Form 10-K/A ALBEMARLE CORP For: Dec 31

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________________

FORM 10-K/A

(Amendment No. 2)

________________________________________

| Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the fiscal year ended December 31 , 2021

or

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the transition period from to

Commission file number 001-12658

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (980 ) - 299-5700

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for at least the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity stock held by non-affiliates of the registrant was approximately $19.7 billion based on the last reported sale price of common stock on June 30, 2021, the last business day of the registrant’s most recently completed second quarter.

Number of shares of common stock outstanding as of February 11, 2022: 117,036,615

Documents Incorporated by Reference

Portions of Albemarle Corporation’s definitive Proxy Statement for its 2022 Annual Meeting of Shareholders filed with the U.S. Securities and Exchange Commission pursuant to Regulation 14A under the Securities Exchange Act of 1934, as amended, are incorporated by reference into Part III of this Annual Report on Form 10-K.

EXPLANATORY NOTE

On February 22, 2022, Albemarle Corporation (“Albemarle” or the “Company”) filed its Annual Report on Form 10-K for the year ended December 31, 2021 (the “2021 Form 10-K”) with the Securities and Exchange Commission (the “Original Filing”). In addition, the Company filed Amendment No. 1 to the Original Filing (“Amendment No. 1”) on March 2, 2022 to amend the Aggregate Annual Production table within the Mineral Properties section of Part I, Item 2. Properties of the Original Filing.

This Amendment No. 2 to the Original Filing (“Amendment No. 2”) is being filed to: (i) amend certain disclosures within the Mineral Properties section of Part I, Item 2. Properties of the 2021 Form 10-K; (ii) revise the disclosure regarding our disclosure controls and procedures in Part II, Item 9A. Controls and Procedures of the 2021 Form 10-K to reflect management’s conclusion that the Company’s disclosure controls and procedures were not effective at December 31, 2021 solely as a result of the updated disclosures responding to Item 601(b)(96) and subpart 1300 of Regulation S-K included in this Amendment No. 2; and (iii) file amended versions the Company’s material individual mineral property technical report summaries as revised Exhibits 96.1, 96.2, 96.3, 96.4, 96.5 and 96.6 to this Amendment No. 2.

This Amendment No. 2 also updates, amends and supplements Part IV, Item 15. Exhibits and Financial Schedules of the 2021 Form 10-K to include, among other items, the filing of new certifications of the Company’s Chief Executive Officer and Chief Financial Officer pursuant to Rule 13a-14(a) as Exhibits 31.1 and 31.2, as well as third-party consents for the technical report summaries in Exhibits 23.1, 23.2, 23.3, 23.4, 23.5 and 23.6.

Except as described above, this Amendment No. 2 does not amend, update or change any other information set forth in the 2021 Form 10-K (including in the consolidated financial statements included therein) and does not reflect or purport to reflect any information or events occurring after the original filing date or modify or update those disclosures affected by subsequent events. Accordingly, this Amendment No. 2 should be read in conjunction with the Original Filing and Amendment No. 1 and the Company’s other filings with the Securities and Exchange Commission. This Amendment No. 2 consists solely of the preceding cover page, this explanatory note, Part I, Item 2. Properties, Part II, Item 9A. Controls and Procedures, Part IV, Item 15. Exhibits and Financial Schedules, a signature page and the exhibits filed herewith.

3

PART I

| Item 2. | Properties. | ||||

We operate globally, with our principal executive offices located in Charlotte, North Carolina and regional shared services offices located in Budapest, Hungary and Dalian, China. Each of these properties are leased. We and our affiliates also operate regional sales and administrative offices in various locations throughout the world, which are generally leased.

We believe that our production facilities, research and development facilities, and sales and administrative offices are generally well maintained, effectively used and are adequate to operate our business. During 2021, the Company’s manufacturing plants operated at approximately 86% capacity, in the aggregate.

Set forth below is information regarding our production facilities operated by us and our affiliates. Additional details regarding our significant mineral properties can be found below the table.

| Location | Principal Use | Owned/Leased | ||||||||||||

| Lithium | ||||||||||||||

| Chengdu, China | Production of lithium carbonate and technical and battery-grade lithium hydroxide | Owned | ||||||||||||

Greenbushes, Australia(a) | Production of lithium spodumene minerals and lithium concentrate | Owned(e) | ||||||||||||

Kemerton, Australia(a)(b) | Production of lithium carbonate and technical and battery-grade lithium hydroxide | Owned(e) | ||||||||||||

| Kings Mountain, NC | Production of technical and battery-grade lithium hydroxide, lithium salts and battery-grade lithium metal products | Owned | ||||||||||||

| La Negra, Chile | Production of technical and battery-grade lithium carbonate and lithium chloride | Owned | ||||||||||||

| Langelsheim, Germany | Production of butyllithium, lithium chloride, specialty products, lithium hydrides, cesium and special metals | Owned | ||||||||||||

| New Johnsonville, TN | Production of butyllithium and specialty products | Owned | ||||||||||||

Salar de Atacama, Chile(a) | Production of lithium brine and potash | Owned(f) | ||||||||||||

Silver Peak, NV(a) | Production of lithium brine, technical-grade lithium carbonate and lithium hydroxide | Owned | ||||||||||||

| Taichung, Taiwan | Production of butyllithium | Owned | ||||||||||||

Wodgina, Australia(a)(c) | Production of lithium spodumene minerals and lithium concentrate | Owned and leased(e) | ||||||||||||

| Xinyu, China | Production of lithium carbonate and technical and battery-grade lithium hydroxide | Owned | ||||||||||||

| Bromine | ||||||||||||||

| Baton Rouge, LA | Research and product development activities, and production of flame retardants | Leased | ||||||||||||

Magnolia, AR(a) | Production of flame retardants, bromine, inorganic bromides, agricultural intermediates and tertiary amines | Owned | ||||||||||||

Safi, Jordan(a) | Production of bromine and derivatives and flame retardants | Owned and leased(e) | ||||||||||||

| Twinsburg, OH | Production of bromine-activated carbon | Leased | ||||||||||||

| Catalysts | ||||||||||||||

| Amsterdam, the Netherlands | Production of refinery catalysts, research and product development activities | Owned | ||||||||||||

| Bitterfeld, Germany | Refinery catalyst regeneration, rejuvenation, and sulfiding | Owned(e) | ||||||||||||

| La Voulte, France | Refinery catalysts regeneration and treatment, research and development activities | Owned(e) | ||||||||||||

| McAlester, OK | Refinery catalyst regeneration, rejuvenation, pre-reclaim burn off, as well as specialty zeolites and additives marketing activities | Owned(e) | ||||||||||||

| Mobile, AL | Production of tin stabilizers | Owned(e) | ||||||||||||

| Niihama, Japan | Production of refinery catalysts | Leased(e) | ||||||||||||

Pasadena, TX(d) | Production of aluminum alkyls, orthoalkylated anilines, refinery catalysts and other specialty chemicals; refinery catalysts regeneration services and research and development activities | Owned | ||||||||||||

| Santa Cruz, Brazil | Production of catalysts, research and product development activities | Owned(e) | ||||||||||||

| Takaishi City, Osaka, Japan | Production of aluminum alkyls | Owned(e) | ||||||||||||

4

(a) See below for further discussion of these significant mineral extraction facilities.

(b) Construction of Train I of the Kemerton, Australia facility was completed in the fourth quarter of 2021. Due to the ongoing labor shortages and COVID-19 pandemic travel restrictions in Western Australia, Train II construction is expected to be completed in the second half of 2022. Commercial sales volume from Train I will begin in 2022 and Train II in 2023.

(c) Since its acquisition in 2019, the Wodgina mine idled production of spodumene until the market demand supported bringing the mine back into production. MARBL recently announced its intention to resume spodumene concentrate production at this site, with the production restart expected during the second quarter of 2022.

(d) The Pasadena, Texas location includes three separate manufacturing plants which are owned, primarily utilized by Catalysts, including one plant that is owned by an unconsolidated joint venture.

(e) Owned or leased by joint venture.

(f) Ownership will revert to the Chilean government once we have sold all remaining amounts under our contract with the Chilean government pursuant to which we obtain lithium brine in Chile.

Mineral Properties

Set forth below are details regarding our mineral properties operated by us and our affiliates which have been prepared in accordance with the requirements of subpart 1300 of Regulation S-K, issued by the Securities and Exchange Commission (“SEC”). As used in this Annual Report on Form 10-K, the terms “mineral resource,” “measured mineral resource,” “indicated mineral resource,” “inferred mineral resource,” “mineral reserve,” “proven mineral reserve” and “probable mineral reserve” are defined and used in accordance with subpart 1300 of Regulation S-K. Under subpart 1300 of Regulation S-K, mineral resources may not be classified as “mineral reserves” unless the determination has been made by a qualified person (“QP”) that the mineral resources can be the basis of an economically viable project.

