Form 8-K CIT GROUP INC For: Jul 28

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): July 28, 2016 (July 28, 2016)

CIT GROUP INC.

(Exact name of registrant as specified in its charter)

| Delaware | 001-31369 | 65-1051192 |

| (State or other | (Commission | (IRS Employer |

| jurisdiction of | File Number) | Identification No.) |

| incorporation) |

11 West 42nd Street

New York, New York 10036

(Address of registrant's principal executive office)

Registrant's telephone number, including area code: (212) 461-5200

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

[ ] Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

[ ] Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

[ ] Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

[ ] Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Section 2 – Financial Information

Item 2.02. Results of Operations and Financial Condition.

This Current Report on Form 8-K includes as an exhibit a press release, dated July 28, 2016, reporting the financial results of CIT Group Inc. (the “Company”) as of and for the quarter ended June 30, 2016. The press release is attached as Exhibit 99.1. This press release includes certain non-GAAP financial measures. A reconciliation of those measures to the most directly comparable GAAP measures is included as a table to the press release. The information furnished under this Item 2.02, including Exhibit 99.1, shall be considered filed for purposes of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Section 7 – Regulation FD

Item 7.01. Regulation FD Disclosure.

In addition, this Form 8-K includes a copy of the Company’s presentation to analysts and investors of its Second Quarter 2016 Financial Results for the quarter ended June 30, 2016, which is attached as Exhibit 99.2. The information included in Exhibit 99.2 shall not be considered filed for purposes of the Exchange Act. The Company also provides supplementary financial information on its website, which is not incorporated by reference in this Form 8-K.

Section 9 – Financial Statements and Exhibits

Item 9.01. Financial Statements and Exhibits.

| (d) | Exhibits. |

| 99.1 | Press release issued by CIT Group Inc. on July 28, 2016 reporting its financial results as of and for the quarter ended June 30, 2016. | |

|

99.2

|

Presentation by CIT Group Inc. on July 28, 2016 regarding its Second Quarter 2016 Financial Results.

|

Forward-Looking Statements

This Form 8-K contains forward-looking statements within the meaning of applicable federal securities laws that are based upon our current expectations and assumptions concerning future events, which are subject to a number of risks and uncertainties that could cause actual results to differ materially from those anticipated. The words “expect,” “anticipate,” “estimate,” “forecast,” “initiative,” “objective,” “plan,” “goal,” “project,” “outlook,” “priorities,” “target,” “intend,” “evaluate,” “pursue,” “commence,” “seek,” “may,” “would,” “could,” “should,” “believe,” “potential,” “continue,” or the negative of any of those words or similar expressions is intended to identify forward-looking statements. All statements contained in this Form 8-K, other than statements of historical fact, including without limitation, statements about our plans, strategies, prospects and expectations regarding future events and our financial performance, are forward-looking statements that involve certain risks and uncertainties. While these statements represent our current judgment on what the future may hold, and we believe these judgments are reasonable, these statements are not guarantees of any events or financial results, and our actual results may differ materially. Important factors that could cause our actual results to be materially different from our expectations include, among others, the risk that CIT is unsuccessful in implementing its strategy and business plan, the risk that CIT is unable to react to and address key business and regulatory issues, the risk that CIT is unable to achieve the projected revenue growth from its new business initiatives or the projected expense reductions from efficiency improvements, and the risk that CIT becomes subject to liquidity constraints and higher funding costs. We describe these and other risks that could affect our results in Item 1A, “Risk Factors,” of our latest Annual Report on Form 10-K for the year ended December 31, 2015, which was filed with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on the forward-looking statements contained in this Form 8-K. These forward-looking statements speak only as of the date on which the statements were made. CIT undertakes no obligation to update publicly or otherwise revise any forward-looking statements, except where expressly required by law.

2

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| CIT GROUP INC. | ||

| (Registrant) | ||

| | ||

| By: | /s/ E. Carol Hayles | |

| E. Carol Hayles | ||

| Executive Vice President & | ||

| Chief Financial Officer | ||

Dated: July 28, 2016

3

Exhibit 99.1

1

FOR IMMEDIATE RELEASE

CIT REPORTS SECOND QUARTER 2016 NET INCOME OF $14 MILLION ($0.07 PER DILUTED SHARE);

INCOME FROM CONTINUING OPERATIONS OF $181 MILLION ($0.90 PER DILUTED SHARE)

- Net Income includes After-Tax Charges of ($163) million ($0.80) Per Diluted Share Related to Discontinued Operations – Increased Interest Curtailment Reserve and related contingent liabilities in Financial Freedom, the reverse mortgage servicing business that was part of the OneWest Bank acquisition in 2015;

- Stable Core Operating Trends – Pre-tax income from continuing operations improved over $70 million from the prior quarter resulting from a lower credit provision; Non-accrual loans fell by 4%;

- Advanced Commercial Air Separation – Filed Initial Form 10 Registration Statement for C2 Aviation Capital and progressed to second round of bidding in conjunction with our dual track process;

- Continued Portfolio Optimization – Executed a definitive agreement to sell our Canadian Equipment and Corporate Finance Business; Transferred remaining Business Air assets to held for sale;

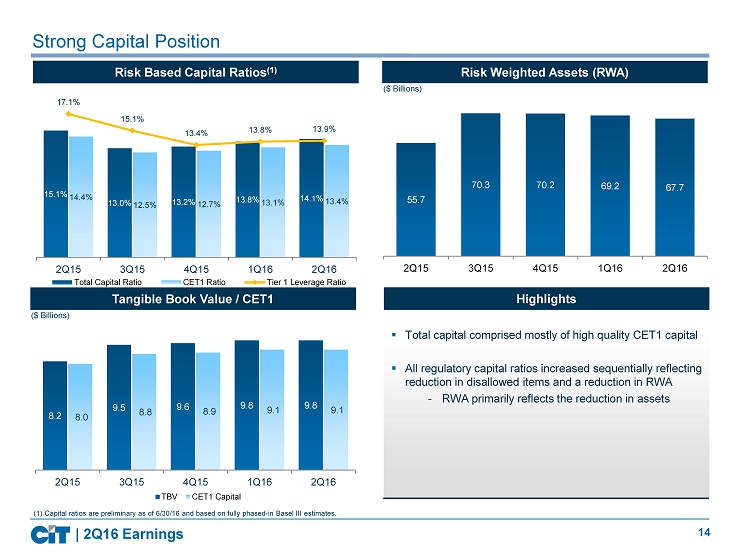

- Maintained Strong Capital Ratios – Common Equity Tier 1 of 13.4% and Total Capital Ratio of 14.1%.

NEW YORK, NY – July 28, 2016 – CIT Group Inc. (NYSE: CIT), today reported net income of $14 million, $0.07 per diluted share, for the quarter ended June 30, 2016, compared to net income of $115 million, $0.66 per diluted share for the year-ago quarter. Income from continuing operations for the second quarter was $181 million, $0.90 per diluted share compared to $115 million, $0.66 per diluted share in the year-ago quarter.

Net income for the six month period ended June 30, 2016 was $161 million, $0.80 per diluted share, compared to $219 million, $1.24 per diluted share, for the period ended June 30, 2015. Income from continuing operations for the six month period ended June 30, 2016 was $333 million, $1.65 per diluted share, compared to $219 million, $1.24 per diluted share for the six month period ended June 30, 2015.

The loss of $167 million in discontinued operations relates to Financial Freedom, a reverse mortgage servicing business that was part of the OneWest Bank acquisition in August 2015. As disclosed in CIT’s Form 10-K for fiscal year 2015, CIT determined that there was a material weakness related to the Home Equity Conversion Mortgage (“HECM”) interest curtailment reserve associated with this business. During the current quarter, as a result of the ongoing process to remediate the material weakness and taking into consideration the investigation being conducted by the Office of Inspector General (“OIG”) for the Department of Housing and Urban Development, the Company recorded additional reserves, due to a change in estimate, of $230 million. This review and the related investigation are ongoing and, as a result, the amount of this reserve could change prior to the filing of the current quarter Form 10-Q.

2

“We are disappointed that the additional charges arising from the legacy Financial Freedom business, which was part of the OneWest Bank acquisition, offset the improved earnings from continuing operations. Despite the impact it had on our financial results, we made good progress this quarter advancing our strategic goals,” said Ellen Alemany, Chief Executive Officer. “We filed the initial Form 10 Registration Statement for C2 Aviation Capital as part of our Commercial Air separation and have advanced to the second round of the bidding process. We entered into a definitive agreement to sell our Canadian Equipment and Corporate Finance Business and we transferred our remaining Business Air assets to held for sale. We remain committed to executing on our strategy to grow our core businesses, reduce operating expenses and improve returns.”

3

Summary of Second Quarter Financial Results from Continuing Operations

All references in this section relate to continuing operations and therefore do not include any of the assets or results of operations of the discontinued operations.

On August 3, 2015, CIT acquired IMB HoldCo LLC, the parent company of OneWest Bank, which impacts the comparability of current results to prior periods. The current and prior quarters reflect a full quarter of OneWest Bank’s results of operations while the prior-year period does not include any results from OneWest Bank.

Selected Financial Highlights (Continuing Operations)

| Change from: | ||||||||||||||||||||

| 2Q16 | 1Q16 | 2Q15 | Prior Quarter* | Prior Year* | ||||||||||||||||

| ($ in millions, except per share data) | ||||||||||||||||||||

| Pre-tax income | $ | 275 | $ | 204 | $ | 153 | $ | 71 | $ | 122 | ||||||||||

| Net income | $ | 181 | $ | 152 | $ | 115 | $ | 29 | $ | 66 | ||||||||||

| Diluted earnings per share (EPS) | $ | 0.90 | $ | 0.75 | $ | 0.66 | $ | 0.14 | $ | 0.24 | ||||||||||

| Pre-tax return on average earning assets (ROAEA) | 1.86 | % | 1.38 | % | 1.49 | % | 0.48 | % | 0.37 | % | ||||||||||

| Return on average earning assets (ROAEA) | 1.22 | % | 1.02 | % | 1.12 | % | 0.20 | % | 0.10 | % | ||||||||||

