Form F-1/A Seanergy Maritime Holdin

Tweet

Tweet Share

ShareTable of Contents

As filed with the Securities and Exchange Commission on May 2, 2019

Registration No. 333-221058

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 9

TO

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Seanergy Maritime Holdings Corp.

(Exact name of registrant as specified in its charter)

| Republic of the Marshall Islands | 4412 | N.A. | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

Seanergy Maritime Holdings Corp.

154 Vouliagmenis Avenue

166 74 Glyfada

Athens, Greece

Tel: +30 213 0181507

(Address and telephone number of Registrant’s principal executive offices)

With copies to:

| Gary J. Wolfe, Esq. Seward & Kissel LLP One Battery Park Plaza New York, New York 10004 (212) 574-1200 (telephone number) (212) 480- 8421 (facsimile number) |

Barry I. Grossman, Esq. Lawrence A. Rosenbloom, Esq. Joshua N. Englard, Esq. Ellenoff Grossman & Schole LLP 1345 Avenue of the Americas New York, New York 10105 (212) 370-1300 (telephone number) (212) 370-7889 (facsimile number) | |

|

Seward & Kissel LLP One Battery Park Plaza (Name, Address and telephone number of agent for service) | ||

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered(1) |

Proposed Maximum Aggregate Offering Price(2) |

Amount of Registration Fee | ||

| Units consisting of: |

||||

| (i) Common shares, par value $0.0001 per share |

$17,250,000 | |||

| (ii) Class B Warrants to purchase common shares, par value $0.0001 per share(3)(4) |

— | |||

| (iii) Class C Warrants to purchase common shares, par value $0.0001 per share(3) |

— | |||

| Pre-funded warrants to purchase common shares(3)(5)(6) |

— | |||

| Common shares, par value $0.0001 per share, underlying Class B Warrants and Class C Warrants(4)(8) |

$37,950,000 | |||

| Common shares, par value $0.0001 per share, underlying pre-funded warrants(5) |

— | |||

| Representative’s common share purchase warrant(7) |

— | |||

| Common shares underlying representative’s common share purchase warrant(8) |

$1,078,125 | |||

| Total |

$56,278,125 | $6,821(9) | ||

|

| ||||

|

| ||||

| (1) | Includes common shares, Class B Warrants and Class C Warrants the underwriter has the option to purchase to cover over-allotments, if any. Pursuant to Rule 416, there are also being registered such indeterminable additional securities as may be issued to prevent dilution as a result of stock splits, stock dividends or similar transactions. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) of the Securities Act of 1933, as amended. |

| (3) | In accordance with Rule 457(i) under the Securities Act, no separate registration fee is required with respect to the warrants registered hereby. |

| (4) | Based on a per-share exercise price for the Class B Warrants and Class C Warrants of 110% of the public offering price per unit in this offering. Includes shares issuable under certain circumstances upon full exercise of the Class C Warrants pursuant to the cashless exercise provision therein. |

| (5) | The proposed maximum aggregate offering price of the common shares proposed to be sold in the offering will be reduced on a dollar-for-dollar basis on the offering price of any pre-funded warrants offered and sold in the offering, and as such the proposed maximum offering price of the common shares and pre-funded warrants (including the common shares issuable upon exercise of the pre-funded warrants) if any, is $17,250,000. |

| (6) | The registrant may issue pre-funded warrants to purchase common shares in the offering. The purchase price of each pre-funded warrant will equal the price per share at which shares of common shares are being sold to the public in this offering, minus $0.01, which constitutes the pre-funded portion of the exercise price, and the remaining unpaid exercise price of the pre-funded warrant will equal $0.01 per share (subject to adjustment as provided for therein). |

| (7) | No fee pursuant to Rule 457(g) under the Securities Act. |

| (8) | Based on a per-share exercise price of 110% of the unit price for the Class B Warrants, 110% of the unit price for the Class C Warrants, and 125% of the unit price for the Representative’s common share purchase warrant. |

| (9) | Previously paid. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 2, 2019

PRELIMINARY PROSPECTUS

3,685,500

Units Consisting of Common Shares or

Pre-Funded Warrants to Purchase Common Shares and

Class B Warrants to Purchase Common Shares and

Class C Warrants to Purchase Common Shares

Seanergy Maritime Holdings Corp.

We are offering 3,685,500 units, each unit consisting of (i) one common share, par value $0.0001 per share, (ii) one Class B Warrant to purchase one common share and (iii) one Class C Warrant to purchase one common share pursuant to this prospectus for $ per unit. Each Class B Warrant will have an exercise price of $ per share, subject to downward adjustment under certain circumstances seven months after issuance, will be exercisable upon issuance and will expire three years from issuance. Each Class C Warrant will have an exercise price of $ per share, will be exercisable upon issuance, and will expire six months from issuance. Beginning 30 days after issuance, each Class C Warrant will be exercisable on a cashless basis under certain circumstances for a number of common shares calculated according to a formula based on the market price at the time of exercise.

We are also offering to each purchaser, with respect to the purchase of units that would otherwise result in the purchaser’s beneficial ownership exceeding 4.99% of our outstanding common shares immediately following the consummation of this offering, the opportunity to purchase units including one pre-funded warrant in lieu of one common share in the unit. Subject to limited exceptions, a holder of pre-funded warrants will not have the right to exercise any portion of its pre-funded warrants if the holder, together with its affiliates, would beneficially own in excess of 4.99% (or, at the election of the holder, such limit may be increased to up to 9.99%) of the number of common shares outstanding immediately after giving effect to such exercise. Each pre-funded warrant will be exercisable for one common share. The purchase price of each unit including a pre-funded warrant will be equal to the price per unit including one common share, minus $0.01, and the remaining exercise price of each pre-funded warrant will equal $0.01 per share. The pre-funded warrants will be immediately exercisable and may be exercised at any time until all of the pre-funded warrants are exercised in full. For each unit including a pre-funded warrant we sell (without regard to any limitation on exercise set forth therein), the number of units including a common share we are offering will be decreased on a one-for-one basis.

The common shares and pre-funded warrants, if any, can each be purchased in this offering only with the accompanying Class B Warrants and Class C Warrants (other than pursuant to the underwriters’ option to purchase additional units) as part of a unit, but the components of the units will immediately separate upon issuance.

Jelco Delta Holding Corp., or Jelco, our principal shareholder, has agreed to participate in a private placement of $6,200,000 of units at the public offering price, in exchange for the waiver or forgiveness of certain payment obligations of ours as described in “The Offering—Concurrent Private Placement.” Each such unit issued in the private placement would consist of one common share, one Class B Warrant and one Class C Warrant, and the closing of the private placement is conditioned upon the closing of this offering.

Our common shares and Class A Warrants are listed on the Nasdaq Capital Market under the symbols “SHIP” and “SHIPW”, respectively. On May 1, 2019, the last reported sale price of our common shares on the Nasdaq Capital Market was $3.80 per share. We have applied to list the Class B Warrants offered hereby on the Nasdaq Capital Market. No assurance can be given that our application will be approved.

There is currently no established trading market for the units, pre-funded warrants, Class B Warrants or Class C Warrants. In addition, we do not intend to apply for the listing of the units, pre-funded warrants or Class C Warrants on any national securities exchange or other trading market and we do not expect an active trading market to develop for these securities. Without an active trading market, the liquidity of the pre-funded warrants and the Class C Warrants will be limited.

Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 17 of this prospectus for a discussion of information that should be considered in connection with an investment in our securities.

| Per Unit | Total | |||||||

| Public offering price |

$ | $ | ||||||

| Underwriters fees and commissions(1) |

$ | $ | ||||||

| Proceeds to the Company, before expenses |

$ | $ | ||||||

| (1) | We have agreed to issue a warrant, or the Representative’s Warrant, to the representative of the underwriters, or the Representative. We have additionally agreed to reimburse the underwriters for expenses incurred by them in an amount not to exceed $90,000. We refer you to “Underwriting” beginning on page 132 of this prospectus for additional information regarding total compensation and other items of value payable to the underwriters. |

We have granted the underwriters an option for a period of up to 45 days to purchase up to 552,825 additional common shares or pre-funded warrants, 552,825 Class B Warrants and/or 552,825 Class C Warrants.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Delivery of the units to purchasers in the offering is expected to be made on or about , 2019.

