Form 6-K DIAGEO PLC For: Feb 05

Tweet

Tweet Share

Share�

�

�

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

�

FORM�6-K

�

Report of Foreign Private Issuer

Pursuant to Rule�13a-16 or 15d-16 of the

Securities Exchange Act of 1934

�

5 February�2015

�

Commission File Number 1-10691

�

DIAGEO plc

(Translation of registrant�s name into English)

�

Lakeside Drive, Park Royal, London NW10 7HQ, England

(Address of principal executive offices)

�

Indicate by check mark whether the registrant files or will file annual reports under cover Form�20-F or Form�40-F.

�

|

� |

Form�20-F��x |

Form�40-F��o |

�

Indicate by check mark whether the registrant is submitting the Form�6-K in paper as permitted by Regulation S-T Rule�101(b)(1): o

�

Indicate by check mark whether the registrant is submitting the Form�6-K in paper as permitted by Regulation S-T Rule�101(b)(7): o

�

This report on Form�6-K shall be deemed to be filed and incorporated by reference in the registration statements on Form�F-3 (File No.�333-110804, 333-132732, 333-153488 and 333-179426) and registration statements on Form�S-8 (File Nos. 333-169934, 333-162490, 333-153481, 333-154338 and 333-182315) and to be a part thereof from the date on which this report is furnished, to the extent not superseded by documents or reports subsequently filed or furnished.

�

�

�

�

�

|

� |

� |

Page |

|

� |

3 | |

|

� |

3 | |

|

� |

3 | |

|

� |

4 | |

|

� |

� |

� |

|

� |

6 | |

|

� |

� |

� |

|

� |

9 | |

|

� |

� |

� |

|

� |

10 | |

|

� |

10 | |

|

� |

10 | |

|

� |

10 | |

|

� |

11 | |

|

� |

31 | |

|

� |

32 | |

|

Definitions and reconciliation of non-GAAP measures to GAAP measures |

� |

32 |

|

� |

� |

� |

|

� |

38 | |

|

� |

� |

� |

|

� |

F-1 | |

|

� |

F-2 | |

|

Unaudited condensed consolidated statement of comprehensive income |

� |

F-3 |

|

� |

F-4 | |

|

Unaudited condensed consolidated statement of changes in equity |

� |

F-5 |

|

� |

F-6 | |

|

Notes to the unaudited condensed consolidated financial information |

� |

F-7 |

|

� |

� |

� |

|

� |

A-1 | |

|

� |

� |

� |

|

� |

� |

�

�

�

Diageo plc is a public limited company incorporated under the laws of England and Wales. As used herein, except as the context otherwise requires, the term �company� refers to Diageo plc and the terms �group� and �Diageo� refer to the company and its consolidated subsidiaries. References used herein to �shares� and �ordinary shares� are, except where otherwise specified, to Diageo plc�s ordinary shares.

�

PRESENTATION OF FINANCIAL INFORMATION

�

Diageo plc�s fiscal year ends on 30 June. The company publishes its consolidated financial statements in pounds sterling. In this document, references to �pounds sterling�, �sterling�, ���, �pence� or �p� are to UK currency, references to �US dollars�, �US$�, �$� or ��� are to US currency and references to the �euro� or ��� are to the euro currency. For the convenience of the reader, this document contains translations of certain pounds sterling amounts into US dollars at specified rates, or, if not so specified, the noon buying rate in New York City for cable transfers in pounds sterling as certified for customs purposes by the Federal Reserve Bank of New York (the �noon buying rate�) on 31 December�2014 of �1 = $1.56. No representation is made that the pounds sterling amounts have been, could have been or could be converted into US dollars at the rates indicated or at any other rates.

�

Diageo�s condensed consolidated financial information has been prepared in accordance with IAS 34 �Interim Financial Reporting� as adopted for use in the European Union (EU) and International Financial Reporting standards (IFRS) as issued by the International Accounting Standards Board (IASB). References to IFRS hereafter should be construed as references to both IFRS as adopted by the EU and IFRS as issued by the IASB. Unless otherwise indicated, all financial information contained in this document has been prepared in accordance with IFRS. This interim condensed consolidated financial information is unaudited and has been prepared on the basis of accounting policies consistent with those applied in the consolidated financial statements for the year ended 30 June�2014.

�

The business review, selected consolidated financial data and financial information included in this document for the six months ended 31 December�2014 and 31 December�2013 have been derived from the published Diageo interim condensed consolidated financial information.

