Form N-CSR GOLDMAN SACHS TRUST For: Nov 30

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive,

Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| Copies to: | ||

| Caroline Kraus, Esq |

Geoffrey R.T. Kenyon, Esq. | |

| Goldman Sachs & Co. LLC |

Dechert LLP | |

| 200 West Street |

One International Place, 40th Floor | |

| New York, New York 10282 |

100 Oliver Street | |

| Boston, MA 02110 | ||

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: November 30

Date of reporting period: November 30, 2020

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| The Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds

| Annual Report | November 30, 2020 | |||

| MLP Energy Infrastructure Fund | ||||

Goldman Sachs MLP Energy Infrastructure Fund

| 1 | ||||

| 11 | ||||

| 13 | ||||

| 16 | ||||

| 23 | ||||

| 36 | ||||

| 37 | ||||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||

PORTFOLIO RESULTS

Goldman Sachs MLP Energy Infrastructure Fund

Investment Objective and Principal Investment Strategy

The Fund seeks total return through current income and capital appreciation.

In April 2020, the Board of Trustees of the Goldman Sachs Trust approved changes to the Fund’s principal investment strategy, effective at the close of business on June 26, 2020. When the Reporting Period began on December 1, 2019, the Fund invested, under normal circumstances, at least 80% of its net assets plus any borrowings for investment purposes (measured at the time of purchase) (“Net Assets”) in energy infrastructure master limited partnership (“MLP”) investments. After June 26, 2020, the Fund invests, under normal circumstances, at least 80% of its Net Assets in U.S. and non-U.S. equity or fixed income securities issued by energy infrastructure companies, including MLPs and “C” corporations. The Fund’s investments in MLPs will consist of at least 25% of the Fund’s total assets as measured at the time of purchase. The Fund intends to concentrate its investments in the energy sector.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Energy and Infrastructure Team discusses the Goldman Sachs MLP Energy Infrastructure Fund’s (the “Fund”) performance and positioning for the 12-month period ended November 30, 2020 (the “Reporting Period”). The performance information reported herein reflects the Fund’s current and prior investment strategies.

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Investor, Class R6, Class R and Class P Shares generated average annual total returns, without sales charges, of -27.84%, -28.33%, -27.48%, -27.56%, -27.61%, -28.12% and -27.55%, respectively. These returns compare to the -24.45% average annual total return of the Alerian MLP Index. The Alerian MLP Index is a leading measure of energy infrastructure master limited partnerships (“MLPs”).1 |

| Q | How did energy-related assets overall perform during the Reporting Period? |

| A | Energy-related assets broadly sold off during the Reporting Period. Energy infrastructure MLPs generally, as measured by the Alerian MLP Index,1 produced a total return of -24.45%. The broader midstream2 sector, as measured by the Alerian Midstream Energy Index3 (“AMNA Index”) (which includes both energy MLPs and “C” corporations), generated a total return of -17.82%. |

| In December 2019, when the Reporting Period began, the growth outlooks for the U.S. shale industry and the global economy were positive and stable overall. Conditions abruptly changed in early 2020 with the emergence and spread of COVID-19 and the start of a crude oil producer price war, which together created a more challenging and uncertain global environment for the energy markets and energy-related equities. |

| The energy markets experienced unprecedented weakness during the first quarter of 2020, driven by two factors. The first was a demand-side shock, as quarantine efforts and travel restrictions implemented to reduce the spread of COVID-19 led to a sharp drop in demand. The second was a supply-side shock, as the Organization of the Petroleum Exporting Countries (“OPEC”) and Russia failed to reach an agreement on production cuts and entered into a crude oil price war, which ultimately added supply to an already oversupplied market. Crude oil prices fell, with the prices of |

| 1 | Source: Alerian. The Alerian MLP Index is the leading gauge of energy infrastructure Master Limited Partnerships (MLPs). The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis (AMZX). It is not possible to invest directly in an unmanaged index. |

| 2 | The midstream component of the energy industry is usually defined as those companies providing products or services that help link the supply side (i.e., energy producers) and the demand side (i.e., energy end-users for any type of energy commodity. Such midstream businesses can include, but are not limited to, those that process, store, market and transport various energy commodities. |

| 3 | Source: Alerian. The Alerian Midstream Energy Index is a broad-based composite of North American energy infrastructure companies. The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return (AMNA), total-return (AMNAX), net total-return (AMNAN), and adjusted net total-return (AMNTR) basis. |

1

PORTFOLIO RESULTS

| West Texas Intermediate (“WTI”) and Brent crude oil declining approximately 25% and 24%, respectively, on March 9th, the first trading day after the OPEC+ talks collapsed.4 (OPEC+ is composed of OPEC countries and non-OPEC oil producing countries, most notably Russia.) Crude oil prices then continued to trend down fueled by market uncertainty about demand given the global economic impact of COVID-19 as well as by shorter-term concerns around U.S. storage constraints. |

| Energy-related equities sold off during the first quarter of 2020 on investor uncertainty about the ultimate impact on the U.S. shale industry of the simultaneous demand-side and supply-side shocks. We believe the sell-off was exacerbated in the midstream sector by technical selling, as closed-end funds de-levered to reduce volatility and, in some cases, to maintain compliance with leverage covenants. We estimate more than $3 billion in holdings were sold by closed-end funds during the first 15 trading days of March.5 Midstream equities were also pressured during the first calendar quarter by the magnitude of uncertainty within the equities and energy markets broadly, even though midstream cash flows are predominantly volume based and generally less sensitive to commodity price fluctuations due to contractual agreements, which we believe help manage one-to-one exposure between midstream cash flows and volume declines. Furthermore, in response to severe commodity price weakness during the first calendar quarter, a number of midstream energy companies announced plans to strengthen their balance sheets, with some keeping their distributions flat, some cutting distribution payout levels, and many reducing their expected capital expenditures for 2020. In most cases, these defensive actions were rewarded by investors. |

| In April 2020, the energy markets and energy-related equities experienced some relief, as the crude oil price war appeared to reach a resolution. OPEC+ members met, starting on April 9th, and proposed their largest-ever production cut of 9.7 million barrels per day on April 12th.6 Saudi Arabia subsequently deepened its commitment to the production cut, reducing output by an additional 1.0 million barrels per day. Several other countries also announced voluntary production cuts. Despite the April OPEC+ production agreement, significant crude oil oversupply led to logistical issues and storage capacity constraints in the U.S. that same month, resulting in unprecedentedly low WTI crude oil prices and even negative WTI crude oil futures contracts for the first time in history. Midstream equities remained relatively resilient during April, as we believe many investors looked past transient supply-side issues and instead valued equities on longer-dated commodity price expectations. |

| In May 2020, market expectations about the supply-demand gap started to ease, as crude oil demand improved relative to the troughs seen in early April and global supply levels began to react to lower prices in the marketplace. In particular, production cuts from OPEC+ members, as well as market-driven reductions in U.S. production, slowed inventory builds relative to their April levels. Meanwhile, future production activity indicators, such as rig counts and 2020 capital expenditure expectations for exploration and production companies, fell substantially. As a result, the crude oil market started to show signs of tightening in May, enabling prices to rebound off their prior month lows. At the same time, energy-related equities, particularly midstream equities, continued to experience a meaningful recovery from their lows in mid-March. The Alerian MLP Index and the AMNA Index recorded gains of 148% and 107%, respectively, between March 18th and June 8th. They retreated thereafter, dropping 32% and 24%, respectively, from June 9th through the end of October. We believe the drop in midstream equity performance from mid-June through October 2020 was driven largely by weak investor sentiment, not fundamentals. In our view, the weakness in sentiment was due to a number of factors, including uncertainty about the then-upcoming U.S. elections, given the seemingly unfavorable oil and gas policy views of Democratic politicians. Midstream equities were also hurt, in our opinion, by environmental, social and governance-related capital allocation headwinds and terminal value7 concerns for oil and gas assets given growing interest in renewable energy. Meanwhile, the fundamental backdrop for energy-related companies improved considerably. First, oil demand picked up steam. We track traffic data across the world, and within the largest cities in Asia and Europe, traffic congestion grew closer to pre-COVID-19 levels. Although the recovery in U.S. traffic congestion was comparatively slower, we also started to see improvement domestically. Second, on the supply side, we witnessed production discipline from OPEC+ countries and U.S. shale producers, |

| 4 | Source of crude oil price data: Bloomberg. |

| 5 | Source of sales data: Bloomberg and U.S. Capital Advisors. |

| 6 | Source of production cut data: OPEC and Bloomberg. |

| 7 | Terminal value is the value of a business or project beyond the forecast period when future cash flows can be estimated. Terminal value assumes a business will grow at a set growth rate forever after the forecast period. |

