Form 6-K ING GROEP NV For: Feb 11

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For 11 February, 2015

Commission File Number 1-14642

ING Groep N.V.

Bijlmerplein 888

1102 MG Amsterdam

The Netherlands

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T rule 101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T rule 101(b)(7): ¨

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ¨ No x

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b).

This Report contains a copy of the following:

The Press Release issued on 11 February, 2015

|

| PRESS RELEASE |

11 February, 2015

|

NG Bank posts 2014 underlying net profit of EUR 3,424 million;

Dividends reinstated with EUR 0.12 per ordinary share

|

•

|

ING Bank full-year 2014 underlying net profit of EUR 3,424 million, up 8.5% from full-year 2013

|

|

•

|

Strong full-year 2014 results reflect higher interest results, strict expense control and lower risk costs

|

|

•

|

4Q14 underlying net result of EUR 548 million reflects redundancy provisions, annual Dutch bank tax and negative CVA/DVA

|

|

•

|

Full-year 2014 underlying return on IFRS-EU equity improved to 9.9%; year-end fully-loaded CET 1 ratio strengthened to 11.4%

|

|

•

|

ING Group full-year 2014 net result EUR 1,251 million (EUR 0.32 per share), including special items and Insurance results

|

|

•

|

4Q14 net result was EUR 1,176 million (EUR 0.30 per share) including results from discontinued operations of NN Group and Voya

|

|

•

|

Significant progress on restructuring in 2014: Dutch State fully repaid, NN Group stake reduced to 68%, Voya stake down to 19%

|

|

•

|

ING reinstates dividend payments on ordinary shares and will propose to pay EUR 0.12 per share at the AGM in May

|

|

•

|

Financial strength enables ING to propose to pay a cash dividend of EUR 470 million, or EUR 0.12 per ordinary share

|

|

•

|

ING intends to pay a minimum of 40% of ING Group’s annual net profits to shareholders, through dividends, effective from 2015

|

CEO STATEMENT

“2014 was an important and successful year for ING,” said Ralph Hamers, CEO of ING Group. “We launched our ‘Think Forward’ strategy, repaid the Dutch State ahead of schedule and moved closer to completing our restructuring plan. We are proud to have solidified our repositioning as a leading European bank and pleased to see that both NN Group and Voya are thriving as standalone companies. Today, I am delighted to announce the reinstatement of dividend payments on ordinary shares with a proposed cash dividend of EUR 0.12 per share.”

“In 2014, ING Bank welcomed over one million new customers and established half a million primary banking relationships. I am grateful for the loyalty of our customers and for the dedication of our employees to deliver a differentiating experience to our customers every day. Following the launch of ‘Think Forward’, our Chief Innovation Officer and Chief Operations Officer have been working together to deliver innovations and service improvements to our customers as quickly as possible. We have already introduced a steady stream of improvements during 2014, the most recent being biometrics technology in Belgium, and are excited about other new projects that will debut this year.”

“ING Bank posted a strong set of full-year 2014 results, despite some headwinds in the fourth quarter. Interest results were robust, risk costs approached normalised levels and our continued vigilance on costs was evident as we invested for the further digitalisation of our banking services in the Netherlands and extended our ongoing transformation programme within Commercial Banking. Our fourth-quarter result was dampened by redundancy provisions related to these actions, the annual Dutch bank tax and negative CVA/ DVA impacts which lowered the underlying result before tax to EUR 783 million. Excluding those items, the underlying result before tax was a strong EUR 1,376 million. ING Bank’s underlying net profit for the full-year 2014 was EUR 3,424 million, up 8.5% from 2013. The improvement was driven by higher interest results, disciplined expense control and lower risk costs, and despite negative CVA/DVA impacts. The full-year underlying return on IFRS-EU equity rose to 9.9% and ING Bank ended the year with a fully-loaded CET1 ratio of 11.4%.”

“Our efforts to support our customers and the economy contributed to strong commercial growth during 2014. The Bank grew net lending by EUR 14.7 billion in 2014, driven by robust growth in our core lending businesses and despite further reductions in the run- off portfolios. Net lending assets in the core businesses grew by EUR 18.5 billion in 2014, or 3.8%, which is in line with our strategy. Total net inflow of funds entrusted amounted to EUR 16.8 billion, demonstrating the strength of our deposit-gathering capabilities.”

“ING has started 2015 with a strong financial position and a clear focus on empowering our growing customer base through outstanding products and customer service. I am optimistic about the prospects for our bank and am confident that we are well positioned to build on our strategic momentum. We remain committed to reaching our Ambition 2017 targets and are pleased that we are able to begin returning capital to our shareholders. Our intention is to pay a minimum of 40% of ING Group’s annual net profits to shareholders, through dividends, with effect from 2015. Furthermore, at the end of each financial year, the Board will recommend whether to return additional capital to shareholders dependent on financial, strategic and regulatory considerations.”

|

Investor enquiries

|

Press enquiries

|

Table of contents

|

|||

|

T: +31 20 576 6396

|

T: +31 20 576 5000

|

Share information

|

2

|

||

|

Economic environment

|

3

|

||||

|

Consolidated results

|

4

|

||||

|

Investor conference call

|

Press conference

|

Segment reporting

|

9

|

||

|

11 February 2015 at 9:00 CET

|

11 February 2015 at 10:30 CET

|

Corporate Line

|

16

|

||

|

+31 20 794 8500 (NL)

|

Bijlmerplein 888, Amsterdam

|

Consolidated balance sheet

|

17

|

||

|

+44 20 7190 1537 (UK)

|

Or via Q&A at +31 20 531 5871 (NL)

|

Risk & Capital management

|

20

|

||

|

+1 480 629 9031 (US)

|

or +44 203 365 3210 (UK)

|

Business & Sustainability highlights

|

24

|

||

|

Live audio webcast at www.ing.com

|

Live audio webcast at www.ing.com

|

Appendix

|

25

|

SHARE INFORMATION

|

Financial calendar

|

Share information

|

||||||||||

| ● |

Publication of 2014 Annual Report ING Groep N.V.: Thursday, 19 March 2015

|

||||||||||

| ● |

Publication results 1Q2015: Thursday, 7 May 2015

|

4Q2014

|

3Q2014

|

2Q2014

|

1Q2014

|

||||||

| ● |

Annual General Meeting: Monday, 11 May 2015

|

Shares (in millions, end of period)

|

|||||||||

| ● |

Publication results 2Q2015: Wednesday, 5 August 2015

|

Total number of shares

|

3,858.9

|

3,858.5

|

3,858.1

|

3,843.8

|

|||||

| ● | Publication results 3Q2015: Wednesday, 4 November 2015 |

Treasury shares

|

4.3

|

2.0

|

7.7

|

4.2

|

|||||

| (These dates are provisional.) |

Shares outstanding

|

3,854.6

|

3,856.5

|

3,850.4

|

3,839.6

|

||||||

|

Average number of shares

|

3,856.2

|

3,854.5

|

3,850.1

|

3,837.4

|

|||||||

|

Listing information

|

Share price (in euros)

|

||||||||||

|

ING ordinary shares are registered shares with a par value of EUR 0.24 per share. The (depositary receipts for) ordinary shares of ING Group are listed on the exchanges of Amsterdam, Brussels and New York (NYSE).

|

End of period

|

10.83

|

11.31

|

10.26

|

10.00

|

||||||

|

High

|

11.78

|

11.95

|

10.83

|

10.93

|

|||||||

|

|

Tickers

|

Security codes

|

Low

|

10.07

|

9.60

|

9.44

|

9.63

|

||||

|

Stock exchanges

|

(Bloomberg, Reuters)

|

(ISIN, SEDOL1)

|

Net result per share (in euros)

|

0.30

|

0.24

|

0.28

|

-0.50

|

||||

|

Euronext Amsterdam

|

INGA NA, ING.AS

|

NL0000303600, 7154182

|

Shareholders' equity per share (end of period, in euros)

|

13.08

|

12.23

|

12.59

|

11.82

|

||||

|

New York Stock Exchange

|

ING US, ING.N

|

US4568371037, 2452643

|

Dividend per share (in euros)

|

0.12

|

n.a.

|

0

|

n.a.

|

||||

|

Price/earnings ratio 1)

|

33.8

|

62.8

|

n.a.

|

n.a.

|

|||||||

|

American Depositary Receipts (ADRs)

|

Price/book ratio

|

0.83

|

0.92

|

0.81

|

0.85

|

||||||

| For questions related to the ING ADR

program, please contact

|

J.P. Morgan Transfer Agent Service

Center

|

1) Four-quarter rolling average.

|

|||||||||

| J.P. Morgan Shareholder Services:

JPMorgan Chase Bank, N.A.

