Form 8-K HYSTER-YALE MATERIALS For: Mar 23

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d)

of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): March 23, 2015

HYSTER-YALE MATERIALS HANDLING, INC.

(Exact name of registrant as specified in its charter)

| DELAWARE | 000-54799 | 31-1637659 | ||

| (State or other jurisdiction of incorporation) |

(Commission File Number) |

(IRS Employer Identification No.) |

| 5875 LANDERBROOK DRIVE, SUITE 300, CLEVELAND, OHIO | 44124-4069 | |

| (Address of principal executive offices) | (Zip code) |

(440) 449-9600

(Registrant’s telephone number, including area code)

N/A

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| Item 2.02 | Results of Operations and Financial Condition. |

On March 23, 2015, Hyster-Yale Materials Handling, Inc. (the “Company”) posted on its website, www.hyster-yale.com, an updated investor presentation for its Investor Day. A copy is attached as Exhibit 99 hereto.

| Item 7.01 | Regulation FD Disclosure. |

The information disclosed above under Item 2.02 with respect to the investor presentation and background information is incorporated herein by reference.

The information contained in this Current Report on Form 8-K, including Exhibit 99, is furnished pursuant to Item 2.02 and Item 7.01 of Form 8-K and shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, or otherwise subject to the liability of that section, nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, except as shall be expressly stated by specific reference in such filing.

| Item 9.01 | Financial Statements and Exhibits. |

(d) Exhibits.

| Exhibit Number |

Description | |

| 99 | Hyster-Yale Materials Handling, Inc. Investor Presentation, dated March 23, 2015 | |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Date: March 23, 2015 | HYSTER-YALE MATERIALS HANDLING, INC. | |||||

| By: | /s/ Kenneth C. Schilling | |||||

| Name: | Kenneth C. Schilling | |||||

| Title: | Senior Vice President and Chief Financial Officer | |||||

EXHIBIT INDEX

| Exhibit |

Description | |

| 99 | Hyster-Yale Materials Handling, Inc. Investor Presentation, dated March 23, 2015 | |

Exhibit

99 |

Christina

Kmetko

Investor Relations |

Safe

Harbor Statement The following information includes forward-looking

statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section

21E of the Securities Exchange Act of 1934, as amended. Any and all statements

regarding the Company’s expected future financial position, results of

operations, cash flows, business strategy, budgets, projected costs, capital

expenditures, products, competitive positions, growth opportunities, plans,

goals

and

objectives

of

management

for

future

operations,

as

well

as

statements

that

include

words

such

as

“anticipate,”

“if,”

“believe,”

“plan,”

“estimate,”

“expect,”

“intend,”

“may,”

“could,”

“should,”

“will,”

and other similar expressions are forward-looking statements. Such

forward-looking statements are inherently uncertain, and readers must

recognize that actual results may differ materially from the expectations of the Company’s management. The

Company does not undertake a duty to update such forward-looking statements.

Among the factors that could cause plans, actions and results to differ

materially from current expectations include, without limitation, reduction in

demand for lift trucks and related aftermarket parts and service on a global

basis, the ability of dealers, suppliers and end-users to obtain financing at

reasonable rates, or at all, as a result of current economic and market

conditions, the political and economic uncertainties in Eastern Europe and Brazil,

customer acceptance of pricing, delays in delivery or increases in costs,

including transportation costs, of raw materials or sourced products and labor or

changes in or unavailability of quality suppliers, exchange rate

fluctuations, changes in non-U.S. import tariffs and monetary policies and

other changes in the regulatory climate in the non-U.S. countries in which the

Company operates and/or sells products, delays in manufacturing and delivery

schedules, bankruptcy of or loss of major dealers, retail customers or

suppliers, customer acceptance of, changes in the costs of, or delays in the

development of new products, introduction of new products by, or more

favorable product pricing offered by, competitors, product liability or other

litigation, warranty claims or returns of products, the effectiveness of the cost

reduction programs implemented globally, including the successful implementation of

procurement and sourcing initiatives, changes mandated by federal, state and

other regulation, including health, safety or environmental legislation, delays in or increased costs associated with the Brazil plant construction

and relocation, the successful commercialization of Nuvera Fuel Cells' technology

and integration of the acquisition, the introduction of a more accepted

product to the market by a competitor, making the Nuvera technology less marketable

and other risks identified in the Company’s Annual Report on Form

10-K

and

other

filings

with

the

Securities

and

Exchange

Commission.

Many

of

these

factors

are

outside

of

the

Company’s

control. |

Today’s Presenters

Christina Kmetko

Investor Relations

Al Rankin

Chairman, President and Chief Executive Officer of Hyster-Yale

Colin Wilson

President and Chief Executive Officer of NACCO Materials Handling Group

Vickie Rickey

Senior Vice President, Asia-Pacific and Brazil

Chuck Pascarelli

Senior Vice President, President, Americas

Ralf Mock

Senior Vice President, Managing Director, Europe, Middle East and Africa

Rajiv Prasad

Senior Vice President, Global Product Development, Manufacturing and Supply Chain Strategy

Scott Blanchet

Vice President of Product Management, Nuvera

Jon Taylor

Vice President, Business Development and CEO of Nuvera

Ken Schilling

Senior Vice President and Chief Financial Officer |

Agenda

11:30

11:35

Welcome and Introductions

11:35

12:05

Overview - Our Business

12:05

12:35

Our Brands, Markets and Growth Strategies

12:35

01:00

Growth in our JAPIC and Brazil Business Operations

01:00

01:20

Growth in our Americas Operations

01:20

01:35

Break

01:35

01:55

Growth in our EMEA Operations

01:55

02:15

The Products and Technology to Help Us Grow

02:15

02:25

Nuvera Products

02:25

02:35

Commercialization of our Nuvera Business

02:35

02:50

Financial Overview and the Importance of Volume Growth

02:50

02:55

Our Commitment to Growth: Our Products

02:55

03:00

Our Commitment to Growth: 7% Target and Substantial Cash Generation

03:00

03:45

Questions

03:45

05:00

Booth Walk-Throughs

Hyster-Yale Investor Day |

Overview:

Our

Business

Alfred M.

Rankin, Jr.

Chairman, President and

Chief Executive Officer

Hyster-Yale Materials Handling

Chairman

NACCO Materials Handling Group |

Our

Business is Materials Handling 7 |

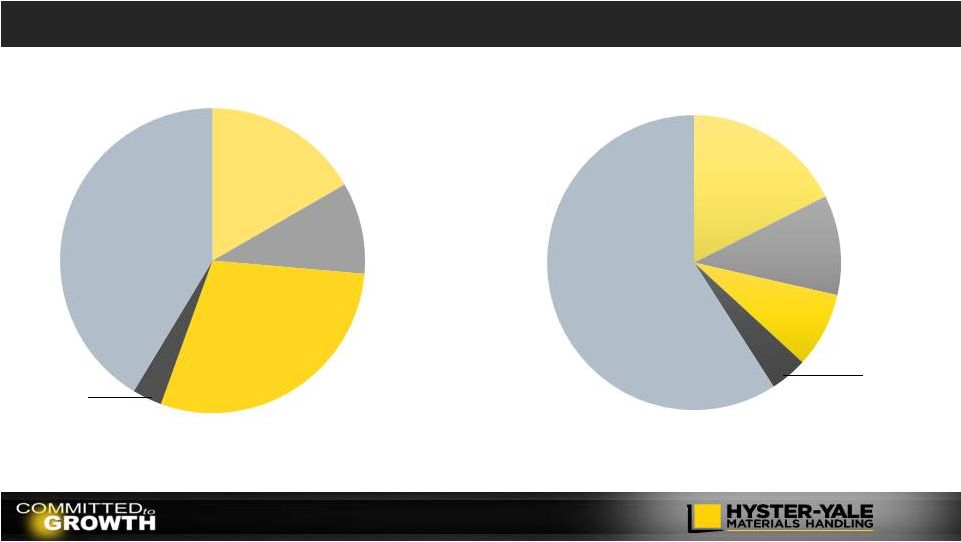

Lift

Truck Industry Total Industry = 1,088k Units

Market

Size

-

Units

Market Size -

$

8

_____________________

Source: WITS. 2014 Orders Reports.

_____________________

Source: Internal Company estimates

Estimated Industry Revenue Mix

Class 1

17%

Class 2

10%

Class 3

29%

Class 4

3%

Class 5

41%

Class 1

18%

Class 2

11%

Class 3

8%

Class 4

4%

Class 5

59% |

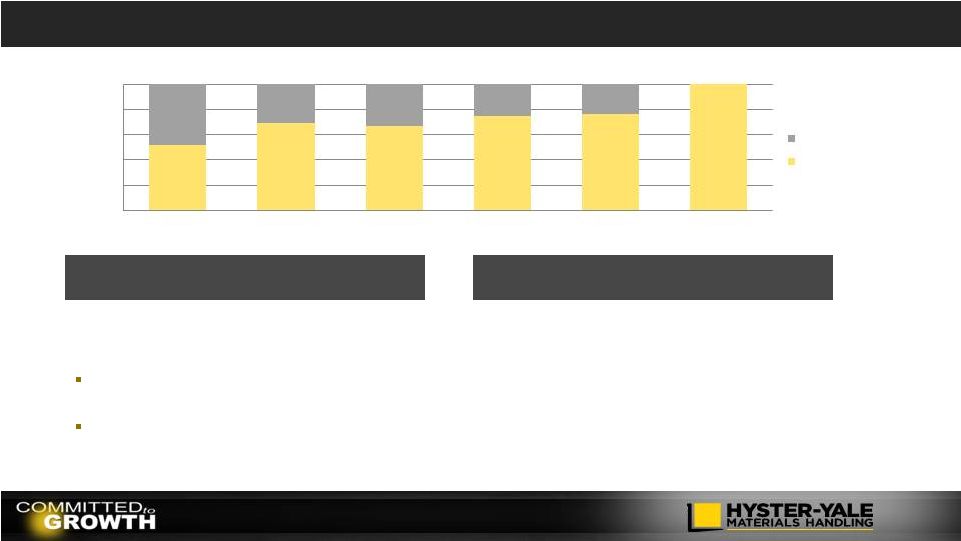

Industry Overview

(units in thousands)

Global Lift Truck Industry Size

_____________________

Trend line represents 4.5% CAGR from 2006-2008 Average Industry Size. Source:

WITS. Represents order intake. Global Lift Truck Industry Breakdown

(Units) Long-term

CAGR

(2004

–

2014)

=

4.5%

In last 5 years, global market lift

truck growth significantly outpaced

GDP growth at 2.4x

(1)

GDP

Global Lift Truck Industry Size

Global Industry Growth

_____________________

Source: WITS. FY 12/31/14 and 12/31/13 order intake.