�

The principal executive office of the company is located at Lakeside Drive, Park Royal, London NW10 7HQ, England and its telephone number is +44 (0)20 8978 6000.

�

TRADEMARKS, TRADE NAMES AND MARKET DATA

�

This report on Form�6-K includes names of Diageo�s products which constitute trademarks or trade names which Diageo owns or which others own and license to Diageo for use. All rights reserved. � Diageo plc 2015.

�

The market data and competitive set classifications are taken from independent industry sources in the markets in which Diageo operates.

�

�

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

�

This document contains �forward-looking� statements. These statements can be identified by the fact that they do not relate only to historical or current facts. In particular, forward-looking statements include all statements that express forecasts, expectations, plans, outlook and projections with respect to future matters, including trends in results of operations, margins, growth rates, overall market trends, the impact of changes in interest or exchange rates, the availability or cost of financing to Diageo, anticipated cost savings or synergies, expected investments, the completion of Diageo�s strategic transactions and restructuring programmes, anticipated tax rates, expected cash payments, outcomes of litigation, anticipated deficit reductions in relation to pension schemes and general economic conditions. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements, including factors that are outside Diageo�s control.

�

These factors include, but are not limited to:

�

������������������ changes in political or economic conditions in countries and markets in which Diageo operates, including changes in levels of consumer spending, failure of customer, supplier and financial counterparties or imposition of import, investment or currency restrictions;

������������������ changes in consumer preferences and tastes, demographic trends or perceptions about health related issues, or contamination, counterfeiting or other circumstances which could harm the integrity or sales of Diageo�s brands;

������������������ developments in any litigation or other similar proceedings (including with tax, customs and other regulatory authorities) directed at the drinks and spirits industry generally or at Diageo in particular, or the impact of a product recall or product liability claim on Diageo�s profitability or reputation;

������������������ the effects of climate change and regulations and other measures to address climate change including any resulting impact on the cost and supply of water;

������������������ changes in the cost or supply of raw materials, labour and/or energy;

������������������ legal and regulatory developments, including changes in regulations regarding production, product liability, distribution, importation, labelling, packaging, consumption or advertising; changes in tax law, rates or requirements (including with respect to the impact of excise tax increases) or accounting standards; and changes in environmental laws, health regulations and the laws governing labour and pensions;

������������������ the costs associated with monitoring and maintaining compliance with anti-corruption and other laws and regulations, and the costs associated with investigating alleged breaches of internal policies, laws or regulations, whether initiated internally or by external regulators, and any penalties or fines imposed as a result of any breaches;

������������������ ability to maintain Diageo�s brand image and corporate reputation, and exposure to adverse publicity, whether or not justified, and any resulting impacts on Diageo�s reputation and the likelihood that consumers choose products offered by Diageo�s competitors;

������������������ increased competitive product and pricing pressures and unanticipated actions by competitors that could impact Diageo�s market share, increase expenses and hinder growth potential;

������������������ the effects of Diageo�s strategic focus on premium drinks, the effects of business combinations, partnerships, acquisitions or disposals, existing or future, and the ability to realise expected synergies and/or costs savings;

������������������ Diageo�s ability to complete existing or future business combinations, restructuring programmes, acquisitions and disposals;

������������������ contamination, counterfeiting or other events that could adversely affect the perception of Diageo�s brands;

������������������ increased costs or shortages of talent;

������������������ disruption to production facilities or business service centres, and systems change programmes, existing or future, and the ability to derive expected benefits from such programmes;

������������������ changes in financial and equity markets, including significant interest rate and foreign currency exchange rate fluctuations and changes in the cost of capital, which may reduce or eliminate Diageo�s access to or increase the cost of financing or which may affect Diageo�s financial results and movements to the value of Diageo�s pension funds;

������������������ renewal of supply, distribution, manufacturing or licence agreements (or related rights) and licences on favourable terms when they expire;

������������������ technological developments that may affect the distribution of products or impede Diageo�s ability to protect its intellectual property rights.

�

All oral and written forward-looking statements made on or after the date of this document and attributable to Diageo are expressly qualified in their entirety by the above factors and the �Risk factors� contained in the annual report on Form 20-F for the year ended 30 June 2014 filed with the US Securities and Exchange Commission (SEC). Any forward-looking statements made by or on behalf of Diageo speak only as of the date they are made. Diageo does not undertake to update forward-looking statements to reflect any changes in Diageo�s expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is based. The reader should, however, consult any additional disclosures that Diageo may make in any documents which it publishes and/or files with the US Securities and Exchange Commission (SEC). All readers, wherever located, should take note of these disclosures.

