Form 10-Q CNL Healthcare Propertie For: Jun 30

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM |

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the quarterly period ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to ______

Commission file number:

(Exact name of registrant as specified in its charter) |

|

||

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

||

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code ( |

||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

Accelerated filer |

|

|

Smaller reporting company |

||

Emerging growth company |

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

None |

N/A |

N/A |

The number of shares of common stock of the registrant outstanding as of August 11, 2022 was

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

INDEX

|

|

Page |

PART I. FINANCIAL INFORMATION |

|

|

|

|

|

Item 1. |

Condensed Consolidated Financial Information (unaudited): |

|

|

2 |

|

|

3 |

|

|

Condensed Consolidated Statements of Comprehensive Income (Loss) |

4 |

|

Condensed Consolidated Statements of Stockholders’ Equity and Redeemable Noncontrolling Interest |

5 |

|

7 |

|

|

8 |

|

Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 |

Item 3. |

35 |

|

Item 4. |

36 |

|

|

|

|

PART II. OTHER INFORMATION |

|

|

|

|

|

Item 1. |

36 |

|

Item 1A. |

36 |

|

Item 2. |

36 |

|

Item 3. |

36 |

|

Item 4. |

36 |

|

Item 5. |

36 |

|

Item 6. |

36 |

|

|

|

|

|

37 |

|

|

38 |

|

Exhibits |

|

|

Item 1. Condensed Consolidated Financial Information

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(in thousands, except per share data)

|

|

June 30, |

|

|

December 31, |

|

||

ASSETS |

|

2022 |

|

|

2021 |

|

||

Real estate investment properties, net (including VIEs $ |

|

$ |

|

|

$ |

|

||

Assets held for sale |

|

― |

|

|

|

|

||

Cash (including VIEs $ |

|

|

|

|

|

|

||

Restricted cash (including VIEs $ |

|

|

|

|

|

|

||

Other assets (including VIEs $ |

|

|

|

|

|

|

||

Deferred rent, lease incentives and intangibles, net |

|

|

|

|

|

|

||

Total assets |

|

$ |

|

|

$ |

|

||

LIABILITIES AND EQUITY |

|

|

|

|

|

|

||

Liabilities: |

|

|

|

|

|

|

||

Mortgages and other notes payable, net (including VIEs $ |

|

$ |

|

|

|

|

||

Credit facilities |

|

|

|

|

|

|

||

Accounts payable and accrued liabilities (including VIEs $ |

|

|

|

|

|

|

||

Other liabilities (including VIEs $ |

|

|

|

|

|

|

||

Due to related parties |

|

|

|

|

|

|

||

Total liabilities |

|

|

|

|

|

|

||

|

|

|

|

|

|

|||

Stockholders' equity: |

|

|

|

|

|

|

||

Preferred stock, $ |

|

― |

|

|

― |

|

||

Excess shares, $ |

|

― |

|

|

― |

|

||

Common stock, $ |

|

|

|

|

|

|

||

Capital in excess of par value |

|

|

|

|

|

|

||

Accumulated income |

|

|

|

|

|

|

||

Accumulated distributions |

|

|

( |

) |

|

|

( |

) |

Accumulated other comprehensive income |

|

|

|

|

|

|

||

Total stockholders' equity |

|

|

|

|

|

|

||

Noncontrolling interest |

|

|

|

|

|

|

||

Total equity |

|

|

|

|

|

|

||

Total liabilities and equity |

|

$ |

|

|

$ |

|

||

|

|

|

|

|

|

|

||

The abbreviation VIEs above means variable interest entities. |

|

|

|

|

|

|

||

See accompanying notes to condensed consolidated financial statements.

2

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(in thousands, except per share data)

|

|

Quarter Ended |

|

|

Six Months Ended |

|

||||||||||

|

|

June 30, |

|

|

June 30, |

|

||||||||||

|

|

2022 |

|

|

2021 |

|

|

2022 |

|

|

2021 |

|

||||

Revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Total revenues |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Property operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

||||

General and administrative expenses |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Asset management fees |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Property management fees |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Depreciation and amortization |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Total operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Operating income |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Other income (expense): |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Interest and other income |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Interest expense and loan cost amortization |

|

|

( |

) |

|

|

( |

) |

|

|

( |

) |

|

|

( |

) |

Gain on change of control of a joint venture |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Equity in earnings of unconsolidated entity |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Total other (expense) income |

|

|

( |

) |

|

|

( |

) |

|

|

|

|

|

( |

) |

|

Income (loss) before income taxes |

|

|

|

|

|

( |

) |

|

|

|

|

|

( |

) |

||

Income tax (expense) benefit |

|

|

( |

) |

|

|

|

|

|

( |

) |

|

|

|

||

Income (loss) from continuing operations |

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|||

Loss from discontinued operations |

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|||

Net income (loss) |

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|||

Less: Amounts attributable to noncontrolling interests |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Net income (loss) from continuing operations |

|

|

|

|

|

( |

) |

|

|

|

|

|

( |

) |

||

Net income (loss) attributable to common stockholders |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Net income (loss) per share of common stock (basic and diluted) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Continuing operations |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|||

Discontinued operations |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|||

Weighted average number of shares of common stock outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

||||

See accompanying notes to condensed consolidated financial statements.

3

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

(in thousands)

|

|

Quarter Ended |

|

|

Six Months Ended |

|

||||||||||

|

|

June 30, |

|

|

June 30, |

|

||||||||||

|

|

2022 |

|

|

2021 |

|

|

2022 |

|

|

2021 |

|

||||

Net income (loss) |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|||

Other comprehensive income: |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Unrealized gain on derivative financial instruments, net |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Unrealized gain on derivative financial instruments of equity method investments |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Total other comprehensive income |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Comprehensive income (loss) |

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|||

Less: Comprehensive income (loss) attributable to noncontrolling interest |

|

|

|

|

|

( |

) |

|

|

|

|

|

( |

) |

||

Comprehensive income (loss) attributable to common stockholders |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|||

See accompanying notes to condensed consolidated financial statements.

