Form N-CSR Principal Real Estate For: Oct 31

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22742

PRINCIPAL REAL ESTATE INCOME FUND

(exact name of registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

Andrea E. Kuchli

Principal Real Estate Income Fund

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: October 31

Date of reporting period: 11/1/2015 – 10/31/2016

| Item 1. |

Reports to Shareholders.

|

TABLE OF CONTENTS

|

Performance Overview

|

1

|

|

Report of Independent Registered Public Accounting Firm

|

8

|

|

Statement of Investments

|

9

|

|

Statement of Assets and Liabilities

|

15

|

|

Statement of Operations

|

16

|

|

Statements of Changes in Net Assets

|

17

|

|

Statement of Cash Flows

|

18

|

|

Financial Highlights

|

19

|

|

Notes to Financial Statements

|

21

|

|

Dividend Reinvestment Plan

|

31

|

|

Trustees & Officers

|

33

|

|

Additional Information

|

|

|

Portfolio Holdings

|

39

|

|

Proxy Voting

|

39

|

|

Section 19(A) Notices

|

39

|

|

Unaudited Tax Information

|

40

|

|

Data Privacy Policies and Procedures

|

40

|

|

Custodian and Transfer Agent

|

40

|

|

Legal Counsel

|

41

|

|

Independent Registered Public Accounting Firm

|

41

|

www.principalcef.com

|

Principal Real Estate Income Fund

|

Performance Overview

|

|

October 31, 2016 (Unaudited)

|

INVESTMENT OBJECTIVE

The Principal Real Estate Income Fund’s (“PGZ” or the “Fund”) investment objective is to seek to provide high current income, with capital appreciation as a secondary objective, by investing in commercial real estate related securities.

PERFORMANCE OVERVIEW

Principal Real Estate Income Fund (“PGZ” or the “Fund”) was launched June 25, 2013. As of October 31, 2016, the Fund was 62.7% allocated to commercial mortgage backed securities (“CMBS”) and 34.2% allocated to global real estate securities, primarily real estate investment trusts (“REITs”). For the 12-month period ended October 31, 2016, the Fund delivered a net return, at market price, of 4.80%, assuming dividends are reinvested back into the Fund, based on the closing share price of $16.62 on October 31, 2016. This compares to the return of the S&P 500® Index, over the same time period, of 4.51% assuming dividends are reinvested into the index. This also compares to the return of the Barclays U.S. Aggregate Bond Index of 4.37% and the MSCI World Index of 1.18%.

The October 31, 2016 closing market price of $16.62 represented a 12.6% discount to the Fund’s Net Asset Value (“NAV”). This compares to an average 12.21% discount for equity real estate closed-end funds and a 5.91% discount for mortgage-backed securities closed-end funds (source: Bloomberg). These discounts to NAV reflect the volatility that has occurred in the closed-end fund market since June 2013, as expectations for higher interest rates have negatively impacted the attractiveness of the market.

Based on NAV, the Fund returned 5.94%, including dividends, for the 12-month period ended October 31, 2016. During the first 3 months of the period, Fund investments were impacted by the extreme market volatility that followed the decision by the Federal Reserve (the “FED”) to raise interest rates in December 2015 with expectations for four additional rate hikes in 2016. Demand for risk assets dropped dramatically as fears of a policy error by the FED gripped investors as the outlook for economic growth in the market was not consistent with the outlook implied by the FED’s plan. The strength of the U.S. Dollar and the impact it had on oil prices and what that implied for global growth were also big contributors to the fear in the market. There were record fund flows out of High Yield mutual funds and exchange traded funds (“ETFs”) and 10 year treasury yields rallied 65 basis points by mid-February to a 6-month low of 1.66%. This change in fund flows negatively impacted prices for both global REITS and CMBS. Equity markets started to recover the second half of February which helped REIT performance but CMBS spreads did not start to recover from the dramatic repricing in the market until mid-March when the FED revised their outlook for 2016 to two rate hikes instead of four. There were record fund flows back into High Yield mutual funds and ETFs following this announcement and CMBS spreads tightened in response to demand coming back to the market. CMBS spreads also benefited from a period of relatively low new issue supply during the summer as the demand for yield continued to be strong. The overall impact of the heightened market volatility that started during the 4th quarter of 2015 and accelerated the first six weeks of 2016 is reflected in the NAV Price of the Fund declining 8.10% for the 3 months ended February 29, 2016, compared to increasing 8.81% for the next 6 months ended July 31, 2016. Starting in August, interest rates started moving higher as the FED came back into play around a potential rate hike in September which impacted the demand for yield focused stocks like REITS. Higher rates also impacted CMBS returns at the same time that the pace of new issuance increased from the summer lows which pressured spreads as well. The impact of these changes is reflected in the NAV Price of the Fund declining 6.89% for the next 2 months ended October 31, 2016. This volatility in price movement came during a period when CMBS and global real estate securities continued to benefit from the ongoing improvement in real estate fundamentals. In the U.S., demand for space is outpacing supply in most markets which is helping to stabilize or increase rents and lower vacancies across major property types in major markets across the country, resulting in higher net operating income at the property level. Globally, real estate markets are exhibiting a generally solid investment landscape with pockets of both strength and weakness.

|

Annual Report | October 31, 2016

|

1

|

|

Principal Real Estate Income Fund

|

Performance Overview

|

|

October 31, 2016 (Unaudited)

|

CMBS

The CMBS holdings within the Fund returned approximately 2.90% for the 12 months ended October 31, 2016. The attribution of returns is best described when looking at the first 6 month return of -2.04% compared to the second 6 month return of 5.06%. The extreme increase in market volatility during the first 6 months of the period resulted in an historical spread widening driven by FED induced economic concerns and forced sellers of CMBS at a time when liquidity was limited in the market. While spreads on AAA and AA rated 2.0 CMBS recovered by April, the credit curve from AAA to BBB remained steeper than the beginning of the period due to hedge funds not coming back to the market and liquidity remaining a concern. The fund is overweight BBB and BB rated 2.0 CMBS relative to the benchmark. The recovery in spreads on legacy CMBS took longer than on-the-run bonds as investors continued to discount the ability for 2007 vintage CMBS loans to refinance in 2017 due to expectations that the cost of risk retention taking effect at the end of 2016 would result in a higher cost of capital and possibility could be prohibitive for borrowers looking to refinance legacy loans. Prices on legacy securities did start to increase late in the period as the execution on the first risk retention compliance deal that priced in September was stronger than expected. The recovery of Fund returns was impacted by the limited recovery of 2.0 CMBS and the lag in recovery of legacy positions and contributed to portfolio returns lagging the Barclays CMBS Investment Grade Index return for the 12 month period of 4.58%. The index is comprised of over 90% AAA rated securities. The volatility in CMBS returns was driven primarily by changes in technical factors, especially for 2.0 CMBS securities held in the portfolio as commercial real estate fundamentals remained strong. The delinquency rate on loans securing 2.0 CMBS remained low during the period as 4-6% annual property level income growth since 2012 and appreciation in property values allowed borrowers to perform on their mortgages. For legacy bonds, the refinance rate for loans maturing during 2016 remained strong with a 75-80% payoff rate driven by accommodative interest rates, availability of capital from the first mortgage market and most importantly, the availability of capital from the high yield debt market to help borrowers fill the gap between the 2006-2007 vintage loan amount and the first mortgage being offered from lenders in the 2.0 CMBS market. With respect to interest rates, another drag on portfolio performance was the duration of the CMBS bonds held in the portfolio being shorter than the market during a period where interest rates declined. The duration of the CMBS portfolio in the Fund was 3.29 years as of October 31, 2016.

