Form 6-K CREDIT SUISSE GROUP AG For: Oct 22

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

Form 6-K

______________

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

October 22, 2015

Commission File Number 001-15244

CREDIT SUISSE GROUP AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

______________

Commission File Number 001-33434

CREDIT SUISSE AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

______________

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

|

Form 20-F ☒

|

Form 40-F ☐

|

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

This report on Form 6-K of Credit Suisse Group AG and Credit Suisse AG hereby incorporates by reference into the Registration Statement on Form F-3 (file no. 333-202913) and the Registration Statement on Form S-8 (file no. 333-101259) the following slides of the presentation “Overview of Financials and Capital” by David Mathers: Slide no. 10, Slide no. 32, Slide no. 38, Slide no. 42 and Slide no. 43.

October 22, 2015 Credit Suisse Strategy and ObjectivesTidjane Thiam

Disclaimer The 3Q15 financial information is subject to further review We have not finalized our 3Q15 Financial Report and our independent registered public accounting firm has not completed its review of the condensed consolidated financial statements (unaudited) for the period. Accordingly, the 3Q15 financial information contained in this presentation is subject to completion of quarter-end procedures, which may result in changes to that information. Certain reclassifications have been made to prior periods to conform to the current presentation.The re-segmented financial information is preliminary and subject to further review Unless otherwise noted, this presentation contains certain historical financial information that has been re-segmented to approximate what our results under our new structure would have been, had it been in place from January 1, 2014. Such information is preliminary in nature and subject to review, evaluation and refinement, has not been audited or reviewed by our independent public accountants and can be expected to change in certain respects before any final re-segmentation is published. In addition, “Illustrative”, “Ambition” and “Goal” presentations are not intended to be viewed as targets or projections, nor are they considered to be Key Performance Indicators. All such presentations are subject to a large number of inherent risks, assumptions and uncertainties, many of which are completely outside of our control. Accordingly, this information should not be relied on for any purpose. We may not achieve the benefits of our strategic initiatives We may not achieve all of the expected benefits of our strategic initiatives. Factors beyond our control, including but not limited to the market and economic conditions, changes in laws, rules or regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives. Cautionary statement regarding forward -looking statements This presentation contains forward-looking statements that involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements. A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in "Risk Factors” in our Annual Report on Form 20-F for the fiscal year ended December 31, 2014 and in “Cautionary statement regarding forward-looking information" in our second quarter 2015 Financial Report filed with the US Securities and Exchange Commission, and in other public filings and press releases. We do not intend to update these forward-looking statements except as may be required by applicable law. Statement regarding capital, liquidity and leverage As of January 1, 2013, Basel 3 was implemented in Switzerland along with the Swiss “Too Big to Fail” legislation and regulations thereunder (in each case, subject to certain phase-in periods). As of January 1, 2015, the Bank for International Settlements (BIS) leverage ratio framework, as issued by the Basel Committee on Banking Supervision (BCBS), was implemented in Switzerland by FINMA. Our related disclosures are in accordance with our interpretation of such requirements, including relevant assumptions. Changes in the interpretation of these requirements in Switzerland or in any of our assumptions or estimates could result in different numbers from those shown in this presentation. Capital and ratio numbers for periods prior to 2013 are based on estimates, which are calculated as if the Basel 3 framework had been in place in Switzerland during such periods. Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. Leverage amounts for 4Q14, which are presented in order to show meaningful comparative information, are based on estimates which are calculated as if the BIS leverage ratio framework had been implemented in Switzerland at such time. Beginning in 2015, the Swiss leverage ratio is calculated as Swiss total capital, divided by period-end leverage exposure. The look-through BIS tier 1 leverage ratio and CET1 leverage ratio are calculated as look-through BIS tier 1 capital and CET1 capital, respectively, divided by end-period leverage exposure. Selling restrictions This document is not an offer to sell or a solicitation of offers to purchase or subscribe for securities of Credit Suisse Group AG. This document is not a prospectus within the meaning of article 652a of the Swiss Code of Obligations, nor is it a listing prospectus as defined in the listing rules of the SIX Swiss Exchange AG or any other exchange or regulated trading facility in Switzerland or a prospectus under any other applicable laws. Copies of this document may not be sent to jurisdictions, or distributed in or sent from jurisdictions, in which this is barred or prohibited by law. The information contained herein shall not constitute an offer to sell or the solicitation of an offer to buy, in any jurisdiction in which such offer or solicitation would be unlawful prior to registration, exemption from registration or qualification under the securities laws of any jurisdiction. A decision to invest in securities of Credit Suisse Group AG should be based exclusively on a written agreement with Credit Suisse Group AG or an offering and listing prospectus to be published by Credit Suisse Group AG for such purpose. This document and the information contained herein is not for publication or distribution into the United States of America and should not be distributed or otherwise transmitted into the United States or to U.S. persons (as defined in the U.S. Securities Act of 1933, as amended (the “Securities Act”)) or publications with a general circulation in the United States. This document does not constitute an offer or invitation to subscribe for or to purchase any securities in the United States of America. The securities referred to herein have not been and will not be registered under the Securities Act or the laws of any state and may not be offered or sold in the United States of America absent registration or an exemption from registration under Securities Act. There will be no public offering of the securities in the United States of America. The information contained herein does not constitute an offer of securities to the public in the United Kingdom. No prospectus offering securities to the public will be published in the United Kingdom. This document is only being distributed to and is only directed at (i) persons who are outside the United Kingdom or (ii) to investment professionals falling within article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the “Order”) or (iii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within article 49(2)(a) to (d) of the Order (all such persons together being referred to as “relevant persons”). The securities are only available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such securities will be engaged in only with, relevant persons. Any person who is not a relevant person should not act or rely on this document or any of its contents. 2 October 21, 2015

1) Subject to approval by EGM (EGM: Extraordinary General Meeting) 2) Until we reach our capital target however, we will recommend CHF 0.70 per share with a scrip alternative; we will discontinue the scrip once we have clarity on regulatory requirements and litigation risks. In any event, we will not continue with the scrip beyond 2017 3 Our strategy is to:Be a leading Private Bank and Wealth Manager with strong Investment Banking capabilities and……grow profitably and generate capital through the cycleWe are taking a number of management actions to improve our ability to generate capital internally, includingRight-sizing the Investment Bank, with significant reduction where returns do not exceed cost of capital;A disciplined capital allocation that combines stable capital consumption and improved business profitability;A reduction in our fixed costs;Transitioning non-core assets and implementing closures.To ensure the Group has the strong capital position required to support the implementation of its strategy, we are complementing these actions by raising external capital1) through the combination of a non-preemptive placing of CHF 1.36bn and a rights issue of CHF 4.70bn. Together these actions will result in a pro-forma CET1 ratio of 12.2% and a pro-forma CET1 leverage ratio of 3.6% based on YE2015 targetsAs the strategy is executed, we intend to generate approximately CHF 23-25bn of Operating Free Capital by 2020 of which we intend to distribute at least 40% to shareholders2)We intend to return excess capital to shareholders October 21, 2015

Our organization 4 Note: New management structure effective October 22, 2015 and will be the basis for our reporting in the fourth quarter of 2015 and the 2015 Annual Report, going forward Chief Executive OfficerTidjane Thiam Chief Operating OfficerPierre-Olivier Bouée Chief Finance OfficerDavid Mathers General CounselRomeo Cerutti Chief Risk OfficerJoachim Oechslin HR & CommsPeter Goerke Chief Compliance & Regulatory OfficerLara Warner Geographic structure will drive client focus and better align with regulationDecentralization will increase accountability and cost competitivenessMaintain global linkages for Investment Banking and TradingMaterial strengthening of controls and increase centralization of information Integrated private and investment bank for our APAC domiciled (U)HNW, corporate, and institutional clients Advisory and underwriting platforms covering the Americas and EMEA International Wealth ManagementIqbal Khan Swiss Universal BankThomas Gottstein AsiaPacificHelman Sitohang Investment Banking & Capital MarketsJim Amine Global MarketsTim O’Hara Sales & trading platforms covering the Americas and EMEA Universal bank for our Swiss domiciled private clients (retail, WM), commercial and institutional clients (excl. AM services) Global WM arm serving our non-Swiss and non-APAC domiciled (U)HNW clients, and Global AM business, including Swiss products and clients October 21, 2015

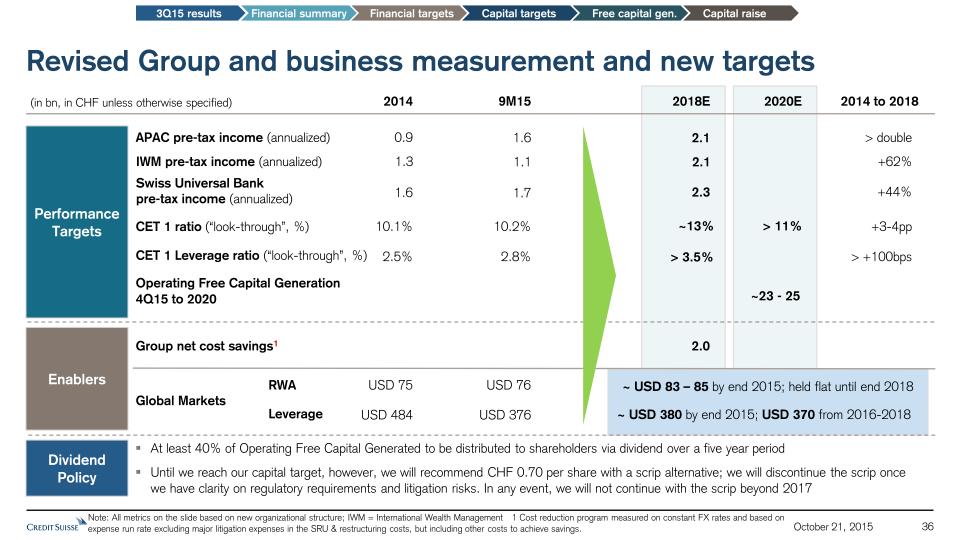

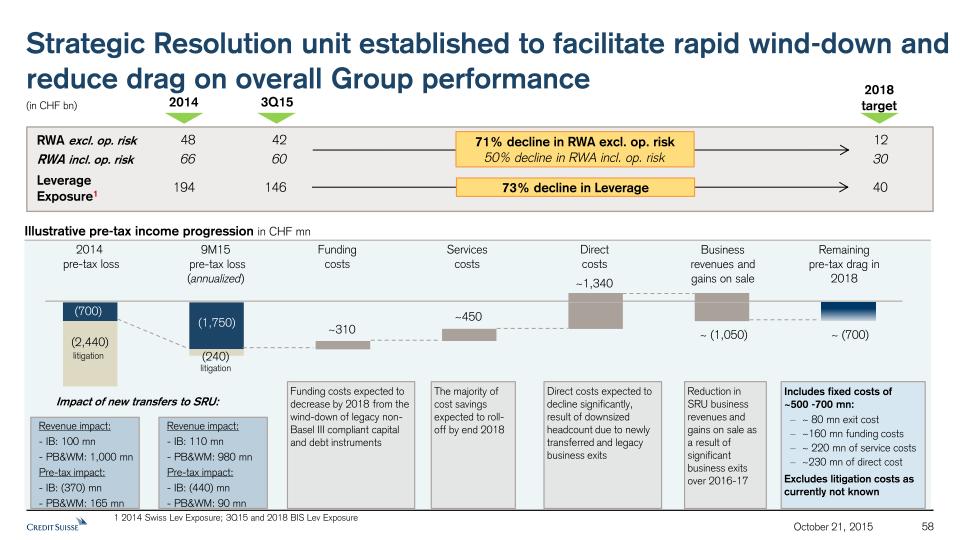

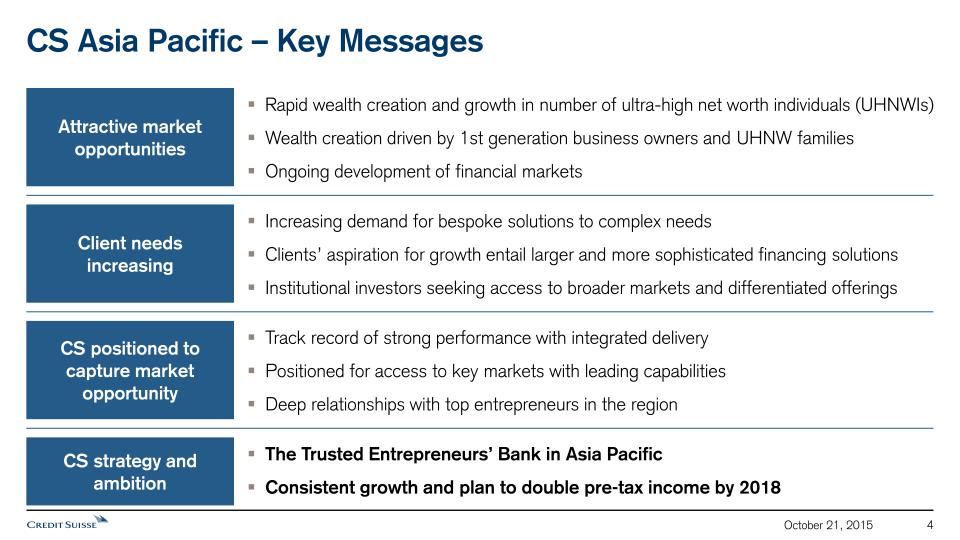

Profitable growth More than double PTI of Asia Pacific from CHF 0.9bn in 2014 to CHF 2.1bn in 2018Increase PTI in International Wealth Management from CHF 1.3bn in 2014 to CHF 2.1bn in 2018Grow PTI for the Swiss Universal Bank from CHF 1.6bn in 2014 to CHF 2.3bn in 2018Realize CHF 3.5bn in cost reduction by end-2018Invest CHF 1.5bn in growth initiativesLeading overall to an absolute reduction of our cost base by a net CHF 2bn1) to below CHF 19bn, with further potential efficiency gains post-2018 1) Based on 2015 cost base; Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses in the SRU & restructuring costs, but including other costs to achieve savings.Note: 2018 figures illustrative; Under new structure, new management structure effective October 22, 2015; SRU=Strategic Resolution Unit 5 October 21, 2015