4

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY AND REDEEMABLE NONCONTROLLING INTEREST

QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

(in thousands, except per share data)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

Common Stock |

|

|

Capital in |

|

|

|

|

|

|

|

|

Other |

|

|

Total |

|

|

Non- |

|

|

|

|

||||||||||||

|

|

Number |

|

|

Par |

|

|

Excess of |

|

|

Accumulated |

|

|

Accumulated |

|

|

Comprehensive |

|

|

Stockholders' |

|

|

controlling |

|

|

Total |

|

|||||||||

|

|

of Shares |

|

|

Value |

|

|

Par Value |

|

|

Income |

|

|

Distributions |

|

|

Income (Loss) |

|

|

Equity |

|

|

Interest |

|

|

Equity |

|

|||||||||

Balance at March 31, 2022 |

|

|

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

||||||||

Net income |

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

― |

|

|

― |

|

|

|

|

|

|

|

|

|

|

|||||||||

Other comprehensive income |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

|

|

|

― |

|

|

|

|

|||||||||

Cash distributions declared |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

( |

) |

|

― |

|

|

|

( |

) |

|

― |

|

|

|

( |

) |

||||||

Balance at June 30, 2022 |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Balance at December 31, 2021 |

|

|

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

||||||||

Net income |

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

― |

|

|

― |

|

|

|

|

|

|

|

|

|

|

|||||||||

Other comprehensive income |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

|

|

|

― |

|

|

|

|

|||||||||

Cash distributions declared |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

( |

) |

|

― |

|

|

|

( |

) |

|

― |

|

|

|

( |

) |

||||||

Balance at June 30, 2022 |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

||||||||

See accompanying notes to condensed consolidated financial statements.

5

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY AND REDEEMABLE NONCONTROLLING INTEREST

QUARTER AND SIX MONTHS ENDED JUNE 30, 2021 (UNAUDITED)

(in thousands, except per share data)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

Redeemable |

|

|

Common Stock |

|

|

Capital in |

|

|

|

|

|

|

|

|

Other |

|

|

Total |

|

|

Non- |

|

|

|

|

|||||||||||||

|

|

Noncontrolling |

|

|

Number |

|

|

Par |

|

|

Excess of |

|

|

Accumulated |

|

|

Accumulated |

|

|

Comprehensive |

|

|

Stockholders' |

|

|

controlling |

|

|

Total |

|

||||||||||

|

|

Interest |

|

|

of Shares |

|

|

Value |

|

|

Par Value |

|

|

Income |

|

|

Distributions |

|

|

Income (Loss) |

|

|

Equity |

|

|

Interest |

|

|

Equity |

|

||||||||||

Balance at March 31, 2021 |

|

$ |

|

|

|

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

( |

) |

|

$ |

|

|

$ |

|

|

$ |

|

||||||||

Net income (loss) |

|

|

|

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

― |

|

|

― |

|

|

|

|

|

|

( |

) |

|

|

|

|||||||||

Other comprehensive income |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

|

|

|

― |

|

|

|

|

||||||||||

Distributions to noncontrolling |

|

|

( |

) |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

( |

) |

||||||||

Cash distributions declared |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

( |

) |

|

― |

|

|

|

( |

) |

|

― |

|

|

|

( |

) |

|||||||

Reclassification of redeemable noncontrolling interest |

|

|

( |

) |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

― |

|

|||||||||

Balance at June 30, 2021 |

|

$ |

— |

|

|

|

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

( |

) |

|

$ |

|

|

$ |

|

|

$ |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

Balance at December 31, 2020 |

|

$ |

|

|

|

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

( |

) |

|

$ |

|

|

$ |

|

|

|

|

||||||||

Net income (loss) |

|

|

|

|

― |

|

|

― |

|

|

― |

|

|

|

( |

) |

|

― |

|

|

― |

|

|

|

( |

) |

|

|

( |

) |

|

|

( |

) |

||||||

Other comprehensive income |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

|

|

|

― |

|

|

|

|

||||||||||

Distributions to noncontrolling |

|

|

( |

) |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

( |

) |

|

|

( |

) |

|||||||

Cash distributions declared |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

( |

) |

|

― |

|

|

|

( |

) |

|

― |

|

|

|

( |

) |

|||||||

Reclassification of redeemable noncontrolling interest |

|

|

( |

) |

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

― |

|

|

|

|

|

― |

|

|||||||||

Balance at June 30, 2021 |

|

$ |

— |

|

|

|

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

( |

) |

|

$ |

|

|

$ |

|

|

$ |

|

|||||||

See accompanying notes to condensed consolidated financial statements.

6

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(in thousands)

|

|

Six Months Ended June 30, |

|

|||||

|

|

2022 |

|

|

2021 |

|

||

Operating activities: |

|

|

|

|

|

|

||

Net cash flows provided by operating activities – continuing operations |

|

$ |

|

|

$ |

|

||

Net cash flows used in operating activities – discontinued operations |

|

|

|

|

|

( |

) |

|

Net cash flows provided by operating activities |

|

|

|

|

|

|

||

Investing activities: |

|

|

|

|

|

|

||

Acquisition of joint venture interest, net of cash acquired |

|

|

( |

) |

|

|

|

|

Net proceeds from sale of property |

|

|

|

|

|

|

||

Capital expenditures |

|

|

( |

) |

|

|

( |

) |

Other investing activities |

|

|

( |

) |

|

|

|

|

Net cash used in investing activities – continuing operations |

|

|

( |

) |

|

|

( |

) |

Net cash provided by investing activities – discontinued operations |

|

|

|

|

|

|

||

Net cash (used in) provided by investing activities |

|

|

( |

) |

|

|

|

|

Financing activities: |

|

|

|

|

|

|

||

Distributions to stockholders |

|

|

( |

) |

|

|

( |

) |

Draws on line of credit |

|

|

|

|

|

|

||

Principal payments on mortgages and other notes payable |

|

|

( |

) |

|

|

( |

) |

Other financing activities |

|

|

( |

) |

|

|

( |

) |

Net cash flows used in financing activities |

|

|

( |

) |

|

|

( |

) |

Net increase in cash and restricted cash |

|

|

|

|

|

|

||

Cash and restricted cash at beginning of period, including assets held for sale |

|

|

|

|

|

|

||

Cash and restricted cash at end of period, including assets held for sale |

|

$ |

|

|

$ |

|

||

|

|

|

|

|

|

|

||

Supplemental disclosure of non-cash investing and financing activities: |

|

|

|

|

|

|

||

Real estate investment properties |

|

$ |

|

|

$ |

|

||

Intangibles |

|

|

|

|

|

|

||

Mortgages and notes payable |

|

|

( |

) |

|

|

|

|

Net assets recognized upon the change in control of the Windsor Manor Joint Venture (Note 4) |

|

$ |

|

|

$ |

|

||

See accompanying notes to condensed consolidated financial statements.