9

_____________________

Source: WITS. 2014 Orders Reports.

_____________________

(1) Calculated based on CAGRs for new truck sales and GDP for 2009-2014

Europe

31%

China

25%

Americas

25%

Asia Pacific 7%

Middle East &

Africa

5%

Change over Prior Year

Total

Americas

Brazil

EMEA

JAPIC

+8%

+8%

-13%

+8%

+8%

951

872

547

794

975

944

1,009

1,088

0

300

600

900

1,200

2007

2008

2009

2010

2011

2012

2013

2014

Japan 7% |

Sources of Revenue

2014

Worldwide

Sales

by

Product

2014

Retail

Shipments

by

End

Market

(1)

_____________________

(1)

Represents Hyster-Yale North American unit shipments by industry.

(2)

Includes Big Truck sales that represent 11.3% of total sales.

10

Americas

67%

Europe, Africa

& Middle East

25%

Asia-Pacific

8%

Manufacturing

27%

Wholesale Distribution

14%

Food & Beverage

13%

Rental

10%

Home Centers/ Retail

11%

Freight & Logistics

10%

Paper

6%

Other

9%

Internal

Combustion

Engine

Units

(2)

55%

Electric

Units

28%

Parts

13%

Other

4%

2014 Sales by Geography |

Hyster-Yale Business Structure

Public Company

Governance

Small Corporate Staff

Geographic

11

Platform to Integrate

Other Brands

Operating Company

Execution of Strategy

Public entity

Guides Strategic Vision

Hyster-Yale (HY)

NACCO Materials Handling Group

(NMHG

)

Hyster

®

Brand

Yale

®

Brand

UTILEV

®

Nuvera

®

Future?

Hyster-Yale

The Public

Company

11 Directors

(7 independent)

NACCO Materials

Handling Group

The Operating

Company

HY Board plus Operating

Company CEO and one

additional independent

director

Over 5,400

Employees

•

Hyster-Yale

Executives

•

Legal

•

Finance

•

Internal Audit

•

Tax |

Our

Long-Term Philosophy Long-term

growth

Long-term

shareholders

Shareholder

protection

Senior

management

incentivized as

long-term

shareholders

Increase

shareholder

value

Return on Capital

Employed and

Market Share

Increase focus

12 |

Key

Events Since 1989 Wednesfield(UK)/

Brunswick (USA)

Danville (USA)

Lenoir (USA)

Irvine (UK)

Modena (Italy)

Elimination of Retiree

Medical

Freezing Defined

Benefit Plans

Engineering

Manufacturing

Supply Chain

Information

Technology

Moved from 2 Brand

companies to

1 company

managing several

brands

Co-located

Area Leadership

Restructured

Distribution network

Plants Rationalized

Benefits

Restructured

Functions

Consolidated

Marketing Structure

Evolved

13 |

Hyster-Yale Today: An Efficient and Productive Organization

14 |

The

Transition 15

Maturity of key programs designed to put

us in the position of having the right

products at the right cost and right

quality

Commitment to the marketing and

support programs which can enable a

period of share gain

Hyster-Yale spin-off from

NACCO Industries

Two years

ago the

company

reached

a key

transition

point |

Hyster-Yale Snapshot

Hyster-Yale Materials Handling, Inc. (NYSE: HY)

Leading global designer, manufacturer and marketer of

lift trucks and provider of aftermarket parts and support

Headquartered in Cleveland, Ohio

Over 5,400 employees globally

FY 12/31/14 Revenue –

$2.8 billion

FY 12/31/14 Net income

(1)

-

$109.8 million

FY 12/31/14 EBITDA

(1)(2)

–

$182.6 million

12/31/14 Net cash –

$79.9 million

FY 12/31/14 ROTCE

(1)(2)

of 28.3% (Net cash basis)

16

(1)

Net income, EBITDA and ROTCE for the FY 12/31/14 include a $17.7 million pre-tax

gain on the sale of the Brazil land and facility.

(2)

EBITDA and ROTCE are non-GAAP measures and should not be considered in isolation or

as a substitute for GAAP measures. For discussion of non-GAAP items and the

related reconciliations to GAAP measures, see information in the Appendix at the end of

this presentation. |

Over

the next three years…. A period of

share growth

Get to

115,000

trucks irrespective of industry size

Use of cash to support

technology accelerators

Fuel Cells

Automation

Telemetry

Use of cash to

support strategic

alliances

17 |

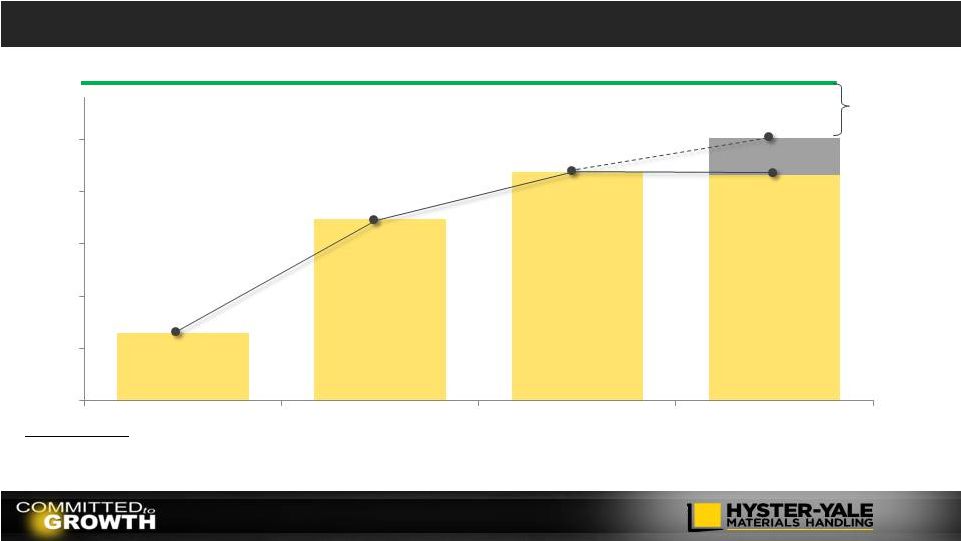

Operating

Profit at the

mid-point of

the next cycle

Operating

Profit at the

peak of this

cycle

18

7%

7%

With adequate

volume

growth we

can meet our

public

operating

profit

commitments |

$30

million fixed cost absorption by moving from 75%

capacity utilization to full utilization of our

manufacturing capacity

$40 million

by meeting target economics in standard

margin net of increased SG&A spread

over more units

25,000

units of additional

volume

$70 million

of operating profit

19 |

Mission Statement Redefined

Be a leading globally integrated designer, manufacturer

and marketer of a complete range of high quality,

application-tailored lift trucks, offering the lowest cost of

ownership, outstanding parts and service support and

the best overall value.

Our transition had its roots in our initiation of the Good to Great strategic

thinking process in 2010 which began with a redefinition of NMHG’s

mission statement 20 |

The

Basic Philosophies That Guide Our Actions Global supplier of lift

trucks and related

services

Best at understanding and

addressing the needs of

customers

Brands focused on unique

segments of the market

Market share growth

Market through exclusive,

independent, certified

distribution

Sell direct to large

customers

Capture full aftermarket

potential

Customer

Internal

Distribution

Full line product supplier to meet the

needs of major customer segments

Modular/scalable components to create

the right product at right cost

Supply chain organization to deliver high

quality / low cost components

Assemble in market of sale to meet

customer needs quickly

Product quality to deliver the best uptime

in the industry

An environment that motivates and retains

high quality employees

21 |

The

“Hedgehog” Concept

22

An ECONOMIC ENGINE driven

by market share leadership

which generates greater relative

economies of scale, parts volume

and ancillary services

PASSIONATE ABOUT

market share leadership

gained by understanding

customer

needs

and

delivering the product

performance, quality and

cost to meet those needs

BEST AT independent

distribution and direct

selling

to deliver the

right truck and services

for each customer

application at the lowest

cost of ownership

What drives

our economic

engine?

What can we

be Best in

World at?

What are we

passionate

about? |

Hyster-Yale’s Economic Engine

23

Hyster-Yale’s

economic

engine

is

driven

by

increasing

unit

volume

as

our

“hedgehog”

approach

gets

embedded in all our activities and our flywheels increase momentum…

Geographic

and Product

Balance

Worldwide Distribution

Strength to Drive

Market Share

Parts and Service

Volume

Large Lift Truck

Population in Service

Volume

Economies

of Scale

A large lift truck population base drives parts and service volume resulting in enhanced

profitability for dealers and Hyster-Yale Design

Component

Commonality

Supply Chain

Manufacturing

Quality

Marketing

Parts

Infrastructure

Capital Requirements |

Core

Strategic Initiatives Basic Business Areas

Our strategies are designed to drive increased share,

which in turn increases the lift truck population, which

drives parts and service volumes.

