Form 8-K NAVISTAR INTERNATIONAL For: Jun 04

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): June 4, 2015

NAVISTAR INTERNATIONAL CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 1-9618 | 36-3359573 | ||

| (State or other jurisdiction of incorporation or organization) |

(Commission File No.) |

(I.R.S. Employer Identification No.) | ||

| 2701 Navistar Drive Lisle, Illinois |

60532 | |||

| (Address of principal executive offices) | (Zip Code) | |||

Registrant’s telephone number, including area code (331) 332-5000

(Former name or former address, if changed since last report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| ITEM 2.02 | RESULTS OF OPERATIONS AND FINANCIAL CONDITION |

In accordance with General Instruction B.2. to Form 8-K, the following information shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, except as shall be expressly set forth by specific reference in such a filing.

The information regarding the results of operations and financial condition of Navistar International Corporation (the “Company”) responsive to this Item 2.02, and contained in Exhibit 99.1 filed herewith, is incorporated into this Item 2.02 by reference.

| ITEM 7.01 | REGULATION FD DISCLOSURE |

In accordance with General Instruction B.2. to Form 8-K, the following information shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, except as shall be expressly set forth by specific reference in such a filing.

On June 4, 2015, the Company filed its Quarterly Report on Form 10-Q for the period ended April 30, 2015 with the Securities and Exchange Commission. The Company’s press release announcing the filing is attached as Exhibit 99.1 to this Current Report and is incorporated by reference herein.

The Company, which is one of the largest combined commercial truck, school bus and mid-range diesel engine producers, will present via live web cast its fiscal 2015 second quarter financial results on Thursday, June 4th. A live web cast is scheduled at approximately 9:00 AM Eastern. Speakers on the web cast will include: Troy Clarke, President and Chief Executive Officer; Walter Borst, Executive Vice President and Chief Financial Officer; and other company leaders. A copy of the slides containing financial and operating information to be used as part of the web cast are attached as Exhibit 99.2 to this Current Report and are incorporated by reference herein.

The web cast can be accessed through a link on the investor relations page of Company’s web site at http://www.navistar.com/navistar/investors/webcasts. Investors are advised to log on to the website at least 15 minutes prior to the start of the web cast to allow sufficient time for downloading any necessary software. The web cast will be available for replay at the same address approximately three hours following its conclusion, and will remain available for a period of at least 12 months.

Navistar International Corporation (NYSE: NAV) is a holding company whose subsidiaries and affiliates produce International® brand commercial and military trucks, MaxxForce® brand diesel engines, and IC Bus™ brand school and commercial buses. The Company also provides truck and diesel engine service parts. Another affiliate offers financing services. Additional information is available at www.Navistar.com.

ITEM 9.01. FINANCIAL STATEMENTS AND EXHIBITS

(d) Exhibits.

The following documents are filed herewith:

| Exhibit No. |

Description | |

| 99.1 | Press Release. | |

| 99.2 | Slide Presentation for Second Quarter 2015 Financial Results Web Cast to be held on June 4, 2015. | |

Forward Looking Statements

Information provided and statements contained in this report that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. Such forward-looking statements only speak as of the date of this report and the Company assumes no obligation to update the information included in this report. Such forward-looking statements include information concerning our possible or assumed future results of operations, including descriptions of our business strategy. These statements often include words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” or similar expressions. These statements are not guarantees of performance or results and they involve risks, uncertainties, and assumptions. For a further description of these factors, see the risk factors set forth in our filings with the Securities and Exchange Commission, including our annual report on Form 10-K for the fiscal year ended October 31, 2014 and our quarterly report on Form 10-Q for the quarter ended April 30, 2015. Although we believe that these forward-looking statements are based on reasonable assumptions, there are many factors that could affect our actual financial results or results of operations and could cause actual results to differ materially from those in the forward-looking statements. All future written and oral forward-looking statements by us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to above. Except for our ongoing obligations to disclose material information as required by the federal securities laws, we do not have any obligations or intention to release publicly any revisions to any forward-looking statements to reflect events or circumstances in the future or to reflect the occurrence of unanticipated events.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| NAVISTAR INTERNATIONAL CORPORATION (Registrant) | ||

| By: | /s/ WALTER G. BORST | |

| Name: | Walter G. Borst | |

| Title: |

Executive Vice President and Chief Financial Officer | |

Dated: June 4, 2015

EXHIBIT INDEX

| Exhibit No. |

Description | |

| 99.1 | Press Release. | |

| 99.2 | Slide Presentation for Second Quarter 2015 Financial Results Web Cast to be held on June 4, 2015. | |

Exhibit 99.1

|

Navistar International Corporation 2701 Navistar Dr. Lisle, IL 60532 USA P: 331-332-5000 W: navistar.com |

| Media contact: | Steve Schrier, 331-332-2264 | |

| Investor contact: | Kevin Sadowski, 331-332-2406 | |

| Web site: | www.Navistar.com/newsroom |

NAVISTAR REPORTS SECOND QUARTER RESULTS

| • | Reports net loss of $64 million, or $0.78 per share, on revenues of $2.7 billion |

| • | Generates $102 million of adjusted EBITDA in the quarter |

| • | Chargeouts up 38 percent vs. last quarter; up 10 percent year-over-year |

| • | Ends quarter with $784 million in manufacturing cash on positive cash flow for the quarter |

| • | Expects to achieve in excess of 8 percent EBITDA margin run rate exiting FY2015 |

| • | Forecasts FY2016 industry retail deliveries of Class 6-8 trucks and buses in the United States and Canada to be in the same range as FY2015—350,000 to 380,000 units |

LISLE, Ill. — June 4, 2015 — Navistar International Corporation (NYSE: NAV) today announced a second quarter 2015 net loss of $64 million, or $0.78 per diluted share, compared to a second quarter 2014 net loss of $297 million, or $3.65 per diluted share. Revenues in the quarter were $2.7 billion. Chargeouts in the company’s core markets (Class 6-8 trucks and buses in the United States and Canada) were up 38 percent over last quarter.

Second quarter 2015 EBITDA was $85 million versus an EBITDA loss of $119 million in the same period one year ago. The $204 million year-over-year improvement was driven by an increase in truck segment sales, favorable product mix and the continuation of lower warranty expense and cost reductions. Prior year results included $149 million in asset impairment charges related to the company’s South American engine operations.

Second quarter 2015 adjusted EBITDA was $102 million compared to $82 million in the second quarter of 2014. The second quarter included one-time net charges of $17 million, compared to one-time charges of $201 million in the second quarter of 2014.

The company was cash flow positive in the second quarter 2015 and finished the quarter with $784 million in manufacturing cash, cash equivalents and marketable securities.

“Our results reflect continued progress in improving enterprise-wide business operations and positive momentum in the North American industry,” said Troy A. Clarke, Navistar president and chief executive officer. “We continue to make solid improvements in our North American truck and parts businesses and are especially encouraged by the progress in our bus business as well as increased market share in our medium-duty business where we saw significant improvement in sales to major rental and leasing fleets and strong results in dealer-led sales.”

Highlights from the quarter include a 10 percent year-over-year increase in chargeouts in the company’s core markets (Class 6-8 trucks and buses in the United States and Canada). This included a 24 percent increase in Class 6 and 7 medium trucks and a 9 percent increase in combined Class 8 trucks.

During the quarter, the company continued its best-in-class technology integration strategy with its first-to-market announcement of Bendix® Wingman® Fusion®—the industry’s most advanced safety system—available on the company’s International® brand Class 8 on-highway tractors.

In addition, the company continued its mission to be the ‘Uptime’ leader in the industry with the purchase of a test track and proving grounds in New Carlisle, Ind. The Navistar Proving Grounds is a key strategic addition to the company’s product development operations, allowing for comprehensive testing and validation of new vehicles and innovative technologies. The site will also be used as a customer center to showcase new products and give customers an opportunity to experience new products firsthand.

The company continued to take actions to reduce fixed costs and improve its manufacturing capacity utilization with the sale of its foundry operations in Waukesha, Wis. Navistar will complete its exit from the foundry business as operations in Indianapolis wind down by the end of the summer. As a result, the company anticipates more than $13 million in annual savings.

