Form 10-K Vintage Wine Estates, For: Jun 30

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number

(Exact name of registrant as specified in its charter)

|

|

|

||

(State or other jurisdiction of incorporation or organization) |

|

|

|

(I.R.S. Employer Identification No.) |

______________________________

(Address of principal executive offices)

Registrant’s telephone number, including area code: (

______________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer.” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

☒ |

Smaller reporting company |

||

|

|

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of December 31, 2020, the last business day of the registrant's most recently completed second fiscal quarter, was approximately $

As of October 1, 2021,

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this Report, to the extent not set forth herein, is incorporated herein by reference from the registrant’s definitive proxy statement relating to the registrant's next Annual Meeting of Stockholders (the "Proxy Statement"). The Proxy Statement, or an amendment to this Report, shall be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Report relates.

TABLE OF CONTENTS

1 |

||

|

1 |

|

Item 1. |

1 |

|

Item 1A. |

10 |

|

Item 1B. |

19 |

|

Item 2. |

19 |

|

Item 3. |

20 |

|

Item 4. |

21 |

|

|

|

|

|

22 |

|

Item 5. |

22 |

|

Item 6. |

23 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

24 |

Item 7A. |

38 |

|

Item 8. |

40 |

|

Item 9. |

80 |

|

Item 9A. |

80 |

|

|

|

|

|

82 |

|

Item 10. |

82 |

|

Item 11. |

82 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

82 |

Item 13. |

Certain Relationships and Related Transactions and Director Independence |

82 |

Item 14. |

82 |

|

|

|

|

|

83 |

|

Item 15. |

83 |

|

Item 16. |

87 |

|

88 |

||

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Investors are cautioned that statements that are not strictly historical statements of fact constitute forward-looking statements, including, without limitation, statements under the captions “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business” and are identified by words like “believe,” “expect,” “may,” “will,” “should,” “seek,” “anticipate,” or “could” and similar expressions.

Forward-looking statements are not assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in the forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those expressed or implied by forward-looking statements include those discussed under the heading “Item 1A. Risk Factors” as well as those discussed elsewhere in this Annual Report on Form 10-K and in future Quarterly Reports on Form 10-Q or other reports filed with the Securities and Exchange Commission ("SEC").

Any forward-looking statement made by us in this report is based only on information currently available to us and speaks only as of the date of this report. We undertake no obligation to publicly revise or update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

References to a fiscal year refer to our fiscal year ended June 30 of the specified year.

Part I.

Item 1. Business

Our Company

Vintage Wine Estates, Inc. (“VWE”, “we”, “us”, "our" or “the Company”) is a leading vintner in the United States ("U.S."), offering a collection of wines produced by award-winning, heritage wineries, popular lifestyle wines, innovative new wine brands, packaging concepts, as well as craft spirits. Our name brands include Layer Cake, Cameron Hughes, Clos Pegase, B.R. Cohn, Firesteed, Bar Dog, Kunde, Cherry Pie and many others. Since our founding over 20 years ago, we have grown organically through wine brand creation and through acquisitions to become the 15th largest wine producer based on cases of wine shipped in California. We’ve exceeded 20% net revenue and adjusted EBITDA compound annual growth rates since 2010. We now sell nearly 2 million cases annually.

Our key differentiator is our diversification—what we call our three-legged stool business model.

We are diversified in our brand collection, producing over 50 brands ranging in retail price from $10 to $150, with a focus on the growing segment between $10 and $20. Eighty percent of our business is done in this critical segment.

We are diversified in our omni-channel sales strategy balanced between direct-to-consumer, 30% of sales, traditional wholesale, 33% of sales and business-to-business at 35% of sales. Our direct-to-consumer segment is particularly robust. Where most wine companies have two direct sales levers to pull: tasting rooms and wine clubs, we have six: tasting rooms, wine clubs, ecommerce, Cameron Hughes, Windsor/custom label design and engraving, and QVC/HSN.

We are diversified in our sourcing with a strong asset base of 2,800 owned and leased vineyard acres located in the premier winegrowing regions of the U.S. and 10 owned winery estates. These properties extend from the Central Coast of California to storied appellations in Napa Valley and Sonoma County, north to Oregon and Washington. We obtain fruit for our wines from owned and leased vineyards, as well as other sources, including independent growers and the spot wine market.

Vintage Wine Estates has completed over 20 acquisitions in the past 10 years and completed over 10 acquisitions in the past 5 years. We generally acquire the brands and inventories of a targeted business, eliminating redundant corporate overhead. We then integrate the acquired assets into our highly efficient production, distribution and omni channel selling networks, quickly increasing the sales and margins of the acquired business.

Our growth has allowed us to reinvest in our business and create the scale and infrastructure needed to successfully manage a variety of different wine brands and channels and reduce costs. Our owned winery facilities have the current capacity to produce up to 7 million cases of wine per year. We are in the process of completing a $45 million investment into our Ray’s Station production facility, which includes a high-speed bottling facility with the capacity to bottle over 13.5 million cases annually and a 364,000 square foot warehouse and distribution center. This project will be complete at the end of Q1 FY 22.

1

Additional bottling capacity will not only be used for our products, but also will allow us to further expand our bottling and fulfillment services offered to third parties on a contract basis. The additional capacity of the bottling facility may not initially be fully utilized but provides us with capacity consistent with our growth plans. Our scale and consolidated operations are expected to enable us to increase margins of the businesses that we acquire, providing accretive value promptly after the acquisition. We intend to continue to grow our business organically and through acquisitions, with a view towards making two to three acquisitions per year over the next five years.

Our acquisition strategy is to acquire brands and inventories while eliminating redundant corporate overhead, increasing gross margins of the acquired businesses by leveraging scale economies, and driving revenue growth through our distribution network. Gross margins improve by incorporating brands into a more efficient operating system. In addition, operating margins improve from synergies of acquisitions.

There are more than 11,000 wineries in the U.S., with the largest 50 wineries controlling approximately 90% of the market share by volume, but less than 60% of consumer spending. We plan to use our financial capacity to: (i) continue to acquire family-owned brands from small wineries, (ii) acquire non-core brands from medium sized and large competitors, and (iii) potentially acquire one or more large businesses in our industry.

Our primary unique selling proposition for a seller is that we have a strong track record of closing once the price and structure are agreed upon. We also believe our managers are perceived as excellent brand stewards, having increased the market share and profitability of virtually all of our acquired brands. We intend to be a disciplined acquirer, exercising cost discipline, with a focus on the industry’s growth in premium and super-premium wines. We expect that the fragmented nature of the wine industry, coupled with our infrastructure and experience, will enable us to continue to gain market share.

Our innovation strategy is focused on creating and building new wine brands for today’s wine consumer. In the past five years, we have launched over 15 new wine brands, which are primarily sold to major national retail accounts and through direct-to-consumer channels. We also develop private labels and produce wine for major retail clients, including Costco and Target, to sell as proprietary brands. The ability to create new wine brands and quickly bring them to market allows us to respond swiftly to trends and changing consumer tastes and needs.

Our mission is to maintain an entrepreneurial spirit, stay humble and focus on the customer. We respect the ways people buy wine—at the estate wineries, at retail, in restaurants, on the telephone, on the internet, on television and by mail.

