Form 6-K Vale S.A. For: Jul 28

Tweet

Tweet Share

Share

United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the

Securities Exchange Act of 1934

For the month of

July 2016

Vale S.A.

Avenida das Américas, No. 700 – Bloco 8, Sala 218

22640-100 Rio de Janeiro, RJ, Brazil

(Address of principal executive office)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.)

(Check One) Form 20-F x Form 40-F o

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1))

(Check One) Yes o No x

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7))

(Check One) Yes o No x

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.)

(Check One) Yes o No x

(If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b). 82- .)

www.vale.com

App Vale Investors & Media

iOS: https://itunes.apple.com/us/app/vale-investor-media-english/id1087126847?ls=1&mt=8

Android: https://play.google.com/store/apps/details?id=com.theirapp.valeeg

Tel.: (55 21) 3485-3900

Investor Relations Department

André Figueiredo

Carla Albano Miller

Fernando Mascarenhas

Andrea Gutman

Bruno Siqueira

Claudia Rodrigues

Denise Caruncho

Mariano Szachtman

Renata Capanema

BM&F BOVESPA: VALE3, VALE5

NYSE: VALE, VALE.P

EURONEXT PARIS: VALE3, VALE5

LATIBEX: XVALO, XVALP

Except where otherwise indicated the operational and financial information in this release is based on the consolidated figures in accordance with IFRS and, with the exception of information on investments and behavior of markets, quarterly financial statements are reviewed by the company’s independent auditors. The main subsidiaries that are consolidated are the following: Companhia Portuária da Baía de Sepetiba, Compañia Minera Miski Mayo S.A.C., Mineração Corumbaense Reunida S.A., Minerações Brasileiras Reunidas S.A., Salobo Metais S.A., Vale International Holdings GmbH, Vale Canada Holdings Inc., Vale Canada Limited, Vale Fertilizantes S.A., Vale International S.A., Vale Malaysia Minerals Sdn. Bhd., Vale Manganês S.A., Vale Moçambique S.A., Vale Nouvelle-Calédonie S.A.S. and Vale Shipping Holding Pte. Ltd.

Contents

|

4 | |

|

|

|

|

9 | |

|

|

|

|

11 | |

|

|

|

|

Adjusted earnings before interest, taxes, depreciation and amortization |

14 |

|

|

|

|

15 | |

|

|

|

|

23 | |

|

|

|

|

29 | |

|

|

|

|

30 | |

|

|

|

|

32 | |

|

|

|

|

33 | |

|

|

|

|

45 | |

|

|

|

|

55 | |

|

|

|

|

59 | |

|

|

|

|

62 |

Rio de Janeiro, July 28, 2016 — Vale S.A. (Vale) delivered a sound operational performance in 2Q16, reaching several production records for a second quarter, namely: (i) Carajás iron ore production of 36.5 Mt; (ii) nickel production of 78.5 kt, (iii) copper production of 105.6 kt; and (iv) gold production of 109,000 oz.

Net revenues totaled US$ 6.626 billion in 2Q16, increasing US$ 907 million vs. 1Q16 as a result of higher sales volumes of iron ore fines (US$ 462 million) and higher sales prices for iron ore fines (US$ 129 million) and pellets (US$ 98 million).

Costs and expenses increased to US$ 5.287 billion in 2Q16 from the US$ 4.565 billion recorded in 1Q16, mainly due to the impact of higher sales volumes (US$ 457 million) and exchange rate (US$ 283 million), being partially offset by cost reduction initiatives (US$ 165 million).

Adjusted EBITDA was US$ 2.383 billion in 2Q16, 18.9% higher than in 1Q16 mainly driven by Ferrous Minerals (US$ 398 million) and Base Metals (US$ 47 million). Adjusted EBITDA margin was 36.0% in 2Q16, increasing from the 35.1% recorded in 1Q16.

Adjusted EBITDA amounted to US$ 4.388 billion in 1H16 against US$ 3.585 billion(1) in 1H15, increasing US$ 803 million, despite the US$ 860 million decrease in net operating revenues driven by lower sales prices (US$ 1.533 billion). The increase in adjusted EBITDA was mainly driven by our efforts to reduce costs(2) (US$ 1.193 billion) and expenses¹² (US$ 564 million).

Capital expenditures totaled US$ 1.368 billion in 2Q16, decreasing by US$ 81 million vs. 1Q16. Investments in project execution totaled US$ 905 million in 2Q16, with expenditures associated with the S11D project accounting for US$ 540 million. Sustaining capex totaled US$ 463 million in 2Q16, decreasing US$ 66 million from the US$ 529 million recorded in 1Q16.

Net income totaled US$ 1.106 billion in 2Q16 vs. US$ 1.776 billion in 1Q16, decreasing US$ 670 million mostly as a result of a US$ 1.038 billion Samarco related provision(3). Underlying earnings (after adjusting net income for one-off effects) were US$ 709 million in 2Q16, mainly after the adjustments for exchange rate (US$ 1.960 billion), provision for Samarco liabilities (US$ 1.038 billion) and currencies and interest rate swaps (US$ 483 million).

(1) Net of US$ 230 million of the goldstream transaction in 1H15.

(2) Net of depreciation

(3) For more information on the Samarco related provision, please see the section “Update on Samarco Mineração S.A.” of this release.

Gross debt totaled US$ 31.814 billion as of June 30th, 2016, increasing slightly from the US$ 31.470 billion as of March 31st, 2016, mainly as a result of the impact of the appreciation of the Brazilian Real (BRL) on the translation of the BRL denominated debt into USD(4), which was partially offset by net debt payments of US$ 375 million in 2Q16.

Net debt decreased to US$ 27.508 billion as of June 30th, 2016 from US$ 27.661 billion as of March 31st, 2016, with a cash balance of US$ 4.306 billion. The decrease in net debt was mainly driven by the positive free cash flow of US$ 761 million in 2Q16, which was partially offset by the exchange rate impact on the translation of the BRL denominated debt into USD.

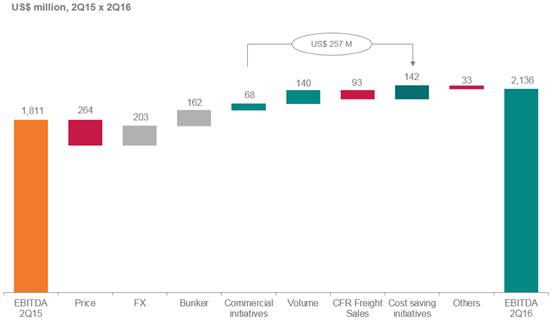

EBITDA from the Ferrous Minerals business segment increased 23% in 2Q16 vs. 1Q16 driven by higher realized prices and higher sales volumes

· Adjusted EBITDA for Ferrous Minerals was US$ 2.136 billion in 2Q16, US$ 398 million higher than the US$ 1.738 billion achieved in 1Q16, mainly as a result of higher realized sales prices (US$ 262 million) and higher sales volumes (US$ 246 million), which were partially offset by exchange rate variations (US$ 147 million).

· Cash flow generation, simplified by measuring adjusted EBITDA less sustaining and growth capex, was US$ 1.367 billion in 2Q16, increasing US$ 538 million (65%) from the US$ 829 million recorded in 1Q16.

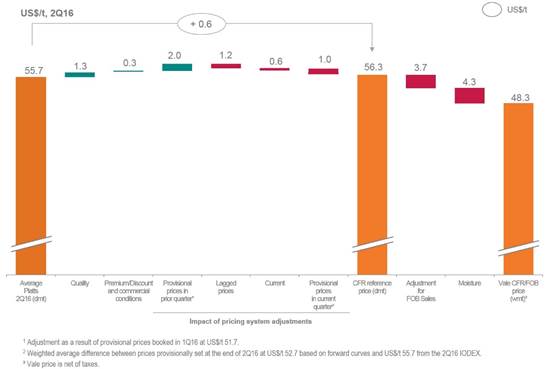

· CFR dmt reference price for iron ore fines (ex-ROM) increased by US$ 1.6/t from US$ 54.7/t in 1Q16 to US$ 56.3/t in 2Q16, equivalent to a price realization of 101% of the average Platts IODEX 62% of US$ 55.7/t in 2Q16, whereas the combined CFR/FOB wmt price for iron ore fines (ex-ROM)(5) increased by US$ 1.8/t from US$ 46.5/t in 1Q16 to US$ 48.3/t in 2Q16.

· Average Fe content of iron ore fines production decreased slightly, as planned, from 64.3% in 1Q16 to 63.6% in 2Q16, mainly in response to market demand for higher silica ores.