The company provided the following guidance for the third quarter:

| • | Q3-2015 EBITDA of $125 million – $175 million, excluding pre-existing warranty and one-time items. |

| • | Q3-2015 manufacturing cash, cash equivalents and marketable securities between $750 million – $850 million. |

Additionally, the company projects a continued strong North American industry for FY2016 with retail deliveries of Class 6-8 trucks and buses in the United States and Canada to be in the same range as FY2015— 350,000 to 380,000 units—with a stronger mix of school buses and medium-duty trucks.

“We continue to take the right actions to improve the business and expect to achieve in excess of an 8 percent EBITDA margin run rate as we exit the year,” Clarke added. “We think 2016 will be another strong year for the North American industry and we believe we’re well positioned to take advantage of favorable market conditions for our core businesses.”

Summary of Financial Results:

| (Unaudited) | ||||||||||||||||

| Second Quarter | First Half | |||||||||||||||

| (in millions, except per share data) | 2015 | 2014 | 2015 | 2014 | ||||||||||||

| Sales and revenues, net |

$ | 2,693 | $ | 2,746 | $ | 5,114 | $ | 4,954 | ||||||||

| Segment Results: |

||||||||||||||||

| Truck |

$ | (51 | ) | $ | (129 | ) | $ | (69 | ) | $ | (337 | ) | ||||

| Parts |

133 | 133 | 278 | 241 | ||||||||||||

| Global Operations |

1 | (162 | ) | (14 | ) | (197 | ) | |||||||||

| Financial Services |

22 | 24 | 46 | 47 | ||||||||||||

| Loss from continuing operations, net of tax(A) |

$ | (64 | ) | $ | (298 | ) | $ | (106 | ) | $ | (547 | ) | ||||

| Net loss(A) |

(64 | ) | (297 | ) | (106 | ) | (545 | ) | ||||||||

| Diluted loss per share from continuing operations(A) |

$ | (0.78 | ) | $ | (3.66 | ) | $ | (1.30 | ) | $ | (6.73 | ) | ||||

| Diluted loss per share(A) |

$ | (0.78 | ) | $ | (3.65 | ) | $ | (1.30 | ) | $ | (6.70 | ) | ||||

| (A) | Amounts attributable to Navistar International Corporation. |

Truck Segment — For the second quarter 2015, the Truck segment recorded a loss of $51 million, compared with a year-ago second quarter loss of $129 million. The Truck segment’s year-over-year improvement was driven by increased chargeouts, improved product costs and lower charges for adjustments to pre-existing warranties—reflecting quality improvements in recent model years and continued efforts to reduce overall cost per repair.

Parts Segment — For the second quarter 2015, the Parts segment recorded a profit of $133 million, flat compared to second quarter 2014. Sales and margin improvements in North American commercial markets were offset by a decrease in export and Blue Diamond Parts sales.

Global Operations Segment — For the second quarter 2015, the Global Operations segment recorded a profit of $1 million compared to a year-ago second quarter loss of $162 million. The year-over-year improvement was primarily due to one-time non-cash asset impairment charges that occurred in the second quarter of 2014. The remaining improvements in segment loss were primarily due to lower manufacturing and structural costs as a result of restructuring and cost-reduction efforts.

Financial Services Segment — For the second quarter 2015, the Financial Services segment recorded a profit of $22 million compared to second quarter 2014 profit of $24 million, reflecting an increase in revenue that was more than offset by a higher provision for loan losses in Mexico and lower income from intercompany loans.

About Navistar

Navistar International Corporation (NYSE: NAV) is a holding company whose subsidiaries and affiliates produce International® brand commercial and military trucks, proprietary diesel engines, and IC Bus™ brand school and commercial buses. An affiliate also provides truck and diesel engine service parts. Another affiliate offers financing services. Additional information is available at www.Navistar.com.

Forward-Looking Statement

Information provided and statements contained in this report that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. Such forward-looking statements only speak as of the date of this report and the company assumes no obligation to update the information included in this report. Such forward-looking statements include information concerning our possible or assumed future results of operations, including descriptions of our business strategy. These statements often include words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” or similar expressions. These statements are not guarantees of performance or results and they involve risks, uncertainties, and assumptions. For a further description of these factors, see the risk factors set forth in our filings with the Securities and Exchange Commission, including our annual report on Form 10-K for the fiscal year ended October 31, 2014 and our quarterly report on Form 10Q for the quarter ended April 30, 2015. Although we believe that these forward-looking statements are based on reasonable assumptions, there are many factors that could affect our actual financial results or results of operations and could cause actual results to differ materially from those in the forward-looking statements. All future written and oral forward-looking statements by us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to above. Except for our ongoing obligations to disclose material information as required by the federal securities laws, we do not have any obligations or intention to release publicly any revisions to any forward-looking statements to reflect events or circumstances in the future or to reflect the occurrence of unanticipated events.

Navistar International Corporation and Subsidiaries

Consolidated Statements of Operations

(Unaudited)

| Three Months | Six Months | |||||||||||||||

| Ended April 30, | Ended April 30, | |||||||||||||||

| (in millions, except per share data) | 2015 | 2014 | 2015 | 2014 | ||||||||||||

| Sales and revenues |

||||||||||||||||

| Sales of manufactured products, net |

$ | 2,658 | $ | 2,708 | $ | 5,043 | $ | 4,877 | ||||||||

| Finance revenues |

35 | 38 | 71 | 77 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Sales and revenues, net |

2,693 | 2,746 | 5,114 | 4,954 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Costs and expenses |

||||||||||||||||

| Costs of products sold |

2,360 | 2,468 | 4,405 | 4,482 | ||||||||||||

| Restructuring charges |

6 | 8 | 9 | 11 | ||||||||||||

| Asset impairment charges |

1 | 151 | 8 | 169 | ||||||||||||

| Selling, general and administrative expenses |

243 | 237 | 484 | 476 | ||||||||||||

| Engineering and product development costs |

76 | 83 | 155 | 173 | ||||||||||||

| Interest expense |

75 | 74 | 152 | 156 | ||||||||||||

| Other (income) expense, net |

(28 | ) | (8 | ) | (31 | ) | 6 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total costs and expenses |

2,733 | 3,013 | 5,182 | 5,473 | ||||||||||||

| Equity in income of non-consolidated affiliates |

1 | 3 | 3 | 3 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss from continuing operations before income taxes |

(39 | ) | (264 | ) | (65 | ) | (516 | ) | ||||||||

| Income tax expense |

(18 | ) | (23 | ) | (25 | ) | (11 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss from continuing operations |

(57 | ) | (287 | ) | (90 | ) | (527 | ) | ||||||||

| Income from discontinued operations, net of tax |

— | 1 | — | 2 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss |

(57 | ) | (286 | ) | (90 | ) | (525 | ) | ||||||||

| Less: Net income attributable to non-controlling interests |

7 | 11 | 16 | 20 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss attributable to Navistar International Corporation |

$ | (64 | ) | $ | (297 | ) | $ | (106 | ) | $ | (545 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Amounts attributable to Navistar International Corporation common shareholders: |

||||||||||||||||

| Loss from continuing operations, net of tax |

$ | (64 | ) | $ | (298 | ) | $ | (106 | ) | $ | (547 | ) | ||||

| Income from discontinued operations, net of tax |

— | 1 | — | 2 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss |

$ | (64 | ) | $ | (297 | ) | $ | (106 | ) | $ | (545 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) per share: |

||||||||||||||||

| Basic: |

||||||||||||||||

| Continuing operations |

$ | (0.78 | ) | $ | (3.66 | ) | $ | (1.30 | ) | $ | (6.73 | ) | ||||

| Discontinued operations |

— | 0.01 | — | 0.03 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | (0.78 | ) | $ | (3.65 | ) | $ | (1.30 | ) | $ | (6.70 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted: |

||||||||||||||||

| Continuing operations |

$ | (0.78 | ) | $ | (3.66 | ) | $ | (1.30 | ) | $ | (6.73 | ) | ||||

| Discontinued operations |

— | 0.01 | — | 0.03 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | (0.78 | ) | $ | (3.65 | ) | $ | (1.30 | ) | $ | (6.70 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average shares outstanding: |

