Form 8-K PROCTER & GAMBLE Co For: Jan 26

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934

|

Date of Report (Date of earliest event reported)

|

January 26, 2016

|

|

THE PROCTER & GAMBLE COMPANY

|

|

(Exact name of registrant as specified in its charter)

|

|

Ohio

|

|

1-434

|

|

31-0411980

|

|

(State or other jurisdiction

of incorporation)

|

|

(Commission File Number)

|

|

(IRS Employer

Identification Number)

|

|

One Procter & Gamble Plaza, Cincinnati, Ohio

|

|

45202

|

|

(Address of principal executive offices)

|

|

Zip Code

|

|

(513) 983-1100

|

|

45202

|

|

(Registrant's telephone number, including area code)

|

|

Zip Code

|

|

o

|

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

|

| o |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

|

|

o

|

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

|

|

o

|

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

|

ITEM 7.01 REGULATION FD DISCLOSURE

On January 26, 2016, The Procter & Gamble Company (the "Company") issued a press release announcing its second quarter results and hosted a conference call related to those results. The Company is furnishing on Form 8-K a series of slides referenced in the conference call, which are also posted on the Company's website.

The Company is furnishing this 8-K pursuant to Item 7.01, "Regulaton FD Disclosure."

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this Report to be signed on its behalf by the undersigned hereunto duly authorized.

|

THE PROCTER & GAMBLE COMPANY

|

||||||

|

BY:

|

/s/ Susan S. Whaley

|

|||||

|

Susan S. Whaley

|

||||||

|

Assistant Secretary

|

||||||

|

January 26, 2016

|

||||||

EXHIBIT(S)

99. Informational Slides Provided by The Procter & Gamble Company dated January 26, 2016.

Procter & GambleEarnings Release:Q2 FY 2016 Results January 26, 2016

Business ResultsQ2 FY 2016

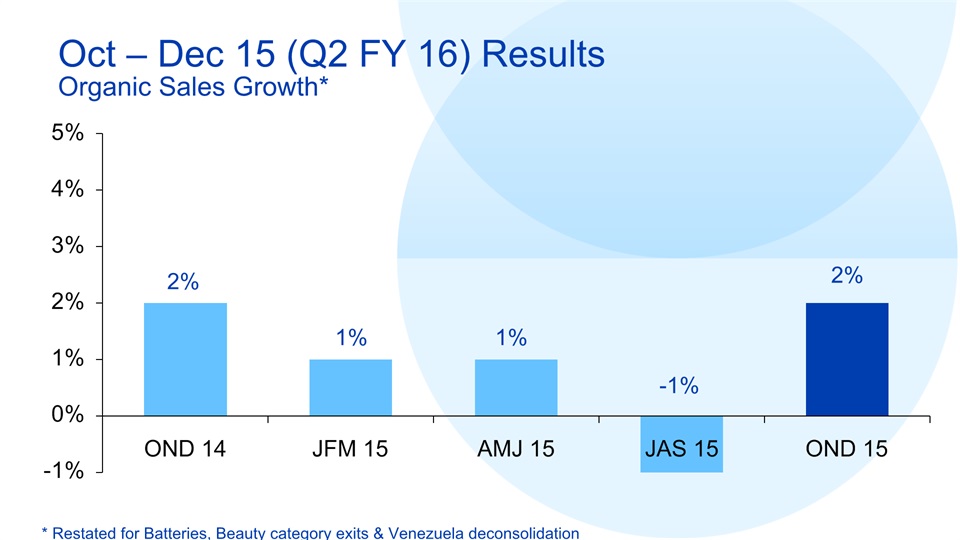

Oct – Dec 15 (Q2 FY 16) ResultsOrganic Sales Growth* * Restated for Batteries, Beauty category exits & Venezuela deconsolidation

Oct – Dec 15 (Q2 FY 16) ResultsCore EPS Growth* * Restated for Batteries & Beauty category exits Core EPS includes 350 basis points of operating margin improvement, including 270 basis points of productivity savings.