Maxim Group LLC

The date of this prospectus is , 2019.

Table of Contents

| Page | ||||

| ii | ||||

| ii | ||||

| iv | ||||

| 1 | ||||

| 9 | ||||

| 12 | ||||

| 17 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 45 | ||||

| 47 | ||||

| 67 | ||||

| 102 | ||||

| 106 | ||||

| 108 | ||||

| 109 | ||||

| 112 | ||||

| 118 | ||||

| 122 | ||||

| 132 | ||||

| 142 | ||||

| 142 | ||||

| 142 | ||||

| 142 | ||||

| 143 | ||||

| II-17 | ||||

i

Table of Contents

You should rely only on the information contained and incorporated by reference into this prospectus and in any free writing prospectus that we authorize to be distributed to you. We have not, and the underwriters have not, authorized anyone to provide you with additional or different information or to make representations other than those contained in this prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. This document may only be used where it is legal to sell these securities. You should assume that the information contained in this prospectus is accurate only as of the date of this prospectus. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer is not permitted.

We obtained certain statistical data, market data and other industry data and forecasts used or incorporated by reference into this prospectus from publicly available information. While we believe that the statistical data, industry data, forecasts and market research are reliable, we have not independently verified the data, and we do not make any representation as to the accuracy of the information.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus and the documents incorporated by reference into this prospectus contain certain forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include, but are not limited to, statements regarding our or our management’s expectations, hopes, beliefs, intentions or strategies regarding the future and other statements that are other than statements of historical fact. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate”, “believe”, “continue”, “could”, “estimate”, “expect”, “intend”, “may”, “might”, “plan”, “possible”, “potential”, “predict”, “project”, “should”, “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements in this prospectus and the documents incorporated by reference into this prospectus are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation, management’s examination of historical operating trends, data contained in our records and other data available from third parties. Although we believe that these assumptions were reasonable when made, because these assumptions are inherently subject to significant uncertainties and contingencies that are difficult or impossible to predict and are beyond our control, we cannot assure you that we will achieve or accomplish these expectations, beliefs or projections. As a result, you are cautioned not to rely on any forward-looking statements.

Many of these statements are based on our assumptions about factors that are beyond our ability to control or predict and are subject to risks and uncertainties that are described more fully in the section herein entitled “Risk Factors”. Any of these factors or a combination of these factors could materially affect our future results of operations and the ultimate accuracy of the forward-looking statements. In addition to these important factors and matters discussed elsewhere herein and in the documents incorporated by reference herein, important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements include, among other things:

| • | changes in shipping industry trends, including charter rates, vessel values and factors affecting vessel supply and demand; |

| • | changes in seaborne and other transportation patterns; |

| • | changes in the supply of or demand for drybulk commodities, including drybulk commodities carried by sea, generally or in particular regions; |

ii

Table of Contents

| • | changes in the number of newbuildings under construction in the drybulk shipping industry; |

| • | changes in the useful lives and the value of our vessels and the related impact on our compliance with loan covenants; |

| • | the aging of our fleet and increases in operating costs; |

| • | changes in our ability to complete future, pending or recent acquisitions or dispositions; |

| • | our ability to achieve successful utilization of our expanded fleet; |

| • | changes to our financial condition and liquidity, including our ability to pay amounts that we owe and obtain additional financing to fund capital expenditures, acquisitions and other general corporate activities; |

| • | risks related to our business strategy, areas of possible expansion or expected capital spending or operating expenses; |

| • | changes in the availability of crew, number of off-hire days, classification survey requirements and insurance costs for the vessels in our fleet; |

| • | changes in our ability to leverage the relationships and reputation in the drybulk shipping industry of V.Ships Limited, or V.Ships, our technical manager, and Fidelity Marine Inc., or Fidelity, our commercial manager; |

| • | changes in our relationships with our contract counterparties, including the failure of any of our contract counterparties to comply with their agreements with us; |

| • | loss of our customers, charters or vessels; |

| • | damage to our vessels; |

| • | potential liability from future litigation and incidents involving our vessels; |

| • | our future operating or financial results; |

| • | acts of terrorism and other hostilities; |

| • | changes in global and regional economic and political conditions; |

| • | changes in governmental rules and regulations or actions taken by regulatory authorities, particularly with respect to the drybulk shipping industry; |

| • | our ability to continue as a going concern; and |

| • | other factors listed from time to time in registration statements, reports or other materials that we have filed with or furnished to the U.S. Securities and Exchange Commission, or the Commission, including our most recent annual report on Form 20-F, which is incorporated by reference into this prospectus. |

Should one or more of the foregoing risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Consequently, there can be no assurance that actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected consequences to, or effects on, us. Given these uncertainties, prospective investors are cautioned not to place undue reliance on such forward-looking statements.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable laws. If one or more forward-looking statements are updated, no inference should be drawn that additional updates will be made with respect to those or other forward-looking statements.

iii

Table of Contents

ENFORCEABILITY OF CIVIL LIABILITIES

We are incorporated under the laws of the Republic of the Marshall Islands and our principal executive offices are located outside the United States. Certain of our directors and officers reside outside the United States. In addition, substantially all of our assets and the assets of certain of our directors and officers are located outside the United States. As a result, it may not be possible for you to serve legal process within the United States upon us or any of these persons. It may also not be possible for you to enforce, both in and outside the United States, judgments you may obtain in United States courts against us or these persons in any action, including actions based upon the civil liability provisions of U.S. federal or state securities laws.

Furthermore, there is substantial doubt that courts in jurisdictions outside of the U.S. (i) would enforce judgments of U.S. courts obtained in actions against us or our directors or officers based upon the civil liability provisions of applicable U.S. federal and state securities laws or (ii) would enforce, in original actions, liabilities against us or our directors or officers based on those laws.

iv

Table of Contents

This summary highlights certain information that appears elsewhere in this prospectus or in documents incorporated by reference herein, and this summary is qualified in its entirety by that more detailed information. This summary may not contain all of the information that may be important to you. We urge you to carefully read this entire prospectus and the documents incorporated by reference herein. As an investor or prospective investor, you should also review carefully the sections entitled “Cautionary Statement Regarding Forward-Looking Statements” and “Risk Factors” in this prospectus and in our Annual Report on Form 20-F for the year ended December 31, 2018.

Unless the context otherwise requires, as used in this prospectus, the terms “Company”, “Seanergy”, “we”, “us” and “our” refer to Seanergy Maritime Holdings Corp. and all of its subsidiaries, and “Seanergy Maritime Holdings Corp.” refers only to Seanergy Maritime Holdings Corp. and not to its subsidiaries. We use the term deadweight ton, or dwt, in describing the size of our vessels. Dwt, expressed in metric tons, each of which is equivalent to 1,000 kilograms, refers to the maximum weight of cargo and supplies that a vessel can carry. Unless otherwise indicated, all references in this prospectus to “$” or “dollars” are to U.S. dollars, and financial information presented in this prospectus is derived from the financial statements incorporated by reference in this prospectus that were prepared in accordance with accounting principles generally accepted in the United States, or U.S. GAAP.

Overview

We are Seanergy Maritime Holdings Corp., an international shipping company specializing in the worldwide seaborne transportation of drybulk commodities, primarily iron ore and coal. We believe we have established a reputation in the international drybulk shipping industry for operating and maintaining vessels with high standards of performance, reliability and safety. Our management team is comprised of executives with extensive experience operating large and diversified fleets, who have strong relationships to a growing number of international charterers.

Our fleet was acquired at a historically low point in the shipping cycle. In 2015, we acquired eight modern drybulk vessels (six Capesize and two Supramax vessels). In 2016 and 2017, we acquired three additional Capesize drybulk vessels. In October and November 2018, we sold our two Supramax vessels and purchased an additional Capesize vessel and we became the only pure-play Capesize shipping company publicly listed in the U.S. capital markets. We refer to the ten vessels that we presently operate as our “Fleet”. Since March 2015, we have invested approximately $300 million to acquire our Fleet.

