Form 8-K BALTIMORE GAS & ELECTRIC For: Nov 09 Filed by: EXELON GENERATION CO LLC

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

November 9, 2015

Date of Report (Date of earliest event reported)

| Commission File Number |

Exact Name of Registrant as Specified in Its Charter; State of Incorporation; Address of Principal Executive Offices; and Telephone Number |

IRS Employer | ||

| 1-16169 |

EXELON CORPORATION (a Pennsylvania corporation) 10 South Dearborn Street P.O. Box 805379 Chicago, Illinois 60680-5379 (800) 483-3220 |

23-2990190 | ||

| 333-85496 |

EXELON GENERATION COMPANY, LLC (a Pennsylvania limited liability company) 300 Exelon Way Kennett Square, Pennsylvania 19348-2473 (610) 765-5959 |

23-3064219 | ||

| 1-1839 |

COMMONWEALTH EDISON COMPANY (an Illinois corporation) 440 South LaSalle Street Chicago, Illinois 60605-1028 (312) 394-4321 |

36-0938600 | ||

| 000-16844 |

PECO ENERGY COMPANY (a Pennsylvania corporation) P.O. Box 8699 2301 Market Street Philadelphia, Pennsylvania 19101-8699 (215) 841-4000 |

23-0970240 | ||

| 1-1910 |

BALTIMORE GAS AND ELECTRIC COMPANY (a Maryland corporation) 2 Center Plaza 110 West Fayette Street Baltimore, Maryland 21201 (410) 234-5000 |

52-0280210 | ||

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Section 7 – Regulation FD

Item 7.01. Regulation FD Disclosure.

On November 8-11, 2015, Exelon Corporation (Exelon) will participate in the Edison Electric Institute Financial Conference. Attached as Exhibit 99.1 to this Current Report on Form 8-K are the presentation slides and handouts to be used at the conference.

Section 9 – Financial Statements and Exhibits

Item 9.01. Financial Statements and Exhibits.

| (d) | Exhibits. |

| Exhibit |

Description | |

| 99.1 | Presentation slides and handouts | |

* * * * *

This combined Form 8-K is being furnished separately by Exelon, Exelon Generation Company, LLC, Commonwealth Edison Company, PECO Energy Company, and Baltimore Gas and Electric Company (Registrants). Information contained herein relating to any individual Registrant has been furnished by such Registrant on its own behalf. No Registrant makes any representation as to information relating to any other Registrant.

This Current Report includes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 that are subject to risks and uncertainties. The factors that could cause actual results to differ materially from these forward-looking statements include those discussed herein as well as those discussed in (1) Exelon’s 2014 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) ITEM 8. Financial Statements and Supplementary Data: Note 22; (2) Exelon’s Third Quarter 2015 Quarterly Report on Form 10-Q in (a) Part II, Other Information, ITEM 1A. Risk Factors; (b) Part 1, Financial Information, ITEM 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) Part I, Financial Information, ITEM 1. Financial Statements: Note 19; and (3) other factors discussed in filings with the Securities and Exchange Commission by the Registrants. Readers are cautioned not to place undue reliance on these forward-looking statements, which apply only as of the date of this Current Report. None of the Registrants undertakes any obligation to publicly release any revision to its forward-looking statements to reflect events or circumstances after the date of this Current Report.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, each Registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| EXELON CORPORATION |

| /s/ Jonathan W. Thayer |

| Jonathan W. Thayer |

| Senior Executive Vice President and Chief Financial Officer |

| Exelon Corporation |

| EXELON GENERATION COMPANY, LLC |

| /s/ Bryan P. Wright |

| Bryan P. Wright |

| Senior Vice President and Chief Financial Officer Exelon Generation Company, LLC |

| COMMONWEALTH EDISON COMPANY |

| /s/ Joseph R. Trpik, Jr. |

| Joseph R. Trpik, Jr. |

| Senior Vice President, Chief Financial Officer and Treasurer |

| Commonwealth Edison Company |

| PECO ENERGY COMPANY |

| /s/ Phillip S. Barnett |

| Phillip S. Barnett |

| Senior Vice President, Chief Financial Officer and |

| Treasurer |

| PECO Energy Company |

| BALTIMORE GAS AND ELECTRIC COMPANY |

| /s/ David M. Vahos |

| David M. Vahos |

| Vice President, Chief Financial Officer and Treasurer |

| Baltimore Gas and Electric Company |

November 9, 2015

EXHIBIT INDEX

| Exhibit |

Description | |

| 99.1 | Presentation slides and handouts | |

Edison Electric Institute Financial Conference November 8–11, 2015 Exhibit 99.1 |

1 2015 EEI Financial Conference Cautionary Statements Regarding Forward-Looking Information

This presentation contains certain forward-looking statements

within the meaning of the Private Securities

Litigation Reform Act of 1995, that are subject to risks and uncertainties. The factors that could cause actual results to differ materially from the

forward-looking statements made by Exelon Corporation,

Commonwealth Edison Company, PECO Energy Company,

Baltimore Gas and Electric Company and Exelon

Generation Company, LLC (Registrants) include those factors

discussed herein, as well as the items discussed

in (1) Exelon’s 2014 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s Discussion and Analysis of Financial

Condition and Results of Operations and (c) ITEM 8. Financial

Statements and Supplementary Data: Note 22; (2)

Exelon’s Third Quarter 2015 Quarterly Report on

Form 10-Q in (a) Part II, Other Information, ITEM 1A. Risk

Factors; (b) Part 1, Financial Information, ITEM

2. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) Part I, Financial Information, ITEM 1. Financial

Statements: Note 19; and (3) other factors discussed in filings

with the SEC by the Registrants. Readers are

cautioned not to place undue reliance on these forward- looking statements, which apply only as of the date of this presentation. None of the

Registrants undertakes any obligation to publicly release any

revision to its forward- looking statements to

reflect events or circumstances after the date of this presentation. |

2 2015 EEI Financial Conference 2015: An Exceptional Year of Performance Our utilities are performing at their best levels, our generation business is world class and our

Constellation

business

maximizes

its

value.

We

will

deliver

earnings

between

$2.40

-

$2.60

(1)

per share.

• On track to invest $3.7 billion this year to

make the grid smarter, more reliable, and more resilient

• Exceeding $1 billion in net income this year at Exelon Utilities

• Constructive regulatory environments across our jurisdictions

–

PECO rate case settlement

–

ComEd formula rate

–

Recent BGE unanimous rate case settlement

• Industry leading operational excellence – 1 st Quartile SAIFI performance – 1 st Quartile CAIDI performance at ComEd and PECO, 2 nd Quartile at BGE – 1 st Quartile Customer Satisfaction – Top Decile Gas Odor Response • Successful generation to load matching strategy

is protecting earnings •

Active role in policy development to deliver Capacity

Performance construct •

#1

Provider

of

retail

electricity,

serving

34

TWhs

more

than

our

nearest

competitor

• Top 10 marketer of natural gas • World Class Operator – 2015 Nuclear capacity factor through 3Q: 93.8% – 2015 Power dispatch match through 3Q: 98.7% – 2015 Renewables energy capture 3Q: 95.6% (1) Represents adjusted (non-GAAP) operating earnings. Refer to slide 31 for a list of adjustments from GAAP EPS to

adjusted (non-GAAP) operating earnings |

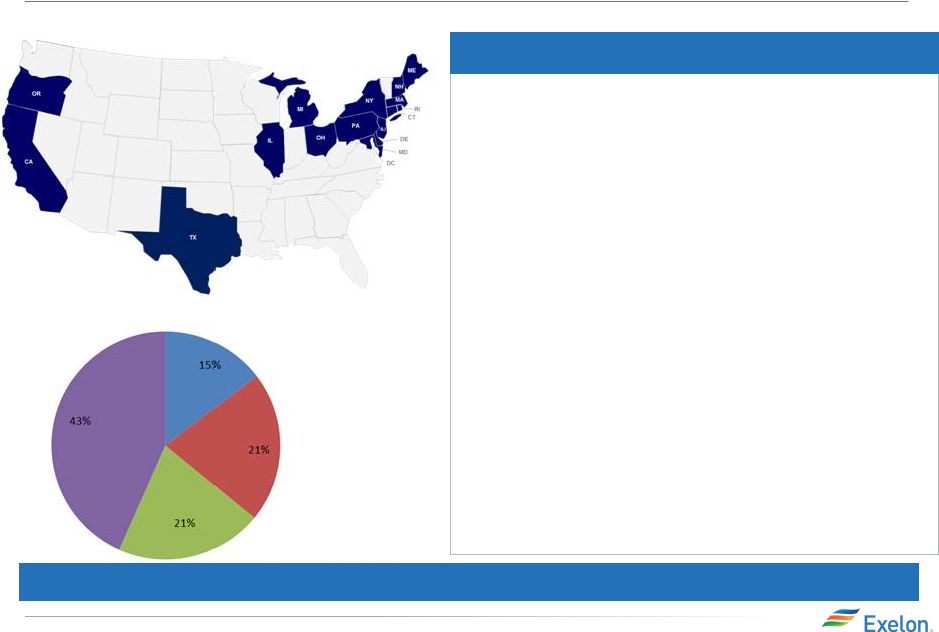

3 2015 EEI Financial Conference Looking Ahead • The Exelon Strategy • Addressing Key Immediate Issues 1) Capital Allocation 2) Pepco Holdings Acquisition 3) Extending Clinton One Year 4) Cost Management Initiative • The Foundation for Exelon’s Growth |

The Exelon Strategy |

5 2015 EEI Financial Conference Our Key Objectives Employ our integrated model to deliver stable

growth, sustainable earnings and an attractive dividend • Stable Growth – Grow our regulated and contracted businesses and optimize our existing generation portfolio • Sustainable Earnings – Utilities, contracted assets, and balanced generation to load strategy profits are an engine for predictable earnings

and our generation business positions us to capture market

upside •

Attractive Dividend

–

Dividend will be covered by the utilities, insulated

from the earnings volatility of the generation

business |

6 2015 EEI Financial Conference How We Will Meet Our Objectives We will produce stable earnings growth of 3-5% per year

from 2015 to 2018 (1)

• Investing more than $18 billion in Exelon’s current utilities through 2020 to modernize the grid and

better serve our customers ($11 billion from

2016-2018) We will sustain earnings growth while also preserving the benefit of market upside

through:

• Ensuring operating excellence across every business • Shifting our earnings mix to be more regulated through investments in Exelon’s utilities and the

acquisition of Pepco Holdings (Expect earnings to be ~60%

regulated in 2018) •

Effectively managing our costs

• Growing the amount of contracted assets in our Exelon Generation portfolio

• Maximizing the value of our generation fleet and customer base through our proven generation to

load matching strategy

• Hedging our generation in a manner that preserves upside from our fundamental price view

We will continue to deliver an attractive dividend of $1.24 per share (2) • Targeting dividend funding entirely from regulated utilities

• Our business mix protects our dividend regardless of changing phases of the commodities cycle

(1)

Growth target is a net income compounded annual growth rate

(CAGR), assumes September 30, 2015 market prices, and does not include our fundamental market view of prices (2) Dividends are subject to declaration by the Exelon Board of Directors |

7 2015 EEI Financial Conference We Are Well Down the Path of Delivering on Our Key Objectives

2011

(Pre-CEG Merger)

• 25,544 MW (Total Capacity) • 67% Nuclear • 151 TWh Generation • 5.4M Electric Customers • 0.5M Gas Customers • $791M Net Income (1) • $13B Rate Base • 6,054 Miles of Transmission Lines 2011 Earnings (1) • 29% Utilities • 71% Generation World Class Generator Top Performing Utilities Preeminent Competitive Energy Company Transforming the Business Mix 2014 (Post-CEG Merger) • 32,753 MW (Total Capacity) • 59% Nuclear (3) • 205 TWh Generation • 6.7M Electric Customers • 1.2M Gas Customers • $962M Net Income (1) • $20B Rate Base • 7,435 Miles of Transmission Lines 2014 Earnings (1) • 47% Utilities • 53% Generation 2018 (Post-PHI Merger) • 34,800 MW (Total Capacity) • 56% Nuclear (3) • 206 TWh Generation • 8.6M Electric Customers • 1.3M Gas Customers • $1.5B-1.7B Net Income (1,2) • $38B Rate Base • ~12,000 Miles of Transmission Lines • 48 States, DC, & Canada • ~210 TWh/yr • 6-8 Bcf of Gas 2018 Earnings (1,4) • ~60% Utilities • ~40% Generation (1) Represents adjusted (non-GAAP) operating earnings. Refer to slide 31 for a list of adjustments from GAAP EPS to adjusted (non-GAAP) operating earnings.