· C1 cash cost FOB port per metric ton for iron ore fines ex-royalties totaled US$ 13.2/t in 2Q16, US$ 0.9/t higher than the US$ 12.3/t recorded in 1Q16, due to the impact of the BRL appreciation against the USD.

· C1 cash cost FOB port per metric ton of iron ore fines in BRL was R$ 46.1/t in 2Q16, R$ 1.4/t lower than the R$ 47.5/t recorded in 1Q16, mainly due to improved

(4) In 2Q16, from end to end, the BRL appreciated 9.8% against the USD.

(5) After adjusting for moisture and the effects of FOB sales on 34% of the total sales volumes

operational performance, ongoing cost-cutting initiatives and increased fixed-costs dilution on seasonally higher production volumes.

· Unit maritime freight cost per iron ore metric ton was US$ 11.8/t in 2Q16, US$ 0.5/t higher than the US$ 11.3/t recorded in 1Q16, mainly driven by the negative impact of higher bunker oil prices in our chartering contracts.

· Iron ore fines and pellets EBITDA break-even, measured by unit cash costs and expenses on a landed-in-China basis (and adjusted for quality, pellets margins differential and moisture, excluding ROM), increased from US$ 28.0/dmt in 1Q16 to US$ 28.5/dmt in 2Q16, mainly driven by (i) the impact on C1 cash cost of the appreciation of BRL against the USD (US$ 1.2/t); (ii) higher bunker oil prices (US$ 0.4/t); and (iii) higher royalties (US$ 0.5/t), due to higher iron ore prices; and were partially offset by higher pellet premiums (US$ 0.3/t) and by the dividends received from the pelletizing plants (US$ 0.7/t)(6).

· Iron ore and pellets cash break-even on a landed-in-China basis, including sustaining capex per ton of US$ 1.8/t, decreased from US$ 30.9/ dmt in 1Q16 to US$ 30.3/ dmt in 2Q16.

· Physical progress reached 90% at the S11D mine and plant, 70% at the S11D logistic sites and 92% at the S11D railway spur.

EBITDA from the Base Metals business segment increased 14% in 2Q16 vs. 1Q16 as operational improvements more than offset negative exchange rate impacts

· Nickel realized prices were positively impacted by improving premiums over the LME, increasing 4.5% in 2Q16 vs. 1Q16 vs. the 3.8% increase of LME nickel prices in the same period.

· Adjusted EBITDA was US$ 376 million in 2Q16, US$ 47 million higher than in 1Q16, as a result of lower costs (US$ 50 million) and higher prices (US$ 48 million), which offset the negative exchange rate impacts (US$ 56 million).

· Adjusted EBITDA for VNC totaled negative US$ 50 million in 2Q16, in line with the previous quarter and US$ 28 million better than in 2Q15 as VNC’s unit costs net of by-product credits reached US$ 12,208/t in 2Q16, decreasing from the US$ 20,471/t in 2Q15 and the US$ 12,711/t in 1Q16.

(6) Dividends usually paid every 6 months (at second and fourth quarters).

· Salobo’s EBITDA totaled US$ 122 million in 2Q16, decreasing US$ 9 million from the US$ 131 million recorded in 1Q16, mainly as a result of the negative impact of the appreciation of the BRL (US$ 13 million).

· Salobo achieved a monthly production record of 14.6 kt of copper in concentrates in May and is expected to reach its full production capacity on a monthly basis during 2H16.

EBITDA from Coal was positively impacted by lower costs in Mozambique with the ramp-up of the Nacala Logistics Corridor

· Adjusted EBITDA was negative US$ 110 million in 2Q16 vs. negative US$ 93 million in 1Q16, having decreased US$ 17 million mainly as a result of geological instability issues at Carborough Downs (US$ 29 million).

· Production cost per ton at Nacala Port in Mozambique decreased by 39% to US$ 103/t in 2Q16 from US$ 168/t in 1Q16, and should further improve in the coming quarters as Nacala ramp ups and Moatize II starts up in early August.

· Total mine movement in Mozambique reached a new monthly record of 12.7 Mt in June due to higher equipment productivity and the development of new mining areas to supply the Moatize II coal handling and processing plant.

EBITDA from the Fertilizers business segment decreased, mainly driven by lower prices and the appreciation of the BRL

· Adjusted EBITDA for Fertilizers decreased to US$ 32 million in 2Q16 from US$ 70 million in 1Q16, mainly driven by the negative effect of the appreciation of the BRL, which impacted costs, expenses and revenues (US$ 13 million), and by lower prices (US$ 11 million).

· Realized prices for fertilizer nutrients decreased in 2Q16 vs 1Q16 for almost all of our products, with prices decreasing by 6.7% for Potash, 1.8% for MAP, 0.4% for TSP, 9.5% for SSP and 14.5% for phosphate rock.

The S11D project — the most important project in our history — is being commissioned and, meanwhile, we remain committed to our divestment program, having sold three very large ore carriers of 400,000 deadweight tons to ICBC Financial Leasing in 2Q16. The transaction totaled US$ 269 million and the amount will be received in August.

Looking forward, we remain fully focused on improving our operations, maintaining our capex discipline and strengthening our balance sheet.

Selected financial indicators

|

|

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

% |

|

% |

|

|

US$ million |

|

(A) |

|

(B) |

|

(C) |

|

(A/B) |

|

(A/C) |

|

|

Net operating revenues |

|

6,626 |

|

5,719 |

|

6,965 |

|

16 |

|

(5 |

) |

|

Adjusted EBIT |

|

1,339 |

|

1,154 |

|

1,040 |

|

16 |

|

29 |

|

|

Adjusted EBIT margin (%) |

|

20.2 |

|

20.2 |

|

14.9 |

|

— |

|

— |

|

|

Adjusted EBITDA |

|

2,383 |

|

2,005 |

|

2,213 |

|

19 |

|

8 |

|

|

Adjusted EBITDA margin (%) |

|

36.0 |

|

35.1 |

|

31.8 |

|

— |

|

— |

|

|

Net income (loss) |

|

1,106 |

|

1,776 |

|

1,675 |

|

(38 |

) |

(34 |

) |

|

Underlying earnings |

|

709 |

|

514 |

|

973 |

|

38 |

|

(27 |

) |

|

Underlying earnings per share on a fully diluted basis (US$ / share) |

|

0.14 |

|

0.10 |

|

0.19 |

|

— |

|

— |

|

|

Total gross debt |

|

31,814 |

|

31,470 |

|

29,773 |

|

1 |

|

7 |

|

|

Cash and cash equivalent |

|

4,306 |

|

3,809 |

|

3,264 |

|

13 |

|

32 |

|

|

Total Net Debt |

|

27,508 |

|

27,661 |

|

26,509 |

|

(1 |

) |

4 |

|

|

Total gross debt/ adjusted EBITDA (x) |

|

4.2 |

|

4.2 |

|

3.3 |

|

— |

|

— |

|

|

Capital expenditures |

|

1,368 |

|

1,449 |

|

2,119 |

|

(6 |

) |

(35 |

) |

|

|

|

1H16 |

|

1H15 |

|

% |

|

|

US$ million |

|

(A) |

|

(B) |

|

(A/B) |

|

|

Net operating revenues |

|

12,345 |

|

13,205 |

|

(7 |

) |

|

Adjusted EBIT |

|

2,493 |

|

1,580 |

|

58 |

|

|

Adjusted EBIT margin (%) |

|

20.2 |

|

12.0 |

|

— |

|

|

Adjusted EBITDA |

|

4,388 |

|

3,815 |

|

15 |

|

|

Adjusted EBITDA margin (%) |

|

35.5 |

|

28.9 |

|

— |

|

|

Adjusted EBITDA net of the goldstream transaction in 1H15 |

|

4,388 |

|

3,585 |

|

22 |

|

|

Underlying earnings |

|

1,223 |

|

294 |

|

316 |

|

|

Underlying earnings per share on a fully diluted basis (US$ / share) |

|

0.24 |

|

0.06 |

|

— |

|

|

Capital expenditures |

|

2,817 |

|

4,328 |

|

(35 |

) |

Net operating revenues in 2Q16 were US$ 6.626 billion, 15.9% higher than in 1Q16. The increase in sales revenues was mainly due to higher sales volumes in iron ore fines (US$ 462 million), and higher sales prices for iron ore fines (US$ 129 million) and for pellets (US$ 98 million).

The tables below show net operating revenues by destination and by business areas, with the following highlights:

· Net revenue by destination was marked by: (i) the decrease in sales to Asia from 57.4% in 1Q16 to 55.4% in 2Q16, as revenues from other regions increased more than revenues from Asia, and (ii) the increase in sales to the Middle East from 2.7% in 1Q16 to 3.6% in 2Q16.