�

This document includes names of Diageo�s products, which constitute trademarks or trade names which Diageo owns, or which others own and license to Diageo for use. All rights reserved. � Diageo plc 2015.

�

�

The information in this document does not constitute an offer to sell or an invitation to buy shares in Diageo plc or an invitation or inducement to engage in any other investment activities.

�

This document includes information about Diageo�s target debt rating. A security rating is not a recommendation to buy, sell or hold securities and may be subject to revision or withdrawal at any time by the assigning rating organisation. Each rating should be evaluated independently of any other rating.

�

Past performance cannot be relied upon as a guide to future performance.

�

The contents of the company�s website (www.diageo.com) should not be considered to form part of or be incorporated into this document.

�

�

SELECTED CONSOLIDATED FINANCIAL DATA

�

The selected consolidated financial data set out below has been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted for use in the European Union (EU) and IFRS as issued by the International Accounting Standards Board (IASB) and should be read in conjunction with, and are qualified in their entirety by reference to, the unaudited financial information and notes presented elsewhere in this document and to Diageo�s annual report on Form�20-F for the year ended 30 June�2014.

�

The following table presents selected consolidated financial data for Diageo: for the six months ended 31 December�2014 and 31 December�2013 and as at the respective period ends, derived from the unaudited interim condensed consolidated financial information presented elsewhere in this document; and for the five years ended 30 June�2014 and as at the respective year ends, derived from Diageo�s consolidated financial statements audited by Diageo�s independent auditor. The unaudited interim condensed consolidated financial information, in the opinion of Diageo management, includes all adjustments, consisting solely of normal, recurring adjustments, necessary to present fairly the information contained therein. The results of operations for the six months ended 31 December�2014 are not necessarily indicative of the results for the year ending 30 June�2015.