Improve our capital position 6 1 Internal capital generationRight-size the Investment BankReallocate capitalReduce fixed costsTransition non-core assets & implement closures Capital raising 2 October 21, 2015

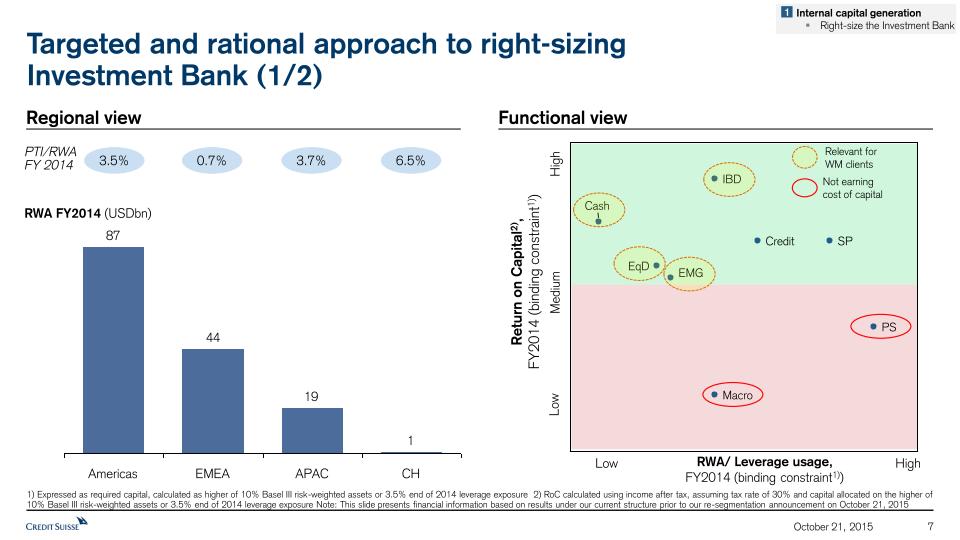

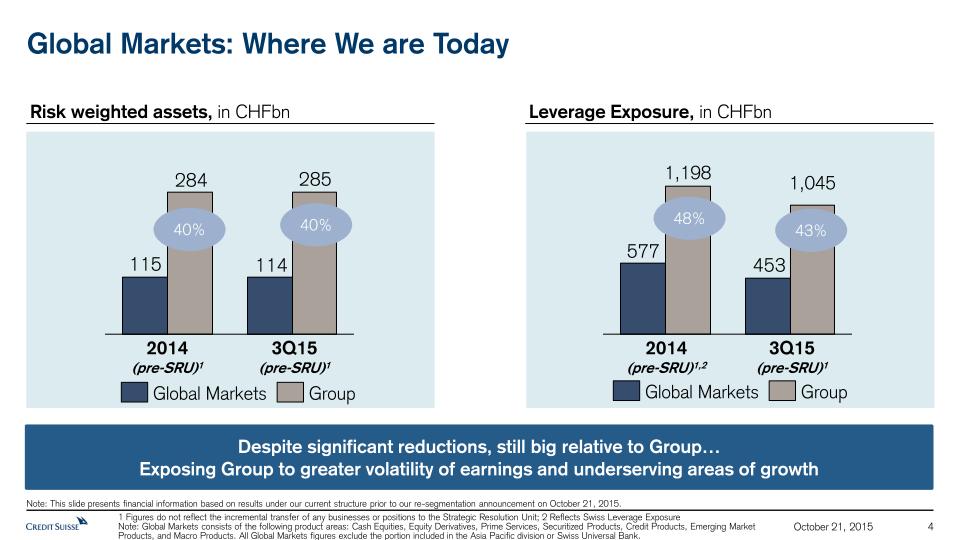

3.5% 0.7% 3.7% 6.5% PTI/RWAFY 2014 1) Expressed as required capital, calculated as higher of 10% Basel III risk-weighted assets or 3.5% end of 2014 leverage exposure 2) RoC calculated using income after tax, assuming tax rate of 30% and capital allocated on the higher of 10% Basel III risk-weighted assets or 3.5% end of 2014 leverage exposure Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 Regional view Functional view IBD PS EqD Cash EMG Credit SP Macro Low Medium High RWA/ Leverage usage,FY2014 (binding constraint1)) Low High Return on Capital2), FY2014 (binding constraint1)) Relevant for WM clients Targeted and rational approach to right-sizing Investment Bank (1/2) RWA FY2014 (USDbn) CH APAC EMEA Americas 7 Not earning cost of capital 1 Internal capital generationRight-size the Investment Bank October 21, 2015

Targeted and rational approach to right-sizing Investment Bank(2/2) -79% 20151) 2Q 2015 2Q 2015 -72% 20151) 1) Expected Note: APAC IB included; Strategic business only; This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 8 AboveCoC Belowcost ofcapital(CoC) 2Q 2015 158 126 Prime (USD bn) Macro (USDbn) -25% 20151) 2Q 2015 -50% 20151) 2Q 2015 Leverage RWA Leverage RWA RWA down CHF 20bnLeverage down CHF 87bn RWA breakdown, in USDbn YE 2015 target 1 Internal capital generationRight-size the Investment Bank October 21, 2015

Investment Bank: targeted reduction of RWA and Leverage – current structure (incl. APAC) RWA, USDbn (current structure, strategic) 1) Expected 2) Expressed as required capital, calculated as either 10% of Basel III risk-weighted assets or 3.5% of leverage exposure Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015, strategic only. BIS LVE for leverage exposure 9 Leverage, USDbn (current structure, strategic) YE20151) Below CoC 2Q 2015 158 Above CoC 118 491 Above CoC Below CoC 2Q 2015 YE20151) 635 -63% -16% -42% -13% RoC2) (%) ~19% ~15% ~13% ~10% 1 Internal capital generationRight-size the Investment Bank Includes APAC IB Includes APAC IB October 21, 2015

Planned RWA reduction at Investment Bank optimizes PTI/RWA arbitrage 10 PTI/RWA at YE2015 pro forma Index, (Pre-optimization=100) Maximumcapital release Current plan Pre-optimization Note: Excl. Asia and IBD CH. All numbers based on FYFC 2015 as of 30.09.2015; Source: Credit Suisse data Reduction in RWAvs Pre-optimizationUSD bn -40 -68 1 Internal capital generationRight-size the Investment Bank October 21, 2015

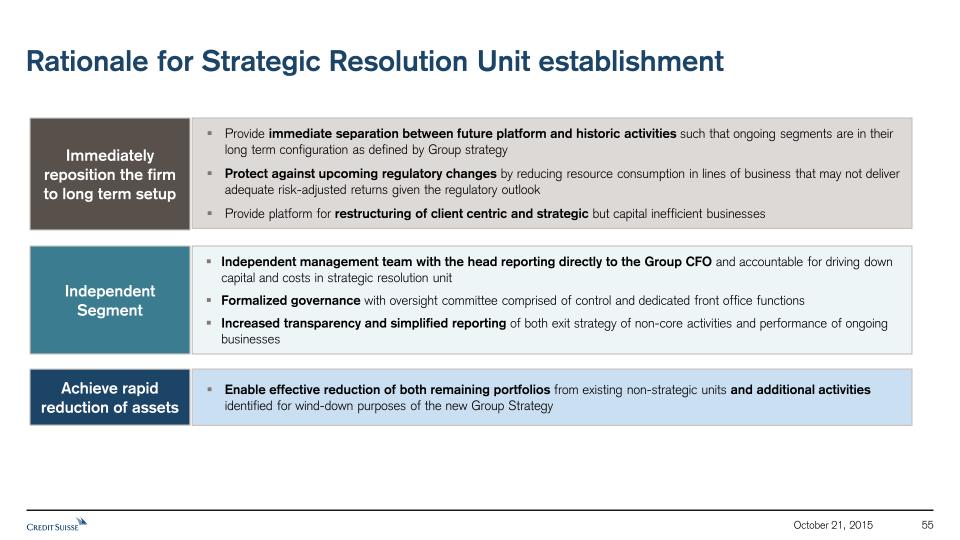

11 1) Expected 2) Illustrative 3) Pre-regulatory change; Post-regulatory change RWA would amount to USD 174bn of which USD 142bn is IB core 4) Strategic Resolution Unit Note: New management structure effective October 22, 2015 IBCM & GM core SRU RWA excl. Ops Risk4) IB (IBCM & GM) RWA and Leverage expected to remainstable after restructuring – new structure IB (IBCM & GM) RWAUSDbn (new structure, incl. SRU) IB (IBCM & GM) LeverageUSDbn (new structure, incl. SRU) IBCM & GM Core SRU4) 1 Internal capital generationRight-size the Investment Bank SRU Ops Risk RWA4) 20202)3) 134 7 20182) 136 YE20151) 154 20202) 430 35 20182) 436 YE20151) 554 Excludes APAC IB Excludes APAC IB October 21, 2015

Improving return on capital – Swiss Universal Bank 1) Expressed as required capital, calculated as higher of 10% Basel III risk-weighted assets or 3.5% end of year leverage exposure 2) Illustrative 3) Target 4) Any such IPO would involve the sale of a minority stake and would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG 5) Legal entity Credit Suisse (Schweiz) AG Note: New management structure effective October 22, 2015 12 PTI(CHF bn) RoC1)(%) 1.6 2.33) 2014 2018 Transparency and market disciplineAttractive, stable earnings stream to investorsValue of Swiss franchise highlightedIncentive alignment for management of Swiss Universal Bank5)Currency to take advantage of potential market consolidation IPO4) of Swiss Universal Bank5) expected to support the delivery of growth and profitability 1 Internal capital generationReallocate capital 13% 17%2) October 21, 2015

Improving return on capital and capital allocation 20184) 20153) 26% 27% 20184) 20153) 24% 33% 20184) 20153) 11% 19% APAC IWM Investment Bank (IBCM and GM) % of RWA allocated2) 11% 18% 37% 17% 17% 44% RoC1) 1) RoC calculated using income after tax, assuming tax rate of 30% and capital allocated on the higher of 10% Basel III risk-weighted assets or 3.5% average leverage exposure, based on 9M15 Annualized 2) Excluding Corporate Center and SRU 3) Expected 4) Illustrative Note: New management structure effective October 22, 2015; IBCM=Investment Banking and Capital Markets; GM=Global MarketsNote: Numbers not adding up due to rounding 1 Internal capital generationReallocate capital 13 20184) 20153) 13% 17% Swiss Universal Bank 28% 28% October 21, 2015

1) Expected; 2) Includes LE program, IT architecture simplification, other corporate center programs and realignment costsNote: Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses in the SRU & restructuring costs, but including other costs to achieve savings; New management structure effective October 22, 2015 Reducing fixed costs while investing in growthIn CHFbn 14 2018cost base target 18.5-19.0 Invest in growth +1.5 Business exits & run-down of additional SRU portfolio -1.3 Workforce strategy, technology & London right-sizing -0.9 Wind-down of Corp. Center costs -0.1 Run-down of SRU portfolio(planned run-down of prior NSU) -0.3 Substantial completion of Corp. Center programs2) -0.9 2015cost base1) 20.5-21.0 CHF -1.2bnpreviously planned cost reduction CHF -2.3bnadditional cost reduction 1 Internal capital generationReduce fixed costs CHF +1.5bnInvestment in growth October 21, 2015

The Group is expected to deliver profitable growth … 15 Illustrative pre-tax income progression, CHFbn Return onTangible Equity C/I ratio1) 10% ~14% 9% 79% ~66% 81% ~+5pp ~(15)pp 2014 Illustrative 2018 9M15 1) Expected, excludes impact of FVoD and certain litigation provisions as disclosed in our Financial Report and assumes a tax rate of 30% for return on tangible equity 2) Includes Corporate Center Note: 2014 and 9M15 reflects Core results; New management structure effective October 22, 2015 ~9 – 10 Illustrative 2018 Strategic Resolution Unit (SRU) wind-down (revenue loss) -0.8 Gross cost savings Growth investment -1.5 Target growth to 2018 3.0-4.0 Full year 2015 pre-tax income1) 4.5 1.1 APAC Swiss Universal Bank Other divisions2) 9M15 Ann. October 21, 2015