7

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

1. Organization

CNL Healthcare Properties, Inc. (the “Company”) is a Maryland corporation that elected to be taxed as a real estate investment trust (“REIT”) for United States (“U.S.”) federal income tax purposes. The Company has been and intends to continue to be organized and operate in a manner that allows it to remain qualified as a REIT for U.S. federal income tax purposes. The Company conducts substantially all of its operations either directly or indirectly through: (1) an operating partnership, CHP Partners, LP (“Operating Partnership”), in which the Company is the sole limited partner and its wholly-owned subsidiary, CHP GP, LLC, is the sole general partner; (2) a wholly-owned taxable REIT subsidiary (“TRS”), CHP TRS Holding, Inc.; (3) property owner and lender subsidiaries, which are single purpose entities; and (4) investments in joint ventures.

The Company is externally managed and advised by CNL Healthcare Corp. (“Advisor”), which is an affiliate of CNL Financial Group, LLC (“Sponsor”). The Sponsor is an affiliate of CNL Financial Group, Inc. (“CNL”). The Advisor is responsible for managing the Company’s day-to-day operations, serving as a consultant in connection with policy decisions to be made by the board of directors, and for identifying, recommending and executing on possible strategic alternatives and dispositions on the Company’s behalf pursuant to an advisory agreement among the Company, the Operating Partnership and the Advisor. Substantially all of the Company’s operating, administrative and certain property management services are provided by affiliates of the Advisor. In addition, certain property management services are provided by third-party property managers.

In 2017, the Company began evaluating possible strategic alternatives to provide liquidity to the Company’s stockholders. As part of executing under possible strategic alternatives, the Company’s board of directors committed to a plan to sell

As of June 30, 2022, the Company’s seniors housing portfolio was geographically diversified with properties in

2. Summary of Significant Accounting Policies

Basis of Presentation and Consolidation — The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q and do not include all of the information and note disclosures required by generally accepted accounting principles in the U.S. (“GAAP”). The unaudited condensed consolidated financial statements reflect all normal recurring adjustments, which, in the opinion of management, are necessary for the fair statement of the Company’s results for the interim period presented. Operating results for the six months ended June 30, 2022 may not be indicative of the results that may be expected for the year ending December 31, 2022. Amounts as of December 31, 2021 included in the unaudited condensed consolidated financial statements have been derived from audited consolidated financial statements as of that date but do not include all disclosures required by GAAP. These unaudited condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021.

8

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

2. Summary of Significant Accounting Policies (Continued)

The accompanying unaudited condensed consolidated financial statements include the Company’s accounts, the accounts of wholly owned subsidiaries or subsidiaries for which the Company has a controlling interest, the accounts of

Government Grant Income — On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) was signed into law which provided, among other things, for the establishment of a Provider Relief Fund under the direction of the Department of Health and Human Services (“HHS”). Provider relief funds received under the CARES Act are deemed governmental grants provided that the recipient attests to and complies with certain terms and conditions. Grant income is recognized upon receipt of provider relief funds and when all the conditions of the grant have been met. During the six months ended June 30, 2022 and 2021, the Company recorded approximately $

Risks and Uncertainties — In March 2020, the World Health Organization declared the outbreak of the novel coronavirus (“COVID-19”) as a pandemic around the globe. Since the onset of the pandemic, the Company has operated and continues to operate its communities through the disruptions and uncertainties of the pandemic, including disruptions from new variants of the virus. Although more normalized activities have resumed, at this time the Company cannot predict the full extent of the impacts of the COVID-19 pandemic on the Company and its operations, and the COVID-19 pandemic may continue to have a material and adverse impact on our financial condition, results of operations and cash flows.

Use of Estimates — The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the date of the consolidated financial statements, the reported amounts of revenues and expenses during the reporting periods and the disclosure of contingent liabilities. For example, significant assumptions are made in the analysis of real estate impairments, the valuation of contingent assets and liabilities, and the valuation of restricted common stock (“Restricted Stock”) shares issued to the Advisor. Accordingly, actual results could differ from those estimates.

Assets Held For Sale, net and Discontinued Operations — The Company determines to classify a property as held for sale once management has the authority to approve and commits to a plan to sell the property, the property is available for immediate sale, there is an active program to locate a buyer, the sale of the property is probable and the transfer of the property is expected to occur within one year. Upon the determination to classify a property as held for sale, the Company ceases recording further depreciation and amortization relating to the associated assets and those assets are measured at the lower of its carrying amount or fair value less disposition costs and are presented separately in the consolidated balance sheets for all periods presented. In addition, the Company classifies assets held for sale as discontinued operations if the disposal represents a strategic shift that has (or will have) a major effect on the Company’s operations and financial results. For any disposal(s) qualifying as discontinued operations, the Company allocates interest expense and loan cost amortization that directly relates to either: (1) expense on mortgages and other notes payable collateralized by properties classified as discontinued operations; or (2) expense on the Company’s Credit Facilities, which is allocated based on the value of the properties that are classified as discontinued operations since these properties are included in the Credit Facilities’ unencumbered pool of assets and the related indebtedness is required to be repaid upon sale of the properties.

Reclassifications — Certain amounts in the prior years’ consolidated balance sheet have been reclassified to conform to the current year’s presentation.