Oct – Dec 15 (Q2 FY 16) ResultsCurrency Neutral Core EPS Growth* * Restated for Batteries & Beauty category exits

Business SegmentsQ2 FY 2016

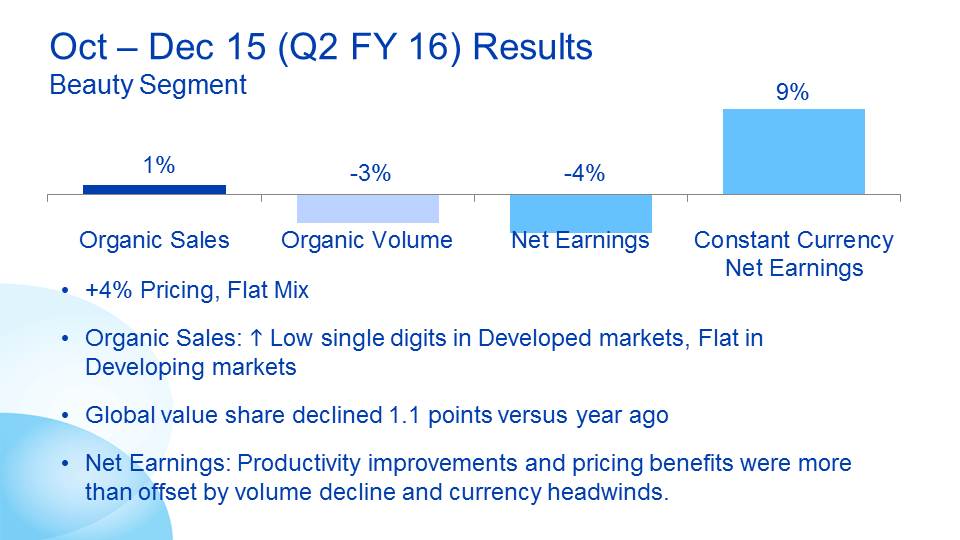

Oct – Dec 15 (Q2 FY 16) ResultsBeauty Segment 1% -3% -4% +4% Pricing, Flat MixOrganic Sales: h Low single digits in Developed markets, Flat in Developing marketsGlobal value share declined 1.1 points versus year agoNet Earnings: Productivity improvements and pricing benefits were more than offset by volume decline and currency headwinds.

Oct – Dec 15 (Q2 FY 16) ResultsGrooming Segment 3% -1% -19% +6% Pricing, -2% MixOrganic Sales: h Low single digits in Developed markets, h Mid-single digits in Developing marketsGlobal value share declined 1.4 points versus year agoNet Earnings: Productivity improvements and pricing were more than offset by volume decline, mix hurts and currency headwinds. -5%

Category HighlightsQ2 FY 2016

Oct – Dec 15 (Q2 FY 16) ResultsBeauty Highlights Hair Care organic sales were flat versus year ago. Developing markets were up versus year ago, including double-digit organic sales growth in Latin America. Developed markets declined as growth in Head & Shoulders was more than offset by challenges on Herbal Essences and Vidal Sassoon. Skin & Personal Care organic sales grew low single digits versus year ago, as double-digit growth on SKII and strong Old Spice sales in the U.S. were partially offset by declining Olay sales. By Category Organic Sales Growth IYA Global Developed Developing Hair Care ~= - + Skin & Personal Care + + ~= + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than1%.

Oct – Dec 15 (Q2 FY 16) ResultsGrooming Highlights Shave Care organic sales were up low single digits versus year ago, as price increases and growth on Fusion FlexBall and Venus Swirl were partially offset by increased competitive activity and category softness in the U.S.Appliances organic sales grew low single digits behind innovation expansion and strong in-store execution. By Category Organic Sales Growth IYA Global Developed Developing Grooming + + + + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than1%.