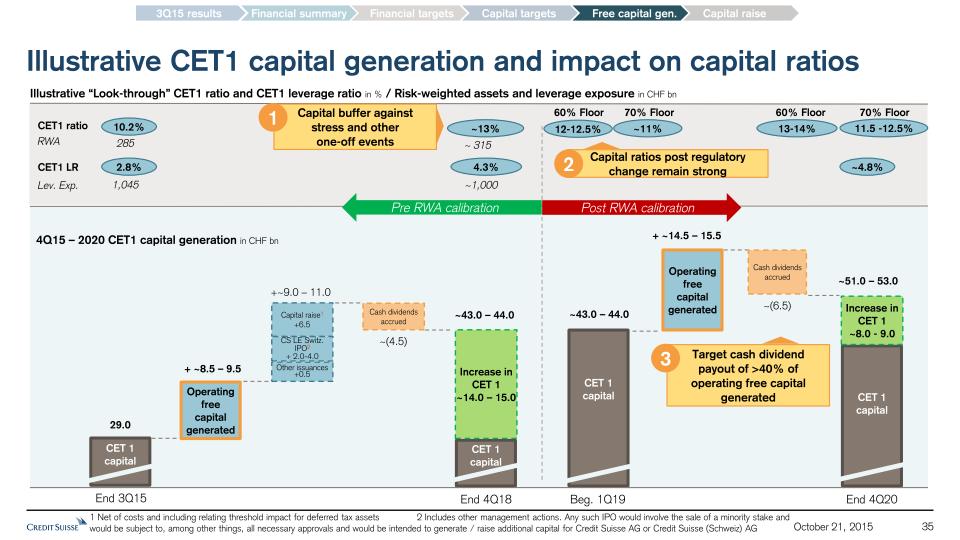

… and return capital to shareholdersIllustrative 4Q2015 to 2020, in CHFbn 1) Capital impact from targeted IPO of Credit Suisse (Schweiz) AG as well as disposal of non-core assets, does not include material capital impact / benefit from cost savings and exposure reductions; any such IPO would involve the sale of a minority stake and would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG 2) Free Capital generated 3) Including impact on capital applying RWA floors at 60% 4) Net of costs and including relating threshold impact for deferred tax assets; subject to approval by EGM (EGM: Extraordinary General Meeting) 5) Until we reach our capital target however, we will recommend CHF 0.70 per share with a scrip alternative; we will discontinue the scrip once we have clarity on regulatory requirements and litigation risks. In any event, we will not continue with the scrip beyond 2017 Note: Under the free capital generation concept, capital is calculated using 10% to convert RWA into capital and 3.5% for leverage exposure due to the anticipated TBTF requirement of 3.5% CET1 leverage ratio and 10% CET1 requirement; New management structure effective October 22, 2015 IPO & disposals1) CapitalRaise Capital raise plus IPO & disposals Targeted Operating FCG2)4Q15 to ‘20 Free Capital Generated Business moves & Asset disposals Regulatory and Capital Requirements FCG after businessmoves ®. req. Cash dividends accrued5) NetFCG2) OtherIssuances 16 2-4 6.54) 9-11 23-25 33-35 (1) (7)3) 25-27 ~(11) 14-16 0.5 At least 40% of Operating Free Capital generated planned to be returned to shareholders October 21, 2015

Our 3Q15 results further emphasize the need for change Progress on capital “Look-through” Swiss Total Leverage ratio of 4.5%, of which BIS Tier 1 leverage ratio of 3.9% and CET1 leverage ratio of 2.8%“Look-through” CET1 capital slightly down QoQ to 10.2% Asia Pacific 48% year-to-date increase in overall pre-tax income to CHF 1,129mnWealth Management with YoY double-digit growth in NNA in 3Q15 and 9M159M15 Investment Banking revenues increase of 15%, driven by equities Reduce exposure to volatile IB and tilt towards stable, high-return businesses Build a strong capital position Accelerate growth by focusing on UHNWI in other EM APAC key opportunity Private Banking & Wealth Management Strategic pre-tax income of CHF 753mn with RoC of 20%, impacted by weaker client activity and adverse market conditionsStrong strategic NNA of CHF 17.3bn of which CHF 10.5bn from WMC with growth across all regions Strategic pre-tax income of USD 291mn significantly lower QoQ and YoY, primarily due to lower fixed income results driven by muted client activityReduction in leverage exposure to USD 615 bn; early achievement of USD 600-620 bn year-end target Investment Banking Implications for strategy Credit Suisse Group Group pre-tax income (excluding revenue impact from fair value on own debt) of CHF 238mn. Group Strategic pre-tax income for the quarter of CHF 826mn, a 49% decrease from 3Q149M15 return on equity of 9%, of which 11% for the Strategic business Drive capital allocation to high return businesses with cost discipline Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 17 October 21, 2015

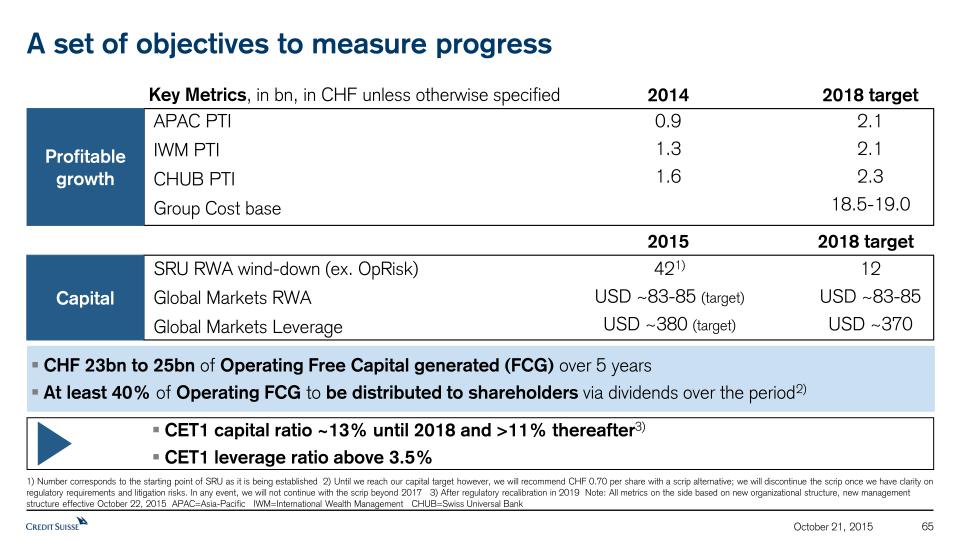

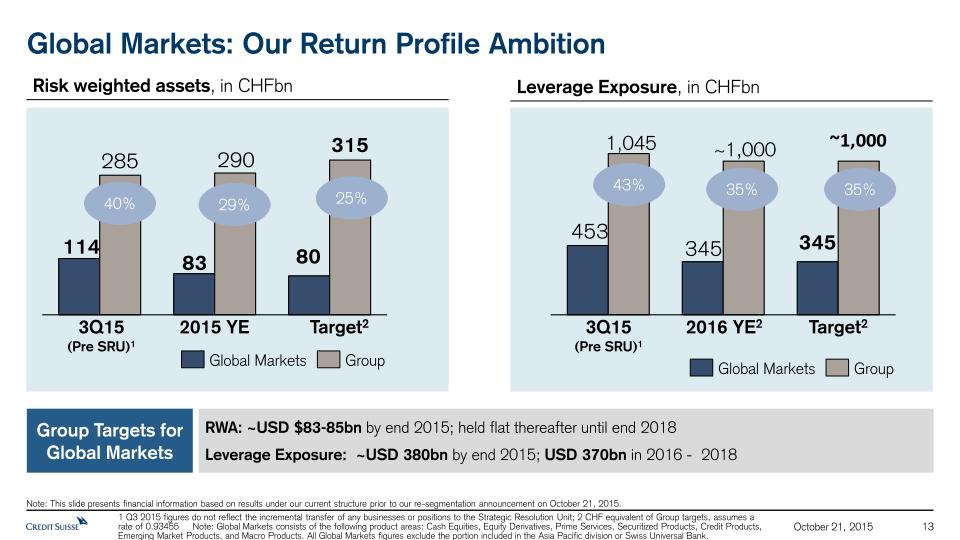

18 A set of objectives to measure progress Key Metrics, in bn, in CHF unless otherwise specified 2018 target Capital SRU RWA wind-down (ex. OpRisk)Global Markets RWAGlobal Markets Leverage 421) USD ~83-85 (target)USD ~380 (target) 12USD ~83-85USD ~370 1) Number corresponds to the starting point of SRU as it is being established 2) Until we reach our capital target however, we will recommend CHF 0.70 per share with a scrip alternative; we will discontinue the scrip once we have clarity on regulatory requirements and litigation risks. In any event, we will not continue with the scrip beyond 2017 3) After regulatory recalibration in 2019 Note: All metrics on the side based on new organizational structure, new management structure effective October 22, 2015 APAC=Asia-Pacific IWM=International Wealth Management CHUB=Swiss Universal Bank 2014 2015 Profitable growth APAC PTIIWM PTICHUB PTIGroup Cost base 2.12.12.318.5-19.0 0.91.31.6 2018 target CHF 23bn to 25bn of Operating Free Capital generated (FCG) over 5 yearsAt least 40% of Operating FCG to be distributed to shareholders via dividends over the period2) CET1 capital ratio ~13% until 2018 and >11% thereafter3)CET1 leverage ratio above 3.5% October 21, 2015

19 Time (GMT) Topic Speaker 11.00 – 11.05 Welcome Urs Rohner, Chairman of the Board 11.05 – 12.00 Overview & Summary Tidjane Thiam, Chief Executive Officer 12.00 – 13.00 Financials & Capital (incl. 3Q15 results) David Mathers 13.00 – 14.00 Lunch 14.00 – 14.30 Swiss Universal Bank Thomas Gottstein 14.30 – 15.10 Asia Pacific Helman Sitohang 15.10 – 15.40 International Wealth Management Iqbal Khan 15.40 – 16.20 Coffee break 16.20 – 16.40 Global Markets Tim O’Hara 16.40 – 17.00 Investment Banking & Capital Markets Jim Amine 17.00 – 19.30 Q&A session All Agenda for the day October 21, 2015

Agenda for today Credit Suisse Strategy Capital position 1 2 20 October 21, 2015

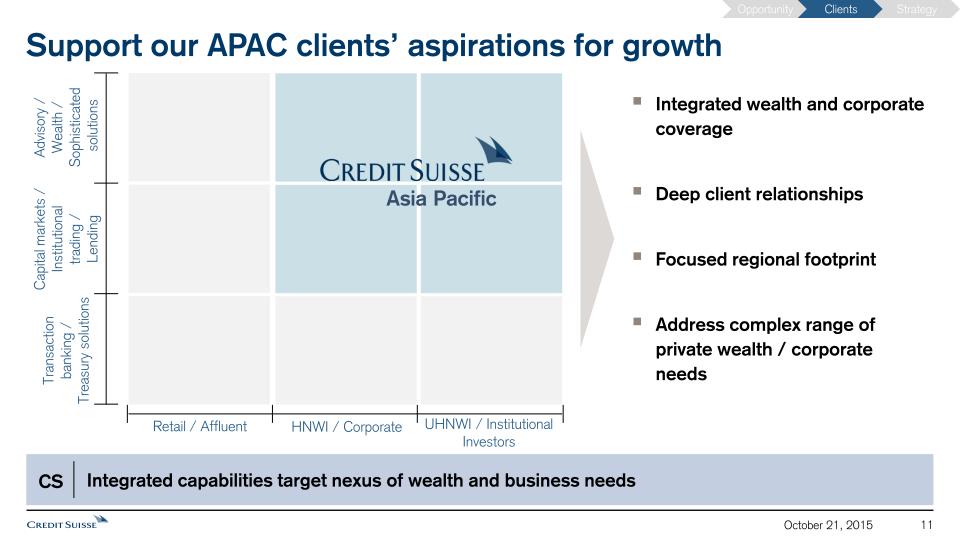

Our ambition is to be a leading Private Bank and Wealth Manager with strong Investment Banking capabilities Capture the Wealth Management opportunity in Emerging Markets by accelerating growth in Asia Pacific and by replicating our successful model in other Emerging Markets APAC and other EM SwissUniversal Bank InvestmentBank Create a Swiss Universal Bank to expand our position with Swiss private, corporate and institutional clients and participate in domestic consolidation opportunities Right-size the Investment Bank to optimize its profitability and capital usage, reduce volatility of earnings and support Wealth Management customer needs 21 October 21, 2015

31 94 2019 2014 63 Global wealth is expected to continue growing Estimated global wealth development 2014-19, in CHFtr Source: BCG Global Wealth Report 2015. UHNW and HNW individual’s wealth, excl. pension and insurance HNWI=USD1-20mm wealth, UHNWI>USD20mm wealth 22 October 21, 2015

Emerging Markets expected to drive ~60% of wealth increaseby 2019 Estimated global wealth development 2014-19, in CHFtr Source: BCG Global Wealth Report 2015. UHNW and HNW individual’s wealth, excl. pension and insurance HNWI=USD1-20mm wealth, UHNWI>USD20mm wealth Note: Numbers not adding up due to rounding 2014 94 2019 31 63 Mature Markets EmergingMarkets 47% 53% 60% 40% 39% 61% 23 October 21, 2015