4 New York Plaza, Floor 12

New York, NY 1004

Attention: Depositary Receipts Group

Fax: (+1 212) 552-1950

In the U.S.: (866) JPM-ADRS

Outside the US.: +1 866 576-2377

|

ADR shareholders can contact: JPMorgan Chase Bank N.A.

P.O. Box 64504

St. Paul, MN 55164-0854

In the US: +1 800 990 1135

Outside the US: +1 651 453 2128

e-mail: [email protected]

|

|

|||||||||

|

Or visit J.P. Morgan Depositary Receipts Services. Web: www.adr.com

|

|||||||||||

|

Note for editors

|

|||||||||||

|

For further information on ING, please visit www.ing.com. Frequent news updates can be found in the Newsroom or via the @ING_news Twitter feed. Photos of ING operations, buildings and its executives are available for download at Flickr. Footage (B-roll) of ING is available via videobankonline.com, or can be requested by emailing [email protected]. ING presentations are available at SlideShare. For convenient access to the latest financial information and press releases both online and offline, download the ING Group Investor Relations and Media app for iOS on the Apple Store or for Android on Google Play.

|

|||||||||||

Relative share price performance

1 JANUARY 2014 TO 1 JANUARY 2015

| 2 | ING GROUP PRESS RELEASE 4Q2014 |

ECONOMIC ENVIRONMENT

|

ECONOMIC ACTIVITY

|

CURRENCY MARKETS

|

|

|

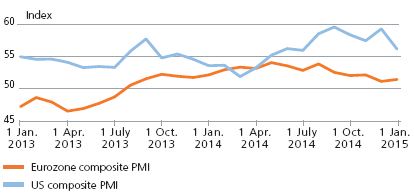

● On balance the composite purchasing managers’ index for the eurozone, weakened somewhat further during the fourth quarter. It still points to growth, albeit very slow growth.

● In the US, the composite PMI also slipped, but remained at levels consistent with reasonably strong economic growth.

● The PMIs are regarded as timely indicators of underlying trends in economic activity.

|

● The weakening trend in the euro’s exchange rate, which started in June (after the ECB cut interest rates and announced a series of TLTROs), extended into the fourth quarter as expectations of further ECB stimulus (i.e. quantitative easing) mounted and the US Federal Reserve hinted at the start of interest rate normalisation in 2015.

|

|

|

|

|

|

INTEREST RATES

|

CREDIT MARKETS

|

|

|

● The slope of the eurozone yield curve flattened sharply in the fourth quarter, as long-term yields tumbled on the back of weak growth, falling inflation and the anticipation of quantitative easing by the ECB. US long-term yields were also dragged lower, leading to a flatter US yield curve.

|

● Credit market sentiment in both the US and the eurozone was little changed in the fourth quarter of 2014. Credit spreads remain at subdued levels.

|

|

|

|

|

| STOCK MARKETS |

CONSUMER CONFIDENCE

|

|

|

● Equity indices resumed their upward trend in the fourth quarter, especially in the US. At the same time, however, equity markets also saw some bouts of volatility related to the sharp drop in oil prices and ongoing geopolitical tensions.

|

● Consumer confidence in the eurozone declined somewhat in the fourth quarter of 2014, but started to rise again at the end of the year. The sharp drop in oil prices is supporting consumer purchasing power.

|

|

|

|

| ING GROUP PRESS RELEASE 4Q2014 | 3 |

CONSOLIDATED RESULTS

|

Consolidated result

|

||||||||

|

4Q2014

|

4Q20131)

|

Change

|

3Q2014

|

Change

|

FY2014

|

FY20131)

|

Change

|

|

|

Profit and loss data (in EUR million)

|

||||||||

|

Interest result

|

3,208

|

2,946

|

8.9%

|

3,156

|

1.6%

|

12,376

|

11,804

|

4.8%

|

|

Commission income

|

556

|

562

|

-1.1%

|

579

|

-4.0%

|

2,290

|

2,244

|

2.0%

|

|

Investment income

|

25

|

64

|

-60.9%

|

37

|

-32.4%

|

206

|

319

|

-35.4%

|

|

Other income

|

-34

|

242

|

171

|

424

|

938

|

-54.8%

|

||

|

Total underlying income

|

3,756

|

3,815

|

-1.5%

|

3,942

|

-4.7%

|

15,296

|

15,305

|

-0.1%

|

|

Staff expenses

|

1,204

|

1,194

|

0.8%

|

1,194

|

0.8%

|

4,844

|

4,863

|

-0.4%

|

|

Other expenses

|

1,339

|

1,125

|

19.0%

|

921

|

45.4%

|

4,047

|

3,695

|

9.5%

|

|

Intangibles, amortisation and impairments

|

29

|

32

|

-9.4%

|

19

|

52.6%

|

88

|

136

|

-35.3%

|

|

Operating expenses

|

2,572

|

2,351

|

9.4%

|

2,134

|

20.5%

|

8,979

|

8,694

|

3.3%

|

|

Gross result

|

1,183

|

1,464

|

-19.2%

|

1,808

|

-34.6%

|

6,317

|

6,611

|

-4.4%

|

|

Addition to loan loss provision

|

400

|

560

|

-28.6%

|

322

|

24.2%

|

1,594

|

2,288

|

-30.3%

|

|

Underlying result before tax

|

783

|

904

|

-13.4%

|

1,486

|

-47.3%

|

4,724

|

4,323

|

9.3%

|

|

Taxation

|

215

|

199

|

8.0%

|

349

|

-38.4%

|

1,221

|

1,078

|

13.3%

|

|

Minority interests

|

20

|

19

|

5.3%

|

14

|

42.9%

|

79

|

90

|

-12.2%

|

|

Underlying net result

|

548

|

686

|

-20.1%

|

1,123

|

-51.2%

|

3,424

|

3,155

|

8.5%

|

|

Net gains/losses on divestments

|

202

|

-6

|

||||||

|

Net result from divested units

|

-37

|

|||||||

|

Special items after tax

|

-18

|

-19

|

-117

|

-1,021

|

-82

|

|||

|

Net result Banking

|

530

|

666

|

-20.4%

|

1,006

|

-47.3%

|

2,606

|

3,031

|

-14.0%

|

|

Net result Insurance Other

|

14

|

-26

|

43

|

107

|

117

|

|||

|

Net result IC elimination between ING Bank and NN Group

|

-12

|

-22

|

-3

|

-55

|

-97

|

|||

|

Net result from discontinued operations NN Group2)

|

226

|

-171

|

-159

|

65

|

455

|

|||

|

Net result from discontinued operations Voya Financial

|

418

|

179

|

41

|

-1,471

|

40

|

|||

|

Net result ING Group

|

1,176

|

626

|

87.7%

|

928

|

26.8%

|

1,251

|

3,545

|

-64.7%

|

|

Net result per share (in EUR)3)

|

0.30

|

0.16

|

87.5%

|

0.24

|

25.0%

|

0.32

|

0.93

|

-65.6%

|

|

Capital ratios (end of period)

|

||||||||

|

ING Group shareholders' equity (in EUR billion)

|

47

|

6.9%

|

50

|

46

|

9.7%

|

|||

|

ING Bank shareholders' equity (in EUR billion)