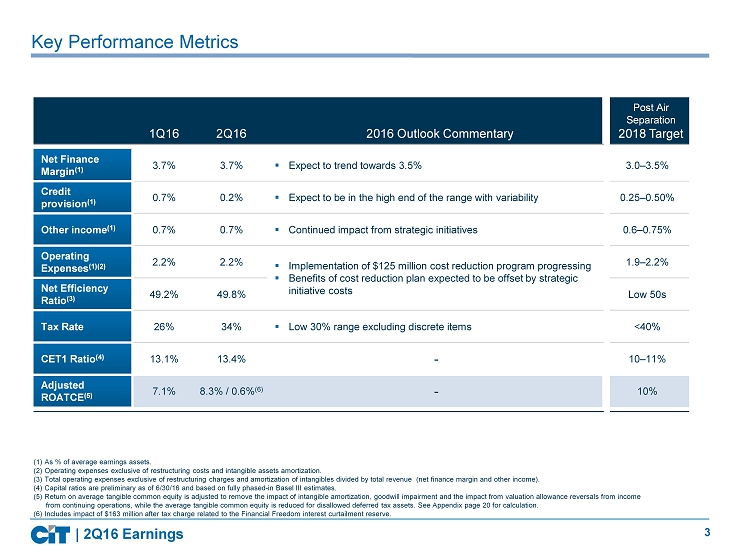

| Adjusted return on tangible common equity (ROTCE)(1) | 8.26 | % | 7.08 | % | 5.89 | % | 1.18 | % | 2.37 | % | ||||||||||

| Net finance margin(1) | 3.65 | % | 3.74 | % | 3.33 | % | -0.08 | % | 0.32 | % | ||||||||||

| Net efficiency ratio(1) | 49.8 | % | 49.2 | % | 57.4 | % | 0.60 | % | -7.58 | % | ||||||||||

| Tangible book value per share (TBVPS)(1) | $ | 48.45 | $ | 48.39 | $ | 47.51 | $ | 0.06 | $ | 0.93 | ||||||||||

| CET 1 Ratio(2) | 13.4 | % | 13.1 | % | 14.4 | % | 0.3 | % | -1.0 | % | ||||||||||

| Total Capital Ratio(2) | 14.1 | % | 13.8 | % | 15.1 | % | 0.3 | % | -1.0 | % | ||||||||||

| Net charge-offs as % of AFR | 0.53 | % | 0.65 | % | 0.48 | % | -0.12 | % | 0.05 | % | ||||||||||

| Allowance for loan losses as % of finance receivables | 1.31 | % | 1.29 | % | 1.14 | % | 0.02 | % | 0.17 | % | ||||||||||

| Average earning assets | $ | 59,229 | $ | 59,206 | $ | 41,159 | $ | 23 | $ | 18,070 | ||||||||||

| Financing and leasing assets | $ | 49,725 | $ | 50,286 | $ | 35,846 | $ | (561 | ) | $ | 13,879 | |||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

| (1) See "Non-GAAP Measurements" at the end of this press release and page 23 for reconciliation of non-GAAP to GAAP financial information. | ||||||||||||||||||||

| (2) Ratios based on the fully phased-in basis. | ||||||||||||||||||||

Income from continuing operations of $181 million included net after-tax charges of $9 million from discrete items related to our strategic initiatives. Discrete items included charges related to a goodwill impairment on the business aircraft assets transferred to held for sale and a restructuring charge resulting from operating expense reduction initiatives. In addition to these items, income this quarter included a lower credit provision primarily in the oil and gas portfolio and a mark-to-market benefit on the total return swap (“TRS”).

Tangible book value per share1 increased slightly to $48.45. Estimated Common Equity Tier 1 and Total Capital ratios at June 30, 2016 increased to 13.4% and 14.1%, respectively, as calculated under the fully phased-in Regulatory Capital Rules. Average earning assets2 for the June 30, 2016 quarter were relatively flat at $59.2 billion reflecting growth in Transportation Finance offset by a reduction in Commercial Banking and run-off in the

1 Adjusted ROATCE, Tangible book value and tangible book value per share are non-GAAP measures. See “Non-GAAP Measurements” at the end of this press release and page 25 for reconciliation of non-GAAP to GAAP financial information.

2 Average earning asset components include interest earning cash, investments, securities and indemnification assets. See “Non-GAAP Measurements” at the end of this press release and page 25 for reconciliation of Earning Assets non-GAAP to GAAP financial information.

4

liquidating portfolios. The ROTCE3 of 8.26% increased from the prior quarter reflecting earnings from continuing operations while the increase from the year-ago quarter reflects the lower capital levels primarily due to the acquisition of OneWest Bank.

Income Statement Highlights:

| Net Finance Revenue* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Interest income | $ | 495 | $ | 495 | $ | 284 | $ | (0 | ) | $ | 212 | |||||||||

| Rental income on operating leases | 569 | 575 | 532 | (6 | ) | 38 | ||||||||||||||

| Finance revenue | 1,065 | 1,071 | 816 | (6 | ) | 249 | ||||||||||||||

| Interest expense | (283 | ) | (286 | ) | (265 | ) | 4 | (17 | ) | |||||||||||

| Depreciation on operating lease equipment | (176 | ) | (175 | ) | (158 | ) | (1 | ) | (19 | ) | ||||||||||

| Maintenance and other operating lease expenses | (65 | ) | (56 | ) | (49 | ) | (9 | ) | (16 | ) | ||||||||||

| Net finance revenue | $ | 541 | $ | 553 | $ | 343 | $ | (12 | ) | $ | 198 | |||||||||

| Average earning assets | $ | 59,229 | $ | 59,206 | $ | 41,159 | $ | 23 | $ | 18,070 | ||||||||||

| Net finance margin | 3.65 | % | 3.74 | % | 3.33 | % | -0.08 | % | 0.32 | % | ||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Net finance revenue4 was $541 million in the current quarter, compared to $553 million in the prior quarter and $343 million in the year-ago quarter. Net finance revenue as a percentage of average earning assets (“net finance margin”) decreased from the prior quarter and increased from the year-ago quarter. The decreases in net finance revenue and net finance margin from the prior quarter were driven primarily by higher maintenance and other operating lease costs and lower rental revenue as the prior quarter reflected elevated collections on remarketed aircraft.

Average earning assets were essentially flat compared to the prior quarter reflecting growth in Aerospace, Rail, Real Estate Finance, and Other Consumer Banking, driven by new business volume, offset by assets sales and higher prepayments in Commercial Finance and run-off in the liquidating portfolios.

The increases in net finance revenue, net finance margin and average earning assets from the year-ago quarter reflected the benefits from the OneWest Bank acquisition.

3 Adjusted Return on Tangible Common Equity, which adjusts tangible common equity for the reversal of the valuation allowance and the amortization of intangibles in the numerator and the disallowed deferred tax asset related to regulatory capital in the denominator, is a non-GAAP measure. See “Non-GAAP Measurements” at the end of this press release and page 25 for reconciliation of non-GAAP to GAAP financial information.

4 Net finance revenue, net finance margin and net operating lease revenue are non-GAAP measures. See “Non-GAAP Measurements” at the end of this press release and page 25 for reconciliation of non-GAAP to GAAP financial information.

5

| Other Income* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Fee revenues | $ | 28 | $ | 33 | $ | 25 | $ | (5 | ) | $ | 3 | |||||||||

| Gains on sales of leasing equipment | 28 | 11 | 22 | 17 | 7 | |||||||||||||||

| Factoring commissions | 24 | 26 | 27 | (2 | ) | (3 | ) | |||||||||||||

| Net gain (losses) on derivatives and foreign currency exchange | 10 | 9 | (5 | ) | 1 | 15 | ||||||||||||||

| Gains on loan and portfolio sales | 8 | 0 | 2 | 7 | 6 | |||||||||||||||

| Gains (losses) on investments | 6 | (4 | ) | 4 | 10 | 3 | ||||||||||||||

| Gain on OREO sales | 4 | 2 | - | 2 | 4 | |||||||||||||||

| Impairment on assets held for sale | (17 | ) | (22 | ) | (11 | ) | 5 | (6 | ) | |||||||||||

| Other revenues | 13 | 46 | (0 | ) | (32 | ) | 14 | |||||||||||||

| Total other income | $ | 104 | $ | 101 | $ | 64 | $ | 3 | $ | 41 | ||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Other income of $104 million included gains on assets sales, primarily in Rail, mostly offset by impairment charges on certain rail assets when transferred to held for sale, and a $4 million goodwill impairment charge on the remaining business aircraft assets, also transferred to assets held for sale. The current quarter also included a $9 million mark-to-market benefit on the TRS and a $5 million mark-to-market benefit on the mortgage backed securities. The prior quarter included $10 million of net benefits from international business exits,$18 million benefit from the mark-to-market on the TRS partially offset by a $4 million mark-to-market charge on the mortgage backed securities. The year-ago quarter included a $9 million tax-related charge (that was fully offset with a benefit to the tax provision) and a $6 million negative mark-to-market on the TRS.

| Operating Expenses* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Compensation and benefits | $ | (156 | ) | $ | (172 | ) | $ | (136 | ) | $ | 16 | $ | (20 | ) | ||||||

| Technology | (31 | ) | (30 | ) | (25 | ) | (1 | ) | (6 | ) | ||||||||||

| Professional fees | (40 | ) | (39 | ) | (21 | ) | (1 | ) | (19 | ) | ||||||||||

| Net occupancy expense | (17 | ) | (18 | ) | (9 | ) | 1 | (9 | ) | |||||||||||

| Advertising and marketing | (4 | ) | (5 | ) | (7 | ) | 1 | 2 | ||||||||||||

| Other expenses | (73 | ) | (57 | ) | (37 | ) | (16 | ) | (36 | ) | ||||||||||

| Operating expenses before provision for severance and facilities exiting and intangible asset amortization | (321 | ) | (322 | ) | (233 | ) | - | (88 | ) | |||||||||||

| Provision for severance and facilities exiting activities | (10 | ) | (20 | ) | (1 | ) | 11 | (9 | ) | |||||||||||

| Intangible asset amortization | (6 | ) | (6 | ) | (1 | ) | - | (6 | ) | |||||||||||

| Total operating expenses | $ | (338 | ) | $ | (349 | ) | $ | (235 | ) | $ | 11 | $ | (103 | ) | ||||||

| Net efficiency ratio | 49.8 | % | 49.2 | % | 57.4 | % | -0.6 | % | 7.6 | % | ||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Operating expenses excluding restructuring costs and intangible asset amortization5 were relatively flat to the prior quarter at $321 million. The current quarter reflected elevated costs primarily associated with the Commercial Air separation and higher FDIC insurance, offset by lower employee cost as the prior quarter included the annual benefit restarts. The current quarter also included $8 million of other expenses related to real estate owned (“REO”) that occurred in prior periods. The increase from the prior year reflected the addition of OneWest Bank. The net efficiency ratio5 of 50% reflected lower net finance revenue partially offset by lower operating

5 Operating expenses excluding restructuring costs and intangible asset amortization and Net efficiency ratio is a non-GAAP measure. See “Non-GAAP Measurements” at the end of this press release and page 25 for reconciliation of non-GAAP to GAAP financial information.

6

expenses as compared to the prior quarter and improvement from the prior year reflects the addition of OneWest Bank. Headcount at June 30, 2016 was 4,650, down from 4,740 in the prior quarter, due to strategic initiatives, and up from 3,360 a year-ago, due to the OneWest Bank acquisition. Restructuring costs in this quarter and the prior quarter related to our strategic initiatives to reduce operating expenses, while the amortization of intangibles was primarily due to the OneWest Bank acquisition.

