Form SC 14D9 FIVE STAR QUALITY CARE, Filed by: Thomas William F

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

SCHEDULE 14D-9

(RULE 14d-101)

Solicitation/Recommendation Statement Under

Section 14(d)(4) of the Securities Exchange Act of 1934

Five Star Quality Care, Inc.

(Name of Subject Company)

William F. Thomas

Robert D. Thomas

Gemini Properties

(Name of Person(s) Filing Statement)

COMMON STOCK, $0.01 PAR VALUE PER SHARE

(including associated preferred stock purchase rights)

(Title of Class of Securities)

33832D106

(CUSIP Number of Class of Securities)

William F. Thomas

1516 South Boston Avenue, Suite 301

Tulsa, Oklahoma 74119

(918) 592-4400

(Name, address and telephone number of person authorized to receive notices

and communications on behalf of the person filing statement)

with a copy to:

Andrew Freedman, Esq.

Olshan Frome Wolosky LLP

1325 Avenue of the Americas

New York, New York 10019

(212) 451-2300

| ¨ | Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer. |

| Item 1. | Subject Company Information. |

Name and Address

The name of the subject company to which this Solicitation/Recommendation Statement on Schedule 14D-9 (this “Schedule 14D-9”) relates is Five Star Quality Care, Inc., a Maryland corporation (the “Company”). The address of the Company’s principal executive office is 400 Centre Street, Newton, Massachusetts 02458. The Company’s telephone number is 617-796-8387.

Securities

This Schedule 14D-9 relates to the common stock, $0.01 par value per share (the “Shares), of the Company. Based on information set forth in Amendment No. 1 to the Company’s Solicitation/Recommendation Statement on Schedule 14D-9 filed with Securities and Exchange Commission (the “SEC”) on October 28, 2016, as of the close of business on October 27, 2016, there were 49,519,051 Shares outstanding.

| Item 2. | Identity And Background Of Filing Person. |

Name and Address

Gemini Properties, William F. Thomas and Robert D. Thomas (collectively, the “Thomas Group”) are the persons filing this Schedule 14D-9. The business address of each of Gemini Properties, William F. Thomas and Robert D. Thomas is 1516 South Boston Avenue, Suite 301, Tulsa, Oklahoma 74119. The telephone number of each of Gemini Properties, William F. Thomas and Robert D. Thomas is 918-592-4400.

Tender Offer

This Schedule 14D-9 relates to the tender offer (the “Tender Offer”) by ABP Acquisition LLC, a Maryland limited liability company (the “Purchaser”), a wholly owned subsidiary of ABP Trust ("ABP Trust"), which is owned by Barry M. Portnoy, a managing director of the Company, and Adam D. Portnoy, as disclosed in the Tender Offer Statement on Schedule TO filed by the Purchaser with the SEC on October 6, 2016 (as amended or supplemented from time to time, and together with the exhibits thereto, the “Schedule TO”), to purchase up to 18,000,000 Shares at a price of $3.00 per Share, net to the seller in cash, without interest and less any required withholding taxes, upon the terms and subject to the conditions set forth in the Offer to Purchase, dated October 6, 2016 (as it may be amended or supplemented from time to time), and the related Letter of Transmittal (as it may be amended or supplemented from time to time).

As set forth in the Schedule TO, the address of the Purchaser is Two Newton Place, 255 Washington Street, Suite 300, Newton, Massachusetts 02458, and its telephone number is (617) 928-1300.

| Item 3. | Past Contacts, Transactions, Negotiations And Agreements. |

None.

| Item 4. | The Solicitation Or Recommendation. |

Recommendation

The Thomas Group recommends that shareholders of the Company not tender their Shares in the Tender Offer.

Reasons

The Thomas Group encourages other shareholders not to tender their Shares in the Tender Offer because it believes the $3.00 per share offer price is inadequate and significantly undervalues the Company.

Reference is made to the press release attached hereto as Exhibit 1 and incorporated by reference herein.