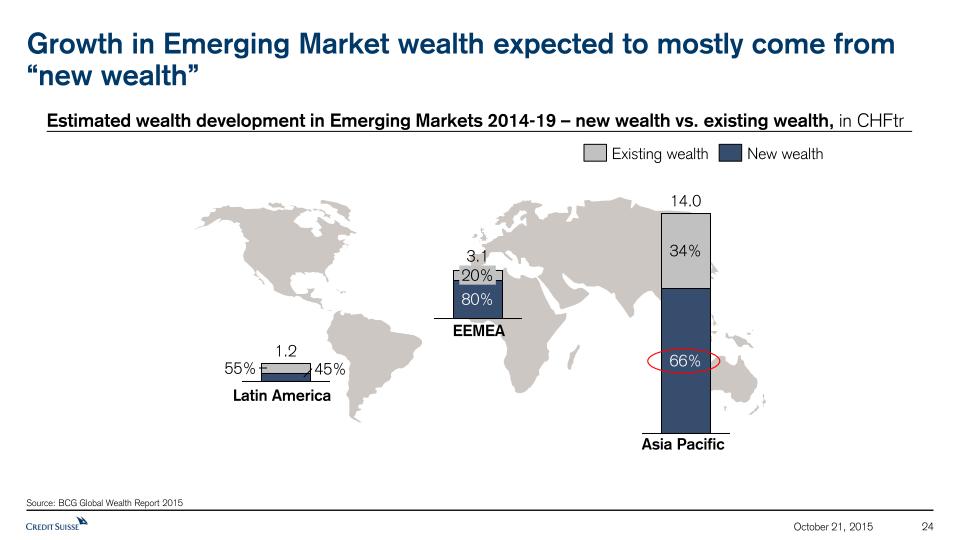

Growth in Emerging Market wealth expected to mostly come from “new wealth” Source: BCG Global Wealth Report 2015 Estimated wealth development in Emerging Markets 2014-19 – new wealth vs. existing wealth, in CHFtr 1.2 45% 55% Existing wealth New wealth Latin America 20% 3.1 80% EEMEA 34% 14.0 66% Asia Pacific 24 October 21, 2015

LatAm Asia1) EEMEA CS client focus 1) Ex-JapanSource: Credit Suisse Research Institute Note: Numbers not adding up due to rounding 4th 3% 3rd 11% 2nd 27% 1st 57% 5th+ 2% 14% 3rd 68% 1st 5th+ 9% 2nd 9% 0% 4th 1st 7% 3rd 16% 5th+ 12% 5% 2nd 4th 61% First generation entrepreneurs driving new wealth generation, not only in Asia but also in other Emerging Markets…Generational ownership 1st to 5th generation (in %) 25 October 21, 2015

… while ownership profile more balanced in Mature MarketsGenerational ownership 1st to 5th generation (in %) 14% 5th+ 3rd 16% 4th 8% 2nd 1st 27% 35% 13% 2nd 1st 5th+ 21% 31% 22% 14% 4th 3rd Western Europe U.S. Source: Credit Suisse Research Institute Note: Numbers not adding up due to rounding 26 October 21, 2015

In Mature Markets, the US is expected to remain the largest pool of wealth US, Japan, Western Europe estimated wealth in 2014 and 2019, in CHFtr WesternEurope 9 Japan 3 US 26 12 3 33 2014 2019 Largest national market: Germany ~CHF 1.4tr Largest national market: Germany ~CHF 2.3tr Source: BCG Global Wealth Report 2015. UHNW and HNW individual’s wealth, excl. pension and insurance 27 October 21, 2015

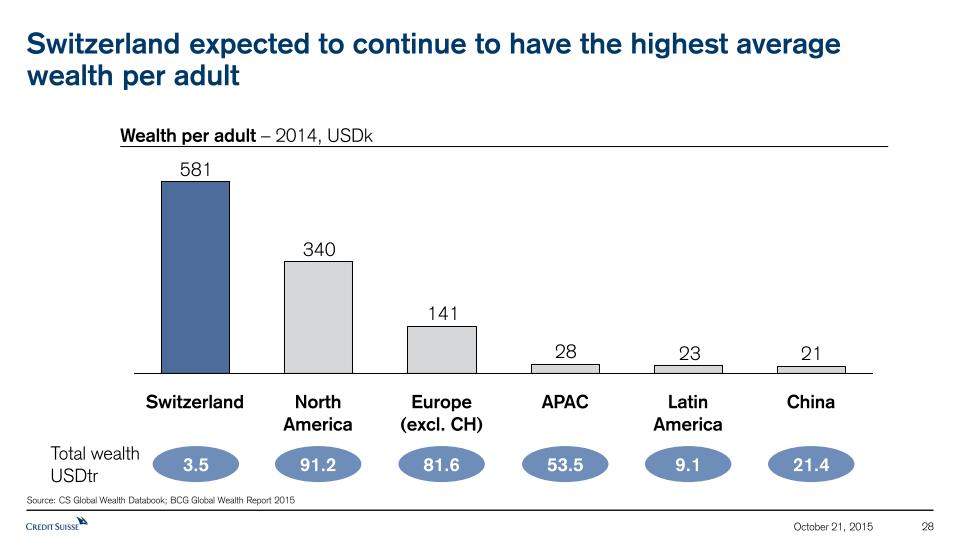

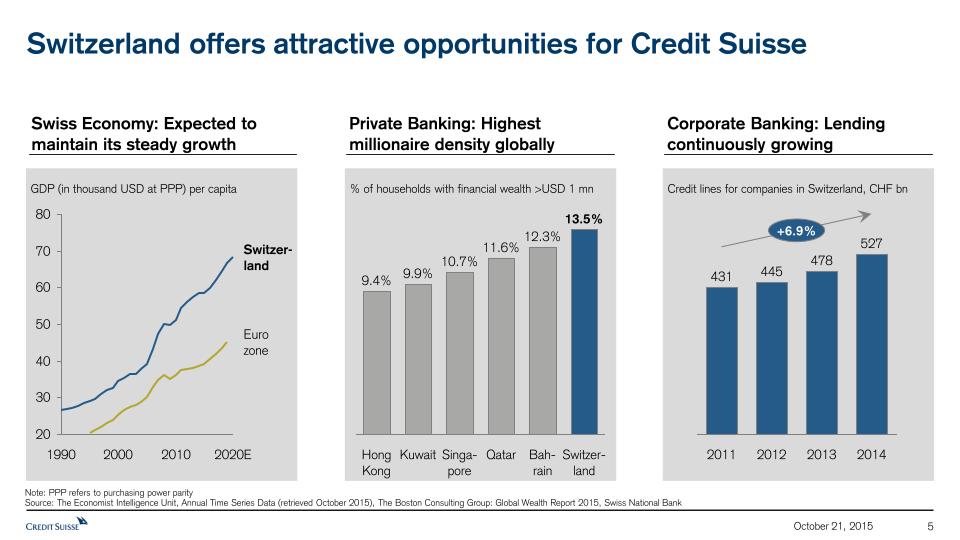

Switzerland expected to continue to have the highest average wealth per adult Source: CS Global Wealth Databook; BCG Global Wealth Report 2015 NorthAmerica Switzerland China LatinAmerica APAC Europe(excl. CH) Wealth per adult – 2014, USDk 3.5 91.2 81.6 53.5 9.1 21.4 Total wealthUSDtr 28 October 21, 2015

Despite slower growth, Mature Markets expected to remain important Source: BCG Global Wealth Report 2015. UHNW and HNW individual’s wealth, excl. pension and insurance HNWI=USD1-20mm wealth, UHNWI>USD20mm wealth Note: Numbers not adding up due to rounding 2019 45% 2017 81 57% 43% 2016 94 53% 47% 2018 87 55% 75 58% MatureMarkets 2015 70 59% 41% 2014 63 61% 39% 2013 54 66% 34% 2012 46 68% 32% Emerging Markets 42% Estimated global wealth in 2012-19, in CHFtr 29 October 21, 2015

The Wealth Management opportunity for Credit Suisse Significant growth in APAC and Other EM + Large pool of wealth in Mature Markets Most attractive long term opportunity for Wealth Management Switzerland – our home market – providing stability to earningsFocused approach in US & Western Europe given highly competitive environment Balanced approach 30 October 21, 2015

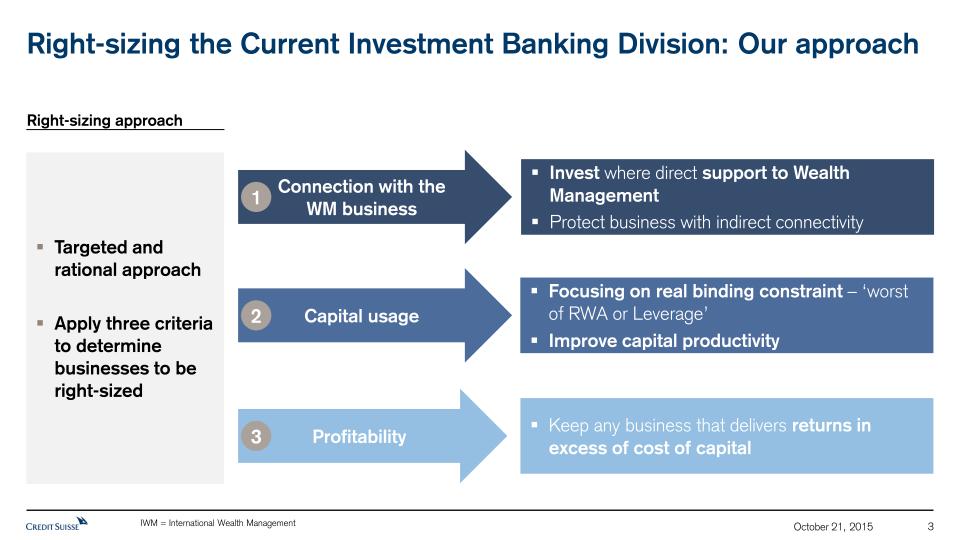

Connection with the WM business 1 Invest where direct support toWealth ManagementProtect business with indirect connectivity Targeted and rational approachApply three criteria to determine businesses to be right-sized Right-size the Investment Bank: our approach Profitability 3 Capital usage 2 Keep any business that delivers returns in excess of cost of capitalAvoid cliff effect when right-sizing Focus on real binding constraint – ‘worst of RWA or Leverage’ Improve capital productivity Right-sizing approach 31 October 21, 2015

Revenues generated by UHNW clients from using IB products and services UHNWI needs CS IB solutions CS IB Deal revenue mix1) Financing Investments Hedging Capital markets access Trading Share backed lending / Loan syndication Shares / Funds / Derivatives Interest rate, FX, Equity / Credit ECM / DCM / M&A deals AES / Prime Services for Private Clients 19% 33% 41% 100% 2% 1) Revenue mix of integrated bank revenues where WM clients used episodic IB solutions, based on current reporting structure Note: this slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 32 2014 October 21, 2015

PTI/RWAFY 2014 1) Expressed as required capital, calculated as higher of 10% Basel III risk-weighted assets or 3.5% end of 2014 leverage exposure 2) RoC calculated using income after tax, assuming tax rate of 30% and capital allocated on the higher of 10% Basel III risk-weighted assets or 3.5% end of 2014 leverage exposure Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015, APAC IB included Regional view Functional view Strong IB franchise and returns with exception of EMEA region and Macro / Prime Services business RWA FY2014 (USDbn) 33 Americas CH APAC EMEA 3.5% 0.7% 3.7% 6.5% IBD PS EqD Cash EMG Credit SP Macro Low Medium RWA/ Leverage usage,FY2014 (binding constraint1)) Low High Return on Capital2), FY2014 (binding constraint1) Relevant for WM clients Not earning cost of capital High October 21, 2015

Investment Bank: Business profitability and capital allocation RoC1 FY2014 EQ FID IBD Capital FY20141 IBD Credit EQ Derivatives SecuritizedProducts Cash EMG Prime Macro FY2014 IB profitability and capital usage 1) RoC calculated using income after tax, assuming tax rate of 30% and capital allocated on the higher of 10% Basel III risk-weighted assets or 3.5% end of 2014 leverage exposure Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015, APAC IB included; Represents “fully allocated” view, i.e., IB funding costs, operational risk and Corporate Bank costs have been allocated to individual IB businesses Avg. ~12.5% RoC1 34 October 21, 2015