|

37

|

4.1%

|

38

|

33

|

16.2%

|

|||

|

ING Bank common equity Tier 1 ratio fully loaded

|

11.1%

|

11.4%

|

10.0%

|

|||||

|

ING Bank common equity Tier 1 phased in

|

11.2%

|

11.2%

|

11.7%

|

|||||

|

Client balances (end of period, in EUR billion)

|

||||||||

|

Residential Mortgages

|

276.4

|

-0.8%

|

274.3

|

272.7

|

0.6%

|

|||

|

Other Lending

|

230.8

|

0.4%

|

231.7

|

216.7

|

6.9%

|

|||

|

Funds Entrusted

|

483.3

|

-0.9%

|

479.1

|

465.0

|

3.0%

|

|||

|

AUM/Mutual Funds

|

64.8

|

1.4%

|

65.7

|

60.0

|

9.5%

|

|||

|

Profitability and efficiency

|

||||||||

|

Underlying interest margin Banking

|

1.53%

|

1.45%

|

1.53%

|

1.51%

|

1.42%

|

|||

|

Underlying cost/income ratio Banking

|

68.5%

|

61.6%

|

54.1%

|

58.7%

|

56.8%

|

|||

|

Underlying return on equity based on IFRS-EU equity ING Bank4)

|

5.9%

|

8.1%

|

12.7%

|

9.9%

|

9.0%

|

|||

|

Employees ING Bank (FTEs, end of period)

|

52,854

|

0.1%

|

52,898

|

63,805

|

-17.1%

|

|||

|

Risk

|

||||||||

|

Non-performing loans/total loans (end of period)

|

2.8%

|

3.0%

|

2.8%

|

|||||

|

Stock of provisions/provisioned loans (end of period)

|

38.5%

|

35.5%

|

38.6%

|

|||||

|

Underlying risk costs in bps of average RWA

|

54

|

81

|

44

|

55

|

83

|

|||

|

Risk-weighted assets ING Bank (end of period, in EUR billion)

|

294.9

|

0.5%

|

296.3

|

282.5

|

4.9%

|

|||

1) The figures of this period have been restated to reflect the classification of NN Group as Held for sale/Discontinued operations.

2) The 4Q2014 net result from discontinued operations NN Group includes EUR 82 million reversal of impairments.

3) Result per share differs from IFRS earnings per share in respect of attributions to the core Tier 1 securities.

4) Annualised underlying net result divided by average IFRS-EU shareholders’ equity of ING Bank N.V.

Note: Underlying figures are non-GAAP measures. These are derived from figures according to IFRS-EU by excluding impact from divestments, special items, Insurance Other, intercompany eliminations between ING Bank and NN Group, and discontinued operations.

| 4 | ING GROUP PRESS RELEASE 4Q2014 |

CONSOLIDATED RESULTS

|

ING Bank posted a strong set of full-year 2014 results. Higher interest results, strict cost control and lower risk costs drove the underlying net profit to EUR 3,424 million, or 8.5% higher than in 2013. This strong performance was achieved despite EUR 273 million of negative CVA/DVA impacts in 2014, and EUR 375 million of redundancy provisions recorded in the fourth quarter which related principally to the further digitalisation of our banking services in the Netherlands. Including the net result of the legacy Insurance businesses, the 2014 net result of ING Group was EUR 1,251 million. In the fourth quarter, ING Bank recorded robust interest results and continued to be vigilant about expenses. The fourth-quarter result before tax was EUR 783 million, and included negative CVA/ DVA impacts, redundancy provisions and the annual Dutch bank tax. The fourth-quarter net result of ING Group was EUR 1,176 million, supported by the profit on the sale of Voya shares in November 2014 and the strong net result of NN Group.

Banking

ING Bank’s fourth-quarter underlying result before tax of EUR 783 million was good on the back of steady growth in the interest result. However, credit and debt valuation adjustments (CVA/ DVA), reported within Commercial Banking and the Corporate Line, amounted to EUR -80 million for the quarter, against EUR-17 million in the fourth quarter of 2013 and EUR -69 million in the previous quarter. Furthermore, the fourth quarter included a redundancy provision of EUR 375 million, which was mainly related to measures to further expand digital banking in the Netherlands and to enhance operational excellence, as well as measures to accelerate the transformation programme in Commercial Banking. Restructuring costs were EUR 76 million in the fourth quarter of 2013 and EUR 24 million in the previous quarter. Finally, the annual Dutch bank tax, which was paid in full in the fourth quarter, was EUR 138 million for 2014 and EUR 149 million for 2013. Excluding these factors, the underlying result before tax was EUR 1,376 million in the fourth quarter, up 20.1% from the same quarter of 2013, reflecting higher net interest income, lower expenses and lower risk costs. On a like-for-like basis, the pre-tax result was down 12.9% from the previous quarter due to lower income, reflecting seasonality in Financial Markets and a decline in income at Bank Treasury, as well as higher risk costs, which were positively affected in the third quarter by the release on a large file in Commercial Banking.

Customers

In 2014, ING Bank welcomed over one million new customers and established half a million primary banking relationships. Commercial momentum was solid as we continued to support customers’ financial needs throughout the year. The net inflow of funds entrusted was EUR 16.8 billion in 2014, including a

|

reduction in Commercial Banking. In Retail Banking, net funds entrusted increased by EUR 19.2 billion. Net lending assets grew by EUR 14.7 billion in 2014, driven by strong growth in our core lending businesses, partly offset by reductions in the run- off portfolios of WUB and Lease. Net lending assets in the core businesses grew by EUR 18.5 billion, or 3.8%, in 2014. There was strong growth in Retail Banking outside the Netherlands and in Structured Finance and Transaction Services at Commercial Banking. Net lending assets in the core businesses of Retail Netherlands declined due to higher prepayments of Dutch mortgages and a reduction in business lending.

Total underlying income

Total underlying income was robust at EUR 3,756 million, down only 1.5% year-on-year. The decline was primarily due to EUR 80 million of negative CVA/DVA impacts recorded in Commercial Banking and the Corporate Line versus EUR -17 million of CVA/ DVA impacts in the fourth quarter of 2013. Furthermore, the fourth quarter of 2013 included a EUR 99 million positive one- off result on the unwinding of the IABF and EUR 68 million of income from ING Vysya Bank when it was still fully consolidated. Excluding these items, underlying income rose 4.6%, mainly attributable to Retail Banking. Compared with the previous quarter, which included EUR 69 million of negative CVA/DVA impacts, total underlying income declined 4.7%, mainly due to seasonally lower income at Financial Markets and a decline in Bank Treasury.

The ongoing political and economic turmoil affected fourth-quarter business growth in some specific regions and products. Total net lending decreased by EUR 1.0 billion (adjusted for currency impacts, the sale of a mortgage portfolio in Australia and additional transfers of WUB mortgages to NN Bank). The net production of residential mortgages was EUR -0.2 billion due to declines in the Netherlands and in Germany, more than offsetting the growth in most other countries. Other lending declined by EUR 0.9 billion. Retail Netherlands reported a decline in other lending due to low demand in business lending, while in Commercial Banking the decline was mainly caused by decreases in short-term products (such as Trade Finance Services and Trade & Commodity Finance), the run-off of the lease portfolio and a further reduction in Russian exposures. Net growth in other lending in Retail Banking outside of the Netherlands and in Industry Lending within Commercial Banking was not high enough to offset these declines.

Funds entrusted (adjusted for currency impacts) recorded a net outflow of EUR 3.1 billion in the fourth quarter of 2014, following EUR 5.3 billion of reductions in Commercial Banking, which were mainly due to lower deposits from asset managers and corporate treasuries at year-end. In Retail Banking, net funds entrusted rose by EUR 2.2 billion, as net outflows in the Benelux were more than offset by growth in Germany and Rest of World.

The underlying interest result rose 8.9% to EUR 3,208 million year-on-year. Excluding the deconsolidation impact of ING Vysya Bank, the increase was 10.9%. The interest result on customer lending activities rose primarily due to higher margins on

|

| ING GROUP PRESS RELEASE 4Q2014 | 5 |

CONSOLIDATED RESULTS

|

mortgages and higher volumes on other lending. The interest result on funds entrusted also improved due to growth in volumes and higher margins on savings. However, the margin on current accounts declined year-on-year.

