Form PRER14A ALERE INC.

Tweet

Tweet Share

ShareTable of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. 1)

Filed by the Registrant x Filed by a party other than the Registrant ¨

Check the appropriate box:

| x | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| ¨ | Definitive Additional Materials | |

| ¨ | Soliciting Material Under Rule 14a-12 | |

ALERE INC.

(Name of Registrant as Specified In Its Charter)

Payment of Filing Fee (Check the appropriate box):

| ¨ | No fee required | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11 | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| x | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount previously paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing party:

| |||

| (4) | Date Filed:

| |||

Table of Contents

PRELIMINARY PROXY MATERIAL SUBJECT TO COMPLETION

[ ], 2016

Dear Fellow Stockholder:

You are cordially invited to attend a special meeting of holders of shares of common stock of Alere Inc., a Delaware corporation (“Alere” or the “Company”), on [ ], 2016 at [ ], local time, at [ ].

On January 30, 2016, the Company entered into an Agreement and Plan of Merger (the “merger agreement”) with Abbott Laboratories, an Illinois corporation (“Abbott”), providing for, subject to the satisfaction or waiver (if permissible under applicable law) of specified conditions, the acquisition of the Company by Abbott at a price of $56.00 per share of common stock in cash. Subject to the terms and conditions of the merger agreement, Angel Sub, Inc., a Delaware corporation and a wholly owned subsidiary of Abbott (“Merger Sub”), which became party to the merger agreement through execution of a joinder agreement to the merger agreement on February 2, 2016, will be merged with and into the Company (the “merger”), with the Company surviving the merger as a subsidiary of Abbott (the “surviving corporation”). At the special meeting, the holders of shares of common stock of the Company will vote on the adoption of the merger agreement.

If the merger is completed, you will be entitled to receive $56.00 in cash, without interest and less any applicable withholding taxes, for each share of common stock, par value $0.001 per share, of the Company (“Company common stock”) you own at the effective time of the merger (unless you do not vote in favor of the adoption of the merger agreement and properly demand appraisal for such shares in compliance with Delaware law).

The proxy statement accompanying this letter provides you with more specific information concerning the special meeting, the merger agreement, the merger and the other transactions contemplated by the merger agreement. We encourage you to carefully read the accompanying proxy statement and the copy of the merger agreement attached as Annex A thereto.

The board of directors of the Company (the “Board”) carefully reviewed and considered the terms and conditions of the merger agreement, the merger and the other transactions contemplated by the merger agreement. The Board approved the merger agreement, declared the merger agreement, the merger and the other transactions contemplated by the merger agreement to be advisable and in the best interests of the Company and its stockholders, directed that the adoption of the merger agreement be submitted to holders of Company common stock and recommended that the holders of Company common stock vote their shares to adopt the merger agreement at a meeting of the holders of Company common stock. Accordingly, the Board recommends a vote “FOR” the proposal to adopt the merger agreement, the nonbinding compensation proposal and the adjournment proposal.

Whether or not you plan to attend the special meeting and regardless of the number of shares you own, your careful consideration of, and vote on, the merger agreement is important and we encourage you to vote promptly. The merger cannot be completed unless the merger agreement is adopted by stockholders holding at least a majority of the outstanding shares of Company common stock entitled to vote thereon at the special meeting. The failure to vote will have the same effect as a vote against the proposal to adopt the merger agreement.

After reading the accompanying proxy statement, please make sure to vote your shares of Company common stock by promptly voting electronically or telephonically as described in the accompanying proxy statement, or, if you received a paper copy of the proxy card, by completing, dating, signing and returning your proxy card, or attending our special meeting of holders of Company common stock in person. Instructions regarding all three methods of voting are provided on the proxy card. If you hold shares through an account with a brokerage firm, bank or other nominee, please follow the instructions you receive from them to vote your shares of Company common stock. If you have any questions or need assistance voting your shares, please contact our proxy solicitor, Innisfree M&A Incorporated, toll-free at (888) 750-5834.

Thank you for your continued support of Alere. For those of you who plan to visit with us in person at the special meeting, we look forward to seeing you.

Very truly yours,

Gregg J. Powers

Chairman of the Board

The merger has not been approved or disapproved by the Securities and Exchange Commission or any state securities commission. Neither the Securities and Exchange Commission nor any state securities commission has passed upon the merits or fairness of the merger or upon the adequacy or accuracy of the information contained in this document or the accompanying proxy statement. Any representation to the contrary is a criminal offense.

The accompanying proxy statement is dated [ ], 2016 and is first being mailed to holders of Company common stock on or about [ ], 2016.

Table of Contents

ALERE INC.

51 Sawyer Road, Suite 200

Waltham, Massachusetts 02453

NOTICE OF SPECIAL MEETING OF HOLDERS OF SHARES OF COMMON STOCK

| Time and Date: | [ ] local time, on [ ], 2016 | |

| Place: | [ ] |

Purpose:

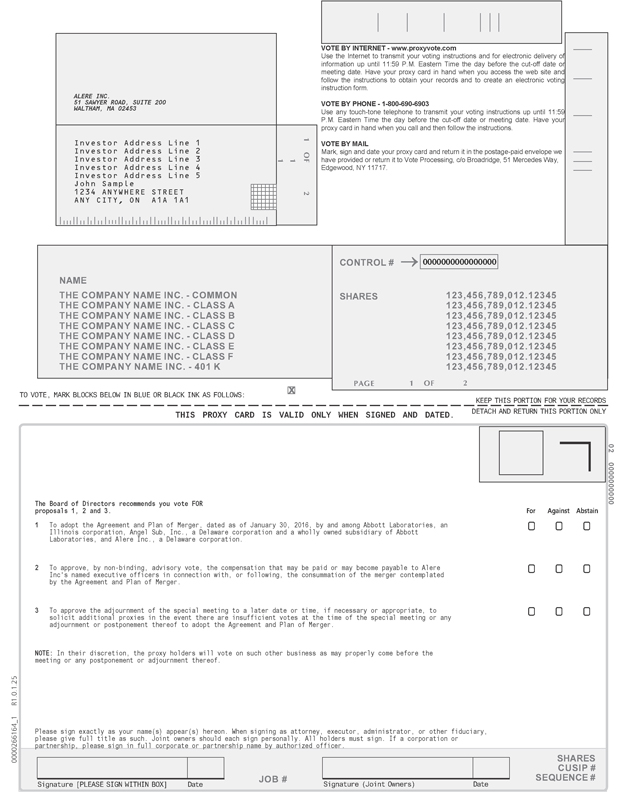

| 1. | To consider and vote on a proposal to adopt the Agreement and Plan of Merger, dated as of January 30, 2016 (the “merger agreement”), by and among Abbott Laboratories, an Illinois corporation (“Abbott”), Alere Inc., a Delaware corporation (“Alere” or the “Company”), and Angel Sub, Inc., a Delaware corporation and a wholly owned subsidiary of Abbott which became party to the merger agreement through execution of a joinder agreement to the merger agreement on February 2, 2016. |

| 2. | To consider and vote on a nonbinding, advisory proposal to approve the compensation that may be paid or may become payable to the Company’s named executive officers in connection with, or following, the consummation of the merger (this nonbinding, advisory proposal, which we refer to as the “nonbinding compensation proposal”, relates only to contractual obligations of the Company in existence prior to consummation of the merger that may result in a payment to the Company’s named executive officers in connection with, or following, the consummation of the merger and does not relate to any new compensation or other arrangements between the Company’s named executive officers and Abbott or, following the merger, the surviving corporation and its subsidiaries). |

| 3. | To consider and vote on a proposal to adjourn the special meeting to a later date or time, if necessary or appropriate, to solicit additional proxies in the event there are insufficient votes at the time of the special meeting or any adjournment or postponement thereof to adopt the merger agreement, which we refer to as the “adjournment proposal”. |

Record Date:

Holders of common stock, par value $0.001 per share, of the Company (“Company common stock”) and holders of Series B Convertible Perpetual Preferred Stock, par value $0.001 per share, of the Company (the “convertible preferred stock”), each as of record as of the close of business on [ ], 2016, are entitled to notice of the special meeting and any adjournments or postponements thereof. Only holders of Company common stock as of record as of the close of business on [ ], 2016 are entitled to vote at the special meeting and any adjournments or postponements thereof.