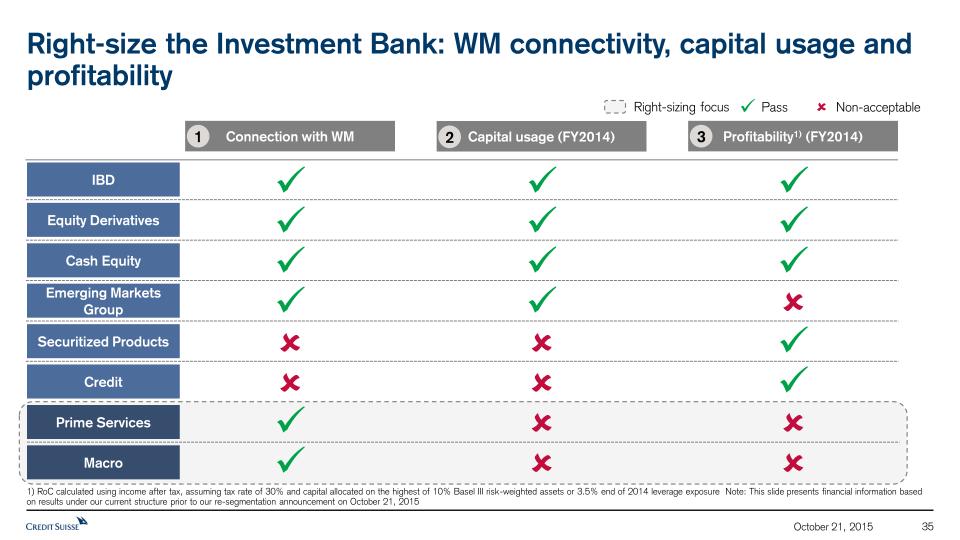

Right-size the Investment Bank: WM connectivity, capital usage and profitability Right-sizing focus 1) RoC calculated using income after tax, assuming tax rate of 30% and capital allocated on the highest of 10% Basel III risk-weighted assets or 3.5% end of 2014 leverage exposure Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 û û û û ü ü ü ü ü ü ü ü ü ü ü ü Connection with WM Capital usage (FY2014) Profitability1) (FY2014) IBD Equity Derivatives Cash Equity Securitized Products Credit Emerging Markets Group Prime Services Macro û û ü û û ü ü û Pass Non-acceptable û 1 2 3 35 ü û October 21, 2015

Macro Leverage, in USDbn 2Q15 3Q15 20151) Right-size the Investment Bank: Macro Macro RWA, in USDbn Largely exit in EMEA and APACMaintain core US -79% -72% 1) Expected Note: APAC IB included; Strategic business only; This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 36 October 21, 2015

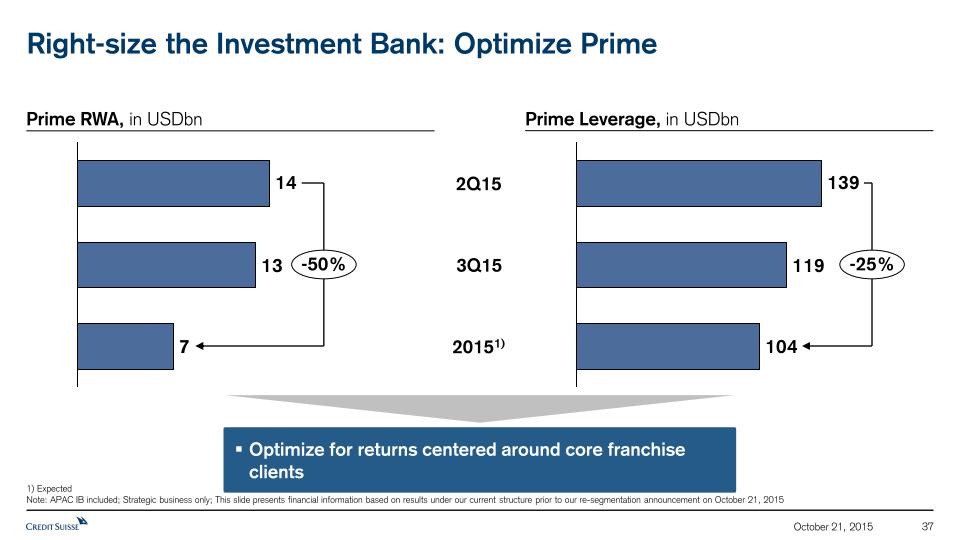

Right-size the Investment Bank: Optimize Prime 2Q15 -25% Optimize for returns centered around core franchise clients -50% Prime Leverage, in USDbn Prime RWA, in USDbn 3Q15 20151) 1) Expected Note: APAC IB included; Strategic business only; This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 37 October 21, 2015

2014; USDtr 2030; USDtr CAGR 2014-2030 2.1 9.8 Corporate Bond Value 5.6 1.5 EquitiesCapitalization 9% 9% Corporate Bond Value 5.9 0.7 EquitiesCapitalization 18.9 2.7 12% 15% Corporate Bond Value 42.0 4.8 EquitiesCapitalization 82.4 8.5 15% 15% •% 1) Only Emerging Markets within APACSource: Credit Suisse Research Institute (Emerging Capital Markets: the road to 2030). Latin America EEMEA APAC1) Prime is important for the Equity franchise which is a core component of the Emerging Markets opportunity 38 October 21, 2015

Right-size the Investment Bank: Optimize Prime Investment Bank Monthly Net Revenue Volatility1), in USDbn 1) Source: Credit Suisse Internal DataNotes: APAC IB included; This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 06 07 08 09 10 11 12 13 14 1H’15 2.0 1.2 0.8 0.4 0.0 -0.4 -0.8 -2.4 IBD Prime Services Equities Fixed Income 39 October 21, 2015

Right-size the Investment Bank: Optimize Prime 1) Leverage exposure data is spot period-end 2) 2012-14 RoA calculated using 5-quarter average leverage exposures, 2015 quarterly data is calculated using spot period-end leverage exposure 3) ExpectedNotes: SLR – Swiss Leverage Exposure; BIS – Bank for International Settlements; APAC IB included; This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 PrimeRoA2)in bps 83 83 94 128 133 2014 SLR 4Q2015 BIS3) 2013 SLR 3Q2015 BIS 2012 SLR PrimeLeverageExposure1)in USDbn -47% Prime Leverage Exposure and Prime Return on Assets 40 October 21, 2015

Investment Bank: targeted reduction of RWA and Leverage RWA, USDbn 1) ExpectedNote: APAC IB included, This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on Oct 21, 2015; Strategic IB business only; BIS LVE for leverage exposure 41 Leverage, USDbn YE 20151) Below CoC 2Q 2015 158 Above CoC 118 491 Above CoC Below CoC 2Q 2015 YE 20151) 635 -63% -16% -42% -13% October 21, 2015

Optimized Investment Bank expected to deliver returns above cost of capital RWA in CHFbn 1) IB new structure, i.e. excl. APAC IB and SRU positions (SRU – Strategic Resolution Unit) 2) 9M15 PTI annualized 3) RoC calculated using income after tax, assuming tax rate of 30% and capital allocated on the highest of 10% Basel III risk-weighted assets or 3.5% leverage exposure 4) Illustrative Note: New management structure effective October 22, 2015 Return on capital3) LE in CHFbn 10%2) 19% PTI in CHFbn 9M15 20184) 92 102 392 369 2.02) 3.5 New Structure: IBCM + Global Markets1) 42 October 21, 2015

APAC: Expected to double revenues – from CHF 3.3bn in 2014 to CHF 6.8bn in 2020Net revenues in CHFbn +13% 20202) 20182) 2014 Context Strategic Actions A leading Entrepreneurs’ Bank with sophisticated advisory solutionsTop equities and credit franchises with disciplined risk management Focus on billionaires, next generation and lower tier entrepreneursGrow credit via bespoke lending solutionsExpand RM base; drive RM productivity through digitalizationReplicate success of Integrated Bank approach in SEA1)Expand footprint in Greater China (China onshore, scaling up China offshore, Taiwan)Address Japan savings opportunity with integrated solutions RevenueCAGR 1) SEA=South-East Asia 2) Illustrative Note: New management structure effective October 22, 2015 43 October 21, 2015

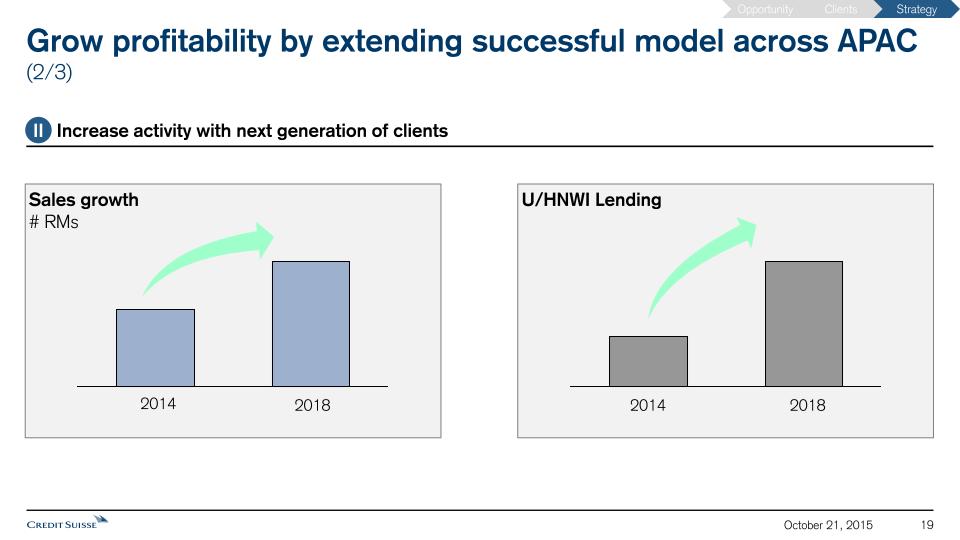

APAC: Profitable growthPTI in CHFbn 44 >2x 20201) 2018Target 2014 Over the period of 2011 to 2014:RM growth +21% AuM growth +70% WMC APAC PTI 4x 1) IllustrativeNote: New management structure effective October 22, 2015 October 21, 2015

IWM: Replicate our success in Asia Pacific in other Emerging MarketsNet revenues in CHFbn +7% 20205) 20185) 2014 1) Euromoney Magazine Survey 2015 for 'Best Private Banking Services Overall‘. Ranking does not distinguish between on/off-shore 2) CEE=Central and Eastern Europe 3) MENA=Middle-East and North Africa 4) Lux=Luxembourg5) Illustrative Note: Includes Asset Management division; New management structure effective October 22, 2015 Context Strategic Actions Leading market positions1) in EM and DM:#1 in CEE2), #1 in MENA3), #2 in LatAm#3 position in Western Europe Create dedicated, fully accountable managerial platform for intl. UHNW clientsDouble lending volume by 2020 (15% p.a.)Grow RMs in EM by 5% p.a. Improve joint PB/IB coverageBuild out London, Lux4), CH as hubs and add new spokes / advisory offices in selected locationsDigitize service model for lower wealth bands: new offering focused on clients <5m AuM 45 RevenueCAGR October 21, 2015

IWM: Profitable growthPTI in CHFbn +13% 20201) 2018 Target 2014 Growth trajectory to benefit from finalization of regularizationTransition sub-scale platforms in Western Europe towards more profitable models CAGR 46 1) IllustrativeNote: New management structure effective October 22, 2015 October 21, 2015

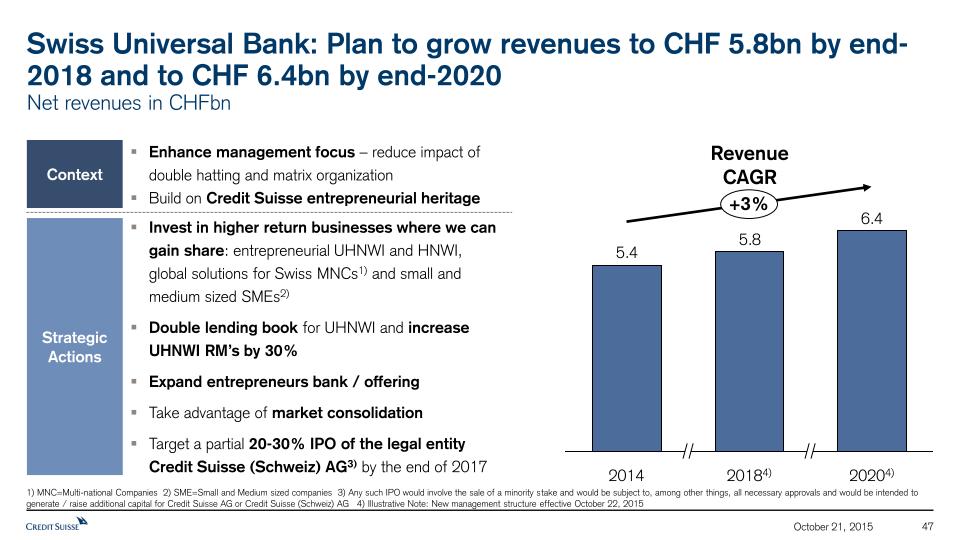

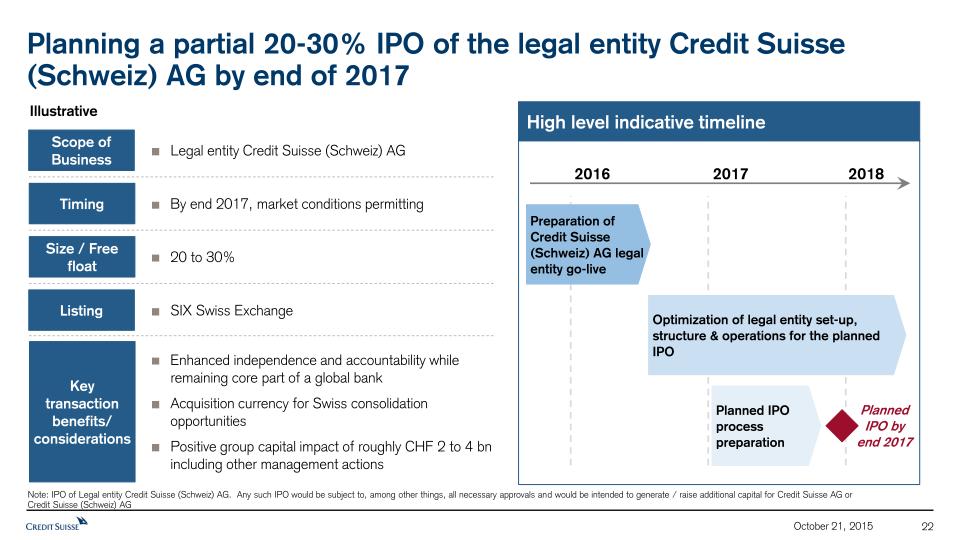

Swiss Universal Bank: Plan to grow revenues to CHF 5.8bn by end-2018 and to CHF 6.4bn by end-2020Net revenues in CHFbn 2014 20204) +3% 20184) Context Strategic Actions Enhance management focus – reduce impact of double hatting and matrix organizationBuild on Credit Suisse entrepreneurial heritage Invest in higher return businesses where we can gain share: entrepreneurial UHNWI and HNWI, global solutions for Swiss MNCs1) and small and medium sized SMEs2)Double lending book for UHNWI and increase UHNWI RM’s by 30%Expand entrepreneurs bank / offeringTake advantage of market consolidationTarget a partial 20-30% IPO of the legal entity Credit Suisse (Schweiz) AG3) by the end of 2017 1) MNC=Multi-national Companies 2) SME=Small and Medium sized companies 3) Any such IPO would involve the sale of a minority stake and would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG 4) Illustrative Note: New management structure effective October 22, 2015 47 RevenueCAGR October 21, 2015