Geographic

and Product

Balance

Worldwide

Distribution

Strength

to Drive

Market Share

Parts and Service

Volume

Large Lift Truck

Population in Service

Volume

Economies

of Scale

Design

Component Commonality

Supply Chain

Manufacturing

Quality

Marketing

Parts

Infrastructure

Capital Requirements

Improve

Warehouse

Position

Enhance

Independent

Distribution

Succeed in

Asia

Enhance Big

Truck Market

Position

Strengthen the Sales and

Marketing Organization

Low Cost of

Ownership

Understand

Customer Needs

And core strategic initiatives were designed to drive the economic engine by

increasing share… 24

Commercialize

Nuvera’s

Technology |

Early

Stage Mid Stage

Achieved

Breakthrough

Understand Customer Needs

Low Cost of Ownership

Enhance Independent Distribution

Improve Warehouse Position

Succeed in Asia

Enhance Big Truck Market Position

Strengthen Sales and Marketing Organization

Commercialize Nuvera’s Fuel Cell Technology

We believe our core strategic initiative flywheels

are in various stages of momentum…

Core

Strategic

Initiatives

–

Stages

of

Momentum

25 |

Early

Stage Mid Stage

Achieved

Breakthrough

Product Improvement

Supply Chain

Manufacturing

Quality

Pricing

Dealer Structure and Excellence

Area Sales Management

Account Identification and Coverage

Solutions Groups

Aftermarket

Fleet

We believe momentum is gaining in all key

areas of the business…

Key

Business

Areas

–

Stages

of

Momentum

26 |

27

The HY “hedgehog”

can

lead to a thicket of activities which

can generate a leadership share and

profitability position in our industry.

requires the

creation of a unique, valuable and sustainable

position involving a different set of

activities from our competitors…

Deliver greater value to customers or create

comparable value at lower prices, or both.

Long-term competitive advantage |

People Philosophy

Drive P&L’s

closer to the

customer

Base incentive

compensation

on corporate

and individual

targets

Promote

from

within

Inject

expertise

through

external

hires

Ensure

shareholder

protection

28

Develop a

culture of

accountability |

Our

Brands, Markets, and

Growth

Strategies

Colin Wilson

President and Chief Executive

Officer

NACCO Materials Handling Group |

NACCO

Materials Handling Group and Hyster-Yale Materials Handling are Formed

Hyster founded

in Portland

Oregon as the

Willamette

Ersted

Company

1929

1944

1959

Company name

officially

changed to

Hyster

Company

First Hyster

container

handling

trucks

1875

1920

Yale Lock

Mfg. broadens

its scope into

materials

handling

Yale and Towne

launched a new

battery powered low-

lift platform truck

1963

Yale forklift

truck business

merges with

Eaton Mfg.