General:

For more information concerning the special meeting, the merger agreement, the merger and the other transactions contemplated by the merger agreement, please review the accompanying proxy statement and the copy of the merger agreement attached as Annex A thereto.

The board of directors of the Company (the “Board”) carefully reviewed and considered the terms and conditions of the merger agreement, the merger and the other transactions contemplated by the merger agreement. The Board approved the merger agreement, declared the merger agreement, the merger and the other transactions contemplated by the merger agreement to be advisable and in the best interests of the Company and its stockholders, directed that the adoption of the merger agreement be submitted to holders of Company common stock and recommended that the holders of Company common stock vote their shares to adopt the merger agreement at a meeting of the holders of Company common stock.

Table of Contents

Accordingly, the Board recommends a vote “FOR” the proposal to adopt the merger agreement, “FOR” the nonbinding compensation proposal and “FOR” the adjournment proposal.

Under Delaware law, holders of Company common stock who do not, among other things, vote in favor of the adoption of the merger agreement and holders of shares of convertible preferred stock that are outstanding immediately prior to the effective time of the merger, in each case, who are entitled to demand and who properly demand appraisal of such shares, will have the right to seek appraisal of the fair value of their shares as determined by the Delaware Court of Chancery if the merger is completed, but only if they properly submit a written demand for such an appraisal prior to the vote on the adoption of the merger agreement and strictly comply with the other Delaware law procedures explained in the attached proxy statement. The applicable Delaware law is reproduced in its entirety in Annex C to the attached proxy statement, and a summary of these provisions can be found under “Appraisal Rights” in the accompanying proxy statement.

Regardless of whether you plan to personally attend the meeting, please vote telephonically or electronically for the matters before our stockholders as described in the accompanying proxy statement, or promptly fill in, date, sign and return the enclosed proxy card in the accompanying pre-paid envelope to ensure that your shares are represented at the meeting. You may revoke your proxy before it is voted. If you attend the meeting, you may choose to vote in person even if you have previously sent in your proxy card.

|

|

| Ellen Chiniara, Esq. Secretary |

Waltham, Massachusetts

[ ], 2016

Table of Contents

| Page | ||||

| 1 | ||||

| QUESTIONS AND ANSWERS ABOUT THE SPECIAL MEETING AND THE MERGER |

10 | |||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 20 | ||||

| 20 | ||||

| 21 | ||||

| 21 | ||||

| 21 | ||||

| 21 | ||||

| Voting by Company Directors, Executive Officers and Principal Securityholders |

22 | |||

| 22 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 25 | ||||

| 26 | ||||

| 26 | ||||

| 37 | ||||

| 37 | ||||

| 40 | ||||

| 47 | ||||

| 51 | ||||

| 52 | ||||

| 53 | ||||

| 53 | ||||

| Interests of the Company’s Directors and Executive Officers in the Merger |

53 | |||

| 61 | ||||

| 63 | ||||

| 63 | ||||

| 64 | ||||

| 65 | ||||

| 65 | ||||

| 65 | ||||

Table of Contents

| 66 | ||||

| 66 | ||||

| 66 | ||||

| 67 | ||||

| 68 | ||||

| Covenants Regarding Conduct of Business by Alere Pending the Effective Time |

70 | |||

| 72 | ||||

| 74 | ||||

| 76 | ||||

| 76 | ||||

| 76 | ||||

| 77 | ||||

| 78 | ||||

| 78 | ||||

| 79 | ||||

| 79 | ||||

| 80 | ||||

| 80 | ||||

| 80 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

81 | |||

| 84 | ||||

| 89 | ||||

| 91 | ||||

| 92 | ||||

| 93 |

Table of Contents

ALERE INC.

51 Sawyer Road, Suite 200

Waltham, Massachusetts 02453

SPECIAL MEETING OF HOLDERS OF SHARES OF COMMON STOCK

TO BE HELD ON [ ], 2016

PROXY STATEMENT

This proxy statement contains information relating to a special meeting of holders of common stock of Alere Inc., a Delaware corporation, which we refer to as “Alere”, the “Company”, “we”, “us” or “our”. The special meeting will be held on [ ], 2016, at [ ] local time, at [ ]. We are furnishing this proxy statement to holders of shares of common stock, par value $0.001 per share, of the Company, which we refer to as “Company common stock”, as part of the solicitation of proxies by the Company’s board of directors, which we refer to as the “Board”, for use at the special meeting and at any adjournments or postponements thereof. This proxy statement is dated [ ], 2016 and is first being mailed to holders of Company common stock on or about [ ], 2016.

This summary term sheet highlights selected information in this proxy statement and may not contain all of the information about the merger agreement or the merger that is important to you. We have included page references in parentheses to direct you to more complete descriptions of the topics presented in this summary term sheet. You should carefully read this proxy statement in its entirety, including the annexes hereto and the other documents to which we have referred you, for a more complete understanding of the matters being considered at the special meeting. You may obtain, without charge, copies of any of the documents we file with the U.S. Securities and Exchange Commission (the “SEC”) by following the instructions under the section of this proxy statement entitled “Where You Can Find Additional Information” beginning on page 93.

The Parties

(page 17)

Alere delivers reliable and actionable health information through rapid diagnostic tests, resulting in better clinical and economic healthcare outcomes globally. Our high-performance diagnostics for infectious disease, cardiometabolic disease and toxicology are designed to meet the growing global demand for accurate, easy-to-use and cost-effective near-patient tests. Our goal is to make Alere products accessible to more people around the world, even those located in remote and resource-limited areas, by making them affordable and usable in any setting. By making critical clinical diagnostic information available to doctors and patients in an actionable timeframe, Alere products help streamline healthcare delivery and improve patient outcomes. Our company, formerly known as Inverness Medical Innovations, Inc., was formed in 2001. Since that time, we have grown our businesses through strategic acquisitions, tactical use of our intellectual property portfolio and organic growth. In July 2010, our company changed its name to Alere Inc. Our common stock is listed on the New York Stock Exchange, which we refer to as “the NYSE”, under the trading symbol “ALR”. Our Series B Convertible Perpetual Preferred Stock, $0.001 par value per share (the “convertible preferred stock”), designated pursuant to the Certificate of Designations, Preferences and Rights filed with the Secretary of State of the State of Delaware on May 8, 2008, which we refer to as the “Certificate of Designations”, is listed on the NYSE under the trading symbol “ALRpB”. Alere’s principal executive offices are located at 51 Sawyer Road, Suite 200, Waltham, Massachusetts 02453 and our telephone number is (781) 647-3900.

Abbott Laboratories, which we refer to as “Abbott”, is an Illinois corporation, incorporated in 1900. Abbott’s principal business is the discovery, development, manufacture and sale of a broad and diversified line of health care products. Abbott common stock is listed on the NYSE under the trading symbol “ABT”. Abbott

1

Table of Contents

common stock is also listed on the Chicago Stock Exchange, the London Stock Exchange and the SIX Swiss Exchange. Abbott’s principal executive office is located at 100 Abbott Park Road, Abbott Park, Illinois 60064-6400 and its telephone number is (224) 667-6100.

