Form 8-K SunCoke Energy, Inc. For: Jan 28

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of Earliest Event Reported): January 28, 2016

SUNCOKE ENERGY, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 001-35243 | 90-0640593 | ||

| (State of Incorporation) | (Commission File Number) |

(IRS Employer Identification No.) |

| 1011 Warrenville Road, Suite 600 | ||

| Lisle, Illinois | 60532 | |

| (Address of principal executive offices) | (Zip code) |

Registrant’s telephone number, including area code: (630) 824-1000

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Item 2.02. Results of Operations and Financial Condition.

On January 28, 2016, SunCoke Energy, Inc. (the “Company”) issued a press release announcing its fourth quarter and full year financial results for 2015. A copy of this press release is attached as Exhibit 99.1 and is incorporated herein by reference.

Item 7.01. Regulation FD Disclosure.

As noted above, on January 28, 2016, the Company issued a press release announcing its financial results for its fourth quarter and full year financial results for 2015. Additional information concerning the Company’s financial results for the fourth quarter and full year of 2015 will be presented in a slide presentation to investors during a previously announced teleconference on January 28, 2016. A copy of the slide presentation is attached as Exhibit 99.2 and is incorporated herein by reference.

The information in this report, being furnished pursuant to Items 2.02, 7.01 and 9.01 of Form 8-K, shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that Section, and is not incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as expressly set forth by specific reference in such filing.

Safe Harbor Statement

Statements contained in the exhibit to this report that state the Company’s or management’s expectations or predictions of the future are forward-looking statements intended to be covered by the safe harbor provisions of the Securities Act of 1933 and the Securities Exchange Act of 1934. The Company’s actual results could differ materially from those projected in such forward-looking statements. Factors that could affect those results include those mentioned in the documents that the Company has filed with the Securities and Exchange Commission.

Item 9.01 Financial Statements and Exhibits.

(d) Exhibits

| Exhibit No. |

Description | |

| 99.1 | SunCoke Energy, Inc. Press Release, announcing fourth quarter and full year 2015 earnings (January 28, 2016). | |

| 99.2 | SunCoke Energy, Inc. Slide Presentation regarding fourth quarter and full year 2015 earnings (January 28, 2016). | |

SIGNATURES

Pursuant to the requirements of the Exchange Act, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| SUNCOKE ENERGY, INC. | ||

| By: | /s/ Fay West | |

| Fay West | ||

| Senior Vice President and Chief Financial Officer | ||

Date: January 28, 2016

EXHIBIT INDEX

| Exhibit No. |

Exhibit | |

| 99.1 | SunCoke Energy, Inc. Press Release, announcing fourth quarter and full year 2015 earnings (January 28, 2016). | |

| 99.2 | SunCoke Energy, Inc. Slide Presentation regarding fourth quarter and full year 2015 earnings (January 28, 2016). | |

Exhibit 99.1

Investors:

Kyle Bland: 630-824-1907

Media:

Steve Carlson: 630-824-1783

SUNCOKE ENERGY, INC. ANNOUNCES FOURTH QUARTER

AND FULL-YEAR 2015 RESULTS

| • | Net income attributable to shareholders in fourth quarter 2015 was $19.0 million, or $0.30 per share, up $84.5 million versus the prior year period primarily due to a debt extinguishment gain in the current period and the lapping of Coal Mining and India impairment charges recognized in fourth quarter 2014 |

| • | Adjusted EBITDA increased $2.4 million to $54.3 million in fourth quarter 2015, reflecting the benefit from the Convent Marine Terminal (“CMT”) acquisition offset largely by Indiana Harbor underperformance, the impact from Haverhill Chemicals and timing of coke sales |

| • | Full-year 2015 Consolidated Adjusted EBITDA of $185.8 million in line with our revised 2015 guidance range of $180 million to $190 million |

LISLE, Ill. (January 28, 2016) - SunCoke Energy, Inc. (NYSE: SXC) today reported fourth quarter net income attributable to SXC of $19.0 million, or $0.30 per share. Full-year 2015 net loss attributable to SXC was $22.0 million, or $0.34 per share, an improvement of $104.1 million versus the same prior year period primarily due to impairment charges on our Coal Mining and India Coke segments taken during the second and fourth quarters of 2014.

“While 2015 was a challenging year across the steel and coal industries, we achieved our revised financial guidance and remain confident in our underlying business model and the value we provide to each of our customers,” said Fritz Henderson, President, Chairman and Chief Executive Officer of SunCoke Energy, Inc. “In 2015, we expanded our Coal Logistics platform, implemented a more holistic approach to stabilizing Indiana Harbor, further streamlined our corporate overhead and executed our capital allocation strategy.”

Looking forward, we expect 2016 Consolidated Adjusted EBITDA to be between $210 million and $235 million. This outlook reflects our view for sustained performance in our Domestic Coke and Coal Logistics businesses coupled with the full-year benefit of the Convent acquisition and improvement at our Indiana Harbor facility.

Henderson continued, “We will continue to work tirelessly towards managing through the current market conditions and executing against our 2016 objectives.”

1

2015 CONSOLIDATED RESULTS(1)

| Three Months Ended December 31, |

Years Ended December 31, |

|||||||||||||||||||||||

| (Dollars in millions) |

2015 | 2014 | Increase/ (Decrease) |

2015 | 2014 | Increase/ (Decrease) |

||||||||||||||||||

| Revenues |

$ | 353.6 | $ | 395.0 | $ | (41.4 | ) | $ | 1,362.7 | $ | 1,503.8 | $ | (141.1 | ) | ||||||||||

| Operating income (loss) |

$ | 24.8 | $ | (21.6 | ) | $ | 46.4 | $ | 79.8 | $ | (62.4 | ) | $ | 142.2 | ||||||||||

| Adjusted EBITDA(2) |

$ | 54.3 | $ | 51.9 | $ | 2.4 | $ | 185.8 | $ | 210.7 | $ | (24.9 | ) | |||||||||||

| Net income (loss) attributable to SXC |

$ | 19.0 | $ | (65.5 | ) | $ | 84.5 | $ | (22.0 | ) | $ | (126.1 | ) | $ | 104.1 | |||||||||

| (1) | The current and prior year periods are not comparable due to the impact of Convent Marine Terminal, which was acquired on August 12, 2015. |

| (2) | See definition of Adjusted EBITDA and reconciliation elsewhere in this release. |

Total revenues from operations were $353.6 million and $1,362.7 million in fourth quarter and full-year 2015, respectively, a decrease of $41.4 million and $141.1 million, respectively, compared with the same prior year periods. Excluding Indiana Harbor, we continue to achieve contract maximums, but volumes in excess of maximums as well as spot sales were lower in 2015 as compared to the prior year periods. Additionally, these decreases in revenue reflect the pass-through of lower coal prices and lower coal-to-coke yields in our Domestic Coke business. These impacts were partly offset by additional revenue from Convent Marine Terminal, which was acquired in August 2015 and contributed revenues of $22.9 million and $28.6 million to the fourth quarter and full-year 2015, respectively.

Operating income was $24.8 million and $79.8 million in the fourth quarter and full-year 2015, respectively, compared to an operating loss of $21.6 million and $62.4 million in the same prior year periods, which included non-cash impairment charges of our coal mining business of $30.8 million and $150.3 million, respectively. Additionally, the current year periods benefited from lower severance charges as compared to the same prior year periods, which included charges related to our coal mining operations.

Adjusted EBITDA increased $2.4 million to $54.3 million in fourth quarter 2015, but decreased $24.9 million to $185.8 million in the full-year 2015. Both fourth quarter and full-year 2015 were favorably impacted by the contributions from CMT of $15.6 million and $21.0 million, respectively. Underperformance and lower cost recovery at Indiana Harbor as well as the impact of the reorganization of the Haverhill Chemicals LLC facility partly offset the contributions of CMT during the fourth quarter 2015 and more than offset CMT’s contribution to the full-year 2015.

Fourth quarter 2015 net income attributable to SXC was $19.0 million, or $0.30 per share, up from a loss of $65.5 million, or $0.98 per share, in the same prior year period. Full-year 2015 net loss attributable to SXC was $22.0 million, or $0.34 per share, versus $126.1 million, or $1.83 per share, for full-year 2014.

In the fourth quarter 2014 we recorded a non-cash impairment charge on our investment in VISA SunCoke, our Indian cokemaking joint venture, of $30.5 million, and an additional impairment charge of $19.4 million was recorded in third quarter 2015. Additionally, the prior year fourth quarter and full-year periods included non-cash impairment charges related to the coal business of $30.8 million, or $18.8 million, net of tax, and $150.3 million, or $92.2 million, net of tax, respectively.

2

The fourth quarter 2015 also benefited from $8.9 million of gains on debt extinguishment, offsetting losses on extinguishment of debt associated with the Granite City dropdown earlier in the year. The fourth quarter of 2015 also included higher income tax benefits of $16.0 million driven by a deduction related to the liquidation of a coal mining subsidiary for tax purposes.

3

FOURTH QUARTER 2015 SEGMENT RESULTS

Domestic Coke

Domestic Coke consists of cokemaking facilities and heat recovery operations at our Jewell, Indiana Harbor, Haverhill, Granite City and Middletown plants.

| Three Months Ended December 31, |

||||||||||||

| (Dollars in millions, except per ton amounts) |

2015 | 2014 | Increase/ (Decrease) |

|||||||||

| Revenues |

$ | 302.5 | $ | 360.4 | $ | (57.9 | ) | |||||

| Adjusted EBITDA(1) |

$ | 45.3 | $ | 64.4 | $ | (19.1 | ) | |||||

| Sales Volume (in thousands of tons) |

1,013 | 1,103 | (90 | ) | ||||||||

| Adjusted EBITDA per ton(2) |

$ | 44.72 | $ | 58.39 | $ | (13.67 | ) | |||||

| (1) | See definitions of Adjusted EBITDA and reconciliation elsewhere in this release. |

| (2) | Reflects Domestic Coke Adjusted EBITDA divided by Domestic Coke sales volumes. |

| • | Segment revenues were affected by the pass-through of lower coal prices as well as a decrease in volume of 90 thousand tons. |

| • | Adjusted EBITDA decreased $19.1 million to $45.3 million, reflecting underperformance and lower cost recovery at Indiana Harbor, which decreased Adjusted EBITDA by $10.1 million, as well as lower sales volumes at our other Domestic Coke facilities, which decreased Adjusted EBITDA $4.1 million, and the impact of the reorganization of the Haverhill Chemicals LLC facility, with whom we had a steam supply agreement. |

Coal Logistics

Coal Logistics consists of the coal handling and blending services operated by SXCP at CMT located on the Mississippi river in Louisiana, Lake Terminal in East Chicago, IN and Kanawha River Terminals, LLC, which has terminals along the Ohio, Big Sandy and Kanawha rivers in West Virginia and Kentucky. The current and prior year periods are not comparable due to the impact of CMT, which was acquired on August 12, 2015.

| Three Months Ended December 31, |

||||||||||||

| (Dollars in millions, except per ton amounts) |

2015 | 2014 | Increase/ (Decrease) |

|||||||||

| Revenues |

$ | 31.1 | $ | 8.1 | $ | 23.0 | ||||||

| Coal Logistics Adjusted EBITDA(1) |

$ | 20.4 | $ | 3.4 | $ | 17.0 | ||||||

| Coal tons handled (thousands of tons) |

5,555 | 4,301 | 1,254 | |||||||||

| Coal Logistics Adjusted EBITDA per ton(2) |

$ | 3.67 | $ | 0.79 | $ | 2.88 | ||||||

| (1) | See definitions of Adjusted EBITDA and reconciliation elsewhere in this release. |

| (2) | Reflects Coal Logistics Adjusted EBITDA divided by Coal Logistics tons handled. |

| • | Revenues were up $23.0 million, driven by a $22.9 million contribution from CMT. |

| • | Adjusted EBITDA was up $17.0 million, driven by a $15.6 million contribution from CMT. During the period, Convent handled 1,395 thousand tons of coal. |

4

Brazil Coke

Brazil Coke consists of a cokemaking facility in Vitória, Brazil, which we operate for an affiliate of ArcelorMittal. Brazil Coke earns operating and technology licensing fees based on production and recognizes a dividend on a preferred stock investment assuming certain minimum production levels are achieved.

| • | Segment Adjusted EBITDA remained largely flat at $12.3 million. |

5

India Coke

India Coke consists of our 49 percent interest in VISA SunCoke, a joint venture with VISA Steel. As a result of the continued deterioration of market factors, the Company recorded a $30.5 million non-cash impairment charge in the fourth quarter of 2014. During the third quarter of 2015, the Company impaired the remaining investment balance to zero and, consequently, suspended equity method accounting of the joint venture meaning it is no longer included in our consolidated financial statements. In accordance with GAAP, our share of future earnings of the joint venture will only be included in our results once the cumulative investment balance is no longer negative.

