Form 8-K SunCoke Energy, Inc. For: Jul 21

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of Earliest Event Reported): July 21, 2015

SUNCOKE ENERGY, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 001-35243 | 90-0640593 | ||

| (State of Incorporation) | (Commission File Number) |

(IRS Employer Identification No.) |

| 1011 Warrenville Road, Suite 600 Lisle, Illinois |

60532 | |

| (Address of principal executive offices) | (Zip code) |

Registrant’s telephone number, including area code: (630) 824-1000

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| Item 2.02. | Results of Operations and Financial Condition. |

On July 21, 2015, SunCoke Energy, Inc. (the “Company”) issued a press release announcing its financial results for the second quarter of 2015. A copy of this press release is attached as Exhibit 99.1 and is incorporated herein by reference.

| Item 7.01. | Regulation FD Disclosure. |

As noted above, on July 21, 2015, the Company issued a press release announcing its financial results for the second quarter of 2015. Additional information concerning the Company’s financial results for the second quarter of 2015 will be presented in a slide presentation to investors during a previously announced teleconference on July 21, 2015. A copy of the slide presentation is attached as Exhibit 99.2 and is incorporated herein by reference.

The information in this report, being furnished pursuant to Items 2.02, 7.01 and 9.01 of Form 8-K, shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that Section, and is not incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as expressly set forth by specific reference in such filing.

Safe Harbor Statement

Statements contained in the exhibit to this report that state the Company’s or management’s expectations or predictions of the future are forward-looking statements intended to be covered by the safe harbor provisions of the Securities Act of 1933 and the Securities Exchange Act of 1934. The Company’s actual results could differ materially from those projected in such forward-looking statements. Factors that could affect those results include those mentioned in the documents that the Company has filed with the Securities and Exchange Commission.

| Item 9.01 | Financial Statements and Exhibits. |

(d) Exhibits

| Exhibit |

Description | |

| 99.1 | SunCoke Energy, Inc. Press Release, announcing earnings (July 21, 2015). | |

| 99.2 | SunCoke Energy, Inc. Slide Presentation regarding earnings (July 21, 2015). | |

SIGNATURES

Pursuant to the requirements of the Exchange Act, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| SUNCOKE ENERGY, INC. | ||

| By: | /s/ Fay West | |

| Fay West | ||

| Senior Vice President and Chief Financial Officer | ||

Date: July 21, 2015

EXHIBIT INDEX

| Exhibit |

Exhibit | |

| 99.1 | SunCoke Energy, Inc. Press Release, announcing earnings (July 21, 2015). | |

| 99.2 | SunCoke Energy, Inc. Slide Presentation regarding earnings (July 21, 2015). | |

Exhibit 99.1

Investors:

Lisa Ciota: 630-824-1907

Media:

Steve Carlson: 630-824-1783

SUNCOKE ENERGY, INC. ANNOUNCES SECOND QUARTER 2015 RESULTS AND

REAFFIRMS FULL YEAR GUIDANCE

| • | Net loss attributable to SXC was $13.5 million, or $0.21 per share, reflecting non-cash pension termination charges of $10.9 million, net of tax, or $0.17 per share |

| • | Adjusted EBITDA, excluding the one-time, non-cash pension termination charges of $12.6 million, was $46.0 million. |

| • | Domestic Coke operations generated Adjusted EBITDA of $56.2 million and reflects the timing of planned maintenance outages |

| • | Significantly increased dividend, raising quarterly rate 100 percent to $0.15 per share |

| • | Entered into agreement to contribute additional 23 percent interest in Granite City to SunCoke Energy Partners, L.P. |

LISLE, Ill. (July 21, 2015) - SunCoke Energy, Inc. (NYSE: SXC) today reported a second quarter 2015 loss attributable to shareholders of $13.5 million, or $0.21 per share, reflecting pension termination charges of $0.17 per share and lower cost recovery at our Indiana Harbor facility. The second quarter 2014 net loss attributable to shareholders was $49.2 million, or $0.71 per share, including a Coal Mining impairment of $51.0 million, net of tax, or $0.74 per share.

“We delivered second quarter results in line with annual targets, which anticipated the impact of a non-cash pension charge and lower operating cost pass-through mechanism at Indiana Harbor,” said Fritz Henderson, Chairman and Chief Executive Officer of SunCoke Energy, Inc. “This puts us on track to achieve our 2015 consolidated Adjusted EBITDA guidance of $190 million to $210 million before considering the benefits anticipated from recent announcements by SunCoke Energy Partners.”

Henderson continued, “These announcements, including the expected acquisition of Convent Marine Terminal and the initiation of a unit repurchase program at SXCP, are expected to drive higher cash distributions to us as general partner and majority owner of the partnership. We remain committed to returning this incremental cash in line with our long-term strategy of returning 80 to 90 percent of our free cash flow to shareholders.”

SXC also announced it entered into a contribution agreement with SunCoke Energy Partners, L.P. (NYSE: SXCP) to contribute a 23 percent interest in the Granite City cokemaking operations for $67 million. This transaction is expected to close in the third quarter 2015, concurrently with the execution of long-term financing related to the Convent Marine Terminal acquisition.

1

In light of announcements made this morning by SXCP, we have issued our second quarter results two days early. We have also moved up our investor conference call to this morning at 10:00am ET. More information can be found below.

2

SECOND QUARTER CONSOLIDATED RESULTS

| Three Months Ended June 30, | ||||||||||||

| (Dollars in millions) |

2015 | 2014 | Increase/ (Decrease) |

|||||||||

| Revenues |

$ | 348.2 | $ | 372.2 | $ | (24.0 | ) | |||||

| Operating income (loss) |

6.4 | (71.4 | ) | 77.8 | ||||||||

| Adjusted EBITDA(1) |

33.4 | 60.8 | (27.4 | ) | ||||||||

| Net loss attributable to SXC |

(13.5 | ) | (49.2 | ) | 35.7 | |||||||

| (1) | See definition of Adjusted EBITDA and reconciliation elsewhere in this release. |

Revenues declined $24.0 million to $348.2 million in second quarter 2015 compared with the same prior year period, reflecting the pass-through of lower coal costs in our Domestic Coke segment on relatively flat sales volumes.

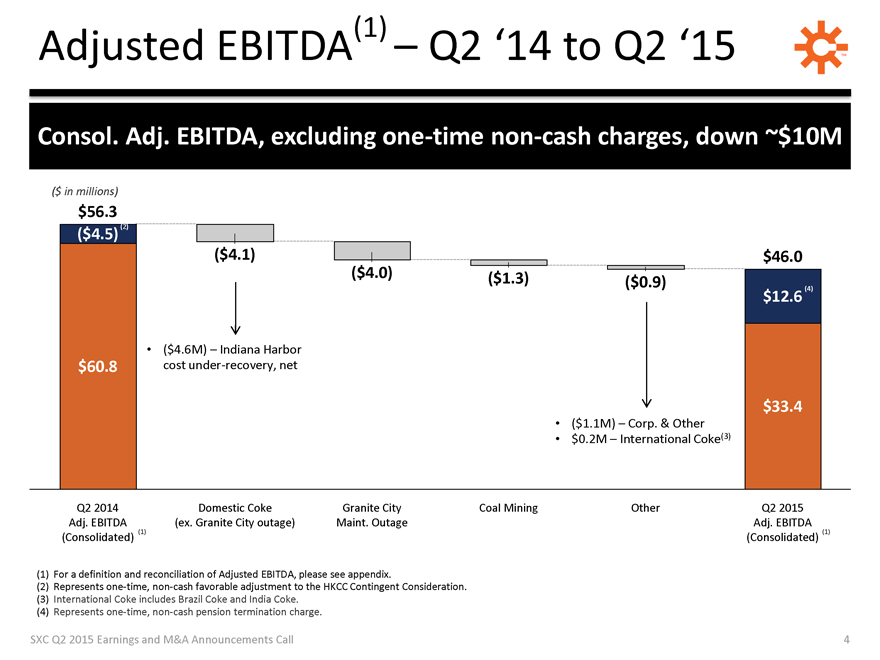

Operating income was $6.4 million in the current period and compares favorably to the prior year period, which included the Coal Mining impairment of $103.1 million. Adjusted EBITDA declined $27.4 million, primarily as a result of one-time, non-cash pension plan termination charges of $12.6 million and the absence of a one-time, non-cash gain of $4.5 million recorded in the prior year period. Adjusted EBITDA was further impacted by lower cost recovery at Indiana Harbor, net of lower spending, of $4.6 million and the timing of planned maintenance outages of approximately $4.0 million.

Net loss attributable to SXC was $13.5 million, or $0.21 per share, in second quarter 2015, reflecting the items described above, net of tax. Prior year net loss attributable to SXC was $49.2 million, or $0.71 per share, including a Coal Mining impairment of $51.0 million, net of tax, or $0.74 per share.