Angel Sub, Inc., which we refer to as “Merger Sub”, was formed by Abbott solely for the purpose of completing the merger. Merger Sub became a party to the merger agreement through execution of a joinder agreement to the merger agreement on February 2, 2016. Upon the consummation of the merger, Merger Sub will cease to exist. Merger Sub’s principal executive office is located at 100 Abbott Park Road, Abbott Park, Illinois 60064-6400 and its telephone number is (224) 667-6100.

The Merger

(page 26)

The Company and Abbott entered into an Agreement and Plan of Merger, which we refer to as the “merger agreement”, on January 30, 2016. A copy of the merger agreement is included as Annex A to this proxy statement. Merger Sub became party to the merger agreement through execution of a joinder agreement to the merger agreement on February 2, 2016. Under the terms of the merger agreement, subject to the satisfaction or waiver (if permissible under applicable law) of specified conditions, Merger Sub will be merged with and into the Company, which we refer to as the “merger”. The Company will survive the merger as a subsidiary of Abbott (the “surviving corporation”).

Upon the consummation of the merger, each share of Company common stock that is issued and outstanding immediately prior to the effective time (defined below under “The Merger Agreement—Closing and Effective Time of the Merger”) of the merger, other than shares of Company common stock owned by the Company as treasury stock, or owned by Abbott or Merger Sub and other than shares of Company common stock owned by wholly owned subsidiaries of the Company or Abbott (other than Merger Sub) that Abbott has elected to be canceled and other than shares of Company common stock owned by stockholders who have properly exercised appraisal rights of such shares in accordance with Section 262 of the General Corporation Law of the State of Delaware (the “DGCL”), will be converted into the right to receive $56.00 in cash (the “merger consideration”), without interest and less any applicable withholding taxes.

The Special Meeting

(page 18)

The special meeting will be held on [ ], 2016, at [ ] local time. At the special meeting, holders of Company common stock will be asked to, among other things, vote for the adoption of the merger agreement. Please see the section of this proxy statement entitled “The Special Meeting” for additional information on the special meeting, including how to vote your shares of Company common stock.

Stockholders Entitled to Vote; Vote Required to Adopt the Merger Agreement

(page 19)

You may vote the shares of Company common stock at the special meeting that you owned at the close of business on [ ], 2016, the record date for the special meeting. As of the close of business on the record date, there were [ ] shares of Company common stock outstanding and entitled to vote. You may cast one vote for each share of Company common stock that you held on the record date. The adoption of the merger agreement by the holders of Company common stock requires the affirmative vote of stockholders holding at least a majority of the outstanding shares of Company common stock entitled to vote thereon as of the close of business on the record date.

Background of the Merger

(page 26)

A description of the process we undertook that led to the proposed merger, including our discussions with Abbott, is included in this proxy statement under “The Merger—Background of the Merger”.

2

Table of Contents

Reasons for the Merger; Recommendation of the Board

(page 37)

After careful consideration, the Board determined to approve the merger agreement and recommend the adoption of the merger agreement by the holders of Company common stock. Accordingly, the Board recommends a vote “FOR” the proposal to adopt the merger agreement. The Board also recommends a vote “FOR” the nonbinding compensation proposal and “FOR” the adjournment proposal (each, as described below under “Questions and Answers about the Special Meeting and the Merger—What proposals will be considered at the special meeting?”).

The Board believes that the merger agreement and the merger are advisable and in the best interests of the Company and its stockholders. For a discussion of the material factors that the Board considered in determining to recommend the adoption of the merger agreement, please see the section of this proxy statement entitled “The Merger—Reasons for the Merger” beginning on page 37.

Opinion of the Company’s Financial Advisor

(page 40)

At a meeting of the Board on January 30, 2016, J.P. Morgan Securities LLC, which we refer to as “J.P. Morgan”, rendered its oral opinion, subsequently confirmed in writing, to the Board that, as of such date and based upon and subject to the factors and assumptions set forth in its opinion, the consideration to be paid to the holders of Company common stock in the proposed merger was fair, from a financial point of view, to such holders.

The full text of J.P. Morgan’s written opinion, dated January 30, 2016, which sets forth the assumptions made, procedures followed, matters considered and limitations on the review undertaken by J.P. Morgan in connection with the opinion, is attached as Annex B to this proxy statement and is incorporated herein by reference. The Company’s stockholders are urged to read the opinion in its entirety. J.P. Morgan’s written opinion is addressed to the Board, is directed only to the fairness, from a financial point of view, of the merger consideration to be paid to the holders of Company common stock in the proposed merger and does not constitute a recommendation to any Company stockholder as to how such stockholder should vote at the special meeting. The summary of the opinion of J.P. Morgan set forth in this proxy statement is qualified in its entirety by reference to the full text of such opinion. For a more complete description of J.P. Morgan’s opinion, see the section entitled “The Merger—Opinion of the Company’s Financial Advisor” beginning on page 40 and Annex B to this proxy statement.

Certain Effects of the Merger

(page 51)

Upon the consummation of the merger, Merger Sub will be merged with and into the Company, and the Company will continue to exist following the merger as a subsidiary of Abbott.

Following the consummation of the merger, shares of Company common stock will no longer be traded on the NYSE or any other public market, and the registration of shares of Company common stock under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), will be terminated.

Effects on the Company if the Merger Is Not Completed

(page 52)

In the event that the proposal to adopt the merger agreement does not receive the required approval from the holders of Company common stock, or if the merger is not completed for any other reason, the holders of Company common stock will not receive any payment for their shares of Company common stock in connection with the merger. Instead, the Company will remain an independent public company and stockholders will continue to own their shares of Company common stock. Under certain circumstances, if the merger agreement is terminated, the Company may be obligated to pay to Abbott a termination fee. Please see the sections of this proxy statement entitled “The Merger Agreement—Termination Fee” beginning on page 79.

3

Table of Contents

Treatment of Convertible Preferred Stock

(page 53)

Holders of convertible preferred stock are not entitled to vote on the proposal to adopt the merger agreement, the nonbinding compensation proposal or the adjournment proposal. Each share of convertible preferred stock issued and outstanding immediately prior to the effective time of the merger (other than shares of convertible preferred stock owned by stockholders who have properly exercised appraisal rights of such shares in accordance with Section 262 of the DGCL) will remain issued and outstanding following the effective time of the merger as one share of Series B Convertible Preferred Stock, par value $0.001 per share, of the surviving corporation. The Certificate of Designations governing the terms of the convertible preferred stock will not be altered as a result of the merger. For information regarding the effects of the merger on the holders of convertible preferred stock, please see the document titled “Questions and Answers about Alere’s Series B Preferred Stock” filed by the Company with the SEC on Schedule 14A on February 12, 2016.

Treatment of Equity and Equity-Based Awards

(page 66)

At the effective time of the merger, subject to all required withholding taxes:

| • | each option to purchase shares of Company common stock, which we refer to as a “Company stock option”, other than rights under the Company’s Employee Stock Purchase Plan, which we refer to as the “ESPP”, whether vested or unvested, will be canceled and converted into the right to receive an amount in cash equal to the product of (x) the number of shares of Company common stock underlying such unexercised Company stock option and (y) the excess (if any) of the merger consideration over the exercise price per share of such Company stock option, and each outstanding Company stock option that has an exercise price that is greater than or equal to the merger consideration will be canceled for no consideration; and |

| • | each restricted stock unit of the Company, which we refer to as a “Company RSU”, that is outstanding immediately prior to the effective time of the merger will be canceled and converted into the right to receive an amount in cash equal to the product of (x) the number of shares of Company common stock subject to such Company RSU and (y) the merger consideration. |

In addition, the merger agreement provides that prior to the effective time of the merger, the ESPP will continue in effect, but no new offering periods under the ESPP will commence during the period from the date of the merger agreement through the effective time of the merger, no person will be permitted to increase his or her payroll elections through the ESPP and no new individuals will be permitted to commence participation in the ESPP. See “The Merger Agreement—Treatment of Equity and Equity-Based Awards” beginning on page 66.

