Form 8-K SPRINT Corp For: Nov 03

Tweet

Tweet Share

ShareNews Release |  | |

SPRINT HITS INFLECTION POINT IN ITS TURNAROUND BY REPORTING POSITIVE POSTPAID PHONE NET ADDITIONS AND RECORD LOW POSTPAID CHURN IN THE SECOND FISCAL QUARTER OF 2015

• | First national carrier on record to improve postpaid churn from the April-June quarter to the July-September quarter |

• | Best-ever Sprint platform postpaid churn of 1.54 percent improved 64 basis points year-over-year |

• | Sprint platform total net additions of 1.1 million improved nearly 80 percent compared to the prior year quarter |

◦ | Nearly 4 million total net additions in last four quarters |

• | Sprint platform postpaid net additions of 553,000 compared to net losses of 272,000 in prior year quarter |

◦ | Postpaid net port positive for the third consecutive quarter |

• | Sprint platform postpaid phone net additions of 237,000 mark the first quarterly additions in over two years |

◦ | Improved sequentially for the sixth consecutive quarter and by over 700,000 year-over-year |

◦ | Includes 199,000 prepaid to postpaid migrations |

• | Operating loss of $2 million; Adjusted EBITDA* of $2.0 billion grew 45 percent year-over-year |

OVERLAND PARK, Kan. - Nov. 3, 2015 - Sprint Corporation (NYSE: S) today reported operating results for the second fiscal quarter of 2015, including growth in postpaid phone customers for the first time in over two years, record low postpaid churn, and over 1 million total net additions. The company also reported net operating revenue of $8 billion, operating loss of $2 million, and Adjusted EBITDA* of $2 billion.

“As seen in our quarterly results, American consumers are happy to switch to Sprint because they appreciate great products and great service at a great price,” said Sprint CEO Marcelo Claure. “This quarter marked an inflection point in our turnaround journey, as we achieved positive postpaid phone net additions for the first time in over two years. In addition, we set another record low for postpaid churn and improved sequentially in the September quarter, something no US carrier has ever done before.”

Company Reaches Important Milestone with Positive Postpaid Phone Net Additions

During the past year, Sprint has focused on attracting and retaining more postpaid phone customers by providing an improved customer experience and a compelling value proposition, including the launch of the iPhone® Forever program, which allows customers to always be eligible to upgrade to the latest iPhone. The company reported positive postpaid phone net additions in the quarter for the first time in over two years and, based on October results, has seen positive postpaid phone net additions for six consecutive months, a streak not seen in nearly three years.

The company also reported the following Sprint platform results:

• | Total net additions were 1.1 million compared to 590,000 in the prior year quarter - an improvement of 466,000 year-over-year. |

• | Postpaid net additions of 553,000 compared to net losses of 272,000 in the prior year quarter - an improvement of 825,000 year-over-year. During the quarter 199,000 prepaid customers with consistent payment history migrated to postpaid, with 175,000 of these migrations now included as postpaid customers under their respective Boost and Virgin brands. Excluding total migrations from prepaid, postpaid net additions would have been 354,000 and improved by 626,000 year-over-year. |

News Release | | |

• | Postpaid phone net additions were 237,000 compared to net losses of 500,000 in the prior year quarter - an improvement of 737,000 year-over-year. Excluding migrations from prepaid, postpaid phone net additions would have been 38,000 and improved by 538,000 year-over-year. |

• | Prepaid net losses of 363,000 compared to net additions of 35,000 in the prior year quarter - a decline of 398,000 year-over-year. Excluding migrations to postpaid, prepaid net losses would have been 164,000 and declined by 199,000 year-over year. |

• | Wholesale net additions of 866,000 compared to 827,000 in the prior year quarter - an improvement of 39,000 year-over-year. |

Quarterly Financial Results

• | Net operating revenues of $8 billion decreased six percent year-over-year, as customer shifts to rate plans associated with device financing options and postpaid phone customer losses from prior periods drove lower wireless service revenues. Wireless service revenues plus installment plan billings and lease revenue of $7.1 billion increased slightly from the prior year period. |

• | Consolidated Adjusted EBITDA* of $2 billion grew 45 percent from the prior year period, as expense reductions more than offset the decline in service revenues. Total expenses improved primarily due to lower cost of product expenses related to device leasing options for which the associated cost is recorded as depreciation expense and lower bad debt expense as a result of a higher acquisition mix of prime credit quality customers in recent quarters. |

• | Operating loss of $2 million compares to an operating loss of $192 million in the year-ago quarter, an improvement of $190 million due to the items identified in Adjusted EBITDA* above, partially offset by higher depreciation expenses related to leased device assets and severance costs related to work force reductions in the prior year quarter. |

• | Net loss of $585 million, or $0.15 per share, compared to a net loss of $765 million, or $0.19 per share, in the year-ago period. |

• | Total liquidity was $5.9 billion at the end of the quarter, and the company had an additional $1.2 billion of availability under vendor financing agreements that can be used toward the purchase of 2.5 GHz network equipment. |

Further Cost Reductions Expected

Sprint plans to achieve a sustainable reduction of $2 billion or more of run rate operating expenses in fiscal 2016, excluding any transformation program costs to achieve that run rate benefit.

Funding the Turnaround

Sprint continues to work toward utilizing its assets to help fund the business and fuel future growth. The company has made significant progress working with SoftBank and others to establish a handset leasing company and expects to close in the next few weeks. In combination with the aforementioned plans for significant operating expense reductions, Sprint expects the handset leasing company and other upcoming financing structures to sufficiently meet the company’s cash needs for the foreseeable future.

Network Experience Continues to Improve With Carrier Aggregation Deployment

Sprint remains focused on building a network that delivers the consistent reliability, capacity and speed that customers demand. During the quarter, the company continued deploying two-channel (2x20 MHz) carrier aggregation in the 2.5 GHz band, which produces more capacity and higher data speeds, in 80 markets across the country. Sprint currently has twelve devices that are 2x20 capable, including the recently introduced iPhone® 6s and Galaxy® S6 models.

Third-party sources continue to validate Sprint’s improvements in the network experience.

• | Independent mobile analytics firm RootMetrics® awarded Sprint almost 55 percent more first-place (outright or shared) RootScore® Awards for overall, reliability, speed, data, call, or text network performance in the 54 metro markets measured so far in the second half of 2015 compared to the year-ago periodi. The company also saw median downlink speeds in these markets increase by 66 percent on average from the year-ago period, including impressive results in the Denver market, where Sprint received a first-place ranking in network speed for its broad deployment of 2x20 carrier aggregation. |

News Release | | |

• | PC Magazine looked at speed test results for LTE connections on Sprint iPhones in early October, finding average download speeds on the two new devices were 50 percent faster than the last generation and the iPhone® 6s demonstrated peak speeds of over 120 Mbps. |

The company remains committed to its plan of significantly densifying the network and continuing to improve performance.

Financial Outlook

• | Including transformation program costs, the company now expects fiscal year 2015 Adjusted EBITDA* to be at the low end of the previous expectation of $7.2 to $7.6 billion. This excludes any impacts from the potential sale of certain devices being leased by our customers. |

• | The company continues to expect fiscal year 2015 cash capital expenditures to be approximately $5 billion, excluding the impact of leased devices sold through indirect channels. |

Conference Call and Webcast

• | Date/Time: 8:30 a.m. (ET) Tuesday, Nov. 3, 2015 |

• | Call-in Information |

◦ | U.S./Canada: 866-360-1063 (ID: 56083433) |

◦ | International: 706-634-7849 (ID: 56083433) |

• | Webcast available via the Internet at www.sprint.com/investors |

• | Additional information about results, including the “Quarterly Investor Update,” is available on our Investor Relations website |

Contact Information

• | Media Contact: Dave Tovar, 913-315-1451, [email protected] |

• | Investor Contact: Jud Henry, 800-259-3755, [email protected] |

News Release | | |

Wireless Operating Statistics (Unaudited)

Quarter To Date | Year To Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Sprint platform (1): | ||||||||||||||||

Net additions (losses) (in thousands) | ||||||||||||||||

Postpaid (2) | 553 | 310 | (272 | ) | 863 | (453 | ) | |||||||||

Prepaid (2) | (363 | ) | (366 | ) | 35 | (729 | ) | (507 | ) | |||||||

Wholesale and affiliate | 866 | 731 | 827 | 1,597 | 1,330 | |||||||||||

Total Sprint platform wireless net additions | 1,056 | 675 | 590 | 1,731 | 370 | |||||||||||

End of period connections (in thousands) | ||||||||||||||||

Postpaid (2) | 30,569 | 30,016 | 29,465 | 30,569 | 29,465 | |||||||||||

Prepaid (2) | 14,977 | 15,340 | 14,750 | 14,977 | 14,750 | |||||||||||

Wholesale and affiliate | 12,322 | 11,456 | 9,706 | 12,322 | 9,706 | |||||||||||

Total Sprint platform end of period connections | 57,868 | 56,812 | 53,921 | 57,868 | 53,921 | |||||||||||

