Form 10-K WEIS MARKETS INC For: Dec 27

Tweet

Tweet Share

ShareSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X]ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 27, 2014

OR

[ ]TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________to_________

Commission File Number 1-5039

WEIS MARKETS, INC.

(Exact name of registrant as specified in its charter)

|

PENNSYLVANIA

1000 S. Second Street |

24-0755415 |

|

Sunbury, Pennsylvania Registrant's telephone number, including area code: (570) 286-4571

|

17801-0471 Registrant's web address: www.weismarkets.com |

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class Common stock, no par value Securities registered pursuant to Section 12(g) of the Act: None |

Name of each exchange on which registered New York Stock Exchange

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer [ ] |

Accelerated filer [X] |

||

|

Non-accelerated filer [ ] |

(Do not check if a smaller reporting company) |

Smaller reporting company [ ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of Common Stock held by non-affiliates of the Registrant is approximately $545,000,000 as of June 28, 2014 the last business day of the most recently completed second quarter.

Shares of common stock outstanding as of March 12, 2015 - 26,898,443.

DOCUMENTS INCORPORATED BY REFERENCE: Selected portions of the Weis Markets, Inc. definitive proxy statement dated March 12, 2015 are incorporated by reference in Part III of this Form 10-K.

WEIS MARKETS, INC.

WEIS MARKETS, INC.

Weis Markets, Inc. is a Pennsylvania business founded by Harry and Sigmund Weis in 1912 and incorporated in 1924. The Company is engaged principally in the retail sale of food in Pennsylvania and surrounding states. There was no material change in the nature of the Company's business during fiscal 2014. The Company’s stock has been traded on the New York Stock Exchange since 1965 under the symbol “WMK.” The Weis family currently owns approximately 65% of the outstanding shares. Robert F. Weis serves as Chairman of the Board of Directors, and Jonathan H. Weis, son of Robert F. Weis, serves as Vice Chairman, President and Chief Executive Officer.

The Company's retail food stores sell groceries, dairy products, frozen foods, meats, seafood, fresh produce, floral, pharmacy services, deli products, prepared foods, bakery products, beer and wine, fuel and general merchandise items, such as health and beauty care and household products. The Company advertises its products and promotes its brand through weekly newspaper circulars; radio and television ads; e-mail blasts; and on-line via its website, social media and mobile applications. Printed circulars are used extensively on a weekly basis to advertise featured items. The Company utilizes a loyalty marketing program, “Weis Club Preferred Shopper,” which enables customers to receive discounts, promotions and fuel rewards. The Company currently owns and operates 163 retail food stores. The Company’s operations are reported as a single reportable segment.

The following table provides additional detail on the percentage of consolidated net sales contributed by product category for fiscal years 2014, 2013 and 2012, respectively:

|

2014 |

2013 |

2012 |

||||

|

Center Store (1) |

57.9 |

% |

59.0 |

% |

59.5 |

% |

|

Fresh (2) |

29.0 | 28.7 | 28.1 | |||

|

Pharmacy Services |

9.0 | 8.6 | 8.7 | |||

|

Fuel |

3.9 | 3.5 | 3.5 | |||

|

Other |

0.2 | 0.2 | 0.2 | |||

|

Consolidated net sales |

100.0 |

% |

100.0 |

% |

100.0 |

% |

__________

(1) Consists primarily of groceries, dairy products, frozen foods, beer and wine, and general merchandise items, such as health and beauty care and household products.

(2) Consists primarily of meats, seafood, fresh produce, floral, deli products, prepared foods and bakery products.

At the end of 2014, Weis Markets, Inc. operated 25 stores in Maryland, 5 stores in New Jersey, 9 stores in New York, 122 stores in Pennsylvania and 2 stores in West Virginia, for a total of 163 retail food stores operating under the Weis Markets trade name.

1

WEIS MARKETS, INC.

Item 1.Business: (continued)

All retail food store locations operate as conventional supermarkets. The retail food stores range in size from 8,000 to 70,000 square feet, with an average size of approximately 50,000 square feet. The following summarizes the number of stores by size categories as of year-end:

|

2014 |

2014 |

2013 |

2013 |

|||||

|

Square feet |

Number of stores |

% of Total |

Number of stores |

% of Total |

||||

|

55,000 to 70,000 |

56 | 34% | 53 | 32% | ||||

|

45,000 to 54,999 |

70 | 43% | 72 | 44% | ||||

|

35,000 to 44,999 |

22 | 13% | 22 | 13% | ||||

|

25,000 to 34,999 |

9 | 6% | 12 | 7% | ||||

|

Under 25,000 |

6 | 4% | 6 | 4% | ||||

|

Total |

163 | 100% | 165 | 100% | ||||

The following schedule shows the changes in the number of retail food stores, total square footage and store additions/remodels as of year-end:

|

2014 |

2013 |

2012 |

2011 |

2010 |

||||||

|

Beginning store count |

165 | 163 | 161 | 164 | 164 | |||||

|

New stores (1) |

1 | 4 | 4 | 1 |

--- |

|||||

|

Opened relocated stores |

1 |

--- |

1 | 1 |

--- |

|||||

|

Closed stores |

(3) | (2) | (2) | (4) |

--- |

|||||

|

Closed relocated stores |

(1) |

--- |

(1) | (1) |

--- |

|||||

|

Ending store count |

163 | 165 | 163 | 161 | 164 | |||||

|

Total square feet (000’s), at year-end |

8,202 | 8,211 | 8,054 | 7,877 | 7,887 | |||||

|

Additions/major remodels |

8 | 12 | 13 | 9 | 4 | |||||

____________________

(1) On June 11, 2012, Weis Markets, Inc. acquired three former Genuardi’s stores located in Conshohocken, Doylestown and Norristown, Pennsylvania from Safeway Inc.

The Company supports its retail operations through a centrally located distribution facility, its own transportation fleet, three manufacturing facilities and its store support center. The Company is required to use a significant amount of working capital to provide for the necessary amount of inventory to meet demand for its products through efficient use of buying power and effective utilization of space in its distribution facilities. The manufacturing facilities consist of a meat processing plant, an ice cream plant and a milk processing plant.

The Company operates in a highly competitive market place. The number and the variety of competitors vary by market. The Company’s principal competition consists of international, national, regional and local food chains, as well as independent food stores. The Company also faces substantial competition from convenience stores, membership warehouse clubs, specialty retailers, supercenters and large-scale drug and pharmaceutical chains. The Company continues to effectively compete by offering a strong combination of value, quality and service.

The Company currently employs approximately 18,200 full-time and part-time associates.

2

WEIS MARKETS, INC.

Item 1. Business: (continued)

Trade Names and Trademarks. The Company has invested significantly in the development and protection of “Weis Markets” both as a trade name and a trademark and considers it to be an important asset. The Company is the exclusive licensee of more than 60 other trademarks registered and/or pending in the United States Patent and Trademark Office from WMK Holdings, Inc., including trademarks for its product lines and promotions such as Weis, Weis 2 Go, Weis Wonder Chicken, Price Freeze, Weis Gas-n-Go and Weis Nutri-Facts. Each trademark registration is for an initial period of 10 years and may be renewed so long as it is in continued use in commerce.

The Company considers its trademarks to be of material importance to its business and actively defends and enforces its rights.

The Company maintains a corporate web site at www.weismarkets.com. The Company makes available, free of charge, on the “Corporate Information” section of its web site, its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, as soon as reasonably practicable after the Company electronically files such material or furnishes it to the U.S. Securities and Exchange Commission (SEC) by clicking on the “SEC Information” link.