Oct – Dec 15 (Q2 FY 16) ResultsHealth Care Highlights Oral Care organic sales grew low single digits. Developed market organic sales increased mid-single digits behind strong growth on power toothbrushes and in the premium tier Pro-Health and 3D White franchises. Developing markets were flat as growth on power toothbrushes and price increases were offset by challenges in China.Personal Health Care organic sales increased mid-single digits driven by pricing and strong growth in developing markets. By Category Orga

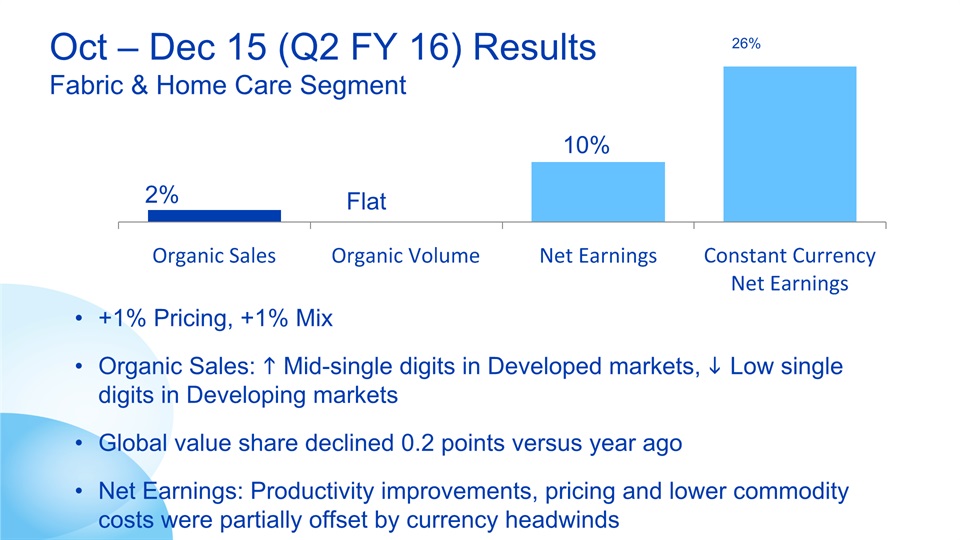

Oct – Dec 15 (Q2 FY 16) ResultsFabric & Home Care Highlights Fabric Care organic sales were up low single digits versus year ago. Developed markets increased mid-single digits driven by strong innovation in the U.S, where Fabric Care value share grew half-a-point in the December quarter. Developing markets declined as price increases and new compact liquid detergent launches were more than offset by customer inventory adjustments and declines due to de-prioritizing less profitable brands.Home Care organic sales grew mid-single digits versus year ago driven by solid growth in the U.S. behind strong innovation in the dish care business and benefits from recent pricing taken for devaluation. + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than1%. By Category Organic Sales Growth IYA Global Developed Developing Fabric Care + + - Home Care + + +

Oct – Dec 15 (Q2 FY 16) ResultsBaby, Feminine & Family Care Highlights Baby Care organic sales declined low single digits versus year ago as strong growth on Pampers in the U.S was more than offset by softness in international markets. In the U.S., Pampers value share was up more than one point versus year ago behind premium innovation.Feminine Care organic sales grew mid-single digits versus year ago behind strong share growth in the U.S. and pricing in developing markets.Family Care organic sales were flat as growth in the U.S. was offset by decline in Mexico as we shift our focus from low-tier to premium-tier products. By Category Organic Sales Growth IYA Global Developed Developing Baby Care - ~= - Feminine Care + + + Family Care ~= + - + represents growth above 1%, ~= represents growth of 1% to decline of 1%; - represents decline greater than1%.

FY 2016 Guidance

FY 2016 Guidance*Sales FY’16 Organic Sales Growth In-line to Up Low Single Digits Currency -7% Venezuela & Minor brand divestitures -2% to -3% All-in Sales Growth Down High Single Digits * Guidance assumes that Batteries & transitioning Beauty businesses are accounted for as discontinued operations Maintaining organic sales growth guidance of in-line to up low single digits versus fiscal 2015. Expect all-in sales growth to be down high single digits versus fiscal 2015.