Our Business Combination

We were formed in 2019 as Bespoke Capital Acquisition Corp. (“BCAC”), a special purpose acquisition corporation incorporated under the laws of the Province of British Columbia. BCAC was organized for the purpose of effecting an acquisition of one or more businesses or assets by way of a merger, amalgamation, share exchange, asset acquisition, share purchase, reorganization or any other similar business combination involving BCAC.

On June 7, 2021, BCAC consummated its business combination (the “Business Combination”) with Vintage Wine Estates, Inc., a California corporation ("Legacy VWE"), pursuant to a transaction agreement dated February 3, 2021. As a result of the Business Combination and the related transactions, BCAC changed its jurisdiction of incorporation from the Province of British Columbia to the State of Nevada, BCAC changed its name to “Vintage Wine Estates, Inc.” and Legacy VWE became our wholly-owned subsidiary.

For accounting purposes, and in accordance with generally accepted accounting principles, BCAC was treated as the acquired company and Legacy VWE was treated as the acquirer.

Core Business Segments

We report our results of operations through the following segments: Wholesale, Business-to-Business ("B2B"), Direct-to-Consumer ("DTC") and Other.

Fundamentally, we are an omni-channel consumer goods business that happens to operate in the wine industry. Unlike wine companies that solely or mainly sell to wholesale distributors, we sell our products through a number of different channels.

A description of our segments follows:

Wholesale

Our wholesale operations generate revenue from products sold to distributors, who then sell them to off-premise retail locations such as grocery stores, specialty and multi-national retail chains, as well as on-premise locations such as restaurants and bars.

We have longstanding relationships with our distribution network and marketing companies, including with industry leaders such as Deutsch Family Wine and Spirits, Republic National Distributing Company and Southern Glazer’s Wine & Spirits. Through these relationships, our products are sold in all 50 states and in 37 countries outside the U.S. In addition to our geographical reach, our products are available for purchase at 34,500 off-premise locations as of June 30, 2021 including leading national chains such as Costco, Kroger, Target, Albertsons and Total Wine & More. Our products were also sold at 17,657 restaurants and bars as of June 30, 2021.

2

Our wholesale segment generated $72.9 million and $75.4 million of revenue for the fiscal years ended June 30, 2021 and June 30, 2020, respectively.

Business-to-Business

Our B2B sales segment generates revenue from the sale of private label wines and custom winemaking services.

We work with national retailers, including Costco, Albertsons, Target and other major retailers, to provide private label wines incremental to their existing beverage alcohol business. Retailers generally earn higher margins on sales of their private label wines than on sales of third-party wines. Consequently, retailers are increasingly offering more private label products in their stores. We expect retailers’ demand for private labels to continue to increase and believe that our private label business will continue to grow. Retailers frequently request brand, label and product line extensions.

Our custom winemaking services are governed by long-term contracts with other wine industry participants and include services such as fermentation, barrel aging, procurement of dry goods, bottling and cased goods storage. Additionally, we believe that our custom winemaking services business allows us to maximize our production assets’ throughput and efficiency and thus improves profit margins for our proprietary brands.

Our B2B segment generated $77.4 million and $54.1 million of revenue for the fiscal years ended June 30, 2021 and June 30, 2020, respectively.

Direct-to-Consumer

Our DTC segment generates revenue from sales made directly to the consumer. DTC sales have higher gross profit margins than wholesale sales because DTC sales allow us to capture the profit margin that otherwise would go to our distribution partners on sales in the wholesale segment. As a result, our profit margins in the DTC segment are significantly higher than in our other segments while operating margins are consistent with other segments. We believe that our DTC business is one of the largest in the U.S. wine industry.

Our DTC sales are made primarily through our tasting rooms, wine clubs and e-commerce.

Tasting Rooms — We currently operate 14 tasting rooms that served over 135,000 visitors during the fiscal year ended June 30, 2021, down from over 188,000 for the fiscal year ended June 30, 2020 due to the effects of the COVID-19 pandemic. We expect that, after there has been availability and public acceptance of effective COVID-19 vaccines and travel restrictions have been lifted, tasting room volumes will, over time, increase from the current lows. Our tasting rooms are designed to provide a welcoming atmosphere where we can introduce the consumer to our brands with a view towards developing an authentic relationship over time. These tasting rooms feature our exclusive, low-production wines, at higher-than-average price points, as well as our more accessible, higher-production, wines. Visitors are encouraged to taste, and then purchase, our wines.

Wine Clubs — We currently offer 26 branded wine clubs and had more than 35,000 wine club members as of June 30, 2021. Our wine club members sign up to purchase regular shipments of our wines and receive additional benefits such as volume discounts, exclusive visits to our tasting rooms, invitations to member-only events, access to winemakers and the ability to try each of our wines before they are widely sold in stores. We leverage digital technology through virtual tastings and mixers, giving members new ways to network with one another.

E-Commerce — Sales through our various brand websites are a growing part of DTC sales. We have an active email list with over 859,000 subscribers. Our digital marketing team drafted and sent over 5,200 unique emails that generated over 64 million impressions for the fiscal year ended June 30, 2021. We have used digital marketing since the early 2000s, recently increasing our e-commerce customer conversion rate to 9.3%, which is substantially above the food and drink industry’s e-commerce conversion rate of 1.7%, as of August 2021.

Custom Label Design and Engraving — We also offer custom label design and engraving services whereby customers can design and engrave wine bottles to their specifications. We believe that we are the only wine producer with the ability to do custom engraving on wine bottles. As a result, we are able to offer our services profitably at a lower price than competitors that need to outsource bottle engraving. In addition to our core private label customers, we have created custom bottles for weddings, major corporate events and other promotional opportunities.

Our DTC segment generated $66.6 million and $55.6 million of revenue for the fiscal years ended June 30, 2021 and June 30, 2020, respectively.

Other

Our Other segment generates revenue from grape and bulk sales, storage services and for the year ended June 30, 2020, revenue under the Sales Pro and Master Class business line sold in 2019. We record corporate level expenses, non-direct selling expenses and other expenses not specifically allocated to the results of operations in our Other segment.

Our Other segment generated $3.8 million and $4.8 million of revenue for the years ended June 30, 2021 and 2020, respectively.

Our Diversified Portfolio

Our asset base and product portfolio have been strategically built to provide significant flexibility throughout the business cycle. Our wine portfolio has three tiers: lifestyle brands, luxury brands, and digitally native brands. We also produce and sell craft spirits.

3

Lifestyle Brands

Our lifestyle wines primarily sell through off-premise channels at retail prices ranging from $10.00 to $25.00 per bottle. The lifestyle tier accounts for more of our branded case volume than the luxury tier due to the lifestyle tier’s wider distribution and lower pricing. Our lifestyle brands are designed to deliver a compelling price-to-quality ratio. We believe our infrastructure, sourcing network and bottling-on-demand capabilities allow us to adjust production in line with market demand.

Our lifestyle brands include the following, among others:

Layer Cake — Layer Cake is a vintage-dated, premium wine brand featuring Cabernet Sauvignon, Pinot Noir and Chardonnay and other varietals sourced from various vineyards from around the world. The wines are designed to be approachable and food-friendly, with layers of flavor. Layer Cake is distributed nationally, at retail prices between $11.99 and $19.99 per bottle.