The Company’s Corporate Governance materials can be found in the “Corporate Information” section of the Company’s web site. These materials include the corporate governance guidelines; the charters of the Audit, Compensation and Disclosure Committees; and both the Code of Business Conduct and Ethics and the Code of Ethics for the CEO and CFO. A copy of the foregoing corporate governance materials is available upon written request to the Company’s principal executive offices.

In addition to risks and uncertainties in the ordinary course of business common to all businesses, important factors are listed below specific to the Company and its industry, which could materially impact its future performance.

The Company’s industry is highly competitive. If the Company is unable to compete effectively, the Company’s financial condition and results of operations could be materially affected.

The retail food industry is intensely price competitive, and the competition the Company encounters may have a negative impact on product retail prices. The financial results may be adversely impacted by a competitive environment that could cause the Company to reduce retail prices without a reduction in its product cost to maintain market share; thus reducing sales and gross profit margins.

The trade area of the Company is located within a region and is subject to the economic, social and climate variables of that region.

The majority of the Company’s stores are concentrated in central and northeast Pennsylvania, central Maryland, suburban Baltimore regions and New York’s Southern Tier. Changes in economic and social conditions in the Company’s operating regions, including fluctuations in the inflation rate along with changes in population and employment and job growth rates, affect customer shopping habits. These changes may negatively impact sales and earnings. Business disruptions due to weather and catastrophic events historically have been few. The Company’s geographic regions could receive an extreme variance in the amount of annual snowfall that may materially affect sales and expense results.

The Company may be unable to retain key management personnel.

The Company's success depends to a significant degree upon the continued contributions of senior management. The loss of any key member of management may prevent the Company from implementing its business plans in a timely manner. In addition, employment conditions specifically may affect the Company’s ability to hire and train qualified associates.

3

WEIS MARKETS, INC.

Item 1a. Risk Factors: (continued)

Food safety issues could result in the loss of consumer confidence in the Company.

Customers count on the Company to provide them with safe and wholesome food products. Concerns regarding the safety of food products sold in its stores could cause shoppers to avoid purchasing certain products from the Company, or to seek alternative sources of supply for all of their food needs, even if the basis for the concern is outside of the Company’s control. A loss in confidence on the part of its customers would be difficult and costly to reestablish. As such, any issue regarding the safety of any food items sold by the Company, regardless of the cause, could have a substantial and adverse effect on operations.

The failure to execute expansion plans could have a material adverse effect on the Company's business and results of its operations.

Circumstances outside the Company’s control could negatively impact anticipated capital investments in store, distribution and manufacturing projects, information technology and equipment. The Company cannot determine with certainty whether its new stores will be successful. The failure to expand by successfully opening new stores as planned, or the failure of a significant number of these stores to perform as planned, could have a material adverse effect on the Company’s business and results of its operations.

Disruptions or security breaches in the Company’s information technology systems could adversely affect results.

The Company’s business is highly dependent on complex information technology systems that are vital to its continuing operations. If the Company was to experience difficulties maintaining existing systems or implementing new systems, significant losses could be incurred due to disruptions in its operations. Additionally, these systems contain valuable proprietary data as well as receipt and storage of personal information about its associates and customers, in particular electronic payment data and personal health information that, if breached, would have an adverse effect on the Company. Such an occurrence could adversely affect the Company’s reputation with its customers, associates, and vendors, as well as the Company’s operations, results of operations, financial condition and liquidity, and could result in litigation against the Company or the imposition of penalties. Moreover, a security breach could require the expenditure of significant additional resources to further upgrade the security measures that the Company employs to guard such important personal information against cyberattacks and other attempts to access such information and could result in a disruption of operations.

The Company is affected by certain operating costs which could increase or fluctuate considerably.

Associate expenses contribute to the majority of the Company’s operating costs. The Company's financial performance is potentially affected by increasing wage and benefit costs, a competitive labor market, regulatory wage increases and the risk of unionized labor disruptions of its non-union workforce. The Company's profit is particularly sensitive to the cost of oil. Oil prices directly affect the Company's product transportation costs, as well as its utility and petroleum-based supply costs. It also affects the costs of its suppliers, which impacts its cost of goods.

Various aspects of the Company’s business are subject to federal, state and local laws and regulations.

The Company is subject to various federal, state and local laws, regulations and administrative practices that affect the Company’s business. The Company must comply with numerous provisions regulating health and sanitation standards, food labeling, equal employment opportunity, minimum wages and licensing for the sale of food, drugs and alcoholic beverages. The Company’s compliance with these regulations may require additional capital expenditures and could adversely affect the Company’s ability to conduct the Company’s business as planned. Management cannot predict either the nature of future laws, regulations, interpretations or applications, or the effect either additional government regulations or administrative orders, when and if promulgated, or disparate federal, state, and local regulatory schemes would have on the Company’s future business. They could, however, require the reformulation of certain products to meet new standards, the recall or discontinuance of certain products not able to be reformulated, additional record keeping, expanded documentation of the properties of certain products, expanded or different labeling and/or scientific substantiation. Any or all of such requirements could have an adverse effect on the Company’s results of operations and financial condition.

4

WEIS MARKETS, INC.

Item 1a. Risk Factors: (continued)

Unexpected factors affecting self-insurance claims and reserve estimates could adversely affect the Company.

The Company uses a combination of insurance and self-insurance to provide for potential liabilities for workers' compensation, general liability, vehicle accident, property and associate medical benefit claims. Management estimates the liabilities associated with the risks retained by the Company, in part, by considering historical claims experience, demographic and severity factors and other actuarial assumptions which, by their nature, are subject to a high degree of variability. Any projection of losses concerning workers’ compensation and general liability is subject to a high degree of variability. Among the causes of this variability are unpredictable external factors affecting future inflation rates, discount rates, litigation trends, legal interpretations, benefit level changes and claim settlement patterns.

The Company was liable for associate health claims up to an annual maximum of $750,000 per member prior to March 1, 2012, $1,250,000 per member prior to March 1, 2013, $2,000,000 per member prior to March 1, 2014 and an unlimited amount per member as of March 1, 2014. As of March 1, 2014, the Company purchased stop loss insurance which carries a $500,000 specific deductible with a $250,000 aggregating deductible. The Company is liable for workers' compensation claims up to $2,000,000 per claim. Property and casualty insurance coverage is maintained with outside carriers at deductible or retention levels ranging from $100,000 to $1,000,000. The Company, for the benefit of cost savings, has accepted the risk of an unusual amount of independent multiple material claims arising, which could have a significant impact on earnings.

Changes in tax laws may result in higher income tax.

The Company's future effective tax rate may increase from current rates due to changes in laws and the status of pending items with various taxing authorities. Currently, the Company benefits from a combination of its corporate structure and certain state tax laws.

The Company’s investment portfolio may suffer losses from changes in market interest rates and changes in market conditions which could adversely affect results of operations or liquidity.

As of December 27, 2014, the Company had $23.0 million in cash and cash equivalents, $74.0 million in marketable securities and $9.1 million in SERP (Supplemental Executive Retirement Plan) investment (level 1 mutual funds). The Company’s marketable securities consist of municipal bonds and equity securities. These investments are subject to general credit, liquidity, market and interest rate risks. Substantially all of these securities are subject to interest rate and credit risk and will decline in value if interest rates increase or one of the issuers’ credit ratings is reduced. As a result, the Company may experience a reduction in value or loss of liquidity from investments, which may have a negative impact on the Company’s results of operations, liquidity and financial condition. The Federal Deposit Insurance Corporation (FDIC) insures amounts up to $250,000 per depositor, per insured bank, for each account ownership category. The Company has balances in bank accounts that may exceed the insured amount leaving the Company exposed for any amounts over the $250,000 limit.

