will not participate in any appreciation in the value of any Reference Asset, which may be significant, even though you will be exposed to the depreciation in the value of the Least Performing Reference Asset if the Notes are not redeemed and the Final Value of the Least Performing Reference Asset is less than its Barrier Value.

|

|

●

|

You May Not Receive Any Contingent Coupon Payments on the Notes—The Issuer will not necessarily make periodic coupon payments on the Notes. You will receive a Contingent Coupon on a Contingent Coupon Payment Date only if the Closing Value of each Reference Asset on the related Observation Date is greater than or equal to its respective Coupon Barrier Value. If the Closing Value of any Reference Asset on an Observation Date is less than its Coupon Barrier Value, you will not receive a Contingent Coupon on the related Contingent Coupon Payment Date. If the Closing Value of at least one Reference Asset is less than its respective Coupon Barrier Value on each Observation Date, you will not receive any Contingent Coupons during the term of the Notes.

|

|

●

|

Because the Notes Are Linked to the Least Performing Reference Asset, You Are Exposed to Greater Risks of No Contingent Coupons and Sustaining a Significant Loss of Principal at Maturity Than If the Notes Were Linked to a Single Reference Asset—The risk that you will not receive any Contingent Coupons and lose a significant portion or all of your principal amount in the Notes at maturity is greater if you invest in the Notes as opposed to substantially similar securities that are linked to the performance of a single Reference Asset. With multiple Reference Assets, it is more likely that the Closing Value of at least one Reference Asset will be less than its Coupon Barrier Value on the specified Observation Dates or less than its Barrier Value on the Final Valuation Date, and therefore, it is more likely that you will not receive any Contingent Coupons and that you will suffer a significant loss of principal at maturity. Further, the performance of the Reference Assets may not be correlated or may be negatively correlated. The lower the correlation between multiple Reference Assets, the greater the potential for one of those Reference Assets to close below its Coupon Barrier Value or Barrier Value on an Observation Date or the Final Valuation Date, respectively.

|

It is impossible to predict what the correlation among the Reference Assets will be over the term of the Notes. The Reference Assets represent different equity markets. These different equity markets may not perform similarly over the term of the Notes.

Although the correlation of the Reference Assets’ performance may change over the term of the Notes, the Contingent Coupon rate is determined, in part, based on the correlation of the Reference Assets’ performance calculated using our internal models at the time when the terms of the Notes are finalized. A higher Contingent Coupon is generally associated with lower correlation of the Reference Assets, which reflects a greater potential for missed Contingent Coupons and for a loss of principal at maturity.

|

●

|

You Are Exposed to the Market Risk of Each Reference Asset—Your return on the Notes is not linked to a basket consisting of the Reference Assets. Rather, it will be contingent upon the independent performance of each Reference Asset. Unlike an instrument with a return linked to a basket of underlying assets in which risk is mitigated and diversified among all the components of the basket, you will be exposed to the risks related to each Reference Asset. Poor performance by any Reference Asset over the term of the Notes may negatively affect your return and will not be offset or mitigated by any increases or lesser declines in the value of any other Reference Asset. To receive a Contingent Coupon, the Closing Value of each Reference Asset must be greater than or equal to its Coupon Barrier Value on the applicable Observation Date. In addition, if the Notes have not been redeemed prior to scheduled maturity, and if the Final Value of any Reference Asset is less than its Barrier Value, you will be exposed to the full decline in the Least Performing Reference Asset from its Initial Value. Accordingly, your investment is subject to the market risk of each Reference Asset.

|

|

●

|

The Notes Are Subject to Volatility Risk—Volatility is a measure of the degree of variation in the price of an asset (or level of an index) over a period of time. The amount of any coupon payments that may be payable under the Notes is based on a number of factors, including the expected volatility of the Reference Assets. The amount of such coupon payments will be paid at a per annum rate that is higher than the fixed rate that we would pay on a conventional debt security of the same tenor and is higher than it otherwise would have been had the expected volatility of the Reference Assets been lower. As volatility of a Reference Asset increases, there will typically be a greater likelihood that (a) the Closing Value of that Reference Asset on one or more Observation Dates will be less than its Coupon Barrier Value and (b) the Final Value of that Reference Asset will be less than its Barrier Value.