(2)

Includes after-tax interest expense of (~$150M) for debt

held at Corporate related to utility investment

(3)

Includes CENG at ownership; does not assume put

exercised (4)

Based on September 30, 2015 market prices

• 4 States • ~59 TWh/yr • <1 Bcf of Gas per day • 48 States, DC & Canada • ~155 TWh/yr • 4-6 Bcf of Gas per day |

Addressing Key Immediate Issues 1) Capital Allocation 2) Pepco Holdings Acquisition 3) Extending Clinton One Year 4) Cost Management Initiative |

Capital Allocation |

10 2015 EEI Financial Conference Delivering Value to Shareholders Through a Principled Capital

Allocation Policy

• Every capital decision is made to maximize value to our customers and shareholders • We are harvesting free cash flow from Exelon Generation to:

–

First, invest in utilities where we can earn an appropriate return,

–

Invest in contracted assets where we can meet return thresholds, and/or

–

Return capital to shareholders by retiring debt, repurchasing our shares, or increasing our dividend if required investment returns are not met

• We are committed to maintaining an attractive dividend • Our strong balance sheet underpins our capital allocation policy |

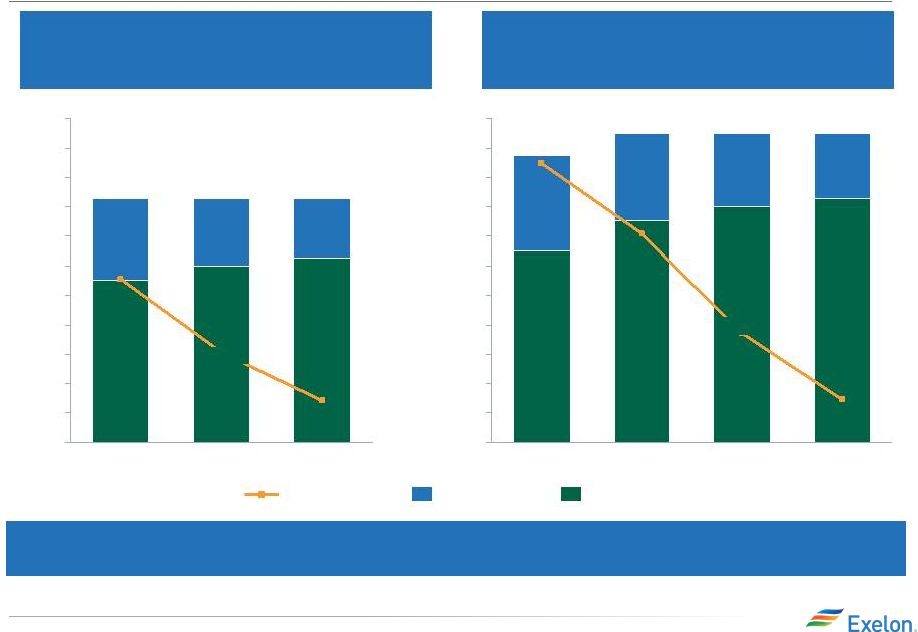

11 2015 EEI Financial Conference Redeploying Exelon Generation’s Free Cash Flow to Maximize Shareholder

Value

2016-2018 Exelon Generation Free Cash Flow

(1,2,3)

and Planned Growth Investment ($M)

~$2,700

~$4,150

Committed Contracted

Generation Growth CapEx

Available for Investing in

Utilities, Contracted Assets

or Returning Capital to

Shareholders

($750)

Committed Non-Contracted

Generation Growth CapEx

($700)

Cumulative ExGen

FCF 2016-18

If investments do not meet our thresholds, we will return

capital to shareholders (1) Free Cash Flow = Adjusted Cash Flow from Operations less Base CapEx and Nuclear Fuel. Free Cash Flow is midpoint of

a range based on September 30, 2015 market prices. Adjusted Cash Flow From Operations (non-GAAP) primarily includes net cash flows from operating activities and net cash flows

from investing activities excluding capital expenditures. Reconciliation of Free Cash Flow to GAAP can be found on slide 32. (2)

Does not include an extension of bonus depreciation. A two

year extension of bonus depreciation would add ~$200 million of Free Cash Flow

(3) Does not include impacts of PHI, which would decrease Free Cash Flow by (~$100M)

|

12 2015 EEI Financial Conference Capital Allocation — Disciplined Commitment to Growth We will prioritize investment in assets that minimize earnings volatility and support

stable earnings growth

Note: Including PHI would increase combined rate base by

$10 billion in 2018; Exelon Utilities 2016-2018 capital investment is $11 billion for existing Exelon utilities ($15 billion including PHI); Exelon Generation 2016-2018 investment opportunities total $1.6

billion No incremental equity issuance needed to

fund investment Exelon Utilities

Exelon Generation

• Investing in utility infrastructure to benefit our customers by making the grid smarter, more reliable, and more resilient - $18 billion from 2016 to 2020 (existing Exelon Utilities) - $25 billion from 2016 to 2020 (including PHI) • Targeting long-term ROE of 10% • Growing existing rate base from $22 billion in 2015 to $28 billion in 2018 • Earnings CAGR of 7-9% from 2015-2018 • Going forward, we will invest in assets with contracted cash flows - We are reviewing development opportunities that may result in investment of $2.8 billion from 2016 through 2020 - Approximately half of any growth investment will be funded through structured financing • Projects must earn attractive return ( 10% ROE) |

Pepco Holdings Acquisition |

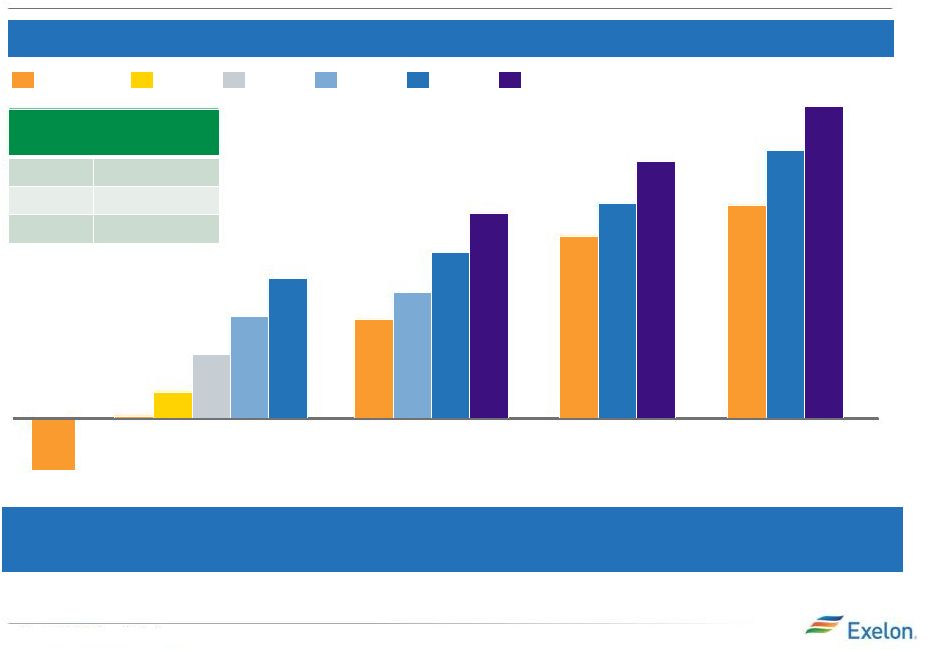

14 2015 EEI Financial Conference Projected Earnings Accretion at Various Earned ROE Levels

(1,2,3)

PHI Acquisition Increases Sustainability of Earnings

Growth Operational improvements should drive

enhanced regulatory outcomes, positively

impacting EPS

$0.06

$0.10

$0.13

2017

$0.02

~$0.00

9% ROE

8% ROE

7% ROE

6% ROE

10% ROE

Base Plan

(1)

~$0.10

$0.12

2018

$0.16

$0.20

~$0.18

2019

$0.21

$0.25

$0.29

$0.25

2020

~$0.20

(~$0.05)

2016

Q3 2015 Guidance

PHI Accretion

2017

~$0.00

2018

$0.07 to $0.12

2019

$0.15 to $0.20

(1)

Base Plan accretion figures represent midpoint of updated

guidance range from Q3 2015 earnings call and reflect current PHI business plan (2) Chart above illustrates accretion at various weighted average distribution earned ROEs for PHI

(3)

Accretion is measured against Exelon standalone plan, which

excludes the impact of PHI acquisition debt and equity Note: Represents adjusted (non-GAAP) operating earnings. Refer to slide 31 for a list of adjustments from GAAP

EPS to adjusted (non-GAAP) operating earnings |

15 2015 EEI Financial Conference BGE: A Proven Track Record of Enhancing Utility Value

• Increased reliability by 10% per year and customer satisfaction by 3% per year • Increased ROE by more than 250 basis points from 2011 to 2015 and grew net income 15% annually over same period • Continued system investments in reliability and safety necessitate continued rate cases for capital recovery Delivering value to our customers and regulators by improving reliability while providing

investors with predictable cost recovery and earnings

growth 2015E

2014

2013

2012

2011

Operating Net Income

Operating ROE

SAIFI and Customer Satisfaction Index

Operating ROE (%) and Net Income ($M)

0%

2%

4%

6%

8%

10%

0

50

100

150

200

250

300

1.2

1.0

0.9

0.8

0.8

6.8

7.2

7.7

7.6

7.7

5.0

5.5

6.0

6.5

7.0

7.5

8.0

0.0

0.4

0.8

1.2

1.6

2011

2012

2013

2014

2015E

SAIFI (2.5 Beta)

Customer Satisfaction Index

Note: 2012 ROE and Net Income normalized by excluding

one-time $112M rate credit as part of EXC-CEG merger. Operating net income represents adjusted (non-GAAP) operating earnings. Refer to slide 31 for a list of adjustments from GAAP EPS to adjusted

(non-GAAP) operating earnings |

Extending Clinton One Year |

17 2015 EEI Financial Conference We Will Continue to Operate Clinton for Another Year What has changed in 2015? • Recent upward movement in MISO capacity prices -- $150/MWd in MISO 2015 auction and Illinois Power Authority Zone 4 procurement auction