The Company is a controlled Company due to the common stock holdings of the Weis family.

The Weis family’s share ownership represents approximately 65% of the combined voting power of the Company’s common stock as of December 27, 2014. As a result, the Weis family has the power to elect a majority of the Company’s directors and approve any action requiring the approval of the shareholders of the Company, including adopting certain amendments to the Company’s charter and approving mergers or sales of substantially all of the Company’s assets. Currently, two of the Company’s six directors are members of the Weis family.

Changes in vendor promotions or allowances, including the way vendors target their promotional spending, and the Company's ability to effectively manage these programs could significantly impact margins and profitability.

The Company cooperatively engages in a variety of promotional programs with its vendors. As the parties assess the results of specific promotions and plan for future promotions, the nature of these programs and the allocation of dollars among them changes over time. The Company manages these programs to maintain or improve margins while at the same time increasing sales. A reduction in overall promotional spending or a shift by vendors in promotional spending away from certain types of promotions that the Company and its customers have historically utilized could have a significant impact on profitability.

5

WEIS MARKETS, INC.

Item 1b. Unresolved Staff Comments:

There are no unresolved staff comments.

As of December 27, 2014, the Company owned and operated 82 of its retail food stores, and leased and operated 81 stores under operating leases that expire at various dates through 2029. The Company owns all trade fixtures and equipment in its stores and several parcels of vacant land, which are available as locations for possible future stores or other expansion.

The Company owns and operates one distribution center in Milton, Pennsylvania of approximately 1.1 million square feet, and one in Northumberland, Pennsylvania totaling approximately 76,000 square feet. The Company also owns one warehouse complex in Sunbury, Pennsylvania totaling approximately 551,000 square feet. The Company utilizes 259,000 square feet of its Sunbury location to operate its ice cream plant, meat processing plant and milk processing plant.

Neither the Company nor any subsidiary is presently a party to, nor is any of their property subject to, any pending legal proceedings, other than routine litigation incidental to the business that would not have a material adverse effect on the financial results. The Company estimates any exposure to these legal proceedings and establishes accruals for the estimated liabilities, where it is reasonably possible to estimate and where an adverse outcome is probable.

6

WEIS MARKETS, INC.

Executive Officers of the Registrant

The following sets forth the names and ages of the Company’s executive officers as of March 12, 2015, indicating all positions held during the past five years:

|

Name |

Age |

Title |

||

|

Robert F. Weis (a) |

95 |

Chairman of the Board |

||

|

Jonathan H. Weis (b) |

47 |

Vice Chairman, President and Chief Executive Officer |

||

|

Kurt A. Schertle (c) |

43 |

Chief Operating Officer |

||

|

Scott F. Frost (d) |

52 |

Senior Vice President, Chief Financial Officer and Treasurer |

||

|

David W. Gose II (e) |

48 |

Senior Vice President of Operations |

||

|

Harold G. Graber (f) |

59 |

Senior Vice President of Real Estate and Development and Secretary |

||

|

James E. Marcil (g) |

56 |

Senior Vice President of Human Resources |

|

(a) |

Robert F. Weis. The Company has employed Mr. Weis since 1946. Mr. Weis served as Chairman and Treasurer from 1995 until April 2002, at which time he was appointed Chairman of the Board. |

|

(b) |

Jonathan H. Weis. The Company has employed Mr. Weis since 1989. Mr. Weis served the Company as Vice President of Property Management and Development from 1996 until April 2002, at which time he was appointed as Vice President and Secretary. In January of 2004, the Board appointed Mr. Weis as Vice Chairman and Secretary. Mr. Weis became the Company's interim President and Chief Executive Officer in September 2013 and was appointed as President and Chief Executive Officer in February 2014. |

|

(c) |

Kurt A. Schertle. The Company hired Mr. Schertle on March 1, 2009 as its Vice President of Sales and Merchandising, which included the responsibility of overseeing the Marketing Department. In February 2010, Mr. Schertle was promoted to Senior Vice President of Sales and Merchandising. In July 2012, Mr. Schertle was promoted to Executive Vice President of Sales and Merchandising at which time, he assumed the additional responsibility of overseeing the Company’s Supply Chain. In September 2013, Mr. Schertle assumed the additional responsibility of overseeing Store Operations and Mr. Schertle was promoted to Chief Operating Officer in March 2014. |

|

(d) |

Scott F. Frost. Mr. Frost joined the Company full-time in 1984 and he has held various positions since then, including but not limited to, Controller, Assistant Treasurer and Acting Chief Financial Officer. The Company appointed Mr. Frost as Vice President, Chief Financial Officer and Treasurer in October 2009. In January 2011, Mr. Frost was promoted to Senior Vice President, Chief Financial Officer and Treasurer. Mr. Frost also served as Assistant Secretary of the Company during the past five years. |

|

(e) |

David W. Gose II. Mr. Gose joined the Company in May 2014 as Senior Vice President of Operations. Prior to joining the Company, Mr. Gose was Senior Director and Regional General Manager of Walmart Ohio, a retail store SuperCenter, from February 2010 until May 2014. Walmart Ohio consisted of 92 stores that geographically included all stores South of Toledo, Cleveland, Akron and Youngstown. |

|

(f) |

Harold G. Graber. Mr. Graber joined the Company in October 1989 as the Director of Real Estate. Mr. Graber, who served the Company as Vice President for Real Estate since 1996, was promoted to Senior Vice President of Real Estate and Development in February 2010. Mr. Graber was appointed as Secretary of the Company in February 2014. |

|

(g) |

James E. Marcil. Mr. Marcil joined the Company in September 2002 as Vice President of Human Resources. In February 2010, Mr. Marcil was promoted to Senior Vice President of Human Resources. |

7

WEIS MARKETS, INC.

Table of Contents

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities:

The Company's stock is traded on the New York Stock Exchange (ticker symbol WMK). The approximate number of shareholders, including individual participants in security position listings on December 27, 2014 as provided by the Company's transfer agent was 5,364. High and low stock prices and dividends paid per share for the last two fiscal years were:

|

2014 |

2013 |

|||||||||||||||||

|

Stock Price |

Dividend |

Stock Price |

Dividend |

|||||||||||||||

|

Quarter |

High |

Low |

Per Share |

High |

Low |

Per Share |

||||||||||||

|

First |

$ |

52.82 |

$ |

46.12 |

$ |

0.30 |

$ |

41.98 |

$ |

37.90 |

$ |

0.30 | ||||||

|

Second |

50.56 | 42.54 | 0.30 | 47.92 | 39.34 | 0.30 | ||||||||||||

|

Third |

46.97 | 39.09 | 0.30 | 51.92 | 45.12 | 0.30 | ||||||||||||

|

Fourth |

48.00 | 38.23 | 0.30 | 54.13 | 46.15 | 0.30 | ||||||||||||

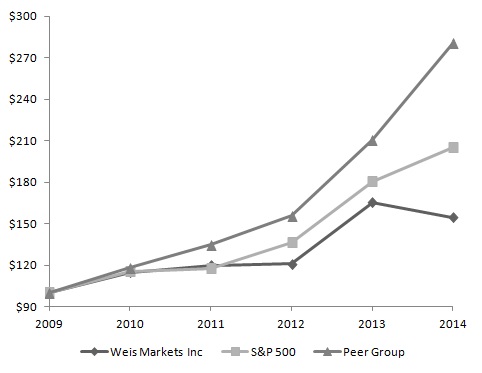

The following line graph compares the yearly percentage change in the cumulative total shareholder return on the Company’s common stock against the cumulative total return of the S&P Composite-500 Stock Index and the cumulative total return of a published group index for the Retail Grocery Stores Industry (“Peer Group”), provided by Value Line, Inc., for the period of five years. The graph depicts $100 invested at the close of trading on the last trading day preceding the first day of the fifth preceding year in Weis Markets, Inc. common stock, S&P 500, and the Peer Group. The cumulative total return assumes reinvestment of dividends.

