Form 8-K ENDURANCE SPECIALTY HOLD For: Aug 28

Tweet

Tweet Share

Share

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

Current Report

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

August 28, 2015

Date of Report (Date of earliest event reported)

Endurance Specialty Holdings Ltd.

(Exact name of registrant as specified in its charter)

| Bermuda | 1-31599 | 98-0392908 | ||

| (State or Other Jurisdiction of Incorporation) |

(Commission File Number) |

(I.R.S. Employer Identification No.) |

Waterloo House, 100 Pitts Bay Road, Pembroke HM 08, Bermuda

(Address of principal executive offices, including zip code)

(441) 278-0400

(Registrant’s telephone number, including area code)

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| Item 7.01. | Regulation FD Disclosure. |

Beginning on August 31, 2015, executives of Endurance Specialty Holdings Ltd. (the “Company”) will present the information about the Company described in the slides attached to this report as Exhibit 99.1 to various investors. The slides set forth in Exhibit 99.1 are incorporated by reference herein.

In accordance with general instruction B.2 of Form 8-K, the information in this Item 7.01 of this Current Report on Form 8-K, including exhibits, furnished pursuant to Item 7.01 shall not be deemed “filed” for the purposes of Section 18 of the Securities Exchange Act of 1934, or otherwise subject to the liability of that section. Accordingly, the information in Item 7.01 of this Current Report on Form 8-K will not be incorporated by reference into any registration statement filed by the Company under the Securities Act of 1933, as amended, unless specifically identified therein as being incorporated therein by reference. The furnishing of the information in this Current Report on Form 8-K is not intended to, and does not, constitute a determination or admission by the Company that the information in this Current Report on Form 8-K is material or complete, or that investors should consider this information before making an investment decision with respect to any security of the Company or any of its affiliates.

| Item 9.01. | Financial Statements and Exhibits |

| (c) | Exhibits |

The following exhibit is filed as part of this report:

| Exhibit No. |

Description | |

| 99.1 | Slides from Presentation by Management | |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| Dated: August 28, 2015 | ||||||

| By: | /s/ John V. Del Col | |||||

| Name: | John V. Del Col | |||||

| Title: | General Counsel & Secretary | |||||

EXHIBIT INDEX

| Exhibit No. |

Description | |

| 99.1 | Slides from Presentation by Management | |

Endurance Specialty Holdings

Investor Presentation

June 30, 2015

Exhibit 99.1 |

Forward Looking Statements and Regulation G Disclaimer

2 Safe Harbor for Forward Looking Statements

Some of the statements in this presentation may include forward-looking

statements which reflect our current views with respect to future events and financial performance. Such statements include forward-looking statements both with respect to us in general and the insurance and reinsurance sectors specifically, both as to

underwriting and investment matters. Statements which include the

words "should," "expect," "intend,"

"plan," "believe," "project," "anticipate," "seek," "will," and similar statements of a future or forward-looking nature identify forward-looking statements in this

presentation for purposes of the U.S. federal securities laws or otherwise. We

intend these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements in the Private Securities Litigation Reform Act of 1995. All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or may be important

factors that could cause actual results to differ materially from those indicated in the forward-looking statements. These factors include, but are not limited to, the effects of competitors’

pricing policies, greater frequency or severity of claims and loss activity, changes in market conditions in the agriculture insurance industry, termination of or changes in the terms of the U.S. multiple peril crop

insurance program, a decreased demand for property and casualty

insurance or reinsurance, changes in the availability, cost or quality of

reinsurance or retrocessional coverage, our inability to renew business previously underwritten or acquired, our inability to maintain our applicable financial strength ratings, our inability to effectively integrate acquired operations, uncertainties in our

reserving process, changes to our tax status, changes in insurance

regulations, reduced acceptance of our existing or new products and services, a

loss of business from and credit risk related to our broker counterparties, assessments for high risk or otherwise uninsured individuals, possible terrorism or the outbreak of war, a loss of key personnel, political conditions, changes in insurance

regulation, changes in accounting policies, our investment

performance, the valuation of our invested assets, a breach of our investment

guidelines, the unavailability of capital in the future, developments in the world’s financial and capital markets and our access to such markets, government intervention in the insurance and reinsurance industry, illiquidity in the credit markets, changes in

general economic conditions and other factors described in our

Annual Report on Form 10-K and for the year ended December 31, 2104 and

Quarterly Report on Form 10-Q for the period ended June 30, 2015. Forward-looking statements speak only as of the date on which they are made, and we undertake no obligation publicly to update or

revise any forward-looking statement, whether as a result of new

information, future developments or otherwise.

Regulation G Disclaimer

In this presentation, management has included and discussed certain

non-GAAP measures. Management believes that these non-GAAP measures, which may be defined differently by other companies, better explain the Company's results of operations in a manner that allows for a more complete understanding of the underlying

trends in the Company's business. However, these measures

should not be viewed as a substitute for those determined in accordance with GAAP. For a complete description of non-GAAP measures and reconciliations, please review the Investor

Financial Supplement on our web site at

www.endurance.bm. The

combined ratio is the sum of the loss, acquisition expense and general and administrative expense ratios. Endurance presents the combined ratio as a measure that is commonly recognized as a

standard of performance by investors, analysts, rating agencies and other users

of its financial information. The combined ratio, excluding prior year net loss reserve development, enables investors, analysts, rating agencies and other users of its financial information to more easily analyze Endurance’s results of underwriting

activities in a manner similar to how management analyzes Endurance’s underlying business performance. The combined ratio, excluding prior year net loss reserve development, should not be viewed as a

substitute for the combined ratio. Net premiums written is

a non-GAAP internal performance measure used by Endurance in the management of its operations. Net premiums written represents net premiums written and deposit premiums, which are premiums on contracts that are deemed as either transferring only significant timing risk or transferring only

significant underwriting risk and thus are required to be accounted

for under GAAP as deposits. Endurance believes these amounts are

significant to its business and underwriting process and excluding them distorts the analysis of its premium trends. In addition to presenting gross premiums written determined in accordance with GAAP, Endurance believes that net premiums written enables investors,

analysts, rating agencies and other users of its financial

information to more easily analyze Endurance’s results of underwriting

activities in a manner similar to how management analyzes Endurance’s underlying business performance. Net premiums written should not be viewed as a substitute for gross premiums written determined in accordance with GAAP.