�

|

� |

� |

Six�months�ended�31�December |

� |

Year�ended�30�June |

� | ||||||||||||

|

Income�statement |

� |

2014 |

� |

2014 |

� |

2013 |

� |

2014 |

� |

2013 |

� |

2012 |

� |

2011 |

� |

2010 |

� |

|

data(1)(6) |

� |

$�million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

|

Sales |

� |

13,609 |

� |

8,724 |

� |

8,014 |

� |

13,980 |

� |

15,276 |

� |

14,392 |

� |

13,043 |

� |

12,793 |

� |

|

Operating profit |

� |

2,602 |

� |

1,668 |

� |

2,040 |

� |

2,707 |

� |

3,380 |

� |

3,108 |

� |

2,552 |

� |

2,538 |

� |

|

Profit for the period |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

|

Continuing operations(2) |

� |

2,128 |

� |

1,364 |

� |

1,746 |

� |

2,264 |

� |

2,550 |

� |

2,032 |

� |

1,960 |

� |

1,727 |

� |

|

Discontinued operations(3) |

� |

� |

� |

� |

� |

(92 |

) |

(83 |

) |

� |

� |

(11 |

) |

� |

� |

(19 |

) |

|

Total profit for the period(2) |

� |

2,128 |

� |

1,364 |

� |

1,654 |

� |

2,181 |

� |

2,550 |

� |

2,021 |

� |

1,960 |

� |

1,708 |

� |

�

|

Per�share�data |

� |

$ |

� |

pence |

� |

pence |

� |

pence |

� |

pence |

� |

pence |

� |

pence |

� |

pence |

� |

|

Dividend per share(4) |

� |

0.34 |

� |

21.5 |

� |

19.7 |

� |

51.7 |

� |

47.4 |

� |

43.5 |

� |

40.4 |

� |

38.1 |

� |

|

Earnings per share |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

|

Basic |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

|

Continuing operations(2) |

� |

0.82 |

� |

52.3 |

� |

67.5 |

� |

93.0 |

� |

98.0 |

� |

76.6 |

� |

74.3 |

� |

65.2 |

� |

|

Discontinued operations(3) |

� |

� |

� |

� |

� |

(3.7 |

) |

(3.3 |

) |

� |

� |

(0.4 |

) |

� |

� |

(0.8 |

) |

|

Basic earnings per share |

� |

0.82 |

� |

52.3 |

� |

63.8 |

� |

89.7 |

� |

98.0 |

� |

76.2 |

� |

74.3 |

� |

64.4 |

� |

|

Diluted |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

|

Continuing operations(2) |

� |

0.81 |

� |

52.2 |

� |

67.2 |

� |

92.6 |

� |

97.4 |

� |

76.2 |

� |

74.1 |

� |

65.1 |

� |

|

Discontinued operations(3) |

� |

� |

� |

� |

� |

(3.7 |

) |

(3.3 |

) |

� |

� |

(0.4 |

) |

� |

� |

(0.8 |

) |

|

Diluted earnings per share |

� |

0.81 |

� |

52.2 |

� |

63.5 |

� |

89.3 |

� |

97.4 |

� |

75.8 |

� |

74.1 |

� |

64.3 |

� |

�

|

� |

� |

million |

� |

million |

� |

million |

� |

million |

� |

million |

� |

million |

� |

million |

� |

million |

� |

|

Average shares |

� |

2,506 |

� |

2,506 |

� |

2,507 |

� |

2,506 |

� |

2,502 |

� |

2,495 |

� |

2,493 |

� |

2,486 |

� |

�

|

� |

� |

As�at�31�December |

� |

As�at�30�June |

� | ||||||||||||

|

� |

� |

2014 |

� |

2014 |

� |

2013 |

� |

2014 |

� |

2013 |

� |

2012 |

� |

2011 |

� |

2010 |

� |

|

Balance�sheet�data(1)(6) |

� |

$�million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

|

Total assets |

� |

43,540 |

� |

27,910 |

� |

24,245 |

� |

22,964 |

� |

24,991 |

� |

22,269 |

� |

19,720 |

� |

19,394 |

� |

|

Net assets |

� |

13,566 |

� |

8,696 |

� |

8,038 |

� |

7,590 |

� |

8,088 |

� |

6,792 |

� |

5,959 |

� |

4,762 |

� |

|

Net borrowings(5) |

� |

16,642 |

� |

10,668 |

� |

9,096 |

� |

8,850 |

� |

8,403 |

� |

7,573 |

� |

6,480 |

� |

6,980 |

� |

|

Equity attributable to the parent company�s equity shareholders |

� |

11,276 |

� |

7,228 |

� |

7,086 |

� |

6,823 |

� |

7,036 |

� |

5,588 |

� |

5,245 |

� |

4,007 |

� |

|

Share capital |

� |

1,243 |

� |

797 |

� |

797 |

� |

797 |

� |

797 |

� |

797 |

� |

797 |

� |

797 |

� |

�

This information should be read in conjunction with the notes on pages�7 to 8.

�

�

Notes to the selected consolidated financial data

�

(1)�IFRS accounting policies The unaudited condensed consolidated financial information for the six months ended 31 December�2014 has been prepared in accordance with IAS 34 �Interim Financial Reporting� as issued by the International Accounting Standards Board (IASB) and adopted for use in the European Union.

�

(2)�Exceptional items Exceptional items are charges or credits which, in management�s judgement, need to be disclosed by virtue of their size or incidence in order for the user to obtain a proper understanding of the financial information. Such items are included within the income statement caption to which they relate. An analysis of exceptional items is as follows:

�

|

� |

� |

Six�months�ended |

� |

Year�ended�30�June |

� | ||||||||||

|

� |

� |

2014 |

� |

2013 |

� |

2014 |

� |

2013 |

� |

2012 |

� |

2011 |

� |

2010 |

� |

|

� |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

|

Items included in operating profit |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

|

Restructuring programmes |

� |

(26 |

) |

(20 |

) |

(163 |

) |

(69 |

) |

(96 |

) |

(111 |

) |

(142 |

) |

|

Duty settlements |

� |

(145 |

) |

� |

� |

� |

� |

� |

� |

� |

� |

(127 |

) |

� |

� |

|

Brand impairment |

� |

� |

� |

� |

� |

(264 |

) |

(50 |

) |

(59 |

) |

(39 |

) |

(35 |

) |

|

Pension changes � past service credits |

� |

� |

� |

� |

� |

� |

� |

20 |

� |

115 |

� |

� |

� |

� |

� |

|

SEC settlement |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

(12 |

) |

� |

� |

|

� |

� |

(171 |

) |

(20 |

) |

(427 |

) |

(99 |

) |

(40 |

) |

(289 |

) |

(177 |

) |

|

Non-operating items |

� |

98 |

� |

138 |

� |

140 |

� |

(83 |

) |

147 |

� |

(14 |

) |

(15 |

) |

|

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

|

Items included in taxation |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