Comparative Five-Year Total Returns

|

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

|||||||

|

Weis Markets, Inc. |

100.00 | 114.55 | 119.79 | 120.79 | 165.42 | 154.54 | ||||||

|

S&P 500 |

100.00 | 115.06 | 117.49 | 136.29 | 180.43 | 205.13 | ||||||

|

Peer Group |

100.00 | 117.87 | 134.54 | 155.75 | 210.72 | 280.61 | ||||||

8

WEIS MARKETS, INC.

Item 6. Selected Financial Data:

The following selected historical financial information has been derived from the Company's audited consolidated financial statements. This information should be read in connection with the Company's Consolidated Financial Statements and the Notes thereto, as well as "Management's Discussion and Analysis of Financial Condition and Results of Operations," included in Item 7.

Five Year Review of Operations

|

52 Weeks |

52 Weeks |

52 Weeks |

53 Weeks |

52 Weeks |

||||||||||

|

(dollars in thousands, except shares, |

Ended |

Ended |

Ended |

Ended |

Ended |

|||||||||

|

per share amounts and store information) |

Dec. 27, 2014 |

Dec. 28, 2013 |

Dec. 29, 2012 |

Dec. 31, 2011 |

Dec. 25, 2010 |

|||||||||

|

Net sales |

$ |

2,776,683 |

$ |

2,692,588 |

$ |

2,701,405 |

$ |

2,752,504 |

$ |

2,620,378 | ||||

|

Costs and expenses |

2,693,972 | 2,581,406 | 2,574,373 | 2,638,224 | 2,515,062 | |||||||||

|

Income from operations |

82,711 | 111,182 | 127,032 | 114,280 | 105,316 | |||||||||

|

Investment and other income |

2,287 | 4,684 | 3,882 | 3,326 | 2,069 | |||||||||

|

Income before provision for income taxes |

84,998 | 115,866 | 130,914 | 117,606 | 107,385 | |||||||||

|

Provision for income taxes |

29,831 | 44,145 | 48,403 | 42,022 | 39,094 | |||||||||

|

Net income |

55,167 | 71,721 | 82,511 | 75,584 | 68,291 | |||||||||

|

Retained earnings, beginning of year |

971,022 | 931,579 | 881,346 | 864,132 | 827,042 | |||||||||

| 1,026,189 | 1,003,300 | 963,857 | 939,716 | 895,333 | ||||||||||

|

Cash dividends |

32,278 | 32,278 | 32,278 | 58,370 | 31,201 | |||||||||

|

Retained earnings, end of year |

$ |

993,911 |

$ |

971,022 |

$ |

931,579 |

$ |

881,346 |

$ |

864,132 | ||||

|

Weighted-average shares outstanding, diluted |

26,898,443 | 26,898,443 | 26,898,443 | 26,898,443 | 26,898,443 | |||||||||

|

Cash dividends per share |

$ |

1.20 |

$ |

1.20 |

$ |

1.20 |

$ |

2.17 |

$ |

1.16 | ||||

|

Basic and diluted earnings per share |

$ |

2.05 |

$ |

2.67 |

$ |

3.07 |

$ |

2.81 |

$ |

2.54 | ||||

|

Working capital |

$ |

223,776 |

$ |

211,528 |

$ |

229,748 |

$ |

223,742 |

$ |

234,889 | ||||

|

Total assets |

$ |

1,191,119 |

$ |

1,148,242 |

$ |

1,090,440 |

$ |

1,029,004 |

$ |

992,081 | ||||

|

Shareholders’ equity |

$ |

857,832 |

$ |

834,053 |

$ |

795,690 |

$ |

745,886 |

$ |

728,127 | ||||

|

Number of grocery stores |

163 | 165 | 163 | 161 | 164 | |||||||||

9

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations:

Overview

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A) is intended to help the reader understand Weis Markets, Inc., its operations and its present business environment. The MD&A is provided as a supplement to and should be read in conjunction with the consolidated financial statements and the accompanying notes thereto contained in “Item 8. Financial Statements and Supplementary Data” of this report. The following analysis should also be read in conjunction with the Financial Statements included in the Quarterly Reports on Form 10-Q and the Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission, as well as the cautionary statement captioned “Forward-Looking Statements” immediately following this analysis. This overview summarizes the MD&A, which includes the following sections:

• Company Overview - a general description of the Company’s business and strategic imperatives.

• Results of Operations - an analysis of the Company’s consolidated results of operations for the three years presented in the Company’s consolidated financial statements.

• Liquidity and Capital Resources - an analysis of cash flows, aggregate contractual obligations, and off-balance sheet

arrangements.

• Critical Accounting Policies and Estimates - a discussion of accounting policies that require critical judgments and estimates.

Company Overview

General

Weis Markets, Inc. was founded in 1912 by Harry and Sigmund Weis in Sunbury, Pennsylvania. Today, the Company ranks among the top 50 food and drug retailers in the United States in revenues generated. As of December 27, 2014, the Company operated 163 retail food stores in Pennsylvania and four surrounding states: Maryland, New Jersey, New York and West Virginia.

Company revenues are generated in its retail food stores from the sale of a wide variety of consumer products including groceries, dairy products, frozen foods, meats, seafood, fresh produce, floral, pharmacy services, deli products, prepared foods, bakery products, beer and wine, fuel, and general merchandise items, such as health and beauty care and household products. The Company supports its retail operations through a centrally located distribution facility, its own transportation fleet, three manufacturing facilities and its administrative offices. The Company's operations are reported as a single reportable segment.

10

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Company Overview, (continued)

Strategic Imperatives

The following strategic imperatives will be focused upon by the Company to attempt to ensure the success of the Company in the coming years:

|

· |

Establish a Sales Driven Culture – The Company continues to focus on sales and profits growth, improved operating practices, increased productivity and positive cash flow. The Company believes disciplined growth will increase its market share and operating profits, resulting in enhanced shareholder value. The Company’s method of driving sales includes focused preparation and execution of sales programs, investing in new stores and remodels, and strategic acquisitions. Communicating clear executable standards and aligning performance measures across the organization will help to instill a sales-driven operating environment. |

|

· |

Continuously Upgrade Organizational Talent Pool – In support of the Company’s growth and sales building strategies, the Company is committed to growing leaders at every level throughout the organization through enhanced leadership development programs, succession planning, and establishing rewarding career paths. The Company believes that improved associate talent directly impacts the ability to execute strategic plans and views this as a strategic imperative for future growth. |

|

· |

Become More Relevant to Consumers – Understanding the consumer is crucial to the Company’s strategic plan. Research can be done by studying the wants and needs of core consumers and casual consumers. Measuring customer satisfaction and sharing insights across the organization will help communication between management and its consumers. The Company strives to build customer loyalty by purchasing produce from local growers and supporting organizations within the communities it serves. It will continue to invest in new stores, remodels and additions and strategic acquisitions, to help retain and attract new consumers. |

|

· |

Create Meaningful Differentiation – The Company has identified product pricing, locally focused store assortments, shopping experience, overall convenience and customer service as critical components of future success. The strategy includes developing improved customer service training and setting customer service measurements and goals. As part of this strategy, management is committed to offering its customers a strong combination of quality, service and value. It will continue to offer competitive prices on name brand and private brand products to exceed customers’ expectations. |

|

· |

Significantly Improve Decision Support and Measurement – The Company will continue to make investments in its information technology systems and distribution network. This will help improve associate productivity, store conditions and the overall customer experience with user-friendly, support driven systems. These systems will also continue to play a key role in the measurement of the Company’s strategic decisions and provide valuable insight into customer behavior, shopping trends, and financial returns. Management will continue to streamline its supply chain by focusing on improving inventory turns, cost per case, in-stock position and overall service levels, which will help to improve in-store conditions and result in increased sales and profits. |

|

· |

Focus on Sustainability Strategies – The Company views being good stewards in the communities in which we operate as an important component of overall success. The Company’s sustainability program operates under a structure of four key pillars: green design, natural resource conservation, food and agricultural impact and social responsibility. The goal of the sustainability strategy is to reduce the Company’s overall carbon footprint by reducing greenhouse gas emissions and reducing the impact on climate change. The Company is seeking to reduce its carbon footprint by 20% by the year 2020. To accomplish this, the Company intends to institute new sustainability programs and to improve existing sustainability programs. Since 2008, the Company has been measuring the carbon footprint of the entire enterprise and has reduced the carbon emissions by a total of 14.8%. |