Industrial Truck

Division

1950

Yale added gas,

LP gas and

diesel-powered

fork lift trucks to

its range

1964

Hyster introduces

the famous

Monotrol®

pedal

1971

Yale forges a

partnership

with

Sumitomo

Ltd

1989

1989

Hyster and

Yale merge to

form NACCO

Materials

Handling

Group

30

2012

2012

1985

Yale acquired

by NACCO

Industries

1989

Hyster

acquired by

NACCO

Industries

Hyster-Yale

formed as

independent

public company

following spin-off

by NACCO |

Brand

Management 31

NMHG Major Accounts

Dealer

Dealer

NMHG Dealer Oversight

Dealer |

UTILEV

Introduced in 2011

Addresses the utility segment of the market

Contract manufactured in China

32 |

Our

Business Has Been Transformed Comprehensive, updated product line

Average product age since last

upgrade –

less than 4 years

Designed to meet customer needs

and provide low overall cost of

ownership

Multiple power solutions to meet

performance, cost, and environmental

needs

Product Range

Manufacturing

Globally integrated, lean operations

with economies of scale

Assembled in market of sale

Continuous efficiency improvements

DFT implementation globally

33 |

Our

Business Has Been Transformed Centralized supply chain

management

Highly flexible low cost

supply chain

30%+ low cost country

sourcing

Concentrated supplier base

Intense focus on supplier

quality

Supply Chain

Aftermarket

Quality

Customer driven

programs

North America’s warranty

rates reduced by 50%+

Model Year upgrades

High first time fill %

Comprehensive all

makes parts program

Strong Fleet

management program

Telematics solutions

across product line

34 |

Our

Competitive Advantages 35

•

Able to meet customers needs globally

•

Global economies of scale

•

New investment in alternative energy solutions

•

Young/ fresh product line

•

Source of aftermarket profitability

•

Barrier to entry

Global

Full Product Line

Field Population

Dealer Relationships

•

Independent distribution model

•

Exclusive distribution

•

Combine OEM excellence with entrepreneurial

distribution focused on customer

•

Long relationships

•

Able to meet most needs

•

National Account programs

Customer Relationships

•

High performance metrics

•

Large fleet program

Aftermarket Support

Employee Relationships

•

Engaged workforce

•

Experienced leadership

•

Equal treatment

•

High return for our stockholders

•

Low capital employed structure

•

Partnership relationships to limit capital needs

Focus on Return on Capital |

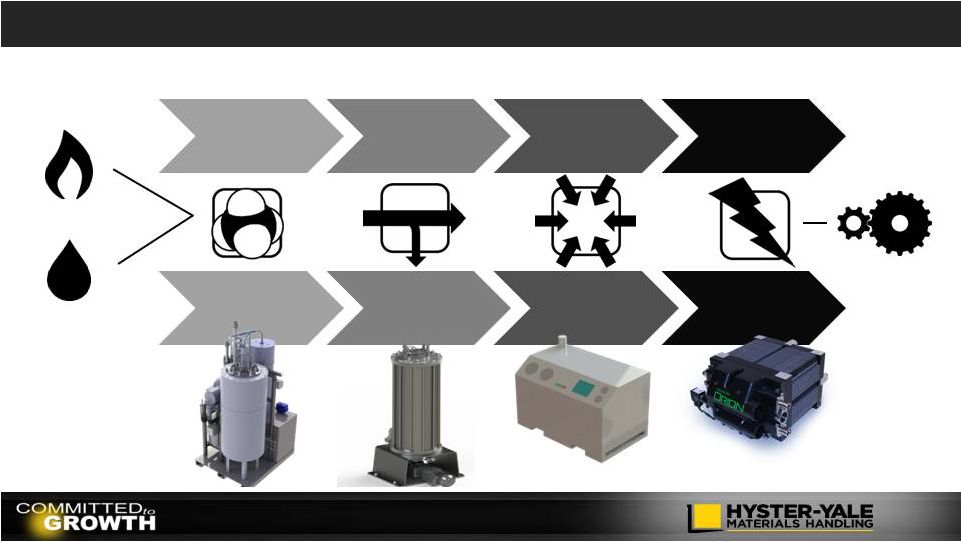

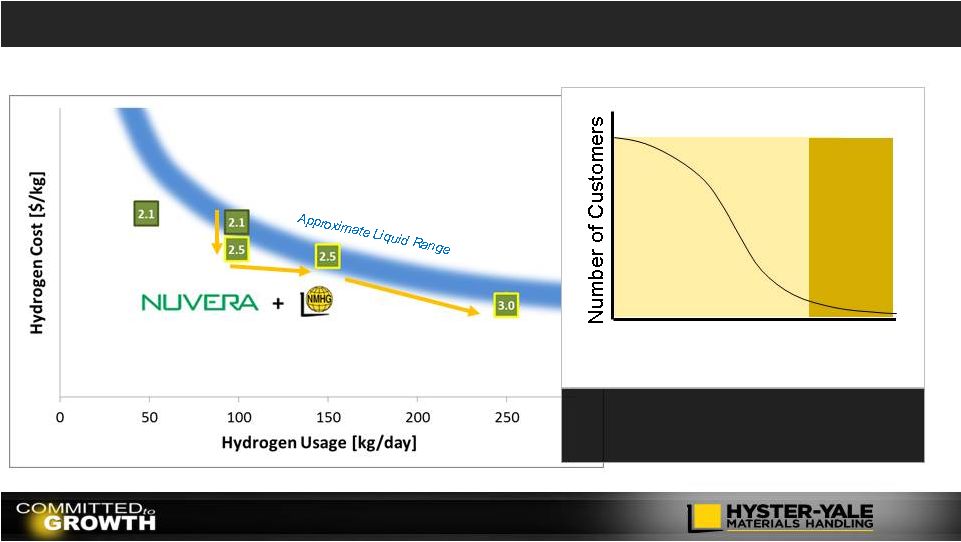

NMHG

Acquired Nuvera in December 2014 Participate in hydrogen generation and

compression opportunities

Enter fast growing hydrogen fuel cell market

Provide integrated solution for customers

Revenue and margin from sale of power source

36

We plan to: |

Our

Core Strategies 37 |

Global Structure

Corporate

Strategy

Product Development

Supply Chain

Global Finance

Information Technology

Geographic

Sales and Marketing

Manufacturing

Human Resources

Regional Finance

Aftermarket

38 |

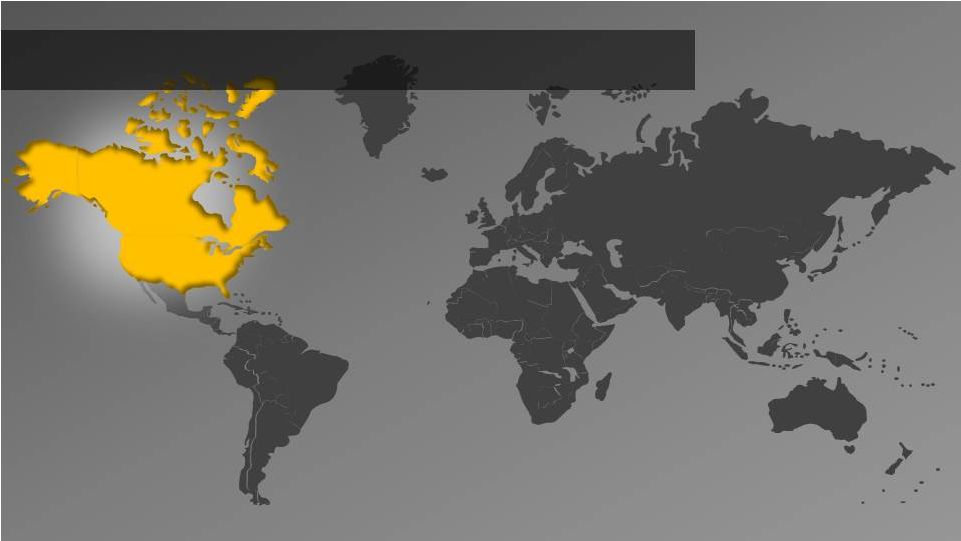

NMHG

Organized on a Geographic Basis The Americas

Population: 1 Billion

GDP : $25 Trillion (USD)

Lift Truck Industry : 267,600

Europe, Middle East,

and Africa

Population: 2.5 Billion

GDP: $29 Trillion (USD)

Lift Truck Industry: 388,800

39

_____________________

Source:

Industry: WITS. 2014 Orders Reports

GDP:

http://knoema.com/nwnfkne/world-gdp-ranking-2014-data-and-charts

Population:

http://www.worldometers.info/world-population/population-bycountry/

Asia-Pacific

Population: 3.8 Billion

GDP: $24 Trillion (USD)

Lift Truck Industry: 432,900 |

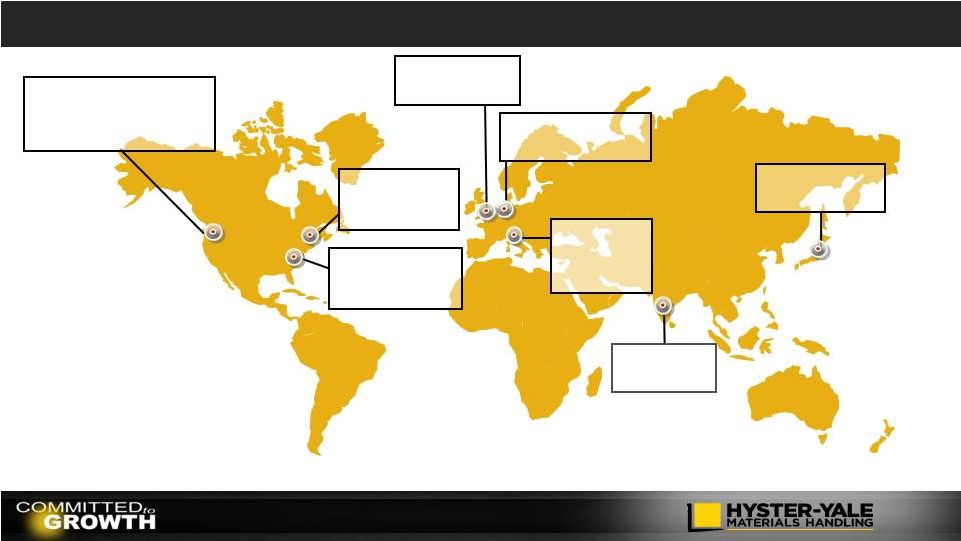

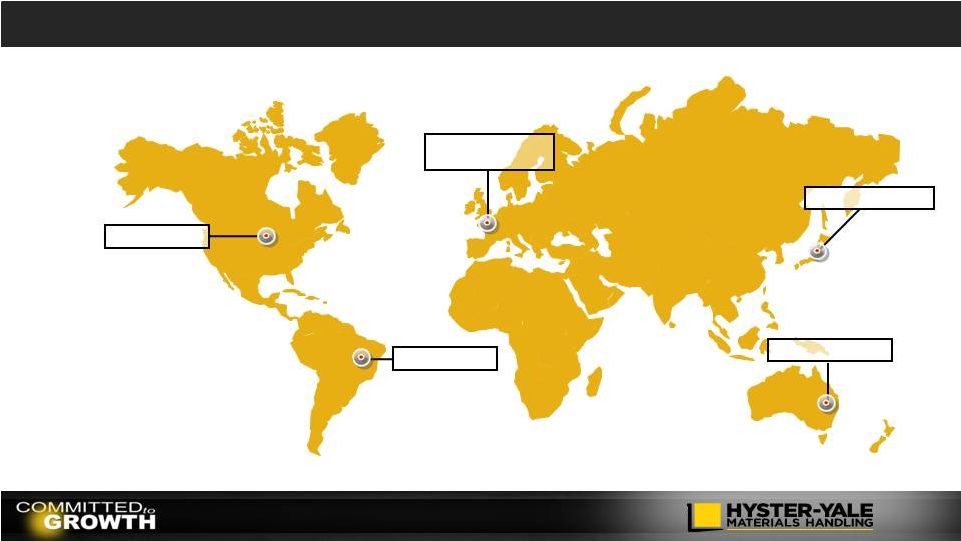

Sao

Paulo, Brazil Marketing

operations for

Brazil

Cleveland, Ohio

Hyster-Yale

corporate

headquarters

Sydney, Australia

Divisional headquarters;

sales and marketing for

Asia-Pacific

Headquarters

Obu, Japan (JV)

Headquarters for

Sumitomo-NACCO JV

Our Global Footprint

40

Frimley, Surrey UK

Divisional

headquarters and

marketing and sales

operations for Hyster

®

and Yale

®

in Europe

Greenville, North

Carolina

Divisional

headquarters and

marketing and sales

operations for

Hyster®

and Yale®

in Americas |

Greenville, North

Carolina

Americas warehouse

development center

Fairview, Oregon

Counterbalanced development

center for design and testing of lift

trucks, prototype equipment and

component parts

Development

Centers

Nijmegen, Netherlands

Big trucks development

center

Masate, Italy

European

warehouse

development

center

Obu, Japan (JV)

Sumitomo-NACCO JV

development center

Billerica,

Massachusetts

Nuvera research and

development

Frimley, Surrey UK

Engineering Concept

Center

Our Global Footprint

41

Pune, India

Engineering

design services |

Ramos

Arizpé, Mexico Manufacture of component

parts

Sulligent, Alabama

Manufacture of component

parts

Berea, Kentucky

Manufacture of lift

trucks and component

parts

Manufacturing

Nijmegen,

Netherlands

Manufacture of lift

trucks

Greenville, North

Carolina

Manufacture of lift

trucks and

component parts

Masate, Italy

Manufature

of lift trucks

Craigavon,

Northern Ireland

Manufacture of lift

trucks and

component parts

Cavite, Philippines

Manufacture of

components for

Sumitomo-NACCO JV

Hanoi, Vietnam

Manufacture of

components for

Sumitomo-NACCO JV

Obu, Japan (JV)

Manufacture of lift

trucks

Shanghai, China

(JV)

Manufacture of lift

trucks

Itu, Brazil

Manufacture of lift trucks

Our Global Footprint

42 |

Parts

Distribution

Nijmegen,

Netherlands

Sydney, Australia

Danville, Illinois

Itu, Brazil

Obu, Japan (JV)