2

PORTFOLIO RESULTS

| which narrowed the supply-demand gap and provided upside support for crude oil prices. Third, many midstream energy companies had significantly reduced their capital expenditures, a welcome and appropriate change, in our view. Finally, even with the dramatic decline in oil demand during the second quarter of 2020, midstream cash flows were rather resilient. If one were to look at a list of the most prominent midstream energy companies, their earnings before interest, taxes, depreciation and amortization (“EBITDA”) were only down an average of approximately 11% year-over-year during the second calendar quarter. During that same quarter, the share prices of these companies fell an average of 44%, demonstrating the disconnect between equity price performance and the sector’s fundamentals, in our view. |

| During November 2020, energy markets and energy-related securities experienced strong rebounds. WTI and Brent crude oil prices rose 27% and 25%, respectively. Energy-related securities rallied, with the Alerian MLP Index and AMNA Index up 24% and 19%, respectively. We believe the strong performance was driven by positive COVID-19 vaccine news, which materially improved the outlook for energy demand, and by resilient earnings of midstream energy companies. Nine of the top 10 U.S. midstream energy companies beat consensus EBITDA expectations for the third calendar quarter by an average of 7.5%, while |

| also posting healthy distribution coverage ratios8 and strong free cash flow outlooks. Price performance was also bolstered, in our view, by the announcement of share buyback programs, with $2.3 billion authorized in November alone, and continued cost rationalization,9 with consensus expectations for 2021 midstream capital expenditures declining more than 50% relative to the estimates at 2019 year-end, greatly increasing market expectations for free cash flow and capital return to investors. At the same time, the market appeared to view the U.S. election results as relatively benign, given that a Democratic President could be coupled with a potentially Republican Senate, alleviating investors’ worst-case concerns about punitive legislation against the oil and gas sector. Finally, we believe energy-related equities benefited from a growth to value rotation, as promising COVID-19 vaccine news and potential economic reopening led many investors to focus on undervalued businesses. This view is supported, we believe, by the approximately 550 basis point outperformance of the Russell 1000 Value Index10 versus the Russell 1000 Growth Index11 between October 1, 2020 and the end of the Reporting Period. (A basis point is 1/100th of a percentage point.) |

| Q | What key factors were responsible for the Fund’s relative performance during the Reporting Period? |

| A | Security selection and severe weakness in the energy markets drove the Fund’s performance during the Reporting Period. The Fund posted negative absolute returns and underperformed the Alerian MLP Index, as high quality midstream energy equities, which are favored by our investment process, generally lagged lower quality midstream energy equities. In managing the Fund, we focus on what we consider to be high quality midstream energy companies with strong dividend and distribution coverage ratios, healthy balance sheets and robust free cash flow outlooks. These stocks outperformed during the severe market weakness in March 2020, while lower quality midstream stocks, which we define as smaller cap, high-beta12 companies with non-investment grade balance sheets, experienced steep declines. However, as the midstream energy sector recovered from its March lows, lower quality midstream stocks, which we believe were oversold, meaningfully outperformed higher quality midstream stocks, and the Fund’s minimal exposure to lower quality stocks compared to the Alerian MLP Index detracted from its relative performance. We note that while volatility may lead to periods of underperformance for higher quality names, these companies have historically outperformed over a |

| 8 | The distribution coverage ratio is an energy company’s distributable cash flow divided by the total amount of distributions it has paid out. It is an indication of an energy company’s ability to maintain its current cash distribution level. |

| 9 | Cost rationalization addresses the sources of costs through the supply chain. |

| 10 | The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® Index companies with lower price-to-book ratios and lower expected growth values. The Russell 1000® Index measures the performance of the large-cap segment of the U.S. equity universe and includes approximately 1000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000® Index represents approximately 92% of the U.S. market. |

| 11 | The Russell 1000® Growth Index is an unmanaged index of common stock prices that measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. |

| 12 | In this context, a high-beta company means any midstream company whose stock has a trailing one-year beta to the AMNA Index that is greater than 1.2. Beta is a measure of a stock’s volatility relative to an index or the overall market. A beta greater than 1.0 indicates that the stock’s price is theoretically more volatile than the index or overall market. |

3

PORTFOLIO RESULTS

| longer time frame, and we believe they have offered better risk-adjusted returns. |

| Regarding its exposures, the Fund was negatively impacted by weak stock selection in the petroleum pipeline transportation, natural gas pipeline transportation, and gathering and processing subsectors.13 On the positive side, the Fund benefited from its holdings in the power generation subsector, positioning that proved to be rather defensive amid volatility in the energy markets. The subsector also provided the Fund with exposure to renewable power generation, an industry that has experienced increased investor interest as well as supportive corporate and regulatory announcements, which added further to relative returns. (Power generating companies are not represented in the Alerian MLP Index.) |

| Q | What individual holdings detracted from the Fund’s relative performance during the Reporting Period? |

| A | Compared to the Alerian MLP Index, the Fund was hurt during the Reporting Period by its underweight positions in Tallgrass Energy, LP; Western Midstream Partners, LP; and DC Midstream, LP. |

| Detracting most from relative performance was the Fund’s underweight position in Tallgrass Energy, LP (TGE), a midstream provider that primarily engages in the transportation of crude oil and natural gas in addition to providing storage, water management and processing services. On January 31, 2019, Blackstone Infrastructure Partners (“BIP”) announced a definitive agreement to acquire 100% of the membership interests in TGE’s general partners and an approximately 44% economic interest in TGE itself. After the deal was completed during March 2019, TGE’s equity price significantly underperformed the midstream sector, as represented by the Alerian MLP Index. In August 2019, TGE received a non-binding preliminary proposal letter from BIP offering to acquire all outstanding Class A shares of the company for $19.50 per share in cash. Subsequently in December 2019, TGE announced it had entered into a definitive merger agreement pursuant to which BIP, together with its affiliates, would acquire all of the publicly held outstanding Class A shares of TGE for $22.45 per share in cash. Although TGE’s stock initially rallied, there were significant delays following the announcement, which raised investor uncertainty around the prospects of the deal closing, leading TGE to trade significantly below the agreement’s offering price. In March 2020, BIP confirmed its commitment to the deal, and the Fund established a modest, though still underweight, position in the stock. After March 18th, the date we initiated the position, through the transaction’s closing date of April 17th, TGE rallied approximately 68% to reflect the original offering price, and, as a result, the Fund’s underweight position hurt its relative performance. |

| The Fund was also hampered by its underweight in Western Midstream Partners, LP (WES), a midstream energy company that engages in the business of gathering, compressing, treating, processing and transporting natural gas, natural gas liquids and crude oil. WES performed well during the Reporting Period, largely because the company took several steps to fix its balance sheet and focus on cash flow growth. WES announced a distribution cut of 50% for 2020 and said it would reduce future capital expenditures, with the intention of using the excess cash flow to de-lever its balance sheet and buy back its stock. Additionally, as commodity prices stabilized, the outlook for the company’s largest customer, Occidental Petroleum, improved. |

| An underweight position in DCP Midstream, LP (DCP), one of the largest natural gas gatherers in North America and a top producer and primary marketer of natural gas liquids, detracted from the Fund’s relative returns. Severe weakness in the energy markets led to a steep decline in DCP’s stock price, largely, we believe, because of the company’s high leverage and direct commodity exposure relative to many of its peers. DCP’s management team responded to the sell-off with a 50% distribution cut, a meaningful reduction in 2020 capital expenditures and an announcement of additional cost savings initiatives in an effort to strengthen the company’s balance sheet. Although DCP’s capital discipline was generally viewed positively, we believe the market remained concerned about the company’s ability to decrease leverage given a reduction in producer activity and weak commodity prices. We sold the Fund’s position in DCP during April 2020 and reallocated the proceeds to companies that we believed had comparatively stronger balance sheets and less commodity price sensitivity. By the end of the Reporting Period, crude oil supply/demand had largely balanced and prices had stabilized, with market expectations for U.S. total liquids production rising from trough levels. Amid an improving macro environment for the energy market, DCP reported strong second calendar quarter earnings that significantly beat consensus estimates and reaffirmed its management’s original, pre-COVID-19 guidance for the |

| 13 | Sector and subsector allocations are defined by GSAM and may differ from sector allocations used by the Alerian MLP Index. |