SECOND QUARTER SEGMENT RESULTS

Domestic Coke

Domestic Coke consists of cokemaking facilities and heat recovery operations at our Jewell, Indiana Harbor, Haverhill, Granite City and Middletown plants.

| Domestic Coke Results |

Three Months Ended June 30, | |||||||||||

| (in millions, except per ton amounts) |

2015 | 2014 | Increase/ (Decrease) |

|||||||||

| Revenues |

$ | 326.5 | $ | 344.5 | $ | (18.0 | ) | |||||

| Adjusted EBITDA(1) |

$ | 56.2 | $ | 64.3 | (8.1 | ) | ||||||

| Sales Volume (thousands of tons) |

1,110 | 1,059 | 51 | |||||||||

| Adjusted EBITDA per ton(1) |

$ | 50.63 | $ | 60.72 | $ | (10.09 | ) | |||||

| (1) | See definitions of Adjusted EBITDA and Adjusted EBITDA per Ton and reconciliation elsewhere in this release. |

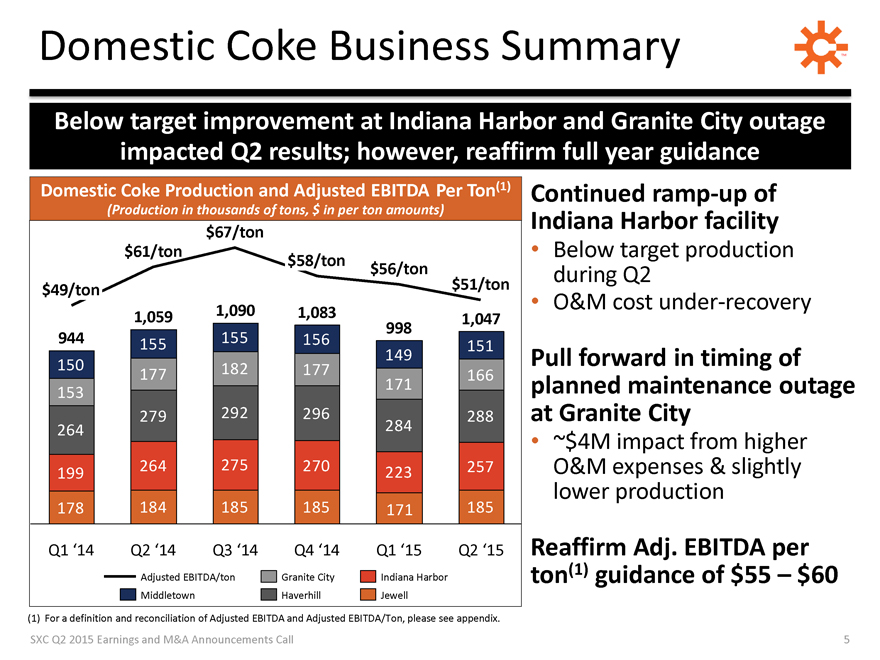

| • | Segment revenues were affected by the pass-through of lower coal price, partially offset by an increase in volume of 51 thousand tons. |

| • | Adjusted EBITDA was $56.2 million, down as a result of the change in Indiana Harbor’s cost recovery mechanism in 2015 from an annually negotiated budget amount with a cap for certain expenses to a fixed recovery per ton as well as the impact of the timing of planned maintenance outages. Second quarter 2015 was also impacted by lost revenues and higher expenses associated with the previously announced planned shutdown of Haverhill Chemicals LLC, which were in line with management’s expectations. |

3

Coal Logistics

Coal Logistics consists of the coal handling and blending services operated by SXCP at Lake Terminal in East Chicago, IN, and Kanawha River Terminals, LLC (KRT), which has terminals along the Ohio, Big Sandy, and Kanawha rivers in West Virginia and Kentucky.

| Coal Logistics Results |

Three Months Ended June 30, | |||||||||||

| (in millions, except per ton amounts) |

2015 | 2014 | Increase/ (Decrease) |

|||||||||

| Revenues |

$ | 8.6 | $ | 10.7 | $ | (2.1 | ) | |||||

| Adjusted EBITDA(1) |

5.0 | 5.0 | — | |||||||||

| Tons handled (thousands of tons) |

4,366 | 5,605 | (1,239 | ) | ||||||||

| Adjusted EBITDA per ton(1) |

$ | 1.15 | 0.89 | $ | 0.26 | |||||||

| (1) | See definitions of Adjusted EBITDA and Adjusted EBITDA per ton and reconciliation elsewhere in this release. |

| • | Adjusted EBITDA remained consistent at $5.0 million as a result of more favorable pricing and lower costs, offsetting the decrease in volume. |

Brazil Coke

Brazil Coke consists of a cokemaking facility in Vitória, Brazil, which we operate for an affiliate of ArcelorMittal. Brazil Coke earns operating and technology licensing fees based on production and recognizes a dividend on a preferred stock investment assuming certain minimum production levels are achieved.

| • | Segment Adjusted EBITDA remained reasonably consistent at $2.6 million. |

India Coke

India Coke consists of our 49 percent interest in our VISA SunCoke joint venture, which owns a 440 thousand ton cokemaking facility and associated steam generation unit in Odisha, India. Financial results for VISA SunCoke are recorded on a one-month lag and represent our 49 percent share of the joint venture’s results.

| • | Adjusted EBITDA remained relatively flat at a loss of $0.4 million in second quarter 2015. Import competition from China continues to depress coke pricing in India, resulting in weak margins. |

Coal Mining

Coal Mining consists of our metallurgical coal mining activities conducted in Virginia and West Virginia, currently mined by contractors. A majority of the metallurgical coal produced by our coal mining business is sold to our Jewell Coke facility for conversion into coke.

| • | Adjusted EBITDA was a loss of $5.4 million, down $5.8 million primarily as a result of a one-time, non-cash favorable $4.5 million fair value adjustment to the Harold Keene Coal Co., Inc. (HKCC) contingent consideration arrangement in the prior year period. |

While we continue to pursue a strategic exit from our Coal Mining business, we no longer believe a sale is probable due to the prolonged market challenges and sharply lower prices impacting the metallurgical coal industry. Instead, the company continues to significantly rationalize its mining operations to reduce ongoing costs. Therefore, these operations are no longer reported as discontinued and the related assets and liabilities are reported as held and used in our Coal Mining segment.

Corporate and Other

Corporate and other expenses in second quarter 2015 were $24.6 million, up $13.7 million versus second quarter 2014, primarily due to $12.6 million in pension plan termination charges.

4

Interest Expense, Net

Interest expense, net, decreased $14.1 million to $13.0 million in second quarter 2015, primarily related to prior year financing charges in connection with the dropdown of an additional 33 percent interest in our Haverhill and Middletown cokemaking operations to SXCP.

Cash Flow

Cash provided by operating activities was $76.6 million for year to date 2015 compared to $25.3 million in the same respective period of 2014. The increase primarily reflects improved operating performance, adjusted for non-cash items, in the current period and working capital changes associated with lower inventory levels.

Cash used in investing activities was $22.5 million for year to date 2015 and was $55.3 million lower than the prior year of $77.8 million in the same respective period of 2014, which included refurbishment work at Indiana Harbor and higher environmental remediation capital expenditures at our Haverhill cokemaking facility.

Dividends Declared

On July 16, 2015, our Board of Directors declared a quarterly cash dividend of $0.15 per share, up 100 percent versus the previous quarterly rate. This dividend will be paid on September 10, 2015 to stockholders of record at the close of business on August 19, 2015.

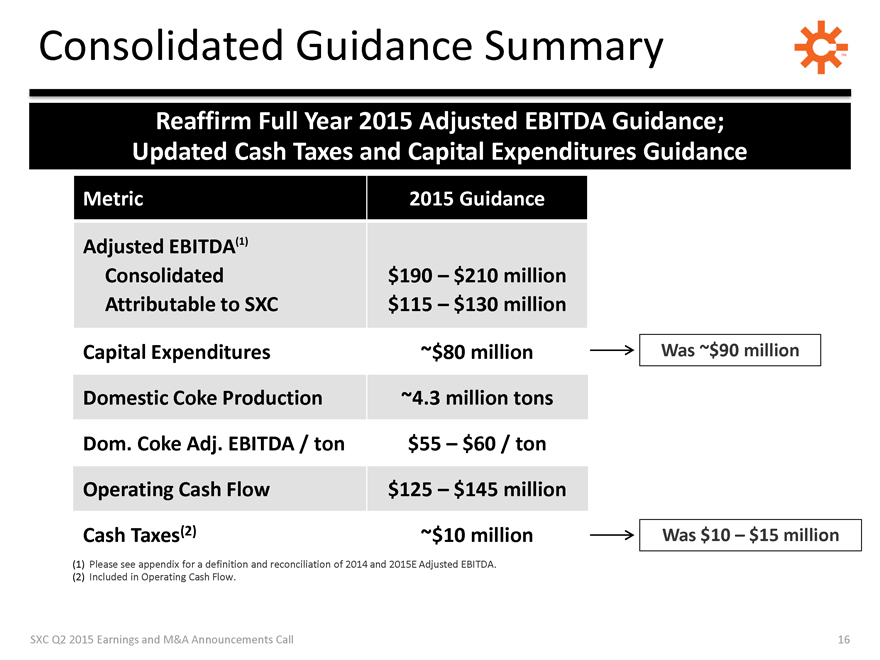

2015 OUTLOOK

We reaffirm our 2015 guidance excluding expected benefits of Convent Marine Terminal acquisition and Granite City 23 percent dropdown:

| • | Domestic coke production is expected to be approximately 4.3 million tons |

| • | Domestic coke Adjusted EBITDA per ton is expected to be at the lower end of our $55 per ton and $60 per ton range |

| • | Consolidated Adjusted EBITDA is expected to be between $190 million to $210 million |

| • | Adjusted EBITDA attributable to SXC is expected to be between $115 million and $130 million, reflecting the impact of public ownership in SXCP |

| • | Capital expenditures are projected to be approximately $80 million |

| • | Cash generated by operations is estimated to be between $125 million and $145 million |

| • | Cash taxes are projected to be approximately $10 million |

RELATED COMMUNICATIONS

We will host an investor conference call at 10:00 a.m. Eastern Time (9:00 a.m. Central Time) today. This conference call will be webcast live and archived for replay in the Investor Relations section of www.suncoke.com. Investors may participate in this call by dialing 1-800-588-4973 in the U.S. or 1-847-230-5643 if outside the U.S., confirmation code 40130618.

UPCOMING EVENTS

Additionally, we plan to participate in the following investor conferences:

| • | Citi MLP/Midstream Infrastructure Conference, August 19-20, 2015, Las Vegas, NV |

| • | Deutsche Bank Leveraged Finance Conference, September 28-30, 2015, Scottsdale, AZ |

5

SUNCOKE ENERGY, INC.

SunCoke Energy, Inc. (NYSE: SXC) supplies high-quality coke to the integrated steel industry under long-term take-or-pay coke contracts that pass through commodity and certain operating costs to customers. We utilize an innovative heat-recovery cokemaking technology that captures excess heat for steam or electrical power generation. Our cokemaking facilities are located in Illinois, Indiana, Ohio, Virginia, Brazil and India. We are the sponsor of SunCoke Energy Partners, L.P. (NYSE: SXCP), a publicly traded master limited partnership, holding a 2 percent general partner interest, 56 percent limited partnership interest and all of the incentive distribution rights. In addition, we own approximately 110 million tons of proven and probable coal reserves in Virginia and West Virginia. To learn more about SunCoke Energy, Inc., visit our website at www.suncoke.com.

