Form 424B2 WELLS FARGO & COMPANY/MN

Filed Pursuant to Rule 424(b)(2)

File No. 333-221324

| Title of Each Class of Securities Offered |

Maximum Aggregate Offering Price |

Amount of Registration Fee(1) |

||||||

| Medium-Term Notes, Series S, Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index |

$56,793,870 | $7,070.84 | ||||||

| (1) | The total filing fee of $7,070.84 is calculated in accordance with Rule 457(r) of the Securities Act of 1933 (the “Securities Act”) and will be paid by wire transfer within the time required by Rule 456(b) of the Securities Act. |

| Pricing Supplement No. 14 (To Product Supplement No. EQUITY INDICES LIRN-1 dated February 27, 2018, Prospectus Supplement dated January 24, 2018 and Prospectus dated November 3, 2017) |

Filed Pursuant to Rule 424(b)(2) Registration Statement No. 333-221324 |

|

5,679,387 Units $10 principal amount per unit CUSIP No. 94988U540 |

Pricing Date Settlement Date Maturity Date |

March 28, 2018 April 5, 2018 March 26, 2021 | ||||

|

||||||

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index | ||||||

| ◾ | 1-to-1 downside exposure to decreases in the Index beyond a 25% decline, with up to 75% of your principal at risk | |||||

| ◾ | Maturity of approximately three years | |||||

| ◾ | 149.05% leveraged upside exposure to increases in the Index | |||||

| ◾ | All payments occur at maturity and are subject to the credit risk of Wells Fargo & Company; if Wells Fargo & Company defaults on its obligations, you could lose some or all of your investment | |||||

| ◾ | No periodic interest payments or dividends | |||||

| ◾ | In addition to the underwriting discount set forth below, the notes include a hedging-related charge of $0.075 per unit. See “Structuring the Notes” | |||||

| ◾ | Limited secondary market liquidity, with no exchange listing; intended to be held to maturity | |||||

| ◾ | The notes are unsecured obligations of Wells Fargo & Company. The notes are not deposits or other obligations of a depository institution and are not insured by the Federal Deposit Insurance Corporation, the Deposit Insurance Fund or any other governmental agency of the United States or any other jurisdiction

|

|||||

The notes are being issued by Wells Fargo & Company (“Wells Fargo”). The notes have complex features and investing in the notes involves risks not associated with an investment in conventional debt securities. See “Risk Factors” beginning on page TS-7 of this term sheet and beginning on page PS-6 of product supplement EQUITY INDICES LIRN-1.

The initial estimated value of the notes as of the pricing date is $9.68 per unit, which is less than the public offering price listed below. The initial estimated value of the notes was determined for us as of the date of this term sheet by Wells Fargo Securities, LLC using its proprietary pricing models. The actual value of your notes at any time will reflect many factors and cannot be predicted with accuracy. See “Summary” on the following page, “Risk Factors” beginning on page TS-7 of this term sheet and “Structuring the Notes” on page TS-14 of this term sheet for additional information.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this Note Prospectus (as defined below) is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit | Total | |||||||

| Public offering price |

$ | 10.000 | $ | 56,793,870.000 | ||||

| Underwriting discount |

$ | 0.225 | $ | 1,277,862.075 | ||||

| Proceeds, before expenses, to Wells Fargo |

$ | 9.775 | $ | 55,516,007.925 | ||||

The notes:

|

Are Not FDIC Insured

|

Are Not Bank Guaranteed

|

May Lose Value

|

Merrill Lynch & Co.

March 28, 2018

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

Summary

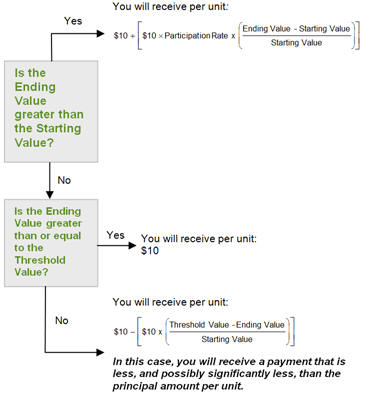

The Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021 (the “notes”) are our senior unsecured debt securities. The notes are not deposits or other obligations of a depository institution and are not insured by the Federal Deposit Insurance Corporation, the Deposit Insurance Fund or any other governmental agency of the United States or any other jurisdiction. The notes will rank equally with all of our other unsecured and unsubordinated debt. Any payments due on the notes, including any repayment of principal, will be subject to the credit risk of Wells Fargo. The notes provide you a leveraged return if the Ending Value of the Market Measure, which is the EURO STOXX 50® Index (the “Index”), is greater than its Starting Value. If the Ending Value is equal to or less than the Starting Value but greater than or equal to the Threshold Value, you will receive the principal amount of your notes. If the Ending Value is less than the Threshold Value, you will lose a portion, which could be significant, of the principal amount of your notes. Any payments on the notes will be calculated based on the $10 principal amount per unit and will depend on the performance of the Index, subject to our credit risk. See “Terms of the Notes” and “The Index” below.

The public offering price of each note of $10 includes certain costs that are borne by you. Because of these costs, the estimated value of the notes on the pricing date is less than the public offering price. The costs included in the public offering price relate to selling, structuring, hedging and issuing the notes, as well as to our funding considerations for debt of this type.

The costs related to selling, structuring, hedging and issuing the notes include (a) the underwriting discount, (b) the projected profit that our hedge counterparty (which may be MLPF&S or one of its affiliates) expects to realize for assuming risks inherent in hedging our obligations under the notes and (c) hedging and other costs relating to the offering of the notes.