• Fleet capacity revenue uplift due to Capacity Performance of $1.4B, beyond our

expectations; MISO will now consider similar market

reforms •

EPA’s Clean Power Plan finalized. Development of

Illinois compliance program in 2016, could

facilitate significant upside from implementation •

Legislative engagement on Illinois Low Carbon Portfolio

Standard. Resolution of budget crisis should

facilitate legislative consideration in 2016 •

Improved operating efficiency and agile nuclear fuel procurement

strategy •

Over the last 2 years Clinton has deferred approximately $100M

of strategic capital, minimizing the cost of

maintaining the optionality at Clinton •

Significant potential NiHub

upside in the out-years not yet reflected in illiquid

forward markets

“If we do not see a path to sustain profitability for these

units . . . we will be forced to retire

them.” -- Chris Crane, July 31, 2014 |

18 2015 EEI Financial Conference More Progress Necessary for Clinton to Operate Beyond 2017

1)

MISO Reforms:

• MISO is committed to evaluate Zone 4 market design • Illinois Commerce Commission is holding workshops to examine

potential fixes to address Zone 4

• Reforms must provide strong revenues like the PJM reforms

effectuated

2)

Areas of Additional Progress Needed:

• Passage of Low Carbon Portfolio Standard • Illinois implementation of EPA’s Clean Power Plan must fully recognize

the value of Clinton |

Cost Management Initiative |

20 2015 EEI Financial Conference The Sustainability and Growth of Our Earnings Will be Supported by an Aggressive Cost Management Program • Exelon has launched a cost management program across to provide

sustainable improvement to the Company’s earnings

trajectory •

• Estimated EPS benefit of $0.13 to $0.18 (1,2) • An additional $50 million of nuclear fuel

savings already reflected in hedge

disclosures

• Savings to begin in 2016 and will be fully realized in 2018 (1) Based on projected 2018 share count of 965M shares, which assumes PHI merger closes

(2)

Represents adjusted (non-GAAP) operating earnings.

Refer to slide 31 for a list of adjustments from GAAP EPS to adjusted (non-GAAP) operating earnings The initiative will achieve $300-$350 million of annual cost savings at

Exelon Generation and Corporate |

Financial Data |

The Foundation for Exelon’s Growth |

23 2015 EEI Financial Conference 2015 Operating Earnings Guidance 2015 Initial Guidance $2.25 - $2.55 (1) $1.15 - $1.35 $0.45 - $0.55 $0.35 - $0.45 $0.20 - $0.30 ExGen ComEd PECO BGE 2015 Revised Guidance (Disclosed on Q3 2015 Earnings Call) $2.40 - $2.60 (1) $1.35 - $1.45 $0.45 - $0.55 $0.35 - $0.45 $0.25 - $0.35 ~($0.10) ExGen PECO ComEd BGE HoldCo (1) Earnings guidance for OpCos may not add up to consolidated EPS guidance. Represents adjusted (non-GAAP) operating earnings. Refer to slide

31 for a list of adjustments from GAAP EPS to

adjusted (non-GAAP) operating earnings

. |

24 2015 EEI Financial Conference Exelon Utilities ($M) Exelon Generation($M) (1) 2018E 3,575 2017E 3,800 2016E 3,950 2015E 3,700 Smart Grid/Smart Meter Gas Delivery Electric Transmission Electric Distribution 2016E 3,025 2015E 3,675 1,950 2017E 2018E 100 2,575 Base Nuclear Fuel Committed Growth Our Capital Plan Drives Stable Earnings Growth 475 350 300 400 400 450 825 975 650 550 2,100 2,225 2,500 2,400 175 250 1,225 1,100 925 950 1,300 1,225 1,000 900 1,150 700 650 Note: Numbers rounded to nearest $25M (1) Figures reflect cash CapEx and CENG fleet at 100%; 2014 EEI presentation showed CENG fleet at ownership; Does not include

potential pipeline of contracted generation growth

mentioned on slides 11 and 12 |

25 2015 EEI Financial Conference Exelon’s Existing Utilities Drive Stable Earnings Growth

$1,400

$1,250

$1,450

$1,350

$1,300

$1,200

$1,150

$1,100

$1,050

$1,000

$0

$1,425

2018

2017

2015

$1,250

$1,150

2016

$1,350

$1,275

$1,200

$1,000

Projected average earnings growth of ~7-9% per year from

2015-2018 $1,100

Note: Does not include PHI net income and represents

adjusted (non-GAAP) operating earnings. Refer to slide 31 for a list of adjustments from GAAP EPS to adjusted (non-GAAP) operating earnings. Does not include an extension of bonus depreciation. Impact of a 2-year bonus depreciation

extension for 2015 and 2016 would be ~($10M) in 2015 and ~($25M) a year in 2016- 2018. Excludes after-tax interest expense held at Corporate for debt associated with existing utility

investment, which is (~$25M) a year. |

26 2015 EEI Financial Conference Continued Focus on Our Balance Sheet Our strong balance sheet supports our disciplined commitment to growth

Exelon Consolidated

(1)

FFO/Debt

Exelon Consolidated FFO/Debt

S&P Threshold

(2)

Solid investment grade credit ratings are a financial

priority (1)

Metrics include PHI financing. Because of ring-fencing,

S&P deconsolidates BGE's and PHI’s financial profile from Exelon and analyzes them solely as equity investments (2) Exelon Consolidated threshold of 18% is based on the S&P Exelon Corp Summary Report published on August 5,

2015 (3)

Current senior unsecured ratings as of 11/3/2015 for Exelon,

Exelon Generation and BGE and senior secured ratings for ComEd and PECO (4) All ratings are “Stable” outlook, except for at Fitch, which has ComEd on “Positive” and Exelon on

“Ratings Watch Negative,” and Moody’s, which has ComEd on “Positive” outlook 20% 20% 20% 15% 16% 17% 18% 19% 20% 21% 2016 2017 2018 Current Ratings (3,4) ExCorp ComEd PECO BGE ExGen Recent Commentary Moody’s Baa2 A2 Aa3 A3 Baa2 “Exelon maintains a strong consolidated financial profile…which

should produce steady

ratios of cash flow to debt in the low 20% range which, when

combined with adequate liquidity reserves and a

growing focus on regulated investment opportunities, positions Exelon firmly within its current rating category.” Moody’s Issuer Comment, June 11, 2015

S&P

BBB-

A-

A-

A-

BBB

“ExGen

generates

a

significant

portion

of

earnings

from

its

retail

operations.

Through

retail

and wholesale channels, ExGen now provides nearly 5% of total

U.S. power demand, and enjoys regional diversity.

The company's generation units are well positioned to grow where capacity available for competitive supply has room to grow. We expect these incremental

revenue streams to make the consolidated Exelon somewhat more

resilient to commodity prices.” S&P

Summary Analysis; March 9, 2015 Fitch

BBB+

A-

A

A-

BBB

“The majority of capital

investment is allocated to EXC’s three utility subsidiaries, which should provide a more stable earnings base.“ Fitch Full Ratings Report; October 15, 2015

“Exgen’s

financial position has stabilized in recent years, and remains

solidly within the investment-grade category.

” Fitch Full Ratings Report; September 11, 2015 |

27 2015 EEI Financial Conference Exelon-PHI Debt Maturity Profile (1) 2023 800 2021 2022 1,425 900 2020 3,650 2019 950 25 2018 1,600 2017 2,925 25 75 2016 1,575 100 2015 PHI Regulated EXC Regulated PHI Holdco ExCorp ExGen As of 10/31/15 ($M) Debt Exchange Underway on Exelon Corp Notes due 2025, 2035 and 2045

(1)

ExCorp debt includes acquisition debt, including $1,150M

mandatory convertible units remarketing in 2017; ExGen debt includes legacy CEG debt; Excludes securitized debt and non-recourse debt

|

28 2015 EEI Financial Conference EPS Sensitivities (1) Based on September 30, 2015 market conditions and hedged position. Gas price sensitivities are based on an assumed

gas-power relationship derived from an internal model that is updated periodically. Power prices sensitivities are derived by adjusting the power price assumption while keeping all

other price inputs constant. Due to correlation of the various assumptions, the EPS impact calculated by aggregating individual sensitivities may not be equal to the EPS impact

calculated when correlations between the various assumptions are also considered. Represents adjusted (non-GAAP) operating earnings. Refer to slide 31 for a list of adjustments from

GAAP EPS to adjusted (non-GAAP) operating earnings (2) Assumes 2018/2019 auction cleared volumes (3) Share count used to calculated EPS impact assumes PHI transaction closes

2015

2016

2017

2018

Fully Open

Henry Hub Natural Gas

+$1/MMBtu

($0.00)

$0.08

$0.31

$0.46

$0.56

-$1/MMBtu

$0.01

($0.08)

($0.30)

($0.46)

($0.55)

NiHub ATC Energy Price

+$5/MWh

($0.00)

$0.07

$0.19

$0.28

$0.31

-$5/MWh

$0.00

($0.07)

($0.19)

($0.28)

($0.31)

PJM-W ATC Energy Price

+$5/MWh

($0.00)

$0.03

$0.09

$0.16

$0.19

-$5/MWh

$0.00

($0.03)

($0.09)

($0.16)

($0.19)

PJM Capacity Market

(2)

+$10/MW-day

$0.04

-$10/MW-day

($0.04)

30 Year Treasury Rate

+50 basis points

$0.02

$0.03

$0.03

-50 basis points

($0.02)

($0.03)

($0.03)

Share Count

(3)

(millions)

893

927

947

965 |

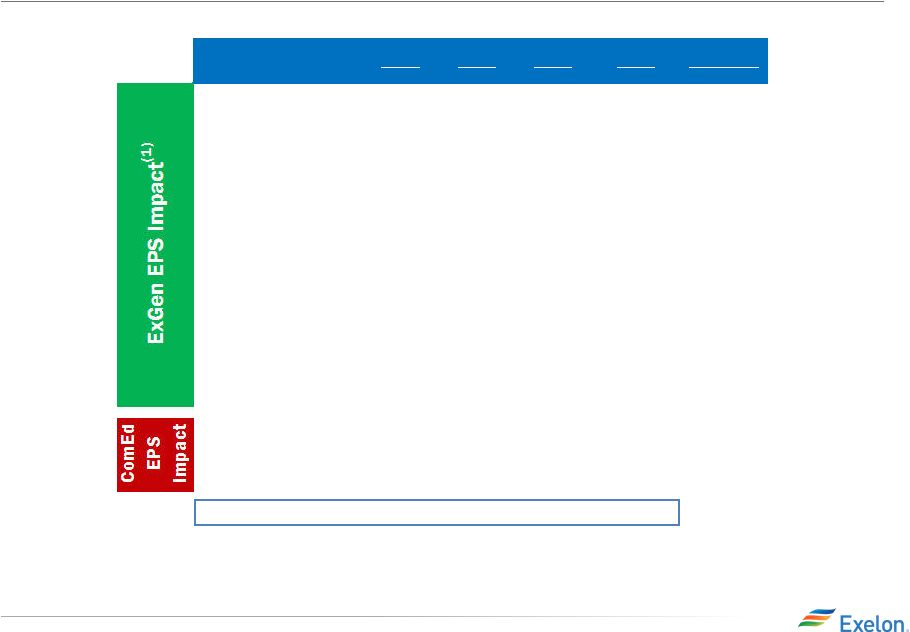

29 2015 EEI Financial Conference Modeling Combined Exelon & Pepco Holdings Pro Forma EPS

