Form 6-K ENCANA CORP For: Mar 27

Tweet

Tweet Share

Share

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934

| For: March 27, 2015 | Commission File Number: 1-15226 |

ENCANA CORPORATION

(Translation of registrant’s name into English)

Suite 4400, 500 Centre Street SE

PO Box 2850

Calgary, Alberta, Canada T2P 2S5

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20- F Form 40-F ü

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

|

|

|

|

DOCUMENTS FILED AS PART OF THIS FORM 6-K

See the Exhibit Index to this Form 6-K.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Date: March 27, 2015 | ENCANA CORPORATION | |||||||||||

| (Registrant) | ||||||||||||

| By: | /s/ Jocelyn S. Salazar | |||||||||||

| Name: | Jocelyn S. Salazar | |||||

| Title: | Assistant Corporate Secretary |

Form 6-K Exhibit Index

| Exhibit No. |

||

| 99.1 | 2014 Annual Report | |

Exhibit 99.1

|

A transformative year | |||

|

2014 was a remarkable year for Encana. The successful execution of the strategy, which is built around a disciplined focus on profitable growth, saw the company complete virtually all of its key deliverables two years ahead of schedule. The speed of this achievement demonstrates the effectiveness of the strategy and the highly driven culture built by Doug Suttles and his leadership team.

Entering the year, Encana embarked on the right course of action at the right time by restructuring and resizing its organization, resulting in an approximately 25 percent workforce reduction. The company modified core processes such as capital allocation which led to a focused investment on seven growth assets, down from almost 30 funded areas the prior year. Strong efficiency improvements across the company highlighted Encana’s relentless drive for operational excellence.

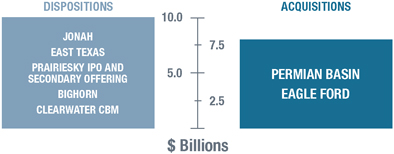

The year was also marked by the transformation of Encana’s portfolio with the divestiture of non-core assets, including the initial public offering and secondary offering of PrairieSky Royalty Ltd., coupled with major acquisitions in the top two oil plays in the U.S.; the Eagle Ford and the Permian Basin. These transactions have delivered a balanced liquids and natural gas portfolio and have made Encana more resilient to dynamic market conditions.

As Chairman of the Board, my focus is to continue our commitment to strong governance and corporate responsibility, while leading the Board of Directors in stewarding Encana towards building value for its shareholders. The Board of Directors continues to believe Encana’s strategy is the best way to grow profitability and maximize |

shareholder value over the long term. With commodity prices expected to be volatile through 2015, the company will continue to make prudent decisions to ensure it emerges even stronger from this downturn.

On behalf of the Board of Directors, I’d like to thank Encana’s Executive Leadership Team and staff. Their achievements through 2014 have put the company in a position of relative strength and on a path to sustainable success.

CLAYTON WOITAS CHAIRMAN OF THE BOARD | |||

1

2

PORTFOLIO TRANSFORMATION

In 2014, we completed around $18 billion of acquisition and divestiture activity and built a balanced commodity portfolio, rich with investment opportunities in premium positions in Canada and the United States. We focused around 86 percent of our capital investment toward seven growth assets, down from nearly 30 assets the previous year.

Creating a focused, balanced and higher margin portfolio

We dramatically reshaped our portfolio and replaced lower margin natural gas production with higher margin liquids. We divested non-core assets and acquired two strategic assets in two of North America’s best oil plays.

61 percent increase in liquids production

We grew total annual production from 54,000 bbls/d in 2013 to 87,000 bbls/d in 2014. Our five original growth assets; Montney, Duvernay, DJ Basin, San Juan and Tuscaloosa Marine Shale performed exceptionally. The acquisition of two new growth assets; in the Eagle Ford and the Permian Basin, made an immediate contribution to our liquids production.

Shifting to higher value production

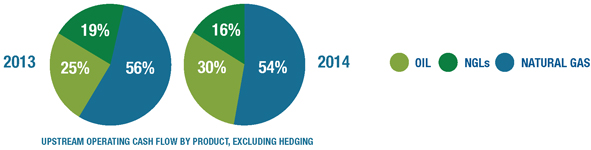

We are focused on high value production rather than production volume growth. In 2014, we delivered a 14 percent increase in year-over-year cash flow. We delivered this cash flow growth on approximately seven percent lower total production in a similar commodity price environment compared to 2013.

3

|

Efficient, competitive and resilient | |||

|

The transformation we undertook through 2014 occurred at a pace that surpassed our own high expectations. The result of our hard work is a competitive, resilient, low-cost and lean Encana. We have a focused portfolio rich with investment opportunities and premium positions in two of the best resource plays in Canada; the Montney and the Duvernay, and two of the best in the United States; the Eagle Ford and the Permian Basin.

The steps we took during 2014 were designed to deliver sustainable value to our shareholders by growing cash flow per share. We focused on higher value production rather than volume growth and directed our capital investment toward assets with scale and low supply costs – in short, the assets that provide the highest returns. This capital discipline was complemented by around $18 billion of acquisition and divestiture activity, which enabled us to dramatically reshape our portfolio and replace lower margin natural gas production with higher margin liquids.

Our cultural change has been just as dramatic and important to the transformation of the company. By embracing our values of One, Agile and Driven, our staff has harnessed the technical strength, knowledge and stability of a large organization, while adopting the mindset of a small, entrepreneurial company. They continue to relentlessly identify and implement ways to enhance efficiencies and streamline processes. In addition, in 2014 they delivered the best ever safety record in company history; an impressive accomplishment during a period of significant change.

The recent market volatility is a sharp reminder that we are in the commodity business. While we did not predict the recent drop in commodity prices, we knew that it was a possibility sometime during the execution of our long-term strategy. |

With this in mind, our strategy was designed to create a competitive and resilient company able to deliver shareholder value through commodity price cycles.

While oil traded at approximately $100 per barrel, our staff delivered material efficiency improvements throughout the company. In a lower price environment, we see significant opportunity to deliver further enduring efficiencies.

We will continue to take a prudent view of commodity prices and will protect our balance sheet throughout 2015 by exercising strict financial discipline. Equally important, we will maintain a capital allocation philosophy that is consistent with our strategy by prioritizing investment to our four most strategic assets: the Eagle Ford, Permian Basin, Montney and Duvernay.

Our team’s accomplishments in 2014 should not be overshadowed by today’s low commodity environment. In fact, it makes their achievements even more important. We are in a position of relative strength with a culture and strategy that keep us on the path to becoming a leading North American resource play company.

On behalf of the Executive Leadership Team, I want to thank our Board of Directors for their ongoing support and say a special thank you to all Encana staff for a remarkable 2014.