Our funding considerations take into account the higher issuance, operational and ongoing management costs of market-linked debt such as the notes as compared to our conventional debt of the same maturity, as well as our liquidity needs and preferences. Our funding considerations are reflected in the fact that we determine the economic terms of the notes based on an assumed funding rate that is generally lower than the interest rates implied by secondary market prices for our debt obligations and/or by other traded instruments referencing our debt obligations, which we refer to as our “secondary market rates.” As discussed below, our secondary market rates are used in determining the estimated value of the notes.

If the costs relating to selling, structuring, hedging and issuing the notes were lower, or if the assumed funding rate we use to determine the economic terms of the notes were higher, the economic terms of the notes would be more favorable to you and the estimated value would be higher. The initial estimated value of the notes as of the pricing date is set forth on the cover page of this term sheet.

Our affiliate, Wells Fargo Securities, LLC (“WFS”), calculated the initial estimated value of the notes set forth on the cover page of this term sheet, based on its proprietary pricing models. Based on WFS’s proprietary pricing models and related market inputs and assumptions, WFS determined an estimated value for the notes by estimating the value of the combination of hypothetical financial instruments that would replicate the payout on the notes, which combination consists of a non-interest bearing, fixed-income bond (the “debt component”) and one or more derivative instruments underlying the economic terms of the notes (the “derivative component”). For more information about the initial estimated value and the structuring of the notes, see “Risk Factors” beginning on page TS-7 of this term sheet and “Structuring the Notes” on page TS-14 of this term sheet.

| Leveraged Index Return Notes® |

TS-2 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

| Terms of the Notes | Redemption Amount Determination | |||

|

Issuer: |

Wells Fargo & Company (“Wells Fargo”) |

On the maturity date, you will receive a cash payment per unit determined as follows:

| ||

|

Principal Amount: |

$10.00 per unit |

|||

|

Term: |

Approximately three years |

|||

|

Market Measure: |

The EURO STOXX 50® Index (Bloomberg symbol: “SX5E”), a price return index |

|||

|

Starting Value: |

3,331.25 |

|||

|

Ending Value: |

The average of the closing levels of the Market Measure on each calculation day occurring during the maturity valuation period. The scheduled calculation days are subject to postponement in the event of Market Disruption Events, as described on page PS-19 of product supplement EQUITY INDICES LIRN-1. |

|||

|

Threshold Value: |

2,498.44 (75% of the Starting Value, rounded to two decimal places). |

|||

|

Participation Rate: |

149.05% |

|||

|

Maturity Valuation Period: |

March 17, 2021, March 18, 2021, March 19, 2021, March 22, 2021 and March 23, 2021 |

|||

|

Fees and Charges: |

The underwriting discount of $0.225 per unit listed on the cover page and the hedging related charge of $0.075 per unit. See “Structuring the Notes” on page TS-14. |

|||

|

Joint Calculation Agents: |

WFS and Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”), acting jointly. |

|||

The terms and risks of the notes are contained in this term sheet and in the following:

| ◾ | Product supplement EQUITY INDICES LIRN-1 dated February 27, 2018: https://www.sec.gov/Archives/edgar/data/72971/000119312518060466/d506913d424b2.htm |

| ◾ | Prospectus supplement dated January 24, 2018: https://www.sec.gov/Archives/edgar/data/72971/000119312518018256/d466041d424b2.htm |

| ◾ | Prospectus dated November 3, 2017:

https://www.sec.gov/Archives/edgar/data/72971/000119312518018238/d528188d424b2.htm |

These documents (together, the “Note Prospectus”) have been filed as part of a registration statement with the SEC, which may, without cost, be accessed on the SEC website as indicated above or obtained from MLPF&S by calling 1-800-294-1322. Before you invest, you should read the Note Prospectus, together with this term sheet, for information about us and this offering. Any prior or contemporaneous oral statements and any other written materials you may have received are superseded by the Note Prospectus. Capitalized terms used but not defined in this term sheet have the meanings set forth in product supplement EQUITY INDICES LIRN-1. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to Wells Fargo.

“Leveraged Index Return Notes®” and “LIRNs®” are registered service marks of Bank of America Corporation, the parent company of MLPF&S.

| Leveraged Index Return Notes® |

TS-3 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

Investor Considerations

We urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| Leveraged Index Return Notes® |

TS-4 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

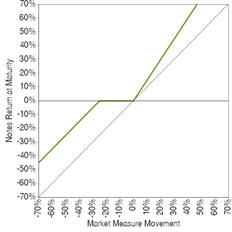

Hypothetical Payout Profile

Hypothetical Payments at Maturity

The following table and examples are for purposes of illustration only. They are based on hypothetical values and show hypothetical returns on the notes. They illustrate the calculation of the Redemption Amount and total rate of return based on a hypothetical Starting Value of 100, a hypothetical Threshold Value of 75, the Participation Rate of 149.05%, a hypothetical public offering price of $10.00 per unit and a range of hypothetical Ending Values. The actual amount you receive and the resulting total rate of return will depend on the actual Starting Value, Threshold Value, Ending Value, the actual price you pay for the notes and whether you hold the notes to maturity. The following examples do not take into account any tax consequences from investing in the notes.