Churn | ||||||||||||||||

Postpaid | 1.54 | % | 1.56 | % | 2.18 | % | 1.55 | % | 2.12 | % | ||||||

Prepaid | 5.07 | % | 5.08 | % | 3.76 | % | 5.07 | % | 4.10 | % | ||||||

Supplemental data - connected devices | ||||||||||||||||

End of period connections (in thousands) | ||||||||||||||||

Retail postpaid | 1,576 | 1,439 | 1,039 | 1,576 | 1,039 | |||||||||||

Wholesale and affiliate | 7,338 | 6,620 | 4,635 | 7,338 | 4,635 | |||||||||||

Total | 8,914 | 8,059 | 5,674 | 8,914 | 5,674 | |||||||||||

Supplemental data - total company | ||||||||||||||||

End of period connections (in thousands) | ||||||||||||||||

Sprint platform (1) | 57,868 | 56,812 | 53,921 | 57,868 | 53,921 | |||||||||||

Transactions (3) | 710 | 856 | 1,116 | 710 | 1,116 | |||||||||||

Total | 58,578 | 57,668 | 55,037 | 58,578 | 55,037 | |||||||||||

Sprint platform ARPU (1) (a) | ||||||||||||||||

Postpaid | $ | 54.02 | $ | 55.48 | $ | 60.58 | $ | 54.74 | $ | 61.33 | ||||||

Prepaid | $ | 27.54 | $ | 27.81 | $ | 27.19 | $ | 27.68 | $ | 27.28 | ||||||

NON-GAAP RECONCILIATION - ABPA*, POSTPAID PHONE ARPU AND ABPU* (Unaudited)

(Millions, except accounts, connections, ABPA*, ARPU, and ABPU*)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Sprint platform ABPA* (1) (b) | ||||||||||||||||

Postpaid service revenue | $ | 4,900 | $ | 4,964 | $ | 5,377 | $ | 9,864 | $ | 10,930 | ||||||

Add: Installment plan billings and lease revenue | 694 | 554 | 193 | 1,248 | 330 | |||||||||||

Total for Sprint platform postpaid connections | $ | 5,594 | $ | 5,518 | $ | 5,570 | $ | 11,112 | $ | 11,260 | ||||||

Sprint platform postpaid accounts (in thousands) | 11,226 | 11,175 | 11,521 | 11,201 | 11,637 | |||||||||||

Sprint platform postpaid ABPA* | $ | 166.05 | $ | 164.63 | $ | 161.12 | $ | 165.34 | $ | 161.23 | ||||||

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Sprint platform postpaid phone ARPU and ABPU* (1) | ||||||||||||||||

Postpaid phone service revenue | $ | 4,615 | $ | 4,682 | $ | 5,096 | $ | 9,297 | $ | 10,390 | ||||||

Add: Installment plan billings and lease revenue | 665 | 531 | 183 | 1,196 | 312 | |||||||||||

Total for Sprint platform postpaid phone connections | $ | 5,280 | $ | 5,213 | $ | 5,279 | $ | 10,493 | $ | 10,702 | ||||||

Sprint platform postpaid average phone connections (in thousands) | 24,915 | 24,856 | 25,499 | 24,885 | 25,785 | |||||||||||

Sprint platform postpaid phone ARPU (a) | $ | 61.74 | $ | 62.79 | $ | 66.62 | $ | 62.26 | $ | 67.16 | ||||||

Sprint platform postpaid phone ABPU* (c) | $ | 70.64 | $ | 69.91 | $ | 69.02 | $ | 70.27 | $ | 69.18 | ||||||

(a) ARPU is calculated by dividing service revenue by the sum of the monthly average number of connections in the applicable service category. Changes in average monthly service revenue reflect connections for either the postpaid or prepaid service category who change rate plans, the level of voice and data usage, the amount of service credits which are offered to connections, plus the net effect of average monthly revenue generated by new connections and deactivating connections.

Sprint platform postpaid phone ARPU represents revenues related to our postpaid phone connections.

(b) Sprint platform postpaid ABPA* is calculated by dividing service revenue earned from connections plus installment plan billings and lease revenue by the sum of the monthly average number of accounts during the period.

(c) Sprint platform postpaid phone ABPU* is calculated by dividing postpaid phone service revenue earned from postpaid phone connections plus installment plan billings and lease revenue by the sum of the monthly average number of postpaid phone connections during the period.

News Release | | |

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

(Millions, except per Share Data)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net operating revenues | ||||||||||||||||

Service revenue | $ | 6,880 | $ | 7,037 | $ | 7,449 | $ | 13,917 | $ | 15,132 | ||||||

Equipment revenue | 1,095 | 990 | 1,039 | 2,085 | 2,145 | |||||||||||

Total net operating revenues | 7,975 | 8,027 | 8,488 | 16,002 | 17,277 | |||||||||||

Net operating expenses | ||||||||||||||||

Cost of services (exclusive of depreciation and amortization below) | 2,453 | 2,393 | 2,429 | 4,846 | 4,949 | |||||||||||

Cost of products (exclusive of depreciation and amortization below) | 1,290 | 1,365 | 2,372 | 2,655 | 4,530 | |||||||||||

Selling, general and administrative | 2,224 | 2,187 | 2,301 | 4,411 | 4,585 | |||||||||||

Depreciation and amortization | 1,743 | 1,588 | 1,294 | 3,331 | 2,575 | |||||||||||

Impairments (4) | 85 | — | — | 85 | — | |||||||||||

Other, net | 182 | (7 | ) | 284 | 175 | 311 | ||||||||||

Total net operating expenses | 7,977 | 7,526 | 8,680 | 15,503 | 16,950 | |||||||||||

Operating (loss) income | (2 | ) | 501 | (192 | ) | 499 | 327 | |||||||||

Interest expense | (542 | ) | (542 | ) | (510 | ) | (1,084 | ) | (1,022 | ) | ||||||

Other income, net | 5 | 4 | 8 | 9 | 9 | |||||||||||

Loss before income taxes | (539 | ) | (37 | ) | (694 | ) | (576 | ) | (686 | ) | ||||||

Income tax (expense) benefit | (46 | ) | 17 | (71 | ) | (29 | ) | (56 | ) | |||||||

Net loss | $ | (585 | ) | $ | (20 | ) | $ | (765 | ) | $ | (605 | ) | $ | (742 | ) | |

Basic and diluted net loss per common share | $ | (0.15 | ) | $ | (0.01 | ) | $ | (0.19 | ) | $ | (0.15 | ) | $ | (0.19 | ) | |

Weighted average common shares outstanding | 3,969 | 3,967 | 3,949 | 3,968 | 3,947 | |||||||||||

Effective tax rate | -8.5 | % | 45.9 | % | -10.2 | % | -5.0 | % | -8.2 | % | ||||||

NON-GAAP RECONCILIATION - NET LOSS TO ADJUSTED EBITDA* (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net loss | $ | (585 | ) | $ | (20 | ) | $ | (765 | ) | $ | (605 | ) | $ | (742 | ) | |

Income tax expense (benefit) | 46 | (17 | ) | 71 | 29 | 56 | ||||||||||

Loss before income taxes | (539 | ) | (37 | ) | (694 | ) | (576 | ) | (686 | ) | ||||||

Other income, net | (5 | ) | (4 | ) | (8 | ) | (9 | ) | (9 | ) | ||||||

Interest expense | 542 | 542 | 510 | 1,084 | 1,022 | |||||||||||

Operating (loss) income | (2 | ) | 501 | (192 | ) | 499 | 327 | |||||||||

Depreciation and amortization | 1,743 | 1,588 | 1,294 | 3,331 | 2,575 | |||||||||||

EBITDA* | 1,741 | 2,089 | 1,102 | 3,830 | 2,902 | |||||||||||

Impairments (4) | 85 | — | — | 85 | — | |||||||||||

Severance and exit costs (5) | 25 | 13 | 284 | 38 | 311 | |||||||||||

Litigation (6) | 157 | — | — | 157 | — | |||||||||||

Reduction in liability - U.S. Cellular asset acquisition (7) | — | (20 | ) | — | (20 | ) | — | |||||||||

Adjusted EBITDA* | $ | 2,008 | $ | 2,082 | $ | 1,386 | $ | 4,090 | $ | 3,213 | ||||||

Adjusted EBITDA margin* | 29.2 | % | 29.6 | % | 18.6 | % | 29.4 | % | 21.2 | % | ||||||

Selected items: | ||||||||||||||||

Cash paid for capital expenditures - network and other | $ | 1,162 | $ | 1,802 | $ | 1,143 | $ | 2,964 | $ | 2,389 | ||||||

Cash paid for capital expenditures - leased devices | $ | 573 | $ | 544 | $ | — | $ | 1,117 | $ | — | ||||||

News Release | | |

WIRELESS STATEMENTS OF OPERATIONS (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net operating revenues | ||||||||||||||||

Service revenue | ||||||||||||||||

Sprint platform (1): | ||||||||||||||||

Postpaid | $ | 4,900 | $ | 4,964 | $ | 5,377 | $ | 9,864 | $ | 10,930 | ||||||

Prepaid | 1,252 | 1,300 | 1,197 | 2,552 | 2,418 | |||||||||||

Wholesale, affiliate and other | 185 | 181 | 181 | 366 | 344 | |||||||||||

Total Sprint platform | 6,337 | 6,445 | 6,755 | 12,782 | 13,692 | |||||||||||

Total transactions (3) | 84 | 105 | 135 | 189 | 285 | |||||||||||

Total service revenue | 6,421 | 6,550 | 6,890 | 12,971 | 13,977 | |||||||||||

Equipment revenue | 1,095 | 990 | 1,039 | 2,085 | 2,145 | |||||||||||

Total net operating revenues | 7,516 | 7,540 | 7,929 | 15,056 | 16,122 | |||||||||||