Interests of the Company’s Directors and Executive Officers in the Merger

(page 53)

The Company’s directors and executive officers have interests in the merger that may be different from, or in addition to, the interests of the Company’s stockholders generally. The members of the Board were aware of and considered these interests in reaching the determination to approve the merger agreement and deem the merger agreement, the merger and the other transactions contemplated by the merger agreement to be advisable and in the best interests of the Company, and in recommending that the holders of Company common stock vote for the approval of the merger agreement. These interests include:

| • | each Company stock option and Company RSU, whether vested or unvested, will be cashed out upon the effective time of the merger in accordance with the terms of the merger agreement (as described below in “The Merger Agreement—Treatment of Equity and Equity-Based Awards”); |

| • | each of the Company’s executive officers is party to a change of control agreement with the Company that provides severance and other benefits (including in certain cases a golden parachute excise tax gross-up) in the case of a qualifying termination of employment in connection with or following a change of control, which will include the completion of the merger; |

4

Table of Contents

| • | employees of the Company (including the executive officers) are eligible to receive retention awards (as of the date of this proxy statement, no determinations have been made as to whether any executive officer will receive an award or the amounts of any such potential awards to any such individual, although the parties have agreed that the aggregate amount of retention awards will not exceed $25 million); and |

| • | the Company’s directors and executive officers are entitled to continued indemnification and insurance coverage under the merger agreement. |

Please see the section entitled “The Merger—Interests of the Company’s Directors and Executive Officers in the Merger” beginning on page 53 of this proxy statement for additional information about these financial interests.

Common Stock Ownership of Directors and Executive Officers

(page 22)

As of [ ], 2016, the directors and executive officers of Alere beneficially owned in the aggregate [ ] shares of Company common stock, or approximately [ ]% of the outstanding shares of Company common stock. We currently expect that each of these individuals will vote all of his or her shares of Company common stock in favor of each of the proposals to be presented at the special meeting, although none of them are obligated to do so.

Financing of the Merger

(page 53)

The merger agreement does not contain any financing-related closing condition and Abbott has represented that it will have sufficient funds at closing to fund the payment of the merger consideration and any other payments required in connection with consummation of the merger. Abbott has informed the Company that it expects that funds needed by Abbott and Merger Sub in connection with the merger will be derived from (i) the proceeds from the sale of debt securities; (ii) borrowings under Abbott’s existing or, if any, new loan agreements; (iii) cash on hand; or (iv) any combination of the foregoing. Abbott has obtained a commitment letter for a 364-day senior unsecured bridge term loan facility for an amount not to exceed $9 billion to provide back-up financing in conjunction with the merger.

Conditions of the Merger

(page 78)

Each party’s obligation to consummate the merger is subject to the satisfaction or waiver (if permissible under applicable law), on or prior to the closing date of the merger, which we refer to as the “closing date”, of the following conditions:

| • | no judgment enacted, promulgated, issued, entered, amended or enforced by any court of competent jurisdiction, or any other governmental entity or applicable law (collectively, “restraints”) shall be in effect enjoining or otherwise prohibiting the consummation of the merger; |

| • | the expiration or early termination of the waiting period (including any extension thereof) applicable to the merger under (i) the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (the “HSR Act”) and (ii) the antitrust laws of Brazil, Canada, China, the European Union, Japan, South Africa and South Korea (the “non-U.S. antitrust laws”) and the receipt of governmental approvals under the non-U.S. antitrust laws; |

| • | the adoption of the merger agreement by the holders of a majority of the outstanding shares of Company common stock; |

| • | subject to certain materiality and other qualifiers, the accuracy of the representations and warranties of the other party; and |

| • | performance in all material respects by the other party of its obligations under the merger agreement. |

5

Table of Contents

In addition, Abbott’s obligation to consummate the merger is also subject to the absence of any effect, change, event or occurrence that, individually or in the aggregate, has had or would reasonably be expected to have a material adverse effect on the Company (which term is described in the section entitled “The Merger Agreement—Representations and Warranties”).

The consummation of the merger is not conditioned upon Abbott’s receipt of financing.

Before the closing, each of the Company and Abbott may waive any of the conditions to its obligation to consummate the merger even though one or more of the conditions described above has not been met, except where waiver is not permissible under applicable law.

Regulatory Approvals Required for the Merger

(page 63)

The consummation of the merger is subject to review under the HSR Act and the non-U.S. antitrust laws. As described above in the section entitled “—Conditions of the Merger”, the obligations of Abbott and the Company to effect the merger are subject to the expiration or termination of the waiting period (and any extension thereof) applicable to the merger under the HSR Act and the non-U.S. antitrust laws and the receipt of governmental approvals under the non-U.S. antitrust laws.

The merger agreement includes covenants obligating each of the parties to use reasonable best efforts to cause the merger to be consummated and to take certain actions to resolve objections under any antitrust laws.

No Solicitation; Board Recommendation

(page 72)

The merger agreement generally restricts the Company’s ability to solicit takeover proposals (as defined below under “The Merger Agreement—No Solicitation; Board Recommendation”) from third parties (including by furnishing non-public information), or to participate in discussions or negotiations with third parties regarding any takeover proposal. Under certain circumstances, however, and in compliance with certain obligations contained in the merger agreement, the Company is permitted to engage in negotiations with, and provide information to, third parties that have made an unsolicited takeover proposal that the Board determines in good faith, after consultation with its financial advisors and outside legal counsel, constitutes a superior proposal (as defined below under “The Merger Agreement—No Solicitation; Board Recommendation”) or is reasonably likely to result in a superior proposal and that the failure to do so is reasonably likely to be inconsistent with the directors’ fiduciary duties under applicable law. Under certain circumstances, the Company is permitted to terminate the merger agreement prior to the adoption of the merger agreement by the holders of Company common stock in connection with entering into a definitive agreement with respect to a superior proposal, subject to the concurrent payment by the Company of a $177 million termination fee to Abbott.

Termination

(page 79)

The merger agreement may be terminated at any time prior to the effective time of the merger in the following circumstances:

| • | by mutual written consent of the Company and Abbott; |

| • | by either Abbott or the Company, if: |

| • | the merger is not consummated by January 30, 2017 (the “outside date”) (which will be automatically extended to April 30, 2017 if the expiration or termination of the waiting period (and any extension thereof) applicable to the merger under the HSR Act or the non-U.S. antitrust laws or the receipt of any governmental approvals under the non-U.S. antitrust laws has not occurred, but all other closing conditions have been fulfilled or are capable of being satisfied); provided that the right to so terminate the merger agreement will not be available to a party whose breach of any provision of the merger agreement results in the failure of the merger to be consummated on or before the outside date; |