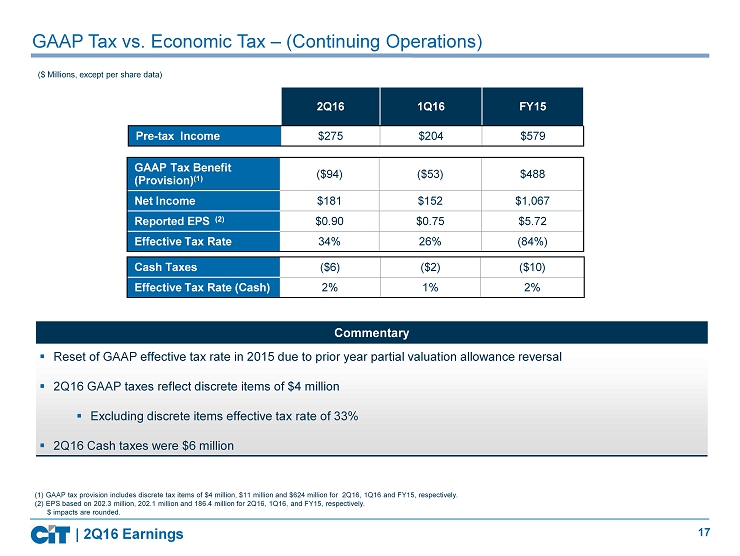

Income Taxes

The provision for income taxes of $94 million for the quarter included $4 million of net discrete tax expense. The prior quarter had an income tax expense of $53 million for the quarter, including $14 million of discrete tax benefits from the resolution of a tax position on an international portfolio that had been previously sold. The current effective tax rate was 34% for the quarter, up from 26% in the prior quarter and 25% in the year-ago quarter. The increase in the effective tax rate is mainly attributable to the impact of discrete items compared to the prior quarter and increased domestic earnings, which shifted the geographic mix of earnings compared to the year-ago quarter. Cash taxes were a net payment of $6 million compared to less than $1 million in the prior quarter and $4 million in the year-ago quarter.

7

Balance Sheet Highlights:

| Earning Assets* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Loans (including assets held for sale) | $ | 32,700 | $ | 33,475 | $ | 20,448 | $ | (775 | ) | $ | 12,252 | |||||||||

| Operating lease equipment, net (including assets held for sale) | 17,025 | 16,811 | 15,398 | 214 | 1,627 | |||||||||||||||

| Financing and Leasing Assets | 49,725 | 50,286 | 35,846 | (561 | ) | 13,879 | ||||||||||||||

| Interest bearing cash | 7,083 | 7,135 | 4,225 | (52 | ) | 2,858 | ||||||||||||||

| Investment securities | 3,229 | 2,897 | 1,693 | 332 | 1,536 | |||||||||||||||

| Indemnification asset | 376 | 389 | - | (14 | ) | 376 | ||||||||||||||

| Securities purchased under agreements to resell | - | - | 750 | - | (750 | ) | ||||||||||||||

| Credit balances of factoring clients | (1,215 | ) | (1,361 | ) | (1,373 | ) | 146 | 158 | ||||||||||||

| Total Earning Assets | $ | 59,197 | $ | 59,346 | $ | 41,140 | $ | (149 | ) | $ | 18,057 | |||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Earning assets at June 30, 2016 declined slightly from the prior quarter, as collections and sales of loans offset $2.8 billion in new originations. The increase from the year-ago quarter principally reflects the assets acquired from OneWest Bank.

Interest bearing cash and investment securities were $10.3 billion at June 30, 2016, and consisted of $7.1 billion of cash ($0.6 billion of which was restricted cash), and $3.2 billion of investment securities, primarily debt securities, Federal Home Loan Bank (“FHLB”) stock and equities. The increase in investment securities from the prior quarter reflects the initiative to deploy cash into liquid investments. In addition, there was $1.0 billion of non-interest bearing cash and other restricted balances.

Of the total cash and investment securities $1.7 billion of the interest bearing cash and investment securities was at the financial holding company, $8.2 billion was at CIT Bank and the remaining $1.4 billion includes amounts at the operating subsidiaries and restricted balances. In addition, there was $1.0 billion of non-interest bearing cash primarily at the operating subsidiaries and other restricted balances.

| Deposits and Borrowings* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Total Deposits | $ | 32,879 | $ | 32,893 | $ | 17,268 | $ | (14 | ) | $ | 15,611 | |||||||||

| Unsecured borrowings | $ | 10,591 | $ | 10,587 | $ | 10,684 | $ | 4 | $ | (93 | ) | |||||||||

| Secured borrowings | 6,919 | 7,425 | 5,645 | (506 | ) | 1,274 | ||||||||||||||

| Total Borrowings | $ | 17,510 | $ | 18,013 | $ | 16,330 | $ | (502 | ) | $ | 1,181 | |||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Deposits were essentially flat from the prior quarter. The decline in secured borrowings related to the amortization, redemption and maturities of structured financings. The increase in secured borrowings from June 30, 2015 primarily reflected FHLB borrowings related to the acquisition of OneWest Bank in the third quarter of 2015, offset by a reduction in other secured borrowings. At June 30, 2016, deposits represented approximately 65% of CIT’s funding, with unsecured and secured borrowings comprising 21% and 14% of the funding mix, respectively. The weighted average coupon rate on outstanding deposits and borrowings was 2.20% at June 30, 2016, down from 2.22% at March 31, 2016 and 3.04% at June 30, 2015.

8

| Capital* | Change from: | |||||||||||||||||||

| ($ in millions, except per share data) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Common Stockholders' Equity | $ | 11,124 | $ | 11,126 | $ | 8,807 | $ | (2 | ) | $ | 2,317 | |||||||||

| Tangible Common Equity | $ | 9,786 | $ | 9,760 | $ | 8,220 | $ | 25 | $ | 1,566 | ||||||||||

| Total risk-based capital(1) | $ | 9,539 | $ | 9,524 | $ | 8,409 | $ | 15 | $ | 1,130 | ||||||||||

| Risk-weighted assets(1) | $ | 67,733 | $ | 69,192 | $ | 55,665 | $ | (1,459 | ) | $ | 12,068 | |||||||||

| Book value per share (BVPS) | $ | 55.07 | $ | 55.16 | $ | 50.91 | $ | (0.09 | ) | $ | 4.16 | |||||||||

| Tangible book value per share (TBVPS) | $ | 48.45 | $ | 48.39 | $ | 47.51 | $ | 0.06 | $ | 0.93 | ||||||||||

| CET 1 Ratio(1) | 13.4 | % | 13.1 | % | 14.4 | % | 0.3 | % | -1.0 | % | ||||||||||

| Total Capital Ratio(1) | 14.1 | % | 13.8 | % | 15.1 | % | 0.3 | % | -1.0 | % | ||||||||||

| Tier 1 Leverage Ratio(1) | 13.9 | % | 13.8 | % | 17.7 | % | 0.1 | % | -3.8 | % | ||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

| (1) Balances and ratios based on the fully phased-in basis. | ||||||||||||||||||||

Common stockholders’ equity and tangible common equity were essentially unchanged from the prior quarter. The acquisition of OneWest Bank was the main contributor to the increase from June 30, 2015, primarily due to the issuance of common shares and the reversal of the valuation allowance on our Federal deferred tax asset in the third quarter of 2015. Tangible common equity also increased from June 30, 2015, but by a lower amount due to the increase in goodwill and intangibles resulting from the acquisition of OneWest Bank. While regulatory capital also reflected the trends noted above, the increase was less than the common equity increase since the majority of the deferred tax asset balance is disallowed for regulatory capital purposes. All regulatory capital ratios increased from the prior quarter reflecting a reduction in risk weighted assets. The decline in capital ratios from the prior year reflected the acquisition of OneWest Bank as growth in regulatory capital was more than offset by the increase in the risk-weighted assets. The ratios presented are estimated Common Equity Tier 1 and Total Capital ratios under the fully phased-in Regulatory Capital Rules.

Book value per share and tangible book value per share were relatively flat. Both amounts also increased from June 30, 2015, as the increase in equity outpaced the increase in shares outstanding.

In July 2016, the Board approved a $0.15 cash dividend payable on August 26, 2016 to common shareholders of record as of August 12, 2016.

9

Asset Quality

| Asset Quality* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Net charge-offs (NCO) | $ | 41 | $ | 51 | $ | 24 | $ | (10 | ) | $ | 18 | |||||||||

| NCO % of AFR | 0.53 | % | 0.65 | % | 0.48 | % | -0.12 | % | 0.05 | % | ||||||||||

| Non-accrual | $ | 283 | $ | 295 | $ | 198 | $ | (12 | ) | $ | 85 | |||||||||

| OREO | $ | 90 | $ | 100 | $ | - | $ | (10 | ) | $ | 90 | |||||||||

| Provision for credit losses | $ | 28 | $ | 99 | $ | 18 | $ | (71 | ) | $ | 10 | |||||||||

| Total Portfolio Allowance as a % of Finance Receivables (FR) | 1.31 | % | 1.29 | % | 1.14 | % | 0.02 | % | 0.17 | % | ||||||||||

| Allowance for loan losses plus principal loss discount as % of FR (before principal loss discount) / Commercial | 1.83 | % | 1.87 | % | 1.79 | % | -0.04 | % | 0.04 | % | ||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

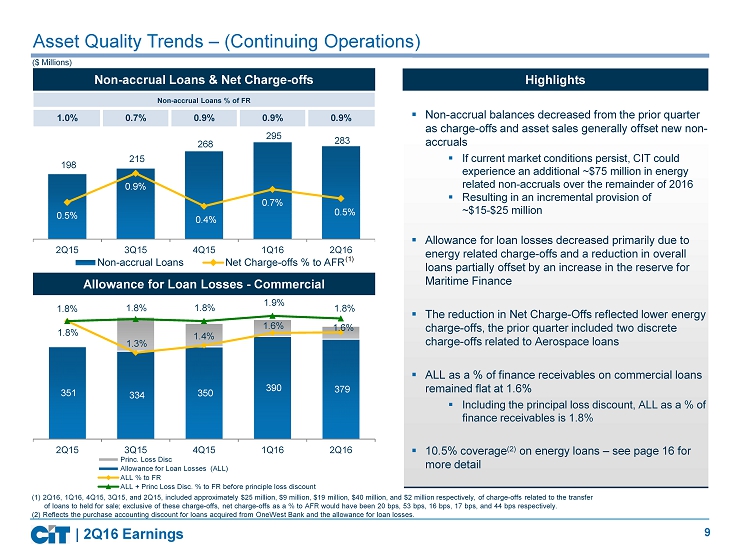

Excluding the impact relating to assets transferred to held for sale in all periods, net charge-offs were $16 million (0.21% of average finance receivables), compared to $42 million (0.53%) in the prior quarter and $22 million (0.45%) in the year-ago quarter. The current quarter net charge-offs includes $17 million in the energy (oil and gas) portfolio, of which $10 million related to loans which were sold or transferred to assets held for sale. Prior quarter net charge-offs included $15 million in the energy (oil and gas) portfolio .

Non-accrual loans of $283 million (0.93% of finance receivables) decreased from the prior quarter as charge-offs and asset sales generally offset a modest level of new non-accruals. The increase compared to the year-ago quarter is primarily due to increases in the energy portfolio. The provision for credit losses decreased from the prior quarter elevated levels, as portfolio quality was relatively unchanged and charge-offs, excluding the impact relating to assets transferred to held for sale, were lower.