2016

2017

2018

Source of Data

Exelon

Utilities Net Income

($M)

$1,175

$1,275

$1,350

Model using midpoint of Net

Income

guidance

from slide

25

Exelon

Generation Net Income

($M)

$X,XXX

$X,XXX

$X,XXX

Model using Gross Margin disclosure

from slide 45

Corporate Net Income

($M)

($25)

($25)

($25)

Model using interest

expense

information in note on slide 25

Exelon Standalone Net Income

($M)

$X,XXX

$X,XXX

$X,XXX

Standalone Share Count

(millions)

877

881

886

Approximate share

count when PHI

equity issuance is excluded

Standalone EPS

$X.XX

$X.XX

$X.XX

Take

Exelon standalone Net Income and

divide by standalone share count

PHI Accretion

Guidance

($0.05)

$0.00

$0.10

Midpoint

of Q3 2015 guidance for PHI

accretion from slide 14

Pro

Forma EPS

$X.XX

$X.XX

$X.XX

Take Exelon

standalone Net Income and

add PHI accretion

Pro

Forma

Share Count

(millions)

927

947

965

From slide 28 |

30 2015 EEI Financial Conference • Exelon’s pension funding and investment strategies have continued to drive improvements

in the overall funded status of Exelon’s pension

plans •

Given the continued improvements in the funded status of the

Exelon Corporation Retirement Program (ECRP),

traditional defined benefit plan (87% funded at October 31, 2015), and its positive exposure to an improving rate environment; Exelon is evaluating

opportunities to optimize our pension contribution strategy

going forward •

Exelon’s standard Pension/OPEB assumptions and

sensitivities will be provided as part of Q4 2015

earnings disclosures Pension and OPEB

Update Pension Funded Status: %

Funded (1)

Pension Unfunded Status ($B)

Note: October 2015 numbers are preliminary estimates and

are subject to change $500M

(1) Assets as a % of PBO Liability

December

31,

2014

October 31, 2015

$3.4B

$2.9B

December

31,

2014

October 31, 2015

81%

84% |

31 2015 EEI Financial Conference GAAP to Operating Adjustments • Exelon’s 2015 adjusted (non-GAAP) operating earnings excludes the earnings effects of the following:

–

Mark-to-market adjustments from economic hedging

activities –

Unrealized losses from NDT fund investments to the extent not

offset by contractual accounting as described in

the notes to the consolidated financial statements

–

Certain

costs

incurred

associated

with

the

Integrys

and

pending

Pepco

Holdings,

Inc.

acquisitions

–

Mark-to-market adjustments from forward-starting

interest rate swaps related to anticipated financing for the pending PHI acquisition – Non-cash amortization of intangible assets, net, related to commodity contracts recorded at fair value at

the

date

of

acquisition

of

Integrys

in

2014

–

Non-cash benefit pursuant to the annual update of the

Generation nuclear decommissioning obligation

related to the non-regulatory units

–

Impairment of investment in long-term generating

leases –

Favorable settlement of certain income tax positions on

Constellation’s pre-acquisition tax returns

–

Generation’s non-controlling interest related to CENG

exclusion items –

Other unusual items |

32 2015 EEI Financial Conference Free Cash Flow GAAP to Non-GAAP Reconciliation 2016-2018 ExGen Free Cash Flow Calculation ($M) 2016-2018 Estimate Adjusted Cash from Operations (1) $10,250 Non-Growth Capital Expenditures ($2,975) Nuclear Fuel Capital Expenditures ($3,125) Free Cash Flow before Growth CapEx and Dividend $4,150 (1) Adjusted Cash Flow From Operations (non-GAAP) primarily includes net cash flows from operating activities and net cash

flows from investing activities excluding capital expenditures |

Exelon Utilities |

34 2015 EEI Financial Conference Operations Metric At CEG Merger (2012) Post CEG Merger (2015) BGE PECO ComEd BGE PECO ComEd Electric Operations OSHA Recordable Rate OSHA Severity Rate 2.5 Beta SAIFI (Outage Frequency) 2.5 Beta CAIDI (Outage Duration) Customer Operations Customer Satisfaction Service Level % of Calls Answered in <30 sec Abandon Rate Gas Operations Percent of Calls Responded to in <1 Hour No Gas Operations No Gas Operations

3rd Party Damages per 1000 Gas

Locates

Overall Rank

Electric Utility Panel of 24

Utilities

23

rd

2

nd

2

nd

2

nd

2

nd

2

nd

Operational Excellence Drives Value for Customers,

Communities, and Shareholders

Q1 Q2 Q3 Q4 Performance Quartiles Exelon Utilities has identified and transferred best practices at each of its utilities to

improve operating performance in areas such as:

• System Performance • Emergency Preparedness • Corrective and Preventive Maintenance |

35 2015 EEI Financial Conference 2018E 950 2017E 875 2016E 825 2015E 700 2018E 725 75 2017E 725 75 2016E 700 2015E 600 75 2018E 1,900 2017E 2,200 2016E 2,425 2015E 2,425 Exelon Utilities: Capital Plan Smart Grid/Smart Meter (1) Gas Delivery Electric Transmission Electric Distribution ($ in millions) (1)

Smart Meter/Smart Grid CapEx net of proceeds from U.S.

Department of Energy (DOE) grant; For BGE, includes CapEx from Smart Energy Savers program of ~$10M per year

125

175

175

175

175

225

225

250

575

625

375

300

100

175

225

225

200

1,450

1,475

1,625

1,475

350

400

475

475

300

350

400

475

125

200

325

400

50

25

50

25

25

25 |

36 2015 EEI Financial Conference Exelon Utilities: Rate Base (1,4) and ROE Targets 2015E Long-Term Target Equity Ratio 52% ~50-53% Earned ROE 9-10% 10% 2015E Long-Term Target Equity Ratio ~46% ~50-53% (2) Earned ROE ~8% Based on 30-yr US Treasury (3) ($ in billions) (1) ComEd, PECO and BGE rate base represents end-of-year. Numbers may not add due to rounding

(2)

Equity component for distribution rates will be the actual

capital structure adjusted for goodwill

(3)

Earned ROE will reflect the weighted average of 11.5% allowed

transmission ROE and distribution ROE resulting from 30-year Treasury plus 580 basis points for each calendar year (4) Rate base does not include extension of bonus depreciation

2015E

Long-Term Target

Equity Ratio

54%

~50-53%

Earned ROE

11-12%

10%

1.5

1.7

1.5

1.6

8.0

8.9

9.8

10.5

3.9

4.2

4.4

4.7

3.1

3.2

3.4

3.6

2.8

3.2

3.6

3.7

0.8

0.9

0.9

1.0

1.0

1.1

1.4

1.2

1.4

1.3

2018E

6.4

2017E

5.9

2016E

5.3

0.7

2015E

5.0

0.6

2018E

7.3

2017E

6.9

2016E

6.5

6.0

2015E

2018E

14.2

2017E

13.4

12.1

2016E

2015E

10.8

Gas

Transmission

Distribution |

37 2015 EEI Financial Conference BGE 2015 load growth is greater than 2014, attributed to improving economic conditions and moderate customer growth, partially offset by energy efficiency. Exelon Utilities Load 2015E 2014 PECO 2015 load growth is flat to 2014, driven by slowly improving economic conditions coupled with solid residential customer growth, offset by energy efficiency. (0.6%) 2015E 2014 Philadelphia GMP 1.8% Philadelphia Unemployment 5.2% Baltimore GMP 2.3% Baltimore Unemployment 5.5% 2015E (0.1%) 2014 Large C&I Residential Small C&I All Customers ComEd 2015 load growth is lower than 2014 (impacts of energy efficiency partially offset by slowly improving economy) with Residential and Large C&I trending downward. Chicago GMP 2.1% Chicago Unemployment 5.4% 0.0% 0.1% 0.1% 0.5% 0.2% 0.0% 0.1% (0.1%) (1.6%) (1.2%) 0.5% 1.0% (0.8%) 1.2% 0.1% (0.7%) 0.2% (0.8%) 0.3% (0.3%) (1.3%) 0.7% Notes: Data is weather normalized. Source of economic outlook data is IHS (September 2015). Assumes 2015 GDP

of 2.5% and U.S. unemployment of 5.1%. ComEd has the ROE collar as part of the distribution formula rate and BGE is decoupled which mitigates the load risk. QTD

and YTD actual data can be found in earnings release tables. BGE amounts have been adjusted for prior quarter true-ups.

|

38 2015 EEI Financial Conference ComEd April 2015 Distribution Formula Rate Docket # 15-0287 Filing Year 2014 Calendar Year Actual Costs and 2015 Projected Net Plant Additions are used to set the rates for calendar year 2016. Rates currently in effect (docket 14-0312) for calendar year 2015 were based on 2013 actual costs and 2014

projected net plant additions

Reconciliation Year

Reconciles

Revenue

Requirement

reflected

in

rates

during

2014

to

2014

Actual

Costs

Incurred.

Revenue

requirement

for

2014

is

based

on

docket

13-0318

(2012

actual

costs

and

2013

projected

net

plant

additions)

approved

in

December

2013 and reflects the impacts of PA 98-0015

(SB9) Common Equity Ratio

~ 46%

for

both

the

filing

and

reconciliation

year

ROE

9.14%

for the filing year (2014

30-yr

Treasury Yield of 3.34% + 580 basis point risk premium) and 9.09% for the reconciliation year (2014 30-yr Treasury Yield of 3.34% + 580 basis point risk premium – 5 basis points performance metrics penalty). For 2015 and 2016, the actual allowed ROE reflected in net income will ultimately be based on the

average of the 30-year Treasury Yield during the respective

years plus 580 basis point spread, absent any metric penalties Requested Rate of Return ~ 7% for both the filing and reconciliation years Rate Base (1) $8,277 million – Filing year (represents projected year-end rate base using 2014 actual plus 2015 projected capital additions). 2015 and 2016 earnings will reflect 2015 and 2016 year-end rate base

respectively. $7,082 million -

Reconciliation year (represents

year-end rate base for 2014)

Revenue Requirement

Decrease

(1)

$55M decrease ($145M decrease due to the 2014 reconciliation offset by a $90M increase related to the filing year).

The 2014 reconciliation impact on net

income was recorded in 2014 as a regulatory asset.

Timeline

• 04/15/15 Filing Date • 240 Day Proceeding • ICC order expected to be issued by December 11, 2015 The 2015 distribution formula rate filing establishes the net revenue requirement used to set the rates that will take effect in January 2016 after the Illinois Commerce Commission's (ICC’s) review. There are two components to the annual distribution formula rate

filing: •

Filing Year: Based on prior year costs (2014) and current

year (2015) projected plant additions. •

Annual Reconciliation: For the prior calendar year (2014), this

amount reconciles the revenue requirement reflected in rates during the prior year (2014) in effect to the actual costs for that year. The annual reconciliation impacts cash flow in the following year (2016) but the earnings impact has been recorded in the prior year (2014) as a regulatory asset.