FY 2016 Guidance*Earnings Per Share FY’16 Constant Currency Core EPS Growth Up Mid to High Single Digits Core EPS Growth -3% to -8% All-in EPS Growth +38% to +46% * Guidance assumes that Batteries & transitioning Beauty businesses are accounted for as discontinued operations Maintaining constant currency core EPS guidance of mid to high singles, with current outlook at the low end of this range.Reducing core EPS guidance to a range of -3% to -8% versus fiscal 2015 due to a $0.26 per share greater FX impact than expected at the beginning of the fiscal year.

FY 2016 GuidanceCash Generation & Usage Adjusted Free Cash Flow Productivity: 100%Capital Spending, % Sales: 5% to 6%Dividends: $7B+Share Retirement/Repurchases*: $8B to $9B * Includes shares retired at the close of the Duracell transaction. Given very strong progress to date, we are increasing our free cash flow productivity target from 90% to 100% of earnings.

FY 2016 GuidancePotential Headwinds Not Included in Guidance Further foreign currency weaknessChange in market growth rates Further unrest in the Middle East, Russia & the UkraineFurther deterioration in markets like Argentina and Brazil – with softened market conditions

FY 2016 GuidancePotential Tailwinds Not Included in Guidance Strengthening of foreign currencies Expansion of marketsU.S. economic growth accelerates

Forward Looking Statements Certain statements in this release or presentation, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives, and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “opportunity,” “plan,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties that may cause results to differ materially from those expressed or implied in the forward-looking statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events or otherwise. Risks and uncertainties to which our forward-looking statements are subject include, without limitation: (1) the ability to successfully manage global financial risks, including foreign currency fluctuations, currency exchange or pricing controls and localized volatility; (2) the ability to successfully manage local, regional or global economic volatility, including disruptions in credit markets, reduced market growth rates or changes affecting our credit rating, and generate sufficient income and cash flow to allow the Company to effect the expected share repurchases and dividend payments; (3) the ability to maintain key manufacturing and supply arrangements (including sole supplier and sole manufacturing plant arrangements) and manage disruption of business due to factors outside of our control, such as natural disasters and acts of war or terrorism; (4) the ability to successfully manage cost fluctuations and pressures, including commodity prices, raw materials, labor costs, energy costs and pension and health care costs, and achieve cost savings described in our announced productivity plan; (5) the ability to stay on the leading edge of innovation, obtain necessary intellectual property protections and successfully respond to technological advances attained by, and patents granted to, competitors; (6) the ability to compete with our local and global competitors in new and existing sales channels by successfully responding to competitive factors, including prices, promotional incentives and trade terms for products; (7) the ability to manage and maintain key customer relationships; (8) the ability to protect our reputation and brand equity by successfully managing real or perceived issues, including concerns about safety, quality, efficacy or similar matters that may arise; (9) the ability to successfully manage the financial, legal, reputational and operational risk associated with third party relationships, such as our suppliers, contractors and external business partners; (10) the ability to rely on and maintain key information technology systems and networks (including Company and third-party systems and networks) and maintain the security and functionality of such systems and networks and the data contained therein; (11) the ability to successfully manage regulatory and legal requirements and matters (including, without limitation, those laws and regulations involving product liability, intellectual property, antitrust, privacy, accounting standards and environmental) and to resolve pending matters within current estimates; (12) the ability to manage changes in applicable tax laws and regulations; (13) the ability to successfully manage our portfolio optimization strategy, as well as ongoing acquisition, divestiture and joint venture activities, to achieve the Company’s overall business strategy, without impacting the delivery of base business objectives; and (14) the ability to successfully achieve productivity improvements and manage ongoing organizational changes, while successfully identifying, developing and retaining particularly key employees, especially in key growth markets where the availability of skilled or experienced employees may be limited. For additional information concerning factors that could cause actual results to materially differ from those projected herein, please refer to our most recent 10-K, 10-Q and 8K reports.