6

Table of Contents

| • | a restraint that enjoins or otherwise prohibits consummation of the merger is in effect and has become final and nonappealable; provided that the party seeking to so terminate the merger agreement has used the required efforts to prevent the entry of and to remove such restraint in accordance with its obligations under the merger agreement; or |

| • | the holders of Company common stock fail to adopt the merger agreement at the special meeting (including any adjournments and postponements thereof); |

| • | by Abbott: |

| • | in the event of certain uncured breaches of the merger agreement by the Company; or |

| • | if the Board or a committee thereof makes an adverse recommendation change (as defined below under “The Merger Agreement—No Solicitation; Board Recommendation”); or |

| • | by the Company: |

| • | in the event of certain uncured breaches of the merger agreement by Abbott or Merger Sub; or |

| • | prior to the adoption of the merger agreement by the holders of Company common stock at the special meeting, in connection with entering into a definitive agreement with respect to a superior proposal, subject to the concurrent payment of the termination fee (as described below under “The Merger Agreement—Termination Fee”). |

Termination Fee

(page 79)

If the merger agreement is terminated in the following circumstances, the Company will be required to pay Abbott a termination fee of $177 million:

| • | by either Abbott or the Company because (i) the holders of Company common stock fail to adopt the merger agreement at the special meeting or (ii) the outside date has arrived and, in each such case, (A) a bona fide takeover proposal shall have been publicly made, publicly proposed or otherwise publicly communicated after the date of the merger agreement and not withdrawn prior to the earlier of the completion of the special meeting (including any adjournment or postponement thereof) and the time of termination and (B) at any time on or prior to the 12-month anniversary of such termination, the Company enters into a definitive agreement with respect to a takeover proposal (whether or not such takeover proposal was the same takeover proposal referred to in clause (A) and provided that the term “takeover proposal” shall have the meaning defined below under “The Merger Agreement—No Solicitation; Board Recommendation” except that all references to 25% shall be deemed to be references to 50%) and such takeover proposal is subsequently consummated, even if after such 12-month anniversary; |

| • | by the Company prior to the adoption of the merger agreement by the holders of Company common stock in order to accept a superior proposal and enter into a definitive agreement in connection with that superior proposal; or |

| • | by Abbott because the Board or a committee thereof makes an adverse recommendation change (as defined below under “The Merger Agreement—No Solicitation; Board Recommendation”). |

Appraisal Rights

(page 84)

Under the DGCL, holders of Company common stock who do not vote in favor of adoption of the merger agreement will have the right to seek appraisal and receive the fair value of their shares of Company common stock as determined by the Delaware Court of Chancery in lieu of receiving the merger consideration if the merger is completed, but only if they strictly comply with the procedures and requirements set forth in Section 262 of the DGCL. Any holder of record of shares of Company common stock intending to exercise appraisal rights, among other things, must properly submit a written demand for appraisal to us prior to the vote on the

7

Table of Contents

proposal to adopt the merger agreement, must not vote in favor of the proposal to adopt the merger agreement, must continue to hold the shares of Company common stock through the effective time of the merger and must otherwise comply with all of the procedures required by Section 262 of the DGCL.

Holders of convertible preferred stock are not entitled to vote on the proposal to adopt the merger agreement, but holders of shares of convertible preferred stock that are outstanding immediately prior to the effective time of the merger will have the right to seek appraisal and receive the fair value of their shares of convertible preferred stock as determined by the Delaware Court of Chancery, but only if they strictly comply with the procedures and requirements set forth in Section 262 of the DGCL. Any holder of record of shares of convertible preferred stock intending to exercise appraisal rights, among other things, must properly submit a written demand for appraisal to us prior to the vote by the holders of Company common stock on the proposal to adopt the merger agreement, must continue to hold the shares of convertible preferred stock through the effective time of the merger and must otherwise comply precisely with all of the procedures required by Section 262 of the DGCL.

The relevant provisions of the DGCL are included as Annex C to this proxy statement. We urge you to read these provisions carefully and in their entirety. Moreover, due to the complexity of the procedures for exercising the right to seek appraisal, stockholders who are considering exercising such rights are encouraged to seek the advice of legal counsel. Failure to comply strictly with all of the procedures required by Section 262 of the DGCL will result in loss of the right of appraisal. You should be aware that the fair value of your shares of Company common stock or convertible preferred stock as determined under Section 262 of the DGCL could be more than, the same as, or less than the value that you are entitled to receive under the terms of the merger agreement.

Material U.S. Federal Income Tax Consequences of the Merger

(page 61)

The receipt of cash pursuant to the merger will be a taxable transaction for U.S. federal income tax purposes and may also be a taxable transaction under applicable state, local or foreign income or other tax laws. Generally, for U.S. federal income tax purposes, if you are a holder of Company common stock who is a U.S. holder (as defined below in the section of this proxy statement entitled “The Merger—Material U.S. Federal Income Tax Consequences of the Merger”), you will recognize gain or loss equal to the difference between the amount of cash you receive in the merger and your adjusted tax basis in the shares of Company common stock converted into cash in the merger. If you are a holder of Company common stock who is a non-U.S. holder (as defined below in the section of this proxy statement entitled “The Merger—Material U.S. Federal Income Tax Consequences of the Merger”), the merger will generally not be a taxable transaction to you under U.S. federal income tax laws unless you have certain connections to the United States, but may be a taxable transaction to you under non-U.S. federal income tax laws, and you are encouraged to seek tax advice regarding such matters. Because individual circumstances may differ, we recommend that you consult your own tax advisor to determine the particular tax effects to you.

You should read the section of this proxy statement entitled “The Merger—Material U.S. Federal Income Tax Consequences of the Merger” beginning on page 61 for a more complete discussion of the material U.S. federal income tax consequences of the merger.

Current Price of Common Stock

(page 86)

The closing sale price of Company common stock on the NYSE on September 16, 2016 was $44.07. You are encouraged to obtain current market quotations for Company common stock in connection with voting your shares of Company common stock.

8

Table of Contents

Additional Information

(page 93)

You can find more information about the Company in the periodic reports and other information we file with the SEC. The information is available at the SEC’s public reference facilities and at the website maintained by the SEC at www.sec.gov. See “Where You Can Find Additional Information” beginning on page 93.

9

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE SPECIAL MEETING AND THE MERGER

The following questions and answers are intended to briefly address some commonly asked questions regarding the special meeting and the merger. These questions and answers may not address all questions that may be important to you as a holder of Company common stock. You should read the more detailed information contained elsewhere in this proxy statement, the annexes to this proxy statement and the documents referred to in this proxy statement.

| Q: | Why am I receiving this proxy statement? |

| A: | On January 30, 2016, the Company entered into the merger agreement with Abbott, and Merger Sub became a party to the merger agreement through the execution of a joinder agreement to the merger agreement on February 2, 2016. Pursuant to the merger agreement, Merger Sub will be merged with and into Alere, with Alere surviving the merger as a subsidiary of Abbott. |

You are receiving this proxy statement in connection with the solicitation of proxies by the Board in favor of the proposal to adopt the merger agreement and the other matters to be voted on at the special meeting described below under “—What proposals will be considered at the special meeting?”

| Q: | As a holder of Company common stock, what will I receive in the merger? |

| A: | If the merger is completed, you will be entitled to receive $56.00 in cash, without interest and less any applicable withholding taxes, for each share of Company common stock that you own immediately prior to the effective time of the merger. |

The exchange of shares of Company common stock for cash pursuant to the merger will be a taxable transaction for U.S. federal income tax purposes. Please see the section of this proxy statement entitled “The Merger—Material U.S. Federal Income Tax Consequences of the Merger” beginning on page 61 for a more detailed description of the United States federal income tax consequences of the merger. You should consult your own tax advisor for a full understanding of how the merger will affect your federal, state, local and/or non-U.S. taxes.