DEFINITIONS

| • | Adjusted EBITDA represents earnings before interest, taxes, depreciation, depletion and amortization (“EBITDA”) adjusted for impairments, coal rationalization costs, sales discounts, and interest, taxes, depreciation and amortization attributable to our equity method investment. Prior to the expiration of our nonconventional fuel tax credits in November 2013, Adjusted EBITDA included an add-back of sales discounts related to the sharing of these credits with customers. Any adjustments to these amounts subsequent to 2013 have been included in Adjusted EBITDA. Our Adjusted EBITDA also includes EBITDA attributable to our equity method investment. EBITDA and Adjusted EBITDA do not represent and should not be considered alternatives to net income or operating income under GAAP and may not be comparable to other similarly titled measures in other businesses. Management believes Adjusted EBITDA is an important measure of the operating performance and liquidity of the Company’s net assets and its ability to incur and service debt, fund capital expenditures and make distributions. Adjusted EBITDA provides useful information to investors because it highlights trends in our business that may not otherwise be apparent when relying solely on GAAP measures and because it eliminates items that have less bearing on our operating performance and liquidity. EBITDA and Adjusted EBITDA are not measures calculated in accordance with GAAP, and they should not be considered a substitute for net income, operating cash flow or any other measure of financial performance presented in accordance with GAAP. |

| • | Adjusted EBITDA attributable to SXCP represents Adjusted EBITDA less Adjusted EBITDA attributable to noncontrolling interests. |

| • | Free cash flow represents distributions from SXCP plus SXC retained Adjusted EBITDA less cash interest, cash taxes, capital expenditures and any adjustments for any non-cash items. |

FORWARD-LOOKING STATEMENTS

Some of the statements included in this press release constitute “forward-looking statements” (as defined in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended). Forward-looking statements include all statements that are not historical facts and may be identified by the use of such words as “believe,” “expect,” “plan,” “project,” “intend,” “anticipate,” “estimate,” “predict,” “potential,” “continue,” “may,” “will,” “should” or the negative of these terms or similar expressions. Forward-looking statements are inherently uncertain and involve significant known and unknown risks and uncertainties (many of which are beyond the control of SXC) that could cause actual results to differ materially.

6

Such risks and uncertainties include, but are not limited to domestic and international economic, political, business, operational, competitive, regulatory and/or market factors affecting SXC, as well as uncertainties related to: pending or future litigation, legislation or regulatory actions; liability for remedial actions or assessments under existing or future environmental regulations; gains and losses related to acquisition, disposition or impairment of assets; recapitalizations; access to, and costs of, capital; the effects of changes in accounting rules applicable to SXC; and changes in tax, environmental and other laws and regulations applicable to SXC’s businesses.

Forward-looking statements are not guarantees of future performance, but are based upon the current knowledge, beliefs and expectations of SXC management, and upon assumptions by SXC concerning future conditions, any or all of which ultimately may prove to be inaccurate. The reader should not place undue reliance on these forward-looking statements, which speak only as of the date of this press release. SXC does not intend, and expressly disclaims any obligation, to update or alter its forward-looking statements (or associated cautionary language), whether as a result of new information, future events or otherwise after the date of this press release except as required by applicable law.

In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, SXC has included in its filings with the Securities and Exchange Commission cautionary language identifying important factors (but not necessarily all the important factors) that could cause actual results to differ materially from those expressed in any forward-looking statement made by SXC. For information concerning these factors, see SXC’s Securities and Exchange Commission filings such as its annual and quarterly reports and current reports on Form 8-K, copies of which are available free of charge on SXC’s website at www.suncoke.com. All forward-looking statements included in this press release are expressly qualified in their entirety by such cautionary statements. Unpredictable or unknown factors not discussed in this release also could have material adverse effects on forward-looking statements.

###

7

SunCoke Energy, Inc.

Consolidated Statements of Operations

(Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| (Dollars and shares in millions, except per share amounts) | ||||||||||||||||

| Revenues |

||||||||||||||||

| Sales and other operating revenue |

$ | 347.6 | $ | 371.7 | $ | 671.5 | $ | 729.7 | ||||||||

| Other income |

0.6 | 0.5 | 0.7 | 2.1 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

348.2 | 372.2 | 672.2 | 731.8 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Costs and operating expenses |

||||||||||||||||

| Cost of products sold and operating expenses |

296.0 | 290.0 | 558.1 | 594.0 | ||||||||||||

| Selling, general and administrative expenses |

19.4 | 21.9 | 32.0 | 43.8 | ||||||||||||

| Depreciation, depletion and amortization expense |

26.4 | 28.6 | 50.2 | 57.6 | ||||||||||||

| Asset impairment |

— | 103.1 | — | 103.1 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total costs and operating expenses |

341.8 | 443.6 | 640.3 | 798.5 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income (loss) |

6.4 | (71.4 | ) | 31.9 | (66.7 | ) | ||||||||||

| Interest expense, net |

13.0 | 27.1 | 36.3 | 39.2 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss before income tax (benefit) expense and loss from equity method investment |

(6.6 | ) | (98.5 | ) | (4.4 | ) | (105.9 | ) | ||||||||

| Income tax (benefit) expense |

(0.8 | ) | (50.8 | ) | 0.3 | (55.0 | ) | |||||||||

| Loss from equity method investment |

0.7 | 0.9 | 1.4 | 1.5 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss |

(6.5 | ) | (48.6 | ) | (6.1 | ) | (52.4 | ) | ||||||||

| Less: Net income attributable to noncontrolling interests |

7.0 | 0.6 | 11.4 | 4.6 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss attributable to SunCoke Energy, Inc. |

$ | (13.5 | ) | $ | (49.2 | ) | $ | (17.5 | ) | $ | (57.0 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss attributable to SunCoke Energy, Inc. per common share: |

||||||||||||||||

| Basic |

(0.21 | ) | (0.71 | ) | (0.27 | ) | (0.82 | ) | ||||||||

| Diluted |

(0.21 | ) | (0.71 | ) | (0.27 | ) | (0.82 | ) | ||||||||

| Weighted average number of common shares outstanding: |

||||||||||||||||

| Basic |

65.2 | 69.5 | 65.7 | 69.6 | ||||||||||||

| Diluted |

65.2 | 69.5 | 65.7 | 69.6 | ||||||||||||

8

SunCoke Energy, Inc.

Consolidated Balance Sheets

(Unaudited)

| June 30, 2015 |

December 31, 2014 |

|||||||

| (Dollars in millions, except par value amounts) |

||||||||

| Assets |

||||||||

| Cash and cash equivalents |

$ | 201.7 | $ | 139.0 | ||||

| Receivables |

56.7 | 78.2 | ||||||

| Inventories |

107.6 | 142.2 | ||||||

| Income tax receivable |

6.9 | 6.0 | ||||||

| Deferred income taxes |

18.5 | 26.4 | ||||||

| Other current assets |

6.9 | 3.6 | ||||||

|

|

|

|

|

|||||

| Total current assets |

398.3 | 395.4 | ||||||

|

|

|

|

|

|||||

| Investment in Brazilian cokemaking operations |

41.0 | 41.0 | ||||||

| Equity method investment in VISA SunCoke Limited |

20.3 | 22.3 | ||||||

| Properties, plants and equipment, net |

1,453.0 | 1,480.0 | ||||||

| Goodwill and other intangible assets, net |

21.2 | 22.0 | ||||||

| Deferred charges and other assets |

16.4 | 25.4 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 1,950.2 | $ | 1,986.1 | ||||

|

|

|

|

|

|||||

| Liabilities and Equity |

||||||||

| Accounts payable |

$ | 95.9 | $ | 121.3 | ||||

| Accrued liabilities |

43.3 | 67.5 | ||||||

| Interest payable |

21.8 | 19.9 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

161.0 | 208.7 | ||||||

|

|

|

|

|

|||||

| Long-term debt |

699.1 | 633.5 | ||||||

| Accrual for black lung benefits |

44.6 | 43.9 | ||||||

| Retirement benefit liabilities |

32.1 | 33.6 | ||||||

| Deferred income taxes |

316.9 | 321.9 | ||||||

| Asset retirement obligations |

22.1 | 22.2 | ||||||

| Other deferred credits and liabilities |

14.6 | 16.9 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

1,290.4 | 1,280.7 | ||||||

|

|

|

|

|

|||||

| Equity |

||||||||

| Preferred stock, $0.01 par value. Authorized 50,000,000 shares; no issued shares at June 30, 2015 and December 31, 2014 |

— | — | ||||||

| Common stock, $0.01 par value. Authorized 300,000,000 shares; issued 71,398,975 and 71,251,529 shares at June 30, 2015 and December 31, 2014, respectively |

0.7 | 0.7 | ||||||

| Treasury stock, 6,161,395 and 4,977,115 shares at June 30, 2015 and December 31, 2014, respectively |

(125.0 | ) | (105.0 | ) | ||||

| Additional paid-in capital |

541.2 | 543.6 | ||||||

| Accumulated other comprehensive loss |

(17.3 | ) | (21.5 | ) | ||||

| Retained (deficit) earnings |

(12.4 | ) | 13.9 | |||||

|

|

|

|

|

|||||

| Total SunCoke Energy, Inc. stockholders’ equity |

387.2 | 431.7 | ||||||

| Noncontrolling interests |

272.6 | 273.7 | ||||||

|

|

|

|

|

|||||

| Total equity |

659.8 | 705.4 | ||||||

|

|

|

|

|

|||||

| Total liabilities and equity |

$ | 1,950.2 | $ | 1,986.1 | ||||

|

|

|

|

|

|||||

9

SunCoke Energy, Inc.