Firesteed — Founded in 1982, Firesteed is one of Oregon’s most recognized wine marques, well-known as an award-winning, high scoring top Pinot Noir producer. Located in Oregon’s Willamette Valley and considered a foundation brand for Oregon Pinot Noir, Firesteed serves the growing interest in and demand for authentic, cool-climate Oregon Pinot Noir. The signature wine, Firesteed Pinot Noir, is notably 100% Pinot Noir, with no blending wines added to alter the pure varietal character. Recognizing the appeal and demand for Oregon Pinot Noir, Firesteed is one of our top retail sales priorities. Firesteed wines are also available for sale DTC through our e-commerce channel and wine club. Firesteed wines sell at retail prices between $16.00 and $40.00 per bottle.

Bar Dog — Bar Dog is vintage-dated, premium California wine, including Chardonnay, Cabernet Sauvignon and Pinot Noir varietals, along with Red Blend. Bar Dog launched as a first-to-market brand in Target stores in 2019 and now is distributed nationally with significant room to be distributed further. Bar Dog’s Cabernet Sauvignon has earned 94 points from the Toronto International Wine Competitions, its Red Wine and Chardonnay have earned Gold Medals, and its Pinot Noir has earned a Silver Medal from the San Francisco International Wine Competition. These wines sell at retail prices between $12.00 and $20.00 per bottle.

Middle Sister — Middle Sister is a non-vintage, premium California wine. The star of the “sisters” is Middle Sister Sweet & Savvy, the top-selling California Moscato in the United States, featuring a sister of color on the label. Middle Sister is a longstanding lifestyle brand, launched over 15 years ago in Target stores. It enjoys strong brand equity with a devoted consumer base. Middle Sister was the first wine label to feature a cast of stick figure characters on the label, engaging consumers in a novel, cheeky and humorous way. Middle Sister also was one of the early wine industry adopters of social media, having launched at the same time that Facebook was becoming a widely-used consumer platform. Middle Sister wines sell at a retail price of $10.00 per bottle.

Cherry Pie — Cherry Pie wines are a vintage, premium California wine. These wines are 100% Pinot Noir sourced from select, cooler climate vineyards in Northern California and the Central Coast that highlight the variety. These wines sell at a retail prices between $20.00 and $50.00 per bottle.

Cartlidge & Browne — Cartlidge & Browne is a legacy, premium California wine brand founded in 1980. Cartlidge & Brown wines appeals to consumers looking for quality and value. The brand continues to grow on the strength of longstanding trust in the wine quality and its appealing price point, with national distribution in retail chains, independent retailers and on-premise. Cartlidge & Brown wines sell at a retail price of $12.00 per bottle.

GAZE Wine Cocktails — GAZE Wine Cocktails are refreshing, light, low-alcohol blends of Green Tea Moscato, Blueberry Pomegranate Moscato and White Peach Moscato. GAZE Wine Cocktails blend quality California wine with natural ingredients popular with wellness-minded consumers. The GAZE package is a sleek, portable, recyclable aluminum bottle with a resealable twist-off closure and bright, fashion-forward silkscreened graphics. The Blueberry Pomegranate Moscato flavor was awarded 94 points and a Double Gold award at the 2019 San Francisco International Wine Competition. A case of six GAZE Wine Cocktails sells at a retail price of $36.00.

Luxury Brands

Our super-premium to ultra-premium wines are generally smaller-production, estate-based wines. We also have a tier of more widely sourced and available appellation wines. Our luxury wines consistently garner 90+ scores, awards and accolades from top wine industry publications. They appeal to the wine aficionado who is intensely interested in the winemaker’s craft, the influence that vineyards and sites have on the wine, and the details of the vintage from budbreak to bottle.

Our luxury brands sell primarily at wine retailers, on-premise and through wine clubs and tasting rooms at prices ranging from $16.00 to $150.00 per bottle.

Our luxury brands include the following:

Girard — Girard is a super-premium brand founded more than forty years ago. Girard wines use small batch fermentation techniques and classic blending techniques, which have consistently produced award-winning wines. Girard's tasting room room and production facility are in Calistoga, located in the northern end of Napa Valley, attraction for both tourists and wine collectors. Girard wines are offered in high-end grocery stores and

4

restaurants, as well as in the tasting rooms and other e-commerce channels. Girard wines sell through wholesale, e-commerce, wine clubs and at the winery, at retail prices between $18.00 and $100.00 per bottle.

Clos Pegase — Clos Pegase is one of the best known assets in our luxury portfolio. Renowned architect Michael Graves submitted a neo-classical design for this winery to an international competition and was awarded the commission. The winery was completed in 1987 and has been recognized as one of the world’s great winery buildings. The winery features extensive caves for the cellaring and aging of wines and a drought-tolerant heritage garden. A companion winery house was completely restored to the original vision in 2019. In keeping with the high aesthetics of the winery, Clos Pegase wines are a benchmark for Napa Valley luxury wines. Two estate vineyards in the Calistoga American Viticultural Area (“AVA”) for Bordeaux varietal red wines, Applebone and Tenma, and Mitsuko’s Vineyard in the Carneros AVA for Pinot Noir. Chardonnay and other varieties produce world-class, award-winning wines. Clos Pegase wines are distributed nationally at wholesale and at the winery, and through e-commerce and wine clubs, selling at retail prices between $22.00 and $125.00 per bottle.

Laetitia Vineyard and Winery — The Laetitia estate, located approximately three miles from the Pacific Ocean in Arroyo Grande on California’s south-central coast, is a well-known name in California’s sparkling wine market. The 1,800-acre estate was founded as a sparkling wine producer in the 1980s, as the cooler climate, site and soils resembled those in the Champagne region of France. Laetitia has earned a reputation as a top California sparkling wine producer and continues to make a range of luxury sparkling wines, as well as Pinot Noir and Chardonnay varietals and Rhône-style wines. All Laetitia wines currently in wholesale distribution have scores of 90 points or higher from leading wine publications. The winery is a popular wine tourism destination, where guests can enjoy views of the vineyards and the Pacific Ocean as they enjoy the wines. Laetitia also features a private winery guest house for trade and media hospitality. Laetitia wines are sold at wholesale, the tasting room, wine clubs and e-commerce at retail prices between $24.00 and $65.00 per bottle.

Swanson Vineyards — In Napa Valley, Swanson Vineyards is strongly associated with Merlot. Founded in 1995 in the Rutherford AVA (generally better recognized for Cabernet Sauvignon), it was determined that Swanson’s site and soils resembled those of Château Pétrus in Bordeaux, France. We believe Swanson offered Napa Valley its first luxury wine tasting experience when it opened the Salon in 2001. Swanson Vineyards wines are distributed through wholesale, e-commerce and wine clubs at retail prices between $21.00 and $140.00 per bottle.

Kunde Family Winery — The Kunde Family Winery was established in 1904 and celebrated its 117th harvest in 2020. Kunde sources grapes from the Kunde family’s 1,800-acre sustainable vineyard and winery, which is the largest contiguous private property in Sonoma Valley, California. The Kunde brand is known for Cabernet Sauvignon, Merlot, Chardonnay and Zinfandel and is consistently recognized as one of the top ten brands in Sonoma. Kunde wines have earned scores of 90 points or higher for many of its wines across the portfolio. Kunde wines sell at the winery, and through wholesale, e-commerce and wine clubs at retail prices between $18.00 and $100.00 per bottle.