Except for that portion of mineral resources classified as mineral reserves, mineral resources do not have demonstrated economic value. Inferred mineral resources are estimates based on limited geological evidence and sampling and have a too high of a degree of uncertainty as to their existence to apply relevant technical and economic factors likely to influence the prospects of economic extraction in a manner useful for evaluation of economic viability. Estimates of inferred mineral resources may not be converted to a mineral reserve. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. A significant amount of exploration must be completed in order to determine whether an inferred mineral resource may be upgraded to a higher category. Therefore, it cannot be assumed that all or any part of an inferred mineral resource exists, that it can be the basis of an economically viable project, that it will ever be upgraded to a higher category, or that all or any part of the mineral resources will ever be converted into mineral reserves. See risk factor - “Our inability to acquire or develop additional reserves that are economically viable could have a material adverse effect on our future profitability,” in Item 1A. Risk Factors.

Overview

At December 31, 2021, we had the following mineral extraction facilities:

5

| Location | Business Segment | Ownership % | Extraction Type | Stage | |||||||||||||||||||

| Australia | |||||||||||||||||||||||

| Greenbushes | Lithium | 49% | Hard rock | Production | |||||||||||||||||||

| Wodgina | Lithium | 60%(a) | Hard rock | Production(b) | |||||||||||||||||||

| Chile | |||||||||||||||||||||||

| Salar de Atacama | Lithium | 100% | Brine | Production | |||||||||||||||||||

| Jordan | |||||||||||||||||||||||

Safi(c) | Bromine | 50% | Brine | Production | |||||||||||||||||||

| United States | |||||||||||||||||||||||

| Kings Mountain, NC | Lithium | 100% | Hard rock | Development | |||||||||||||||||||

Magnolia, AR(c) | Bromine | 100% | Brine | Production | |||||||||||||||||||

Silver Peak, NV(c) | Lithium | 100% | Brine | Production | |||||||||||||||||||

(a) Through our MARBL joint venture, we own 60% interest in the Wodgina Project.

(b) Following the Wodgina acquisition in 2019, the Wodgina mine idled production of spodumene until market demand supported bringing the mine back into production. In October 2021, our 60%-owned MARBL joint venture announced its intention to resume spodumene concentrate production at the Wodgina mine, with the production restart expected during the second quarter of 2022.

(c) Site includes on-site, or otherwise near-by exclusive, conversion facilities. See individual property disclosure below for further details.

Aggregate annual production from our mineral extraction facilities is shown in the below table. Amounts represent Albemarle’s attributable portion based on ownership percentages noted above and are shown in thousands of metric tonnes of lithium metal and bromine production. Lithium and bromine is extracted as brine or hard rock concentrate at the extraction facilities. These are then further converted into various compounds and products at on-site processing facilities or other conversion facilities owned by Albemarle around the world. In addition, the brine or concentrate can be used by tolling entities for further processing.

| Aggregate Annual Production (metric tonnes in thousands) | |||||||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2021 | 2020 | 2019 | |||||||||||||||

| Lithium | |||||||||||||||||

Australia(a) | |||||||||||||||||

Greenbushes(b) | 13 | 8 | 11 | ||||||||||||||

| Chile | |||||||||||||||||

Salar de Atacama(c) | 8 | 8 | 7 | ||||||||||||||

| United States | |||||||||||||||||

| Silver Peak, NV | 2 | 2 | 1 | ||||||||||||||

| Bromine | |||||||||||||||||

| Jordan | |||||||||||||||||

Safi(d)(e) | 57 | 56 | 56 | ||||||||||||||

| United States | |||||||||||||||||

Magnolia, AR(f) | 71 | 74 | 73 | ||||||||||||||

(a) Wodgina had no production during the periods presented in the table.

(b) Production from Greenbushes represents 49% of production of the Greenbushes mine which is attributable to the Company’s interest in the Talison Lithium Australia Pty Ltd joint venture.

(c) The Salar de Atacama operation also produces potash (potassium chloride), bichofite, halite and sylvinite as byproducts. However, the Company does not consider production of these byproducts as material to the economics of the operation.

(d) Production from Safi represents the 50% production by the Jordan Bromine Project which is attributable to the Company’s interest in the Jordan Bromine Company Limited (“JBC”) joint venture.

6

(e) The Safi operation also produces potassium hydroxide (“KOH”) as a byproduct. However, the Company does not consider production of these byproducts as material to the economics of the operation.

(f) In addition, elemental sulfur and sodium hydrosulfide solution (“NaHS”) are manufactured from the sour gas produced by the Magnolia operation. However, the Company does not consider these products as material to the economics of the operation.

See individual property disclosure below for further details regarding mineral rights, titles, property size, permits and other information for our significant mineral extraction properties. The extracted brine or hard rock is processed at facilities on location (as described below) or processed, or further processed, at other facilities throughout the world.

The following table provides a summary of our mineral resources, exclusive of reserves, at December 31, 2021. The below mineral resource amounts are rounded and shown in thousands of metric tonnes. The amounts represent Albemarle’s attributable portion based on ownership percentages noted above. The relevant technical information supporting mineral resources for each material property is included in the "”Material Individual Properties” section below, as well as the in the technical report summaries filed as Exhibits 96.1 to 96.6 to this report.

| Measured Mineral Resources | Indicated Mineral Resources | Measured and Indicated Mineral Resources | Inferred Mineral Resources | ||||||||||||||||||||||||||||||||||||||||||||

| Amount (‘000s metric tonnes) | Grade (Li2O%) | Amount (‘000s metric tonnes) | Grade (Li2O%) | Amount (‘000s metric tonnes) | Grade (Li2O%) | Amount (‘000s metric tonnes) | Grade (Li2O%) | ||||||||||||||||||||||||||||||||||||||||

| Lithium - Hard Rock: | |||||||||||||||||||||||||||||||||||||||||||||||

| Australia | |||||||||||||||||||||||||||||||||||||||||||||||

| Greenbushes | — | — | 16,900 | 1.47% | 16,900 | 1.47% | 20,000 | 1.05% | |||||||||||||||||||||||||||||||||||||||

Wodgina(a) | — | — | 13,400 | 1.39% | 13,400 | 1.39% | 98,500 | 1.15% | |||||||||||||||||||||||||||||||||||||||

| United States | |||||||||||||||||||||||||||||||||||||||||||||||

| Kings Mountain, NC | — | — | 46,816 | 1.37% | 46,816 | 1.37% | 42,869 | 1.10% | |||||||||||||||||||||||||||||||||||||||

| Amount (‘000s metric tonnes) | Concentration (mg/L) | Amount (‘000s metric tonnes) | Concentration (mg/L) | Amount (‘000s metric tonnes) | Concentration (mg/L) | Amount (‘000s metric tonnes) | Concentration (mg/L) | ||||||||||||||||||||||||||||||||||||||||

| Lithium - Brine: | |||||||||||||||||||||||||||||||||||||||||||||||

| Chile | |||||||||||||||||||||||||||||||||||||||||||||||

| Salar de Atacama | 717 | 2,211 | 642 | 1,747 | 1,360 | 1,959 | 131 | 1,593 | |||||||||||||||||||||||||||||||||||||||

| United States | |||||||||||||||||||||||||||||||||||||||||||||||

| Silver Peak, NV | 10 | 152 | 25 | 143 | 35 | 145 | 63 | 121 | |||||||||||||||||||||||||||||||||||||||

(a) Through our MARBL joint venture, we own a 60% interest in the Wodgina project. We are therefore reporting 60% of Wodgina’s mineral resources.

The feedstock for the Safi, Jordan site, owned 50% by Albemarle through its JBC joint venture, is drawn from the Dead Sea, a nonconventional reservoir owned by the nations of Israel and Jordan. As such, there are no specific resources owned by JBC, but Albemarle’s joint venture partner, Arab Potash Company (“APC”) has exclusive rights granted by the Hashemite Kingdom of Jordan to withdraw brine from the Dead Sea and process it to extract minerals. The measured resource of bromide ion attributable to Albemarle’s 50% interest in its JBC joint venture is estimated to be approximately 177.5 million metric tonnes. JBC is extracting approximately 1 percent of the bromine available in Jordan’s share of the Dead Sea. Bromide concentration in the Dead Sea is estimated to average approximately 5,000 parts per million (“ppm”).

There are no mineral resource estimates at the Magnolia, AR bromine extraction site. All bromine mineral accumulations of economic interest and with reasonable prospects for eventual economic extraction within the Magnolia production lease area are either currently on production or subject to an economically viable future development plan and are classified as mineral reserves.

The following table provides a summary of our mineral reserves at December 31, 2021. The below mineral reserve amounts are rounded and shown in thousands of metric tonnes. The amounts represent Albemarle’s attributable portion based on ownership percentages noted above. The relevant technical information supporting mineral reserves for each material property is included in the "”Material Individual Properties” section below, as well as the in the technical report summaries filed as Exhibits 96.1 to 96.6 to this report.