||||||||||||||||

| Basic |

81.6 | 81.4 | 81.5 | 81.3 | ||||||||||||

| Diluted |

81.6 | 81.4 | 81.5 | 81.3 | ||||||||||||

Navistar International Corporation and Subsidiaries

Consolidated Balance Sheets

| April 30, | October 31, | |||||||

| 2015 | 2014 | |||||||

| (in millions, except per share data) | (Unaudited) | |||||||

| ASSETS |

||||||||

| Current assets |

||||||||

| Cash and cash equivalents |

$ | 583 | $ | 497 | ||||

| Restricted cash and cash equivalents |

— | 40 | ||||||

| Marketable securities |

273 | 605 | ||||||

| Trade and other receivables, net |

502 | 553 | ||||||

| Finance receivables, net |

1,929 | 1,758 | ||||||

| Inventories |

1,245 | 1,319 | ||||||

| Deferred taxes, net |

38 | 55 | ||||||

| Other current assets |

206 | 186 | ||||||

|

|

|

|

|

|||||

| Total current assets |

4,776 | 5,013 | ||||||

| Restricted cash |

113 | 131 | ||||||

| Trade and other receivables, net |

18 | 25 | ||||||

| Finance receivables, net |

225 | 280 | ||||||

| Investments in non-consolidated affiliates |

68 | 73 | ||||||

| Property and equipment (net of accumulated depreciation and amortization of $2,590 and $2,535, respectively) |

1,407 | 1,562 | ||||||

| Goodwill |

38 | 38 | ||||||

| Intangible assets (net of accumulated amortization of $113 and $109, respectively) |

74 | 90 | ||||||

| Deferred taxes, net |

134 | 145 | ||||||

| Other noncurrent assets |

72 | 86 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 6,925 | $ | 7,443 | ||||

|

|

|

|

|

|||||

| LIABILITIES and STOCKHOLDERS’ DEFICIT |

||||||||

| Liabilities |

||||||||

| Current liabilities |

||||||||

| Notes payable and current maturities of long-term debt |

$ | 1,211 | $ | 1,295 | ||||

| Accounts payable |

1,450 | 1,564 | ||||||

| Other current liabilities |

1,345 | 1,372 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

4,006 | 4,231 | ||||||

| Long-term debt |

3,992 | 3,929 | ||||||

| Postretirement benefits liabilities |

2,770 | 2,862 | ||||||

| Deferred taxes, net |

14 | 14 | ||||||

| Other noncurrent liabilities |

887 | 1,025 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

11,669 | 12,061 | ||||||

| Redeemable equity securities |

1 | 2 | ||||||

| Stockholders’ deficit |

||||||||

| Series D convertible junior preference stock |

3 | 3 | ||||||

| Common stock (86.8 shares issued, and $0.10 par value per share and 220 shares authorized, all at both dates) |

9 | 9 | ||||||

| Additional paid-in capital |

2,498 | 2,500 | ||||||

| Accumulated deficit |

(4,788 | ) | (4,682 | ) | ||||

| Accumulated other comprehensive loss |

(2,284 | ) | (2,263 | ) | ||||

| Common stock held in treasury, at cost (5.3 and 5.4 shares, respectively) |

(213 | ) | (221 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ deficit attributable to Navistar International Corporation |

(4,775 | ) | (4,654 | ) | ||||

| Stockholders’ equity attributable to non-controlling interests |

30 | 34 | ||||||

|

|

|

|

|

|||||

| Total stockholders’ deficit |

(4,745 | ) | (4,620 | ) | ||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ deficit |

$ | 6,925 | $ | 7,443 | ||||

|

|

|

|

|

|||||

Navistar International Corporation and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(Unaudited)

| Six Months Ended | ||||||||

| April 30, | ||||||||

| (in millions) | 2015 | 2014 | ||||||

| Cash flows from operating activities |

||||||||

| Net loss |

$ | (90 | ) | $ | (525 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

| Depreciation and amortization |

118 | 122 | ||||||

| Depreciation of equipment leased to others |

35 | 63 | ||||||

| Deferred taxes, including change in valuation allowance |

(7 | ) | (2 | ) | ||||

| Asset impairment charges |

8 | 169 | ||||||

| Amortization of debt issuance costs and discount |

19 | 27 | ||||||

| Stock-based compensation |

8 | 12 | ||||||

| Provision for doubtful accounts, net of recoveries |

(3 | ) | 9 | |||||

| Equity in income of non-consolidated affiliates, net of dividends |

5 | 7 | ||||||

| Write-off of debt issuance cost and discount |

— | 1 | ||||||

| Other non-cash operating activities |

(20 | ) | (15 | ) | ||||

| Changes in other assets and liabilities, exclusive of the effects of businesses disposed |

(310 | ) | (194 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in operating activities |

(237 | ) | (326 | ) | ||||

|

|

|

|

|

|||||

| Cash flows from investing activities |

||||||||

| Purchases of marketable securities |

(162 | ) | (788 | ) | ||||

| Sales of marketable securities |

431 | 902 | ||||||

| Maturities of marketable securities |

63 | 182 | ||||||

| Net change in restricted cash and cash equivalents |

53 | (21 | ) | |||||

| Capital expenditures |

(45 | ) | (50 | ) | ||||

| Purchases of equipment leased to others |

(20 | ) | (108 | ) | ||||

| Proceeds from sales of property and equipment |

5 | 20 | ||||||

| Proceeds from sales of affiliates |

7 | 5 | ||||||

|

|

|

|

|

|||||

| Net cash provided by investing activities |

332 | 142 | ||||||

|

|

|

|

|

|||||

| Cash flows from financing activities |

||||||||

| Proceeds from issuance of securitized debt |

250 | 152 | ||||||

| Principal payments on securitized debt |

(169 | ) | (81 | ) | ||||

| Proceeds from issuance of non-securitized debt |

84 | 473 | ||||||

| Principal payments on non-securitized debt |

(146 | ) | (509 | ) | ||||

| Net increase in notes and debt outstanding under revolving credit facilities |

5 | 3 | ||||||

| Principal payments under financing arrangements and capital lease obligations |

(1 | ) | (14 | ) | ||||

| Debt issuance costs |

(7 | ) | (13 | ) | ||||

| Proceeds from financed lease obligations |

20 | 34 | ||||||

| Proceeds from exercise of stock options |

1 | 18 | ||||||

| Dividends paid by subsidiaries to non-controlling interest |

(20 | ) | (30 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in financing activities |

17 | 33 | ||||||

|

|

|

|

|

|||||

| Effect of exchange rate changes on cash and cash equivalents |

(26 | ) | (10 | ) | ||||

|

|

|

|

|

|||||

| Increase (decrease) in cash and cash equivalents |

86 | (161 | ) | |||||

| Cash and cash equivalents at beginning of the period |

497 | 755 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of the period |

$ | 583 | $ | 594 | ||||

|

|

|

|

|

|||||

Navistar International Corporation and Subsidiaries

Segment Reporting

(Unaudited)

We define segment profit (loss) as net income (loss) from continuing operations attributable to Navistar International Corporation excluding income tax benefit (expense). The following tables present selected financial information for our reporting segments:

| Corporate | ||||||||||||||||||||||||

| Global | Financial | and | ||||||||||||||||||||||

| (in millions) | Truck | Parts | Operations | Services(A) | Eliminations | Total | ||||||||||||||||||

| Three Months Ended April 30, 2015 |

||||||||||||||||||||||||

| External sales and revenues, net |

$ | 1,933 | $ | 607 | $ | 115 | $ | 35 | $ | 3 | $ | 2,693 | ||||||||||||

| Intersegment sales and revenues (B) |

33 | 6 | 15 | 25 | (79 | ) | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total sales and revenues, net |

$ | 1,966 | $ | 613 | $ | 130 | $ | 60 | $ | (76 | ) | $ | 2,693 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) from continuing operations attributable to NIC, net of tax |

$ | (51 | ) | $ | 133 | $ | 1 | $ | 22 | $ | (169 | ) | $ | (64 | ) | |||||||||

| Income tax expense |

— | — | — | — | (18 | ) | (18 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Segment profit (loss) |