We believe the outlook for CMBS remains positive looking forward through 2017 based on our positive outlook for real estate fundamentals driving strong property level income growth over the next 2-3 years. In our view this income growth should be positive for the credit quality of the underlying CMBS loans and should help support growth in property values even if interest rates start to increase. Longer term, the ability for CMBS issuance to maintain and grow volume levels in the face of risk retention will be important for the market as the height of the maturity cycle hits in 2017.

|

2

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Performance Overview

|

|

October 31, 2016 (Unaudited)

|

GLOBAL REAL ESTATE SECURITIES

The global real estate securities holdings within the Fund returned approximately 9.6%, notably outperforming both global equities, as measured by the MSCI World Index (+1.8%) and global bonds, as measured by the J.P. Morgan Global Government Bond Index (+4.5%) for the 12-months ended October 31, 2016. The investment landscape over the past year has been heavily influenced by both sharp shifts in investor perceptions about their outlook for central bank actions as well as surprising geo-political events. Late in 2015, investors were positioning for several interest rate hikes by the FED in 2016 yet those expectations rapidly evaporated as growth in the U.S. and global economy as well as inflation expectations continued to underwhelm. A surprise move by the Bank of Japan (BOJ) to establish negative short term interest rates in early 2016 was broadly perceived as evidence that the BOJ, and central banks more generally, were running out of options to stimulate growth and inflation. Further adding to investor nervousness was the surprise BREXIT vote for Britain to leave the European Union. As such, investor sentiment toward the macroeconomic outlook has been and remains very cautious. Weak economic data points, concern regarding the effectiveness of loose monetary policy, and Brexit have all fueled cautious investor sentiment. Investor nervousness has caused bond yields to drop to historic lows and caused equity investors to favor income oriented sectors with resilient income streams, such as REITs.

Stylistically within the REIT sector, for the trailing 12 months, investors have strongly favored high dividend-yielding, low volatility stocks with a relatively modest preference for larger cap stocks. This environment, strongly characterized by an investor thirst for yield, favorably benefited the portfolio.

Portfolio returns at the country level, in local terms, were strongest in Canada at 26.3% followed by Hong Kong at 23.2% and China and the U.S. at about 20% each. In USD-terms, Japan was strongest at 26%, closely followed by Canada at 25.3% and Australia at 23.9%. Currency effects detracted from the portfolio returns by 1.55% almost entirely driven by the weakness in the British Pound following BREXIT. The leading contributor to performance continues to be the approximately 50% allocation to the United States which returned 19.7% for the period. Within the U.S., the portfolio especially benefited from its holdings in several owners of U.S. healthcare properties including Senior Housing Properties Trust, Medical Properties Trust, and Welltower which each returned over 20%. Similarly, the portfolio benefited from its holdings in several owners of net-lease properties including Spirit Realty, Agree Realty, and STORE Capital as they too each returned over 20% for the period. U.S. healthcare as well as U.S. net-lease companies performed especially well during the period as they are amongst the highest dividend yielding U.S. property sectors and as highlighted previously, high dividend yielding stocks were especially in favor during the period.

Our proprietary financial model utilized to measure global real estate securities valuation levels indicates securities traded at attractive levels at the end of October 2016. This measure examines the spread between the stocks’ forward looking implied unlevered internal rates of returns (“IRRs”) to global treasury yields. That spread, or ‘risk premium’, of 5.07% as of the end of October is comfortably in excess of the trailing 10 year average of 4.6%. Global REITs remain a yield plus growth oriented investment and therefore have remained well supported amidst extraordinarily low sovereign yields across the globe. We anticipate, however, that as investors increasingly focus on the prospects of the FED raising short term interest rates in December, there may well be periods of heightened volatility in the coming months for all investment asset classes, and particularly yield-oriented asset classes such as REITs. While an upward drift in long term sovereign yields might create volatility, we do not anticipate it being a permanent obstacle to REIT prices heading higher as many property sectors and/or geographies within the REIT space already trade at discounted valuations. It is possible, however, that leadership within the REIT space shifts as investors place greater favor in those REITs with greater growth outlooks over those with the highest dividend yields.

|

Annual Report | October 31, 2016

|

3

|

|

Principal Real Estate Income Fund

|

Performance Overview

|

|

October 31, 2016 (Unaudited)

|

References:

The Premium/Discount is the amount (stated in dollars or percent) by which the selling or purchase price of a fund is greater than (premium) or less than (discount) its face amount/value or net asset value (NAV).

Duration is a measure of the sensitivity of the price (the value of principal) of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. The duration number is a calculation involving present value, yield, coupon, final maturity and call features. The bigger the duration number, the greater the interest-rate risk or reward for bond prices. Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices.

2.0 CMBS is defined as bonds issued post-2009.

S&P 500® Index – A large cap U.S. equities index that includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Barclays U.S. Aggregate Bond Index – A broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed rate taxable bond market, including Treasuries, government related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass throughs), ABS, and CMBS.

MSCI World Index – MSCI’s market capitalization weighted index is composed of companies representative of the market structure of 23 developed market countries in North America, Europe, and the Asia/Pacific Region.

J.P. Morgan Global Government Bond Index – is a widely used benchmark for measuring performance and quantifying risk across international fixed income bond markets. The index measures the total, principal, and interest returns in each market and can be reported in 19 different currencies. By including only traded issues available to international investors, the index provides a realistic measure of market performance.

A bond rating is a grade given to bonds by private, independent ratings services that indicates their credit quality. Investment grade bonds range from AAA to BBB- and will usually see bond yields increase as ratings decrease.

The internal rate of return on an investment is defined as the discount rate at which the present value of all future cash flows is equal to the initial investment or, in other words, the rate at which an investment breaks even.

Issuance information – JPMorgan

|

4

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Performance Overview

|

|

October 31, 2016 (Unaudited)

|

PERFORMANCE as of October 31, 2016

|

TOTAL RETURNS(1)

|

ANNUALIZED | ||

|

Fund

|

1 Year

|

3 Year

|

Since Inception(2)

|

|

Net Asset Value (NAV)(3)

|

5.94%

|

8.64%

|

9.40%

|

|

Market Price(4)

|

4.80%

|

7.48%

|

3.65%

|

|

Barclays U.S. Aggregate Bond Index

|

4.37%

|

3.48%

|

3.77%

|

|

MSCI World Index

|

1.18%

|

3.82%

|

7.57%

|

|

(1)

|

Total returns assume reinvestment of all distributions.

|

|

(2)

|

The Fund commenced operations on June 25, 2013.

|

|

(3)

|

Performance returns are net of management fees and other Fund expenses.

|

|

(4)

|

Market price is the value at which the Fund trades on an exchange. This market price can be higher or lower than its NAV.

|

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data please call 855.838.9485.