Return on Equity (ROE) is comprised using the average common equity calculated

as the arithmetic average of the beginning and ending common equity balances for stated periods. The Company presents various measures of Return on Equity that are commonly recognized as a standard of performance by investors, analysts, rating

agencies and other users of its financial information. |

• “A” ratings from A.M. Best and S&P • $3.8 billion of total capital as of June 30, 2015. MRH acquisition drives pro- forma total capital to greater than $5 billion. • Conservative, short-duration, AA- rated investment portfolio • Prudent reserves that have historically developed favorably since our inception • Diversified and efficient capital structure • Since inception, returned nearly $2.1 billion to investors through dividends and share repurchases Endurance Has Strong Foundation to Build on Strong balance sheet, diversified portfolio and robust infrastructure 3 Strategic Initiatives • Substantially expanded global underwriting and leadership talent • Optimized balance of insurance and reinsurance portfolios to lower volatility and improve profitability • Increased strategic purchases of reinsurance and retrocession to support growth and manage cycle • Streamlined support operations to generate significant savings to fund underwriting additions • Financial results beginning to reflect transformation initiatives Diversified Portfolio of Businesses • Gross premiums written of $3.2 billion on a trailing 12 month basis • Book of business contains insurance and reinsurance exposures as well as short tail and long tail lines • Proven leader in the U.S. agriculture insurance industry • Focus on specialty lines of business, with market recognized, industry- leading talent • Montpelier acquisition further diversifies distribution and market access with Lloyd’s and 3 rd party capital Strong Balance Sheet and Capital Strong and seasoned franchise • Inception to date operating ROE of 11.1% • 10 year book value per share plus dividends CAGR of 9.5% • Continuous improvement in performance and market positioning |

Larger book of

business with

lower volatility and improved return characteristics We Have Transformed Our Specialty Insurance and Reinsurance Businesses Starting in 2013 we rebalanced our insurance and reinsurance portfolios while expanding

our global underwriting talent to enhance our positioning and relevance in the

market The core of our underwriting leadership and talent is now in

place. Our goal is to produce a more consistent level

of profitability while reducing volatility in order to deliver excellent sustainable results for our shareholders. 4 Restructured business • Withdrawal from unprofitable lines and accounts • Management of limits • Strategic purchases of reinsurance and retrocessional coverages Improved underwriting talent • Attracted and retained teams of high quality underwriters • Expanded underwriting and product capabilities in insurance and reinsurance specialty lines • Newly added teams are generating strong premium flows with improved margins Expanding our international operations • Launched London based international insurance operation in 2014 and acquired MRH Lloyd’s franchise in 2015 • Zurich based marine and energy reinsurance team started in August 2014 • Expanded catastrophe reinsurance presence in Singapore Restructured operations • Streamlined leadership and operations to create efficiencies |

Specialty Insurance Strategic Direction – Scale, Balance and Diversification Expanded underwriting talent, refocused underwriting, rebalanced portfolio and improved

positioning and relevance in the global market

5 2012 $1.4B 2Q2015 * $1.9B Insurance Gross Premiums Written Agriculture 63% U.S. Specialty 23% Bermuda 14% Agriculture 46% U.S. Specialty 35% Bermuda 9% London 10% • Improved market presence through hiring of nearly 150 world class specialty underwriters in the U.S and London

• Increased market relevance with expanded geographies and products including: U.S. (Primary and excess

casualty, inland and ocean marine, numerous professional liability classes,

E&S property and commercial property) and London (energy,

property, professional lines and newly acquired Lloyd’s operation)

• Rebalanced portfolio by managing limits and by reducing unprofitable classes of business including NY City

contractors, DIC property, and numerous casualty exposures while growing

diversified specialty lines Rebalancing

Specialty Growth

Paired With * Based on a trailing 12 month basis. Excludes impact of Montpelier acquisition. |

Reinsurance Strategic Direction – Portfolio Enhancement Enhanced profitability by recruiting top flight underwriting talent, developing strategic

partnerships with key clients and brokers, and improving underwriting and risk

selection 6

2012 $1.1B 2Q2015 * $1.3B Reinsurance Gross Premiums Written Specialty 25% Property 19% Catastrophe 25% Professional 19% Rebalancing Specialty Growth Casualty 12% Specialty 11% Property 31% Catastrophe 34% Professional 5% Casualty 19% Paired With • Expanded specialty focus through hiring of industry leading specialty teams in Trade Credit and Surety, Marine and

Energy and Agriculture

• Improved balance and profit potential through re-underwriting and non-renewals in: treaty property, UK Motor, low

margin casualty treaties as well as numerous contracts that no

longer met our profit targets •

Enhanced leadership team and hired highly regarded North American team of

underwriters Significantly expanded profitable U.S. casualty and

professional lines quota share business •

Further expanded our international specialty book by an additional $70 million

at 1/1/2015 renewals * Based on a trailing 12 month basis.

Excludes impact of Montpelier acquisition. |

Portfolio Diversified by Product, Distribution Source and Geography

The transformation of Endurance has expanded product and geographic

diversification 7

2Q2015 * Gross Premiums Written: $3.2 Billion Reinsurance (39%) Insurance (61%) Casualty Professional Liability Property Per Risk Small Business Surety Clash Americas Property Catastrophe Asia Property Catastrophe Europe Property Catastrophe Workers Compensation Catastrophe U.S. Sponsored Multi Peril Crop Insurance (MPCI) Hail and other named peril covers Professional Lines Property Primary and Excess Casualty Miscellaneous E&O Healthcare Ocean/Inland Marine Surety Healthcare Excess Casualty Professional Lines Europe P&C - 2% Bermuda 6% U.S. Specialty 21% Global Catastrophe 10% North America 16% Agriculture 28% Global Specialty 10% Aviation & Space Marine & Energy Agriculture (International) Trade Credit, Surety and Political Risk Structured Reinsurance Weather Personal Accident Asia P&C - 1% International 6% Property Professional Lines Energy * Based on a trailing 12 month basis. Excludes impact of Montpelier acquisition. |