|

Tax credit on exceptional operating items |

� |

38 |

� |

3 |

� |

99 |

� |

27 |

� |

19 |

� |

51 |

� |

39 |

� |

|

Tax on non-operating items |

� |

� |

� |

� |

� |

� |

� |

28 |

� |

� |

� |

3 |

� |

10 |

� |

|

Loss of future tax amortisation |

� |

� |

� |

� |

� |

� |

� |

� |

� |

(524 |

) |

� |

� |

� |

� |

|

Settlements with tax authorities |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

� |

66 |

� |

� |

� |

|

� |

� |

38 |

� |

3 |

� |

99 |

� |

55 |

� |

(505 |

) |

120 |

� |

49 |

� |

|

Exceptional items included in continuing operations |

� |

(35 |

) |

121 |

� |

(188 |

) |

(127 |

) |

(398 |

) |

(183 |

) |

(143 |

) |

|

Discontinued operations net of taxation (note 3) |

� |

� |

� |

(92 |

) |

(83 |

) |

� |

� |

(11 |

) |

� |

� |

(19 |

) |

|

Exceptional items |

� |

(35 |

) |

29 |

� |

(271 |

) |

(127 |

) |

(409 |

) |

(183 |

) |

(162 |

) |

�

(3)�Discontinued operations In the six months ended 31 December�2013 discontinued operations represented a charge after taxation of �92 million (year ended 30 June�2014 � �83 million; 2013�� �nil; 2012� �11 million; 2011�� �nil; 2010� �19 million) in respect of the settlement of the litigation in Australia and New Zealand and anticipated future payments to thalidomide injured individuals and thalidomide organisations.

�

(4)�Dividends The board expects that Diageo will pay an interim dividend in April�and a final dividend in October�of each year. Approximately 40% of the total dividend in respect of any financial year is expected to be paid as an interim dividend and approximately 60% as a final dividend. The payment of any future dividends, subject to shareholder approval, will depend upon Diageo�s earnings, financial condition and such other factors as the board deems relevant. Proposed dividends are not considered to be a liability until they are approved by the board for the interim dividend and by the shareholders at the annual general meeting for the final dividend.

�

The table below sets out the amounts of interim, final and total cash dividends paid by the company on each ordinary share. The dividends are translated into US dollars per ADS (each ADS representing four ordinary shares) at the actual rate on each of the respective dividend payment dates.

�

|

� |

� |

� |

� |

Six�months�ended |

� |

Year�ended�30�June |

� | ||||||||||

|

� |

� |

� |

� |

2014 |

� |

2013 |

� |

2014 |

� |

2013 |

� |

2012 |

� |

2011 |

� |

2010 |

� |

|

� |

� |

� |

� |

pence |

� |

pence |

� |

pence |

� |

pence |

� |

pence |

� |

pence |

� |

pence |

� |

|

Per ordinary share |

� |

Interim |

� |

21.5 |

� |

19.7 |

� |

19.7 |

� |

18.1 |

� |

16.6 |

� |

15.5 |

� |

14.6 |

� |

|

� |

� |

Final |

� |

� |

� |

� |

� |

32.0 |

� |

29.3 |

� |

26.9 |

� |

24.9 |

� |

23.5 |

� |

|

� |

� |

Total |

� |

21.5 |

� |

19.7 |

� |

51.7 |

� |

47.4 |

� |

43.5 |

� |

40.4 |

� |

38.1 |

� |

�

|

� |

� |

� |

� |

$ |

� |

$ |

� |

$ |

� |

$ |

� |

$ |

� |

$ |

� |

$ |

� |

|

Per ADS |

� |

Interim |

� |

1.29 |

� |

1.31 |

� |

1.31 |

� |

1.10 |

� |

1.05 |

� |

1.01 |

� |

0.89 |

� |

|

� |

� |

Final |

� |

� |

� |

� |

� |

2.06 |

� |

1.89 |

� |

1.72 |

� |

1.59 |

� |

1.48 |

� |

|

� |

� |

Total |

� |

1.29 |

� |

1.31 |

� |

3.37 |

� |

2.99 |

� |

2.77 |

� |

2.60 |

� |

2.37 |

� |

�

�

Note: The interim dividend for the six months ended 31 December�2014 will be paid on 7 April�2015, and payment to US ADR holders will be made on 10 April�2015. In the table above, an exchange rate of �1 = $1.50 has been assumed for this dividend, but the exact amount of the payment to US ADR holders will be determined by the rate of exchange on 7 April�2015.