11

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Results of Operations

Analysis of Consolidated Statements of Income

|

(dollars in thousands except per share amounts) |

Percent Changes |

||||||||||||||

|

For the Fiscal Years Ended December 27, 2014, |

2014 |

2013 |

2012 |

2014 vs. |

2013 vs. |

||||||||||

|

December 28, 2013 and December 29, 2012 |

(52 weeks) |

(52 weeks) |

(52 weeks) |

2013 |

2012 |

||||||||||

|

Net sales |

$ |

2,776,683 |

$ |

2,692,588 |

$ |

2,701,405 | 3.1 |

% |

(0.3) |

% |

|||||

|

Cost of sales, including warehousing and distribution expenses |

2,023,721 | 1,947,120 | 1,958,852 | 3.9 | (0.6) | ||||||||||

|

Gross profit on sales |

752,962 | 745,468 | 742,553 | 1.0 | 0.4 | ||||||||||

|

Gross profit margin |

27.1 |

% |

27.7 |

% |

27.5 |

% |

|||||||||

|

Operating, general and administratives expenses |

670,251 | 634,286 | 615,521 | 5.7 | 3.0 | ||||||||||

|

O, G & A, percent of net sales |

24.1 |

% |

23.6 |

% |

22.8 |

% |

|||||||||

|

Income from operations |

82,711 | 111,182 | 127,032 | (25.6) | (12.5) | ||||||||||

|

Operating margin |

3.0 |

% |

4.1 |

% |

4.7 |

% |

|||||||||

|

Investment income |

2,287 | 4,684 | 3,468 | (51.2) | 35.1 | ||||||||||

|

Investment income, percent of net sales |

0.1 |

% |

0.2 |

% |

0.1 |

% |

|||||||||

|

Other income |

- |

- |

414 |

- |

(100.0) | ||||||||||

|

Other income, percent of net sales |

- |

% |

- |

% |

0.0 |

% |

|||||||||

|

Income before provision for income taxes |

84,998 | 115,866 | 130,914 | (26.6) | (11.5) | ||||||||||

|

Provision for income taxes |

29,831 | 44,145 | 48,403 | (32.4) | (8.8) | ||||||||||

|

Effective tax rate |

35.1 |

% |

38.1 |

% |

37.0 |

% |

|||||||||

|

Net income |

$ |

55,167 |

$ |

71,721 |

$ |

82,511 | (23.1) |

% |

(13.1) |

% |

|||||

|

Net income, percent of net sales |

2.0 |

% |

2.7 |

% |

3.1 |

% |

|||||||||

|

Basic and diluted earnings per share |

$ |

2.05 |

$ |

2.67 |

$ |

3.07 | (23.2) |

% |

(13.0) |

% |

|||||

Income is earned by selling merchandise at price levels that produce revenues in excess of cost of merchandise sold and operating and administrative expenses. Although the Company may experience short term fluctuations in its earnings due to unforeseen short-term operating cost increases, it historically has been able to increase revenues and maintain stable earnings from year to year.

Net Sales

The Company's revenues are earned and cash is generated as merchandise is sold to customers at the point of sale. Discounts provided to customers by the Company at the point of sale are recognized as a reduction in sales as products are sold or over the life of a promotional program if redeemable in the future. Discounts provided by vendors, usually in the form of paper coupons, are not recognized as a reduction in sales provided the coupons are redeemable at any retailer that accepts coupons.

Total store sales increased 3.1% in 2014 compared to 2013. Excluding fuel sales, total store sales increased 2.8%. Total store sales decreased 0.3% in 2013 compared to 2012. Excluding fuel sales, total store sales decreased 0.4% in 2013 compared to 2012.

When calculating the percentage change in comparable store sales, the Company defines a new store to be comparable when it has been in operation for five full quarters. Relocated stores and stores with expanded square footage are included in comparable store sales since these units are located in existing markets and are open during construction. Planned store dispositions are excluded from the calculation. The Company only includes retail food stores in the calculation.

12

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Results of Operations (continued)

Comparable store sales increased 2.0% in 2014 compared to 2013. Excluding fuel sales, comparable store sales increased 1.7%. The 2014 sales increase is attributed to the Company’s current pricing initiatives and sales building programs. Comparable store sales decreased 2.6% in 2013 compared to 2012. Excluding fuel sales, comparable store sales decreased 2.7% in 2013 compared to 2012. The 2013 sales decline is attributed to increased competition, cycling the 2012 sales impact of Hurricane Sandy and a decline in food stamp/SNAP (the United States Department of Agriculture’s Supplemental Nutrition Assistance Program) spending in its stores, which accelerated in the fourth quarter of 2013 with the reduction in SNAP benefits that went into effect on November 1, 2013.

The Company continues to make progress in a market impacted by a slowly recovering economy. It attributes the 2014 sales increase to its continued investments in lower pricing and disciplined sales building programs. In addition to targeted promotional activity in key regional markets, the Company started an aggressive sales building program in 2014, notably its “Three Ways to Save” sales initiative, which included the seasonal “Price Freeze” or “Get Grillin’” promotional program, Everyday Lower Prices (EDLP) and Lowest Price Guarantee program. On December 29, 2013, the Company launched a twelfth round of its "Price Freeze" program. This program froze prices on more than 2,000 products for a thirteen-week period. On March 30, 2014, the Company entered into another "Get Grillin'" promotional program. The "Get Grillin'" promotional program was a fifteen-week reduced pricing program on top items throughout the store that our customers found to be the most seasonally relevant. This program lowered prices on approximately 1,200 items. The EDLP program lowered prices on more than 1,000 regularly purchased items. The Lowest Price Guarantee program offers discounts on four items every week that the Company guarantees to be the lowest compared to local competitors. Compared to 2013, the Company generated a 1.5% increase in average sales per customer transaction in 2014, while identical customer store visits increased by 0.6%. Compared to 2012, the Company generated a 0.7% increase in average sales per customer transaction in 2013, while the number of identical customer store visits declined by 3.3%.

The Company’s results also benefited from increased operational efficiencies and improved in-stock conditions at store level. In addition, the Company’s Gold Card program, an extension of its existing Preferred Club Shopper program, continues to target the Company’s best shoppers with personalized offers and strong values to help them save money. The Company also continues to offer its "Gas Rewards" program in most markets. The "Gas Rewards" program allows Weis Preferred Shoppers club card members to earn gas discounts resulting from their in-store purchases. Customers can redeem these gas discounts at Sheetz convenience stores, located in most of the Company's markets, at Manley's Mighty Mart Valero locations, in the Binghamton, NY market or at any of the twenty-seven Weis Gas-n-Go locations.