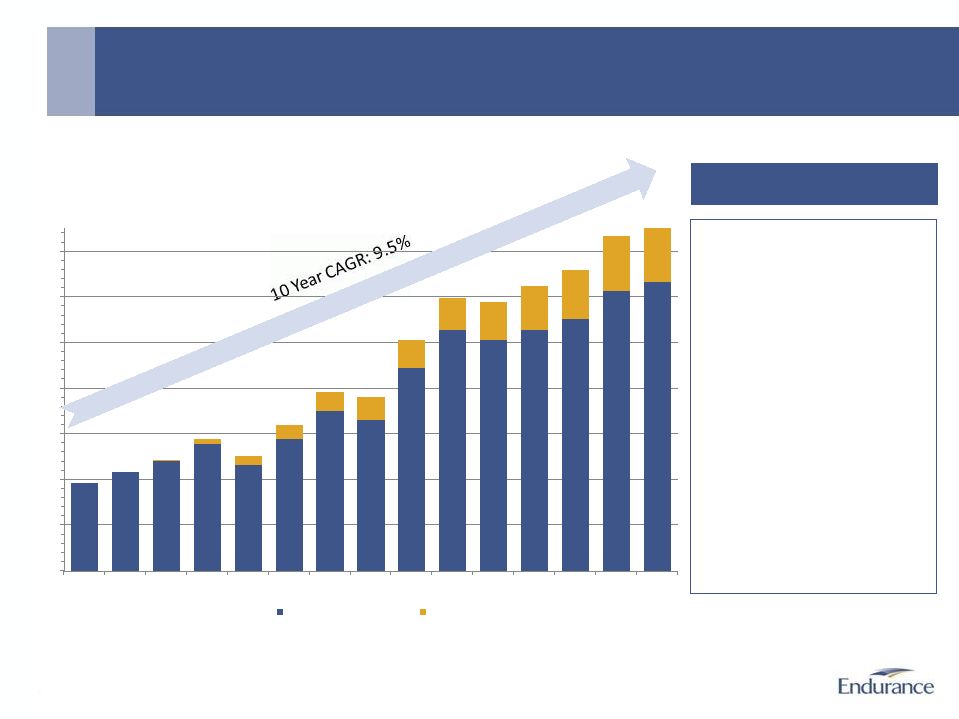

19.37 21.73 24.03 27.91 23.17 28.87 35.05 33.06 44.61 52.74 50.56 52.88 55.18 61.33 63.32 0.32 1.13 2.13 3.13 4.13 5.13 6.13 7.13 8.33 9.57 10.85 12.21 12.91 $0 $10 $20 $30 $40 $50 $60 $70 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2Q15 Book Value Per Share Cumulative Dividends Endurance’s Financial Results Diluted book value per common share has grown strongly 8 Growth in Diluted Book Value Per Common Share ($) From December 31, 2001 – June 30, 2015 • 2005 – Hurricanes Katrina, Rita and Wilma • 2008 – Credit crisis and related impact of marking assets to market • 2009 – Post crisis asset recovery • 2011 – High frequency of global catastrophes • 2012 – Superstorm Sandy and Midwest drought Significant Impacts to Book Value |

0% 5% 10% 15% 20% 25% 30% 1/1/11 7/1/11 1/1/12 7/1/12 1/1/13 7/1/13 1/1/14 7/1/14 1/1/15 7/1/15 Largest 1 in 100 PML as a % of Shareholders’ Equity Excellent Financial Strength and Risk Based Capital Position Strong flexibility to pursue value enhancing growth initiatives Endurance has significantly expanded its risk based capital position through strong results, prudent catastrophe

risk management and leverage of reinsurance market while also returning nearly

$2.1 billion to shareholders since inception through share

repurchases and dividends. We maintain excellent financial strength and flexibility to pursue our strategic objectives and profitably grow our business for the benefit of our shareholders.

9 Significantly Reduced Catastrophe Exposures* Excellent Financial Strength with Diversified Capital Base* * Excludes impact of Montpelier acquisition. 200 200 200 200 200 200 430 430 430 430 430 103 391 447 447 449 447 448 528 528 527 527 528 528 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 Common Equity Preferred Equity Debt 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2Q15 |

• Fixed maturity portfolio duration is 3.08 years in order to balance investment yield and interest rate risk • Investment quality (AA- average) has remained high as the portfolio is conservatively managed in a challenging economy – 33.0% of investments are cash/short term or US backed – Minimal exposure to sovereign debt or bank debt of European peripheral countries • Increased allocations to non-core fixed income to diversify portfolio, improve return potential and reduce interest rate risk • Other investments of $623.9 million consist of alternative funds (86.1%) and specialty funds (13.9%) – Alternative funds predominantly include hedge funds; complemented with some private equity funds. Hedge funds are mostly a balanced mix of credit and equity oriented strategies. – Specialty funds include high yield loan funds Conservatively Positioned Investment Portfolio Endurance maintains a high quality, short duration investment portfolio 10 $6.6 Billion Investment Portfolio at June 30, 2015* Cash and Short Term 8.8% Municipals and Foreign Government 3.0% Other Investments 9.5% Asset Backed and Non Agency Mortgage Backed – 26.5% Equities 6.3% Investment Portfolio Highlights * Excludes impact of Montpelier acquisition. U.S. Government / and U.S. Government Backed – 24.2% Corporate Securities 21.7% |

Acquisition of Montpelier Re

Closed on July 31, 2015 -

Key Transaction Terms

11 Transaction • Endurance acquired all of the common shares of Montpelier in a cash and stock acquisition Value • $1.9 billion purchase price • 1.22x Montpelier’s June 30 th unaudited GAAP common shareholders’ equity ($1.58 billion) Consideration Mix • Consideration mix of approximately 25% cash to Montpelier shareholders and 75% stock, including on a per

share basis:

$9.89 per share special pre-closing dividend of cash, and

0.472 Endurance shares (fixed exchange ratio)

Pro Forma Endurance

Ownership • 69% by existing Endurance shareholders • 31% by existing Montpelier shareholders Management and Board • Current Endurance management to remain in place • Increased Endurance’s Board of Directors at closing to include 3 current Montpelier Directors

Preferred Share

Redemption • Montpelier redeemed its preferred shares prior to their shareholder meeting at $26 per preferred share, or

$156 million in aggregate, plus declared and unpaid dividends, if any, to the

date of redemption |

The Acquisition of Montpelier Re is Strategically and Financially

Compelling Transaction Highlights

12 Increased Scale and Market Presence • Transaction creates an enterprise with over $3.6 billion (1) of annual gross premiums written • Increased size allows organization to better capitalize on distribution relationships and more effectively

compete across all market conditions

Diversified Platform

Across Products and

Geographies • Good-sized and scalable Lloyd’s platform expands distribution and product capabilities and provides

access to new markets to further accelerate Endurance’s London market

insurance growth strategy •

Addition of established third party capital management franchise (Blue

Capital) expands market presence, enhances capital flexibility

and provides stable source of income •

Montpelier’s attractive property catastrophe business complements

existing reinsurance portfolio •

Insurance to remain above 50% of the combined diversified portfolio

(1)

Stronger Balance

Sheet and Capital

Position • With common shareholders’ equity of $4.1 billion (2) and total capital of $5.5 billion (2) , the combined company will have a substantially improved financial profile • Larger, stronger balance sheet better positions combined company to pursue growth, withstand

volatility and manage capital

Manageable Integration Risk • Endurance immediately implemented integration and transition plans upon closing of the transaction

Financially Attractive

• Meaningful transaction synergies, including more than $70 million of annual run-rate cost savings. Above

original estimate of greater than $60 million.