Coal Mining

Coal Mining consists of our metallurgical coal mining activities conducted in Virginia and West Virginia, currently mined by contractors. A majority of the metallurgical coal produced by our coal mining business is sold to our Jewell Coke facility for conversion into coke.

| • | Adjusted EBITDA was a loss of $5.5 million, an improvement of $1.5 million as compared to the same prior year period due to savings associated with the rationalization of our coal mining business and transition to our current contract mining model. |

Corporate and Other

Corporate and other expenses, including legacy costs, in fourth quarter 2015 were $18.2 million, down $1.5 million versus fourth quarter 2014 primarily due to lower black lung charges, partly offset by severance costs in the current year period related to a reduction in force at our corporate facility.

Interest Expense, Net

Net interest expense decreased $6.3 million to $5.8 million in fourth quarter 2015, primarily related to an $8.9 million gain on extinguishment of debt, partly offset by interest incurred on higher debt balances.

2016 OUTLOOK

Our 2016 guidance is as follows:

| • | Domestic coke production is expected to be approximately 4.1 million tons |

| • | Consolidated Adjusted EBITDA is expected to be between $210 million and $235 million |

| • | Adjusted EBITDA attributable to SXC is expected to be between $105 million and $124 million, reflecting the impact of public ownership in SXCP |

| • | Capital expenditures are projected to be approximately $45 million |

| • | Cash generated by operations is estimated to be between $150 million and $170 million |

| • | Cash taxes are projected to be between $4 million and $9 million |

RELATED COMMUNICATIONS

Today, we will host an investor conference call at 11:00 a.m. Eastern Time (10:00 a.m. Central Time). Investors may participate in this call by dialing 1-877-201-0168 in the U.S. or 1-647-788-4901 if outside the U.S., confirmation code 22719293. This conference call will be webcast live and archived for replay in the Investor Relations section of www.suncoke.com.

6

UPCOMING EVENTS

We plan to participate in the following investor conferences:

| • | Barclays Select Series 2016: MLP Corporate Access Day on March 1, 2016 in New York, NY |

| • | Morgan Stanley’s MLP/Diversified Natural Gas Conference on March 2, 2016 in New York, NY |

SUNCOKE ENERGY, INC.

SunCoke Energy, Inc. (NYSE: SXC) supplies high-quality coke to the integrated steel industry under long-term, take-or-pay contracts that pass through commodity and certain operating costs to customers. We utilize an innovative heat-recovery cokemaking technology that captures excess heat for steam or electrical power generation. We are the sponsor of SunCoke Energy Partners, L.P. (NYSE: SXCP), a publicly traded master limited partnership, holding a 2 percent general partner interest, 53 percent limited partnership interest and all of the incentive distribution rights. Our cokemaking facilities are located in Illinois, Indiana, Ohio, Virgina, Brazil and India. To learn more about SunCoke Energy, Inc., visit our website at www.suncoke.com.

DEFINITIONS

| • | Adjusted EBITDA represents earnings before interest, taxes, depreciation, depletion and amortization (“EBITDA”) adjusted for impairments, coal rationalization costs, sales discounts, Coal Logistics deferred revenue and interest, taxes, depreciation and amortization attributable to our equity method investment. Prior to the expiration of our nonconventional fuel tax credits in November 2013, Adjusted EBITDA included an add-back of sales discounts related to the sharing of these credits with customers. Any adjustments to these amounts subsequent to 2013 have been included in Adjusted EBITDA. Coal Logistics deferred revenue adjusts for differences between the timing of recognition of take-or-pay shortfalls into revenue for GAAP purposes versus the timing of payments from our customers. This adjustment aligns Adjusted EBITDA more closely with cash flow. Our Adjusted EBITDA also includes EBITDA attributable to our equity method investment. EBITDA and Adjusted EBITDA do not represent and should not be considered alternatives to net income or operating income under GAAP and may not be comparable to other similarly titled measures in other businesses. Management believes Adjusted EBITDA is an important measure of the operating performance and liquidity of the Company’s net assets and its ability to incur and service debt, fund capital expenditures and make distributions. Adjusted EBITDA provides useful information to investors because it highlights trends in our business that may not otherwise be apparent when relying solely on GAAP measures and because it eliminates items that have less bearing on our operating performance and liquidity. EBITDA and Adjusted EBITDA are not measures calculated in accordance with GAAP, and they should not be considered a substitute for net income, operating cash flow or any other measure of financial performance presented in accordance with GAAP. |

| • | Adjusted EBITDA attributable to SXC/SXCP represents consolidated Adjusted EBITDA less Adjusted EBITDA attributable to noncontrolling interests. |

| • | Legacy Costs include royalty revenues, costs associated with former mining employee-related liabilities prior to the implementation of our current contractor mining business. |

7

FORWARD-LOOKING STATEMENTS

Some of the statements included in this press release constitute “forward-looking statements” (as defined in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended). Forward-looking statements include all statements that are not historical facts and may be identified by the use of such words as “believe,” “expect,” “plan,” “project,” “intend,” “anticipate,” “estimate,” “predict,” “potential,” “continue,” “may,” “will,” “should” or the negative of these terms or similar expressions. Forward-looking statements are inherently uncertain and involve significant known and unknown risks and uncertainties (many of which are beyond the control of SXC) that could cause actual results to differ materially.

Such risks and uncertainties include, but are not limited to domestic and international economic, political, business, operational, competitive, regulatory and/or market factors affecting SXC, as well as uncertainties related to: pending or future litigation, legislation or regulatory actions; liability for remedial actions or assessments under existing or future environmental regulations; gains and losses related to acquisition, disposition or impairment of assets; recapitalizations; access to, and costs of, capital; the effects of changes in accounting rules applicable to SXC; and changes in tax, environmental and other laws and regulations applicable to SXC’s businesses.

Forward-looking statements are not guarantees of future performance, but are based upon the current knowledge, beliefs and expectations of SXC management, and upon assumptions by SXC concerning future conditions, any or all of which ultimately may prove to be inaccurate. The reader should not place undue reliance on these forward-looking statements, which speak only as of the date of this press release. SXC does not intend, and expressly disclaims any obligation, to update or alter its forward-looking statements (or associated cautionary language), whether as a result of new information, future events or otherwise after the date of this press release except as required by applicable law.

In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, SXC has included in its filings with the Securities and Exchange Commission cautionary language identifying important factors (but not necessarily all the important factors) that could cause actual results to differ materially from those expressed in any forward-looking statement made by SXC. For information concerning these factors, see SXC’s Securities and Exchange Commission filings such as its annual and quarterly reports and current reports on Form 8-K, copies of which are available free of charge on SXC’s website at www.suncoke.com. All forward-looking statements included in this press release are expressly qualified in their entirety by such cautionary statements. Unpredictable or unknown factors not discussed in this release also could have material adverse effects on forward-looking statements.

###

8

SunCoke Energy, Inc.

Consolidated Statements of Operations

(Unaudited)

| Three Months Ended December 31, |

Years Ended December 31, |

|||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| (Dollars and shares in millions, except per share amounts) |

||||||||||||||||

| Revenues |

||||||||||||||||

| Sales and other operating revenue |

$ | 343.6 | $ | 384.8 | $ | 1,351.3 | $ | 1,490.7 | ||||||||

| Other income, net |

10.0 | 10.2 | 11.4 | 13.1 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

353.6 | 395.0 | 1,362.7 | 1,503.8 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Costs and operating expenses |

||||||||||||||||

| Cost of products sold and operating expenses |

274.0 | 326.2 | 1,098.4 | 1,212.9 | ||||||||||||

| Selling, general and administrative expenses |

21.5 | 33.7 | 75.4 | 96.7 | ||||||||||||

| Depreciation and amortization expenses |

33.3 | 25.9 | 109.1 | 106.3 | ||||||||||||

| Asset and goodwill impairment |

— | 30.8 | — | 150.3 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total costs and operating expenses |

328.8 | 416.6 | 1,282.9 | 1,566.2 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income (loss) |

24.8 | (21.6 | ) | 79.8 | (62.4 | ) | ||||||||||

| Interest expense, net |

5.8 | 12.1 | 56.7 | 63.2 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) before income tax (benefit) expense and loss from equity method investment |

19.0 | (33.7 | ) | 23.1 | (125.6 | ) | ||||||||||

| Income tax benefit |

(13.9 | ) | (9.9 | ) | (8.8 | ) | (58.8 | ) | ||||||||

| Loss from equity method investment |

— | 32.0 | 21.6 | 35.0 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

32.9 | (55.8 | ) | 10.3 | (101.8 | ) | ||||||||||

| Less: Net income attributable to noncontrolling interests |

13.9 | 9.7 | 32.3 | 24.3 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) attributable to SunCoke Energy, Inc. |

$ | 19.0 | $ | (65.5 | ) | $ | (22.0 | ) | $ | (126.1 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) attributable to SunCoke Energy, Inc. per common share: |

||||||||||||||||

| Basic |

$ | 0.30 | $ | (0.98 | ) | $ | (0.34 | ) | $ | (1.83 | ) | |||||

| Diluted |

$ | 0.30 | $ | (0.98 | ) | $ | (0.34 | ) | $ | (1.83 | ) | |||||

| Weighted average number of common shares outstanding: |

||||||||||||||||

| Basic |

64.0 | 66.7 | 65.0 | 68.8 | ||||||||||||

| Diluted |

64.0 | 66.7 | 65.0 | 68.8 | ||||||||||||

9

SunCoke Energy, Inc.