Given the retroactive ratemaking provision in the Energy

Infrastructure Modernization Act legislation, ComEd net income during the year will be based on actual costs with a regulatory asset/liability recorded to reflect any under/over recovery

reflected in rates. Revenue Requirement in

rate filings impacts cash flow Note:

Disallowance of any items in the 2015 distribution formula rate filing could impact 2015 earnings in the form of a regulatory asset adjustment

(1)

Amounts represent ComEd’s position filed in surrebuttal

testimony on August 20, 2015 |

39 2015 EEI Financial Conference PECO Electric Distribution Rate Case & Proposed Settlement

Docket #

R-2015-2468981

Test Year

2016 Calendar Year

Requested

Revenue Requirement

$190M

Requested

Common Equity Ratio

(1)

53.36%

Requested Rate of Return

ROE: 10.95%; ROR:

8.19%

Proposed Rate Base

$4.1B

Proposed

Revenue

Requirement

Settlement

Increase

$127M

Authorized Returns

(2)

N/A

System Average Increase as % of overall bill

2.9%

Timeline

• 3/27/15 – PECO filed electric distribution rate case with PaPUC • 9/10/15 Settlement filed with all intervening parties

• 10/28/15 – ALJ issued Recommended Decision that settlement be approved • December 2015 – PUC Decision • Increased rates effective on January 1, 2016 The proposed Revenue Requirement increase of $127M represents 67% of the

Company’s original proposal

(1)

Reflects PECO’s expected capital structure as of

12/31/2016 (2)

Due to the “black box” nature of the settlement,

Authorized Return was not agreed upon by the parties in determining the ultimate revenue requirement increase |

40 2015 EEI Financial Conference PECO Electric LTIIP - System 2020 • PECO filed its Electric Long Term Infrastructure Improvement Plan (“LTIIP”) along with its

associated recovery mechanism the Distribution System Improvement

Charge (“DSIC”) on March 27, 2015

(with Electric Distribution Rate Case) o

LTIIP includes $275 million in incremental capital spending

from 2016-2020 focusing on the following

areas: Cable Replacement

Storm Hardening Programs

Substation replacement and upgrades

o DSIC mechanism will allow recovery of eligible LTIIP spend between rate cases if the

electric distribution ROE falls below the DSIC ROE established

by PaPUC. The current Electric DSIC ROE is

10.0%. o

Approved on 10/22/15

• PECO also proposed the concept of constructing one or more pilot microgrid projects as part of a future LTIIP update ($50-$100M). The objective is to evaluate and test emerging

microgrid

technologies that could enhance reliability and resiliency by

replacing obsolete infrastructure as an

alternative to traditional solutions. LTIIP

guarantees at least 10% ROE on capital improvements made on behalf of PECO customers |

41 2015 EEI Financial Conference PHI Capital Plan and Rate Base 675 700 725 700 350 350 350 375 275 325 325 275 2018E 1,350 2017E 1,400 2016E 1,375 2015E (2) 1,300 Pepco DPL ACE 4.0 4.4 4.8 5.1 2.4 2.5 2.7 3.0 1.7 1.9 2.2 2.1 10.2 2018E 2017E 9.6 2016E 8.8 2015E 8.1 (1) Source: PHI Third Quarter Earnings Materials 10/31/14 (2) Denotes year end rate base (3) CapEx numbers rounded to nearest $25M; totals might not add due to rounding

Capital Expenditures ($M)

(1,3)

Rate Base ($B)

(1,2) |

42 2015 EEI Financial Conference Settlement Party testimony (Oct 30) Non- settling party testimony (Nov 17) Public Interest Hearings (Dec 2-4) Initial Briefs Due

(Dec 11)

Reply Briefs

Due

(Dec 18)

Expected

PSC Order

(Q1 2016)

Pepco Holdings: DCPSC Procedural Timeline

|

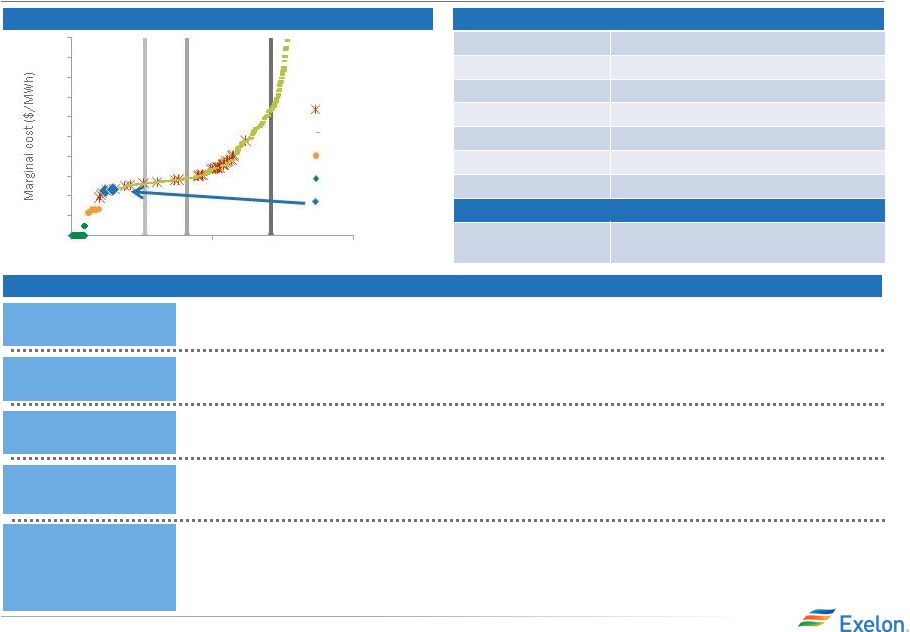

Exelon Generation |

44 2015 EEI Financial Conference 15 11 6 12 17 14 17 18 48 75 25 97 Our Generation to Load Strategy Delivers Sustainable Earnings

in Volatile Markets

• Since the Constellation merger, we have improved our generation to load match through growing our customer load business,

both organically and through disciplined

acquisitions like Integrys •

This strategy and hedging with a fundamentals driven approach

has meaningfully benefitted earnings over the last two years

• High volatility: We captured higher prices for our generation during periods of extreme weather while managing our load obligations. During periods of high volatility, generation availability is of utmost importance. During the polar vortex of 2014, our 2

GW of peaking capability created

significant

value

in

the

energy

and

ancillary

markets.

During

the

polar

vortex,

we

made

~$100

million

(3)

• Low volatility: During periods of low volatility, we captured higher margins as we realized a lower cost to serve our customers

and we optimized the value of our dispatchable fleet through load sales. This year alone, we have made ~$250 million as result of lower cost to serve load • Generation to Load match also provides us with an important channel to market for our hedging activities which is

important in times of low liquidity and in places

where there is not an active market (1)

Owned

and

contracted

generation

capacity

converted

from

MW

to

MWh

assuming

100%

capacity

factor

(CF)

for

all

technology

types,

except

for

renewable

capacity

which

is

shown

at

estimated

CF

(2)

Expected generation and load shown in the chart above will not

tie out with load volume and ExGen disclosures; Load shown above does not include indexed products and generation reflects a net owned and contracted position; Estimates as of 9/30/2015 (3) Excludes the impact of plant outages, primarily at Calvert Cliffs prior to us operating the plant

2012 Generation Load Match (TWh)

(1,2)

116

118

Midwest

14

New England

Canada

South/West/

26

New York

43

Mid-Atlantic

30

ERCOT

Intermediate

Baseload

Peaking

Renewables

Expected Generation

Expected Load

Generation Capacity:

8

14

8

9

20

13

13

17

64

63

38

97

38

95

18

10

111

25

2016 Generation Load Match (TWh)

(1,2)

Midwest

New England

Canada

South/West/

New York

Mid-Atlantic

ERCOT |

45 2015 EEI Financial Conference Exelon Generation – Optimizing the Portfolio and Positioning it for Market Upside (1) Gross margin categories rounded to nearest $50M (2) Total Gross Margin (Non-GAAP) is defined as operating revenues less purchased power and fuel

expense, excluding revenue related to decommissioning, gross

receipts tax, Exelon Nuclear Partners, operating

services agreement with Fort Calhoun and variable interest entities. Total Gross Margin is also net of direct cost of sales for certain Constellation businesses

(3)

Excludes EDF’s equity ownership share of the CENG Joint

Venture (4)

Mark-to-Market of Hedges assumes mid-point of hedge

percentages •

Capacity Performance added approximately $1B in gross margin over the 2016 to 2018 period • Timing of hedge decisions creates value • Positioning portfolio to reflect our fundamental views – currently carrying a larger open position in 2017 and 2018 • Intra-year hedging flexibility to take advantage of volatility

• Using cross-commodity spreads in NiHub: 7-10% of the portfolio in 2017 is in

cross-commodity hedges and

3-6% in 2018 Gross Margin Category ($M) (1) 2015 2016 2017 2018 Open Gross Margin(including South, West, & Canada hedged

GM)

(3)

$5,150

$5,650

$5,800

$6,100

Mark-to-Market of Hedges

(3,4)

$2,200

$1,200

$750

$250

Power New Business / To Go

$50

$500

$800

$1,000

Non-Power Margins Executed

$400

$200

$100

$50

Non-Power New Business / To Go

$50

$250

$350

$450

Total Gross Margin

(2)

$7,850

$7,800

$7,800

$7,850 |

46 2015 EEI Financial Conference Electric Load Serving Business: Market Landscape Total U.S. Power Market 2015 (3,725 TWh load) (1)

Eligible Non-

Switched

Eligible

Switched

Muni/Co-Op Market

Other

Ineligible

Constellation Active Retail Electric Markets

Improved competitive landscape observed across many

markets •

Conditions have improved in many markets as impacts of the

Polar Vortex have played out

• Some suppliers have taken steps to reduce exposure to weather-

sensitive customer loads following the Polar

Vortex Retail transactions and new entrant

activity down in 2015 •

M&A, exits and divestiture activity down from 2014

levels •

Fewer new entrants have entered the market in 2015

Competitive retail market expected to grow modestly over the

next five years (2015-2019)

• C&I switched market to grow by about 8% • Residential switched market to grow by about 7% Market Landscape (1) (1) Sources are EIA, DNV GL, and internal estimates Existing suppliers continue to expand market footprint and

product portfolio

• Several existing suppliers have expanded into new states

• Energy efficiency and distributed energy among most popular for

cross-selling opportunities

Constellation is the #1 Provider of Retail Electricity in the

United States |

47 2015 EEI Financial Conference Our Electric Load Serving Business Provides Sustainable Earnings and Stable Earnings Growth 70-80% 20-30% 2016E 165 70-80% 20-30% 2015E 165 60-70% 30-40% 2017E 165 2018E 210 75-85% 15-25% 2017E 70-80% 20-30% 2015E 195 65-75% 25-35% 210 75-85% 15-25% 2016E 210 Retail Load (2) Total Contracted Wholesale Load 2015 EEI Commercial Load Projections (1) 2015 – 2018 TWh 2014 EEI Commercial Load Projections (1,3) 2015 – 2017 TWh (1) Numbers and percentages are rounded to the nearest 5 (2) Index load expected to be 25% to 35% of total forecasted retail load

(3)

Excludes Integrys

acquisition completed in November 2014

Our growing load business provides a channel to market

that reduces the reliance on lower margin over-

the-counter products

0

20

40

60

80

100

120

140

160

180

200

220

0

20

40

60

80

100

120

140

160

180

200

220 |

48 2015 EEI Financial Conference Our NiHub Strategy Recognizes the Lack of Liquidity and Disconnect Between our Fundamental View of Prices Incremental coal retirements will lead to continued volatility and higher dispatch costs, creating