For recent actual levels of the Index, see “The Index” section below. The Index is a price return index and as such the Ending Value will not include any income generated by dividends paid on the stocks included in the Index, which you would otherwise be entitled to receive if you invested in those stocks directly. In addition, all payments on the notes are subject to issuer credit risk.

| Ending Value |

Percentage Change from the Starting Value to the Ending Value |

Redemption Amount per Unit |

Total Rate of Return on the Notes | |||

| 0.00 | -100.00% | $2.50000 | -75.0000% | |||

| 50.00 | -50.00% | $7.50000 | -25.0000% | |||

| 65.00 | -35.00% | $9.00000 | -10.0000% | |||

| 75.00(1) | -25.00% | $10.00000 | 0.0000% | |||

| 80.00 | -20.00% | $10.00000 | 0.0000% | |||

| 90.00 | -10.00% | $10.00000 | 0.0000% | |||

| 95.00 | -5.00% | $10.00000 | 0.0000% | |||

| 100.00(2) | 0.00% | $10.00000 | 0.0000% | |||

| 105.00 | 5.00% | $10.74525 | 7.4525% | |||

| 110.00 | 10.00% | $11.49050 | 14.9050% | |||

| 120.00 | 20.00% | $12.98100 | 29.8100% | |||

| 130.00 | 30.00% | $14.47150 | 44.7150% | |||

| 140.00 | 40.00% | $15.96200 | 59.6200% | |||

| 150.00 | 50.00% | $17.45250 | 74.5250% | |||

| 160.00 | 60.00% | $18.94300 | 89.4300% |

| (1) | This is the hypothetical Threshold Value. |

| (2) | The hypothetical Starting Value of 100 used in these examples has been chosen for illustrative purposes only. The actual Starting Value is 3,331.25, which was the closing level of the Market Measure on the pricing date. |

| Leveraged Index Return Notes® |

TS-5 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

Redemption Amount Calculation Examples

Example 1

The Ending Value is 50.00, or 50.00% of the Starting Value:

| Starting Value: | 100.00 |

| Threshold Value: | 75.00 |

| Ending Value: | 50.00 |

| $10 – | $10 × | (

|

75 – 50 100 |

)

|

= $7.50 Redemption Amount per unit | |||||||||||

Example 2

The Ending Value is 90.00, or 90.00% of the Starting Value:

| Starting Value: | 100.00 |

| Threshold Value: | 75.00 |

| Ending Value: | 90.00 |

Redemption Amount (per unit) = $10.00, the principal amount, since the Ending Value is less than the Starting Value but equal to or greater than the Threshold Value.

Example 3

The Ending Value is 150.00, or 150.00% of the Starting Value:

| Starting Value: | 100.00 |

| Ending Value: | 150.00 |

| $10 + | $10 × 149.05% × | (

|

150 – 100 100 |

)

|

= $17.4525 Redemption Amount per unit |

| Leveraged Index Return Notes® |

TS-6 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

Risk Factors

There are important differences between the notes and a conventional debt security. An investment in the notes involves significant risks, including those listed below. You should carefully review the more detailed explanation of risks relating to the notes in the “Risk Factors” sections beginning on page PS-6 of product supplement EQUITY INDICES LIRN-1 identified above. We also urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| ◾ | Depending on the performance of the Index as measured shortly before the maturity date, your investment may result in a loss; there is no guaranteed return of principal. As a result, even if the value of the Index has increased at certain times during the term of the notes, if the Ending Value is less than the Threshold Value, you will receive less than, and possibly lose a significant portion of, your principal amount. |

| ◾ | Your return on the notes may be less than the yield you could earn by owning a conventional fixed or floating rate debt security of comparable maturity. There will be no periodic interest payments on notes as there would be on a conventional fixed-rate or floating-rate debt security having the same maturity. |

| ◾ | The notes are subject to the credit risk of Wells Fargo. The notes are our obligations and are not, either directly or indirectly, an obligation of any third party. Any amounts payable under the notes are subject to our creditworthiness, and you will have no ability to pursue any securities included in the Index for payment. As a result, our actual and perceived creditworthiness may affect the value of the notes and, in the event we were to default on our obligations, you may not receive any amounts owed to you under the terms of the notes. |

| ◾ | Your investment return may be less than a comparable investment directly in the stocks included in the Index. |

| ◾ | The estimated value of the notes is determined by our affiliate’s pricing models, which may differ from those of MLPF&S or other dealers. The estimated value of the notes was determined for us by WFS using its proprietary pricing models and related market inputs and assumptions. Based on these pricing models and related market inputs and assumptions, WFS determined an estimated value for the notes by estimating the value of the combination of hypothetical financial instruments that would replicate the payout on the notes, which combination consists of a non-interest bearing, fixed-income bond (the “debt component”) and one or more derivative instruments underlying the economic terms of the notes (the “derivative component”). |

The estimated value of the debt component is based on a reference interest rate, determined by WFS as of a date near the time of calculation that generally tracks our secondary market rates. Because WFS does not continuously calculate our reference interest rate, the reference interest rate used in the calculation of the estimated value of the debt component may be higher or lower than our secondary market rates at the time of that calculation. Because the reference interest rate is generally higher than the assumed funding rate that is used to determine the economic terms of the notes, using the reference interest rate to value the debt component generally results in a lower estimated value for the debt component, which we believe more closely approximates a market valuation of the debt component than if we had used the assumed funding rate. WFS calculated the estimated value of the derivative component based on a proprietary derivative-pricing model, which generated a theoretical price for the derivative instruments that constitute the derivative component based on various inputs, including, but not limited to, Index performance; interest rates; volatility of the Index; volatility of the U.S. dollar/euro exchange rate; correlation between that exchange rate and the level of the Index; the time remaining to maturity; and dividend yields on the securities included in the Index. These inputs may be market-observable or may be based on assumptions made by WFS in its discretion.