Our Global Footprint

43 |

Pune,

India Supply chain

services

Irvine, Scotland

European Divisional

Support Centre

Charlotte, North Carolina

Customer experience and

training center

Customer

Experience and

Support Centers

Fairview, Oregon

Global administrative

center

Kuala Lumpur,

Malaysia

Asia support office

Our Global Footprint

44

Shanghai, China

Supply chain

procurement center

Hefei, China

Supply chain

procurement center |

Country Economy Maturity Drives the Type of Lift Truck Used

Premium

Standard

Utility

Indicative Map Only

Company’s estimate of predominance of type of demand

45 |

Our

Product

Range

–

Designed

to

Meet

Customer

Needs

Premium

46 |

Standard

Our

Product

Range

–

Designed

to

Meet

Customer

Needs

47 |

Utility

Our

Product

Range

–

Designed

to

Meet

Customer

Needs

48 |

Types

of Trucks Used Vary by Market 49

_____________________

Source: WITS. 2014 Orders Reports

North

America

Class 1: 18%

Class 2/3: 45%

Class 4/5: 37%

Latin America

/Brazil

Class 1: 8%

Class 2/3: 36%

Class 4/5: 56%

Western

Europe

Class 1: 19%

Class 2/3: 64%

Class 4/5: 17

Middle East

& Africa

Class 1: 15%

Class 2/3: 25%

Class 4/5: 60%

Eastern

Europe

Class 1: 16%

Class 2/3: 54%

Class 4/5: 30%

Asia

Class 1: 17%

Class 2/3: 25%

Class 4/5: 58%

Pacific

Class 1: 14%

Class 2/3: 36%

Class 4/5: 50 |

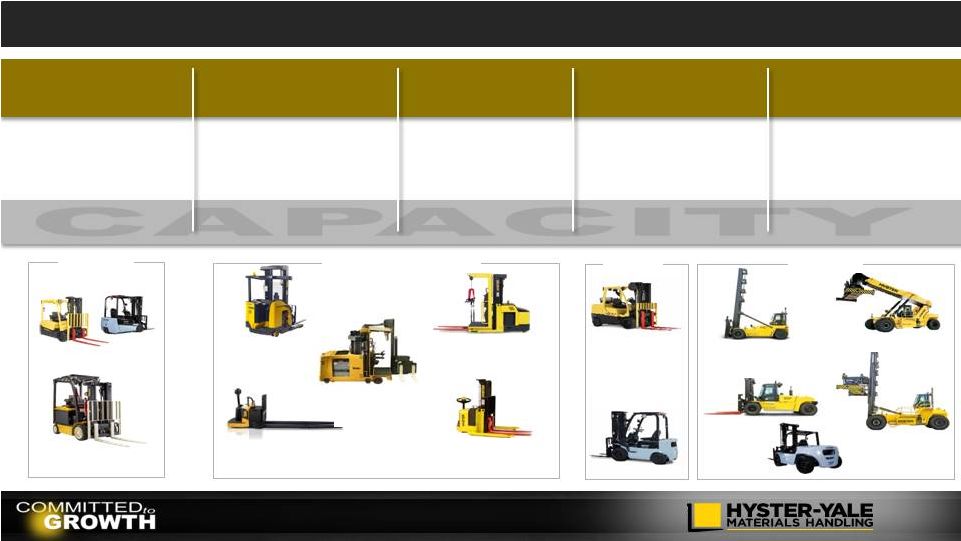

NMHG

Is a True Full Line Supplier Electric

Counterbalanced

Rider Trucks

Electric Narrow

Aisle Trucks

Electric Hand

Trucks

Internal

Combustion Engine

(cushion tire)

Internal

Combustion Engine

(pneumatic tire)

Electric

CB

3 wheel Electric

4 wheel Electric

Pallet Trucks

Stackers

Very Narrow

Aisle Trucks

Order Pickers

Reach Trucks

Internal

Combustion

Engine

ICE CB

Laden Container

Handlers

Big Trucks

Empty Container

Handlers

Forklifts

Reach Stackers

CLASS 1

CLASS 2

CLASS 3

CLASS 4

CLASS 5

1.0T to 5.5T

1.5T to 6.0T

1.5T to 8.0T

1.0T to 7.0T

1.0T to 52.0T

Warehouse Equipment

50 |

Meeting the Needs of Customers

Understanding Customer

Needs

Improving Warehouse

Position

Big Truck Position

Counterbalanced product

Warehouse product

Big Truck product

51 |

Aftermarket Support Is Critical to the Customer’s Purchase Decision

Dealer support and service

Parts availability

52

_____________________

Source: 2007 Deloitte Survey on Customer Purchase Decision-Making

3.4

3.5

3.8

3.9

4.1

4.2

4.4

4.4

4.6

4.7

5.0

5.2

5.2

5.2

5.3

5.4

5.5

Financing options / lease programs

Product customization

Fleet services programs

Green / environmentally friendly

Breadth of product features/options

Quick delivery / lead time

Manufacturer's reputation

Initial purchase price

Dealer relationship / reputation

Ergonomics / comfort

Warranty / backing of product

Total cost of ownership

Quality

Safety

Reliability

NOTE:

Based

on

6

points

scale

with

1=

“Not

Important”

and

6

=

“Critically

Important” |

Shipment direct to vans

Aftermarket Support Is Critical to the Customer’s Purchase Decision

•

Distribution cost compression

through warehouse automation

•

Transaction cost compression

through greater use of technology

•

Pricing optimization

through structured analytics

powered by bespoke software

Global inventory visibility

Comprehensive

parts availability

At the right cost

At the point of

consumption

53 |

Key

Relationships…Our People Success

Through

People

54

Performance

Management

Competencies

/ Behaviors

Accountability

Employee

Engagement

Equal

Opportunity

for All

Reward

Over

5,400

people

worldwide |

Key

Relationships…Our Customers The Customer

Direct to customer sales to

major accounts

Account Identification

Teams

Solutions Groups

Special Application teams

Global Account teams

Investment in global CRM

system

Understanding

Customer Needs

Blue Chip Customer Base

55 |

Key

Relationships…Our Dealers The Dealer

Independent

Exclusive

Entrepreneurial

Committed

partner

Dual-line or

single

Over 1,000

global dealer

locations

Enhancing

performance

Dealer Excellence programs

Dealer incentives

Term-based contracts

Strengthening the

distribution footprint

Sales and Service territories

(SSTs)

Competitor conversions

In-territory acquisitions

More than

2,000

application

consultants

Over 11,000

service technicians

Strong

Independent

Distribution

56 |

57

Key relationships…Our Financing Partners |

Key

Relationships…Joint Ventures and Licensees Maini Materials

Movement

(Yale)

TIL Limited

(Hyster)

Hangcha

(UTILEV)

Sumitomo-

NACCO

Materials

Handling

Our Partners

Succeed in Asia

58 |

Growth in Our

JAPIC and

Brazil

Operations

Victoria L.

Rickey

Senior Vice President, Asia-

Pacific and Brazil

NACCO Materials Handling Group |

JAPIC

(Japan,

Asia

Pacific,

India,

China) |

9%

Compound

Annual

Growth

–

China

16%

JAPIC Markets

Increasingly important region

Significant opportunity for growth

Domestic production in the market is critical

61

_____________________

Source: WITS. Orders Reports.

_____________________

Source: WITS Orders Reports.

_____________________

_____________________

Source: JIVA (Japan); CITA (China); KOCEMA (Korean); SIMEHM (India); WITS (Asia &

Pacific) 30%

38%

40%

39%

38%

40%

40%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

JAPIC

Global

18,444

54,463

81,203

8,745

274,992

0

50,000

100,000

150,000

200,000

250,000

300,000

Pacific

Asia

Japan

Indian SC

China

2014 Industry Bookings

0

100,000

200,000

300,000

400,000

500,000

2008

2009

2010

2011

2012

2013

2014

Industry Bookings

Pacific

Asia

Japan

India

China

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

Japan

Asia

Korea*

Pacific

India

China

2014 Domestic Production

Source: WITS. 2014 Orders Reports.; For Indian Subcontinent data is WITS plus SIMHEM

2008

2009

2010

2011

2012

2013

2014 |

Lift

truck market per million population Very low lift truck usage…

62

_____________________

Lift truck market per million population

Population in millions

1447

1666

421

756

409

1402

39

358

127

418

India SC

MEA

Latin America

Asia

Eastern Europe

China

Pacific

North America

Japan

Western Europe

6

33

64

73

144

196

473

613

639

655

Source: WITS. 2014 Orders Reports.; For Indian Subcontinent data is WITS plus SIMHEM

Population – www.worldometers.info/world-populations by country |

Japan

Sumitomo-NACCO (SN)

Sumitomo Heavy

Industries, Ltd.

NACCO Materials

Handling Group

50%

50%

Incorporated May 1, 1972

2014 -Approximately

700 employees

Sales and manufacture of

Class 1, 2, 4, and 5 product

NMHG exclusive

distribution rights outside

of Japan

Distribution Network

SN Materials Handling

Sales Company

(February 21,1981)

Cavite,

Philippines

1996

Hanoi,

Vietnam

2008

Obu,

Japan

1972

3 Manufacturing Locations

63

Growth Strategies

Implement Demand Flow Manufacturing

Reduce lead time and enhance quality

Re-engineer Service Operation

Grow Major Account Business

Introduce New Electric Product

Revise Dealer Management Structure

_____________________

Source: WITS. 2014 Orders Reports.

25%

24%

5%

46%

2014 Japan Market

Class 1

Class 2

Class 3

Class 4 & 5 |

Asia

Advanced

•

Singapore

•

Taiwan

•

South Korea

Newly

Industrial

•

Thailand

•

Malaysia

•

Indonesia

•

Philippines

•

Vietnam

Emerging

•

Cambodia

•

Myanmar

•

Laos

Asian

Markets

Growth Strategies

Opportunities

•

Mixed markets

•

Largely Internal Combustion

•

Rental business developing

•

Large utility segment

Build Asian Infrastructure

Improve Dealer Performance

Grow Warehouse and Big Truck Business

Expand Major Account Team

Expand UTILEV Range

34%

of market*

South Korea is

64

_____________________

Source: WITS 2014 Orders Reports.

_____________________

*Source: WITS 2014 Orders Reports.

37 dealer locations and 154 salespeople

17%

13%

12%

58%

2014 Asia Market

Class 1

Class 2

Class 3

Class 4 & 5 |

Succeed in Asia

Dealer Conversion

New Malaysian

dealer

Share of Hyster has

doubled in Malaysia

since signing

Converting large rental

fleet over the next 4

years

Major Account Victories

Nearly 100 Class 5 trucks

Sold on basis of previous strong service

satisfaction with Hyster Thai dealer

100+ trucks

won on Japanese account initiative

Global

$2B+

tire

manufacturer

operating

in a large facility in Thailand

Japanese

accounts

in

Asia

for temperature control,

manufacturing, and safety

systems

65

Conquest

sale

in

growing

Philippine market

Well-known,

multinational

beverage

corporation

with

extensive brand recognition |

Pacific

•

Mature cyclical market

•

Large long term rental

•

Telemetry

•

Significant major account business

Close Distribution Gaps

Improve Dealer Performance

Grow Warehouse Market Business

Build Yale Major Account Business

Expand UTILEV Range

83%

of market

Growth

in the

Warehouse

Market

over last

8 years

Growth Strategies

Australia is

Opportunities

66

_____________________

Source: WITS. 2014 Orders Reports.

_____________________

Source: WITS. 2014 Orders Reports.