Consolidated Balance Sheets

(Unaudited)

| December 31, | ||||||||

| 2015 | 2014 | |||||||

| (Dollars in millions, except par value amounts) |

||||||||

| Assets |

||||||||

| Cash and cash equivalents |

$ | 123.4 | $ | 139.0 | ||||

| Receivables |

65.2 | 78.2 | ||||||

| Inventories |

122.1 | 142.2 | ||||||

| Income tax receivable |

11.6 | 6.0 | ||||||

| Deferred income taxes |

— | — | ||||||

| Other current assets |

3.8 | 3.6 | ||||||

|

|

|

|

|

|||||

| Total current assets |

326.1 | 369.0 | ||||||

|

|

|

|

|

|||||

| Restricted cash |

18.2 | 0.5 | ||||||

| Investment in Brazilian cokemaking operations |

41.0 | 41.0 | ||||||

| Equity method investment in VISA SunCoke Limited |

— | 22.3 | ||||||

| Properties, plants and equipment, net |

1,593.4 | 1,480.0 | ||||||

| Goodwill |

71.1 | 11.6 | ||||||

| Other intangible assets, net |

190.2 | 10.4 | ||||||

| Deferred charges and other assets |

15.5 | 24.9 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 2,255.5 | $ | 1,959.7 | ||||

|

|

|

|

|

|||||

| Liabilities and Equity |

||||||||

| Accounts payable |

$ | 99.9 | $ | 121.3 | ||||

| Accrued liabilities |

45.8 | 71.3 | ||||||

| Current portion of long-term debt |

1.1 | — | ||||||

| Interest payable |

18.9 | 19.9 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

165.7 | 212.5 | ||||||

|

|

|

|

|

|||||

| Long-term debt |

997.7 | 633.5 | ||||||

| Accrual for black lung benefits |

44.7 | 40.1 | ||||||

| Retirement benefit liabilities |

31.3 | 33.6 | ||||||

| Deferred income taxes |

349.0 | 295.5 | ||||||

| Asset retirement obligations |

22.2 | 22.2 | ||||||

| Other deferred credits and liabilities |

22.1 | 16.9 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

1,632.7 | 1,254.3 | ||||||

|

|

|

|

|

|||||

| Equity |

||||||||

| Preferred stock, $0.01 par value. Authorized 50,000,000 shares; no issued shares at December 31, 2015 and 2014 |

— | — | ||||||

| Common stock, $0.01 par value. Authorized 300,000,000 shares; issued 71,489,448 shares and 71,251,529 shares at December 31, 2015 and 2014, respectively |

0.7 | 0.7 | ||||||

| Treasury stock, 7,477,657 shares and 4,977,115 shares at December 31, 2015 and 2014 respectively |

(140.7 | ) | (105.0 | ) | ||||

| Additional paid-in capital |

486.1 | 543.6 | ||||||

| Accumulated other comprehensive loss |

(19.8 | ) | (21.5 | ) | ||||

| Retained (deficit) earnings |

(36.4 | ) | 13.9 | |||||

|

|

|

|

|

|||||

| Total SunCoke Energy, Inc. stockholders’ equity |

289.9 | 431.7 | ||||||

| Noncontrolling interests |

332.9 | 273.7 | ||||||

|

|

|

|

|

|||||

| Total equity |

622.8 | 705.4 | ||||||

|

|

|

|

|

|||||

| Total liabilities and equity |

$ | 2,255.5 | $ | 1,959.7 | ||||

|

|

|

|

|

|||||

10

SunCoke Energy, Inc.

Consolidated Statements of Cash Flows

(Unaudited)

| Years Ended December 31, | ||||||||

| 2015 | 2014 | |||||||

| (Dollars in millions) | ||||||||

| Cash Flows from Operating Activities: |

||||||||

| Net income (loss) |

$ | 10.3 | $ | (101.8 | ) | |||

| Adjustments to reconcile net (loss) income to net cash provided by operating activities: |

||||||||

| Asset and goodwill impairment |

— | 150.3 | ||||||

| Loss from equity method investment |

21.6 | 35.0 | ||||||

| Depreciation and amortization expense |

109.1 | 106.3 | ||||||

| Deferred income tax benefit |

(5.6 | ) | (64.4 | ) | ||||

| Settlement loss and payments in excess of expense for pension plan |

13.1 | (7.5 | ) | |||||

| Gain on curtailment and payments in excess of expense for postretirement plan benefits |

(8.0 | ) | (0.6 | ) | ||||

| Share-based compensation expense |

7.2 | 9.8 | ||||||

| Excess tax benefit from share-based awards |

— | (0.3 | ) | |||||

| Loss on extinguishment of debt |

0.5 | 15.4 | ||||||

| Changes in working capital pertaining to operating activities (net of acquisitions): |

||||||||

| Receivables |

18.8 | 13.3 | ||||||

| Inventories |

23.2 | (12.6 | ) | |||||

| Accounts payable |

(17.9 | ) | (33.0 | ) | ||||

| Accrued liabilities |

(28.7 | ) | (8.0 | ) | ||||

| Interest payable |

(1.0 | ) | 1.7 | |||||

| Income taxes |

(5.6 | ) | 1.0 | |||||

| Accrual for black lung benefits |

6.0 | 11.5 | ||||||

| Other |

(1.9 | ) | (3.8 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

141.1 | 112.3 | ||||||

|

|

|

|

|

|||||

| Cash Flows from Investing Activities: |

||||||||

| Capital expenditures |

(75.8 | ) | (125.2 | ) | ||||

| Acquisition of businesses, net of cash received |

(191.7 | ) | — | |||||

| Restricted cash |

(17.7 | ) | — | |||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(285.2 | ) | (125.2 | ) | ||||

|

|

|

|

|

|||||

| Cash Flows from Financing Activities: |

||||||||

| Proceeds from issuance of common units of SunCoke Energy Partners, L.P., net of offering costs |

— | 90.5 | ||||||

| Proceeds from issuance of long-term debt |

260.8 | 268.1 | ||||||

| Repayment of long-term debt |

(248.1 | ) | (276.5 | ) | ||||

| Debt issuance costs |

(5.7 | ) | (5.8 | ) | ||||

| Proceeds from revolving facility |

292.4 | 40.0 | ||||||

| Repayment of revolving facility |

(50.0 | ) | (80.0 | ) | ||||

| Dividends paid |

(28.0 | ) | (3.8 | ) | ||||

| Cash distributions to noncontrolling interests |

(43.3 | ) | (32.3 | ) | ||||

| Shares repurchased |

(35.7 | ) | (85.1 | ) | ||||

| SunCoke Energy Partners, L.P. units repurchased |

(12.8 | ) | — | |||||

| Proceeds from exercise of stock options |

(1.1 | ) | 2.9 | |||||

| Excess tax benefit from share-based awards |

— | 0.3 | ||||||

|

|

|

|

|

|||||

| Net cash provided by (used in) financing activities |

128.5 | (81.7 | ) | |||||

|

|

|

|

|

|||||

| Net (decrease) increase in cash and cash equivalents |

(15.6 | ) | (94.6 | ) | ||||

| Cash and cash equivalents at beginning of year |

139.0 | 233.6 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of year |

$ | 123.4 | $ | 139.0 | ||||

|

|

|

|

|

|||||

| Supplemental Disclosure of Cash Flow Information |

||||||||

| Interest paid |

$ | 58.1 | $ | 45.8 | ||||

| Income taxes paid, net of refunds of $1.5 million and $4.6 million in 2015 and 2014, respectively |

$ | 2.4 | $ | 9.1 | ||||

11

SunCoke Energy, Inc.

Segment Financial and Operating Data

(unaudited)

The following tables set forth financial and operating data for the three and twelve months ended December 31, 2015 and 2014:

| Three Months Ended December 31, |

Years Ended December 31, |

|||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| (Dollars in millions) | ||||||||||||||||

| Sales and other operating revenues: |

||||||||||||||||

| Domestic Coke |

$ | 302.5 | $ | 360.4 | $ | 1,243.6 | $ | 1,388.3 | ||||||||

| Brazil Coke |

7.6 | 9.8 | 34.0 | 37.0 | ||||||||||||

| Coal Logistics(1) |

31.1 | 8.1 | 60.8 | 36.2 | ||||||||||||

| Coal Logistics intersegment sales |

5.1 | 5.2 | 20.4 | 18.8 | ||||||||||||

| Coal Mining |

2.4 | 6.5 | 12.9 | 29.2 | ||||||||||||

| Coal Mining intersegment sales |

26.7 | 29.7 | 101.0 | 136.0 | ||||||||||||

| Elimination of intersegment sales |

(31.8 | ) | (34.9 | ) | (121.4 | ) | (154.8 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total sales and other operating revenue |

$ | 343.6 | $ | 384.8 | $ | 1,351.3 | $ | 1,490.7 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA(2) |

||||||||||||||||

| Domestic Coke |

$ | 45.3 | $ | 64.4 | $ | 210.1 | $ | 247.9 | ||||||||

| Brazil Coke |

12.3 | 12.2 | 22.4 | 18.9 | ||||||||||||

| India Coke |

— | (1.4 | ) | (1.9 | ) | (3.1 | ) | |||||||||

| Coal Logistics(1) |

20.4 | 3.4 | 38.4 | 14.3 | ||||||||||||

| Coal Mining |

(5.5 | ) | (7.0 | ) | (18.9 | ) | (16.0 | ) | ||||||||

| Corporate and Other, including legacy costs, net(3) |

(18.2 | ) | (19.7 | ) | (64.3 | ) | (51.3 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA(1) |

$ | 54.3 | $ | 51.9 | $ | 185.8 | $ | 210.7 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Coke Operating Data: |

||||||||||||||||

| Domestic Coke capacity utilization (%) |

96 | 101 | 97 | 98 | ||||||||||||

| Domestic Coke production volumes (thousands of tons) |

1,028 | 1,083 | 4,122 | 4,175 | ||||||||||||

| Domestic Coke sales volumes (thousands of tons) |

1,013 | 1,103 | 4,115 | 4,184 | ||||||||||||

| Domestic Coke Adjusted EBITDA per ton(4) |

$ | 44.72 | $ | 58.39 | $ | 51.06 | $ | 59.25 | ||||||||

| Brazilian Coke production—operated facility (thousands of tons) |

436 | 419 | 1,760 | 1,516 | ||||||||||||

| Coal Logistics Operating Data:(1) |

||||||||||||||||

| Tons handled (thousands of tons) |

5,555 | 4,301 | 18,864 | 19,037 | ||||||||||||

| Coal Logistics Adjusted EBITDA per ton handled(5) |

$ | 3.67 | $ | 0.79 | $ | 2.04 | $ | 0.75 | ||||||||

| (1) | The current and prior year periods are not comparable due to the impact of CMT, which was acquired on August 12, 2015. |

| (2) | See definition of Adjusted EBITDA and reconciliation to GAAP elsewhere in this release. |

| (3) | Legacy costs, net include costs associated with former mining employee-related liabilities prior to the implementation of our current contractor mining business net of certain royalty revenues. See details of these legacy items below. |

| (4) | Reflects Domestic Coke Adjusted EBITDA divided by Domestic Coke sales volumes. |

| (5) | Reflects Coal Logistics Adjusted EBITDA divided by Coal Logistics tons handled. |

12

| Three Months Ended December 31, |

Years Ended December 31, |

|||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| (Dollars in millions) | ||||||||||||||||

| Black lung (charges) benefit |

$ | (6.5 | ) | $ | (12.8 | ) | $ | (9.8 | ) | $ | (14.3 | ) | ||||

| Postretirement benefit plan (expense) benefit |

(0.1 | ) | 2.9 | 3.6 | 3.7 | |||||||||||

| Defined benefit plan expense |

— | — | (13.1 | ) | (0.2 | ) | ||||||||||

| Workers compensation expense |

(0.7 | ) | (1.3 | ) | (2.3 | ) | (4.6 | ) | ||||||||

| Other |

— | 0.1 | (0.4 | ) | 0.7 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total legacy costs, net |

$ | (7.3 | ) | $ | (11.1 | ) | $ | (22.0 | ) | $ | (14.7 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

13

SunCoke Energy, Inc.