Intent to Not Tender

The members of the Thomas Group do not intend to tender any of their Shares in the Tender Offer.

| Item 5. | Persons/Assets Retained, Employed, Compensated Or Used. |

The Thomas Group has not directly or indirectly employed, retained or compensated any person to make solicitations or recommendations on its behalf in connection with the Tender Offer.

| Item 6. | Interest In Securities Of The Subject Company. |

No transactions in Shares have been effected during the past 60 days by the Thomas Group or, to the best of the Thomas Group’s knowledge, any of its directors, executive officers, subsidiaries, affiliates or associates.

| Item 7. | Purposes Of The Transaction And Plans Or Proposals. |

Not applicable.

| Item 8. | Additional Information To Be Furnished. |

Not applicable.

| Item 9. | Exhibits. |

| Exhibit No. | Description |

| 1 | Press Release, dated November 7, 2016. |

SIGNATURE

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

Dated: November 8, 2016

|

/s/ William F. Thomas | |

| WILLIAM F. THOMAS |

|

/s/ Robert D. Thomas | |

|

ROBERT D. THOMAS

|

| GEMINI PROPERTIES | |||

| By: |

/s/ William F. Thomas | ||

| Name: | William F. Thomas | ||

| Title: | Partner | ||

| By: |

/s/ Robert D. Thomas | ||

| Name: | Robert D. Thomas | ||

| Title: | Partner | ||

Exhibit 1

THE THOMAS GROUP DELIVERS OPEN LETTER TO FIVE STAR SHAREHOLDERS

Urges Shareholders to Reject the Inadequate Tender Offer Commenced by Five Star Managing Director Barry Portnoy and His Son

Expresses Severe Disappointment that an Inherently Conflicted and Entrenched Board Has Paved the Way for the Portnoy’s Unfair and Undervalued Tender Offer

Believes There are Better Alternatives Available to Maximize Value and Position the Company as a Best-in-Class Industry Leader

Announces Nomination of a Highly Qualified Candidate, David Ford, for Election at Five Star’s 2017 Annual Meeting of Shareholders

TULSA, OKLAHOMA, November 7, 2016 – Gemini Properties, together with William F. Thomas and Robert D. Thomas (collectively, the “Thomas Group”), a significant shareholder of Five Star Quality Care, Inc. (NASDAQ: FVE)(“Five Star” or the “Company”), with beneficial ownership of approximately 6.8% of the Company’s outstanding shares, announced today that it has delivered an open letter to Five Star shareholders urging shareholders to reject the inadequate and unfair tender offer launched by an entity controlled by Five Star Managing Director Barry Portnoy and his son. The Thomas Group also announced in the letter that last week they nominated David Ford for election to the Five Star Board of Directors at the Company’s 2017 Annual Meeting of Shareholders.

The full text of the letter follows:

November 7, 2016

Fellow Shareholders:

We are writing to you to express our deep concerns regarding the improper manner in which the misaligned Board of Directors (the “Board”) of Five Star Quality Care, Inc. (“Five Star” or the “Company”) is permitting Managing Director Barry M. Portnoy (“B. Portnoy”) to firm up his value-destructive grip on our Company and to urge you to reject the inadequate, coercive and unilateral $3.00 per share tender offer that is set to expire at midnight this Thursday, November 10, 2016. As you may know, ABP Acquisition LLC is a wholly owned subsidiary of ABP Trust (collectively “ABP”), an entity owned by B. Portnoy and his son Adam (“A. Portnoy”, and together with B. Portnoy, the “Portnoys”). Collectively, this group has commenced a tender offer to acquire your pro-rata portion of 18 million shares of Five Star common stock (the “Portnoy Tender Offer”).

Gemini Properties, together with William F. Thomas and Robert D. Thomas (collectively, the “Thomas Group” or “us” or “we”), is a significant shareholder of the Company, with beneficial ownership of approximately 6.8% of the Company’s outstanding shares. Our views of the Portnoy Tender Offer are that:

| · | The Portnoy Tender Offer is grossly undervalued, fraught with deep conflicts of interest, and fails to provide full and fair value to Five Star shareholders. |

| · | The purpose of the Portnoy Tender Offer is to enrich the Portnoys and to increase B. Portnoy’s effective control over the Company at the expense of Five Star shareholders. |

With fairness as the only natural guiding principle, any reasonable person would question why Five Star’s purported “Independent Directors”1 have unilaterally elected to provide one of their Managing Directors the exclusive rights to a bid process not open to others. In fact, these “Independent Directors” have intentionally precluded us from proceeding with a competing offer that would provide shareholders a 15% cash premium to the Portnoy Tender Offer. The Independent Directors have provided little to no explanation of how choosing the interests of their Managing Director over the best interests of shareholders is consistent with their fiduciary duties. This is likely because they have no good reason other than seeking to further their own personal interests and those of their controlling Managing Director.