|

PS—12

Accordingly, you should understand that a higher coupon payment amount reflects, among other things, an indication of a greater likelihood that you will (a) not receive coupon payments with respect to one or more Observation Dates and/or (b) incur a loss of principal at maturity than would have been the case had the amount of such coupon payments been lower. In addition, actual volatility over the term of the Notes may be significantly higher than the expected volatility at the time the terms of the Notes were determined. If actual volatility is higher than expected, you will face an even greater risk that you will not receive coupon payments and/or that you will lose some or all of your principal at maturity for the reasons described above.

|

●

|

Early Redemption and Reinvestment Risk—While the original term of the Notes is as indicated on the cover of this pricing supplement, the Notes may be redeemed prior to maturity, as described above, and the holding period over which you may receive any coupon payments that may be payable under the Notes could be as short as approximately six months.

|

The Redemption Price that you would receive on a Call Settlement Date, together with any coupon payments that you may have received prior to the Call Settlement Date, may be less than the aggregate amount of payments that you would have received had the Notes not been redeemed. There is no guarantee that you would be able to reinvest the proceeds from an investment in the Notes in a comparable investment with a similar level of risk in the event the Notes are redeemed prior to the Maturity Date. No additional payments will be due after the relevant Call Settlement Date. The fact that the Notes may be redeemed prior to maturity may also adversely impact your ability to sell your Notes and the price at which they may be sold.

It is more likely that we will redeem the Notes at our sole discretion prior to maturity to the extent that the expected interest payable on the Notes is greater than the interest that would be payable on other instruments issued by us of comparable maturity, terms and credit rating trading in the market. We are less likely to redeem the Notes prior to maturity when the expected interest payable on the Notes is less than the interest that would be payable on other comparable instruments issued by us, which includes when the value of any Reference Asset is less than its Coupon Barrier Value. Therefore, the Notes are more likely to remain outstanding when the expected interest payable on the Notes is less than what would be payable on other comparable instruments and when your risk of not receiving a Contingent Coupon is relatively higher.

|

●

|

If the Notes Are Not Redeemed Prior to Scheduled Maturity, the Payment at Maturity, If Any, is Based Solely on the Closing Value of the Least Performing Reference Asset on the Final Valuation Date—If the Notes are not redeemed prior to scheduled maturity, the Final Value of any Reference Asset will be based solely on its Closing Value on the Final Valuation Date, and your payment at maturity, if any, will be determined based solely on the performance of the Least Performing Reference Asset from the Initial Valuation Date to the Final Valuation Date. Accordingly, if the value of the Least Performing Reference Asset drops on the Final Valuation Date, the payment at maturity on the Notes, if any, may be significantly less than it would have been had it been linked to the value of the Reference Asset at any time prior to such drop.

|

If the Final Value of the Least Performing Reference Asset is less than its Barrier Value, you will lose some or all of the principal amount of your Notes. Your losses will not be offset in any way by virtue of the Reference Asset Return of any other Reference Asset being higher than the Reference Asset Return of the Least Performing Reference Asset.

|

●

|

Contingent Repayment of Any Principal Amount Applies Only at Maturity or upon Any Redemption—You should be willing to hold your Notes to maturity or any redemption. Although the Notes provide for the contingent repayment of the principal amount of your Notes at maturity, provided that the Final Value of the Least Performing Reference Asset is greater than or equal to its Barrier Value, or upon any redemption, if you sell your Notes prior to such time in the secondary market, if any, you may have to sell your Notes at a price that is less than the principal amount even if at that time the value of each Reference Asset has increased from its Initial Value. See “Many Economic and Market Factors Will Impact the Value of the Notes” below.