_____________________

Source: WITS Orders Reports.

31 dealers and 63 salespeople

14%

14%

21%

51%

2014 Pacific Market

Class 1

Class 2

Class 3

Class 4 & 5

13%

36%

51%

2014

10%

32%

58%

2006

Electric

Warehouse

ICE |

Pacific Success

67

Converted 120+ trucks

Sold on basis of “greening their

environment”

from ICE to Electric CB

275+ trucks

won on expertise in Telemetry

Commercial

carrier

for

large Pacific country and

member of a major

international airline alliance

Well-known,

multinational

beverage corporation

with

extensive brand recognition

Substantial Big Truck deal

22 ReachStackers

9 laden handlers

3 18-ton trucks

One

of

Australia's

largest

rail

freight

businesses

with

significant regional intermodal

terminal capacity

Major Account Victories |

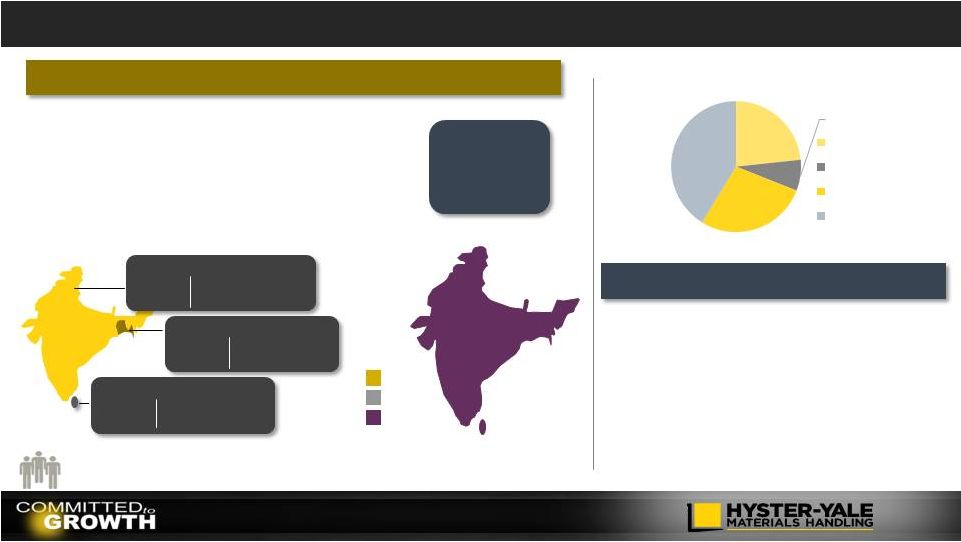

Indian Subcontinent Markets

Growth Strategies

Opportunities

•

Emerging

market

(below

Utility)

•

Significant local production = 64%

•

Large electric segment

•

Growing rental demand

•

Significant US/EMEA major account business

•

Strong local partners with technology licensing

Increase Market Coverage

Penetrate Major Accounts

Add Additional Utility Products

Leverage China Sourcing

Expand UTILEV Range

Launch Rental Business

93%

of market

India is

Pop.

1.27B

2014 GDP Growth

9.1%

INDIA

Pop.

0.158B

2014 GDP Growth

15.4%

BANGLADESH

Pop.

0.021B

2014 GDP Growth

7.3%

SRI LANKA

68

_____________________

Source:

http://knoema.com/nwnfkne/world-gdp-ranking-2014-data-and-charts; https://www.cia.gov

_____________________

Source: 2014 WITS plus SIMHEM

_____________________

Source: 2014 WITS plus SIMHEM

Premium

Standard

Utility

_____________________

Indicative Map Only. Company’s estimate of predominance of type of

demand 14 dealer locations; relationships with Maini (Yale) and TIL

(Hyster) 23%

8%

28%

41%

2014 India Market

Class 1

Class 2

Class 3

Class 4 & 5 |

Leverage

Partnerships

–

India

Product and dealer relationship

TIL manufactures ReachStackers under

license in India

Delivered

100 ReachStacker

in

2014

Exporting to Hyster Pacific

TIL Limited

Maini

Product and dealer relationship

Maini manufactures electric trucks under

license in India

Distribute counterbalanced and warehouse

trucks in India

69

th |

China

Shanghai Hyster Forklift, Ltd.

Approximately

200 total headcount

Build small internal combustion

and 4-wheel electric trucks

Formed

in

1997

–

Began

Production in

1999

Joint Venture with Sumitomo-NACCO

Factory 6,400 sq. mtrs

Land 12,000 sq. mtrs.

Distribution Network

Dealers = 29

70

Growth Strategies

Expand Dealer Network and Sales Coverage

Localize High Volume Products

Grow Major Account Business

Grow Warehouse Business

Mature Demand Flow Manufacturing

_____________________

Source: WITS 2014

13%

2%

12%

73%

2014 China Market

Class 1

Class 2

Class 3

Class 4 & 5

Hyster

28

Dual line 1 |

Our

Partner

for

Utility

-

Hangcha

71

UTILEV production began in 2011

Class 1,3,4 and 5 UTILEV product

contract manufactured in China |

Brazil |

Brazil

Industry

–

3.9

%

CAGR

% of the global market

Market shifting to electric

FINAME financing on local content

73

_____________________

Source: WITS Orders Reports.

_____________________

Source: WITS.Orders Reports.

_____________________

Source: FEM, JIVA, KOCEMA, ITA, WITS as of 2014

_____________________

Source: WITS Orders Reports.

37%

48%

63%

52%

2008

2014

ICE

Electric

2%

2%

3%

2%

2%

2%

2%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2008

2009

2010

2011

2012

2013

2014

Brazil

Global

16,830

8,417

22,913

22,560

18,786

24,381

21,166

-

5,000

10,000

15,000

20,000

25,000

30,000

2008

2009

2010

2011

2012

2013

2014

Industry Bookings

65.4%

46.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

NMHG Total Brazil Bookings Locally

Built

% of Total Industry Locally Built |

Brazil

Growth Strategies

Opportunities

Begin Local Production of

Class 1, 2, and 3

Grow Warehouse and Big Truck

Business

Grow Major Account Business

Enhance Strong Dealer Network

Mature Demand Flow

Manufacturing

Grow Aftermarket

•

World’s

fifth

largest

country

(1)

•

Largest economy in Latin America and

7th

largest

world

economy

(1)

•

Industrial production recovery after

monetary and fiscal adjustments

expected in 2016

•

Fundamentals bring confidence to long

term growth

NMHG Brasil

founded in 1957

Sao Paulo and Itu, Brazil

Marketing Operations

Parts Distribution Center

Manufacturing Facility

74

_____________________

(1) Source:

http://knoema.com/nwnfkne/world-gdp-ranking-2014-data-and-charts; https://www.cia.gov |

Brazil Success

75

Converted 200+ trucks

150+ trucks

Won on global account leverage

Large full service Brazilian

logistic company

purchasing to support

various industries

Well-known, US auto

manufacturer

with

extensive brand recognition

Penetrated 11 new Reach Stacker accounts

Three large customers > €

2M

Inroads made in Brazilian

Ports, Terminals, and Rental

Fleets

with

dedicated

team

Major

Account

Victories

–

2014

Growth

2.5

times

2013

Big

Truck

Victories

–

2014

Growth

3

times

2013 |

New

Brazil Plant and Office 76 |

Growth in Our

Americas

Operations

Chuck

Pascarelli

Senior Vice President,

President, Americas

NACCO Materials Handling Group |

Latin America |

Latin

America Key Countries Dominate the Market

Latin American Industry Size Stable

Diverse Customer Mix

Latin America as % of Global Market

79

_____________________

Source: WITS Orders Reports.

_____________________

Source: WITS Orders Reports.

_____________________

Source: WITS. 2014 Orders Reports.

_____________________

Source: Internal Company estimates.

24,201

12,135

22,029

32,457

29,698

27,720

27,032

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2008

2009

2010

2011

2012

2013

2014

Manufacturing

& Automakers,

25%

Home Centers/

Retail, 16%

Food &

Beverage, 15%

Paper &

Forrestry, 12%

Port, 10%

Mining, 2%

Others, 19%

3%

2%

3%

3%

3%

3%

2%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2008

2009

2010

2011

2012

2013

2014

Latin America

Global

Mexico

34%

Argentina

23%

Chile

12%

Columbia

6%

Peru

4%

Rest of Latin

America

21% |

Latin

America Utility Truck Industry Latin American Utility Truck Market

7,786 units

Electric Rider

5%

I.C.E.

79%

Warehouse

16%

80

_____________________

Source: 2014 CITA

_____________________

Source: 2014 CITA

Argentina

46%

Venezula

7%

Chile

11%

Mexico

8%

Uruguay

6%

Rest of

Latin

America

22% |

Latin

America 81

•

Growing electric segment

•

Expanding ports business

•

Three-tier demand: premium, standard, utility

Opportunities

Growth Strategies

Execute dual brand distribution

Improve dealer performance

Grow UTILEV, warehouse, and

Big Truck business

Penetrate large Latin

American-based accounts

2014 Latin America Market

_____________________

Source: WITS 2014 Orders Reports.

Premium

Standard

Utility

_____________________

Indicative Map Only. Company’s estimate of predominance of type of

demand 10%

9%

21%

60%

Class 1

Class 2

Class 3

Class 4 & 5 |

Success in Improving Warehouse Position

Largest retail company in Chile

and the third largest listed retail company in Latin America

with over 1000 stores.