7

| Proven Mineral Reserves | Probable Mineral Reserves | Total Mineral Reserves | |||||||||||||||||||||||||||||||||

| Amount (‘000s metric tonnes) | Grade (Li2O%) | Amount (‘000s metric tonnes) | Grade (Li2O%) | Amount (‘000s metric tonnes) | Grade (Li2O%) | ||||||||||||||||||||||||||||||

Lithium - Hard Rock(a): | |||||||||||||||||||||||||||||||||||

| Australia | |||||||||||||||||||||||||||||||||||

| Greenbushes | — | — | 69,900 | 1.95% | 69,900 | 1.95% | |||||||||||||||||||||||||||||

| Amount (‘000s metric tonnes) | Concentration (mg/L) | Amount (‘000s metric tonnes) | Concentration (mg/L) | Amount (‘000s metric tonnes) | Concentration (mg/L) | ||||||||||||||||||||||||||||||

| Lithium - Brine: | |||||||||||||||||||||||||||||||||||

| Chile | |||||||||||||||||||||||||||||||||||

| Salar de Atacama | 323 | 2,190 | 324 | 1,927 | 647 | 2,071 | |||||||||||||||||||||||||||||

| United States | |||||||||||||||||||||||||||||||||||

| Silver Peak, NV | 13 | 88 | 49 | 83 | 62 | 84 | |||||||||||||||||||||||||||||

| Bromine: | |||||||||||||||||||||||||||||||||||

| United States | |||||||||||||||||||||||||||||||||||

Magnolia, AR(b) | 2,497 | 574 | 3,071 | ||||||||||||||||||||||||||||||||

(a) The Wodgina mine is at an initial assessment level, and as a result, contains no mineral reserves. Mineral reserve estimates are not applicable for the Kings Mountain site.

(b) The concentration of bromine at the Magnolia site varies based on the physical location of the field and can range up to over 6,000 mg/L.

All bromine reserves reported by Albemarle for the JBC project are classified as proven mineral reserves. The mineral reserve estimate for the Safi, Jordan bromine site attributable to Albemarle’s 50% interest in its JBC joint venture is approximately 2.45 million metric tonnes of bromine from the Dead Sea. This estimate is based on the time available under the concession agreement with the Hashemite Kingdom of Jordan and the processing capability of the JBC plant. As only approximately one percent of the available resource is consumed from the Dead Sea, as noted above, the reserve estimate is based on the amount the JBC plant can produce over until the end of 2058, when the APC concession agreement ends. Bromine concentration used to calculate the reserve estimate from the Dead Sea was approximately 8,890 ppm based on historical pumping.

Mineral resource and reserve estimates were prepared by a QP with an effective date provided in the individual technical report summaries filed as Exhibits 96.1 to 96.6 to this report. Differences from those amounts in the technical report summaries represent depletion from the effective date of the report until December 31, 2021. Our mineral resource and reserve estimates are based on many factors, including the area and volume covered by our mining rights, assumptions regarding our extraction rates based upon an expectation of operating the mines on a long-term basis and the quality of in-place reserves.

Internal Controls

The modeling and analysis of our mineral resources and reserves was developed by our site personnel and reviewed by several levels of internal management, as well as the QP for each site. The development of such resources and reserves estimates, including related assumptions, were prepared by a QP.

When determining resources and reserves, as well as the differences between resources and reserves, management developed specific criteria, each of which must be met to qualify as a resource or reserve, respectively. These criteria, such as demonstration of economic viability, points of reference and grade, are specific and attainable. The QP and management agree on the reasonableness of the criteria for the purposes of estimating resources and reserves. Calculations using these criteria are reviewed and validated by the QP.

Estimations and assumptions were developed independently for each significant mineral location. All estimates require a combination of historical data and key assumptions and parameters. When possible, resources and data from public information and generally accepted industry sources, such as governmental resource agencies, were used to develop these estimations.

Each site has developed quality control and quality assurance (“QC/QA”) procedures, which were reviewed by the QP, to ensure the process for developing mineral resource and reserve estimates were sufficiently accurate. QC/QA procedures include

8

independent checks (duplicates) on samples by third party laboratories, blind blank/standard insertion into sample streams, duplicate sampling, among others. In addition, the QPs reviewed the consistency of historical production at each site as part of their analysis of the QC/QA procedures. See details of the controls for each site in the technical summary reports filed as Exhibits 96.1 to 96.6 to this report.

We recognize the risks inherent in mineral resource and reserve estimates, such as the geological complexity, the interpretation and extrapolation of field and well data, changes in operating approach, macroeconomic conditions and new data, among others. The capital, operating and economic analysis estimates rely on a range of assumptions and forecasts that are subject to change. In addition, certain estimates are based on mineral rights agreements with local and foreign governments. Any changes to these access rights could impact the estimates of mineral resources and reserves calculated in these reports. Overestimated resources and reserves resulting from these risks could have a material effect on future profitability.

Material Individual Properties

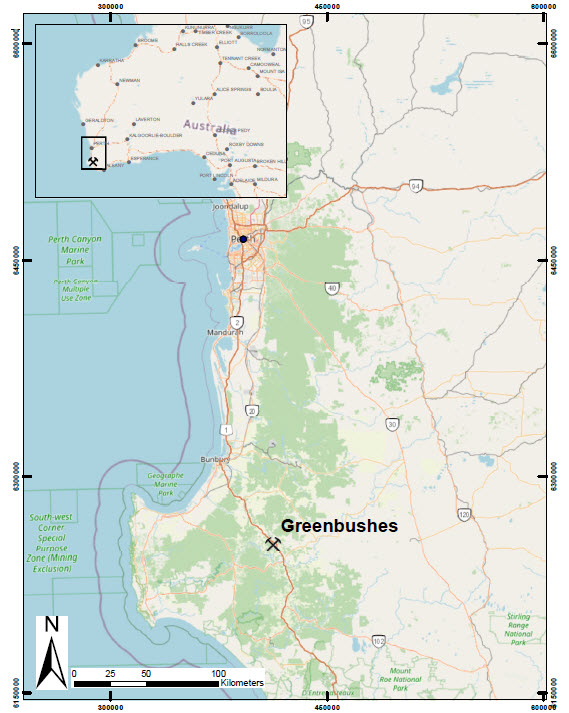

Greenbushes, Australia

The Greenbushes mine is a hard rock, open pit mine (latitude 33° 52´S, longitude 116° 04´ E) located approximately 250km south of Perth, Western Australia, 90km southeast of the port of Bunbury, a major bulk-handling port in the southwest of Western Australia. The lithium mining operation is near the Greenbushes townsite located in the Shire of Bridgetown-Greenbushes. Access to the Greenbushes Mine is via the paved South Western Highway between Bunbury and Bridgetown to Greenbushes Township and via the paved Maranup Ford Road to the Greenbushes Mine.

Lithium production from the Greenbushes Mine has been undertaken continuously for more than 20 years. Modern exploration has been undertaken on the property since the mid-1980s, first by Greenbushes Limited, then by Lithium Australia Ltd and in turn by Sons of Gwalia prior to the acquisition of Greenbushes by Talison in 2007. Initial exploration focused largely on tantalum, with the emphasis changing to lithium from around 2000. In 2014, Rockwood acquired a 49% ownership interest

9

in Windfield, which owns 100% of Talison, from Sichuan Tianqi Lithium Industries Inc. This 49% ownership in Windfield was assumed by Albemarle in 2015 as part of the acquisition of Rockwood. We purchase lithium concentrate from Windfield, and our investment in the joint venture is reported as an unconsolidated equity investment on our balance sheet.

About 55% of the tenements held by Talison are covered by Western Australia’s State Forest, which is under the authority of the Western Australia Department of Biodiversity, Conservation and Attractions. The majority of the remaining land is private land that covers about 40% of the surface rights. The remaining ground comprises crown land, road reserves and other miscellaneous reserves. The tenements cover a total area of approximately 10,000 hectares and include the historic Greenbushes tin, tantalum and current lithium mining areas. See section 3 of the Greenbushes technical report summary, filed as Exhibit 96.1 to this report, for a listing of tenements held by the Greenbushes site. Talison holds the mining rights for all lithium minerals on these tenements. The operating open pit lithium mining and processing plant area covers approximately 2,000 hectares comprising three mining leases. All lithium mining activities, including tailings storage, processing plant operations, open pits and waste rock dumps, are currently carried out within the boundaries of the three mining leases plus two general purpose leases. In order to keep the granted tenements in good standing, Talison is required to maintain permits, make an annual contribution to the statutory Mining Rehabilitation Fund and pay a royalty on concentrate sales for lithium mineral production as prescribed under the Mining Act 1978 in Western Australia. There are no private royalties that apply to the Greenbushes property. Talison reviews and renews all tenements on an annual basis.

The Greenbushes deposit consists of a main, rare-metal zoned pegmatite body, with numerous smaller footwall pegmatite dykes and pods. The primary intrusion and its subsidiary dykes and pods are concentrated within shear zones on the boundaries of granofels, ultramafic schists and amphibolites. The pegmatites are crosscut by ferrous-rich, mafic dolerite which is of paramount importance to the currant mining methods. The pegmatite body is over 3 km long (north by northwest), up to 300 meters wide (normal to dip), strikes north to northwest and dips moderately to steeply west to southwest.

The major minerals from the Greenbushes pegmatite are quartz, spodumene, albite and K-feldspar. The main lithium-bearing minerals are spodumene (containing approximately 8% lithium oxide) and varieties kunzite and hiddenite. Minor to trace lithium minerals include lepidolite mica, amblygonite and lithiophilite. Lithium is readily leached in the weathering environment and thus is virtually non-existent in weathered pegmatite. Exploration drilling at Greenbushes has been ongoing for over 40 years, including drilling in 2020, using reverse circulation and diamond drill holes.