Total Annual Expense Ratio as a Percentage of Net Assets Attributable to Common Shares including interest expense, as of October 31, 2016, 2.82%.

Total Annual Expense Ratio as a Percentage of Net Assets Attributable to Common Shares excluding interest expense, as of October 31, 2016, 2.07%.

The Fund is a closed-end fund and does not continuously issue shares for sale as open-end mutual funds do. Since the initial public offering, the Fund now trades only in the secondary market. Investors wishing to buy or sell shares need to place orders through an intermediary or broker and additional charges or commissions will apply. The share price of a closed-end fund is based on the market’s value.

Barclay’s U.S. Aggregate Bond Index – A broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed rate taxable bond market, including Treasuries, government related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass throughs), ABS, and CMBS.

MSCI World Index – MSCI’s market capitalization weighted index is composed of companies representative of the market structure of 23 developed market countries in North America, Europe, and the Asia/Pacific Region.

Indices are unmanaged; their returns do not reflect any fees, expenses, or sales charges.

An investor cannot invest directly in an index.

ALPS Advisors, Inc. is the investment adviser to the Fund.

ALPS Portfolio Solutions Distributor, Inc. is a FINRA member.

Principal Real Estate Investors, LLC is the investment sub-adviser to the Fund. Principal Real Estate Investors, LLC is not affiliated with ALPS Advisors, Inc. or any of its affiliates.

Secondary market support provided to the Fund by ALPS Fund Services, Inc.’s affiliate, ALPS Portfolio Solutions Distributor, Inc.

|

Annual Report | October 31, 2016

|

5

|

|

Principal Real Estate Income Fund

|

Performance Overview

|

|

October 31, 2016 (Unaudited)

|

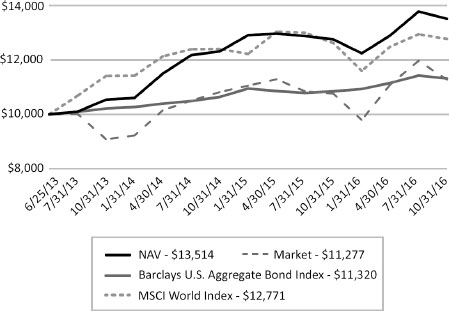

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

The graph below illustrates the growth of a hypothetical $10,000 investment assuming the purchase of common shares of beneficial interest at the closing market price (NYSE: PGZ) of $20.00 on June 25, 2013 (the date of commencement of operations), and tracking its progress through October 31, 2016.

Past performance does not guarantee future results. Performance will fluctuate with changes in market conditions. Current performance may be lower or higher than the performance data shown. Performance information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund shares. An investment in the Fund involves risk, including loss of principal.

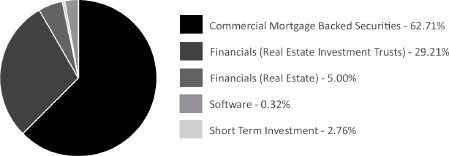

SECTOR ALLOCATION^

|

^

|

Holdings are subject to change.

|

|

Percentages are based on total investments of the Fund.

|

|

6

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Performance Overview

|

|

October 31, 2016 (Unaudited)

|

GEOGRAPHIC BREAKDOWN as of October 31, 2016

|

% of Total Investments

|

|

|

United States

|

83.18%

|

|

Japan

|

3.24%

|

|

Australia

|

2.26%

|

|

Netherlands

|

1.95%

|

|

Singapore

|

1.75%

|

|

Hong Kong

|

1.36%

|

|

France

|

1.23%

|

|

Great Britain

|

1.01%

|

|

Finland

|

0.79%

|

|

Canada

|

0.69%

|

|

Germany

|

0.69%

|

|

Mexico

|

0.66%

|

|

Spain

|

0.51%

|

|

Luxembourg

|

0.27%

|

|

Jersey

|

0.21%

|

|

Guernsey

|

0.14%

|

|

South Africa

|

0.06%

|

|

100.00%

|

Holdings are subject to change.

|

Annual Report | October 31, 2016

|

7

|

Principal Real Estate Income Fund

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees of

Principal Real Estate Income Fund

We have audited the accompanying statement of assets and liabilities, including the statement of investments, of Principal Real Estate Income Fund (the “Fund”) as of October 31, 2016, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the four periods in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of October 31, 2016, by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Principal Real Estate Income Fund as of October 31, 2016, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the four periods in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

COHEN & COMPANY, LTD.

Cleveland, Ohio

December 22, 2016

|

8

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Statement of Investments

|

October 31, 2016

|

Description

|

Shares

|

Value

(Note 2)

|

||||||

|

COMMON STOCKS (50.42%)

|

||||||||

|

Computer Software (0.47%)

|

||||||||

|

InterXion Holding N.V.(a)

|

16,400

|

$

|

610,572

|

|||||

|

Real Estate Management/Services (2.79%)

|

||||||||

|

Aeon Mall Co., Ltd.

|

17,500

|

260,322

|

||||||

|

Atrium European Real Estate, Ltd.

|

96,100

|

411,320

|

||||||

|

Citycon OYJ

|

389,193

|

912,578

|

||||||

|

Deutsche Wohnen AG

|

25,000

|

815,629

|

||||||

|

Mitsubishi Estate Co., Ltd.

|

34,000

|

674,845

|

||||||

|

Sponda OYJ

|

125,000

|

591,687

|

||||||

|

3,666,381

|

||||||||

|

Real Estate Operation/Development (4.51%)

|

||||||||

|

ADO Properties SA(b)(c)

|

13,937

|

507,862

|

||||||

|

Croesus Retail Trust

|

2,282,730

|

1,411,068

|

||||||

|

Inmobiliaria Colonial SA

|

60,000

|

423,710

|

||||||

|

Mitsui Fudosan Co., Ltd.

|

50,000

|

1,139,744

|

||||||

|

New World Development Co., Ltd.

|

931,000

|

1,160,816

|

||||||

|

Sumitomo Realty & Development Co., Ltd.

|

28,000

|

737,713

|

||||||

|

TLG Immobilien AG

|

12,000

|

251,341

|

||||||

|

Tokyo Tatemono Co., Ltd.

|

22,000

|

280,271

|

||||||

|

5,912,525

|

||||||||

|

REITS-Apartments (2.36%)

|

||||||||

|

Apartment Investment & Management Co., Class A

|

19,700

|

868,179

|

||||||

|

Essex Property Trust, Inc.

|

8,600

|

1,841,174

|

||||||

|

Japan Rental Housing Investments, Inc.

|

500

|

386,669

|

||||||

|

3,096,022

|

||||||||

|

REITS-Diversified (13.80%)

|

||||||||

|

Altarea SCA

|

8,469

|

1,617,651

|

||||||

|

Crombie Real Estate Investment Trust

|

20,897

|

210,793

|

||||||

|

Crown Castle International Corp.

|

19,000

|

1,728,810

|

||||||

|

Dexus Property Group

|

210,000

|

1,428,138

|

||||||

|

Duke Realty Corp.