Viansa — Viansa is known for its Italian varietals and its 270-degree views of the Sonoma Valley. Viansa was one of the first wineries to use the tasting room as a place to host and entertain guests. Viansa’s hilltop villa and estate, referred to as the “Summit of Sonoma,” has a panoramic view of Sonoma Valley. The site features olive tree-lined vineyards, a 97-acre wetland preserve, an event pavilion, and tasting patios that overlook the marketplace area. Viansa has been a notable Sonoma attraction for more than 30 years. Viansa wines are sold exclusively at the winery, through wine clubs and e-commerce at retail prices between $22.00 and $125.00 per bottle.

B.R. Cohn Winery —The B.R. Cohn Winery is located between the Mayacamas and Sonoma Mountain ranges, in the heart of California’s Sonoma Valley. Sonoma is pictured by some as a free-spirited cousin of Napa Valley. The history and heritage of B.R. Cohn may support this impression. Founded by the legendary rock and roll manager of the Doobie Brothers and other rock acts in the 1980s, the B.R. Cohn estate is an ideal site for growing Cabernet Sauvignon and other red Bordeaux varietals. Numerous musical events are hosted on the estate, including the Sonoma Harvest Music Festival held annually in September (with the exception of September 2020 due to COVID-19 restrictions). Alongside a range of small-lot estate wines, the Silver Label tier markets the B.R. Cohn wines to consumers at a more affordable price point. B.R. Cohn Silver Label wines, including Cabernet Sauvignon, Merlot, Chardonnay and Pinot Noir varietals and Sauvignon Blanc, are in wide wholesale and e-commerce distribution. B.R. Cohn wines sell at the winery, and through wholesale, e-commerce and wine clubs, at retail prices between $17.00 and $100.00 per bottle.

Craft Spirits

In addition to wine production and distribution, which is our core business, we are in the spirits business. We own the brand No. 209 Gin and Splinter Group Spirits, whose brands consists of Straight Edge Bourbon Whiskey, Slaughterhouse American Whiskey, and Whip Saw Rye. We also team with leading spirits manufacturers and distributors to develop products for our customers. We have collaborated with another spirits manufacturer to create Partner Vermouth, which is a sweet vermouth from the gardens and vineyards of California wine country.

We believe that we can use the spirits business to further expand our private label business with existing B2B customers. We expect that interest in selling private label products (due to the increased margins that we earn relative to sales of third party products) will lead to more retailers selling private label spirits. We believe that we can use our significant distribution network and production capabilities to increase our spirits private label business with both existing and new B2B customers.

Our Competitive Strengths

5

We believe that our strengths include a diversified brand portfolio and infrastructure, a customer-centric and innovation-driven culture, a demonstrated success in acquiring and integrating new assets into our platform, strong working relationships with distributor and retail networks, access to low-cost and flexible debt financing, and an experienced management team assembled and led by Patrick Roney.

Diversified Brand Portfolio and Infrastructure

Our diversified wine sourcing, brand positioning and omni-channel sales strategy result in a nimble, scalable business model, enabling us to bring our products to market rapidly and navigate ever-changing consumer demand flexibly. We believe the efficiencies of our infrastructure have been reflected in our historical results.

Strong Relationships with Distributors and Retailers

We have longstanding working relationships with many of the wine industry’s largest distributors and retailers, which facilitates the distribution of our products to customers in as many locations as possible.

We believe that our existing arrangements with distributors also provide a scalable platform for us to introduce new products into the market and further expand our revenue and market share. The distribution market has experienced and continues to undergo significant consolidation. As a result, it is harder for newer or smaller wine and alcohol businesses to gain traction with major distributors, which limits their ability to get their products into the major wholesale and retail markets. We believe that our longstanding working relationships with the largest distributors and retailers—forged over many years—give us an advantage over newer and smaller competitors.

We have powerful, long-standing relationships with national retailers, including Costco, Albertson’s, Target and others. In addition, we believe that we have a seven-figure annual case volume expansion opportunity with our national chain account clients by placing more brands with existing customers and adding new major customers.

Customer-Centric and Innovation-Driven Culture

We have created more than 15 new brands over the last 5 years to address specific consumer needs and market opportunities. We take a holistic approach with new brands, evaluating key attributes such as price points, packaging format, demographic and psychographic trends. We create new brands organically through an efficient concept-to-launch process, which generally requires less than six months in total and can sometimes be completed in less than three months. We believe that our efficient new product development and rapid speed to market gives us and our private label retailers an advantage over competitors because it enables us to quickly address actual or perceived unmet consumer needs and can help us better align brand strategy with consumer demand.

6

Demonstrated Success Acquiring and Integrating New Assets

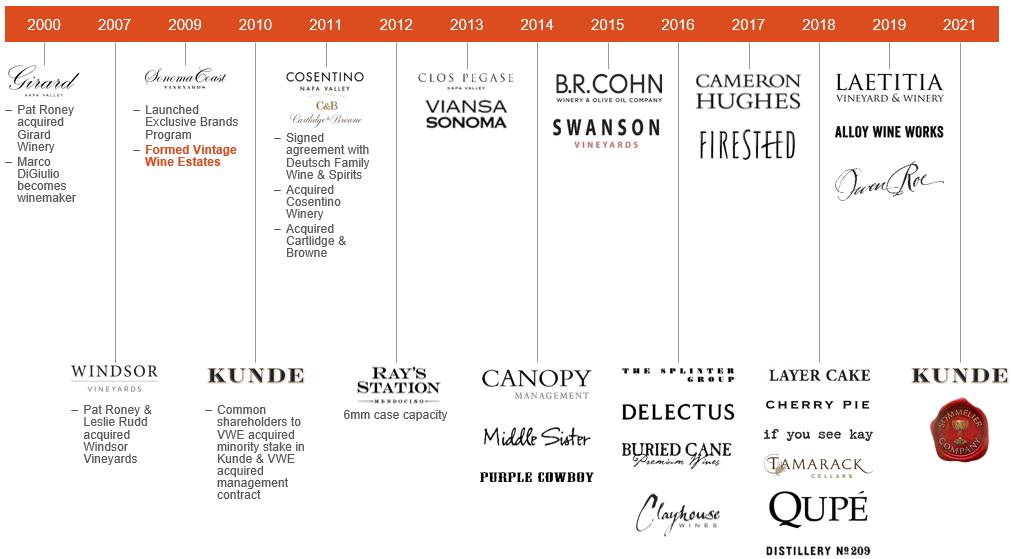

We believe we have completed more brand mergers and acquisitions in the U.S. wine industry over the last 10 years than any other company in the industry. As illustrated in the following chart, we have completed more than 20 acquisitions since 2010.

Historically, our acquisitions have generated a strong return on equity. Over the three years immediately preceding the COVID-19 pandemic, we reviewed, on average, over 20 acquisitions per year, submitted an average of four letters of intent and completed an average of two acquisitions per year. We have historically targeted a significant increase in the target company’s EBITDA within three years of the acquisition. To achieve these results, our acquisitions are subject to a rigorous, data-driven, due diligence and underwriting process, to assure that minimum financial thresholds with meaningful upside can be satisfied in each transaction.