Reconciliations of Non-GAAP Information

Adjusted EBITDA to Net Income

| Three Months Ended December 31, |

Years Ended December 31, |

|||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| (Dollars in millions) | ||||||||||||||||

| Adjusted EBITDA attributable to SunCoke Energy, Inc. |

$ | 29.4 | $ | 33.2 | $ | 104.6 | $ | 150.0 | ||||||||

| Add: Adjusted EBITDA attributable to noncontrolling interests (1) |

24.9 | 18.7 | 81.2 | 60.7 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA |

$ | 54.3 | $ | 51.9 | $ | 185.8 | $ | 210.7 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Subtract: |

||||||||||||||||

| Adjustment to unconsolidated affiliate earnings (2) |

— | 31.1 | 20.8 | 33.5 | ||||||||||||

| Nonrecurring coal rationalization costs (3) |

0.2 | 17.7 | 0.6 | 18.5 | ||||||||||||

| Depreciation and amortization expense |

33.3 | 25.9 | 109.1 | 106.3 | ||||||||||||

| Interest expense, net |

5.8 | 12.1 | 56.7 | 63.2 | ||||||||||||

| Income tax benefit |

(13.9 | ) | (9.9 | ) | (8.8 | ) | (58.8 | ) | ||||||||

| Sales discounts provided to customers due to sharing of nonconventional fuel tax credits(4) |

— | — | — | (0.5 | ) | |||||||||||

| Asset and goodwill impairment |

— | 30.8 | — | 150.3 | ||||||||||||

| Coal Logistics deferred revenue(5) |

(4.0 | ) | — | (2.9 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 32.9 | $ | (55.8 | ) | $ | 10.3 | $ | (101.8 | ) | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Add |

||||||||||||||||

| Asset and goodwill impairment |

— | 30.8 | — | 150.3 | ||||||||||||

| Depreciation and amortization |

33.3 | 25.9 | 109.1 | 106.3 | ||||||||||||

| Deferred income tax benefit |

(12.5 | ) | (6.4 | ) | (5.6 | ) | (64.4 | ) | ||||||||

| (Gain) loss on extinguishment of debt |

(8.9 | ) | — | 0.5 | 15.4 | |||||||||||

| Changes in working capital and other |

13.3 | 59.4 | 26.8 | 6.5 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net cash provided by operating activities |

$ | 58.1 | $ | 53.9 | $ | 141.1 | $ | 112.3 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Reflects non-controlling interest in Indiana Harbor and the portion of SXCP owned by public unitholders. |

| (2) | Reflects share of interest, taxes, impairment, depreciation and amortization related to VISA SunCoke. |

| (3) | Nonrecurring coal rationalization costs include employee severance, contract termination costs and other one-time costs to idle mines incurred during the execution of our coal rationalization plan. |

| (4) | At December 31, 2013, we had $13.6 million accrued related to sales discounts to be paid to our customer at our Granite City facility. During the first quarter of 2014, we settled this obligation for $13.1 million which resulted in a gain of $0.5 million. The gain was recorded in sales and other operating revenue on our Combined and Consolidated Statement of Income. |

| (5) | Coal Logistics deferred revenue adjusts for differences between the timing of recognition of take-or-pay shortfalls into revenue for GAAP purposes versus the timing of payments from our customers. This adjustment aligns Adjusted EBITDA more closely with cash flow. |

14

SunCoke Energy, Inc

Reconciliation of Non-GAAP Information

Estimated 2016 Consolidated Adjusted EBITDA to Estimated Net Loss

and Net Cash Provided by Operating Activities

| 2016 | ||||||||

| Low | High | |||||||

| Net Cash Provided by Operating activities |

$ | 150 | $ | 170 | ||||

| Less: |

||||||||

| Depreciation and amortization expense |

104 | 104 | ||||||

| Changes in working capital and other |

10 | 12 | ||||||

|

|

|

|

|

|||||

| Net Income |

$ | 36 | $ | 54 | ||||

|

|

|

|

|

|||||

| Add: |

||||||||

| Depreciation and amortization expense |

104 | 104 | ||||||

| Interest expense,net |

62 | 58 | ||||||

| Income tax expense |

3 | 14 | ||||||

| Non recurring coal rationalization costs |

5 | 5 | ||||||

|

|

|

|

|

|||||

| Adjusted EBITDA (Consolidated) |

$ | 210 | $ | 235 | ||||

|

|

|

|

|

|||||

| Adjusted EBITDA attributable to noncontrolling interest(1) |

(105 | ) | (111 | ) | ||||

|

|

|

|

|

|||||

| Adjusted EBITDA attributable to SXC |

$ | 105 | $ | 124 | ||||

|

|

|

|

|

|||||

| (1) | Represents Adjusted EBITDA attributable to DTE Energy’s interest in Indiana Harbor, as well as to SXCP public unitholders. Adjusted EBITDA attributable to SXCP includes a priority income allocation in an amount equal to the incentive distribution rights allocated 100% to the general partner. |

15

Exhibit 99.2

SunCoke Energy, Inc. Q4 2015 Earnings Conference call January 28, 2016 sunCoke Energytm

This slide presentation should be reviewed in conjunction with the Fourth Quarter 2015 earnings release of SunCoke Energy, Inc. (SXC) and conference call held on January 28, 2016 at 11:00 a.m. ET. Some of the information included in this presentation constitutes “forward-looking statements” as defined in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. All statements in this presentation that express opinions, expectations, beliefs, plans, objectives, assumptions or projections with respect to anticipated future performance of SXC or SunCoke Energy Partners, L.P. (SXCP), in contrast with statements of historical facts, are forward-looking statements. Such forward-looking statements are based on management’s beliefs and assumptions and on information currently available. Forward-looking statements include information concerning possible or assumed future results of operations, business strategies, financing plans, competitive position, potential growth opportunities, potential operating performance improvements, the effects of competition and the effects of future legislation or regulations. Forward-looking statements include all statements that are not historical facts and may be identified by the use of forward-looking terminology such as the words “believe,” “expect,” “plan,” “intend,” “anticipate,” “estimate,” “predict,” “potential,” “continue,” “may,” “will,” “should” or the negative of these terms or similar expressions. Although management believes that its plans, intentions and expectations reflected in or suggested by the forward-looking statements made in this presentation are reasonable, no assurance can be given that these plans, intentions or expectations will be achieved when anticipated or at all. Moreover, such statements are subject to a number of assumptions, risks and uncertainties. Many of these risks are beyond the control of SXC and SXCP, and may cause actual results to differ materially from those implied or expressed by the forward-looking statements. Each of SXC and SXCP has included in its filings with the Securities and Exchange Commission cautionary language identifying important factors (but not necessarily all the important factors) that could cause actual results to differ materially from those expressed in any forward-looking statement. For more information concerning these factors, see the Securities and Exchange Commission filings of SXC and SXCP. All forward-looking statements included in this presentation are expressly qualified in their entirety by such cautionary statements. Although forward-looking statements are based on current beliefs and expectations, caution should be taken not to place undue reliance on any such forward-looking statements because such statements speak only as of the date hereof. SXC and SXCP do not have any intention or obligation to update publicly any forward-looking statement (or its associated cautionary language) whether as a result of new information or future events or after the date of this presentation, except as required by applicable law. This presentation includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. Reconciliations of non-GAAP financial measures to GAAP financial measures are provided in the Appendix at the end of the presentation. Investors are urged to consider carefully the comparable GAAP measures and the reconciliations to those measures provided in the Appendix. SXC Q4 2015 Earnings Call 1

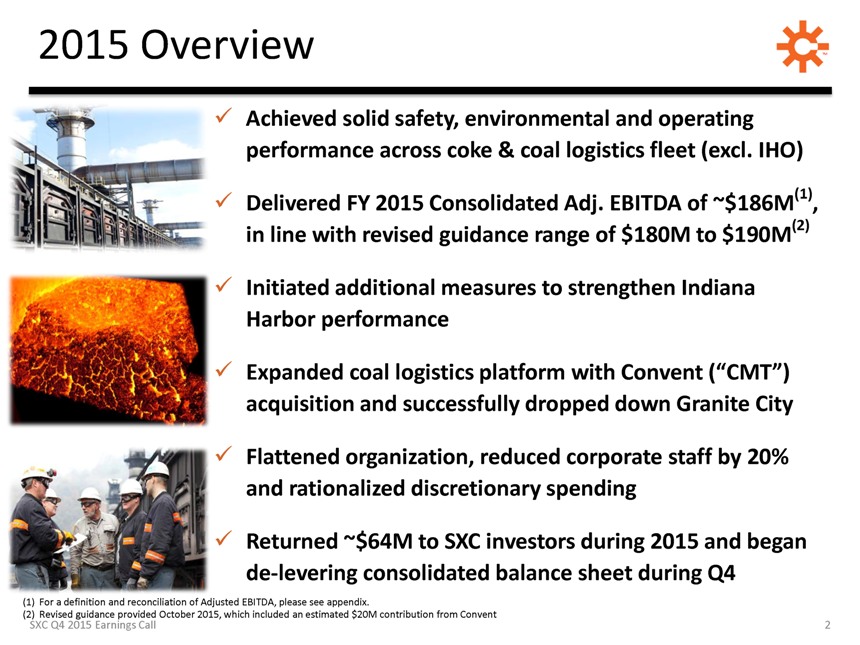

Achieved solid safety, environmental and operating performance across coke & coal logistics fleet (excl. IHO) Delivered FY 2015 Consolidated Adj. EBITDA of ~$186M (1) , in line with revised guidance range of $180M to $190M (2) Initiated additional measures to strengthen Indiana Harbor performance Expanded coal logistics platform with Convent (“CMT”) acquisition and successfully dropped down Granite City Flattened organization, reduced corporate staff by 20% and rationalized discretionary spending Returned ~$64M to SXC investors during 2015 and began de-levering consolidated balance sheet during Q4 (1) For a definition and reconciliation of Adjusted EBITDA, please see appendix. (2) Revised guidance provided October 2015, which included an estimated $20M contribution from Convent SXC Q4 2015 Earnings Call 2