DOUG SUTTLES PRESIDENT & CEO | |||

5

|

PILLARS |

||||

|

Encana is structured and organized around four core competencies that we believe every exploration and production company needs to excel at in order to deliver sustainable shareholder value.

|

| |||

|

TOP TIER ASSETS |

CAPITAL ALLOCATION |

|||

|

We will always be on the lookout for the best rocks and focus our capital on a limited number of core growth assets characterized by high returns, scale and running room. Our strategy is centered on diversifying our commodity mix and growing value in top tier assets.

|

A highly disciplined, dynamic and centrally controlled capital allocation program will help ensure that we are directing our investment dollars in a manner that is consistent with our strategy. By concentrating capital on our core growth assets, we believe we can generate the most value for our shareholders. |

|||

|

MARKET FUNDAMENTALS |

OPERATIONAL EXCELLENCE |

|||

|

We will actively monitor and manage the effects of market volatility to enable us to respond to the ever-changing trade winds inherent in the oil and gas business. Leveraging our industry-leading commodity market expertise to inform our capital allocation decisions is critical to both managing risk and maximizing margins. |

Operational excellence is one of Encana’s strengths and we will continuously work to maintain this competitive advantage. We strive to increase profitability by running our operations in the most efficient and cost effective manner possible. Our best-in-class operators will focus on efficiency, safety and integrated and collaborative thinking in order to maximize value across our asset base.

|

|||

|

BALANCE SHEET STRENGTH |

||||

|

Underpinning these four core competencies is balance sheet strength. Maintaining financial flexibility and investment grade credit ratings are an important part of how we think about managing our business. Balance sheet strength allows us to capitalize on opportunities as they arise and demonstrates the sustainability of our business model through commodity cycles. |

||||

6

FOCUSED INVESTMENT

Our portfolio is rich with high quality oil, natural gas liquids and natural gas investment opportunities. Around 80 percent of our 2015 capital program is expected to be focused on our four most strategic growth assets: the Eagle Ford, Permian Basin, Montney and Duvernay.

7

| 8 |

| 9 |

| Annual Report 2014 | Encana Corporation 11 |

| 12 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 13 |

| 14 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 15 |

| 16 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 17 |

| 18 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 19 |

| 20 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 21 |

| 22 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 23 |

| 24 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 25 |

| 26 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 27 |

| 28 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 29 |

| 30 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 31 |

| 32 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 33 |

| 34 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 35 |

| 36 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 37 |

| 38 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 39 |

| 40 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 41 |

| 42 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 43 |

| 44 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 45 |

| 46 Encana Corporation | Annual Report 2014 |

| Annual Report 2014 | Encana Corporation 47 |

| 48 Encana Corporation | Annual Report 2014 |

| MANAGEMENT REPORT

|

|

Management’s Responsibility for Consolidated Financial Statements

The accompanying Consolidated Financial Statements of Encana Corporation (the “Company”) are the responsibility of Management. The Consolidated Financial Statements have been prepared by Management in United States dollars in accordance with generally accepted accounting principles in the United States and include certain estimates that reflect Management’s best judgments.

The Company’s Board of Directors has approved the information contained in the Consolidated Financial Statements. The Board of Directors fulfills its responsibility regarding the financial statements mainly through its Audit Committee, which has a written mandate that complies with the current requirements of Canadian securities legislation and the United States Sarbanes-Oxley Act of 2002 and voluntarily complies, in principle, with the Audit Committee guidelines of the New York Stock Exchange. The Audit Committee meets at least on a quarterly basis.

Management’s Assessment of Internal Control over Financial Reporting

Management is also responsible for establishing and maintaining adequate internal control over the Company’s financial reporting. The internal control system was designed to provide reasonable assurance to the Company’s Management regarding the preparation and presentation of the Consolidated Financial Statements.

Internal control systems, no matter how well designed, have inherent limitations. Therefore, even those systems determined to be effective can provide only reasonable assurance with respect to financial statement preparation and presentation. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Management has assessed the design and effectiveness of the Company’s internal control over financial reporting as at December 31, 2014. In making its assessment, Management has used the Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission to evaluate the effectiveness of the Company’s internal control over financial reporting. Based on our evaluation, Management has concluded that the Company’s internal control over financial reporting was effectively designed and operating effectively as at that date.

Management has excluded Athlon Energy Inc. from its assessment of internal control over financial reporting as at December 31, 2014 because it was acquired by the Company through a business combination during 2014. Assets attributable to Athlon Energy Inc. as of December 31, 2014 represented approximately 13 percent of the Company’s total assets as of December 31, 2014, and revenues attributable to Athlon Energy Inc. for the period from November 13, 2014 to December 31, 2014 represented approximately 2 percent of the Company’s total revenues for the year ended December 31, 2014.

PricewaterhouseCoopers LLP, an independent firm of chartered accountants, was appointed by a vote of shareholders at the Company’s last annual meeting to audit and provide independent opinions on both the Consolidated Financial Statements and the Company’s internal control over financial reporting as at December 31, 2014, as stated in their Auditor’s Report. PricewaterhouseCoopers LLP has provided such opinions.

|

| |||

| Douglas J. Suttles | Sherri A. Brillon | |||

| President & Chief Executive Officer | Executive Vice-President & Chief Financial Officer | |||

| March 3, 2015 | ||||

Annual Report 2014 | Encana Corporation 49

|

AUDITOR’S REPORT

|

INDEPENDENT AUDITOR’S REPORT

To the Shareholders of Encana Corporation

We have completed an integrated audit of Encana Corporation’s 2014, 2013 and 2012 Consolidated Financial Statements and its internal control over financial reporting as at December 31, 2014. Our opinions, based on our audits, are presented below.

Report on the Consolidated Financial Statements

We have audited the accompanying Consolidated Financial Statements of Encana Corporation, which comprise the Consolidated Balance Sheet as at December 31, 2014 and December 31, 2013 and the Consolidated Statements of Earnings, Comprehensive Income, Changes in Shareholders’ Equity and Cash Flows for each of the three years in the period ended December 31, 2014, and the related notes, which comprise a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these Consolidated Financial Statements in accordance with accounting principles generally accepted in the United States of America and for such internal control as management determines is necessary to enable the preparation of Consolidated Financial Statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these Consolidated Financial Statements based on our audits. We conducted our audits as at December 31, 2014 and December 31, 2013 and for the years then ended in accordance with Canadian generally accepted auditing standards and the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the Consolidated Financial Statements are free from material misstatement. Canadian generally accepted auditing standards also require that we comply with ethical requirements.

An audit involves performing procedures to obtain audit evidence, on a test basis, about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the company’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances. An audit also includes evaluating the appropriateness of accounting principles and policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion on the Consolidated Financial Statements.

Opinion

In our opinion, the Consolidated Financial Statements present fairly, in all material respects, the financial position of Encana Corporation and its subsidiaries as at December 31, 2014 and December 31, 2013 and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2014 in accordance with accounting principles generally accepted in the United States of America.

50 Encana Corporation | Annual Report 2014

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

We have also audited Encana Corporation and its subsidiaries’ internal control over financial reporting as at December 31, 2014, based on criteria established in Internal Control – Integrated Framework (2013), issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”).

Management’s Responsibility for Internal Control over Financial Reporting

Management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting included in the accompanying Management’s Assessment of Internal Control over Financial Reporting.

Auditor’s Responsibility

Our responsibility is to express an opinion on the company’s internal control over financial reporting based on our audit. We conducted our audit of internal control over financial reporting in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects.

An audit of internal control over financial reporting includes obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, testing and evaluating the design and operating effectiveness of internal control based on the assessed risk, and performing such other procedures as we consider necessary in the circumstances.

We believe that our audit provides a reasonable basis for our audit opinion on the company’s internal control over financial reporting.

Definition of Internal Control over Financial Reporting

A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial reporting includes those policies and procedures that: (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Inherent Limitations

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions or that the degree of compliance with the policies or procedures may deteriorate.

As described in Management’s Report on Internal Control over Financial Reporting, management has excluded Athlon Energy Inc. from its assessment of internal control over financial reporting as at December 31, 2014 because it was acquired by the Company through a business combination during 2014. We have also excluded Athlon Energy Inc. from our audit of internal control over financial reporting. Assets attributable to Athlon Energy Inc. as of December 31, 2014 represented approximately 13 percent of the Company’s total assets as of December 31, 2014, and revenues attributable to Athlon Energy Inc. for the period from November 13, 2014 to December 31, 2014 represented approximately 2 percent of the Company’s total revenues for the year ended December 31, 2014.