Net operating expenses | ||||||||||||||||

Cost of services (exclusive of depreciation and amortization below) | 2,111 | 2,005 | 1,988 | 4,116 | 4,037 | |||||||||||

Cost of products (exclusive of depreciation and amortization below) | 1,290 | 1,365 | 2,372 | 2,655 | 4,530 | |||||||||||

Selling, general and administrative | 2,136 | 2,096 | 2,199 | 4,232 | 4,392 | |||||||||||

Depreciation and amortization | 1,694 | 1,540 | 1,232 | 3,234 | 2,444 | |||||||||||

Impairments (4) | 85 | — | — | 85 | — | |||||||||||

Other, net | 181 | (8 | ) | 248 | 173 | 271 | ||||||||||

Total net operating expenses | 7,497 | 6,998 | 8,039 | 14,495 | 15,674 | |||||||||||

Operating income (loss) | $ | 19 | $ | 542 | $ | (110 | ) | $ | 561 | $ | 448 | |||||

WIRELESS NON-GAAP RECONCILIATION (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Operating income (loss) | $ | 19 | $ | 542 | $ | (110 | ) | $ | 561 | $ | 448 | |||||

Impairments (4) | 85 | — | — | 85 | — | |||||||||||

Severance and exit costs (5) | 24 | 12 | 248 | 36 | 271 | |||||||||||

Litigation (6) | 157 | — | — | 157 | — | |||||||||||

Reduction in liability - U.S. Cellular asset acquisition (7) | — | (20 | ) | — | (20 | ) | — | |||||||||

Depreciation and amortization | 1,694 | 1,540 | 1,232 | 3,234 | 2,444 | |||||||||||

Adjusted EBITDA* | $ | 1,979 | $ | 2,074 | $ | 1,370 | $ | 4,053 | $ | 3,163 | ||||||

Adjusted EBITDA margin* | 30.8 | % | 31.7 | % | 19.9 | % | 31.2 | % | 22.6 | % | ||||||

Selected items: | ||||||||||||||||

Cash paid for capital expenditures - network and other | $ | 1,003 | $ | 1,640 | $ | 989 | $ | 2,643 | $ | 2,109 | ||||||

Cash paid for capital expenditures - leased devices | $ | 573 | $ | 544 | $ | — | $ | 1,117 | $ | — | ||||||

News Release | | |

WIRELINE STATEMENTS OF OPERATIONS (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net operating revenues | ||||||||||||||||

Voice | $ | 212 | $ | 233 | $ | 294 | $ | 445 | $ | 621 | ||||||

Data | 43 | 49 | 53 | 92 | 109 | |||||||||||

Internet | 323 | 328 | 340 | 651 | 685 | |||||||||||

Other | 31 | 20 | 21 | 51 | 39 | |||||||||||

Total net operating revenues | 609 | 630 | 708 | 1,239 | 1,454 | |||||||||||

Net operating expenses | ||||||||||||||||

Cost of services (exclusive of depreciation and amortization below) | 495 | 534 | 593 | 1,029 | 1,219 | |||||||||||

Selling, general and administrative | 85 | 87 | 88 | 172 | 173 | |||||||||||

Depreciation and amortization | 48 | 46 | 60 | 94 | 127 | |||||||||||

Other, net | 1 | 1 | 35 | 2 | 39 | |||||||||||

Total net operating expenses | 629 | 668 | 776 | 1,297 | 1,558 | |||||||||||

Operating loss | $ | (20 | ) | $ | (38 | ) | $ | (68 | ) | $ | (58 | ) | $ | (104 | ) | |

WIRELINE NON-GAAP RECONCILIATION (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Operating loss | $ | (20 | ) | $ | (38 | ) | $ | (68 | ) | $ | (58 | ) | $ | (104 | ) | |

Severance and exit costs (5) | 1 | 1 | 35 | 2 | 39 | |||||||||||

Depreciation and amortization | 48 | 46 | 60 | 94 | 127 | |||||||||||

Adjusted EBITDA* | $ | 29 | $ | 9 | $ | 27 | $ | 38 | $ | 62 | ||||||

Adjusted EBITDA margin* | 4.8 | % | 1.4 | % | 3.8 | % | 3.1 | % | 4.3 | % | ||||||

Selected items: | ||||||||||||||||

Cash paid for capital expenditures - network and other | $ | 63 | $ | 68 | $ | 65 | $ | 131 | $ | 124 | ||||||

News Release | | |

CONDENSED CONSOLIDATED CASH FLOW INFORMATION (Unaudited)

(Millions)

Year to Date | ||||||

9/30/15 | 9/30/14 | |||||

Operating activities | ||||||

Net loss | $ | (605 | ) | $ | (742 | ) |

Impairments (4) | 85 | — | ||||

Depreciation and amortization | 3,331 | 2,575 | ||||

Provision for losses on accounts receivable | 278 | 493 | ||||

Share-based and long-term incentive compensation expense | 40 | 65 | ||||

Deferred income tax expense | 28 | 28 | ||||

Amortization of long-term debt premiums, net | (157 | ) | (149 | ) | ||

Other changes in assets and liabilities: | ||||||

Accounts and notes receivable | (1,357 | ) | (828 | ) | ||

Inventories and other current assets | 173 | (155 | ) | |||

Accounts payable and other current liabilities | (509 | ) | 503 | |||

Non-current assets and liabilities, net | 125 | (146 | ) | |||

Other, net | 365 | 63 | ||||

Net cash provided by operating activities | 1,797 | 1,707 | ||||

Investing activities | ||||||

Capital expenditures - network and other | (2,964 | ) | (2,389 | ) | ||

Capital expenditures - leased devices | (1,117 | ) | — | |||

Expenditures relating to FCC licenses | (45 | ) | (79 | ) | ||

Reimbursements relating to FCC licenses | — | 95 | ||||

Change in short-term investments, net | 63 | 53 | ||||

Proceeds from sales of assets and FCC licenses | 4 | 101 | ||||

Other, net | (21 | ) | (6 | ) | ||

Net cash used in investing activities | (4,080 | ) | (2,225 | ) | ||

Financing activities | ||||||

Proceeds from debt and financings | 434 | — | ||||

Repayments of debt, financing and capital lease obligations | (206 | ) | (363 | ) | ||

Proceeds from issuance of common stock, net | 8 | 46 | ||||

Other, net | 9 | — | ||||

Net cash provided by (used in) financing activities | 245 | (317 | ) | |||

Net decrease in cash and cash equivalents | (2,038 | ) | (835 | ) | ||

Cash and cash equivalents, beginning of period | 4,010 | 4,970 | ||||

Cash and cash equivalents, end of period | $ | 1,972 | $ | 4,135 | ||

RECONCILIATION TO CONSOLIDATED FREE CASH FLOW* (NON-GAAP) (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net cash provided by operating activities | $ | 1,669 | $ | 128 | $ | 1,028 | $ | 1,797 | $ | 1,707 | ||||||

Capital expenditures - network and other | (1,162 | ) | (1,802 | ) | (1,143 | ) | (2,964 | ) | (2,389 | ) | ||||||

Capital expenditures - leased devices | (573 | ) | (544 | ) | — | (1,117 | ) | — | ||||||||

(Expenditures) reimbursements relating to FCC licenses, net | (19 | ) | (26 | ) | (38 | ) | (45 | ) | 16 | |||||||

Proceeds from sales of assets and FCC licenses | 3 | 1 | 81 | 4 | 101 | |||||||||||

Other investing activities, net | (18 | ) | (3 | ) | (3 | ) | (21 | ) | (6 | ) | ||||||

Free cash flow* | $ | (100 | ) | $ | (2,246 | ) | $ | (75 | ) | $ | (2,346 | ) | $ | (571 | ) | |

News Release | | |

CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited)

(Millions)

9/30/15 | 3/31/15 | |||||

ASSETS | ||||||

Current assets | ||||||

Cash and cash equivalents | $ | 1,972 | $ | 4,010 | ||

Short-term investments | 103 | 166 | ||||

Accounts and notes receivable, net | 1,980 | 2,290 | ||||

Device and accessory inventory | 889 | 1,359 | ||||

Deferred tax assets | 63 | 62 | ||||

Prepaid expenses and other current assets | 2,089 | 1,890 | ||||

Total current assets | 7,096 | 9,777 | ||||

Property, plant and equipment, net | 21,061 | 19,721 | ||||

Goodwill | 6,575 | 6,575 | ||||

FCC licenses and other | 40,025 | 39,987 | ||||

Definite-lived intangible assets, net | 5,155 | 5,893 | ||||

Other assets | 939 | 1,077 | ||||

Total assets | $ | 80,851 | $ | 83,030 | ||

LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||

Current liabilities | ||||||

Accounts payable | $ | 3,527 | $ | 4,347 | ||

Accrued expenses and other current liabilities | 4,333 | 5,293 | ||||

Current portion of long-term debt, financing and capital lease obligations | 1,395 | 1,300 | ||||

Total current liabilities | 9,255 | 10,940 | ||||

Long-term debt, financing and capital lease obligations | 32,570 | 32,531 | ||||

Deferred tax liabilities | 13,929 | 13,898 | ||||

Other liabilities | 3,940 | 3,951 | ||||

Total liabilities | 59,694 | 61,320 | ||||

Stockholders' equity | ||||||

Common stock | 40 | 40 | ||||

Treasury shares, at cost | — | (7 | ) | |||

Paid-in capital | 27,517 | 27,468 | ||||

Accumulated deficit | (5,988 | ) | (5,383 | ) | ||

Accumulated other comprehensive loss | (412 | ) | (408 | ) | ||

Total stockholders' equity | 21,157 | 21,710 | ||||

Total liabilities and stockholders' equity | $ | 80,851 | $ | 83,030 | ||

NET DEBT* (NON-GAAP) (Unaudited)