Q4 and Full Year 2015 Overview TM Q4’15 vs. ($ in millions, except volumes) Q4’15 Q4’14 Q4’14 Domestic Coke Sales Volumes 1,013 1,103 (90) Coal Logistics Volumes(2) 5,555 4,301 1,254 Coke Adj. EBITDA(3) $57.6 $75.2 ($17.6) Coal Logistics Adj. EBITDA $20.4 $3.4 $17.0 Coal Mining Adj. EBITDA ($5.5) ($7.0) $1.5 Corporate and Other, including Legacy Costs ($18.2) ($19.7) $1.5 Adjusted EBITDA (Consolidated)(1) $54.3 $51.9 $2.4 Consolidated Adj. EBITDA(1) up $2.4M vs. Q4 ‘14 primarily due to $15.6M benefit of Convent acquisition Largely offset by IHO underperformance and lower coke sales FY Consolidated Adj. EBITDA of ~$186M(1) In-line with guidance of $180M – $190M (4) , including $21M benefit from Convent Decrease vs. 2014 largely due to IHO underperformance, lower domestic coke results and higher Legacy Costs Q4 ‘15 EPS of $0.30 includes gain on debt extinguishment and income tax benefit For a definition and reconciliation of Adjusted EBITDA, please see appendix. Coal Logistics volumes during Q4 2015 include volumes from Convent Marine Terminal. Coke Adjusted EBITDA includes Domestic Coke, Brazil Coke and India Coke segments. Revised guidance provided October 2015, which included an estimated $20M contribution from Convent SXC Q4 2015 Earnings Call 3

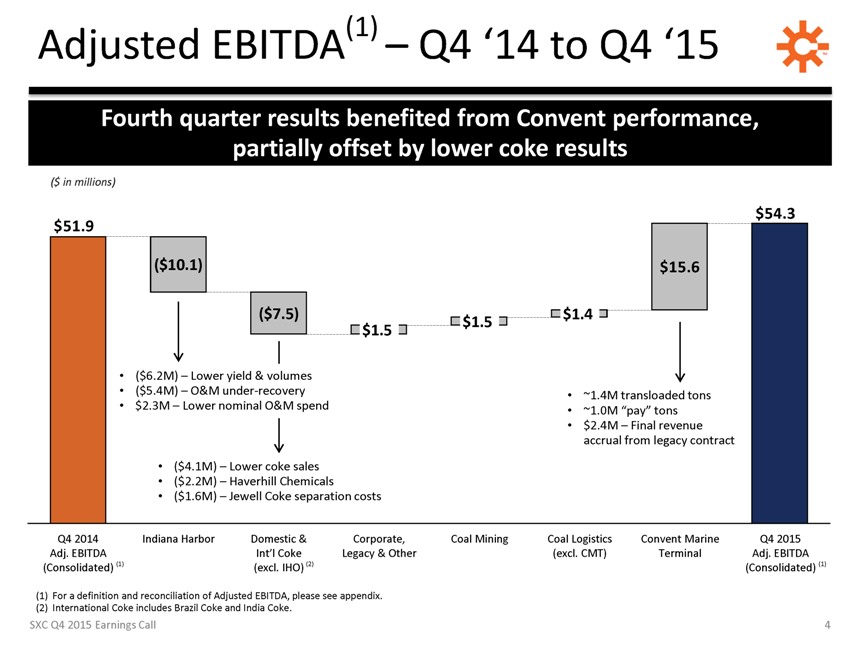

Adjusted EBITDA(1) – Q4 ‘14 to Q4 ‘15 TM • ($6.2M) – Lower yield & volumes • ($5.4M) – O&M under-recovery • ~1.4M transloaded tons • $2.3M – Lower nominal O&M spend • ~1.0M “pay” tons • $2.4M – Final revenue accrual from legacy contract • ($ 4.1M) – Lower coke sales • ($ 2.2M) – Haverhill Chemicals • ($ 1.6M) – Jewell Coke separation costs Q4 2014 Indiana Harbor Domestic & Corporate, Coal Mining Coal Logistics Convent Marine Q4 2015 Adj. EBITDA Int’l Coke Legacy & Other (excl. CMT) Terminal Adj. EBITDA (Consolidated) (1) (excl. IHO) (2) (Consolidated) (1) For a definition and reconciliation of Adjusted EBITDA, please see appendix. International Coke includes Brazil Coke and India Coke. SXC Q4 2015 Earnings Call 4

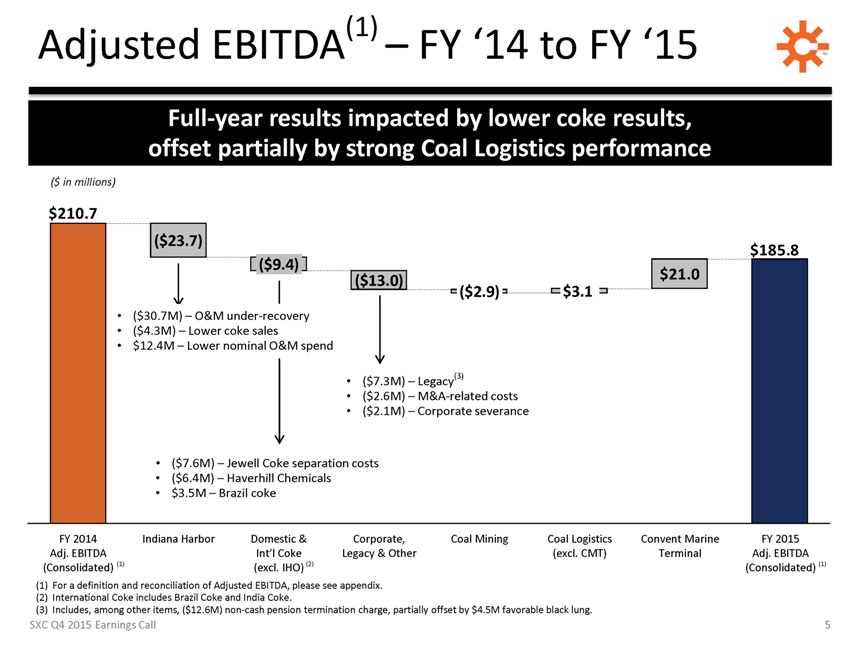

Adjusted EBITDA(1) – FY ‘14 to FY ‘15 TM Full-year results impacted by lower coke results, offset partially by strong Coal Logistics performance ($ in millions) $210.7 • ($30.7M) – O&M under-recovery • ($4.3M) – Lower coke sales • $12.4M – Lower nominal O&M spend • ($7.3M) – Legacy(3) • ($2.6M) – M&A-related costs • ($2.1M) – Corporate severance • ($7.6M) – Jewell Coke separation costs • ($6.4M) – Haverhill Chemicals • $3.5M – Brazil coke FY 2014 Indiana Harbor Domestic & Corporate, Coal Mining Coal Logistics Convent Marine FY 2015 Adj. EBITDA Int’l Coke Legacy & Other (excl. CMT) Terminal Adj. EBITDA (Consolidated) (1) (excl. IHO) (2) (Consolidated) (1) For a definition and reconciliation of Adjusted EBITDA, please see appendix. International Coke includes Brazil Coke and India Coke. Includes, among other items, ($12.6M) non-cash pension termination charge, partially offset by $4.5M favorable black lung. SXC Q4 2015 Earnings Call 5

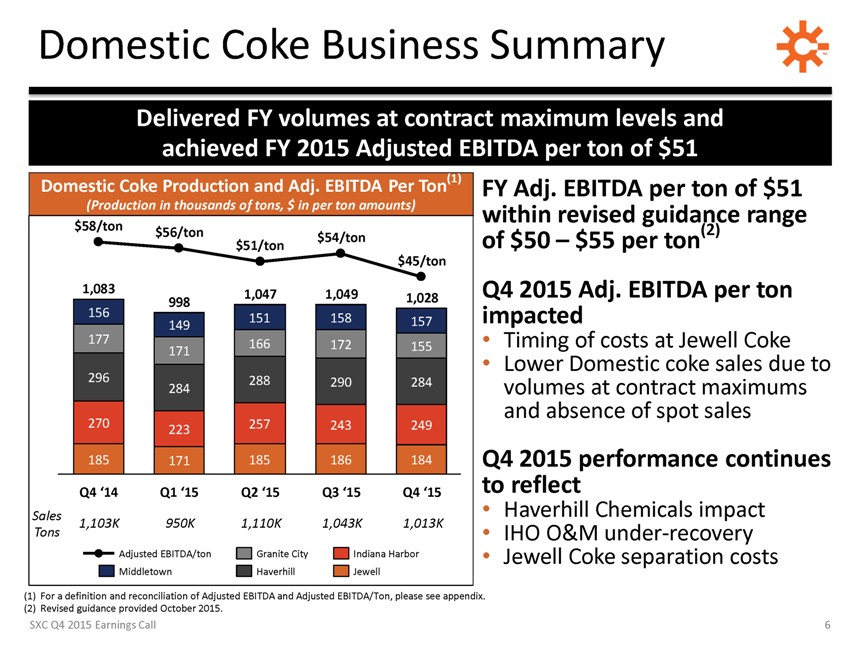

Domestic Coke Business Summary TM For a definition and reconciliation of Adjusted EBITDA and Adjusted EBITDA/Ton, please see appendix. Revised guidance provided October 2015. SXC Q4 2015 Earnings Call 6

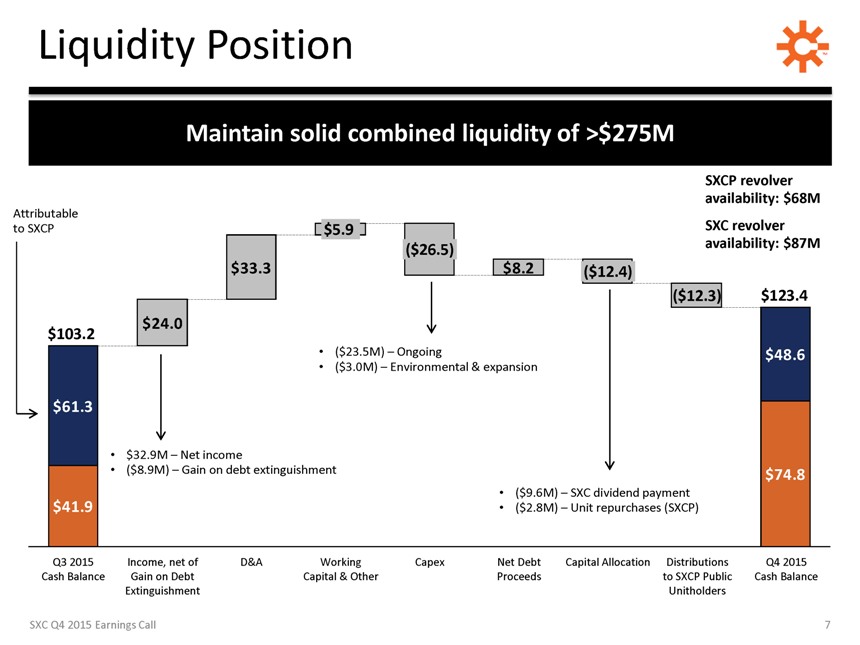

• ($ 9.6M) – SXC dividend payment $ 41.9 • ($ 2.8M) – Unit repurchases (SXCP) Q3 2015 Income, net of D&A Working Capex Net Debt Capital Allocation Distributions Q4 2015 Cash Balance Gain on Debt Capital & Other Proceeds to SXCP Public Cash Balance Extinguishment Unitholders SXC Q4 2015 Earnings Call 7