• Expected to be immediately accretive to EPS and ROE, excluding non-recurring integration and

transaction costs

• Neutral to book value per share and modestly dilutive to tangible book value per share

• Potential for enhanced capital management over time Notes 1. Based on 2014 figures 2. Figures as of 12/31/14, pro forma for transaction. Based on Endurance closing share price of $64.30 as of 3/30/2015.

Shareholders’ equity and total capital exclude non-controlling interests |

Transaction Provides Increased Scale and Stronger Balance Sheet

13 2014 Gross Premiums Written of Peer Companies $Bn Notes 1. Pro forma for Platinum acquisition 2. As of 12/31/2014, XL, PRE + AXS and RNR common shareholders’ equity shown pro forma for stock issued in connection with transactions based on publicly filed pro forma

financial disclosure 3.

As of 12/31/2014, pro forma for the acquisition of MRH, does not include impact

of purchase accounting adjustments or transaction expenses Common

Shareholders’ Equity of Peer Companies

(12/31/14) $Bn

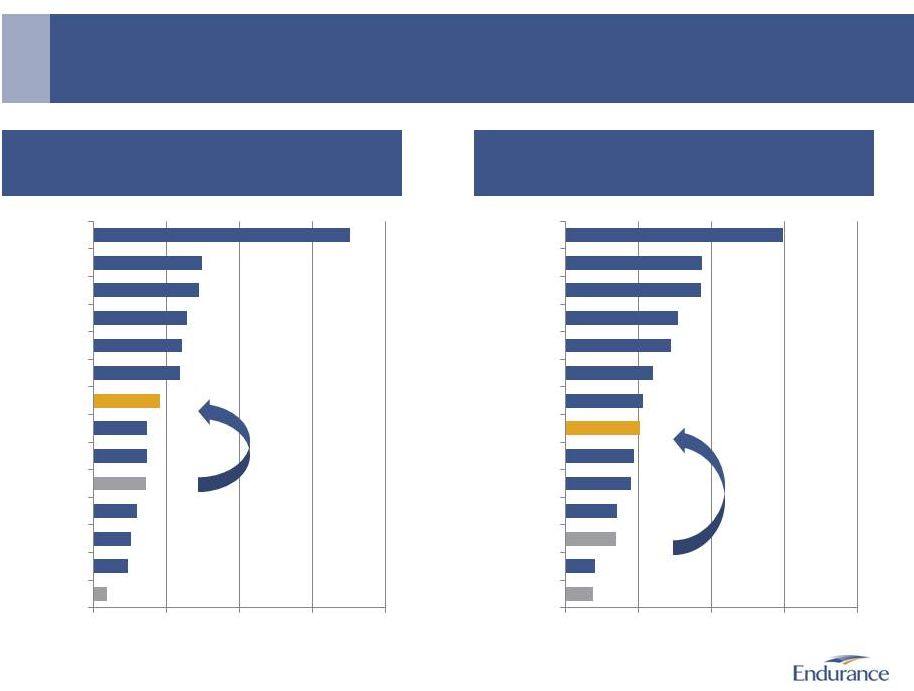

(1) (2) (2) (3) 11.9 7.5 7.5 6.2 5.8 4.8 4.2 4.1 3.8 3.6 2.9 2.8 1.6 1.5 0 4 8 12 16 XL + CGL Y RE PRE ACGL AXS RNR ENH + MRH AWH VR AHL ENH AGII MRH 14.1 5.9 5.7 5.1 4.8 4.7 3.6 2.9 2.9 2.9 2.4 2.1 1.9 0.7 0 4 8 12 16 XL + CGL PRE RE Y ACGL AXS ENH + MRH AWH AHL ENH VR AGII MRH RNR |

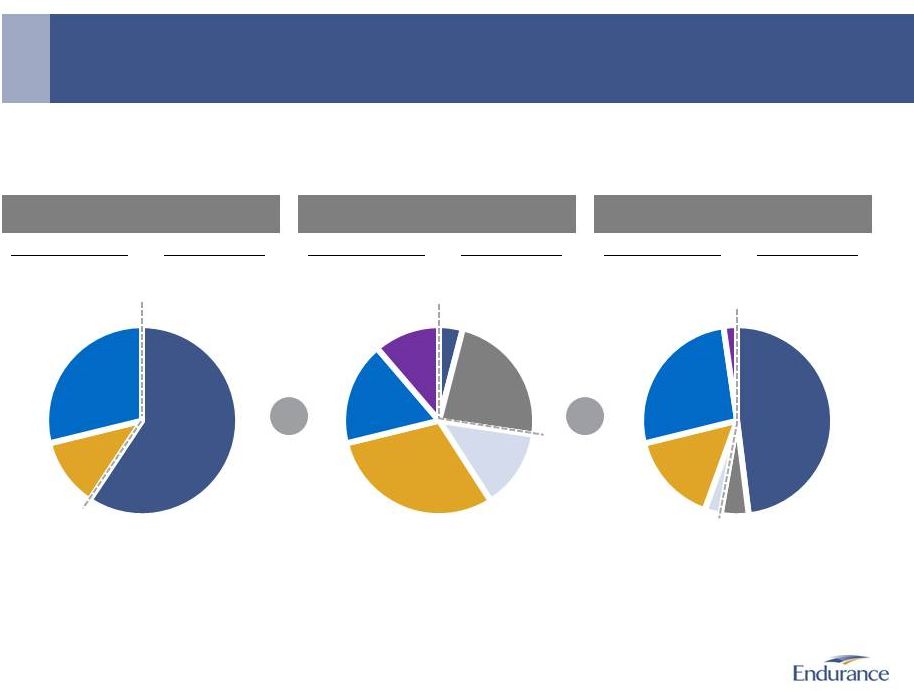

14 Endurance (1) Montpelier (1) (2) Combined Insurance 59% Property Catastrophe Reinsurance 30% Other Reinsurance 18% Other Insurance 4% + = Collateralized Re 11% Lloyd’s Insurance 23% GPW: $2.9Bn GPW: $0.7Bn GPW: $3.6Bn Property Catastrophe Reinsurance 16% Other Reinsurance 26% Other Insurance 48% Lloyd’s Insurance 5% • Meaningfully greater scale in reinsurance with premiums up ~35% • Overall business mix remains balanced, with over 50% insurance Property Catastrophe Reinsurance 12% Other Reinsurance 29% Collateralized Re 2% Notes 1. Based on full year 2014 gross premiums written 2. Montpelier insurance includes Property and Specialty Individual Risk; reinsurance includes Property Catastrophe – Treaty, Property Specialty – Treaty, and Other Specialty – Treaty Insurance: 59% $1.7Bn Reinsurance: 41% $1.2Bn Insurance: 27% $0.2Bn Reinsurance: 73% $0.5Bn Insurance: 53% $1.9Bn Reinsurance: 47% $1.7Bn Combined Business Well Diversified Across Business Lines and Platforms Lloyd’s Reinsurance 14% Lloyd’s Reinsurance 3% |