Experienced Management Team

Our senior leaders have decades of experience in the wine and spirits industry and have gone through numerous economic and consumer cycles, providing them with unique insight and historical perspectives that less experienced leaders do not have. Vintage Wine Estates was founded by Patrick Roney and Leslie Rudd, who passed away in 2018. Mr. Roney has spent more than 30 years in the wine, spirits and food industries and has held senior leadership roles at leading brands such as Seagram’s, Chateau St. Jean, Dean & Deluca and the Kunde Family Winery. Throughout his career, Mr. Roney has demonstrated a keen understanding of and ability to anticipate market trends and consumer behaviors. Mr. Roney also has also been able to attract some of the top talent in the industry, including President, Terry Wheatley. Mrs. Wheatley has spent her entire career in the wine and spirits industry at leading firms, including at E.J. Gallo and the Sutter Home/Trinchero Family Estate. Mrs. Wheatley also started her own wine brand, creation, sales and marketing company, Canopy Management, leveraging her long-term relationships with the wine industry’s top buyers to bring a portfolio of innovative wine brands to market. We acquired Canopy Brands in 2014.

Our Strategy

We are currently the 15th largest wine producer by cases shipped in California. We have been able to grow our business despite economic recessions. We intend to continue to grow our business by prioritizing the following goals: (i) increasing sales of our existing brands, (ii) continuing to develop new and innovative products, (iii) executing on our acquisition pipeline, (iv) continuing to grow our private label business, and (v) continuing to invest in and expand production capacity to meet the needs of our brands and our customers.

Increasing Sales of Existing Brands

We seek to grow our existing brands by increasing penetration within existing on-premise and off-premise retailers, selling into new retailers and distributors and investing in and expanding our DTC segment. Given the strength of our brands and our strong reputation with consumers, we

7

believe we can increase the number of varietals and blends that are offered in retail and on-premise locations. As consumer shopping behaviors continue to evolve and change, we are well positioned to continue to increase sales and conversions through our off-premise retailers’ digital channels with the investment in a dedicated eGrocery team to manage and support the digital shelf online as well as in popular delivery apps and services. We will continue to invest in our DTC business and intend to capitalize on the consumer’s willingness to purchase more products online. Additionally, as government implemented measures in response to COVID-19 subside, we expect tasting room sales to increase, which should generally lead to increased wine club participation. Additionally, regulatory authorities across the U.S. have relaxed regulations regarding delivery of alcohol directly to consumers. As consumers have grown more used to obtaining alcoholic beverages this way, we expect DTC sales to continue to increase. While it is too soon to know if these relaxed regulations will be permanently enacted in each state, we believe we are well-positioned to take advantage of a consumer shift to DTC sales.

Developing New Brands and Innovative Products

We believe that we can continue to develop new brands and products that address consumer demand and sell these new products into our omni-channel distribution system. These new products are expected to diversify our revenue further and expand our addressable market to additional categories beyond wine. We believe our integrated infrastructure allows us to capitalize on emerging trends faster than many of our competitors, giving us an advantage in new product development. Additionally, upon federal legalization of cannabis, we expect to seek to produce and sell cannabis infused beverages through our distribution channels. We are at the early stage of developing this strategy and no material assets have been created from this initiative as of the date hereof. We do not intend to enter this sector unless cannabis is federally legalized in the U.S. and there is no assurance if or when cannabis will be federally legalized.

Executing our Acquisition Pipeline

There continues to be consolidation of distributors and retailers in the wine industry, creating uncertainty for smaller wine companies and further limiting their ability to garner attention in the wholesale channel. As a result, we expect more brands to look for buyers of their businesses, which may create more attractive acquisition opportunities for us in the future. Given our scale and infrastructure, we are generally able to increase margins of acquired businesses relatively quickly, adding value to the enterprise from the outset. While other, larger wine companies have recently been preoccupied with other strategic initiatives, we remain committed and highly active with our merger and acquisition ("M&A") strategy.

Growing Private Label Sales

We intend to expand our private label business by increasing sales of existing products, creating product line extensions and developing new brands for new customers. We believe the largest retailers will continue to increase their private label offerings. We also believe that, in addition to private label wine sales, we are well-positioned to expand our private label options to include spirits and other products.

Expanding Production Capacity

We believe we have opportunities to make capital investments that satisfy our financial return requirements while expanding our capacity to meet additional demand for our private brands and private label customers over time. We are in the process of completing a $45 million investment in state-of-the-art technology upgrades to our Ray’s Station production facility. The upgraded facility, together with existing facilities, will allow us to produce and ship approximately 15 million cases of wine per year and store over 3 million cases of wine. The new facility will put our production and distribution capacity at levels comparable to the top 5 wine producers in the U.S. This facility also will allow us to automate a number of processes that were previously completed manually, leading to increased efficiencies and margins.

We are one of a few vertically integrated winery companies that has our own pick-and-pack capabilities, leading to substantial per case cost savings. Notably, we have recently added a second warehouse facility in Cincinnati, Ohio. This is significantly more efficient than outsourcing this work and is currently the fastest growing portion of the wine business versus wholesale or private label.

Our capital expenditures have been at elevated levels in recent years, and as projects are completed, the business is expected to significantly increase margins with modest platform investments required going forward.

Competition

The wine industry and alcohol markets generally are intensely competitive. Our wines compete domestically and internationally with premium or higher quality wines produced in Europe, South America, South Africa, Australia and New Zealand, as well as North America. We compete on the basis of quality, price, brand recognition and distribution capability. The ultimate consumer has many choices of products from both domestic and international producers. Our wines may be considered to compete with all alcoholic and nonalcoholic beverages.

At any given time, there are more than 400,000 wine choices available to U.S. consumers, differing with one another based on vintage, variety or blend, location and other factors. Accordingly, we experience competition from nearly every segment of the wine industry. Additionally, some of our competitors have greater financial, technical, marketing and other resources, offer a wider range of products, and have greater name recognition, which may give them greater negotiating leverage with distributors and allow them to offer their products in more locations and/or on better terms than us. Nevertheless, we believe that our diverse brand offerings, scalable infrastructure and relationships with the largest wholesalers and retailers will allow us to continue growing our business.

8

Seasonality

There is a degree of seasonality in the growing cycles, procurement and transportation of grapes. The wine industry in general tends to experience seasonal fluctuations in revenue and net income. Typically, we have lower sales and net income during our third fiscal quarter (January through March) and higher sales and net income during our second fiscal quarter (October through December) due to the usual timing of seasonal holiday buying, as well as wine club shipments. We expect these trends to continue.

Human Capital Management

We are committed to fostering a work environment that values diversity and inclusion. This commitment includes providing equal access to and participation in, equal employment opportunities, programs and services without regard to race, religion, color, origin, disability, sex, sexual orientation, gender identity, veteran status, age or stereotypes based thereon. We welcome team members' differences, experiences, and beliefs, and we are investing in a more productive, engaged, diverse and inclusive workforce.

We monitor human capital metrics to ensure we are executing on our core values and making progress towards our diversity and inclusion commitments. As of June 30, 2021, we had 563 full-time employees. Among our employees, 44% identify as female and 56% identify as male. None of our employees are represented by a labor union, and none of our employees have entered into a collective bargaining agreement with us. We offer a highly competitive compensation and benefits program to attract and retain top talent.