The estimated value of the notes is not an independent third-party valuation and certain inputs to these models may be determined by WFS in its discretion. WFS’s views on these inputs may differ from those of MLPF&S and other dealers, and WFS’s estimated value of the notes may be higher, and perhaps materially higher, than the estimated value of the notes that would be determined by MLPF&S or other dealers in the market. WFS’s models and its inputs and related assumptions may prove to be wrong and therefore not an accurate reflection of the value of the notes.

| ◾ | The estimated value of the notes on the pricing date, based on WFS’s proprietary pricing models, is less than the public offering price. The public offering price of the notes includes certain costs that are borne by you. Because of these costs, the estimated value of the notes on the pricing date is less than the public offering price. The costs included in the public offering price relate to selling, structuring, hedging and issuing the notes, as well as to our funding considerations for debt of this type. The costs related to selling, structuring, hedging and issuing the notes include the underwriting discount, the projected profit that our hedge counterparty (which may be MLPF&S or one of its affiliates) expects to realize for assuming risks inherent in hedging our obligations under the notes and hedging and other costs relating to the offering of the notes. Our funding considerations are reflected in the fact that we determine the economic terms of the notes based on an assumed funding rate that is generally lower than our secondary market rates. If the costs relating to selling, structuring, hedging and issuing the notes were lower, or if the assumed funding rate we use to determine the economic terms of the notes were higher, the economic terms of the notes would be more favorable to you and the estimated value would be higher. |

| ◾ | The public offering price you pay for the notes exceeds the initial estimated value. If you attempt to sell the notes prior to maturity, their market value may be lower than the price you paid for them and lower than the initial estimated value. This is due to, among other things, the assumed funding rate used to determine the economic terms of the notes, and the inclusion in the public offering price of the underwriting discount and the estimated cost of hedging our obligations under the notes (which |

| Leveraged Index Return Notes® |

TS-7 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

| includes a hedging related charge), as further described in “Structuring the Notes” on page TS-14. These factors, together with customary bid ask spreads, other transaction costs and various credit, market and economic factors over the term of the notes, including changes in the level of the Index, are expected to reduce the price at which you may be able to sell the notes in any secondary market and will affect the value of the notes in complex and unpredictable ways. |

| ◾ | The initial estimated value does not represent the price at which we, MLPF&S or any of our respective affiliates would be willing to purchase your notes in any secondary market (if any exists) at any time. The value of your notes at any time after issuance will vary based on many factors that cannot be predicted with accuracy, including the performance of the Index, our creditworthiness and changes in market conditions. MLPF&S has advised us that any repurchases by them or their affiliates are expected to be made at prices determined by reference to their pricing models and at their discretion, and these prices will include MLPF&S’s trading commissions and mark-ups. If you sell your notes to a dealer other than MLPF&S in a secondary market transaction, the dealer may impose its own discount or commission. |

| ◾ | The notes will be not listed on any securities exchange or quotation system and a trading market is not expected to develop for the notes. None of us, MLPF&S or any of our respective affiliates is obligated to make a market for, or to repurchase, the notes. There is no assurance that any party will be willing to purchase your notes at any price in the secondary market. If a secondary market does exist, it may be limited, which may affect the price you receive upon any sale. Consequently, you should be willing to hold the notes until the maturity date. |

| ◾ | If you attempt to sell the notes prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the principal amount. The following factors are expected to affect the value of the notes: value of the Index at such time; volatility of the Index; economic and other conditions generally; interest rates; dividend yields; exchange rate movements and volatility; our creditworthiness; and time to maturity. |

| ◾ | Our trading, hedging and other business activities, and those of the agents or one or more of our respective affiliates, may affect your return on the notes and their market value and create conflicts of interest with you. Our business, hedging and trading activities, and those of MLPF&S and our respective affiliates (including trading in shares of companies included in the Index), and any hedging and trading activities we, MLPF&S or our respective affiliates engage in for our clients’ accounts, may adversely affect the level of the Index and, therefore, adversely affect the market value of and return on the notes and may create conflicts of interest with you. We, the agents, and our respective affiliates may also publish research reports on the Index or one of the companies included in the Index, which may be inconsistent with an investment in the notes and may adversely affect the level of the Index. For more information about the hedging arrangements related to the notes, see “Structuring the Notes” on page TS-14. |

| ◾ | You must rely on your own evaluation of the merits of an investment linked to the Index. |

| ◾ | The Index sponsor may adjust the Index in a way that affects its level, and has no obligation to consider your interests. |

| ◾ | You will have no rights of a holder of the securities included in the Index, and you will not be entitled to receive securities or dividends or other distributions by the issuers of those securities. |

| ◾ | While we, MLPF&S or our respective affiliates may from time to time own securities of companies included in the Index, we, MLPF&S and our respective affiliates do not control any company included in the Index, and have not verified any disclosure made by any company. |

| ◾ | Your return on the notes may be affected by factors affecting the international securities markets, specifically changes in the countries represented by the Index. In addition, you will not obtain the benefit of any increase in the value of the euro against the U.S. dollar which you would have received if you had owned the securities included in the Index during the term of your notes, although the level of the Index may be adversely affected by general exchange rate movements in the market. |