Through the Independent Directors’ unfortunate actions, shareholders now urgently stand at a crossroads critical to the future of Five Star, as Managing Director B. Portnoy is seeking to have us tender our shares at a bargain basement price of only $3.00 per share. Fortunately, we, as shareholders, have the ability to control the future of Five Star by rejecting the Portnoy Tender Offer. If you have already tendered, we urge you to revoke your instructions before the November 10th deadline.

Let us explain.

Although the list is endless, we have narrowed our discussion to six reasons why we believe you should reject the Portnoy Tender Offer.

| 1) | The Portnoy Tender Offer is Grossly Undervalued |

Just eleven months ago, B. Portnoy and the Board rejected our $325 million proposal to acquire certain assets for cash that equated to $6.50 per share to Five Star. Our offer, which valued only a portion of the balance sheet, was more than twice the $3.00 per share Portnoy Tender Offer.

| 2) | A Non-Competitive and Unfair Process |

Last month, in our response to the Portnoy Tender Offer, the Five Star Independent Directors effectively denied our right to concurrently offer shareholders an alternative tender option even though it was priced at $3.45 per share, a 15% premium over the Portnoy Tender Offer. Unfortunately, given the Board’s denial, we will no longer be able to commence our tender offer.

The Independent Directors have provided the Portnoys with a unilateral opportunity to take effective control of the Company without a competitive process and without paying a control premium. We believe this is a direct result of their unfailing allegiance to the Portnoys given the cobweb of interrelationships that has created an inherently conflicted governance structure.

1 Independent Directors include: Barbara Gilmore, Donna Fraiche and Bruce Gans.

If successful, the Portnoy Tender Offer will further increase and secure Mr. Portnoy’s control over the Company, thereby threatening and further undermining the rights of Five Star shareholders.

| 3) | Pro-rata Risk |

Tendering your shares, which the Portnoys will purchase on a pro-rata basis, is tantamount to giving-up effective control of your Company to the Portnoys and to a Portnoys-beholden Board whose actions have already placed us all in the unfortunate situation we now find ourselves.

| 4) | Consideration of Alternatives |

If one feels pressured to hit the tender button as the only alternative, we urge you to reconsider! The Independent Directors have responsibilities and owe duties to all shareholders. Our rejection would serve as a referendum that the status quo is clearly untenable and a hopeful call to action for the Board to seriously evaluate how to transform Five Star into an industry leader.

| 5) | Election of New Independent Director |

Retaining your shares maintains your right to vote and importantly, your right to elect directors that will protect your best interests. Last week, we nominated David Ford as an Independent Director candidate for election to the Board at the 2017 Annual Meeting of Shareholders (the “2017 Annual Meeting”). Mr. Ford, the recently retired Vice Chairman of Aegis Senior Communities LLC, is an experienced seniors housing operator who is truly independent with no ties to the Portnoy family or the Thomas Group. He also deeply understands the positive financial outcomes premised on serving all owners. Isn’t an experienced senior housing executive with significant operational expertise something that we should all obviously expect of an independent Five Star board member? See Exhibit A of this letter for Mr. Ford’s biography, which demonstrates that he is clearly qualified for this role.

| 6) | Envisioning a Better Future |

An overwhelming rejection by shareholders of the Portnoy Tender Offer would demonstrate to the Board and B. Portnoy that shareholders believe Five Star has a very promising future with upside that they want to participate in and not turn over to the Portnoys. This bright future for our investment requires a truly independent board, which we are taking the first steps to achieve at the 2017 Annual Meeting.

Why are we invested in Five Star?

Simply stated, we believe Five Star can become an industry leader. However the Portnoys try to distort our intent, they would be hard-pressed to understand what drives us. We began the senior living portion of our business in 1989 and now own and operate over two thousand senior living residences, which are centered on a deeply engrained value system committed to the seniors we serve. As identical twins, and whose business interests are purposely and identically aligned, we each can easily say that we awake each morning thinking what we can do for each other; that simple principle extends to how we think about the seniors we serve, the associates who serve them and the partners who have invested with us over these years. Believing that Five Star could become one of the best-in-class operators of the senior living business, we began investing in the Company in 2012.

Regrettably, Five Star’s Independent Directors appear to be ignoring their fiduciary duties to the detriment of the shareholders they are charged with representing and, in our view, have breached these duties by exclusively permitting their Managing Director to buy-out shareholders at a woefully inadequate price.