· Contribution by business segments in 2Q16 was generally in line with 1Q16, with the Ferrous Minerals business segment representing 68.5% of Vale’s total net revenues.

Net operating revenue by destination

|

US$ million |

|

2Q16 |

|

% |

|

1Q16 |

|

% |

|

2Q15 |

|

% |

|

|

North America |

|

511 |

|

7.7 |

|

496 |

|

8.7 |

|

574 |

|

8.2 |

|

|

USA |

|

230 |

|

3.5 |

|

209 |

|

3.7 |

|

241 |

|

3.5 |

|

|

Canada |

|

281 |

|

4.2 |

|

278 |

|

4.9 |

|

332 |

|

4.8 |

|

|

Mexico |

|

— |

|

— |

|

9 |

|

0.2 |

|

— |

|

— |

|

|

South America |

|

994 |

|

15.0 |

|

814 |

|

14.2 |

|

1,163 |

|

16.7 |

|

|

Brazil |

|

903 |

|

13.6 |

|

719 |

|

12.6 |

|

1,040 |

|

14.9 |

|

|

Others |

|

91 |

|

1.4 |

|

95 |

|

1.7 |

|

123 |

|

1.8 |

|

|

Asia |

|

3,668 |

|

55.4 |

|

3,281 |

|

57.4 |

|

3,618 |

|

51.9 |

|

|

China |

|

2,700 |

|

40.7 |

|

2,454 |

|

42.9 |

|

2,584 |

|

37.1 |

|

|

Japan |

|

405 |

|

6.1 |

|

340 |

|

5.9 |

|

417 |

|

6.0 |

|

|

South Korea |

|

188 |

|

2.8 |

|

199 |

|

3.5 |

|

184 |

|

2.6 |

|

|

Others |

|

376 |

|

5.7 |

|

288 |

|

5.0 |

|

433 |

|

6.2 |

|

|

Europe |

|

1,137 |

|

17.2 |

|

936 |

|

16.4 |

|

1,277 |

|

18.3 |

|

|

Germany |

|

358 |

|

5.4 |

|

280 |

|

4.9 |

|

381 |

|

5.5 |

|

|

Italy |

|

125 |

|

1.9 |

|

115 |

|

2.0 |

|

115 |

|

1.6 |

|

|

Others |

|

654 |

|

9.9 |

|

542 |

|

9.5 |

|

781 |

|

11.2 |

|

|

Middle East |

|

240 |

|

3.6 |

|

152 |

|

2.7 |

|

286 |

|

4.1 |

|

|

Rest of the World |

|

76 |

|

1.2 |

|

40 |

|

0.7 |

|

47 |

|

0.7 |

|

|

Total |

|

6,626 |

|

100.0 |

|

5,719 |

|

100.0 |

|

6,965 |

|

100.0 |

|

Net operating revenues by destination

Net operating revenue by business areas

|

US$ million |

|

2Q16 |

|

% |

|

1Q16 |

|

% |

|

2Q15 |

|

% |

|

|

Ferrous minerals |

|

4,541 |

|

68.5 |

|

3,804 |

|

66.5 |

|

4,552 |

|

65.4 |

|

|

Iron ore fines |

|

3,508 |

|

52.9 |

|

2,917 |

|

51.0 |

|

3,391 |

|

48.7 |

|

|

ROM |

|

5 |

|

0.1 |

|

4 |

|

0.1 |

|

33 |

|

0.5 |

|

|

Pellets |

|

868 |

|

13.1 |

|

753 |

|

13.2 |

|

972 |

|

14.0 |

|

|

Manganese ore |

|

36 |

|

0.5 |

|

31 |

|

0.5 |

|

32 |

|

0.5 |

|

|

Ferroalloys |

|

25 |

|

0.4 |

|

16 |

|

0.3 |

|

21 |

|

0.3 |

|

|

Others |

|

99 |

|

1.5 |

|

83 |

|

1.5 |

|

103 |

|

1.5 |

|

|

Coal |

|

145 |

|

2.2 |

|

154 |

|

2.7 |

|

146 |

|

2.1 |

|

|

Metallurgical coal |

|

77 |

|

1.2 |

|

104 |

|

1.8 |

|

137 |

|

2.0 |

|

|

Thermal coal |

|

68 |

|

1.0 |

|

50 |

|

0.9 |

|

9 |

|

0.1 |

|

|

Base metals |

|

1,447 |

|

21.8 |

|

1,353 |

|

23.7 |

|

1,648 |

|

23.7 |

|

|

Nickel |

|

710 |

|

10.7 |

|

650 |

|

11.4 |

|

874 |

|

12.5 |

|

|

Copper |

|

443 |

|

6.7 |

|

435 |

|

7.6 |

|

483 |

|

6.9 |

|

|

PGMs |

|

99 |

|

1.5 |

|

96 |

|

1.7 |

|

125 |

|

1.8 |

|

|

Gold |

|

154 |

|

2.3 |

|

130 |

|

2.3 |

|

128 |

|

1.8 |

|

|

Silver |

|

10 |

|

0.2 |

|

9 |

|

0.2 |

|

7 |

|

0.1 |

|

|

Others |

|

31 |

|

0.5 |

|

33 |

|

0.6 |

|

31 |

|

0.4 |

|

|

Fertilizer nutrients |

|

464 |

|

7.0 |

|

384 |

|

6.7 |

|

568 |

|

8.2 |

|

|

Potash |

|

22 |

|

0.3 |

|

23 |

|

0.4 |

|

31 |

|

0.4 |

|

|

Phosphates |

|

363 |

|

5.5 |

|

290 |

|

5.1 |

|

445 |

|

6.4 |

|

|

Nitrogen |

|

60 |

|

0.9 |

|

58 |

|

1.0 |

|

78 |

|

1.1 |

|

|

Others |

|

19 |

|

0.3 |

|

13 |

|

0.2 |

|

14 |

|

0.2 |

|

|

Others |

|

29 |

|

0.4 |

|

24 |

|

0.4 |

|

51 |

|

0.7 |

|

|

Total |

|

6,626 |

|

100.0 |

|

5,719 |

|

100.0 |

|

6,965 |

|

100.0 |

|

Costs and expenses increased to US$ 5.287 billion in 2Q16 from the US$ 4.565 billion recorded in 1Q16, representing an increase of 15.8%, mainly due to the impact of higher sales volumes (US$ 457 million) and exchange rate variations (US$ 283 million), partially offset by cost reduction initiatives (US$ 165 million).

Costs and expenses

|

US$ million |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Costs |

|

4,795 |

|

4,249 |

|

5,186 |

|

|

Expenses |

|

492 |

|

316 |

|

739 |

|

|

Total costs and expenses |

|

5,287 |

|

4,565 |

|

5,925 |

|

|

Depreciation |

|

927 |

|

850 |

|

988 |

|

|

Costs and expenses ex-depreciation |

|

4,360 |

|

3,715 |

|

4,937 |

|

COST OF GOODS SOLD (COGS)

COGS totaled US$ 4.795 billion(7) in 2Q16, increasing US$ 546 million from the US$ 4.249 billion recorded in 1Q16, as a result of higher sales volumes (US$ 457 million) and exchange rate variations (US$ 254 million), which were partially offset by cost reduction initiatives (US$ 165 million).

COGS totaled US$ 9.044 billion in 1H16, decreasing US$ 1.310 billion from the US$ 10.354 billion recorded in 1H15, despite the increase in volumes in most of the business segments.

Further details on cost performance are provided in the “Performance of the Business Segments” section.

COGS by business segment

|

US$ million |

|

2Q16 |

|

% |

|

1Q16 |

|

% |

|

2Q15 |

|

% |

|

|

Ferrous minerals |

|

2,579 |

|

53.8 |

|

2,169 |

|

51.1 |

|

3,035 |

|

58.5 |

|

|

Base metals |

|

1,424 |

|

29.7 |

|

1,346 |

|

31.7 |

|

1,442 |

|

27.8 |

|

|

Coal |

|

250 |

|

5.2 |

|

325 |

|

7.6 |

|

233 |

|

4.5 |

|

|

Fertilizers |

|

482 |

|

10.1 |

|

360 |

|

8.5 |

|

441 |

|

8.5 |

|

|

Other products |

|

60 |

|

1.2 |

|

49 |

|

1.2 |

|

35 |

|

0.7 |

|

|

Total COGS |

|

4,795 |

|

100.00 |

|

4,249 |

|

100.0 |

|

5,186 |

|

100.0 |

|

|

Depreciation |

|

866 |

|

|

|

810 |

|

|

|

882 |

|

|

|

|

COGS, ex-depreciation |

|

3,929 |

|

|

|

3,439 |

|

|

|

4,304 |

|

|

|

(7) COGS currency exposure in 2Q16 was as follows: 53% Brazilian Reais, 29% US dollar, 14% Canadian dollar, 3% Euros and 1% other currencies.