The Procter & Gamble Company Regulation G Reconciliation of Non-GAAP Measures

In accordance with the SEC's Regulation G, the following provides definitions of the non-GAAP measures used in the earnings call and associated slides and the reconciliation to the most closely related GAAP measure. We believe that these measures provide useful perspective of underlying business trends and results and provide a more comparable measure of year-on-year results. These measures are also used to evaluate senior management and are a factor in determining their at-risk compensation. These non-GAAP measures are not intended to be considered by the user in place of the related GAAP measure, but rather as supplemental information to more fully understand our business results. These non-GAAP measures may not be the same as similar measures used by other companies due to possible differences in method and in the items or events being adjusted.

The measures provided are as follows:

|

1.

|

Organic Sales Growth—page 3

|

|

2.

|

Core EPS and Currency-Neutral Core EPS—pages 4-5

|

|

3.

|

Core Operating Profit Margin—page 6

|

|

4.

|

Core Selling, General and Administrative Expense (SG&A) as a Percentage of Net Sales—page 6

|

|

5.

|

Core Gross Margin—page 6

|

|

6.

|

Core Effective Tax Rate—page 6

|

|

7.

|

Adjusted Free Cash Flow—page 7

|

|

8.

|

Adjusted Free Cash Flow Productivity—page 7

|

The Core earnings measures included in the following reconciliation tables refer to the equivalent GAAP measures adjusted as applicable for the following items:

|

•

|

charges for incremental restructuring due to increased focus on productivity and cost savings,

|

|

•

|

charge in 2015 related to the change in accounting for our Venezuelan subsidiaries

|

|

•

|

charges for European legal matters, and

|

|

•

|

charges for balance sheet impacts from the devaluation of the foreign currency exchange rate in Venezuela prior to deconsolidation.

|

We do not view these items to be part of our sustainable results.

Organic sales growth: Organic sales growth is a non-GAAP measure of sales growth excluding the impacts of the Venezuela deconsolidation, acquisitions, divestitures and foreign exchange from year-over-year comparisons. We believe this provides investors with a more complete understanding of underlying sales trends by providing sales growth on a consistent basis.

Core EPS and currency-neutral Core EPS: Core EPS is a measure of the Company's diluted net earnings per share from continuing operations adjusted as indicated. Currency-neutral Core EPS is a measure of the Company's Core EPS excluding the incremental current year impact of foreign exchange. The tables below provide a reconciliation of revised diluted net earnings per share to Core EPS and of Core EPS to currency-neutral Core EPS.

Core operating profit margin: This is a measure of the Company's operating margin adjusted for items as indicated.

Core selling, general and administrative expense (SG&A) as a percentage of sales: This is a measure of the Company's SG&A as a percentage of sales adjusted for items as indicated.

Core gross margin: This is a measure of the Company's gross margin adjusted for items as indicated.

Core tax rate: This is a measure of the Company's tax rate on continuing operations adjusted for items as indicated.

Adjusted free cash flow: Adjusted free cash flow is defined as operating cash flow less capital spending excluding tax payments for the Pet divestiture. We view adjusted free cash flow as an important measure because it is one factor used in determining the amount of cash available for dividends and discretionary investment.

Adjusted free cash flow productivity: Adjusted free cash flow productivity is defined as the ratio of adjusted free cash flow to net earnings excluding impairment and Venezuela charges. The Company's long-term target is to generate annual free cash flow at or above 90 percent of net earnings.

1. Organic sales growth:

The reconciliation of reported sales growth to organic sales is as follows:

|

Three Months Ended December 31, 2015

|

Net Sales Growth

|

Foreign Exchange Impact

|

Acquisition/

Divestiture Impact* |

Organic Sales Growth

|

|||

|

Beauty

|

(10)%

|

7%

|

4%

|

1%

|

|||

|

Grooming

|

(10)%

|

12%

|

1%

|

3%

|

|||

|

Health Care

|

(5)%

|

8%

|

-

|

3%

|

|||

|

Fabric Care and Home Care

|

(7)%

|

8%

|

1%

|

2%

|

|||

|

Baby, Feminine and Family Care

|

(10)%

|

7%

|

3%

|

-

|

|||

|

Total P&G

|

(9)%

|

8%

|

3%

|

2%

|

*Acquisition/Divestiture Impact also includes the Venezuela deconsolidation, the mix impacts of acquisitions and divestitures and rounding impacts necessary to reconcile net sales to organic sales.