There are far better alternatives available to maximize value for Five Star shareholders. Below is a further examination of the six reasons mentioned above to reject the Portnoy Tender Offer.

| 1) | The Portnoy Tender Offer is Grossly Undervalued |

On November 30, 2015, we met with B. Portnoy, Five Star President and CEO Bruce J. Mackey and Senior Housing Properties Trust (“SNH”) President and COO David J. Hegarty to discuss our analysis and present a comprehensive strategy for Five Star. This strategy included a plan for Five Star to reinvest in its existing leased assets, enhance cash flows, deleverage the balance sheet, and increase the Company’s long-term value. Our plan left Five Star’s leased and managed portfolio entirely intact. The leased portfolio comprises approximately 90% of Five Star’s senior communities.

To provide the capital required to execute on this strategy, we offered to acquire the senior living assets wholly owned by Five Star. These assets represented only 10% of Five Star’s senior communities. The result of that offer, or for that matter any subsequent offer that would have been generated in a bidding process, which we would have of course expected, would have provided proceeds equivalent to more than twice the Portnoy Tender Offer of $3 per share when extrapolated across all outstanding shares.

In our meeting, B. Portnoy stated that if he were to sell any assets, Five Star would run a process to ensure maximum value. As shareholders, we would agree with this decision. However, both our strategy and our subsequent offer were totally dismissed by B. Portnoy and subsequently, by the Board.

If the Portnoy Tender Offer is successful, Mr. Portnoy will effectively control enough shares to block all future shareholder proposals, including the election of shareholder-nominated board candidates.

| 2) | A Non-Competitive and Unfair Process |

As major shareholders of Five Star, we have some clear observations of recent events and decisions that have occurred. Based on the resounding, unsolicited support of our fellow shareholders who have contacted us, we know that our concerns are shared among a significant portion of Five Star’s ownership.

Personally, we are mystified that Five Star’s Independent Directors jeopardized their fiduciary responsibilities by allowing their Managing Director to negotiate an exclusive ownership exemption under Five Star’s Charter. This decision granted the Portnoys the singular right to make a material tender offer for effective control of the Company at a price of $3.00 per share, which values the entire Company at less than half of the value of the proposal we made for only a portion of the assets less than 11 months ago.

| 3) | Pro-rata Risk |

If the Portnoy Tender Offer is successful, shareholders will have relinquished control of their remaining shares to ABP for at least 10 years. Legitimate risks previously disclosed by Five Star include:

| · | Effect on Trading Volume and Liquidity of Five Star Common Stock. The number of outstanding shares owned by Five Star shareholders other than ABP would decline, thereby reducing the number of shares that might otherwise trade publicly and in turn, could reduce trading liquidity and increase the volatility of Five Star’s share price in the market. In addition, as specifically stated by Five Star in its SC 14D9, “this reduction could impact the Company’s ability to raise capital on an expedited basis, as well as limit the Company’s ability to raise capital that might adversely impact the Company’s future usage of net operating losses.” |

| · | Concentration of Control. ABP would beneficially own a significant percentage of Five Star’s outstanding shares, which, according to Five Star, “may enable [ABP] to have significant influence on matters requiring stockholder approval, including the election of directors, amendments to the Company’s charter and bylaws and significant transactions, such as purchases or sales of assets, mergers and other business combinations. This concentration of ownership may discourage acquisitions by others of a significant stake in the Company and may deter, delay or prevent a change in control of the Company or unsolicited acquisition proposals that other stockholders of the Company may consider favorable. It may also inhibit efforts by other stockholders of the Company to change the direction or management of the Company or the Board.” (emphasis added) |

| 4) | Consideration of Alternatives |

Since our initial investment in 2012, we have neither seen nor heard the strategic plan for turning Five Star’s declining value around. To our knowledge, we are the only party who has presented a strategic plan to increase shareholder value.

Reasoned thinking should lead shareholders to soundly decline the Portnoy Tender Offer and instead, to maintain hope and have patience, as alternatives should provide more significant financial outcomes. Importantly, if shareholders reject the Portnoy Tender Offer, we believe it would be incumbent upon the Board to listen to the will of its shareholders and implement a turnaround plan for the Company.

| 5) | Election of New Independent Director |

The Company’s onerous Bylaw requirements, which we note only the Board can amend, to nominate an individual for election to the Board require a shareholder to continuously own at least 3% of the outstanding shares for a minimum of three years. In order to meet this requirement, we have patiently held a sizable ownership stake since 2012.

