Form DEFA14A MONSANTO CO /NEW/

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant x Filed by a party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| ¨ | Definitive Additional Materials | |

| x | Soliciting Material Pursuant to §240.14a-12 | |

MONSANTO COMPANY

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount previously paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing party:

| |||

| (4) | Date Filed:

| |||

|

|

Creating a Global Leader in Agriculture

Innovation Engine to Deliver Enhanced Solutions for the Next Generation of Farming

Media Conference Call | September 14, 2016

|

|

Forward-Looking Statements

Certain statements contained in this communication may constitute “forward-looking statements.” Actual results could differ materially from those projected or forecast in the forward-looking statements. The factors that could cause actual results to differ materially include the following: the risk that Monsanto Company’s (“Monsanto”) stockholders do not approve the transaction; uncertainties as to the timing of the transaction; the possibility that the parties may be unable to achieve expected synergies and operating efficiencies in the merger within the expected timeframes or at all and to successfully integrate Monsanto’s operations into those of Bayer Aktiengesellschaft (“Bayer”); such integration may be more difficult, time-consuming or costly than expected; revenues following the transaction may be lower than expected; operating costs, customer loss and business disruption (including, without limitation, difficulties in maintaining relationships with employees, customers, clients or suppliers) may be greater than expected following the transaction; the retention of certain key employees at Monsanto; risks associated with the disruption of management’s attention from ongoing business operations due to the transaction; the conditions to the completion of the transaction may not be satisfied, or the regulatory approvals required for the transaction may not be obtained on the terms expected or on the anticipated schedule; the parties’ ability to meet expectations regarding the timing, completion and accounting and tax treatments of the merger; the impact of indebtedness incurred by Bayer in connection with the transaction and the potential impact on the rating of indebtedness of

Bayer; the effects of the business combination of Bayer and Monsanto, including the combined company’s future financial condition, operating results, strategy and plans; other factors detailed in Monsanto’s Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) for the fiscal year ended August 31, 2015 and Monsanto’s other filings with the SEC, which are available at http://www.sec.gov and on Monsanto’s website at www.monsanto.com; and other factors discussed in Bayer’s public reports which are available on the

Bayer website at www.bayer.com. Bayer and Monsanto assume no obligation to update the information in this communication, except as otherwise required by law. Readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of the date hereof.

Page 2 Media Conference Call September 14, 2016

|

|

Additional Information

This communication relates to the proposed merger transaction involving Monsanto and Bayer. In connection with the proposed merger, Monsanto and Bayer intend to file relevant materials with the SEC, including Monsanto’s proxy statement on Schedule 14A (the “Proxy Statement”). This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval, and is not a substitute for the Proxy Statement or any other document that Monsanto may file with the SEC or send to its stockholders in connection with the proposed merger. STOCKHOLDERS OF MONSANTO ARE URGED TO READ ALL

RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE PROXY STATEMENT, WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors and security holders will be able to obtain the documents (when available) free of charge at the SEC’s web site, http://www.sec.gov, and Monsanto’s website, www.monsanto.com, and Monsanto stockholders will receive information at an appropriate time on how to obtain transaction-related documents for free from Monsanto. In addition, the documents (when available) may be obtained free of charge by directing a request to Corporate Secretary, Monsanto Company, 800 North Lindbergh Boulevard, St. Louis, Missouri 63167, or by calling (314) 694-8148.

Monsanto, Bayer and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from the holders of Monsanto common stock in respect of the proposed transaction. Information about the directors and executive officers of Monsanto is set forth in the proxy statement for

Monsanto’s 2016 annual meeting of stockholders, which was filed with the SEC on December 10, 2015, and in Monsanto’s Annual Report on Form 10-K for the fiscal year ended August 31, 2015, which was filed with the SEC on October 29, 2015. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the Proxy Statement and other relevant materials to be filed with the SEC in respect of the proposed transaction when they become available.

Page 3 Media Conference Call September 14, 2016

|

|

Bayer and Monsanto to Create a Global

Leader in Agriculture

Realizes a shared vision of integrated agricultural offering delivering enhanced solutions for growers

Creates a leading innovation engine for the next generation of farming

Significant value creation through considerable synergy potential

Reinforces Bayer as a global innovation-driven Life Science company

Joint organisation will further evolve its strong culture of innovation, sustainability and social responsibility

Page 4 Media Conference Call September 14, 2016

|

|

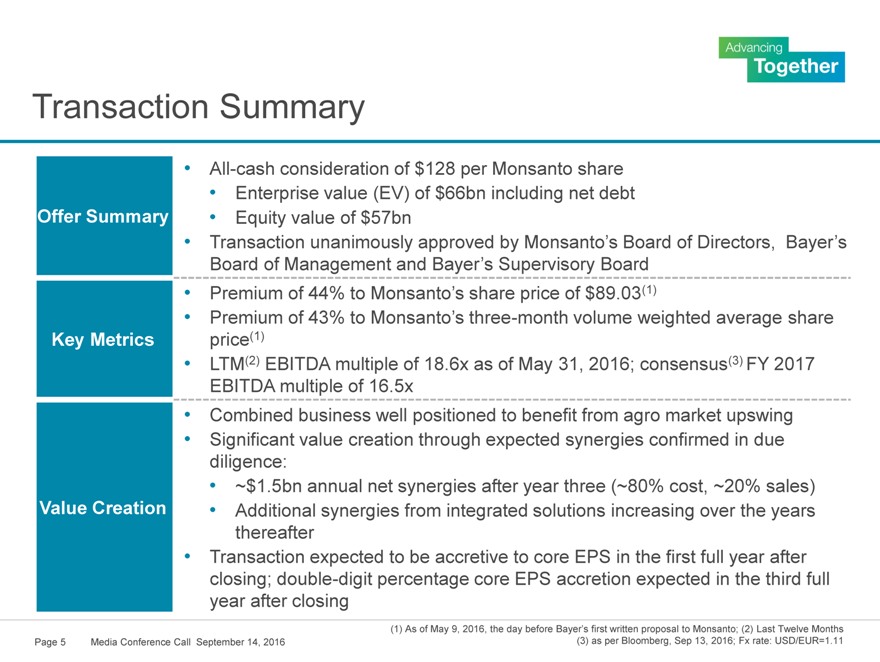

Transaction Summary

All-cash consideration of $128 per Monsanto share

Enterprise value (EV) of $66bn including net debt

Offer Summary Equity value of $57bn

Transaction unanimously approved by Monsanto’s Board of Directors, Bayer’s

Board of Management and Bayer’s Supervisory Board

Premium of 44% to Monsanto’s share price of $89.03(1)

Premium of 43% to Monsanto’s three-month volume weighted average share

Key Metrics price(1)

LTM(2) EBITDA multiple of 18.6x as of May 31, 2016; consensus(3) FY 2017

EBITDA multiple of 16.5x

Combined business well positioned to benefit from agro market upswing

Significant value creation through expected synergies confirmed in due

diligence:

~$1.5bn annual net synergies after year three (~80% cost, ~20% sales)

Value Creation Additional synergies from integrated solutions increasing over the years

thereafter

Transaction expected to be accretive to core EPS in the first full year after

closing; double-digit percentage core EPS accretion expected in the third full

year after closing

(1) As of May 9, 2016, the day before Bayer’s first written proposal to Monsanto; (2) Last Twelve Months

Page 5 Media Conference Call September 14, 2016(3) as per Bloomberg, Sep 13, 2016; Fx rate: USD/EUR=1.11

|

|

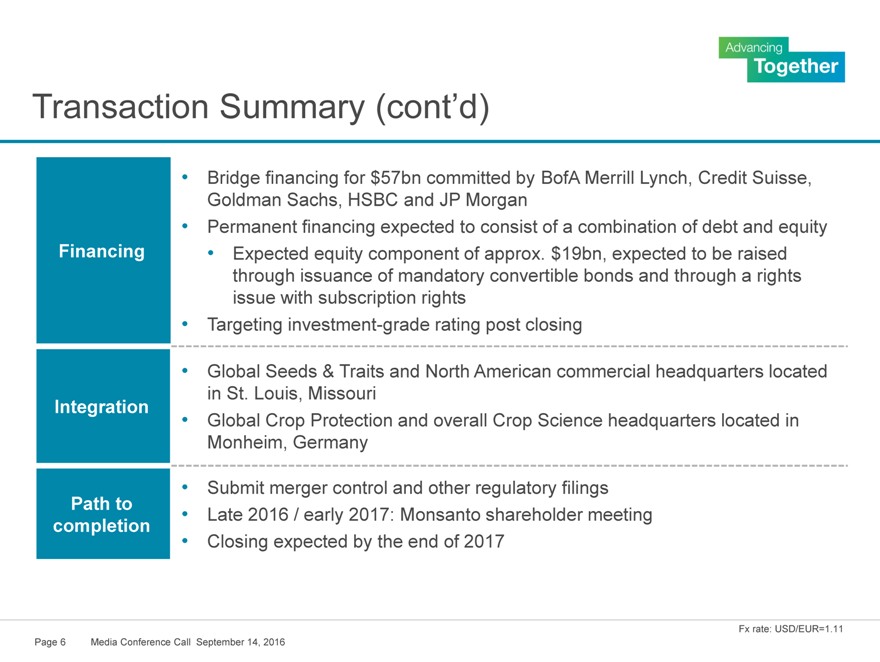

Transaction Summary (cont’d)