The allowance for loan losses was $399 million (1.31% of finance receivables, 1.55% excluding loans subject to loss sharing agreements with the FDIC) at June 30, 2016, compared to $405 million (1.29% of finance receivables, 1.52% excluding loans subject to loss sharing agreements with the FDIC) at March 31, 2016 and $351 million (1.79% of finance receivables) at June 30, 2015. The slight decrease in allowance for loan losses from the prior quarter primarily reflected a reduction due to energy related charge-offs and lower loan balances, partially offset by approximately $10 million increase in the reserve for maritime finance loans, while the increase from the year-ago quarter was concentrated in the energy and maritime portfolios. Including the impact of the principal loss discount on credit impaired loans, which is essentially a reserve for credit losses on the discounted loans, the commercial loan allowance to finance receivables was 1.83% compared to 1.87% at March 31, 2016. The consumer loans ratio was 7.20% at June 30, 2016 and 7.86% at March 31, 2016, respectively, as most of the consumer loans purchased were credit impaired and are partially covered by loss sharing agreements with the FDIC. The decrease from the prior quarter was driven by the shift in asset mix as new originations offset the run-off of the purchased credit impaired portfolio.

CIT’s loans to the oil and gas industry totaled $0.8 billion or 2.7% of total loans at June 30, 2016, of which 47% were criticized. The decline of $0.1 billion in oil and gas loans was driven by loan sales and pay downs. The portfolio has loss coverage of about 10.5% of the principal balance, reflecting the purchase accounting discount for loans acquired from OneWest Bank and the allowance for loan losses. If market conditions remain the same, the portfolio will likely experience additional downward credit migration.

10

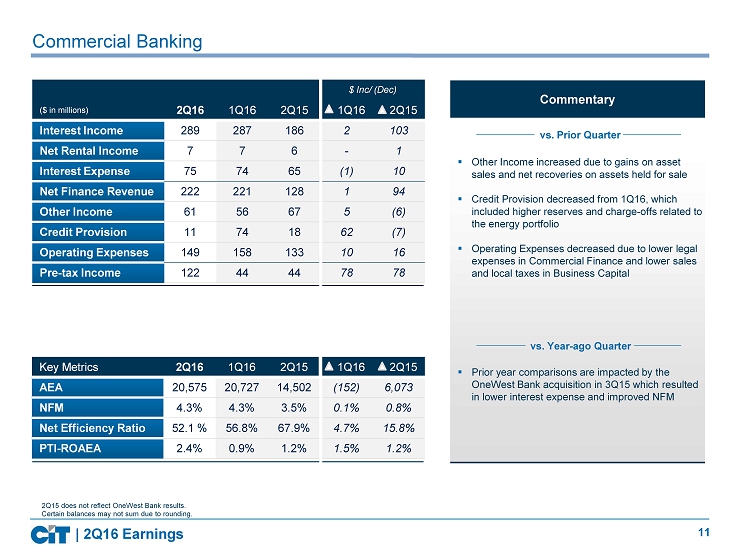

Commercial Banking

| Earnings Summary* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Interest income | $ | 289 | $ | 287 | $ | 186 | $ | 2 | $ | 103 | ||||||||||

| Rental income on operating leases | 29 | 27 | 24 | 2 | 5 | |||||||||||||||

| Interest expense | (75 | ) | (74 | ) | (65 | ) | (1 | ) | (10 | ) | ||||||||||

| Depreciation on operating lease equipment | (22 | ) | (20 | ) | (18 | ) | (2 | ) | (4 | ) | ||||||||||

| Net finance revenue | 222 | 221 | 128 | 1 | 94 | |||||||||||||||

| Other income | 61 | 56 | 67 | 5 | (6 | ) | ||||||||||||||

| Provision for credit losses | (11 | ) | (74 | ) | (18 | ) | 62 | 7 | ||||||||||||

| Operating expenses | (149 | ) | (158 | ) | (133 | ) | 10 | (16 | ) | |||||||||||

| Income before income taxes | $ | 122 | $ | 44 | $ | 44 | $ | 78 | $ | 78 | ||||||||||

| Select Average Balances | ||||||||||||||||||||

| Average finance receivables | $ | 21,041 | $ | 21,131 | $ | 15,041 | $ | (90 | ) | $ | 6,000 | |||||||||

| Average earning assets | $ | 20,575 | $ | 20,727 | $ | 14,502 | $ | (152 | ) | $ | 6,073 | |||||||||

| Statistical Data | ||||||||||||||||||||

| Pre-tax ROAEA | 2.38 | % | 0.85 | % | 1.22 | % | 1.53 | % | 1.16 | % | ||||||||||

| Net finance margin | 4.31 | % | 4.26 | % | 3.52 | % | 0.05 | % | 0.79 | % | ||||||||||

| New business volume | $ | 2,048 | $ | 1,581 | $ | 1,523 | $ | 467 | $ | 525 | ||||||||||

| Net efficiency ratio | 52.1 | % | 56.8 | % | 67.9 | % | 4.7 | % | 15.8 | % | ||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Commercial Banking pre-tax earnings increased from the prior quarter due to lower credit costs and operating expenses, while the increase from the year-ago quarter also reflects the addition from OneWest Bank.

Financing and leasing assets, which comprise the majority of earning assets, were $21.5 billion at June 30, 2016, down slightly from $22.0 billion at March 31, 2016, mostly driven by the decrease in financing and leasing assets in Commercial Finance, and up from $15.4 billion a year-ago, reflecting the acquisition of OneWest Bank. New lending and leasing volume exceeded $2 billion and was up from the prior and year-ago quarters, driven by strong origination activity in Real Estate Finance, while factored volume was down from both the prior and year-ago quarters.

Net finance revenue was essentially flat to the prior quarter, and included interest recoveries of $6 million on a loan previously charged off. The increase from the year-ago quarter reflected higher earning assets and purchase accounting accretion on loans acquired from OneWest Bank. Net finance margin of 4.31% was up slightly from the prior and year-ago quarters from interest recoveries on loans previously charged off. In addition, the increase from the prior year was also due to purchase accounting accretion on acquired loans.

Other income increased from the prior quarter primarily due to gains on asset sales and recoveries of previous impairments on assets held for sale, partially offset by lower capital market fees and factoring commissions. The decline from the year-ago quarter reflected lower gains on asset sales and lower factoring commissions.

Operating expenses decreased from the prior quarter, as the prior quarter included higher legal expenses in Commercial Finance and higher sales and local taxes in Business Capital. The increase from the year-ago quarter reflected the acquisition of OneWest Bank.

11

Net charge-offs were $35 million (0.66% of average finance receivables), compared to $32 million (0.60%) in the prior quarter and $25 million (0.67%) in the year-ago quarter. Excluding assets transferred to held for sale in all periods, net charge-offs were $16 million in the current quarter, compared to $30 million in the prior quarter and $24 million in the year-ago quarter. The decrease in the current quarter compared to the prior quarter primarily related to energy loans. Non-accrual loans were $208 million (1.00% of finance receivables), compared to $215 million (1.00%) at March 31, 2016, and $98 million (0.65%) a year-ago. The increase in balances from the year-ago quarter was primarily related to loans in the energy sector. The provision for credit losses decreased from the prior quarter, which included higher reserves and charge-offs related to the energy portfolio.

Transportation Finance

| Earnings Summary* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Interest income | $ | 50 | $ | 53 | $ | 44 | $ | (3 | ) | $ | 6 | |||||||||

| Rental income on operating leases | 537 | 545 | 498 | (8 | ) | 39 | ||||||||||||||

| Interest expense | (147 | ) | (148 | ) | (149 | ) | 2 | 2 | ||||||||||||

| Depreciation on operating lease equipment | (155 | ) | (155 | ) | (137 | ) | 0 | (18 | ) | |||||||||||

| Maintenance and other operating lease expenses | (65 | ) | (56 | ) | (49 | ) | (9 | ) | (16 | ) | ||||||||||

| Net finance revenue | 220 | 238 | 208 | (17 | ) | 13 | ||||||||||||||

| Other income | 12 | 19 | 14 | (7 | ) | (2 | ) | |||||||||||||

| Provision for credit losses | (16 | ) | (23 | ) | (1 | ) | 7 | (15 | ) | |||||||||||

| Operating expenses | (62 | ) | (61 | ) | (64 | ) | (2 | ) | 2 | |||||||||||

| Income before income taxes | $ | 154 | $ | 173 | $ | 157 | $ | (19 | ) | $ | (2 | ) | ||||||||

| Select Average Balances | ||||||||||||||||||||

| Average finance receivables | $ | 2,726 | $ | 3,333 | $ | 3,048 | $ | (607 | ) | $ | (322 | ) | ||||||||

| Average operating leases | $ | 16,477 | $ | 16,364 | $ | 14,720 | $ | 113 | $ | 1,757 | ||||||||||

| Average earning assets | $ | 20,946 | $ | 20,620 | $ | 18,957 | $ | 326 | $ | 1,989 | ||||||||||

| Statistical Data | ||||||||||||||||||||

| Pre-tax ROAEA | 2.94 | % | 3.36 | % | 3.30 | % | -0.41 | % | -0.36 | % | ||||||||||

| Net finance margin | 4.21 | % | 4.61 | % | 4.38 | % | -0.40 | % | -0.18 | % | ||||||||||

| New business volume | $ | 461 | $ | 246 | $ | 744 | $ | 215 | $ | (283 | ) | |||||||||

| Net efficiency ratio | 26.1 | % | 23.7 | % | 28.8 | % | -2.4 | % | 2.7 | % | ||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Transportation Finance pre-tax earnings decreased from the prior quarter, as lower net finance revenue and other income offset lower credit costs, and were essentially flat with the year-ago quarter, as higher net finance revenue on increased average earning assets was offset by higher credit costs, largely in Maritime. The current quarter results also reflected charges related to the transfer of the remaining Business Air portfolio to held for sale and increased operating expenses related to the planned Commercial Air separation.

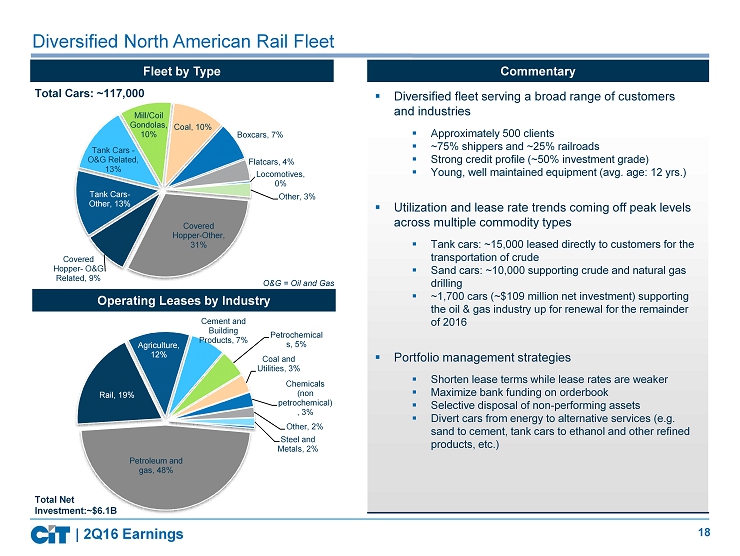

Financing and leasing assets totaled $20.0 billion at June 30, 2016, compared to $19.9 billion at March 31, 2016 and $18.3 billion at June 30, 2015. Assets grew sequentially in Aerospace and Rail and grew in all three divisions (Aerospace, Rail and Maritime) from a year ago. Assets held for sale of $0.8 billion principally included the Business Air portfolio, as the remaining Business Air assets were transferred to held for sale during the quarter. New business volume for the quarter totaled $0.5 billion, up from the prior quarter reflecting additional aircraft and railcar deliveries.