Having now fulfilled the three-year requirement, we recently nominated David Ford for election as an Independent Director candidate to the Board at the 2017 Annual Meeting. Mr. Ford is a highly qualified, truly independent director candidate. Given this Board’s troubling track record of placing its own interests ahead of shareholders, we believe immediate change to the Board is required to ensure shareholders’ interests remain paramount.

We believe Mr. Ford possesses the relative business experience, character, leadership skills and most importantly, objectivity, necessary to explore value-enhancing opportunities and make decisions with the best interests of shareholders in mind. Mr. Ford’s career highlights include positions in seniors housing, real estate, operations, legal, board representation, non-profit work, and a track record for serving others. See Exhibit A for Mr. Ford’s biography.

| 6) | Envisioning a Better Future |

We believe the inherent value of Five Star is not reflected in its stock price and that significant value can be unlocked given the obvious demographic changes occurring throughout the next 30 years and favorable industry dynamics currently available to the Company. In fact, we believe this discounted valuation likely reflects a combination of the market’s concerns about the Company’s deterioration under the watch of its entrenched, insular and conflicted Board as well as the market’s failure to ascribe appropriate value to Five Star’s numerous positive attributes. Five Star has an attractive, geographically diverse portfolio as well as a strong presence in the industry as one of the largest operators in the sector.

Unfortunately, Five Star’s disastrous corporate governance is, in our view, the single greatest barrier preventing the Company from achieving sustainable shareholder value. With the right governance structure in place, we believe Five Star can become a best-in-class senior housing leader with a market capitalization that reflects its true value.

It is indeed perplexing that the Board does not see the economic possibilities in decreasing leverage, reinvesting strategically in areas that provide double digit returns, increasing cash flow, all the while actually firming up the lease coverage on Five Star’s existing leases, which we believe would make the Company a stronger partner who is truly building economic value for its lessors, including SNH and its subsidiaries. Moreover, if Five Star were to execute upon these opportunities and demonstrate a deep commitment to its customers and associates, we believe the Company would be recognized as one of the best lease operators in the nation.

The Portnoy Tender Offer is not the best option for the Company or its shareholders. Help us put pressure on the Board and the Portnoys by rejecting their efforts to buy-out shareholders at what we believe to be a woefully inadequate price. There are better alternatives to maximize value for shareholders, including by instilling accountability on the Board through the election of independent candidates nominated by unaffiliated shareholders.

As important as these reasons are for not tendering, perhaps the largest opportunity for upside value is changing Five Star’s woeful lack of board independence and poor corporate governance.

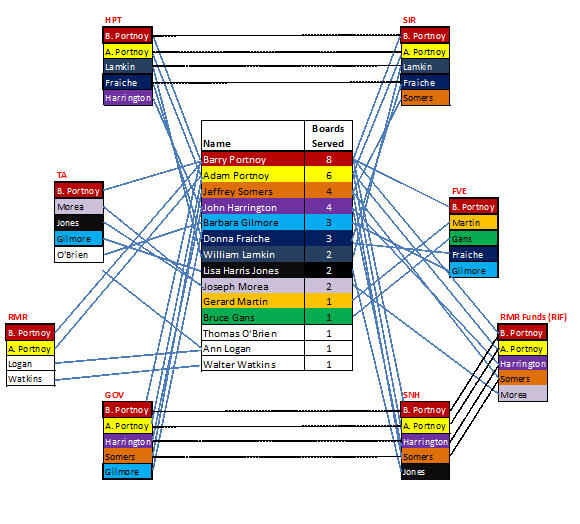

The current, elaborate web of conflicting relationships among the Portnoys, Five Star external manager RMR LCC and its affiliated entities (collectively, “RMR”), SNH, other Five Star directors and officers, and third parties represents, in our view, disenfranchisement at its core. In addition to the overlapping Board positions reflected in Exhibit B of this letter, consider the following: 2

RMR Conflicts

| · | B. Portnoy is a Managing Director, officer and controlling shareholder of RMR Group Inc. (“RMR Inc.”), the controlling shareholder of RMR LLC, and Chairman of RMR LLC. |

| · | A. Portnoy is the President and CEO of RMR LLC and a Managing Director, President and CEO of RMR Inc. |

| · | RMR LLC provides management services to both Five Star and SNH. |

| · | A majority of Five Star’s Independent Directors serve as independent directors or independent trustees of other companies to which RMR LLC or its affiliates provide management services. |