Opinion

In our opinion, Encana Corporation and its subsidiaries maintained, in all material respects, effective internal control over financial reporting as at December 31, 2014, based on criteria established in Internal Control – Integrated Framework (2013) issued by COSO.

|

| PricewaterhouseCoopers LLP |

| Chartered Accountants |

| Calgary, Alberta, Canada |

| March 3, 2015 |

| Annual Report 2014 | Encana Corporation 51 |

|

CONSOLIDATED STATEMENT OF EARNINGS

|

| For the years ended December 31 ($ millions, except per share amounts) |

2014 | 2013 | 2012 | |||||||||||||

| Revenues, Net of Royalties |

(Note 2 | ) | $ | 8,019 | $ | 5,858 | $ | 5,160 | ||||||||

| Expenses |

(Note 2 | ) | ||||||||||||||

| Production and mineral taxes |

133 | 134 | 105 | |||||||||||||

| Transportation and processing |

1,505 | 1,476 | 1,231 | |||||||||||||

| Operating |

735 | 859 | 794 | |||||||||||||

| Purchased product |

1,191 | 441 | 349 | |||||||||||||

| Depreciation, depletion and amortization |

1,745 | 1,565 | 1,956 | |||||||||||||

| Impairments |

(Note 9 | ) | — | 21 | 4,695 | |||||||||||

| Accretion of asset retirement obligation |

(Note 15 | ) | 52 | 53 | 53 | |||||||||||

| Administrative |

(Note 19 | ) | 327 | 439 | 392 | |||||||||||

| Interest |

(Note 5 | ) | 654 | 563 | 522 | |||||||||||

| Foreign exchange (gain) loss, net |

(Note 6 | ) | 403 | 325 | (107 | ) | ||||||||||

| (Gain) loss on divestitures |

(Notes 4,18 | ) | (3,426 | ) | (7 | ) | — | |||||||||

| Other |

(Note 3 | ) | 71 | 1 | 1 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| 3,390 | 5,870 | 9,991 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Net Earnings (Loss) Before Income Tax |

4,629 | (12 | ) | (4,831 | ) | |||||||||||

| Income tax expense (recovery) |

(Note 7 | ) | 1,203 | (248 | ) | (2,037 | ) | |||||||||

|

|

|

|

|

|

|

|||||||||||

| Net Earnings (Loss) |

3,426 | 236 | (2,794 | ) | ||||||||||||

| Net earnings attributable to noncontrolling interest |

(Note 18 | ) | (34 | ) | — | — | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Net Earnings (Loss) Attributable to Common Shareholders |

$ | 3,392 | $ | 236 | $ | (2,794 | ) | |||||||||

|

|

|

|

|

|

|

|||||||||||

| Net Earnings (Loss) per Common Share |

||||||||||||||||

| Basic & Diluted |

(Note 16 | ) | $ | 4.58 | $ | 0.32 | $ | (3.79 | ) | |||||||

CONSOLIDATED STATEMENT

OF COMPREHENSIVE INCOME

| For the years ended December 31 ($ millions) |

2014 | 2013 | 2012 | |||||||||||||

| Net Earnings (Loss) |

$ | 3,426 | $ | 236 | $ | (2,794 | ) | |||||||||

| Other Comprehensive Income (Loss), Net of Tax |

||||||||||||||||

| Foreign currency translation adjustment |

(Note 17 | ) | 22 | (46 | ) | 81 | ||||||||||

| Pension and other post-employment benefit plans |

(Notes 17,21 | ) | (17 | ) | 60 | 13 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Other Comprehensive Income |

5 | 14 | 94 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Comprehensive Income (Loss) |

3,431 | 250 | (2,700 | ) | ||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Comprehensive Income Attributable to Noncontrolling Interest |

(Note 18 | ) | (34 | ) | — | — | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Comprehensive Income (Loss) Attributable to Common Shareholders |

$ | 3,397 | $ | 250 | $ | (2,700 | ) | |||||||||

|

|

|

|

|

|

|

|||||||||||

See accompanying Notes to Consolidated Financial Statements

52 Encana Corporation | Annual Report 2014

| CONSOLIDATED BALANCE SHEET

|

|

| As at December 31 ($ millions) |

2014 | 2013 | ||||||||||

| Assets |

||||||||||||

| Current Assets |

||||||||||||

| Cash and cash equivalents |

$ | 338 | $ | 2,566 | ||||||||

| Accounts receivable and accrued revenues |

(Note 8 | ) | 1,307 | 988 | ||||||||

| Risk management |

(Note 23 | ) | 707 | 56 | ||||||||

| Income tax receivable |

509 | 562 | ||||||||||

| Deferred income taxes |

(Note 7 | ) | — | 118 | ||||||||

|

|

|

|

|

|||||||||

| 2,861 | 4,290 | |||||||||||

| Property, Plant and Equipment, at cost: |

(Note 9 | ) | ||||||||||

| Natural gas and oil properties, based on full cost accounting |

||||||||||||

| Proved properties |

42,615 | 51,603 | ||||||||||

| Unproved properties |

6,133 | 1,068 | ||||||||||

| Other |

2,711 | 3,148 | ||||||||||

|

|

|

|

|

|||||||||

| Property, plant and equipment |

51,459 | 55,819 | ||||||||||

| Less: Accumulated depreciation, depletion and amortization |

(33,444 | ) | (45,784 | ) | ||||||||

|

|

|

|

|

|||||||||

| Property, plant and equipment, net |

(Note 2 | ) | 18,015 | 10,035 | ||||||||

| Cash in Reserve |

73 | 10 | ||||||||||

| Other Assets |

(Note 10 | ) | 394 | 526 | ||||||||

| Risk Management |

(Note 23 | ) | 65 | 204 | ||||||||

| Deferred Income Taxes |

(Note 7 | ) | 296 | 939 | ||||||||

| Goodwill |

(Notes 2, 3, 4, 11, 18 | ) | 2,917 | 1,644 | ||||||||

|

|

|

|

|

|||||||||

| (Note 2 | ) | $ | 24,621 | $ | 17,648 | |||||||

|

|

|

|

|

|||||||||

| Liabilities and Shareholders’ Equity |

||||||||||||

| Current Liabilities |

||||||||||||

| Accounts payable and accrued liabilities |

(Note 12 | ) | $ | 2,243 | $ | 1,895 | ||||||

| Income tax payable |

15 | 29 | ||||||||||

| Risk management |

(Note 23 | ) | 20 | 25 | ||||||||

| Current portion of long-term debt |

(Note 13 | ) | — | 1,000 | ||||||||

| Deferred income taxes |

(Note 7 | ) | 128 | 3 | ||||||||

|

|

|

|

|

|||||||||

| 2,406 | 2,952 | |||||||||||

| Long-Term Debt |

(Note 13 | ) | 7,340 | 6,124 | ||||||||

| Other Liabilities and Provisions |

(Note 14 | ) | 2,484 | 2,520 | ||||||||

| Risk Management |

(Note 23 | ) | 7 | 5 | ||||||||

| Asset Retirement Obligation |

(Note 15 | ) | 870 | 900 | ||||||||

| Deferred Income Taxes |

(Note 7 | ) | 1,829 | — | ||||||||

|

|

|

|

|

|||||||||

| 14,936 | 12,501 | |||||||||||

|

|

|

|

|

|||||||||

| Commitments and Contingencies |

(Note 25 | ) | ||||||||||

| Shareholders’ Equity |

||||||||||||

| Share capital – authorized unlimited common shares, without par value 2014 issued and outstanding: 741.2 million shares (2013: 740.9 million shares) |