• Endurance has undergone a fundamental transformation to improve profitability and enhance market

relevance – Since John Charman joined Endurance in mid 2013 as Chairman and CEO Endurance has meaningfully

expanded its global specialty insurance and reinsurance capabilities

– Endurance has rebalanced its insurance and reinsurance portfolios to lower volatility and improve

profitability

• Benefits started to emerge in 2014 and have continued into 2015 • Endurance maintains excellent balance sheet strength and liquidity – Capital levels meaningfully exceed rating agency minimums, providing support for growth

– High quality investment portfolio; fixed maturity investments have an average credit quality of AA-

– Prudent reserving philosophy and strong reserve position; strong, consistent history of favorable

development • While market conditions are increasingly competitive, the outlook for Endurance remains attractive

– Industry leading specialty underwriting talent driving growth and improved underwriting and risk

selection; accident year loss ratios improved in both segments during

2014 and remained stable year to date in 2015

– Active management of exposures and reinsurance purchases has reduced expected portfolio volatility

– Expanded footprint of our specialty insurance and reinsurance franchise is improving market presence

and relevance

• Montpelier acquisition provides compelling value to Endurance’s shareholders

– New strategic capabilities with increased scale and market presence – Enhanced combined balance sheet and capital position – Manageable integration risk Conclusion Endurance is a compelling investment opportunity 15 |

Appendix |

Overview of ARMtech |

• Multi Peril Crop Insurance (MPCI) is an insurance product regulated by the USDA that provides farmers

with yield or revenue protection

– Offered by 18 licensed companies – Pricing is set by the government and agent compensation limits are also imposed - no pricing cycle exists – Reduced downside risks due to Federally sponsored reinsurance and loss sharing

– Agriculture insurance provides strong return potential, diversification in Endurance’s portfolio of

(re)insurance risks and is an efficient user of capital

• ARMtech is a leading specialty crop insurance business – Approximate 8% market share in MPCI (with estimated 201,000 total agriculture policies in force)

and is 5th largest of 18 MPCI industry participants

– MPCI 2015 crop year* estimated gross written premiums of $796 million – Portfolio is well diversified by geography and by crop • ARMtech was founded by software developers and has maintained a strong focus on providing industry

leading service through leveraging technology

• Endurance purchased ARMtech in December 2007 at a purchase price of approximately $125 million – ARMtech has grown MPCI policy count by 65.7% since 2007 Overview of ARMtech ARMtech has been a strong contributor to Endurance since its acquisition 18 * 2015 crop year is defined as July 1, 2014 through June 30, 2015 |

• ARMtech has built a market leading specialty crop insurance business through its focus on offering excellent service supported by industry leading technology. • MPCI policy count has grown 65.7% over the past seven years in a line of business not subject to the property/casualty pricing cycle. • ARMtech is a leader in using technology to deliver high quality service and to satisfy the intense compliance and documentation standards imposed on the industry by the U.S. Federal Government. • 2014 and 2015 industry premiums impacted by declines in commodity prices ARMtech is a Leader in Crop Insurance ARMtech’s focus on technology and service has allowed it to steadily grow its business

19 Written Premiums and Policy Counts by Crop Year Using technology and service to expand premiums ARMtech has demonstrated its ability to grow market share and premiums over time through its leading edge

technology and superior delivery of service and compliance.

* Estimated 2015 crop year premiums and policy

count ** Reflects cessions to the Federal Government as part

of the MPCI Program and not third party reinsurance purchases

103 108 134 244 378 363 372 526 488 534 469 448 106 98 134 140 187 220 157 276 332 380 337 348 0 20 40 60 80 100 120 140 160 180 200 220 $0 $100 $200 $300 $400 $500 $600 $700 $800 $900 $1,000 Crop Hail and LRP Premium Retained MPCI Premium** Ceded MPCI Premium Policy Count [000's] |

• 2015 estimated crop year MPCI net written premiums of $448.0 million*** are 4.4% lower than crop year 2014 – Commodity prices for spring crops declined 14% on average compared to a year ago – Estimated policy count growth of approximately 10.2% • The portfolio of 2015 crop risk is balanced by crop and geography • Purchased excess of loss reinsurance to reimburse for losses from 90% to 95% on MPCI portfolio as well as 90% quota share for crop hail products • The decline in estimated 2015 crop year MPCI net written premiums is principally due to declines in crop commodity prices and increased cessions to the federal government and third parties, partially offset by increased policy counts and new products ARMtech is Increasing Market Share and Geographic Diversification 2012 through 2015 were very strong marketing years for ARMtech ARMtech continues to focus on diversifying its business geographically while managing its exposure to Texas through

active use of available reinsurance protections.

20 Estimated 2015 Net Written Crop Year Premiums * Group One States – IL, IN, IA, MN, NE Group Two States – States other than Group One and Group Three states Group Three States – CT, DE, MA, MD, NV, NH, NJ, NY, PA, UT, WY, WV ** Estimated 2015 crop year premiums *** Reflects cessions to the Federal Government as part of the MPCI Program and not third party reinsurance purchases MPCI Net Written Premiums by Crop Year and State Grouping *,*** 62.5 100.5 104.6 77.2 129.9 149.9 163.4 136.4 115.5 126.2 202.3 189.9 200.6 257.1 228.1 265.5 217.4 234.4 52.0 68.8 58.8 82.2 131.8 105.1 99.4 108.0 92.4 $0 $100 $200 $300 $400 $500 $600 2007 2008 2009 2010 2011 2012 2013 2014 2015** Group One States Group Two States (Excl. Texas) Texas Group Three States |