Bridge financing for $57bn committed by BofA Merrill Lynch, Credit Suisse,

Goldman Sachs, HSBC and JP Morgan

Permanent financing expected to consist of a combination of debt and equity

Financing Expected equity component of approx. $19bn, expected to be raised

through issuance of mandatory convertible bonds and through a rights

issue with subscription rights

Targeting investment-grade rating post closing

Global Seeds & Traits and North American commercial headquarters located

in St. Louis, Missouri

Integration

Global Crop Protection and overall Crop Science headquarters located in

Monheim, Germany

Submit merger control and other regulatory filings

Path to Late 2016 / early 2017: Monsanto shareholder meeting

completion

Closing expected by the end of 2017

Fx rate: USD/EUR=1.11

Page 6 Media Conference Call September 14, 2016

|

|

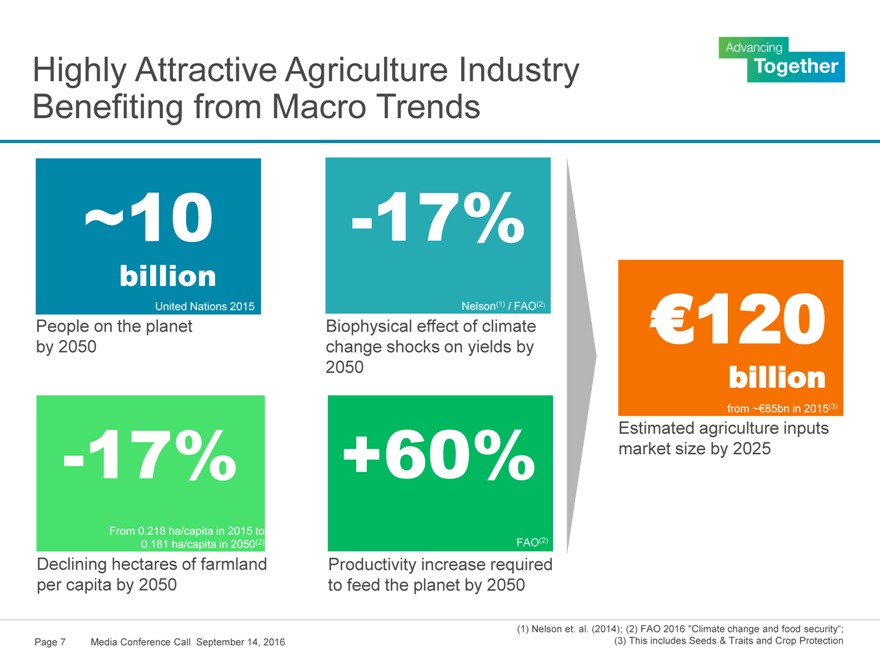

Highly Attractive Agriculture Industry

Benefiting from Macro Trends

~10 -17%

billion

United Nations 2015 Nelson(1) / FAO(2)

People on the planet Biophysical effect of climate €120

by 2050 change shocks on yields by

2050billion

from ~€85bn in 2015(3)

Estimated agriculture inputs

-17% +60% market size by 2025

From 0.218 ha/capita in 2015 to

0.181 ha/capita in 2050(2) FAO(2)

Declining hectares of farmland Productivity increase required

per capita by 2050 to feed the planet by 2050

(1) Nelson et. al. (2014); (2) FAO 2016 “Climate change and food security“;

Page 7 Media Conference Call September 14, 2016 (3) This includes Seeds & Traits and Crop Protection