$ | (51 | ) | $ | 133 | $ | 1 | $ | 22 | $ | (151 | ) | $ | (46 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Depreciation and amortization |

$ | 47 | $ | 4 | $ | 5 | $ | 12 | $ | 6 | $ | 74 | ||||||||||||

| Interest expense |

— | — | — | 18 | 57 | 75 | ||||||||||||||||||

| Equity in income (loss) of non-consolidated affiliates |

1 | 1 | (1 | ) | — | — | 1 | |||||||||||||||||

| Capital expenditures (C) |

24 | — | 1 | 2 | 1 | 28 | ||||||||||||||||||

| Corporate | ||||||||||||||||||||||||

| Global | Financial | and | ||||||||||||||||||||||

| (in millions) | Truck | Parts | Operations | Services(A) | Eliminations | Total | ||||||||||||||||||

| Three Months Ended April 30, 2014 |

||||||||||||||||||||||||

| External sales and revenues, net |

$ | 1,829 | $ | 614 | $ | 265 | $ | 38 | $ | — | $ | 2,746 | ||||||||||||

| Intersegment sales and revenues |

60 | 16 | 6 | 19 | (101 | ) | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total sales and revenues, net |

$ | 1,889 | $ | 630 | $ | 271 | $ | 57 | $ | (101 | ) | $ | 2,746 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) from continuing operations attributable to NIC, net of tax |

$ | (129 | ) | $ | 133 | $ | (162 | ) | $ | 24 | $ | (164 | ) | $ | (298 | ) | ||||||||

| Income tax expense |

— | — | — | — | (23 | ) | (23 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Segment profit (loss) |

$ | (129 | ) | $ | 133 | $ | (162 | ) | $ | 24 | $ | (141 | ) | $ | (275 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Depreciation and amortization |

$ | 71 | $ | 4 | $ | 6 | $ | 11 | $ | 7 | $ | 99 | ||||||||||||

| Interest expense |

— | — | — | 17 | 57 | 74 | ||||||||||||||||||

| Equity in income (loss) of non-consolidated affiliates |

1 | 1 | 1 | — | — | 3 | ||||||||||||||||||

| Capital expenditures (C) |

26 | 1 | 1 | — | 1 | 29 | ||||||||||||||||||

| (in millions) | Truck | Parts | Global Operations |

Financial Services(A) |

Corporate and Eliminations |

Total | ||||||||||||||||||

| Six Months Ended April 30, 2015 |

||||||||||||||||||||||||

| External sales and revenues, net |

$ | 3,564 | $ | 1,221 | $ | 253 | $ | 71 | $ | 5 | $ | 5,114 | ||||||||||||

| Intersegment sales and revenues (B) |

72 | 18 | 29 | 49 | (168 | ) | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total sales and revenues, net |

$ | 3,636 | $ | 1,239 | $ | 282 | $ | 120 | $ | (163 | ) | $ | 5,114 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) from continuing operations attributable to NIC, net of tax |

$ | (69 | ) | $ | 278 | $ | (14 | ) | $ | 46 | $ | (347 | ) | $ | (106 | ) | ||||||||

| Income tax expense |

— | — | — | — | (25 | ) | (25 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Segment profit (loss) |

$ | (69 | ) | $ | 278 | $ | (14 | ) | $ | 46 | $ | (322 | ) | $ | (81 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Depreciation and amortization |

$ | 99 | $ | 7 | $ | 12 | $ | 24 | $ | 11 | $ | 153 | ||||||||||||

| Interest expense |

— | — | — | 38 | 114 | 152 | ||||||||||||||||||

| Equity in income (loss) of non-consolidated affiliates |

3 | 2 | (2 | ) | — | — | 3 | |||||||||||||||||

| Capital expenditures (C) |

38 | — | 3 | 2 | 2 | 45 | ||||||||||||||||||

| (in millions) | Truck | Parts | Global Operations |

Financial Services(A) |

Corporate and Eliminations |

Total | ||||||||||||||||||

| Six Months Ended April 30, 2014 |

||||||||||||||||||||||||

| External sales and revenues, net |

$ | 3,220 | $ | 1,188 | $ | 469 | $ | 77 | $ | — | $ | 4,954 | ||||||||||||

| Intersegment sales and revenues |

120 | 28 | 14 | 35 | (197 | ) | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total sales and revenues, net |

$ | 3,340 | $ | 1,216 | $ | 483 | $ | 112 | $ | (197 | ) | $ | 4,954 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) from continuing operations attributable to NIC, net of tax |

$ | (337 | ) | $ | 241 | $ | (197 | ) | $ | 47 | $ | (301 | ) | $ | (547 | ) | ||||||||

| Income tax expense |

— | — | — | — | (11 | ) | (11 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Segment profit (loss) |

$ | (337 | ) | $ | 241 | $ | (197 | ) | $ | 47 | $ | (290 | ) | $ | (536 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Depreciation and amortization |

$ | 129 | $ | 8 | $ | 14 | $ | 21 | $ | 13 | $ | 185 | ||||||||||||

| Interest expense |

— | — | — | 34 | 122 | 156 | ||||||||||||||||||

| Equity in income (loss) of non-consolidated affiliates |

2 | 2 | (1 | ) | — | — | 3 | |||||||||||||||||

| Capital expenditures (C) |

38 | 5 | 4 | 1 | 2 | 50 | ||||||||||||||||||

| (in millions) | Truck | Parts | Global Operations |

Financial Services |

Corporate and Eliminations |

Total | ||||||||||||||||||

| Segment assets, as of: |

||||||||||||||||||||||||

| April 30, 2015 |

$ | 2,104 | $ | 669 | $ | 514 | $ | 2,611 | $ | 1,027 | $ | 6,925 | ||||||||||||

| October 31, 2014 |

2,245 | 672 | 657 | 2,598 | 1,271 | 7,443 | ||||||||||||||||||

| (A) | Total sales and revenues in the Financial Services segment include interest revenues of $44 million and $89 million for the three and six months ended April 30, 2015, respectively and $42 million and $82 million for the three and six months ended April 30, 2014, respectively. |

| (B) | During the second quarter of 2015, we identified a $35 million adjustment related to the first quarter of 2015 Intersegment sales and revenues. As a result, the Truck segment and Corporate and Eliminations should have reported Intersegment sales and revenues of $39 million and $(89) million, respectively, and reported Total sales and revenues, net, of $1,670 million and $(87) million, respectively, for the three months ended January 31, 2015. The adjustment did not impact the consolidated results for the first quarter of 2015. |

| (C) | Exclusive of purchases of equipment leased to others. |

SEC Regulation G Non-GAAP Reconciliation

The financial measures presented below are unaudited and not in accordance with, or an alternative for, financial measures presented in accordance with U.S. generally accepted accounting principles (“GAAP”). The non-GAAP financial information presented herein should be considered supplemental to, and not as a substitute for, or superior to, financial measures calculated in accordance with GAAP and are reconciled to the most appropriate GAAP number below.

Earnings (loss) Before Interest, Income Taxes, Depreciation, and Amortization (“EBITDA”):

We define EBITDA as our consolidated net income (loss) from continuing operations attributable to Navistar International Corporation, net of tax, plus manufacturing interest expense, income taxes, and depreciation and amortization. We believe EBITDA provides meaningful information to the performance of our business and therefore we use it to supplement our GAAP reporting. We have chosen to provide this supplemental information to investors, analysts and other interested parties to enable them to perform additional analyses of operating results.

Adjusted EBITDA:

We believe that adjusted EBITDA, which excludes certain identified items that we do not consider to be part of our ongoing business, improves the comparability of year to year results, and is representative of our underlying performance. Management uses this information to assess and measure the performance of our operating segments. We have chosen to provide this supplemental information to investors, analysts and other interested parties to enable them to perform additional analyses of operating results, to illustrate the results of operations giving effect to the non-GAAP adjustments shown in the below reconciliations, and to provide an additional measure of performance.