Three lithium mineral processing plants are currently operating on the Greenbushes site, two chemical grade plants and a technical grade plant. Tailings are discharged to the tailings storage facility without the need for any neutralization process. Additional infrastructure on site includes power and water supply facilities, a laboratory, administrative offices, occupational health/safety/training offices, dedicated mines rescue area, stores, storage sheds, workshops and engineering offices. The Greenbushes site also leases production drills, excavators, trucks and various support equipment to extract the ore deposit by open pit methods. Talison’s power is delivered by a local distribution system and reticulated and metered within the site. Water is sourced from rainfall and stored in several process dams located on site. We consider the condition of all of our plants, facilities and equipment to be suitable and adequate for the businesses we conduct, and we maintain them regularly. As of December 31, 2021, our 49% ownership interest of the gross asset value of the facilities at the Greenbushes site was approximately $415.6 million.

Talison ships the chemical-grade lithium concentrate in vessels to our facilities in Meishan and Xinyu, China to process into battery-grade lithium hydroxide. In addition, the output from Talison can be used by tolling entities in China to produce both lithium carbonate and lithium hydroxide.

A summary of the Greenbushes facility’s lithium mineral resources and reserves as of December 31, 2021 are shown in the following tables. This is the first period estimated mineral resources, exclusive of reserves, and reserves have been developed for Greenbushes since being acquired by Albemarle. SRK Consulting (U.S.) Inc. (“SRK”), a third-party firm comprising mining experts in accordance with Item 1302(b)(1) of Regulation S-K, served as the QP and prepared the estimates of lithium mineral resources and reserves at the Greenbushes facility, with an effective date of June 30, 2021. A copy of the QP’s amended technical report summary with respect to the lithium mineral resource and reserve estimates at the Greenbushes facility, dated December 16, 2022 is filed as Exhibit 96.1 to this report. The amounts represent Albemarle’s attributable portion based on a 49% ownership percentage, and are presented as metric tonnes of lithium ore in thousands.

10

| Amount | Grade (Li2O%) | ||||||||||

| Indicated mineral resources: | |||||||||||

| Resource Pit | 15,600 | 1.54% | |||||||||

| Reserve Pit | 1,300 | 0.64% | |||||||||

| Inferred mineral resources: | |||||||||||

| Resource Pit | 11,700 | 1.05% | |||||||||

| Reserve Pit | 8,200 | 1.05% | |||||||||

| Stockpiles | 100 | 1.40% | |||||||||

•Mineral resources are reported exclusive of mineral reserves. Mineral resources are not mineral reserves and do not have demonstrated economic viability.

•Resources have been reported as in situ (hard rock within optimized pit shell) and stockpile (mined and stored on surface as blasted/crushed material).

•Resources have been categorized subject to the opinion of a QP based on the amount/robustness of informing data for the estimate, consistency of geological/grade distribution, survey information, and have been validated against long term mine reconciliation for the in-situ volumes.

•Resources which are contained within the mineral reserve pit design may be excluded from reserves due to an Inferred classification or because they sit in the incremental cutoff grade range between the resource and reserve cutoff grade. They are disclosed separately from the resources contained within the Resource Pit. There is reasonable expectation that some Inferred resources within the mineral reserve pit design may be converted to higher confidence materials with additional drilling and exploration effort.

•All Measured and Indicated Stockpile resources have been converted to mineral reserves.

•Mineral resources are reported considering a nominal set of assumptions for reporting purposes:

◦Mass Yields (“MY”) for chemical grade material are based on Greenbushes chemical grade plant 1 (“CGP1”) life-of-mine (“LoM”) feed MY formula. For the LoM material, MY is assumed at 29.49% and is subject to a 97% recovery limitation when the lithium oxide grade exceeds 5.5%. Mass yield varies as a function of grade, and may be reported herein at lower mass yields than the CGP1 average.

◦Pit optimization and economics for derivation of cutoff grade include mine gate pricing of $672/metric tonne of 6% Li2O concentrate, $4.75/metric tonne mining cost (LoM average cost-variable by depth), $17.87/metric tonne processing cost, $4.91/metric tonne G&A cost, and $2.66/metric tonne sustaining capital cost.

◦Costs estimated in Australian Dollars (“AUD”) were converted to US Dollars based on an exchange rate of AUD 0.76:$1.00.

◦These economics define a cutoff grade of 0.573% Li2O.

◦An overall 43% pit slope angle, 0% mining dilution, and 100% mining recovery.

◦Resources were reported above this 0.573% Li2O cutoff grade and are constrained by an optimized break-even pit shell.

◦No infrastructure movement capital costs have been added to the optimization.

◦Resources are reported with a cutoff grade between 0.5% and 0.7% Li2O.

◦Stockpile resources have been previously mined between nominal cutoff grades of 0.5 to 0.7% Li2O.

•Mineral resources tonnage and contained metal have been rounded to reflect the accuracy of the estimate, and numbers may not add due to rounding.

| Amount | Grade (Li2O%) | ||||||||||

| Probable mineral reserves: | |||||||||||

| Reserve Pit | 67,650 | 1.97% | |||||||||

| Stockpiles | 2,250 | 1.31% | |||||||||

•Mineral reserves are reported exclusive of mineral resources.

•Indicated in situ resources have been converted to Probable reserves.

•Measured and Indicated stockpile resources have been converted to Probable mineral reserves.

•Mineral reserves are reported considering a nominal set of assumptions for reporting purposes:

◦Mineral reserves are based on a mine gate price of $577/metric tonne of chemical grade concentrate (6% Li2O).

◦Mineral reserves assume 80% mining recovery for ore/waste contact areas and 100% for non-waste contact material.

◦Mineral reserves are diluted at approximately 20% at zero grade for ore/waste contact areas in addition to internal dilution built into the resource model (2.7% with the assumed selective mining unit of 5 m x 5 m x 5 m).

◦The MY for reserves processed through the chemical grade plants is estimated by the based on Greenbushes’ MY formula and the LoM mass yield is 29.49% subject to a 97% recovery limitation when the lithium oxide grade exceeds 5.5%.

◦The MY for reserves processed through the chemical grade plant chemical grade plant 2 (“CGP2”) in the next three to four years is estimated by the based on Greenbushes’ MY formula for a LoM mass yield of 16.77%, and is subject to a 97% recovery limitation when the lithium oxide grade exceeds 5.5%. The CGP2 plant is going through a ramp up period where lower recoveries are expected until all equipment has been optimized and additional capital is spent.

11

◦The MY for reserves processed through the technical grade plant is estimated by the based on Greenbushes’ MY formula and the LoM mass yield is 46.18%. There is approximately 3.5 million metric tonnes of technical grade plant feed at 4% Li2O

◦Although Greenbushes produces a technical grade product from the current operation, it is assumed that the reserves reported herein will be sold as a chemical grade product. This assumption is necessary because feed for the technical grade plant is currently only defined at the grade control or blasting level. Therefore, it is conservatively assumed that concentrate produced by the technical grade plant will be sold at the chemical grade product price

◦Pit optimization and economics for derivation of cutoff grade include mine gate pricing of $577/metric tonne of 6% Li2O concentrate, $4.75/metric tonne mining cost (LoM average cost-variable by depth), $17.87/metric tonne processing cost, $4.91/metric tonne G&A cost, and $2.66/metric tonne sustaining capital cost. The mine gate price is based on 650/metric tonne-concentrate cost-insurance-freight (“CIF”) less $73/metric tonne-concentrate for government royalty and transportation to China.

◦Costs estimated in AUD were converted to US Dollars based on an exchange rate of AUD 0.76:$1.00.

◦The price, cost and mass yield parameters, along with the internal constraints of the current operations, result in a mineral reserves cutoff grade of 0.7% Li2O.

◦The cutoff grade of 0.7% Li2O was applied to reserves that are constrained by the ultimate pit design and are detailed in a yearly mine schedule.

◦Stockpile reserves have been previously mined and are reported at a 0.7% Li2O cutoff grade.

•Waste tonnage within the reserve pit is 459 metric tonnes at a strip ratio of 3.32:1 (waste to ore – not including reserve stockpiles).

•Mineral reserve tonnage, grade and mass yield have been rounded to reflect the accuracy of the estimate, and numbers may not add due to rounding.

The LoM sustaining capital cost of $2.66/metric tonne of ore was used only for the purposes of pit optimization and cut-off grade calculation. This sustaining capital cost was based on estimates of LoM annual sustaining capital costs for Greenbushes that was included in the 2021 budget. Subsequent to pit optimization, design and scheduling, a detailed estimate of LoM sustaining capital costs was prepared.

Key assumptions and parameters relating to the lithium mineral resources and reserves at the Greenbushes facility are discussed in sections 11 and 12, respectively, of the Greenbushes technical report summary.