9

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

2. Summary of Significant Accounting Policies (Continued)

Recently Adopted Accounting Pronouncements — In Q1 2020, the FASB issued ASU 2020-04, “Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting” (“ASU 2020-04”). ASU 2020-04 contains practical expedients for reference rate reform related activities that impact debt, leases, derivatives and other contracts. The guidance in ASU 2020-04 is optional and may be elected over time as reference rate reform activities occur. During the year ended December 31, 2020, the Company elected to apply the hedge accounting expedients related to probability and the assessments of effectiveness for future LIBOR-indexed cash flows to assume that the index upon which future hedged transactions will be based matches the index on the corresponding derivatives. Application of these expedients preserves the presentation of derivatives consistent with past presentation. As of June 30, 2022, the Company does not anticipate that this guidance will have a material impact on its consolidated financial statements; however, the Company will continue to assess the potential impact on its variable rate debt contracts and future hedging relationships, as applicable.

3. Revenue

The following table presents disaggregated revenue related to the Company’s resident fees and services during the quarter and six months ended June 30, 2022 and 2021:

|

|

Quarter Ended June 30, |

|

|||||||||||||||||||||

|

|

Number of |

|

|

Revenues |

|

|

Percentage |

|

|||||||||||||||

Resident fees and services: |

|

2022 |

|

|

2021 |

|

|

2022 |

|

|

2021 |

|

|

2022 |

|

|

2021 |

|

||||||

Independent living |

|

|

|

|

|

|

|

$ |

|

|

$ |

|

|

|

% |

|

|

% |

||||||

Assisted living |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

|

|

% |

||||||

Memory care |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

|

|

% |

||||||

Other revenues |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

|

|

% |

||||||

|

|

|

|

|

|

|

|

$ |

|

|

$ |

|

|

|

% |

|

|

% |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

Six Months Ended June 30, |

|

|||||||||||||||||||||

|

|

Number of |

|

|

Revenues |

|

|

Percentage |

|

|||||||||||||||

Resident fees and services: |

|

2022 |

|

|

2021 |

|

|

2022 |

|

|

2021 |

|

|

2022 |

|

|

2021 |

|

||||||

Independent living |

|

|

|

|

|

|

|

$ |

|

|

$ |

|

|

|

% |

|

|

% |

||||||

Assisted living |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

|

|

% |

||||||

Memory care |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

|

|

% |

||||||

Other revenues |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

|

|

% |

||||||

|

|

|

|

|

|

|

|

$ |

|

|

$ |

|

|

|

% |

|

|

% |

||||||

10

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

4. Acquisition

As of December 31, 2021, the Company held an interest in five properties through a

As the Company previously held an equity method investment in the Windsor Manor Joint Venture, the acquisition resulted in a gain on change of control of a joint venture of approximately $

The following table summarizes the fair market value of the assets and liabilities recorded as part of the acquisition, adjusted on a relative fair value basis for the difference between the consideration transferred and the fair market value of the net assets acquired, of the Windsor Manor Joint Venture as of the acquisition date (in thousands):

Equity method investment in unconsolidated joint venture |

|

$ |

|

|

Consideration paid for additional 25% interest in joint venture |

|

|

|

|

Total equity method investment and consideration paid |

|

$ |

|

|

|

|

|

|

|

Cash |

|

$ |

|

|

Restricted Cash |

|

|

|

|

Prepaid and other assets |

|

|

|

|

Real estate assets |

|

|

|

|

Intangibles(1) |

|

|

|

|

Total assets acquired |

|

|

|

|

Accounts payable and accrued expenses |

|

|

( |

) |

Other liabilities |

|

|

( |

) |

Mortgages and notes payable |

|

|

( |

) |

Total liabilities assumed |

|

|

( |

) |

Net assets acquired |

|

$ |

|

|

_____________

FOOTNOTE:

5. Real Estate Assets, net

The gross carrying amount and accumulated depreciation of the Company’s real estate assets as of June 30, 2022 and December 31, 2021 are as follows, excluding the one asset held for sale (in thousands):

|

|

June 30, |

|

|

December 31, |

|

||

|

|

2022 |

|

|

2021 |

|

||

Land and land improvements |

|

$ |

|

|

$ |

|

||

Building and building improvements |

|

|

|

|

|

|

||

Furniture, fixtures and equipment |

|

|

|

|

|

|

||

Less: accumulated depreciation |

|

|

( |

) |

|

|

( |

) |

Real estate investment properties, net |

|

$ |

|

|

$ |

|

||

Depreciation expense on the Company’s real estate investment properties, net was approximately $

11

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

6. Asset Held For Sale and Discontinued Operations

In March 2022, the Company received an unsolicited offer and entered into a purchase and sale agreement for the Hurst Specialty Hospital with an unrelated third party and classified this property as held for sale as of December 31, 2021 in the accompanying condensed consolidated balance sheet. Assets held for sale consisted of real estate held for sale, net as of December 31, 2021. The Company sold this property in April 2022, received net sales proceeds of $

The sale of the Hurst Specialty Hospital did not cause a strategic shift in the Company's operations, and was not considered significant; therefore, this property did not qualify as discontinued operations. The Company did not have any properties for which it had classified the revenues and expenses as discontinued operations during the quarter and six months ended June 30, 2022.

During the six months ended June 30, 2021, the Company classified the revenues and expenses related to the Company’s acute care property sold in January 2021 as discontinued operations in the accompanying condensed consolidated statements of operations. This property was identified for sale as part of the plan to sell the MOB/Healthcare portfolio and the Company determined that the sale of these properties represented a strategic shift in the Company’s operations. The Company recorded a loss from discontinued operations of approximately $