Manufacturing Cash, Cash Equivalents, and Marketable Securities:

Manufacturing cash, cash equivalents, and marketable securities represents the Company’s consolidated cash, cash equivalents, and marketable securities excluding cash, cash equivalents, and marketable securities of our financial services operations. We include marketable securities with our cash and cash equivalents when assessing our liquidity position as our investments are highly liquid in nature. We have chosen to provide this supplemental information to investors, analysts and other interested parties to enable them to perform additional analyses of our ability to meet our operating requirements, capital expenditures, equity investments, and financial obligations.

Structural costs consists of Selling, general and administrative expenses and Engineering and product development costs.

EBITDA reconciliation:

| Three Months Ended April 30, |

||||||||

| (in millions) | 2015 | 2014 | ||||||

| Loss from continuing operations attributable to NIC, net of tax |

$ | (64 | ) | $ | (298 | ) | ||

| Plus: |

||||||||

| Depreciation and amortization expense |

74 | 99 | ||||||

| Manufacturing interest expense(A) |

57 | 57 | ||||||

| Less: |

||||||||

| Income tax benefit (expense) |

(18 | ) | (23 | ) | ||||

|

|

|

|

|

|||||

| EBITDA |

$ | 85 | $ | (119 | ) | |||

|

|

|

|

|

|||||

| (A) | Manufacturing interest expense is the net interest expense primarily generated for borrowings that support the manufacturing and corporate operations, adjusted to eliminate intercompany interest expense with our Financial Services segment. The following table reconciles Manufacturing interest expense to the consolidated interest expense: |

10

| Three Months Ended April 30, |

||||||||

| 2015 | 2014 | |||||||

| (in millions) | ||||||||

| Interest expense |

$ | 75 | $ | 74 | ||||

| Less: Financial services interest expense |

18 | 17 | ||||||

|

|

|

|

|

|||||

| Manufacturing interest expense |

$ | 57 | $ | 57 | ||||

|

|

|

|

|

|||||

Adjusted EBITDA reconciliation:

| Three Months Ended April 30, |

||||||||

| (in millions) | 2015 | 2014 | ||||||

| EBITDA (reconciled above) |

$ | 85 | $ | (119 | ) | |||

| Less significant items of: |

||||||||

| Adjustments to pre-existing warranties(A) |

18 | 42 | ||||||

| Other restructuring charges and strategic initiatives(B) |

2 | 8 | ||||||

| Asset impairment charges(C) |

1 | 151 | ||||||

| Gain on settlement(D) |

(10 | ) | — | |||||

| Brazil truck business actions(E) |

6 | — | ||||||

|

|

|

|

|

|||||

| Total Adjustments |

$ | 17 | $ | 201 | ||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 102 | $ | 82 | ||||

|

|

|

|

|

|||||

| (A) | Adjustments to pre-existing warranties reflect changes in our estimate of warranty costs for products sold in prior periods. Such adjustments typically occur when claims experience deviates from historic and expected trends. Our warranty liability is generally affected by component failure rates, repair costs, and the timing of failures. Future events and circumstances related to these factors could materially change our estimates and require adjustments to our liability. In addition, new product launches require a greater use of judgment in developing estimates until historical experience becomes available. |

| (B) | In the second quarter of 2014, we incurred restructuring charges of $8 million related to cost reduction actions that included a reduction-in-force in the U.S. |

| (C) | In the second quarter of 2015, the Company concluded it had a triggering event related to certain operating leases, as a result, the Truck segment recorded $1 million of asset impairment charges. In the second quarter of 2014, we recognized a non-cash charge of $149 million for the impairment of certain intangible assets of our Brazilian engine reporting unit. Due to slower than expected growth in the Brazilian economy causing declines in actual and forecasted results, we tested the goodwill of our Brazilian engine reporting unit and trademark for potential impairment. As a result, we determined that the entire $142 million balance of goodwill and $7 million of trademark were impaired. |

| (D) | In the second quarter of 2015, the Global Operations segment recognized a $10 million gain resulting from a customer settlement, which includes an offsetting restructuring charge of $4 million. |

| (E) | In the second quarter of 2015 our Global Operations segment recorded $6 million in inventory charges to right size the Brazil Truck business. |

Manufacturing segment cash and cash equivalents and marketable securities reconciliation:

| As of April 30, 2015 | ||||||||||||

| (in millions) | Manufacturing Operations |

Financial Services Operations |

Consolidated Balance Sheet |

|||||||||

| Assets |

||||||||||||

| Cash and cash equivalents |

$ | 536 | $ | 47 | $ | 583 | ||||||

| Marketable securities |

248 | 25 | 273 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total Cash and cash equivalents and Marketable securities |

$ | 784 | $ | 72 | $ | 856 | ||||||

|

|

|

|

|

|

|

|||||||

11

Q2 2015 EARNINGS PRESENTATION JUNE 4, 2015 Exhibit 99.2 |

2 NYSE: NAV Q2 2015 Earnings – 6/4/2015 Safe Harbor Statement Information provided and statements contained in this report that are not purely historical are

forward- looking statements within the

meaning of Section 27A of the Securities

Act of 1933, as amended,

Section

21E of the Securities Exchange Act of 1934, as amended,

and the Private Securities Litigation

Reform Act of 1995. Such forward-looking statements

only speak as of the date of this report and the Company assumes no obligation to update the information included in this report. Such forward-

looking statements include information concerning our

possible or assumed future results of

operations, including descriptions of our business

strategy. These statements often include words such as “believe,” “expect,” “anticipate,” “intend,” “plan,”

“estimate,” or similar expressions. These statements are not guarantees of performance or results and they involve risks, uncertainties, and

assumptions. For a further description of these factors,

see the risk factors set forth in our filings with the Securities and Exchange Commission, including our annual report on Form 10-K for the year ended

October 31, 2014 and our quarterly report

on Form 10-Q for the quarter ended April 30, 2015. Although we believe that these forward-looking statements are based on reasonable assumptions,

there are many factors that could affect our actual

financial results or results of operations and could cause actual results to differ materially from those in the forward-looking statements. All future written

and oral forward-looking statements by

us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to above. Except for our ongoing

obligations to disclose material information as required

by the federal securities laws, we do not have any obligations or intention to release publicly any revisions to any forward-looking statements to

reflect events or circumstances in the

future or to reflect the occurrence of unanticipated events. |

3 NYSE: NAV Q2 2015 Earnings – 6/4/2015 Other Cautionary Notes The financial information herein contains audited and unaudited information and has been prepared

by management in good faith and based on data currently

available to the Company. Certain

non-GAAP measures are used in this presentation to assist the reader in understanding our core manufacturing business. We believe this information is useful and relevant to assess and

measure the performance of our core manufacturing

business as it illustrates manufacturing

performance. It also excludes financial services and

other items that may not be related to the core manufacturing business or underlying results. Management often uses this information to assess and

measure

the

underlying

performance

of

our

operating

segments.

We

have

chosen

to

provide

this

supplemental information to investors, analysts, and

other interested parties to enable them to

perform additional analyses of operating results. The

non-GAAP numbers are reconciled to the most appropriate GAAP number in the appendix of this presentation. |

4 NYSE: NAV Q2 2015 Earnings – 6/4/2015 Agenda Overview Troy Clarke Financial Results Walter Borst Summary Troy Clarke |

NYSE: NAV 2 QUARTER 2015 RESULTS Troy Clarke, President & CEO * * * * * * * * * * * |

6 NYSE: NAV Q2 2015 Earnings – 6/4/2015 Q2 Performance • Generated positive manufacturing cash flow • Increased core chargeouts (A) to 18,600 trucks - Up 38% from Q1 2015 - Up 10% from Q2 2014 • Grew adjusted EBITDA • Achieving cost reductions • Taking actions towards improving capacity utilization

• Investing in the core business 2nd Quarter Summary (A) Includes U.S. and Canada School bus and Class 6-8

medium and heavy truck.

|

7 NYSE: NAV Q2 2015 Earnings – 6/4/2015 Industry Momentum Expected to Continue Optimistic Class 8 industry outlook • Lower energy costs • Favorable business conditions • Better new truck fuel economy and safety Positive Medium-duty truck industry outlook • Business investment growth • Housing market expansion |

8 NYSE: NAV Q2 2015 Earnings – 6/4/2015 It’s Uptime at International! • Over 130,000 connected vehicles • Announced making OnCommand Connection standard on all new truck sales • Trained over 100 dealer specialists covering dealers in all major markets • Expanded service into Canada • Entering School Bus market with dedicated product |

NYSE: NAV FINANCIAL RESULTS Walter Borst, Executive Vice President & CFO * * * * * * * * * * * |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Income Statement Summary Note: This slide contains non-GAAP information; please see the

REG G in appendix for a detailed reconciliation.