| ◾ | There may be potential conflicts of interest involving the calculation agents, one of which is our affiliate and one of which is MLPF&S. As joint calculation agents, we will determine any values of the Index and make any other determination necessary to calculate any payments on the notes. In making these determinations, we may be required to make discretionary judgments that may adversely affect any payments on the notes. See the sections entitled “Description of LIRNs—Market Disruption Events,” “—Adjustments to an Index,” and “—Discontinuance of an Index” in the accompanying product supplement. |

| ◾ | The U.S. federal tax consequences of the notes are uncertain, and may be adverse to a holder of the notes. See “United States Federal Income Tax Considerations” below, “Risk Factors—General Risks Relating to LIRNs—The U.S. federal tax consequences of an investment in the LIRNs are unclear” beginning on page PS-12 of product supplement EQUITY INDICES LIRN-1 and “United States Federal Tax Considerations” beginning on page PS-29 of product supplement EQUITY INDICES LIRN-1. |

| Leveraged Index Return Notes® |

TS-8 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

Other Terms of the Notes

The following definition shall supersede and replace the definition of a “Market Measure Business Day” set forth in product supplement EQUITY INDICES LIRN-1.

Market Measure Business Day

A “Market Measure Business Day” means a day on which:

(A) the Eurex (or any successor) is open for trading; and

(B) the Index or any successor thereto is calculated and published.

The Index

All disclosures contained in this term sheet regarding the Index, including, without limitation, its make-up, method of calculation, and changes in its components, have been derived from publicly available sources. That information reflects the policies of, and is subject to change by, the index sponsor. The consequences of the index sponsor discontinuing publication of the Index are discussed in the section entitled “Description of LIRNs—Discontinuance of an Index” on page PS-20 of product supplement EQUITY INDICES LIRN-1. None of us, the calculation agents, or MLPF&S has independently verified the accuracy or completeness of any information with respect to the Index in connection with the notes, nor accepts any responsibility for the calculation, maintenance or publication of the Index or any successor index.

In addition, information about the Index may be obtained from other sources including, but not limited to, the index sponsor’s website (including information regarding the Index’s sector weightings and country weights). We are not incorporating by reference into this term sheet the website or any material it includes. Neither we nor the agent makes any representation that such publicly available information regarding the Index is accurate or complete.

The Index is calculated, maintained and published by STOXX, a wholly owned subsidiary of Deutsche Börse AG. Publication of the Index began on February 26, 1998, based on an initial index value of 1,000 on December 31, 1991. The Index is published in The Wall Street Journal and disseminated on STOXX’s website.

The Index does not reflect the payment of dividends on the stocks underlying it and therefore the payment on the notes will not produce the same return you would receive if you were able to purchase such underlying stocks and hold them until maturity.

Index Composition

The Index is composed of 50 component stocks of market sector leaders in terms of free-float market capitalization from within the EURO STOXX Supersector indexes, which includes stocks selected from 11 Eurozone countries: Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain. At any given time, some eligible countries may not be represented in the Index. The component stocks have a high degree of liquidity and represent the largest companies across all supersectors as defined by the Industry Classification Benchmark.

Component Selection. The composition of the Index is reviewed by STOXX annually in September. Within each of the 19 EURO STOXX Supersector indexes, the respective index component stocks are ranked by free-float market capitalization. The largest stocks are added to the selection list until the coverage is close to, but still less than, 60% of the free-float market capitalization of the corresponding EURO STOXX Total Market Index Supersector Index. If the next highest-ranked stock brings the coverage closer to 60% in absolute terms, then it is also added to the selection list. All remaining stocks that are current Index components are then added to the selection list. The stocks on the selection list are then ranked by free-float market capitalization. The 40 largest stocks on the selection list are chosen as index components. The remaining 10 stocks are then selected from the largest current stocks ranked between 41 and 60. If the number of index components is still below 50, then the largest remaining stocks on the selection list are added until the Index contains 50 stocks.

Ongoing Maintenance of Component Stocks

The component stocks of the Index are monitored on an ongoing monthly basis for deletion and quarterly basis for addition. Changes to the composition of the Index due to corporate actions (including mergers and takeovers, spin-offs, sector changes and bankruptcy) are announced immediately, implemented two trading days later and become effective on the next trading day after implementation.

The component stocks of the Index are subject to a “fast exit” rule. A component stock is deleted if it ranks 75 or below on the monthly selection list and it ranked 75 or below on the selection list of the previous month. The highest-ranked non-component stock will replace the exiting component stock. The Index is also subject to a “fast entry” rule. All stocks on the latest selection lists and initial public offering (IPO) stocks are reviewed for a fast-track addition on a quarterly basis. A stock is added if it qualifies for the latest blue-chip

| Leveraged Index Return Notes® |

TS-9 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

selection list generated at the end of February, May, August or November and if it ranks within the lower buffer (between 1 and 25) on the selection list. If added, the stock replaces the smallest component stock.

A deleted stock is replaced immediately to maintain the fixed number of stocks. The replacement is based on the latest monthly selection list. In the case of a merger or takeover where a component stock is involved, the original component stock is replaced by the new component stock. In the case of a spin-off, if the original stock was a component stock, then each spin-off stock qualifies for addition if it lies within the higher buffer on the latest selection list. The largest qualifying spin-off stock replaces the original component stock, while the next qualifying spin-off stock replaces the lowest ranked component stock and likewise for other qualifying spin-off stocks.