|

|

●

|

Owning the Notes is Not the Same as Owning Any Reference Asset or Any Securities to which Any Reference Asset Provides Exposure—The return on the Notes may not reflect the return you would realize if you actually owned any Reference Asset or any securities to which any Reference Asset provides exposure. As a holder of the Notes, you will not have voting rights or rights to receive dividends or other distributions or any other rights that holders of any Reference Asset or any securities to which any Reference Asset provides exposure may have.

|

|

●

|

Tax Treatment—Significant aspects of the tax treatment of the Notes are uncertain. You should consult your tax advisor about your tax situation. See “Tax Considerations” below.

|

Risks Relating to the Issuer

|

●

|

Credit of Issuer—The Notes are unsecured and unsubordinated debt obligations of the Issuer, Barclays Bank PLC, and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Notes, including any repayment of principal, is subject to the ability of Barclays Bank PLC to satisfy its obligations as they come due and is not guaranteed by any third party. As a result, the actual and perceived creditworthiness of Barclays Bank PLC may affect the market value of the Notes, and in the event Barclays Bank PLC were to default on its obligations, you may not receive any amounts owed to you under the terms of the Notes.

|

|

●

|

You May Lose Some or All of Your Investment If Any U.K. Bail-in Power Is Exercised by the Relevant U.K. Resolution Authority—Notwithstanding and to the exclusion of any other term of the Notes or any other agreements, arrangements or understandings between Barclays Bank PLC and any holder or beneficial owner of the Notes, by acquiring the Notes, each holder and beneficial owner of the Notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority as set forth under “Consent to U.K. Bail-in Power” in this pricing supplement. Accordingly, any U.K. Bail-in Power may be exercised in such a manner as to result in you and other holders and

|

PS—13

beneficial owners of the Notes losing all or a part of the value of your investment in the Notes or receiving a different security from the Notes, which may be worth significantly less than the Notes and which may have significantly fewer protections than those typically afforded to debt securities. Moreover, the relevant U.K. resolution authority may exercise the U.K. Bail-in Power without providing any advance notice to, or requiring the consent of, the holders and the beneficial owners of the Notes. The exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority with respect to the Notes will not be a default or an Event of Default (as each term is defined in the senior debt securities indenture) and the trustee will not be liable for any action that the trustee takes, or abstains from taking, in either case, in accordance with the exercise of the U.K. Bail-in Power by the relevant U.K. resolution authority with respect to the Notes. See “Consent to U.K. Bail-in Power” in this pricing supplement as well as “U.K. Bail-in Power,” “Risk Factors—Risks Relating to the Securities Generally—Regulatory action in the event a bank or investment firm in the Group is failing or likely to fail could materially adversely affect the value of the securities” and “Risk Factors—Risks Relating to the Securities Generally—Under the terms of the securities, you have agreed to be bound by the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority” in the accompanying prospectus supplement.

Risks Relating to the Reference Assets

|

●

|

Historical Performance of the Reference Assets Should Not Be Taken as Any Indication of the Future Performance of the Reference Assets Over the Term of the Notes—The value of each Reference Asset has fluctuated in the past and may, in the future, experience significant fluctuations. The historical performance of a Reference Asset is not an indication of the future performance of that Reference Asset over the term of the Notes. The historical correlation among the Reference Assets is not an indication of the future correlation among them over the term of the Notes. Therefore, the performance of the Reference Assets individually or in comparison to each other over the term of the Notes may bear no relation or resemblance to the historical performance of any Reference Asset.

|

|

●

|

Certain Features of Exchange-Traded Funds Will Impact the Value of the Notes—The performance of each Reference Asset will not fully replicate the performance of its respective Underlying Index (as defined below), and each Reference Asset may hold securities not included in its respective Underlying Index. The value of each Reference Asset is subject to:

|

|

■

|

Management Risk. This is the risk that the investment strategy for each Reference Asset, the implementation of which is subject to a number of constraints, may not produce the intended results. However, each Reference Asset is not actively managed and the investment advisor of each Reference Asset will generally not attempt to take defensive positions in declining markets.