Holders of shares of Company common stock who properly exercise and perfect their appraisal rights under the DGCL and comply precisely with the procedures and requirements set forth in Section 262 of the DGCL will not receive the merger consideration, but will instead be paid the fair value of their shares, as determined by the Delaware Court of Chancery, unless such holder subsequently withdraws or otherwise loses such holder’s rights to demand for appraisal.

| Q: | What will happen to outstanding Company equity compensation awards in the merger? |

At the effective time of the merger, subject to all required withholding taxes:

| • | each Company stock option, other than rights under ESPP, whether vested or unvested, will be canceled and converted into the right to receive an amount in cash equal to the product of (x) the number of shares of Company common stock underlying such Company stock option and (y) the excess (if any) of the merger consideration over the exercise price per share of such Company stock option, and each outstanding Company stock option that has an exercise price that is greater than or equal to the merger consideration will be canceled for no consideration; and |

| • | each Company RSU that is outstanding immediately prior to the effective time of the merger will be canceled and converted into the right to receive an amount in cash equal to the product of (x) the number of shares of Company common stock subject to such Company RSU and (y) the merger consideration. |

In addition, the merger agreement provides that prior to the effective time, no new offering periods under the ESPP will commence during the period from the date of the merger agreement through the effective time, no person will be permitted to increase his or her payroll elections through the ESPP and no new individuals will be permitted to commence participation in the ESPP. See “The Merger Agreement—Treatment of Equity and Equity-Based Awards” beginning on page 66.

10

Table of Contents

| Q: | What will happen to the outstanding convertible preferred stock in the merger? |

| A: | Holders of convertible preferred stock are not entitled to vote on the proposal to adopt the merger agreement, the nonbinding compensation proposal or the adjournment proposal. Each share of convertible preferred stock issued and outstanding immediately prior to the effective time of the merger (other than shares of convertible preferred stock owned by stockholders who have properly exercised appraisal rights of such shares in accordance with Section 262 of the DGCL) will remain issued and outstanding following the effective time of the merger as one share of Series B Convertible Preferred Stock, par value $0.001 per share, of the surviving corporation. The Certificate of Designations governing the terms of the convertible preferred stock will not be altered as a result of the merger. |

For more information regarding the effects of the merger on the holders of convertible preferred stock, please see the document titled “Questions and Answers about Alere’s Series B Preferred Stock” filed by the Company with the SEC on Schedule 14A on February 12, 2016.

| Q: | When and where is the special meeting of our stockholders? |

| A: | The special meeting will be held on [ ], 2016, at [ ] local time, at [ ]. |

| Q: | Who is entitled to vote at the special meeting? |

| A: | Only holders of record of Company common stock as of the close of business on [ ], 2016, the record date for the special meeting, are entitled to vote the shares of Company common stock they held on the record date at the special meeting. As of the close of business on the record date, there were [ ] shares of Company common stock outstanding and entitled to vote. Each stockholder is entitled to one vote for each share of Company common stock held by such stockholder on the record date on each of the proposals presented in this proxy statement. |

| Q: | What proposals will be considered at the special meeting? |

| A: | At the special meeting, holders of Company common stock will be asked to consider and vote on the following proposals: |

| • | a proposal to adopt the merger agreement; |

| • | a nonbinding, advisory proposal to approve the compensation that may be paid or may become payable to the Company’s named executive officers in connection with, or following, the consummation of the merger (this nonbinding, advisory proposal, which we refer to as the “nonbinding compensation proposal”, relates only to contractual obligations of the Company in existence prior to consummation of the merger that may result in a payment to the Company’s named executive officers in connection with, or following, the consummation of the merger and does not relate to any new compensation or other arrangements between the Company’s named executive officers and Abbott or, following the merger, the surviving corporation and its subsidiaries); and |

| • | a proposal to adjourn the special meeting to a later date or time, if necessary or appropriate, to solicit additional proxies in the event there are insufficient votes at the time of the special meeting or any adjournment or postponement thereof to adopt the merger agreement, which we refer to as the “adjournment proposal”. |

| Q: | What constitutes a quorum for purposes of the special meeting? |

| A: | A majority of all of the issued and outstanding shares of Company common stock entitled to vote, present in person or represented by proxy, constitutes a quorum for the transaction of business at any meeting of the holders of Company common stock. Abstentions will be counted for purposes of determining the presence of a quorum. “Broker non-votes” (as described under “The Special Meeting—Quorum”) will not be counted for purposes of determining the presence of a quorum unless the broker, bank, trust, custodian or other nominee (we refer to those organizations collectively as “broker”) has been instructed to vote on at least one of the proposals presented in this proxy statement. If, however, less than a quorum is present or represented |

11

Table of Contents

| at the special meeting, the holders of Company common stock representing a majority of the voting power present or represented at the meeting may adjourn the meeting from time to time, and the meeting may be held as adjourned without further notice other than announcement at the meeting. |

| Q: | What vote of our stockholders is required to approve each of the proposals? |

| A: | The adoption of the merger agreement by holders of Company common stock requires the affirmative vote of stockholders holding at least a majority of the outstanding shares of Company common stock entitled to vote thereon as of the close of business on the record date. Abstentions, failures to vote and “broker non-votes” will have the same effect as a vote “AGAINST” the proposal to approve the merger agreement. Note that you may vote to adopt the merger agreement and vote not to approve the nonbinding compensation proposal or adjournment proposal and vice versa. |

The approval of the nonbinding compensation proposal by holders of Company common stock requires the approval by a majority of the votes cast for or against that proposal at the special meeting. Assuming a quorum is present at the special meeting, abstentions, failures to vote and “broker non-votes” will have no effect on the outcome of the nonbinding compensation proposal.

The approval of the adjournment proposal requires the approval by a majority of the votes cast for or against that proposal at the special meeting. Assuming a quorum is present at the special meeting, abstentions, failures to vote and “broker non-votes” will have no effect on the outcome of the nonbinding compensation proposal. If less than a majority of the outstanding shares of Company common stock entitled to vote are present in person or represented by proxy at the special meeting, a majority of the shares present or represented at the meeting may also adjourn the meeting under Alere’s Amended and Restated By-Laws.

| Q: | How does the Board recommend that I vote? |

| A: | The Board recommends a vote “FOR” the proposal to adopt the merger agreement, “FOR” the nonbinding compensation proposal and “FOR” the adjournment proposal |

For a discussion of the factors that the Board considered in determining to recommend the adoption of the merger agreement, please see the section of this proxy statement entitled “The Merger—Reasons for the Merger” beginning on page 37. In addition, in considering the recommendation of the Board with respect to the merger agreement, you should be aware that some of the Company’s directors and executive officers have interests that may be different from, or in addition to, the interests of the Company’s stockholders generally. Please see the section of this proxy statement entitled “The Merger—Interests of the Company’s Directors and Executive Officers in the Merger” beginning on page 53.

| Q: | How do the Company’s directors and executive officers intend to vote? |

| A: | As of [ ], 2016, the directors and executive officers of Alere beneficially owned in the aggregate [ ] shares of Company common stock, or approximately [ ]% of the outstanding shares of Company common stock. We currently expect that each of these individuals will vote all of his or her shares of Company common stock in favor of each of the proposals to be presented at the special meeting, although none of them are obligated to do so. |

| Q: | Do any of the Company’s directors or executive officers have any interests in the merger that are different from, or in addition to, my interests as a stockholder? |

| A: | In considering the proposals to be voted on at the special meeting, you should be aware that the Company’s directors and executive officers have interests in the merger that may be different from, or in addition to, your interests as a stockholder. The members of the Board were aware of and considered these interests in reaching the determination to approve the merger agreement and deem the merger agreement, the merger |