12

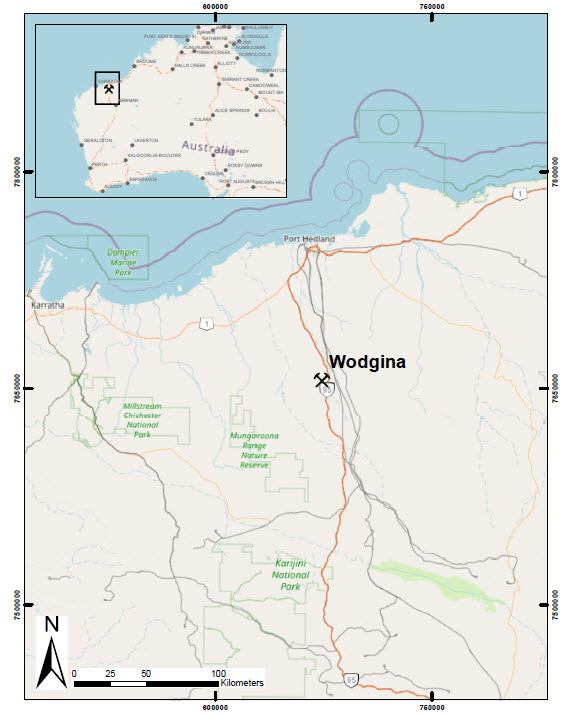

Wodgina, Australia

The Wodgina property, which includes a hard rock, open pit mine (latitude -21° 11' 25"S, longitude 118° 40' 25"E) is located approximately 110 km south-southeast of Port Hedland, Western Australia between the Turner and Yule Rivers. The area includes multiple prominent greenstone ridges up to 180 m above mean sea level surrounded by granitic plains and lowlands. The property is accessible via National Highway 1 to National highway 95 to the Wodgina camp road. All roads to site are paved. The nearest large regional airport is in Port Hedland which also hosts an international deep-water port facility. In addition, a site dedicated all-weather airstrip is located near to site, capable of landing certain aircrafts.

The Wodgina pegmatite deposits were discovered in 1902. Since then, the pegmatite-hosted deposits have been mined for tin, tantalum, beryl, and lithium by various companies. Mining occurred sporadically until Goldrim Mining formed a new partnership with Pan West Tantalum Pty Ltd., who opened open pit mining at the site in 1989 and progressively expanded during the 1990s. Active mining at the Mt. Cassiterite pit has been started and stopped regularly between 2008 and the present. The mine was placed on care and maintenance in 2008, 2012, and most recently in 2019. In 2016, MRL acquired the mine and upgraded the processing facilities and site infrastructure to 750ktpa spodumene plant producing 6% spodumene concentrate, completed in 2019. On October 31, 2019, we completed the acquisition of a 60% interest in this hard rock lithium mine project and formed an unincorporated joint venture with MRL, named MARBL. We formed MARBL for the exploration, development, mining, processing and production of lithium and other minerals (other than iron ore and tantalum) from the Wodgina Project. Following the acquisition, MARBL’s production of spodumene was idled until market demand supported bringing the mine back into production. In October 2021, our 60%-owned MARBL joint venture announced its intention to resume spodumene concentrate production at the Wodgina mine, with the production restart expected during the second quarter of 2022.

Wodgina holds mining tenements within the Karriyarra native title claim and are subject to the Land Use Agreement dated March 2001 between the Karriyarra People and Gwalia Tantalum Ltd (now Wodgina Lithium, a 100% subsidiary of MRL, our MARBL joint venture partner). See section 3 of the Wodgina technical report summary, filed as Exhibit 96.2 to this report, for a listing of all mining and exploration land tenements, which are in good standing and no known impediments exist. Certain

13

tenements are due for renewal in 2026 and another in 2030. Drilling and exploration activities have been conducted throughout the mining life of the Wodgina property.

The Wodgina mine is a pegmatite lithium deposit with spodumene the dominant mineral. The lithium mineralization occurs as 10 - 30 cm long grey-white spodumene crystals within medium grained pegmatites comprising primarily of quartz, feldspar, spodumene, and muscovite. Typically, the spodumene crystals are oriented orthogonal to the pegmatite contacts.

The facilities at Wodgina consist of a three stage crushing plant, the spodumene concentration plant, administrative offices, an accommodation camp, a power station, gas pipeline, three mature and reliable water bore fields, extension for future tailing storage and a fleet of owned and leased mine production equipment. The gas pipeline feeds the site power station to provide the power to the facilities. Water is obtained from the dedicated water bore fields. We consider the condition of all of our plants, facilities and equipment to be suitable and adequate for the businesses we conduct, and we maintain them regularly. As of December 31, 2021, our 60% ownership interest of the gross asset value of the facilities at our Wodgina site was approximately $192.2 million.

A summary of the Wodgina facility’s lithium mineral resources as of December 31, 2021 are shown in the following tables. This is the first period estimated mineral resources have been developed for Wodgina since being acquired by Albemarle. SRK served as the QP and prepared the estimates of lithium mineral resources and reserves at the Wodgina facility, with an effective date of September 30, 2020. A copy of the QP’s amended technical report summary with respect to the lithium mineral resource estimates at the Wodgina facility, dated December 16, 2022, is filed as Exhibit 96.2 to this report. Mineral resources for Wodgina represent 60% interest in the Wodgina Project. which is attributable to the Company’s interest in the MARBL joint venture. Amounts are presented as metric tonnes of lithium ore in thousands.

| Amount | Grade (Li2O%) | ||||||||||

| Indicated mineral resources | 13,400 | 1.39% | |||||||||

| Measured and Indicated mineral resources | 13,400 | 1.39% | |||||||||

| Inferred mineral resources | 98,500 | 1.15% | |||||||||

• All significant figures are rounded to reflect the relative accuracy of the estimates.

• The Mineral Resource estimate has been classified in accordance with SEC S-K 1300 guidelines and definitions.

• The Cassiterite Deposit comprises the historically mined Mt. Cassiterite pit and undeveloped North Hill areas.

• Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. Inferred Mineral Resources have a high degree of uncertainty as to their economic and technical feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resources can be upgraded to Measured or Indicated Mineral Resources.

• Metallurgical recovery of lithium has been estimated on a block basis at a consistent 65% based on documentation from historic plant production.

• To demonstrate reasonable prospects for eventual economic extraction of Mineral Resources, a cut-off grade of 0.5% Li2O based on metal recoverability assumptions, long-term lithium price assumptions of $584/metric tonne, variable mining costs averaging $3.40/metric tonne, processing costs and G&A costs totaling $23/metric tonne.

• There are no known legal, political, environmental, or other risks that could materially affect the potential development of the Mineral Resources based on the level of study completed for this property.

The Wodgina mine is at an initial assessment level, and as a result, contains no mineral reserves. Key assumptions and parameters relating to the lithium mineral resources at the Wodgina facility are discussed in section 11 of the Wodgina technical report summary.

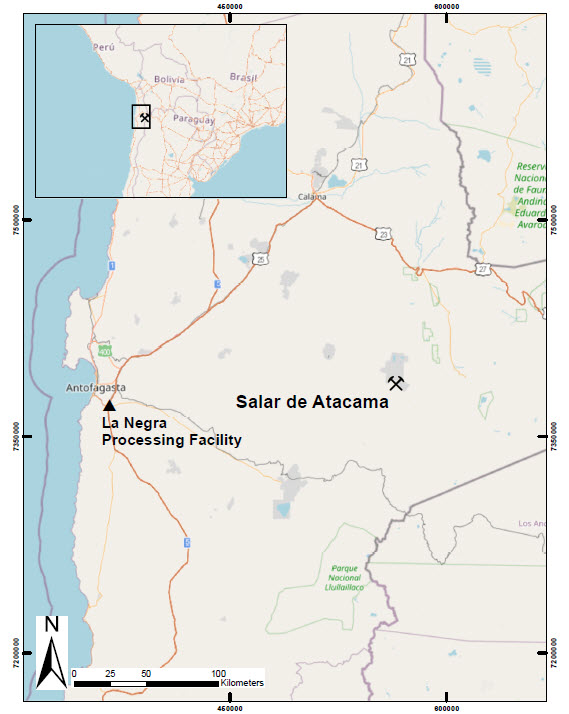

Salar de Atacama/La Negra, Chile

14

The Salar de Atacama is located in the commune of San Pedro de Atacama, with the operations approximately 100 kilometers to the south of this commune, in the extreme east of the Antofagasta Region and close to the border with the republics of Argentina and Bolivia. Access to the property is on the major four-lane paved Panamericana Route 5 north from Antofagasta, Chile approximately 60 km northeast to B-385. On B-385, a two-lane paved highway, the Albemarle Salar de Atacama project (latitude 23°38'31.52"S, longitude 68°19'30.31"W) is approximately 175 km to the east. The site has a small private airport that serves the project. A small paved runway airport is also located near San Pedro de Atacama and a large international airport is located in Antofagasta. The La Negra plant (latitude 23°45'20.31"S, longitude 70°18'36.92"W) has direct access roads and located approximately 20 km by paved four lane highway Route 28 southeast of Antofagasta turning north approximately 3 km on Route 5.