|

|

■

|

Derivatives Risk. Each Reference Asset may invest in derivatives, including forward contracts, futures contracts, options on futures contracts, options and swaps. A derivative is a financial contract, the value of which depends on, or is derived from, the value of an underlying asset such as a security or an index. Compared to conventional securities, derivatives can be more sensitive to changes in interest rates or to sudden fluctuations in market prices, and thus each Reference Asset’s losses, and, as a consequence, the losses on your Notes, may be greater than if each Reference Asset invested only in conventional securities.

|

|

■

|

Transaction costs and fees. Unlike its respective Underlying Index, each Reference Asset will reflect transaction costs and fees that will reduce its performance relative to its respective Underlying Index.

|

Generally, the longer the time remaining to maturity, the more the market price of the Notes will be affected by the factors described above. In addition, each Reference Asset may diverge significantly from the performance of its respective Underlying Index due to differences in trading hours between such Reference Asset and the securities composing its Underlying Index or other circumstances. During periods of market volatility, the component securities held by each Reference Asset may be unavailable in the secondary market, market participants may be unable to calculate accurately the intraday net asset value per share of each Reference Asset and the liquidity of each Reference Asset may be adversely affected. This kind of market volatility may also disrupt the ability of market participants to create and redeem shares in each Reference Asset. Further, market volatility may adversely affect, sometimes materially, the prices at which market participants are willing to buy and sell shares of each Reference Asset. As a result, under these circumstances, the market value of each Reference Asset may vary substantially from the net asset value per share of each Reference Asset. Because the Notes are linked to the performance of each Reference Asset and not its Underlying Index, the return on your Notes may be less than that of an alternative investment linked directly to its Underlying Index.

|

●

|

Adjustments to any Reference Asset or its Underlying Index Could Adversely Affect the Value of the Notes or Result in the Notes Being Accelerated—The investment adviser of any Reference Asset may add, delete or substitute the component securities held by that Reference Asset or make changes to its investment strategy, and the sponsor of the Underlying Index that any Reference Asset is designed to track may add, delete, substitute or adjust the securities composing its Underlying Index or make other methodological changes to its Underlying Index that could affect its performance. In addition, if the shares of any Reference Asset are delisted or if any Reference Asset is liquidated or otherwise terminated, the Calculation Agent may select a successor fund that the Calculation Agent determines to be comparable to that Reference Asset or, if no successor fund is available, the Maturity Date of the Notes will be accelerated for a payment determined by the Calculation Agent. Any of these actions could adversely affect the value of any Reference Asset and, consequently, the value of the Notes. Any amount payable upon acceleration could be significantly less than the amount(s) that would be due on the securities if they were not accelerated. See “Reference Assets—Exchange-Traded Funds—Adjustments Relating to Securities with an Exchange-Traded Fund as a Reference Asset—Discontinuance of an Exchange-Traded Fund” in the accompanying prospectus supplement.

|

PS—14

|

●

|

Anti-Dilution Protection Is Limited, and the Calculation Agent Has Discretion to Make Anti-Dilution Adjustments—The Calculation Agent may in its sole discretion make adjustments affecting the amounts payable on the Notes upon the occurrence of certain events that the Calculation Agent determines have a diluting or concentrative effect on the theoretical value of the shares of any Reference Asset. However, the Calculation Agent might not make such adjustments in response to all events that could affect the shares of any Reference Asset. The occurrence of any such event and any adjustment made by the Calculation Agent (or a determination by the Calculation Agent not to make any adjustment) may adversely affect any amounts payable on the Notes. See “Reference Assets—Exchange-Traded Funds—Adjustments Relating to Securities with an Exchange-Traded Fund as a Reference Asset—Anti-dilution Adjustments” in the accompanying prospectus supplement.

|

|

●

|

The Notes May Become Subject to Executive Orders That Could Adversely Affect Your Investment In The Notes—Pursuant to recent executive orders, U.S. persons are prohibited from engaging in transactions in, or possession of, publicly traded securities of certain companies that are determined to be linked to the People’s Republic of China military, intelligence and security apparatus, or securities that are derivative of, or are designed to provide investment exposure to, those securities. Although we do not believe that the Notes are subject to those executive orders at this time, it is possible that those executive orders could be expanded or modified to include the Notes.