|

23,700

|

619,755

|

||||||

|

Empiric Student Property PLC

|

150,000

|

203,337

|

||||||

|

EPR Properties

|

8,400

|

610,848

|

||||||

|

Equinix, Inc.

|

2,100

|

750,288

|

||||||

|

Frasers Logistics & Industrial Trust(a)(c)

|

786,387

|

545,455

|

||||||

|

Klepierre

|

18,000

|

736,338

|

||||||

|

Liberty Property Trust

|

32,200

|

1,301,846

|

||||||

|

Londonmetric Property PLC

|

145,000

|

264,623

|

||||||

|

Mapletree Commercial Trust

|

139,600

|

153,522

|

||||||

|

Merlin Properties Socimi SA

|

50,000

|

562,048

|

||||||

|

Mirvac Group

|

443,000

|

704,309

|

||||||

|

Nomura Real Estate Master Fund, Inc.

|

250

|

405,264

|

||||||

|

Secure Income REIT PLC

|

15,401

|

58,720

|

||||||

|

Annual Report | October 31, 2016

|

9

|

|

Principal Real Estate Income Fund

|

Statement of Investments

|

October 31, 2016

|

Description

|

Shares

|

Value

(Note 2)

|

||||||

|

REITS-Diversified (13.80%) (continued)

|

||||||||

|

Segro PLC

|

80,187

|

$

|

429,107

|

|||||

|

Sekisui House REIT, Inc.

|

307

|

414,817

|

||||||

|

Spring Real Estate Investment Trust

|

2,870,000

|

1,210,088

|

||||||

|

STAG Industrial, Inc.

|

65,120

|

1,502,319

|

||||||

|

Stockland

|

180,100

|

605,549

|

||||||

|

Viva Energy REIT(a)

|

310,137

|

533,182

|

||||||

|

Wereldhave N.V.

|

33,988

|

1,522,075

|

||||||

|

18,118,882

|

||||||||

|

REITS-Health Care (4.13%)

|

||||||||

|

Care Capital Properties, Inc.

|

35,000

|

929,950

|

||||||

|

Medical Properties Trust, Inc.

|

25,000

|

348,500

|

||||||

|

Physicians Realty Trust

|

24,000

|

474,480

|

||||||

|

Sabra Health Care REIT, Inc.

|

29,500

|

687,350

|

||||||

|

Senior Housing Properties Trust

|

91,000

|

1,935,570

|

||||||

|

Welltower, Inc.

|

15,319

|

1,049,811

|

||||||

|

5,425,661

|

||||||||

|

REITS-Hotels (1.70%)

|

||||||||

|

Hoshino Resorts REIT, Inc.

|

30

|

175,932

|

||||||

|

Hospitality Properties Trust

|

25,600

|

700,416

|

||||||

|

Hospitality Property Fund Ltd., Class B

|

110,000

|

106,625

|

||||||

|

Japan Hotel REIT Investment Corp.

|

700

|

473,252

|

||||||

|

Sunstone Hotel Investors, Inc.

|

62,000

|

778,720

|

||||||

|

2,234,945

|

||||||||

|

REITS-Manufactured Homes (1.12%)

|

||||||||

|

Sun Communities, Inc.

|

19,083

|

1,468,055

|

||||||

|

REITS-Mortgage (0.28%)

|

||||||||

|

CYS Investments, Inc.

|

43,100

|

371,522

|

||||||

|

|

||||||||

|

REITS-Office Property (4.73%)

|

||||||||

|

Alexandria Real Estate Equities, Inc.

|

8,000

|

862,480

|

||||||

|

alstria office REIT-AG

|

20,000

|

258,081

|

||||||

|

Brandywine Realty Trust

|

38,100

|

590,550

|

||||||

|

Champion Real Estate Investment Trust

|

405,000

|

230,293

|

||||||

|

City Office REIT, Inc.

|

84,500

|

1,061,320

|

||||||

|

Corporate Office Properties Trust

|

13,500

|

360,315

|

||||||

|

Investa Office Fund

|

165,000

|

532,186

|

||||||

|

Kilroy Realty Corp.

|

10,500

|

754,215

|

||||||

|

SL Green Realty Corp.

|

10,400

|

1,021,488

|

||||||

|

Viva Industrial Trust

|

939,500

|

540,234

|

||||||

|

6,211,162

|

||||||||

|

REITS-Regional Malls (3.22%)

|

||||||||

|

Simon Property Group, Inc.

|

22,700

|

4,221,292

|

||||||

|

10

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Statement of Investments

|

October 31, 2016

|

Description

|

Shares

|

Value

(Note 2)

|

||||||

|

REITS-Shopping Centers (4.18%)

|

||||||||

|

Aventus Retail Property Fund, Ltd.

|

95,000

|

$

|

164,767

|

|||||

|

Equity One, Inc.

|

11,000

|

313,500

|

||||||

|

Fortune Real Estate Investment Trust

|

587,000

|

711,465

|

||||||

|

Hammerson PLC

|

64,500

|

435,004

|

||||||

|

Kenedix Retail REIT Corp.

|

418

|

1,008,429

|

||||||

|

NewRiver Retail, Ltd.

|

149,000

|

565,366

|

||||||

|

Ramco-Gershenson Properties Trust

|

18,400

|

319,056

|

||||||

|

Scentre Group REIT

|

115,000

|

368,293

|

||||||

|

Vastned Retail N.V.

|

41,600

|

1,598,781

|

||||||

|

|

5,484,661

|

|||||||

|

REITS-Single Tenant (2.67%)

|

||||||||

|

Agree Realty Corp.

|

15,700

|

759,095

|

||||||

|

Spirit Realty Capital, Inc.

|

118,000

|

1,405,380

|

||||||

|

STORE Capital Corp.

|

48,881

|

1,333,963

|

||||||

|

3,498,438

|

||||||||

|

REITS-Storage/Warehousing (1.44%)

|

||||||||

|

CubeSmart

|

22,000

|

573,540

|

||||||

|

National Storage Affiliates Trust

|

54,545

|

1,067,991

|

||||||

|

Safestore Holdings PLC

|

56,000

|

245,594

|

||||||

|

1,887,125

|

||||||||

|

REITS-Warehouse/Industrials (3.02%)

|

||||||||

|

Granite Real Estate Investment Trust

|

8,000

|

251,696

|

||||||

|

Japan Logistics Fund, Inc.

|

115

|

250,134

|

||||||

|

PLA Administradora Industrial S de RL de CV

|

645,000

|

1,069,824

|

||||||

|

Prologis Property Mexico SA de CV

|

120,000

|

201,894

|

||||||

|

Prologis, Inc.

|

17,000

|

886,720

|

||||||

|

Terreno Realty Corp.