4

PORTFOLIO RESULTS

| 2020 calendar year. In the week after the positive earnings announcement, average analyst consensus for the company’s 2021 price target increased considerably, and its stock traded higher. As a result, during the Reporting Period overall, the Fund’s underweight position in DCP detracted from its relative performance. |

| Q | What individual holdings added to the Fund’s relative performance during the Reporting Period? |

| A | Relative to the Alerian MLP Index, the Fund benefited from its lack of exposure to NGL Energy Partners LP, its overweight in Targa Resources Corp. and its underweight in Phillips 66 Partners LP. |

| Contributing most positively to the Fund’s relative performance was a lack of exposure to NGL Energy Partners LP (NGL), a diversified midstream MLP that provides multiple services, including transportation, storage, blending and marketing of crude oil, natural gas liquids, refined products/renewables and water solutions. NGL was negatively affected when one of the largest customers on its premier asset—Grand Mesa, a crude oil pipeline—entered into bankruptcy and fought to have its contracts with NGL rejected. In addition, in response to COVID-19 related weakness, NGL cut its distribution twice after the start of calendar year 2020. Counterparty concerns and the announcement of the two distribution cuts weighed on NGL’s equity price performance during the Reporting Period. |

| Adding further to relative returns was the Fund’s overweight in Targa Resources Corp. (TRGP), an independent midstream services provider primarily engaged in gathering, storing, processing and transporting crude oil, natural gas and refined petroleum products. The severe weakness in energy markets due to COVID-19-related demand destruction and the simultaneous OPEC+ producer price war led to an outsized decline in TRGP’s share price, largely due to the company’s high leverage ratio.14 However, its management team quickly took steps to strengthen the company’s balance sheet and to increase the company’s focus on free cash flow, which included an 89% dividend cut during 2020 and a reduction in capital expenditures. Then, later in the Reporting Period, TRGP announced it intended to buy back stock. Additionally, given that the company’s main area of operations is in the Permian Basin and it has an integrated asset profile, TRGP benefited from the stabilization of crude oil prices, as such stability greatly improved the company’s leverage and earnings profile, and the outlook for TRGP became increasingly positive, in our view. |

| The Fund’s relative performance was further bolstered during the Reporting Period by an underweight position in Phillips 66 Partners LP (PSXP), which owns, operates, develops and acquires crude oil, refined petroleum product and natural gas liquids pipelines and terminals and other transportation and midstream assets predominantly in the central and Gulf Coast regions of the U.S. PSXP’s performance was hurt by investor concerns around the potential shut-down of the Dakota Access Pipeline of which PSXP is a 25% owner through a joint venture. During the 2019 calendar year, this asset contributed approximately 18% of PSXP’s adjusted EBITDA. Fears that the pipeline might be closed by a federal district court led to heightened volatility in PSXP’s share price. To manage active portfolio risk should there be an unexpectedly positive court ruling, as well as to free up capital for other investments, we eliminated the Fund’s long position in PSXP during November 2020. However, we maintained measured exposure to the stock through the use of a call spread strategy.15 |

| Q | Were there any notable purchases or sales during the Reporting Period? |

| A | During the Reporting Period, the Fund initiated a position in Enbridge, Inc. (ENB), which provides energy transportation, distribution and related services in North America. We viewed the company’s size, scale, investment grade rating and overall defensive position as a compelling investment opportunity. |

| During a period of severe market uncertainty driven by the COVID-19 outbreak, the Fund initiated a position in NextEra Energy, Inc. (NEE). We considered NEE as an attractive investment opportunity because of what we viewed as the company’s low volatility earnings profile, focus on renewable energy sources and regulated rates of return that could help to protect its earnings from the impacts of COVID-19. |

| 14 | A leverage ratio indicates the level of debt incurred by a business against several other accounts in its balance sheet, income statement, or cash flow statement. A high leverage ratio generally indicates that a company has been aggressive in financing its growth with debt. |

| 15 | A call spread strategy involves purchasing call options at a specific strike price, while also selling the same number of calls of the same asset and expiration date but at a higher strike price. A call option is an option that gives the holder the right, but not the obligation, to buy an underlying asset at an agreed-upon price at any time up to an agreed-upon date. |

5

PORTFOLIO RESULTS

| In addition, during the Reporting Period, the Fund established a position in Rice Acquisition Corp. (RICE/U), a special-purpose acquisition company (SPAC), through an initial public offering. A SPAC raises capital through an initial public offering for the purpose of acquiring an existing company and driving shareholder value through strategic management and operational expertise. We decided to allocate capital to RICE/U as we are confident in its management team, members of which previously served as executive officers of Rice Energy Inc. and Rice Midstream Partners LP. In our opinion, they are well equipped to deliver upon their objective of producing attractive and sustainable risk-adjusted returns through the development of the world’s clean energy supply, a theme we believe may become more prominent in the global energy mix over the next several decades. |

| Among notable sales during the Reporting Period was the Fund’s investment in Noble Midstream Partners LP (NBLX). We exited the position in an effort to reduce portfolio risk during severe energy market uncertainty. We allocated the proceeds to companies that had what we viewed as comparatively stronger balance sheets and less commodity price sensitivity. |

| We eliminated the Fund’s investment in Genesis Energy, LP (GEL), a midstream MLP that provides energy infrastructure and logistics services. A significant portion of GEL’s cash flow comes from its soda ash segment, and soda ash demand was negatively impacted by the spread of COVID-19. Additionally, cash flows from soda ash can have greater variability than those from more traditional midstream business segments because of the length and nature of soda ash contracts. Because of uncertainty around the performance of GEL’s soda ash segment, COVID-19-related impacts to its more traditional midstream segments and the company’s relatively high level of leverage, we decided to exit the Fund’s position in the stock. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, the Fund used listed equity options to implement a call spread as we sought to maintain exposure to PSXP after eliminating the Fund’s long investment in the stock. The use of listed equity options had a positive impact on the Fund’s performance during the Reporting Period. |

| Q | What is the Fund’s tactical view and strategy for the months ahead? |

| A | At the end of the Reporting Period, we had a positive outlook for the energy markets and energy-related equities in 2021. Taking a macro perspective, we noted that crude oil demand had improved toward the end of the Reporting Period, not only internationally, but also in the U.S., and we believed the COVID-19 vaccine would only accelerate this trend. Additionally, in our view, U.S. producers were demonstrating unprecedented supply-side discipline and OPEC+ members were showing solidarity. Assuming global production remained disciplined and demand increased on the back of rapid testing and a vaccine, Goldman Sachs Global Investment Research was forecasting at the end of the Reporting Period that Brent crude oil prices could hit $63 per barrel in 2021. Furthermore, a decline in U.S.-based upstream16 drilling activity seemed to have reduced the need for more pipeline projects, which led many midstream energy companies to shift their focus from new project spending to debt reduction and possible share buyback programs during the Reporting Period. Coupled with lower distribution payouts, this should result in strong free cash flow into 2021, in our view. We thought the shift in capital allocation was long overdue, and more free cash flow-centric business models may well be a key factor for the long-term sustainability of the midstream energy sector. In our opinion, the sector’s free cash flow potential has also created a significant opportunity for share repurchase programs, which we believe could be a meaningful catalyst for a recovery in equity prices, given the depressed valuations at the end of the Reporting Period. |

| Looking toward 2025, we believe the midstream energy sector has the potential to generate $35-$45 billion of excess cash after distributions and capital expenditures, which amounts to nearly 15% of the market capitalization of midstream energy companies generating positive free cash flow at the end of the Reporting Period. To put this in context, Wells Fargo said it expects the midstream energy sector to generate nearly $7 billion of excess cash in 2021 alone. If just 50% of that excess cash is used for share buyback programs, we believe it could reverse almost all of the investment outflows experienced from January 2020 through the end of |

| 16 | The upstream component of the energy industry is usually defined as those operations stages in the oil and gas industry that involve exploration and production. Upstream operations deal primarily with the exploration stages of the oil and gas industry, with upstream firms taking the first steps to first locate, test and drill for oil and gas. Later, once reserves are proven, upstream firms will extract any oil and gas from the reserve. |