(Note 16 | ) | 2,450 | 2,445 | ||||||||

| Paid in surplus |

(Notes 16, 18, 20 | ) | 1,358 | 15 | ||||||||

| Retained earnings |

5,188 | 2,003 | ||||||||||

| Accumulated other comprehensive income |

(Note 17 | ) | 689 | 684 | ||||||||

|

|

|

|

|

|||||||||

| Total Shareholders’ Equity |

9,685 | 5,147 | ||||||||||

|

|

|

|

|

|||||||||

| $ | 24,621 | $ | 17,648 | |||||||||

|

|

|

|

|

|||||||||

See accompanying Notes to Consolidated Financial Statements

Approved by the Board of Directors

|

| |||

| Clayton H. Woitas | Jane L. Peverett | |||

| Director | Director | |||

Annual Report 2014 | Encana Corporation 53

|

CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

|

| For the year ended December 31, 2014 ($ millions) |

Share Capital |

Paid in Surplus |

Retained Earnings |

Accumulated Other Comprehensive Income |

Non- Controlling Interest |

Total Shareholders’ Equity |

||||||||||||||||||||||

| Balance, December 31, 2013 |

$ | 2,445 | $ | 15 | $ | 2,003 | $ | 684 | $ | — | $ | 5,147 | ||||||||||||||||

| Share-Based Compensation |

(Note 20 | ) | — | (2 | ) | — | — | — | (2 | ) | ||||||||||||||||||

| Net Earnings (Loss) |

— | — | 3,392 | — | 34 | 3,426 | ||||||||||||||||||||||

| Dividends on Common Shares |

(Note 16 | ) | — | — | (207 | ) | — | — | (207 | ) | ||||||||||||||||||

| Common Shares Issued Under Dividend Reinvestment Plan |

(Note 16 | ) | 5 | — | — | — | — | 5 | ||||||||||||||||||||

| Other Comprehensive Income |

(Note 17 | ) | — | — | — | 5 | — | 5 | ||||||||||||||||||||

| Sale of Noncontrolling Interest |

(Note 18 | ) | — | 1,345 | — | — | 117 | 1,462 | ||||||||||||||||||||

| Distributions to Noncontrolling Interest Owners |

(Note 18 | ) | — | — | — | — | (18 | ) | (18 | ) | ||||||||||||||||||

| Sale of Investment in PrairieSky |

(Note 18 | ) | — | — | — | — | (133 | ) | (133 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Balance, December 31, 2014 |

$ | 2,450 | $ | 1,358 | $ | 5,188 | $ | 689 | $ | — | $ | 9,685 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| For the year ended December 31, 2013 ($ millions) |

Share Capital |

Paid in Surplus |

Retained Earnings |

Accumulated Other Comprehensive Income |

Non- Controlling Interest |

Total Shareholders’ Equity |

||||||||||||||||||||||

| Balance, December 31, 2012 |

$ | 2,354 | $ | 10 | $ | 2,261 | $ | 670 | $ | — | $ | 5,295 | ||||||||||||||||

| Share-Based Compensation |

(Note 20 | ) | — | 3 | — | — | — | 3 | ||||||||||||||||||||

| Net Earnings (Loss) |

— | — | 236 | — | — | 236 | ||||||||||||||||||||||

| Common Shares Cancelled |

(Note 16 | ) | (2 | ) | 2 | — | — | — | — | |||||||||||||||||||

| Dividends on Common Shares |

(Note 16 | ) | — | — | (494 | ) | — | — | (494 | ) | ||||||||||||||||||

| Common Shares Issued Under Dividend Reinvestment Plan |

(Note 16 | ) | 93 | — | — | — | — | 93 | ||||||||||||||||||||

| Other Comprehensive Income |

(Note 17 | ) | — | — | — | 14 | — | 14 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Balance, December 31, 2013 |

$ | 2,445 | $ | 15 | $ | 2,003 | $ | 684 | $ | — | $ | 5,147 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| For the year ended December 31, 2012 ($ millions) |

Share Capital |

Paid in Surplus |

Retained Earnings |

Accumulated Other Comprehensive Income |

Non- Controlling Interest |

Total Shareholders’ Equity |

||||||||||||||||||||||

| Balance, December 31, 2011 |

$ | 2,354 | $ | 5 | $ | 5,643 | $ | 576 | $ | — | $ | 8,578 | ||||||||||||||||

| Share-Based Compensation |

(Note 20 | ) | — | 5 | — | — | — | 5 | ||||||||||||||||||||

| Net Earnings (Loss) |

— | — | (2,794 | ) | — | — | (2,794 | ) | ||||||||||||||||||||

| Dividends on Common Shares |

(Note 16 | ) | — | — | (588 | ) | — | — | (588 | ) | ||||||||||||||||||

| Other Comprehensive Income |

— | — | — | 94 | — | 94 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Balance, December 31, 2012 |

$ | 2,354 | $ | 10 | $ | 2,261 | $ | 670 | $ | — | $ | 5,295 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

See accompanying Notes to Consolidated Financial Statements

54 Encana Corporation | Annual Report 2014

| CONSOLIDATED STATEMENT OF CASH FLOWS

|

|

| For the years ended December 31 ($ millions) |

2014 | 2013 | 2012 | |||||||||||||

| Operating Activities |

||||||||||||||||

| Net earnings (loss) |

$ | 3,426 | $ | 236 | $ | (2,794 | ) | |||||||||

| Depreciation, depletion and amortization |

1,745 | 1,565 | 1,956 | |||||||||||||

| Impairments |

(Note 9 | ) | — | 21 | 4,695 | |||||||||||

| Accretion of asset retirement obligation |

(Note 15 | ) | 52 | 53 | 53 | |||||||||||

| Deferred income taxes |

(Note 7 | ) | 960 | (57 | ) | (1,837 | ) | |||||||||

| Unrealized (gain) loss on risk management |

(Note 23 | ) | (444 | ) | 345 | 1,465 | ||||||||||

| Unrealized foreign exchange (gain) loss |

(Note 6 | ) | 440 | 330 | (112 | ) | ||||||||||

| (Gain) loss on divestitures |

(Notes 4,18 | ) | (3,426 | ) | (7 | ) | — | |||||||||

| Other |

(34 | ) | 62 | 82 | ||||||||||||

| Net change in other assets and liabilities |

(43 | ) | (80 | ) | (78 | ) | ||||||||||

| Net change in non-cash working capital |

(Note 24 | ) | (9 | ) | (179 | ) | (323 | ) | ||||||||

|

|

|

|

|

|

|

|||||||||||

| Cash From (Used in) Operating Activities |

2,667 | 2,289 | 3,107 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Investing Activities |

||||||||||||||||

| Capital expenditures |

(Note 2 | ) | (2,526 | ) | (2,712 | ) | (3,476 | ) | ||||||||

| Acquisitions |

(Note 4 | ) | (3,016 | ) | (184 | ) | (379 | ) | ||||||||

| Corporate acquisition |

(Note 3 | ) | (5,962 | ) | — | — | ||||||||||

| Proceeds from divestitures |

(Note 4 | ) | 4,345 | 705 | 4,043 | |||||||||||

| Proceeds from sale of investment in PrairieSky |

(Notes 4,18 | ) | 2,172 | — | — | |||||||||||

| Cash in reserve |

(63 | ) | 44 | 415 | ||||||||||||

| Net change in investments and other |

321 | 252 | (242 | ) | ||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Cash From (Used in) Investing Activities |