(Millions)

9/30/15 | 3/31/15 | |||||

Total Debt | $ | 33,965 | $ | 33,831 | ||

Less: Cash and cash equivalents | (1,972 | ) | (4,010 | ) | ||

Less: Short-term investments | (103 | ) | (166 | ) | ||

Net debt* | $ | 31,890 | $ | 29,655 | ||

News Release | | |

SCHEDULE OF DEBT (Unaudited)

(Millions)

9/30/15 | |||||

ISSUER | COUPON | MATURITY | PRINCIPAL | ||

Sprint Corporation | |||||

7.25% Notes due 2021 | 7.250% | 09/15/2021 | $ | 2,250 | |

7.875% Notes due 2023 | 7.875% | 09/15/2023 | 4,250 | ||

7.125% Notes due 2024 | 7.125% | 06/15/2024 | 2,500 | ||

7.625% Notes due 2025 | 7.625% | 02/15/2025 | 1,500 | ||

Sprint Corporation | 10,500 | ||||

Sprint Communications, Inc. | |||||

Export Development Canada Facility (Tranche 2) | 4.077% | 12/15/2015 | 500 | ||

Export Development Canada Facility (Tranche 3) | 3.783% | 12/17/2019 | 300 | ||

6% Senior notes due 2016 | 6.000% | 12/01/2016 | 2,000 | ||

9.125% Senior notes due 2017 | 9.125% | 03/01/2017 | 1,000 | ||

8.375% Senior notes due 2017 | 8.375% | 08/15/2017 | 1,300 | ||

9% Guaranteed notes due 2018 | 9.000% | 11/15/2018 | 3,000 | ||

7% Guaranteed notes due 2020 | 7.000% | 03/01/2020 | 1,000 | ||

7% Senior notes due 2020 | 7.000% | 08/15/2020 | 1,500 | ||

11.5% Senior notes due 2021 | 11.500% | 11/15/2021 | 1,000 | ||

9.25% Debentures due 2022 | 9.250% | 04/15/2022 | 200 | ||

6% Senior notes due 2022 | 6.000% | 11/15/2022 | 2,280 | ||

Sprint Communications, Inc. | 14,080 | ||||

Sprint Capital Corporation | |||||

6.9% Senior notes due 2019 | 6.900% | 05/01/2019 | 1,729 | ||

6.875% Senior notes due 2028 | 6.875% | 11/15/2028 | 2,475 | ||

8.75% Senior notes due 2032 | 8.750% | 03/15/2032 | 2,000 | ||

Sprint Capital Corporation | 6,204 | ||||

Clearwire Communications LLC | |||||

14.75% First-priority senior secured notes due 2016 | 14.750% | 12/01/2016 | 300 | ||

8.25% Exchangeable notes due 2040 | 8.250% | 12/01/2040 | 629 | ||

Clearwire Communications LLC | 929 | ||||

Secured equipment credit facilities | 1.991% - 2.385% | 2017 - 2020 | 889 | ||

Tower financing obligation | 6.093% | 08/31/2021 | 244 | ||

Capital lease obligations and other | 2.348% - 10.517% | 2015 - 2023 | 173 | ||

Total principal | 33,019 | ||||

Net premiums | 946 | ||||

Total debt | $ | 33,965 | |||

*This table excludes (i) our unsecured revolving bank credit facility, which will expire in 2018 and has no outstanding balance, (ii) $435 million in letters of credit outstanding under the unsecured revolving bank credit facility, and (iii) all capital leases and other financing obligations.

News Release | | |

NOTES TO THE FINANCIAL INFORMATION (Unaudited)

(1) | Sprint platform refers to the Sprint network that supports the wireless service we provide through our multiple brands. |

(2) | During the quarter ended September 30, 2015, the Company introduced a program to provide certain tenured Boost and Virgin Mobile prepaid subscribers with an extension of credit for their use of wireless service. Subscribers who opt-into this program may also qualify for certain device offers and/or service credits. Approximately 175,000 subscribers migrated from the prepaid subscriber base and into the postpaid subscriber base under their respective Boost and Virgin Mobile brands as a result of their decision to choose to participate in this program. In mid-June 2015, we implemented a program targeting our high tenure prepaid subscribers with consistent payment history, providing them the option to become a postpaid subscriber. During the three-month period ended September 30, 2015, approximately 24,000 prepaid subscribers with a consistent payment history switched to a postpaid plan as part of this program. |

(3) | Postpaid and prepaid connections from transactions are defined as retail postpaid and prepaid connections acquired from Clearwire in July 2013 who had not deactivated or been recaptured on the Sprint platform. |

(4) | During the three-month period ended September 30, 2015, we recorded $85 million of asset impairments primarily related to network development costs that are no longer relevant as a result of changes in the Company's network plans. |

(5) | Severance and exit costs consist of lease exit costs primarily associated with tower and cell sites, access exit costs related to payments that will continue to be made under our backhaul access contracts for which we will no longer be receiving any economic benefit, and severance costs associated with reduction in our work force. |

(6) | For the second quarter of fiscal year 2015, litigation activity is a result of unfavorable developments in connection with pending litigation. |

(7) | As a result of the U.S. Cellular asset acquisition, we recorded a liability related to network shut-down costs, which primarily consisted of lease exit costs, for which we agreed to reimburse U.S. Cellular. During the first quarter of fiscal year 2015, we revised our estimate and, as a result, reduced the liability resulting in approximately $20 million of income. |

News Release | | |

*FINANCIAL MEASURES

Sprint provides financial measures determined in accordance with GAAP and adjusted GAAP (non-GAAP). The non-GAAP financial measures reflect industry conventions, or standard measures of liquidity, profitability or performance commonly used by the investment community for comparability purposes. These measurements should be considered in addition to, but not as a substitute for, financial information prepared in accordance with GAAP. We have defined below each of the non-GAAP measures we use, but these measures may not be synonymous to similar measurement terms used by other companies.

Sprint provides reconciliations of these non-GAAP measures in its financial reporting. Because Sprint does not predict special items that might occur in the future, and our forecasts are developed at a level of detail different than that used to prepare GAAP-based financial measures, Sprint does not provide reconciliations to GAAP of its forward-looking financial measures.

The measures used in this release include the following:

EBITDA is operating income/(loss) before depreciation and amortization. Adjusted EBITDA is EBITDA excluding severance, exit costs, and other special items. Adjusted EBITDA Margin represents Adjusted EBITDA divided by non-equipment net operating revenues for Wireless and Adjusted EBITDA divided by net operating revenues for Wireline. We believe that Adjusted EBITDA and Adjusted EBITDA Margin provide useful information to investors because they are an indicator of the strength and performance of our ongoing business operations. While depreciation and amortization are considered operating costs under GAAP, these expenses primarily represent non-cash current period costs associated with the use of long-lived tangible and definite-lived intangible assets. Adjusted EBITDA and Adjusted EBITDA Margin are calculations commonly used as a basis for investors, analysts and credit rating agencies to evaluate and compare the periodic and future operating performance and value of companies within the telecommunications industry.

Sprint Platform Postpaid ABPA is average billings per account and calculated by dividing postpaid service revenue earned from postpaid customers plus installment plan billings and lease revenue by the sum of the monthly average number of postpaid accounts during the period. We believe that ABPA provides useful information to investors, analysts and our management to evaluate average Sprint platform postpaid customer billings per account as it approximates the expected cash collections, including installment plan billings and lease revenue, per postpaid account each month.

Sprint Platform Postpaid Phone ABPU is average billings per postpaid phone user and calculated by dividing service revenue earned from postpaid phone customers plus installment plan billings and lease revenue by the sum of the monthly average number of postpaid phone connections during the period. We believe that ABPU provides useful information to investors, analysts and our management to evaluate average Sprint platform postpaid phone customer billings as it approximates the expected cash collections, including installment plan billings and lease revenue, per postpaid phone user each month.

Free Cash Flow is the cash provided by operating activities less the cash used in investing activities other than short-term investments, including changes in restricted cash, if any. We believe that Free Cash Flow provides useful information to investors, analysts and our management about the cash generated by our core operations after interest and dividends, if any, and our ability to fund scheduled debt maturities and other financing activities, including discretionary refinancing and retirement of debt and purchase or sale of investments.

Net Debt is consolidated debt, including current maturities, less cash and cash equivalents, short-term investments and, if any, restricted cash. We believe that Net Debt provides useful information to investors, analysts and credit rating agencies about the capacity of the company to reduce the debt load and improve its capital structure.