•

Create a focus and

passion within our

dealer network to sell

our products and

solutions

•

Offer the strongest

warehouse product line

in the industry

Focus

Success

82

•

Competitor conversion

•

220

warehouse

trucks

[Class

1,

2,

&

3]

•

Telematics strategy supports conversion

•

Maintenance through dealer |

North America |

North

American Market Business Unit Approach Drives Focus

North American Industry Steady Growth

Diverse Customer Industry Mix

North America as % of Global Market

Electric

60% of units

40% of revenue

ICE

40% of units

60% revenue

Big

Trucks

2% of ICE

units, but

9% of

overall

revenue

84

_____________________

Source: WITS.Orders Reports.

_____________________

Source: WITS.Orders Reports.

_____________________

Source: Internal Company estimates.

_____________________

Represents Hyster-Yale North American unit shipments by industry

Manufacturing

27%

Wholesale Distribution

14%

Food & Beverage

13%

Rental

10%

Home Centers/Retail

11%

Freight & Logistics

10%

Paper

6%

Other

9%

18%

18%

17%

17%

19%

20%

20%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2008

2009

2010

2011

2012

2013

2014

North America

Global

159,279

98,338

136,050

169,589

181,191

200,939

219,444

0

50,000

100,000

150,000

200,000

250,000

2008

2009

2010

2011

2012

2013

2014 |

Opportunities and Growth Strategies

Developing

customer awareness through account identification

Developing

customer relationships

Developing

strong brand and company identity

Developing

dealer relationships

Developing

professional salespeople

Developing

highly-trained technicians

The NMHG Experience Center

in Charlotte, North Carolina

85 |

Strong Independent Distribution

Exclusive sales and service coverage

coast to coast

52

Hyster and

Yale dealer

organizations

362

branch

locations

4,670

technicians

106

dealer

technical

trainers

86 |

Dealer Conversion

Third-generation, 88-year old heavy equipment company based in

southeastern United States with 1200 employees across five states

Their

Expectations

A partner with

shared values

Their

Choice

NACCO Materials

Handling Group

The

Result

Purchased a larger, lower-performing

dealership and transformed it to profitability

within 6 months

Percentage of growth in key metrics

since conversion (2011 to 2014)

87

_____________________

Source: LiftOne LLC

High-quality equipment

Market-focused features

Product support

Employee support

Customer support

Integrity

Accountability

Adaptability

Positive and engaged people

Customer driven

Sales

194%

Employees

187%

Branches

143%

Units Shipped

498% |

Sales

Transformation Framework Sales Messaging

Sales

Execution

Sales

Process

Talent

Sales

Messaging

Technology

88

Awareness

and Account

Identification

Focused on process and cadence

Focus on customer business

Leading, coaching, and mentoring

Selling across decision maker levels

Differentiated, consistent message

Solving customer business issues |

Success in Understanding Customer Needs

Second-largest retailer in the United

States

With over 450 membership-only warehouse club

stores in the United States

•

Solutions Groups

•

Application Centers

Focus

Success

89

•

Custom-designed product

•

Enhanced customer productivity

•

Competitor account conversion

•

Entry into new market segment |

Success in Low Cost of Ownership

Large regional home improvement

retailer

•

Solutions focused

•

Energy/fuel consumption

•

Alternative power

•

Fleet Management

•

Intelligent design

requiring less maintenance

Focus

Success

90

•

>3,000 unit order

•

Significant fleet replacement

•

Conversion to lease financing

•

Fleet management

•

Incremental service/parts revenue |

Success in Big Trucks

Second-busiest container port in the

United States

•

Product/Application

Management

•

Marketing & Sales

Coordination

•

Industry Focused (Sales,

Applications, Marketing)

•

Structured to expand as

industry penetration occurs

•

World class service

support

Focus

Success

91

•

25 container handlers plus future orders

•

Hyster absent from port for over 10 years

•

Regained confidence of customer base

•

Collaborative effort between Hyster and local dealer

|

Growth in Our

EMEA

Operations

Ralf A. Mock

Senior Vice President

Managing Director

Europe, Middle East and Africa

NACCO Materials Handling Group |

Europe, Middle East, and Africa |

EMEA

Market 94

Markets are recovering

Stable contributor to world markets

Continuous shift to electrics

Stable volumes throughout markets

_____________________

Source: WITS. Orders Reports.

_____________________

Source: WITS.Orders Reports.

_____________________

Source: WITS. Orders Reports.

_____________________

Source: WITS. Orders Reports.

296,080

179,812

220,119

264,003

247,043

245,719

273,624

70,911

20,538

39,881

55,252

54,398

58,794

58,775

43,984

39,298

48,926

49,890

52,829

55,410

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2008

2009

2010

2011

2012

2013

2014

Total Bookings

Western Europe

Eastern Europe

Middle East & Africa

47%

41%

38%

38%

37%

35%

36%

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2008

2009

2010

2011

2012

2013

2014

EMEA

Global

72%

17%

11%

2008

Western Europe

Eastern Europe

Middle East & Africa

69%

75%

31%

25%

0

100,000

200,000

300,000

400,000

500,000

2008

2014

ICE

Electric

71%

15%

14%

2014

22,4783

- |

Transformation of the Dealer Network

95

25% of the EMEA market

restructured in 2014

EMEA Distribution

165

dealers

440

locations

871

salespeople

3,482

technicians

Significant restructuring

since 2009

Dual-Brand: 12% of industry

Single-Brand: 54% of industry

Competitor Conversion

Management Buy Out |

Western Europe

96

Recovery has been steady

Slight declining contribution

Continual shift to electrics

_____________________

Source: WITS. Orders Reports.

_____________________

Source: WITS. Orders Reports.

_____________________

Source: WITS. Orders Reports.

_____________________

Indicative Map Only. Company’s estimate of predominance of type of demand

Applications drive need for premium product

34%

33%

28%

27%

26%

24%

25%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2008

2009

2010

2011

2012

2013

2014

Western Europe

Global

78%

83%

22%

17%

0

50,000

100,000

150,000

200,000

250,000

300,000

2008

2014

ICE

Electric

296,080

179,812

220,119

264,003

247,043

245,719

273,624

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2008

2009

2010

2011

2012

2013

2014

Total Bookings

Premium

Standard

Utility |

UK

Ireland

France

Spain

Portugal

Germany

Neth.

Belgium

Italy

Switz.

Austria

Hungary

Slovakia

Poland

Ukraine

Russia

Slovenia.

Croatia

Bosnia

Serbia

Romania

Moldova

Belarus

Latvia

Estonia

Lithuania

Denm.

Norway

Sweden

Finland

Bulgaria

Macedo.

Albania

Greece

Malta

Turkey

Biggest Markets in Western Europe

97

27%

19%

12%

11%

7%

5%

_____________________

Source: WITS. 2014 Orders Reports.

Units and percentage of Western Europe market

Netherlands

Spain

Italy

UK

France

Germany |

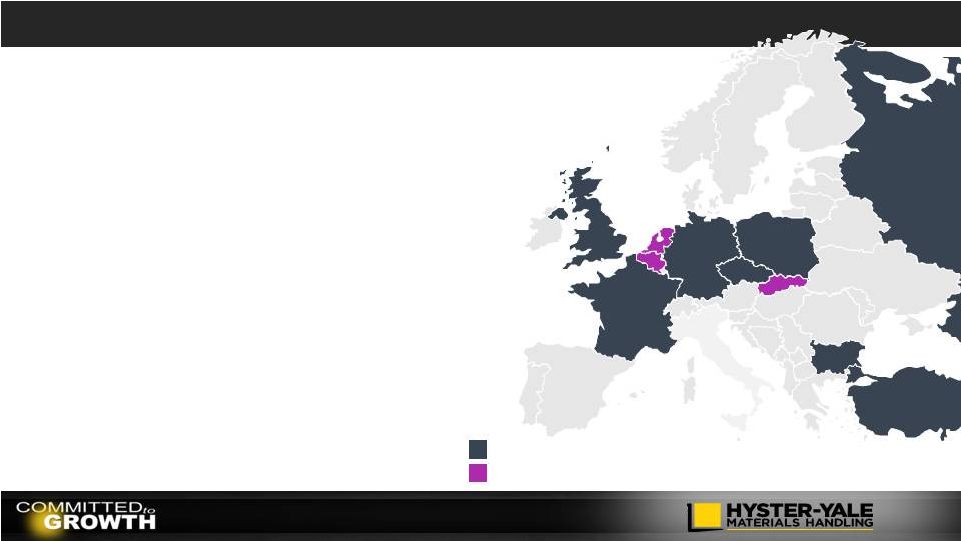

Enhance

Independent

Distribution

–

Western

Europe

98

Germany

France

United Kingdom

Italy

Spain

New Hyster

network of 16

dealers

Strengthened

support team

Enhanced

major accounts

Strong Hyster

dealer

Rental concept

with a solid

truck base

Strong dual line

dealer

Brand and

industry focus

Dedicated teams

Flexible fleet

Strong Hyster

dealer

Dual brand

dealer in Milan

& Bergamo

Long-term

established

Hyster dealer

Major account

presence

Established

Yale network

Strengthened

with 2 extra

dealers

Entrepreneurial

Yale network

New national

account focus

Strong dual line

dealer

Brand and

industry focus

Dedicated teams

Flexible fleet

Established

Yale network

Dual brand

dealer in Milan

& Bergamo

New national

account focus

Established

Yale network

Strong local

presence

OEM Support: Industry Strategy, Account Identification, Big Trucks, Major Account

Focus |

Western Europe Successes

Successes

99

Customer conversions in automotive, packaging and food

Major Accounts

Gain conquest business with large logistics company and

major automotive manufacturer

Warehouse

Penetration

of

ports

and

metals

industry

–

application

solutions

Big Truck

111

dealers

–

17

new

in

2014

5 dealer conversions from competition in 2014

Coverage

Focus

Launch of new reach truck and power pallet truck range

Product |

Eastern Europe

100

Steadily recovering market

Stable part of global market

Dramatic shift to electrics

Applications require standard and utility trucks

_____________________

Source: WITS. Orders Reports.