EXPENSES

Total expenses increased 55.7% to US$ 492 million in 2Q16 from the US$ 316 million recorded in 1Q16, due to the increase in other expenses (US$ 125 million), SG&A (US$ 21 million), R&D (US$ 18 million), and pre-operating and stoppage expenses (US$ 12 million).

SG&A totaled US$ 140 million in 2Q16, representing a 17.6% increase from the US$ 119 million recorded in 1Q16, and an 11.9% decrease from the US$ 159 million recorded in 2Q15. SG&A, net of depreciation, increased by US$ 11 million in 2Q16 vs. 1Q16, mainly as a result of the impact of: (i) exchange rate variations (US$ 6 million); (ii) higher personnel expenses (US$ 3 million); (iii) higher selling expenses (US$ 2 million) and (iv) higher services expenses (US$ 1 million).

R&D expenses totaled US$ 78 million in 2Q16, representing a 30.0% increase from the US$ 60 million recorded in 1Q16 and a 33.9% decrease from the US$ 118 million recorded in 2Q15. R&D expenses stem mostly from nickel (US$ 21 million) and iron ore and pellets (US$ 20 million).

Pre-operating and stoppage expenses totaled US$ 114 million in 2Q16, representing an 11.8% increase from the US$ 102 million recorded in 1Q16 mainly driven by the Nacala Logistic Corridor and the S11D project expenses. Pre-operating and stoppage expenses decreased 56.0% from the US$ 259 million recorded in 2Q15.

Other operating expenses totaled US$ 160 million in 2Q16, increasing US$ 125 million in comparison with the US$ 35 million recorded in 1Q16, mainly due to contingencies increase (US$ 32 million), higher disposals and write-off of assets (US$ 21 million), and insurance claims and externalities (US$ 13 million). Other expenses decreased US$ 43 million vs. 2Q15.

Total expenses decreased to US$ 808 million in 1H16, from the US$ 1.271 billion recorded in 1H15. After deducting the positive one-off effect of US$ 230 million from the goldstream transaction recorded in 1Q15, expenses decreased 46.2%.

Expenses

|

US$ million |

|

2Q16 |

|

% |

|

1Q16 |

|

% |

|

2Q15 |

|

% |

|

|

SG&A ex-depreciation |

|

107 |

|

— |

|

96 |

|

— |

|

125 |

|

— |

|

|

SG&A |

|

140 |

|

28 |

|

119 |

|

38 |

|

159 |

|

22 |

|

|

Administrative |

|

126 |

|

26 |

|

107 |

|

34 |

|

151 |

|

20 |

|

|

Personnel |

|

58 |

|

12 |

|

51 |

|

16 |

|

74 |

|

10 |

|

|

Services |

|

18 |

|

4 |

|

16 |

|

5 |

|

26 |

|

4 |

|

|

Depreciation |

|

33 |

|

7 |

|

23 |

|

7 |

|

34 |

|

5 |

|

|

Others |

|

17 |

|

3 |

|

17 |

|

5 |

|

17 |

|

2 |

|

|

Selling |

|

14 |

|

3 |

|

12 |

|

4 |

|

8 |

|

1 |

|

|

R&D |

|

78 |

|

16 |

|

60 |

|

19 |

|

118 |

|

16 |

|

|

Pre-operating and stoppage expenses (1) |

|

114 |

|

23 |

|

102 |

|

32 |

|

259 |

|

35 |

|

|

VNC |

|

— |

|

— |

|

— |

|

— |

|

116 |

|

16 |

|

|

Long Harbour |

|

45 |

|

9 |

|

49 |

|

16 |

|

68 |

|

9 |

|

|

S11D |

|

19 |

|

4 |

|

15 |

|

5 |

|

14 |

|

2 |

|

|

Moatize |

|

9 |

|

2 |

|

1 |

|

— |

|

11 |

|

1 |

|

|

Others |

|

41 |

|

8 |

|

37 |

|

12 |

|

50 |

|

7 |

|

|

Other operating expenses |

|

160 |

|

33 |

|

35 |

|

11 |

|

203 |

|

27 |

|

|

Total Expenses |

|

492 |

|

100 |

|

316 |

|

100 |

|

739 |

|

100 |

|

|

Depreciation |

|

61 |

|

— |

|

40 |

|

— |

|

106 |

|

— |

|

|

Expenses ex-depreciation |

|

431 |

|

— |

|

276 |

|

— |

|

633 |

|

— |

|

(1) Includes US$ 29 million of depreciation charges in 2Q16, US$ 26 million in 1Q16 and US$ 72 million in 2Q15

Adjusted earnings before interest, taxes, depreciation and amortization(8)

Adjusted EBITDA was US$ 2.383 billion in 2Q16, 18.9% higher than in 1Q16 mainly as a result of the improvement in the Ferrous Minerals EBITDA (US$ 398 million). Adjusted EBITDA margin was 36.0% in 2Q16, improving from the 35.1% recorded in 1Q16.

Adjusted EBIT was US$ 1.339 billion in 2Q16, 16.0% higher than in 1Q16.

Adjusted EBITDA

|

US$ million |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Net operating revenues |

|

6,626 |

|

5,719 |

|

6,965 |

|

|

COGS |

|

(4,795 |

) |

(4,249 |

) |

(5,186 |

) |

|

SG&A |

|

(140 |

) |

(119 |

) |

(159 |

) |

|

Research and development |

|

(78 |

) |

(60 |

) |

(118 |

) |

|

Pre-operating and stoppage expenses |

|

(114 |

) |

(102 |

) |

(259 |

) |

|

Other operational expenses |

|

(160 |

) |

(35 |

) |

(203 |

) |

|

Adjusted EBIT |

|

1,339 |

|

1,154 |

|

1,040 |

|

|

Depreciation, amortization & depletion |

|

927 |

|

850 |

|

988 |

|

|

Dividends received |

|

117 |

|

1 |

|

185 |

|

|

Adjusted EBITDA |

|

2,383 |

|

2,005 |

|

2,213 |

|

Adjusted EBITDA by business area

|

US$ million |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Ferrous minerals |

|

2,136 |

|

1,738 |

|

1,811 |

|

|

Coal |

|

(110 |

) |

(93 |

) |

(102 |

) |

|

Base metals |

|

376 |

|

329 |

|

406 |

|

|

Fertilizer nutrients |

|

32 |

|

70 |

|

163 |

|

|

Others |

|

(51 |

) |

(39 |

) |

(65 |

) |

|

Total |

|

2,383 |

|

2,005 |

|

2,213 |

|

(8) Net revenues less costs and expenses net of depreciation plus dividends received.

Net income totaled US$ 1.106 billion in 2Q16 vs. US$ 1.776 billion in 1Q16. The US$ 670 million decrease was mostly driven by a Samarco related provision (US$ 1.038 billion), which was partly offset by the improvement in the EBITDA in 2Q16 vs. 1Q16 (US$ 378 million).

Underlying earnings (after adjusting for one-off effects) were US$ 709 million in 2Q16, mainly after the adjustments for: (i) exchange rate variation (US$ 1.960 billion); (ii) Samarco related provisions (US$ 1.038 billion) and currencies and interest rate swaps (US$ 483 million).

For more information on the Samarco related provision, please see the section “Update on Samarco Mineração S.A.” of this release.

Underlying earnings

|

US$ million |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Underlying earnings |

|

709 |

|

514 |

|

973 |

|

|

Items excluded from basic earnings |

|

|

|

|

|

|

|

|

Gain (loss) on fair value on non-current assets |

|

(66 |

) |

— |

|

(55 |

) |

|

Shareholders Debentures |

|

(86 |

) |

(116 |

) |

361 |

|

|

Foreign Exchange |

|

1,960 |

|

1,611 |

|

521 |

|

|

Monetary variation |

|

(51 |

) |

(56 |

) |

(39 |

) |

|

Currency and interest rate swaps |

|

483 |

|

486 |

|

243 |

|

|

Fair value on financial instruments |

|

(31 |

) |

(13 |

) |

(18 |

) |

|

Gain (loss) on sale of investments |

|

— |

|

— |

|

79 |

|

|

Other provisions for losses on investments |

|

(1,038 |

) |

— |

|

— |

|

|

Income tax over excluded items |

|

(774 |

) |

(650 |

) |

(390 |

) |

|

Net Income (loss) |

|

1,106 |

|

1,776 |

|

1,675 |

|

Net financial results showed a gain of US$ 2.091 billion vs. a gain of US$ 1.425 billion in 1Q16. The main components of the 2Q16 net financial results are: (i) financial expenses (-US$ 611 million); (ii) financial revenues (US$ 34 million); (iii) foreign exchange and monetary gains (US$ 1.909 billion); (iv) currency and interest rate swap gains (US$ 483 million); and (v) gains on other derivatives (US$ 276 million), composed mainly of bunker oil derivatives gains of US$ 148 million.