(A)

Includes U.S. and Canada School bus and Class 6-8

medium and heavy truck.

(B) Amounts attributable to Navistar

International Corporation. $ in millions,

except per share and units Quarters Ended

April 30

2015

2014

Chargeouts

(A)

18,600

16,900

Sales and Revenues

$2,693

$2,746

Income

(Loss)

from

Continuing

Operations,

Net

of

Tax

(B)

$(64)

($298)

Diluted Income (Loss) Per Share from Continuing

Operations (B)

($0.78)

($3.66)

EBITDA

$85

($119)

10 |

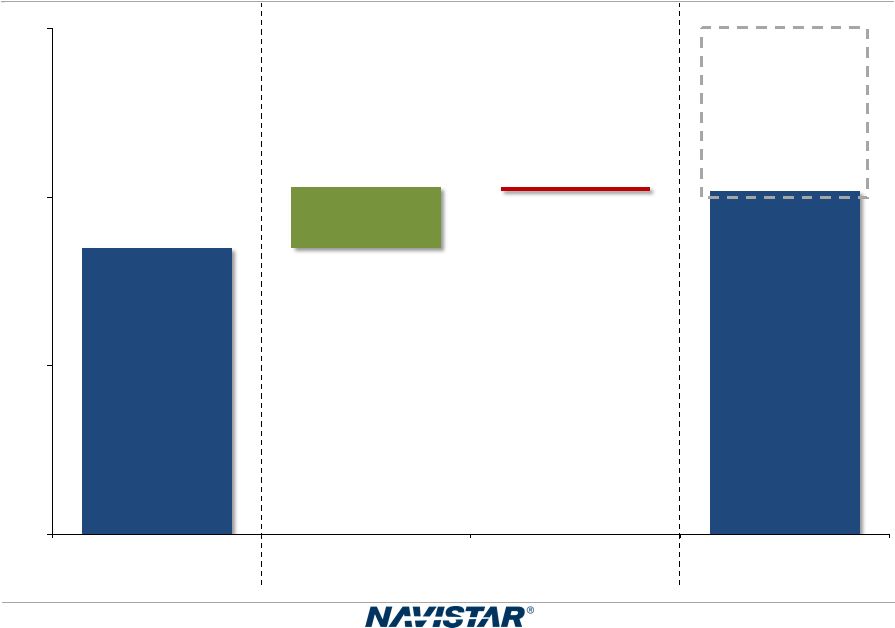

NYSE: NAV Q2 2015 Earnings – 6/4/2015 $85 $102 ($1) $18 $0 $50 $100 $150 Q2 2015 Actual EBITDA Pre-existing Warranty Adjustment One-time Items Q2 2015 Adjusted EBITDA Q2 Guidance:

$100-$150

Q2 2015 EBITDA

$ in millions

Note:

This slide contains non-GAAP information; please

see the REG G in appendix for a detailed

reconciliation. * Excluding

pre-existing warranty and one-time items. * 11 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Q2 2015 Segment Results $ in millions Beginning in the first quarter of 2015, the Company realigned its reporting

segments. The segment results have been restated to

reflect this change. Sales and

Revenues Segment Profit

Quarters Ended

April 30

Quarters Ended

April 30

Segment

2015

2014

2015

2014

Truck

$1,966

$1,889

($51)

($129)

Parts

$613

$630

$133

$133

Global Operations

$130

$271

$1

($162)

Financial Services

$60

$57

$22

$24

12 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Second Quarter Progress (A) Includes U.S. and Canada School bus and Class 6-8 medium

and heavy truck.

(B) Excludes amounts related to

pre-existing warranties.

Note:

This slide contains non-GAAP information; please

see the REG G in appendix for a detailed

reconciliation. 15,000

17,500

20,000

2Q14

2Q15

Chargeouts

(A)

7%

10%

13%

2Q14

2Q15

Structural Costs %

Manufacturing Revenue

2.5%

3.0%

3.5%

2Q14

2Q15

Current Warranty Expense

(B)

%

Manufacturing Revenue

2%

3%

4%

2Q14

2Q15

Adjusted EBITDA Margin

13 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Operational Cost Savings 1.2% 1.7% 1.5 – 1.8% 0% 1% 2% 2013 2014 2015 Gross Material Savings* % Manufacturing Revenue *Excludes incremental SCR costs $44 $79 $40 – $60 $0 $25 $50 $75 $100 2013 2014 2015 Manufacturing Savings Actual Forecast 14 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Used Truck Update • Q2 ending gross inventory balance of $375 million • Inventory expected to peak at $425 million 15 |

Q2 2015 Earnings – 6/4/2015 Q2 2015 Manufacturing Cash Update $ in millions *Guidance as provided on 3/3/2015 **Cash balance includes marketable

securities ^ Excluding one-time items

and pre-existing warranty

Note:

This slide contains non-GAAP information; please

see the REG G in appendix for a detailed

reconciliation.

Guidance*

Actual

Q1 2015 Manufacturing

Cash Balance**

$733

$733

Consolidated Adjusted EBITDA

^

$100 -

$150

$102

Capex/Cash Interest/Pension & OPEB

Funding ($120) -

($110)

($114)

Change in Net Working Capital/Debt and

Warranty/Other ^

($13) –

$27

$63

Q2 2015 Manufacturing Cash Balance**

$700-800

$784

16 |

Q2 2015 Earnings – 6/4/2015 Guidance: Q3 2015 Manufacturing Cash $ in millions * Cash balance includes marketable securities. ** Excluding one-time items and pre-existing warranty

Note:

This slide contains non-GAAP information; please

see the REG G in appendix for a detailed

reconciliation. Q3 2015

Guidance

Q2 2015 Manufacturing

Cash Balance*

$784

Consolidated Adjusted EBITDA**

$125 -

$175

Capex/Cash Interest/Pension & OPEB

Funding ($155) -

($145)

Change in Net Working Capital/Debt and

Warranty/Other ($4) -

$36

Q3 2015 Manufacturing Cash Balance*

$750 -

$850

17 |

Q2 2015 Earnings – 6/4/2015 3.8% 0% 2% 4% 6% 8% 10% Q1 Q2 Q3 Q4 8-10% Adjusted EBITDA Margin Improvement $ in millions Note: This slide contains non-GAAP information; please see the

REG G in appendix for a detailed reconciliation.

•

Q2 adjusted EBITDA

margin up 160 basis

points sequentially

• Cost improvements expected to continue in second half of 2015 • Q3 chargeouts expected to be up 8% year-over- year 2.2% 4.3- 6.3% 2015 Adjusted EBITDA Margin 2015 Actual 2015 Forecast 18 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Q2 2015 Accomplishments: • Increased core truck chargeouts by 1,700 units year-over-year • Higher market share sequentially • Additional cost reductions • Improved working capital • Positive manufacturing cash flow Adjusted EBITDA goal exiting 2015: On track Summing It Up 19 |

NYSE: NAV SUMMARY Troy Clarke, President & CEO * * * * * * * * * * * |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Q3 2015 • Chargeouts up 8% year-over-year • Adjusted EBITDA of $125-$175 million • Manufacturing cash balance of $750-$850 million

2015 Full Year

• Class 6-8 truck and bus industry: 350,000 to 380,000

-

Class 8 industry: 250,000 to 280,000

• Additional cost reduction opportunities • Expect Q4 adjusted EBITDA margin exceeding 8% 2016 Full Year • Class 6-8 truck and bus industry: 350,000-380,000

Expectations

21 |

NYSE: NAV APPENDIX * * * * * * * * * * * * * |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Navistar Financial Corporation Highlights • Financial Services Segment profit of $22 million for Q2 2015, $46 million YTD