Compared with the third quarter of 2014, the underlying interest result increased 1.6%. This was mainly attributable to higher interest results on customer lending, which were partly offset by a decline in Financial Markets. The fourth-quarter underlying interest margin of ING Bank was 1.53%, which was stable compared with the previous quarter (but up eight basis points year-on-year). The interest margin on total lending activities improved, driven by higher margins on mortgages in the Benelux and higher margins in Industry Lending. Although ING reduced client savings rates in several countries, the margin on funds entrusted decreased slightly in the quarter due to continued margin pressure on savings and current accounts caused by the low interest rate environment.

Commission income declined 1.1% from the fourth quarter of 2013 to EUR 556 million, which was mainly due to the deconsolidation impact of ING Vysya Bank. This was largely offset by higher commission income in Retail Belgium and Retail Germany. On a sequential basis, commission income dropped 4.0%, mainly due to lower fees in Retail International.

Investment income declined to EUR 25 million from EUR 64 million in the fourth quarter of 2013. This was mainly due to lower net realised gains on bonds and equities, lower dividend income and lower income from real estate investments. Compared with the third quarter of 2014, which included the EUR 22 million annual dividend from Bank of Beijing, investment income dropped by EUR 11 million.

Other income fell to EUR -34 million from EUR 242 million in the fourth quarter of 2013. The decline was partly caused by negative CVA/DVA impacts (EUR -80 million in the fourth quarter of 2014 versus EUR -17 million in the previous year) and the EUR 99 million one-off result on the unwinding of the IABF in the fourth quarter of 2013. Excluding both impacts, other income dropped by EUR 114 million year-on-year due to higher negative valuation results on non-trading derivatives. Other income fell by EUR 205 million compared with the third quarter of 2014, which included EUR -69 million of CVA/DVA impacts. The decline was mainly caused by lower net trading results and higher negative valuation results.

|

Operating expenses

Underlying operating expenses rose 9.4% year-on-year to EUR 2,572 million. The increase was primarily due to three provisions recorded in the current quarter: EUR 325 million of redundancy provisions following ING’s November 2014 announcement that it is taking the next steps in digital banking in the Netherlands; EUR 39 million of repositioning costs at Commercial Banking to support the further optimisation of ING’s international network; and EUR 11 million of costs for further restructuring at WUB. By comparison, the fourth quarter of 2013 included EUR 76 million of additional restructuring costs in Retail Netherlands.

Excluding the impact of the aforementioned provisions and the deconsolidation impact of ING Vysya Bank, operating expenses were 1.9% lower year-on-year. The decline was mainly attributable to the benefits of the ongoing cost-savings initiatives and a large release from deposit guarantee scheme (DGS) related provisions booked in the Corporate Line, which more than offset higher pension costs in the Netherlands and additional investments in Retail International and Industry Lending to support business growth.

Compared with the third quarter of 2014, expenses increased 20.5%. Excluding redundancy provisions (EUR 375 million in the fourth quarter and EUR 24 million in the third quarter of 2014), expenses rose by EUR 87 million, or 4.1%. This was fully attributable to the annual Dutch bank tax of EUR 138 million, which was paid in the fourth quarter. The fourth-quarter underlying cost/income ratio for ING Bank was 68.5%, up from 61.6% a year ago. The full-year 2014 underlying cost/income ratio rose to 58.7% from 56.8% in 2013. However, excluding CVA/DVA impacts and the redundancy/restructuring provisions in both years, the cost/income ratio improved to 55.1% from 56.2% in 2013.

The current cost-savings programmes at ING Bank, including the additional measures taken in the fourth quarter of 2014, are expected to reduce total annual expenses by EUR 1.2 billion by 2017 and by EUR 1.3 billion by 2018. Of these targeted amounts, EUR 662 million of savings have already been achieved. Total headcount reductions related to these initiatives are estimated at 9,540 FTEs, of which 5,677 FTEs have already left ING Bank since the start of the programmes.

The total number of internal staff rose slightly to 52,898 FTEs at year-end. This is 44 FTEs higher than at the end of September 2014 and due to growth outside the Benelux. The strong decline versus year-end 2013 was for 11,105 FTEs caused by the deconsolidation of ING Vysya Bank.

|

| 6 | ING GROUP PRESS RELEASE 4Q2014 |

CONSOLIDATED RESULTS

|

Loan loss provisions

ING Bank added EUR 400 million to the provision for loan losses in the fourth quarter, down from EUR 560 million a year ago and also lower than in the first two quarters of 2014, but up from EUR 322 million in the previous quarter. The sequential increase was attributable to Commercial Banking, where General Lending was positively affected by a release on a large file in the third quarter. Higher risk costs were also visible in Industry Lending, due to some larger files in Structured Finance, and there was a modest increase at Real Estate Finance after two quarters of negligible risk costs. Net additions in Retail Benelux declined on both comparable quarters. This was mainly attributable to a further decline of risk costs for Dutch mortgages to EUR 41 million in this quarter, next to lower risk costs for business lending in both countries. At Retail International, net additions were slightly higher than in the previous quarter, but they were lower than a year ago, supported by the deconsolidation of ING Vysya Bank. Total NPLs at ING Bank rose to EUR 16.9 billion from EUR 15.7 billion at the end of September 2014, mainly due to alignment with EBA rules on forbearance. The NPL ratio increased to 3.0% of total credit outstandings compared with 2.8% at the end of the third quarter.

Total risk costs were 54 basis points of average risk-weighted assets versus 44 basis points in the previous quarter and 81 basis points in the fourth quarter of 2013. Most businesses, with the exception of Retail Netherlands, are now operating at around a normalised level of risk costs as the overall economic environment gradually improves.

Underlying result before tax

The fourth-quarter 2014 underlying result before tax was EUR 783 million, a decline of 13.4% compared with the same quarter of 2013. However, excluding the redundancy provisions, CVA/DVA impacts and the Dutch bank tax, the underlying result before tax jumped 20.1%.

On a sequential basis, the underlying result before tax fell 47.3%. This was next to the redundancy provisions, mainly caused by the annual Dutch bank tax, which was paid in the fourth quarter, combined with lower income and higher risk costs in Commercial Banking.

|

Net result Banking

ING Bank’s underlying net result fell to EUR 548 million from EUR 686 million in the fourth quarter of 2013 and EUR 1,123 million in the third quarter of 2014. The effective underlying tax rate was 27.5% compared with 22.0% in the fourth quarter of 2013 and 23.5% in the previous quarter.

ING Bank’s fourth-quarter net result was EUR 530 million, including EUR -18 million of special items after tax, which were fully related to the restructuring programmes in Retail Netherlands announced before 2013.

The full-year 2014 underlying return on IFRS-EU equity rose to 9.9% from 9.0% in 2013. Excluding the redundancy provisions, the full-year 2014 underlying return would have been 10.7%. The improvement was driven by higher underlying results combined with a modest decline in the average equity base. The decline in the average equity base was caused by dividend payments to ING Group throughout both years and the write-down in the net pension asset in the first quarter of 2014. The Ambition 2017 target range for return on IFRS-EU equity is 10-13%.

Net result ING Group

ING Group’s fourth-quarter net result was EUR 1,176 million, compared with EUR 626 million in the fourth quarter of 2013 and EUR 928 million in the third quarter of 2014. These figures include the net results of the legacy Insurance businesses.

|

| ING GROUP PRESS RELEASE 4Q2014 | 7 |

CONSOLIDATED RESULTS

|

For the fourth quarter of 2014, ING Group recorded a net result from the discontinued operations of NN Group of EUR 226 million, compared with EUR -171 million one year earlier and EUR -159 million in the third quarter of 2014. The fourth-quarter 2014 result represents ING’s 68.1% stake in NN Group’s net result of EUR 197 million. The fourth-quarter 2014 net result from the discontinued operations of NN Group also includes a EUR 82 million gain on the partial reversal of the EUR 333 million write- down in the third quarter of 2014 for certain other non-current assets, as NN Group divested some of these assets in the fourth quarter.