Our talented employees drive our mission and share core values that both stem from and define our culture, which plays an invaluable role in our execution at all levels in our organization. Our culture is based on these shared core values which we believe contribute to our success and the continued growth of the organization. Our core values are used in candidate screening and in employee evaluations to help reinforce their importance in our organization:

We continue to focus on workplace safety by providing training and bringing awareness to workplace best practices in our continuous efforts to reduce workplace injuries and accidents. We acted quickly to respond to safety protocols as a result of the COVID-19 pandemic to protect the health and safety of our team members. To support team members, we provided temporary pay increases to certain employees, offered remote work where possible, purchased additional sanitation supplies and increased personal protective materials provided to staff.

Trademarks

Trademarks are an essential part of our business. We sell our products under a number of trademarks, which we own or use under license. We also have multiple licenses and distribution agreements for the import, sale, production and distribution of our products. Depending on the jurisdiction, trademarks are valid as long as the trademarks are in use and their registrations are properly maintained. These licenses and distribution agreements have varying terms and durations.

Government Regulation

The alcoholic beverage industry is subject to extensive regulation by the Alcohol and Tobacco Tax and Trade Bureau (“TTB”) (and other federal agencies), each state’s liquor authority and potentially local authorities as well, depending on location. As a result, there is a complex multi-jurisdictional regime governing alcoholic beverage manufacturing, distribution, sales and marketing in the U.S. Regulatory agencies issue permits and licenses for manufacturing, distribution and retail sale (with requirements varying depending on location), govern “trade practice” activity at each tier and also regulate how each tier of the alcohol industry may interact with another tier. In addition, these laws, rules, regulations and interpretations are constantly changing as a result of litigation, legislation and agency priorities. We take regulatory compliance very seriously, and to facilitate compliance with applicable requirements, we have a team of seven compliance professionals. We also use leading compliance software providers (Avalara and SOVOS) to assist the compliance team with data management and reporting cycles. Additionally, we consult with outside regulatory counsel on compliance issues on a regular basis and utilize Compliance Connection, an outside compliance company, on an as needed basis.

We maintain licenses and permits to produce and wholesale wine in Oregon and Washington with state regulatory agencies and TTB. We maintain licenses and permits to import, produce, and wholesale wine, and to import, rectify and wholesale distilled spirits with California regulatory authorities and TTB. In addition to licenses for our primary production activity, we maintain hundreds of ancillary permits to support our wholesale and DTC segments. Most states require permitting and registrations with the state for shipments to wholesalers or consumers within the state, and these permits often also require local registration and tax reporting. We manage our permit compliance internally, with our team responsible for managing

9

renewals, tax payments and reporting in a timely manner. Specifically, we complete the following to satisfy our regulatory obligations: (i) prepare TTB’s monthly Report of Wine Premises Operations, (ii) complete monthly TTB export division reports which coincide with the monthly Report of Wine Premises Operations, (iii) complete bi-weekly excise TTB tax returns, (iv) prepare and complete California Department of Tax and Fee Administration’s (CDTFA) winegrower, beer/wine importer, and distilled spirits reports and tax returns, (v) prepares and completes Washington state’s winegrower, beer/wine importer, and distilled spirits reports and tax returns, (vi) file annual grape crush and purchase reports with the U.S. Food and Drug Administration (“FDA”), (vii) regularly update corporate filings with the TTB, as well as state Alcohol Beverage regulatory agencies as required, and (viii) complete biennial registrations with the FDA.

In California, we maintain licenses with: (i) the California Department of Food and Agriculture to purchase grapes, (ii) a potable water system permit with the California Division of Drinking Water, (iii) a hazardous material business plan permit with the County of Mendocino California Division of Environmental Health, and (iv) a storm water pollution prevention plan permit with the State of California State Water Resources Control Board. Additionally, food processing facilities, which includes wineries, must register with the FDA, and we maintain such registrations for our winery facilities.

We believe that we possess all licenses and permits material to operating our business.

Sale of our wine is subject to federal alcohol tax, payable at the time wine is removed from the bonded area of the winery for sale. In December 2017, the federal government passed comprehensive tax legislation that included the Craft Beverage Modernization and Tax Reform Act. This legislation modified federal alcohol tax rates by expanding the lower $1.07 per gallon tax rate to wines up to 16.0% alcohol content with wines containing higher alcohol levels being taxed at $1.57 per gallon. We are also subject to certain taxes at the state and local levels.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports are available free of charge on our website, www.vintagewineestates.com, under "Investor Overview — Investor Relations — SEC Filings" as soon as reasonably practicable after we electronically file them with, or furnish them to, the SEC. The SEC also maintains a website, www.sec.gov, where you can search for annual, quarterly and current reports, proxy and information statements, and other information regarding us and other public companies.

Item 1A. Risk Factors

In addition to the other information in this report and our other filings with the Securities and Exchange Commission ("SEC"), you should carefully consider the risks and uncertainties described below, which could materially and adversely affect our business, financial condition and results of operations. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that affect us.

Risks Related to Our Operations

The ongoing COVID-19 pandemic has had, and will likely continue to have, adverse effects on the economy and on our business.

The outbreak of COVID-19, which the World Health Organization declared a pandemic in March 2020, has spread across the world and has disrupted the global economy and most industries, including the wine industry. Efforts to control the pandemic have slowed economic activity and disrupted, and reduced the efficiency of, normal business activities across the United States. The pandemic has resulted in authorities implementing numerous unprecedented measures such as travel restrictions, quarantines, shelter-in-place orders and workplace shutdowns. These measures have impacted, and will likely continue to impact, our business, customers, supply chain and employees.

We have experienced declines in visitors to our tasting rooms primarily due to travel restrictions, shelter-in-place orders and workplace shutdowns resulting from the COVID-19 pandemic. In response to governmental directives and recommended safety measures, we modified our workplace practices. While we have implemented personal safety measures at all of our facilities where our employees are working onsite, any actions that we take may not be sufficient to mitigate the risk of infection and could result in a significant number of COVID-19 related claims. Changes to state workers’ compensation laws, as have recently occurred in California, could increase VWE’s potential liability for such claims.

In the longer term, the COVID-19 pandemic is likely to adversely affect the economies and financial markets and could result in an economic downturn and a recession. It is uncertain how this would affect demand for our products. While VWE continues to see robust demand in its industry, and has seen little impact to its results of operations from the COVID-19 pandemic, the environment remains uncertain and it may not be sustainable over the longer term. The degree to which the pandemic ultimately impacts our business and results of operations will depend on future developments beyond our control, including the severity of the pandemic, the extent of actions to contain the virus, the availability and efficacy of a vaccine or other treatment, how quickly and to what extent normal economic and operating conditions can resume, and the severity and duration of the economic downturn that results from the pandemic.

Consumer demand for wine and alcoholic beverages could decline, which could adversely affect our results of operations.

We rely on consumers’ demand for our wine and other products. Consumer demand may decline due to a variety of factors, including a general decline in economic conditions, changes in the spending habits of consumers generally, a generational or demographic shift in consumer

10

preferences, increased activity of anti-alcohol groups, increased state or federal taxes on alcoholic beverage products and concerns about the health consequences of consuming alcoholic beverage products. Furthermore, our ability to effectively manage production and inventory is inherently linked to actual and expected consumer demand for our products, particularly given the long product lead time and agricultural nature of the wine business. Unanticipated changes in consumer demand or preferences could have adverse effects on our ability to manage supply and capture growth opportunities, and substantial declines in the demand for one or more of our product categories could harm our results of operations, financial condition and prospects.