|

The sponsor of the underlying index for the ICLN Fund has recently removed the equity securities of a small number of companies from the index from which the constituents of that underlying index are drawn in response to these executive orders. If the issuer of any of the equity securities held by the ICLN Fund is in the future designated as such a prohibited company, the value of that company may be adversely affected, perhaps significantly, which would adversely affect the performance of the ICLN Fund. In addition, under these circumstances, the sponsor of the underlying index for the ICLN Fund and the ICLN Fund is expected to remove the equity securities of that company from the underlying index and the ICLN Fund, respectively. Any changes to the composition of the ICLN Fund in response to these executive orders could adversely affect the performance of the ICLN Fund. Under those circumstances, the value of the Notes could be adversely affected, and transactions in, or holdings of, the Notes may become prohibited under U.S. law. You may suffer significant losses if you are forced to divest the Notes when the value of the Notes declines.

|

●

|

The Notes Are Subject to Risks Associated with Non-U.S. Securities Markets—Certain component securities of the ICLN Fund are issued by non-U.S. companies in non-U.S. securities markets. Investments in securities linked to the value of such non-U.S. equity securities, such as the Notes, involve risks associated with the securities markets in the home countries of the issuers of those non-U.S. equity securities, including risks of volatility in those markets, governmental intervention in those markets and cross shareholdings in companies in certain countries. Also, there is generally less publicly available information about companies in some of these jurisdictions than there is about U.S. companies that are subject to the reporting requirements of the SEC, and generally non-U.S. companies are subject to accounting, auditing and financial reporting standards and requirements and securities trading rules different from those applicable to U.S. reporting companies. The prices of securities in non-U.S. markets may be affected by political, economic, financial and social factors in those countries, or global regions, including changes in government, economic and fiscal policies and currency exchange laws.

|

|

●

|

The Notes Are Subject to Risks Associated with Emerging Markets—Certain component securities of the ICLN Fund have been issued by non-U.S. companies located in emerging market countries. Emerging markets pose further risks in addition to the risks associated with investing in foreign equity markets generally, as described in the previous risk factor. Countries with emerging markets may have relatively unstable governments, may present the risks of nationalization of businesses, restrictions on foreign ownership and prohibitions on the repatriation of assets, and may have less protection of property rights than more developed countries. The economies of countries with emerging markets may be based on only a few industries, may be highly vulnerable to changes in local or global trade conditions, and may suffer from extreme and volatile debt burdens or inflation rates. Local securities markets may trade a small number of securities and may be unable to respond effectively to increases in trading volume, potentially making prompt liquidation of holdings difficult or impossible at times. Moreover, the economies in such countries may differ unfavorably from the economy in the United States in such respects as growth of gross national product, rate of inflation, capital reinvestment, resources, self-sufficiency and balance of payment positions.

|

|

●

|

An Investment in the Notes Involves Industry Concentration Risk—As described below under “Information Regarding the Reference Assets”, the investment objective of each Reference Asset is to provide investment results that, before fees and expenses, correspond generally to the price and yield performance of publicly traded equity securities of companies in one particular sector or group of industries. The performance of companies in the relevant sector will be influenced by many complex and unpredictable factors, including industry competition, interest rates, geopolitical events, government regulation and supply and demand for the products and services offered by such companies. Any adverse development in the sector tracked by the Reference Assets may have a material adverse effect on the securities held in the portfolio of the Reference Assets and, as a result, may have a material adverse effect on the value of the Reference Assets and the value of the Notes.