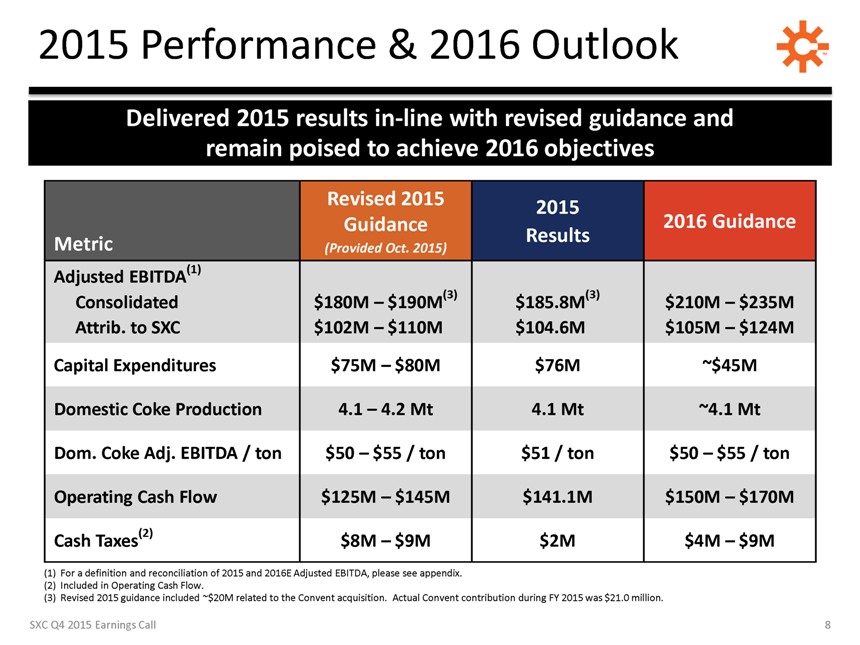

Delivered 2015 results in-line with revised guidance and remain poised to achieve 2016 objectives Revised 2015 2015 Guidance 2016 Guidance Metric (Provided Oct. 2015) Results Adjusted EBITDA (1) Consolidated $180M – $190M (3) $185.8M (3) $210M – $235M Attrib. to SXC $102M – $110M (1) $104.6M (1) $105M – $124M Capital Expenditures $75M – $80M $76M ~$45M Domestic Coke Production 4.1 – 4.2 Mt 4.1 Mt ~4.1 Mt Dom. Coke Adj. EBITDA / ton $50 – $55 / ton $51 / ton $50 – $55 / ton Operating Cash Flow $125M – $145M $141.1M $150M – $170M Cash Taxes (2) $8M – $9M $2M $4M – $9M For a definition and reconciliation of 2015 and 2016E Adjusted EBITDA, please see appendix. Included in Operating Cash Flow. Revised 2015 guidance included ~$20M related to the Convent acquisition. Actual Convent contribution during FY 2015 was $21.0 million. SXC Q4 2015 Earnings Call 8

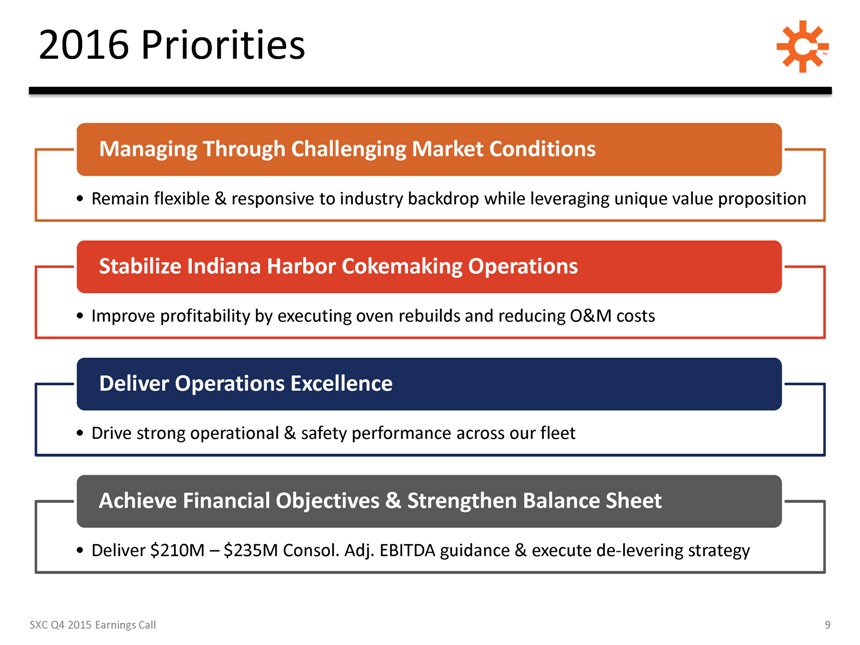

Managing Through Challenging Market Conditions • Remain flexible & responsive to industry backdrop while leveraging unique value proposition Stabilize Indiana Harbor Cokemaking Operations • Improve profitability by executing oven rebuilds and reducing O&M costs Deliver Operations Excellence • Drive strong operational & safety performance across our fleet Achieve Financial Objectives & Strengthen Balance Sheet • Deliver $210M – $235M Consol. Adj. EBITDA guidance & execute de-levering strategy SXC Q4 2015 Earnings Call 9

QUESTIONS SXC Q4 2015 Earnings Call 10

Investor Relations 630-824-1907 www.suncoke.com

APPENDIX SXC Q4 2015 Earnings Call 12

Adjusted EBITDA represents earnings before interest, taxes, depreciation, depletion and amortization (“EBITDA”) adjusted for impairments, coal rationalization costs, sales discounts, Coal Logistics deferred revenue and interest, taxes, depreciation and amortization attributable to our equity method investment. Prior to the expiration of our nonconventional fuel tax credits in November 2013, Adjusted EBITDA included an add-back of sales discounts related to the sharing of these credits with customers. Any adjustments to these amounts subsequent to 2013 have been included in Adjusted EBITDA. Coal Logistics deferred revenue adjusts for differences between the timing of recognition of take-or-pay shortfalls into revenue for GAAP purposes versus the timing of payments from our customers. This adjustment aligns Adjusted EBITDA more closely with cash flow. Our Adjusted EBITDA also includes EBITDA attributable to our equity method investment. EBITDA and Adjusted EBITDA do not represent and should not be considered alternatives to net income or operating income under GAAP and may not be comparable to other similarly titled measures in other businesses. Management believes Adjusted EBITDA is an important measure of the operating performance and liquidity of the Company’s net assets and its ability to incur and service debt, fund capital expenditures and make distributions. Adjusted EBITDA provides useful information to investors because it highlights trends in our business that may not otherwise be apparent when relying solely on GAAP measures and because it eliminates items that have less bearing on our operating performance and liquidity. EBITDA and Adjusted EBITDA are not measures calculated in accordance with GAAP, and they should not be considered a substitute for net income, operating cash flow or any other measure of financial performance presented in accordance with GAAP. EBITDA represents earnings before interest, taxes, depreciation, depletion and amortization. Adjusted EBITDA attributable to SXC/SXCP represents Adjusted EBITDA less Adjusted EBITDA attributable to noncontrolling interests. Adjusted EBITDA/Ton represents Adjusted EBITDA divided by tons sold/handled. Non recurring Coal Rationalization Costs include employee severance, contract termination costs and other one-time costs to idle mines incurred during the execution of our coal rationalization plan. Legacy Costs include royalty revenues, costs associated with former mining employee-related liabilities prior to the implementation of our current contractor mining business. SXC Q4 2015 Earnings Call 13

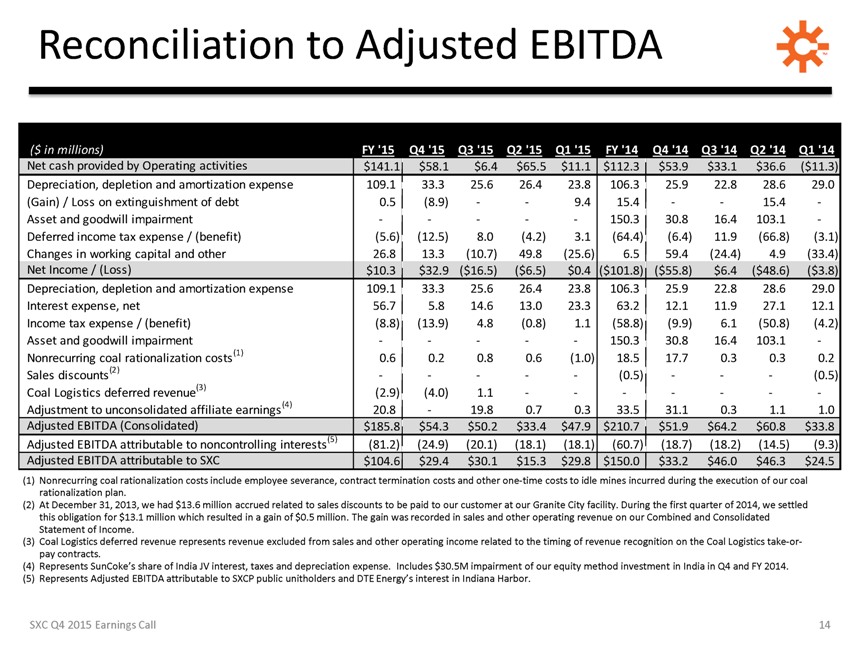

Reconciliation to Adjusted EBITDA TM ($ in millions) FY ‘15 Q4 ‘15 Q3 ‘15 Q2 ‘15 Q1 ‘15 FY ‘14 Q4 ‘14 Q3 ‘14 Q2 ‘14 Q1 ‘14 Net cash provided by Operating activities $141.1 $58.1 $6.4 $65.5 $11.1 $ 112.3 $53.9 $33.1 $36.6 ($11.3) Depreciation, depletion and amortization expense 109.1 33.3 25.6 26.4 23.8 106.3 25.9 22.8 28.6 29.0 (Gain) / Loss on extinguishment of debt 0.5 (8.9) — 9.4 15.4 — 15.4—Asset and goodwill impairment — —— 150.3 30.8 16.4 103.1—Deferred income tax expense / (benefit) (5.6) (12.5) 8.0 (4.2) 3.1 (64.4) (6.4) 11.9 (66.8) (3.1) Changes in working capital and other 26.8 13.3 (10.7) 49.8 (25.6) 6.5 59.4 (24.4) 4.9 (33.4) Net Income / (Loss) $10.3 $32.9 ($16.5) ($6.5) $0.4 ($ 101.8) ($55.8) $6.4 ($48.6) ($3.8) Depreciation, depletion and amortization expense 109.1 33.3 25.6 26.4 23.8 106.3 25.9 22.8 28.6 29.0 Interest expense, net 56.7 5.8 14.6 13.0 23.3 63.2 12.1 11.9 27.1 12.1 Income tax expense / (benefit) (8.8) (13.9) 4.8 (0.8) 1.1 (58.8) (9.9) 6.1 (50.8) (4.2) Asset and goodwill impairment — —— 150.3 30.8 16.4 103.1—Nonrecurring coal rationalization costs (1) 0.6 0.2 0.8 0.6 (1.0) 18.5 17.7 0.3 0.3 0.2 Sales discounts (2) — —— (0.5) ——(0.5) Coal Logistics deferred revenue (3) (2.9) (4.0) 1.1 — — ——Adjustment to unconsolidated affiliate earnings (4) 20.8—19.8 0.7 0.3 33.5 31.1 0.3 1.1 1.0 Adjusted EBITDA (Consolidated) $185.8 $54.3 $50.2 $33.4 $47.9 $ 210.7 $51.9 $64.2 $60.8 $33.8 Adjusted EBITDA attributable to noncontrolling interests (5) (81.2) (24.9) (20.1) (18.1) (18.1) (60.7) (18.7) (18.2) (14.5) (9.3) Adjusted EBITDA attributable to SXC $104.6 $29.4 $30.1 $15.3 $29.8 $ 150.0 $33.2 $46.0 $46.3 $24.5 Nonrecurring coal rationalization costs include employee severance, contract termination costs and other one-time costs to idle mines incurred during the execution of our coal rationalization plan. At December 31, 2013, we had $13.6 million accrued related to sales discounts to be paid to our customer at our Granite City facility. During the first quarter of 2014, we settled this obligation for $13.1 million which resulted in a gain of $0.5 million. The gain was recorded in sales and other operating revenue on our Combined and Consolidated Statement of Income. Coal Logistics deferred revenue represents revenue excluded from sales and other operating income related to the timing of revenue recognition on the Coal Logistics take-or- pay contracts. Represents SunCoke’s share of India JV interest, taxes and depreciation expense. Includes $30.5M impairment of our equity method investment in India in Q4 and FY 2014. Represents Adjusted EBITDA attributable to SXCP public unitholders and DTE Energy’s interest in Indiana Harbor. SXC Q4 2015 Earnings Call 14