The free float factors and outstanding number of shares for each component stock that STOXX uses to calculate the Index, as described below, are reviewed, calculated and implemented on a quarterly basis and are fixed until the next quarterly review. Certain extraordinary adjustments to the free float factors and/or the number of outstanding shares are implemented and made effective more quickly. The timing depends on the magnitude of the change. Each component’s weight is capped at 10% of the Index’s total free float market capitalization. The free float factor reduces the component stock’s number of shares to the actual amount available on the market. All holdings that are larger than five percent of the total outstanding number of shares and held on a long-term basis are excluded from the index calculation (including, but not limited to, stock owned by the company itself, stock owned by governments, stock owned by certain individuals or families, and restricted shares).

Calculation of the Index

The Index is calculated with the “Laspeyres formula,” which measures the aggregate price changes in the component stocks against a fixed base quantity weight. The formula for calculating the Index value can be expressed as follows:

| Index = |

Free-float market capitalization of the Index |

|||||

| Divisor |

The “free-float market capitalization of the Index” is equal to the sum of the products of the closing price, the number of shares, the free float factor and the weighting cap factor for each component stock as of the time the Index is being calculated. The component stocks trade in euros and thus, no currency conversion is required. The cap factor limits the weight of a component within the Index to a maximum of 10%.

The Index is also subject to a divisor, which is adjusted to maintain the continuity of the Index values across changes due to corporate actions. The following is a summary of the adjustments to any component stock made for corporate actions and the effect of such adjustment on the divisor, where shareholders of the component stock will receive “B” number of shares for every “A” share held (where applicable).

| (1) | Special cash dividend |

Cash distributions that are outside the scope of the regular dividend policy or that the company defines as an extraordinary distribution.

Adjusted price = closing price – dividend announced by the company * (1 – withholding tax, if applicable)

Divisor: decreases

| (2) | Split and reverse split: |

Adjusted price = closing price * A/B

New number of shares = old number of shares * B/A

Divisor: no change

| (3) | Rights offering: |

Adjusted price = (closing price * A + subscription price * B) / (A + B)

New number of shares = old number of shares * (A + B) / A

Divisor: increases

| (4) | Stock dividend: |

Adjusted price = closing price * A / (A + B)

New number of shares = old number of shares * (A + B) / A

Divisor: no change

| (5) | Stock dividend from treasury stock (if treated as extraordinary dividend): |

Adjusted close = close – close * B / (A + B)

Divisor: decreases

| Leveraged Index Return Notes® |

TS-10 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

| (6) | Stock dividend of another company: |

Adjusted price = (closing price * A – price of other company * B) / A

Divisor: decreases

| (7) | Return of capital and share consolidation: |

Adjusted price = (closing price – capital return announced by company * (1 – withholding tax)) * A / B

New number of shares = old number of shares * B / A

Divisor: decreases

| (8) | Repurchase shares / self tender: |

Adjusted price = ((price before tender * old number of shares) – (tender price * number of tendered shares)) / (old number of shares – number of tendered shares)

New number of shares = old number of shares – number of tendered shares

Divisor: decreases

| (9) | Spin-off: |

Adjusted price = (closing price * A – price of spin-off shares B) / A

Divisor: decreases

| (10) | Combination stock distribution (dividend or split) and rights offering: |

For this corporate action, the following additional assumptions apply:

| • | Shareholders receive B new shares from the distribution and C new shares from the rights offering for every A shares held |

| • | If A is not equal to one, all the following “new number of shares” formulas need to be divided by A: |

| o | If rights are applicable after stock distribution (one action applicable to another): |

Adjusted price = (closing price * A + subscription price * C * (1 + B / A)) /((A + B) * (1 + C / A))

New number of shares = old number of shares * ((A + B) * (1 + C / A)) / A

Divisor: increases

| o | If stock distribution is applicable after rights (one action applicable to another): |

Adjusted price = (closing price * A + subscription price * C) / ((A + C) * (1 + B / A))

New number of shares = old number of shares * ((A + C) * (1 + B / A))

Divisor: increases

| o | Stock distribution and rights (neither action is applicable to the other): |

Adjusted price = (closing price * A + subscription price * C) / (A + B + C)

New number of shares = old number of shares * (A + B + C) / A

Divisor: increases

| (11) | Addition / deletion of a company: |

No price adjustments are made. The net change in market capitalization determines the divisor adjustment.

| (12) | Free Float and shares changes: |

No price adjustments are made. The net change in market capitalization determines the divisor adjustment.

| Leveraged Index Return Notes® |

TS-11 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

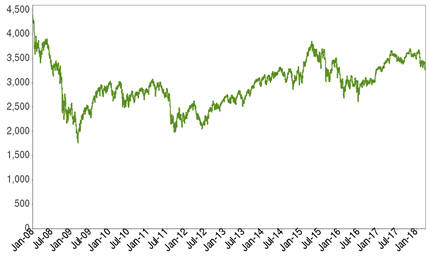

The following graph shows the daily historical performance of the Index in the period from January 1, 2008 through March 28, 2018. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On the pricing date, the closing level of the Index was 3,331.25.

Historical Performance of the Index

This historical data on the Index is not necessarily indicative of the future performance of the Index or what the value of the notes may be. Any historical upward or downward trend in the level of the Index during any period set forth above is not an indication that the level of the Index is more or less likely to increase or decrease at any time over the term of the notes.