Organic Sales

Prior Periods

|

Total Company

|

Net Sales Growth

|

Foreign Exchange Impact

|

Acquisition/ Divestiture Impact*

|

Organic Sales Growth

|

||||

|

OND 2014

|

(4)%

|

6%

|

-

|

2%

|

||||

|

JFM 2015

|

(7)%

|

8%

|

-

|

1%

|

||||

|

AMJ 2015

|

(9)%

|

9%

|

1%

|

1%

|

||||

|

JAS 2015

|

(12)%

|

9%

|

2%

|

(1)%

|

||||

*Acquisition/Divestiture Impact includes volume and mix impacts of acquired and divested businesses, as well as rounding impacts necessary to reconcile net sales to organic sales.

Guidance

|

Total Company

|

Net Sales Growth

|

Foreign Exchange Impact

|

Acquisition/ Divestiture Impact*

|

Organic Sales Growth

|

||||

|

FY 2016

Estimate

|

Down high single digits

|

7%

|

2% to 3%

|

In line to up low single digits

|

*Acquisition/Divestiture Impact also includes the Venezuela deconsolidation, the mix impacts of acquisitions and divestitures and rounding impacts necessary to reconcile net sales to organic sales

2. Core EPS and currency-neutral Core EPS:

|

Three Months Ended December 31

|

|||

|

2015

|

2014

|

||

|

Diluted Net Earnings Per Share from Continuing Operations

|

$1.01

|

$0.92

|

|

|

Incremental Restructuring

|

0.03

|

0.02

|

|

|

Charges for European Legal Matters

|

-

|

0.01

|

|

|

Core EPS

|

$1.04

|

$0.95

|

|

|

Percentage change vs. prior period

|

9%

|

||

|

Currency Impact to Earnings

|

0.11

|

||

|

Currency-Neutral Core EPS

|

$1.15

|

||

|

Percentage change vs. prior period

|

21%

|

||

Note – All reconciling items are presented net of tax. Tax effects are calculated consistent with the nature of the underlying transaction.

Guidance

|

Total Company

|

Diluted EPS Growth

|

Impact of Incremental Non-Core Items*

|

Core EPS Growth

|

Foreign Exchange Impact

|

Currency-Neutral Core EPS

|

|

FY 2016 (Estimate)

|

38% to 46%

|

(41)% to (54)%

|

(3)% to (8)%

|

10%

|

Up mid-to-high single digits

|

*Includes change in discontinued operations (includes Batteries impairments) and the absence of significant one-time items (e.g. Venezuela charge)

Core EPS and Currency-Neutral Core EPS

Prior Periods

|

OND 14

|

OND 13

|

JFM 15

|

JFM 14

|

AMJ 15

|

AMJ 14

|

JAS 15

|

JAS 14

|

FY 15

|

|

|

Diluted Net Earnings Per Share from Continuing Operations, attributable to P&G

|

$ 0.92

|

$ 1.00

|

$ 0.82

|

$ 0.83

|

$ 0.17

|

$ 0.83

|

$ 0.96

|

$ 0.93

|

$ 2.84

|

|

Incremental Restructuring

|

0.02

|

0.02

|

0.06

|

0.04

|

0.02

|

0.03

|

0.02

|

0.02

|

0.17

|

|

Venezuela B/S Remeasurement & Devaluation Impacts

|

-

|

-

|

-

|

0.10

|

-

|

-

|

0.04

|

0.04

|

0.04

|

|

Charges for Pending European Legal Matters

|

0.01

|

-

|

-

|

-

|

(0.01)

|

0.02

|

-

|

-

|

0.01

|

|

Venezuela Deconsolidation Charge

|

-

|

-

|

-

|

|

0.71

|

-

|

-

|

-

|

0.71

|

|

Rounding

|

-

|

0.01

|

0.01

|

(0.01)