12

Table of Contents

| and the other transactions contemplated by the merger agreement to be advisable and in the best interests of the Company, and in recommending that the holders of Company common stock vote for the approval of the merger agreement. These interests include: |

| • | each Company stock option and Company RSU, whether vested or unvested, will be cashed out upon the effective time of the merger in accordance with the terms of the merger agreement (as described below in “The Merger Agreement—Treatment of Equity and Equity-Based Awards”); |

| • | each of the Company’s executive officers is party to a change of control agreement with Company that provides severance and other benefits (including in certain cases a golden parachute excise tax gross-up) in the case of a qualifying termination of employment in connection with or following a change of control, which will include completion of the merger; |

| • | employees of the Company (including the executive officers) are eligible to receive retention awards (as of the date of this proxy statement, no determinations have been made as to whether any executive officer will receive an award or the amounts of any such potential awards to any such individual, although the parties have agreed that the aggregate amount of retention awards will not exceed $25 million); and |

| • | The Company’s directors and executive officers are entitled to continued indemnification and insurance coverage under the merger agreement. |

For more information, please see the section of this proxy statement entitled “The Merger—Interests of the Company’s Directors and Executive Officers in the Merger” beginning on page 53.

| Q: | What happens if I sell my shares of Company common stock before the special meeting? |

| A: | The record date for the special meeting is earlier than the date of the special meeting. If you own shares of Company common stock on the record date, but transfer your shares after the record date but before the effective time of the merger, you will retain your right to vote such shares at the special meeting. However, the right to receive the merger consideration will pass to the person to whom you transferred your shares. |

| Q: | How do I cast my vote if I am a stockholder of record? |

| A: | If you are a stockholder with shares of Company common stock registered in your name, you may vote such shares in person at the special meeting or by submitting a proxy for the special meeting via the internet, by telephone or by completing, signing, dating and mailing the enclosed proxy card in the envelope provided. For more detailed instructions on how to vote using one of these methods, please see the section of this proxy statement entitled “The Special Meeting—Voting Procedures” beginning on page 20. |

If you are a holder of record of shares of Company common stock and you submit a proxy card or voting instructions but do not direct how to vote on each item, the persons named as proxies will vote in favor of the proposal to adopt the merger agreement, the nonbinding compensation proposal and the adjournment proposal.

| Q: | How do I cast my vote if my shares of Company common stock are held in “street name” by my broker? |

| A: | If you are a stockholder with shares of Company common stock held in “street name”, which means your shares are held in an account at a broker, you must follow the instructions from your broker in order to vote such shares. Without following those instructions, your shares will not be voted, which will have the same effect as a vote “AGAINST” the proposal to approve the merger agreement. |

| Q: | What will happen if I abstain from voting or fail to vote on any of the proposals? |

| A: | If you abstain from voting, fail to cast your vote in person or by proxy or fail to give voting instructions to your broker, it will have the same effect as a vote “AGAINST” the proposal to approve the merger agreement. |

13

Table of Contents

Assuming a quorum is present at the special meeting, abstentions, failures to vote and “broker non-votes” will have no effect on the outcome of the nonbinding compensation proposal or the adjournment proposal.

| Q: | Can I change my vote after I have delivered my proxy? |

| A: | Yes. If you are a stockholder with shares of Company common stock registered in your name, once you have given your proxy vote for the matters described in this proxy statement, you may revoke it at any time prior to the time it is voted, by filing with the Secretary of the Company an instrument revoking the proxy, by submitting a new proxy bearing a later date, by using the telephone or internet proxy submission procedures described under “The Special Meeting—Voting Procedures” or by completing, signing, dating and returning a new proxy card by mail to the Company, or by attending the special meeting and voting in person. Merely attending the special meeting will not, by itself, revoke a proxy. Please note, however, that only your last-dated proxy will count. Please note that if you want to revoke your proxy by sending a new proxy card or an instrument revoking the proxy to the Company, you should ensure that you send your new proxy card or instrument revoking the proxy in sufficient time for it to be received by the Company prior to the special meeting. |

If you are a stockholder with shares of Company common stock held in “street name”, you should follow the instructions of your broker regarding the revocation of proxies. If your broker allows you to submit a proxy via the internet or by telephone, you may be able to change your vote by submitting a new proxy via the internet or by telephone or by mail.

| Q: | What should I do if I receive more than one set of voting materials? |

| A: | You may receive more than one set of voting materials, including multiple copies of this proxy statement or multiple proxy or voting instruction cards. For example, if you hold your shares of Company common stock in more than one brokerage account, you will receive a separate voting instruction card for each brokerage account in which you hold shares of Company common stock. If you are a holder of Company common stock of record and your shares of Company common stock are registered in more than one name, you will receive more than one proxy card. Please submit each proxy and voting instruction card that you receive to ensure that all your shares of Company common stock are voted. |

| Q: | If I hold my shares of Company common stock in certificated form, should I send in my stock certificates now? |

| A: | No. Promptly after the effective time of the merger, each holder of a certificate representing any Company common stock that has been converted into the right to receive the merger consideration, will be sent a letter of transmittal describing the procedure for surrendering your shares in exchange for the merger consideration. If you hold your shares in certificated form, you will receive your cash payment after the paying agent receives your stock certificates and any other documents requested in the instructions. You should not return your stock certificates with the enclosed proxy card, and you should not forward your stock certificates to the paying agent without a letter of transmittal. If you hold shares of Company common stock in non-certificated book-entry form, you will not be required to deliver a stock certificate, and you will receive your cash payment after the paying agent receives the documents requested in the instructions. |

| Q: | Am I entitled to exercise appraisal rights instead of receiving the merger consideration for my shares of Company common stock? |

| A: | Holders of Company common stock and convertible preferred stock are entitled to appraisal rights under Section 262 of the DGCL so long as they follow the procedures precisely and satisfy the conditions set forth in Section 262 of the DGCL. For more information regarding appraisal rights, see “Appraisal Rights” beginning on page 84. In addition, a copy of Section 262 of the DGCL is attached as Annex C to this proxy statement. Failure to strictly comply with Section 262 of the DGCL may result in your waiver of, or inability to exercise, appraisal rights. |

14

Table of Contents

| Q: | When is the merger expected to be completed? |

| A: | We are working toward completing the merger as promptly as possible. We are confident that the merger will be completed in accordance with the terms set forth in the merger agreement, but we cannot be certain when or if the conditions of the merger will be satisfied or (if permissible under applicable law) waived. The merger cannot be completed until the conditions to closing are satisfied or (if permissible under applicable law) waived, including the adoption of the merger agreement by the holders of Company common stock at the special meeting and the receipt of certain regulatory approvals. |

| Q: | What effect will the merger have on the Company? |

| A: | If the merger is consummated, Merger Sub will be merged with and into the Company, and the Company will continue to exist following the merger as a subsidiary of Abbott. Following such consummation of the merger, shares of Company common stock will no longer be traded on the NYSE or any other public market, and the registration of shares of Company common stock under the Exchange Act will be terminated. |

| Q: | What happens if the merger is not completed? |

| A: | If the event that the proposal to adopt the merger agreement does not receive the required approval from the holders of Company common stock, or if the merger is not completed for any other reason, the holders of Company common stock will not receive any payment for their Company common stock in connection with the merger. Instead, the Company will remain an independent public company and stockholders will continue to own their shares of Company common stock. The Company common stock will continue to be registered under the Exchange Act and listed and traded on the NYSE. Under certain circumstances, if the merger is not completed, the Company may be obligated to pay to Abbott a termination fee. Please see the section of this proxy statement entitled “The Merger Agreement—Termination Fee” and beginning on page 79. |

| Q: | What is householding and how does it affect me? |

| A: | The SEC permits companies to send a single set of certain disclosure documents to stockholders who share the same address and have the same last name, unless contrary instructions have been received, but only if the applicable company provides advance notice and follows certain procedures. In such cases, each stockholder continues to receive a separate notice of the meeting and proxy card. This practice, known as “householding”, is designed to reduce duplicate mailings and save significant printing and postage costs as well as natural resources. |