$2-$3/MWh of power price

upside in NiHub

in 2017-2018

Forward market heat rates expanded again through

2015 •

Our portfolio is positioned to take advantage of

expected volatility and power price upside

• 2017-2018 average upside of $2-$3/MWh • Power exposure in NiHub above purely ratable: • 17-20% behind ratable in 2017 • 13-15% behind ratable in 2018 • The increased reliance on natural gas as coal plants retire

has impacted prices

• Our PJM forecast includes 20+GW of new CCGTs, full compliance with state renewables requirements and essentially flat load growth, in addition to coal retirements

0 5 10 15 20 25 30 35 2012-2014 2015 2016 PJM/MISO Coal Retirements PJM & MISO Annual Coal Retirements PJM & MISO Cumulative Coal Retirements 26 27 28 29 30 31 32 2017 2018 Nihub ATC Prices ($/MWh) Nihub Forecast (09/30) Nihub Market (09/30) 8.0 8.5 9.0 9.5 10.0 10.5 11.0 2016_NiHub_HR 2017_NiHub_HR 2018_NiHub_HR |

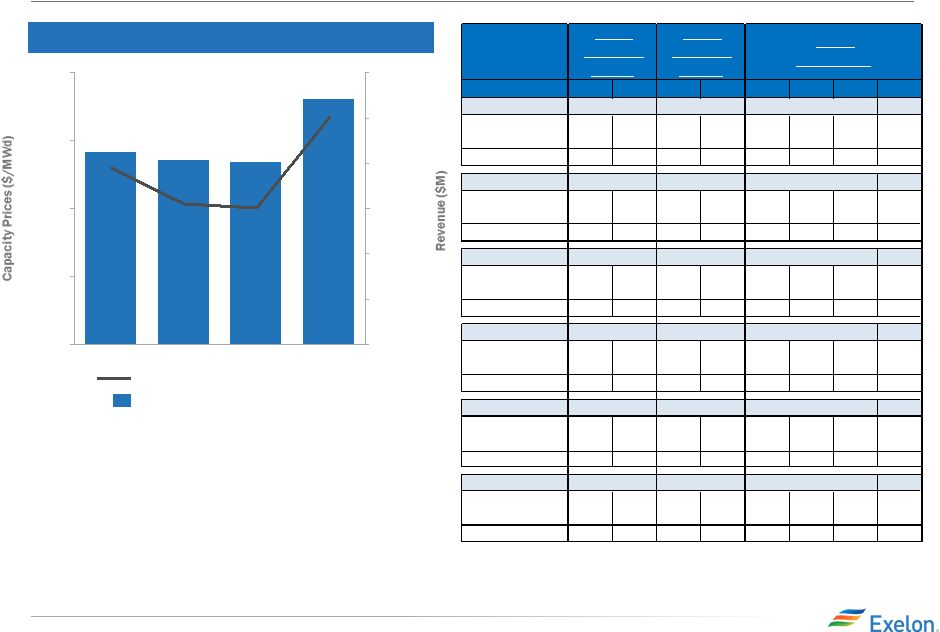

49 2015 EEI Financial Conference Capacity Markets: PJM $142 $136 $135 $181 $1,400 $1,300 $1,200 $1,100 $1,000 $900 $800 $200 $150 $100 $50 $0 2018 2017 2016 2015 Exelon Fleet Weighted Price ($/MWd) Revenue ($M) PJM Capacity Revenues (1,2,3) (1) Revenues reflect capacity cleared in Base, CP transitional & incremental auctions and are for calendar

years (2) Revenues reflect owned and contracted

generation (3) Reflects 50.01% ownership at

CENG (4) Volumes at ownership.

Rounded. Cleared Volumes

(MWs)

(4)

CP

Price

CP

Price

CP

Price

Base

Price

ComEd

Fossil/Other

-

$134.00

-

$151.50

-

$215.00

25

$200.21

Nuclear

9,950

$134.00

9,975

$151.50

8,625

$215.00

-

$200.21

Total

9,950

$134.00

9,975

$151.50

8,625

$215.00

25

$200.21

EMAAC

Fossil/Other

25

$134.00

850

$151.50

2,075

$225.42

1,050

$210.63

Nuclear

3,950

$134.00

4,950

$151.50

4,325

$225.42

-

$210.63

Total

3,975

$134.00

5,800

$151.50

6,400

$225.42

1,050

$210.63

SWMAAC

Fossil/Other

-

$134.00

-

$151.50

-

$164.77

-

$149.98

Nuclear

425

$134.00

825

$151.50

850

$164.77

-

$149.98

Total

425

$134.00

825

$151.50

850

$164.77

-

$149.98

BGE

Fossil/Other

75

$134.00

150

$151.50

300

$164.77

425

$149.98

Nuclear

-

$134.00

-

$151.50

-

$164.77

-

$149.98

Total

75

$134.00

150

$151.50

300

$164.77

425

$149.98

Rest of MAAC/RTO

Fossil/Other

-

$134.00

-

$151.50

265

$164.77

50

$149.98

Nuclear

775

$134.00

800

$151.50

-

$164.77

-

$149.98

Total

775

$134.00

800

$151.50

265

$164.77

50

$149.98

GRAND TOTAL

Fossil/Other

100

1,000

2,640

1,550

Nuclear

15,100

16,550

13,800

-

Total

15,200

17,550

16,440

1,550

16/17

Transition

Auction

17/18

Transition

Auction

18/19

Base Auction |

50 2015 EEI Financial Conference Capacity Markets: ISO-NE, NYISO, MISO (1) ISO-NE: ISO New England; NEMA: Northeastern Massachusetts and Boston; SEMA: Southeastern Massachusetts

(2)

NYISO: New York Independent System Operator

(3)

Represents offered capacity at ownership

(4)

AMIL: Ameren Illinois AMIL capacity price represents PRA auction

clearing price for Zone 4 in $/MWd

2015/2016

2016/2017

2017/2018

2018/2019

ISO-NE

(1)

NEMA

Capacity

(3)

(MW)

2,100

2,100

2,100

2,100

Price ($/MWd)

$104

$222

$500

$318

SEMA

Capacity

(3)

(MW)

35

35

35

230

Price ($/MWd)

$104

$105

$234

$557

NYISO

(2)

Capacity

(3)

(MW)

1,100

1,100

1,100

1,100

MISO

Zone 4

Capacity

(3)

(MW)

1,100

1,100

1,100

1,100

Price ($/MWd)

(4)

$150 |

51 2015 EEI Financial Conference Natural Gas Marketing Platform Active Natural Gas Markets Supply ~4-6 Bcf per day delivered in competitive markets growing to 6-8 Bcf by 2018 Transportation Active shipper on more than 45 interstate pipelines on a daily basis

Trading

Active

participant

in

all

major

supply

basins,

markets,

and

trading

points

in

North

America

Volume Management

Schedule, nominate and balance behind more than 120

LDCs Gas Generation

Gas Toll

Owned gas storage

contracts

Major office locations |

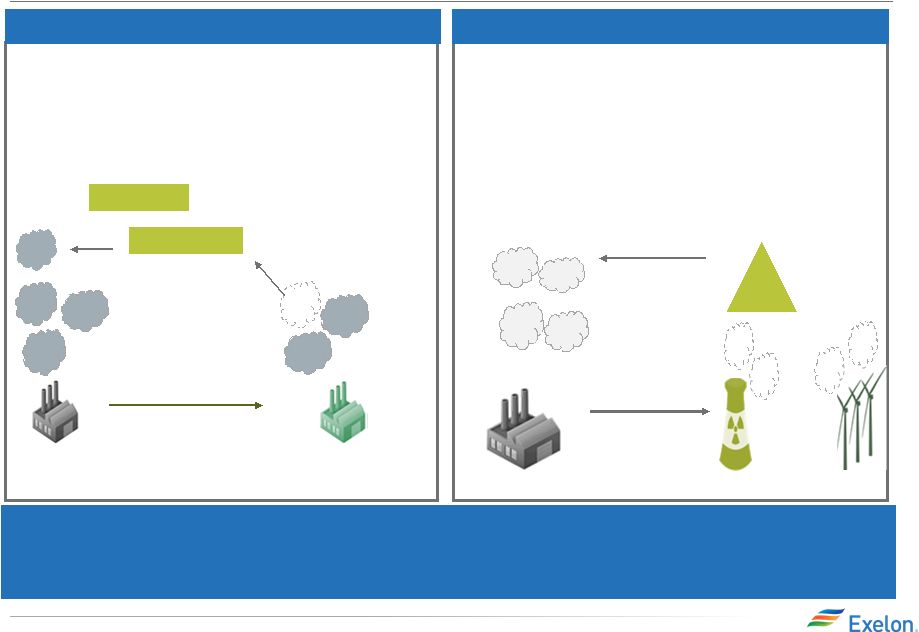

52 2015 EEI Financial Conference • States distribute allowances equal to the number of CO2 emissions allowed • At the end of each compliance period, affected electric generating units (EGUs) must surrender allowances equal to

their emissions

• States may allow affected EGUs to buy or sell allowances

with other parties

One

=

one

ton

of

CO2

emissions

allowance

allowance

State Mass Goal

$

A facility that produces more

emissions than it has allowances may

purchase allowances from another

facility that has extra allowances

State Rate Standard: 1,000 lb/MWh

Rate

Standard

$

ERC

Rate

Standard

or

Emissions Rate: 0 lb/MWh

Emissions Rate: 2,000 lb/MWh

• Emission rate credits (ERCs) are created when incremental

nuclear or incremental renewables generate

electricity •

Emitting generators must purchase sufficient ERCs to

reduce their emission rate to the target level

EPA Clean Power Plan: Compliance

Pathways Mass Budget

Emissions Rate

Exelon recommends that states adopt mass-based plans that

include both existing and new units because that is

the best way to level the playing field and ensure that clean

resources like nuclear receive value for the carbon- free, always-on electricity that Exelon provides. It is also the best way to minimize overall costs to consumers

and preserve electric reliability while achieving

verifiable carbon reductions |

53 2015 EEI Financial Conference Exelon Nuclear Fleet Overview (including CENG and Salem) Plant Location Type/ Containment Net Generation Capacity (MW) (5) License Extension Status / License Expiration (1) Ownership Spent Fuel Storage/ Date to lose full core discharge capacity (2) Braidwood, IL (Units 1 and 2) PWR Concrete/Steel Lined 2,389 Filed application in May 2013 (decision expected in early 2016)/ 2026, 2027 100% Dry Cask Byron, IL (Units 1 and 2) PWR Concrete/Steel Lined 2,347 Filed application in May 2013 (decision expected in 2015)/ 2024, 2026 100% Dry Cask Clinton, IL (Unit 1) BWR Concrete/Steel Lined / Mark III 1,069 2026 100% Dry Cask (2016) Dresden, IL (Units 2 and 3) BWR Steel Vessel / Mark I 1,845 Renewed / 2029, 2031 100% Dry Cask LaSalle, IL (Units 1 and 2) BWR Concrete/Steel Lined / Mark II 2,320 Filed application December 2014 (decision expected 2017)/2022, 2023 100% Dry Cask Quad Cities, IL (Units 1 and 2) BWR Steel Vessel / Mark I 1,403 Renewed / 2032 75% Exelon, 25% Mid- American Holdings Dry Cask Limerick, PA (Units 1 and 2) BWR Concrete/Steel Lined / Mark II 2,317 Renewed / 2044, 2049 100% Dry Cask Oyster Creek, NJ (Unit 1) BWR Steel Vessel / Mark I 625 Renewed / 2029(3) 100% Dry Cask Peach Bottom, PA (Units 2 and 3) BWR Steel Vessel / Mark I 1,221 Renewed / 2033, 2034 50% Exelon, 50% PSEG Dry Cask TMI, PA (Unit 1) PWR Concrete/Steel Lined 837 Renewed / 2034 100% 2023 Salem, NJ (Units 1 and 2) PWR Concrete/Steel Lined 1,005 Renewed / 2036, 2040 42.6% Exelon, 57.4% PSEG Dry Cask Calvert Cliffs, MD (Units 1and 2) PWR Concrete/Steel Lined 878 Renewed / 2034, 2036 100% CENG(4) Dry Cask R.E. Ginna, NY (Unit 1) PWR Concrete/Steel Lined 288 Renewed / 2029 100% CENG(4) Dry Cask Nine Mile Point, NY (Units 1 and 2) BWR Steel Vessel / Mark I Concrete/Steel Vessel/ Mark II 838 Renewed / 2029, 2046 100% CENG (4) / 82% CENG (4) , 18% Long Island Power Authority Dry Cask (1) Operating license renewal process takes approximately 4-5 years from commencement until completion of NRC review (2) The date for loss of full core reserve identifies when the on-site storage pool will no longer have sufficient space to

receive a full complement of fuel from the reactor core; Dry cask storage will be in operation at those sites prior to losing full core discharge capacity in their on-site storage pools (3) On December 8, 2010, Exelon announced that it will permanently cease generation operations at Oyster Creek by December 31,