Financial results

|

US$ million |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Financial expenses |

|

(611 |

) |

(630 |

) |

(215 |

) |

|

Gross interest |

|

(452 |

) |

(412 |

) |

(405 |

) |

|

Capitalization of interest |

|

213 |

|

177 |

|

177 |

|

|

Tax and labour contingencies |

|

— |

|

(21 |

) |

(17 |

) |

|

Shareholder debentures |

|

(86 |

) |

(116 |

) |

361 |

|

|

Others |

|

(157 |

) |

(144 |

) |

(187 |

) |

|

Financial expenses (REFIS) |

|

(129 |

) |

(114 |

) |

(144 |

) |

|

Financial income |

|

34 |

|

60 |

|

30 |

|

|

Derivatives(1) |

|

759 |

|

440 |

|

235 |

|

|

Currency and interest rate swaps |

|

483 |

|

486 |

|

243 |

|

|

Others(2) (bunker oil, commodities, etc) |

|

276 |

|

(46 |

) |

(8 |

) |

|

Foreign Exchange |

|

1,960 |

|

1,611 |

|

521 |

|

|

Monetary variation |

|

(51 |

) |

(56 |

) |

(39 |

) |

|

Financial result, net |

|

2,091 |

|

1,425 |

|

532 |

|

(1) The net derivatives gains of US$ 759 million in 2Q16 are comprised of settlement losses of US$ 353 million and market-to-market gains of US$ 1.112 billion.

(2) Other derivatives includes mainly bunker oil derivatives gains of US$ 148 million

Equity income from affiliated companies

Equity income from affiliated companies was US$ 190 million in 2Q16 vs. US$ 156 million in 1Q16. The main contributors to equity income were CSP (US$ 116 million), VLI (US$ 21 million) and Aliança Geração Energia (US$ 18 million).

THE IMPACT OF BUNKER OIL HEDGING ON VALE’S FINANCIAL PERFORMANCE

Vale’s financial performance has been impacted by the bunker oil hedge previously contracted. The outstanding bunker oil hedge position is marked-to-market and recorded as financial results, as a proxy for future cash flow. The outstanding hedge position will be settled at the end of 2016(9).

The impact on the financial statements can be summarized as follows:

(i) In 2Q16: a positive impact of US$ 148 million recognized in 2Q16 as financial results due to the net position of: (i) the positive impact of the mark-to-market of the open positions on June 30th, 2016; and (ii) the negative impact of the realized loss on the settlements which occurred in the quarter.

(ii) In 3Q16 and 4Q16: financial results will be impacted by the changes in the mark-to-market of the outstanding derivative position at the end of each quarter and by the gains or losses related to the settlements recorded in each quarter.

(9) Costs are no longer impacted in 2016, since all outstanding bunker oil hedge position recorded under hedge accounting program was settled up to 4Q15.

(iii) In 1Q17 and subsequent quarters: financial results will no longer be impacted since all outstanding bunker oil hedge position will be settled up to 4Q16.

Impact of bunker oil hedging on Vale’s financial performance

|

|

|

Concept |

|

Current |

|

Drivers of future impact |

| ||||||

|

Freight |

|

Hedge |

|

Impact of |

|

Impact incurred |

|

Type of |

|

Bunker oil derivative |

|

Average strike |

|

|

FOB |

|

No |

|

Impact on financial results |

|

US$ 148 million increase in financial results |

|

Forward |

|

705 |

|

511 |

|

|

|

|

|

|

Zero Cost Collar |

|

1,080 |

|

300 - 380 |

| ||||

EFFECTS OF CURRENCY PRICE VOLATILITY ON VALE’S FINANCIAL PERFORMANCE

In 2Q16, from end to end, the Brazilian Real (BRL) appreciated 9.8% against the US Dollar (USD) from BRL 3.56/ USD as of March 31st, 2016 to BRL 3.21/ USD as of June 30th, 2016. On a quarterly average, the BRL appreciated 10.1%, from an average BRL 3.90/ USD in 1Q16 to an average BRL 3.51/ USD in 2Q16.

The end-to-end appreciation of the BRL against the USD and other currencies caused mainly non-cash gains of US$ 2.443 billion on our earnings before taxes in 2Q16, driven by its impact on:

· The net position of the USD and other currency denominated liabilities and the USD and other currency denominated assets (accounts receivable and others) — which amounted to a gain of US$ 1.960 billion in 2Q16, recorded in the financial statements as “Foreign exchange”.

· The changes in fair value and the settlements of the currency swaps from the BRL and other currencies to the USD, which caused one-off gains of US$ 483 million.

The BRL appreciation on a quarterly average brought negative impacts to Vale’s cash flows. In 2Q16 most of our revenues were denominated in USD, while our COGS were 53% denominated in BRL, 29% in USD and 14% in Canadian dollars (CAD) and about 60% of our capital expenditures were denominated in BRL. The appreciation of the BRL and of other currencies in 2Q16 increased our costs and expenses by US$ 283 million.

Update on Samarco Mineração S.A. (Samarco)

Historical Events

Following the Samarco dam failure on November 5th, 2015, the Brazilian mining authority (DNPM) and the State Department for Environment and Sustainable Development of Minas Gerais (SEMAD) ordered the suspension of Samarco’s operations.

On March 2nd, 2016, Samarco and its shareholders, Vale and BHP Billiton Brasil Ltda. (BHPB), entered into an agreement in connection with the R$ 20.2 billion lawsuit (Agreement) with the Federal Government, the States of Espírito Santo and Minas Gerais and other governmental authorities (Brazilian Authorities) for the implementation of remediation and compensation programs for the areas and communities impacted by the Samarco dam failure. The Agreement does not establish assumption of civil, criminal or administrative responsibilities related to Samarco dam failure.

Under the Agreement, Samarco, Vale and BHPB agreed to establish a Foundation to develop and execute the abovementioned programs, to be funded by Samarco as follows: R$ 2.0 billion (US$ 623 million) in 2016, R$ 1.2 billion (US$ 374 million) in 2017 and R$ 1.2 billion (US$ 374 million) in 2018. Amounts that Samarco already spent on remediation and compensation will be deducted from its funding obligations. From 2019 to 2021, annual contributions to the Foundation will range from R$ 800 million (US$ 249 million) to R$ 1.6 billion (US$ 498 million), and will be set based on the programs approved for each year. From 2022 onwards, Samarco will provide the necessary funds in order to complete the remaining remediation and compensation programs approved for each relevant year. The Foundation will allocate an annual amount of R$ 240 million (US$ 75 million) for a period of 15 years to implement the compensation and remediation programs, with these annual amounts already included in the abovementioned annual contributions for the first six years. Through the end of 2018, the Foundation will also set aside R$ 500 million (US$ 156 million) for basic sanitation programs in the affected areas, as follows: R$ 50 million in 2016, R$ 200 million in 2017 and R$ 250 million in 2018.

The term of the Agreement is 15 years, renewable for successive one-year periods until all its obligations have been fulfilled.

Under the terms of the Agreement, in the event of Samarco not meeting its funding obligations with the Foundation, both Vale and BHPB will provide funds to the Foundation in proportion to their current shareholding stakes in Samarco (50%).

On June 28th, 2016, the Foundation was established by Samarco and its shareholders, with commencement date planned for August 1st, 2016.

The Agreement is already effective among the parties, though its judicial ratification is suspended. There is no assurance as to whether or when the court will ratify the Agreement. Vale understands that the Agreement establishes effective long-term programs to remediate and compensate for the impacts of the Samarco dam failure.

Potential resumption of Samarco’s operation

Samarco is currently unable to conduct its mining and processing activities. On June 23, 2016, Samarco filed the Environmental Impact Study and the Environment Impact Report (EIA / RIMA) in the State Department for Environment and Sustainable Development of Minas Gerais (SEMAD). These studies are part of the licensing process for the use of exhausted pits for tailings disposal.

Given the current status of the licensing process, Samarco cannot make a reliable estimation of how and when its operations will be resumed. Nonetheless, Samarco’s current assessment is that the probability of resuming operations in 2016 is highly unlikely.