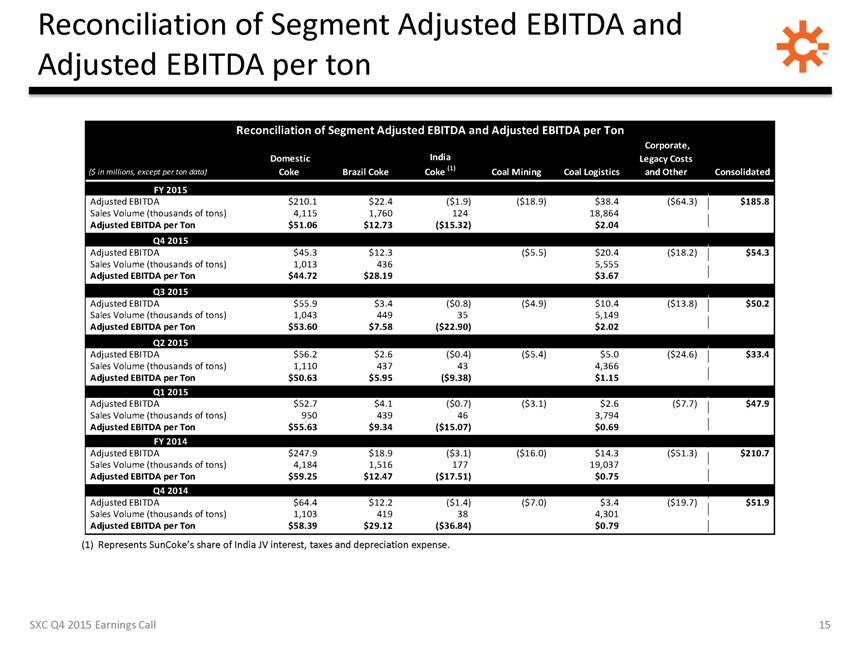

Reconciliation of Segment Adjusted EBITDA and Adjusted EBITDA per ton TM Reconciliation of Segment Adjusted EBITDA and Adjusted EBITDA per Ton Corporate, Domestic India Legacy Costs ($ in millions, except per ton data) Coke Brazil Coke Coke (1) Coal Mining Coal Logistics and Other Consolidated FY 2015 Adjusted EBITDA $210.1 $22.4 ($1.9) ($18.9) $38.4 ($64.3) $185.8 Sales Volume (thousands of tons) 4,115 1,760 124 18,864 Adjusted EBITDA per Ton $51.06 $12.73 ($15.32) $2.04 Q4 2015 Adjusted EBITDA $45.3 $12.3 ($5.5) $20.4 ($18.2) $54.3 Sales Volume (thousands of tons) 1,013 436 5,555 Adjusted EBITDA per Ton $44.72 $28.19 $3.67 Q3 2015 Adjusted EBITDA $55.9 $3.4 ($0.8) ($4.9) $10.4 ($13.8) $50.2 Sales Volume (thousands of tons) 1,043 449 35 5,149 Adjusted EBITDA per Ton $53.60 $7.58 ($22.90) $2.02 Q2 2015 Adjusted EBITDA $56.2 $2.6 ($0.4) ($5.4) $5.0 ($24.6) $33.4 Sales Volume (thousands of tons) 1,110 437 43 4,366 Adjusted EBITDA per Ton $50.63 $5.95 ($9.38) $1.15 Q1 2015 Adjusted EBITDA $52.7 $4.1 ($0.7) ($3.1) $2.6 ($7.7) $47.9 Sales Volume (thousands of tons) 950 439 46 3,794 Adjusted EBITDA per Ton $55.63 $9.34 ($15.07) $0.69 FY 2014 Adjusted EBITDA $247.9 $18.9 ($3.1) ($16.0) $14.3 ($51.3) $210.7 Sales Volume (thousands of tons) 4,184 1,516 177 19,037 Adjusted EBITDA per Ton $59.25 $12.47 ($17.51) $0.75 Q4 2014 Adjusted EBITDA $64.4 $12.2 ($1.4) ($7.0) $3.4 ($19.7) $51.9 Sales Volume (thousands of tons) 1,103 419 38 4,301 Adjusted EBITDA per Ton $58.39 $29.12 ($36.84) $0.79 (1) Represents SunCoke’s share of India JV interest, taxes and depreciation expense. SXC Q4 2015 Earnings Call 15

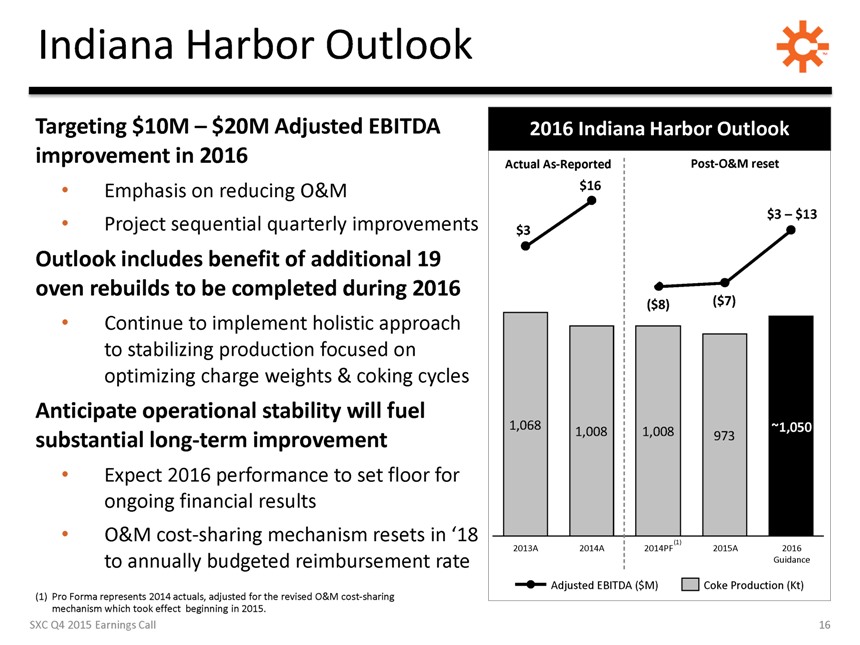

Outlook includes benefit of additional 19 oven rebuilds to be completed during 2016 Continue to implement holistic approach to stabilizing production focused on optimizing charge weights & coking cycles Anticipate operational stability will fuel substantial long-term improvement 1,068 1,008 1,008 973 ~1,050 • Expect 2016 performance to set floor for ongoing financial results • O&M cost-sharing mechanism resets in ‘18 (1) 2013A 2014A 2014PF 2015A 2016 to annually budgeted reimbursement rate Guidance Adjusted EBITDA ($M) Coke Production (Kt) Pro Forma represents 2014 actuals, adjusted for the revised O&M cost-sharing mechanism which took effect beginning in 2015. SXC Q4 2015 Earnings Call 16

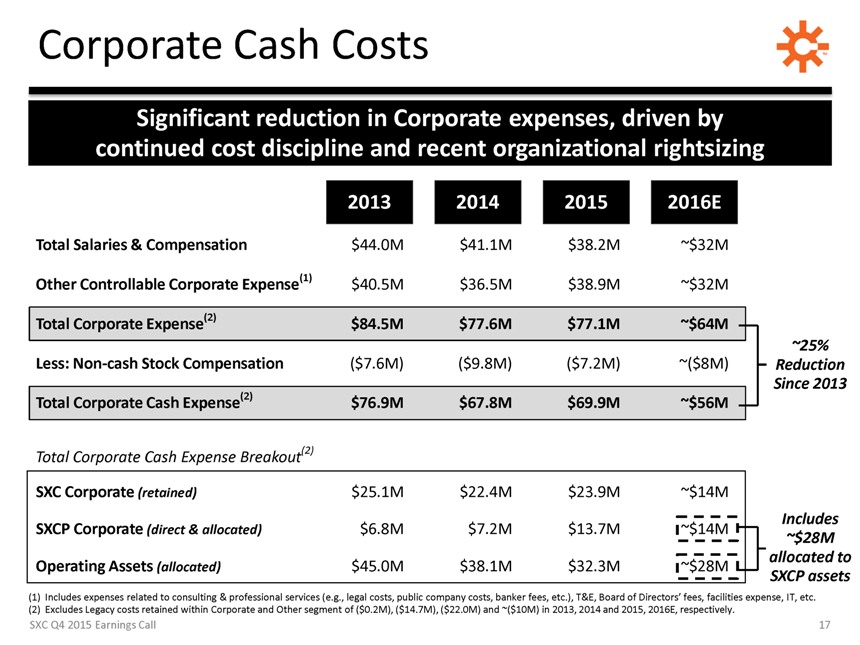

Significant reduction in Corporate expenses, driven by continued cost discipline and recent organizational rightsizing 2013 2014 2015 2016E Total Salaries & Compensation $44.0M $41.1M $38.2M ~$32M Other Controllable Corporate Expense (1) $40.5M $36.5M $38.9M ~$32M Total Corporate Expense (2) $84.5M $77.6M $77.1M ~$64M ~25% Less: Non-cash Stock Compensation ($7.6M) ($9.8M) ($7.2M) ~($8M) Reduction Since 2013 Total Corporate Cash Expense (2) $76.9M $67.8M $69.9M ~$56M Total Corporate Cash Expense Breakout(2) SXC Corporate (retained) $25.1M $22.4M $23.9M ~$14M Includes SXCP Corporate (direct & allocated) $6.8M $7.2M $13.7M ~$14M ~$28M Operating Assets (allocated) $45.0M $38.1M $32.3M ~$28M allocated to SXCP assets Includes expenses related to consulting & professional services (e.g., legal costs, public company costs, banker fees, etc.), T&E, Board of Directors’ fees, facilities expense, IT, etc. Excludes Legacy costs retained within Corporate and Other segment of ($0.2M), ($14.7M), ($22.0M) and ~($10M) in 2013, 2014 and 2015, 2016E, respectively. SXC Q4 2015 Earnings Call 17