Swiss Universal Bank: Profitable growthPTI in CHFbn +11% 20201) 2018 Target 2014 End-to-end accountability and responsibility over Swiss costs and investmentsIncreased cost efficiency through footprint optimization, automation and operational leverage CAGR 48 1) IllustrativeNote: New management structure effective October 22, 2015 October 21, 2015

The Group is expected to deliver profitable growth … 49 Illustrative pre-tax income progression, CHFbn Return onTangible Equity C/I ratio1) 10% ~14% 9% 79% ~66% 81% ~+5pp ~(15)pp 2014 Illustrative 2018 9M15 1) Expected, excludes impact of FVoD and certain litigation provisions as disclosed in our Financial Report and assumes a tax rate of 30% for return on tangible equity 2) Includes Corporate Center Note: 2014 and 9M15 reflects Core results; New management structure effective October 22, 2015 Gross cost savings -0.8 Strategic Resolution Unit (SRU) wind-down (revenue loss) Growth investment -1.5 Target growth to 2018 3.0-4.0 Full year 2015 pre-tax income1) 4.5 1.1 ~9 – 10 Illustrative 2018 APAC Swiss Universal Bank Other divisions2) 9M15 Ann. October 21, 2015

Agenda for today Credit Suisse Strategy Capital position 1 2 50 October 21, 2015

Our current capital position Source: company quarterly financial disclosure Our capital position has impacted our ability to deliver value for our stakeholders:Impacted strategic flexibilityRestricted ability to implement necessary restructuring measuresImpacted the amount of distributions available for shareholders CS vs. select peer’s CET 1 RWA ratios, Q2 2015 10.3% 10.4% 11.0% 11.1% 11.4% 11.4% 11.7% 12.5% 14.4% 51 October 21, 2015

Anticipated regulatory developments highlight need for capital buffer 52 2016 2017 2018 2019 2020 Recalibrated leverage ratio likely to be primary capital constraint until 2019, however… …RWA uplift resulting from capital floors above 60% will drive the binding constraint1) from the start of 2019 Final rules for advanced models expected by 2016 The impact of FRTB will primarily affect market risk assets in investment banking and is estimated at ~50bps2)Our initial estimate of the incremental impact of a floor against revised standard models is 25-100bps2) if the floor is set at 60%, and 100-250bps2) if the floor is set at 70%. The impact of a floor will affect both market and credit risks across both investment banking and private banking assets. These estimates are inherently uncertain given that implementation is expected several years in the future CS targeting ~13% CET1 capital ratio by the end of 2018 Leverage ratio recalibration RWA uplift TBTF rules effective from January 1st, 2019Implied minimum CET1 capital of CHF 35bn required, and minimum Tier 1 capital of CHF 50bn 1) The binding constraint is determined as the worse of 3.5% of leverage exposure and 10% of RWA due to the anticipated TBTF requirement of 3.5% CET 1 leverage ratio and 10% CET 1 requirement 2) Reflects post-mitigation estimates of current expectations Note: New management structure effective October 22, 2015; Future numbers expected / illustrative CET1 capital ratio targeted to remain at ~11% afterimplementation of rules Standardized Approach to counterparty Credit Risk rules effective from January 1st, 2017; minimal impact expected Final Swiss TBTF rules expected imminentlySwiss TBTF rules anticipated to require 5% Tier 1 leverage ratio, and 3.5% CET1 leverage ratio CS targeting 5-6% Tier 1 leverage ratio by end 2017, of which 3.5-4.0% is expected to be met through common equity October 21, 2015

Improve our capital position 53 1 Internal capital generationRight-size the Investment BankReallocate capitalReduce fixed costsTransition non-core assets & implement closures Capital raising 2 October 21, 2015

Evolution of Credit Suisse Group operating expenses, in CHFbn In spite of our efforts, our total cost base has not significantly decreased in absolute terms 2013 2011 2010 2012 2014 54 1 Internal capital generationReduce fixed costs Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 October 21, 2015

Shared Services workforce increased by 6,000 FTE from 2011 to 2014 as growth in offshoring was not fully reflected in headcount reduction in the main operating centers Workforce outside CoEs2) Evolution of the Shared Services1) workforce (Employees & Contractors), in FTE 1) Includes all ShS (IT, Finance, Ops, Risk, GC, CRES, TB&C and non-Core ShS) 2) Includes employees, contractors, and outsourced workforce; Centers of Excellences include India, Wroclaw and Raleigh Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 Workforce at CoEs2) 34,800 2011 33,600 +6% 2014 39,500 35,000 2013 2012 55 CAGR 1 Internal capital generationReduce fixed costs October 21, 2015

1) Expected; 2) Includes LE program, IT architecture simplification, other corporate center programs and realignment costsNote: Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses in the SRU & restructuring costs, but including other costs to achieve savings; New management structure effective October 22, 2015 CHF 3.5bn in gross savings which, combined with the planned investments, is expected to lead to an absolute reduction in the cost base by a net CHF2bn to CHF19bn by end-2018 56 Invest in growth 18.5-19.0 2018cost base target +1.5 Business exits & run-down of additional SRU portfolio -1.3 -0.9 Workforce strategy, technology & London right-sizing -0.3 Run-down of SRU portfolio(planned run-down of prior NSU) -0.1 Wind-down of Corp. Center costs Substantial completion of Corp. Center programs2) -0.9 2015cost base1) 20.5-21.0 CHF -1.2bnpreviously planned cost reduction CHF -2.3bnadditional cost reduction 1 Internal capital generationReduce fixed costs CHF +1.5bninvestmentin growth Further cost savings intended beyond 2018 October 21, 2015

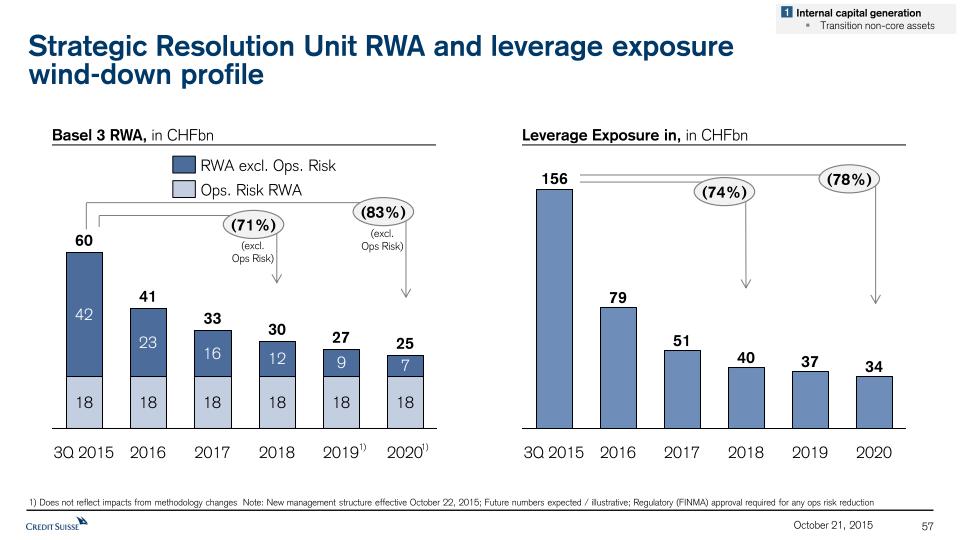

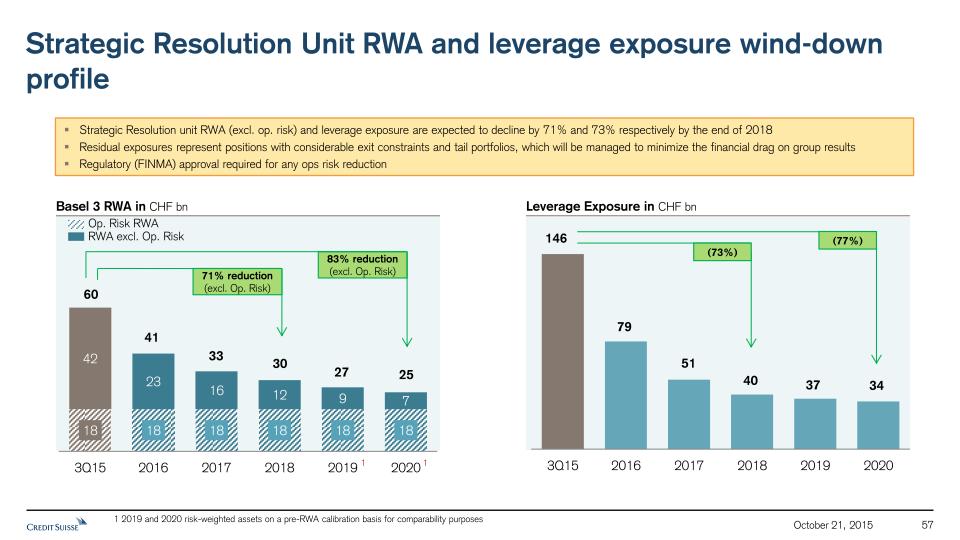

Basel 3 RWA, in CHFbn Leverage Exposure in, in CHFbn Strategic Resolution Unit RWA and leverage exposurewind-down profile 1) Does not reflect impacts from methodology changes Note: New management structure effective October 22, 2015; Future numbers expected / illustrative; Regulatory (FINMA) approval required for any ops risk reduction 1) 1) 57 3Q 2015 60 33 2016 41 25 2019 27 2018 30 2017 2020 Ops. Risk RWA RWA excl. Ops. Risk 2020 2019 2018 2017 2016 3Q 2015 (78%) (74%) (83%) (71%) (excl. Ops Risk) (excl. Ops Risk) 1 Internal capital generationTransition non-core assets October 21, 2015

Our current US Private Banking operation did not meet sufficient profitability and return criteria US Wealth Management market attractive, but requires appropriate business modelBrokerage model challenged as it requires scale and value accrues to brokers, not shareholders Decision taken to transition CS PB USNew coverage model focused on UHNWI to be introduced that integrates investment banking coverage and WM services Challenged CS PB US position despite improvements Cost / Income ratio (1H 2015) Assets under Management (USDtr, 1H2015) PB US Source: Company public disclosures 1) FYFC as of May 2015 Note: This slide presents financial information based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 Bubble size reflects AuM WM Americas 58 Approx. average non-US CS IWM CIR1) 1 Internal capital generationTransition non-core assets October 21, 2015

Streamlining Western Europe Footprint This will help to adjust our service model to client proposition Consolidate Booking Centers Develop Hub and Spoke Model Move Towards Advisory Office Model This is expected to deliver CHF 50-60mn annual cost reduction from booking center consolidation alone This will be achieved without impacting client service 59 1 Internal capital generationImplement closures October 21, 2015

We intend to execute a partial IPO2) (20 to 30% stake) of the Swiss Universal Bank1) by end of 2017 Partial IPO of Swiss Universal Bank1) Attractive, stable earnings stream to Swiss and international investorsValue of Swiss franchise highlightedTransparency and market discipline to support the delivery of profit growthIncentive alignment for management of legal entity Swiss Universal Bank1)Currency to take advantage of potential consolidation in the Swiss Private Banking marketControl retained by Credit Suisse Group 1) Legal entity Credit Suisse (Schweiz) AG2) Any such IPO would involve the sale of a minority stake and would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG 60 1 Internal capital generationReallocate capital October 21, 2015

Improve our capital position 61 1 Internal capital generationRight-size the Investment BankReallocate capitalReduce fixed costsTransition non-core assets & implement closures Capital raising 2 October 21, 2015

We have announced a CHF 4.70bn rights issue supplemented by a CHF 1.36bn non-preemptive placing Announced a non-preemptive placing of CHF 1.36bn to institutional investorsFirmly underwritten rights issue of CHF 4.70bn Total capital raise of CHF 6.0bn1) 62 Size Timing EGM approval 19th November with rights trading thereafter 2 Capital raising 1) Net of expenses Note: Subject to approval by EGM (EGM: Extraordinary General Meeting) October 21, 2015