|

|

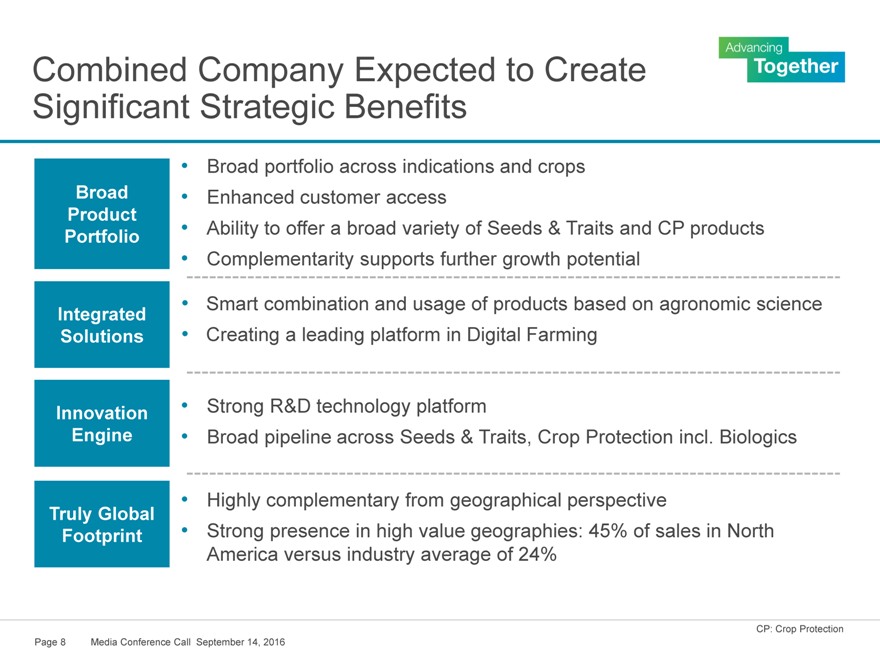

Combined Company Expected to Create

Significant Strategic Benefits

Broad portfolio across indications and crops

Broad Enhanced customer access

Product

Portfolio Ability to offer a broad variety of Seeds & Traits and CP products

Complementarity supports further growth potential

Integrated Smart combination and usage of products based on agronomic science

Solutions Creating a leading platform in Digital Farming

Innovation Strong R&D technology platform

Engine Broad pipeline across Seeds & Traits, Crop Protection incl. Biologics

Highly complementary from geographical perspective

Truly Global

Footprint Strong presence in high value geographies: 45% of sales in North

America versus industry average of 24%

CP: Crop Protection

Page 8 Media Conference Call September 14, 2016

|

|

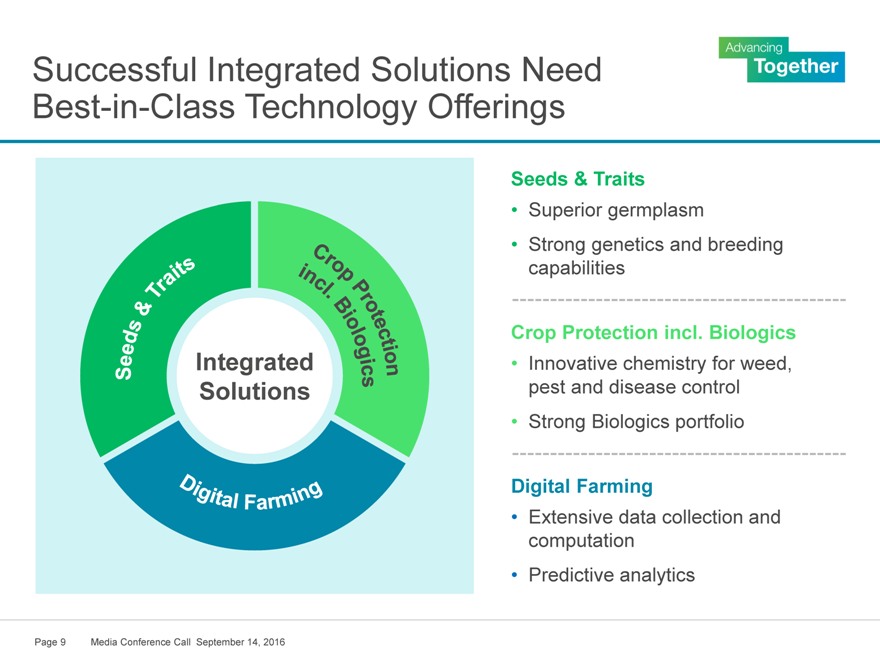

Successful Integrated Solutions Need

Best-in-Class Technology Offerings

Seeds & Traits

Superior germplasm

Strong genetics and breeding capabilities

Crop Protection incl. Biologics

Integrated Innovative chemistry for weed, Solutions pest and disease control

Strong Biologics portfolio

Digital Farming

Extensive data collection and computation

Predictive analytics

Page 9 Media Conference Call September 14, 2016

|

|

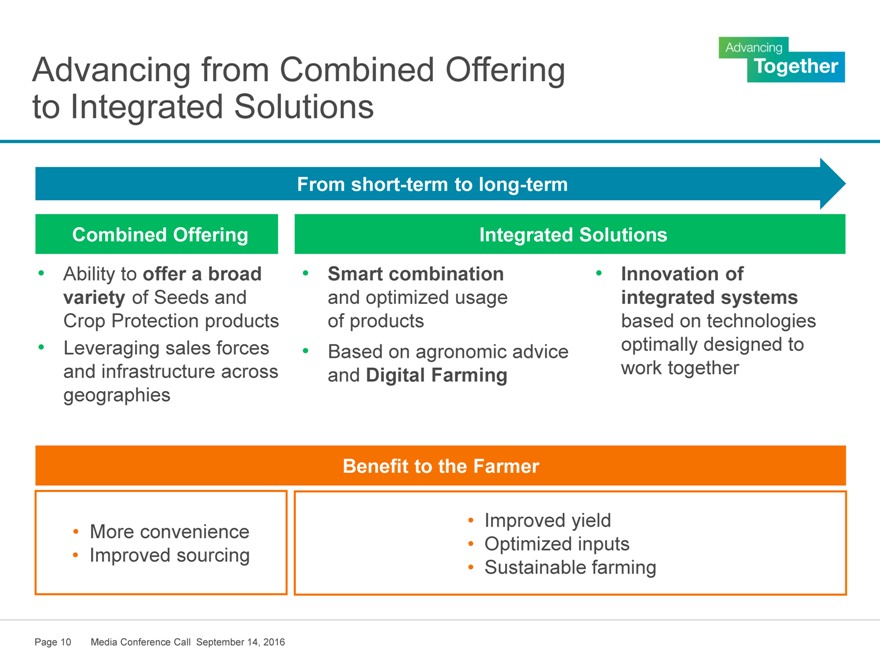

Advancing from Combined Offering

to Integrated Solutions

From short-term to long-term

Combined Offering Integrated Solutions

Ability to offer a broad Smart combination Innovation of

variety of Seeds and and optimized usageintegrated systems

Crop Protection products of productsbased on technologies

Leveraging sales forces Based on agronomic adviceoptimally designed to

and infrastructure across and Digital Farmingwork together

geographies

Benefit to the Farmer

More convenience Improved yield

Improved sourcing Optimized inputs

Sustainable farming

Page 10 Media Conference Call September 14, 2016

|

|

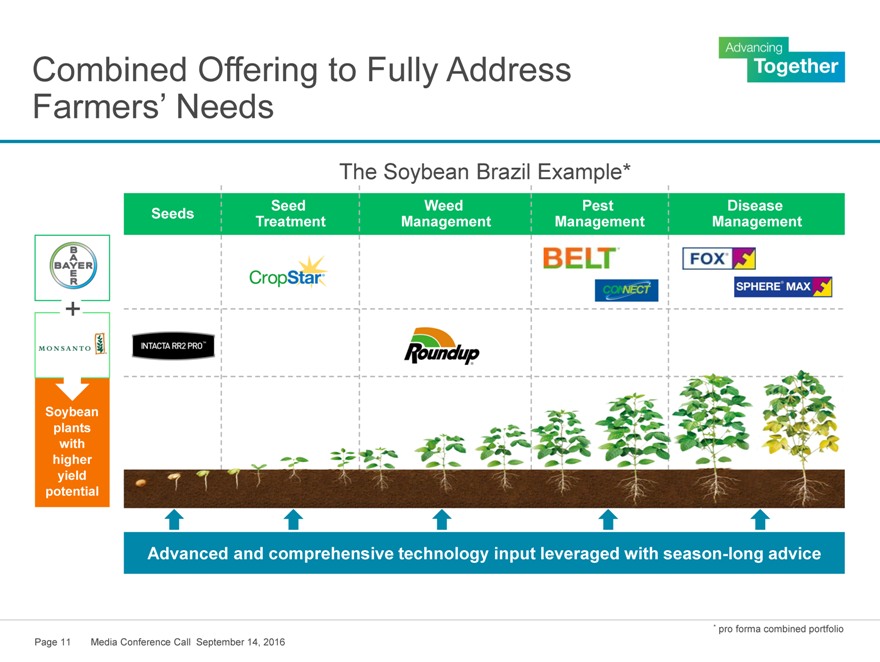

Combined Offering to Fully Address

Farmers’ Needs

The Soybean Brazil Example*

Seed Weed Pest Disease Seeds Treatment Management Management Management

+

Soybean plants with higher yield potential

+

Advanced and comprehensive technology input leveraged with season-long advice

* pro forma combined portfolio Page 11 Media Conference Call September 14, 2016

|

|

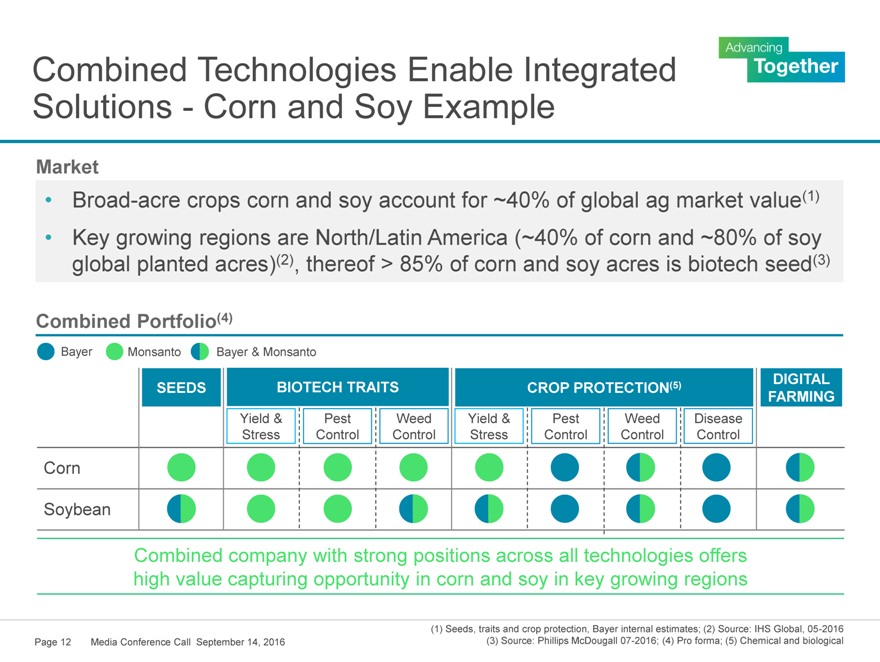

Combined Technologies Enable Integrated

Solutions—Corn and Soy Example

Market

Broad-acre crops corn and soy account for ~40% of global ag market value(1)

Key growing regions are North/Latin America (~40% of corn and ~80% of soy global planted acres)(2), thereof > 85% of corn and soy acres is biotech seed(3)

Combined Portfolio(4)

Bayer Monsanto Bayer & Monsanto

DIGITAL SEEDS BIOTECH TRAITS CROP PROTECTION(5) FARMING

Yield & Pest Weed Yield & Pest Weed Disease Stress Control Control Stress Control Control Control

Corn

Soybean

Combined company with strong positions across all technologies offers high value capturing opportunity in corn and soy in key growing regions