6

PORTFOLIO RESULTS

| the Reporting Period. We have seen several billion dollars of share buyback authorizations from midstream companies during 2020 year to date through November, and we anticipate more buyback programs may be announced in coming calendar quarters. In our opinion, these programs could be accretive to shareholder value and may also be a strong technical tailwind for midstream equity prices. |

| At the end of the Reporting Period, we believed the risk-reward profile of midstream equities had grown increasingly positive. In managing the Fund, we intended to remain focused on companies we deemed to be of high quality, with strong dividend and distribution coverage ratios, healthy balance sheets and robust free cash flow outlooks. At the end of the Reporting Period, we believed the Fund was well positioned to benefit from a potential rebound in midstream equity prices we expect to see in 2021. |

7

FUND BASICS

Goldman Sachs MLP Energy Infrastructure Fund

as of November 30, 2020

| TOP TEN HOLDINGS AS OF 11/30/201 | ||||||||

| Holding | % of Net Assets | Line of Business | ||||||

| Enterprise Products Partners LP | 10.5 | % | Pipeline Transportation | Natural Gas | |||||

| MPLX LP | 9.5 | Gathering + Processing | ||||||

| Magellan Midstream Partners LP | 8.8 | Pipeline Transportation | Petroleum | ||||||

| Energy Transfer LP | 7.1 | Pipeline Transportation | Natural Gas | ||||||

| Plains All American Pipeline LP | 6.6 | Pipeline Transportation | Petroleum | ||||||

| ONEOK, Inc. | 5.7 | Gathering + Processing | ||||||

| The Williams Cos., Inc. | 5.5 | Gathering + Processing | ||||||

| Targa Resources Corp. | 5.4 | Gathering + Processing | ||||||

| Cheniere Energy, Inc. | 4.7 | Other | Liquefaction | ||||||

| Pembina Pipeline Corp. | 2.9 | Pipeline Transportation | Petroleum | ||||||

| 1 | The top 10 holdings may not be representative of the Fund’s future investments. |

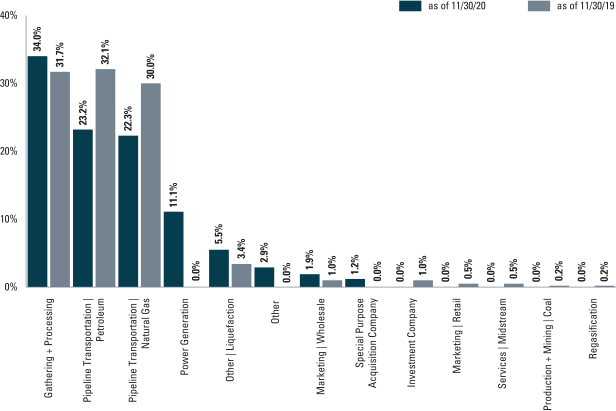

| FUND SECTOR ALLOCATIONS2 |

| 2 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of total net assets. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance.

8

FUND BASICS

Index Definitions

The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor’s using a float-adjusted market capitalization methodology. The Alerian MLP Index is disseminated by the New York Stock Exchange real-time on a price return basis (NYSE: AMZ). The corresponding total return index is calculated and disseminated daily through ticker AMZX. The Alerian MLP Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index.

9

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Performance Summary

November 30, 2020

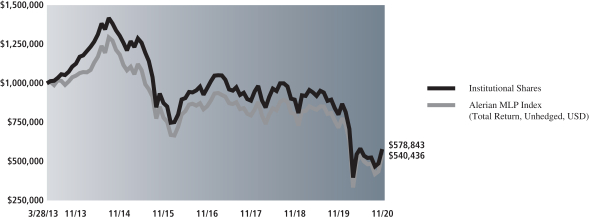

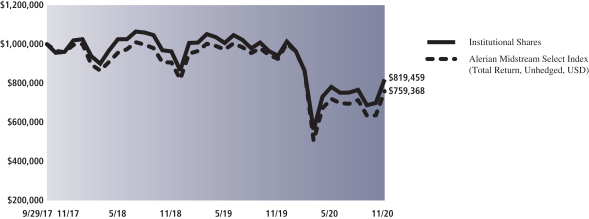

The following graph shows the value, as of November 30, 2020, of a $1,000,000 investment made on March 28, 2013 (commencement of operations) in Institutional Shares at NAV. For comparative purposes, the performance of the Fund’s benchmark, the Alerian MLP Index (Total Return, Unhedged, USD) is shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our website at www.GSAMFUNDS.com to obtain the most recent month-end returns.

| MLP Energy Infrastructure Fund’s Lifetime Performance |

Performance of a $1,000,000 investment, with distributions reinvested, from March 28, 2013 through November 30, 2020.

| Average Annual Total Return through November 30, 2020* | One Year | Five Years | Since Inception | |||||||

| Class A (Commenced March 28, 2013) |

||||||||||

| Excluding sales charges |

-27.84% | -8.26% | -7.23% | |||||||

| Including sales charges |

-31.75% | -9.28% | -7.91% | |||||||

|

| ||||||||||

| Class C (Commenced March 28, 2013) |

||||||||||

| Excluding contingent deferred sales charges |

-28.33% | -8.90% | -7.89% | |||||||

| Including contingent deferred sales charges |

-28.55% | -8.90% | -7.89% | |||||||

|

| ||||||||||

| Institutional (Commenced March 28, 2013) |

-27.48% | -7.89% | -6.87% | |||||||

|

| ||||||||||

| Investor (Commenced March 28, 2013) |

-27.56% | -8.00% | -6.99% | |||||||

|

| ||||||||||

| Class R6 (Commenced April 2, 2018) |

-27.61% | N/A | -12.85% | |||||||

|

| ||||||||||

| Class R (Commenced March 28, 2013) |

-28.12% | -8.47% | -7.46% | |||||||

|

| ||||||||||

| Class P (Commenced April 16, 2018) |

-27.55% | N/A | -15.53% | |||||||

|

| ||||||||||

| * | These returns assume reinvestment of all distributions at NAV and reflect a maximum initial sales charge of 5.50% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Investor, Class R6, Class R and Class P Shares do not involve a sales charge, such a charge is not applied to their Average Annual Total Return. |