(4,729 | ) | (1,895 | ) | 361 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Financing Activities |

||||||||||||||||

| Issuance of revolving long-term debt |

(Notes 13,23 | ) | 1,277 | — | 1,721 | |||||||||||

| Repayment of revolving long-term debt |

(Note 3 | ) | (335 | ) | — | (1,724 | ) | |||||||||

| Repayment of long-term debt |

(Note 13 | ) | (2,152 | ) | (500 | ) | (503 | ) | ||||||||

| Dividends on common shares |

(Note 16 | ) | (202 | ) | (401 | ) | (588 | ) | ||||||||

| Proceeds from sale of noncontrolling interest |

(Note 18 | ) | 1,462 | — | — | |||||||||||

| Distributions to noncontrolling interest owners |

(Note 18 | ) | (18 | ) | — | — | ||||||||||

| Capital lease payments and other financing arrangements |

(Note 9 | ) | (71 | ) | (8 | ) | (17 | ) | ||||||||

|

|

|

|

|

|

|

|||||||||||

| Cash From (Used in) Financing Activities |

(39 | ) | (909 | ) | (1,111 | ) | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Foreign Exchange Gain (Loss) on Cash and Cash Equivalents Held in Foreign Currency |

(127 | ) | (98 | ) | 22 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Increase (Decrease) in Cash and Cash Equivalents |

(2,228 | ) | (613 | ) | 2,379 | |||||||||||

| Cash and Cash Equivalents, Beginning of Year |

2,566 | 3,179 | 800 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Cash and Cash Equivalents, End of Year |

$ | 338 | $ | 2,566 | $ | 3,179 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Cash, End of Year |

$ | 142 | $ | 161 | $ | 92 | ||||||||||

| Cash Equivalents, End of Year |

196 | 2,405 | 3,087 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Cash and Cash Equivalents, End of Year |

$ | 338 | $ | 2,566 | $ | 3,179 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Supplementary Cash Flow Information | (Note 24 | ) | ||||||||||||||

See accompanying Notes to Consolidated Financial Statements

Annual Report 2014 | Encana Corporation 55

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A) NATURE OF OPERATIONS

Encana Corporation and its subsidiaries (“Encana” or the “Company”) are in the business of the exploration for, the development of, and the production and marketing of natural gas, oil and natural gas liquids (“NGLs”). The term liquids is used to represent Encana’s oil, NGLs and condensate.

B) BASIS OF PRESENTATION

The Consolidated Financial Statements include the accounts of Encana and are presented in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”).

In these Consolidated Financial Statements, unless otherwise indicated, all dollar amounts are expressed in United States (“U.S.”) dollars. Encana’s financial results are consolidated in Canadian dollars; however, the Company has adopted the U.S. dollar as its reporting currency to facilitate a more direct comparison to other North American oil and gas companies. All references to US$ or to $ are to United States dollars and references to C$ are to Canadian dollars.

C) PRINCIPLES OF CONSOLIDATION

The Consolidated Financial Statements include the accounts of Encana and entities in which it holds a controlling interest. The noncontrolling interest represented the third party equity ownership in a former consolidated subsidiary, PrairieSky Royalty Ltd. (“PrairieSky”). See Note 18 for further details regarding the noncontrolling interest. As of September 26, 2014, Encana no longer holds an interest in PrairieSky. All intercompany balances and transactions are eliminated on consolidation. For upstream joint interest operations where Encana retains an undivided interest in jointly owned property, the Company records its proportionate share of assets, liabilities, revenues and expenses. Investments in non-controlled entities over which Encana has the ability to exercise significant influence are accounted for using the equity method.

D) FOREIGN CURRENCY TRANSLATION

Monetary assets and liabilities of the Company that are denominated in foreign currencies are translated at the rates of exchange in effect at the period end date. Any gains or losses are recorded in the Consolidated Statement of Earnings. Foreign currency revenues and expenses are translated at the rates of exchange in effect at the time of the transaction.

Assets and liabilities of foreign operations are translated at period end exchange rates, while the related revenues and expenses are translated using average rates over the period. Translation gains and losses relating to the foreign operations are included in accumulated other comprehensive income (“AOCI”). Recognition of Encana’s accumulated translation gains and losses into net earnings occurs upon complete or substantially complete liquidation of the Company’s investment in the foreign operation.

For financial statement presentation, assets and liabilities are translated into the reporting currency at period end exchange rates, while revenues and expenses are translated using average rates over the period. Gains and losses relating to the financial statement translation are included in AOCI.

E) USE OF ESTIMATES

Preparation of the Consolidated Financial Statements in conformity with U.S. GAAP requires Management to make informed estimates and assumptions and use judgments that affect reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the Consolidated Financial Statements and the reported amounts of revenues and expenses during the period. Such estimates primarily relate to unsettled transactions and events as of the date of the Consolidated Financial Statements. Accordingly, actual results may differ from estimated amounts as future events occur.

Significant items subject to estimates and assumptions are:

| • | Estimates of proved reserves and related future cash flows used for depletion and ceiling test impairment calculations |

| • | Estimated fair value of long-term assets used for impairment calculations |

| • | Fair value of reporting units used for the assessment of goodwill |

| • | Estimates of future taxable earnings used to assess the realizable value of deferred tax assets |

| • | Fair value of asset retirement obligations and costs |

| • | Fair value of derivative instruments |

| • | Fair value attributed to assets acquired and liabilities assumed in business combinations |

| • | Tax interpretations, regulations and legislation in the various jurisdictions in which the Company and its subsidiaries operate |

| • | Accruals for long-term performance-based compensation arrangements, including whether or not the performance criteria will be met and measurement of the ultimate payout amount |

| • | Recognized values of pension assets and obligations, as well as the pension costs charged to net earnings, depend on certain actuarial and economic assumptions |

| • | Accruals for legal claims, environmental risks and exposures |

56 Encana Corporation | Annual Report 2014

F) REVENUE RECOGNITION

Revenues associated with Encana’s natural gas and liquids are recognized when production is sold to a purchaser at a fixed or determinable price, delivery has occurred, title has transferred and collectability of the revenue is probable. Realized gains and losses from the Company’s financial derivatives related to natural gas and oil commodity prices are recognized in revenue when the contract is settled. Unrealized gains and losses related to these contracts are recognized in revenue based on the changes in fair value of the contracts at the end of the respective periods.

Market optimization revenues and purchased product expenses are recorded on a gross basis when Encana takes title to the product and has the risks and rewards of ownership. Purchases and sales of products that are entered into in contemplation of each other with the same counterparty are recorded on a net basis. Revenues associated with the services provided where Encana acts as agent are recorded as the services are provided.

G) PRODUCTION AND MINERAL TAXES

Costs paid by Encana to certain mineral and non-mineral interest owners based on production of natural gas and liquids are recognized when the product is produced.

H) TRANSPORTATION AND PROCESSING

Costs paid by Encana for the transportation and processing of natural gas and liquids are recognized when the product is delivered and the services provided.

I) OPERATING

Operating costs paid by Encana for oil and gas properties in which the Company has a working interest. Expenses are net of amounts capitalized in accordance with the full cost method of accounting.

J) EMPLOYEE BENEFIT PLANS

The Company sponsors defined contribution and defined benefit plans, providing pension and other post-employment benefits to its employees in Canada and the U.S. As of January 1, 2003, the defined benefit pension plan was closed to new entrants.