License Agreement

STOXX Limited (“STOXX”) and its licensors (the “Licensors”) have no relationship to Wells Fargo & Company, other than the licensing of the EURO STOXX 50® Index and the related trademarks for use in connection with the notes.

STOXX and its Licensors do not: (i) Sponsor, endorse, sell or promote the notes; (ii) recommend that any person invest in the notes; (iii) have any responsibility or liability for or make any decisions about the timing, amount or pricing of the notes; (iv) have any responsibility or liability for the administration, management or marketing of the notes; (v) Consider the needs of the notes or the owners of the notes in determining, composing or calculating the EURO STOXX 50® Index or have any obligation to do so.

STOXX and its Licensors will not have any liability in connection with the notes. Specifically, STOXX and its Licensors do not make any warranty, express or implied, and disclaim any and all warranty about: the results to be obtained by the notes, the owner of the notes or any other person in connection with the use of the EURO STOXX 50® Index and the data included in the EURO STOXX 50® Index; the accuracy or completeness of the EURO STOXX 50® Index and its data; the merchantability and the fitness for a particular purpose or use of the EURO STOXX 50® Index and its data.

STOXX and its Licensors will have no liability for any errors, omissions or interruptions in the EURO STOXX 50® Index or its data. Under no circumstances will STOXX or its Licensors be liable for any lost profits or indirect, punitive, special or consequential damages or losses, even if STOXX or its Licensors knows that they might occur.

The licensing agreement between Wells Fargo & Company and STOXX is solely for their benefit and not for the benefit of the owners of the notes or any other third parties.

| Leveraged Index Return Notes® |

TS-12 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

Supplement to the Plan of Distribution

Under our distribution agreement with MLPF&S, MLPF&S will purchase the notes from us as principal at the public offering price indicated on the cover of this term sheet, less the indicated underwriting discount.

We will deliver the notes against payment therefor in New York, New York on a date that is greater than two business days following the pricing date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in two business days, unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade the notes more than two business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The notes will not be listed on any securities exchange. In the original offering of the notes, the notes will be sold in minimum investment amounts of 100 units. If you place an order to purchase the notes, you are consenting to MLPF&S acting as a principal in effecting the transaction for your account.

MLPF&S has advised us that it or its affiliates may repurchase and resell the notes, with repurchases and resales being made at prices related to then-prevailing market prices or at negotiated prices determined by reference to their pricing models and at their discretion, and these prices will include MLPF&S’s trading commissions and mark-ups. MLPF&S may act as principal or agent in these market-making transactions; however, it is not obligated to engage in any such transactions. MLPF&S has informed us that at MLPF&S’s discretion, assuming no changes in market conditions from the pricing date, MLPF&S may offer to buy the notes in the secondary market at a price that may exceed the initial estimated value of the notes for a short initial period after the issuance of the notes. Any price offered by MLPF&S for the notes is expected to be based on then-prevailing market conditions and other considerations, including the performance of the Index and the remaining term of the notes. However, none of us, MLPF&S, or any of our respective affiliates is obligated to purchase your notes at any price or at any time, and we cannot assure you that we, MLPF&S, or any of our respective affiliates will purchase your notes at a price that equals or exceeds the initial estimated value of the notes.

MLPF&S has informed us that, as of the date of this term sheet, it expects that if you hold your notes in a MLPF&S account, the value of the notes shown on your account statement will be based on MLPF&S’s estimate of the value of the notes if MLPF&S or another of its affiliates were to make a market in the notes, which it is not obligated to do; and that estimate will be based upon the price that MLPF&S may pay for the notes in light of then-prevailing market conditions, and other considerations, as mentioned above, and will include transaction costs. Any such price may be higher than or lower than the initial estimated value of the notes.

The distribution of the Note Prospectus in connection with these offers or sales will be solely for the purpose of providing investors with the description of the terms of the notes that was made available to investors in connection with their initial offering. Secondary market investors should not, and will not be authorized to, rely on the Note Prospectus for information regarding Wells Fargo or for any purpose other than that described in the immediately preceding sentence.

| Leveraged Index Return Notes® |

TS-13 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

Structuring the Notes

The notes are our debt securities, the return on which is linked to the performance of the Index. As is the case for all of our debt securities, including our market-linked notes, the economic terms of the notes reflect our actual or perceived creditworthiness at the time of pricing. Because of the higher issuance, operational and ongoing management costs of market-linked notes as compared to our conventional debt of the same maturity, as well as our liquidity needs and preferences, the assumed funding rate we use in pricing market-linked notes is generally lower than the interest rates implied by secondary market prices for our debt obligations and/or by other traded instruments referencing our debt obligations. This relatively lower assumed funding rate, which is reflected in the economic terms of the notes, along with other costs relating to selling, structuring, hedging and issuing the notes, resulted in the initial estimated value of the notes on the pricing date being less than the public offering price. If the costs relating to selling, structuring, hedging and issuing the notes were lower, or if the funding rate we use to determine the economic terms of the notes were higher, the economic terms of the notes would be more favorable to you and the estimated value would be higher.

The Redemption Amount payable at maturity will be calculated based on the $10 principal amount per unit and will depend on the performance of the Index. In order to meet these payment obligations, at the time we issue the notes, we expect to enter into certain hedging arrangements (which may include call options, put options or other derivatives) with MLPF&S or one of its affiliates. The terms of these hedging arrangements are determined by seeking bids from market participants, which may include us, MLPF&S and one of our respective affiliates, and take into account a number of factors, including our creditworthiness, interest rate movements, the volatility of the Index, the tenor of the notes and the tenor of the hedging arrangements. The economic terms of the notes and their initial estimated value depend in part on the terms of these hedging arrangements.