In the early 1960s, water with high concentrations of salts was discovered in the Salar de Atacama Basin. In January 1975, one of our predecessors, Foote Mineral Company, signed a long-term contract with the Chilean government for mineral rights with respect to the Salar de Atacama consisting exclusively of the right to access lithium brine, covering an area of approximately 16,700 hectares. See section 3 of the Salar de Atacama technical report summary, filed as Exhibit 96.3 to this report, for a listing of mining concessions at the Salar de Atacama site. The contract originally permitted the production and sale of up to 200,000 metric tons of lithium metal equivalent (“LME”), a calculated percentage of LCE. In 1981, the first construction of evaporation ponds in the Salar de Atacama began. The following year, the construction of the lithium carbonate plant in La Negra began. In 1990, the facilities at the Salar de Atacama were expanded with a new well system and the capacity of the lithium carbonate plant in the La Negra plant was expanded. In 1998, the lithium chloride plant in La Negra began operating, the same year that Chemetall purchased Foote Mineral Company. Subsequently, in 2004, Chemetall was acquired by Rockwood, and in 2015, Rockwood was acquired by Albemarle. Effective January 1, 2017, the Chilean government and Albemarle entered into an annex to the original agreement through which its duration was modified, extending it until the balance of: (a) the original 200,000 metric tons of LME and an additional 262,132 metric tons of LME granted through this annex have been exploited, processed, and sold, or (b) on January 1, 2044, whichever comes first. In addition, the amended agreement provides for commission payments to the Chilean government based on sales price/metric ton on the amounts sold under the additional quota granted, our support of research and development in Chile of lithium applications and solar energy,

15

and our support of local communities in Northern Chile. Albemarle currently operates its extraction and production facilities in Chile under this mineral rights agreement with the Chilean government.

The Salar de Atacama is a salt flat, the largest in Chile, located in the Atacama desert in northern Chile, which is the driest place on the planet and thus has an extremely high annual rate of evaporation and extremely low annual rainfall. Our extraction through evaporation process works as follows: snow in the Andes Mountains melts and flows into underground pools of water containing brine, which generally have high concentrations of lithium. We then pump the water containing brine above ground through a series of pumps and wells into a network of large evaporation ponds. Over the course of approximately eighteen months, the desert sun evaporates the water causing other salts to precipitate and leaving behind concentrated lithium brine. If weather conditions are not favorable, the evaporation process may be prolonged. After we obtain the lithium brine from the Salar de Atacama, we process it into lithium carbonate and lithium chloride at our manufacturing facilities in nearby La Negra, Chile.

The filling materials of the Salar de Atacama Basin are dominated by the Vilama Formation and the more recently, in geologic time, by evaporitic and clastic materials that are currently being deposited in the basin. These units house the basin's aquifer system and are composed of evaporitic chemical sediments that include carbonate, gypsum and halite intervals interrupted by volcanic deposits of large sheets of ignimbrite, volcanic ash and smaller classical deposits. Lithium-rich brines are extracted from the halite aquifer that is located within the nucleus of the salt flat. The Salar de Atacama basin contains a continental system of lithium-rich brine. These types of systems have six common (global) characteristics: arid climate; closed basin that contains a salt flat (salt crust), a salt lake, or both; igneous and/or hydrothermal activity; tectonic subsidence; suitable sources of lithium; and sufficient time to concentrate the lithium in the brine.

In the Salar de Atacama basin, lithium-rich brines are found in a halite aquifer. Carbonate and sulfates are found near the edges of the basin. The average, minimum and maximum concentrations of lithium in the Salar de Atacama basin are approximately 1,400, 900 and 7,000 mg/L, respectively. From 2017 through 2019, two drilling campaigns were carried out in order to obtain geological and hydrogeological information at the Albemarle mining concession.

The facilities at the Salar de Atacama consist of extraction wells, evaporation and concentration ponds, leaching plants, a potash plant, a drying plant, services and general areas, including salt stockpiles, as well as a fleet of owned and leased equipment. In addition, the site includes administrative offices, an operations building and a laboratory. The extracted concentrated lithium brine is sent to the La Negra plant by truck for processing. The Salar de Atacama has its own powerhouse that generates the energy necessary for the entire operation of the facilities. We also have permanent and continuous groundwater exploitation rights for two wells that are for industrial use and to supply the Salar de Atacama facilities. The La Negra facilities consist of a boron removal plant, a calcium and magnesium removal plant, two lithium carbonate conversion plants, a lithium chloride plant, evaporation-sedimentation ponds, an offsite area where the raw materials are housed and the inputs that are used in the process are prepared, a dry area where the various products are prepared, as well as a fleet of owned and leased equipment. La Negra is supplied electricity from a local company and has rights to a well in the Peine community for its water supply. We are currently constructing a third lithium carbonate conversion plant expected to be completed mid-2021, followed by a six-month commissioning and qualification process. We consider the condition of all of our plants, facilities and equipment to be suitable and adequate for the businesses we conduct, and we maintain them regularly. As of December 31, 2021, the combined gross asset value of our facilities at the Salar de Atacama and in La Negra, Chile (not inclusive of construction in process) was approximately $941.9 million.

A summary of the Salar de Atacama facility’s lithium mineral resources and reserves as of December 31, 2021 are shown in the following tables. This is the first period estimated mineral resources (exclusive of reserves) and reserves have been developed for Salar de Atacama. SRK served as the QP and prepared the estimates of lithium mineral resources and reserves at the Salar de Atacama facility, with an effective date of August 31, 2022. A copy of the QP’s amended technical report summary with respect to the lithium mineral resource and reserve estimates at the Salar de Atacama facility, dated December 16, 2022, is filed as Exhibit 96.3 to this report. Differences from the amounts in the technical report summary represent depletion since the effective date of the technical report summary until December 31, 2021. The amounts represent Albemarle’s attributable portion based on a 100% ownership percentage, and are presented as metric tonnes of lithium metal in thousands.

| Amount | Concentration (mg/L) | ||||||||||

| Measured mineral resources | 717 | 2,211 | |||||||||

| Indicated mineral resources | 642 | 1,747 | |||||||||

| Measured and Indicated mineral resources | 1,360 | 1,959 | |||||||||

| Inferred mineral resources | 131 | 1,593 | |||||||||

16

•Mineral resources are reported exclusive of mineral reserves. Mineral resources are not mineral reserves and do not have demonstrated economic viability.

•Given the dynamic reserve versus the static resource, a direct measurement of resources post-reserve extraction is not practical. Therefore, as a simplification, to calculate mineral resources, exclusive of reserves, the quantity of lithium pumped in the life of mine plan was subtracted from the overall resource without modification to lithium concentration. Measured and indicated resource were deducted proportionate to their contribution to the overall mineral resource.

•Resources are reported on an in-situ basis.

•Resources are reported between the elevations of 2,299 meters above mean sea level (“mamsl”) and 2,200 masl. Resources are reported as lithium metal.

•Resources have been categorized subject to the opinion of a QP based on the amount/robustness of informing data for the estimate, consistency of geological/grade distribution, survey information.

•Resources have been calculated using drainable porosity estimated from measured values in Upper Halite and volcanic, gypsum and clastic units, and bibliographical values based on the lithology and QP’s experience in similar deposits.

•The estimated economic cutoff grade utilized for resource reporting purposes is 670 mg/l lithium, based on the following assumptions:

◦A technical grade lithium carbonate price of $11,000/metric tonne CIF La Negra. This is a 10% premium to the price utilized for reserve reporting purposes. The 10% premium applied to the resource versus the reserve was selected to generate a resource larger than the reserve, ensuring the resource fully encompassed the reserve while still maintaining reasonable prospect for eventual economic extraction.

◦Recovery factors for the salar operation increase gradually over the span of four years, from the current 40% to the proposed Salar Yield Improvement Program (“SYIP”) 65% recovery in 2025. After that point, evaporation pond recovery is assumed constant at 65%, considering the installation of a liming plant is assumed in 2027. An additional recovery factor of 80% lithium recovery is applied to the La Negra lithium carbonate plant.

◦A fixed average annual brine pumping rate of 442 L/s is assumed, consistent with Albemarle’s permit conditions.

◦Operating cost estimates are based on a combination of fixed brine extraction, G&A and plant costs and variable costs associated with raw brine pumping rate or lithium production rate. Average life of mine operating cost is calculated at approximately $3,000/metric tonne CIF Asia.

◦Sustaining capital costs are included in the cutoff grade calculation and post the SYIP installation, average around $54 million per year.

◦Government royalties are excluded from the cutoff grade calculation as these costs are variable, depending upon price. A 3.5% community royalty is included in the cutoff grade as this royalty is fixed.

•Mineral Resources tonnage and contained metal have been rounded to reflect the accuracy of the estimate, and numbers may not add due to rounding.

| Amount | Concentration (mg/L) | ||||||||||

| Proven mineral reserves: | |||||||||||

| In Situ | 299 | 2,150 | |||||||||

| In Process | 24 | 2,685 | |||||||||

| Probable mineral reserves: | |||||||||||

| In Situ | 324 | 1,927 | |||||||||

| Total mineral reserves: | |||||||||||

| In Situ | 623 | 2,047 | |||||||||

| In Process | 24 | 2,685 | |||||||||

•In process reserves quantify the prior 24 months of pumping data and reflect the raw brine, at the time of pumping. These reserves represent the first 24 months of feed to the lithium process plant in the economic model.

•Proven reserves have been estimated as the lithium mass pumped during Years 2020 through 2030 of the proposed LoM plan.

•Probable reserves have been estimated as the lithium mass pumped from 2030 until the end of the proposed LoM plan (2041).

•Reserves are reported as lithium metal

•This mineral reserve estimate was derived based on a production pumping plan truncated in March 2042 (i.e., approximately 21 years). This plan was truncated to reflect the projected depletion of Albemarle’s authorized lithium production quota.