• U.S. financing availability of $232 million as of April 30, 2015

• Financial Services Debt/Equity Leverage of 3.9:1 • Retail accounts funding facility renewed in May 2015 for $100 million

• GE announced intent to sell assets of GE Capital which include Navistar Capital

Retail Notes

Bank Facility

Dealer Floor Plan

• $840 million facility ($500 million revolver and $340 million term loan matures in December 2016) – Funding for retail notes, wholesale notes, retail accounts, and dealer open accounts • On balance sheet • NFSC wholesale trust as of April 2015 – $1 billion funding facility – Variable portion matures January 2016 – Term portions mature September 2015 and October 2016 • On balance sheet • Broader product offering • Enhanced ability to support large fleets • Better access to less expensive capital 23 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Chargeouts - 1,000 2,000 3,000 4,000 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 School Bus - 2,000 4,000 6,000 8,000 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Class 6-7 Medium - 2,000 4,000 6,000 8,000 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Class 8 Heavy - 1,000 2,000 3,000 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Class 8 Severe 24 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Retail Market Share in Commercial Vehicle Segments Class 6/7 Medium-Duty Class 8 Severe Service Class 8 Heavy Three Months Ended April 30, January 31, October 31, July 31, April 30, 2015 2015 2014 2014 2014 Core Markets (U.S. and Canada) Class 6 and 7 medium trucks ................................................

27%

21%

19%

20%

26%

Class 8 heavy trucks

............................................................. 12% 10% 15% 14% 14% Class 8 severe service trucks ................................................

15%

14%

14%

15%

17%

Combined class 8 trucks

....................................................... 13% 11% 15% 14% 15% 25 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Worldwide Truck Chargeouts We define chargeouts as trucks that have been invoiced to customers. The units held in dealer inventory represent

the principal difference between retail

deliveries and chargeouts. This table summarizes our

approximate worldwide chargeouts from our continuing operations. We define our Core markets to include U.S. and Canada School bus and Class 6 through 8 medium and heavy

truck. Our Core markets include CAT- branded units sold to Caterpillar under our North America supply agreement.

(A)

Other markets primarily consist of Export Truck and

Mexico and also includes chargeouts

related to BDT of 2,600 units and 2,100 units during

the three months ended April 30, 2015 and

2014, respectively, and 6,000 and 4,500 during the six months ended April 30, 2015 and 2014. Three Months Ended April 30, % Change Six Months Ended April 30, % Change (in units) 2015 2014 Change 2015 2014 Change Core Markets (U.S. and Canada) School buses .........................................

2,300

2,700

(400)

(15)%

5,000

4,700

300

6 %

Class 6 and 7 medium trucks.................

6,700

5,400

1,300

24 %

10,700

8,600

2,100

24 %

Class 8 heavy trucks .............................

7,300

6,700

600

9 %

12,100

11,200

900

8 %

Class 8 severe service trucks ................

2,300

2,100

200

10 %

4,300

3,900

400

10 %

Total Core Markets.................................. 18,600 16,900 1,700 10 % 32,100 28,400 3,700 13 % Non "core" military ...............................

—

100

(100)

—

%

—

100

(100)

—

%

Other markets

(A)

.....................................

5,400

6,700

(1,300)

(19)%

12,400

12,100

300

2 %

Total worldwide unit................................ 24,000 23,700 300 1 % 44,500 40,600 3,900 10 % Combined class 8 trucks........................ 9,600 8,800 800 9 % 16,400 15,100 1,300 9 % 26 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Worldwide Engine Shipments Three Months Ended April 30, % Change Six Months Ended April 30, % Change (in units) 2015 2014 Change 2015 2014 Change OEM sales-South America.................. 11,600 24,500 (12,900) (53)% 27,300 44,900 (17,600) (39)% Intercompany sales..............................

7,000

10,100

(3,100)

(31)%

13,600

19,600

(6,000)

(31)%

Other OEM sales.................................

2,600

2,900

(300)

(10)%

5,500

5,300

200

4 %

Total

sales.....................................

21,200

37,500

(16,300)

(43)%

46,400

69,800

(23,400)

(34)%

27 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 U.S. and Canada Dealer Stock Inventory* *Includes U.S. and Canada Class 4-8 and school bus inventory, but does not include U.S. IC Bus.

28 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Frequently Asked Questions Q1: What is included in Corporate and Eliminations? A: The primary drivers of Corporate and Eliminations are Corporate SG&A, pension and OPEB expense (excluding

amounts allocated to the segments), annual

incentive, manufacturing interest expense, and the elimination of intercompany sales and profit between segments. Q2: What is included in your equity in loss of non-consolidated affiliates?

A:

Equity in loss of non-consolidated affiliates is

derived from our ownership interests in partially-owned affiliates that are not consolidated. Q3: What is your net income attributable to non-controlling interests?

A:

Net income attributable to non-controlling interests

is the result of the consolidation of subsidiaries in which we do not own 100%, and is primarily comprised of Ford's non-controlling interest in our Blue Diamond Parts joint

venture. Q4:

What are your expected 2015 and beyond pension funding

requirements? A:

Future contributions are dependent upon a number of

factors, principally the changes in values of plan assets, changes in interest rates and the impact of any funding relief currently under consideration. For the three and six months ended April

30, 2015, we contributed $32 million and

$62 million, respectively, to our U.S. and Canadian pension plans (the “Plans”) to meet the minimum required contributions for all plans. We currently anticipate additional contributions of approximately $51

million to the Plans during the remainder

of 2015. Future contributions are dependent upon a number of factors, principally the changes in values of plan assets, changes in interest rates, the impact of any future funding relief, and the impact of funding resulting from the closure of our Chatham plant. We currently expect that from 2016 through 2018, the Company will be required to contribute at least $100

million per year to the Plans, depending on

asset performance and discount rates.

29 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Frequently Asked Questions Q5: What is your expectation for future cash tax payments?

A:

Our cash tax payments are expected to remain low in 2015

and will gradually increase as we utilize available net operating losses (NOLs) and tax credits in future years. Q6: What is the current balance of net operating losses as compared to other deferred tax assets?

A:

As of October 31, 2014 the Company has deferred tax

assets for U.S. federal NOLs valued at $870 million, state NOLs valued at $144 million, and foreign NOLs valued at $199 million, for a total undiscounted cash value of $1.2 billion. In addition to NOLs, the Company has deferred tax assets for accumulated tax credits of $256 million and other deferred tax assets of $1.9

billion resulting in net

deferred

tax

assets

before

valuation

allowances

of

approximately

$3.4

billion.

Of

this

amount,

$3.2

billion

is

subject

to

a

valuation allowance at the end of FY2014.

Q7:

How does your FY 2015 Class 8 industry outlook compare to

ACT Research? A:

U.S. and Canadian Class 8 Truck Sales

Reconciliation to ACT

-

Retail Sales

2015

ACT*

302,500

CY to FY adjustment

(4,935)

Total (ACT comparable Class 8 to Navistar)

297,565

Navistar Industry Retail Deliveries Combined Class 8

Trucks 250,000

280,000

Navistar difference from ACT

47,565

17,565

*Source:

ACT

N.A.

Commercial

Vehicle

Outlook

-

May

2015

16.0%

5.9%

30 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Frequently Asked Questions Q8: What is your manufacturing interest expense for Fiscal Year 2015?

A:

For the three and six months ended April 30, 2015,

Manufacturing interest was $57 million and $114 million, respectively. Annual manufacturing interest for 2015 is forecasted to be down approximately 5% compared to 2014. For reference,

interest expense was $243 million and $251

million for FY 2014 and 2013, respectively.

Q9:

What should we assume for capital expenditures in Fiscal

Year 2015? A:

For the three and six months ended April 30, 2015,

capital expenditures were $28 million and $45 million, respectively. Annual Capital expenditures for 2015 is forecasted to be between $125 - 150 million. In comparison, capital expenditures were $88 million and $167 million for FY 2014 and 2013, respectively.

31 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Outstanding Debt Balances April 30, October 31, (in millions) 2015 2014 Manufacturing operations Senior Secured Term Loan Credit Facility, as amended, due 2017, net of unamortized discount of

$3, at both

dates………………………………………………………………………………………

$

694

$

694

8.25% Senior Notes, due 2021, net of unamortized

discount of $19 and $20, respectively………… 1,181 1,180 4.50% Senior Subordinated Convertible Notes, due 2018, net of unamortized discount of $17 and

$19,

respectively……………………………………………………………………………………...