In November 2014, ING sold 34.5 million shares of common stock in Voya Financial, Inc., reducing ING’s stake in Voya from 32.5% to approximately 19%. As a result, ING lost significant influence on Voya and will account for its stake in Voya as an available-for-sale investment going forward. The financial impact of the November transaction is reflected in the EUR 418 million net result from discontinued operations of Voya. It reflects the difference between the EUR 2.1 billion book value of ING’s 32.5% investment in Voya (which equals the market value at the date of deconsolidation on 25 March 2014) and the market value of this stake at the time of the transaction.

ING Group’s net profit per share was EUR 0.30 for the fourth quarter of 2014 and EUR 0.32 for the full year 2014.

Dividend

As stated in our Ambition 2017 targets, ING is committed to returning capital to shareholders through a sustainable dividend policy. Effective from 2015, ING intends to pay a minimum of 40% of ING Group’s annual net profits by way of dividend, consisting of both an interim and a final dividend.

Furthermore, the Board will recommend whether to return additional capital to shareholders at the end of each financial year. Such decisions will reflect considerations including expected future capital requirements, growth opportunities available to the Group, the net earnings of the Group, and regulatory approvals as appropriate.

The Board proposes to pay a final 2014 dividend of EUR 470 million, or EUR 0.12 per (depositary receipt for an) ordinary share, subject to the approval of shareholders at the Annual General Meeting in May 2015.

|

| 8 | ING GROUP PRESS RELEASE 4Q2014 |

|

Retail Banking: Consolidated profit and loss account

|

||||||||||

|

Total Retail Banking

|

Retail Benelux | Retail International | ||||||||

|

Netherlands

|

Belgium

|

Germany

|

Rest of World

|

|||||||

| In EUR million |

4Q2014

|

4Q2013

|

4Q2014

|

4Q2013

|

4Q2014

|

4Q2013

|

4Q2014

|

4Q2013

|

4Q2014

|

4Q2013

|

|

Profit & loss

|

||||||||||

|

Interest result

|

2,341

|

2,205

|

980

|

930

|

495

|

479

|

390

|

357

|

477

|

439

|

|

Commission income

|

318

|

319

|

119

|

116

|

94

|

80

|

44

|

32

|

61

|

91

|

|

Investment income

|

5

|

11

|

0

|

0

|

3

|

1

|

0

|

0

|

2

|

10

|

|

Other income

|

27

|

24

|

-15

|

-3

|

21

|

27

|

-23

|

-11

|

45

|

11

|

|

Total underlying income

|

2,691

|

2,559

|

1,084

|

1,043

|

613

|

587

|

411

|

378

|

584

|

551

|

|

Staff and other expenses

|

1,861

|

1,632

|

928

|

669

|

360

|

386

|

197

|

179

|

376

|

398

|

|

Intangibles amortisation and impairments

|

12

|

2

|

4

|

0

|

0

|

-1

|

0

|

0

|

8

|

2

|

|

Operating expenses

|

1,873

|

1,633

|

932

|

669

|

359

|

386

|

197

|

179

|

385

|

400

|

|

Gross result

|

818

|

926

|

152

|

374

|

254

|

202

|

214

|

199

|

199

|

151

|

|

Addition to loan loss provision

|

248

|

384

|

165

|

234

|

18

|

70

|

16

|

25

|

50

|

54

|

|

Underlying result before tax

|

570

|

542

|

-13

|

140

|

236

|

131

|

198

|

174

|

149

|

97

|

|

Client balances (in EUR billion)1)

|

||||||||||

|

Residential Mortgages

|

274.3

|

272.7

|

129.3

|

132.7

|

32.8

|

30.9

|

63.2

|

62.1

|

49.0

|

46.9

|

|

Other Lending

|

96.0

|

94.3

|

34.8

|

36.3

|

37.1

|

34.0

|

5.0

|

4.4

|

19.0

|

19.6

|

|

Funds Entrusted

|

405.6

|

389.4

|

113.8

|

112.1

|

82.2

|

78.3

|

113.5

|

105.9

|

96.1

|

93.0

|

|

AUM/Mutual Funds

|

65.5

|

59.9

|

19.7

|

17.7

|

27.4

|

26.9

|

7.7

|

6.8

|

10.6

|

8.5

|

|

Profitability and efficiency1)

|

||||||||||

|

Cost/income ratio

|

69.6%

|

63.8%

|

86.0%

|

64.1%

|

58.6%

|

65.7%

|

47.9%

|

47.3%

|

65.9%

|

72.6%

|

|

Return on equity based on 10.0% common equity Tier 12)

|

10.2%

|

10.3%

|

-1.2%

|

6.2%

|

27.5%

|

16.8%

|

21.6%

|

20.5%

|

9.2%

|

7.2%

|

|

Risk1)

|

||||||||||

|

Risk costs in bps of average RWA

|

65

|

105

|

111

|

155

|

28

|

129

|

26

|

43

|

46

|

52

|

|

Risk-weighted assets (end of period)

|

154,467

|

152,134

|

59,821

|

64,354

|

26,515

|

23,338

|

24,542

|

23,756

|

43,588

|

40,685

|

|

1)

|

Key figures based on underlying figures.

|

|

2)

|

Underlying after-tax return divided by average equity based on 10.0% common equity Tier 1 ratio (annualised).

|

|

Retail Banking posted strong full-year 2014 results. The underlying profit before tax rose by 23.5% to EUR 3,158 million on the back of healthy business growth and substantially lower risk costs in most markets. In the fourth quarter, the underlying result before tax was EUR 570 million (or EUR 895 million, excluding EUR 325 million of redundancy provisions mainly related to taking the next steps in digital banking in the Netherlands). The result for the quarter improved strongly versus a year ago, increasing 44.8% excluding redundancy provisions. Compared to the previous quarter, the like-for-like result declined by EUR 75 million (or 7.7%), mainly due to the annual Dutch bank tax, which was booked fully in the fourth quarter, and higher IT investments. Retail Banking attracted EUR 2.2 billion of funds entrusted in the fourth quarter; net lending grew by EUR 0.9 billion.

|

Underlying income in the fourth quarter rose 5.2% from a year ago to EUR 2,691 million. The increase was driven by higher interest results in most countries due to higher volumes and improved margins on lending and savings. Compared with the third quarter of 2014, income declined 1.7% as slightly higher interest results were more than offset by lower fee income, negative hedge ineffectiveness and lower dividends. Net funds entrusted grew by EUR 2.2 billion in the fourth quarter, despite outflows in the Netherlands and Belgium. Net lending increased by EUR 0.9 billion as continued growth in Belgium and Rest of World outpaced declines in the Netherlands and Germany.

Operating expenses rose 14.7% from the fourth quarter of 2013 to EUR 1,873 million; this included EUR 325 million of redundancy provisions versus EUR 76 million a year ago. Excluding these provisions, expenses were 0.6% lower year-on- year, supported by the deconsolidation of ING Vysya Bank and the cost-savings initiatives. Compared with the previous quarter, like-for-like expenses were EUR 68 million higher, mainly due to the annual Dutch bank tax and higher IT investments.

Risks costs were EUR 248 million, down 35.4% from a year ago, and 13.6% lower than in the third quarter. The sequential decline was mainly in the Benelux due to a model refinement in Belgium and lower risk costs for Dutch mortgages.

The underlying return on equity based on a 10% common equity Tier 1 ratio was 10.2% in the fourth quarter, compared with 10.3% a year ago. On a full-year basis, the return on equity rose to 15.0% from 12.9% in 2013.

|

| ING GROUP PRESS RELEASE 4Q2014 | 9 |

SEGMENT REPORTING: RETAIL BANKING

|

RETAIL NETHERLANDS

Retail Netherlands recorded a EUR 13 million pre-tax loss in the fourth quarter, due to EUR 314 million of redundancy provisions to take the next step in digital banking in the Netherlands (as announced on 25 November 2014) and EUR 11 million for further restructuring at WUB (related to outsourcing of back- office activities). Excluding these provisions, the underlying result before tax was EUR 312 million, up from EUR 216 million a year ago when excluding the EUR 76 million additional restructuring provision taken in that quarter. The improvement compared with a year ago was attributable to higher interest margins and lower risk costs. Compared with the third quarter of 2014, which included a provision of EUR 24 million for additional redundancies, the result before tax declined, mainly due to the annual Dutch bank tax of EUR 33 million which was paid in full in the fourth quarter.