News Release | | |

SAFE HARBOR

This release includes “forward-looking statements” within the meaning of the securities laws. The words “may,” “could,” “should,” “estimate,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “target,” “plan,” “providing guidance,” and similar expressions are intended to identify information that is not historical in nature. All statements that address operating performance, events or developments that we expect or anticipate will occur in the future - including statements relating to our network, connections growth, and liquidity; and statements expressing general views about future operating results - are forward-looking statements. Forward-looking statements are estimates and projections reflecting management’s judgment based on currently available information and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. With respect to these forward-looking statements, management has made assumptions regarding, among other things, the development and deployment of new technologies and services; efficiencies and cost savings of new technologies and services; customer and network usage; connection growth and retention; service, speed, coverage and quality; availability of devices; availability of various financings, including any leasing transactions; the timing of various events and the economic environment. Sprint believes these forward-looking statements are reasonable; however, you should not place undue reliance on forward-looking statements, which are based on current expectations and speak only as of the date when made. Sprint undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our company's historical experience and our present expectations or projections. Factors that might cause such differences include, but are not limited to, those discussed in Sprint Corporation’s Annual Report on Form 10-K for the fiscal year ended March 31, 2015. You should understand that it is not possible to predict or identify all such factors. Consequently, you should not consider any such list to be a complete set of all potential risks or uncertainties.

About Sprint:

Sprint (NYSE: S) is a communications services company that creates more and better ways to connect its customers to the things they care about most. Sprint served more than 58.6 million connections as of September 30, 2015 and is widely recognized for developing, engineering and deploying innovative technologies, including the first wireless 4G service from a national carrier in the United States; leading no-contract brands including Virgin Mobile USA, Boost Mobile, and Assurance Wireless; instant national and international push-to-talk capabilities; and a global Tier 1 Internet backbone. Sprint has been named to the Dow Jones Sustainability Index (DJSI) North America for the past five years. You can learn more and visit Sprint at www.sprint.com or www.facebook.com/sprint and www.twitter.com/sprint.

i Rankings based on 54 corresponding RootMetrics Metro RootScore Reports from 2H 2014 and 2H 2015 (July 1 - Oct 12, 2015) for mobile performance as tested on best available plans and devices on four mobile networks across all available network types. Your experiences may vary. The RootMetrics award is not an endorsement of Sprint. Visit www.rootmetrics.com for more details.

###

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________

FORM 8-K

_______________________________________

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported) November 3, 2015

_______________________________________

SPRINT CORPORATION

(Exact name of Registrant as specified in its charter)

_______________________________________

Delaware | 1-04721 | 46-1170005 | ||

(State of Incorporation) | (Commission File Number) | (I.R.S. Employer Identification No.) | ||

6200 Sprint Parkway, Overland Park, Kansas | 66251 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code (855) 848-3280

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

o | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

o | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

o | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

o | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Item 2.02 Results of Operations and Financial Condition.

On November 3, 2015, Sprint Corporation announced its results for the quarter ended September 30, 2015. The press release is furnished as Exhibit 99.1 and its Quarterly Investor Update is attached as Exhibit 99.2.

Item 9.01 Financial Statements and Exhibits.

(d) Exhibits

The following exhibits are furnished with this report:

Exhibit No. | Description | ||

99.1 | Press Release Announcing Results for the Quarter Ended September 30, 2015 | ||

99.2 | Quarterly Investor Update | ||

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

SPRINT CORPORATION | ||||||||

Date: November 3, 2015 | /s/ Timothy O’Grady | |||||||

By: | Timothy O’Grady | |||||||

Corporate Secretary | ||||||||

EXHIBIT INDEX

Number | Exhibit | ||

99.1 | Press Release Announcing Results for the Quarter Ended September 30, 2015 | ||

99.2 | Quarterly Investor Update | ||

SPRINT HITS INFLECTION POINT IN ITS TURNAROUND BY REPORTING POSITIVE POSTPAID PHONE NET ADDITIONS AND RECORD LOW POSTPAID CHURN IN THE SECOND FISCAL QUARTER OF 2015

• | First national carrier on record to improve postpaid churn from the April-June quarter to the July-September quarter |

• | Best-ever Sprint platform postpaid churn of 1.54 percent improved 64 basis points year-over-year |

• | Sprint platform total net additions of 1.1 million improved nearly 80 percent compared to the prior year quarter |

◦ | Nearly 4 million total net additions in last four quarters |

• | Sprint platform postpaid net additions of 553,000 compared to net losses of 272,000 in prior year quarter |

◦ | Postpaid net port positive for the third consecutive quarter |

• | Sprint platform postpaid phone net additions of 237,000 mark the first quarterly additions in over two years |

◦ | Improved sequentially for the sixth consecutive quarter and by over 700,000 year-over-year |

◦ | Includes 199,000 prepaid to postpaid migrations |

• | Operating loss of $2 million; Adjusted EBITDA* of $2.0 billion grew 45 percent year-over-year |

| TABLE OF CONTENTS | ||

Customer Metrics | 3 | ||

Sales | 5 | ||

Network | 6 | ||

Financials | 7 | ||

The Sprint Quarterly Investor Update is a publication of the Sprint Investor Relations department, which can be reached by phone at 1-800-259-3755 or via e-mail at [email protected]. | Financial and Operational Results Tables | 11 | |

Notes to the Financial Information | 18 | ||

Financial Measures | 19 | ||

Trended financial performance metrics can also be found on our Investor Relations website at sprint.com/investors. | Safe Harbor | 20 | |

During the past year, Sprint has focused on attracting and retaining more postpaid phone customers by providing an improved customer experience and a compelling value proposition, including the launch of the iPhone® Forever program, which allows customers to always be eligible to upgrade to the latest iPhone. The company reported positive postpaid phone net additions in the quarter for the first time in over two years and, based on October results, has seen positive postpaid phone net additions for six consecutive months, a streak not seen in nearly three years.

The company had 58.6 million connections at the end of the quarter, with 57.9 million on the Sprint platform, including 30.6 million postpaid, 15.0 million prepaid, and 12.3 million wholesale and affiliate connections. The Sprint platform had 1.1 million net additions in the current quarter compared with 675,000 in the previous quarter and 590,000 in the year-ago period. The quarterly and year-over-year improvement was primarily attributable to stronger retail net additions and the company has had nearly 4 million Sprint platform net additions over the last four quarters.

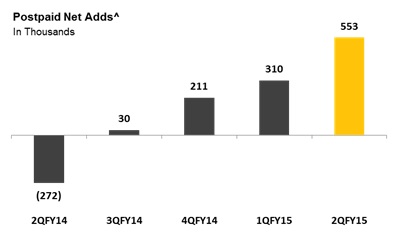

Postpaid^

• | Net additions were 553,000 during the quarter, compared to 272,000 net losses in the year-ago period and 310,000 net additions in the prior quarter. During the quarter 199,000 prepaid customers with consistent payment history migrated to postpaid, with 175,000 of these migrations now included as postpaid customers under their respective Boost and Virgin brands. Excluding total migrations from prepaid, postpaid net additions would have been 354,000. The year-over-year improvement was driven by significantly lower churn combined with higher prime credit quality gross additions while the sequential improvement was primarily driven by higher prime credit quality gross additions. The prime mix of postpaid gross additions was the highest for a September quarter in the last seven years. |

• | Churn was once again at a record low of 1.54 percent compared to 2.18 percent for the year-ago period and 1.56 percent for the prior quarter. The 64 basis point year-over-year improvement was primarily driven by improved quality of recently acquired customers and improved network experience. Sequentially, these same drivers more than offset typical seasonal pressure. |

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | ^ indicates results specific to Sprint Platform 3 |

• | Phone net additions of 237,000, including 199,000 migrations from prepaid, compared to losses of 500,000 for the year-ago period and 12,000 in the prior quarter. Excluding the migrations, net additions would have been 38,000, demonstrating the sixth consecutive quarter of sequential improvement. The year-over-year improvement was primarily driven by lower churn and a ten percent increase in prime credit quality gross additions. The company ended the quarter with 25.1 million phone connections. |

• | Tablet net additions were 228,000 in the quarter compared to 261,000 for the year-ago period and 271,000 for the prior quarter. Both the year-over-year and sequential declines were due to lower gross additions as the company continues to focus on growing phone connections. The company ended the quarter with 3.1 million tablet connections. |

Prepaid^

• | Net losses of 363,000 during the quarter, including 199,000 migrations to postpaid, compared to net additions of 35,000 in the year-ago quarter and net losses of 366,000 in the prior quarter. Excluding migrations to postpaid, net losses would have been 164,000. The year-over-year decline was mostly driven by increased competitive pressure, while the sequential improvement was primarily driven by a return to growth in the Assurance brand. |

• | Churn was 5.07 percent compared to 3.76 percent for the year-ago period and 5.08 percent for the prior quarter. The increase in year-over-year churn was primarily due to an increase in competitive offers in the market. |

Wholesale & Affiliate^

• | Net additions were 866,000 in the quarter, compared to 827,000 in the year-ago quarter and 731,000 in the prior quarter. Connected devices represented the majority of the net additions. |

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | ^ indicates results specific to Sprint Platform 4 |

Retail Sales on the Sprint platform were 7.5 million during the quarter compared to 6.9 million in the year-ago quarter and 7.3 million in the prior quarter. The nine percent year-over-year increase was primarily driven by higher prepaid sales.