10

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

November 30, 2020

| Shares | Description | Value |

||||||

| Common Stocks – 100.9% | ||||||||

| Gathering + Processing – 34.0% | ||||||||

| 1,845,367 | Antero Midstream Corp. | $ | 12,437,774 | |||||

| 842,915 | Crestwood Equity Partners LP | 13,747,944 | ||||||

| 1,558,299 | DCP Midstream LP | 25,166,529 | ||||||

| 4,451,327 | MPLX LP | 93,655,920 | ||||||

| 1,558,588 | ONEOK, Inc. | 55,906,551 | ||||||

| 2,274,291 | Targa Resources Corp. | 53,445,838 | ||||||

| 2,568,553 | The Williams Cos., Inc. | 53,888,242 | ||||||

| 1,994,992 | Western Midstream Partners LP | 25,735,397 | ||||||

|

|

|

|||||||

| 333,984,195 | ||||||||

|

|

|

|||||||

| Marketing | Wholesale – 1.9% | ||||||||

| 673,310 | Sunoco LP | 18,711,285 | ||||||

|

|

|

|||||||

| Other – 2.9% | ||||||||

| 69,326 | American Water Works Co., Inc. | 10,633,222 | ||||||

| 269,324 | Darling Ingredients, Inc.* | 13,002,963 | ||||||

| 26,235 | Vestas Wind Systems A/S | 5,347,046 | ||||||

|

|

|

|||||||

| 28,983,231 | ||||||||

|

|

|

|||||||

| Other | Liquefaction – 5.5% | ||||||||

| 126,682 | Cheniere Energy Partners LP | 4,826,584 | ||||||

| 817,947 | Cheniere Energy, Inc.* | 46,369,415 | ||||||

| 61,844 | New Fortress Energy, Inc. | 2,666,095 | ||||||

|

|

|

|||||||

| 53,862,094 | ||||||||

|

|

|

|||||||

| Pipeline Transportation | Natural Gas – 22.3% | ||||||||

| 11,321,582 | Energy Transfer LP | 69,967,377 | ||||||

| 5,336,605 | Enterprise Products Partners LP | 103,530,137 | ||||||

| 633,409 | Equitrans Midstream Corp. | 5,168,617 | ||||||

| 718,197 | Kinder Morgan, Inc. | 10,327,673 | ||||||

| 448,873 | TC Energy Corp. | 19,718,991 | ||||||

| 329,173 | TC PipeLines LP | 10,171,446 | ||||||

|

|

|

|||||||

| 218,884,241 | ||||||||

|

|

|

|||||||

| Pipeline Transportation | Petroleum – 23.2% | ||||||||

| 797,997 | Enbridge, Inc. | 24,905,486 | ||||||

| 184,536 | Holly Energy Partners LP | 2,498,617 | ||||||

| 2,094,742 | Magellan Midstream Partners LP | 86,198,633 | ||||||

| 1,060,009 | NuStar Energy LP | 14,087,520 | ||||||

| 702,021 | PBF Logistics LP | 6,549,856 | ||||||

| 1,134,652 | Pembina Pipeline Corp. | 28,922,280 | ||||||

| 8,204,406 | Plains All American Pipeline LP | 65,142,984 | ||||||

|

|

|

|||||||

| 228,305,376 | ||||||||

|

|

|

|||||||

| Power Generation – 11.1% | ||||||||

| 453,860 | Atlantica Sustainable Infrastructure PLC | 15,608,245 | ||||||

| 170,571 | Boralex, Inc. Class A | 5,390,186 | ||||||

| 127,430 | CMS Energy Corp. | 7,842,042 | ||||||

| 110,224 | Duke Energy Corp. | 10,213,356 | ||||||

| 60,349 | Eversource Energy | 5,281,141 | ||||||

| 129,674 | National Grid PLC ADR | 7,349,922 | ||||||

| 209,474 | NextEra Energy Partners LP | 13,295,315 | ||||||

| 176,557 | NextEra Energy, Inc. | 12,992,830 | ||||||

| 319,946 | Northland Power, Inc. | 10,965,424 | ||||||

| 27,482 | Orsted A/S(a) | 4,944,744 | ||||||

|

|

|

|||||||

| Common Stocks – (continued) | ||||||||

| Power Generation – (continued) | ||||||||

| 250,371 | The AES Corp. | 5,117,583 | ||||||

| 155,609 | Xcel Energy, Inc. | 10,481,822 | ||||||

|

|

|

|||||||

| 109,482,610 | ||||||||

|

|

|

|||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $1,319,528,405) | $ | 992,213,032 | ||||||

|

|

|

|||||||

| Units | Description | Value | ||||||

| Special Purpose Acquisition Company*(b) – 1.2% | ||||||||

| 1,135,900 | Rice Acquisition Corp. | $ | 11,767,924 | |||||

| (Cost $11,359,000) | ||||||||

|

|

|

|||||||

| TOTAL INVESTMENTS – 102.1% |

||||||||

| (Cost $1,330,887,405) | $ | 1,003,980,956 | ||||||

|

|

|

|||||||

| |

LIABILITIES IN EXCESS OF OTHER ASSETS – (2.1)% |

(20,764,120 | ) | |||||

|

|

|

|||||||

| NET ASSETS – 100.0% | $ | 983,216,836 | ||||||

|

|

|

|||||||

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. | ||

| * |

Non-income producing security. | |

| (a) |

Exempt from registration under Rule 144A of the Securities Act of 1933. | |

| (b) |

Units consist of 1 share of common stock and 1/2 warrant. | |

|

| ||||

| Investment Abbreviations: | ||||

| ADR |

—American Depositary Receipt | |||

| LP |

—Limited Partnership | |||

| PLC |

—Public Limited Company | |||

|

| ||||

| The accompanying notes are an integral part of these financial statements. | 11 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Schedule of Investments (continued)

November 30, 2020

| ADDITIONAL INVESTMENT INFORMATION |

PURCHASED AND WRITTEN OPTIONS CONTRACTS — At November 30, 2020, the Fund had the following purchased and written options:

EXCHANGE TRADED OPTIONS ON EQUITIES CONTRACTS

| Description | Exercise Price |

Expiration Date |

Number of Contracts |

Notional Amount |

Market Value |

Premiums Paid (Received) by Fund |

Unrealized Appreciation/ (Depreciation) |

|||||||||||||||||||||

| Purchased option contracts |

|

|||||||||||||||||||||||||||

| Calls |

|

|||||||||||||||||||||||||||

| Phillips 66 Partners LP FLEX |

$ | 27.500 | 03/19/2021 | 3,750 | $ | 375,000 | $ | 857,891 | $ | 626,250 | $ | 231,641 | ||||||||||||||||

| Phillips 66 Partners LP FLEX |

27.500 | 06/18/2021 | 3,750 | 375,000 | 1,095,908 | 881,625 | 214,283 | |||||||||||||||||||||

| Total purchased options |

|

7,500 | $ | 750,000 | $ | 1,953,799 | $ | 1,507,875 | $ | 445,924 | ||||||||||||||||||

| Description | Exercise Price |

Expiration Date |

Number of Contracts |

Notional Amount |

Market Value |

Premiums Paid (Received) by Fund |

Unrealized Appreciation/ (Depreciation) |

|||||||||||||||||||||||

| Written option contracts |

|

|||||||||||||||||||||||||||||

| Calls |

|

|||||||||||||||||||||||||||||

| Phillips 66 Partners LP |

$ | 35.000 | 06/18/2021 | (3,750 | ) | $ | (375,000 | ) | $ | (496,875 | ) | $ | (367,500 | ) | $ | (129,375 | ) | |||||||||||||

| Phillips 66 Partners LP |

35.000 | 03/19/2021 | (3,750 | ) | (375,000 | ) | (234,375 | ) | (146,250 | ) | (88,125 | ) | ||||||||||||||||||

| Total written options | (7,500 | ) | $ | (750,000 | ) | $ | (731,250 | ) | $ | (513,750 | ) | $ | (217,500 | ) | ||||||||||||||||

| Total | $ | 1,222,549 | $ | 994,125 | $ | 228,424 | ||||||||||||||||||||||||

| 12 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Statement of Assets and Liabilities

November 30, 2020

|

|

||||||

| Assets: | ||||||

| Investments of unaffiliated issuers, at value (cost $1,330,887,405) |

$ | 1,003,980,956 | ||||

| Purchased options, at value (premium paid $1,507,875) |

1,953,799 | |||||

| Cash |

1,395,226 | |||||

| Foreign currencies, at value (cost $137,923) |

137,901 | |||||

| Receivables: |

||||||

| Fund shares sold |

2,585,968 | |||||

| Due from broker |

2,386,913 | |||||

| Dividends |

1,256,005 | |||||

| Investments sold |

1,150,503 | |||||

| Collateral on options contracts |

261,062 | |||||

| Reimbursement from investment adviser |

111,532 | |||||

| Other assets |

22,415 | |||||

| Total assets | 1,015,242,280 | |||||

| Liabilities: | ||||||

| Written option contracts, at value (premium received $513,750) |

731,250 | |||||

| Payables: |

||||||

| Current Tax liability |

17,251,712 | |||||

| Fund shares redeemed |

3,243,291 | |||||

| Investments purchased |

978,170 | |||||

| Management fees |

760,844 | |||||

| Distribution and service fees and transfer agent fees |

61,121 | |||||

| Deferred taxes, net |

8,415,897 | |||||

| Accrued expenses |

583,159 | |||||

| Total liabilities | 32,025,444 | |||||

| Net Assets: | ||||||

| Paid-in capital |

2,521,500,372 | |||||

| Total distributable earnings (loss) |

(1,538,283,536 | ) | ||||

| NET ASSETS | $ | 983,216,836 | ||||

| Net Assets: |

||||||

| Class A |

$ | 34,023,509 | ||||

| Class C |

24,897,466 | |||||

| Institutional |

182,235,854 | |||||

| Investor |

32,395,629 | |||||

| Class R6 |

181,968,440 | |||||

| Class R |

795,723 | |||||

| Class P |

526,900,215 | |||||

| Total Net Assets |

$ | 983,216,836 | ||||

| Shares Outstanding $0.001 par value (unlimited shares authorized): |

||||||

| Class A |

1,983,839 | |||||

| Class C |

1,567,480 | |||||

| Institutional |

10,213,406 | |||||

| Investor |

1,840,329 | |||||

| Class R6 |

10,187,380 | |||||

| Class R |

47,583 | |||||

| Class P |

29,423,040 | |||||

| Net asset value, offering and redemption price per share:(a) |

||||||

| Class A |

$17.15 | |||||

| Class C |

15.88 | |||||

| Institutional |

17.84 | |||||

| Investor |

17.60 | |||||

| Class R6 |

17.86 | |||||

| Class R |

16.72 | |||||

| Class P |

17.91 | |||||

| (a) | Maximum public offering price per share for Class A Shares is $18.15. At redemption, Class C Shares may be subject to a contingent deferred sales charge, assessed on the amount equal to the lesser of the current net asset value or the original purchase price of the shares. |

| The accompanying notes are an integral part of these financial statements. | 13 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Statement of Operations