2019; Oyster Creek’s current NRC license expires in 2029 (4) Exelon Generation has a 50.01% ownership interest in CENG. EDF has a 49.99% ownership interest in CENG. (5) Net generation capacity is stated at proportionate ownership share. Based on 2015 projected full year |

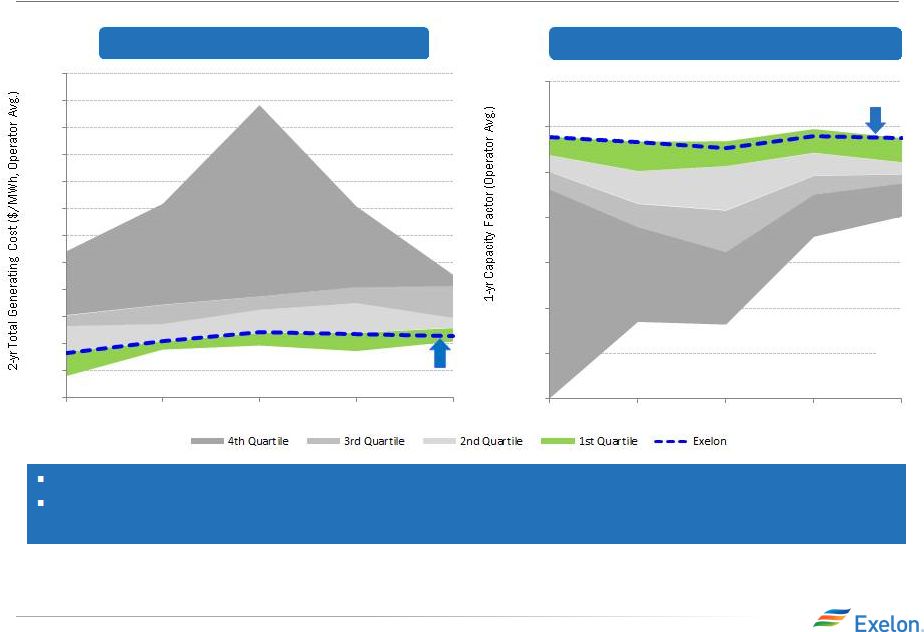

54 2015 EEI Financial Conference World Class Nuclear Operator (1) 31% 14% 1,208 1,169 1,104 Nuclear Total Generating Cost ($/MWh) (2) Capacity Factor (%) (3) Exelon is consistently one of the lowest-cost and most efficient producers of electricity in the nation

Over the next five years, Exelon Nuclear projects a negative

cost CAGR, while maintaining strong generation

performance $31.37

2014 Exelon Exelon 20 25 30 35 40 45 50 55 60 65 70 75 80 2010 2011 2012 2013 2014 65% 70% 75% 80% 85% 90% 95% 100% 2010 2011 2012 2013 2014 (1) 2010 – 2013 Exelon fleet averages exclude Salem, Ft. Calhoun, and CENG; 2014 Exelon fleet averages exclude Salem and

Ft. Calhoun (2) Total Generating Cost is defined as cost to produce one MWh of energy, including fuel, materials, labor, contracting,

capital expenditures, insurance and the majority of

overhead expenses including benefit costs associated with labor

but excludes property taxes, unit contingent costs and risks, costs due to unknown future regulatory changes, and suspended DOE nuclear waste storage fee (effective May 2014) (3) Source: Platts Nuclear News, Nuclear Energy Institute and Energy Information Administration (Department of Energy)

|

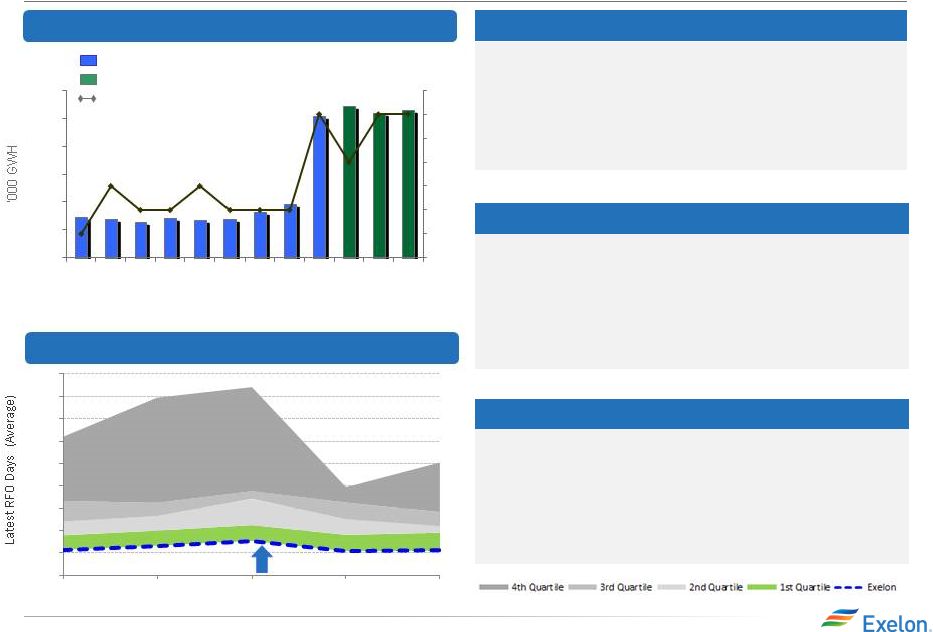

55 2015 EEI Financial Conference Net nuclear generation data at ownership excluding Salem for all years

CENG excluded in years 2007–2014 but included in 2015 and

beyond 2016 and 2018 include Clinton Refueling Only

outage of shortened duration Nuclear Output and

Refueling Outages Fleet Average Refueling Outage

Duration (Days) 31%

36%

14%

14%

Nuclear Output

1,208

1,169

1,104

Nuclear Refueling Cycle

• All Exelon-owned units are on a 24 month cycle except for Braidwood U1/U2, Byron U1/U2, Ginna, and Salem U1/U2, which are on 18 month cycles • Starting in 2015 Clinton is on annual cycles Actual / Forecast Target # of Refueling Outages 2015 Refueling Outage Impact • 14 planned refueling outages, including 1 at Salem • 7 spring refueling outages and 6 fall refueling outages • 1 Salem fall refueling outage 2016 Refueling Outage Impact • 12 planned refueling outages, including 1 at Salem • 7 spring refueling outages and 4 fall refueling outages • 1 Salem spring refueling outage 2010-2013 Exelon fleet averages exclude Salem and CENG. 2014 Exelon fleet average excludes Salem

7 8 9 10 11 12 13 14 125 130 135 140 145 150 155 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 15 25 35 45 55 65 75 85 95 105 2010 2011 2012 2013 2014 Exelon |

56 2015 EEI Financial Conference Nuclear Fuel Costs (1) Projected Exelon Uranium Demand (2) Components of Fuel Expense in 2015 2015 – 2020: 100% hedged in volume 2 1 0 11 10 9 8 7 6 5 4 3 2020E 2019E 2018E 2017E 2016E 2015E Enrichment 32% Tax/Interest 2% Conversion 4% Uranium 46% Fabrication 16% Projected Exelon Average Uranium Cost vs. Mar Projected Total Nuclear Fuel Spend (3) 0 200 400 600 800 1,000 1,200 2020E 887 2019E 949 2018E 953 2017E 964 2016E 975 2015E 971 Nuclear Fuel Capex Nuclear Fuel Expense (Amortization) Over the last year, Exelon has reduced capital requirements for nuclear fuel by ~$265M (2015 to 2019)

(1)

All charts exclude Salem (2)

Includes 100% of requirements (3)

CENG included at ownership. Including Salem and 100% of CENG

total cash capital expenditures are $1.3B, $1.2B, $1.0B, $0.9B, $0.9B, and $0.9B for 2015 - 2020

|

57 2015 EEI Financial Conference Constellation Energy Nuclear Group (CENG) Operating Service

Agreement Terms

• Nuclear Operating services agreement • Integrated CENG and their 3 plants into Exelon Nuclear with transfer of operating licenses

• Loan to CENG and distributions to EDF/Exelon Generation • CENG $400M special distribution paid to EDF on April 1, 2014

• Exelon Generation made $400M loan to CENG at 5.25% annual interest rate to fund special distribution to

EDF (As of September 30, 2015, the loan balance, including

interest, was $296M) •

Exelon Generation receives priority payment from CENG’s

available cash flows until loan is fully repaid •

Exelon Generation also entitled to receive aggregate preferred

distributions of $400M plus a return of 8.5% per

annum from April 1, 2014 (No amounts have been paid on this special distribution) • Option for EDF to sell its 49.99% interest in CENG to Exelon Generation

• Exercisable from January 2016 to June 2022 • Process and timeline allows for possible negotiated agreement on price

• If no negotiated agreement on price, price is determined by arbitration process to determine fair market

value

• Arbitration process could take up to 10 months or longer before binding decision is made on price

• Price would be adjusted for EDF share of remaining loan balance and special distribution to Exelon

Generation

• Regulatory approvals could take several months but might run concurrently with arbitration process

• Exelon has limited rights to defer closing up to 6 months |

58 2015 EEI Financial Conference Exelon Fossil Generation Fleet Overview (1) 100%, unless otherwise indicated (2) Fossil/Hydro Capacity values shown represent summer ratings as of September 2015. Net Generation Capacity (MW) is

stated at proportionate ownership share

(3)

Includes Perryman 2 (51MW), which will retire on in Q1

2016. Includes Perryman 6 (110MW) that went COD in June 2015 (4) Includes Riverside 4 (74MW), which is scheduled for retirement in May 2016

Station

Location

Number

of

Units

Primary Fuel

Type

Percent

Owned

(1)

Net Generation

Capacity (MW)

(2)

Notch Cliff

Baltimore, MD

8

Gas

118

Pennsbury

Morrisville, PA

2

Landfill Gas

6

Perryman

(3)