Consolidated Statements of Cash Flows

(Unaudited)

| Six Months Ended June 30, | ||||||||

| 2015 | 2014 | |||||||

| (Dollars in millions) | ||||||||

| Cash Flows from Operating Activities: |

||||||||

| Net loss |

$ | (6.1 | ) | $ | (52.4 | ) | ||

| Adjustments to reconcile net loss to net cash provided by operating activities: |

||||||||

| Asset impairment and goodwill |

— | 103.1 | ||||||

| Depreciation, depletion and amortization expense |

50.2 | 57.6 | ||||||

| Deferred income tax benefit |

(1.1 | ) | (69.9 | ) | ||||

| Settlement loss and expense for pension plan |

13.1 | 0.1 | ||||||

| Gain on curtailment and payments in excess of expense for postretirement plan benefits |

(5.5 | ) | (2.6 | ) | ||||

| Share-based compensation expense |

4.2 | 5.3 | ||||||

| Excess tax benefit from share-based awards |

— | (0.2 | ) | |||||

| Loss from equity method investment |

1.4 | 1.5 | ||||||

| Loss on extinguishment of debt |

9.4 | 15.4 | ||||||

| Changes in working capital pertaining to operating activities: |

||||||||

| Receivables |

21.5 | 21.2 | ||||||

| Inventories |

36.0 | (5.1 | ) | |||||

| Accounts payable |

(25.4 | ) | (32.5 | ) | ||||

| Accrued liabilities |

(18.9 | ) | (17.2 | ) | ||||

| Interest payable |

1.9 | (3.3 | ) | |||||

| Income taxes |

(0.9 | ) | 10.1 | |||||

| Other |

(3.2 | ) | (5.8 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

76.6 | 25.3 | ||||||

|

|

|

|

|

|||||

| Cash Flows from Investing Activities: |

||||||||

| Capital expenditures |

(22.5 | ) | (77.8 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(22.5 | ) | (77.8 | ) | ||||

|

|

|

|

|

|||||

| Cash Flows from Financing Activities: |

||||||||

| Net proceeds from issuance of SunCoke Energy Partners, L.P. units |

— | 88.7 | ||||||

| Proceeds from issuance of long-term debt |

210.8 | 268.1 | ||||||

| Repayment of long-term debt |

(149.5 | ) | (271.5 | ) | ||||

| Debt issuance costs |

(4.8 | ) | (5.8 | ) | ||||

| Proceeds from revolving facility |

— | 40.0 | ||||||

| Repayment of revolving facility |

— | (72.0 | ) | |||||

| Cash distribution to noncontrolling interests |

(18.7 | ) | (14.8 | ) | ||||

| Shares repurchased |

(20.0 | ) | (10.1 | ) | ||||

| Proceeds from exercise of stock options, net of shares withheld for taxes |

(0.4 | ) | 0.5 | |||||

| Excess tax benefit from share-based awards |

— | 0.2 | ||||||

| Dividends paid |

(8.8 | ) | — | |||||

|

|

|

|

|

|||||

| Net cash provided by financing activities |

8.6 | 23.3 | ||||||

|

|

|

|

|

|||||

| Net increase (decrease) in cash and cash equivalents |

62.7 | (29.2 | ) | |||||

| Cash and cash equivalents at beginning of period |

139.0 | 233.6 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of period |

$ | 201.7 | $ | 204.4 | ||||

|

|

|

|

|

|||||

10

SunCoke Energy, Inc.

Segment Financial and Operating Data

The following tables set forth financial and operating data for the three and six months ended June 30, 2015 and 2014:

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| (Dollars in millions) | ||||||||||||||||

| Sales and other operating revenues: |

||||||||||||||||

| Domestic Coke |

$ | 326.5 | $ | 344.5 | $ | 629.6 | $ | 678.0 | ||||||||

| Brazil Coke |

8.5 | 9.0 | 18.4 | 18.3 | ||||||||||||

| Coal Logistics |

8.6 | 10.7 | 15.9 | 19.4 | ||||||||||||

| Coal Logistics intersegment sales |

4.9 | 4.5 | 9.6 | 8.7 | ||||||||||||

| Coal Mining |

4.0 | 7.5 | 7.6 | 14.0 | ||||||||||||

| Coal Mining intersegment sales |

24.8 | 35.4 | 49.0 | 69.3 | ||||||||||||

| Elimination of intersegment sales |

(29.7 | ) | (39.9 | ) | (58.6 | ) | (78.0 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total sales and other operating revenue |

$ | 347.6 | $ | 371.7 | $ | 671.5 | $ | 729.7 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA(1): |

||||||||||||||||

| Domestic Coke |

$ | 56.2 | $ | 64.3 | $ | 108.9 | $ | 111.1 | ||||||||

| Brazil Coke |

2.6 | 2.5 | 6.7 | 4.2 | ||||||||||||

| India Coke |

(0.4 | ) | (0.5 | ) | (1.1 | ) | (0.4 | ) | ||||||||

| Coal Logistics |

5.0 | 5.0 | 7.6 | 7.1 | ||||||||||||

| Coal Mining |

(5.4 | ) | 0.4 | (8.5 | ) | (6.1 | ) | |||||||||

| Corporate and Other, including legacy costs, net(2) |

(24.6 | ) | (10.9 | ) | (32.3 | ) | (21.3 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Adjusted EBITDA |

$ | 33.4 | $ | 60.8 | $ | 81.3 | $ | 94.6 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Coke Operating Data: |

||||||||||||||||

| Domestic Coke capacity utilization (%) |

99 | 100 | 97 | 95 | ||||||||||||

| Domestic Coke production volumes (thousands of tons) |

1,047 | 1,059 | 2,045 | 2,003 | ||||||||||||

| Domestic Coke sales volumes (thousands of tons) |

1,110 | 1,059 | 2,059 | 2,007 | ||||||||||||

| Domestic Coke Adjusted EBITDA per ton(3) |

$ | 50.63 | $ | 60.72 | $ | 52.89 | $ | 55.36 | ||||||||

| Brazilian Coke production—operated facility (thousands of tons) |

437 | 413 | 876 | 665 | ||||||||||||

| Indian Coke sales (thousands of tons)(4) |

87 | 85 | 182 | 207 | ||||||||||||

| Coal Logistics Operating Data: |

||||||||||||||||

| Tons handled (thousands of tons) |

4,366 | 5,605 | 8,160 | 9,964 | ||||||||||||

| Coal Logistics Adjusted EBITDA per ton handled(5) |

$ | 1.15 | $ | 0.89 | $ | 0.93 | $ | 0.71 | ||||||||

| (1) | See definition of Adjusted EBITDA and reconciliation to GAAP elsewhere in this release. |

| (2) | Legacy costs, net include costs associated with former mining employee-related liabilities prior to the implementation of our current contractor mining business net of certain royalty revenues. See details of these legacy items below. |

| (3) | Reflects Domestic Coke Adjusted EBITDA divided by Domestic Coke sales volumes. |

| (4) | Represents 100% of VISA SunCoke sales volumes. |

| (5) | Reflects Coal Logistics Adjusted EBITDA divided by Coal Logistics tons handled. |

11

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| (Dollars in millions) | ||||||||||||||||

| Royalty income |

$ | 0.1 | $ | 0.2 | $ | 0.1 | $ | 0.3 | ||||||||

| Black lung charges |

(1.0 | ) | (0.5 | ) | (1.9 | ) | (1.0 | ) | ||||||||

| Postretirement benefit plan (expense) benefit |

(0.1 | ) | 0.3 | 3.8 | 0.6 | |||||||||||

| Defined benefit plan expense |

(12.9 | ) | (0.1 | ) | (13.1 | ) | (0.1 | ) | ||||||||

| Workers compensation expense |

(0.5 | ) | (1.1 | ) | (1.4 | ) | (2.3 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total legacy costs, net |

$ | (14.4 | ) | $ | (1.2 | ) | $ | (12.5 | ) | $ | (2.5 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

12

SunCoke Energy, Inc.

Reconciliations of Non-GAAP Information

Adjusted EBITDA to Net Income (Loss)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| (Dollars in millions) | ||||||||||||||||

| Adjusted EBITDA attributable to SunCoke Energy, Inc. |

$ | 15.3 | $ | 46.3 | $ | 45.1 | $ | 70.8 | ||||||||

| Add: Adjusted EBITDA attributable to noncontrolling interests(1) |

18.1 | 14.5 | 36.2 | 23.8 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA |

$ | 33.4 | $ | 60.8 | $ | 81.3 | $ | 94.6 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Subtract: |

||||||||||||||||

| Adjustment to unconsolidated affiliate earnings(2) |

0.7 | 1.1 | 1.0 | 2.1 | ||||||||||||

| Nonrecurring coal rationalization costs(3) |

0.6 | 0.3 | (0.4 | ) | 0.5 | |||||||||||

| Depreciation, depletion and amortization expense |

26.4 | 28.6 | 50.2 | 57.6 | ||||||||||||

| Interest expense, net |

13.0 | 27.1 | 36.3 | 39.2 | ||||||||||||

| Income tax expense (benefit) |

(0.8 | ) | (50.8 | ) | 0.3 | (55.0 | ) | |||||||||

| Sales discounts provided to customers due to sharing of nonconventional fuel tax credits(4) |

— | — | — | (0.5 | ) | |||||||||||

| Asset and goodwill impairment |

— | 103.1 | 103.1 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss |

$ | (6.5 | ) | $ | (48.6 | ) | $ | (6.1 | ) | $ | (52.4 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Add: |

||||||||||||||||

| Asset and goodwill impairment |

— | 103.1 | — | 103.1 | ||||||||||||

| Depreciation, depletion and amortization |

26.4 | 28.6 | 50.2 | 57.6 | ||||||||||||

| Deferred income tax benefit |

(4.2 | ) | (66.8 | ) | (1.1 | ) | (69.9 | ) | ||||||||

| Loss on extinguishment of debt |

— | 15.4 | 9.4 | 15.4 | ||||||||||||

| Changes in working capital and other |

49.8 | 4.9 | 24.2 | (28.5 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net cash provided by operating activities |

$ | 65.5 | $ | 36.6 | $ | 76.6 | $ | 25.3 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Reflects noncontrolling interest in Indiana Harbor and the portion of SXCP owned by public unitholders. |

| (2) | Reflects share of interest, taxes, depreciation and amortization related to VISA SunCoke. |

| (3) | Nonrecurring coal rationalization costs include employee severance, contract termination costs and other one-time costs to idle mines incurred during the execution of our coal rationalization plan. |

| (4) | At December 31, 2013, we had $13.6 million accrued related to sales discounts to be paid to our Granite City customer. During the first quarter of 2014, we settled this obligation for $13.1 million which resulted in a gain of $0.5 million. This gain is recorded in sales and other operating revenue on our Consolidated Statement of Operations. |

13

SunCoke Energy, Inc.