We are subject to significant competition, which could adversely affect our profitability.

VWE’s wines compete for sales with thousands of other domestic and foreign wines. VWE’s wines also compete with other alcoholic beverages and, to a lesser degree, non-alcoholic beverages. As a result of this intense competition, we have been subject to, and may continue to be subject to, upward pressure on selling and promotional expenses. In addition, some of our competitors have greater financial, technical, marketing and public relations resources available to them than we do. These circumstances could adversely impact our revenues, margins, market share and profitability.

Our wholesale operations and wholesale revenues largely depend on independent distributors whose performance and continuity is not assured.

Our wholesale operations and wholesale revenues depend largely on independent distributors whose performance and continuity is not assured. Our wholesale operations generate revenue from products sold to distributors, who then sell them to off-premise retail locations such as grocery stores, specialty and multi-national retail chains, as well as on-premise locations such as restaurants and bars. Sales to distributors are expected to continue to represent a substantial portion of our revenues in the future. A change in relationships with one or more significant distributors could harm our business and reduce sales. The laws and regulations of several states prohibit changes of distributors except under certain limited circumstances, which makes it difficult to terminate a distributor for poor performance without reasonable cause as defined by applicable statutes. Difficulty or inability with respect to replacing distributors, poor performance of major distributors or inability to collect accounts receivable from major distributors could harm our business. There can be no assurance that existing distributors and retailers will continue to purchase our products or provide ours products with adequate levels of promotional support. Consolidation at the retail tier, among club and chain grocery stores in particular, can be expected to heighten competitive pressure to increase marketing and sales spending or constrain or reduce prices.

The loss or significant decline of sales to one or more of our more important distributors, marketing companies or retailers could have adverse effects on our results of operations, financial condition and prospects.

We derive significant revenue from distributors and marketing companies such as Deutsch Family Wine and Spirits, Republic National Distributing Company and Southern Glazer’s Wine & Spirits, and from retail business customers such as Costco, Albertson’s and Target. The loss of one or more of these customers, or significant decline in the volume of sales made to them, could have adverse effects on our results of operations, financial condition and prospects.

The strength of VWE’s brands is critical to our success.

Our reputation as a premier producer of wine and spirits among our customers and the wine industry is critical to the success of our business and our growth strategy. The wine market is driven by a relatively small number of active and well-regarded wine critics within the industry who have disproportionate influence over the perceived quality and value of wines. If we are unable to maintain the actual or perceived quality of our wines and other alcoholic beverage products, or if our wines otherwise do not meet the subjective expectations or tastes of one or more of a relatively small number of wine critics, the actual or perceived quality and value of one or more of our wines could be harmed, which could negatively impact not only the value of that wine, but also the value of the vintage, the particular brand or our broader portfolio. The winemaking process is a long and labor-intensive process that is built around yearly vintages, which means that once a vintage has been released we are not able to make further adjustments to satisfy wine critics or consumers. As a result, we are dependent on our winemakers and tasting panels to ensure that our wine products meet our exacting quality standards.

Any contamination or other quality control issue could have an adverse effect on sales of the impacted wine or our broader portfolio of winery brands. If any of our wines become unsafe or unfit for consumption, cause injury or are otherwise improperly packaged or labeled, we may have to engage in a product recall and/or be subject to liability and incur additional costs. A widespread recall, multiple recalls, or a significant product liability judgment against us could cause our wines to be unavailable for a period of time, depressing demand and our brand reputation. Even if a product liability claim is unsuccessful or is not fully pursued, any resulting negative publicity could adversely affect our reputation with existing and potential customers and accounts, as well as our corporate and individual winery brands image in such a way that current and future sales could be diminished. In addition, should a competitor experience a recall or contamination event, we could face decreased consumer confidence by association as a producer of similar products.

Additionally, third parties may sell wines or inferior brands that imitate our winery brands or that are counterfeit versions of our labels, and customers could be duped into thinking that these imitation labels are our authentic wines. A negative consumer experience with such a wine could cause them to refrain from purchasing our brands in the future and damage our brand integrity. Any failure to maintain the actual or perceived quality of our wines could materially and adversely affect our business, results of operations and financial results.

11

Damage to our reputation or loss of consumer confidence in our wines for any of these or other reasons could result in decreased demand for our wines and could have a material adverse effect on our business, operational results and financial results, as well as require additional resources to rebuild our reputation, competitive position and winery brand strength.

Our advertising and promotional investments may not be effective.

In the ordinary course of conducting its business, we regularly incur significant advertising and promotional expenditures to enhance our winery brands and raise consumer awareness in both existing and emerging categories. Variations in the levels of advertising and promotional expenditures in the past have caused, and are expected in the future to continue to cause, variability in our results of operations. While we strive to invest only in effective advertising and promotional activities, it is difficult to correlate such investments with sales results. There is no guarantee that advertising and promotional expenditures will be effective in building brand strength or in growing repeat sales.

Decreases in wine quality ratings by important rating organizations could adversely affect our business.

Many of VWE’s brands are issued ratings by local or national wine rating organizations. In the wine industry, higher product ratings usually translate into greater demand and higher pricing. Although some VWE brands have been rated highly in the past, and VWE believes its farming and winemaking activities are of a quality to generate good ratings in the future, VWE has no control over ratings issued by third parties, which may or may not be favorable in the future. Significant or persistent declines in the ratings issued to VWE wines could have adverse effects on its business.

We may not be fully insured against catastrophic events and losses, which may adversely affect our financial condition.

A significant portion of our activities are located in California and the Pacific Northwest, which regions are increasingly prone to seismic activity, landslides, wildfires and other natural disasters (collectively, “catastrophes”). Although VWE insures against catastrophes, including through our use of a wholly-owned captive insurance company and by carrying insurance to cover our own property damage, business interruption and certain production assets, we may not be fully insured against all catastrophes, the occurrence of which may (i) disrupt our operations, (ii) delay production, shipments and revenue and (iii) result in significant expenses to repair or replace damaged vineyards or facilities. Any disruption caused by a catastrophe could adversely affect our business, results of operations or financial condition.

Our inability to protect its trademarks and other intellectual property rights could adversely affect its business.

VWE’s business relies on intellectual property, mainly consisting of trademarks, customer lists and business practices. VWE does not register its business practices or customer lists, but they are kept highly confidential and considered trade secrets and, as such, are accessible to a very limited number of people within VWE. Although VWE believes that it does not rely significantly on any individual intellectual property right, a breach of confidentiality with respect to the customer lists or business practices, or loss of access to them, or the future expiration of intellectual property trademark rights, could have adverse impacts on VWE’s business.

VWE relies in part on confidentiality agreements, ownership of intellectual property, and non-competition agreements with employees, vendors and third parties in order to protect its intellectual property. It is possible that these agreements could be breached and that VWE might lack an adequate remedy for breach. Disputes may arise concerning the ownership of intellectual property or the extent to which the confidentiality agreements remain in force. Furthermore, VWE’s trade secrets may become revealed to its competitors or developed independently by them, in which case VWE will not be able to enjoy exclusive use of some of its formulas or maintain confidentiality concerning its products.