7. Variable Interest Entities

As of June 30, 2022 and December 31, 2021, the Company had

12

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

8. Indebtedness

The following table provides details of the Company's indebtedness as of June 30, 2022 and December 31, 2021, (in thousands):

|

As of June 30, |

|

|

As of December 31, |

|

||

|

2022 |

|

|

2021 |

|

||

Mortgages payable and other notes payable: |

|

|

|

|

|

||

Fixed rate debt(1) |

$ |

|

|

$ |

|

||

Variable rate debt(1)(2)(6) |

|

|

|

|

|

||

Premium(3) |

|

|

|

|

|

||

Loan costs, net |

|

( |

) |

|

|

( |

) |

Total mortgages and other notes payable, net |

|

|

|

|

|

||

Credit facilities: |

|

|

|

|

|

||

Revolving Credit Facility(4)(5)(6) |

|

|

|

|

|

||

Term Loan Facility(4)(6) |

|

|

|

|

|

||

2021 Term Loan Facility(4)(6) |

|

|

|

|

|

||

Loan costs, net related to Term Loan Facilities |

|

( |

) |

|

|

( |

) |

Total credit facilities, net |

|

|

|

|

|

||

Total indebtedness, net |

$ |

|

|

$ |

|

||

_____________

FOOTNOTES:

In June 2022, the Company refinanced secured indebtedness of approximately $

The Company had liquidity of approximately $

13

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

8. Indebtedness (continued)

The following is a schedule of future principal payments for the Company’s total indebtedness for the remainder of 2022, each of the next four years and thereafter, in the aggregate, as of June 30, 2022 (in thousands):

2022 |

$ |

|

|

2023 |

|

|

|

2024 |

|

|

|

2025 |

|

— |

|

2026 |

|

— |

|

Thereafter |

|

— |

|

|

$ |

|

The following table provides the details of the fair market value and carrying value of the Company’s indebtedness as of June 30, 2022 and December 31, 2021 (in millions):

|

|

June 30, |

|

|

December 31, |

|

||||||||||

|

|

2022 |

|

|

2021 |

|

||||||||||

|

|

Fair |

|

|

Carrying |

|

|

Fair |

|

|

Carrying |

|

||||

Mortgages and other notes payable, net |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

||||

Credit facilities, net |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

||||

These fair market values are based on current rates and spreads the Company would expect to obtain for similar borrowings. Since this methodology includes inputs that are less observable by the public and are not necessarily reflected in active markets, the measurement of the estimated fair values related to the Company’s mortgage notes payable is categorized as Level 3 on the three-level valuation hierarchy.

Generally, the loan agreements for the Company’s mortgage loans contain customary financial covenants and ratios; including (but not limited to) the following: debt service coverage ratio, minimum occupancy levels, limitations on incurrence of additional indebtedness, etc. The loan agreements also contain customary events of default and remedies for the lenders. As of June 30, 2022, the Company was in compliance with all financial covenants related to its mortgage loans.

14

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

9. Related Party Arrangements

In May 2022, the Company extended its advisory agreement with the Advisor through June 2023.

The Company paid approximately $

The expenses and fees incurred by and reimbursable to the Company’s related parties, including amounts included in income from discontinued operations, for the quarter and six months ended June 30, 2022 and 2021, and related amounts unpaid as of June 30, 2022 and December 31, 2021 are as follows (in thousands):

|

|

Quarter Ended |

|

|

Six Months Ended |

|

|

Unpaid amounts as of (1) |

|

|||||||||||||||

|

|

June 30, |

|

|

June 30, |

|

|

June 30, |

|

|

December 31, |

|

||||||||||||

|

|

2022 |

|

|

2021 |

|

|

2022 |

|

|

2021 |

|

|

2022 |

|

|

2021 |

|

||||||

Reimbursable expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Operating expenses (2) |

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Investment services fee (3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Disposition fee (4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Asset management fees (5) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

|

$ |

|

||||||

_______________

FOOTNOTES:

10. Equity

In March 2022, the Board approved a reduction in the quarterly distribution rate to $

During the quarter and six months ended June 30, 2022, the Company declared cash distributions of approximately $

15

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTER AND SIX MONTHS ENDED JUNE 30, 2022 (UNAUDITED)

11. Income Taxes

The accompanying condensed consolidated financial statements include an interim tax provision for the quarter and six months ended June 30, 2022 and 2021. For the quarter and six months ended June 30, 2022, the Company recorded an income tax expense of approximately $

12. Commitments and Contingencies

From time to time, the Company may be a party to legal proceedings in the ordinary course of, or incidental to the normal course of, its business, including proceedings to enforce its contractual or statutory rights. While the Company cannot predict the outcome of these legal proceedings with certainty, based upon currently available information, the Company does not believe the final outcome of any pending or threatened legal proceeding will have a material adverse effect on its results of operations or financial condition.

As a result of the Company’s completed seniors housing developments continuing to move towards or achieving stabilization, the Company monitors the lease-up of these properties to determine whether the established performance metrics have been met as of each reporting period. As of June 30, 2022, the Company had

The Company’s Advisor has approximately

13. Subsequent Events

In July 2022, the Company entered into a purchase and sale agreement for the sale of its Fieldstone Memory Care and Fieldstone at Pear Orchard properties (the “Fieldstone Sale Agreement”) with an unrelated third party buyer for a gross sales price of $

16

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Caution Concerning Forward-Looking Statements

Statements contained under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Quarterly Report on Form 10-Q for the quarter and six months ended June 30, 2022 that are not statements of historical or current fact may constitute “forward-looking statements” within the meaning of the Federal Private Securities Litigation Reform Act of 1995. The Company intends that such forward-looking statements be subject to the safe harbor created by Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements are statements that do not relate strictly to historical or current facts, but reflect management’s current understandings, intentions, beliefs, plans, expectations, assumptions and/or predictions regarding the future of the Company’s business and its performance, the economy, and other future conditions and forecasts of future events and circumstances. Forward-looking statements are typically identified by words such as “believes,” “expects,” “anticipates,” “intends,” “estimates,” “plans,” “continues,” “may,” “will,” “seeks,” “should,” and “could” and words and terms of similar substance in connection with discussions of future operating or financial performance, business strategy and portfolios, projected growth prospects, cash flows, costs and financing needs, legal proceedings, amount and timing of anticipated future distributions, estimated net asset value per share of the Company’s common stock, and/or other matters. The Company’s forward-looking statements are not guarantees of future performance. While the Company’s management believes its forward-looking statements are reasonable, such statements are inherently susceptible to uncertainty and changes in circumstances. As with any projection or forecast, forward-looking statements are necessarily dependent on assumptions, data and/or methods that may be incorrect or imprecise, and may not be realized. The Company’s forward-looking statements are based on management’s current expectations and a variety of risks, uncertainties and other factors, many of which are beyond the Company’s ability to control or accurately predict. Although the Company believes that the expectations reflected in such forward-looking statements are based upon reasonable assumptions, the Company’s actual results could differ materially from those set forth in the forward-looking statements due to a variety of risks, uncertainties and other factors.