•The estimated economic cutoff grade for the Project is 783 mg/L lithium, based on the assumptions discussed below. The truncated production pumping plan remained well above the economic cutoff grade (i.e., the economic cutoff grade did not result in a limiting factor to the estimation of the reserve).

◦A technical grade lithium carbonate price of $10,000/metric tonne CIF Asia.

◦Recovery factors for the salar operation increase gradually over the span of 4 years, from the current 40% to the proposed SYIP 65% recovery in 2025. After that point, evaporation pond recovery is assumed constant at 65%, considering the installation of a liming plant is assumed in 2027. An additional recovery factor of 80% lithium recovery is applied to the La Negra lithium carbonate plant.

◦A fixed average annual brine pumping rate of 442 L/s is assumed, consistent with Albemarle’s permit conditions.

◦Operating cost estimates are based on a combination of fixed brine extraction, G&A and plant costs and variable costs associated with raw brine pumping rate or lithium production rate. Average life of mine operating cost is calculated at approximately $3,000/metric tonne CIF Asia.

17

◦Sustaining capital costs are included in the cutoff grade calculation and post the SYIP installation, average around $54M per year.

◦Government royalties are excluded from the cutoff grade calculation as these costs are variable, depending upon price. A 3.5% community royalty is included in the cutoff grade as this royalty is fixed.

•Mineral reserve tonnage, grade and mass yield have been rounded to reflect the accuracy of the estimate and numbers may not add due to rounding.

Key assumptions and parameters relating to the lithium mineral resources and reserves at the Salar de Atacama facility are discussed in sections 11 and 12, respectively, of the Salar de Atacama technical report summary.

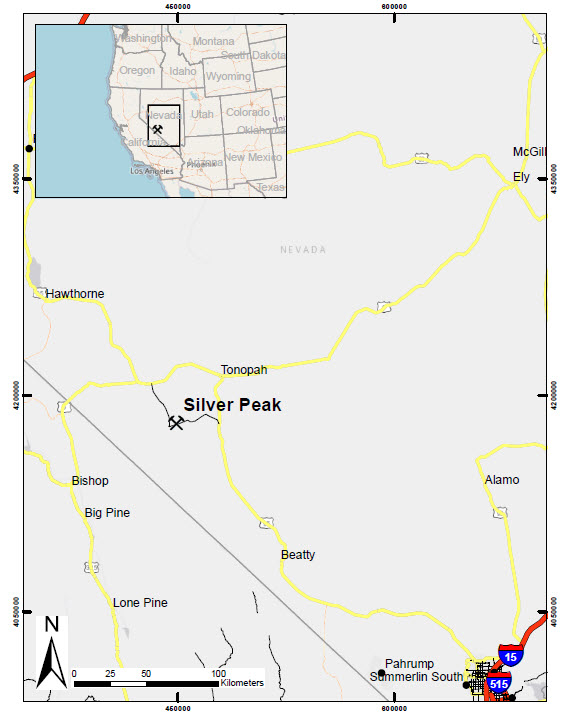

Silver Peak, Nevada

The Silver Peak site (latitude 37.751773°N, longitude 117.639027°W) is located in a rural area approximately 30 miles southwest of Tonopah, in Esmeralda County, Nevada. It is located in the Clayton Valley, an arid valley historically covered with dry lake beds (playas). The operation borders the small unincorporated town of Silver Peak, Nevada. Albemarle uses the Silver Peak site for the production of lithium brines, which are used to make lithium carbonate and, to a lesser degree, lithium hydroxide. Access to the site is off of the paved highway SR-265 in the town of Silver Peak, Nevada. The administrative offices are located on the south side of the road. The process facility is on the north side of the road and the brine operations are located approximately three miles east of Silver Peak on Silver Peak Road and occupy both the north and south sides of the road. In addition, access to the site is also possible via gravel/dirt roads from Tonopah, Nevada and Goldfield, Nevada.

Lithium brine extraction in the Clayton Valley began in the mid-1960’s by one of our predecessors, the Foote Mineral Company. Since that time, lithium brine operations have been operated on a continuous basis. In 1998, Chemetall purchased Foote Mineral Company. Subsequently, in 2004, Chemetall was acquired by Rockwood, and in 2015, Rockwood was acquired by Albemarle. Our mineral rights in Silver Peak consist of our right to access lithium brine pursuant to our permitted and certified senior water rights, a settlement agreement with the U.S. government, originally entered into in June 1991, and our patented and unpatented land claims. Pursuant to the 1991 agreement, our water rights and our land claims, we have rights to all

18

lithium that we can remove economically from the Clayton Valley Basin in Nevada. See section 3 of the Silver Peak technical report summary, filed as Exhibit 96.4 to this report, for a listing of patented and unpatented claims at the Silver Peak site. We have been operating at the Silver Peak site since 1966. Our Silver Peak site covers a surface of over 13,500 acres, more than 10,500 acres of which we own through a subsidiary. The remaining acres are owned by the U.S. government from whom we lease the land pursuant to unpatented land claims that are renewed annually. Actual surface disturbance associated with the operations is 7,390 acres, primarily associated with the evaporation ponds. The manufacturing and administrative activities are confined to an area approximately 20 acres in size.

We extract lithium brine from our Silver Peak site through substantially the same evaporation process we use at the Salar de Atacama. We process the lithium brine extracted from our Silver Peak site into lithium carbonate at our plant in Silver Peak. It is hypothesized that the current levels of lithium dissolved in brine originate from relatively recent dissolution of halite by meteoric waters that have penetrated the playa in the last 10,000 years. The halite formed in the playa during the aforementioned climatic periods of low precipitation and that the concentrated lithium was incorporated as liquid inclusions into the halite crystals. There are no current exploration activities on the Silver Peak lithium operation. However, in January 2021, we announced that we will expand capacity in Silver Peak and begin a program to evaluate clays and other available Nevada resources for commercial production of lithium. Beginning in 2021, we plan to invest $30 million to $50 million to double the current production in Silver Peak by 2025, with the aim of making full use of the brine water rights.

The facilities at Silver Peak consist of extraction wells, evaporation and concentration ponds, a lithium carbonate plant, a lithium anhydrous plant, a lithium hydroxide plant, a liming plant, wellfield and mill maintenance, a shipping and packaging facility and administrative offices, as well as a fleet of owned and leased equipment. Silver Peak is supplied electricity from a local company and we currently have two operating fresh water wells nearby that supply water to the facilities. We consider the condition of all of our plants, facilities and equipment to be suitable and adequate for the businesses we conduct, and we maintain them regularly. As of December 31, 2021, the gross asset value of our facilities at our Silver Peak site was approximately $60.8 million.

A summary of the Silver Peak facility’s lithium mineral resources and reserves as of December 31, 2021 are shown in the following tables. This is the first period estimated mineral resources and reserves have been developed for Silver Peak. SRK served as the QP and prepared the estimates of lithium mineral resources (exclusive of reserves) and reserves at the Silver Peak facility, with an effective date of June 30, 2021. A copy of the QP’s amended technical report summary with respect to the lithium mineral resource and reserve estimates at the Silver Peak facility, dated December 16, 2022, is filed as Exhibit 96.4 to this report. Differences from the amounts in the technical report summary represent depletion since the effective date of the technical report summary until December 31, 2021. The amounts represent Albemarle’s attributable portion based on a 100% ownership percentage, and are presented as metric tonnes of lithium metal in thousands.

| Amount | Concentration (mg/L) | ||||||||||

| Measured mineral resources | 10 | 152 | |||||||||

| Indicated mineral resources | 25 | 143 | |||||||||

| Measured and Indicated mineral resources | 35 | 145 | |||||||||

| Inferred mineral resources | 63 | 121 | |||||||||

•Mineral resources are reported exclusive of mineral reserves. Mineral resources are not mineral reserves and do not have demonstrated economic viability.

•Given the dynamic reserve versus the static resource, a direct measurement of resources post-reserve extraction is not practical. Therefore, as a simplification, to calculate mineral resources, exclusive of reserves, the quantity of lithium pumped in the LoM plan was subtracted from the overall resource without modification to lithium concentration. Measured and indicated resource were deducted proportionate to their contribution to the overall mineral resource.

•Resources are reported on an in situ basis.

•Resources are reported as lithium metal.

•Resources have been categorized subject to the opinion of a QP based on the amount/robustness of informing data for the estimate, consistency of geological/grade distribution, survey information.

•Resources have been calculated using drainable porosity estimated from bibliographical values based on the lithology and QP’s experience in similar deposits.

•The estimated economic cutoff grade utilized for resource reporting purposes is 50 mg/L lithium, based on the following assumptions:

◦A technical grade lithium carbonate price of $11,000/metric tonne CIF North Carolina. This is a 10% premium to the price utilized for reserve reporting purposes. The 10% premium applied to the resource versus the reserve was selected to generate a resource larger than the reserve, ensuring the resource fully encompassed the reserve while still maintaining reasonable prospect for eventual economic extraction.

19

◦Recovery factors for the wellfield are = -206.23*(Li wellfield feed)2 +7.1903*(wellfield Li feed)+0.4609. An additional recovery factor of 85% lithium recovery is applied to the lithium carbonate plant.