Comparable center store sales decreased by 0.2% in 2014 compared to 2013. Comparable center store sales decreased 3.4% in 2013 compared to 2012. Center store was impacted by stagnant sales performance in key center store categories, increased competition and a decline in food stamp/SNAP spending in its stores, which accelerated in the fourth quarter of 2013 with the reduction in SNAP benefits that went into effect on November 1, 2013.

Comparable dairy sales increased 3.4% in 2014 compared to 2013. These increases are mainly attributed to commodity price inflation throughout the dairy category, with milk, cheese and butter seeing the largest increases. Despite the significant commodity price inflation, the Company was able to grow unit sales ahead of remaining market in 2014 as compared to 2013, through the continual promotion of dairy products in the EDLP and Lowest Price Guarantee programs.

Comparable fresh sales increased 3.0% in 2014 compared to 2013. This increase was primarily driven by the meat, seafood, deli and food service departments.

Comparable meat sales increased 3.8% in 2014 compared to 2013. In January 2014, the Company introduced the “Great Meals Start Here” program, which focuses on superior customer service along with educating our customers about our quality and our ability to cut fresh meat within the stores. This program coupled with price inflation; more strategic meat advertising; and a focus on improving store conditions and resetting the stores to better serve our customers’ needs has contributed to the increase in meat sales. Comparable meat sales decreased 2.5% in 2013 compared to 2012. With the cost of meat rising, the Company made the strategic decision to reduce retail prices in order to encourage meat sales. The Company sold 256,084 more pounds of meat in 2013, compared to 2012. Although total tonnage of meat sold increased, comparable meat sales decreased over the previous fiscal year due to the retail price reduction strategy.

Comparable seafood sales increased 5.1% in 2014 compared to 2013. The increase is credited to the Company’s renewed attention to promoting fresh seafood items, enhancing product variety and the Company’s ongoing commitment to the EDLP program.

13

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Results of Operations (continued)

Comparable deli sales increased 2.8% in 2014 compared to 2013. The sales increase is attributed to the EDLP program, particularly in slicing meats and cheeses, an increased focus on customer service and an expanded variety in the dips and spreads category. Comparable deli sales decreased 4.6% in 2013 compared to 2012. Sales declined in 2013 as a result of emergency sales surges in October 2012, which was caused by flooding due to Hurricane Sandy, which impacted regions of Pennsylvania and southern New York, where the majority of the Company's stores are located. Customers were unable to prepare meals at home for extended periods of time in 2012, resulting in increased deli sales. Additionally, 2013 sales were negatively affected by deli salad recalls occurring in September and which continued to impact the fourth quarter of 2013, due to a disruption in supply.

Comparable food service sales increased 6.6% in 2014 compared to 2013. This increase is due to increased promotional activity on key items within the department, partially through the EDLP program; an emphasis on delivering consistent product quality; the successful launch of new items within the department; and the conversion to “fresh” fried chicken in 48 stores.

Comparable pharmacy sales increased 8.5% in 2014 compared to 2013. Pharmacy sales experienced significant price inflation in 2014 but were negatively affected in 2013 due to the conversion of brand to generic drugs. In addition to price inflation, the sales increase is also attributable to an increased number of prescriptions being filled, partially due to the Company’s in-store pet medication and medication synchronization programs. Also contributing to the increase, are some of the Company’s stores having expanded pharmacy hours and more individuals are eligible for healthcare benefits under the Affordable Care Act. Comparable pharmacy sales decreased 2.2% in 2013 compared to 2012. Pharmacy sales were impacted by a $15.3 million and a $10.4 million decline in 2013 and 2012, respectively, due to the conversion of brand drugs to generic. Generics are sold at lower retail prices, decreasing total pharmacy sales. While sales dropped significantly in dollars because of the increased utilization of generic pharmaceuticals, the number of units sold in comparable stores also decreased 0.4% in 2013 compared to 2012. As part of management's strategy to offset this decline, the Company emphasized a continued focus on immunization while implementing in-store pet medications and a medication synchronization program.

Comparable fuel sales increased 0.4% in 2014 compared to 2013. Comparable fuel sales declined 8.3% in 2013 compared to 2012. Sales were affected by fuel price deflation in 2013, which resulted in lower retail gas sales.

Management remains confident in its ability to generate sales growth in a highly competitive environment, but also understands some competitors have greater financial resources and could use these resources to take measures which could adversely affect the Company's competitive position.

Cost of Sales and Gross Profit

Cost of sales consists of direct product costs (net of discounts and allowances), distribution center and transportation costs, as well as manufacturing facility operations.

According to the latest U.S. Bureau of Labor Statistics’ report, the annual Seasonally Adjusted Food-at-Home Consumer Price Index increased 2.4% in 2014, 0.9% in 2013 and 2.4% in 2012. Even though the U.S. Bureau of Labor Statistics’ index rates may be reflective of a trend, it will not necessarily be indicative of the Company’s actual results. Despite the fluctuation of retail and wholesale prices, the Company maintained a gross profit rate of 27.1% in 2014, 27.7% in 2013 and 27.5% in 2012. The gross profit rate declined in 2014 as a result of the implementation of the Company’s Three Ways to Save sales initiative, which consisted of the EDLP and Lowest Price Guarantee programs throughout the year, the “Price Freeze” program in the first quarter and the “Get Grillin’” program in the second quarter.

The Company experienced a LIFO charge of $911,000 for 2014, compared to a charge of $692,000 for 2013 and a charge of $1.2 million for 2012. With the exception of pharmacy, the Company expects wholesale price inflation to increase slightly in 2015.

The Company's profitability is impacted by the cost of oil. Fluctuating fuel prices affect the delivered cost of product and the cost of other petroleum-based supplies. As a percentage of sales, the cost of diesel fuel used by the Company to deliver goods from its distribution center to its stores decreased by 0.02% in 2014 compared to 2013 and remained unchanged in 2013 compared to 2012. According to the U.S. Department of Energy, the 52-week average diesel fuel price for the Central Atlantic States decreased $0.01 per gallon to $4.00 per gallon as of December 22, 2014, compared to $4.01 per gallon as of December 23, 2013. Diesel fuel prices for the Central Atlantic States peaked in February 2014 at $4.36 and steadily fell to $3.39 as of December 22, 2014. Based upon the U.S. Energy Information Administration’s current projections, the Company is expecting diesel fuel prices to remain below $3.00 during 2015.

14

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Results of Operations (continued)

Although the Company experienced product cost inflation and deflation in various commodities in 2014, 2013 and 2012, management cannot accurately measure the full impact of inflation or deflation on retail pricing due to changes in the types of merchandise sold between periods, shifts in customer buying patterns and the fluctuation of competitive factors.

Operating, General and Administrative Expenses

Business operating costs including expenses generated from administration and purchasing functions, are recorded in "Operating, general and administrative expenses." Business operating costs include items such as wages, benefits, utilities, repairs and maintenance, advertising costs and credits, rent, insurance, equipment depreciation, leasehold amortization and costs for outside provided services.

The Company may not be able to recover rising expenses through increased prices charged to its customers. Any delay in the Company's response to unforeseen cost increases or competitive pressures that prevent its ability to raise prices may cause earnings to suffer. A majority of our associates are paid hourly rates related to federal and state minimum wage laws. Although we have and will continue to attempt to pass along any increased labor costs through food price increases, there can be no assurance that all such increased labor costs can be reflected in our prices or that increased prices will be absorbed by consumers without diminishing consumer spending to some degree. However, to date, we have not experienced a significant reduction in profit margins as a result of changes in such laws, and management does not anticipate any significant related future reductions in gross profit margins.