Important factors that could cause the Company's actual results to vary materially from those expressed or implied in its forward-looking statements include, but are not limited to government regulation, economic, strategic, political and social conditions and the following:

17

Given these uncertainties, the Company cautions you not to place undue reliance on forward-looking information.

For further information regarding risks and uncertainties associated with the Company’s business and other important factors that could cause the Company’s actual results to vary materially from those expressed or implied in its forward-looking statements, please refer to the factors listed and described in the Company’s reports filed from time to time with the SEC, including, but not limited to, the Company’s quarterly reports on Form 10-Q and the Company’s annual reports on Form 10-K, copies of which may be obtained from the Company’s website at www.cnlhealthcareproperties.com. One of the most significant factors is the ongoing and potential impact of the current outbreak of the COVID-19 pandemic on the economy and the broader financial markets, which may have a significant negative impact on the Company’s financial condition, results of operations and cash flows. The Company is unable to predict whether the continuing effects of the COVID-19 pandemic will trigger a further economic slowdown or a recession and to what extent the Company will experience disruptions related to the COVID-19 pandemic in the third quarter of 2022 or thereafter.

18

All written and oral forward-looking statements attributable to the Company or persons acting on its behalf are qualified in their entirety by this cautionary note. Forward-looking statements speak only as of the date on which they are made, and the Company undertakes no obligation to, and expressly disclaims any obligation to, publicly release the results of any revisions to its forward-looking statements to reflect new information, changed assumptions, the occurrence of unanticipated subsequent events or circumstances, or changes to future operating results over time, except as otherwise required by law.

Introduction

The following discussion is based on the condensed consolidated financial statements as of June 30, 2022 (unaudited) and December 31, 2021. Amounts as of December 31, 2021 included in the unaudited condensed consolidated balance sheets have been derived from the audited consolidated financial statements as of that date. This information should be read in conjunction with the accompanying unaudited condensed consolidated balance sheets and the notes thereto, as well as the audited consolidated financial statements, notes and management’s discussion and analysis included in our Annual Report on Form 10-K for the year ended December 31, 2021.

Overview

CNL Healthcare Properties, Inc. is a Maryland corporation that elected to be taxed as a REIT for U.S. federal income tax purposes. We have and intend to continue to be organized and operate in a manner that allows us to remain qualified as a REIT for federal income tax purposes. The terms “us,” “we,” “our,” “Company” and “CNL Healthcare Properties” include CNL Healthcare Properties, Inc. and each of its subsidiaries.

Substantially all of our assets are held by, and all operations are conducted, either directly or indirectly, through: (1) the Operating Partnership in which we are the sole limited partner and our wholly owned subsidiary, CHP GP, LLC, is the sole general partner; (2) a wholly owned TRS, CHP TRS Holding, Inc.; (3) property owner subsidiaries and lender subsidiaries, which are single purpose entities; and (4) investments in joint ventures.

We are externally managed and advised by CNL Healthcare Corp. (the “Advisor”). Our Advisor has responsibility for our day-to-day operations, serving as our consultant in connection with policy decisions to be made by our board of directors, and for identifying, recommending and executing on Possible Strategic Alternatives (as described below under “Possible Strategic Alternatives”), and dispositions on our behalf pursuant to an advisory agreement. For additional information on our Advisor, its affiliates or other related parties, as well as the fees and reimbursements we pay, see Note 9. “Related Party Arrangements.”

As of June 30, 2022, our seniors housing investment portfolio consisted of interests in 72 properties, consisting of a geographically diversified portfolio of 71 seniors housing communities and one vacant land parcel. The types of seniors housing properties that we own include independent and assisted living facilities, continuing care retirement communities and Alzheimer’s/memory care facilities. Five of our 71 seniors housing properties were previously owned through an unconsolidated joint venture and became wholly-owned effective January 1, 2022.

Market Conditions

During the last half of 2021, we continued to experience the operational impacts of a challenging labor market. Labor costs increased at an accelerated rate during the last half of 2021 due to increases throughout all wage classifications within our communities and an increased focus on attracting and retaining staff at our communities. The “great resignation” resulted in an increase in the number of vacant positions at our communities and COVID-19 staff infections contributed to staff absences due to quarantine requirements under CDC guidelines. These factors led to an increase in the usage of temporary agency labor which led to incremental, measurable labor costs beginning in the middle of 2021. During 2022, we have begun to slowly reduce our reliance on agency labor as a result of hiring and filling some of the vacant staff roles as well as a decline in absences from lower COVID staff infections and more relaxed CDC quarantine requirements. However, we expect that historically low unemployment rates, wage pressures, overtime pay and continued reliance on temporary agency labor will result in higher labor costs and lower NOI margins during the rest of 2022.

19

During 2021, we began to experience the impact of higher inflation levels in the form of higher food costs and virtually all other operating expenses. This has contributed and continues to contribute to property NOI margin compressions in our managed seniors housing communities. We anticipate that operating expenses will continue to increase which will result in continued operating margin compressions during the remainder of 2022.

Macro-economic and geo political events around the globe have contributed to volatile credit markets. As part of its effort to reduce the rising levels of inflation, the Federal Reserve enacted several interest rate hikes during 2022 and projects additional rate increases during the rest of 2022. The interest rate increases to date and any further interest rate increases during 2022 will contribute to higher interest expense on our variable rate debt. We have purchased interest rate caps for interest rate protection on a portion of our unhedged variable rate debt and continue to monitor opportunities to further protect the remaining variable rate debt.