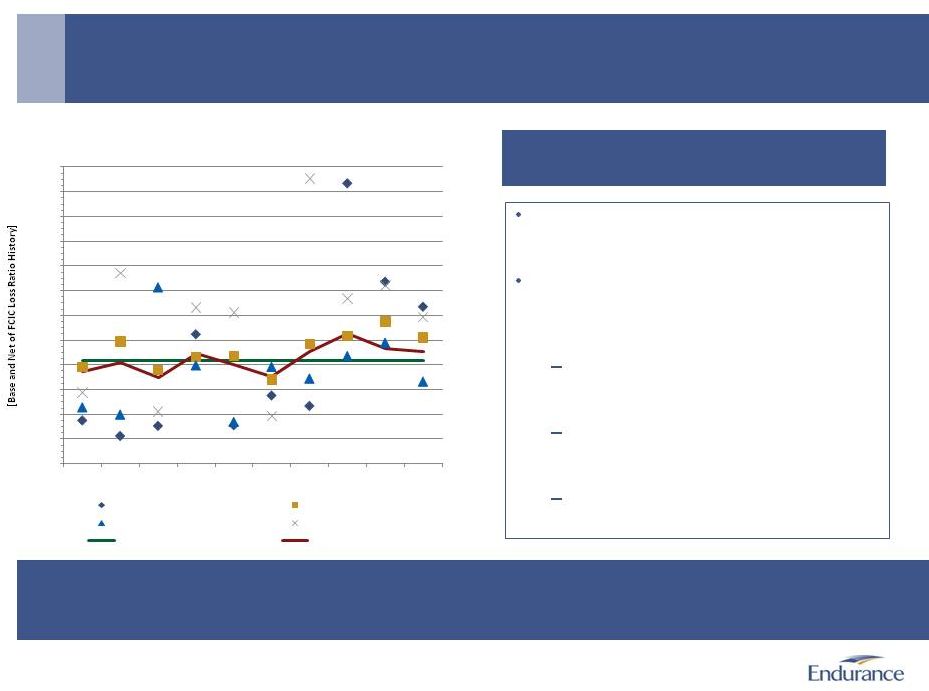

• While individual states can produce large loss ratios, the U.S. Federal reinsurance program has historically reduced loss ratio volatility. • ARMtech’s business has historically produced stable profits over time after reflecting the reinsurance terms set out in the current standard crop reinsurance agreement – Historic average loss ratio post U.S. Federal cessions has been 83.5% (adjusted for the 2011 Federal reinsurance terms) – The best year was 2007 with a 69.8% net loss ratio and the worst was 2012 with a 104.0% net MPCI loss ratio – ARMtech’s current expense run rate after the A&O subsidy is approximately 7% - 8% Agriculture Insurance is Not Correlated with the P&C Cycle FCIC reinsurance lowers volatility 21 Stable Results in Volatile Times Historic MPCI Crop Year Loss Ratio Results (Pre and Post Federal Reinsurance) While individual states can produce highly varied gross loss ratios on a year to year basis, the U.S. Federal

reinsurance program has historically mitigated that volatility and leaves ARMtech with a business which is not correlated to the traditional P&C pricing cycle and has high risk adjusted return potential.

0% 20% 40% 60% 80% 100% 120% 140% 160% 180% 200% 220% 240% 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Gross L/R Group 1 States Gross L/R Group 2 States Gross L/R Group 3 States Gross L/R Texas Avg. Net L/R Net L/R All States |

Overview of ARMtech

ARMtech’s recognition of premiums and earnings are influenced by growing seasons 22 Seasonality of MPCI Business First Quarter Third Quarter Second Quarter Recognition of annual written premiums 60% - 65% Spring crops 20% - 25% Spring crop acreage report adjustments Winter crops 10% - 15% Spring crop adjustments due to actual cessions 5% - 10% Winter crop adjustments Recognition of annual earned premiums 10%-15% Largely driven by winter crops 30% - 35% Largely driven by spring crops 25% - 30% Driven by spring crops and winter crops 25% - 30% Largely driven by spring crops Harvest Harvest of winter crops Harvest of spring crops Fourth Quarter Commodity price setting Setting of base prices for spring crops (forward commodity price for fourth quarter) Setting of base prices for winter crops (forward commodity price for second quarter) Harvest price determined for winter crops Harvest price determined for spring crops |

2.3% 0.2% 0.5% 1.1% 1.0% 0.4% 5.9% 3.9% 5.4% 2.0% 3.3% 21.2% 1.7% 1.5% 0.9% 3.3% 8.9% 6.5% 0.6% 1.9% 0.9% 3.8% 3.3% 1.2% 2.5% 3.4% 1.5% 4.0% 3.3% 1.7% 0.7% Geographic Diversification of Crop Insurance Business ARMtech maintains a geographically diversified portfolio of risk 23 ARMtech’s 2015 Estimated Crop Year MPCI Net Written Premiums |

Diversification of Crops Within ARMtech’s Portfolio Underwritten risks diversified by geography and commodity type 24 ARMtech’s 2015 Estimated Crop Year MPCI Net Written Premiums Iowa – 6.0% Nebraska – 3.7% Minnesota – 2.7% Indiana – 2.4% South Dakota – 2.1% Missouri – 1.7% Texas – 1.7% North Dakota – 1.6% Illinois – 1.4% Colorado – 1.2% Kentucky – 1.0% Tennessee – 0.7% Ohio – 0.6% Kansas – 0.5% Mississippi – 0.5% South Carolina – 0.4% Wisconsin – 0.4% Maryland – 0.2% All other states – 1.4% Corn (30.2%) Texas – 10.7% Georgia – 1.5% Alabama – 0.7% Mississippi – 0.6% South Carolina – 0.4% All other states – 1.0% Cotton (14.9%) Iowa – 2.9% Minnesota – 2.4% Mississippi – 2.0% Kentucky – 1.5% Nebraska – 1.4% North Dakota – 1.4% Indiana –1.3% Missouri – 1.2% Tennessee – 1.2% Arkansas – 0.8% South Dakota – 0.7% Ohio – 0.6% Illinois – 0.5% All other states – 2.8% Soybeans (20.7%) Other Crops (21.8%) Wheat (12.4%) Texas – 3.6% Colorado – 1.5% North Dakota – 1.5% Kansas – 0.8% Oklahoma – 0.7% Minnesota – 0.7% All other states – 3.6% Grain Sorghum – 3.6% Citrus, Nursery & Orange Trees - 2.2% Apples – 1.9% Pasture, Rangeland, Forage – 1.6% Peanuts – 1.6% Tobacco – 1.1% Potatoes – 1.0% Dry Beans – 0.8% Barley – 0.7% Rice – 0.6% All other crops – 6.7% |

Agriculture Insurance Contains Four Layers of Risk Mitigation

Farmers retention, ceding premiums to the U.S. Federal Government, limitations

on losses and gains and purchase of stop loss

protection 25

45.0% of MPCI Premiums Ceded to U.S. Federal Government

Assigned Risk Fund

“Higher Risk Policies”

Commercial Fund

“Lower Risk Policies”