Postpaid^

• | Device financing take rate was 64 percent for the quarter (51 percent on leasing and 13 percent on installment plans), compared to 27 percent for the year-ago period (three percent on leasing and 24 percent on installment plans) and flat sequentially. At the end of the quarter, 37 percent of the postpaid connection base was active on a device financing agreement (22 percent on leasing and 15 percent on installment plans). |

• | Upgrade rate was 7.8 percent during the quarter compared to 8.0 percent for the year-ago quarter and 7.9 percent for the prior quarter. |

• | Smartphones comprised 97 percent of phones sold in the quarter, a two percentage point increase year-over-year and flat with the prior quarter. At the end of the quarter, smartphones represented 90 percent of the 25.1 million ending phone connection base. |

• | LTE devices represented 79 percent of the 30.6 million ending connection base compared to 62 percent at the end of the year-ago quarter. The percentage of the smartphone base with LTE capable devices rose to 92 percent at the end of the quarter, a 19 percentage point increase from the year-ago period. |

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | ^ indicates results specific to Sprint Platform 5 |

Sprint remains focused on building a network that delivers the consistent reliability, capacity and speed that customers demand. During the quarter, the company continued deploying two-channel (2x20 MHz) carrier aggregation in the 2.5 GHz band, which produces more capacity and higher data speeds, in 80 markets across the country. Sprint currently has twelve devices that are 2x20 capable, including the recently introduced iPhone® 6s and Galaxy® S6 models.

Third-party sources continue to validate Sprint’s improvements in the network experience.

• | Independent mobile analytics firm RootMetrics® awarded Sprint almost 55 percent more first-place (outright or shared) RootScore® Awards for overall, reliability, speed, data, call, or text network performance in the 54 metro markets measured so far in the second half of 2015 compared to the year-ago periodi. The company also saw median downlink speeds in these markets increase by 66 percent on average from the year-ago period, including impressive results in the Denver market, where Sprint received a first-place ranking in network speed for its broad deployment of 2x20 carrier aggregation. |

• | PC Magazine looked at speed test results for LTE connections on Sprint iPhones in early October, finding average download speeds on the two new devices were 50 percent faster than the last generation and the iPhone® 6s demonstrated peak speeds of over 120 Mbps. |

The company remains committed to its plan of significantly densifying the network and continuing to improve performance.

i Rankings based on 54 corresponding RootMetrics Metro RootScore Reports from 2H 2014 and 2H 2015 (July 1 - Oct 12, 2015) for mobile performance as tested on best available plans and devices on four mobile networks across all available network types. Your experiences may vary. The RootMetrics award is not an endorsement of Sprint. Visit www.rootmetrics.com for more details.

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | 6 |

Revenues

• | Net operating revenues of $8 billion for the quarter decreased six percent when compared to the year-ago quarter and one percent when compared to the prior quarter. The year-over-year decrease was driven by lower wireless service revenues due to customer shifts to rate plans associated with device financing options as well as postpaid phone customer losses from prior periods. |

• | Wireless service revenues of $6.4 billion for the quarter were down seven percent year-over-year and two percent sequentially due to customer shifts to rate plans associated with device financing options. |

• | Wireless service revenues + installment plan billings and lease revenues of $7.1 billion for the quarter increased slightly year-over-year and were flat sequentially. The year-over-year decline in wireless service revenues due to customer shifts in rate plans associated with device financing options were offset by higher installment plan billings and lease revenues associated with the growing popularity of the those offerings. |

• | Wireless equipment revenues of $1.1 billion for the quarter increased five percent year-over-year and 11 percent sequentially. The year-over-year increase was driven by higher installment and lease revenue, partially offset by lower upfront revenue recognition as customers continue to shift preferences from subsidy and installment sales to leasing, which recognize revenues over time. The sequential increase was primarily driven by higher leasing revenues. |

• | Wireline revenues of $609 million for the quarter declined $99 million year-over-year and $21 million sequentially. The year-over-year and sequential declines were primarily driven by lower voice rates. |

• | Postpaid Phone Average Billings Per User (ABPU)^* of $70.64 for the quarter increased two percent year-over-year and one percent sequentially. The increases were primarily related to higher installment billings and lease revenues associated with device financing, partially offset by a shift to lower priced rate plans offered in conjunction with device financing options. |

• | Postpaid Average Billings Per Account (ABPA)^* of $166.05 for the quarter increased three percent year-over-year and one percent sequentially. Both year-over-year and sequentially, higher installment billings and lease revenues, in addition to growth in lines per account, more than offset the lower rate plans offered in conjunction with device financing options. |

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | ^ indicates results specific to Sprint Platform 7 |

• | Prepaid Average Revenue Per User (ARPU)^ of $27.54 for the quarter increased $0.35 year-over-year and decreased $0.27 sequentially. The year-over-year increase was primarily driven by changes in the mix of our customer base among our prepaid brands, partially offset by pricing changes in our Boost and Virgin brands while the sequential decrease was mostly driven by the aforementioned pricing changes. |

Operating Expenses

• | Cost of services of $2.5 billion for the quarter increased $24 million year-over-year and $60 million sequentially. The year-over-year increase was due to higher wireless service and repair costs, while the sequential increase was primarily due to higher wireless service and repair and seasonally higher roaming expenses. |

• | Cost of products of $1.3 billion for the quarter declined $1.1 billion year-over-year and $75 million sequentially. The year-over-year lower cost of products is related to the introduction of device leasing options, for which the associated cost is recorded as depreciation expense. |

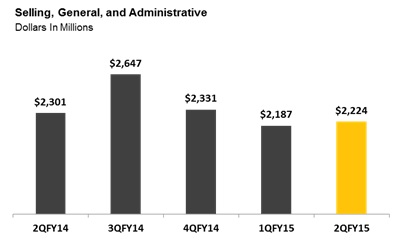

• | SG&A expenses of $2.2 billion for the quarter decreased by $77 million year-over-year and were relatively flat sequentially. The year-over-year decrease was primarily driven by lower bad debt expense as our customer credit profile improved, partially offset by higher expenses related to the RadioShack store expansion. |

• | Depreciation and amortization expense of $1.7 billion for the quarter increased $449 million year-over-year and $155 million sequentially. Both the year-over-year and sequential increases were primarily related to depreciation of devices associated with our leasing options, which were introduced in September 2014. Leased device depreciation was $420 million in the quarter and $276 million in the prior quarter. |

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | ^ indicates results specific to Sprint Platform 8 |

Adjusted EBITDA* & Operating Income (Loss)

• | Adjusted EBITDA* was $2.0 billion for the quarter compared to $1.4 billion in the year-ago quarter and $2.1 billion in the prior quarter. Adjusted EBITDA* increased 45 percent year-over-year as expense reductions more than offset the decline in service revenues. Total expenses improved primarily due to lower cost of product expenses related to device leasing options for which the associated cost is recorded as depreciation expense and lower bad debt expense as a result of a higher acquisition mix of prime credit quality customers in recent quarters. Sequentially, Adjusted EBITDA* was relatively flat. |

• | Operating loss was $2 million in the quarter compared to an operating loss of $192 million in the year-ago quarter and operating income of $501 million in the prior quarter. The improvement from the prior year is due to the items identified in Adjusted EBITDA* above, partially offset by higher depreciation expenses related to leased device assets and severance costs related to work force reductions in the prior year quarter. Sequentially, the reduction in operating income was driven by higher depreciation and an impairment charge related to network assets. |

Capital Expenditures & Free Cash Flow*

• | Cash capital expenditures were $1.7 billion in the quarter compared to $1.1 billion in the year-ago quarter and $2.3 billion in the prior quarter. The year-over-year increase was primarily driven by device leasing in our indirect channels. Capital expenditures associated with device financing were $573 million for the current quarter compared to $544 million in the prior quarter. The sequential decrease of $611 million was primarily driven by lower network capital expenditures. |

• | Free Cash Flow* was negative $100 million for the quarter compared to negative $75 million in the year-ago quarter and negative $2.2 billion in the prior quarter. Normalizing for the $400 million received from the sale of receivables in the quarter and a $500 million repayment under the facility in the prior quarter, free cash flow* would have been negative $500 million in the current quarter and negative $1.7 billion in the prior quarter, respectively. The normalized year-over-year change was primarily impacted by unfavorable changes to working capital and higher capital expenditures, as the shift to installment billing and leasing for devices from the subsidy model shifts customer payments for devices from the point of sale to over time. Sequentially, the improvement was mostly related to lower network-related capital expenditures and favorable changes to working capital. |

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | 9 |

Liquidity & Debt

• | Total liquidity was $5.9 billion at the end of the quarter including $2.1 billion of cash, cash equivalents and short-term investments, $2.9 billion of undrawn borrowing capacity under the revolving bank credit facility, and $900 million of undrawn capacity under the receivables facility. In addition, the company had $1.2 billion of availability under vendor financing agreements that can be utilized toward the purchase of 2.5 GHz network equipment. |

• | Net Debt* excluding net premiums was $30.9 billion at the end of the quarter. This compares to $25.7 billion in the year-ago quarter and $30.8 billion in the prior quarter. |

Device Financing

• | Net Installment receivables at the end of the quarter were $1.1 billion compared to $1.2 billion both at the end of the year-ago quarter and the prior quarter. The year-over-year and sequential decline was primarily driven by billings for prior period sales exceeding new installment billing sales. |

• | Leased Devices included in net PP&E at the end of the quarter were $3.6 billion. The $780 million sequential increase was primarily due to a $1.1 billion increase in leased devices in gross PP&E, which was driven by a 51 percent leasing take rate for postpaid sales in the quarter. |

Financial Outlook

• | Including transformation program costs, the company now expects fiscal year 2015 Adjusted EBITDA* to be at the low end of the previous expectation of $7.2 to $7.6 billion. This excludes any impacts from the potential sale of certain devices being leased by our customers. |

• | The company continues to expect fiscal year 2015 cash capital expenditures to be approximately $5 billion, excluding the impact of leased devices sold through indirect channels. |

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | 10 |

Wireless Operating Statistics (Unaudited)