COVID-19

In March 2020, the World Health Organization declared the outbreak of the novel coronavirus (“COVID-19”) as a pandemic around the globe. Throughout 2020 and 2021, we operated our communities through the disruptions and uncertainties of the pandemic, including disruptions from new variants of the virus. Average occupancy began to decline at the onset of the pandemic starting in the second half of March 2020 and trended lower through February 2021. Starting in March 2021, we began to experience small occupancy gains each month as vaccines became available and regulatory move-in restrictions were lifted or relaxed. The positive marginal occupancy gains have continued through 2022 and have resulted in increases in resident fees and revenues. Absent the arrival of a new variant of the virus, we anticipate continued marginal occupancy improvements each month during the year ending December 31, 2022.

As of June 30, 2022, our 71 seniors housing communities were located throughout the United States in 26 states, and had a population of nearly 7,000 residents and approximately 4,700 community-level staff.

Of our 71 senior housing communities, we owned 15 properties (leased to two separate third party tenants under triple-net leases (“NNN”), and the remaining 56 properties were managed through third party operators. In December 2021, we provided a second round of rent relief in the form of a $1.4 million rent deferral agreement with a tenant that leases two properties under NNN leases. We did not grant any rent concessions as part of any rent deferral provided to this tenant. As of August 11, 2022, we had deferred $1.4 million in rents under the second rent deferral agreement and had collected all other amounts due in accordance with the terms of the tenant's lease agreements. As of August 11, 2022, had collected 100% of all rental amounts due under the lease agreements related to 13 seniors housing properties leased to our other tenant under NNN leases.

Since March 13, 2020, there have been a number of federal, state and local government initiatives to manage the spread of the virus and its impact on the economy, financial markets and continuity of businesses of all sizes and industries. On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) was signed into law which provided, among other things, for the establishment of a Provider Relief Fund under the direction of the Department of Health and Human Services (“HHS”). During the six months ended June 30, 2022 and 2021, we received provider relief funds under the CARES Act, which are deemed governmental grants provided that the recipient attests to and complies with certain terms and conditions, and we recorded approximately $3.9 million and $0.4 million, as other income in the accompanying condensed consolidated statements of operations as all conditions of the grant had been met.

We believe we have taken appropriate actions to manage through the COVID-19 pandemic. Although more normalized activities have resumed, we maintain focus on improving occupancy at the communities which will lead to a positive impact on our financial condition, results of operations and cash flows.

20

Possible Strategic Alternatives

In 2017, we began evaluating possible strategic alternatives to provide liquidity to our stockholders. In April 2018, our board of directors formed a special committee consisting solely of our independent directors (“Special Committee”) to consider possible strategic alternatives, including, but not limited to: (i) the listing of our or one of our subsidiaries’ common stock on a national securities exchange; (ii) an orderly disposition of our assets or one or more of our asset classes and the distribution of the net sale proceeds thereof to our stockholders; and (iii) a potential business combination or other transaction with a third party or parties that provides our stockholders with cash and/or securities of a publicly traded company (collectively, among other options, “Possible Strategic Alternatives”). Since 2018, the Special Committee has engaged KeyBanc Capital Markets Inc. to act as its financial advisor in connection with exploring our Possible Strategic Alternatives.

In connection with our consideration of the Possible Strategic Alternatives, our board of directors suspended both our Reinvestment Plan and our Redemption Plan effective July 11, 2018. In addition, as part of executing on Possible Strategic Alternatives, our board of directors committed to a plan to sell 70 properties which included medical office buildings, post-acute care facilities and acute care hospitals across the US), collectively (the “MOB/Healthcare Portfolio”) plus several skilled nursing facilities. Through December 31, 2021, we sold 69 properties, received net sales proceeds of approximately $1.4497 billion and used the net sales proceeds to: (1) repay indebtedness secured by the properties; (2) strategically rebalance other corporate borrowings; (3) make a special cash distribution in May 2019 of approximately $347.9 million (or $2.00 per share) to our stockholders and (4) retained net sales proceeds for other corporate purposes, because we were focused on maintaining balance sheet strength and liquidity during COVID-19 to enhance financial flexibility. In March 2022, we entered into a purchase and sale agreement for the last property in our MOB/Healthcare Portfolio, the Hurst Specialty Hospital, with an unrelated third party and in April 2022, sold it and received net sales proceeds of $8.3 million.

During the year ended December 31, 2020, we shifted our focus away from the pursuit of larger strategic alternatives to provide further liquidity to our stockholders due to the market and industry disruptions in the seniors housing sector from COVID-19. However, our Special Committee continued working and continues to work with our financial advisor to carefully study market data and pursue potential options to determine suitable liquidity alternatives that are in the best interests of all of our stockholders.

Seniors Housing Portfolio

Our remaining investment focus is in seniors housing communities. We have invested in or developed the following types of seniors housing properties:

Independent Living Facilities. Independent living facilities are age-restricted, multi-family rental or ownership (condominium) housing with central dining facilities that provide residents, as part of a monthly fee, meals and other services such as housekeeping, linen service, transportation, social and recreational activities.

Assisted Living Facilities. Assisted living facilities are usually state-regulated rental properties that provide the same services as independent living facilities, but also provide, in a majority of the units, supportive care from trained employees to residents who are unable to live independently and require assistance with activities of daily living. The additional services may include assistance with bathing, dressing, eating, and administering medications.

Memory Care/Alzheimer’s Facilities. Those suffering from the effects of Alzheimer’s disease or other forms of memory loss need specialized care. Memory care/Alzheimer’s centers provide the specialized care for this population including residential housing and assistance with the activities of daily living.

Portfolio Overview

As of June 30, 2022, our healthcare investment portfolio consisted of interests in 72 properties, comprising 71 seniors housing communities and one vacant land parcel. We completed the sale of two seniors housing managed properties in August 2022.