Total underlying income rose 3.9% from a year ago to EUR 1,084 million. This increase mainly reflects higher interest margins on lending and savings, which more than offset a decline in net lending assets. The decrease in lending was primarily due to lower mortgage volumes. Compared with the previous quarter, income increased slightly by EUR 3 million due to higher margins on mortgages and savings, which were mostly offset by lower volumes. The margin improvement on savings was supported by client rate reductions in both quarters. The mortgage portfolio declined by EUR 1.5 billion, of which EUR 0.2 billion was caused by additional transfers of WUB mortgages to NN Bank and EUR 0.5 billion to the continuing run-off of the WUB portfolio. Part of the decline was also caused by higher redemptions. Other lending, mainly business lending, decreased by EUR 1.2 billion following low business demand. Funds entrusted recorded a net outflow of EUR 1.6 billion, partly related to higher mortgage repayments.

Operating expenses were EUR 932 million in the fourth quarter of 2014. However, excluding the aforementioned redundancy provisions, operating expenses were EUR 607 million, up by only EUR 14 million from a year ago. This increase was mainly due to higher pension costs and increased IT investments, which were only partly offset by the impact of cost-containment initiatives. Compared with the previous quarter, operating expenses excluding the redundancy provisions rose by EUR 60 million. This increase was mainly caused by the annual Dutch bank tax of EUR 33 million, the seasonal impact of the holiday provision, and higher IT investments. The cost-efficiency programmes, including the next steps in digital banking, remain on track to realise EUR 675 million of annual cost savings by the end of 2017. Of this amount, EUR 354 million has already been realised.

|

Risk costs declined to EUR 165 million from EUR 234 million in the fourth quarter of 2013 due to lower net additions in both mortgages and business lending. Compared with the previous mortgages declined to EUR 41 million from EUR 62 million in the third quarter of 2014. The net additions for business lending decreased to EUR 96 million from EUR 104 million; this was partly offset by higher risk costs in consumer lending.

Risk-weighted assets increased by EUR 0.5 billion in the fourth quarter to EUR 59.8 billion.

RETAIL BELGIUM

Retail Belgium delivered another strong underlying fourth-quarter result. The result before tax rose to EUR 236 million from EUR 131 million in the fourth quarter of 2013, reflecting lower risk costs, volume growth in most products and lower expenses. The cost/ income ratio improved by more than seven percentage points to 58.6%. Compared with the third quarter of 2014, the result before tax rose 12.9%, almost entirely caused by lower risk costs.

Total underlying income rose 4.4% from a year ago to EUR 613 million. This increase was mainly due to higher interest results following volume growth in most products, as well as higher management fees. Compared with the previous quarter, income increased marginally by 0.2% as higher margins on mortgages and increased average volumes in current accounts compensated for margin pressure on savings and current accounts. Net lending assets rose by EUR 2.3 billion in the fourth quarter, mainly in non- mortgage lending, while funds entrusted recorded a small outflow of EUR 0.6 billion.

Operating expenses declined by EUR 27 million, or 7.0%, to EUR 359 million compared with the previous year. The decline was partly due to the absence of Belgian bank taxes in the fourth quarter of 2014, whereas the fourth quarter of 2013 included a EUR 11 million charge. The remaining decline is mainly due to lower headcount in the Retail branch network, partly offset by increased IT costs. Compared with the previous quarter, expenses remained flat. The strategic projects announced by ING Belgium remain on track to realise EUR 160 million of cost savings by the end of 2017. Of this amount, savings of EUR 105 million have already been realised.

Risk costs were EUR 18 million, down from EUR 70 million a year ago and EUR 44 million in the previous quarter. The decrease on both comparable quarters was mainly caused by a model

|

| 10 | ING GROUP PRESS RELEASE 4Q2014 |

SEGMENT REPORTING: RETAIL BANKING

|

refinement, which resulted in lower risk costs for business lending and consumer lending. The net addition for mortgages rose to EUR 19 million from EUR 5 million in the previous quarter.

Risk-weighted assets increased by EUR 2.7 billion in the fourth quarter to EUR 26.5 billion. This was mainly caused by lower expected recovery rates in all portfolios and a higher probability of default in the SME portfolio.

RETAIL GERMANY

Retail Germany continued its strong performance with a fourth- quarter 2014 underlying result before tax of EUR 198 million, up from EUR 174 million in the fourth quarter of 2013. The improvement was driven by higher income, mainly reflecting volume growth, and lower risk costs. This was partly offset by higher expenses to support business growth strategies. The cost/ income ratio was 47.9%. Compared with the third quarter of 2014, the result before tax declined 7.0%, mainly due to lower margins on savings and partly offset by lower expenses and risk costs.

Total underlying income was EUR 411 million, up 8.7% from the fourth quarter of 2013. The increase primarily reflects higher interest results from increased lending and savings balances, while the margin was flat compared with a year ago. Higher commission income, mainly caused by more security brokerage transactions, was offset by increased negative hedge ineffectiveness results. Compared with the third quarter of 2014, income was 5.3% lower; this was primarily due to lower margins on savings stemming from the current interest rate environment. Funds entrusted grew by EUR 2.0 billion in the fourth quarter. Retail lending decreased by EUR 0.4 billion, of which EUR 0.5 billion was in residential mortgages, while consumer lending rose by EUR 0.1 billion.

Operating expenses were EUR 197 million, up 10.1% from the fourth quarter of 2013, reflecting an increase in headcount at both ING-DiBa and Interhyp, as well as investments to support business growth and attract primary banking clients. Compared with the previous quarter, expenses were 2.5% lower, mainly due to seasonality in marketing.

Risk costs were EUR 16 million, down from EUR 25 million in the fourth quarter of 2013 and EUR 19 million in the previous quarter, reflecting better performance in the mortgage book (mainly lower observed LGDs). Risk costs in the fourth quarter of 2014 were 26 basis points of average RWA.

|

Risk-weighted assets decreased by EUR 1.5 billion in the fourth quarter to EUR 24.5 billion, mainly reflecting model updates in the investment book and a reduction in operational RWA.

RETAIL REST OF WORLD

The underlying result before tax of Retail Rest of World rose to EUR 149 million from EUR 97 million in the fourth quarter of 2013. The higher result largely reflects better commercial results in Romania, Italy, France and Poland; a one-off gain on the sale of a white label mortgage portfolio in Australia; and lower losses in the UK Legacy run-off portfolio. These effects were partly offset by lower results in Turkey and Spain. Compared with the third quarter of 2014, which included a dividend from Bank of Beijing (of EUR 22 million) and ING’s share in the net profit of ING Vysya Bank (EUR 9 million versus nil this quarter following its reclassification to assets held-for-sale), the result before tax declined by EUR 45 million.

Underlying income rose 6.0% to EUR 584 million compared with a year ago. The improvement was driven by higher interest margins and higher volumes in most countries, a higher result from ING Bank’s stake in TMB, lower losses in the UK legacy run-off portfolio and a EUR 17 million gain on the sale of a mortgage portfolio in Australia. Excluding the deconsolidation of ING Vysya Bank, underlying income grew 17.1%. Compared with the third quarter of 2014, income declined by EUR 27 million, caused by the annual Bank of Beijing dividend being received in the previous quarter and no result from ING’s share in ING Vysya Bank as a result of the reclassification to assets held- for-sale. Lower income in Turkey, Poland and Italy was offset by the gain on the sale of the mortgage portfolio in Australia. Net funds entrusted grew by EUR 2.3 billion in the fourth quarter, mainly driven by Poland, Spain and Australia. Net lending assets (adjusted for currency impacts and the sale of the mortgage portfolio) rose by EUR 1.4 billion, with growth concentrated in Australia, Poland and Turkey.