For the Fiscal Year Ended November 30, 2020

|

|

||||||

| Investment income: | ||||||

| Dividends — unaffiliated issuers (net of tax withholding of $861,054) |

$ | 98,039,646 | ||||

| Dividends — affiliated issuers |

39,038 | |||||

| Less: Return of Capital on Dividends |

(90,787,356 | ) | ||||

| Interest |

58,835 | |||||

| Total investment income | 7,350,163 | |||||

| Expenses: | ||||||

| Management fees |

10,607,099 | |||||

| Transfer Agency fees(a) |

525,917 | |||||

| Professional fees |

466,281 | |||||

| Distribution and Service (12b-1)fees(a) |

363,576 | |||||

| Franchise tax expense |

227,551 | |||||

| Registration fees |

163,125 | |||||

| Custody, accounting and administrative services |

147,754 | |||||

| Printing and mailing costs |

147,282 | |||||

| Service Share fees — Class C |

85,962 | |||||

| Trustee fees |

21,513 | |||||

| Other |

21,014 | |||||

| Total operating expenses, before taxes | 12,777,074 | |||||

| Less — expense reductions |

(287,087 | ) | ||||

| Net operating expenses, before taxes | 12,489,987 | |||||

| NET INVESTMENT LOSS, BEFORE TAXES | (5,139,824 | ) | ||||

| Current and deferred tax expense | (139,064 | ) | ||||

| NET INVESTMENT LOSS, NET OF TAXES | (5,278,888 | ) | ||||

| Realized and unrealized gain (loss): | ||||||

| Net realized gain (loss) from: |

||||||

| Investments — unaffiliated issuers |

(520,453,207 | ) | ||||

| Foreign currency transactions |

43,710 | |||||

| Current and deferred tax expense |

(14,080,343 | ) | ||||

| Net change in unrealized gain (loss) on: |

||||||

| Investments — unaffiliated issuers |

75,974,862 | |||||

| Purchased options |

445,924 | |||||

| Written options |

(217,500 | ) | ||||

| Foreign currency translation |

5,438 | |||||

| Deferred tax benefit |

2,061,924 | |||||

| Net realized and unrealized loss, net of taxes | (456,219,192 | ) | ||||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (461,498,080 | ) | |||

| (a) | Class specific Distribution and/or Service (12b-1) and Transfer Agent fees were as follows: |

| Distribution and/or (12b-1) Service Fees | Transfer Agent Fees | |||||||||||||||||||||||||||||||||||

| Class A |

Class C |

Class R |

Class A |

Class C |

Institutional |

Investor |

Class R6 |

Class R |

Class P |

|||||||||||||||||||||||||||

| $101,330 | $ | 257,887 | $ | 4,359 | $ | 68,906 | $ | 58,454 | $ | 100,392 | $ | 86,230 | $ | 46,843 | $ | 1,482 | $ | 163,610 | ||||||||||||||||||

| 14 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Statements of Changes in Net Assets

| For the Fiscal Year Ended November 30, 2020 |

For the Fiscal Year Ended November 30, 2019 |

|||||||||

| From operations: | ||||||||||

| Net investment loss, net of taxes |

$ | (5,278,888 | ) | $ | (14,172,362 | ) | ||||

| Net realized loss, net of taxes |

(534,489,840 | ) | (32,745,401 | ) | ||||||

| Net change in unrealized gain (loss), net of taxes |

78,270,648 | (188,225,976 | ) | |||||||

| Net decrease in net assets resulting from operations | (461,498,080 | ) | (235,143,739 | ) | ||||||

| Distributions to shareholders: | ||||||||||

| From distributable earnings |

||||||||||

| Class A Shares |

— | (381,978 | ) | |||||||

| Class C Shares |

— | (390,185 | ) | |||||||

| Institutional Shares |

— | (2,761,431 | ) | |||||||

| Investor Shares |

— | (581,787 | ) | |||||||

| Class R6 Shares |

— | (751,716 | ) | |||||||

| Class R Shares |

— | (10,186 | ) | |||||||

| Class P Shares |

— | (4,774,138 | ) | |||||||

| From return of capital |

||||||||||

| Class A Shares |

(3,740,013 | ) | (5,911,900 | ) | ||||||

| Class C Shares |

(3,271,090 | ) | (6,038,926 | ) | ||||||

| Institutional Shares |

(21,684,266 | ) | (42,738,912 | ) | ||||||

| Investor Shares |

(4,311,050 | ) | (9,004,374 | ) | ||||||

| Class R6 Shares |

(14,964,119 | ) | (11,634,374 | ) | ||||||

| Class R Shares |

(83,728 | ) | (157,655 | ) | ||||||

| Class P Shares |

(49,952,163 | ) | (73,889,763 | ) | ||||||

| Total distributions to shareholders | (98,006,429 | ) | (159,027,325 | ) | ||||||

| From share transactions: | ||||||||||

| Proceeds from sales of shares |

969,598,587 | 917,467,591 | ||||||||

| Reinvestment of distributions |

91,996,502 | 150,234,567 | ||||||||

| Cost of shares redeemed |

(1,247,880,583 | ) | (1,206,522,397 | ) | ||||||

| Net decrease in net assets resulting from share transactions | (186,285,494 | ) | (138,820,239 | ) | ||||||

| TOTAL DECREASE | (745,790,003 | ) | (532,991,303 | ) | ||||||

| Net assets: | ||||||||||

| Beginning of year |

1,729,006,839 | 2,261,998,142 | ||||||||

| End of year |

$ | 983,216,836 | $ | 1,729,006,839 | ||||||

| The accompanying notes are an integral part of these financial statements. | 15 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Selected Share Data for a Share Outstanding Throughout the Year

| Goldman Sachs MLP Energy Infrastructure Fund | ||||||||||||||||||||||

| Class A Shares | ||||||||||||||||||||||

| Year Ended November 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data* | ||||||||||||||||||||||

| Net asset value, beginning of year |

$ | 26.10 | $ | 31.90 | $ | 34.00 | $ | 39.40 | $ | 38.10 | ||||||||||||

| Net investment income (loss)(a) |

(0.15 | ) | (0.30 | ) | (0.10 | ) | (0.35 | ) | (0.30 | ) | ||||||||||||

| Net realized and unrealized gain (loss) |

(7.86 | ) | (3.00 | ) | 0.35 | (2.85 | ) | 4.00 | ||||||||||||||

| Total from investment operations |

(8.01 | ) | (3.30 | ) | 0.25 | (3.20 | ) | 3.70 | ||||||||||||||

| Distributions to shareholders from net investment income |

— | (0.15 | ) | (0.80 | ) | (0.25 | ) | — | ||||||||||||||

| Distributions to shareholders from return of capital |

(0.94 | ) | (2.35 | ) | (1.55 | ) | (1.95 | ) | (2.40 | ) | ||||||||||||

| Total distributions |

(0.94 | ) | (2.50 | ) | (2.35 | ) | (2.20 | ) | (2.40 | ) | ||||||||||||

| Net asset value, end of year |

$ | 17.15 | $ | 26.10 | $ | 31.90 | $ | 34.00 | $ | 39.40 | ||||||||||||

| Total return(b) | (27.83 | )% | (11.06 | )% | 0.23 | % | (8.35 | )% | 10.23 | % | ||||||||||||

| Net assets, end of year (in 000s) |

$ | 34,024 | $ | 60,112 | $ | 95,120 | $ | 115,467 | $ | 289,689 | ||||||||||||

| Ratio of total expenses to average net assets after tax (benefit)/expense(c) |

2.64 | % | 1.67 | % | 1.67 | % | 1.52 | % | 1.45 | % | ||||||||||||

| Ratio of net expenses to average net assets after tax (benefit)/expense(c) |

2.61 | % | 1.67 | % | 1.67 | % | 1.52 | % | 1.45 | % | ||||||||||||

| Ratio of net expenses to average net assets before tax (benefit)/expense |

1.49 | % | 1.44 | % | 1.40 | % | 1.42 | % | 1.45 | % | ||||||||||||

| Ratio of net investment loss to average net assets(d) |

(0.81 | )% | (1.02 | )% | (0.34 | )% | (0.85 | )% | (0.87 | )% | ||||||||||||

| Portfolio turnover rate(e) |

139 | % | 51 | % | 68 | % | 42 | % | 104 | % | ||||||||||||

| * | On June 5, 2020, the Fund effected a 5-for-1 reverse share split. All per share data prior to June 5, 2020 has been adjusted to reflect the reverse share split. |