Employee-related costs such as wages, employer paid taxes, health care benefits and retirement plans, comprise approximately 60% of the total “Operating, general and administrative expenses.” Employee-related costs increased $7.7 million or 2.0% in 2014 compared to 2013 and increased $4.6 million or 1.2% in 2013 compared to 2012. As a percent of sales, employee-related costs decreased 0.2% in 2014 compared to 2013 but increased 0.2% in 2013 compared to 2012. As a percent of sales, direct store labor decreased 0.2% in 2014 compared to 2013 but increased 0.3% in 2013 compared to 2012.

The Company expensed $1.1 million, $2.0 million and $1.1 million in 2014, 2013 and 2012, respectively, due to adjustments made to the non-qualified supplemental executive retirement plan resulting from a rise in the equity market. See Note 6 Retirement Plans, of Notes to the Consolidated Financial Statements included in this Annual Report on Form 10-K for more information on the Company’s retirement plans.

The Company’s self-insured health care benefit expenses decreased 0.5% in 2014 compared to 2013 and decreased 14.9% in 2013 compared to 2012. During 2013, the Company incurred less expensive health care claims, compared to 2012. The Company remains concerned about the potential impact that The Patient Protection and Affordable Care Act will have on its future operating expenses.

On September 21, 2013, the Company entered into a separation agreement with the former President and Chief Executive Officer. The Company's "Operating, general and administrative expenses" were negatively impacted by the charge of $6.1 million worth of estimated expenses related to the separation agreement. See Exhibit 10, filed with the quarterly report on Form 10-Q filed on November 7, 2013, for more information pertaining to the separation agreement.

Depreciation and amortization expense was $66.9 million, or 2.4% of net sales, for 2014 compared to $58.3 million, or 2.2% of net sales, for 2013 and $50.7 million, or 1.9% of net sales, for 2012. The increase in depreciation and amortization expense in 2014 compared to 2013 and in 2013 compared to 2012 was the result of additional capital expenditures as the Company implements its capital expansion program. In the first quarter of 2012, the Company changed its accounting policy for property and equipment and switched the depreciation method for this group of assets from accelerated methods to straight-line. See Note 1 (j) to the Consolidated Financial Statements included in this Annual Report on Form 10-K for more information on the Company’s change in accounting estimate related to depreciation expense. See the Liquidity and Capital Resources section for further information regarding the Company’s capital expansion program.

15

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Results of Operations (continued)

The Company recognized pre-tax gains of $2.6 million, $2.9 million and $1.7 million in 2014, 2013 and 2012, respectively, from the sale of two properties in 2014 and 2013 and one property in 2012. In 2013, the Company determined that the asset value of four properties was impaired. As a result, the Company recognized a pre-tax impairment loss of $2.1 million. See Note 1(l) to the Consolidated Financial Statements included in this Annual Report on Form 10-K for more information on the Company's impairment charges. Earnings were further impacted in 2013 by a $680,000 adjustment to liabilities for future expenses on closed stores.

Retail store profitability is sensitive to volatility in utility costs due to the amount of electricity and gas required to operate the Company's stores and facilities. The Company is responding to this volatility in operating costs by employing conservation technologies, procurement strategies and associate energy awareness programs to manage and reduce consumption. The Company continues to be a member of the EPA GreenChill program for advancing environmentally beneficial refrigerant management systems. The Company was awarded the GreenChill Distinguished Partner Award for leadership in refrigerant management due to the demonstrated extraordinary leadership and initiative in achieving GreenChill’s mission in 2013. This past year, the Company received three additional Gold Level Certified Stores. In total, the Company has twelve stores registered under the EPA GreenChill program. In 2012, the Company replaced its existing lighting system at its 1.1 million square-foot distribution center with low watt fluorescent and LED lighting, reducing energy consumption by 80% and operating costs by 30%. Its new store prototypes contain skylights that harvest natural daylight to reduce lighting costs, LED lighting and motion sensors in its frozen departments and energy management systems. All Company stores have an assigned Green Leader to promote in-store energy conservation. Despite these initiatives, the Company’s utility expense increased by $2.1 million or 5.3% in 2014 compared to 2013. The increase is primarily due to higher capacity charges and below average temperatures in the Mid-Atlantic States, the Company’s operating region, in the first quarter of 2014. However, the Company’s utility expense decreased by $1.0 million or 2.6% in 2013 compared to 2012, through the aforementioned initiatives, with the added benefit of clement weather and a declining market in electricity costs.

Investment Income

The Company’s investment portfolio consists of marketable securities, which currently includes municipal bonds and equity securities, as well as the Company’s SERP investment, which is comprised of mutual funds that are maintained within the Company’s non-qualified supplemental executive retirement plan and the non-qualified pharmacist deferred compensation plan. The Company classifies all of its municipal bonds and equity securities as available-for-sale. Investment income declined $2.4 million in 2014 compared to 2013. This decrease is primarily attributed to fewer sales of equity securities and a decline in the Company’s SERP investment. The Company experienced a $1.4 million decrease in gains recognized on the sale of equity securities in 2014 compared to 2013 and the Company’s SERP investment decreased by $797,000 in 2014 compared to 2013. Investment income increased by $1.2 million in 2013 compared to 2012, primarily resulting from the $868,000 increase in gains recognized on the sale of equity securities in 2013 compared to 2012.

Other Income

Upon completion, the Company recognized a gain of $414,000 on the bargain purchase of three former Genuardi locations in the Delaware Valley region of Pennsylvania, from Safeway Inc., in the second quarter of 2012.

Provision for Income Taxes

The effective income tax rate was 35.1%, 38.1% and 37.0% in 2014, 2013 and 2012, respectively. In 2014, pre-tax book income decreased significantly. Tax exempt interest and dividends eligible for a dividends received deduction increased, causing an increase to the net favorable permanent differences. The combination of the decrease to net income before taxes and increase to the net favorable permanent differences resulted in a drop in the effective rate for 2014. The rate increased starting in 2012 due to the decrease in the domestic production deduction also referred to as the Section 199 deduction. The qualifying manufacturing sales decreased during 2012 resulting in a sizeable provision to return adjustment which results in a higher effective tax rate. The effective income tax rate differs from the federal statutory rate of 35% primarily due to the effect of state taxes, net of permanent differences.

16

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Liquidity and Capital Resources

Net cash provided by operating activities was $123.1 million in 2014, compared to $142.6 million in 2013 and $124.0 million in 2012. In 2013, management implemented new inventory control buying procedures that increased distribution center efficiencies. Under these new buying procedures, the distribution center inventory level decreased an average of $9.8 million per period during 2014 compared to 2013 and $7.0 million during the last nine fiscal months of 2013 compared to the same period in 2012. The Company's overall inventory level only decreased by $811,000 in 2014 compared to 2013 and $4.8 million in 2013 compared to 2012 as a result of holding more inventory at year end for the holidays and the addition of larger stores during each year. Working capital increased 5.8% in 2014, decreased 7.9% in 2013 and increased 2.7% in 2012, in each case compared to the prior year. The 2014 working capital increase is primarily attributed to the lower investment in the Company’s capital expansion program during 2014 compared to the previous years. Whereas, the 2013 decrease in working capital is primarily due to the utilization of marketable securities to fund the Company’s capital expansion program.