◦A fixed brine pumping rate of 20,000 acre feet per year (“afpy”), ramped up from current levels over a period of five years.

◦Operating cost estimates are based on a combination of fixed brine extraction, G&A and plant costs and variable costs associated with raw brine pumping rate or lithium production rate. Average life of mine operating costs is calculated at approximately $4,900/metric tonne lithium carbonate CIF North Carolina.

◦Sustaining capital costs are included in the cutoff grade calculation and include a fixed component at $2.5 million per year and an additional component tied to the estimated number of wells replaced per year.

•Mineral resources tonnage and contained metal have been rounded to reflect the accuracy of the estimate, and numbers may not add due to rounding.

| Amount | Concentration (mg/L) | ||||||||||

| Proven mineral reserves: | |||||||||||

| In Situ | 11 | 87 | |||||||||

| In Process | 1 | 103 | |||||||||

| Probable mineral reserves: | |||||||||||

| In Situ | 49 | 83 | |||||||||

| Total mineral reserves: | |||||||||||

| In Situ | 60 | 84 | |||||||||

| In Process | 1 | 103 | |||||||||

•In process reserves quantify the prior 24 months of pumping data and reflect the raw brine, at the time of pumping. These reserves represent the first 24 months of feed to the lithium process plant in the economic model.

•Proven reserves have been estimated as the lithium mass pumped during Years 2021 through 2026 of the proposed LoM plan.

•Probable reserves have been estimated as the lithium mass pumped from 2026 until the end of the proposed LoM plan (2050).

•Reserves are reported as lithium metal.

•This mineral reserve estimate was derived based on a production pumping plan truncated at the end of year 2050 (i.e., approximately 29.5 years). This plan was truncated to reflect the QP’s opinion on uncertainty associated with the production plan as a direct conversion of measured and indicated resource to proven and probable reserve is not possible in the same way as a typical hard-rock mining project.

•The estimated economic cutoff grade for the Silver Peak project is 56 mg/L lithium, based on the assumptions discussed below. The production pumping plan was truncated due to technical uncertainty inherent in long-term production modelling and remained well above the economic cutoff grade (i.e., the economic cutoff grade did not result in a limiting factor to the estimation of the reserve).

◦A technical grade lithium carbonate price of $10,000/metric tonne CIF North Carolina.

◦Recovery factors for the wellfield are = -206.23*(Li wellfield feed)2 +7.1903*(wellfield Li feed)+0.4609. An additional recovery factor of 85% lithium recovery is applied to the lithium carbonate plant.

◦A fixed brine pumping rate of 20,000 afpy, ramped up from current levels over a period of five years.

◦Operating cost estimates are based on a combination of fixed brine extraction, G&A and plant costs and variable costs associated with raw brine pumping rate or lithium production rate. Average life of mine operating costs is calculated at approximately $5,100/metric tonne lithium carbonate CIF North Carolina.

◦Sustaining capital costs are included in the cutoff grade calculation and include a fixed component at $2.5 million per year and an additional component tied to the estimated number of wells replaced per year.

•Mineral reserve tonnage, grade and mass yield have been rounded to reflect the accuracy of the estimate (thousand tonnes), and numbers may not add due to rounding.

Key assumptions and parameters relating to the lithium mineral resources and reserves at the Silver Peak facility are discussed in sections 11 and 12, respectively, of the Silver Peak technical report summary.

20

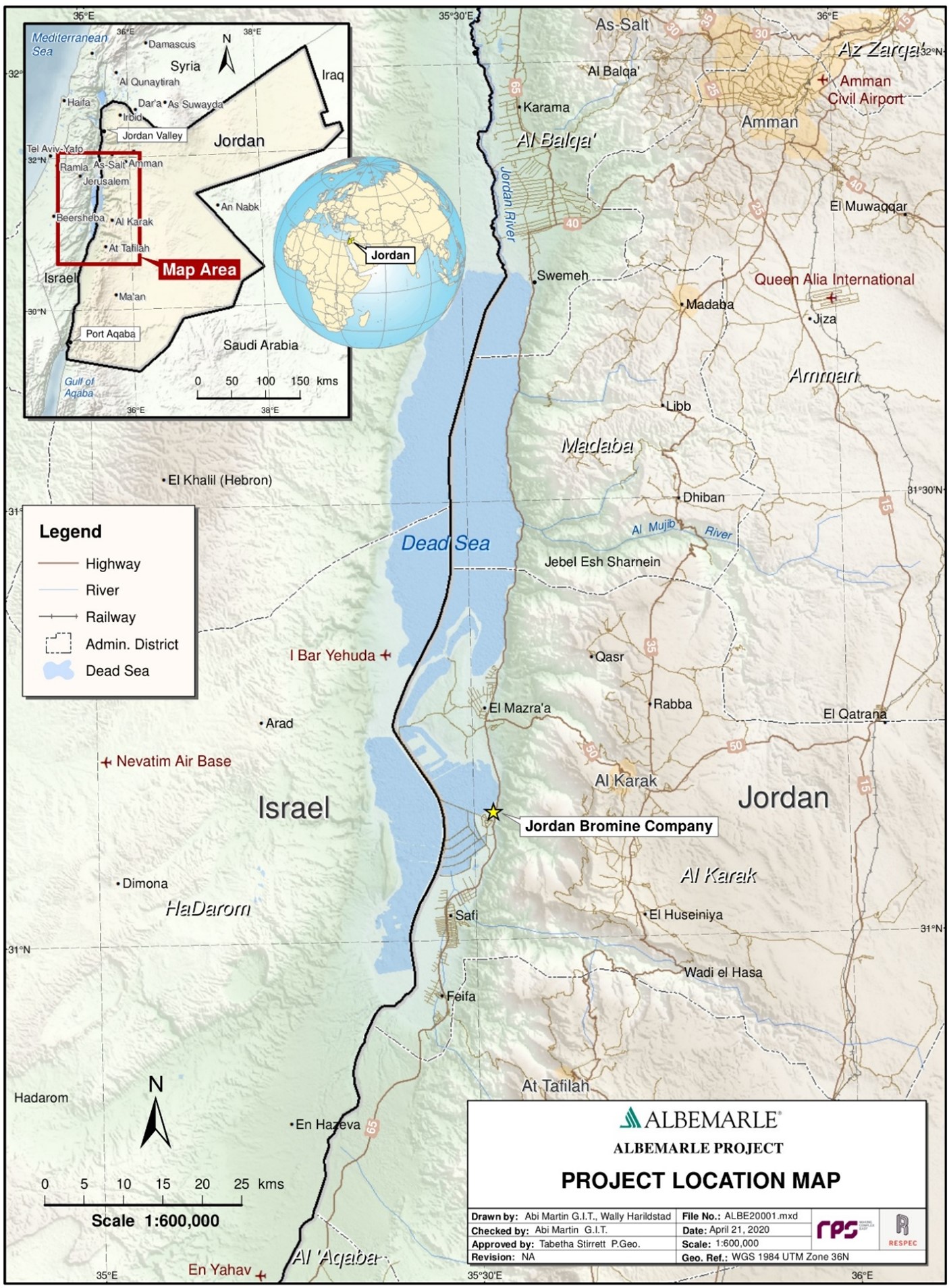

Safi, Jordan

Our 50% interest in JBC, a consolidated joint venture established in 1999, with operations in Safi, Jordan, acquires bromine that is originally sourced from the Dead Sea. JBC processes the bromine at its facilities into a variety of end products. The JBC operation (latitude 31°8'34.85"N , longitude 35°31'34.68"E) is located in Safi, Jordan, and is located on a 26-ha area on the southeastern edge of the Dead Sea, about 6 kilometers north of the of the APC plant. JBC also has a 2-hectare storage facility within the free-zone industrial area at the Port of Aqaba. The Jordan Valley Highway/Route 65 is the primary method of access for supplies and personnel to JBC. The Port of Aqaba is the main entry point for supplies and equipment for JBC, where imported shipping containers are offloaded from ships and are transported by truck to JBC via the Jordan Valley Highway. Aqaba is approximately 205 km south of JBC via Highway 65. Major international airports can be readily accessed either at Amman or Aqaba. Jordan’s railway transport runs north-south through Jordan and is not used to transport JBC employees and product.

In 1958, the Government of the Hashemite Kingdom of Jordan granted APC a concession for exclusive rights to exploit the minerals and salts from the Dead Sea brine until 2058; at that time, APC factories and installations would become the property of the Government. APC was granted its exclusive mineral rights under the Concession Ratification Law No. 16 of 1958. APC produces potash from the brine extracted from the Dead Sea. A concentrated bromide-enriched brine extracted from APC’s evaporation ponds is the feed material for the JBC plant. Following the formation of the joint venture, the JBC bromine plant began operations in 2002. Expansion of the facilities to double its bromine production capacity went into operation in 2017.

The climate, geology and location provide a setting that makes the Dead Sea a valuable large-scale natural resource for potash and bromine. Today, the Dead Sea has a surface area of 583 km2 and a brine volume of 110 km3. The Dead Sea is the world’s saltiest natural lake, containing high concentrations of ions compared to that of regular sea water and an unusually high amount of magnesium and bromine. There is an estimated 900 million tonnes of bromine in the Dead Sea.

21