|

17,000

|

443,700

|

||||||

|

WPT Industrial Real Estate Investment Trust

|

72,800

|

865,592

|

||||||

|

|

3,969,560

|

|||||||

|

TOTAL COMMON STOCKS (Cost $63,137,244)

|

66,176,803

|

|||||||

|

Rate

|

Maturity

Date

|

Principal

Amount

|

Value

(Note 2)

|

|||||||||

|

COMMERCIAL MORTGAGE BACKED SECURITIES (91.57%)

|

||||||||||||

|

Commercial Mortgage Backed Securities-Other (57.40%)

|

||||||||||||

|

Bank of America Commercial Mortgage Trust, Series 2008-1(d)

|

6.270%

|

|

01/10/18

|

$

|

2,500,000

|

$

|

2,488,212

|

|||||

|

CD Commercial Mortgage Trust, Series 2007-CD4(d)

|

5.398%

|

|

12/11/49

|

9,690,942

|

8,168,881

|

|||||||

|

Credit Suisse Commercial Mortgage Trust, Series 2006-C4(d)

|

5.538%

|

|

09/15/39

|

4,030,399

|

4,048,088

|

|||||||

|

Credit Suisse Commercial Mortgage Trust, Series 2007-C1

|

5.416%

|

|

02/15/40

|

10,000,000

|

9,952,825

|

|||||||

|

Annual Report | October 31, 2016

|

11

|

|

Principal Real Estate Income Fund

|

Statement of Investments

|

October 31, 2016

|

Rate

|

Maturity

Date

|

Principal

Amount

|

Value

(Note 2)

|

|||||||||

|

Commercial Mortgage Backed Securities-Other (continued)

|

||||||||||||

|

CSAIL Commercial Mortgage Trust, Series 2015-C4(d)

|

3.585%

|

|

11/11/48

|

$

|

5,000,000

|

$

|

3,433,170

|

|||||

|

FHLMC Multifamily Structured Pass Through Certificates, Series 2011-KAIV(d)(e)

|

3.615%

|

|

06/25/41

|

9,000,000

|

1,306,307

|

|||||||

|

FHLMC Multifamily Structured Pass Through Certificates, Series 2012-K052(d)(e)

|

1.611%

|

|

01/25/26

|

9,690,000

|

1,027,746

|

|||||||

|

FHLMC Multifamily Structured Pass Through Certificates, Series 2012-K706(d)(e)

|

1.903%

|

|

12/25/18

|

59,524,000

|

2,123,626

|

|||||||

|

FHLMC Multifamily Structured Pass Through Certificates, Series 2012-K707(d)(e)

|

1.806%

|

|

01/25/19

|

27,555,000

|

961,890

|

|||||||

|

FHLMC Multifamily Structured Pass Through Certificates, Series 2012-K709(d)(e)

|

1.700%

|

|

04/25/40

|

30,601,130

|

1,150,804

|

|||||||

|

FHLMC Multifamily Structured Pass Through Certificates, Series 2012-K710(d)(e)

|

1.661%

|

|

06/25/42

|

27,830,000

|

1,060,868

|

|||||||

|

Greenwich Capital Commercial Funding Corp. Commercial Mortgage Trust, Series 2007-GG9(d)

|

5.505%

|

|

02/10/17

|

7,500,000

|

7,112,768

|

|||||||

|

JPMorgan Chase Commercial Mortgage Securities Trust, Series 2006-CIBC16

|

5.623%

|

|

05/12/45

|

2,500,000

|

2,505,737

|

|||||||

|

JPMorgan Chase Commercial Mortgage Securities Trust, Series 2006-CIBC17(d)

|

5.489%

|

|

12/12/43

|

3,642,959

|

1,568,851

|

|||||||

|

JPMorgan Chase Commercial Mortgage Securities Trust, Series 2007-CIBC19(d)

|

5.715%

|

|

05/12/17

|

3,500,000

|

2,832,823

|

|||||||

|

JPMorgan Chase Commercial Mortgage Securities Trust, Series 2013-C15(b)(d)(e)

|

1.485%

|

|

10/15/23

|

11,500,000

|

945,850

|

|||||||

|

LB-CMT Commercial Mortgage Trust, Series 2007-C3(d)

|

5.916%

|

|

06/15/17

|

1,000,000

|

994,627

|

|||||||

|

LB-UBS Commercial Mortgage Trust, Series 2006-C7

|

5.407%

|

|

11/15/16

|

2,453,777

|

1,924,529

|

|||||||

|

Morgan Stanley Bank of America Merrill Lynch Trust, Series 2015-C20(b)(d)(e)

|

1.612%

|

|

02/15/25

|

23,967,000

|

2,361,138

|

|||||||

|

Morgan Stanley Capital I Trust, Series 2016-UB11XE(b)(d)(e)

|

1.500%

|

|

08/15/26

|

13,495,500

|

1,401,056

|

|||||||

|

Wachovia Bank Commercial Mortgage Trust, Series 2006-C29(d)

|

5.368%

|

|

11/15/48

|

13,000,000

|

12,971,842

|

|||||||

|

12

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Statement of Investments

|

October 31, 2016

|

Rate

|

Maturity

Date

|

Principal

Amount

|

Value

(Note 2)

|

|||||||||

|

Commercial Mortgage Backed Securities-Other (continued)

|

||||||||||||

|

Wachovia Bank Commercial Mortgage Trust, Series 2007-C30(d)

|

5.413%

|

|

12/15/43

|

$

|

5,000,000

|

$

|

5,001,058

|

|||||

|

75,342,696

|

||||||||||||

|

Commercial Mortgage Backed Securities-Subordinated (34.17%)

|

||||||||||||

|

Bank of America Commercial Mortgage Trust, Series 2006-6

|

5.480%

|

|

10/10/45

|

3,000,000

|

3,005,905

|

|||||||

|

Bank of America Commercial Mortgage Trust, Series 2016-UBS10(b)

|

3.000%

|

|

06/15/49

|

3,500,000

|

2,437,259

|

|||||||

|

Commercial Mortgage Trust, Series 2013-CR11(b)(d)

|

4.371%

|

|

10/10/23

|

5,108,000

|

3,600,460

|

|||||||

|

Commercial Mortgage Trust, Series 2014-CCRE17(b)(d)

|

4.299%

|

|

05/10/24

|

6,000,000

|

3,817,801

|

|||||||

|

Commercial Mortgage Trust, Series 2014-CR14(b)(d)

|

3.496%

|

|

01/10/24

|

2,000,000

|

1,223,489

|

|||||||

|

Goldman Sachs Mortgage Securities Trust, Series 2013-GC13(b)(d)

|

4.065%

|

|

07/10/23

|

3,000,000

|

2,702,013

|

|||||||

|

Goldman Sachs Mortgage Securities Trust, Series 2013-GC16(b)(d)

|

5.320%

|

|

11/10/46

|

2,342,405

|

2,185,206

|

|||||||

|

Goldman Sachs Mortgage Securities Trust, Series 2014-GC22(b)

|

3.582%

|

|

06/10/47

|

2,840,000

|

1,698,342

|

|||||||

|

JPMBB Commercial Mortgage Securities Trust, Series 2013-C15(b)

|

3.500%

|

|

10/15/23

|

2,500,000

|

1,868,451

|

|||||||

|

JPMorgan Chase Commercial Mortgage Securities Trust, Series 2013-C16(b)(d)

|

4.975%

|

|

11/15/23

|

2,117,483

|

2,013,919

|

|||||||

|

Merrill Lynch Mortgage Trust, Series 2006-C1(d)

|

5.554%

|

|

05/12/39

|

9,000,000

|

7,733,916

|

|||||||

|

Merrill Lynch-CFC Commercial Mortgage Trust, Series 2006-2(b)(d)