2 Based on publicly available information, including the Company’s SEC filings.

| · | Five Star President and CEO Bruce Mackey and Treasurer and CFO Richard Doyle are officers and employees of RMR LLC. |

| · | Mr. Doyle was formerly SNH's treasurer and CFO. |

SNH Conflicts

| · | SNH is Five Star’s largest shareholder and has entered into numerous lease and management agreements with Five Star. |

| · | B. Portnoy and A. Portnoy are managing trustees of SNH. |

| · | Five Star Corporate Secretary Jennifer Clark is also SNH’s Secretary. |

| · | Five Star manages a portion of a senior living community for D&R Yonkers LLC, which is owned by SNH’s President and CFO and Five Star’s Treasurer and CFO. |

Other Conflicts

| · | Five Star, ABP Trust, SNH and four other companies to which RMR LLC provides management services currently own AIC, an Indiana insurance company. RMR LLC provides management and administrative services to AIC. All of the Company's directors and all of the trustees and directors of the other AIC shareholders currently serve on the board of directors of AIC. |

| · | B. Portnoy was formerly a Partner and served as Chairman of the law firm Sullivan & Worcester (“S&W”), which now serves as Five Star’s Corporate Counsel. Five Star Vice President and General Counsel Katie Dillon, Corporate Secretary J. Clark and Independent Director B. Gilmore previously worked at S&W. |

Aside from these deeply concerning relationships, we believe RMR LLC’s simultaneous contractual obligations to Five Star and SNH create clear conflicts of interest, particularly given the fact that under Five Star’s business management agreement with RMR LLC, RMR LLC is entitled to prioritize SNH over Five Star in the event of any conflict of interest. In fact, the Company itself acknowledged these potential conflicts stating that its relationships “with SNH and RMR LLC may restrict our ability to grow our business; and we have engaged in, and expect to continue to engage in, transactions with parties that may be considered related parties”.

How can B. Portnoy and the current Independent Directors make decisions that are in the best interest of shareholders when they have competing interests in companies that have significant ties to Five Star? Further, given B. Portnoy’s presence in the Five Star boardroom without the oversight of a truly independent board, he has no incentive to place the interests of Five Star shareholders ahead of his own, which we believe is evidenced by the undervalued Portnoy Tender Offer.

We believe these troubling conflicts can be easily eliminated. By electing a highly qualified, truly independent director who understands his fiduciary responsibilities to shareholders, we can begin to instill accountability and lead Five Star toward a path of growth. Rejecting the Portnoy Tender Offer is the first, and most crucial, step along this path.

Corporate Governance

We find it deeply troubling that B. Portnoy can stand on both sides of the Portnoy Tender Offer, and any other transaction involving SNH or RMR, without being held accountable by the Independent Directors for advancing his personal interests over the interests of Five Star shareholders.

Given the Independent Directors’ ties to the Portnoys, together with their effective rejection of our higher tender offer of $3.45 per share to acquire 10 million shares of Common Stock, we conclude that the Portnoy Tender Offer was neither a fair nor democratic bid process. Indeed, the legal advisor to the Independent Directors during their evaluation of the Portnoy Tender Offer was B. Portnoy’s former firm S&W.

How could Five Star’s Independent Directors approve ownership waivers in order to clear way for the Portnoy Tender Offer yet reject our requests for similar waivers in order to commence a competing tender offer, which clearly represented a premium over the Portnoy Tender Offer? In a true corporate democracy, a well-functioning, independent board would encourage and entertain all offers and seek to create a bidding process so that shareholders receive the most value for their investment.

We also seriously question how the Board could approve lease agreements with SNH and its subsidiaries that contain entrenchment-serving provisions that threaten shareholders’ purported right to nominate director candidates for election at annual meetings. Under the various lease agreements, a change in control is triggered upon the election of just one individual to the Board, thereby triggering a default under such lease agreements.

It appears to us that the Independent Directors have chosen to protect the Portnoys’ interests rather than the interests of Five Star shareholders. We believe this not only represents shareholder disenfranchisement, but is also a breach of the Board’s fiduciary duties to shareholders.