(1) Seeds, traits and crop protection, Bayer internal estimates; (2) Source: IHS Global, 05-2016 Page 12 Media Conference Call September 14, 2016 (3) Source: Phillips McDougall 07-2016; (4) Pro forma; (5) Chemical and biological

|

|

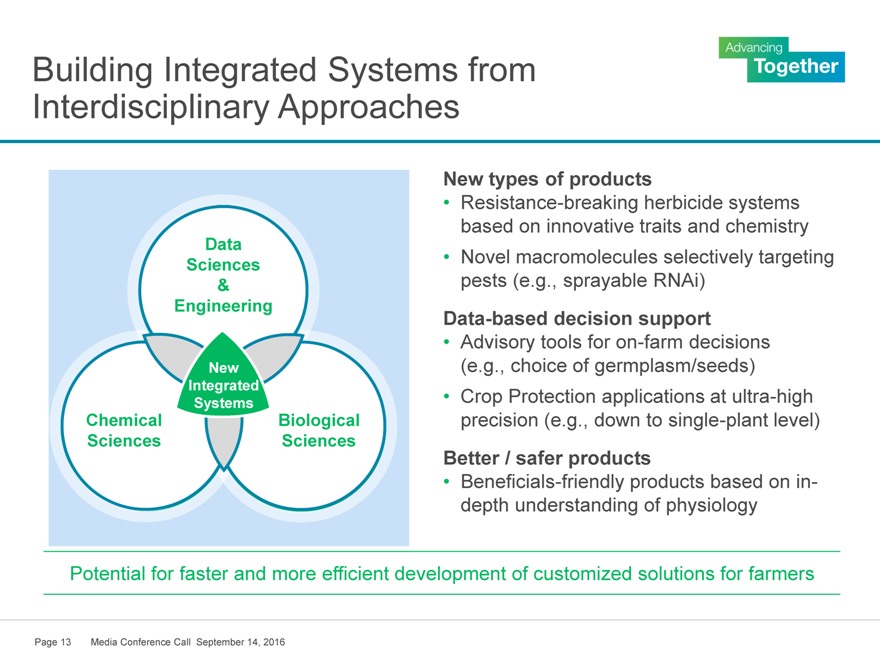

Building Integrated Systems from

Interdisciplinary Approaches

New types of products

Resistance-breaking herbicide systems Data based on innovative traits and chemistry

Sciences Data

Sciences Novel macromolecules selectively targeting

& Engi eering

& pests (e.g., sprayable RNAi)

Ag equipment and data processing/evaluation Engineering

Data-based decision support

Robotics &

Drones Advisory tools for on-farm decisions

Sensor (e.g., choice of germplasm/seeds)

New

Technology

Integrated Satellite

Systems Crop Protection applications at ultra-high

Chemical Technology Biological

Big Data Analytics precision (e.g., down to single-plant level)

Sciences Sciences

Better / safer products

Beneficials-friendly products based on in-depth understanding of physiology

Potential for faster and more efficient development of customized solutions for farmers

Page 13 Media Conference Call September 14, 2016

|

|

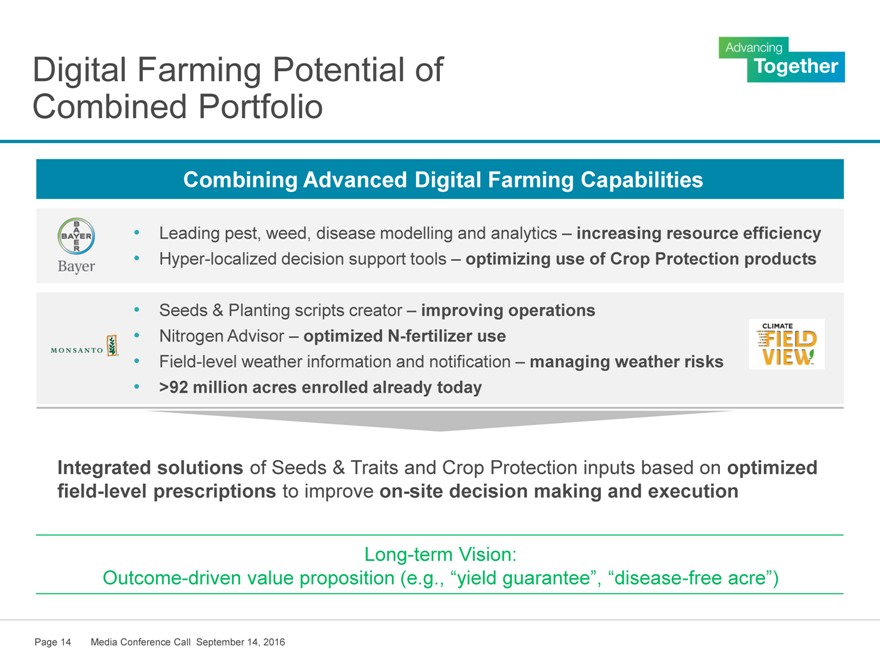

Digital Farming Potential of

Combined Portfolio

Combining Advanced Digital Farming Capabilities

Leading pest, weed, disease modelling and analytics – increasing resource efficiency

Hyper-localized decision support tools – optimizing use of Crop Protection products

Seeds & Planting scripts creator – improving operations

Nitrogen Advisor – optimized N-fertilizer use

Field-level weather information and notification – managing weather risks

>92 million acres enrolled already today

Integrated solutions of Seeds & Traits and Crop Protection inputs based on optimized field-level prescriptions to improve on-site decision making and execution

Long-term Vision:

Outcome-driven value proposition (e.g., “yield guarantee”, “disease-free acre”)

Page 14 Media Conference Call September 14, 2016

|

|

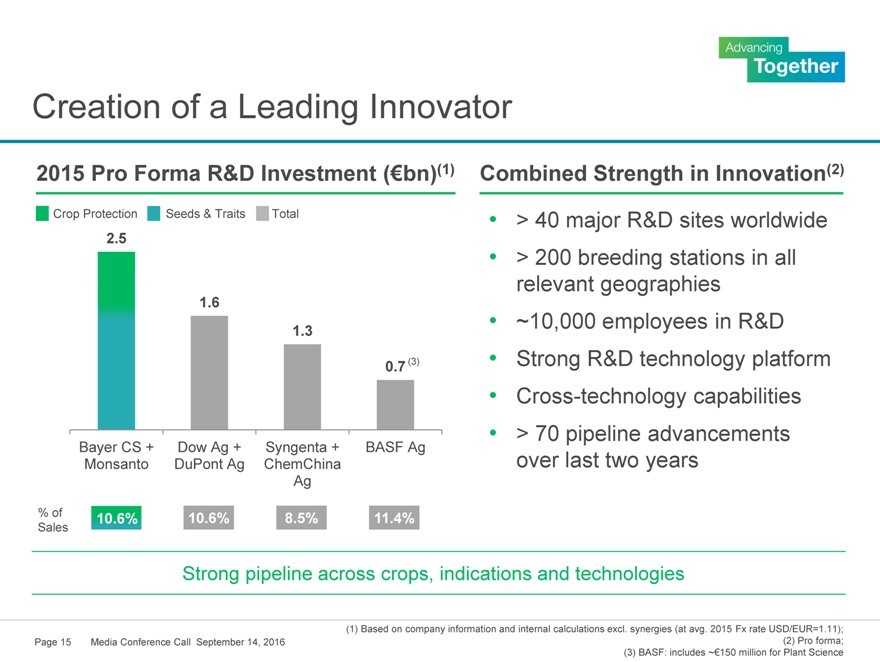

Creation of a Leading Innovator

2015 Pro Forma R&D Investment (€bn)(1) Combined Strength in Innovation(2)

Crop Protection Seeds & Traits Total > 40 major R&D sites worldwide

2.5

> 200 breeding stations in all

relevant geographies

1.6

1.3 ~10,000 employees in R&D

0.7 (3) Strong R&D technology platform

Cross-technology capabilities

> 70 pipeline advancements

Bayer CS + Dow Ag + Syngenta +BASF Ag

Monsanto DuPont Ag ChemChinaover last two years

Ag

% of 10.6% 10.6%8.5%11.4%

Sales

Strong pipeline across crops, indications and technologies

(1) Based on company information and internal calculations excl. synergies (at avg. 2015 Fx rate USD/EUR=1.11);

Page 15 Media Conference Call September 14, 2016 (2) Pro forma;