Operating expenses decreased by EUR 15 million from a year ago to EUR 385 million. Excluding the deconsolidation of ING Vysya Bank, expenses increased 6.1%, mainly due to investments in strategic initiatives and higher marketing costs. Compared with the third quarter of 2014, operating expenses rose by EUR 13 million, mainly owing to EUR 6 million of allocated annual Dutch bank tax, higher marketing expenses and higher costs in Turkey.

Risk costs were EUR 50 million against EUR 54 million in the fourth quarter of 2013, which included EUR 16 million for ING

|

| ING GROUP PRESS RELEASE 4Q2014 | 11 |

SEGMENT REPORTING: RETAIL BANKING

|

Vysya Bank and lower risk costs in Turkey due to releases in that quarter. Compared with the previous quarter, risk costs were EUR 6 million higher, mainly due to higher provisioning in Turkey. Total fourth-quarter risk costs were 46 basis points of average RWA, down from 52 basis points a year ago, but up from 42 basis points in the third quarter of 2014.

Risk-weighted assets increased in the fourth quarter by EUR 0.8 billion to EUR 43.6 billion, mainly due to business growth and increases in the market value of the strategic Asian bank stakes.

|

| 12 | ING GROUP PRESS RELEASE 4Q2014 |

SEGMENT REPORTING: COMMERCIAL BANKING

|

Commercial Banking: Consolidated profit and loss account

|

||||||||||

|

Total Commercial

Banking

|

Industry

Lending

|

General Lending &

Transaction Services

|

Financial Markets

|

Bank Treasury,

Real Estate & Other

|

||||||

|

In EUR million

|

4Q2014

|

4Q2013

|

4Q2014

|

4Q2013

|

4Q2014

|

4Q2013

|

4Q2014

|

4Q2013

|

4Q2014

|

4Q2013

|

|

Profit & loss

|

|

|

||||||||

|

Interest result

|

900

|

748

|

426

|

372

|

242

|

236

|

195

|

75

|

37

|

66

|

|

Commission income

|

239

|

245

|

135

|

127

|

85

|

93

|

19

|

26

|

0

|

-1

|

|

Investment income

|

21

|

54

|

-7

|

25

|

0

|

0

|

6

|

3

|

21

|

25

|

|

Other income excl. CVA/DVA

|

25

|

146

|

-15

|

-15

|

15

|

4

|

24

|

145

|

2

|

12

|

|

Underlying income excl. CVA/DVA

|

1,185

|

1,192

|

539

|

509

|

342

|

332

|

244

|

250

|

60

|

101

|

|

Other income - DVA on structured notes

|

1

|

-14

|

1

|

-14

|

||||||

|

Other income - CVA/DVA on derivatives

|

-73

|

23

|

-73

|

23

|

||||||

|

Total underlying income

|

1,113

|

1,201

|

539

|

509

|

342

|

332

|

172

|

258

|

60

|

101

|

|

Staff and other expenses

|

700

|

630

|

149

|

140

|

193

|

202

|

249

|

233

|

110

|

56

|

|

Intangibles amortisation and impairments

|

16

|

24

|

2

|

0

|

0

|

0

|

0

|

0

|

14

|

25

|

|

Operating expenses

|

716

|

654

|

151

|

139

|

193

|

202

|

249

|

233

|

124

|

80

|

|

Gross result

|

397

|

547

|

388

|

369

|

148

|

131

|

-76

|

26

|

-63

|

21

|

|

Addition to loan loss provision

|

152

|

177

|

122

|

102

|

8

|

47

|

-1

|

0

|

23

|

27

|

|

Underlying result before tax

|

245

|

370

|

266

|

267

|

141

|

84

|

-76

|

26

|

-86

|

-7

|

| Client balances (in EUR billion)1) | ||||||||||

|

Residential Mortgages

|

135.8

|

122.5

|

82.8

|

72.3

|

44.0

|

39.7

|

2.0

|

2.0

|

7.0

|

8.4

|

|

Other Lending

|

||||||||||

|

Funds Entrusted

|

73.5

|

75.6

|

1.3

|

0.7

|

41.7

|

36.2

|

4.7

|

3.9

|

25.8

|

34.8

|

|

AUM/Mutual Funds

|

0.2

|

0.2

|

0.0

|

0.0

|

0.0

|

0.0

|

0.0

|

0.0

|

0.2

|

0.2

|

|

Profitability and efficiency1)

|

||||||||||

|

Cost/income ratio

|

64.3%

|

54.5%

|

28.0%

|

27.4%

|

56.6%

|

60.6%

|

144.3%

|

90.1%

|

204.9%

|

79.5%

|

|

Return on equity based on 10.0% common equity Tier 1 2)

|

5.3%

|

8.5%

|

17.0%

|

16.5%

|

12.3%

|

7.2%

|

-7.3%

|

2.4%

|

-20.4%

|

-5.4%

|

|

Risk1)

|

||||||||||

|

Risk costs in bps of average RWA

|

44

|

56

|

96

|

80

|

8

|

55

|

-1

|

0

|

62

|

71

|

|

Risk-weighted assets (end of period)

|

137,976

|

127,165

|

51,161

|

50,356

|

36,803

|

34,374

|

36,793

|

26,114

|

13,219

|

16,321

|

|

1)

|

Key figures based on underlying figures.

|

|

2)

|

Underlying after-tax return divided by average equity based on 10.0% common equity Tier 1 ratio (annualised).

|

|

Commercial Banking posted a good set of full-year 2014 results on the back of very strong Industry Lending performance, good volume growth, and despite negative CVA/DVA impacts throughout the year and additional redundancy provisions. The underlying result before tax was EUR 1,997 million in 2014, and grew 12.9% versus 2013 excluding these two items. In the fourth quarter, the underlying result before tax was EUR 245 million, down from a year ago, but stable excluding CVA/DVA impacts and redundancy provisions. The decline compared with the previous quarter, was additionally caused by the annual Dutch bank tax and higher risk costs, combined with seasonally lower results in Financial Markets and lower income at Bank Treasury.

|

Total underlying income decreased 7.3% versus the fourth quarter of 2013, mainly due to the negative CVA/DVA adjustments. These CVA/DVA effects, reported within Financial Markets, were EUR-72 million for the quarter, down from EUR 9 million in the fourth quarter of 2013 and EUR -42 million in the previous quarter. Excluding the CVA/DVA impact, income was 0.6% lower than in the fourth quarter of 2013. Industry Lending income was 5.9% higher than last year due to the strong performance of Structured Finance, largely offsetting lower income in Bank Treasury, Real Estate & Other. Total income was down 9.8% on the prior quarter, excluding CVA/DVA effects, driven by seasonality in Financial Markets and lower income in Bank Treasury, which was impacted by the low yield environment and declining investment spreads, as well as negative revaluation of derivatives and lower capital gains on bonds.

The interest result increased 20.3% compared with a year ago, driven by strong volume growth in Structured Finance over the year. This was supported by higher interest results in Financial Markets, partly offset by lower results at Bank Treasury. Compared with the previous quarter, the interest result of Commercial Banking rose 0.8%, mainly due to Structured Finance, on the back of higher volumes and margins, partly offset by lower interest results in Financial Markets.

Commission income was 2.4% lower than in the same quarter

|

| ING GROUP PRESS RELEASE 4Q2014 | 13 |

SEGMENT REPORTING: COMMERCIAL BANKING

|

a year ago and down 1.2% on the third quarter of 2014. Both decreases were caused by General Lending & Transaction Services.

Investment income was EUR 21 million compared with EUR 54 million in the fourth quarter of 2013 and EUR 17 million in the previous quarter. The last quarter of 2013 included gains on the sale of various investments in Industry Lending as well as gains on the sale of assets within Real Estate, whereas this quarter included an EUR 11 million impairment on an equity stake in Corporate Investments.