If you received a householded mailing and you would like to have additional copies of this proxy statement mailed to you, or you would like to opt out of this practice for future mailings, please submit your request to Investor Relations by phone at (858) 805-2232, by mail to Alere Inc., Investor Relations, 51 Sawyer Road, Suite 200, Waltham, MA 02453, or by e-mail to [email protected]. We will promptly send additional copies of this proxy statement upon receipt of such request.

| Q: | Who can help answer my questions? |

| A: | If you need assistance in completing your proxy card or have questions regarding the special meeting, please contact Innisfree M&A Incorporated, which is acting as the Company’s proxy solicitation agent in connection with the merger, toll free at (888) 750-5834. Brokers may call collect at (212) 750-5833. |

15

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Any statements in this proxy statement regarding the proposed merger, the expected timetable for completing, and the Company’s confidence with respect to the completion of, the proposed merger, future financial and operating results, future capital structure and liquidity, benefits and synergies of the proposed merger, future opportunities for the combined company, general business outlook and any other statements about the future expectations, beliefs, goals, plans or prospects of the board or management of the Company constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Readers can identify these statements by forward-looking words such as “may,” “could,” “should,” “would,” “intend,” “will,” “expect,” “anticipate,” “believe,” “estimate,” “continue” or similar words. A number of important factors could cause actual results of Alere and its subsidiaries to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, (i) the risk that the proposed merger with Abbott may not be completed in a timely manner or at all; (ii) the failure to receive, on a timely basis or otherwise, the required approval of the proposed merger with Abbott by Alere’s stockholders; (iii) the possibility that competing offers or acquisition proposals for Alere will be made; (iv) the possibility that any or all of the various conditions to the consummation of the merger may not be satisfied or waived, including the failure to receive any required regulatory approvals from any applicable governmental entities (or any conditions, limitations or restrictions placed on such approvals); (v) the occurrence of any event, change or other circumstance that could give rise to the termination of the merger agreement, including in circumstances which would require Alere to pay a termination fee or other expenses; (vi) the effect of the announcement or pendency of the transactions contemplated by the merger agreement on Alere’s ability to retain and hire key personnel, its ability to maintain relationships with its customers, suppliers and others with whom it does business, or its operating results and business generally; (vii) risks related to diverting management’s attention from Alere’s ongoing business operations; (viii) the risk that stockholder litigation in connection with the transactions contemplated by the merger agreement may result in significant costs of defense, indemnification and liability; and (ix) the risk factors detailed in Part I, Item 1A, “Risk Factors,” of our Annual Report on Form 10-K for the fiscal year ended December 31, 2015 (as filed with the Securities and Exchange Commission on August 8, 2016) and other risk factors identified herein or from time to time in our periodic filings with the SEC. Readers should carefully review these risk factors, and should not place undue reliance on our forward-looking statements. These forward-looking statements are based on information, plans and estimates at the date of this report. We undertake no obligation to update any forward-looking statements to reflect changes in underlying assumptions or factors, new information, future events or other changes.

16

Table of Contents

Alere Inc.

Alere delivers reliable and actionable health information through rapid diagnostic tests, resulting in better clinical and economic healthcare outcomes globally. Our high-performance diagnostics for infectious disease, cardiometabolic disease and toxicology are designed to meet the growing global demand for accurate, easy-to-use and cost-effective near-patient tests. Our goal is to make Alere products accessible to more people around the world, even those located in remote and resource-limited areas, by making them affordable and usable in any setting. By making critical clinical diagnostic information available to doctors and patients in an actionable timeframe, Alere products help streamline healthcare delivery and improve patient outcomes. Our company, formerly known as Inverness Medical Innovations, Inc., was formed in 2001. Since that time, we have grown our businesses through strategic acquisitions, tactical use of our intellectual property portfolio and organic growth. In July 2010, our company changed its name to Alere Inc. Our common stock is listed on the NYSE under the trading symbol “ALR”. Our convertible preferred stock, designated pursuant to the Certificate of Designations, is listed on the NYSE under the trading symbol “ALRpB”. Alere’s principal executive offices are located at 51 Sawyer Road, Suite 200, Waltham, Massachusetts 02453 and our telephone number is (781) 647-3900.

Abbott Laboratories

Abbott Laboratories, which we refer to as “Abbott”, is an Illinois corporation, incorporated in 1900. Abbott’s principal business is the discovery, development, manufacture and sale of a broad and diversified line of health care products. Abbott common stock is listed on the NYSE under the trading symbol “ABT”. Abbott common stock is also listed on the Chicago Stock Exchange, the London Stock Exchange and the SIX Swiss Exchange. Abbott’s principal executive office is located at 100 Abbott Park Road, Abbott Park, Illinois 60064-6400 and its telephone number is (224) 667-6100.

Angel Sub, Inc.

Merger Sub was formed by Abbott on January 29, 2016 solely for the purpose of completing the merger. Merger Sub became a party to the merger agreement through execution of a joinder agreement to the merger agreement on February 2, 2016. Merger Sub is wholly owned by Abbott and has not engaged in any business except for activities incidental to its formation and in connection with the merger and the other transactions contemplated by the merger agreement. Upon the consummation of the merger, Merger Sub will cease to exist. Merger Sub’s principal executive office is located at 100 Abbott Park Road, Abbott Park, Illinois 60064-6400 and its telephone number is (224) 667-6100.

17

Table of Contents

We are furnishing this proxy statement to the holders of Company common stock as part of the solicitation of proxies by the Board for use at the special meeting and at any adjournments or postponements thereof.

The special meeting will be held on [ ], 2016, at [ ] local time, at [ ].

If you plan to attend the meeting, please note that you will need to present government-issued identification showing your name and photograph (i.e., a driver’s license or passport), and, if you are a representative of an institutional investor, professional evidence showing your representative capacity for such entity, in each case to be verified against our stockholder list as of the record date for the meeting. In addition, if your shares of Company common stock are held in the name of a broker, you will need a valid proxy from such entity or a recent brokerage statement or letter from such entity reflecting your stock ownership as of the record date for the meeting.

Purpose of the Special Meeting

The special meeting is being held for the following purposes:

| • | to consider and vote on a proposal to adopt the merger agreement (see the section of this proxy statement entitled “The Merger Agreement” beginning on page 65); |

| • | to consider and vote on a nonbinding, advisory proposal to approve the compensation that may be paid or may become payable to the Company’s named executive officers in connection with, or following, the consummation of the merger (this nonbinding, advisory proposal, which we refer to as the “nonbinding compensation proposal”, relates only to contractual obligations of the Company in existence prior to consummation of the merger that may result in a payment to the Company’s named executive officers in connection with, or following, the consummation of the merger and does not relate to any new compensation or other arrangements between the Company’s named executive officers and Abbott or, following the merger, the surviving corporation and its subsidiaries) (see the section of this proxy statement entitled “The Merger—Interests of the Company’s Directors and Executive Officers in the Merger” beginning on page 53); and |

| • | to consider and vote on a proposal to adjourn the special meeting to a later date or time, if necessary or appropriate, to solicit additional proxies in the event there are insufficient votes at the time of the special meeting or any adjournment or postponement thereof to adopt the merger agreement, which we refer to as the “adjournment proposal”. |

A copy of the merger agreement is attached as Annex A to this proxy statement.