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. |

| (c) | Current and deferred tax expense/benefit for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (d) | Current and deferred tax benefit for the ratio calculation is derived from net investment income (loss) only. |

| (e) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| 16 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout the Year

| Goldman Sachs MLP Energy Infrastructure Fund | ||||||||||||||||||||||

| Class C Shares | ||||||||||||||||||||||

| Year Ended November 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data* | ||||||||||||||||||||||

| Net asset value, beginning of year |

$ | 24.55 | $ | 30.35 | $ | 32.70 | $ | 38.25 | $ | 37.30 | ||||||||||||

| Net investment loss(a) |

(0.29 | ) | (0.50 | ) | (0.35 | ) | (0.60 | ) | (0.60 | ) | ||||||||||||

| Net realized and unrealized gain (loss) |

(7.44 | ) | (2.80 | ) | 0.35 | (2.75 | ) | 3.95 | ||||||||||||||

| Total from investment operations |

(7.73 | ) | (3.30 | ) | — | (3.35 | ) | 3.35 | ||||||||||||||

| Distributions to shareholders from net investment income |

— | (0.15 | ) | (0.80 | ) | (0.25 | ) | — | ||||||||||||||

| Distributions to shareholders from return of capital |

|

(0.94 |

) |

(2.35 | ) | (1.55 | ) | (1.95 | ) | (2.40 | ) | |||||||||||

| Total distributions |

(0.94 | ) | (2.50 | ) | (2.35 | ) | (2.20 | ) | (2.40 | ) | ||||||||||||

| Net asset value, end of year |

$ | 15.88 | $ | 24.55 | $ | 30.35 | $ | 32.70 | $ | 38.25 | ||||||||||||

| Total return(b) | (28.47 | )% | (11.64 | )% | (0.38 | )% | (9.15 | )% | 9.49 | % | ||||||||||||

| Net assets, end of year (in 000s) |

$ | 24,897 | $ | 58,044 | $ | 92,201 | $ | 124,291 | $ | 170,575 | ||||||||||||

| Ratio of total expenses to average net assets after tax (benefit)/expense(c) |

3.39 | % | 2.42 | % | 2.44 | % | 2.28 | % | 2.20 | % | ||||||||||||

| Ratio of net expenses to average net assets after tax (benefit)/expense(c) |

3.37 | % | 2.42 | % | 2.44 | % | 2.28 | % | 2.20 | % | ||||||||||||

| Ratio of net expenses to average net assets before tax (benefit)/expense |

2.24 | % | 2.19 | % | 2.15 | % | 2.17 | % | 2.21 | % | ||||||||||||

| Ratio of net investment loss to average net assets(d) |

(1.63 | )% | (1.77 | )% | (1.06 | )% | (1.60 | )% | (1.63 | )% | ||||||||||||

| Portfolio turnover rate(e) |

139 | % | 51 | % | 68 | % | 42 | % | 104 | % | ||||||||||||

| * | On June 5, 2020, the Fund effected a 5-for-1 reverse share split. All per share data prior to June 5, 2020 has been adjusted to reflect the reverse share split. |

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. |

| (c) | Current and deferred tax expense/benefit for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (d) | Current and deferred tax benefit for the ratio calculation is derived from net investment income (loss) only. |

| (e) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| The accompanying notes are an integral part of these financial statements. | 17 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout the Year

| Goldman Sachs MLP Energy Infrastructure Fund | ||||||||||||||||||||||

| Institutional Shares | ||||||||||||||||||||||

| Year Ended November 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data* | ||||||||||||||||||||||

| Net asset value, beginning of year |

$ | 26.95 | $ | 32.75 | $ | 34.75 | $ | 40.10 | $ | 38.50 | ||||||||||||

| Net investment income (loss)(a) |

(0.11 | ) | (0.20 | ) | 0.10 | (0.15 | ) | (0.25 | ) | |||||||||||||

| Net realized and unrealized gain (loss) |

(8.06 | ) | (3.10 | ) | 0.25 | (3.00 | ) | 4.25 | ||||||||||||||

| Total from investment operations |

(8.17 | ) | (3.30 | ) | 0.35 | (3.15 | ) | 4.00 | ||||||||||||||

| Distributions to shareholders from net investment income |

— | (0.15 | ) | (0.80 | ) | (0.25 | ) | — | ||||||||||||||

| Distributions to shareholders from return of capital |

(0.94 | ) | (2.35 | ) | (1.55 | ) | (1.95 | ) | (2.40 | ) | ||||||||||||

| Total distributions |

(0.94 | ) | (2.50 | ) | (2.35 | ) | (2.20 | ) | (2.40 | ) | ||||||||||||

| Net asset value, end of year |

$ | 17.84 | $ | 26.95 | $ | 32.75 | $ | 34.75 | $ | 40.10 | ||||||||||||

| Total return(b) | (27.54 | )% | (10.77 | )% | 0.67 | % | (8.21 | )% | 10.92 | % | ||||||||||||

| Net assets, end of year (in 000s) |

$ | 182,236 | $ | 502,633 | $ | 651,132 | $ | 1,711,829 | $ | 1,830,614 | ||||||||||||

| Ratio of total expenses to average net assets after tax (benefit)/expense(c) |

2.25 | % | 1.28 | % | 1.43 | % | 1.14 | % | 1.05 | % | ||||||||||||

| Ratio of net expenses to average net assets after tax (benefit)/expense(c) |

2.22 | % | 1.28 | % | 1.43 | % | 1.14 | % | 1.05 | % | ||||||||||||

| Ratio of net expenses to average net assets before tax (benefit)/expense |

1.10 | % | 1.05 | % | 1.01 | % | 1.03 | % | 1.05 | % | ||||||||||||

| Ratio of net investment loss to average net assets(d) |

(0.56 | )% | (0.61 | )% | 0.34 | % | (0.42 | )% | (0.69 | )% | ||||||||||||

| Portfolio turnover rate(e) |

139 | % | 51 | % | 68 | % | 42 | % | 104 | % | ||||||||||||

| * | On June 5, 2020, the Fund effected a 5-for-1 reverse share split. All per share data prior to June 5, 2020 has been adjusted to reflect the reverse share split. |

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. |

| (c) | Current and deferred tax expense/benefit for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (d) | Current and deferred tax benefit for the ratio calculation is derived from net investment income (loss) only. |

| (e) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| 18 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout the Year

| Goldman Sachs MLP Energy Infrastructure Fund | ||||||||||||||||||||||

| Investor Shares | ||||||||||||||||||||||

| Year Ended November 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data* | ||||||||||||||||||||||

| Net asset value, beginning of year |

$ | 26.65 | $ | 32.50 | $ | 34.50 | $ | 39.85 | $ | 38.35 | ||||||||||||

| Net investment income (loss)(a) |

(0.15 | ) | (0.25 | ) | (0.05 | ) | (0.25 | ) | (0.20 | ) | ||||||||||||

| Net realized and unrealized gain (loss) |

(7.96 | ) | (3.10 | ) | 0.40 | (2.90 | ) | 4.10 | ||||||||||||||

| Total from investment operations |

(8.11 | ) | (3.35 | ) | 0.35 | (3.15 | ) | 3.90 | ||||||||||||||

| Distributions to shareholders from net investment income |

— | (0.15 | ) | (0.80 | ) | (0.25 | ) | — | ||||||||||||||

| Distributions to shareholders from return of capital |

(0.94 | ) | (2.35 | ) | (1.55 | ) | (1.95 | ) | (2.40 | ) | ||||||||||||

| Total distributions |

(0.94 | ) | (2.50 | ) | (2.35 | ) | (2.20 | ) | (2.40 | ) | ||||||||||||

| Net asset value, end of year |

$ | 17.60 | $ | 26.65 | $ | 32.50 | $ | 34.50 | $ | 39.85 | ||||||||||||

| Total return(b) | (27.63 | )% | (11.01 | )% | 0.68 | % | (8.26 | )% | 10.69 | % | ||||||||||||

| Net assets, end of year (in 000s) |

$ | 32,396 | $ | 98,506 | $ | 142,664 | $ | 156,974 | $ | 121,705 | ||||||||||||

| Ratio of total expenses to average net assets after tax (benefit)/expense(c) |

2.38 | % | 1.42 | % | 1.43 | % | 1.29 | % | 1.20 | % | ||||||||||||

| Ratio of net expenses to average net assets after tax (benefit)/expense(c) |

2.36 | % | 1.42 | % | 1.43 | % | 1.29 | % | 1.20 | % | ||||||||||||

| Ratio of net expenses to average net assets before tax (benefit)/expense |

1.23 | % | 1.19 | % | 1.15 | % | 1.17 | % | 1.20 | % | ||||||||||||

| Ratio of net investment loss to average net assets(d) |

(0.73 | )% | (0.77 | )% | (0.07 | )% | (0.63 | )% | (0.60 | )% | ||||||||||||

| Portfolio turnover rate(e) |

139 | % | 51 | % | 68 | % | 42 | % | 104 | % | ||||||||||||

| * | On June 5, 2020, the Fund effected a 5-for-1 reverse share split. All per share data prior to June 5, 2020 has been adjusted to reflect the reverse share split. |