We manage our vessels’ operations, insurances, claims and bunkering and have the general supervision of our third-party technical and commercial managers. Pursuant to technical management agreements with our vessel owning subsidiaries, V.Ships, an independent third party, provides technical management for our vessels that includes general administrative and support services, such as crewing and other technical management, accounting related to vessels and provisions. Fidelity, an independent third party, provides exclusive commercial management services for all of the vessels in our fleet pursuant to a commercial management agreement with Seanergy Management Corp., or Seanergy Management, our wholly-owned ship managing subsidiary. Seanergy Management provides us with certain other management services.

1

Table of Contents

Our Fleet

As of the date of this prospectus, we operate a fleet of ten Capesize drybulk vessels with a cargo-carrying capacity of approximately 1,748,581 dwt and an average age of approximately 10 years. The following table lists the vessels in our fleet as of the date of this prospectus:

Fleet

| Vessel Name |

Year Built | Dwt | Flag | Yard |

Type of Current Employment | |||||||||||

| Fellowship |

2010 | 179,701 | MI | Daewoo | Spot | |||||||||||

| Championship (1) |

2011 | 179,238 | MI | Sungdong | Time Charter, (or T/C), Index Linked (2) | |||||||||||

| Partnership |

2012 | 179,213 | MI | Hyundai | T/C Index Linked(3) | |||||||||||

| Knightship (4) |

2010 | 178,978 | LIB | Hyundai | Spot | |||||||||||

| Lordship |

2010 | 178,838 | LIB | Hyundai | T/C Index Linked(5) | |||||||||||

| Gloriuship |

2004 | 171,314 | MI | Hyundai | Spot | |||||||||||

| Leadership |

2001 | 171,199 | BA | Koyo-Imabari | Spot | |||||||||||

| Geniuship |

2010 | 170,058 | MI | Sungdong | Spot | |||||||||||

| Premiership |

2010 | 170,024 | IoM | Sungdong | Spot | |||||||||||

| Squireship |

2010 | 170,018 | LIB | Sungdong | Spot | |||||||||||

| Average Age/Total dwt: |

10 years | 1,748,581 | ||||||||||||||

| (1) | In November 2018, we entered into a financing arrangement with Cargill International SA, or Cargill, according to which this vessel was sold and leased back on a bareboat basis for a five-year period. We have a purchase obligation at the end of the five-year period and we further have the option to repurchase the vessel at any time during the bareboat charter. |

| (2) | This vessel is being chartered by Cargill. The vessel was delivered to the charterer on November 7, 2018 for a period of employment of 60 months, with an additional period of about 16 to about 18 months at the charterer’s option. The net daily charter hire is calculated at an index linked rate based on the five T/C routes of the Baltic Capesize Index, or the BCI TCE. In addition, the time charter provides us with the option to convert the index linked rate to a fixed rate for a period of between 3 and 12 months priced at the then prevailing Capesize forward freight agreement rate, or FFA, for the selected period. |

| (3) | This vessel is being chartered by Uniper Global Commodities SE, or Uniper, and was delivered to the charterer on December 11, 2018 in direct continuation of the vessel’s previous time charter, for a minimum of five months to a maximum of eight months. The net daily charter hire is calculated at an index linked rate based on the BCI TCE. In addition, the time charter provides us an option for any period of time, no less than three months, during the hire to be converted into a fixed rate time charter, with a rate corresponding to the prevailing value of the respective Capesize FFA. |

| (4) | In June 2018, we entered into a financing arrangement with AVIC International Leasing Co., Ltd., or AVIC, according to which this vessel was sold and leased back on a bareboat basis from AVIC’s affiliate, Hanchen Limited, or Hanchen, for an eight-year period. We have a purchase obligation at the end of the eight-year period and we further have the option to repurchase the vessel at any time following the second anniversary of delivery under the bareboat charter. |

| (5) | This vessel is being chartered by Oldendorff Carriers GmbH & Co. KG, or Oldendorff, and was delivered to the charterer on June 28, 2017, in direct continuation of the vessel’s previous time charter, for a period of about 18 months to about 22 months. The net daily charter hire is calculated at an index linked rate based on the BCI TCE. In addition, the time charter provides us with the option to convert the index linked rate to a fixed rate for a period of between 3 and 12 months priced at the then prevailing Capesize FFA for the selected period. |

Key to Flags:

BA – Bahamas, IoM – Isle of Man, LIB – Liberia, MI – Marshall Islands

2

Table of Contents

Drybulk Shipping Industry Trends

Based on information provided by Karatzas Marine Advisors & Co. LLC, or Karatzas Marine Advisors, our industry expert, we believe that the following industry trends create growth opportunities for us as an owner and operator of drybulk vessels:

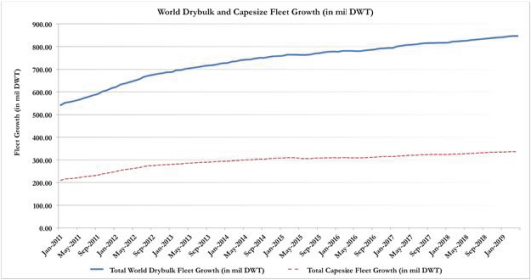

| • | drybulk fleet growth has declined every year from 2011 to 2016, while in 2018 fleet growth was 2.80%, one of the lowest growth rates in the last two decades. Given that the vessel orderbook is currently at a low level and the long lead-time involved in new vessel orders, fleet growth is expected to remain at historically low levels, typically below 3% per annum until 2021; |

| • | global economic activity and industrial production continues to rely on raw materials and commodity consumption. World drybulk trade increased by 2.5% in 2018 and is expected to increase by 2.4% in 2019; |

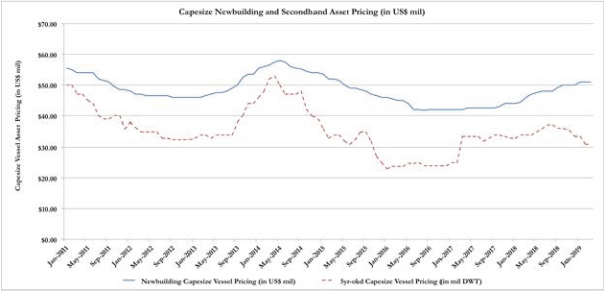

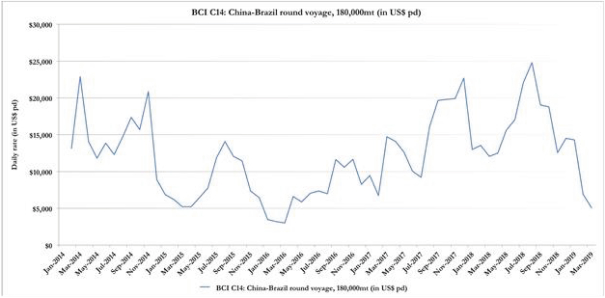

| • | in 2018 and year-to-date 2019, there has been a noticeable rise in vessel prices compared to the price levels seen in 2016. Prices for 5-year and 10-year old 180,000 dwt Capesize vessels averaged approximately $24.5 and $13.8 million, respectively, in 2016, while prices at the end of February 2019 stood at $32.5 million and $24.5 million, respectively. As a matter of comparison, the fifteen-year average for 5-year and 10-year-old Capesize vessels stand at $43 million and $31 million respectively, even when excluding years 2006-2008, considered years of a super-cycle. Despite the significant increase of 80%, which allows for an exit strategy and sale of the vessels, we believe there is upside potential since current asset prices are materially below the fifteen-year historical average; |