Samarco’s free cash flow projection and its impact on Vale’s Financial Statements

Due to the reduced likelihood of resuming operations in 2016 changed substantially Samarco’s future cash flow projections. Nonetheless, Samarco and its shareholders still expect Samarco to generate a significant portion of the funds required to meet its obligations as per the Agreement.

Due to current uncertainties on the licensing process, Vale provisioned an amount of R$ 3.733 billion (US$ 1.163 billion), equivalent to the present value of its estimated secondary responsibility under the Agreement, in its interim financial statements as of June 30 2016 under “Other results in associates and joint ventures”. Given Samarco’s current cash flow projections, it is likely that its shareholders will be called upon to fulfill its obligations under the Agreement and, therefore, Vale expects to contribute about US$ 150 million to the Foundation in 2H16, with this amount offset against the abovementioned R$ 3.7 billion provision.

In addition, Vale intends to make available short-term facilities of up to US$ 100 million to Samarco to support its operations, without undertaking an obligation to Samarco. Funds will be released on an as-needed basis and will be subject to Samarco achieving certain milestones. Likewise, BHPB will make available similar short-term facilities.

Vale will carry out frequent reassessment of the key assumptions used by Samarco and revise the abovementioned provision in a timely manner to reflect new facts and circumstances in its financial statements.

Contingencies related to Samarco dam failure

Vale and certain of its officers have been named as defendants in putative securities class action suits in federal court in New York brought by holders of Vale’s American Depositary Receipts under U.S. federal securities laws. The lawsuits allege that Vale made false and misleading statements or omitted to make disclosures concerning the risks and dangers of the operations of Samarco’s Fundão dam and the adequacy of its related programs and procedures. The plaintiffs have not specified an amount of alleged damages in these actions. Vale intends to vigorously mount a full defense against the allegations.

On May 3, 2016, the Federal Prosecution Office filed a public civil action against Samarco and its shareholders, presenting several demands such as the: (i) adoption of measures for mitigating the social, economic and environmental impacts resulting from the Fundão dam failure and other emergency measures; (ii) payment of compensation to the community; and (iii) payment for collective moral damage. The initial action value claimed by the Federal Prosecution Office is R$ 155 billion (US$ 48 billion).

In addition, Samarco and its shareholders were named as a defendant in several other lawsuits brought by individuals, corporations and governmental entities seeking damages for material or personnel damages.

All lawsuits and petitions are at very early stages, thus it is not possible to determine a range of outcomes and/or reliable estimates of the potential exposure at this time. No contingent liability was quantified and no provision was recognized.

Capital expenditures totaled US$ 1.368 billion in 2Q16 with US$ 905 million in project execution and US$ 463 million in sustaining capital. Capital expenditures decreased US$ 81 million vs. the U$ 1.449 billion spent in 1Q16.

Project Execution and Sustaining by business area

|

US$ million |

|

2Q16 |

|

% |

|

1Q16 |

|

% |

|

2Q15 |

|

% |

|

|

Ferrous minerals |

|

767 |

|

56.1 |

|

917 |

|

63.3 |

|

1,277 |

|

60.3 |

|

|

Coal |

|

159 |

|

11.6 |

|

133 |

|

9.1 |

|

389 |

|

18.3 |

|

|

Base metals |

|

232 |

|

17.0 |

|

269 |

|

18.6 |

|

372 |

|

17.5 |

|

|

Fertilizer nutrients |

|

68 |

|

4.9 |

|

39 |

|

2.7 |

|

49 |

|

2.3 |

|

|

Power generation |

|

16 |

|

1.2 |

|

26 |

|

1.8 |

|

24 |

|

1.1 |

|

|

Steel |

|

126 |

|

9.2 |

|

65 |

|

4.5 |

|

6 |

|

0.3 |

|

|

Others |

|

— |

|

— |

|

— |

|

— |

|

1 |

|

— |

|

|

Total |

|

1,368 |

|

100.0 |

|

1,449 |

|

100.0 |

|

2,119 |

|

100.0 |

|

Evolution of capital expenditures

(US$ million)

Project execution

The Ferrous Minerals and the Coal business segments accounted for about 67% and 16%, respectively, of the total investment in project execution in 2Q16. CSP accounted for 14% of the project execution capex.

Project execution by business area

|

US$ million |

|

2Q16 |

|

% |

|

1Q16 |

|

% |

|

2Q15 |

|

% |

|

|

Ferrous minerals |

|

608 |

|

67.1 |

|

701 |

|

76.2 |

|

1,001 |

|

69.9 |

|

|

Coal |

|

140 |

|

15.5 |

|

118 |

|

12.9 |

|

384 |

|

26.8 |

|

|

Base metals |

|

1 |

|

0.1 |

|

2 |

|

0.3 |

|

11 |

|

0.8 |

|

|

Fertilizer nutrients |

|

14 |

|

1.6 |

|

7 |

|

0.8 |

|

7 |

|

0.5 |

|

|

Power generation |

|

16 |

|

1.7 |

|

26 |

|

2.8 |

|

24 |

|

1.7 |

|

|

Steel |

|

126 |

|

13.9 |

|

65 |

|

7.1 |

|

6 |

|

0.4 |

|

|

Total |

|

905 |

|

100.0 |

|

920 |

|

100.0 |

|

1,434 |

|

100.0 |

|

FERROUS MINERALS

About 89% of the US$ 608 million invested in Ferrous Minerals in 2Q16 relates to the S11D project and the expansion of its associated infrastructure (US$ 540 million).

S11D Plant — Screening, crushing and patios

S11D (including mine, plant and associated logistics — CLN S11D) achieved combined physical progress of 79% in 2Q16 with 90% progress at the mine site and 70% at the logistic infrastructure sites. The duplication of the railway reached 54% physical progress with 243 Km delivered. The railway spur reached 92% physical progress and the on-shore port started up.

S11D Logistics — Port offshore

COAL

Investments in the Moatize II project totaled US$ 37 million in 2Q16. Moatize II showed physical progress of 99% in 2Q16 with the hot commissioning of the handling system being completed. Start-up is expected by early August.

Description and status of main projects

|

Project |

|

Description |

|

Capacity |

|

Status |

|

Ferrous Minerals projects |

|

|

|

|

|

|

|

Carajás Serra Sul S11D |

|

· Development of a mine and processing plant, located in the Southern range of Carajás, Pará, Brazil. |

|

90 |

|

· Cold commissioning on the mine site initiated

· Cold commissioning of the long distance conveyor belt and plant in progress

· Delivery of the electrocenters of the mine 79% completed

· Pre stripping of Systems 3 and 4 concluded |

|

CLN S11D |

|

· Duplication of 570 km railway, with construction of rail spur of 101 km. Acquisition of wagons, locomotives, and onshore and offshore expansions at PDM maritime terminal. |

|

(80) |

(a) |

· Duplication of the railway reached 54% physical progress, totaling 243 Km delivered

· Railway spur connection to EFC Railway concluded

· Onshore port start up initiated

·Offshore expansion achieved 89% physical progress |

|

Coal Projects |

|

|

|

|

|

|

|

Moatize II |

|

· New pit and duplication of the Moatize CHPP, as well as of all related infrastructure in Tete, Mozambique. |

|

11 |

|

· Hot commissioning of the handling system ongoing |

(a) Net additional capacity

Progress indicators(10)

|

|

|

Capacity |

|

Estimated |

|

Executed capex |

|

Estimated capex |

|

Physical |

| ||||

|

Project |

|

(Mtpy) |

|

start-up |

|

2016 |

|

Total |

|

2016 |

|

Total |

|

progress |

|

|

Ferrous minerals projects |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Carajás Serra Sul S11D |

|

90 |

|

2H16 |

|

495 |

|

4,908 |

|

890 |

|

6,405 |

(b) |

90 |

% |

|

CLN S11D |

|

230 (80 |

)(a) |

1H14 to 2H18 |

|

682 |

|

4,851 |

|

1,154 |

|

7,850 |

(c) |

70 |

% |

|

Coal projects |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Moatize II |

|

11 |

|

2H16 |

|

66 |

|

1,971 |

|

134 |

(d) |

2,068 |

(e) |

99 |

% |

(a) Net additional capacity.

(b) Original capex budget of US$ 8.089 billion.

(c) Original capex budget of US$ 11.582 billion .

(d) There was an increase of US$ 29 million in the 2016 budget.

(e) Original capex of U$ 2.068 billion plus US$ 0.45 billion of rolling stock.

(10) Pre-operating expenses were not included in the estimated capex for the year, although included in the total estimated capex column, in line with Vale’s Board of Directors approvals. Estimated capex for the year is only reviewed once a year.