(3) BASF: includes ~€150 million for Plant Science

|

|

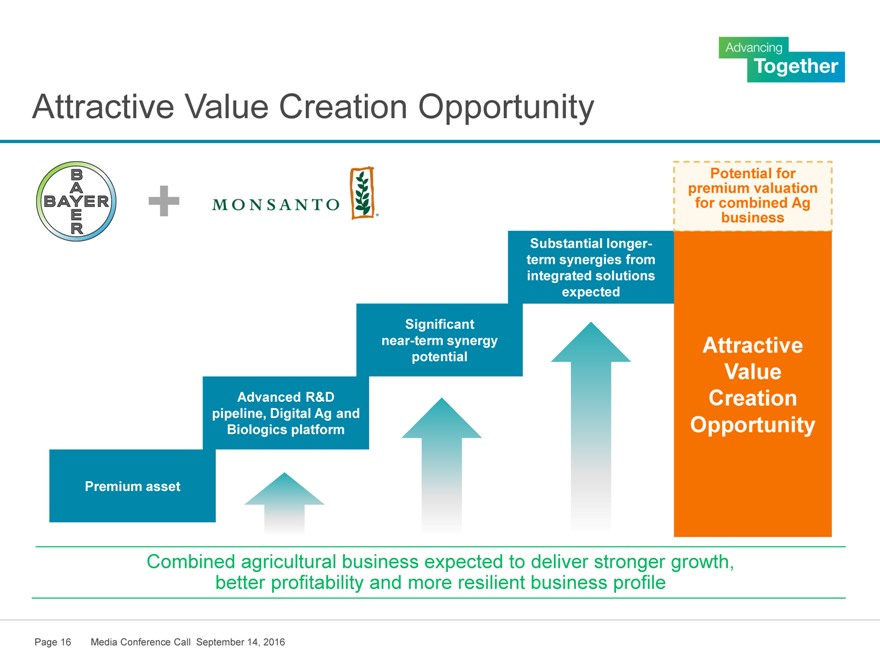

Attractive Value Creation Opportunity

Potential for premium valuation for combined Ag + business

Substantial longer-term synergies from integrated solutions expected

Significant near-term synergy Attractive potential

Value

Advanced R&D Creation pipeline, Digital Ag and Biologics platform Opportunity

Premium asset

Combined agricultural business expected to deliver stronger growth, better profitability and more resilient business profile

Page 16 Media Conference Call September 14, 2016

|

|

A Compelling Transaction for Shareholders

Creating a global leader in agriculture and an innovation engine for the next generation of farming

Convincing strategic logic of combining leading Seeds & Traits, Crop Protection including Biologics, and Digital Farming platforms

Compelling case for value creation through substantial synergy potential and potential premium valuation of combined agricultural business

Expected benefits from improved profitability, earnings accretion and enhanced earnings growth

Bayer expects the transaction to be highly value accretive

Page 17 Media Conference Call September 14, 2016

Bayer and Monsanto

Merger Press

Conference

Wednesday, 14th September 2016

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

Bayer and Monsanto Merger Press Conference

Michael Preuss

Head of Communications, Bayer

Introduction

Thank you very much ladies and gentlemen and good morning from Europe. Welcome to today’s conference call. You have seen that Bayer Monsanto have announced to create a global leader in Agriculture. And with me here on the call are Werner Baumann, the CEO of Bayer, Liam Condon, member of the Board of Management and the head of the Crop Science Division, Johannes Dietsch, CFO of Bayer and Hugh Grant, CEO of Monsanto. Before we start, I would like to draw your attention to the forward-looking statement and additional legal information which is available at the beginning of the presentation.

It should be read in conjunction with this presentation. We really appreciate that you could join us on such short notice and we ask for your understanding that we will close the call after an hour and limit the Q&A session to two questions per person. This presentation will also be made available after the call. And with that, I would like to now hand over to Werner Baumann.

Introduction

Werner Baumann

CEO, Bayer

Thank you Michael. And ladies and gentlemen, good morning and thanks for joining our conference call. We are welcoming you today from the US to pay tribute to an extraordinary event. I am delighted to announce that earlier this morning we signed a merger agreement with Monsanto, one of America’s iconic companies, to combine with Bayer. And I am extending my utmost respect and a very personal welcome to Hugh Grant, who is with us here today. He has kindly agreed to travel with Liam and myself to St. Louis later today to introduce us to his team there which means a lot to us. Hugh and his team have built Monsanto into a really outstanding business.

Since our first announcement on 23rd May, the process that led us to today has been a great testament to the vision and mutual respect of all involved, but especially down to Hugh, that we are now announcing such an agreement together, paving the way for a successful combination of our two great organisations. Before I take you through the highlights of our agreement I would like to hand over to Hugh. Hugh please?

2

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

Introduction

Hugh Grant

CEO, Monsanto

Thank you Werner and good morning to everybody on the line. As Werner said this is a momentous development for Monsanto and for our stakeholders. We have long discussed the value of an enhanced agriculture portfolio, and we are confident that this combination with Bayer will create a leader in agriculture that will accelerate our goals as an innovator in the sector. Our Board of Directors underwent a comprehensive evaluation process alongside legal and financial advisors to identify the most compelling value for our shareholders. We assessed a broad range of strategic options and opportunities, including a standalone path.

Ultimately, the Board unanimously determined that a combination with Bayer represents the most compelling value for our shareholders, employees and critically, the growers and customers that have come to rely on us so much. I, and the rest of our Monsanto Executive Team and our Board of Directors, believe that this combination with Bayer secures our vision to provide growers with the sustainable solutions necessary to meet the agricultural demands of today and tomorrow. We are now entering a new era in agriculture, one in which growers are calling for new solutions and technologies to meet the challenges of the future. Bayer shares in our vision of sustainable agriculture and improving the lives of growers and people around the world.

And together with Bayer, we will deliver on that vision. We will increase innovation across the agriculture industry through enhanced research and development, driving a faster discovery rate and delivering a wider set of enhanced solutions to growers across the globe. So before I turn things back over to Werner this morning, I would like to take a moment to thank all Monsanto employees for their outstanding contributions to our organisation. It is our people who have made this business great, and it is through their dedication, their discipline and their professionalism that we have the opportunity to grow as part of an organisation that shares our values, our passion for innovation, and our commitment to growers and customers around the globe so thank you very much to all of you, and with that I will hand it back to Werner?

Looking ahead

Werner Baumann

CEO, Bayer

So thank you Hugh. As mentioned earlier, this combination is going to create a global leader in agriculture and realise the shared vision of an enhanced agriculture offering that is ultimately going to deliver earlier access to better solutions for growers, so that they can help contribute to closing the gap between supply and demand that is unfolding with an ever growing population in the world. It will also create an innovation engine for the next generation of farming, bringing together two of the most innovative and strongest organisations that have been in the forefront of their respective areas of expertise for a long period of time.

3

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

All together, this will create significant synergy potential. It will also reinforce Bayer as a true leader and an innovation-driven Life Sciences Company in its fields of activity and now, of course, particularly with a significantly strengthened position in crop science. Our joint organisation will further evolve a strong culture of innovation, sustainability and social responsibility. Bayer is a very respected company with a very, very strong tradition in sustainability and responsibility, and is going to be a good host and a good home for a combined crop business that is going to thrive in the future.

Transaction summary

Now let me come to the transaction summary. This transaction is a compelling opportunity for shareholders of both companies. Following receipt of additional information and thorough analysis conducted during the due diligence process we have raised our initial offer and have agreed on an all-cash consideration of $128 per Monsanto share representing a premium of 44% to the Monsanto share price of $89.03 on May 9th, 2016. That is the day of our first proposal. The last 12 months EBITDA multiple is (18.6 times) 18.6x as of May 31st, 2016. And for a more normalised view, we provide the 2017 consensus EBITDA multiple of 16.5x (16.5 times) given the current trough situation of the markets. The transaction was unanimously approved by Monsanto’s Board of Directors as well as Bayer’s Board of Management and our Supervisory Boards.

In combining our two companies, we are well positioned to benefit from a cyclical upswing in the Ag market, and we expect to create substantial value for our shareholders. We have identified significant potential for sales and cost synergies which was confirmed during due diligence. We expect earnings contributions from annual net savings of approximately $1.5 billion after year three plus additional synergies from integrated solutions increasing over the years thereafter. The transaction is expected to be accretive to core EPS in the first full-year after closing, with double-digit percentage core EPS accretion in the third full-year after closing. We expect to earn our cost of capital on this transaction after year four.

As we have previously said, we plan to finance the transaction with a combination of debt and equity. The expected equity component of approximately $19 billion is expected to be raised through issuance of mandatory convertible bonds and through a rights issue with subscription rights. Bridge financing for $57 billion is ready and co-underwritten by five banks. We are targeting an investment grade rating post-closing and remain fully committed to the single “A” credit rating category in the long term.

A Combined Company

Looking ahead to our future as a combined company, we plan for the global Seeds and Traits and also the North American commercial headquarters to be in St. Louis, Missouri, the global Crop Protection and overall Crop Science headquarters in Monheim, Germany, and an important presence in Durham, North Carolina, as well as many other locations throughout the US, and around the world. Digital Farming for the combined business would be based in San Francisco, California. We will work closely with regulators to ensure a successful close. To underline our confidence in the outcome of the regulatory process, we have committed a reverse break-up fee of $2 billion and have made substantial commitments, including divestiture commitments, if required by the regulatory authorities.