Quarter To Date | Year To Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Sprint platform (1): | ||||||||||||||||

Net additions (losses) (in thousands) | ||||||||||||||||

Postpaid (2) | 553 | 310 | (272 | ) | 863 | (453 | ) | |||||||||

Prepaid (2) | (363 | ) | (366 | ) | 35 | (729 | ) | (507 | ) | |||||||

Wholesale and affiliate | 866 | 731 | 827 | 1,597 | 1,330 | |||||||||||

Total Sprint platform wireless net additions | 1,056 | 675 | 590 | 1,731 | 370 | |||||||||||

End of period connections (in thousands) | ||||||||||||||||

Postpaid (2) | 30,569 | 30,016 | 29,465 | 30,569 | 29,465 | |||||||||||

Prepaid (2) | 14,977 | 15,340 | 14,750 | 14,977 | 14,750 | |||||||||||

Wholesale and affiliate | 12,322 | 11,456 | 9,706 | 12,322 | 9,706 | |||||||||||

Total Sprint platform end of period connections | 57,868 | 56,812 | 53,921 | 57,868 | 53,921 | |||||||||||

Churn | ||||||||||||||||

Postpaid | 1.54 | % | 1.56 | % | 2.18 | % | 1.55 | % | 2.12 | % | ||||||

Prepaid | 5.07 | % | 5.08 | % | 3.76 | % | 5.07 | % | 4.10 | % | ||||||

Supplemental data - connected devices | ||||||||||||||||

End of period connections (in thousands) | ||||||||||||||||

Retail postpaid | 1,576 | 1,439 | 1,039 | 1,576 | 1,039 | |||||||||||

Wholesale and affiliate | 7,338 | 6,620 | 4,635 | 7,338 | 4,635 | |||||||||||

Total | 8,914 | 8,059 | 5,674 | 8,914 | 5,674 | |||||||||||

Supplemental data - total company | ||||||||||||||||

End of period connections (in thousands) | ||||||||||||||||

Sprint platform (1) | 57,868 | 56,812 | 53,921 | 57,868 | 53,921 | |||||||||||

Transactions (3) | 710 | 856 | 1,116 | 710 | 1,116 | |||||||||||

Total | 58,578 | 57,668 | 55,037 | 58,578 | 55,037 | |||||||||||

Sprint platform ARPU (1) (a) | ||||||||||||||||

Postpaid | $ | 54.02 | $ | 55.48 | $ | 60.58 | $ | 54.74 | $ | 61.33 | ||||||

Prepaid | $ | 27.54 | $ | 27.81 | $ | 27.19 | $ | 27.68 | $ | 27.28 | ||||||

NON-GAAP RECONCILIATION - ABPA*, POSTPAID PHONE ARPU and ABPU* (Unaudited)

(Millions, except accounts, connections, ABPA*, ARPU, and ABPU*)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Sprint platform ABPA* (1) (b) | ||||||||||||||||

Postpaid service revenue | $ | 4,900 | $ | 4,964 | $ | 5,377 | $ | 9,864 | $ | 10,930 | ||||||

Add: Installment plan billings and lease revenue | 694 | 554 | 193 | 1,248 | 330 | |||||||||||

Total for Sprint platform postpaid connections | $ | 5,594 | $ | 5,518 | $ | 5,570 | $ | 11,112 | $ | 11,260 | ||||||

Sprint platform postpaid accounts (in thousands) | 11,226 | 11,175 | 11,521 | 11,201 | 11,637 | |||||||||||

Sprint platform postpaid ABPA* | $ | 166.05 | $ | 164.63 | $ | 161.12 | $ | 165.34 | $ | 161.23 | ||||||

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Sprint platform postpaid phone ARPU and ABPU* (1) | ||||||||||||||||

Postpaid phone service revenue | $ | 4,615 | $ | 4,682 | $ | 5,096 | $ | 9,297 | $ | 10,390 | ||||||

Add: Installment plan billings and lease revenue | 665 | 531 | 183 | 1,196 | 312 | |||||||||||

Total for Sprint platform postpaid phone connections | $ | 5,280 | $ | 5,213 | $ | 5,279 | $ | 10,493 | $ | 10,702 | ||||||

Sprint platform postpaid average phone connections (in thousands) | 24,915 | 24,856 | 25,499 | 24,885 | 25,785 | |||||||||||

Sprint platform postpaid phone ARPU (a) | $ | 61.74 | $ | 62.79 | $ | 66.62 | $ | 62.26 | $ | 67.16 | ||||||

Sprint platform postpaid phone ABPU* (c) | $ | 70.64 | $ | 69.91 | $ | 69.02 | $ | 70.27 | $ | 69.18 | ||||||

(a) ARPU is calculated by dividing service revenue by the sum of the monthly average number of connections in the applicable service category. Changes in average monthly service revenue reflect connections for either the postpaid or prepaid service category who change rate plans, the level of voice and data usage, the amount of service credits which are offered to connections, plus the net effect of average monthly revenue generated by new connections and deactivating connections.

Sprint platform postpaid phone ARPU represents revenues related to our postpaid phone connections.

(b) Sprint platform postpaid ABPA* is calculated by dividing service revenue earned from connections plus installment plan billings and lease revenue by the sum of the monthly average number of accounts during the period.

(c) Sprint platform postpaid phone ABPU* is calculated by dividing postpaid phone service revenue earned from postpaid phone connections plus installment plan billings and lease revenue by the sum of the monthly average number of postpaid phone connections during the period.

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | 11 |

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

(Millions, except per Share Data)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net operating revenues | ||||||||||||||||

Service revenue | $ | 6,880 | $ | 7,037 | $ | 7,449 | $ | 13,917 | $ | 15,132 | ||||||

Equipment revenue | 1,095 | 990 | 1,039 | 2,085 | 2,145 | |||||||||||

Total net operating revenues | 7,975 | 8,027 | 8,488 | 16,002 | 17,277 | |||||||||||

Net operating expenses | ||||||||||||||||

Cost of services (exclusive of depreciation and amortization below) | 2,453 | 2,393 | 2,429 | 4,846 | 4,949 | |||||||||||

Cost of products (exclusive of depreciation and amortization below) | 1,290 | 1,365 | 2,372 | 2,655 | 4,530 | |||||||||||

Selling, general and administrative | 2,224 | 2,187 | 2,301 | 4,411 | 4,585 | |||||||||||

Depreciation and amortization | 1,743 | 1,588 | 1,294 | 3,331 | 2,575 | |||||||||||

Impairments (4) | 85 | — | — | 85 | — | |||||||||||

Other, net | 182 | (7 | ) | 284 | 175 | 311 | ||||||||||

Total net operating expenses | 7,977 | 7,526 | 8,680 | 15,503 | 16,950 | |||||||||||

Operating (loss) income | (2 | ) | 501 | (192 | ) | 499 | 327 | |||||||||

Interest expense | (542 | ) | (542 | ) | (510 | ) | (1,084 | ) | (1,022 | ) | ||||||

Other income, net | 5 | 4 | 8 | 9 | 9 | |||||||||||

Loss before income taxes | (539 | ) | (37 | ) | (694 | ) | (576 | ) | (686 | ) | ||||||

Income tax (expense) benefit | (46 | ) | 17 | (71 | ) | (29 | ) | (56 | ) | |||||||

Net loss | $ | (585 | ) | $ | (20 | ) | $ | (765 | ) | $ | (605 | ) | $ | (742 | ) | |

Basic and diluted net loss per common share | $ | (0.15 | ) | $ | (0.01 | ) | $ | (0.19 | ) | $ | (0.15 | ) | $ | (0.19 | ) | |

Weighted average common shares outstanding | 3,969 | 3,967 | 3,949 | 3,968 | 3,947 | |||||||||||

Effective tax rate | -8.5 | % | 45.9 | % | -10.2 | % | -5.0 | % | -8.2 | % | ||||||

NON-GAAP RECONCILIATION - NET LOSS TO ADJUSTED EBITDA* (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net loss | $ | (585 | ) | $ | (20 | ) | $ | (765 | ) | $ | (605 | ) | $ | (742 | ) | |

Income tax expense (benefit) | 46 | (17 | ) | 71 | 29 | 56 | ||||||||||

Loss before income taxes | (539 | ) | (37 | ) | (694 | ) | (576 | ) | (686 | ) | ||||||

Other income, net | (5 | ) | (4 | ) | (8 | ) | (9 | ) | (9 | ) | ||||||

Interest expense | 542 | 542 | 510 | 1,084 | 1,022 | |||||||||||

Operating (loss) income | (2 | ) | 501 | (192 | ) | 499 | 327 | |||||||||

Depreciation and amortization | 1,743 | 1,588 | 1,294 | 3,331 | 2,575 | |||||||||||

EBITDA* | 1,741 | 2,089 | 1,102 | 3,830 | 2,902 | |||||||||||

Impairments (4) | 85 | — | — | 85 | — | |||||||||||

Severance and exit costs (5) | 25 | 13 | 284 | 38 | 311 | |||||||||||

Litigation (6) | 157 | — | — | 157 | — | |||||||||||

Reduction in liability - U.S. Cellular asset acquisition (7) | — | (20 | ) | — | (20 | ) | — | |||||||||

Adjusted EBITDA* | $ | 2,008 | $ | 2,082 | $ | 1,386 | $ | 4,090 | $ | 3,213 | ||||||

Adjusted EBITDA margin* | 29.2 | % | 29.6 | % | 18.6 | % | 29.4 | % | 21.2 | % | ||||||