_____________________

Source: WITS. Orders Reports.

_____________________

Source: WITS. Orders Reports.

_____________________

Indicative Map Only. Company’s estimate of predominance of type of demand

70,911

20,538

39,881

55,252

54,398

58,794

58,775

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2008

2009

2010

2011

2012

2013

2014

Total Bookings

8%

4%

5%

6%

6%

6%

5%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2008

2009

2010

2011

2012

2013

2014

Eastern Europe

Global

51%

70%

49%

30%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2008

2014

ICE

Electric

Premium

Standard

Utility |

Eastern Europe Market

101

12%

6%

4%

4%

_____________________

Source: WITS. 2014 Orders Reports.

Units and percentage of Eastern Europe market

UK

Ireland

France

Spain

Portugal

Germany

Neth.

Belgium

Italy

Switz.

Austria

Hungary

Slovakia

Poland

Ukraine

Russia

Slovenia

Croatia

Bosnia

Serbia

Romania

Moldova

Belarus

Latvia

Estonia

Lithuania

Denm.

Norway

Sweden

Finland

Bulgaria

Macedo.

Albania

Greece

Malta

Turkey

33%

26%

Czech Rep.

Slovakia

Romania

Hungary

Cz Republic

Poland

Russia |

Enhance

Independent

Distribution

–

Eastern

Europe

102

Russia

Poland

Czech & Slovak

Republic

Hungary

Romania

Strong Hyster

rental dealer

Big Truck

presence

Major account

successes food

industry

Reinforced

Hyster presence

Big Truck focus

Major Accounts

success in food

distribution

New dealer for

Hyster

Major Accounts

success in

automotive industry

Hyster long-

established

dealer

Hyster long-

established

Strong presence

in Major

Accounts

Entrepreneurial

Yale network

Successes with

standard and

utility product

Strong Yale

presence

Major Accounts

focus

Major Accounts

warehouse

success food

distribution

New ownership Yale

Slovak Republic

Strong dealers

Major Accounts

focus

New dealer

competitor

conversion

New Yale dealer

appointment in

2015

OEM Support: Industry Strategy, Account Identification, Big Trucks, Major Account

Focus |

Eastern Europe Successes

Successes

103

Paper, automotive, food and wholesale customers

Major Accounts

New customers in logistics and established relationship

with major food distributor in Poland

Warehouse

Ports, metal and wood industry business as well as tire

handling solutions for mining industry

Big Truck

22 dealers/ 2 new dealers in 2014

1 dealer conversion from competitors in 2014

Coverage

Focus

Standard and utility product in Russia

Product |

Middle East and Africa

104

Volumes surpass the previous peak

Stable contributions to global market

ICE focus but electric is growing

Wide variety of truck segments

_____________________

Source: WITS. Orders Reports.

_____________________

Source: WITS Orders Reports.

_____________________

Source: WITS. Orders Reports.

_____________________

Indicative Map Only. Company’s estimate of predominance of type of demand

Premium

Standard

Utility

32%

40%

68%

60%

10,000

20,000

30,000

40,000

50,000

2008

2014

ICE

Electric

5%

4%

5%

5%

5%

5%

5%

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2008

2009

2010

2011

2012

2013

2014

MEA

Global

43,984

22,478

39,298

48,926

49,890

52,829

55,410

10,000

20,000

30,000

40,000

50,000

60,000

2008

2009

2010

2011

2012

2013

2014

Total Bookings

- |

Niger

Mauritania

Algeria

Libya

Sudan

Tunisia

Chad

Mali

Egypt

West Sahara

Morocco

Eritrea

Sierra Leone

Liberia

Saudi Arabia

Yemen

Iran

Israel

Oman

Biggest Markets in MEA

105

24%

14%

13%

9%

8%

6%

_____________________

Source: WITS. 2014 Orders Reports.

Units and percentage of Middle East and Africa markets

Algeria

Israel

UAE

S Africa

S Arabia

Turkey

Senegal

Guinea

Nigeria

Burkina

Ivory

Coast

Togo

Ghana

UAE

Qatar

Turkey

Iraq

Jordan

Azerbaijan

Armenia

Georgia

Somalia

Ethiopia

Namibia

Angola

South Africa

Lesotho

Swaziland

Madagascar

Mozambique

Tanzania

Botswana

Zimbabwe

Zambia

D. R.

Congo

Kenya

Cent. Africa Rep

Uganda

Congo

Gabon

Cameroon |

Enhance

Independent

Distribution

–

Middle

East

&

Africa

106

Turkey

South Africa

Saudi Arabia

UAE

Israel

Reinforced

Hyster presence

Big Trucks focus

in ports and

terminals

Long-standing

presence

Long-

established

customer base

Warehouse

focus

Long-established

Hyster presence

Big Trucks focus

Strong dealer

performance

Logistics and

Warehouse

focus

Established

Hyster dealer

Big Truck

presence

Strong new Yale

dealer presence

with a strong

new partner

Special focus on

rental

Strong Yale dealer

growing rapidly

Success with

government

entities

Long-standing

Yale dealer

OEM Support: Industry Strategy, Account Identification, Big Trucks, Major Account

Focus |

Middle East and Africa Successes

Successes

107

Food company in Saudi Arabia

Major Accounts

New reach truck for major automotive company and

targeting VNA consultative solutions

Warehouse

Container handlers for global major account in UAE,

further ports business

Big Truck

32 dealers/ 2 new dealers in 2014

Coverage

Focus

Standard and utility product introduced

Product |

The

Products and the

Technology to

Help us Grow

Rajiv K.

Prasad

Senior Vice President,

Product Development,

Manufacturing and Supply

Chain Strategy

NACCO Materials Handling Group |

Product Philosophy

Full product line

Segmented solutions

Scalable platforms

Leverage core assets

Technology partners

Fit for market and

application

Reliability and durability

Energy efficiency

Operator ergonomics

Fill the factories

Support growth

initiatives

Differentiation

Innovation

Guiding Product

Philosophy

Key Product Attributes

Product Portfolio Focus

109 |

Strong Trucks

110 |

Our

Product Range Class 1

Electric Counterbalanced Rider Trucks

Class 2

Electric Narrow Aisle Trucks

Class 3

Electric Pallet Trucks

Class 4

Internal Combustion Engine (cushion tire)

Class 5

Internal Combustion Engine (pneumatic tire)

111 |

Manufacturing Strategy

Manufacturing

Centers of Excellence for

Key Systems

Process to Determine Core

Competencies

Globally Deployed NMHG

Production System

Supply Chain

Supplier Location

Flexibility

Low Cost Country

Sourcing

Quality <500 PPM

Truck Assembly

In Markets of Sale

Global Centers Where

Scale Has Leverage

Partners in Emerging

Markets

112 |

Transformation of Supplier Quality

SQE

Resources

2001

(2)

2014

(32)

2010

(24)

2006

(14)

Global Quality PPM

Supplier Quality Organization

Global Resources Focused on Supplier

Quality and Supplier Development

ZERO

DEFECT

CULTURE

113

_____________________

Source: Company’s incoming parts quality data collected at each plant

3,028

2,536

1,685

1,558

1,037

600

397

2008

2009

2010

2011

2012

2013

2014 |

SQDCME

Assembly

DFT

Demand Flow Technology (DFT)

Assembly Method

•

•

•

Process, Methods, and Measures

Measures

•

•

•

•

114

Customer Demand Driven

Mixed Model Flow Based on Lean Principles

Sequence of Events (SoE), Operation Methods Sheets

Order Configuration and Scheduling

Slotting -

6 weeks Frozen, Factory Build -

2 weeks Frozen

Line Staging and Sequencing 2-3 Days in Advance

31 total in SQDCME categories

Warranty: <10 Hrs. and <100 Hrs. Warranty

Faults per 100 Trucks

Effectivity, Productivity, Conversion Cost |

Meeting Customer Needs with Special Engineering

115

Aux Hydraulic Cooler

Bigger/Faster Fan

Radiator Cleaning

Point

Solutions

Holistic

Solutions

VD Hydraulic Pump

Hydraulic Fan

Auto Reversing

Result

Cool truck

Issue

Overheating

Unmet

Needs

Customer Need

Met

NMHG Solutions |

Segmentation –

Expanding Standard Range

116

Premium

Comprehensive Premium Truck Range

Application Fit, Strong Trucks and Productivity

High Intensity Usage and Load to Capacity

Standard

Analysis to Identify Standard Segment

Benchmark to Understand Requirements

Expanding Product Offerings

Utility

Low Acquisition Cost

Low Intensity/ Hour Usage

Partner to Offer Solutions

Price

Right Truck

at the

Right Price

for Right

Applications |

Define truck and

non-truck solutions

Provide strategic

advantage for NMHG

Salespeople seen as

solutions providers

Understanding Customer Needs

Application Center Approach

117 |

Warehouse Products

118

Sit with

Moving Mast

Open Skid

Pallets

Flip-down

Platforms

Stand with

Pantograph

Bottom Board

Pallets

Fixed

Platforms

Reach

Pallet

Riders

Japan –

Stand with

Moving Mast

Mainly

Open Skid

Pallets

Flip-down

Platforms

North America

EMEA

JAPIC |

Counterbalanced Products

1.5T

to 9.0T

LP

Diesel Electric

Capacities

Tire Types

Power

119

Pneumatic

Cushion |

Big

Truck Products Fork Lift

Trucks

8 to 48T

Tier IV Emission Engines