MLPF&S has advised us that the hedging arrangements will include a hedging related charge of approximately $0.075 per unit, reflecting an estimated profit to be credited to MLPF&S from these transactions. Since hedging entails risk and may be influenced by unpredictable market forces, additional profits and losses from these hedging arrangements may be realized by us, MLPF&S or any other hedge providers. Any profit in connection with such hedging activity will be in addition to any other compensation that we, the agents, and our respective affiliates receive for the sale of notes, which creates an additional incentive to sell the notes to you.

For further information, see “Risk Factors—General Risks Relating to LIRNs” beginning on page PS-6 and “Use of Proceeds and Hedging” on page PS-16 of product supplement EQUITY INDICES LIRN-1.

| Leveraged Index Return Notes® |

TS-14 |

| Leveraged Index Return Notes® Linked to the EURO STOXX 50® Index, due March 26, 2021

|

|

|

United States Federal Income Tax Considerations

You should read carefully the discussion under “United States Federal Tax Considerations” in the accompanying product supplement and “Selected Risk Considerations” in this term sheet.

In the opinion of our counsel, Davis Polk & Wardwell LLP, which is based on current market conditions, a note should be treated as a prepaid derivative contract that is an “open transaction” for U.S. federal income tax purposes. By purchasing a note, you agree (in the absence of an administrative determination or judicial ruling to the contrary) to this treatment. There is uncertainty regarding this treatment, and the Internal Revenue Service (the “IRS”) or a court might not agree with it.

Assuming this treatment of the notes is respected and subject to the discussion in “United States Federal Tax Considerations” in the accompanying product supplement, the following U.S. federal income tax consequences should result under current law:

| • | You should not recognize taxable income over the term of the notes prior to maturity, other than pursuant to a sale or exchange. |

| • | Upon a sale or exchange of a note (including retirement at maturity), you should recognize capital gain or loss equal to the difference between the amount realized and your tax basis in the note. Such gain or loss should be long-term capital gain or loss if you held the note for more than one year. |

Subject to the discussion below, if you are a non-U.S. holder (as defined in the accompanying product supplement) of the notes, you generally should not be subject to U.S. federal withholding or income tax in respect of any amount paid to you with respect to the notes, provided that (i) income in respect of the notes is not effectively connected with your conduct of a trade or business in the United States, and (ii) you comply with the applicable certification requirements.

In 2007, the U.S. Treasury Department and the IRS released a notice requesting comments on the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. The notice focuses in particular on whether to require holders of these instruments to accrue income over the term of their investment. It also asks for comments on a number of related topics, including the character of income or loss with respect to these instruments; whether short-term instruments should be subject to any such accrual regime; the relevance of factors such as the exchange-traded status of the instruments and the nature of the underlying property to which the instruments are linked; the degree, if any, to which income (including any mandated accruals) realized by non-U.S. investors should be subject to withholding tax; and whether these instruments are or should be subject to the “constructive ownership” regime, which very generally can operate to recharacterize certain long-term capital gain as ordinary income and impose a notional interest charge. While the notice requests comments on appropriate transition rules and effective dates, any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the notes, including the character and timing of income or loss and the degree, if any, to which income realized by non-U.S. persons should be subject to withholding tax, possibly with retroactive effect.

Possible Withholding Under Section 871(m) of the Code. Section 871(m) of the Code and Treasury regulations promulgated thereunder (“Section 871(m)”) generally impose a 30% withholding tax on dividend equivalents paid or deemed paid to non-U.S. holders with respect to certain financial instruments linked to U.S. equities (“U.S. underlying equities”) or indices that include U.S. underlying equities. Section 871(m) generally applies to instruments that substantially replicate the economic performance of one or more U.S. underlying equities, as determined based on tests set forth in the applicable Treasury regulations (a “specified equity-linked instrument” or “specified ELI”). However, the regulations, as modified by an IRS notice, exempt financial instruments issued in 2018 that do not have a “delta” of one. Based on the terms of the notes and representations provided by us, our counsel is of the opinion that the notes should not be treated as transactions that have a “delta” of one within the meaning of the regulations with respect to any U.S. underlying equity and, therefore, should not be specified ELIs subject to withholding tax under Section 871(m).

A determination that the notes are not subject to Section 871(m) is not binding on the IRS, and the IRS may disagree with this treatment. Moreover, Section 871(m) is complex and its application may depend on your particular circumstances. For example, if you enter into other transactions relating to a U.S. underlying equity, you could be subject to withholding tax or income tax liability under Section 871(m) even if the notes are not specified ELIs subject to Section 871(m) as a general matter. You should consult your tax adviser regarding the potential application of Section 871(m) to the notes.

In the event withholding applies, we will not be required to pay any additional amounts with respect to amounts withheld.

You should read the section entitled “United States Federal Tax Considerations” in the accompanying product supplement. The preceding discussion, when read in combination with that section, constitutes the full opinion of Davis Polk & Wardwell LLP regarding the material U.S. federal tax consequences of owning and disposing of the notes.

You should consult your tax adviser regarding all aspects of the U.S. federal income and estate tax consequences of an investment in the notes and any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

| Leveraged Index Return Notes® |

TS-15 |