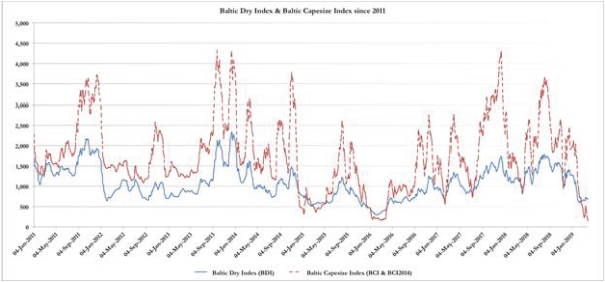

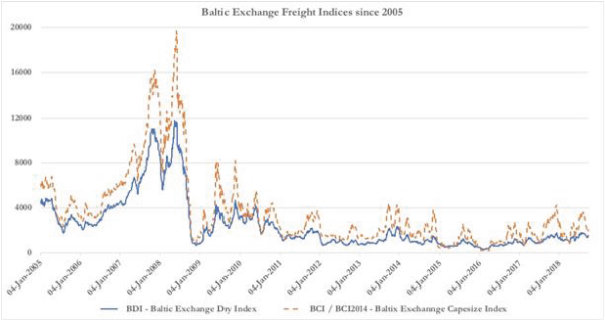

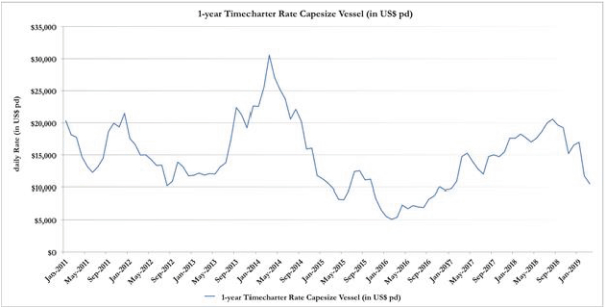

| • | as of February 28, 2019, the average of the BCI TCE, the generally agreed-upon index for spot Capesize shipping rates, was $5,290 per day, 14% higher than the average level in 2016; the fifteen-year average for short-term Capesize vessel time-charters was approximately $37,200 per day, or $25,500 per day when the years of the 2006-2008 super-cycle are excluded. The present Capesize freight market is materially lower than the historical average and we believe there is further upside potential for the market “reverting to the mean”; |

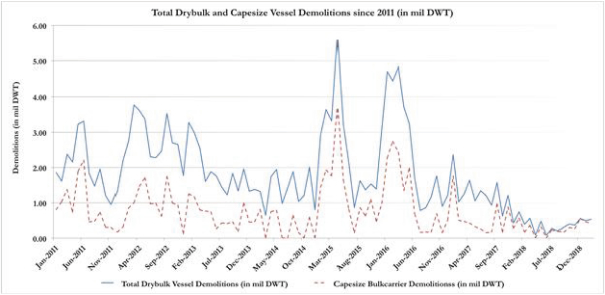

| • | the regulations enacted by the International Maritime Organization, or IMO, mandating higher maintenance standards of vessels, installation of ballast water management systems, and gradually lower emissions will require material capital investments that will render older drybulk vessels uneconomical for retrofitting and will expedite their demolition; and |

| • | charterers’ concerns about environmental and safety standards are shifting their preference toward modern vessels that are owned and operated by reputable and financially stable shipowners. |

The details on the industry trends set forth in this section have been prepared by Karatzas Marine Advisors. We and Karatzas Marine Advisors can provide no assurance, however, that the industry trends described above will continue, that we will be successful in capitalizing on any such opportunities or that we will be able to expand our business. For further discussion of the risks that we face, see “Risk Factors” beginning on page 17 of this prospectus. Please read “The International Drybulk Industry” for more information on the drybulk shipping industry.

Experienced Management

Our leadership has considerable shipping industry expertise. Mr. Tsantanis, our Chairman and Chief Executive Officer, brings more than 20 years of experience in shipping and finance and has held senior management positions in prominent shipping companies prior to leading our Company. Mr. Gyftakis, our Chief Financial Officer, has more than 13 years of experience in senior positions in the shipping finance industry. Our Chief Operations Officer, Chief Technical Officer and General Counsel have a combined experience of 54 years in senior positions in the shipping industry.

3

Table of Contents

Business Strategy & Strengths

Our business strategy is centered on managing our fleet in accordance with world-class standards to produce strong cash flows and to further expand our fleet to build our position as a reliable provider of international seaborne transportation services for drybulk commodities.

Our Fleet Composition

Focus on Capesize Vessels. Our fleet currently consists of ten modern-design Capesize vessels. We are the only pure-play Capesize shipping company listed in the U.S. capital markets. We expect our focus on a single type of vessel within the drybulk space to result in superior operational efficiency and commercial performance in this market. We believe, further, that our focus on the Capesize market will attract a broad shareholder base aiming to gain direct exposure to the favorable fundamentals of iron ore and coal transportation, while minimizing their exposure to the rest of the drybulk market that may be influenced by a much wider range of commodities. We believe our modern-design vessels, which were built at reputable Korean and Japanese shipyards, are preferred by charterers over older vessels since they require lower maintenance and typically have lower operating expenses. According to Karatzas Marine Advisors, seaborne transportation for iron ore and coal has increased by 2.2% in 2016, 4.6% in 2017 and 1.5% in 2018. In addition, the newbuilding orderbook for Capesize vessels currently represents approximately 4% of the current fleet, a significant reduction from the average size of the newbuilding orderbook of the fleet for the last 10 years. Our fleet is expected to be fully compliant with upcoming environmental and safety regulations.

Expanding Our Fleet Through Opportunistic Acquisitions and Disposals. We aim to acquire high-quality Capesize vessels through timely acquisitions at prices that are attractive when compared to the vessels’ future earnings potential. We currently view the Capesize vessel class as providing the highest returns in the drybulk space given existing vessel price levels. In evaluating acquisitions, we consider and analyze, among other things, our expectation of fundamental developments in the drybulk shipping industry sector, the level of liquidity in the resale and charter market, the vessel condition and technical specifications, the expected remaining useful life, as well as the overall strategic positioning of our fleet and customers. For vessels acquired with charters attached, we also consider the credit quality of the charterer and the duration and terms of the contracts in place. Based on our successful track record, commercial expertise and reputation in the marketplace as well as our transparent and public corporate structure, we believe that we are well-positioned to source off-market opportunities to acquire secondhand vessels. As a result, our Company may be able to acquire vessels on more favorable terms than what would be obtained without access to such opportunities.

Assembling a Modern-design Capesize Fleet with Critical Mass. In today’s competitive world, shipping companies with larger fleets can benefit from economies of scale by reducing operating expenses per vessel due to volume price discounting; larger fleets are also preferred by the charterers as they can benefit from such economies of scale themselves. More importantly, shipping companies with larger fleets have better access to financing on competitive terms from shipping banks and lessors, as well as from institutional investors and the capital markets.

Our Fleet Deployment

Revenue Upside Potential through Spot Market Exposure. We believe our current fleet is positioned to capture increasing vessel revenues because of an expected upward trend in spot charter rates. As of the date of this prospectus, our entire fleet is employed in the spot market or under index-linked time charters that allow us to benefit from spot market improvements. The BCI TCE, increased significantly in 2018 by 649% from a record low level of $2,166 per day during March 2016 to $16,213 per day in December 2018. Despite a seasonal softening seen in earnings in the first quarter of 2019, it is expected that the positive trend established in the previous 3 years will continue going forward. The average daily BCI TCE of the last fifteen years from

4

Table of Contents

March 2004 until March 2019 is $37,200. As spot charter rates revert to long-term average levels, we may shift towards employing a greater proportion of our fleet under long term fixed-rate contracts in order to minimize downside risk. Because the spot market is volatile, there can be no assurance that the recent improvements in the drybulk charter market will continue.

Access to Attractive Chartering Opportunities. Our senior management in combination with Fidelity, our commercial manager, has established strong relationships with international miners, charterers and brokers. We believe that these relationships should provide us with access to attractive chartering opportunities. Furthermore, we aim to maintain our fleet at a level that meets or exceeds stringent industry standards as we believe that owning a modern and well-maintained fleet provides us with a competitive advantage in securing favorable employment. It should be noted that despite our management team’s deep industry experience and high-quality fleet, we expect the daily rates obtained on future time and spot charters to still be subject to market fluctuations. As a demonstration of our ability to source attractive employment opportunities, five of our vessels have recently entered long-term T/Cs with durations of three to five years, two of which have already commenced and the remaining three will commence in the third and/or fourth quarter of 2019. As part of the agreements, the charterers have agreed to cover the costs for the installation of exhaust gas cleaning systems, or scrubbers, on our vessels to ensure compliance with the IMO Global Sulphur Cap rules that will be in effect after January 1, 2020. We believe that the willingness of our charterers to invest in our vessels is a testament to the attractive employment opportunities enjoyed by our fleet.