Reconciliations of Non-GAAP Information

Estimated 2015 Consolidated Adjusted EBITDA to Estimated Net Income

| 2015 | ||||||||

| Low | High | |||||||

| Net income |

$ | 21 | $ | 38 | ||||

| Depreciation, depletion and amortization expense |

94 | 94 | ||||||

| Interest expense, net |

66 | 64 | ||||||

| Income tax expense |

5 | 10 | ||||||

| Nonrecurring coal rationalization costs(1) |

1 | 1 | ||||||

| Adjustment to unconsolidated affiliate earnings(2) |

3 | 3 | ||||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 190 | $ | 210 | ||||

|

|

|

|

|

|||||

| EBITDA attributable to noncontrolling interests(3) |

(75 | ) | (80 | ) | ||||

|

|

|

|

|

|||||

| Adjusted EBITDA attributable to SXC |

$ | 115 | $ | 130 | ||||

|

|

|

|

|

|||||

| (1) | Nonrecurring coal rationalization costs include employee severance, contract termination costs and other one-time costs to idle mines incurred during the execution of our coal rationalization plan. |

| (2) | Represents SunCoke’s share of India JV interest, taxes and depreciation expense. |

| (3) | Represents Adjusted EBITDA attributable to SXCP public unitholders and to DTE Energy’s interest in Indiana Harbor. |

14

Exhibit 99.2

SunCoke Energy, Inc.

Q2

2015 Earnings,

M&A Announcement

Conference Call

July 21, 2015

SunCoke Energy™

Forward-Looking Statements

TM

This slide presentation should be reviewed in conjunction with the Second

Quarter 2015 earnings release of SunCoke Energy, Inc. (SXC) and the conference call held on July 21, 2015 at 10:00 a.m. ET.

Some of the information included in

this presentation constitutes “forward-looking statements” as defined in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. All statements in this presentation that

express opinions, expectations, beliefs, plans, objectives, assumptions or projections with respect to anticipated future performance of SXC or SunCoke Energy Partners, L.P. (SXCP), in contrast with statements of historical facts, are

forward-looking statements. Such forward-looking statements are based on management’s beliefs and assumptions and on information currently available. Forward-looking statements include information concerning possible or assumed future results

of operations, business strategies, financing plans, competitive position, potential growth opportunities, potential operating performance improvements, the effects of competition and the effects of future legislation or regulations. Forward-looking

statements include all statements that are not historical facts and may be identified by the use of forward-looking terminology such as the words “believe,” “expect,” “plan,” “intend,” “anticipate,”

“estimate,” “predict,” “potential,” “continue,” “may,” “will,” “should” or the negative of these terms or similar expressions.

Although management believes that its plans, intentions and expectations reflected in or suggested by the forward-looking statements made in this presentation are reasonable, no

assurance can be given that these plans, intentions or expectations will be achieved when anticipated or at all. Moreover, such statements are subject to a number of assumptions, risks and uncertainties. Many of these risks are beyond the control of

SXC and SXCP, and may cause actual results to differ materially from those implied or expressed by the forward-looking statements. Each of SXC and SXCP has included in its filings with the Securities and Exchange Commission cautionary language

identifying important factors (but not necessarily all the important factors) that could cause actual results to differ materially from those expressed in any forward-looking statement. For more information concerning these factors, see the

Securities and Exchange Commission filings of SXC and SXCP. All forward-looking statements included in this presentation are expressly qualified in their entirety by such cautionary statements. Although forward-looking statements are based on

current beliefs and expectations, caution should be taken not to place undue reliance on any such forward-looking statements because such statements speak only as of the date hereof. SXC and SXCP do not have any intention or obligation to update

publicly any forward-looking statement (or its associated cautionary language) whether as a result of new information or future events or after the date of this presentation, except as required by applicable law.

This presentation includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures.

Reconciliations of non-GAAP financial measures to GAAP financial measures are provided in the Appendix at the end of the presentation. Investors are urged to consider carefully the

comparable GAAP measures and the reconciliations to those measures provided in the Appendix.

SXC Q2 2015 Earnings and M&A Announcements Call 1

Management Perspective

Delivered operating results in line with calendar year targets

Significantly

increased dividend, raising quarterly rate 100%

SXCP’s highly accretive Convent Marine Terminal acquisition expected to substantially grow distributions into

50/50 IDR splits

Reached agreement on Granite City 23% dropdown transaction at 7.2x multiple(2)

Reaffirming FY 2015E Consolidated Adjusted EBITDA(1,3) guidance of $190M – $210M

(1) For

a definition and reconciliation of Adjusted EBITDA (Consolidated), please see appendix.

(2) Based on $67M transaction value over ~$9.3M EBITDA run-rate for 23%

interest in Granite City. This transaction is expected to close in the third quarter 2015, concurrently with the execution of long-term financing related to the Convent Marine Terminal acquisition.

(3) Excludes expected benefit of Convent Marine Terminal acquisition.

SXC Q2 2015 Earnings and

M&A Announcements Call 2

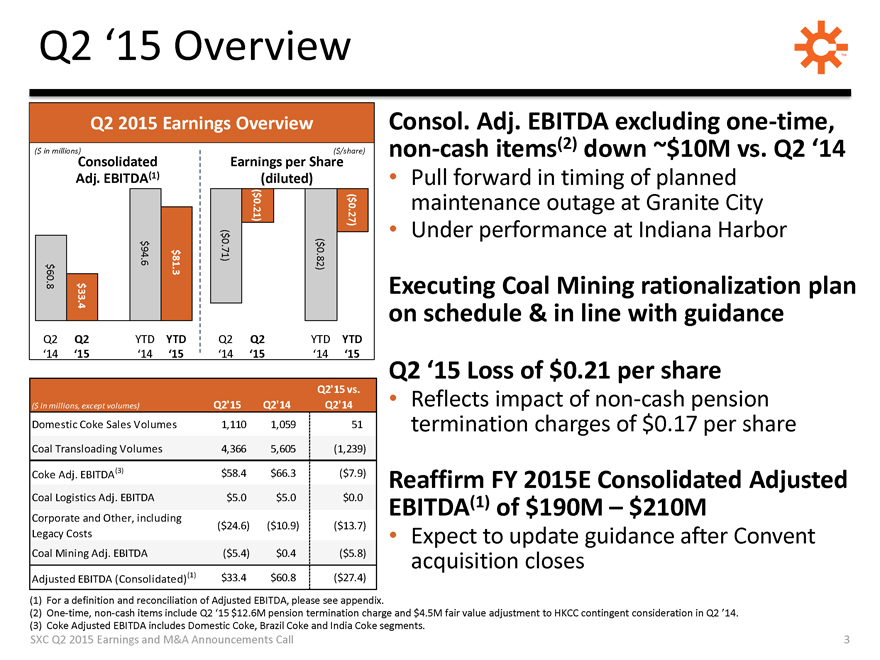

Q2 ‘15 Overview

Q2

2015 Earnings Overview

($ in millions)

Consolidated

Adj. EBITDA(1)

$60.8

$33.4

$94.6

$81.3

Q2

‘14

Q2

‘15

YTD

‘14

YTD

‘15

($/share)

Earnings per Share (diluted)

($0.71)

($0.21)

($0.82)

($0.27)

Q2

‘14

Q2

‘15

YTD

‘14

YTD

‘15

Q2’15 vs.

($ in millions, except volumes)

Q2’15

Q2’14

Q2’14

Domestic Coke Sales Volumes

1,110

1,059

51

Coal Transloading Volumes

4,366

5,605

(1,239)

Coke Adj. EBITDA(3)

$58.4

$66.3

($7.9)

Coal Logistics Adj. EBITDA

$5.0

$5.0

$0.0

Corporate and Other, including

($24.6)

($10.9)

($13.7)

Legacy Costs

Coal Mining Adj. EBITDA

($5.4)

$0.4

($5.8)

Adjusted EBITDA (Consolidated)(1)

$33.4

$60.8

($27.4)

(1) For a definition and reconciliation of Adjusted EBITDA, please see appendix.

(2) One-time, non-cash items include Q2 ‘15 $12.6M pension termination charge and $4.5M fair value adjustment to HKCC contingent consideration in Q2 ’14.

(3) Coke Adjusted EBITDA includes Domestic Coke, Brazil Coke and India Coke segments.

Consol. Adj. EBITDA excluding one-time, non-cash items(2) down ~$10M vs. Q2 ‘14

Pull

forward in timing of planned maintenance outage at Granite City

Under performance at Indiana Harbor

Executing Coal Mining rationalization plan on schedule & in line with guidance

Q2

‘15 Loss of $0.21 per share

Reflects impact of non-cash pension termination charges of $0.17 per share

Reaffirm FY 2015E Consolidated Adjusted EBITDA(1) of $190M – $210M

Expect to update

guidance after Convent acquisition closes

SXC Q2 2015 Earnings and M&A Announcements Call 3

Adjusted EBITDA(1) – Q2 ‘14 to Q2 ‘15

Consol. Adj. EBITDA, excluding one-time non-cash charges, down ~$10M

($ in millions)

$56.3

($4.5) (2)

$60.8

($4.1)

($4.6M) – Indiana Harbor cost under-recovery, net

($4.0)

($1.3)

($0.9)

($1.1M) – Corp. & Other

$0.2M – International Coke(3)

$46.0

$12.6 (4)

$33.4

Q2 2014 Adj. EBITDA

(Consolidated) (1)

Domestic Coke (ex. Granite City outage)

Granite City

Maint. Outage

Coal Mining

Other

Q2 2015 Adj. EBITDA

(Consolidated) (1)

(1) For a definition and reconciliation of Adjusted EBITDA, please see appendix.

(2)

Represents one-time, non-cash favorable adjustment to the HKCC Contingent Consideration.

(3) International Coke includes Brazil Coke and India Coke.

(4) Represents one-time, non-cash pension termination charge.

SXC Q2 2015 Earnings and M&A

Announcements Call 4

Domestic Coke Business Summary

Below target improvement at Indiana Harbor and Granite City outage impacted Q2 results; however, reaffirm full year guidance

Domestic Coke Production and Adjusted EBITDA Per Ton(1)

(Production in thousands of tons, $ in

per ton amounts)

$49/ton $61/ton $67/ton $58/ton $56/ton $51/ton

944 150 153

264 199 178

1,059 155 177 279 264 184

1,090 155 182 292 275 185

1,083 156 177 296 270 185

998 149 171 284 223 171

1,047 151 166 288 257 185

Q1 ‘14 Q2 ‘14 Q3 ‘14 Q4 ‘14 Q1 ‘15 Q2

‘15

Adjusted EBITDA/ton

Middletown

Granite City

Haverhill

Indiana Harbor

Jewell

(1) For a definition and reconciliation of Adjusted EBITDA and Adjusted EBITDA/Ton, please see appendix.