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. |

| (c) | Current and deferred tax expense/benefit for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (d) | Current and deferred tax benefit for the ratio calculation is derived from net investment income (loss) only. |

| (e) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| The accompanying notes are an integral part of these financial statements. | 19 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout Each Period

| Goldman Sachs MLP Energy Infrastructure Fund | ||||||||||||||

| Class R6 Shares | ||||||||||||||

| Year Ended November 30, | Period Ended November 30, 2018(a) |

|||||||||||||

| 2020 | 2019 | |||||||||||||

| Per Share Data* | ||||||||||||||

| Net asset value, beginning of period |

$ | 27.00 | $ | 32.75 | $ | 32.15 | ||||||||

| Net investment income (loss)(b) |

(0.05 | ) | (0.20 | ) | (0.10 | ) | ||||||||

| Net realized and unrealized gain (loss) |

(8.15 | ) | (3.05 | ) | 2.50 | |||||||||

| Total from investment operations |

(8.20 | ) | (3.25 | ) | 2.40 | |||||||||

| Distributions to shareholders from net investment income |

— | (0.15 | ) | (0.65 | ) | |||||||||

| Distributions to shareholders from return of capital |

(0.94 | ) | (2.35 | ) | (1.15 | ) | ||||||||

| Total distributions |

(0.94 | ) | (2.50 | ) | (1.80 | ) | ||||||||

| Net asset value, end of period |

$ | 17.86 | $ | 27.00 | $ | 32.75 | ||||||||

| Total return(c) | (27.60 | )% | (10.60 | )% | 7.15 | % | ||||||||

| Net assets, end of period (in 000s) |

$ | 181,968 | $ | 165,252 | $ | 205,470 | ||||||||

| Ratio of total expenses to average net assets after tax (benefit)/expense(d) |

2.26 | % | 1.26 | % | 1.11 | %(e) | ||||||||

| Ratio of net expenses to average net assets after tax (benefit)/expense(d) |

2.23 | % | 1.26 | % | 1.11 | %(e) | ||||||||

| Ratio of net expenses to average net assets before tax (benefit)/expense |

1.11 | % | 1.04 | % | 1.00 | %(e) | ||||||||

| Ratio of net investment loss to average net assets(f) |

(0.29 | )% | (0.66 | )% | (0.46 | )%(e) | ||||||||

| Portfolio turnover rate(g) |

139 | % | 51 | % | 68 | % | ||||||||

| * | On June 5, 2020, the Fund effected a 5-for-1 reverse share split. All per share data prior to June 5, 2020 has been adjusted to reflect the reverse share split. |

| (a) | Commenced operations on April 2, 2018. |

| (b) | Calculated based on the average shares outstanding methodology. |

| (c) | Assumes investment at the NAV at the beginning of the period, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the period and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| (d) | Current and deferred tax expense/benefit for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (e) | Annualized with the exception of tax expenses. |

| (f) | Current and deferred tax benefit for the ratio calculation is derived from net investment income (loss) only. |

| (g) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| 20 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout the Year

| Goldman Sachs MLP Energy Infrastructure Fund | ||||||||||||||||||||||

| Class R Shares | ||||||||||||||||||||||

| Year Ended November 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data* | ||||||||||||||||||||||

| Net asset value, beginning of year |

$ | 25.60 | $ | 31.40 | $ | 33.55 | $ | 39.05 | $ | 37.80 | ||||||||||||

| Net investment income (loss)(a) |

(0.17 | ) | (0.40 | ) | (0.20 | ) | (0.40 | ) | (0.45 | ) | ||||||||||||

| Net realized and unrealized gain (loss) |

(7.77 | ) | (2.90 | ) | 0.40 | (2.90 | ) | 4.10 | ||||||||||||||

| Total from investment operations |

(7.94 | ) | (3.30 | ) | 0.20 | (3.30 | ) | 3.65 | ||||||||||||||

| Distributions to shareholders from net investment income |

— | (0.15 | ) | (0.80 | ) | (0.25 | ) | — | ||||||||||||||

| Distributions to shareholders from return of capital |

(0.94 | ) | (2.35 | ) | (1.55 | ) | (1.95 | ) | (2.40 | ) | ||||||||||||

| Total distributions |

(0.94 | ) | (2.50 | ) | (2.35 | ) | (2.20 | ) | (2.40 | ) | ||||||||||||

| Net asset value, end of year |

$ | 16.72 | $ | 25.60 | $ | 31.40 | $ | 33.55 | $ | 39.05 | ||||||||||||

| Total return(b) | (28.11 | )% | (11.24 | )% | 0.24 | % | (8.83 | )% | 10.18 | % | ||||||||||||

| Net assets, end of year (in 000s) |

$ | 796 | $ | 1,012 | $ | 2,254 | $ | 2,009 | $ | 2,026 | ||||||||||||

| Ratio of total expenses to average net assets after tax (benefit)/expense(c) |

2.90 | % | 1.92 | % | 1.93 | % | 1.77 | % | 1.70 | % | ||||||||||||

| Ratio of net expenses to average net assets after tax (benefit)/expense(c) |

2.87 | % | 1.92 | % | 1.93 | % | 1.77 | % | 1.70 | % | ||||||||||||

| Ratio of net expenses to average net assets before tax (benefit)/expense |

1.74 | % | 1.69 | % | 1.65 | % | 1.68 | % | 1.70 | % | ||||||||||||

| Ratio of net investment loss to average net assets(d) |

(0.94 | )% | (1.31 | )% | (0.59 | )% | (1.06 | )% | (1.23 | )% | ||||||||||||

| Portfolio turnover rate(e) |

139 | % | 51 | % | 68 | % | 42 | % | 104 | % | ||||||||||||

| * | On June 5, 2020, the Fund effected a 5-for-1 reverse share split. All per share data prior to June 5, 2020 has been adjusted to reflect the reverse share split. |

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. |

| (c) | Current and deferred tax expense/benefit for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (d) | Current and deferred tax benefit for the ratio calculation is derived from net investment income (loss) only. |

| (e) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| The accompanying notes are an integral part of these financial statements. | 21 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout Each Period

| Goldman Sachs MLP Energy Infrastructure Fund | ||||||||||||||

| Class P Shares | ||||||||||||||

| Year Ended November 30, | Period Ended November 30, 2018(a) |

|||||||||||||

| 2020 | 2019 | |||||||||||||

| Per Share Data* | ||||||||||||||

| Net asset value, beginning of period |

$ | 27.05 | $ | 32.85 | $ | 34.80 | ||||||||

| Net investment income (loss)(b) |

(0.08 | ) | (0.20 | ) | (0.15 | ) | ||||||||

| Net realized and unrealized gain (loss) |

(8.12 | ) | (3.10 | ) | — | (c) | ||||||||

| Total from investment operations |

(8.20 | ) | (3.30 | ) | (0.15 | ) | ||||||||

| Distributions to shareholders from net investment income |

— | (0.15 | ) | (0.65 | ) | |||||||||

| Distributions to shareholders from return of capital |

(0.94 | ) | (2.35 | ) | (1.15 | ) | ||||||||

| Total distributions |

(0.94 | ) | (2.50 | ) | (1.80 | ) | ||||||||

| Net asset value, end of period |

$ | 17.91 | $ | 27.05 | $ | 32.85 | ||||||||

| Total return(d) | (27.55 | )% | (10.73 | )% | (0.72 | )% | ||||||||

| Net assets, end of period (in 000s) |

$ | 526,900 | $ | 843,448 | $ | 1,073,157 | ||||||||

| Ratio of total expenses to average net assets after tax (benefit)/expense(e) |