1) Capital impact from targeted IPO of Credit Suisse (Schweiz) AG as well as disposal of non-core assets, does not include material capital impact / benefit from cost savings and exposure reductions; any such IPO would involve the sale of a minority stake and would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG 2) Free Capital generated 3) Including impact on capital applying RWA floors at 60% 4) Net of costs and including relating threshold impact for deferred tax assets; subject to approval by EGM (EGM: Extraordinary General Meeting) 5) Until we reach our capital target however, we will recommend CHF 0.70 per share with a scrip alternative; we will discontinue the scrip once we have clarity on regulatory requirements and litigation risks. In any event, we will not continue with the scrip beyond 2017 Note: Under the free capital generation concept, capital is calculated using 10% to convert RWA into capital and 3.5% for leverage exposure due to the anticipated TBTF requirement of 3.5% CET1 leverage ratio and 10% CET1 requirement; New management structure effective October 22, 2015 IPO & disposals1) CapitalRaise Capital raise plus IPO & disposals Targeted Operating FCG2)4Q15 to ‘20 Free Capital Generated Business moves & Asset disposals Regulatory and Capital Requirements FCG after businessmoves ®. req. Cash dividends accrued5) NetFCG2) OtherIssuances 63 2-4 6.54) 9-11 23-25 33-35 (1) (7)3) 25-27 ~(11) 14-16 0.5 At least 40% of Operating Free Capital generated planned to be returned to shareholders Returning capital to our shareholdersIllustrative 4Q2015 to 2020, in CHFbn October 21, 2015

Profitable Growth Capture the Wealth Management opportunity in Emerging Markets by accelerating growth in Asia Pacific and by replicating our successful model in other Emerging MarketsCreate a Swiss Universal Bank to expand our position with Swiss private, corporate and institutional clients and participate in domestic consolidation opportunitiesRight-size the Investment Bank to optimize its profitability and capital usage, reduce volatility of earnings and support Wealth Management customer needs Our Strategy – Profitable growth and capital generation Capitalgeneration Deliver ~CHF 23-25bn in Operating Free Capital Generation from 4Q2015 to end-2020, with at least 40% planned to be returned through dividends to shareholders1) 1) Until we reach our capital target however, we will recommend CHF 0.70 per share with a scrip alternative; we will discontinue the scrip once we have clarity on regulatory requirements and litigation risks. In any event, we will not continue with the scrip beyond 2017 64 October 21, 2015

65 A set of objectives to measure progress Key Metrics, in bn, in CHF unless otherwise specified 2018 target Capital SRU RWA wind-down (ex. OpRisk)Global Markets RWAGlobal Markets Leverage 421) USD ~83-85 (target)USD ~380 (target) 12USD ~83-85USD ~370 1) Number corresponds to the starting point of SRU as it is being established 2) Until we reach our capital target however, we will recommend CHF 0.70 per share with a scrip alternative; we will discontinue the scrip once we have clarity on regulatory requirements and litigation risks. In any event, we will not continue with the scrip beyond 2017 3) After regulatory recalibration in 2019 Note: All metrics on the side based on new organizational structure, new management structure effective October 22, 2015 APAC=Asia-Pacific IWM=International Wealth Management CHUB=Swiss Universal Bank 2014 2015 Profitable growth APAC PTIIWM PTICHUB PTIGroup Cost base 2.12.12.318.5-19.0 0.91.31.6 2018 target CHF 23bn to 25bn of Operating Free Capital generated (FCG) over 5 yearsAt least 40% of Operating FCG to be distributed to shareholders via dividends over the period2) CET1 capital ratio ~13% until 2018 and >11% thereafter3)CET1 leverage ratio above 3.5% October 21, 2015

In summary 66 This strategy will:Create value for our chosen customersPosition the bank well to deal with an uncertain environmentGenerate capital and reward our shareholders October 21, 2015

Appendix 68 October 21, 2015

Targeted and rational approach to right-sizing IB RWA breakdown in USDbn 1) Credit complex includes SP and GCP 2) Sourced from Credit Suisse Leveraged Finance Strategy 3) From 2014YE exposures Note: APAC IB included 69 BelowCoC 2Q 2015 158 126 AboveCoC Securi-tized products & Credit products1) Lower volatility and concentration risk through reduction of exposures: RWA down by 5% at Q4 20153)Leverage down by 25% at Q4 20153) 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 US HYSpread2) Indication of market volatility Credit Suisse PTI in CP and SP October 21, 2015

October 21, 2015 Credit Suisse StrategyOverview of Financials and CapitalDavid Mathers

Disclaimer (1/2) October 21, 2015 2 The 3Q15 financial information is subject to further review We have not finalized our 3Q15 Financial Report and our independent registered public accounting firm has not completed its review of the condensed consolidated financial statements (unaudited) for the period. Accordingly, the 3Q15 financial information contained in this presentation is subject to completion of quarter-end procedures, which may result in changes to that information. Certain reclassifications have been made to prior periods to conform to the current presentation.The re-segmented financial information is preliminary and subject to further review This presentation contains certain historical financial information that has been re-segmented to approximate what our results under our new structure would have been, had it been in place from January 1, 2014 (“Re-segmented Basis”). Such information is preliminary in nature and subject to review, evaluation and refinement, has not been audited or reviewed by our independent public accountants and can be expected to change in certain respects before any final re-segmentation is published. In addition, “Illustrative”, “Ambition” and “Goal” presentations are not intended to be viewed as targets or projections, nor are they considered to be Key Performance Indicators. All such presentations are subject to a large number of inherent risks, assumptions and uncertainties, many of which are completely outside of our control. Accordingly, this information should not be relied on for any purpose. We may not achieve the benefits of our strategic initiatives We may not achieve all of the expected benefits of our strategic initiatives. Factors beyond our control, including but not limited to the market and economic conditions, changes in laws, rules or regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives. Cautionary statement regarding forward -looking statements This presentation contains forward-looking statements that involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements. A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in "Risk Factors” in our Annual Report on Form 20-F for the fiscal year ended December 31, 2014 and in “Cautionary statement regarding forward-looking information" in our second quarter 2015 Financial Report filed with the US Securities and Exchange Commission, and in other public filings and press releases. We do not intend to update these forward-looking statements except as may be required by applicable law.

Disclaimer (2/2) October 21, 2015 3 Statement regarding capital, liquidity and leverage As of January 1, 2013, Basel 3 was implemented in Switzerland along with the Swiss “Too Big to Fail” legislation and regulations thereunder (in each case, subject to certain phase-in periods). As of January 1, 2015, the Bank for International Settlements (BIS) leverage ratio framework, as issued by the Basel Committee on Banking Supervision (BCBS), was implemented in Switzerland by FINMA. Our related disclosures are in accordance with our interpretation of such requirements, including relevant assumptions. Changes in the interpretation of these requirements in Switzerland or in any of our assumptions or estimates could result in different numbers from those shown in this presentation. Capital and ratio numbers for periods prior to 2013 are based on estimates, which are calculated as if the Basel 3 framework had been in place in Switzerland during such periods. Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. Leverage amounts for 4Q14, which are presented in order to show meaningful comparative information, are based on estimates which are calculated as if the BIS leverage ratio framework had been implemented in Switzerland at such time. Beginning in 2015, the Swiss leverage ratio is calculated as Swiss total capital, divided by period-end leverage exposure. The look-through BIS tier 1 leverage ratio and CET1 leverage ratio are calculated as look-through BIS tier 1 capital and CET1 capital, respectively, divided by end-period leverage exposure. Selling restrictions This document is not an offer to sell or a solicitation of offers to purchase or subscribe for securities of Credit Suisse Group AG. This document is not a prospectus within the meaning of article 652a of the Swiss Code of Obligations, nor is it a listing prospectus as defined in the listing rules of the SIX Swiss Exchange AG or any other exchange or regulated trading facility in Switzerland or a prospectus under any other applicable laws. Copies of this document may not be sent to jurisdictions, or distributed in or sent from jurisdictions, in which this is barred or prohibited by law. The information contained herein shall not constitute an offer to sell or the solicitation of an offer to buy, in any jurisdiction in which such offer or solicitation would be unlawful prior to registration, exemption from registration or qualification under the securities laws of any jurisdiction. A decision to invest in securities of Credit Suisse Group AG should be based exclusively on a written agreement with Credit Suisse Group AG or an offering and listing prospectus to be published by Credit Suisse Group AG for such purpose. This document and the information contained herein is not for publication or distribution into the United States of America and should not be distributed or otherwise transmitted into the United States or to U.S. persons (as defined in the U.S. Securities Act of 1933, as amended (the “Securities Act”)) or publications with a general circulation in the United States. This document does not constitute an offer or invitation to subscribe for or to purchase any securities in the United States of America. The securities referred to herein have not been and will not be registered under the Securities Act or the laws of any state and may not be offered or sold in the United States of America absent registration or an exemption from registration under Securities Act. There will be no public offering of the securities in the United States of America. The information contained herein does not constitute an offer of securities to the public in the United Kingdom. No prospectus offering securities to the public will be published in the United Kingdom. This document is only being distributed to and is only directed at (i) persons who are outside the United Kingdom or (ii) to investment professionals falling within article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the “Order”) or (iii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within article 49(2)(a) to (d) of the Order (all such persons together being referred to as “relevant persons”). The securities are only available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such securities will be engaged in only with, relevant persons. Any person who is not a relevant person should not act or rely on this document or any of its contents.

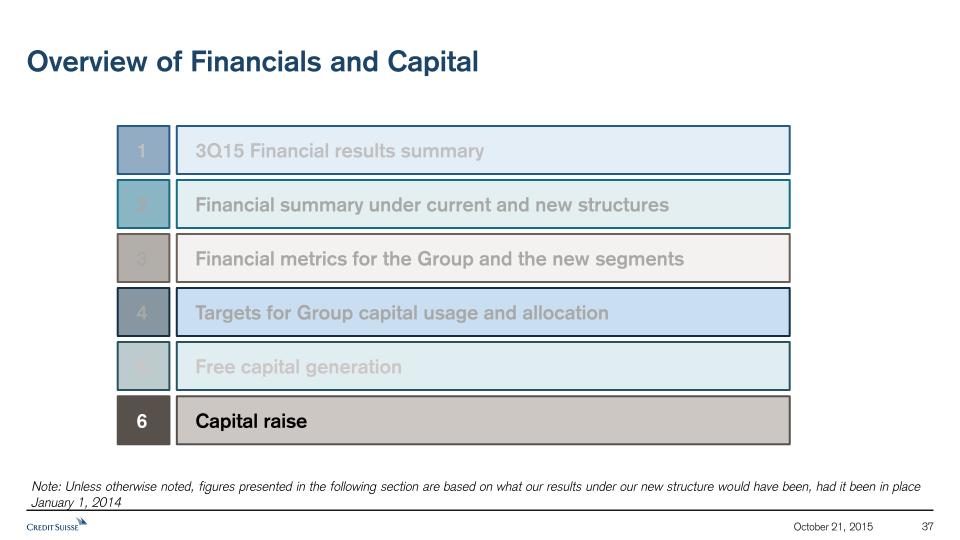

Overview of Financials and Capital October 21, 2015 4 3Q15 Financial results summary 1 Financial summary under current and new structures 2 Financial metrics for the Group and the new segments 3 Targets for Group capital usage and allocation 4 Free capital generation 5 Capital raise 6 Note: Unless otherwise noted, figures presented in the following section are based on results under our current structure prior to our re-segmentation announcement on October 21, 2015 ("Current Reporting Basis")

5 Clear alignment of strategic and financial goals Strategic goals Financial goals in CHF bn Increase the profitability of the stable and high return cash flows in Swiss home market Optimize resource allocation and focus on high-returning businesses with scale Increase resource allocation to APAC and other fee generative and growth areas Achieve CHF 2 bn1 of net cost reductions by end-2018, primarily related to fixed cost base Strengthen equity capital base with focus on maximizing free capital generation Swiss home market Optimize resource allocation Focus on growth areas and recurring fee generation Reduce fixed cost base Strengthen capital base Group operating cost base End-2018 capital ratio targets Swiss Universal Bank Pre-tax income APAC Pre-tax income Risk-weighted assets, ex. CC / ShS 3Q15CurrentStructure 133% ~13% 5 - 6% October 21, 2015 44% Strategic IB57% Strategic PB&WM38% Non-Strategic5% 3Q15 results Financial summary Financial targets Capital targets Free capital gen. 2 bn Capital raise Notes: This slide presents financial information on both a Current Reporting Basis and Re-segmentation Basis. CHUB = Swiss Universal Bank; IWM = International Wealth Management; GM = Global Markets; IBCM = Investment Banking and Capital Markets; APAC = Asia Pacific; SRU = Strategic Resolution Unit; CC = Corporate Center; ShS = Shared Services for this slide and the rest of the presentation 1 Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses in the SRU & restructuring costs, but including other costs to achieve savings IBXX% SRU10% Swiss UB25% IWM16% APAC16% GM27% IBCM7% 20.5-21.0 18.5-19.0 2018ENewStructure