Continued ramp-up of Indiana Harbor facility

Below target production during Q2

O&M cost under-recovery

Pull forward in timing of planned maintenance outage at Granite

City

~$4M impact from higher O&M expenses & slightly lower production

Reaffirm Adj. EBITDA per ton(1) guidance of $55 – $60

SXC Q2 2015 Earnings and M&A

Announcements Call

5

Liquidity Position

Strong

cash position and revolver capacity provide significant financial flexibility

Attributable to SXCP

$165.4 $91.8 $73.6

($6.5)

$12.6

$26.4

$32.5

($14.2)

($4.9)

($9.6)

$201.7 $98.9 $102.8

$13.1M – Timing of interest payments (Feb. & Aug.)

$12.5M – Higher coke sales from inventory

$11.3M – Lower coal

inventory

($8.8M) – Ongoing

($5.4M) – Environmental &

Expansion

SXCP revolver availability: $250M

SXC revolver availability:

$148.5M

Q1 2015 Cash Balance

Net Loss

Pension Termination Charge

DD&A

Working Capital & Other

Capex

SXC Dividend Payment

Distributions to SXCP Public Shareholders

Q2 2015 Cash Balance

SXC Q2 2015 Earnings and M&A Announcements Call

6

STRATEGIC UPDATES

SunCoke

Energy™

SXC Q2 2015 Earnings and M&A Announcements Call

7

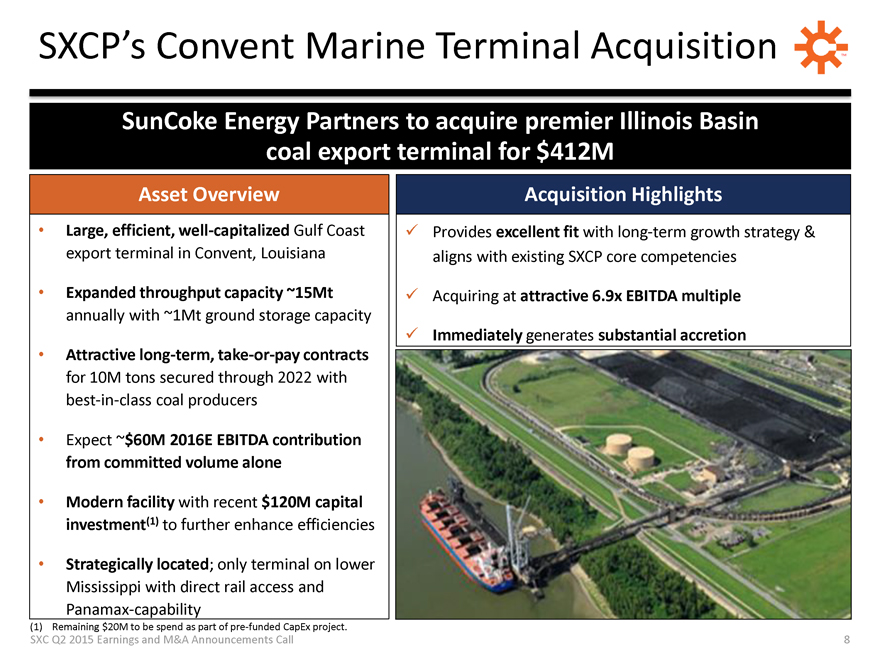

SXCP’s Convent Marine Terminal Acquisition

SunCoke Energy Partners to acquire premier Illinois Basin coal export terminal for $412M

Asset

Overview

Large, efficient, well-capitalized Gulf Coast export terminal in Convent, Louisiana

Expanded throughput capacity ~15Mt annually with ~1Mt ground storage capacity

Attractive

long-term, take-or-pay contracts for 10M tons secured through 2022 with best-in-class coal producers

Expect ~$60M 2016E EBITDA contribution from committed volume

alone

Modern facility with recent $120M capital investment(1) to further enhance efficiencies

Strategically located; only terminal on lower Mississippi with direct rail access and Panamax-capability

(1) Remaining $20M to be spend as part of pre-funded CapEx project.

Acquisition Highlights

Provides excellent fit with long-term growth strategy & aligns with existing SXCP core competencies

Acquiring at attractive 6.9x EBITDA multiple

Immediately generates substantial accretion

SXC Q2 2015 Earnings and M&A Announcements Call

8

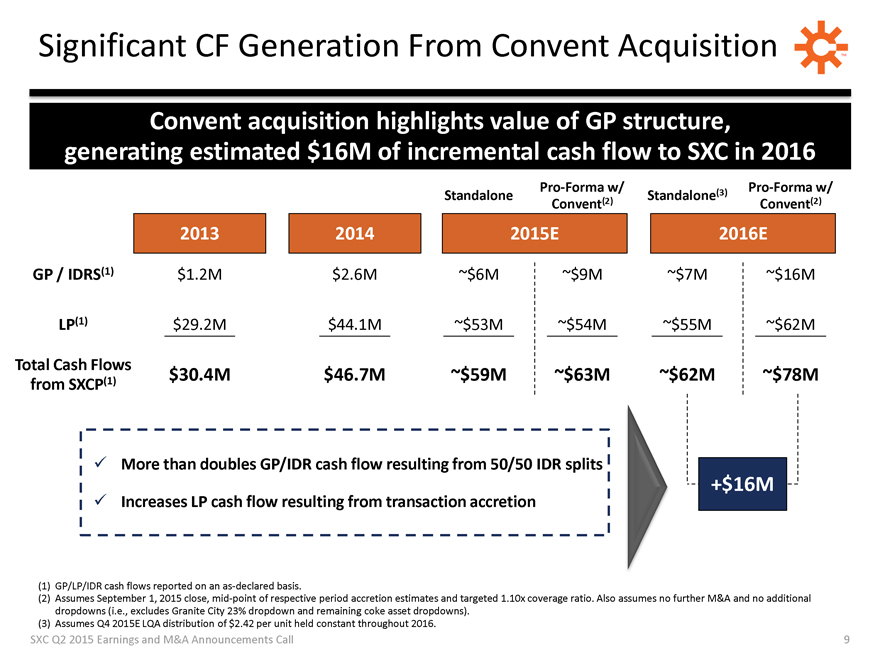

Significant CF Generation From Convent Acquisition

Convent acquisition highlights value of GP structure, generating estimated $16M of incremental cash flow to SXC in 2016

GP / IDRS(1) LP(1) Total Cash Flows from SXCP(1)

2013 $1.2M $29.2M $30.4M

2014 $2.6M $44.1M $46.7M

Standalone Pro-Forma w/ Convent(2)

2015E

~$6M ~$53M ~$59M

~$9M ~$54M ~$63M

Standalone(3)

Pro-Forma w/ Convent(2)

2016E

~$7M ~$55M ~$62M

~$16M ~$62M ~$78M

+$16M

More than doubles GP/IDR cash flow resulting from 50/50 IDR splits

Increases LP cash flow resulting from transaction accretion

(1) GP/LP/IDR cash flows reported

on an as-declared basis.

(2) Assumes September 1, 2015 close, mid-point of respective period accretion estimates and targeted 1.10x coverage ratio. Also

assumes no further M&A and no additional dropdowns (i.e., excludes Granite City 23% dropdown and remaining coke asset dropdowns).

(3) Assumes Q4 2015E LQA

distribution of $2.42 per unit held constant throughout 2016.

SXC Q2 2015 Earnings and M&A Announcements Call

9

Executing Capital Allocation Strategy

Leveraging GP/LP structure and executing balanced capital allocation strategy

Raised SXC

dividend 100% to $0.15 per share, reflecting strategy to distribute significant portion of free cash flow

As we transition to pure-play GP, primary capital

allocation strategy is to distribute 80% to 90% of free cash flow

Anticipate distributing significant portion of free cash flow derived from

SXCP’s Convent transaction ($0.15 to $0.20 per SXC share on annual basis)

Intend to

opportunistically execute against SXC’s remaining $55M share repurchase authorization

Expect to call remaining SXC bonds upon closing of Granite City dropdown

After redemption, more GP appropriate covenants in credit agreement govern restricted payments

SXC Q2 2015 Earnings and M&A Announcements Call

10

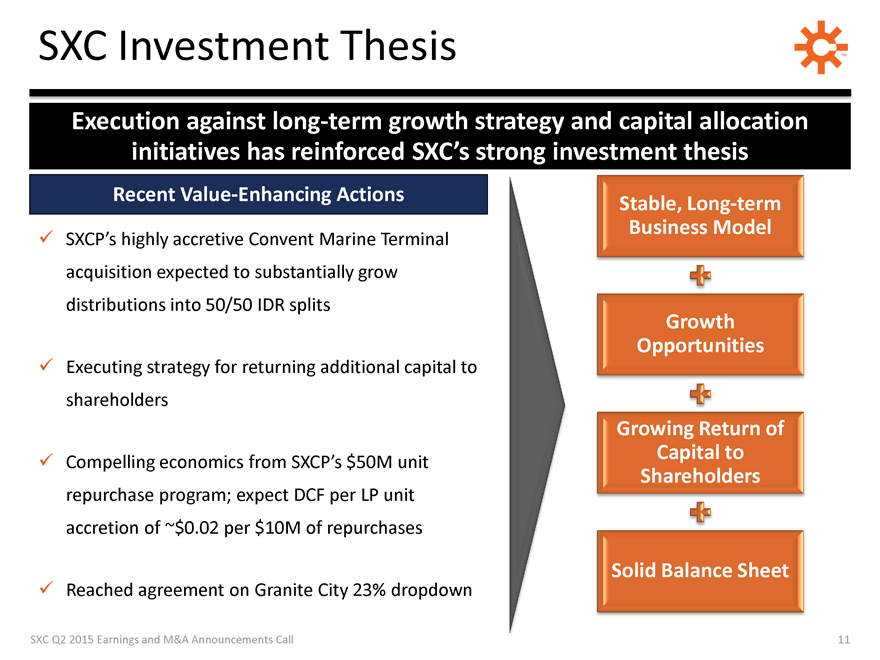

SXC Investment Thesis

Execution against long-term growth strategy and capital allocation initiatives has reinforced SXC’s strong investment thesis