Our Management Structure

Cost Efficient External Commercial and Technical Management. We manage our vessels’ operations, insurance policies and bunkering and have the general supervision of our third-party technical and commercial managers.

V.Ships, an independent third party, provides technical management for our vessels that includes general administrative and support services, such as crewing and other technical management, accounting related to vessels and provisions. Pursuant to our technical management agreements with V.Ships we paid a monthly fee of $8,000 per vessel in 2018 and we have been paying a monthly fee of about $8,200 per vessel starting from January 1, 2019, in exchange for V.Ships providing these technical, support and administrative services. The management fees do not cover expenses such as voyage expenses, vessel operating expenses, maintenance expenses, crewing costs, which are reimbursed by us to V.Ships. The technical management agreements are for an indefinite period until terminated by either party, giving the other notice in writing, in which event the applicable agreement shall terminate after one month from the date upon which such notice is received.

Seanergy Management has entered into a commercial management agreement with Fidelity, an independent third party, pursuant to which Fidelity provides commercial management services for all of the vessels in our fleet. Fidelity serves as commercial broker for Capesize vessels exclusively to us. Under the commercial management agreement, we have agreed to pay the following fees to Fidelity: (i) an annualized net fee of €120,000 payable in twelve equal monthly payments and (ii) a commission fee equal to 0.15% calculated on the collected gross hire/freight/demurrage payable when the relevant hire/freight/demurrage is collected, provided that on an annual basis the total fees payable under (i) and (ii) are capped at $300,000 net. The commercial management agreement may be terminated by either party upon giving one-month prior written notice to the other party or by mutual written agreement without prior notice.

Seanergy Management also provides certain administrative, financial and managerial services to our vessel-owning subsidiaries.

Leverage Manager’s Industry Reputation. We believe that our commercial manager’s and management team’s reputations within the shipping industry and relationship with many of the world’s leading global

5

Table of Contents

charterers, commodity traders and industrial users provide us with numerous benefits that are key to our growth and success. Our commercial manager’s strong track record of high-quality and efficient operations has allowed us to successfully satisfy the operational, safety, environmental and technical vetting criteria of many of the world’s major charterers, including among others Rio Tinto Group, BHP Billiton, Trafigura Group, Glencore plc, Uniper SE, Cargill, Oldendorff, and Fortescue Metals Group Ltd.

Dividend Policy

The declaration, timing and amount of any dividend is subject to the discretion of our board of directors and will be dependent upon our earnings, financial condition, market prospects, capital expenditure requirements, investment opportunities, restrictions in our loan agreements, the provisions of the Marshall Islands law affecting the payment of dividends to shareholders, overall market conditions and other factors. We have not declared any dividends since our inception. Our board of directors may review and amend our dividend policy from time to time in light of our plans for future growth and other factors. In addition, since we are a holding company with no material assets other than the shares of our subsidiaries and affiliates through which we conduct our operations, our ability to pay dividends will depend on our subsidiaries and affiliates distributing to us their earnings and cash flow. Some of our loan agreements limit our ability to pay dividends and our subsidiaries’ ability to make distributions to us. Please see “Item 5. Operating and Financial Review and Prospects – B. Liquidity and Capital Resources – Loan Arrangements” of our audited consolidated financial statements in our Annual Report on Form 20-F, filed with the Commission on March 25, 2019, or the Annual Report, which is incorporated by reference herein.

Borrowing Activities

We currently have six senior secured loan facilities with commercial lenders with an aggregate outstanding balance of $151.2 million, two junior secured loan facilities and one unsecured loan facility with Jelco Delta Holding Corp., or Jelco, a company affiliated with Claudia Restis, who is our principal shareholder, or Sponsor, with an outstanding balance of $24.4 million as of the date of this prospectus and two sale and leaseback financing agreements, with unrelated third parties, with an outstanding balance of $43.9 million as of the date of this prospectus.

The senior secured loan facility with Alpha Bank AE, originally entered into in March 2015, as amended to date, has a maturity date of March 17, 2020, an outstanding balance of $5.6 million as of the date of this prospectus and is repayable through quarterly payments and a balloon instalment of $4.45 million payable at maturity. The senior secured loan facility with Hamburg Commercial Bank AG (formerly known as HSH Nordbank AG), or HCOB, originally entered into in September 2015, as amended to date, has a maturity date of June 30, 2020, an outstanding balance of $34.1 million as of the date of this prospectus and is repayable through quarterly payments and a balloon instalment of $28.8 million payable at maturity. The senior secured loan facility with UniCredit Bank AG, or UniCredit, originally entered into in September 2015, as amended to date, has a maturity date of December 28, 2020, an outstanding balance of $40.8 million as of the date of this prospectus and is repayable through quarterly payments and a balloon instalment of $29.4 million payable at maturity. The senior secured loan facility with Alpha Bank AE, originally entered into in November 2015, as amended to date, has a maturity date of November 10, 2021, an outstanding balance of $29.5 million as of the date of this prospectus and is repayable through quarterly payments and a balloon instalment of $20.25 million payable at maturity. The senior secured loan facility with Amsterdam Trade Bank N.V., or ATB, for a total balance of up to $20.9 million, entered into in February 2019, has a maturity date of November 26, 2022, an outstanding balance of $17.3 million as of the date of this prospectus and is repayable through quarterly installments and a balloon instalment of $13.2 million payable at maturity. Lastly, the senior secured loan facility provided by with Blue Ocean maritime lending funds managed by EnTrustPermal (Wilmington Trust), was

6

Table of Contents

entered into in June 2018, has a maturity date of June 13, 2023, an outstanding balance of $23.9 million as of the date of this prospectus and is repayable through quarterly payments and a balloon instalment of $15.3 million payable at maturity.

Additionally, the junior secured loan facility with Jelco, originally entered into in October 2016, as amended to date, has an outstanding balance of $5.9 million as of the date of this prospectus. The junior secured loan facility with Jelco, originally entered into in May 2017, as amended to date has an outstanding balance of $11.5 million as of the date of this prospectus. Lastly, the unsecured loan facility with Jelco, entered into in March 2019, has an outstanding balance of $7.0 million as of the date of this prospectus.

In June 2018, we entered into an agreement with Hanchen for the sale and leaseback of the Knightship. Under the terms of the agreement, the Knightship was sold for an amount of $26.5 million and was leased back on a bareboat basis for a period of eight years. We have an obligation to purchase the vessel at the end of the eight-year period at a price of $5.3 million. As of the date of this prospectus, the amount outstanding is $18.5 million and is repayable through quarterly payments extending up to the date of the purchase obligation.

In November 2018 we entered into a $26.25 million sale and leaseback agreement for the Championship with Cargill. We sold and chartered back the vessel on a bareboat basis for a five-year period, having a purchase obligation at the end of the fifth year at a price of $14.1 million. As of the date of this prospectus, the amount outstanding is $25.4 million and is repayable through monthly payments of $0.17 million each extending up to the date of the purchase obligation.

As of the date of this prospectus, we are in compliance with all applicable financial covenants under our loan facilities. In February and March 2019, we received approval from the credit committees of certain of our lenders to (i) amend the applicable thresholds of certain financial covenants of its credit facilities until March 31, 2020 and (ii) defer a total of $3.3 million of debt installments that were originally scheduled for 2019 to dates falling in 2020 and 2021. The approvals are subject to the completion of definitive documentation.

On March 26, 2019, we entered into a $7.0 million loan facility with Jelco, the proceeds of which were utilized to (i) refinance a previous working capital loan provided by Jelco with outstanding balance of $2.0 million and (ii) for general corporate purposes. We drew down the entire $7.0 million on March 27, 2019.

As part of the approvals with certain of our lenders, on April 1, 2019, we entered into a supplemental agreement to the facility with HCOB. Pursuant to the terms of the supplemental agreement the Leverage Ratio as defined in the agreement shall not exceed 85% until March 31, 2020 and 75% starting from April 1, 2020. The ratio of EBITDA to interest payments as defined in the supplemental agreement shall not be less than 1:1 until March 31, 2020 and 2:1 starting from April 1, 2020.