12

Net finance revenue was down from the prior quarter, as the impact of higher maintenance and other operating lease expenses and lower rentals offset lower funding costs. Net finance revenue increased from the year-ago quarter primarily reflecting higher average operating lease assets partially offset by higher maintenance and other operating lease expenses. Net finance margin was down from the prior and year-ago quarters reflecting the net finance revenue trends described above. Gross yields in Aerospace and Rail decreased from the prior quarter to 10.9% and 13.2%, respectively, reflecting lower rental rates and higher cash balances in Aerospace.

Other income declined from the prior and year-ago quarters largely reflecting higher gains on asset sales in rail, which were offset by impairments, including a $4 million goodwill impairment charge related to the business aircraft assets transferred to held for sale.

Operating expenses were relatively flat with the prior quarter, as higher costs related to the Commercial Air separation offset lower employee costs. The current and prior quarter included $9 million and $4 million of costs related to the Commercial Air separation initiative, respectively.

Net charge-offs, excluding assets transferred to held for sale, were negligible for the current and year-ago quarters, compared to net charge-offs of $12 million (1.49% of average finance receivables) related to the Aerospace loan portfolio in the prior quarter. Non-accrual loans of $18 million (0.70% of finance receivables) decreased from $22 million (0.78%) at March 31, 2016 and increased from $5 million (0.15%) a year-ago, and principally consisted of business aircraft loans in each of the periods. The provision for credit losses decreased from the prior quarter, but continues to reflect reserve increases in Maritime and elevated charges in the Business Air portfolio related to the assets transferred to held for sale.

Utilization trends were relatively unchanged compared to the prior quarter. All aircraft were on lease or under a commitment at quarter-end resulting in 100% utilization, while Rail utilization remained at approximately 94%. All of our aircraft scheduled for delivery in the next 12 months and approximately 41% of the total railcar order-book have lease commitments.

13

Consumer and Community Banking

| Earnings Summary* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Interest income | $ | 105 | $ | 103 | $ | - | $ | 2 | $ | 105 | ||||||||||

| Interest expense | (6 | ) | (9 | ) | - | 3 | (6 | ) | ||||||||||||

| Net finance revenue | 100 | 94 | - | 5 | 100 | |||||||||||||||

| Other income | 12 | 8 | - | 4 | 12 | |||||||||||||||

| Provision for credit losses | (1 | ) | (3 | ) | - | 2 | (1 | ) | ||||||||||||

| Operating expenses | (93 | ) | (82 | ) | - | (11 | ) | (93 | ) | |||||||||||

| Income before income taxes | $ | 17 | $ | 17 | $ | - | $ | (0 | ) | $ | 17 | |||||||||

| Select Average Balances | ||||||||||||||||||||

| Average finance receivables | $ | 7,156 | $ | 7,160 | $ | - | $ | (5 | ) | $ | 7,156 | |||||||||

| Average earning assets | $ | 7,729 | $ | 7,758 | $ | - | $ | (29 | ) | $ | 7,729 | |||||||||

| Statistical Data | ||||||||||||||||||||

| Pre-tax ROAEA | 0.87 | % | 0.88 | % | - | -0.01 | % | 0.87 | % | |||||||||||

| Net finance margin | 5.15 | % | 4.86 | % | - | 0.29 | % | 5.15 | % | |||||||||||

| New business volume | $ | 261 | $ | 215 | $ | - | $ | 47 | $ | 261 | ||||||||||

| Net efficiency ratio | 79.6 | % | 75.8 | % | - | 3.8 | % | 79.6 | % | |||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Consumer and Community Banking pre-tax earnings remained consistent with the prior quarter. The quarter benefited from higher net finance revenue, higher other income due to gains on REO, and lower credit provision, which were offset by higher operating expenses, primarily from REO expenses ($8 million of which related to prior periods).

Financing and leasing assets totaled $7.2 billion at June 30, 2016, down slightly from March 31, 2016, as the run-off of the Legacy Consumer Mortgage (“LCM”) portfolios offset new volume. The LCM portfolios make up $5.2 billion of the current quarter balance with a significant portion covered by loss sharing agreements with the FDIC. The benefit of these agreements is recorded within the indemnification asset.

Non-accrual loans were $12 million (0.16% of finance receivables) at June 30, 2016, up from $7 million (0.10% of finance receivables) at March 31, 2016. The provision for credit losses decreased slightly from the prior quarter.

14

Non-Strategic Portfolios (NSP)

| Earnings Summary* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Interest income | $ | 23 | $ | 25 | $ | 49 | $ | (2 | ) | $ | (26 | ) | ||||||||

| Rental income on operating leases | 4 | 4 | 10 | 0 | (6 | ) | ||||||||||||||

| Interest expense | (14 | ) | (15 | ) | (34 | ) | 1 | 20 | ||||||||||||

| Depreciation on operating lease equipment | - | - | (4 | ) | - | 4 | ||||||||||||||

| Net finance revenue | 14 | 14 | 21 | (1 | ) | (8 | ) | |||||||||||||

| Other income | 7 | 15 | (1 | ) | (8 | ) | 8 | |||||||||||||

| Provision for credit losses | - | - | 1 | - | (1 | ) | ||||||||||||||

| Operating expenses | (12 | ) | (12 | ) | (35 | ) | 0 | 23 | ||||||||||||

| Income (loss) before income taxes | $ | 8 | $ | 17 | $ | (14 | ) | $ | (9 | ) | $ | 22 | ||||||||

| Select Average Balances | ||||||||||||||||||||

| Average earning assets | $ | 1,385 | $ | 1,517 | $ | 2,558 | $ | (132 | ) | $ | (1,174 | ) | ||||||||

| Statistical Data | ||||||||||||||||||||

| Pre-tax ROAEA | 2.34 | % | 4.38 | % | -2.16 | % | -2.04 | % | 4.50 | % | ||||||||||

| Net finance margin | 3.90 | % | 3.77 | % | 3.30 | % | 0.13 | % | 0.60 | % | ||||||||||

| New business volume | $ | 61 | $ | 44 | $ | 216 | $ | 17 | $ | (154 | ) | |||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

NSP pre-tax earnings for the quarter reflected operations for the remaining businesses in Canada and China. The prior quarter reflected a gain of $24 million from the sale of the U.K. business, partially offset by an $11 million impairment charge on assets held for sale. The year-ago pre-tax loss was driven by the higher level of operating expenses, reflective of the remaining businesses at that time. Financing and leasing assets at June 30, 2016 totaled $1.1 billion, down slightly from $1.2 billion at March 31, 2016 and from $2.1 billion at June 30, 2015. Our remaining NSP businesses are classified as held for sale. During this quarter we reached a definitive agreement to sell the Canadian Equipment and Corporate Finance business (approximately $750 million in financing and leasing assets), subject to regulatory approvals, and expect the transaction to close in the fourth quarter of this year.

15

Corporate & Other

| Earnings Summary* | Change from: | |||||||||||||||||||

| ($ in millions) | 2Q16 | 1Q16 | 2Q15 | Prior Quarter | Prior Year | |||||||||||||||

| Interest income | $ | 28 | $ | 27 | $ | 5 | $ | 0 | $ | 23 | ||||||||||

| Interest expense | (42 | ) | (41 | ) | (18 | ) | (0 | ) | (24 | ) | ||||||||||

| Net finance revenue | (14 | ) | (14 | ) | (13 | ) | (0 | ) | (1 | ) | ||||||||||

| Other income | 13 | 4 | (17 | ) | 9 | 30 | ||||||||||||||

| Operating expenses | (25 | ) | (37 | ) | (4 | ) | 11 | (21 | ) | |||||||||||

| Loss before income taxes | $ | (26 | ) | $ | (47 | ) | $ | (34 | ) | $ | 20 | $ | 8 | |||||||

| Select Average Balances | ||||||||||||||||||||

| Average earning assets | $ | 8,595 | $ | 8,585 | $ | 5,142 | $ | 10 | $ | 3,453 | ||||||||||

| Statistical Data | ||||||||||||||||||||

| Pre-tax ROAEA | -1.21 | % | -2.17 | % | -2.62 | % | 0.95 | % | 1.41 | % | ||||||||||

| Net finance margin | -0.66 | % | -0.65 | % | -1.02 | % | -0.01 | % | 0.36 | % | ||||||||||

| * Certain balances may not sum due to rounding. | ||||||||||||||||||||

Certain items are not allocated to operating segments and are included in Corporate and Other, including interest expense, primarily related to corporate liquidity costs, mark-to-market on certain derivatives, restructuring charges, certain legal costs and other operating expenses. Interest income increased slightly from the prior quarter and is up from a year-ago quarter primarily related to income generated from the investment portfolio. Other income included a $9 million mark-to-market benefit on the TRS and a $5 million mark-to-market benefit on mortgage backed securities in the current quarter, compared to an $18 million benefit on the TRS offset by a $4 million mark-to-market charge on mortgage backed securities in the prior quarter. The prior year quarter included a $9 million tax-related charge, (that was fully offset with a benefit to the tax provision) and a negative mark-to-market adjustment on the TRS of $6 million. Operating expenses for the quarter reflected restructuring charges of $10 million, compared to $20 million in the prior quarter, reflecting our previously announced organizational changes, and $1 million in the year-ago quarter.

Discontinued Operations

Income from discontinued operations, net of taxes, was a loss of $167 million in the current quarter compared to a loss of $5 million in the prior quarter. In the current period, discontinued operations predominantly relates to third-party reverse mortgage servicing activity, known as Financial Freedom, which the Company acquired in the OneWest Bank acquisition.

As a result of the ongoing review to remediate the material weakness, and taking into consideration the investigation being conducted by the OIG, the Company recorded additional reserves, due to a change in estimate, of $230 million during the current quarter.

16

Conference Call and Webcast

Chairwoman and Chief Executive Officer Ellen Alemany and Chief Financial Officer Carol Hayles will discuss these results on a conference call and audio webcast today, July 28, at 8:00 a.m. (EDT). Interested parties may access the conference call live by dialing 888-317-6003 for U.S., 866-284-3684 for Canadian callers or 412-317-6061 for international callers and reference access code “0603321” or access the audio webcast at cit.com/investor. An audio replay of the call will be available until 11:59 p.m. (EDT) on August 28, 2016, by dialing 877-344-7529 for U.S. callers, 855-669-9658 for Canadian callers or 412-317-0088 for international callers with the access code “10089399”, or at cit.com/investor.