Pension expense for the defined contribution pension plan is recorded as the benefits are earned by the employees covered by the plans. Encana accrues for its obligations under its employee defined benefit plans, net of plan assets. The cost of defined benefit pensions and other post-employment benefits is actuarially determined using the projected benefit method based on length of service and reflects Management’s best estimate of salary escalation, retirement ages of employees and expected future health care costs. The expected return on plan assets is based on historical and projected rates of return for assets in the investment plan portfolio. The actual return is based on the fair value of plan assets. The projected benefit obligation is discounted using the market interest rate on high-quality corporate debt instruments as at the measurement date.

Pension expense for the defined benefit pension plan includes the cost of pension benefits earned during the current year, the interest cost on pension obligations, the expected return on pension plan assets, the amortization of the net transitional obligation, the amortization of adjustments arising from pension plan amendments, the amortization of prior service costs, and the amortization of the excess of the net actuarial gain or loss over 10 percent of the greater of the benefit obligation and the fair value of plan assets. Amortization is on a straight-line basis over a period covering the expected average remaining service lives of employees covered by the plans. Actuarial gains and losses related to the change in the over-funded or under-funded status of the defined benefit pension plan and other post-employment benefit plans are recognized in other comprehensive income.

K) INCOME TAXES

Encana follows the liability method of accounting for income taxes. Under this method, deferred income taxes are recorded for the effect of any temporary difference between the accounting and income tax basis of an asset or liability, using the enacted income tax rates and laws expected to apply when the assets are realized and liabilities are settled. Current income taxes are measured at the amount expected to be recoverable from or payable to the taxation authorities based on the income tax rates and laws enacted at the end of the reporting period. The effect of a change in the enacted tax rates or laws is recognized in net earnings in the period of enactment. Income taxes are recognized in net earnings except to the extent that they relate to items recognized directly in shareholders’ equity, in which case the income taxes are recognized directly in shareholders’ equity.

Deferred income tax assets are routinely assessed for realizability. If it is more likely than not that deferred tax assets will not be realized, a valuation allowance is recorded to reduce the deferred tax assets. Encana considers available positive and negative evidence when assessing the realizability of deferred tax assets including historic and expected future taxable earnings, available tax planning strategies and carry forward periods. The assumptions used in determining expected future taxable earnings are consistent with those used in the goodwill impairment assessment.

Encana recognizes the financial statement effects of a tax position when it is more likely than not, based on the technical merits, that the position will be sustained upon examination by a taxing authority. A recognized tax position is initially and subsequently measured as the largest amount of tax benefit that is greater than 50 percent likely of being realized upon settlement with a taxing authority. Liabilities for unrecognized tax benefits that are not expected to be settled within the next 12 months are included in other liabilities and provisions.

Annual Report 2014 | Encana Corporation 57

L) EARNINGS PER SHARE AMOUNTS

Basic net earnings per common share is computed by dividing the net earnings by the weighted average number of common shares outstanding during the period. Diluted net earnings per common share amounts are calculated giving effect to the potential dilution that would occur if stock options were exercised or other contracts to issue common shares were exercised, fully vested, or converted to common shares. The treasury stock method is used to determine the dilutive effect of stock options and other dilutive instruments. The treasury stock method assumes that proceeds received from the exercise of in-the-money stock options and other dilutive instruments are used to repurchase common shares at the average market price.

M) CASH AND CASH EQUIVALENTS

Cash and cash equivalents include cash on hand and short-term investments, such as money market deposits or similar type instruments, with a maturity of three months or less when purchased. Outstanding disbursements issued in excess of applicable bank account balances are excluded from cash and cash equivalents and are recorded in accounts payable and accrued liabilities. Cash in reserve represents cash amounts segregated or held in escrow which are not available for general operating use.

N) PROPERTY, PLANT AND EQUIPMENT

UPSTREAM

Encana uses the full cost method of accounting for its acquisition, exploration and development activities. Under this method, all costs directly associated with the acquisition of, the exploration for, and the development of natural gas and liquids reserves are capitalized on a country-by-country cost centre basis. Capitalized costs exclude costs relating to production, general overhead or similar activities.

Under the full cost method of accounting, the carrying amount of Encana’s natural gas and oil properties within each country cost centre is subject to a ceiling test performed quarterly. A ceiling test impairment is recognized in net earnings when the carrying amount of a country cost centre exceeds the country cost centre ceiling. The carrying amount of a cost centre includes capitalized costs of proved oil and gas properties, net of accumulated depletion and the related deferred income taxes.

The cost centre ceiling is the sum of the estimated after-tax future net cash flows from proved reserves, using the 12-month average trailing prices and unescalated future development and production costs, discounted at 10 percent, plus unproved property costs. The 12-month average trailing price is calculated as the average of the price on the first day of each month within the trailing 12-month period. Any excess of the carrying amount over the calculated ceiling amount is recognized as an impairment in net earnings.

Capitalized costs accumulated within each cost centre are depleted using the unit-of-production method based on proved reserves. Depletion is calculated using the capitalized costs, including estimated retirement costs, plus the undiscounted future expenditures to be incurred in developing proved reserves.

Costs associated with unproved properties are excluded from the depletion calculation until it is determined that proved reserves are attributable or impairment has occurred. Unproved properties are assessed separately for impairment on a quarterly basis. Costs that have been impaired are included in the costs subject to depletion within the full cost pool.

Proceeds from the divestiture of properties are normally deducted from the full cost pool without recognition of gain or loss unless the deduction significantly alters the relationship between capitalized costs and proved reserves in the cost centre, in which case a gain or loss is recognized in net earnings. Generally, a gain or loss on a divestiture would be recognized when 25 percent or more of the Company’s proved reserves quantities in a particular country are sold. For divestitures that result in the recognition of a gain or loss on the sale and constitute a business, goodwill is allocated to the divestiture.

CORPORATE

Costs associated with office furniture, fixtures, leasehold improvements, information technology and aircraft are carried at cost and depreciated on a straight-line basis over the estimated service lives of the assets, which range from three to 25 years. Costs associated with The Bow office building are carried at cost and depreciated on a straight-line basis over the 60-year estimated life of the building. Assets under construction are not subject to depreciation until put into use. Land is carried at cost.

O) CAPITALIZATION OF COSTS

Expenditures related to renewals or betterments that improve the productive capacity or extend the life of an asset are capitalized. Maintenance and repairs are expensed as incurred. Interest is capitalized during the construction phase of major development projects.

58 Encana Corporation | Annual Report 2014

P) BUSINESS COMBINATIONS

Business combinations are accounted for using the acquisition method. The acquired identifiable net assets are measured at their fair value at the date of acquisition. Deferred taxes are recognized for any differences between the fair value of net assets acquired and their tax bases. Any excess of the purchase price over the fair value of the net assets acquired is recognized as goodwill. Any deficiency of the purchase price below the fair value of the net assets acquired is recorded as a gain in net earnings. Associated transaction costs are expensed when incurred.

Q) GOODWILL

Goodwill, which represents the excess of purchase price over fair value of net assets acquired, is assessed for impairment at least annually at December 31. Goodwill and all other assets and liabilities are allocated to reporting units, which are Encana’s country cost centres. To assess impairment, the carrying amount of each reporting unit is determined and compared to the fair value of the reporting unit. If the carrying amount of the reporting unit is higher than its related fair value then goodwill is written down to the reporting unit’s implied fair value of goodwill. The implied fair value of goodwill is determined by deducting the fair value of the reporting unit’s assets and liabilities from the fair value of the reporting unit as if the reporting entity had been acquired in a business combination. Any excess of the carrying value of goodwill over the implied fair value of goodwill is recognized as an impairment and charged to net earnings. Subsequent measurement of goodwill is at cost less any accumulated impairments.