In the absence of a significant deterioration in market conditions, we expect to remain in compliance with all applicable financial covenants following such expiration or adjustment of the currently reduced thresholds in 2019.

For more information regarding our current loan facilities, please see “Item 5. Operating and Financial Review and Prospects – B. Liquidity and Capital Resources – Loan Arrangements” in our Annual Report.

7

Table of Contents

Concurrent Private Placement

Jelco, our principal shareholder, has agreed to participate in a private placement of $6,200,000 of units at the public offering price. As consideration for the units, Jelco has agreed to (i) the waiver of our obligation to make interest payments accrued through March 31, 2019 under our debt facilities with Jelco in an aggregate amount of approximately $2.11 million, (ii) the elimination of interest payments under our debt facilities with Jelco for the period between April 1, 2019 and December 31, 2019 in an aggregate amount of approximately $3.85 million, and (iii) with respect to this offering, the waiver of the mandatory prepayment requirement under our loan agreement with Jelco dated March 26, 2019. The private placement is subject to definitive documentation and other customary closing conditions. Each such unit issued in the private placement to Jelco would consist of one common share, one Class B Warrant and one Class C Warrant, and the closing of such private placement is conditioned upon the closing of this offering.

Corporate Information

We were incorporated under the laws of the Republic of the Marshall Islands on January 4, 2008, originally under the name Seanergy Merger Corp., as a wholly-owned subsidiary of Seanergy Maritime Corp. We changed our name to Seanergy Maritime Holdings Corp. on July 11, 2008. Our principal executive office is located at 154 Vouliagmenis Avenue, 166 74 Glyfada, Athens, Greece. Our registered office is located at Ajeltake Road, Ajeltake Island, Majuro, Marshall Islands MH 96960. Our registered agent in the Republic of the Marshall Islands is: The Trust Company of the Marshall Islands, Inc., Trust Company Complex, Ajeltake Road, Ajeltake Island, Majuro, Marshall Islands MH 96960. Our principal executive office telephone number is +30 213 0181507. Our corporate website address is www.seanergymaritime.com. The information contained on our website does not constitute part of this prospectus. The SEC maintains a website that contains reports, proxy and information statements, and other information that we file electronically at www.sec.gov.

8

Table of Contents

| Common shares presently outstanding |

2,809,223 common shares(1) |

| Securities offered by us |

3,685,500 units, each unit consisting of (i) one common share or pre-funded warrant, (ii) one Class B Warrant to purchase one common share and (iii) one Class C Warrant to purchase one common share. |

| Each Class B Warrant will have an exercise price of $ per share, subject to downward adjustment under certain circumstances seven months after issuance, will be exercisable upon issuance and will expire three years from issuance. Each Class C Warrant will have an exercise price of $ per share, will be exercisable upon issuance, and will expire six months from issuance. Beginning 30 days after issuance, each Class C Warrant will be exercisable on a cashless basis under certain circumstances for a number of common shares calculated according to a formula based on the market price at the time of exercise. |

| We are also offering to each purchaser, with respect to the purchase of units that would otherwise result in the purchaser’s beneficial ownership exceeding 4.99% of our outstanding common shares immediately following the consummation of this offering, the opportunity to purchase units including one pre-funded warrant in lieu of one common share in the unit. Subject to limited exceptions, a holder of pre-funded warrants will not have the right to exercise any portion of its pre-funded warrant if the holder, together with its affiliates, would beneficially own in excess of 4.99% (or, at the election of the holder, such limit may be increased to up to 9.99%) of the number of common shares outstanding immediately after giving effect to such exercise. Each pre-funded warrant will be exercisable for one common share. The purchase price of each unit including a pre-funded warrant will be equal to the price per unit including one common share, minus $0.01, and the remaining exercise price of each pre-funded warrant will equal $0.01 per share. The pre-funded warrants will be immediately exercisable and may be exercised at any time until all of the pre-funded warrants are exercised in full. For each unit including a pre-funded warrant we sell (without regard to any limitation on exercise set forth therein), the number of common shares in the units we are offering will be decreased on a one-for-one basis. Each pre-funded warrant is being sold in a unit with a Class B Warrant and a Class C Warrant, each with the same terms as the Class B Warrants and Class C Warrants accompanying the common shares. Because one Class B Warrant and one Class C Warrant are being sold together in this offering with each common share or, in the alternative, with each pre-funded warrant to purchase one common share, the number of Class B Warrants and Class C Warrants sold in this offering will not change as a result of a change in the mix of our common shares and pre-funded warrants sold. |

9

Table of Contents

| The common shares and pre-funded warrants, if any, can each be purchased in this offering only with the accompanying Class B Warrants and Class C Warrants (other than pursuant to the underwriters’ option to purchase additional securities) as part of a unit, but the components of the units will immediately separate upon issuance. |

| Common shares to be outstanding immediately after this offering |

6,494,723 common shares (7,047,548 common shares if the underwriters exercise their option to purchase additional units in full), assuming no issuance of pre-funded warrants in this offering and no exercise of the Class B Warrants, Class C Warrants or Representative’s Warrant(2) |

| Underwriters’ Over-Allotment Option |

We have granted the underwriters an option for a period of up to 45 days to purchase up to 552,825 additional common shares or pre-funded warrants, 552,825 Class B Warrants and/or 552,825 Class C Warrants. |

| Use of proceeds |

We estimate that we will receive net proceeds of approximately $ million, and approximately $ million if the underwriters exercise their option to purchase additional units in full, after deducting underwriting discounts and commissions and estimated expenses payable by us. |

| We intend to use the net proceeds of this offering for general corporate purposes, which may include, among other things, prepaying debt or partially funding the acquisition of modern Capesize drybulk vessels in accordance with our growth strategy. However, we do not currently have definitive plans for any debt prepayments nor have we identified any potential acquisitions, and we can provide no assurance that we will be able to complete any debt prepayment or the acquisition of any vessel that we are able to identify. See “Use of Proceeds.” |

| Risk factors |

Investing in our securities involves a high degree of risk. See “Risk Factors” below, beginning on page 17, and in our Annual Report on Form 20-F for the year ended December 31, 2018, which is incorporated by reference herein, to read about the risks you should consider before investing in our securities. |

| Listing |

Our common shares and Class A Warrants are listed on the Nasdaq Capital Market under the symbols “SHIP” and “SHIPW”, respectively. We have applied to list the Class B Warrants offered hereunder on the Nasdaq Capital Market. |

| Lock-up agreements |

Subject to certain exceptions, we, all of our executive officers and directors, and certain affiliates have entered into lock-up agreements with the underwriters. Under these agreements, we and each of these persons may not, without the prior written approval of Maxim Group LLC, as representative of the underwriters, offer, sell, contract to sell or otherwise dispose of or hedge common shares or securities convertible into or exchangeable for common shares. These restrictions will be in effect for a period of 120 days after the date of the closing of this offering. |

10

Table of Contents

| (1) | Excludes 2,867,776 shares issuable upon exercise of convertible notes comprised of: |

| • | 281,481 common shares issuable upon exercise of a conversion option pursuant to the convertible note, dated March 12, 2015, as amended, that we issued to Jelco, |

| • | 1,567,777 common shares issuable upon exercise of a conversion option pursuant to the revolving convertible note, dated September 7, 2015, as amended, that we issued to Jelco, and |

| • | 1,018,518 common shares issuable upon exercise of a conversion option pursuant to the convertible note, dated September 27, 2017, as amended, that we issued to Jelco. |

Under each of the convertible notes, Jelco may, at its option, convert the whole or any part of the principal amount under each note at any time into common shares at a conversion price of $13.50 per share. As of the date of this prospectus, $38.72 million of convertible notes was outstanding comprised of:

| • | $3.8 million outstanding under the convertible note, dated March 12, 2015, |

| • | $21.17 million outstanding under the revolving convertible note dated September 7, 2015 and |

| • | $13.75 million outstanding under the convertible note, dated September 27, 2017. |

As of the date of this prospectus, an amount of $3.5 million was available but undrawn under the revolving convertible note, dated September 7, 2015.

| (2) | The number of common shares that will be outstanding after this offering excludes: |

| • | 766,666 common shares issuable upon the exercise of outstanding Class A Warrants at an exercise price of $30.00 per share; |

| • | 37,666 common shares issuable upon the exercise of two outstanding warrants previously issued to the Representative at an exercise price of $28.13 per share; |

| • | common shares issuable upon exercise of the warrants to be issued to the investors and the Representative in connection with this offering; |

| • | common shares issuable upon exercise of the underwriter’s option to purchase additional securities to cover over-allotments; and |

| • | any common shares issued to Jelco as part of units, and any common shares issuable on exercise of warrants included in such units issued to Jelco, in the private placement expected to be consummated following the closing of this offering. See “The Offering — Concurrent Private Placement.” |

11

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The information set forth below should be read in conjunction with “Capitalization” and our audited and unaudited consolidated financial statements and related notes incorporated by reference herein.