About CIT

Founded in 1908, CIT (NYSE: CIT) is a financial holding company with more than $65 billion in assets. Its principal bank subsidiary, CIT Bank, N.A., (Member FDIC, Equal Housing Lender) has more than $30 billion of deposits and more than $40 billion of assets. It provides financing, leasing and advisory services principally to middle market companies across a wide variety of industries primarily in North America, and equipment financing and leasing solutions to the transportation sector. It also offers products and services to consumers through its Internet bank franchise and a network of retail branches in Southern California, operating as OneWest Bank, a division of CIT Bank, N.A. cit.com

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of applicable federal securities laws that are based upon our current expectations and assumptions concerning future events, which are subject to a number of risks and uncertainties that could cause actual results to differ materially from those anticipated. The words “expect,” “anticipate,” “estimate,” “forecast,” “initiative,” “objective,” “plan,” “goal,” “project,” “outlook,” “priorities,” “target,” “intend,” “evaluate,” “pursue,” “commence,” “seek,” “may,” “would,” “could,” “should,” “believe,” “potential,” “continue,” or the negative of any of those words or similar expressions is intended to identify forward-looking statements. All statements contained in this press release, other than statements of historical fact, including without limitation, statements about our plans, strategies, prospects and expectations regarding future events and our financial performance, are forward-looking statements that involve certain risks and uncertainties. While these statements represent our current judgment on what the future may hold, and we believe these judgments are reasonable, these statements are not guarantees of any events or financial results, and our actual results may differ materially. Important factors that could cause our actual results to be materially different from our expectations include, among others, the risk that CIT is unsuccessful in implementing its strategy and business plan, the risk that CIT is unable to react to and address key business and regulatory issues, the risk that CIT is unable to achieve the projected revenue growth from its new business initiatives or the projected expense reductions from efficiency improvements, and the risk that CIT becomes subject to liquidity constraints and higher funding costs. We describe these and other risks that could affect our results in Item 1A, “Risk Factors,” of our latest Annual Report on Form 10-K for the year ended December 31, 2015, which was filed with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on the forward-looking statements contained in this press release. These forward-looking statements speak only as of the date on which the statements were made. CIT undertakes no obligation to update publicly or otherwise revise any forward-looking statements, except where expressly required by law.

Non-GAAP Measurements

Net finance revenue, net operating lease revenue and average earning assets are non-GAAP measurements used by management to gauge portfolio performance. Operating expenses excluding restructuring costs and intangible amortization is a non-GAAP measurement used by management to compare period over period expenses. Net efficiency ratio measures operating expenses (net of restructuring costs and intangible amortization) to our level of total net revenues. Total assets from continuing operations is a non-GAAP measurement used by management to analyze the total asset change on a more consistent basis. Tangible book value and tangible book value per share are non-GAAP metrics used to analyze banks.

###

| CIT MEDIA RELATIONS: | CIT INVESTOR RELATIONS: |

| Matt Klein | Barbara Callahan |

| Director | Senior Vice President |

|

(973) 597-2020

|

(973) 740-5058 |

###

17

CIT GROUP INC. AND SUBSIDIARIES

Unaudited Consolidated Statements of Income

(dollars in millions, except per share data)

| Quarters Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016* | 2016 | 2015 | 2016* | 2015 | ||||||||||||||||

| Interest income | ||||||||||||||||||||

| Interest and fees on loans | $ | 463.6 | $ | 464.5 | $ | 274.8 | $ | 928.1 | $ | 547.2 | ||||||||||

| Other Interest and dividends | 31.7 | 30.9 | 9.0 | 62.6 | 17.6 | |||||||||||||||

| Total interest income | 495.3 | 495.4 | 283.8 | 990.7 | 564.8 | |||||||||||||||

| Interest expense | ||||||||||||||||||||

| Interest on borrowings | (183.1 | ) | (186.9 | ) | (193.0 | ) | (370.0 | ) | (395.3 | ) | ||||||||||

| Interest on deposits | (99.4 | ) | (99.5 | ) | (72.2 | ) | (198.9 | ) | (141.2 | ) | ||||||||||

| Total interest expense | (282.5 | ) | (286.4 | ) | (265.2 | ) | (568.9 | ) | (536.5 | ) | ||||||||||

| Net interest revenue | 212.8 | 209.0 | 18.6 | 421.8 | 28.3 | |||||||||||||||

| Provision for credit losses | (28.1 | ) | (99.3 | ) | (18.4 | ) | (127.4 | ) | (53.0 | ) | ||||||||||

| Net interest revenue, after credit provision | 184.7 | 109.7 | 0.2 | 294.4 | (24.7 | ) | ||||||||||||||

| Non-interest income | ||||||||||||||||||||

| Rental income on operating leases | 569.3 | 575.4 | 531.7 | 1,144.7 | 1,062.3 | |||||||||||||||

| Other income | 104.3 | 100.9 | 63.5 | 205.2 | 149.9 | |||||||||||||||

| Total non-interest income | 673.6 | 676.3 | 595.2 | 1,349.9 | 1,212.2 | |||||||||||||||

| Non-interest expenses | ||||||||||||||||||||

| Depreciation on operating lease equipment | (176.4 | ) | (175.3 | ) | (157.8 | ) | (351.7 | ) | (314.6 | ) | ||||||||||

| Maintenance and other operating lease expenses | (64.9 | ) | (56.2 | ) | (49.4 | ) | (121.1 | ) | (95.5 | ) | ||||||||||

| Operating expenses | (337.5 | ) | (348.5 | ) | (235.0 | ) | (686.0 | ) | (476.6 | ) | ||||||||||

| Loss on debt extinguishment and deposit redemption | (4.1 | ) | (1.6 | ) | (0.1 | ) | (5.7 | ) | (0.1 | ) | ||||||||||

| Total other expenses | (582.9 | ) | (581.6 | ) | (442.3 | ) | (1,164.5 | ) | (886.8 | ) | ||||||||||

| Income from continuing operations before provision for income taxes | 275.4 | 204.4 | 153.1 | 479.8 | 300.7 | |||||||||||||||

| Provision for income taxes | (94.3 | ) | (52.7 | ) | (37.8 | ) | (147.0 | ) | (81.8 | ) | ||||||||||

| Income from continuing operations, before attribution of noncontrolling interests | 181.1 | 151.7 | 115.3 | 332.8 | 218.9 | |||||||||||||||

| Net loss attributable to noncontrolling interests, after tax | - | - | - | - | 0.1 | |||||||||||||||

| Income from continuing operations | 181.1 | 151.7 | 115.3 | 332.8 | 219.0 | |||||||||||||||

| Discontinued operation | ||||||||||||||||||||

| Loss from discontinued operation | (236.3 | ) | (7.4 | ) | - | (243.7 | ) | - | ||||||||||||

| Benefit for income taxes | 69.3 | 2.6 | - | 71.9 | - | |||||||||||||||

| Loss from discontinued operation, net of taxes | (167.0 | ) | (4.8 | ) | - | (171.8 | ) | - | ||||||||||||

| Net income | $ | 14.1 | $ | 146.9 | $ | 115.3 | $ | 161.0 | $ | 219.0 | ||||||||||

| Basic income per common share | ||||||||||||||||||||

| Income from continuing operations | $ | 0.90 | $ | 0.75 | $ | 0.66 | $ | 1.65 | $ | 1.25 | ||||||||||

| Loss from discontinued operation, net of taxes | (0.83 | ) | (0.02 | ) | - | (0.85 | ) | - | ||||||||||||

| Basic income per common share | $ | 0.07 | $ | 0.73 | $ | 0.66 | $ | 0.80 | $ | 1.25 | ||||||||||

| Average number of common shares - basic (thousands) | 201,893 | 201,394 | 173,785 | 201,647 | 175,019 | |||||||||||||||

| Diluted income per common share | ||||||||||||||||||||

| Income from continuing operations | $ | 0.90 | $ | 0.75 | $ | 0.66 | $ | 1.65 | $ | 1.24 | ||||||||||

| Loss from discontinued operation, net of taxes | (0.83 | ) | (0.02 | ) | - | (0.85 | ) | - | ||||||||||||

| Diluted income per common share | $ | 0.07 | $ | 0.73 | $ | 0.66 | $ | 0.80 | $ | 1.24 | ||||||||||

| Average number of common shares - diluted (thousands) | 202,275 | 202,136 | 174,876 | 202,208 | 175,971 | |||||||||||||||

| * Preliminary | ||||||||||||||||||||

18

CIT GROUP INC. AND SUBSIDIARIES

Unaudited Consolidated Balance Sheets

(dollars in millions, except per share data)

| June 30, | March 31, | December 31, | June 30, | |||||||||||||

| 2016* | 2016 | 2015 | 2015 | |||||||||||||

| Assets | ||||||||||||||||

| Total cash and deposits | $ | 8,103.9 | $ | 8,141.8 | $ | 8,301.5 | $ | 5,465.3 | ||||||||

| Securities purchased under agreements to resell | - | - | - | 750.0 | ||||||||||||

| Investment securities | 3,229.1 | 2,896.8 | 2,953.8 | 1,692.9 | ||||||||||||

| Assets held for sale | 2,403.3 | 2,211.2 | 2,092.4 | 1,086.8 | ||||||||||||

| Loans | 30,456.8 | 31,408.6 | 31,671.7 | 19,649.3 | ||||||||||||

| Allowance for loan losses | (399.4 | ) | (404.6 | ) | (360.2 | ) | (350.9 | ) | ||||||||

| Loans, net of allowance for loan losses | 30,057.4 | 31,004.0 | 31,311.5 | 19,298.4 | ||||||||||||

| Operating lease equipment, net | 16,864.6 | 16,665.7 | 16,617.0 | 15,109.6 | ||||||||||||

| Indemnification assets | 375.5 | 389.4 | 414.8 | - | ||||||||||||

| Goodwill | 1,169.7 | 1,195.1 | 1,198.3 | 565.9 | ||||||||||||

| Intangible assets | 168.9 | 170.3 | 176.3 | 21.4 | ||||||||||||

| Unsecured counterparty receivable | 570.2 | 556.3 | 537.8 | 538.2 | ||||||||||||

| Other assets | 3,288.6 | 3,377.5 | 3,297.6 | 2,016.6 | ||||||||||||

| Assets of discontinued operation | 469.1 | 489.5 | 500.5 | - | ||||||||||||

| Total assets | $ | 66,700.3 | $ | 67,097.6 | $ | 67,401.5 | $ | 46,545.1 | ||||||||

| Liabilities | ||||||||||||||||

| Deposits | $ | 32,879.1 | $ | 32,892.7 | $ | 32,782.2 | $ | 17,267.8 | ||||||||

| Credit balances of factoring clients | 1,215.2 | 1,361.0 | 1,344.0 | 1,373.3 | ||||||||||||