2015 Crop Year

Gross Liability

66.9% of risk retained by ARMtech

33.1% of first dollar risk retained by

farmers 14.5% of 2015 Crop Year NWP 85.5% of 2015 Crop Year NWP Loss Sharing (% of loss retained by Loss Ratio Loss Ratio Group 1 States Group 2 & 3 States ARMtech within each 100 - 160 7.5% 100 - 160 65.0% 42.5% applicable band when 160 - 220 6.0% 160 - 220 45.0% 20.0% the loss ratio is above 100%.) 220 - 500 3.0% 220 - 500 10.0% 5.0% Gain Sharing (% of gain retained by Loss Ratio Loss Ratio Group 1 States Group 2 & 3 States ARMtech within each 65 - 100 22.5% 65 - 100 75.0% 97.5% applicable band when 50 - 65 13.5% 50 - 65 40.0% 40.0% the loss ratio is below 100%.) 0 - 50 3.0% 0 - 50 5.0% 5.0% |

ARMtech Has Grown Market Share Over Time Superior service and technology have driven growth in stable market 26 % Change in Crop Year Market Share Market Share MPCI Certified Companies (Owners) 2014 2013 2012 2011 2010 2009 2008 2007 2007 - 2014 Rain and Hail (ACE) (1) 19.9% 20.8% 21.3% 21.8% 22.6% 24.3% 24.1% 25.0% -5.1% Rural Community Insurance Co. (Wells Fargo) 19.1% 20.6% 22.1% 21.8% 22.9% 24.7% 25.2% 25.1% -6.0% NAU Country Insurance Company (QBE) (1) 13.3% 13.1% 13.3% 14.8% 14.4% 13.7% 13.8% 13.3% 0.0% Great American Insurance Co. (American Fin. Group) 8.5% 8.5% 8.5% 8.7% 8.7% 9.1% 10.1% 10.6% -2.2% American Agri-Business Ins. Co. (Endurance) 8.0% 7.7% 7.4% 6.7% 7.0% 6.5% 5.7% 5.9% 2.1% Farmers Mutual Hail Ins. of Iowa (1) 7.7% 8.0% 7.6% 7.8% 8.0% 7.7% 7.3% 7.0% 0.7% CGB Insurance Co. (CGB Diversified Services) 5.3% 4.6% 4.0% 2.7% 2.0% 1.2% 1.2% 1.1% 4.1% Producers Ag Ins. Co. (HCC) 5.1% 4.9% 5.5% 6.4% 6.3% 5.3% 5.2% 4.8% 0.3% Agrinational Insurance Company (Agriserve - ADM) 3.8% 3.1% 2.5% 2.1% 1.5% 0.9% 1.0% 1.1% 2.7% Hudson Insurance Company (Fairfax) (1) 2.3% 2.0% 1.6% 1.2% 1.2% 0.8% 0.6% 0.4% 1.9% Heartland (Everest) 1.8% 2.4% 2.3% 2.4% 3.0% 3.4% 3.3% 3.2% -1.5% AgriLogic (Occidental Fire & Casualty Co.) 1.3% 1.6% 1.8% 1.4% 0.1% 0.0% 0.0% 0.0% 1.3% American Agricultural Ins. Co. (Amer Farm Bureau) 1.1% 1.2% 1.3% 1.3% 1.3% 1.4% 1.4% 1.2% 0.0% Country Mutual Insurance Company 0.8% 0.9% 0.9% 0.9% 1.0% 1.1% 1.2% 1.4% -0.5% Global Ag (XL Reins.) 0.8% 0.4% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.8% International Ag (Starr Indemnity) 0.6% 0.3% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.6% Climate Corp (Atlantic Specialty Ins. Co.) 0.5% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.5% Crop Pro (Technology Insurance Company) 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% Source – National Crop Insurance Services (NCIS) (1) Crop Year Market Share was increased to reflect the acquisition of a company between 2007 and 2014.

|

Other Miscellaneous Information |

Probable Maximum Loss by Zone and Peril

Largest 1 in 100 year PML as of July 1, 2015 is equal to 8.0% of

Shareholders’ Equity as of June 30, 2015

28 Estimated Occurrence Net Loss as of July 1, 2015

July 1, 2014

July 1, 2013

Zone

Peril

10

Year

Return

Period

25

Year

Return

Period

50

Year

Return

Period

100

Year

Return

Period

250

Year

Return

Period

100

Year

Return

Period

100

Year

Return

Period

United States

Hurricane

$112

$157

$200

$265

$362

$284

$350

Europe

Windstorm

69

109

125

220

343

345

331

California

Earthquake

40

120

171

229

354

250

284

Japan

Windstorm

45

96

118

129

181

158

230

Northwest U.S.

Earthquake

—

5

34

98

166

91

89

Japan

Earthquake

18

88

132

154

222

163

137

United States

Tornado/Hail

30

45

59

74

93

78

89

Australia

Earthquake

1

9

34

77

116

121

87

New Zealand

Earthquake

1

6

15

34

72

35

23

Australia

Windstorm

5

17

35

56

81

88

58

New Madrid

Earthquake

—

—

—

10

84

6

7

The net loss estimates by zone above represent estimated losses related to our

property, catastrophe and other specialty lines of business, based upon our catastrophe models and assumptions regarding the location, size, magnitude, and frequency of the catastrophe events utilized to determine

the above estimates. The net loss estimates are presented on an

occurrence basis, before income tax and net of reinsurance recoveries and reinstatement premiums, if applicable. Return period refers to the frequency with which the related size of a catastrophic event is expected to occur.

Actual realized catastrophic losses could differ materially from our net loss

estimates and our net loss estimates should not be considered as representative of the actual losses that we may incur in

connection with any particular catastrophic event. The net loss estimates above rely significantly on computer models created to simulate the effect of catastrophes on insured properties based upon data emanating from past catastrophic events. Since

comprehensive data collection regarding insured losses from

catastrophe events is a relatively recent development in the insurance industry, the data upon which catastrophe models is based is limited, which has the potential to introduce inaccuracies into estimates of losses from catastrophic events, in

particular those that occur infrequently. In addition,

catastrophe models are significantly influenced by management’s assumptions regarding event characteristics, construction of insured property and the cost and duration of rebuilding after the catastrophe. Lastly, changes in Endurance’s underwriting

portfolio risk control mechanisms and other factors, either

before or after the date of the above net loss estimates, may also cause actual results to vary considerably from the net loss estimates above. For a listing of risks related to Endurance and its future performance, please see “Risk Factors” in our Annual Report

on Form 10-K for the year ended December 31, 2014 and in our

Quarterly Report on Form 10-Q for the quarter ended June 30, 2015.

|

• Book value per common share, adjusted for dividends, expanded 1.4% during second quarter 2015

– Net income attributable to common shareholders of $76.0 million • Relatively stable accident year loss ratios in both segments • General and administrative expenses were lower due to expense management and increased ceding

commissions • Light catastrophe activity • Energy losses impacted the insurance segment • Gross written premiums of $861.2 million were 24.9% higher than second quarter 2014

– Insurance gross written premiums of $468.9 million were 45.8% higher than second quarter 2014

• Strong growth in our U.S. specialty and London operations as underwriting investments made over the

last 30 months is attracting new business.