|

5.754%

|

|

06/12/46

|

1,064,501

|

1,062,360

|

|||||||

|

Merrill Lynch-CFC Commercial Mortgage Trust, Series 2006-3(d)

|

5.554%

|

|

11/12/16

|

2,500,000

|

2,392,127

|

|||||||

|

Morgan Stanley Bank of America Merrill Lynch Trust, Series 2013-C8(b)(d)

|

4.062%

|

|

02/15/23

|

3,000,000

|

2,699,407

|

|||||||

|

Morgan Stanley Capital I Trust, Series 2016-UB11E(b)(d)

|

2.709%

|

|

08/15/26

|

5,000,000

|

2,591,462

|

|||||||

|

Wells Fargo Commercial Mortgage Trust, Series 2015-NXS1(d)

|

4.104%

|

|

05/15/48

|

3,440,000

|

2,817,162

|

|||||||

|

Wells Fargo Commercial Mortgage Trust, Series 2015-NXS3(b)

|

3.153%

|

|

09/15/57

|

1,500,000

|

1,009,615

|

|||||||

|

44,858,894

|

||||||||||||

|

TOTAL COMMERCIAL MORTGAGE BACKED SECURITIES (Cost $122,661,873)

|

120,201,590

|

|||||||||||

|

Annual Report | October 31, 2016

|

13

|

|

Principal Real Estate Income Fund

|

Statement of Investments

|

October 31, 2016

|

7-Day

Yield

|

Shares

|

Value

(Note 2)

|

||||||||||

|

SHORT TERM INVESTMENTS (4.04%)

|

||||||||||||

|

State Street Institutional Treasury Plus Money Market Fund

|

0.220%

|

|

5,301,708

|

$

|

5,301,708

|

|||||||

|

TOTAL SHORT TERM INVESTMENTS (Cost $5,301,708)

|

5,301,708

|

|||||||||||

|

TOTAL INVESTMENTS (146.03%) (Cost $191,100,825)

|

$

|

191,680,101

|

||||||||||

|

Liabilities in Excess of Other Assets (-46.03%)

|

(60,420,183

|

)

|

||||||||||

|

NET ASSETS (100.00%)

|

$

|

131,259,918

|

||||||||||

| (a) |

Non-income producing security.

|

| (b) |

Security exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may normally be sold to qualified institutional buyers in transactions exempt from registration. The total value of Rule 144A securities amounts $34,125,690, which represents approximately 26.00% of net assets as of October 31, 2016.

|

| (c) |

Securities were purchased pursuant to Regulation S under the Securities Act of 1933, which exempts securities offered and sold outside of the United States from registration. Such securities cannot be sold in the United States without either an effective registration statement filed pursuant to the Securities Act of 1933, or pursuant to an exemption from registration. As of October 31, 2016, the aggregate market value of those securities was $1,053,317, representing 0.80% of net assets.

|

| (d) |

Interest rate will change at a future date. Interest rate shown reflects the rate in effect at October 31, 2016.

|

| (e) |

Interest only security.

|

See Notes to Financial Statements.

|

14

|

www.principalcef.com

|

Principal Real Estate Income Fund

|

Statement of Assets and Liabilities

|

October 31, 2016

|

|

ASSETS:

|

||||

|

Investments, at value

|

$

|

191,680,101

|

||

|

Receivable for investments sold

|

526,117

|

|||

|

Interest receivable

|

855,219

|

|||

|

Dividends receivable

|

174,562

|

|||

|

Prepaid and other assets

|

38,099

|

|||

|

Total Assets

|

193,274,098

|

|||

|

LIABILITIES:

|

||||

|

Loan payable (Note 3)

|

60,000,000

|

|||

|

Interest due on loan payable

|

128,479

|

|||

|

Payable for investments purchased

|

1,574,138

|

|||

|

Payable to adviser

|

170,882

|

|||

|

Payable to administrator

|

29,902

|

|||

|

Payable to transfer agent

|

2,166

|

|||

|

Payable for trustee fees

|

21,910

|

|||

|

Other payables

|

86,703

|

|||

|

Total Liabilities

|

62,014,180

|

|||

|

Net Assets

|

$

|

131,259,918

|

||

|

NET ASSETS CONSIST OF:

|

||||

|

Paid-in capital

|

$

|

131,315,474

|

||

|

Distributions in excess of net investment income

|

(628,565

|

)

|

||

|

Accumulated net realized gain on investments and foreign currency transactions

|

5,950

|

|||

|

Net unrealized appreciation on investments and translation of assets and liabilities denominated in foreign currencies

|

567,059

|

|||

|

Net Assets

|

$

|

131,259,918

|

||

|

PRICING OF SHARES:

|

||||

|

Net Assets

|

$

|

131,259,918

|

||

|

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value per share)

|

6,899,800

|

|||

|

Net asset value per share

|

$

|

19.02

|

||

|

Cost of Investments

|

$

|

191,100,825

|

||

See Notes to Financial Statements.

|

Annual Report | October 31, 2016

|

15

|

|

Principal Real Estate Income Fund

|

Statement of Operations

|

For the Year Ended October 31, 2016

|

INVESTMENT INCOME:

|

||||

|

Interest

|

$

|

9,836,771

|

||

|

Dividends (net of foreign withholding tax of $156,903)

|

3,189,361

|

|||

|

Total Investment Income

|

13,026,132

|

|||

|

EXPENSES:

|

||||

|

Investment advisory fees

|

2,016,334

|

|||

|

Interest on loan

|

993,591

|

|||

|

Administration fees

|

308,843

|

|||

|

Transfer agent fees

|

28,760

|

|||

|

Audit fees

|

31,000

|

|||

|

Legal fees

|

74,766

|

|||

|

Custodian fees

|

23,247

|

|||

|

Trustee fees

|

81,034

|

|||

|

Printing fees

|

20,945

|

|||

|

Insurance fees

|

41,800

|

|||

|

Excise tax

|

62,621

|

|||

|

Other

|

42,216

|

|||

|

Total Expenses

|

3,725,157

|

|||

|

Net Investment Income

|

9,300,975

|

|||

|

REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS AND FOREIGN CURRENCY:

|

||||

|

Net realized gain/(loss) on:

|

||||

|

Investments

|

2,162,498

|

|||

|

Foreign currency transactions

|

(27,353

|

)

|

||

|

Net realized gain

|

2,135,145

|

|||

|

Net change in unrealized appreciation/(depreciation) on:

|

||||

|

Investments

|

(5,340,153

|

)

|

||

|

Translation of assets and liabilities denominated in foreign currencies

|

(8,638

|

)

|

||

|

Net change in unrealized appreciation

|

(5,348,791

|

)

|

||

|

Net Realized and Unrealized Loss on Investments and Foreign Currency

|

(3,213,646

|

)

|

||

|

Net Increase in Net Assets Resulting from Operations

|

$

|

6,087,329

|

||

See Notes to Financial Statements.