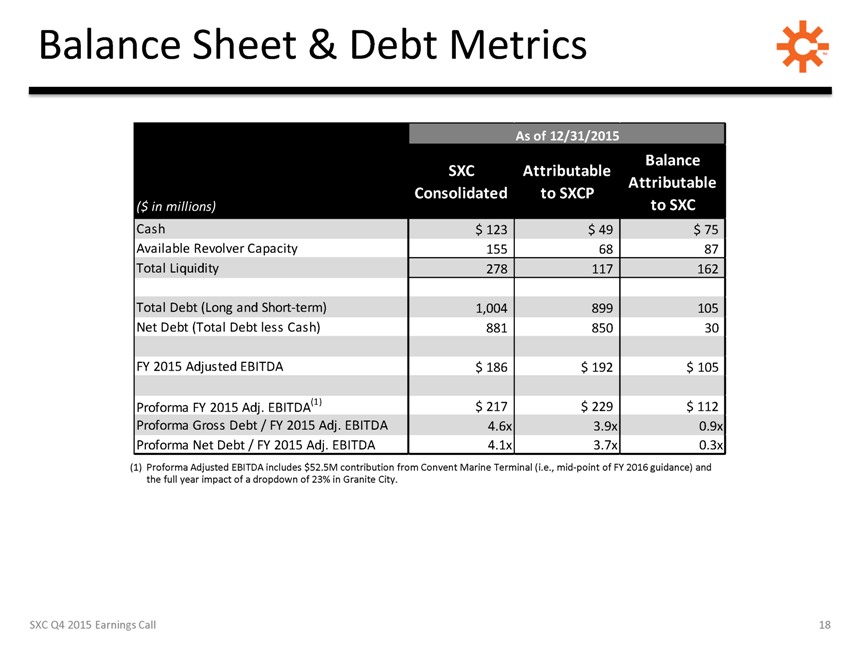

As of 12/31/2015 SXC Attributable Balance Consolidated to SXCP Attributable ($ in millions) to SXC Cash $ 123 $ 49 $ 75 Available Revolver Capacity 155 68 87 Total Liquidity 278 117 162 Total Debt (Long and Short-term) 1,004 899 105 Net Debt (Total Debt less Cash) 881 850 30 FY 2015 Adjusted EBITDA $ 186 $ 192 $ 105 Proforma FY 2015 Adj. EBITDA (1) $ 217 $ 229 $ 112 Proforma Gross Debt / FY 2015 Adj. EBITDA 4.6x 3.9x 0.9x Proforma Net Debt / FY 2015 Adj. EBITDA 4.1x 3.7x 0.3x Proforma Adjusted EBITDA includes $52.5M contribution from Convent Marine Terminal (i.e., mid-point of FY 2016 guidance) and the full year impact of a dropdown of 23% in Granite City. SXC Q4 2015 Earnings Call 18

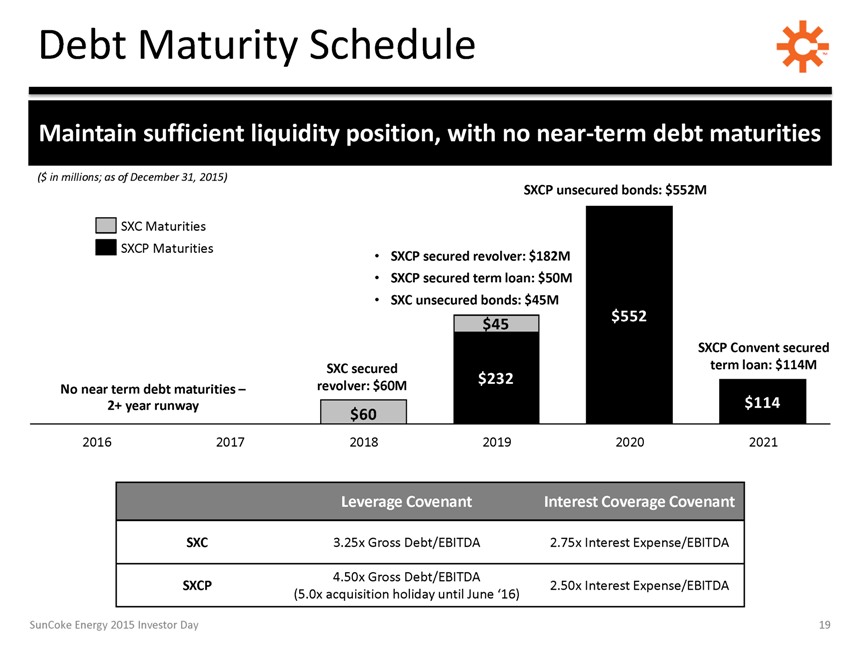

Maintain sufficient liquidity position, with no near-term debt maturities ($ in millions; as of December 31, 2015) SXCP unsecured bonds: $552M SXC Maturities SXCP Maturities • SXCP secured revolver: $182M • SXCP secured term loan: $50M • SXC unsecured bonds: $45M SunCoke Energy 2015 Investor Day 19

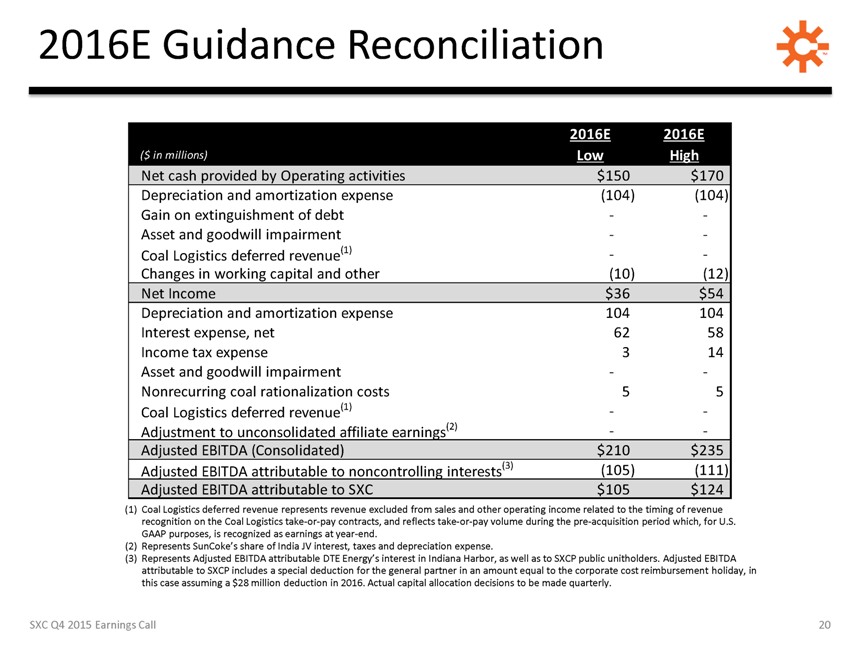

2016E 2016E ($ in millions) Low High Net cash provided by Operating activities $150 $170 Depreciation and amortization expense (104) (104) Gain on extinguishment of debt — Asset and goodwill impairment — Coal Logistics deferred revenue(1) — Changes in working capital and other (10) (12) Net Income $36 $54 Depreciation and amortization expense 104 104 Interest expense, net 62 58 Income tax expense 3 14 Asset and goodwill impairment — Nonrecurring coal rationalization costs 5 5 Coal Logistics deferred revenue(1) — Adjustment to unconsolidated affiliate earnings(2) — Adjusted EBITDA (Consolidated) $210 $235 Adjusted EBITDA attributable to noncontrolling interests(3) (105) (111) Adjusted EBITDA attributable to SXC $105 $124 Coal Logistics deferred revenue represents revenue excluded from sales and other operating income related to the timing of revenue recognition on the Coal Logistics take-or-pay contracts, and reflects take-or-pay volume during the pre-acquisition period which, for U.S. GAAP purposes, is recognized as earnings at year-end. Represents SunCoke’s share of India JV interest, taxes and depreciation expense. Represents Adjusted EBITDA attributable DTE Energy’s interest in Indiana Harbor, as well as to SXCP public unitholders. Adjusted EBITDA attributable to SXCP includes a special deduction for the general partner in an amount equal to the corporate cost reimbursement holiday, in this case assuming a $28 million deduction in 2016. Actual capital allocation decisions to be made quarterly. SXC Q4 2015 Earnings Call 20

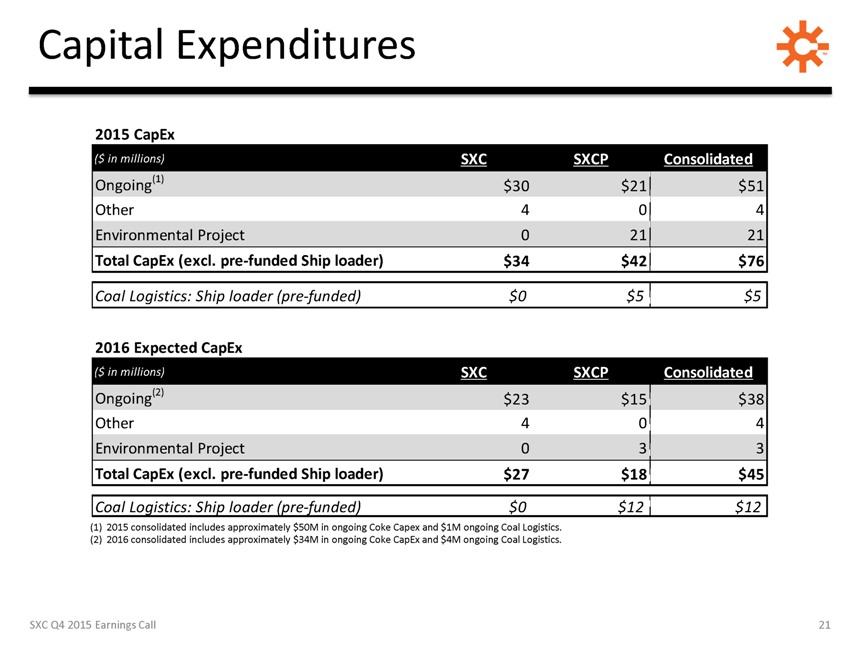

Capital Expenditures TM 2015 CapEx ($ in millions) SXC SXCP Consolidated Ongoing(1) $30 $21 $51 Other 4 0 4 Environmental Project 0 21 21 Total CapEx (excl. pre-funded Ship loader) $34 $42 $76 Coal Logistics: Ship loader (pre-funded) $0 $5 $5 2016 Expected CapEx ($ in millions) SXC SXCP Consolidated Ongoing(2) $23 $15 $38 Other 4 0 4 Environmental Project 0 3 3 Total CapEx (excl. pre-funded Ship loader) $27 $18 $45 Coal Logistics: Ship loader (pre-funded) $0 $12 $12 2015 consolidated includes approximately $50M in ongoing Coke Capex and $1M ongoing Coal Logistics. 2016 consolidated includes approximately $34M in ongoing Coke CapEx and $4M ongoing Coal Logistics. SXC Q4 2015 Earnings Call 21

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Ensysce Biosciences’ CEO Dr. Lynn Kirkpatrick Featured in Xtalks Clinical Edge Magazine

- Michigan-Based Business Leads the Pack With a Healthier Dog Food Option and Delivery Across Michigan and Around It

- Buyer Group International, Inc. is Pleased to Announce That Dr. Michael Curran, an Expert in His Field with a PhD in Ecology, Has Been Appointed as the New Head of Environmental Sustainability

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!