We derived the following consolidated financial data for the years ended as of December 31, 2018, 2017, 2016, 2015 and 2014 from our audited consolidated financial statements, as presented in our most recent annual report on Form 20-F, which is incorporated by reference in this prospectus.

On January 8, 2016, we effected a 1-for-5 reverse split of our common shares. The reverse stock split became effective and the common shares began trading on a split-adjusted basis on the Nasdaq Capital Market at the opening of trading on January 8, 2016. On March 19, 2019, we effected a 1-for-15 reverse split of our common shares in order to cure a deficiency in the minimum bid price of our common shares trading on the Nasdaq Capital Market. The reverse stock split became effective and the common shares began trading on a split-adjusted basis on the Nasdaq Capital Market at the opening of trading on March 20, 2019. On April 3, 2019, we received notice from Nasdaq that we had regained compliance with the listing requirements. As a result of these reverse stock splits, there was no change in the number of authorized shares or the par value of our common shares. All share and per share amounts disclosed herein give effect to these reverse stock splits retroactively, for all periods presented.

12

Table of Contents

Based on our audited consolidated financial statements:

(Amounts in the tables below are in thousands of U.S. dollars, except for share and per share data.)

| Year Ended December 31, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Statement of Income Data: |

||||||||||||||||||||

| Vessel revenue, net |

91,520 | 74,834 | 34,662 | 11,223 | 2,010 | |||||||||||||||

| Voyage expenses |

(40,184 | ) | (34,949 | ) | (21,008 | ) | (7,496 | ) | (1,274 | ) | ||||||||||

| Vessel operating expenses |

(20,742 | ) | (19,598 | ) | (14,251 | ) | (5,639 | ) | (1,006 | ) | ||||||||||

| Voyage expenses - related party |

— | — | — | — | (24 | ) | ||||||||||||||

| Management fees - related party |

— | — | — | — | (122 | ) | ||||||||||||||

| Management fees |

(1,042 | ) | (1,016 | ) | (895 | ) | (336 | ) | — | |||||||||||

| General and administration expenses |

(6,500 | ) | (5,081 | ) | (4,134 | ) | (2,804 | ) | (2,987 | ) | ||||||||||

| General and administration expenses - related party |

— | — | — | (70 | ) | (309 | ) | |||||||||||||

| Loss on bad debts |

— | — | — | (30 | ) | (38 | ) | |||||||||||||

| Amortization of deferred dry-docking costs |

(634 | ) | (870 | ) | (556 | ) | (38 | ) | — | |||||||||||

| Depreciation |

(10,876 | ) | (10,518 | ) | (8,531 | ) | (1,865 | ) | (3 | ) | ||||||||||

| Impairment loss |

(7,267 | ) | — | — | — | — | ||||||||||||||

| Gain on restructuring |

— | — | — | — | 85,563 | |||||||||||||||

| Operating income / (loss) |

4,275 | 2,802 | (14,713 | ) | (7,055 | ) | 81,810 | |||||||||||||

| Interest and finance costs |

(16,415 | ) | (12,277 | ) | (7,235 | ) | (1,460 | ) | (1,463 | ) | ||||||||||

| Interest and finance costs - related party |

(8,881 | ) | (5,122 | ) | (2,616 | ) | (399 | ) | — | |||||||||||

| Gain on debt refinancing |

— | 11,392 | — | — | — | |||||||||||||||

| Interest and other income |

83 | 47 | 20 | — | 14 | |||||||||||||||

| Foreign currency exchange losses, net |

(104 | ) | (77 | ) | (45 | ) | (42 | ) | (13 | ) | ||||||||||

| Total other expenses, net |

(25,317 | ) | (6,037 | ) | (9,876 | ) | (1,901 | ) | (1,462 | ) | ||||||||||

| Net (loss) / income before taxes |

(21,042 | ) | (3,235 | ) | (24,589 | ) | (8,956 | ) | 80,348 | |||||||||||

| Income taxes |

(16 | ) | — | (34 | ) | — | — | |||||||||||||

| Net (loss) / income |

(21,058 | ) | (3,235 | ) | (24,623 | ) | (8,956 | ) | 80,348 | |||||||||||

| Net (loss) / income per common share |

||||||||||||||||||||

| Basic |

(8.40 | ) | (1.35 | ) | (17.97 | ) | (12.47 | ) | 450.90 | |||||||||||

| Weighted average common shares outstanding |

||||||||||||||||||||

| Basic |

2,507,087 | 2,389,719 | 1,370,200 | 718,226 | 178,196 | |||||||||||||||

| As of December 31, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Cash and cash equivalents and restricted cash |

$ | 7,444 | $ | 11,039 | $ | 15,908 | $ | 3,354 | $ | 2,873 | ||||||||||

| Total current assets |

16,883 | 19,498 | 22,329 | 8,278 | 3,207 | |||||||||||||||

| Vessels, net |

243,214 | 254,730 | 232,109 | 199,840 | — | |||||||||||||||

| Total assets |

267,562 | 275,705 | 257,534 | 209,352 | 3,268 | |||||||||||||||

| Total current liabilities |

36,263 | 34,460 | 21,230 | 9,250 | 592 | |||||||||||||||

| Long-term debt and other financial liabilities, net of current portion and deferred finance costs |

179,026 | 175,805 | 198,497 | 176,787 | — | |||||||||||||||

| Due to related parties, noncurrent |

19,349 | 17,342 | 5,878 | — | — | |||||||||||||||

| Long-term portion of convertible notes |

11,124 | 6,785 | 1,097 | 31 | — | |||||||||||||||

| Total Shareholders’ equity / (deficit) |

$ | 21,303 | $ | 41,313 | $ | 30,832 | $ | 23,284 | $ | 2,676 | ||||||||||

13

Table of Contents

| Year Ended December 31, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Cash Flow Data: |

||||||||||||||||||||

| Net cash provided by / (used in) operating activities |

$ | 5,723 | $ | 2,782 | $ | (15,339 | ) | $ | (4,737 | ) | $ | (14,858 | ) | |||||||

| Net cash (used in) / provided by investing activities |

(8,827 | ) | (32,992 | ) | (40,779 | ) | (201,684 | ) | 105,895 | |||||||||||

| Net cash provided by / (used in) financing activities |

(491 | ) | 25,341 | 68,672 | 206,902 | (91,239 | ) | |||||||||||||

| Net (decrease) / increase in cash and cash equivalents and restricted cash |

(3,595 | ) | (4,869 | ) | 12,554 | 481 | (202 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Performance Indicators

The figures shown below are non-GAAP statistical ratios used by management to measure performance of our vessels. For the “Fleet Data” figures, there are no comparable U.S. GAAP measures.