|

|

●

|

The Notes Are Subject to Currency Exchange Risk—Because the value of the ICLN Fund is related to the U.S. dollar value of the component securities held by the ICLN Fund, the values of the ICLN Fund will be exposed to the currency exchange rate risk with respect to each of the currencies in which the component securities held by the ICLN Fund trade. An investor’s net exposure will depend on the extent to which each of those non-U.S. currencies strengthens or weakens against the U.S. dollar and the relative weight of the component securities denominated in those non-U.S. currencies. If, taking into account the relevant weighting, the U.S. dollar strengthens against those non-U.S. currencies, the value of the ICLN Fund will be adversely affected and any payments on the Notes may be reduced.

|

PS—15

Exchange rate movements for a particular currency are volatile and are the result of numerous factors, including the supply of, and the demand for, those currencies, as well as government policy, intervention or actions, but are also influenced significantly from time to time by political or economic developments, and by macroeconomic factors and speculative actions related to the relevant region. Of particular importance to potential currency exchange risk are:

|

■

|

existing and expected rates of inflation;

|

|

■

|

existing and expected interest rate levels;

|

|

■

|

the balance of payments between the countries represented in the ICLN Fund and the United States; and

|

|

■

|

the extent of governmental surpluses or deficits in the countries represented in the ICLN Fund and the United States.

|

All of these factors are in turn sensitive to the monetary, fiscal and trade policies pursued by the governments of the countries represented in the ICLN Fund, the United States and other countries important to international trade and finance.

Risks Relating to Conflicts of Interest

|

●

|

We and Our Affiliates May Engage in Various Activities or Make Determinations That Could Materially Affect the Notes in Various Ways and Create Conflicts of Interest—We and our affiliates play a variety of roles in connection with the issuance of the Notes, as described below. In performing these roles, our and our affiliates’ economic interests are potentially adverse to your interests as an investor in the Notes.

|

In connection with our normal business activities and in connection with hedging our obligations under the Notes, we and our affiliates make markets in and trade various financial instruments or products for our accounts and for the account of our clients and otherwise provide investment banking and other financial services with respect to these financial instruments and products. These financial instruments and products may include securities, derivative instruments or assets that may relate to the Reference Assets or their components, if any. In any such market making, trading and hedging activity, and other financial services, we or our affiliates may take positions or take actions that are inconsistent with, or adverse to, the investment objectives of the holders of the Notes. We and our affiliates have no obligation to take the needs of any buyer, seller or holder of the Notes into account in conducting these activities. Such market making, trading and hedging activity, investment banking and other financial services may negatively impact the value of the Notes.

In addition, the role played by Barclays Capital Inc., as the agent for the Notes, could present significant conflicts of interest with the role of Barclays Bank PLC, as issuer of the Notes. For example, Barclays Capital Inc. or its representatives may derive compensation or financial benefit from the distribution of the Notes and such compensation or financial benefit may serve as incentive to sell the Notes instead of other investments. Furthermore, we and our affiliates establish the offering price of the Notes for initial sale to the public, and the offering price is not based upon any independent verification or valuation.

In addition to the activities described above, we will also act as the Calculation Agent for the Notes. As Calculation Agent, we will determine any values of the Reference Assets and make any other determinations necessary to calculate any payments on the Notes. In making these determinations, the Calculation Agent may be required to make discretionary judgements relating to the Reference Assets, including determining whether a market disruption event has occurred or whether certain adjustments to the Reference Assets or other terms of the Notes are necessary, as further described in the accompanying prospectus supplement. In making these discretionary judgments, our economic interests are potentially adverse to your interests as an investor in the Notes, and any of these determinations may adversely affect any payments on the Notes.

Risks Relating to the Estimated Value of the Notes and the Secondary Market

|

●

|

The Estimated Value of Your Notes is Lower Than the Initial Issue Price of Your Notes—The estimated value of your Notes on the Initial Valuation Date is lower than the initial issue price of your Notes. The difference between the initial issue price of your Notes and the estimated value of the Notes is a result of certain factors, such as any sales commissions to be paid to Barclays Capital Inc. or another affiliate of ours, any selling concessions, discounts, commissions or fees (including any structuring or other distribution related fees) to be allowed or paid to non-affiliated intermediaries, the estimated profit that we or any of our affiliates expect to earn in connection with structuring the Notes, the estimated cost which we may incur in hedging our obligations under the Notes, and estimated development and other costs which we may incur in connection with the Notes.