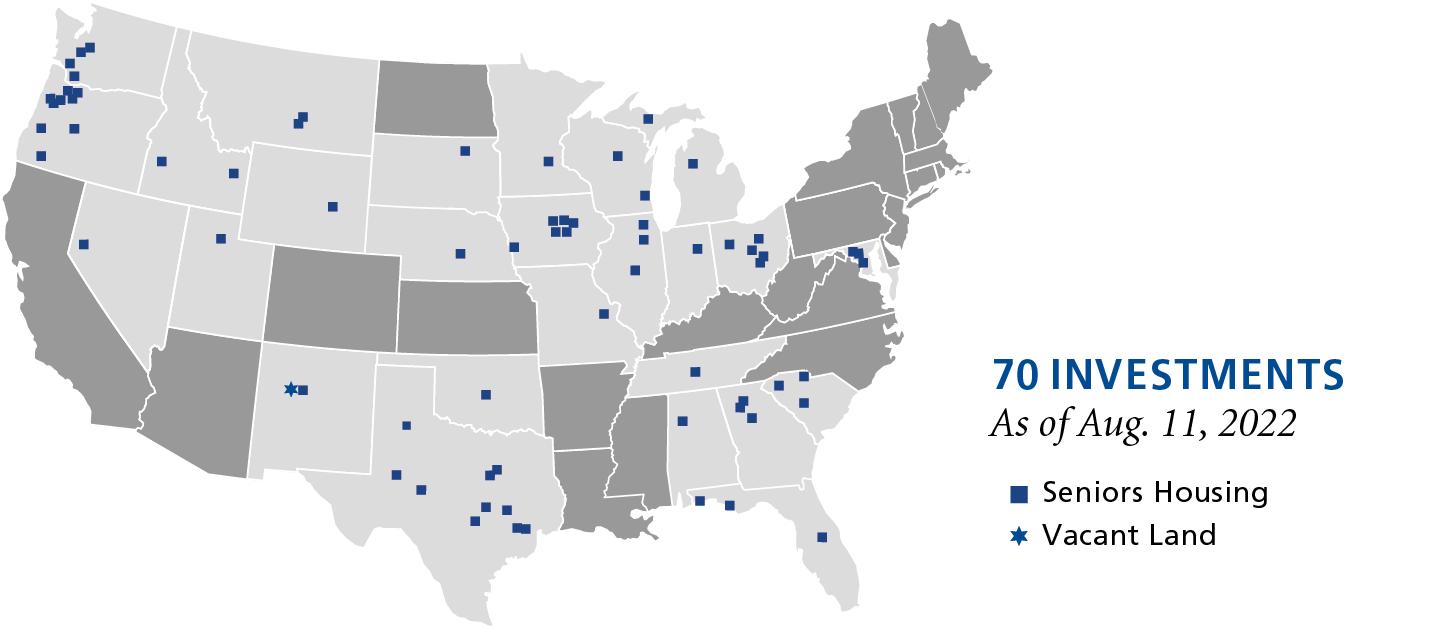

21

We believe demographic trends and compelling supply and demand indicators present a strong case for an investment focus on seniors housing real estate and real estate-related assets. Our seniors housing investment portfolio is geographically diversified with properties in 26 states. The map below shows our seniors housing investment portfolio across geographic regions as of August 11, 2022:

The following table summarizes our seniors housing investment portfolio by investment structure as of August 11, 2022:

Type of Investment |

|

Number of |

|

|

Amount of |

|

|

Percentage |

|

|||

Consolidated investments: |

|

|

|

|

|

|

|

|

|

|||

Seniors housing leased (1) |

|

|

15 |

|

|

$ |

311.0 |

|

|

|

17.8 |

% |

Seniors housing managed (2) |

|

|

54 |

|

|

|

1,427.6 |

|

|

|

82.1 |

% |

Vacant land |

|

|

1 |

|

|

|

1.1 |

|

|

|

0.1 |

% |

|

|

|

70 |

|

|

$ |

1,739.7 |

|

|

|

100.0 |

% |

_____________

FOOTNOTES:

Portfolio Evaluation

While we are not directly impacted by the performance of the underlying properties leased to third-party tenants, we believe that the financial and operational performance of our tenants provides an indication about the stability of our tenants and their ability to pay rent. To the extent that our tenants, managers or joint venture partners experience operating difficulties and become unable to generate sufficient cash to make rent payments to us, there could be a material adverse impact on our consolidated results of operations, liquidity and/or financial condition. Our tenants and managers are generally contractually required to provide this information to us in accordance with their respective lease, management and/or joint venture agreements. Therefore, in order to mitigate the aforementioned risk, we monitor our investments through a variety of methods determined by the type of property.

We monitor the credit of our tenants to stay abreast of any material changes in credit quality. We monitor credit quality by (1) reviewing financial statements that are publicly available or that are required to be delivered to us under the applicable lease, (2) direct interaction with onsite property managers, (3) monitoring news and rating agency reports regarding our tenants (or their parent companies) and their underlying businesses, (4) monitoring the timeliness of rent collections and (5) monitoring lease coverage.

22

When evaluating the performance of our seniors housing portfolio, management reviews property-level operating performance versus budgeted expectations, conducts periodic operational review calls with operators and conducts periodic property inspections or site visits. Management also reviews occupancy levels and monthly revenue per occupied unit, which we define as total revenue divided by average number of occupied units. Similarly, when evaluating the performance of our third-party operators, management reviews monthly financial statements, property-level operating performance versus budgeted expectations, conducts periodic operational review calls with operators and conducts periodic property inspections or site visits. All of the aforementioned operating and statistical metrics assist us in determining the ability of our properties or operators to achieve market rental rates, to assess the overall performance of our diversified healthcare portfolio, and to review compliance with leases, debt, licensure, real estate taxes, and other collateral.

Significant Tenants and Operators

Our real estate portfolio of 69 seniors housing properties is operated by a mix of national or regional operators and the following represent the significant tenants and operators that lease or manage 10% or more of our rentable space as of August 11, 2022, excluding the vacant land parcel:

Tenants |

|

Number of |

|

Rentable |

|

|

Percentage |

|

|

Lease |

||

TSMM Management, LLC |

|

13 |

|

|

1,261 |

|

|

|

77.5 |

% |

|

2025 |

Wellmore, LLC |

|

2 |

|

|

366 |

|

|

|

22.5 |

% |

|

2031-2032 |

|

|

15 |

|

|

1,627 |

|