| Year Ended December 31, | ||||||||||||

| Fleet Data: | 2018 | 2017 | 2016 | |||||||||

| Ownership days(1) |

3,931 | 3,864 | 2,978 | |||||||||

| Available days(2) |

3,918 | 3,851 | 2,755 | |||||||||

| Operating days(3) |

3,902 | 3,837 | 2,745 | |||||||||

| Fleet utilization(4) |

99 | % | 99 | % | 92 | % | ||||||

| Fleet utilization excluding dry-docking off hire days |

100 | % | 100 | % | 100 | % | ||||||

| Average Daily Results: |

||||||||||||

| TCE rate(5) |

$ | 13,156 | $ | 10,395 | $ | 4,974 | ||||||

| Daily Vessel Operating Expenses(6) |

$ | 5,198 | $ | 4,985 | $ | 4,618 | ||||||

| 1) | Ownership days are the total number of calendar days in a period during which we owned or chartered in on bareboat basis each vessel in our fleet. Ownership days are an indicator of the size of our fleet over a period and affect both the amount of revenues and the amount of expenses recorded during that period. |

| 2) | Available days are the number of ownership days less the aggregate number of days that our vessels are off-hire due to major repairs, dry-dockings, lay-up or special or intermediate surveys. The shipping industry uses available days to measure the aggregate number of days in a period during which vessels are available to generate revenues. During the year ended December 31, 2018, we incurred 16 off-hire days. During the year ended December 31, 2017, we incurred 13 off-hire days for one vessel drydocking. During the year ended December 31, 2016, we incurred 173 off-hire days for a vessel lay-up and 64 off-hire days for two vessel surveys. |

| 3) | Operating days are the number of available days in a period less the aggregate number of days that our vessels are off-hire due to unforeseen circumstances. Operating days include the days that our vessels are in ballast voyages without having fixed their next employment. The shipping industry uses operating days to measure the aggregate number of days in a period during which vessels could actually generate revenues. During the year ended December 31, 2018, we incurred 16 off-hires days due to other unforeseen circumstances. During the year ended December 31, 2017, we incurred 13 off-hires days due to other unforeseen circumstances. |

| 4) | Fleet utilization is the percentage of time that our vessels were generating revenues and is determined by dividing operating days by ownership days for the relevant period. |

| 5) | Time Charter Equivalent, or TCE, rate is defined as our net revenue less voyage expenses during a period divided by the number of our operating days during the period. Voyage expenses include port charges, bunker expenses, canal charges and other commissions. We include TCE rate, a non-GAAP measure, as we believe it provides additional meaningful information in conjunction with net revenues from vessels, the most directly comparable U.S. GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and in evaluating their financial performance. Our |

14

Table of Contents

| calculation of TCE rate may not be comparable to that reported by other companies. The following table reconciles our net revenues to TCE rate. |

| Year Ended December 31, | ||||||||||||

| (In thousands of US Dollars, except operating days and TCE rate) | 2018 | 2017 | 2016 | |||||||||

| Net revenues from vessels |

$ | 91,520 | $ | 74,834 | $ | 34,662 | ||||||

| Voyage expenses |

(40,184 | ) | (34,949 | ) | (21,008 | ) | ||||||

| Net operating revenues |

$ | 51,336 | $ | 39,885 | $ | 13,654 | ||||||

| Operating days |

3,902 | 3,837 | 2,745 | |||||||||

| Daily time charter equivalent rate |

$ | 13,156 | $ | 10,395 | $ | 4,974 | ||||||

| 6) | Vessel operating expenses include crew costs, provisions, deck and engine stores, lubricants, insurance, maintenance and repairs. Daily Vessel Operating Expenses are calculated by dividing vessel operating expenses by ownership days for the relevant time periods. We include Daily Vessel Operating Expenses, a non-GAAP measure, as we believe it provides additional meaningful information in conjunction with vessel operating expenses, the most directly comparable U.S. GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and in evaluating their financial performance. Our calculation of Daily Vessel Operating Expenses may not be comparable to that reported by other companies. The following table reconciles our vessel operating expenses to Daily Vessel Operating Expenses. |

| (In thousands of US Dollars, except ownership days and Daily Vessel Operating Expenses) |

Year Ended December 31, | |||||||||||

| 2018 | 2017 | 2016 | ||||||||||

| Vessel operating expenses |

$ | 20,742 | $ | 19,598 | $ | 14,251 | ||||||

| Less: Pre-delivery expenses |

(309 | ) | (337 | ) | (499 | ) | ||||||

| Vessel operating expenses before pre-delivery expenses |

$ | 20,433 | $ | 19,261 | $ | 13,752 | ||||||

| Ownership days |

3,931 | 3,864 | 2,978 | |||||||||

| Daily Vessel Operating Expenses |

$ | 5,198 | $ | 4,985 | $ | 4,618 | ||||||

| Year Ended December 31, | ||||||||||||

| 2018 | 2017 | 2016 | ||||||||||

| Net loss |

$ | (21,058 | ) | $ | (3,235 | ) | $ | (24,623 | ) | |||

| Add: Net interest and finance cost |

25,213 | 17,352 | 9,831 | |||||||||

| Add: Taxes |

16 | — | 34 | |||||||||

| Add: Depreciation and amortization |

11,510 | 11,388 | 9,087 | |||||||||

| EBITDA |

15,681 | 25,505 | (5,671 | ) | ||||||||

| Add: Impairment loss |

7,267 | — | — | |||||||||

| Less: Gain on debt refinancing |

— | 11,392 | — | |||||||||

| Adjusted EBITDA |

$ | 22,948 | $ | 14,113 | $ | (5,671 | ) | |||||

|

|

|

|

|

|

|

|||||||

15

Table of Contents

| 1) | Earnings before interest, taxes, depreciation and amortization, or “EBITDA”, represents the sum of net income/(loss), interest and finance costs, interest income, depreciation and amortization and, if any, income taxes during a period. EBITDA is not a recognized measurement under U.S. GAAP. EBITDA is presented because we believe that this measure is useful to investors as a widely-used means of evaluating operating profitability. EBITDA as presented here may not be comparable to similarly-titled measures presented by other companies. This non-GAAP measure should not be considered in isolation from, as a substitute for, or superior to, financial measures prepared in accordance with U.S. GAAP. |

| Year Ended December 31, | ||||||||||||

| 2018 | 2017 | 2016 | ||||||||||

| Net loss |

$ | (21,058 | ) | $ | (3,235 | ) | $ | (24,623 | ) | |||

| Add: Impairment loss |

7,267 | — | — | |||||||||

| Less: Gain on debt refinancing |

— | 11,392 | — | |||||||||

| Adjusted loss |

$ | (13,791 | ) | $ | (14,627 | ) | $ | (24,623 | ) | |||

16

Table of Contents

An investment in our securities involves a high degree of risk. Before deciding to invest in our securities, you should carefully consider the risks described below and all of the other information contained or incorporated by reference into this prospectus. These risks and uncertainties are not the only risks and uncertainties that we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations. If any of these risks actually occurs, our business, financial condition, results of operations and future growth prospects could be materially adversely affected. In that case, you may lose all or part of your investment in the securities.

Risks Relating to Our Industry

The market values of our vessels may decrease, which could limit the amount of funds that we can borrow or trigger certain financial covenants under our loan agreements, and we may incur an impairment or, if we sell vessels following a decline in their market value, a loss.

The fair market values of our vessels are related to prevailing freight charter rates. While the fair market value of vessels and the freight charter market have a very close relationship as the charter market moves from trough to peak, the time lag between the effect of charter rates on market values of ships can vary. A decrease in the market value of our vessels could require us to raise additional capital in order to remain compliant with our loan covenants and could result in the loss of our vessels and adversely affect our earnings and financial condition.

The fair market value of our vessels may increase or decrease, and we expect the market values to fluctuate depending on a number of factors including:

| • | prevailing level of charter rates; |

| • | general economic and market conditions affecting the shipping industry; |

| • | types and sizes of vessels; |

| • | supply and demand for vessels; |

| • | other modes of transportation; |

| • | cost of newbuildings; |

| • | governmental and other regulations; and |

| • | technological advances. |

In addition, as vessels grow older, they generally decline in value. If the fair market value of our vessels declines, we may not be in compliance with certain covenants in our loan agreements, and our lenders could accelerate our indebtedness or require us to pay down our indebtedness to a level where we are again in compliance with our loan covenants. If any of our loans are accelerated, we may not be able to refinance our debt or obtain additional funding. We expect that we will enter into more loan agreements in connection with our future acquisitions of vessels. For more information regarding our current loan facilities, please see “Item 5. Operating and Financial Review and Prospects – B. Liquidity and Capital Resources – Loan Arrangements – Credit Facilities” in our Report on Form 20-F filed with the Commission on March 25, 2019.