Belcamp, MD

6

Oil/Gas

463

Philadelphia Road

Baltimore, MD

4

Oil

61

Richmond

Philadelphia, PA

2

Oil

98

Riverside

(4)

Baltimore, MD

3

Oil/Gas

113

Salem

Lower Alloways

Creek Twp, NJ

1

Oil

42.59

16

Schuylkill

Philadelphia, PA

2

Oil

30

Southwark

Philadelphia, PA

4

Oil

52

Westport

Baltimore, MD

1

Gas

116

Southeast Chicago

Chicago, IL

8

Gas

296

Framingham

Framingham, MA

3

Oil

33

Medway

West Medway, MA

3

Oil/Gas

117

Mystic 7

Charlestown, MA

1

Oil/Gas

575

Mystic 8, 9

Charlestown, MA

2

Gas

1418

Mystic Jet

Charlestown, MA

1

Oil

9

New Boston

South Boston, MA

1

Oil

16

Wyman

Yarmouth, ME

1

Oil

5.9

36

Grand Prairie

Alberta, Canada

1

Gas

75

Hillabee

Alexander City, AL

1

Gas

722

Sunnyside

Sunnyside, UT

1

Waste Coal

50

26

Station

Location

Number

of

Units

Primary Fuel

Type

Percent

Owned

(1)

Net Generation

Capacity (MW)

(2)

Colorado Bend

Wharton, TX

6

Gas

498

Handley 3

Fort Worth, TX

1

Gas

395

Handley 4, 5

Fort Worth, TX

2

Gas

870

LaPorte

Laporte, TX

4

Gas

152

Mountain Creek 6, 7

Dallas, TX

2

Gas

240

Mountain Creek 8

Dallas, TX

1

Gas

565

Wolf Hollow 1, 2, 3

Granbury, TX

3

Gas

704

Chester

Chester, PA

3

Oil

39

Conowingo

Darlington, MD

11

Hydro

572

Croydon

West Bristol, PA

8

Oil

391

Delaware

Philadelphia, PA

4

Oil

56

Eddystone

Eddystone, PA

4

Oil

60

Eddystone

3, 4

Eddystone, PA

2

Oil/Gas

760

Fairless Hills

Fairless Hills, PA

2

Landfill Gas

60

Falls

Morrisville, PA

3

Oil

51

Gould Street

Baltimore, MD

1

Gas

97

Handsome Lake

Kennerdell, PA

5

Gas

268

Moser

Lower

PottsgroveTwp., PA

3

Oil

51

Muddy Run

Drumore, PA

8

Hydro

1070 |

59 2015 EEI Financial Conference Summer Texas Heat Brings Return of Volatility to ERCOT Demand is Growing • Summer 2015 was hot; record load pushed summer 2015 spot power prices up and led summer forwards higher • Average demand in ERCOT has risen 2-3% in 2015 from 2014 • Reserve margins reserve were as much as 10% lower than projected, falling below 4 GW in August Exelon captured ~$20M of value from this summer’s volatility and our new CCGTs will

be well positioned to replicate this success

Generation assets will be valuable going forward

• Wind generation is forecasted to grow from 13 GW today to nearly 20 GW by 2020, which will increase volatility of the ERCOT dispatch stack • New gas generation development has slowed – with 600MW of peakers in 2016 and Exelon CCGTs in 2017 the only visible gas additions through 2018 • The Public Utilities Commission of Texas has requested that ERCOT examine the Operating Reserve Demand Curve ERCOT Weather: July-September ERCOT Scarcity Indicators: July-September |

60 2015 EEI Financial Conference Texas CCGTs: Unique Opportunity to Grow in ERCOT Key Facts Sites Wharton County and Granbury, TX Total Capacity ~2,200MW Construction Cost $1,475M (~$700/kW); $700M remaining Heat Rate ~6,500 mmBtu/MWh EPC / OEMs Zachry / GE and Alstom Cooling System Air Cooled Commercial Operation By Summer 2017 Expected Economics ROE > 12% ERCOT Dispatch Key Messages • Two of the cleanest, most efficient Combined Cycle Gas Turbines (CCGT) in the nation

• Simplified design provides for easier construction and maintenance, making these units among the most

predictable and least costly to operate and maintain in the

industry •

Plants use air cooling which mitigates water constraint

issues •

Ramp rate of 100 MW/minute can respond quickly to depressed

wind or unexpected outages (market ramp rate ~50

MW/minute) •

Capacity factor will average 75-85%

• Demand continues to grow at more than 1% per year, which results in the need for roughly 700MW of

incremental capacity every year and potential for real-time

prices to go to $9,000/MWh •

New units should see sustainably high spark spreads and

returns, especially if natural gas prices recover •

Potential for coal units in the state to add costly controls or

shutdown could further boost returns as the

Mercury & Air Toxics (MATS) and Regional Haze rules take

effect Efficient

Cost Effective

Environmental

Versatile

Constructive

Market

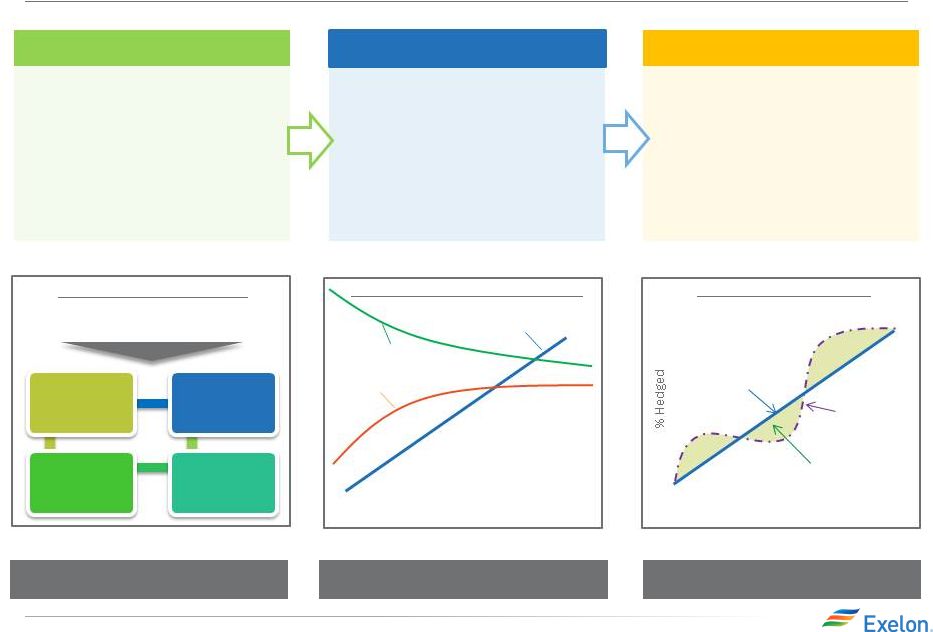

0

10

20

30

40

50

60

70

80

90

100

0

50,000

100,000

Capacity at peak (MW)

Coal

Gas

Uranium

Renewables

Exelon New Build |

61 2015 EEI Financial Conference Exelon Renewable Generation Fleet Overview Station Location Number of Units Primary Fuel Type Percent Owned (1) Net Generation Capacity (MW) (2) AgriWind Bureau Co., IL 4 Wind 99 8 Beebe 1A & 1B Gratiot, MI 55 Wind 131 Blue Breezes/Moore Blue Earth, MN 2 Wind 3 Cisco Jackson Co., MN 4 Wind 99 8 Cowell Pipestone Co., MN 1 Wind 99 2 CP Windfarm Faribault Co., MN 2 Wind 4 Ewington Jackson Co., MN 10 Wind 99 21 EXC City Solar Cook Co., IL 1 Solar 8 Harvest I & II Huron Co., MI 65 Wind 112 Marshall Lyon Co., MN 9 Wind 99 19 Michigan Wind I Bingham Township, MI 46 Wind 69 Michigan Wind II Minden City, MI 50 Wind 90 Norgaard Lincoln Co., MN 7 Wind 99 9 Wolf Nobles Co., MN 5 Wind 99 6 Bluegrass Ridge Gentry Co., MO 27 Wind 57 Conception Nodaway Co., MO 24 Wind 50 Cow Branch Atchinson Co., MO 24 Wind 50 Greensburg Kiowa Co., KS 10 Wind 13 Loess Hills Atchinson Co., MO 4 Wind 5 Shooting Star Kiowa Co., KS 65 Wind 104 Station Location Number of Units Primary Fuel Type Percent Owned (1) Net Generation Capacity (MW) (2) EXC Wind 1,2,3,4 Hansford Co., TX 62 Wind 110 EXC Wind 5,6 Sherman Co., TX 16 Wind 20 EXC Wind 7,8,9,10,11 Moore Co., TX 40 Wind 50 High Plains Moore Co., TX 8 Wind 99.5 10 Whitetail Webb, TX 57 Wind 91 Conowingo Hartfort Co., MD 11 Hydroelectric 572 Criterion Oakland, MD 28 Wind 70 Fairless Falls Twp, PA 2 Landfill Gas 60 Fourmile Garrett Co., MD 16 Wind 40 Muddy Run Lancaster Co., PA 8 Hydro 1,070 Pennsbury Falls Twp, PA 2 Landfill Gas 6 Antelope Valley Solar Ranch LA Country., CA 1 Solar 242 Cassia Twin Falls Co., ID 14 Wind 29 Echo I Umatilla Co., OR 21 Wind 99 35 Echo II Morrow Co., OR 10 Wind 20 Echo III Morrow Co., OR 6 Wind 99 10 High Mesa Twin Fall Co., ID 19 Wind 40 Mountain Home Elsmore Co., ID 20 Wind 42 Threemile Canyon Morrow Co., OR 6 Wind 10 Tuana Springs Twin Fall Co., ID 8 Wind 17 Wildcat Lea, NM 13 Wind 27 (1) 100%, unless otherwise indicated (2) Fossil/Hydro Capacity values shown represent summer ratings as of September 2015. Net Generation Capacity (MW) is

stated at proportionate ownership share

(3)

Constellation Solar is an operation that constructs, owns, and

operates solar facilities at various customer locations. |

62 2015 EEI Financial Conference Exelon Generation Disclosures September 30, 2015 |

63 2015 EEI Financial Conference Portfolio Management Strategy Protect Balance Sheet Ensure Earnings Stability Create Value Strategic Policy Alignment •Aligns hedging program with financial policies and financial outlook •Establish minimum hedge targets to meet financial objectives of the company (dividend, credit rating) •Hedge enough commodity risk to meet future cash requirements under a stress scenario Three-Year Ratable Hedging •Ensure stability in near-term cash flows and earnings •Disciplined approach to hedging •Tenor aligns with customer preferences and market liquidity •Multiple channels to market that allow us to maximize margins •Large open position in outer years to benefit from price upside Bull / Bear Program •Ability to exercise fundamental market views to create value within the ratable framework •Modified timing of hedges versus purely ratable •Cross-commodity hedging (heat rate positions, options, etc.) •Delivery locations, regional and zonal spread relationships Exercising Market Views Purely ratable Actual hedge % Market views on timing, product allocation and regional spreads reflected in actual hedge % High End of Profit Low End of Profit % Hedged Open Generation with LT Contracts Portfolio Management & Optimization Portfolio Management Over Time Align Hedging & Financials Establishing Minimum Hedge Targets Credit Rating Credit Rating Capital & Operating Expenditure Capital & Operating Expenditure Dividend Dividend Capital Structure Capital Structure |