New lines of business or new products and services could subject us to additional risks.

VWE may invest in new lines of business, or may offer new products, such as within its spirits business or, upon federal legalization of cannabis, cannabis-infused beverages. There are risks and uncertainties associated with such efforts, particularly in instances where the markets are not fully developed or are evolving. In developing and marketing new lines of business and new products and services, VWE may invest significant time and resources. External factors, such as regulatory compliance obligations, competitive alternatives, lack of market acceptance and shifting consumer preferences, may also affect the successful implementation of a new line of business or a new product or service. With respect to cannabis-infused beverages, even if the federal government legalizes medical and/or adult-use cannabis, significant delays in the drafting and implementation of industry regulations and licensing and the costs associated with burdensome regulations and taxes could adversely impact VWE’s ability to operate profitably in the cannabis-infused beverage industry. Failure to successfully manage these risks in the development and implementation of new lines of business or new products or services could have adverse effects on VWE’s business, results of operations and financial condition.

Litigation relating to alcohol abuse or the misuse of alcohol could adversely affect our business.

Increased public attention has been directed at the beverage alcohol industry, which we believe is due to concern over problems related to alcohol abuse, including drinking and driving, underage drinking and health consequences from the misuse of alcohol. Adverse developments in these or similar lawsuits or a significant decline in the social acceptability of beverage alcohol products that could result from such lawsuits could materially adversely affect our business.

12

Risks Related to Our Production Activities

If we are unable to obtain adequate supplies of grapes or other raw materials, or if there is an increase in the cost of such materials, our profitability and production of wine could be negatively impacted, which could materially and adversely affect our business, results of operations and financial condition.

We source our grapes from the vineyards that we own and control and from independent growers. Our production activities also require adequate supplies of other quality agricultural, raw and processed materials, including corks, glass bottles, barrels, winemaking additives and agents, water and other supplies. A shortage of grapes of the required variety and quality, or an inability to obtain or significant increase in the price of other requisite raw materials, could impair our ability to produce wines in the quantity and quality demanded by our customers and reduce our profitability.

Any such occurrences could adversely affect our business, results of operations and financial condition.

Drought or inclement weather could reduce the amount of water available for use in our growing and production activities, which could materially and adversely affect our business, results of operations and financial condition.

Water supply and adequate rainfall are critical to the supply of grapes, other agricultural raw materials and generally our ability to operate our business. If climate patterns change or droughts occur, there may be a scarcity of water or poor water quality, which could affect production costs, consistency of yields or impose capacity constraints. VWE depends on sufficient amounts of quality water for operation of its wineries, as well as to irrigate its vineyards and conduct other operations. The suppliers of the grapes and other agricultural raw materials purchased by VWE also depend upon sufficient supplies of quality water for their vineyards and fields. Prolonged or severe drought conditions or restrictions imposed on irrigation options by governmental authorities could have an adverse effect on our business, results of operations and financial condition.

Increases in the cost, disruption of supply or shortage of energy could adversely affect our business.

Our production facilities use a significant amount of energy in their operations, including electricity, propane and natural gas. Increases in the price, disruption of supply or shortage of energy sources, which may result from increased demand, natural disasters, power outages or other causes could increase our operating costs and negatively impact our profitability. VWE has experienced increases in energy costs in the past, and energy costs could rise in the future. In addition, we incur costs in connection with the transportation and distribution of our materials and products. Higher fuel costs will result in higher transportation, freight, and other operating costs, which could significantly increase our production costs and, correlatively, decrease our operating margins and profit.

We could be negatively impacted by the occurrence of wine contamination.

We are subject to certain hazards and product liability risks, such as potential contamination, through tampering or otherwise, of ingredients or products. Contamination of our wine could result in destruction of our wine held in inventory and could cause the need for a product recall, which could significantly damage VWE’s reputation for product quality. We maintains insurance against certain of these kinds of risks, and others, under various insurance policies. However, our insurance may not be sufficient to fully cover any resulting liability or may not continue to be available at a price or on terms that are satisfactory to us.

Risks Related to Information Technology and Cybersecurity

A failure of one or more of our key IT systems, networks, processes, associated sites or service providers could have a material adverse impact on business operations, and if the failure is prolonged, our financial condition.

We rely on IT systems, networks, and services, including internet sites, data hosting and processing facilities and tools, hardware (including laptops and mobile devices), software and technical applications and platforms, some of which are managed, hosted, provided and used by third-parties or their vendors, to assist us in the operation of our business. The various uses of these IT systems, networks and services include, but are not limited to: hosting our internal network and communication systems; tracking bulk wine; supply and demand; planning; production; shipping wines to customers; hosting our winery websites and marketing products to consumers; collecting and storing customer, consumer, employee, stockholder, and other data; processing transactions; summarizing and reporting results of operations; hosting, processing and sharing confidential and proprietary research, business plans and financial information; complying with regulatory, legal or tax requirements; providing data security; and handling other processes necessary to manage our business.

Increased IT security threats and more sophisticated cybercrimes and cyberattacks, including computer viruses and other malicious codes, ransomware, unauthorized access attempts, denial of service attacks, phishing, social engineering, hacking and other types of attacks pose a potential risk to the security of our IT systems, networks and services, as well as the confidentiality, availability, and integrity of our data, and we have in the past, and may in the future, experience cyberattacks and other unauthorized access attempts to our IT systems. Because the techniques used to obtain unauthorized access are constantly changing and often are not recognized until launched against a target, we or our vendors may be unable to anticipate these techniques or implement sufficient preventative or remedial measures.

If we are unable to efficiently and effectively maintain and upgrade our system safeguards, we may incur unexpected costs and certain of our systems may become more vulnerable to unauthorized access. In the event of a ransomware or other cyber-attack, the integrity and safety of our data could be at risk or we may incur unforeseen costs impacting our financial position. If the IT systems, networks or service providers we rely upon

13

fail to function properly, or if we suffer a loss or disclosure of business or other sensitive information due to any number of causes ranging from catastrophic events, power outages, security breaches, unauthorized use or usage errors by employees, vendors or other third parties and other security issues, we may be subject to legal claims and proceedings, liability under laws that protect the privacy and security of personal information (also known as personal data), litigation, governmental investigations and proceedings and regulatory penalties, and we may suffer interruptions in our ability to manage our operations and reputational, competitive or business harm, which may adversely affect our business, results of operations and financial results. In addition, such events could result in unauthorized disclosure of material confidential information, and we may suffer financial and reputational damage because of lost or misappropriated confidential information belonging to us or to our employees, stockholders, customers, suppliers, consumers or others. In any of these events, we could also be required to spend significant financial and other resources to remedy the damage caused by a security breach or technological failure and the reputational damage resulting therefrom, to pay for investigations, forensic analyses, legal advice, public relations advice or other services, or to repair or replace networks and IT systems.

As a result of the COVID-19 pandemic, a greater number of our employees are working remotely and accessing our IT systems and networks remotely, which may further increase our vulnerability to cybercrimes and cyberattacks and increase the stress on our technology infrastructure and systems. Although we maintain cyber risk insurance, this insurance may not be sufficient to cover all of our losses from any future breaches or failures of our IT systems, networks and services.

Our failure to adequately maintain and protect personal information of our customers or our employees in compliance with evolving legal requirements could have a material adverse effect on our business.