R) IMPAIRMENT OF LONG-TERM ASSETS

The carrying value of long-term assets, excluding goodwill and upstream assets included in property, plant and equipment, are assessed for impairment when indicators suggest that the carrying value of an asset or asset group may not be recoverable. If the carrying amount exceeds the sum of the undiscounted cash flows expected to result from the continued use and eventual disposition of the asset or asset group, an impairment is recognized for the excess of the carrying amount over its estimated fair value.

S) ASSET RETIREMENT OBLIGATION

Asset retirement obligations are those legal obligations where the Company will be required to retire tangible long-lived assets such as producing well sites, offshore production platforms and natural gas processing plants. The fair value of estimated asset retirement obligations is recognized in the Consolidated Balance Sheet when incurred and a reasonable estimate of fair value can be made. The asset retirement cost, equal to the initially estimated fair value of the asset retirement obligation, is capitalized as part of the cost of the related long-lived asset. Changes in the estimated obligation resulting from revisions to estimated timing or amount of future cash flows are recognized as a change in the asset retirement obligation and the related asset retirement cost.

Amortization of asset retirement costs is included in depreciation, depletion and amortization in the Consolidated Statement of Earnings. Increases in the asset retirement obligations resulting from the passage of time are recorded as accretion of asset retirement obligation in the Consolidated Statement of Earnings.

Actual expenditures incurred are charged against the accumulated asset retirement obligation.

T) STOCK-BASED COMPENSATION

Obligations for payments of cash or common shares under Encana’s stock-based compensation plans are accrued over the vesting period, net of forfeitures, using fair values. Fair values are determined using observable share prices and/or pricing models such as the Black-Scholes-Merton option-pricing model. For equity-settled stock-based compensation plans, fair values are determined at the grant date and are recognized over the vesting period as compensation costs with a corresponding credit to shareholders’ equity. For cash-settled stock-based compensation plans, fair values are determined at each reporting date and periodic changes are recognized as compensation costs, with a corresponding change to liabilities.

Obligations for payments for share units of Cenovus Energy Inc. (“Cenovus”) held by Encana employees were accrued as compensation costs based on the fair value of the financial liability.

U) LEASES

Leases entered into for the use of an asset are classified as either capital or operating leases. Capital leases transfer to the Company substantially all of the risks and benefits incidental to ownership of the leased item. Capital leases are capitalized upon commencement of the lease term at the lower of the fair value of the leased asset or the present value of the minimum lease payments. Capitalized leased assets are amortized over the estimated useful life of the asset if the lease arrangement contains a bargain purchase option or ownership of the leased asset transfers at the end of the lease term. Otherwise, the leased assets are amortized over the lease term. Amortization of capitalized leased assets is included in depreciation, depletion and amortization in the Consolidated Statement of Earnings. All other leases are classified as operating leases and the payments are recognized on a straight-line basis over the lease term.

Annual Report 2014 | Encana Corporation 59

V) FAIR VALUE MEASUREMENTS

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Valuation techniques include the market, income, and cost approach. The market approach uses information generated by market transactions involving identical or comparable assets or liabilities; the income approach converts estimated future amounts to a present value; the cost approach is based on the amount that currently would be required to replace an asset.

Inputs used in determining fair value are characterized according to a hierarchy that prioritizes those inputs based on the degree to which they are observable. The three input levels of the fair value hierarchy are as follows:

| • | Level 1 – Inputs represent quoted prices in active markets for identical assets or liabilities, such as exchange-traded commodity derivatives. |

| • | Level 2 – Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly, such as quoted market prices for similar assets or liabilities in active markets or other market corroborated inputs. |

| • | Level 3 – Inputs that are not observable from objective sources, such as forward prices supported by little or no market activity or internally developed estimates of future cash flows used in a present value model. |

In determining fair value, the Company utilizes the most observable inputs available. If a fair value measurement reflects inputs at multiple levels within the hierarchy, the fair value measurement is characterized based on the lowest level of input that is significant to the fair value measurement.

The carrying amount of cash and cash equivalents, accounts receivable and accounts payable reported on the Consolidated Balance Sheet approximates fair value. The fair value of long-term debt is disclosed in Note 13. Fair value information related to pension plan assets is included in Note 21. Recurring fair value measurements are performed for risk management assets and liabilities and for share units issued as part of the Split Transaction, as discussed in Notes 16 and 22.

Certain non-financial assets and liabilities are initially measured at fair value, such as asset retirement obligations and assets and liabilities acquired in business combinations or certain non-monetary exchange transactions.

W) RISK MANAGEMENT ASSETS AND LIABILITIES

Risk management assets and liabilities are derivative financial instruments used by Encana to manage economic exposure to market risks relating to commodity prices, foreign currency exchange rates and interest rates. The use of these derivative instruments is governed under formal policies and is subject to limits established by the Board of Directors (“Board”). The Company’s policy is not to utilize derivative financial instruments for speculative purposes.

Derivative instruments that do not qualify for the normal purchases and sales exemption are measured at fair value with changes in fair value recognized in net earnings. The fair values recorded in the Consolidated Balance Sheet reflect netting the asset and liability positions where counterparty master netting arrangements contain provisions for net settlement. Realized gains or losses from financial derivatives related to natural gas and oil commodity prices are recognized in revenues as the contracts are settled. Realized gains or losses from financial derivatives related to power commodity prices are recognized in transportation and processing expense as the related power contracts are settled. Unrealized gains and losses are recognized in revenues and transportation and processing expense accordingly, at the end of each respective reporting period based on the changes in fair value of the contracts.

X) COMMITMENTS AND CONTINGENCIES

Liabilities for loss contingencies arising from claims, assessments, litigation, environmental and other sources are recorded when it is probable that a liability has been incurred and the amount can be reasonably estimated. These accruals are adjusted as additional information becomes available or circumstances change.

60 Encana Corporation | Annual Report 2014

Y) RECENT ACCOUNTING PRONOUNCEMENTS

CHANGES IN ACCOUNTING POLICIES AND PRACTICES

On January 1, 2014, Encana adopted the following Accounting Standards Updates (“ASU”) issued by the Financial Accounting Standards Board (“FASB”), which have not had a material impact on the Company’s Consolidated Financial Statements:

| • | ASU 2013-04, “Obligations Resulting from Joint and Several Liability Arrangements for Which the Total Amount of the Obligation is Fixed at the Reporting Date”, clarifies guidance for the recognition, measurement and disclosure of liabilities resulting from joint and several liability arrangements. The amendments have been applied retrospectively. |

| • | ASU 2013-05, “Parent’s Accounting for the Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity”, clarifies the applicable guidance for certain transactions that result in the release of the cumulative translation adjustment into net earnings. The amendments have been applied prospectively. |

| • | ASU 2013-11, “Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists”, clarifies that a liability related to an unrecognized tax benefit or portions thereof should be presented as a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss or a tax credit carryforward, except under specific situations. The amendments have been applied prospectively. |