Selected items: | ||||||||||||||||

Cash paid for capital expenditures - network and other | $ | 1,162 | $ | 1,802 | $ | 1,143 | $ | 2,964 | $ | 2,389 | ||||||

Cash paid for capital expenditures - leased devices | $ | 573 | $ | 544 | $ | — | $ | 1,117 | $ | — | ||||||

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | 12 |

WIRELESS STATEMENTS OF OPERATIONS (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net operating revenues | ||||||||||||||||

Service revenue | ||||||||||||||||

Sprint platform (1): | ||||||||||||||||

Postpaid | $ | 4,900 | $ | 4,964 | $ | 5,377 | $ | 9,864 | $ | 10,930 | ||||||

Prepaid | 1,252 | 1,300 | 1,197 | 2,552 | 2,418 | |||||||||||

Wholesale, affiliate and other | 185 | 181 | 181 | 366 | 344 | |||||||||||

Total Sprint platform | 6,337 | 6,445 | 6,755 | 12,782 | 13,692 | |||||||||||

Total transactions (3) | 84 | 105 | 135 | 189 | 285 | |||||||||||

Total service revenue | 6,421 | 6,550 | 6,890 | 12,971 | 13,977 | |||||||||||

Equipment revenue | 1,095 | 990 | 1,039 | 2,085 | 2,145 | |||||||||||

Total net operating revenues | 7,516 | 7,540 | 7,929 | 15,056 | 16,122 | |||||||||||

Net operating expenses | ||||||||||||||||

Cost of services (exclusive of depreciation and amortization below) | 2,111 | 2,005 | 1,988 | 4,116 | 4,037 | |||||||||||

Cost of products (exclusive of depreciation and amortization below) | 1,290 | 1,365 | 2,372 | 2,655 | 4,530 | |||||||||||

Selling, general and administrative | 2,136 | 2,096 | 2,199 | 4,232 | 4,392 | |||||||||||

Depreciation and amortization | 1,694 | 1,540 | 1,232 | 3,234 | 2,444 | |||||||||||

Impairments (4) | 85 | — | — | 85 | — | |||||||||||

Other, net | 181 | (8 | ) | 248 | 173 | 271 | ||||||||||

Total net operating expenses | 7,497 | 6,998 | 8,039 | 14,495 | 15,674 | |||||||||||

Operating income (loss) | $ | 19 | $ | 542 | $ | (110 | ) | $ | 561 | $ | 448 | |||||

WIRELESS NON-GAAP RECONCILIATION (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Operating income (loss) | $ | 19 | $ | 542 | $ | (110 | ) | $ | 561 | $ | 448 | |||||

Impairments (4) | 85 | — | — | 85 | — | |||||||||||

Severance and exit costs (5) | 24 | 12 | 248 | 36 | 271 | |||||||||||

Litigation (6) | 157 | — | — | 157 | — | |||||||||||

Reduction in liability - U.S. Cellular asset acquisition (7) | — | (20 | ) | — | (20 | ) | — | |||||||||

Depreciation and amortization | 1,694 | 1,540 | 1,232 | 3,234 | 2,444 | |||||||||||

Adjusted EBITDA* | $ | 1,979 | $ | 2,074 | $ | 1,370 | $ | 4,053 | $ | 3,163 | ||||||

Adjusted EBITDA margin* | 30.8 | % | 31.7 | % | 19.9 | % | 31.2 | % | 22.6 | % | ||||||

Selected items: | ||||||||||||||||

Cash paid for capital expenditures - network and other | $ | 1,003 | $ | 1,640 | $ | 989 | $ | 2,643 | $ | 2,109 | ||||||

Cash paid for capital expenditures - leased devices | $ | 573 | $ | 544 | $ | — | $ | 1,117 | $ | — | ||||||

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | 13 |

WIRELINE STATEMENTS OF OPERATIONS (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net operating revenues | ||||||||||||||||

Voice | $ | 212 | $ | 233 | $ | 294 | $ | 445 | $ | 621 | ||||||

Data | 43 | 49 | 53 | 92 | 109 | |||||||||||

Internet | 323 | 328 | 340 | 651 | 685 | |||||||||||

Other | 31 | 20 | 21 | 51 | 39 | |||||||||||

Total net operating revenues | 609 | 630 | 708 | 1,239 | 1,454 | |||||||||||

Net operating expenses | ||||||||||||||||

Cost of services (exclusive of depreciation and amortization below) | 495 | 534 | 593 | 1,029 | 1,219 | |||||||||||

Selling, general and administrative | 85 | 87 | 88 | 172 | 173 | |||||||||||

Depreciation and amortization | 48 | 46 | 60 | 94 | 127 | |||||||||||

Other, net | 1 | 1 | 35 | 2 | 39 | |||||||||||

Total net operating expenses | 629 | 668 | 776 | 1,297 | 1,558 | |||||||||||

Operating loss | $ | (20 | ) | $ | (38 | ) | $ | (68 | ) | $ | (58 | ) | $ | (104 | ) | |

WIRELINE NON-GAAP RECONCILIATION (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Operating loss | $ | (20 | ) | $ | (38 | ) | $ | (68 | ) | $ | (58 | ) | $ | (104 | ) | |

Severance and exit costs (5) | 1 | 1 | 35 | 2 | 39 | |||||||||||

Depreciation and amortization | 48 | 46 | 60 | 94 | 127 | |||||||||||

Adjusted EBITDA* | $ | 29 | $ | 9 | $ | 27 | $ | 38 | $ | 62 | ||||||

Adjusted EBITDA margin* | 4.8 | % | 1.4 | % | 3.8 | % | 3.1 | % | 4.3 | % | ||||||

Selected items: | ||||||||||||||||

Cash paid for capital expenditures - network and other | $ | 63 | $ | 68 | $ | 65 | $ | 131 | $ | 124 | ||||||

SPRINT QUARTERLY INVESTOR UPDATE - FISCAL 2Q15 | 14 |

CONDENSED CONSOLIDATED CASH FLOW INFORMATION (Unaudited)

(Millions)

Year to Date | ||||||

9/30/15 | 9/30/14 | |||||

Operating activities | ||||||

Net loss | $ | (605 | ) | $ | (742 | ) |

Impairments (4) | 85 | — | ||||

Depreciation and amortization | 3,331 | 2,575 | ||||

Provision for losses on accounts receivable | 278 | 493 | ||||

Share-based and long-term incentive compensation expense | 40 | 65 | ||||

Deferred income tax expense | 28 | 28 | ||||

Amortization of long-term debt premiums, net | (157 | ) | (149 | ) | ||

Other changes in assets and liabilities: | ||||||

Accounts and notes receivable | (1,357 | ) | (828 | ) | ||

Inventories and other current assets | 173 | (155 | ) | |||

Accounts payable and other current liabilities | (509 | ) | 503 | |||

Non-current assets and liabilities, net | 125 | (146 | ) | |||

Other, net | 365 | 63 | ||||

Net cash provided by operating activities | 1,797 | 1,707 | ||||

Investing activities | ||||||

Capital expenditures - network and other | (2,964 | ) | (2,389 | ) | ||

Capital expenditures - leased devices | (1,117 | ) | — | |||

Expenditures relating to FCC licenses | (45 | ) | (79 | ) | ||

Reimbursements relating to FCC licenses | — | 95 | ||||

Change in short-term investments, net | 63 | 53 | ||||

Proceeds from sales of assets and FCC licenses | 4 | 101 | ||||

Other, net | (21 | ) | (6 | ) | ||

Net cash used in investing activities | (4,080 | ) | (2,225 | ) | ||

Financing activities | ||||||

Proceeds from debt and financings | 434 | — | ||||

Repayments of debt, financing and capital lease obligations | (206 | ) | (363 | ) | ||

Proceeds from issuance of common stock, net | 8 | 46 | ||||

Other, net | 9 | — | ||||

Net cash provided by (used in) financing activities | 245 | (317 | ) | |||

Net decrease in cash and cash equivalents | (2,038 | ) | (835 | ) | ||

Cash and cash equivalents, beginning of period | 4,010 | 4,970 | ||||

Cash and cash equivalents, end of period | $ | 1,972 | $ | 4,135 | ||

RECONCILIATION TO CONSOLIDATED FREE CASH FLOW* (NON-GAAP) (Unaudited)

(Millions)

Quarter to Date | Year to Date | |||||||||||||||

9/30/15 | 6/30/15 | 9/30/14 | 9/30/15 | 9/30/14 | ||||||||||||

Net cash provided by operating activities | $ | 1,669 | $ | 128 | $ | 1,028 | $ | 1,797 | $ | 1,707 | ||||||

Capital expenditures - network and other | (1,162 | ) | (1,802 | ) | (1,143 | ) | (2,964 | ) | (2,389 | ) | ||||||

Capital expenditures - leased devices | (573 | ) | (544 | ) | — | (1,117 | ) | — | ||||||||

(Expenditures) reimbursements relating to FCC licenses, net | (19 | ) | (26 | ) | (38 | ) | (45 | ) | 16 | |||||||

Proceeds from sales of assets and FCC licenses | 3 | 1 | 81 | 4 | 101 | |||||||||||

Other investing activities, net | (18 | ) | (3 | ) | (3 | ) | (21 | ) | (6 | ) | ||||||

Free cash flow* | $ | (100 | ) | $ | (2,246 | ) | $ | (75 | ) | $ | (2,346 | ) | $ | (571 | ) | |