| Other liabilities | 3,054.2 | 3,020.2 | 3,158.7 | 2,766.9 | ||||||||||||

| Borrowings | ||||||||||||||||

| Unsecured borrowings | 10,591.2 | 10,587.3 | 10,636.3 | 10,684.2 | ||||||||||||

| Structured financings | 3,923.8 | 4,309.0 | 4,687.9 | 5,497.9 | ||||||||||||

| FHLB advances | 2,995.1 | 3,116.3 | 3,117.6 | 147.4 | ||||||||||||

| Total borrowings | 17,510.1 | 18,012.6 | 18,441.8 | 16,329.5 | ||||||||||||

| Liabilities of discontinued operation | 917.1 | 684.8 | 696.2 | - | ||||||||||||

| Total liabilities | 55,575.7 | 55,971.3 | 56,422.9 | 37,737.5 | ||||||||||||

| Equity | ||||||||||||||||

| Stockholders' equity | ||||||||||||||||

| Common stock | 2.1 | 2.1 | 2.0 | 2.0 | ||||||||||||

| Paid-in capital | 8,749.8 | 8,739.4 | 8,718.1 | 8,615.6 | ||||||||||||

| Retained earnings | 2,656.9 | 2,673.7 | 2,557.4 | 1,781.1 | ||||||||||||

| Accumulated other comprehensive loss | (107.7 | ) | (117.4 | ) | (142.1 | ) | (158.8 | ) | ||||||||

| Treasury stock, at cost | (177.0 | ) | (172.0 | ) | (157.3 | ) | (1,432.8 | ) | ||||||||

| Total common stockholders' equity | 11,124.1 | 11,125.8 | 10,978.1 | 8,807.1 | ||||||||||||

| Noncontrolling interests | 0.5 | 0.5 | 0.5 | 0.5 | ||||||||||||

| Total equity | 11,124.6 | 11,126.3 | 10,978.6 | 8,807.6 | ||||||||||||

| Total liabilities and equity | $ | 66,700.3 | $ | 67,097.6 | $ | 67,401.5 | $ | 46,545.1 | ||||||||

| Book Value Per Common Share | ||||||||||||||||

| Book value per common share | $ | 55.07 | $ | 55.16 | $ | 54.61 | $ | 50.91 | ||||||||

| Tangible book value per common share | $ | 48.45 | $ | 48.39 | $ | 47.77 | $ | 47.51 | ||||||||

| Outstanding common shares (in thousands) | 201,990 | 201,702 | 201,022 | 172,998 | ||||||||||||

| * Preliminary | ||||||||||||||||

19

CIT GROUP INC. AND SUBSIDIARIES

Average Balances and Rates

(dollars in millions)

| Quarters Ended | ||||||||||||||||||||||||

| June 30, 2016 | March 31, 2016 | June 30, 2015 | ||||||||||||||||||||||

| Average Balance | Rate | Average Balance | Rate | Average Balance | Rate | |||||||||||||||||||

| Assets | ||||||||||||||||||||||||

| Interest bearing deposits | $ | 7,113.5 | 0.50 | % | $ | 7,114.0 | 0.47 | % | $ | 4,829.4 | 0.28 | % | ||||||||||||

| Securities purchased under agreements to resell | - | - | - | - | 675.0 | 0.59 | % | |||||||||||||||||

| Investments | 3,130.6 | 2.91 | % | 2,923.5 | 3.08 | % | 1,510.6 | 1.22 | % | |||||||||||||||

| Loans (including held for sale) | ||||||||||||||||||||||||

| U.S. | 31,784.4 | 5.87 | % | 32,091.5 | 5.74 | % | 18,130.4 | 5.41 | % | |||||||||||||||

| Non-U.S. | 1,160.2 | 8.41 | % | 1,291.0 | 8.18 | % | 2,161.3 | 9.01 | % | |||||||||||||||

| Total Loans | 32,944.6 | 5.96 | % | 33,382.5 | 5.84 | % | 20,291.7 | 5.83 | % | |||||||||||||||

| Total interest earning assets / interest income | 43,188.7 | 4.81 | % | 43,420.0 | 4.74 | % | 27,306.7 | 4.39 | % | |||||||||||||||

| Operating lease equipment, net (including held for sale) | ||||||||||||||||||||||||

| U.S. | 8,922.0 | 7.57 | % | 8,831.3 | 8.41 | % | 7,859.0 | 8.93 | % | |||||||||||||||

| Non-U.S. | 8,003.5 | 7.95 | % | 7,890.0 | 8.02 | % | 7,422.2 | 8.04 | % | |||||||||||||||

| Total operating lease equipment, net | 16,925.5 | 7.75 | % | 16,721.3 | 8.23 | % | 15,281.2 | 8.49 | % | |||||||||||||||

| Indemnification assets | 379.8 | -9.06 | % | 401.7 | -3.09 | % | - | - | ||||||||||||||||

| Total earning assets | 60,494.0 | 5.56 | % | 60,543.0 | 5.67 | % | 42,587.9 | 5.91 | % | |||||||||||||||

| Non-interest earning assets | ||||||||||||||||||||||||

| Cash and due from banks | 1,051.4 | 1,331.4 | 952.7 | |||||||||||||||||||||

| Non-interest bearing deposits | ||||||||||||||||||||||||

| Allowance for loan losses | (398.9 | ) | (371.5 | ) | (358.0 | ) | ||||||||||||||||||

| All other non-interest bearing assets | 5,278.8 | 5,298.4 | 3,169.0 | |||||||||||||||||||||

| Assets of discontinued operation | 479.9 | 495.1 | - | |||||||||||||||||||||

| Total Average Assets | $ | 66,905.2 | $ | 67,296.4 | $ | 46,351.6 | ||||||||||||||||||

| Liabilities | ||||||||||||||||||||||||

| Borrowings | ||||||||||||||||||||||||

| Deposits | $ | 31,643.5 | 1.26 | % | $ | 31,829.1 | 1.25 | % | $ | 16,844.6 | 1.71 | % | ||||||||||||

| Borrowings | 17,853.7 | 4.10 | % | 18,210.4 | 4.11 | % | 16,423.8 | 4.70 | % | |||||||||||||||

| Total interest-bearing liabilities | 49,497.2 | 2.28 | % | 50,039.5 | 2.29 | % | 33,268.4 | 3.19 | % | |||||||||||||||

| Non-interest bearing deposits | 1,124.9 | 1,080.2 | 90.3 | |||||||||||||||||||||

| Credit balances of factoring clients | 1,264.9 | 1,337.5 | 1,428.6 | |||||||||||||||||||||

| Other non-interest bearing liabilities | 3,093.3 | 3,063.7 | 2,776.7 | |||||||||||||||||||||

| Liabilities of discontinued operation | 738.1 | 690.2 | - | |||||||||||||||||||||

| Noncontrolling interests | 0.5 | 0.5 | 0.5 | |||||||||||||||||||||

| Stockholders' equity | 11,186.3 | 11,084.8 | 8,787.1 | |||||||||||||||||||||

| Total Average Liabilities and Stockholders' Equity | $ | 66,905.2 | $ | 67,296.4 | $ | 46,351.6 | ||||||||||||||||||

| Six Months Ended | ||||||||||||||||||||||||

| June 30, 2016 | June 30, 2015 | |||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||

| Interest bearing deposits | $ | 7,110.7 | 0.49 | % | $ | 5,390.1 | 0.27 | % | ||||||||||||||||

| Securities purchased under agreements to resell | - | - | 650.0 | 0.52 | % | |||||||||||||||||||

| Investments | 3,045.7 | 2.98 | % | 1,526.2 | 1.11 | % | ||||||||||||||||||

| Loans (including held for sale) | ||||||||||||||||||||||||

| U.S. | 31,904.4 | 5.81 | % | 18,012.5 | 5.39 | % | ||||||||||||||||||

| Non-U.S. | 1,230.6 | 8.26 | % | 2,203.2 | 9.18 | % | ||||||||||||||||||

| Total Loans | 33,135.0 | 5.90 | % | 20,215.7 | 5.83 | % | ||||||||||||||||||

| Total interest earning assets / interest income | 43,291.4 | 4.77 | % | 27,782.0 | 4.29 | % | ||||||||||||||||||

| Operating lease equipment, net (including held for sale) | ||||||||||||||||||||||||

| U.S. | 8,873.5 | 7.99 | % | 7,821.1 | 9.03 | % | ||||||||||||||||||

| Non-U.S. | 7,951.6 | 7.98 | % | 7,424.1 | 8.05 | % | ||||||||||||||||||

| Total operating lease equipment, net | 16,825.1 | 7.99 | % | 15,245.2 | 8.56 | % | ||||||||||||||||||

| Indemnification assets | 390.9 | -5.99 | % | - | - | |||||||||||||||||||

| Total earning assets | 60,507.4 | 5.62 | % | 43,027.2 | 5.85 | % | ||||||||||||||||||

| Non-interest earning assets | ||||||||||||||||||||||||

| Cash and due from banks | 1,217.8 | 930.3 | ||||||||||||||||||||||

| Allowance for loan losses | (382.4 | ) | (352.3 | ) | ||||||||||||||||||||

| All other non-interest bearing assets | 5,271.3 | 3,184.2 | ||||||||||||||||||||||

| Assets of discontinued operation | 487.2 | - | ||||||||||||||||||||||

| Total Average Assets | $ | 67,101.3 | $ | 46,789.4 | ||||||||||||||||||||

| Liabilities | ||||||||||||||||||||||||

| Borrowings | ||||||||||||||||||||||||

| Deposits | $ | 31,727.6 | 1.25 | % | $ | 16,546.2 | 1.71 | % | ||||||||||||||||

| Borrowings | 18,034.8 | 4.10 | % | 17,009.7 | 4.65 | % | ||||||||||||||||||

| Total interest-bearing liabilities | 49,762.4 | 2.29 | % | 33,555.9 | 3.20 | % | ||||||||||||||||||

| Non-interest bearing deposits | 1,103.6 | 98.2 | ||||||||||||||||||||||

| Credit balances of factoring clients | 1,292.6 | 1,459.2 | ||||||||||||||||||||||

| Other non-interest bearing liabilities | 3,087.0 | 2,836.4 | ||||||||||||||||||||||

| Liabilities of discontinued operation | 718.3 | - | ||||||||||||||||||||||

| Noncontrolling interests | 0.5 | (2.0 | ) | |||||||||||||||||||||

| Stockholders' equity | 11,136.9 | 8,841.7 | ||||||||||||||||||||||

| Total Average Liabilities and Stockholders' Equity | $ | 67,101.3 | $ | 46,789.4 | ||||||||||||||||||||