NEW STANDARDS ISSUED NOT YET ADOPTED

| • | As of January 1, 2015, Encana will be required to adopt ASU 2014-08, “Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity”, which amends the criteria and expands the disclosures for reporting discontinued operations. Under the new criteria, only disposals representing a strategic shift in operations would qualify as a discontinued operation. The amendments will be applied prospectively and are not expected to have a material impact on the Company’s Consolidated Financial Statements. |

| • | As of January 1, 2016, Encana will be required to adopt ASU 2014-12, “Compensation – Stock Compensation: Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period”. The standard requires that a performance target that affects vesting and could be achieved after the requisite service period be treated as a performance condition. The amendments will be applied prospectively and are not expected to have a material impact on the Company’s Consolidated Financial Statements. |

| • | As of January 1, 2017, Encana will be required to adopt ASU 2014-09, “Revenue from Contracts with Customers” under Topic 606, which was the result of a joint project by the FASB and International Accounting Standards Board. The new standard replaces Topic 605, “Revenue Recognition”, and other industry-specific guidance in the Accounting Standards Codification. The new standard is based on the principle that revenue is recognized on the transfer of promised goods or services to customers in an amount that reflects the consideration the Company expects to be entitled to in exchange for those goods or services. The standard can be applied using either the full retrospective approach or a modified retrospective approach at the date of adoption. Encana is currently assessing the potential impact of the standard on the Company’s Consolidated Financial Statements. |

2. SEGMENTED INFORMATION

Encana’s reportable segments are determined based on the Company’s operations and geographic locations as follows:

| • | Canadian Operations includes the exploration for, development of, and production of natural gas, oil and NGLs and other related activities within the Canadian cost centre. |

| • | USA Operations includes the exploration for, development of, and production of natural gas, oil and NGLs and other related activities within the U.S. cost centre. |

| • | Market Optimization is primarily responsible for the sale of the Company’s proprietary production. These results are included in the Canadian and USA Operations. Market optimization activities include third party purchases and sales of product to provide operational flexibility for transportation commitments, product type, delivery points and customer diversification. These activities are reflected in the Market Optimization segment. Market Optimization sells substantially all of the Company’s upstream production to third party customers. Transactions between segments are based on market values and are eliminated on consolidation. |

Corporate and Other mainly includes unrealized gains or losses recorded on derivative financial instruments. Once the instruments are settled, the realized gains and losses are recorded in the reporting segment to which the derivative instruments relate.

Annual Report 2014 | Encana Corporation 61

RESULTS OF OPERATIONS

SEGMENT AND GEOGRAPHIC INFORMATION

| Canadian Operations | USA Operations | Market Optimization | ||||||||||||||||||||||||||||||||||

| For the years ended December 31 |

2014 | 2013 | 2012 | 2014 | 2013 | 2012 | 2014 | 2013 | 2012 | |||||||||||||||||||||||||||

| Revenues, Net of Royalties |

$ | 3,310 | $ | 2,824 | $ | 2,760 | $ | 2,902 | $ | 2,763 | $ | 3,365 | $ | 1,248 | $ | 512 | $ | 419 | ||||||||||||||||||

| Expenses |

||||||||||||||||||||||||||||||||||||

| Production and mineral taxes |

15 | 15 | 9 | 118 | 119 | 96 | — | — | — | |||||||||||||||||||||||||||

| Transportation and processing |

835 | 756 | 555 | 658 | 722 | 652 | — | — | — | |||||||||||||||||||||||||||

| Operating |

314 | 372 | 352 | 354 | 411 | 377 | 39 | 38 | 48 | |||||||||||||||||||||||||||

| Purchased product |

— | — | — | — | — | — | 1,191 | 441 | 349 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| 2,146 | 1,681 | 1,844 | 1,772 | 1,511 | 2,240 | 18 | 33 | 22 | ||||||||||||||||||||||||||||

| Depreciation, depletion and amortization |

625 | 601 | 748 | 992 | 818 | 1,102 | 4 | 12 | 12 | |||||||||||||||||||||||||||

| Impairments |

— | — | 1,822 | — | — | 2,842 | — | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| $ | 1,521 | $ | 1,080 | $ | (726 | ) | $ | 780 | $ | 693 | $ | (1,704 | ) | $ | 14 | $ | 21 | $ | 10 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Corporate & Other | Consolidated | |||||||||||||||||||||||

| 2014 | 2013 | 2012 | 2014 | 2013 | 2012 | |||||||||||||||||||

| Revenues, Net of Royalties |

$ | 559 | $ | (241 | ) | $ | (1,384 | ) | $ | 8,019 | $ | 5,858 | $ | 5,160 | ||||||||||

| Expenses |

||||||||||||||||||||||||

| Production and mineral taxes |

— | — | — | 133 | 134 | 105 | ||||||||||||||||||

| Transportation and processing |

12 | (2 | ) | 24 | 1,505 | 1,476 | 1,231 | |||||||||||||||||

| Operating |

28 | 38 | 17 | 735 | 859 | 794 | ||||||||||||||||||

| Purchased product |

— | — | — | 1,191 | 441 | 349 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| 519 | (277 | ) | (1,425 | ) | 4,455 | 2,948 | 2,681 | |||||||||||||||||

| Depreciation, depletion and amortization |

124 | 134 | 94 | 1,745 | 1,565 | 1,956 | ||||||||||||||||||

| Impairments |

— | 21 | 31 | — | 21 | 4,695 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| $ | 395 | $ | (432 | ) | $ | (1,550 | ) | 2,710 | 1,362 | (3,970 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Accretion of asset retirement obligation |

52 | 53 | 53 | |||||||||||||||||||||

| Administrative |

327 | 439 | 392 | |||||||||||||||||||||

| Interest |

654 | 563 | 522 | |||||||||||||||||||||

| Foreign exchange (gain) loss, net |

403 | 325 | (107 | ) | ||||||||||||||||||||

| (Gain) loss on divestitures |

(3,426 | ) | (7 | ) | — | |||||||||||||||||||

| Other |

71 | 1 | 1 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (1,919 | ) | 1,374 | 861 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net Earnings (Loss) Before Income Tax |

4,629 | (12 | ) | (4,831 | ) | |||||||||||||||||||

| Income tax expense (recovery) |

1,203 | (248 | ) | (2,037 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net Earnings (Loss) |

3,426 | 236 | (2,794 | ) | ||||||||||||||||||||

| Net earnings attributable to noncontrolling interest |

(34 | ) | — | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net Earnings (Loss) Attributable to Common Shareholders |

$ | 3,392 | $ | 236 | $ | (2,794 | ) | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

62 Encana Corporation | Annual Report 2014

RESULTS OF OPERATIONS

INTERSEGMENT INFORMATION

| Market Optimization | ||||||||||||||||||||||||||||||||||||

| Marketing Sales | Upstream Eliminations | Total | ||||||||||||||||||||||||||||||||||

| For the years ended December 31 |

2014 | 2013 | 2012 | 2014 | 2013 | 2012 | 2014 | 2013 | 2012 | |||||||||||||||||||||||||||

| Revenues, Net of Royalties |

$ | 7,371 | $ | 5,662 | $ | 4,260 | $ | (6,123 | ) | $ | (5,150 | ) | $ | (3,841 | ) | $ | 1,248 | $ | 512 | $ | 419 | |||||||||||||||

| Expenses |

||||||||||||||||||||||||||||||||||||

| Transportation and processing |

458 | 516 | 528 | (458 | ) | (516 | ) | (528 | ) | — | — | — | ||||||||||||||||||||||||

| Operating |

62 | 75 | 84 | (23 | ) | (37 | ) | (36 | ) | 39 | 38 | 48 | ||||||||||||||||||||||||

| Purchased product |

6,822 | 4,993 | 3,593 | (5,631 | ) | (4,552 | ) | (3,244 | ) | 1,191 | 441 | 349 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Operating Cash Flow |

$ | 29 | $ | 78 | $ | 55 | $ | (11 | ) | $ | (45 | ) | $ | (33 | ) | $ | 18 | $ | 33 | $ | 22 | |||||||||||||||

|

|

|

|