Net cash used in investing activities was $85.8 million in 2014 compared to $106.8 million in 2013 and $107.8 million in 2012. These funds were used primarily to purchase marketable securities and property and equipment in the three fiscal years presented. While the Company purchased marketable securities in all three years presented, the Company’s net marketable securities transactions resulted in the purchase of $8.4 million in 2014, compared to the disposal of $18.7 million in 2013 and the sale of $6.2 million in 2012. Property and equipment purchases totaled $79.2 million in 2014, compared to $128.1 million in 2013 and $115.9 million in 2012, which included the acquisition of a business in 2012. The Company acquired three former Genuardi stores for $6.1 million in 2012. As a percentage of sales, capital expenditures including the acquisition were 2.9%, 4.8% and 4.3% in 2014, 2013 and 2012, respectively. Proceeds from the sale of property and equipment decreased $837,000 in 2014 compared to 2013 despite the sale of properties in each of the first and third quarters of 2014 for a total of $2.8 million. Proceeds from the sale of property and equipment increased $1.9 million in 2013 compared to 2012, primarily due to the sale of two properties for $3.2 million in the second quarter of 2013.

The Company’s capital expansion program includes the construction of new superstores, the expansion and remodeling of existing units, the acquisition of sites for future expansion, new technology purchases and the continued upgrade of the Company’s distribution facilities and transportation fleet. Management estimates that its current development plans will require an investment of approximately $91.8 million in 2015.

Net cash used in financing activities was $32.3 million in 2014, 2013 and 2012, which solely consisted of dividend payments to shareholders. At December 27, 2014, the Company had outstanding letters of credit of $19.9 million. The letters of credit are maintained primarily to support performance, payment, deposit or surety obligations of the Company. The Company does not anticipate drawing on any of them.

Total cash dividend payments on common stock, on a per share basis, amounted to $1.20 in 2014, 2013 and 2012. No treasury stock was purchased in 2014, 2013 or 2012. The Board of Directors’ 2004 resolution authorizing the repurchase of up to one million shares of the Company’s common stock has a remaining balance of 752,468 shares.

The Company has no other commitment of capital resources as of December 27, 2014, other than the lease commitments on its store facilities under operating leases that expire at various dates through 2029. The Company anticipates funding its working capital requirements and its $91.8 million capital expansion program through cash and investment reserves and future internally generated cash flows from operations.

17

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Liquidity and Capital Resources (continued)

The Company’s earnings and cash flows are subject to fluctuations due to changes in interest rates as they relate to available-for-sale securities and any future long-term debt borrowings. The Company’s marketable securities portfolio currently consists of municipal bonds and equity securities. Other short-term investments are classified as cash equivalents on the Consolidated Balance Sheets.

Under its current policies, the Company invests in high-grade marketable debt securities and does not use interest rate derivative instruments to manage exposure to interest rate fluctuations. Currently, the Company’s investment strategy of obtaining marketable debt securities with maturity dates between one and ten years helps to minimize market risk and to maintain a balance between risk and return. The equity securities owned by the Company consist primarily of stock held in large capitalized companies trading on public security exchange markets. The Company’s management continually monitors the risk associated with its marketable securities. A quantitative tabular presentation of risk exposure is located in “Item 7a. Quantitative and Qualitative Disclosures about Market Risk” of this report.

By their nature, these financial instruments inherently expose the holders to market risk. The extent of the Company’s interest rate and other market risk is not quantifiable or predictable with precision due to the variability of future interest rates and other changes in market conditions. However, the Company believes that its exposure in this area is not material.

The Company experienced an unrealized holding gain net of deferred taxes of $927,000 in 2014 and unrealized holding losses net of deferred taxes of $36,000 in 2013 and $9,000 in 2012 (see Consolidated Statements of Comprehensive Income). As of December 27, 2014, the Company had $8.3 million in gross unrealized holding gains and $96,000 in gross unrealized holding losses related to marketable securities. See Note 2 Marketable Securities, of Notes to the Consolidated Financial Statements included in this Annual Report on Form 10-K for more information on the Company’s marketable securities.

Contractual Obligations

The following table represents scheduled maturities of the Company’s long-term contractual obligations as of December 27, 2014.

|

Payments due by period |

||||||||||

|

Less than |

More than |

|||||||||

|

(dollars in thousands) |

Total |

1 year |

1-3 years |

3-5 years |

5 years |

|||||

|

Operating leases |

$ |

199,974 |

$ |

32,826 |

$ |

58,593 |

$ |

43,258 |

$ |

65,297 |

|

Total |

$ |

199,974 |

$ |

32,826 |

$ |

58,593 |

$ |

43,258 |

$ |

65,297 |

Off-Balance Sheet Arrangements

The Company is not a party to any off-balance sheet arrangements that have, or are reasonably likely to have, a current or future effect on the Company’s financial condition, results of operations or cash flows, except for the possibility that the Financial Accounting Standards Board could require the Company's store leases to be recognized on the balance sheet.

Critical Accounting Policies and Estimates

The Company has chosen accounting policies that it believes are appropriate to accurately and fairly report its operating results and financial position, and the Company applies those accounting policies in a consistent manner. The Significant Accounting Policies are summarized in Note 1 to the Consolidated Financial Statements. In the first quarter of 2012, the Company changed its accounting policy for the depreciation of property and equipment. See Note 1 (j) to the Consolidated Financial Statements included in this Annual Report on Form 10-K for more information on the Company’s change in accounting estimate related to depreciation expense.

18

WEIS MARKETS, INC.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations: (continued)

Critical Accounting Policies and Estimates (continued)

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires that the Company makes estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses. These estimates and assumptions are based on historical and other factors believed to be reasonable under the circumstances. The Company evaluates these estimates and assumptions on an ongoing basis and may retain outside consultants, lawyers and actuaries to assist in its evaluation. The Company believes the following accounting policies are the most critical because they involve the most significant judgments and estimates used in preparation of its consolidated financial statements.

Inventories

Inventories are valued at the lower of cost or market, using both the last-in, first-out (LIFO) and average cost methods. The Company’s center store and pharmacy inventories are valued using LIFO and the Company’s fresh inventories are valued using average cost. The Company evaluates inventory shortages throughout the year based on actual physical counts in its facilities. Allowances for inventory shortages are recorded based on the results of these counts and to provide for estimated shortages from the last physical count to the financial statement date.

Property and Equipment

In the first quarter of 2012, the Company changed its accounting policy for property and equipment. Property and equipment continue to be recorded at cost. Prior to January 1, 2012, the Company provided for depreciation of buildings and improvements and equipment using accelerated methods. Effective January 1, 2012, the Company changed its method of depreciation for this group of assets from the accelerated methods to straight-line. Management deemed the change preferable because the straight-line method will more accurately reflect the pattern of usage and the expected benefits of such assets. Management also considered that the change will provide greater consistency with the depreciation methods used by other companies in the Company's industry. The change was accounted for as a change in accounting estimate effected by a change in accounting principle. The net book value of assets acquired prior to January 1, 2012 with useful lives remaining will be depreciated using the straight-line method prospectively. If the Company had continued using accelerated methods, depreciation expense would have been $11.5 million greater in 2012. Had accelerated methods continued to be used, after considering the impact of income taxes, the effect would decrease net income by $6.8 million or $.25 per share in 2012.

Leasehold improvements are unaffected by the change noted above. Leasehold improvements continue to be amortized using the straight line method over the terms of the leases or the useful lives of the assets, whichever is shorter.

Maintenance and repairs are expensed and renewals and betterments are capitalized. When assets are retired or otherwise disposed of, the assets and accumulated depreciation are removed from the respective accounts and any profit or loss on the disposition is credited or charged to “Operating, general and administrative expenses.”

Goodwill and Intangible Assets

Intangible assets with an indefinite useful life are not amortized until their useful life is determined to be no longer indefinite and are tested for impairment annually or more frequently if events or changes in circumstances indicate that the asset might be impaired. Goodwill is not amortized but tested for impairment for each reporting unit on an annual basis and between annual tests in certain circumstances.