Key messages from Credit Suisse 3Q15 results October 21, 2015 6 3Q15 results Financial summary Financial targets Capital targets APAC3Q15 pre-tax income of CHF 256 mn 9M15 pre-tax income of CHF 1,129 mn with 48% YoY increase, benefitting from continued momentum of our One Bank franchise; 3Q15 pre-tax income of CHF 256 mnWealth Management Clients Asia Pacific with double-digit growth in net new assets in both 3Q15 and 9M159M15 Asia Pacific Investment Banking revenues increase of 15%, driven by robust equities results with 40% YoY revenue growth Progress on capital “Look-through” CET1 ratio of 10.2%, down from 10.3% at 2Q15, with RWA increases from model updates and methodology changes“Look-through” Swiss Total Leverage ratio of 4.5%, of which BIS Tier 1 Leverage ratio of 3.9% and CET1 Leverage ratio of 2.8% Free capital gen. Credit Suisse Group3Q15 pre-tax income of CHF 861 mn and return on equity of 7% Group pre-tax income (excluding revenue impact from fair value on own debt) of CHF 238 mn. The significant YoY and QoQ reduction in pre-tax income was driven by lower results in Investment Banking, primarily due to a challenging market environment and lower client activity. Group Strategic pre-tax income for the quarter of CHF 826 mn, a 49% decrease from 3Q149M15 return on equity of 9% (or 6% excluding revenue impact from fair value on own debt); 11% for the Strategic business Capital raise Note: Credit Suisse Group reflects Core results; 3Q15 and 9M15 results based on current reporting structure

Key messages from Credit Suisse 3Q15 results October 21, 2015 7 1 Adjusted for Swisscard deconsolidation. See slide 10 in 3Q15 earnings presentation for details 2 3Q15 results include the impact of the USD 133 mn settlement to resolve a lawsuit related to credit-default swaps Strategic pre-tax income of USD 291 mn significantly lower QoQ and YoY, primarily due to lower fixed income franchise results driven by significantly muted client activity amid challenging market conditions Reduction in leverage exposure to USD 615 bn; early achievement of USD 600-620 bn year-end targetHigher equity sales and trading performance as increased market volatility led to higher client activityUnderwriting and advisory revenues negatively impacted by slowdown in industry-wide issuance; continued share gains in M&A franchise Investment Banking3Q15 pre-tax income of CHF (125) mn2 Private Banking & Wealth Management3Q15 pre-tax income of CHF 647 mn and return on reg. capital of 16% Strategic pre-tax income of CHF 753 mn and Strategic return on regulatory capital of 20%, impacted by weaker client activity and adverse market conditionsWealth Management Clients with growth in net interest income and recurring commissions and fees1 since the beginning of 2015; 3Q15 pre-tax income impacted by lower transaction revenues; 9M15 net margin of 28 bps compared to 27 bps for 9M14 Corporate & Institutional Clients delivered solid net revenues with cost income ratio of 50% in 9M15; lower pre-tax income due to increased credit provisionsAsset Management with growth in fee-based revenues since the beginning of 2015; 3Q15 net revenues impacted by investment-related losses due to market conditionsStrong strategic net new assets of CHF 17.3 bn with contribution from all three businesses; Wealth Management Clients reported net new assets of CHF 10.5 bn with growth in all regions and good contribution from UHNWI client segment 3Q15 results Financial summary Financial targets Capital targets Free capital gen. Capital raise

Results Overview 8 Note: Total Reported reflects Core Results; FVoD denotes Fair Value on own Debt on this slide and throughout the rest of the presentation 1 Return on Equity for Strategic results calculated by dividing annualized Strategic net income by average Strategic shareholders' equity (derived by deducting 10% of Non-Strategic RWA from reported shareholders' equity) 2 Assumes assets managed across businesses relate to Strategic businesses only 3 Excludes revenue impact from FVoD of CHF 623 mn, CHF 228 mn, CHF 318 mn, CHF 995 mn and CHF 246 mn in 3Q15, 2Q15, 3Q14, 9M15 and 9M14, respectively, and pre-tax charge of CHF 1,618 mn relating to the settlements with US authorities regarding the US cross-border matters in 9M14, in Non-Strategic and total reported results in CHF mn 3Q15 2Q15 3Q14 9M15 9M14Net revenues 5,623 6,758 6,287 18,971 19,126Pre-tax income 826 1,812 1,622 4,460 5,341Cost / income ratio 84% 73% 73% 76% 72%Return on equity1 7% 14% 11% 11% 13%Net new assets2 in CHF bn 17.3 15.4 8.8 51.1 36.6 Net revenues 5,982 6,941 6,537 19,596 19,439Pre-tax income 861 1,646 1,301 4,045 2,331 Pre-tax income ex FVoD and settlement impact3 238 1,418 983 3,050 3,703Net income attributable to shareholders 779 1,051 1,025 2,884 1,184Diluted earnings per share in CHF 0.45 0.61 0.61 1.69 0.68Return on equity 7% 10% 10% 9% 4% Return on equity ex FVoD and settlement impact3 2% 8% 7% 6% 8% Net revenues 359 183 250 625 313Pre-tax income / (loss) 35 (166) (321) (415) (3,010) Pre-tax income / (loss) ex FVoD and settlement impact3 (588) (394) (639) (1,410) (1,638) Strategic Non-Strategic Total Reported 3Q15 results Financial summary Financial targets Capital targets Free capital gen. Capital raise October 21, 2015

Overview of Financials and Capital October 21, 2015 9 3Q15 Financial results summary 1 Financial summary under current and new structures 2 Financial metrics for the Group and the new segments 3 Targets for Group capital usage and allocation 4 Free capital generation 5 Capital raise 6 Note: Unless otherwise noted, figures presented in the following section are based on what our results under our new structure would have been, had it been in place January 1, 2014

October 21, 2015 10 Corporate Center Strategic Resolution Unit Separate division of the Group with clear accountability, governance and reporting, established to:Facilitate immediate right-sizing of Investment Banking and focus on rapid wind-down of non-core assets, including those within the current Non-Strategic unitsAchieve these objectives by taking over the exposures that do not fit with the parameters of the right-sized Investment Banking or strategic goals of other business divisionsProvide platform for restructuring of client centric and strategic but capital inefficient businesses Corporate Center will be presented inclusive of overall costs of shared services, providing transparency of the pre- and post-allocated view of these costsResidual Corporate Center financial results will primarily comprise the central corporate costs, the legal entity program and a modest amount of accounting asymmetry Restructuring of divisions Reflecting the new management structure, Credit Suisse’s financial reporting structure will be presented as six reporting segments, including a new Strategic Resolution Unit, with a much simplified Corporate Center Alignment of financial reporting to new management structure 3Q15 results Financial summary Financial targets Capital targets Free capital gen. Capital raise InternationalWealth Management Investment Banking and Capital Markets Swiss Universal Bank Corporate Center Strategic Resolution Unit Global Markets Asia Pacific Credit Suisse Core results New management structure effective October 22, 2015 and will be the basis for our reporting in the fourth quarter of 2015 and the 2015 Annual Report, and going forward

Overview of changes in structure – Private Banking & Wealth Mgmt. October 21, 2015 11 PTI: 1,378 mnRWA: 33 bnLev.: 74 bn PTI: (1,473) mnRWA: 11 bnLev.: 27 bn Full year 2014 in CHF PTI: 3,726 mnRWA: 102 bnLev.: 369 bn PTI: (1,638) mnRWA: 6 bnLev.: 11 bn 3Q15 results Financial summary Financial targets Capital targets Free capital gen. Capital raise PTI: 357 mnRWA: 7 bnLev.: 34 bn PTI: 1,826 mnRWA: 57 bnLev.: 245 bn Investment Banking Strategic Non-Strategic Private Banking & Wealth Management Strategic Non-Strategic Strategic Non-Strategic Corporate Center InternationalWealth Management Investment Banking and Capital Markets Corporate Center Asia Pacific Swiss Universal Bank Strategic Resolution Unit Global Markets PTI = Pre-tax income RWA = Risk-weighted Assets Lev. = Swiss Leverage Exposure

Overview of changes in structure – Investment Banking October 21, 2015 12 PTI: 2,795 mnRWA: 75 bnLev.: 479 bn PTI: 661 mnRWA: 14 bnLev.: 97 bn PTI: (2,231) mnRWA: 55 bnLev.: 166 bn 3Q15 results Financial summary Financial targets Capital targets Free capital gen. Capital raise PTI: 559 mnRWA: 16 bnLev.: 41 bn Investment Banking Strategic Non-Strategic Private Banking & Wealth Management Strategic Non-Strategic Strategic Non-Strategic Corporate Center PTI: 3,744 mnRWA: 150 bnLev.: 722 bn PTI: (1,914) mnRWA: 10 bnLev.: 64 bn InternationalWealth Management Investment Banking and Capital Markets Corporate Center Asia Pacific Swiss Universal Bank Global Markets Full year 2014 in CHF Strategic Resolution Unit PTI = Pre-tax income RWA = Risk-weighted Assets Lev. = Swiss Leverage Exposure PTI: 46 mnRWA: 1 bnLev.: 3 bn

Overview of changes in structure – Corporate Center October 21, 2015 13 InternationalWealth Management Investment Banking and Capital Markets Corporate Center Asia Pacific PTI: (105) mnRWA: -Lev.: - PTI: (419) mnRWA: -Lev.: - PTI: 44 mn1RWA: 16 bnLev.: 32 bn PTI: (251) mnRWA: -Lev.: - PTI: (78) mnRWA: -Lev.: - PTI: 167 mnRWA: -Lev.: - 3Q15 results Financial summary Financial targets Capital targets Free capital gen. Capital raise Swiss Universal Bank Strategic Resolution Unit Global Markets PTI: (44) mnRWA: -Lev.: - Investment Banking Strategic Non-Strategic Private Banking & Wealth Management Strategic Non-Strategic Strategic Non-Strategic Corporate Center PTI = Pre-tax income RWA = Risk-weighted Assets Lev. = Swiss Leverage Exposure 1 Includes impact from FVoD of CHF 543 mn Full year 2014 in CHF PTI: (680) mnRWA: 16 bnLev.: 32 bn PTI: (6) mn1RWA: -Lev.: -

Financial summary under new structure October 21, 2015 14 3Q15 results Financial summary Financial targets Capital targets Free capital gen. Capital raise SwissUniversal Bank Pre-tax Income/ (Loss) 2014 1.6 - o/w Non-Strat.litigations Basel 3 RWA LeverageExposure3 In CHF bn InternationalWM Global Markets Asia Pacific Strategic Resolution Unit Corporate Center Credit Suisse Group1 2014 1.3 - 2014 2.4 - 2014 0.9 - 2014 (3.1) (2.4) 2014 0.0 - 2014 3.6 (2.4) 13 “Worst of” RoC / RoE (%)2 58 33 75 22 66 16 284 248 74 479 131 194 32 1,198 27 10 14 4 Credit Suisse Core results 2014 13 Credit Suisse Core 6.8 - 219 1,005 1 The difference between Credit Suisse Core results (under current structure) and Credit Suisse Group results (under new structure) includes certain entities in which we had no significant economic interest in the unit 2 Division and Credit Suisse Core RoC (return on regulatory capital) is the worst of return on 10% of spot RWA and return on 3.5% of spot Swiss leverage exposure; assumes tax rate of 30% in 2014. RoE (return on equity) calculated for Credit Suisse Group 3 Swiss leverage exposure 0.5 (0.5) CC excl. FVoD FVoD Notes: On this slide and for the rest of the presentation, “worst of” return on capital / equity is based on capital calculated with the binding constraint determined by the worse of 3.5% of leverage exposure and 10% of RWA due to the anticipated TBTF requirement of 3.5% CET1 leverage ratio and 10% CET1 requirement IBCM 2014 0.5 - 16 41 23

Overview of Financials and Capital October 21, 2015 15 3Q15 Financial results summary 1 Financial summary under current and new structures 2 Financial metrics for the Group and the new segments 3 Targets for Group capital usage and allocation 4 Free capital generation 5 Capital raise 6 Note: Unless otherwise noted, figures presented in the following section are based on what our results under our new structure would have been, had it been in place January 1, 2014

16 Clear alignment of strategic and financial goals Strategic goals Financial goals in CHF bn Increase the profitability of the stable and high return cash flows in Swiss home market Optimize resource allocation and focus on high-returning businesses with scale Increase resource allocation to APAC and other fee generative and growth areas Achieve CHF 2 bn1 of net cost reductions by end-2018, primarily related to fixed cost base Strengthen equity capital base with focus on maximizing free capital generation Swiss home market Optimize resource allocation Focus on growth areas and recurring fee generation Reduce fixed cost base Strengthen capital base Group operating cost base End-2018 capital ratio targets Swiss Universal Bank Pre-tax income APAC Pre-tax income Risk-weighted assets, ex. CC / ShS 3Q15CurrentStructure 133% 5 - 6% October 21, 2015 44% Strategic IB57% Strategic PB&WM38% Non-Strategic5% 3Q15 results Financial summary Financial targets Capital targets Free capital gen. 2 bn Capital raise 1 Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses in the SRU & restructuring costs, but including other costs to achieve savings IBXX% SRU10% CHUB25% IWM16% APAC16% GM27% IBCM7% ~13% 2018ENewStructure