Total other income amounted to EUR -47 million, down EUR 201 million from a year ago and partly due to negative CVA/DVA effects in Financial Markets. Compared with the previous quarter, other income fell by EUR 167 million; this was largely due to Financial Markets and lower revaluations of derivatives used for hedging purposes in Bank Treasury.

Operating expenses were 9.5% higher than in the fourth quarter of 2013. The fourth quarter of 2014 included the Dutch bank tax of EUR 72 million, compared with EUR 76 million a year ago, and a redundancy provision of EUR 50 million, of which EUR 11 million is for the next steps in digital banking in the Netherlands as announced on 25 November 2014. The remaining EUR 39 million redundancy provision relates to the ongoing transformation programmes, which will lead to a net additional reduction of staff of around 250 FTEs in the next three years. Both programmes will result in additional structural cost savings of approximately EUR 40 million per annum by 2018. The previously announced restructuring programmes are on track. At the end of 2014, EUR 203 million of cost savings had already been realised out of EUR 340 million targeted by 2017.

Excluding the Dutch bank levies and the redundancy provisions, expenses increased 2.9% year-on-year despite the costs savings from the previously announced restructuring programmes and lower impairments in Real Estate Development. The year-on-year increase was due to inflationary impacts, a higher number of FTEs in Structured Finance to support business growth, higher pension costs in the Netherlands and the weakening of the euro. On a sequential basis, expenses excluding the Dutch bank levies and redundancy provisions rose 6.1% due to new hires in Structured Finance and higher IT investments to improve Commercial Banking’s product offering. The cost/income ratio was 64.3%, up from the 54.5% in the fourth quarter of 2013 and 44.1% in the previous quarter. Excluding CVA/DVA impacts, the redundancy provision and the Dutch bank levies, the cost/income ratio was 50.2% in the fourth quarter.

Risk costs amounted to EUR 152 million for the quarter, down from EUR 177 million in the fourth quarter of 2013, but up from EUR 34 million in the previous quarter, which was positively affected by the release of a large file.

Risk-weighted assets (RWA) declined by EUR 1.1 billion compared with the previous quarter. The underlying return on equity, based on a 10% common equity Tier 1 ratio, was 5.3%, down from 8.5% in the fourth quarter of 2013. The full-year 2014 underlying

|

return on equity was 11.4%, down from 12.8% in 2013. Excluding CVA/DVA impacts, the underlying ROE rose to 12.6% from 11.8% in 2013.

INDUSTRY LENDING

Industry Lending posted an underlying result before tax of EUR 266 million, down 0.4% from the fourth quarter of 2013 as higher income was offset by higher expenses (reflecting investments in future growth) and higher risk costs. Income was up 5.9% year-on-year, driven by higher income in Structured Finance on the back of higher lending volumes. This was partly offset by lower income in Real Estate Finance (REF) and an EUR 11 million impairment on an equity stake in Corporate Investments.

In Structured Finance, the net lending assets, excluding FX impacts, increased by EUR 6.9 billion year-on-year despite a reduction in Russian exposures and the negative impact of the decline in oil prices on volumes. Compared with the previous quarter, the pre-tax result was down 28.7% due to higher risk costs and the Dutch bank tax. Income, excluding the impairment, rose by 0.9%, supported by lending growth and higher margins. Lending volumes, excluding FX impacts, grew by EUR 1.3 billion, of which EUR 0.8 billion related to Structured Finance and EUR 0.5 billion to REF. Expenses increased 22.8% on the previous quarter, mainly due to the Dutch bank tax. The cost/income ratio remained low at 28.0%.

Net additions to loan loss provisions amounted to EUR 122 million, up from EUR 102 million a year ago and EUR 49 million in the third quarter of 2014. The addition to the provision for loan losses was mainly attributable to Structured Finance; the net addition for REF remained low at EUR 25 million for the quarter.

|

| 14 | ING GROUP PRESS RELEASE 4Q2014 |

SEGMENT REPORTING: COMMERCIAL BANKING

|

GENERAL LENDING & TRANSACTION SERVICES

The underlying result before tax from General Lending & Transaction Services was EUR 141 million, up 67.9% from a year ago, mainly due to lower risk costs. Income was slightly higher due to higher income in both Working Capital Solutions and Bank Mendes Gans, offsetting lower income in General Lending, where interest margins continued to be under pressure. Expenses were 4.5% lower than in the previous year, due entirely to the cost savings from the restructuring plans. Compared with the previous quarter, the pre-tax result declined 24.6%, as higher income was offset by higher expenses, reflecting the booking of the Dutch bank tax and higher IT investments. Risk costs were EUR 8 million for the quarter, up from EUR -28 million in the prior quarter, which included the release from a large file.

FINANCIAL MARKETS

Financial Markets posted an underlying result before tax of EUR-76 million, down from EUR 26 million in the fourth quarter of 2013 and EUR 55 million in the previous quarter. Both the year- on-year and quarterly variance were influenced by the negative credit and debt valuation adjustments (CVA/DVA). Results in the current quarter included EUR -72 million of CVA/DVA impacts compared with EUR 9 million a year ago and EUR -42 million in the previous quarter.

Compared with the same quarter a year ago, income excluding CVA/DVA fell 2.4%. Fourth-quarter income is traditionally lower than in the third quarter and 2014 was no exception. Income excluding CVA/DVA declined 18.9% from the previous quarter, mainly reflected in lower credit trading business. Operating expenses rose 6.9% year-on-year as the costs savings from the restructuring plans were more than offset by higher staff expenses, inflationary impacts and the weakening of the euro. Expenses rose 22.1% from the third quarter, mainly due to the annual Dutch bank tax.

|

BANK TREASURY, REAL ESTATE AND OTHER

Bank Treasury, Real Estate and Other booked an underlying result before tax of EUR -86 million (including the EUR 50 million of redundancy provisions), compared with EUR -7 million in the fourth quarter of 2013 and EUR 62 million in the previous quarter. Income declined 40.6% year-on-year, mainly due to portfolio reduction within the run-off businesses.

Sequentially, income fell 53.8% (mainly within Bank Treasury) as the previous quarter included positive revaluation of derivatives for hedging purposes and higher capital gains on bonds. In addition, Bank Treasury income was lower than in the previous quarter due to the low yield environment and declining investment spreads. Expenses rose 55.0% from a year ago and more than doubled on the previous quarter, mainly due to EUR 50 million of redundancy provisions recorded in this quarter. The impairments within the run-off businesses (mainly related to Real Estate Development) amounted to EUR 14 million, down from EUR 25 million a year ago, but up from EUR 5 million in the previous quarter.

|

| ING GROUP PRESS RELEASE 4Q2014 | 15 |

CORPORATE LINE BANKING

|

Banking Corporate Line: Underlying result before tax

|

||

|

In EUR million

|

4Q2014

|

4Q2013

|

|

Income on capital surplus

|

124

|

121

|

|

Solvency costs

|

-37

|

-72

|

|

Financing charges

|

-24

|

-51

|

|

Other Capital Management

|

14

|

149

|

|

Capital Management excl. DVA

|

77

|

148

|

|

Bank Treasury excl. DVA

|

-123

|

-92

|

|

DVA

|

-8

|

-26

|

|

Other

|

21

|

-37

|

|

Underlying result before tax

|

-32

|

-8

|

|

of which: Underlying income

|

-49

|

55

|

|

of which: Operating expenses

|

-17

|

63

|

|

Corporate Line Banking posted an underlying result before tax of EUR -32 million compared with EUR -8 million in the fourth quarter of 2013. Both quarters included substantial positive one-off results: this quarter included a large release from provisions related to regulatory expenses (DGS-related), whereas the fourth quarter of 2013 included the positive result from the unwinding of the IABF following the agreement with the Dutch State. The underlying result before tax in the previous quarter was EUR -137 million.

Capital Management-related results fell to EUR 77 million from EUR 148 million in the fourth quarter of 2013, which included a EUR 99 million one-off result from the unwinding of the IABF.