Institutional Shareholder Services (“ISS”), a leading proxy voting advisory firm, appears to share our concerns with Five Star’s egregious governance structure. With “10” being the worst possible grade, ISS issued the Company an abysmal governance QuickScore of “9” in its 2016 report and a “10” in its 2015 and 2014 reports, indicating severe concerns with Five Star’s corporate governance regime.

ISS also raised concerns with the lack of independence on the Board in each of its 2016, 2015 and 2014 reports and has repeatedly raised concerns with B. Portnoy’s continuous service on more than six publicly-traded boards, recommending that shareholders “WITHHOLD” on his election at the 2014 annual meeting of shareholders (the “2014 Annual Meeting”). Notably, B. Portnoy received support of less than a majority of the votes cast at the 2014 Annual Meeting. Unfortunately, given Five Star’s disastrous corporate governance, B. Portnoy remained on the Board per Five Star’s plurality vote standard in uncontested elections, which is the exact opposite of what is considered best practice. In fact, ISS found B. Portnoy’s continued service on the Board so problematic that it recommended shareholders “WITHHOLD” on the election of D. Fraiche and G. Martin at the 2015 annual meeting of shareholders. We believe B. Portnoy’s continued presence on the Board despite his rejection by shareholders and a leading proxy voting advisory firm demonstrates his deep rooted and unchecked control over Five Star and the Board.

Conclusion

Let your rejection of the Portnoy Tender Offer serve as a referendum that the status quo will no longer be tolerated. At some point, as a reasonable person, one has to finally say “enough is enough”.

B. Portnoy’s historic control of Five Star has paved the way for the Portnoys to take advantage of the low stock price through a “creeping tender offer” that fails to provide full and fair value to Five Star shareholders and effectively precludes competing bids. We believe the unfair and undemocratic bid process (or lack thereof) is a direct result of the Portnoys’ self-dealing and reflects a Board fraught with conflicting ties and relationships to the Portnoys and the entities in which they control, including Five Star’s external manager.

If we do not act now by rejecting the Portnoy Tender Offer, B. Portnoy will effectively have carte blanche control over Five Star and continue his unrestrained campaign of value destruction to the detriment of Five Star shareholders. Given the disastrous governance regime under this Board’s watch, we cannot afford to let B. Portnoy further undermine shareholder rights.

Again, we believe there are better alternatives available for shareholders to maximize the value of their investment. With the right governance structure in place, we believe Five Star can become a best-in-class senior housing leader. It is time for accountability at Five Star. It is time for a new Board comprised of truly independent directors with no ties to the Portnoys and who are committed to representing the best interests of shareholders.

Our nomination of David Ford to the Board at the 2017 Annual Meeting is the first step towards enhancing corporate governance at Five Star. Mr. Ford not only has significant experience in the senior housing industry but he would bring the much needed fresh perspective and objectivity to the Board. Importantly, Mr. Ford has no ties to the Portnoys or the Thomas Group. The creation of a diversified board that is truly independent of the Portnoys, SNH and RMR is paramount to incubating a leadership environment conducive to strategic change.

It is imperative that we, as shareholders, the true owners of the Company, take control over the future of our investment by rejecting the Portnoy Tender Offer. Do not let the Portnoys usurp the opportunities available to maximize the value of your investment. The future of Five Star is in our hands.

As one of the largest shareholders of Five Star, our interests are directly aligned with yours. Together, we can help make Five Star what it should be, a best-in-class operator creating sustainable shareholder value.

Best Regards,

William F. Thomas

Robert D. Thomas

Gemini Properties

Exhibit A

David R. Ford, age 61, is an experienced business and legal advisor to, as well as an investor in, the seniors- housing industry, commercial real-estate ventures and start-up enterprises. Mr. Ford has been an advisor to each of the Walker Group, a real estate advisory firm, since June 2014 and Linked Senior, a developer of interactive software for people living with Alzheimer’s and other forms of dementia in the senior-care market, since March 2016. Mr. Ford is also currently an investor in Aegis Senior Communities LLC (d/b/a Aegis Living), a leading developer and operator of senior-housing communities in California, Nevada and Washington, where he previously served as Vice Chairman of its Board of Managers from 2002 to April 2015. Prior to that, he was the Chief Operating Officer and General Counsel of Maden Technologies LLC, an integrator of outsourced IT solutions and cyber security solutions for the public and private sectors, from 2000 to 2002. For the first two decades of his professional life, he was an attorney in private practice in Washington, D.C., where he specialized in mergers and acquisitions in the healthcare, technology and government-contracting industries.

