Findell Capital Management Issues Statement to Board of Oportun Financial Corporation (OPRT)

Tweet

Tweet Share

ShareGet Alerts OPRT Hot Sheet

Join SI Premium – FREE

Findell Capital Management LLC, ("

The full letter can be read below or can be found at www.findell.us/letters

In summary,

We believe that this overhead must be dramatically cut down and the various fintech initiatives re-examined. For this to happen,

Under such leadership, we believe

Dear Board Members of

We are writing to you as shareholders with a ~4% stake in

Since

We believe this abysmal performance is the direct result of management's strategic decisions coupled with an alarming lack of cost discipline. Rather than remain focused on their proven core competency in providing loans to underserved communities, this team has tried to build a broader suite of financial services. This has left OPRT with an inflated cost structure and little new revenue to show for it.

While we intend to focus on what can be done going forward, it is important to acknowledge prior mistakes. The principal mistake was management's decision to purchase Digit.

On calls, management has repeatedly touted how well the acquisition is going but has failed to point to a single example of a profitable fee stream, cost synergy or cross selling opportunity that could justify this price and the ongoing associated costs. The sell side analysts with whom we spoke are not aware of any either. What this highly dilutive transaction has done is add more than $35mm in ongoing operating expenditures and generated a $108mm goodwill write down.5

While this acquisition is explained as part of an effort to offer a broader set of financial services, the reality is that creating a profitable consumer bank that offers credit cards and other financial products is costly and difficult. Goldman Sachs failed at doing so with Marcus. There is no indication that

Where

Unfortunately, this core business does not appear to be management's focus. This is evident in its capital allocation and hiring.

Personnel numbers in the retail branches and call centers where

What has exploded is corporate overhead (+70%) - employees who make several times more than the branch employees who generate the revenue (see below).7

OPRT | 1H19 | 2019 | 2020 | 2021 | 2022 | Change |

Contact Center | 1420 | 1519 | 1591 | 1582 | 1553 | 9.37 % |

Outsourcing | 453 | 630 | 579 | 652 | 807 | 78.15 % |

Corporate | 513 | 583 | 577 | 746 | 875 | 70.57 % |

Total | 2386 | 2732 | 2747 | 2980 | 3235 | 35.58 % |

It is important to note that this surge in expensive headcount is not being seen by their competitors – which have all shrunk their employee base since 2019 (see below).8

2018 | 2019 | 2020 | 2021 | 2022 | Change | |

OMF | 10200 | 9700 | 8300 | 8800 | 9200 | -9.80 % |

WRLD | 3419 | 3624 | 3744 | 3175 | 3121 | -8.72 % |

CURO | 4300 | 4000 | 3900 | 5200 | 4000 | -6.98 % |

Management's disregard for costs can be seen clearly in the proliferation of officers with overlapping responsibilities.

In addition to a

In addition to a General Counsel, it has a Deputy General Counsel, and a VP Assistant General Counsel.

And, in addition to a

If you can't find an HR officer,

Employees themselves find the layers to be unnecessary as seen in comments on Glassdoor.com (see below).11

Cons

"Too many Sr. Leaders as they try to ramp the company for better positioning of the public's eye."

Advice to Management

"There is no need for so many Directors and Sr. Managers within the same department."

To further compound all the unnecessary headcount,

Stock based compensation is expected to be $33mm in 2023 or roughly ~25% of the current market cap of the company.12 OMF on the other hand is compensating its team at ~1% of the current market cap.13

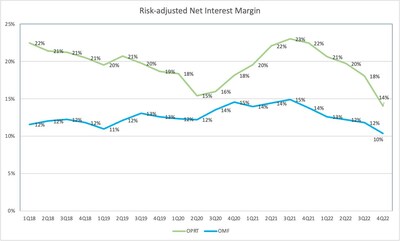

The good news is that the actual core lending business is still very strong.14 Even with some recent credit deterioration,

Management has admitted defeat in loan growth and in July of this past year, they reduced loan volumes by "tightening the credit box."15 This should allow the charge offs to fall over the rest of 2023 and risk-adjusted net interest margin to increase again in the second half of 2023.

But while management has made the right call in reducing loan origination, they have not addressed their oversized personnel costs. On the same earnings call that he talked about reducing credit growth, CEO

If the lending business is shrinking (for good reason), then the expense side must aggressively shrink as well.

In 2019,

The reality is that that $550mm operating expense is still obscenely high relative to

This is illustrative of how much earnings power is being masked by fintech and overhead costs. Even with the token cost reductions, management is keeping its corporate bloat and fruitless fintech endeavors alive.

While it might take longer to get to 2019 expense levels, there are clearly costs that the company can take out in calendar 2023 that would quickly reshape things.

Since 2019, there has been a more than $50mm increase in tech head count and salaries towards fintech initiatives that are not bearing fruit. That should be cut this year. G&A has increased from $15mm in 2019 to $59mm in 2022. That should be cut back to what it was in 2019. Those two initiatives alone would save the company almost $100mm by 2024.

With those savings, we see

We understand that CEO

The only solution here in the long run is for the board to bring on a new management team that is not beholden to prior decisions and can aggressively reduce operating expenditures back to below $450mm and re-underwrite these new business initiatives. The current piece meal approach will not work.

We imagine that our sentiments are shared by others and will become the majority view of shareholders in the future if the course is not quickly changed.

We would welcome a dialogue with the board on how these changes can be made and will reach out accordingly.

Sincerely,

CIO

Contact:

[email protected]

1 Bloomberg

2 https://investor.oportun.com/news-events/press-releases/detail/93/oportun-announces-plan-to-streamline-operations

3 https://www.globenewswire.com/news-release/2023/03/15/2627617/0/en/Oportun-Expands-Executive-Team-with-Key-New-Hires.html

4 https://www.sec.gov/Archives/edgar/data/1538716/000153871622000021/oportunproforma.htm

5 https://www.sec.gov/ix?doc=/Archives/edgar/data/0001538716/000153871622000218/Oportun-20220930.htm

6 SEC Filings

7 https://www.glassdoor.com/Salary/Oportun-Vice-President-Salaries-E991292_D_KO8,22.htm

8 SEC Filings

9 https://oportun.com/team/

10

11 https://www.glassdoor.com/Reviews/Oportun-Reviews-E991292.htm

12 https://d1io3yog0oux5.cloudfront.net/_c2f75a0caa1a3fbe3e423cff7fae2bb8/oportun/db/2227/21469/pdf/Investor+Presentation++%28Dec+2022+10K%29+FINAL+v2.pdf

13 https://s23.q4cdn.com/416720971/files/doc_financials/2021/ar/Final-2021-Annual-Report1.pdf

14 SEC Filings

15

16

17 Bloomberg

18 Findell Estimates

19 Findell Estimates

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/findell-capital-management-llc-issues-statement-to-the-oportun-financial-corporation-board-of-directors-301784449.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/findell-capital-management-llc-issues-statement-to-the-oportun-financial-corporation-board-of-directors-301784449.html

SOURCE

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Fisker (FSR) files form 10-K, sees more job cuts, reiterates going concern doubts

- Goldman Sachs Comments on Sherwin-Williams (SHW) Earnings

- BCB Bancorp (BCBP) PT Lowered to $12 at Keefe, Bruyette & Woods

Create E-mail Alert Related Categories

Corporate News, Hedge FundsRelated Entities

Goldman Sachs, Barclays, Dividend, Layoffs, Earnings, Definitive Agreement, IPOSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!