|

|

●

|

The Estimated Value of Your Notes Might be Lower if Such Estimated Value Were Based on the Levels at Which Our Debt Securities Trade in the Secondary Market—The estimated value of your Notes on the Initial Valuation Date is based on a number of variables, including our internal funding rates. Our internal funding rates may vary from the levels at which our benchmark debt securities trade in the secondary market. As a result of this difference, the estimated value referenced above might be lower if such estimated value were based on the levels at which our benchmark debt securities trade in the secondary market.

|

|

●

|

The Estimated Value of the Notes is Based on Our Internal Pricing Models, Which May Prove to be Inaccurate and May be Different from the Pricing Models of Other Financial Institutions—The estimated value of your Notes on the Initial Valuation Date is based on our internal pricing models, which take into account a number of variables and are based on a number of subjective assumptions, which may or may not materialize. These variables and assumptions are not evaluated or verified on an independent basis. Further, our pricing models may be different from other financial institutions’ pricing models and the methodologies used by us to estimate the value of the Notes may not be consistent with those of other financial institutions which may be purchasers or sellers of Notes in the secondary market. As a result, the secondary market price of

|

PS—16

your Notes may be materially different from the estimated value of the Notes determined by reference to our internal pricing models.

|

●

|

The Estimated Value of Your Notes Is Not a Prediction of the Prices at Which You May Sell Your Notes in the Secondary Market, if any, and Such Secondary Market Prices, If Any, Will Likely be Lower Than the Initial Issue Price of Your Notes and May be Lower Than the Estimated Value of Your Notes—The estimated value of the Notes will not be a prediction of the prices at which Barclays Capital Inc., other affiliates of ours or third parties may be willing to purchase the Notes from you in secondary market transactions (if they are willing to purchase, which they are not obligated to do). The price at which you may be able to sell your Notes in the secondary market at any time will be influenced by many factors that cannot be predicted, such as market conditions, and any bid and ask spread for similar sized trades, and may be substantially less than our estimated value of the Notes. Further, as secondary market prices of your Notes take into account the levels at which our debt securities trade in the secondary market, and do not take into account our various costs related to the Notes such as fees, commissions, discounts, and the costs of hedging our obligations under the Notes, secondary market prices of your Notes will likely be lower than the initial issue price of your Notes. As a result, the price at which Barclays Capital Inc., other affiliates of ours or third parties may be willing to purchase the Notes from you in secondary market transactions, if any, will likely be lower than the price you paid for your Notes, and any sale prior to the Maturity Date could result in a substantial loss to you.

|

|

●

|

The Temporary Price at Which We May Initially Buy The Notes in the Secondary Market And the Value We May Initially Use for Customer Account Statements, If We Provide Any Customer Account Statements At All, May Not Be Indicative of Future Prices of Your Notes—Assuming that all relevant factors remain constant after the Initial Valuation Date, the price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market (if Barclays Capital Inc. makes a market in the Notes, which it is not obligated to do) and the value that we may initially use for customer account statements, if we provide any customer account statements at all, may exceed our estimated value of the Notes on the Initial Valuation Date, as well as the secondary market value of the Notes, for a temporary period after the initial Issue Date of the Notes. The price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market and the value that we may initially use for customer account statements may not be indicative of future prices of your Notes.

|

|

●

|

Lack of Liquidity—The Notes will not be listed on any securities exchange. Barclays Capital Inc. and other affiliates of Barclays Bank PLC intend to make a secondary market for the Notes but are not required to do so, and may discontinue any such secondary market making at any time, without notice. Barclays Capital Inc. may at any time hold unsold inventory, which may inhibit the development of a secondary market for the Notes. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which Barclays Capital Inc. and other affiliates of Barclays Bank PLC are willing to buy the Notes. The Notes are not designed to be short-term trading instruments. Accordingly, you should be willing and able to hold your Notes to maturity.

|

|

●

|