|

16

|

www.principalcef.com

|

Principal Real Estate Income Fund

Statements of Changes in Net Assets

Statements of Changes in Net Assets

|

For the

Year Ended

October 31, 2016

|

For the

Year Ended

October 31, 2015

|

|||||||

|

OPERATIONS:

|

||||||||

|

Net investment income

|

$

|

9,300,975

|

$

|

10,066,328

|

||||

|

Net realized gain on investments and foreign currency transactions

|

2,135,145

|

859,321

|

||||||

|

Net change in unrealized appreciation on investments and translation of assets and liabilities denominated in foreign currencies

|

(5,348,791

|

)

|

(6,868,461

|

)

|

||||

|

Net increase in net assets resulting from operations

|

6,087,329

|

4,057,188

|

||||||

|

DISTRIBUTIONS TO SHAREHOLDERS:

|

||||||||

|

From net investment income

|

(12,005,652

|

)

|

(11,469,338

|

)

|

||||

|

From net realized gains

|

–

|

(432,817

|

)

|

|||||

|

Net decrease in net assets from distributions to shareholders

|

(12,005,652

|

)

|

(11,902,155

|

)

|

||||

|

Net Decrease in Net Assets

|

(5,918,323

|

)

|

(7,844,967

|

)

|

||||

|

NET ASSETS:

|

||||||||

|

Beginning of period

|

137,178,241

|

145,023,208

|

||||||

|

End of period (including undistributed/(distributions in excess of) net investment income of $(628,565) and $212,817)

|

$

|

131,259,918

|

$

|

137,178,241

|

||||

|

OTHER INFORMATION:

|

||||||||

|

Share Transactions:

|

||||||||

|

Shares outstanding - beginning of period

|

6,899,800

|

6,899,800

|

||||||

|

Net increase in shares outstanding

|

–

|

–

|

||||||

|

Shares outstanding - end of period

|

6,899,800

|

6,899,800

|

||||||

See Notes to Financial Statements.

|

Annual Report | October 31, 2016

|

17

|

|

Principal Real Estate Income Fund

|

Statement of Cash Flows

|

For the Year Ended October 31, 2016

|

CASH FLOWS FROM OPERATING ACTIVITIES:

|

||||

|

Net increase in net assets resulting from operations

|

$

|

6,087,329

|

||

|

Adjustments to reconcile net increase in net assets from operations to net cash provided by operating activities:

|

||||

|

Purchases of investment securities

|

(75,469,605

|

)

|

||

|

Proceeds from disposition of investment securities

|

82,558,785

|

|||

|

Net purchases of short-term investment securities

|

(3,364,094

|

)

|

||

|

Net realized (gain)/loss on:

|

||||

|

Investments

|

(2,162,498

|

)

|

||

|

Net change in unrealized (appreciation)/depreciation on:

|

||||

|

Investments

|

5,340,153

|

|||

|

Amortization of discounts and premiums

|

(814,891

|

)

|

||

|

Increase in interest receivable

|

(54,112

|

)

|

||

|

Decrease in dividends receivable

|

7,259

|

|||

|

Decrease in prepaid and other assets

|

16,581

|

|||

|

Decrease in foreign cash due to custodian

|

(181,508

|

)

|

||

|

Increase in interest due on loan payable

|

35,230

|

|||

|

Decrease in payable to transfer agent

|

(6,318

|

)

|

||

|

Decrease in payable to adviser

|

(4,937

|

)

|

||

|

Decrease in payable to administrator

|

(1,804

|

)

|

||

|

Increase in payable for trustee fees

|

33

|

|||

|

Increase in other payables

|

20,049

|

|||

|

Net cash provided by operating activities

|

$

|

12,005,652

|

||

|

CASH FLOWS USED IN FINANCING ACTIVITIES:

|

||||

|

Cash distributions paid

|

$

|

(12,005,652

|

)

|

|

|

Net cash used in financing activities

|

$

|

(12,005,652

|

)

|

|

|

Effect of exchange rates on cash

|

$

|

–

|

||

|

Net increase in cash

|

$

|

–

|

||

|

Cash, beginning balance

|

$

|

–

|

||

|

Cash, ending balance

|

$

|

–

|

||

|

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION:

|

||||

|

Cash paid during the period for interest from bank borrowing

|

$

|

958,361

|

||

See Notes to Financial Statements.

|

18

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Financial Highlights

|

For a share outstanding throughout the periods presented.

|

For the

Year Ended

October 31, 2016

|

For the

Year Ended

October 31, 2015

|

For the

Year Ended

October 31, 2014

|

For the Period

June 25, 2013 (Commencement)

to

October 31, 2013

|

|||||||||||||

|

Net asset value - beginning of period

|

$

|

19.88

|

$

|

21.02

|

$

|

19.68

|

$

|

19.10

|

||||||||

|

Income/(loss) from investment operations:

|

||||||||||||||||

|

Net investment income(a)

|

1.35

|

1.46

|

1.57

|

0.33

|

||||||||||||

|

Net realized and unrealized gain/(loss) on investments

|

(0.47

|

)

|

(0.87

|

)

|

1.44

|

0.70

|

||||||||||

|

Total income from investment operations

|

0.88

|

0.59

|

3.01

|

1.03

|

||||||||||||

|

Less distributions to common shareholders:

|

||||||||||||||||

|

From net investment income

|

(1.74

|

)

|

(1.67

|

)

|

(1.67

|

)

|

(0.41

|

)

|

||||||||

|

From net realized gains

|

–

|

(0.06

|

)

|

–

|

–

|

|||||||||||

|

Total distributions

|

(1.74

|

)

|

(1.73

|

)

|

(1.67

|

)

|

(0.41

|

)

|

||||||||

|

Capital share transactions:

|

||||||||||||||||

|

Common share offering costs charged to paid-in capital

|

–

|

–

|

–

|

(0.04

|

)

|

|||||||||||

|

Total capital share transactions

|

–

|

–

|

–

|

(0.04

|

)

|

|||||||||||

|

Net increase/(decrease) in net asset value

|

(0.86

|

)

|

(1.14

|

)

|

1.34

|

0.58

|

||||||||||

|

Net asset value - end of period

|

$

|

19.02

|

$

|

19.88

|

$

|

21.02

|

$

|

19.68

|

||||||||

|

Market price - end of period

|

$

|

16.62

|

$

|

17.56

|

$

|

19.34

|

$

|

17.76

|

||||||||

|

Total Return(b)

|

5.94

|

%

|

3.61

|

%

|

16.82

|

%

|

5.40

|

%

|

||||||||

|

Total Return - Market Price(b)

|

4.80

|

%

|

(0.54

|

%)

|

19.10

|

%

|

(9.16

|

%)

|

||||||||

|

Supplemental Data:

|

||||||||||||||||

|

Net assets, end of period (in thousands)

|

$

|

131,260

|

$

|

137,178

|

$

|

145,023

|

$

|

135,798

|

||||||||

|

Ratios to Average Net Assets:

|

||||||||||||||||

|

Total expenses

|

2.82

|

%

|

2.59

|

%

|

2.59

|

%

|

2.15

|

%(c)

|

||||||||

|

Total expenses excluding interest expense

|

2.07

|

%

|

2.08

|

%

|

2.04

|

%

|

1.99

|

%(c)

|

||||||||

|

Net investment income

|

7.04

|

%

|

7.02

|

%

|

7.74

|

%

|

5.01

|

%(c)

|

||||||||

|

Total expenses to average managed assets(d)

|

1.94

|

%

|

1.83

|

%

|

1.81

|

%

|

1.93

|

%(c)

|

||||||||

See Notes to Financial Statements.