20

CIT GROUP INC. AND SUBSIDIARIES

Select Accounts

(dollars in millions)

| Quarters Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016 | 2016 | 2015 | 2016 | 2015 | ||||||||||||||||

| OTHER INCOME | ||||||||||||||||||||

| Fee revenues | $ | 28.0 | $ | 32.7 | $ | 25.3 | $ | 60.7 | $ | 47.9 | ||||||||||

| Gains on sales of leasing equipment | 28.0 | 11.2 | 21.5 | 39.2 | 53.5 | |||||||||||||||

| Factoring commissions | 24.1 | 26.4 | 27.0 | 50.5 | 56.5 | |||||||||||||||

| Net gain (losses) on derivatives and foreign currency exchange | 10.4 | 9.3 | (5.0 | ) | 19.7 | (14.7 | ) | |||||||||||||

| Gains on loan and portfolio sales | 7.7 | 0.3 | 2.1 | 8.0 | 8.7 | |||||||||||||||

| Gains (losses) on investments | 6.3 | (4.1 | ) | 3.8 | 2.2 | 4.5 | ||||||||||||||

| Gain on OREO sales | 3.5 | 1.7 | - | 5.2 | - | |||||||||||||||

| Impairment on assets held for sale | (17.0 | ) | (22.1 | ) | (11.0 | ) | (39.1 | ) | (21.1 | ) | ||||||||||

| Other revenues | 13.3 | 45.5 | (0.2 | ) | 58.8 | 14.6 | ||||||||||||||

| Total other income | $ | 104.3 | $ | 100.9 | $ | 63.5 | $ | 205.2 | $ | 149.9 | ||||||||||

| OPERATING EXPENSES | ||||||||||||||||||||

| Compensation and benefits | $ | (155.9 | ) | $ | (172.2 | ) | $ | (135.6 | ) | $ | (328.1 | ) | $ | (282.1 | ) | |||||

| Professional fees | (39.5 | ) | (38.8 | ) | (20.8 | ) | (78.3 | ) | (40.3 | ) | ||||||||||

| Technology | (31.3 | ) | (30.4 | ) | (24.9 | ) | (61.7 | ) | (47.2 | ) | ||||||||||

| Net occupancy expense | (17.4 | ) | (18.4 | ) | (8.6 | ) | (35.8 | ) | (18.0 | ) | ||||||||||

| Advertising and marketing | (4.4 | ) | (5.4 | ) | (6.7 | ) | (9.8 | ) | (15.8 | ) | ||||||||||

| Other expenses | (72.9 | ) | (56.6 | ) | (36.8 | ) | (129.5 | ) | (72.0 | ) | ||||||||||

| Operating expenses, before provision for severance and facilities exiting and intangible asset amortization | (321.4 | ) | (321.8 | ) | (233.4 | ) | (643.2 | ) | (475.4 | ) | ||||||||||

| Provision for severance and facilities exiting activities | (9.7 | ) | (20.3 | ) | (1.1 | ) | (30.0 | ) | (0.1 | ) | ||||||||||

| Intangible asset amortization | (6.4 | ) | (6.4 | ) | (0.5 | ) | (12.8 | ) | (1.1 | ) | ||||||||||

| Total operating expenses | $ | (337.5 | ) | $ | (348.5 | ) | $ | (235.0 | ) | $ | (686.0 | ) | $ | (476.6 | ) | |||||

| June 30, | March 31, | December 31, | June 30, | |||||||||||||||||

| 2016* | 2016 | 2015 | 2015 | |||||||||||||||||

| TOTAL CASH AND INVESTMENT SECURITIES | ||||||||||||||||||||

| Total cash and deposits | $ | 8,103.9 | $ | 8,141.8 | $ | 8,301.5 | $ | 5,465.3 | ||||||||||||

| Securities purchased under agreements to resell | - | - | - | 750.0 | ||||||||||||||||

| Investment securities | 3,229.1 | 2,896.8 | 2,953.8 | 1,692.9 | ||||||||||||||||

| Total cash and investment securities | $ | 11,333.0 | $ | 11,038.6 | $ | 11,255.3 | $ | 7,908.2 | ||||||||||||

| OTHER ASSETS | ||||||||||||||||||||

| Current and deferred federal and state tax assets | $ | 1,180.9 | $ | 1,197.4 | $ | 1,252.5 | $ | 431.2 | ||||||||||||

| Deposits on commercial aerospace equipment | 764.6 | 774.3 | 696.0 | 816.9 | ||||||||||||||||

| Tax credit investments and investments in unconsolidated subsidiaries | 238.1 | 237.9 | 223.9 | 78.6 | ||||||||||||||||

| Property, furniture and fixtures | 191.6 | 192.1 | 197.2 | 144.4 | ||||||||||||||||

| Other counterparty receivables | 146.7 | 179.6 | 59.0 | 28.8 | ||||||||||||||||

| Fair value of derivative financial instruments | 134.0 | 97.4 | 140.7 | 101.5 | ||||||||||||||||

| Other real estate owned and repossessed assets | 91.6 | 105.4 | 127.3 | 2.6 | ||||||||||||||||

| Tax receivables, other than income taxes | 82.1 | 105.7 | 98.2 | 103.0 | ||||||||||||||||

| Other | 459.0 | 487.7 | 502.8 | 309.6 | ||||||||||||||||

| Total other assets | $ | 3,288.6 | $ | 3,377.5 | $ | 3,297.6 | $ | 2,016.6 | ||||||||||||

| OTHER LIABILITIES | ||||||||||||||||||||

| Equipment maintenance reserves | $ | 1,067.2 | $ | 1,042.2 | $ | 1,012.4 | $ | 982.5 | ||||||||||||

| Accrued expenses and accounts payable | 542.8 | 563.6 | 628.1 | 439.2 | ||||||||||||||||

| Current and deferred taxes payable | 364.1 | 354.5 | 363.1 | 345.6 | ||||||||||||||||

| Accrued interest payable | 200.4 | 161.0 | 209.6 | 221.2 | ||||||||||||||||

| Security and other deposits | 197.6 | 179.9 | 263.0 | 265.9 | ||||||||||||||||

| Fair value of derivative financial instruments | 154.6 | 196.5 | 103.0 | 88.1 | ||||||||||||||||

| Valuation adjustment relating to aerospace commitments | 73.1 | 73.1 | 73.1 | 117.1 | ||||||||||||||||

| Other liabilities | 454.4 | 449.4 | 506.4 | 307.3 | ||||||||||||||||

| Total other liabilities | $ | 3,054.2 | $ | 3,020.2 | $ | 3,158.7 | $ | 2,766.9 | ||||||||||||

| * Preliminary | ||||||||||||||||||||

21

CIT GROUP INC. AND SUBSIDIARIES

Financing and Leasing Assets

(dollars in millions)

| June 30, | March 31, | December 31, | June 30, | |||||||||||||

| 2016 | 2016 | 2015 | 2015 | |||||||||||||

| Commercial Banking | ||||||||||||||||

| Commercial Finance | ||||||||||||||||

| Loans | $ | 8,512.9 | $ | 9,329.4 | $ | 9,118.6 | $ | 6,734.8 | ||||||||

| Assets held for sale | 461.3 | 203.4 | 313.6 | 88.2 | ||||||||||||

| Financing and leasing assets | 8,974.2 | 9,532.8 | 9,432.2 | 6,823.0 | ||||||||||||

| Real Estate Finance | ||||||||||||||||

| Loans | 5,566.1 | 5,348.5 | 5,300.6 | 1,941.4 | ||||||||||||

| Assets held for sale | - | 14.4 | 57.0 | - | ||||||||||||

| Financing and leasing assets | 5,566.1 | 5,362.9 | 5,357.6 | 1,941.4 | ||||||||||||

| Business Capital | ||||||||||||||||

| Loans | 6,630.8 | 6,759.3 | 6,510.0 | 6,436.1 | ||||||||||||

| Operating lease equipment, net | 314.8 | 292.6 | 259.0 | 241.9 | ||||||||||||

| Assets held for sale | 10.4 | 11.9 | 44.3 | - | ||||||||||||

| Financing and leasing assets | 6,956.0 | 7,063.8 | 6,813.3 | 6,678.0 | ||||||||||||

| Total Segment | ||||||||||||||||

| Loans | 20,709.8 | 21,437.2 | 20,929.2 | 15,112.3 | ||||||||||||

| Operating lease equipment, net | 314.8 | 292.6 | 259.0 | 241.9 | ||||||||||||

| Assets held for sale | 471.7 | 229.7 | 414.9 | 88.2 | ||||||||||||

| Financing and leasing assets | 21,496.3 | 21,959.5 | 21,603.1 | 15,442.4 | ||||||||||||

| Transportation Finance | ||||||||||||||||

| Aerospace | ||||||||||||||||

| Loans | 904.4 | 1,031.9 | 1,762.3 | 1,739.6 | ||||||||||||

| Operating lease equipment, net | 9,685.6 | 9,594.3 | 9,765.2 | 8,816.7 | ||||||||||||

| Assets held for sale | 764.1 | 723.8 | 34.7 | 243.9 | ||||||||||||

| Financing and leasing assets | 11,354.1 | 11,350.0 | 11,562.2 | 10,800.2 | ||||||||||||

| Rail | ||||||||||||||||

| Loans | 106.9 | 118.1 | 120.9 | 124.7 | ||||||||||||

| Operating lease equipment, net | 6,864.2 | 6,778.8 | 6,592.8 | 6,010.8 | ||||||||||||

| Assets held for sale | 6.9 | 0.4 | 0.7 | 0.9 | ||||||||||||

| Financing and leasing assets | 6,978.0 | 6,897.3 | 6,714.4 | 6,136.4 | ||||||||||||

| Maritime Finance | ||||||||||||||||

| Loans | 1,601.8 | 1,636.7 | 1,658.9 | 1,274.4 | ||||||||||||

| Assets held for sale | 29.6 | 30.5 | 19.5 | 56.4 | ||||||||||||

| Financing and leasing assets | 1,631.4 | 1,667.2 | 1,678.4 | 1,330.8 | ||||||||||||

| Total Segment | ||||||||||||||||

| Loans | 2,613.1 | 2,786.7 | 3,542.1 | 3,138.7 | ||||||||||||

| Operating lease equipment, net | 16,549.8 | 16,373.1 | 16,358.0 | 14,827.5 | ||||||||||||

| Assets held for sale | 800.6 | 754.7 | 54.9 | 301.2 | ||||||||||||

| Financing and leasing assets | 19,963.5 | 19,914.5 | 19,955.0 | 18,267.4 | ||||||||||||

| Consumer and Community Banking | ||||||||||||||||

| Other Consumer Banking | ||||||||||||||||

| Loans | 1,977.1 | 1,879.5 | 1,770.0 | - | ||||||||||||

| Assets held for sale | 3.3 | 2.6 | 3.9 | - | ||||||||||||

| Financing and leasing assets | 1,980.4 | 1,882.1 | 1,773.9 | - | ||||||||||||

| Legacy Consumer Mortgages | ||||||||||||||||

| Loans | 5,156.8 | 5,305.2 | 5,430.4 | - | ||||||||||||

| Assets held for sale | 34.6 | 48.0 | 41.2 | - | ||||||||||||

| Financing and leasing assets | 5,191.4 | 5,353.2 | 5,471.6 | - | ||||||||||||

| Total Segment | ||||||||||||||||

| Loans | 7,133.9 | 7,184.7 | 7,200.4 | - | ||||||||||||

| Assets held for sale | 37.9 | 50.6 | 45.1 | - | ||||||||||||