CSP, Vale’s co-investment in partnership with Dongkuk and Posco in a steel slab plant project with nominal capacity of 3.0 Mtpy(11), started its ramp-up in 2Q16. Vale’s share of the total executed capex is US$ 1.241 billion, with US$ 123 million spent in 2Q16 and no further capital will be disbursement expected from shareholders. Vale will deliver all iron ore required for CSP steel production.

Sustaining capex

Sustaining capital decreased from US$ 529 million in 1Q16 to US$ 463 million in 2Q16. The Base Metals and Ferrous Minerals business segment accounted for 50% and 34%, respectively, of the total sustaining capex in 2Q16.

Sustaining capital for the Ferrous Minerals business segment included, among others: (i) the replacement and acquisition of new equipment (US$ 90 million), (ii) operational enhancements (US$ 20 million); (iii) improvement in the current standards of health and safety and environmental protection (US$ 19 million), (iv) maintenance, improvement and expansion of tailing dams (US$ 16 million). Maintenance of railways and ports in Brazil and Malaysia accounted for US$ 58 million.

Sustaining investments in iron ore fines (excluding sustaining investments in pellets plants) amounted to US$ 122 million, equivalent to US$ 1.8/dmt of iron ore fines in 2Q16, representing a 41% decrease vs. the US$ 2.9/dmt in 1Q16, due to: (i) the carryover of payments from 4Q15, which impacted 1Q16; (ii) the shape of the disbursement curve of sustaining investments, which is concentrated in the second half of the year; and (iii) the dilution of investments due to higher volumes. Sustaining investments for Pellets totaled US$ 32 million, equivalent to US$ 2.9/dmt.

Sustaining capex in the Base Metals business segment was mainly dedicated to: (i) operational enhancement (US$ 144 million), (ii) improvement in the current standards of health and safety and environmental protection (US$ 61 million); (iii) replacement and acquisition of new equipment (US$ 18 million), (iv) maintenance improvements and expansion of tailing dams (US$ 6 million).

Base Metals sustaining capex includes the ongoing investments in the Sudbury smelting unit to reduce SO2 and particulate emissions, the Clean AER project.

(11) Vale’s attributable capacity of 1.5 Mtpy.

Sustaining capex by type - 2Q16

|

US$ million |

|

Ferrous |

|

Coal |

|

Base |

|

Fertilizer |

|

TOTAL |

|

|

Operations |

|

113 |

|

13 |

|

162 |

|

33 |

|

321 |

|

|

Waste dumps and tailing dams |

|

16 |

|

1 |

|

6 |

|

5 |

|

28 |

|

|

Health and Safety |

|

15 |

|

4 |

|

14 |

|

2 |

|

35 |

|

|

CSR - Corporate Social Responsibility |

|

5 |

|

— |

|

47 |

|

11 |

|

63 |

|

|

Administrative & Others |

|

10 |

|

1 |

|

2 |

|

3 |

|

16 |

|

|

Total |

|

159 |

|

19 |

|

231 |

|

54 |

|

463 |

|

Sustaining capex by business area

|

US$ million |

|

2Q16 |

|

% |

|

1Q16 |

|

% |

|

2Q15 |

|

% |

|

|

Ferrous minerals |

|

159 |

|

34.4 |

|

216 |

|

40.7 |

|

276 |

|

40.3 |

|

|

Coal |

|

19 |

|

4.0 |

|

14 |

|

2.7 |

|

4 |

|

0.6 |

|

|

Base metals |

|

231 |

|

50.0 |

|

267 |

|

50.5 |

|

361 |

|

52.7 |

|

|

Fertilizer nutrients |

|

54 |

|

11.6 |

|

32 |

|

6.0 |

|

42 |

|

6.2 |

|

|

Power generation |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

|

Others |

|

— |

|

— |

|

— |

|

0.1 |

|

1 |

|

0.1 |

|

|

Total |

|

463 |

|

100.00 |

|

529 |

|

100.0 |

|

685 |

|

100.0 |

|

Corporate social responsibility

Investments in corporate social responsibility totaled US$ 75 million in 2Q16, of which US$ 51 million dedicated to environmental protection and conservation and US$ 24 million dedicated to social projects.

Portfolio Management

Three very large ore carriers of 400,000 deadweight tons were sold to ICBC Financial Leasing in 2Q16 for US$ 269 million with sales proceeds expected by August 2016.

Free cash flow was US$ 761 million in 2Q16.

Cash generated from operations was US$ 3.115 billion in 2Q16, with non-operational uses of cash flow stemming mainly from: (i) interest on loans (US$ 362 million); (ii) income taxes and REFIS installments (US$ 213 million); (iii) settlement of derivatives in the quarter (US$ 353 million), of which US$ 294 million related to bunker oil; and (iv) investments (US$ 1.232 billion).

Net additions and repayments of loans were negative US$ 375 million, with debt repayments exceeding debt additions in 2Q16.

Free Cash Flow

US$ million

Gross debt totaled US$ 31.814 billion as of June 30th, 2016, increasing slightly from the US$ 31.470 billion as of March 31st, 2016, mainly as a result of the impact of appreciation of the BRL(12) on the translation of BRL denominated debt into USD. The exchange rate impact was partially offset by net debt repayments(13) of US$ 375 million in 2Q16.

On June 7th, 2016 Vale issued, through its wholly owned subsidiary Vale Overseas Limited, US$ 1.250 billion of Guaranteed Notes due in 2021 bearing a coupon of 5.875% per annum. On June 20th, 2016 Vale repaid US$ 1.000 billion of the US$ 3.000 billion disbursed from its Revolving Credit Lines in January 2016.

Net debt decreased by US$ 153 million compared to the end of the previous quarter, totaling US$ 27.508 billion based on a cash position of US$ 4.306 billion as of June 30th, 2016. The decrease in net debt was mainly driven by the positive free cash flow of US$ 761 million in 2Q16, and was partially offset by the impact of the exchange rate on the translation of BRL denominated debt into USD.

Debt position

Gross debt after currency and interest rates swaps was 90% denominated in USD, being 31% based on floating and 69% based on fixed interest rates as of June 30th, 2016.

(12) In 2Q16, from end to end, the BRL appreciated 9.8% against the USD.

(13) Debt repayments less debt additions.

Average debt maturity was 7.6 years and average cost of debt, after the above-mentioned currency and interest rates swaps, increased to 4.23% per annum on June 30th, 2016, against 4.03% per annum on March 31st, 2016. The increase of the average cost of debt was mainly driven by the partial repayment of the Revolving Credit Lines which have a cost of debt lower than Vale’s average.

Interest coverage, measured by the ratio of the LTM(14) adjusted EBITDA to LTM interest payment, remained practically stable at 5.1x in 2Q16 vs. 5.2x in 1Q16.

Gross debt to LTM adjusted EBITDA remained stable at 4.2x as of June 30th, 2016 compared to March 31st, 2016.

Debt indicators

|

US$ million |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Total debt |

|

31,814 |

|

31,470 |

|

29,773 |

|

|

Net debt |

|

27,508 |

|

27,661 |

|

26,509 |

|

|

Total debt / adjusted LTM EBITDA (x) |

|

4.2 |

|

4.2 |

|

3.3 |

|

|

Adjusted LTM EBITDA / LTM interest expenses (x) |

|

5.1 |

|

5.2 |

|

5.9 |

|

(14) Last twelve months.

Performance of the business segments

The Ferrous Minerals business segment accounted for 89.6% of Vale’s adjusted EBITDA in 2Q16, followed by 15.8% from the Base Metals business segment, 1.3% from the Fertilizers business segment, -4.6% from the Coal business segment and -2.1% from Others.