– Reinsurance gross written premiums of $392.3 million increased 6.6% compared to second quarter 2014

• Growth within casualty and professional lines was partially offset by declines within property, catastrophe

and specialty.

• Net written premiums increased 9.3% compared to second quarter 2014, a lower growth level than gross premiums

as significant reinsurance/retrocessional protection has been purchased to

reduce potential volatility. Second Quarter 2015

Highlights Results were driven by strong underwriting margins

supported by light catastrophe losses and favorable

development 29 |

Financial Results for Second Quarter 2015 and 2014

30 $MM (except per share data and %) June 30, 2015 June 30, 2014 $ Change % Change Net premiums written 559.1 511.4 47.7 9.3% Net premiums earned 458.1 481.5 (23.4) -4.9% Net investment income 32.3 39.3 (7.0) -17.8% Net underwriting income 80.5 80.6 (0.1) -0.1% Net income to common shareholders 76.0 75.0 1.0 1.3% Operating income to common shareholders 79.5 71.9 7.6 10.6% Fully diluted net income EPS 1.68 1.68 - 0.0% Fully diluted operating income EPS 1.76 1.61 0.15 9.3% Financial highlights June 30, 2015 June 30, 2014 Operating ROE (annualized) 11.1% 10.9% Net loss ratio 52.2% 53.8% Acquisition expense ratio 18.5% 16.3% General and administrative expense ratio 14.8% 18.0% Combined ratio 85.5% 88.1% Diluted book value per share $63.32 $60.00 Key operating ratios |

Gross Written Premiums for Second Quarter 2015 and 2014

31 In $MM June 30, 2015 June 30, 2014 $ Change % Change Casualty and other specialty 146.1 108.0 38.0 35.3% Agriculture 112.0 80.5 31.5 39.1% Professional lines 96.7 74.7 22.1 29.5% Property, marine and energy 114.1 58.3 55.8 95.7% Total insurance 468.9 321.5 147.4 45.8% Insurance Segment Reinsurance Segment In $MM June 30, 2015 June 30, 2014 $ Change % Change Professional lines 134.2 84.1 50.1 59.6% Casualty 48.1 30.9 17.3 55.7% Catastrophe 139.8 158.4 -18.5 -11.7% Property 30.6 42.9 -12.3 -28.7% Specialty 39.6 51.6 -12.1 -23.3% Total reinsurance 392.3 367.9 24.4 6.6% |

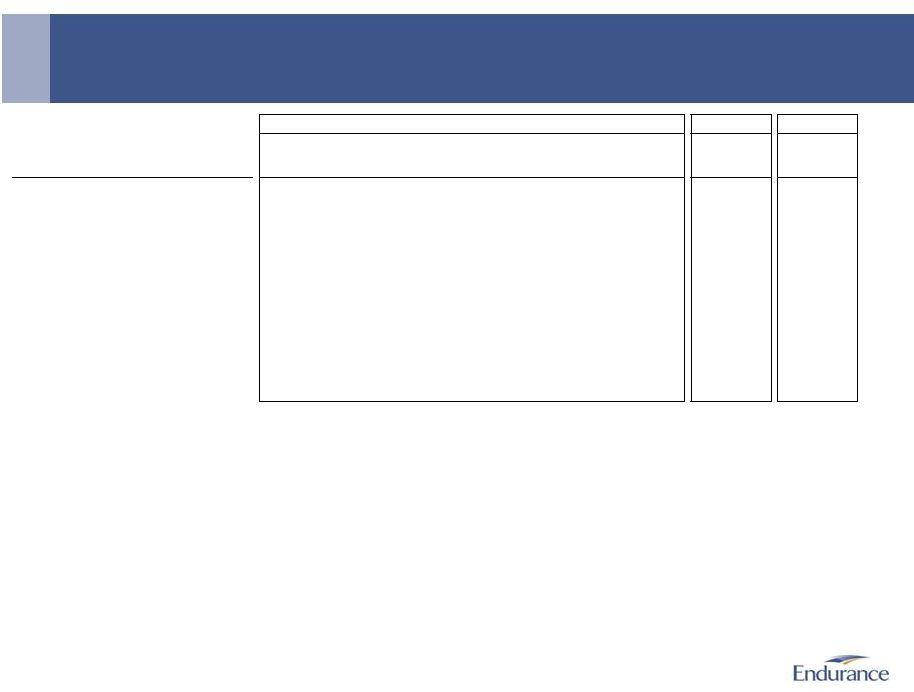

Financial Overview: Inception to Date Financial Performance

In $MM 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2Q15 Inception to date Net premiums written 765 1,598 1,697 1,619 1,586 1,575 1,784 1,606 1,764 1,980 2,029 2,049 1,934 1,324 23,310 Net premiums earned 369 1,174 1,633 1,724 1,639 1,595 1,766 1,633 1,741 1,931 2,014 2,016 1,864 848 21,947 Net underwriting income (loss) 51 179 232 -410 304 322 111 265 195 -252 -48 195 255 164 1,563 Net investment income 43 71 122 180 257 281 130 284 200 147 173 166 132 74 2,260 Net income (loss) before preferred dividend 102 263 356 -220 498 521 100 555 365 -94 163 312 348 193 3,462 Net income (loss) available to common shareholders 102 263 356 -223 483 506 85 539 349 -118 130 279 316 176 3,243 Diluted EPS $1.73 $4.00 $5.28 ($3.60) $6.73 $7.17 $1.33 $9.00 $6.38 ($2.95) $3.00 $6.37 $7.06 $3.91 $55.41 Financial highlights from 2002 through June 30, 2015 Key Operating Ratios 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2Q15 Inception to date Combined ratio 86.2% 84.7% 85.8% 123.5% 81.5% 79.9% 93.5% 84.0% 88.7% 112.9% 102.3% 90.2% 86.0% 84.1% 93.3% Operating ROE 7.8% 17.3% 19.9% (11.9%) 25.7% 23.8% 8.5% 22.0% 12.6% (6.3%) 2.4% 11.9% 11.7% 12.1% 11.1% Book value per share $21.73 $24.03 $27.91 $23.17 $28.87 $35.05 $33.06 $44.61 $52.74 $50.56 $52.88 $55.18 $61.33 $63.32 32 |

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- NV Gold Announces Secured Loan Terms

- FluroTech and GS Heli Announce Execution of Definitive Agreement

- Stockholder Alert: Robbins LLP Informs Investors of the Class Action Filed Against Sharecare, Inc. (SHCR)

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!