4

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

We will submit merger control and other regulatory filings and are confident that we will obtain the necessary regulatory approvals. Monsanto plans to convene a shareholder meeting in late 2016 or early 2017 to vote on the merger agreement and closing of the transaction is expected by the end of 2017. The acquisition of Monsanto is driven by our strong belief that this combination is a powerful response to the enormous challenges facing farmers and the Ag industry overall. By 2050, the world’s population is expected to grow by an additional 3 billion people – this represents about six times the population of Europe today.

Growing Food Market

Land per capita available to grow food, however, is expected to decline by around 17% during the same period. A significant increase in food production of 60% is required to feed the planet. Innovative solutions are a prerequisite to close the gap between food requirement and production level. The combination with Monsanto represents the kind of revolutionary approach to agriculture that will be necessary to sustainably feed the world, as we enable growers with a broad set of enhanced agricultural solutions.

The combination of Bayer’s Crop Science business with Monsanto creates significant strategic benefits. We will have a broad portfolio across indications and crops with enhanced customer access supporting further growth potential due to the complementarity of the products. We are creating a company that can offer integrated solutions, from seeds and traits to crop protection to digital agriculture that helps farmers manage the increasing global food demand. Immediately, we will benefit from our ability to offer a broader variety of Seeds and Traits and Crop Protection products, and from the smart combination and usage of products based on agronomic advice. Furthermore, we would create a leading digital platform in Digital Farming.

In bringing together these two businesses, we will create a leading innovator with a strong R&D technology platform and a broad pipeline across Seeds and Traits, Crop Protection including Biologicals. The combined businesses’ innovation potential will be extraordinary, and in turn could support farmers around the world to close the productivity gap in agriculture. Both businesses are highly complementary regarding segments and geographies. And with that I would like to hand over to Liam Condon.

Merger Highlights

Liam Condon

Member of the Board of Management, Bayer

Thank you Werner. Together, Bayer and Monsanto will have the capabilities and resources to offer farmers truly integrated solutions by combining three areas of expertise: Seeds & Traits, Crop Protection including Biologics, and Digital Farming. Our strong technology offerings will enable farmers to receive the solutions they need, and advice on when and how to apply them. The combination of our two organisations allows us to bring a wide range of benefits directly to farmers, in both the short and long term.

Short Term plans

In the short term, we will have the ability to offer farmers a broader variety of seeds and crop protection products, and by using Bayer and Monsanto’s sales forces and infrastructure, we

5

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

can reach farmers in more places with more products and services. Mid to long term, the combined company plans to provide growers with integrated solutions based on the smart combination and optimised usage of products, agronomic advice and digital agriculture solutions. In the future, we plan to develop integrated systems based on technologies optimally designed to work together. These all result in significant and lasting benefits for farmers: from improved sourcing and increased convenience in the short term, to improved yield with optimised inputs in the mid to long term. And importantly, they support farming in a more efficient and sustainable manner. The combined offering is expected to enable us to address farmers’ needs across crops and indications even more comprehensively than today. This slide shows a soybean plant lifecycle in Brazil. This example demonstrates that together with Monsanto, we will be able to offer dedicated products for each step along the lifecycle of a soybean plant.

The set of innovative technologies combined with season-long advice will help farmers to optimise inputs with a corresponding improvement in yields. The benefits of a comprehensive portfolio are not just theoretical. We already have a blueprint for how our combined and complementary product portfolio of solutions will be advantageous for farmers. Take Canola as an example, with a wider range of products, we can offer farmers innovative solutions throughout the crop cycle. High quality seed varieties provide access to the farmer, whose various needs are then addressed through a complete crop protection and services portfolio for seed treatment and weed, pest and disease control.

Long-term plans

We see significant growth potential for this concept across the combined Bayer Monsanto portfolio. The combined technologies of Bayer and Monsanto will enhance our ability to provide farmers with integrated solutions for commercially important crops like corn and soy. These broad-acre crops account for about 40% of the global agriculture business. With strong positions across all relevant technologies, Bayer and Monsanto combined will be well positioned to provide farmers with integrated solutions they need, now and into the future.

Through an interdisciplinary approach, we are convinced that we will be able to develop more innovative and sustainable solutions based on an integrated systems approach across our chemistry, biological and data science technology platforms. This approach will have significant benefits for farmers by leading not only to more, but also to faster innovation, for example by taking a parallel instead of sequential approach to development. As a concrete example, based on such an integrated approach, new resistance breaking herbicide tolerance systems may become available that are based on optimal parallel development of traits, herbicide chemistry, and high quality germplasm, all of which are available within our soon-to-be combined organisation.

The combination of Monsanto and Bayer in Digital Farming has the potential to bring this transformation to life. For instance, at Bayer we are using satellite imagery to detect disease patterns at a very early stage and give more tailored recommendations so that farmers can spray the right part of the field early on, and not the entire field too late. Amongst other things, Monsanto helps farmers optimise their daily decision making with field level weather information so that farmers can make field management decisions with confidence.

6

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

Our longer term vision is an outcome-driven value proposition. We are not simply selling farmers’ seeds, traits and crop protection products, but optimised field level prescriptions to improve on-site decision making and execution. In the future, we should be able to offer outcomes based solutions, for example a disease, weed-free acre or maybe even a yield guarantee to give some examples. Both companies are built upon a commitment to and belief in the importance of innovation and sustainability that not only allows us to succeed in our field, but also enables us to help solve some of the world’s most pressing issues in agriculture through our combined complementary skills in research and development.

We at Bayer have a leading position and expertise in crop protection research and development while Monsanto is a leader in seeds and traits. So jointly, we will have significant capabilities with around 10,000 employees in research and development and a strong technology platform. Our combined pro forma research and development investment will amount to around €2.5 billion. The combined R&D pipeline is expected to enable us to better serve growers, our customers and address their challenges and needs with tailor-made solutions across crops, indications and technologies. With that I would like to hand back to Werner.

Conclusion

Werner Baumann

CEO, Bayer

Thank you Liam. The combination of Bayer and Monsanto represents an attractive value creation opportunity. The combined Ag business is a premium asset which has the potential to command a premium valuation. Together, we will draw on the collective expertise of both companies to build a leading agricultural player with advanced innovation and R&D capabilities, to the benefit of farmers. We expect significant near term synergy potential and in addition substantial longer term synergies from integrated solutions. As a result, we expect stronger growth, better profitability and a more resilient business profile going forward.

Both Monsanto and we at Bayer are absolutely convinced that the combination of two complementary businesses has a compelling logic and creates value in a major way. It is a synergistic case which has the potential to achieve a premium valuation based on improved profitability, strong earnings accretion and enhanced earnings growth. Overall, we believe this is a highly value accretive transaction which benefits not only the shareholders, but also our customers, our employees and all stakeholders involved. That concludes my remarks. Thank you for your time. And we would be happy to take your questions.

Q&A

Patricia Weiss (Reuters): Hello everybody. I have two questions. The first question would be whether there will be any impact on the Leverkusen site due to the deal? And the other one is what makes you so optimistic about the integrated business model as we actually hear from many farmers unions that they are not so happy about it and they want to choose where to buy what? Thank you very much.

7

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

Werner Baumann: Thanks Patricia for your questions. First, it is way too early to talk about individual sites and impact on individual sites. However, I would say that there is no presence, no operational presence of our crop science business in Leverkusen. Our crop science business is headquartered in Monheim, which is global headquarters. We have, I think, very clearly communicated where the different pieces of the combined organisation are going to be headquartered based on the expertise we have there and that is what this combination is all about as it being driven by growth and innovation. And everything else when it comes to the details of how we best combine the talent and the expertise remains to be developed over the next months to come. The reason for our optimism is, before I hand it over to both Hugh and Liam, simply driven by the fact that when we talk about integrated offering, it does not have anything to do with bundling here which can be done by anybody nor is it our plan or our ambition or intent to prevent farmers from having choice. What we want to do is we want to develop actual better solutions that are optimally adjusted to each other with the different components in order to help farmers drive better outcomes which means higher yields in a more sustainable and environmentally friendly way. And that is what is one of the challenges that modern agriculture faces and we believe that the need to address these issues is growing over time and hence our optimism.

Hugh Grant: Yeah Patricia, I would just add very – it is Hugh Grant here. I would just add to your question on why are you so certain. We have been working on this for the last three or four years. The reception has been phenomenally successful with growers. And my experience around the world is you cannot make a grower do anything that he or she does not want to do. So this needs to be an incremental value and my experience is farmers are starving for innovation. They are looking for the edge that brings them that next kilogram, that next bushel of grain. So to use your words they will absolutely choose where they buy what. That is the nature of the farming. But I think the combined company of Bayer and Monsanto provides better insight that in turn makes the decision making but it is the old story if you are a little bit smarter you are going to make slightly better decisions and that is their appetite today.