Mr. Ford is currently Chairman of the Board of the Washington D.C. chapter of Minds Matter, Inc., an all-volunteer, not-for-profit organization whose mission is to transform the lives of accomplished high school students from low-income families by preparing them for success in college, a position he has held since November 2014. He has also served on the Board of Directors of Teach for America – DC Region, a non-profit organization, since December 2015 and as President of the Cosmos Club, Washington, D.C., a non-profit organization, since May 2016, where he previously served as its Vice President from May 2015 to May 2016. Mr. Ford also previously served on the Executive Board of the American Seniors Housing Association, a non-profit organization, from 2004 to April 2015. In addition, in June 2007, he co-founded Kalorama Village, Inc., a non-profit organization dedicated to helping seniors “age in place”, where he served as a director until 2009.

Mr. Ford received his Bachelor of Arts degree from Rollins College and his J.D. degree from the University of Virginia School of Law. He is a member of the District of Columbia Bar.

During the nomination process, Mr. Ford stated “Caring for the frail elderly is a calling, whether performed by a family member or a public company. Short- and long-term values in a seniors-housing company are both unlocked the same way – by ensuring the highest quality of care and empathy for each resident. While that may sound like a platitude, I believe it is true. Satisfied residents and family members will drive all the sales-side indicators of a successful business: high occupancy, favorable rents, engaged employees, positive brand recognition, etc. For a Company with over 31,000 units spread over a diverse set of facilities, the challenge is to set minimum standards of high-quality performance expectations across the board – and, by rigorous reporting and assessment, to exceed those standards throughout the Company.

If elected to the Board at the 2017 Annual Meeting, I will act in accordance with my fiduciary duties as a director on all matters that come before the Board and will work with the other members of the Board to take those steps that we deem are necessary or advisable to identify and unlock opportunities to drive shareholder value. Additionally, if elected, I am committed to act in the best interests of all of the Company’s shareholders.”

Exhibit B

RMR Cobweb

Investor Contact:

Matt Clifton

(918) 592-4400

CERTAIN INFORMATION CONCERNING THE PARTICIPANTS

Gemini Properties, together with the other participants named herein (collectively, the "Thomas Group"), intends to file a preliminary proxy statement and accompanying proxy card with the Securities and Exchange Commission ("SEC") to be used to solicit votes for the election of its director nominee at the 2017 annual meeting of shareholders of Five Star Quality Care, Inc., a Maryland corporation (the "Company").

THE THOMAS GROUP STRONGLY ADVISES ALL SHAREHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC'S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST.

The participants in the proxy solicitation are William F. Thomas, Robert D. Thomas, Gemini Properties and David R. Ford. As of the date hereof, Gemini Properties directly owns 1,915,164 shares of Common Stock, $.01 par value, of the Company (the “Common Stock”). As of the date hereof, Mr. W. Thomas directly owns 317,511 shares of Common Stock. As a general partner of Gemini Properties, Mr. W. Thomas may be deemed the beneficial owner of the 1,915,164 shares of Common Stock beneficially owned by Gemini Properties. In addition, Mr. W. Thomas may be deemed the beneficial owner of: (i) 20,000 shares of Common Stock by virtue of his role as an advisor to certain donor advised charitable funds, (ii) 2,150 shares of Common Stock by virtue of his role as an advisor to an individual retirement fund for his wife, and (iii) 861,928 shares of Common Stock by virtue of his role as a co-advisor to a donor advised charitable investment fund. Mr. W. Thomas disclaims such beneficial ownership. As a general partner of Gemini Properties, Mr. R. Thomas may be deemed the beneficial owner of the 1,915,164 shares of Common Stock beneficially owned by Gemini Properties. In addition, Mr. R. Thomas may be deemed the beneficial owner of: (i) 39,800 shares of Common Stock by virtue of his position as an advisor to certain family investment funds, (ii) 18,500 shares of Common Stock by virtue of his position as a trustee of a family trust account, (iii) 186,684 shares of Common Stock by virtue of his role as an advisor to a certain donor advised charitable investment fund, and (iv) 861,928 shares of Common Stock by virtue of his role as a co-advisor to a donor advised charitable investment fund. Mr. R. Thomas disclaims such beneficial ownership. As of the date hereof, Mr. Ford does not own any shares of Common Stock.

Create E-mail Alert Related Categories

SEC FilingsRelated Entities

14D9Sign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!