183

181

4.75% Senior Subordinated Convertible Notes, due 2019,

net of unamortized discount of $36 and

$40,

respectively…………………………………………………………………………..………….

375

371

Debt of majority-owned

dealerships…………………………………………………………………. 28 30 Financing arrangements and capital lease

obligations………………………………………………. 50 54 Loan Agreement related to 6.5% Tax Exempt Bonds, due

2040…………………………….……… 225 225 Promissory

Note……………………………………………………………………………...………

5

10

Financed lease

obligations……………………………………………………………………………

141

184

Other…………………….......................…………………………………..........................................

24

29

Total Manufacturing operations

debt……………. ……………………………............................. 2,906 2,958 Less: Current Portion……………………………………………………………………………........

115

100

Net long-term Manufacturing operations

debt…………………………………………………..... $ 2,791 $ 2,858 April 30, October 31, (in millions) 2015 2014 Financial Services operations Asset-backed debt issued by consolidated SPEs, at fixed and variable rates, due serially through

2018…………………………………………………………………………………………………..

$

986

$

914

Bank revolvers, at fixed and variable rates, due dates

from 2015 through 2020……………………. 1,205 1,242 Commercial paper, at variable rates, program matures in

2017……………………………………... 77 74 Borrowings secured by operating and finance leases, at various rates, due serially through 2018….

29

36

Total Financial Services operations debt

………………………………………………………… 2,297 2,266 Less: Current portion

………………………………………………………………………………...

1,096

1,195

Net long-term Financial Services operations

debt………………………………………………... $ 1,201 $ 1,071 32 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 SEC Regulation G Non-GAAP Reconciliation SEC Regulation G Non-GAAP Reconciliation The financial measures presented below are unaudited and not in accordance with, or an alternative for, financial

measures presented in accordance with U.S.

generally accepted accounting principles

("GAAP"). The non-GAAP financial information presented herein should be considered supplemental to, and not as a substitute for, or superior to, financial measures calculated in accordance with GAAP and are reconciled to the most appropriate GAAP number below Earnings (loss) Before Interest, Income Taxes, Depreciation, and Amortization (“EBITDA”):

We define EBITDA as our consolidated net income (loss)

from continuing operations attributable to Navistar International Corporation, net of tax, plus manufacturing interest expense, income taxes, and depreciation and amortization. We believe EBITDA provides

meaningful information to the performance of

our business and therefore we use it to supplement our

GAAP reporting. We have chosen to provide this supplemental information to investors, analysts and other interested parties to enable them to perform additional analyses of operating results..

Adjusted EBITDA:

We believe that adjusted EBITDA, which excludes certain

identified items that we do not consider to be part of our ongoing business, improves the comparability of year to year results, and is representative of our underlying performance. Management uses this

information to assess and measure the

performance of our operating segments. We have chosen to

provide this supplemental information to investors, analysts and other interested parties to enable them to perform additional analyses of operating results, to illustrate the results of operations giving effect to

the non-GAAP adjustments shown in the below reconciliations, and to provide an additional measure of performance.

Adjusted EBITDA margin:

We define Adjusted EBITDA margin as a percentage of the

Company's consolidated sales and revenues. We have chosen to provide this supplemental information to investors, analysts and other interested parties to enable them to perform additional analyses of

operating results, to illustrate the results of operations giving effect to the non-GAAP adjustments shown in the below reconciliations, and to provide

an additional measure of performance.

Manufacturing Cash, Cash Equivalents, and Marketable

Securities: Manufacturing

cash,

cash

equivalents,

and

marketable

securities

represents

the

Company’s

consolidated

cash,

cash

equivalents,

and

marketable

securities

excluding cash, cash equivalents, and marketable

securities of our financial services operations. We include marketable securities with our cash and cash equivalents when assessing our liquidity position as our investments are highly liquid in nature. We have chosen to provide this supplemental information to investors, analysts and other interested parties to enable them to perform additional analyses of our ability to

meet our operating requirements, capital

expenditures, equity investments, and financial

obligations. Structural costs consists of Selling, general and administrative expenses and Engineering and product development

costs. 33

|

NYSE: NAV Q2 2015 Earnings – 6/4/2015 SEC Regulation G Non-GAAP Reconciliations Manufacturing segment cash and cash equivalents and marketable securities reconciliation:

April 31,

January 31,

(in millions)

2015

2015

Manufacturing Operations:

Cash and cash

equivalents……………………………………………………………. $ 536 $ 583 Marketable

securities………………………………………………………….……… 248 150 Manufacturing Cash and cash equivalents and Marketable securities………………. $ 784 $ 733 Financial Services Operations: Cash and cash

equivalents……………………………………………………………. $ 47 $ 37 Marketable

securities………………………………………………………….……… 25 25 Financial Services Cash and cash equivalents and Marketable securities…………… $ 72 $ 62 Consolidated Balance Sheet: Cash and cash

equivalents……………………………………………………………. $ 583 $ 620 Marketable

securities………………………………………………………….……… 273 175 Consolidated Cash and cash equivalents and Marketable securities…………………

$

856

$

795

34 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 SEC Regulation G Non-GAAP Reconciliations Earnings (loss) before interest, taxes, depreciation, and amortization ("EBITDA")

reconciliation

______________________

(A)

Manufacturing interest expense is the net interest

expense primarily generated for borrowings that support the manufacturing and corporate operations, adjusted to eliminate intercompany interest expense with our Financial Services segment. The following

table reconciles Manufacturing interest

expense to the consolidated interest expense: ______________________ * For more detail on the items noted, please see slide 36 footnotes (A),(C),(D),(E), and (F).

(in millions)

EBITDA (reconciled

above) …......…………………………………… $ 85

$

101

$

(119)

Less significant items of:

Adjustments to pre-existing warranties

(A)

………………………...... 18 (57) 42 Asset impairment charges (C) ………...………………………………..

1

7

151

Restructuring charges and strategic

initiatives (D)

………..….……

2

3

8

Gain on settlement

(E)

………………………………………………….. (10) — — Brazil truck business actions (F) …….....………………………………

6

—

—

Total adjustments

17

(47)

201

Adjusted EBITDA

…......………………………………………….....…… $ 102 $

54

$ 82 Adjusted EBITDA Margin

…......………………………………….....….. 3.8% 2.2% 3.0% Quarters Ended April 30, 2015 April 30, 2014 January 31, 2015 (in millions) Loss from continuing operations attributable to NIC, net of tax …………

$

(64)

$

(42)

$

(298)

Plus:

Depreciation and amortization expense

……………………………….. 74 79 99 Manufacturing interest expense (A) ………………………………….….

57

57

57

Less:

Income tax benefit (expense)

…………………………………………… (18) (7) (23) EBITDA

………………………………………………………………………… $ 85 $ 101 $ (119) Quarters Ended

April 30, 2015

April 30, 2014

Janaury 31, 2015

(in millions)

Interest expense

……………………………………………………………….. $ 75 $ 77 $ 74 Less: Financial services interest expense

………………………………….. 18 20 17 Manufacturing interest expense

……………………..……………………… $ 57 $ 57 $ 57 Quarters Ended

April 30, 2015

April 30, 2014

January 31, 2015

35 |

NYSE: NAV Q2 2015 Earnings – 6/4/2015 Significant Items Included Within Our Results Quarters Ended (in millions) April 30, 2015 January 31, 2015 April 30, 2014 Expense (income): Adjustments to pre-existing warranties (A) …………………………………

$

18

$

(57)

$

42

Accelerated depreciation

(B)

………………………………………………..

12

13

—

Asset impairment charges

(C)

……………………………………………….

1

7

151

Other restructuring charges and strategic

initiatives (D)

……………………...

2

3

8

Gain on settlement

(E)

………………………………………………………

(10)

—

—

Brazil truck business actions

(F)

……………………………………………

6

—

—

Brazilian tax adjustments

(G)

……………………………………………….

—

—

29

______________________