Liam Condon: And I would just add what we really want to do with the integrated business model is increase yields, minimise the inputs, optimise use of natural resources, and improve the sustainability footprint. And if we do all this in the right manner it should be leading to a better return on investment for our growers as well. And then it is up to the grower of course to decide which system or which product portfolio they would like to use and their own experience has been in the models where we do have an integrated approach for example, in Canola today, and this is a highly compelling offer for growers. And there is enough competition and other portfolios and systems out there. But the one that offers the most compelling benefits and a better return on investment for farmers should lead to an advantage that we feel is very compelling.

Jack Kaskey (Bloomberg News): Yeah hi. I have a couple questions on Antitrust. First up, what countries are you going to seek antitrust approval from? And secondly, Hugh, you mentioned that the overlaps between your companies are obvious. I was hoping maybe you could go over some of those obvious overlaps - cotton seed seems to be one area, maybe you could confirm?

8

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

Werner Baumann: So on your first question Jack, there are about 30 jurisdictions we need to file with for merger control purposes. Of course, we have very large ones that are the US or Canada or Brazil and also the European Union. And then it goes down to a whole bunch of additional countries we are requested to file. The second question is the overlap question. It is so obvious that you do not even have to comment on it.

Jack Kaskey (Bloomberg News): Will be great if you could.

Werner Baumann: Yeah, but I guess there is a lot of literature out there that comments on what it could be and in some areas is actually fairly consistent with what we have to say. Also with our own assessment, I have to ask you for your understanding that we do not want to preempt a regulatory discussion. We have of course our own assessment, but it is up to the regulatory authorities to tell us what it is that we need to do and not us kind of signalling what we want them to tell us what we should do. So that is the simple truth to the story.

Hugh Grant: Jack, it is Hugh here. The only thing that I would add to Werner’s comments is the unique aspect for this deal is that the overlaps are minimal. And when you look at it from that perspective Monsanto was a seed biotech emerging data science business. Bayer is pre-eminent in chemistry and has an excellent pipeline in chemistry. So when you sketch that on a piece of paper the overlaps are really very small, and as we looked at the deal that was a lot of encouragement compared to other transactions that we considered.

Liam Condon: Also the geographic footprint is very complementary.

Jack Kaskey (Bloomberg News): Thank you.

Operator: And the next question comes from Diane Bartz from Reuters.

Diane Bartz (Reuters): Hi there. The first question I have is the person who said the unique aspects to this deal is that the overlaps are minimal. Who can put a name on that?

Hugh Grant: I am sorry I should have identified myself. That was me Hugh Grant from Monsanto.

Diane Bartz (Reuters): Hugh Grant okay sorry.

Hugh Grant: No, no it’s okay. We have a shared view on that. That was an important element in our conversations. I mean that was one of the discussions that were very intense and that we do have very much aligned view.

Diane Bartz (Reuters): So for example, I know that Bayer bought some assets when Monsanto bought seed. I guess it was in 2008 bought the Delta & Pine Land. How are you going to handle that? My understanding, my imperfect understanding is that that looks like something that would obviously have to be divested because I don’t think it is even legal for you guys to repurchase them is it?

Werner Baumann: Thanks a lot Diane for the question. This is clearly one of the topics that we would be taking up with regulators. And it is an area where ultimately the regulator is going to have to take their decision and they will look. Every regulator will look in their own markets at relevant market shares of specific companies and specific portfolios. And again we do not want to preempt that discussion. So we would basically leave it at that - that the overall overlap is minimal. But for sure there is some overlap and that will be identified by the regulators and then we will follow their decisions.

9

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

Diane Bartz (Reuters): Okay can you detail what the synergies are going to come from?

Johannes Dietsch: Yes of course. Well we have –

Diane Bartz (Reuters): And I am sorry who is speaking?

Johannes Dietsch: This is Johannes Dietsch speaking, CFO of Bayer. We have given a very specific number on synergy target after year three in the amount of $1.5 billion for the combination. And here we see the majority in cost synergies, 1.2 billion out of which 70% roughly lays with SG&A, which are sales and general and administrative cost. And here we will take a view on infrastructure but also on overlaps in administration as well as sales and marketing to reduce the cost base. And with the top line synergies we have given initially an EBITDA impact of 300 million for the year 2021 and we see significant additional synergies from the top line coming there after from the integrated offering. Does it answer your question?

Diane Bartz (Reuters): Yeah that helps a lot. Thank you. And last question is obviously, it is going to be a new administration in the United States. Is that a consideration in your antitrust on review?

Hugh Grant: The way I always look at this is regardless of where you are in the world or the political forces there the reality is there is one spring and there is one harvest. And you are either on time for that spring or you wait a year for the next one. So as we are looking at the combination from a Monsanto perspective we have been much more focused on the innovation horizon rather than the political horizon. And the opportunity from an innovation point of view on bringing to Liam’s point and bringing these two portfolios together where there is minimal overlap is that the opportunity to bring technology to the market faster, more efficiently and in a more meaningful way. And I think regardless of the political community that is a compelling conversation for grower customers.

Michael Preuss: Okay thank you. Then the next question please.

Brian Schwartz (FOX Business): Hi there. I was wondering moving forward is Bayer worried about the regulators and specifically what are you guys worried about moving forward if you have any worries at all after making this deal?

Werner Baumann: The regulatory questions are important and they have been a very, very important topic during our negotiations and contract discussions so that is an area that needed thorough analysis. We had concluded jointly but also independently supported by the Antirust council and our assessment. With that I can only echo what Hugh said, due to the high complementarity of the businesses from a product portfolio, but also from a regional perspective, we do have a very high level of comfort and we see that this whole regulatory process can be concluded before the end of 2017. And that is what we have communicated.

There is a second piece to it which is somewhat unique to the US, particularly in the context of the ChemChina Syngenta acquisition, which was cleared so it got CFIUS support from a national security perspective. We will proactively and voluntarily file for CFIUS review and a) we want to make sure that we can check the box that we do not have any unknown or uncertainty there. And this review goes fairly quick. And b) we also believe that as a western

10

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

privately or private capital market listed company, with more than 150 years’ history as a good corporate citizen in the US and more than 12,000 people that work for us in the US, that this will not be an impediment.

Brian Schwartz (FOX Business): You see that this deal can be included by the end of 2017. There have been other deals that have said similar things and they even post-postponed due to regulators so you are pretty confident you are not going to have any issues with regulators to get this deal done by 2017?

Hugh Grant: This is Hugh Grant here. With the analysis we have done with our main advisors and all the work that we have done we feel confident that we can conclude this transaction in that timeframe. And Werner said that was a meaningful part of the discussions between our two teams. It is one thing to be confident, another thing where you are based out on data and the analysis that we have run looks as we referenced earlier in this conversation on the minimal amount of overlap between the two companies. But for the next 12-15 months that is going to be the focus, getting us over the line.

Michael Preuss: Next question?

Jacob Barker (St. Louis Post-Dispatch Newspaper): Good morning. I am curious what will happen to the Monsanto name?

Hugh Grant: Jacob, thank you. Thanks for calling in. We have not discussed that specifically, but we have said in the past as we look to previous transactions that is something that we would be flexible on. The conversation is focused much more on innovation, much more on future products, and how you can accelerate that. And in the comments that we made earlier today we have committed or Bayer has committed. We have discussed that and St. Louis continues to be the global centre for our seed and biotech innovation worldwide and the commercial hub for North America, so I think for us, this is really good news.

Jacob Barker (St. Louis Post-Dispatch Newspaper): Quick follow up, earlier I think Werner mentioned combined R&D spend is anticipated to be about €2.5 billion. Looking at the last year’s spend, that seems like a pretty significant increase in R&D expenditures?

Liam Condon: I think the 2.5 is just the addition of the 2015 pro forma on R&D numbers. So there is no indication going forward what the actual number would be. This is the simple addition, but what we can say is we are very clearly committed to continuing to invest very heavily in innovation and we see this as the growth driver for the future. And the details of that we will be working out during the integration process.

Jacob Barker (St. Louis Post-Dispatch Newspaper): Okay so that 2.5 billion is the entire company not just crop science R&D?

Liam Condon: No this is crop science R&D plus Monsanto R&D added together pro forma 2015 numbers so not the rest of Bayer R&D. So it is a very, very sizable number and it has increased this year over last year.

Werner Baumann: Jacob, the way I would think of it - this is to Liam’s point, when you look at the sizable challenges that agriculture faces and you look at what needs to be done in agriculture, our perspective with Monsanto has been for a number of years that resources continue to need that - you need to continue to invest on a rising plane to crack the code on future challenges. So the combination of the two companies really brings a new level of

11

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

intensity and unlocks another level of creativity both in terms of whether its dollars or euros. It’s thousands of scientists working on common problems to try and crack the code on the challenges that agriculture faces.