Segment information — 2Q16, as per note of financial statements

|

|

|

|

|

|

|

Expenses |

|

|

|

|

| ||||

|

US$ million |

|

Net |

|

Cost(1) |

|

SG&A and |

|

R&D |

|

Pre operating |

|

Dividends |

|

Adjusted |

|

|

Ferrous minerals |

|

4,541 |

|

(2,228 |

) |

(171 |

) |

(20 |

) |

(46 |

) |

60 |

|

2,136 |

|

|

Iron ore fines |

|

3,508 |

|

(1,652 |

) |

(150 |

) |

(16 |

) |

(34 |

) |

— |

|

1,656 |

|

|

ROM |

|

5 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

5 |

|

|

Pellets |

|

868 |

|

(459 |

) |

(19 |

) |

(4 |

) |

(9 |

) |

60 |

|

437 |

|

|

Others ferrous |

|

99 |

|

(64 |

) |

(3 |

) |

— |

|

— |

|

— |

|

32 |

|

|

Mn & Alloys |

|

61 |

|

(53 |

) |

1 |

|

— |

|

(3 |

) |

— |

|

6 |

|

|

Coal |

|

145 |

|

(237 |

) |

(6 |

) |

(3 |

) |

(9 |

) |

— |

|

(110 |

) |

|

Base metals |

|

1,447 |

|

(1,013 |

) |

(11 |

) |

(22 |

) |

(25 |

) |

— |

|

376 |

|

|

Nickel(3) |

|

1,050 |

|

(776 |

) |

(2 |

) |

(21 |

) |

(25 |

) |

— |

|

226 |

|

|

Copper(4) |

|

397 |

|

(237 |

) |

(9 |

) |

(1 |

) |

— |

|

— |

|

150 |

|

|

Fertilizer nutrients |

|

464 |

|

(396 |

) |

(29 |

) |

(6 |

) |

(4 |

) |

3 |

|

32 |

|

|

Others |

|

29 |

|

(55 |

) |

(52 |

) |

(26 |

) |

— |

|

54 |

|

(51 |

) |

|

Total |

|

6,626 |

|

(3,929 |

) |

(269 |

) |

(78 |

) |

(84 |

) |

117 |

|

2,383 |

|

(1) Excluding depreciation and amortization

(2) Excluding non-recurring effects

(3) Including copper and by products from our nickel operations

(4) Including by products from our copper operations

Adjusted EBITDA of the Ferrous Minerals business segment was US$ 2.136 billion in 2Q16, US$ 325 million higher than in 2Q15, despite the negative impact of lower sales prices (US$ 264 million), which were offset by exchange rate (US$ 203 million), the positive impacts of lower bunker oil prices (US$ 162 million) and real gains in competitiveness (US$ 257 million).

Gains in competitiveness were based mainly on: (i) marketing and commercial initiatives (US$ 68 million); (ii) higher sales volumes (US$ 47 million); and (iii) ongoing cost reduction initiatives(15) (US$ 142 million).

Year-on-year EBITDA variation 2Q16 vs. 2Q15 — Ferrous Minerals business segment

Iron ore

EBITDA

Adjusted EBITDA of iron ore fines was US$ 1.656 billion in 2Q16, 17.5% higher than in 1Q16, mainly as a result of higher sales volumes (US$ 241 million) and higher realized sales prices (US$ 129 million), which were partially offset by the negative impacts of the appreciation of the BRL against the USD (US$ 106 million) and higher costs(16) (US$ 36 million).

(15) Including the positive impact of renegotiations of chartering freight contracts

(16) After excluding the effects of higher volumes and exchange rate variations.

SALES REVENUES AND VOLUME

Net sales revenues of iron ore fines, excluding pellets and Run of Mine (ROM), amounted to US$ 3.508 billion in 2Q16 vs. US$ 2.917 billion in 1Q16, as a result of higher sales volumes (US$ 462 million) and higher iron ore fines sales prices (US$ 129 million) in 2Q16 vs. 1Q16.

Production, including third party purchases and excluding Samarco’s attributable production, reached 86.8 Mt in 2Q16, 9.3 Mt higher than in 1Q16, mainly due to the good performance at the Northern System and weather related seasonality.

Sales volumes of iron ore fines reached 72.7 Mt in 2Q16 vs. 62.7 Mt in 1Q16, 15.9% and 8.1% higher than in 1Q16 and 2Q15, respectively, with iron ore inventory increasing by 1.4 Mt as a result of: (i) production and acquisition of ore from third parties of 86.8 Mt; (ii) deduction of 11.0 Mt of iron ore fines used for the production of pellets; (iii) adjustment of iron ore inventories(17) of 1.3 Mt; (iv) sales of iron ore fines of 72.7 Mt; and (v) deduction of 0.4 Mt of ROM sales.

CFR sales of iron ore fines increased from 43.7 Mt in 1Q16 to 48.0 Mt in 2Q16, representing 66% of all iron ore fines sales volumes in 2Q16 and staying in line with the share of CFR sales in 1Q16. The increase was mainly due to the effects of seasonally higher production volumes in 2Q16.

ROM sales totaled 0.4 Mt in 2Q16, remaining in line with the 0.5 Mt recorded in 1Q16.

Net operating revenue by product

|

US$ million |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Iron ore fines |

|

3,508 |

|

2,917 |

|

3,391 |

|

|

ROM |

|

5 |

|

4 |

|

33 |

|

|

Pellets |

|

868 |

|

753 |

|

972 |

|

|

Manganese & Ferroalloys |

|

61 |

|

47 |

|

53 |

|

|

Others |

|

99 |

|

83 |

|

103 |

|

|

Total |

|

4,541 |

|

3,804 |

|

4,552 |

|

Volume sold

|

‘000 metric tons |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Iron ore fines |

|

72,678 |

|

62,744 |

|

67,230 |

|

|

ROM |

|

405 |

|

520 |

|

4,181 |

|

|

Pellets |

|

11,388 |

|

11,130 |

|

12,231 |

|

|

Manganese ore |

|

354 |

|

515 |

|

385 |

|

|

Ferroalloys |

|

36 |

|

25 |

|

23 |

|

(17) Iron ore inventories are periodically adjusted downwards due to moisture and handling during its processing phases.

REALIZED PRICES

Iron ore sales in 2Q16 were distributed across three pricing systems: (i) 52% based on the current quarter, month and daily spot prices, including provisional price sales that were settled within the quarter; (ii) 34% based on provisional prices with settlement price based on the market price defined on the delivery date, in which case prices had not yet been settled at the end of the quarter; and (iii) 14% linked to past prices (quarter-lagged).

Vale’s CFR dmt reference price for iron ore fines (ex-ROM) increased by US$ 1.6/t from US$ 54.7/t in 1Q16 to US$ 56.3/t in 2Q16, equivalent to a price realization of 101% of the average Platts IODEX 62% of US$ 55.7/t in 2Q16.

Vale’s CFR/FOB wmt price for iron ore fines (ex-ROM) increased by US$ 1.8/t from US$ 46.5/t in 1Q16 to US$ 48.3/t in 2Q16, after adjusting for moisture and the effect of FOB sales, which accounted for 34% of the total sales volumes in 2Q16.

Price realization in 2Q16 was impacted by:

· Provisional prices set at the end of 1Q16 at US$ 51.7/t, which were later adjusted based on the price of delivery in 2Q16, positively impacted prices in 2Q16 by US$ 2.0/t compared to US$ 2.3/t in 1Q16, as a result of the higher realized prices in the beginning of 2Q16.

· Provisional prices set at the end of 2Q16 at US$ 52.7/t vs. the IODEX average of US$ 55.7/t in 2Q16 negatively impacted prices in 2Q16 by US$ 1.0/t compared to a positive impact of US$ 1.5/t in 1Q16.

· Quarter-lagged contracts, priced at US$ 46.4/t based on the average prices for Dec-Jan-Feb negatively impacted prices in 2Q16 by US$ 1.2/t compared to a positive impact of US$ 0.4/t in 1Q16.

Iron ore sales of 24.9 Mt, or 34% of Vale’s sales mix, were recorded under the provisional pricing system, which was set at the end of 2Q16 at US$ 52.7/t. The final prices of these sales and the required adjustment to sales revenues will be determined and recorded in 3Q16.

Price realization — iron ore fines

Average prices

|

US$/ metric ton |

|

2Q16 |

|

1Q16 |

|

2Q15 |

|

|

Iron ore - Metal Bulletin 65% index |

|

59.99 |

|

50.96 |

|

66.02 |

|

|

Iron ore - Platts’s 62% IODEX |

|

55.70 |

|

48.30 |

|

58.45 |

|

|

Iron ore fines CFR reference price (dmt) |

|

56.30 |

|

54.67 |

|

61.50 |

|

|

Iron ore fines CFR/FOB realized price (wmt) |

|

48.30 |

|

46.50 |

|

50.44 |

|

|

ROM |

|

12.35 |

|

8.02 |

|

7.89 |

|

|

Pellets CFR/FOB (wmt) |

|

76.20 |

|

67.65 |

|

79.47 |

|

|

Manganese ore |

|

103.13 |

|

60.56 |

|

82.24 |

|

|

Ferroalloys |

|

690.36 |

|

648.96 |

|

951.61 |

|

COSTS

Costs for iron ore fines amounted to US$ 1.652 billion (or US$ 1.902 billion with depreciation charges) in 2Q16. Costs increased by US$ 36 million vs. 1Q16, after adjustments for the effects of higher sales volumes (US$ 221 million) and exchange rate variations (US$ 86 million). The increase was mainly driven by higher bunker oil prices (US$ 37 million) and royalties (US$ 32 million), which were partly offset by savings in C1 cash costs.

IRON ORE COGS - 1Q16 x 2Q16

|

|

|