|

Annual Report | October 31, 2016

|

19

|

|

Principal Real Estate Income Fund

|

Financial Highlights

|

For a share outstanding throughout the periods presented.

|

For the

Year Ended

October 31, 2016

|

For the

Year Ended

October 31, 2015

|

For the

Year Ended

October 31, 2014

|

For the Period

June 25, 2013

(Commencement)

to

October 31, 2013

|

|||||||||||||

|

Portfolio turnover rate

|

41

|

%

|

22

|

%

|

18

|

%

|

1

|

%(e)

|

||||||||

|

Borrowings at End of Period

|

||||||||||||||||

|

Aggregate Amount Outstanding (in thousands)

|

$

|

60,000

|

$

|

60,000

|

$

|

60,000

|

$

|

60,000

|

||||||||

|

Asset Coverage Per $1,000 (in thousands)

|

$

|

3,188

|

$

|

3,286

|

$

|

3,417

|

$

|

3,263

|

||||||||

|

(a)

|

Calculated using average shares throughout the period.

|

|

(b)

|

Total investment return is calculated assuming a purchase of common share at the opening on the first day and a sale at closing on the last day of each period reported. For purposes of this calculation, dividends and distributions, if any, are assumed to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment returns do not reflect brokerage commissions, if any. Periods less than one year are not annualized.

|

|

(c)

|

Annualized.

|

|

(d)

|

Average managed assets represent net assets applicable to common shares plus average amount of borrowings during the period.

|

|

(e)

|

Not annualized.

|

See Notes to Financial Statements.

|

20

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Notes to Financial Statements

|

October 31, 2016

1. ORGANIZATION

Principal Real Estate Income Fund (the “Fund”) is a Delaware statutory trust registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

The Fund’s investment objective is to seek to provide high current income, with capital appreciation as a secondary investment objective, by investing in commercial real estate related securities.

Investing in the Fund involves risks, including exposure to below-investment grade investments. The Fund’s net asset value will vary and its distribution rate may vary and both may be affected by numerous factors, including changes in the market spread over a specified benchmark, market interest rates and performance of the broader equity markets. Fluctuations in net asset value may be magnified as a result of the Fund’s use of leverage.

2. SIGNIFICANT ACCOUNTING POLICIES

Use of Estimates: The preparation of the financial statements in accordance with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements during the period reported. Management believes the estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the Fund ultimately realizes upon sale of the securities. The Fund is considered an investment company under U.S. GAAP and follows the accounting and reporting guidance applicable to investment companies in the Financial Accounting Standards Board Accounting Standards Codification Topic 946 Financial Services – Investment Companies. The financial statements have been prepared as of the close of the New York Stock Exchange (“NYSE”) on October 31, 2016.

Portfolio Valuation: The net asset value per Common Share of the Fund is determined no less frequently than daily, on each day that the NYSE is open for trading, as of the close of regular trading on the NYSE (normally 4:00 p.m. New York time). The Fund’s net asset value per Common Share is calculated in the manner authorized by the Fund’s Board of Trustees (the “Board”). Net asset value is computed by dividing the value of the Fund’s total assets, less its liabilities by the number of shares outstanding.

The Board has established the following procedures for valuation of the Fund’s assets under normal market conditions. Marketable securities listed on foreign or U.S. securities exchanges generally are valued at closing sale prices or, if there were no sales, at the mean between the closing bid and ask prices on the exchange where such securities are primarily traded.

The Fund values commercial mortgage-backed securities and other debt securities not traded in an organized market on the basis of valuations provided by an independent pricing service, approved by the Board, which uses information with respect to transactions in such securities, interest rate movements, new issue information, cash flows, yields, spreads, credit quality, and other pertinent information as determined by the pricing service, in determining value. If the independent primary or secondary pricing service is unable to provide a price for a security, if the price provided by the independent primary or secondary pricing service is deemed unreliable, or if events occurring after the close of the market for a security but before the time as of which the Fund values its Common Shares would materially affect net asset value, such security will be valued at its fair value as determined in good faith under procedures approved by the Board.

|

Annual Report | October 31, 2016

|

21

|

|

Principal Real Estate Income Fund

|

Notes to Financial Statements

|

October 31, 2016

When applicable, fair value of an investment is determined by the Fund’s Fair Valuation Committee as a designee of the Board. In fair valuing the Fund’s investments, consideration is given to several factors, which may include, among others, the following: the fundamental business data relating to the issuer, borrower, or counterparty; an evaluation of the forces which influence the market in which the investments are purchased and sold; the type, size and cost of the investment; the information as to any transactions in or offers for the investment; the price and extent of public trading in similar securities (or equity securities) of the issuer, or comparable companies; the coupon payments, yield data/cash flow data; the quality, value and salability of collateral, if any, securing the investment; the business prospects of the issuer, borrower, or counterparty, as applicable, including any ability to obtain money or resources from a parent or affiliate and an assessment of the issuer’s, borrower’s, or counterparty’s management; the prospects for the industry of the issuer, borrower, or counterparty, as applicable, and multiples (of earnings and/or cash flow) being paid for similar businesses in that industry; one or more independent broker quotes for the sale price of the portfolio security; and other relevant factors.

Securities Transactions and Investment Income: Investment security transactions are accounted for on a trade date basis. Dividend income is recorded on the ex-dividend date. Certain dividend income from foreign securities will be recorded, in the exercise of reasonable diligence, as soon as the Fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date and may be subject to withholding taxes in these jurisdictions. Interest income, which includes amortization of premium and accretion of discount, is recorded on the accrual basis. Realized gains and losses from securities transactions and unrealized appreciation and depreciation of securities are determined using the first-in/first-out cost basis method for both financial reporting and tax purposes.

Fair Value Measurements: The Fund discloses the classification of its fair value measurements following a three-tier hierarchy based on the inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Fund’s investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

|

22

|

www.principalcef.com

|

|

Principal Real Estate Income Fund

|

Notes to Financial Statements

|

October 31, 2016

|

Level 1 –

|

Unadjusted quoted prices in active markets for identical investments, unrestricted assets or liabilities that a Fund has the ability to access at the measurement date;

|

|

Level 2 –

|

Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and

|

|

Level 3 –

|

Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date.

|

The following is a summary of the inputs used to value the Fund’s investments as of October 31, 2016:

Principal Real Estate Income Fund

|

Investments in Securities at Value*

|

Level 1 -

Quoted Prices

|

Level 2 -

Other Significant

Observable Inputs

|

Level 3 -

Significant

Unobservable

Inputs

|

Total

|

||||||||||||

|

Common Stocks

|

$

|

66,176,803

|

$

|

–

|

$

|

–

|

$

|

66,176,803

|

||||||||

|

Commercial Mortgage Backed Securities

|

–

|

120,201,590

|

–

|

120,201,590

|

||||||||||||

|

Short Term Investments

|

5,301,708

|

–

|

–

|

5,301,708

|