Recent Value-Enhancing Actions

SXCP’s highly accretive Convent Marine Terminal

acquisition expected to substantially grow distributions into 50/50 IDR splits

Executing strategy for returning additional capital to shareholders

Compelling economics from SXCP’s $50M unit repurchase program; expect DCF per LP unit accretion of ~$0.02 per $10M of repurchases

Reached agreement on Granite City 23% dropdown

Stable, Long-term Business Model

Growth Opportunities

Growing Return of Capital to Shareholders

Solid Balance Sheet

SXC Q2 2015 Earnings and M&A Announcements Call 11

QUESTIONS

SunCoke

Energy™

SXC Q2 2015 Earnings and M&A Announcements Call

12

Investor Relations

630-824-1907 www.suncoke.com

SunCoke Energy™

APPENDIX

SunCoke

Energy™

SXC Q2 2015 Earnings and M&A Announcements Call 14

Definitions

Adjusted

EBITDA represents earnings before interest, taxes, depreciation, depletion and amortization (“EBITDA”) adjusted for impairments, coal rationalization costs, sales discounts, and interest, taxes, depreciation and amortization attributable

to our equity method investment. Prior to the expiration of our nonconventional fuel tax credits in November 2013, Adjusted EBITDA included an add-back of sales discounts related to the sharing of these credits with customers. Any adjustments to

these amounts subsequent to 2013 have been included in Adjusted EBITDA. Our Adjusted EBITDA also includes EBITDA attributable to our equity method investment. EBITDA and Adjusted EBITDA do not represent and should not be considered alternatives to

net income or operating income under GAAP and may not be comparable to other similarly titled measures in other businesses. Management believes Adjusted EBITDA is an important measure of the operating performance and liquidity of the Company’s

net assets and its ability to incur and service debt, fund capital expenditures and make distributions. Adjusted EBITDA provides useful information to investors because it highlights trends in our business that may not otherwise be apparent when

relying solely on GAAP measures and because it eliminates items that have less bearing on our operating performance and liquidity. EBITDA and Adjusted EBITDA are not measures calculated in accordance with GAAP, as they should not be considered a

substitute for net income, operating cash flow or any other measure of financial performance presented in accordance with GAAP.

EBITDA represents earnings before

interest, taxes, depreciation, depletion and amortization.

Adjusted EBITDA attributable to SXC/SXCP represents consolidated Adjusted EBITDA less Adjusted EBITDA

attributable to noncontrolling interests.

Adjusted EBITDA/Ton represents Adjusted EBITDA divided by tons sold/handled.

Non recurring Coal Rationalization Costs include employee severance, contract termination costs and other one-time costs to idle mines incurred during the execution of our coal

rationalization plan.

Legacy Costs include royalty revenues, costs associated with former mining employee-related liabilities prior to the implementation of our

current contractor mining business.

SXC Q2 2015 Earnings and M&A Announcements Call 15

Consolidated Guidance Summary

Reaffirm Full Year 2015 Adjusted EBITDA Guidance; Updated Cash Taxes and Capital Expenditures Guidance

Metric

2015 Guidance

Adjusted EBITDA(1)

Consolidated

$190 – $210 million

Attributable to SXC

$115 – $130 million

Capital Expenditures

~$80 million

Was ~$90 million

Domestic Coke Production

~4.3 million tons

Dom. Coke Adj. EBITDA / ton

$55 – $60 / ton

Operating Cash Flow

$125 – $145 million

Cash Taxes(2)

~$10 million

Was $10 – $15 million

(1) Please see appendix for a definition and reconciliation of 2014

and 2015E Adjusted EBITDA.

(2) Included in Operating Cash Flow.

SXC Q2 2015

Earnings and M&A Announcements Call

16

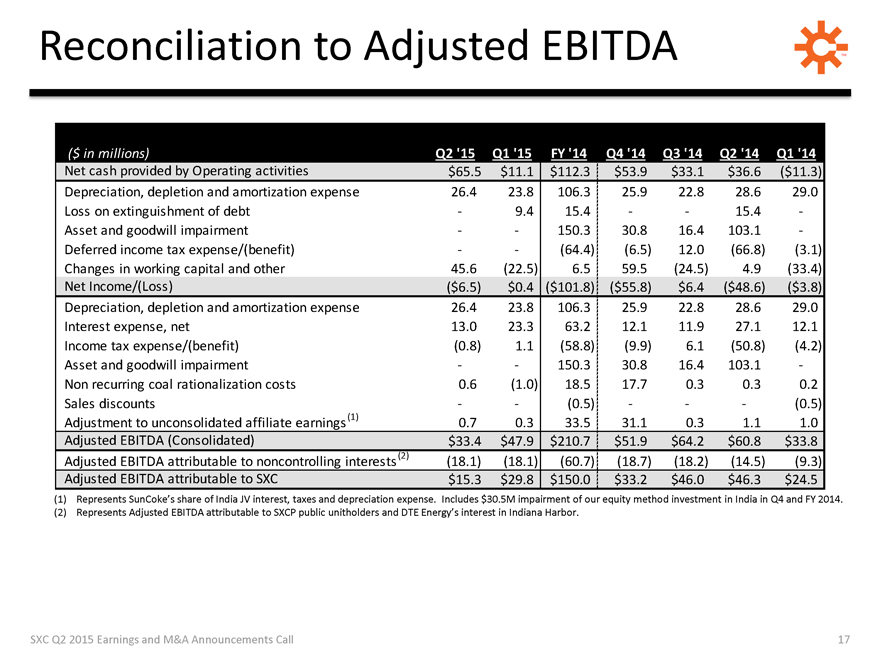

Reconciliation to Adjusted EBITDA

($ in millions)

Q2 ‘15 Q1 ‘15 FY ‘14 Q4 ‘14 Q3 ‘14 Q2 ‘14 Q1

‘14

Net cash provided by Operating activities

$65.5 $11.1 $112.3 $53.9

$33.1 $36.6 ($11.3)

Depreciation, depletion and amortization expense

26.4

23.8 106.3 25.9 22.8 28.6 29.0

Loss on extinguishment of debt

- 9.4 15.4 - -

15.4 -

Asset and goodwill impairment

- - 150.3 30.8 16.4 103.1 -

Deferred income tax expense/(benefit)

- - (64.4) (6.5) 12.0 (66.8) (3.1)

Changes in working capital and other

45.6 (22.5) 6.5 59.5 (24.5) 4.9 (33.4)

Net Income/(Loss)

($6.5) $0.4 ($101.8) ($55.8) $6.4 ($48.6) ($3.8)

Depreciation, depletion and amortization expense

26.4 23.8 106.3 25.9 22.8 28.6 29.0

Interest expense, net

13.0 23.3 63.2 12.1 11.9 27.1 12.1

Income tax expense/(benefit)

(0.8) 1.1 (58.8) (9.9) 6.1 (50.8) (4.2)

Asset and goodwill impairment

- - 150.3 30.8 16.4 103.1 -

Non recurring coal rationalization costs

0.6 (1.0) 18.5 17.7 0.3 0.3 0.2

Sales discounts

- - (0.5) - - - (0.5)

Adjustment to unconsolidated affiliate earnings (1)

0.7 0.3 33.5 31.1 0.3 1.1 1.0

Adjusted EBITDA (Consolidated)

$33.4 $47.9 $210.7 $51.9 $64.2 $60.8 $33.8

Adjusted EBITDA attributable to noncontrolling interests (2)

(18.1) (18.1) (60.7) (18.7)

(18.2) (14.5) (9.3)

Adjusted EBITDA attributable to SXC

$15.3 $29.8 $150.0

$33.2 $46.0 $46.3 $24.5

(1) Represents SunCoke’s share of India JV interest, taxes and depreciation expense. Includes $30.5M impairment of our equity method

investment in India in Q4 and FY 2014.

(2) Represents Adjusted EBITDA attributable to SXCP public unitholders and DTE Energy’s interest in Indiana Harbor.

SXC Q2 2015 Earnings and M&A Announcements Call

17

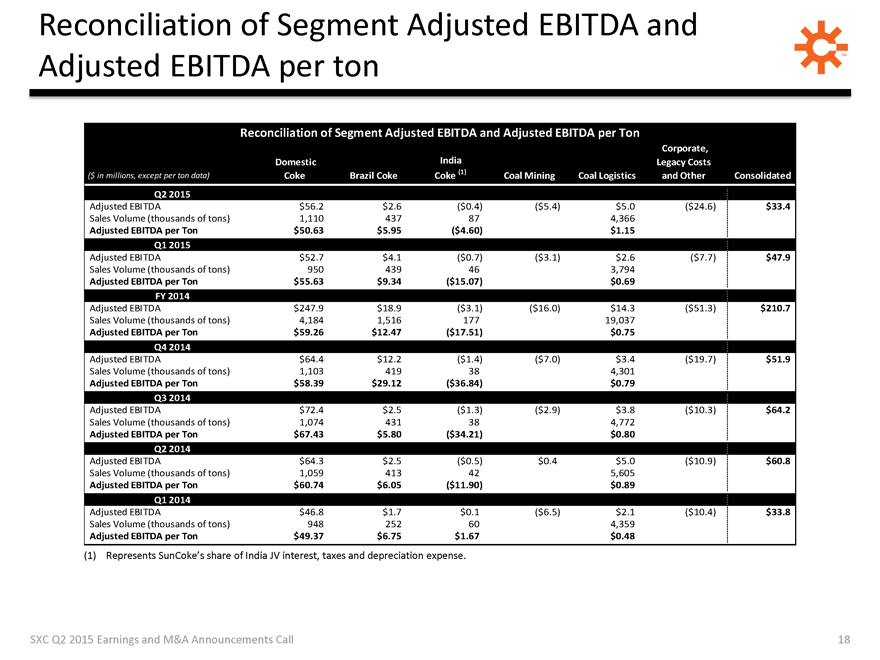

Reconciliation of Segment Adjusted EBITDA and Adjusted EBITDA per ton

Reconciliation of Segment Adjusted EBITDA and Adjusted EBITDA per Ton

($ in millions, except

per ton data)

Domestic Coke

Brazil Coke

India Coke (1)

Coal Mining

Coal Logistics

Corporate, Legacy Costs and Other

Consolidated

Q2 2015

Adjusted EBITDA

$56.2 $2.6 ($0.4) ($5.4) $5.0 ($24.6) $33.4

Sales Volume (thousands of tons)