Michael Preuss: Okay next question.

Unidentified Journalist: Hello everybody. I have two more questions concerning the synergies. You have mentioned that you will realise additional synergies. Can you tell me something about the amount and the way to achieve this aim and do you plan to cut jobs to reach this aim, especially in Germany?

Werner Baumann: Thank you for your question. The additional synergies that were mentioned is something that both Mr. Dietsch and Liam Condon can shed some light on. We have been specific on the cost synergies piece and also on the increments in the 1.5 billion of early sale synergies and the rest as we have been talking about all along of the value proposition. This is going to drive synergistic contributions beyond what each of the companies can do on their own and is driven by innovation and growth. That means by default, this is going to be sales and it does not come from cutting infrastructure. I know you want to take an additional step.

Johannes Dietsch: To develop a synergies of course we have 1.5 billion start off for the year 2021. We see significant additional value of generation from top line synergies from the integrated offer there. Thereafter we have not given specific guidance on the amount and timing of that, but it is clear that we will see additional sales growth going forward with the combination of Monsanto and Bayer Crop Science.

Jacob Bunge (Wall Street Journal): Hi thanks and good morning. Mr. Baumann, you talked in past months about the potential to manage the image that crop biotechnology has in a different way than Monsanto has. And I would like to get your current thinking on and ask you the question that Mr. Bartz responded to earlier as to what you see the future of the Monsanto company name?

Werner Baumann: Yeah thanks Jacob for the question. I think first and foremost what is important is that these are two really great companies that have winning cultures and have been very, very successful in their fields. And that is what we want that common combination to thrive on. And I am talking a little bit with the perspective of the huge respect we have for Monsanto and what Monsanto has done. And I think also that it has taken some thought on what you refer to as what the reputational challenges are going forward. If you establish as a young innovation-driven company, a completely new business model, you have to actually fight for acceptance.

And that is not to everybody’s pleasing. And if you do this there is always a risk that some of these battles stick with you, even though they might be very small and actually exceptions rather than the norm. That is for good and bad what reputation is about and it is not necessarily anything that has to do with business practices, which we actually firmly believe in both companies, have and work with to the highest standards. You also have to ask yourself the question why so many growers. Why for Monsanto as the leading company because they do that voluntarily. Yeah they are not forced to buy from Monsanto because this is a company that provides the best solutions compared to their competitors, and with that provides incremental value to them as customers.

12

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

Now having said that, as in many other areas we will have to discuss and look at where we can create three out of one plus one. And where the assets, be it products, be it IP, be it other intangibles that both parties bring to the table, can be put to work in the best interest and with the best potential for the combined organisation going forward. As far as reputation is concerned there is, you know there is good and let us say not so good reputation depending on the markets and what the markets’ positions were relative to certain issues, so it is actually not very helpful to generalise. But I can tell you that we will jointly look at what the right course of action is going forwards. We have not done this so far because we are at the beginning of a process with today’s announcement and not at the end, but rest assured that we will pay utmost attention to that question.

Johannes Dietsch: Also a question related to material that refers to the divestment level in pro forma sales in both companies that’s been around 1.6 billion. The idea here is that if more than 1.6 billion worth of annual sales needs to be divested as a result of antitrust, can we hold off or what would happen on that case?

Werner Baumann: So we have some contractual provisions which we will not get into the details that define a certain level of divestitures that would be looked at for the deal to close in terms of closing conditions. And that is very much to be seen as a commitment, a contractual commitment to provide for the comfort to you and Monsanto’s board in terms of our commitment. And I think that today we can say our joint commitment to drive this transaction to a successful close and actually bring it over the finish line and that is where I would leave it.

Michael Preuss: Okay do we have a next question then?

Madhvi Sally (The Economic Times India): Hi this is Madhvi Sally from India from The Economic Times. My question was about how do you see the Indian market, do you think it will remain challenging for the combined entity? And my second question would be about what it actually means for the farmers? Will it be an eventful situation for them or as the industry says that it could be some sort of exploitation could happen or there could be monopolisation?

Hugh Grant: This is Hugh Grant here from Monsanto.

Madhvi Sally (The Economic Times India): Hi.

Hugh Grant: Hi good afternoon, good evening.

Madhvi Sally (The Economic Times India): Good evening.

Hugh Grant: I spent many years in India. And if I look at the progress of farming in India over that time it has been exceptional. And if I look at India’s position in cotton and rice production and in the future I think in maize, there is tremendous opportunity. When you talk to those small holders in India the fascinating thing is they are conversant with modern technology and they are hungry for the next generation of technology. So you cannot make farmers do anything they do not want to do, but by presenting them with broader choices and given them more information on their iPhones and more information that relates to their village. You unlock opportunity for those growers. So I am optimistic.

Werner Baumann: Yeah I would chime in there. Thanks a lot for the question. We actually had a media event last week in Monheim and we were also talking a little bit about the

13

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

importance of India today. It is already a hugely important market for Bayer Crop Science as well as for Monsanto. And we spoke a lot about the opportunities for small holders and in particular with the advent of digitalisation mobile technology. How we can contribute to an increase in productivity on the one side but also on sustainability on the other. And this is something where I think when we combine forces we can do a lot more good for Indian farmers and we are looking forward to that.

Madhvi Sally (The Economic Times India): Okay. One last question would be Monsanto is already seeing a challenging market, you know they have in the past few months witnessed frequent flares up with the Indian government, with the latest being Monsanto threatening that they will not introduce their latest chain of genetically modified cotton or re-evaluating the business in India. How do you plan to handle this situation?

Hugh Grant: It is hard to comment on specifics. Here is how I would look at it. For Monsanto, for the new Bayer Monsanto combination, the expectation is that you have a level playing field. And the expectation would be that as you invest in R&D and you unlock the next level of innovation that there are some mechanisms there that you get paid for. And I think growers, my experience worldwide, not just in India. If you can provide incremental yield that improves the conditions for their family or improves exports for the country then it is a reasonable assumption that you should be paid for that innovation. And that is the conversation that I hope to see progressing in India over time.

Michael Preuss: Thanks. Now we have time for one last quick question.

Michael Calhoun (CBS Radio): The folks in St. Louis from past acquisitions are kind of weary when a deal like this is announced. So what kind of reassurance or what kind of plans are there for the St. Louis area specifically when it comes to Monsanto’s heavy involvement with innovation. You mentioned R&D innovation in startups and investing in incubators and accelerators and that sort of thing here. But generally what is the message to the folks in St. Louis?

Hugh Grant: While it does not sound like it, I am a St. Louiser and I have lived there for the last 20 years or so and raised my family there. So as we have discussed this deal that was a particularly important piece. I think two or three points to mention. Number one, St. Louis becomes the global centre for Seeds and Traits, R&D. So what we are doing in St. Louis today is amplified and it will be resourced even further. Number two, St. Louis becomes the commercial hub for North America which is still the most important market for this new company. So I think when you look at the Life Sciences hubs around St. Louis, when you look at the burgeoning entrepreneurial emergence in Life Sciences in St. Louis and you see other companies who have invested in agriculture and invested in science, I think this is good news for St. Louis. And I think between Bayer under Werner’s leadership and Monsanto when you compare the two companies there is a tremendous amount of shared vision and similarities in the culture, and I think that bodes well for St. Louis.

Werner Baumann: Yeah Michael I can only echo what Hugh said we have a heritage of good corporate citizenship. If you look at supporting and working with the communities we live in and we do business in. And this ranges from philanthropic work to supporting things that are closer to our business. I think there is a great example of how to do this and develop something that helps the city, the county and the business the way Monsanto has done this

14

| Bayer and Monsanto Merger Press Conference | Wednesday, 14th September 2016 | |

|

| ||

over the last one and a half to two plus decades. And I do not see any reason to actually question it, but much rather continue to build on it. Having said that, of course, we will engage and look at what we are going to do in supporting the communities in line with the business, the combined business that is now going to be built. But rest assured that we stand fully behind our commitment to the city and the county to the business and the people that work and live there. And that is I think in our mutual interest.

Michael Preuss: Okay then thank you, on behalf of everybody here in the room we would like to thank you for being with us today on the call and thanks for your question and have a nice day. Thank you very much. Bye.

Werner Baumann: Thank you all.

Hugh Grant: Thank you. Bye.

[END OF TRANSCRIPT]

15

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- On the Road Lending Announces Expansion into North Carolina

- Patto di stabilità: i deputati approvano le nuove regole di bilancio

- Reparation ska bli enklare och mer tilltalande för konsumenter

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!