|

-

|

0.01

|

-

|

-

|

(0.01)

|

|

Core EPS

|

$ 0.95

|

$ 1.03

|

$ 0.89

|

$ 0.96

|

$ 0.93

|

$ 0.89

|

$ 0.98

|

$ 0.99

|

$ 3.76

|

|

Percentage change vs. prior period

|

(8)%

|

(7)%

|

4%

|

(1)%

|

|||||

|

Currency Impact to Earnings

|

0.15

|

0.18

|

0.13

|

0.13

|

|||||

|

Currency-Neutral Core EPS

|

$ 1.10

|

$ 1.07

|

$ 1.06

|

$ 1.11

|

|||||

|

Percentage change vs. prior period

|

7%

|

11%

|

19%

|

12%

|

|||||

3. Core operating profit margin:

|

OND 15

|

OND 14

|

|||

|

Operating Profit Margin

|

22.8%

|

19.4%

|

||

|

Incremental Restructuring

|

0.8%

|

0.4%

|

||

|

Charges for European Legal Matters

|

-

|

0.2%

|

||

|

Rounding

|

(0.1)%

|

-

|

||

|

Core Operating Profit Margin

|

23.5%

|

20.0%

|

||

|

Basis Point Change

|

350

|

4. Core selling, general and administrative expense (SG&A) as a percentage of net sales:

|

OND 15

|

OND 14

|

|||

|

SG&A as a % of NOS

|

27.2%

|

29.0%

|

||

|

Incremental Restructuring

|

0.1%

|

-

|

||

|

Charges for European Legal Matters

|

-

|

(0.2)%

|

||

|

Rounding

|

-

|

(0.1)%

|

||

|

Core SG&A as a % of NOS

|

27.3%

|

28.7%

|

||

|

Basis Point Change

|

(140)

|

5. Core gross margin:

|

OND 15

|

OND 14

|

|||

|

Gross Margin

|

50.0%

|

48.3%

|

||

|

Incremental Restructuring

|

0.8%

|

0.4%

|

||

|

Core Gross Margin

|

50.8%

|

48.7%

|

||

|

Basis Point Change

|

210

|

6. Core tax rate:

|

OND 15

|

OND 14

|

|||

|

Effective Tax Rate

|

23.6%

|

23.0%

|

||

|

Charges for European Legal Matters

|

-

|

(0.3)%

|

||

|

Core Tax Rate

|

23.6%

|

22.7%

|

||

|

Basis Point Change

|

90

|

7. Adjusted free cash flow:

|

Operating Cash Flow

|

Capital Spending

|

Free Cash Flow

|

Cash Tax Payment - Pet Sale

|

Adjusted Free Cash Flow

|

|

|

Three Months Ended December 31, 2015

|

$4,480

|

$(691)

|

$3,789

|

-

|

$3,789

|

|

Three Months Ended September 30, 2015

|

$3,538

|

$(532)

|

$3,006

|

-

|

$3,006

|

|

FY 2015

|

$14,608

|

$(3,736)

|

$10,872

|

$729

|

$11,601

|

8. Adjusted free cash flow productivity:

|

Adjusted Free

Cash Flow

|

Net

Earnings

|

Impairment & Deconsolidation Charges

|

Net Earnings Excl.

Impairment Charges |

Adjusted Free Cash

Flow Productivity

|

|

|

Three Months Ended December 31, 2015

|

$3,789

|

$3,228

|

-

|

$3,228

|

117%

|

|

Three Months Ended September 30, 2015

|

$3,006

|

$2,635

|

$350

|

$2,985

|

101%

|

|

FY 2015

|

$11,601

|

$7,144

|

$4,187

|

$11,331

|

102%

|

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Procter & Gamble (PG) PT Raised to $170 at Barclays

- Rush Enterprises, Inc. Reports First Quarter 2024 Results, Announces $0.17 Per Share Dividend

- Tide and Walmart Team Up to Expand Adoption of Washing in Cold with Consumers: For the Love of Their Laundry, Their Wallets and the Planet

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!