1,110 437 87 4,366

Adjusted EBITDA per Ton

$50.63 $5.95 ($4.60) $1.15

Q1 2015

Adjusted EBITDA

$52.7 $4.1 ($0.7) ($3.1) $2.6 ($7.7) $47.9

Sales Volume (thousands of tons)

950 439 46 3,794

Adjusted EBITDA per Ton

$55.63 $9.34 ($15.07) $0.69

FY 2014

Adjusted EBITDA

$247.9 $18.9 ($3.1) ($16.0) $14.3 ($51.3) $210.7

Sales Volume (thousands of tons)

4,184 1,516 177 19,037

Adjusted EBITDA per Ton

$59.26 $12.47 ($17.51) $0.75

Q4 2014

Adjusted EBITDA

$64.4 $12.2 ($1.4) ($7.0) $3.4 ($19.7) $51.9

Sales Volume (thousands of tons)

1,103 419 38 4,301

Adjusted EBITDA per Ton

$58.39 $29.12 ($36.84) $0.79

Q3 2014

Adjusted EBITDA

$72.4 $2.5 ($1.3) ($2.9) $3.8 ($10.3) $64.2

Sales Volume (thousands of tons)

1,074 431 38 4,772

Adjusted EBITDA per Ton

$67.43 $5.80 ($34.21) $0.80

Q2 2014

Adjusted EBITDA

$64.3 $2.5 ($0.5) $0.4 $5.0 ($10.9) $60.8

Sales Volume (thousands of tons)

1,059 413 42 5,605

Adjusted EBITDA per Ton

$60.74 $6.05 ($11.90) $0.89

Q1 2014

Adjusted EBITDA

$46.8 $1.7 $0.1 ($6.5) $2.1 ($10.4) $33.8

Sales Volume (thousands of tons)

948 252 60 4,359

Adjusted EBITDA per Ton

$49.37 $6.75 $1.67 $0.48

(1) Represents SunCoke’s share of India JV interest, taxes and depreciation expense.

SXC

Q2 2015 Earnings and M&A Announcements Call

18

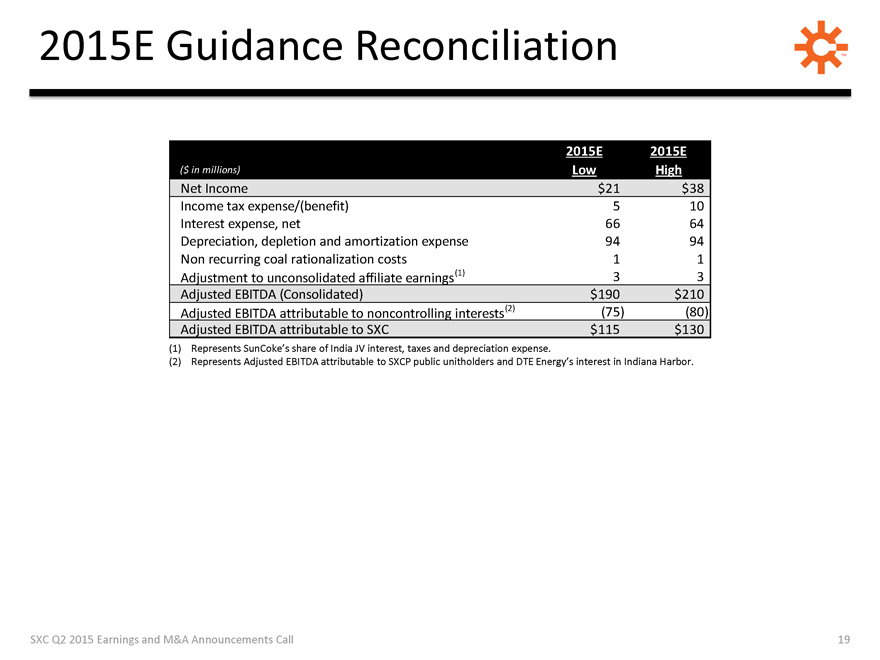

2015E Guidance Reconciliation

2015E

2015E

($ in millions)

Low

High

Net Income

$21

$38

Income tax expense/(benefit)

5

10

Interest expense, net

66

64

Depreciation, depletion and amortization expense

94

94

Non recurring coal rationalization costs

1

1

Adjustment to unconsolidated affiliate earnings(1)

3

3

Adjusted EBITDA (Consolidated)

$190

$210

Adjusted EBITDA attributable to noncontrolling interests(2)

(75)

(80)

Adjusted EBITDA attributable to SXC

$115

$130

(1) Represents SunCoke’s share of India JV interest, taxes and depreciation expense.

(2) Represents Adjusted EBITDA attributable to SXCP public unitholders and DTE Energy’s interest in Indiana Harbor.

SXC Q2 2015 Earnings and M&A Announcements Call

19

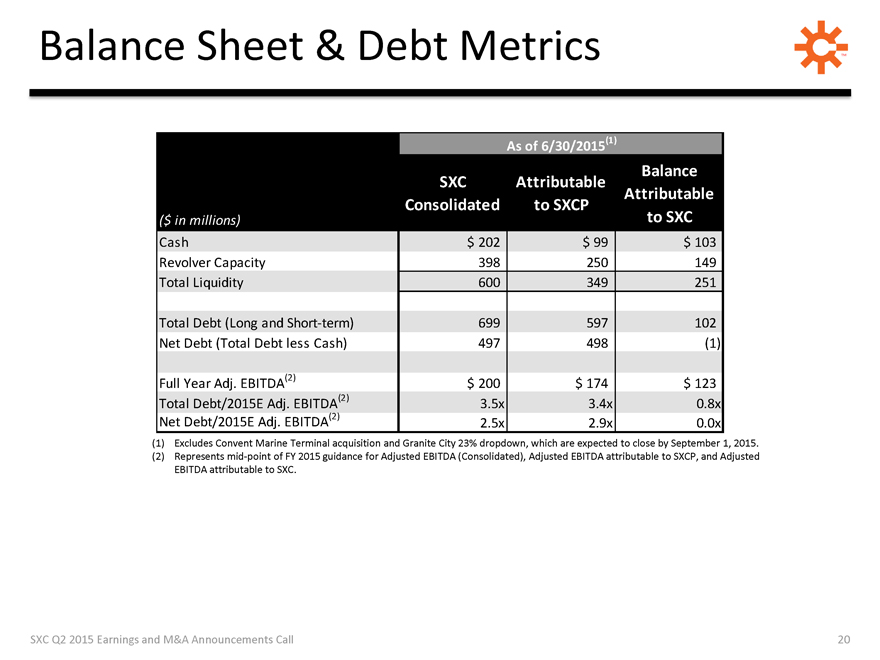

Balance Sheet & Debt Metrics

As of 6/30/2015(1)

($ in millions)

SXC Consolidated

Attributable to SXCP

Balance Attributable to SXC

Cash

$ 202

$ 99

$ 103

Revolver Capacity

398

250

149

Total Liquidity

600

349

251

Total Debt (Long and Short-term)

699

597

102

Net Debt (Total Debt less Cash)

497

498

(1)

Full Year Adj. EBITDA(2)

$ 200

$ 174

$ 123

Total Debt/2015E Adj. EBITDA(2)

3.5x

3.4x

0.8x

Net Debt/2015E Adj. EBITDA(2)

2.5x

2.9x

0.0x

(1) Excludes Convent Marine Terminal acquisition and Granite City 23%

dropdown, which are expected to close by September 1, 2015.

(2) Represents mid-point of FY 2015 guidance for Adjusted EBITDA (Consolidated), Adjusted EBITDA

attributable to SXCP, and Adjusted EBITDA attributable to SXC.

SXC Q2 2015 Earnings and M&A Announcements Call

20

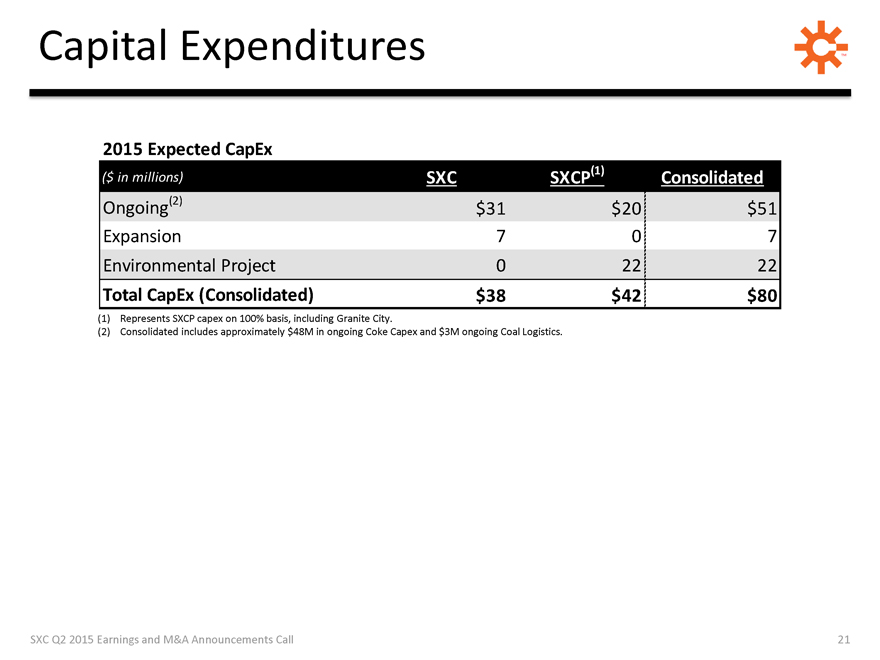

Capital Expenditures

2015

Expected CapEx

($ in millions)

SXC

SXCP(1)

Consolidated

Ongoing(2)

$31

$20

$51

Expansion

7

0

7

Environmental Project

0

22

22

Total CapEx (Consolidated)

$38

$42

$80

(1) Represents SXCP capex on 100% basis, including Granite City.

(2)

Consolidated includes approximately $48M in ongoing Coke Capex and $3M ongoing Coal Logistics.

SXC Q2 2015 Earnings and M&A Announcements Call

21

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- ROSEN, LEADING INVESTOR COUNSEL, Encourages Doximity, Inc. Investors to Secure Counsel Before Important Deadline in Securities Class Action – DOCS

- Quorum Announces Q4 and Year End 2023 Results

- Marex Group plc Announces Pricing of Initial Public Offering

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!