�

Diageo�s dividend philosophy has been�a consistent increase in the annual dividend payable while maintaining dividend cover between 1.8 and 2.2 times earnings per share. In recent years this has allowed the group to increase its dividend by 9% a year. Given the economic slowdown in emerging markets and the associated currency weakness expected in the future both of which had such a significant impact on Diageo�s reported results in the year ended 30 June�2014, the group�s dividend coverage ratio is now below the lower end of the range set.�However cash flow is improving as these results show and the strength of the dollar is providing some offset to emerging market currency weakness. Therefore the interim dividend growth was maintained at 9%,�but this will be reviewed for the full year and if necessary the rate of increase may be changed for the final dividend in order to maintain the coverage ratio, albeit at the lower end of the range.

�

(5)�Net borrowings definition Net borrowings are defined as gross borrowings (short term borrowings and long term borrowings plus finance lease liabilities plus interest rate hedging instruments, cross currency interest rate swaps and funding foreign currency forwards and swaps used to manage borrowings) less cash and cash equivalents.

�

(6)�Exchange rates A substantial portion of the group�s assets, liabilities, revenues and expenses is denominated in currencies other than pounds sterling. For the convenience of the reader, selected consolidated financial information for the six months ended 31�December�2014 has been translated into US dollars at the noon buying rate on 31 December�2014 of �1 = $1.56.

�

The following table shows period end and average US dollar/pound sterling noon buying exchange rates, for the periods indicated, expressed in US dollars per �1.

�

|

� |

� |

Six�months�ended |

� |

Year�ended�30�June |

� | ||||||||||

|

� |

� |

2014 |

� |

2013 |

� |

2014 |

� |

2013 |

� |

2012 |

� |

2011 |

� |

2010 |

� |

|

� |

� |

$ |

� |

$ |

� |

$ |

� |

$ |

� |

$ |

� |

$ |

� |

$ |

� |

|

Period/year end |

� |

1.56 |

� |

1.66 |

� |

1.71 |

� |

1.52 |

� |

1.57 |

� |

1.61 |

� |

1.50 |

� |

|

Average rate* |

� |

1.62 |

� |

1.60 |

� |

1.64 |

� |

1.57 |

� |

1.59 |

� |

1.59 |

� |

1.57 |

� |

�

* The average of the noon buying rates on the last business day of each month during the six months ended 31 December�and during the years ended 30 June.

�

The average exchange rate for the period 1 January�to 30 January�2015 was �1=$1.51 and the noon buying rate on 30 January�2015 was �1=$1.50.

�

These rates have been provided for information only. They are not necessarily the rates that have been used in this document for currency translations or in the preparation of the consolidated financial information. See note 2 to the unaudited condensed consolidated financial information for the actual rates used in the preparation of the consolidated financial information.

�

�

CAPITALISATION AND INDEBTEDNESS

�

The following table sets out on an IFRS basis the unaudited capitalisation of Diageo as at 31 December�2014:

�

|

� |

� |

31�December�2014 |

� |

|

� |

� |

� million |

� |

|

Short term borrowings and bank overdrafts (including current portion of long term borrowings) |

� |

2,845 |

� |

|

� |

� |

� |

� |

|

Long term borrowings |

� |

� |

� |

|

Due from one to five years |

� |

4,077 |

� |

|

Due after five years |

� |

4,441 |

� |

|

� |

� |

8,518 |

� |

|

Finance lease obligations |

� |

276 |

� |

|

Non-controlling interests |

� |

1,468 |

� |

|

� |

� |

� |

� |

|

Equity attributable to the equity shareholders of the parent company |

� |

� |

� |

|

Share capital |

� |

797 |

� |

|

Share premium |

� |

1,345 |

� |

|

Capital redemption reserve |

� |

3,146 |

� |

|

Fair value, hedging and exchange reserve |

� |

(753 |

) |

|

Own shares |

� |

(2,241 |

) |

|

Other retained earnings |

� |

4,934 |

� |

|

� |

� |

7,228 |

� |

|

Total capitalisation |

� |

20,335 |

� |

�

Notes

�

(1)�������������������������������� At 31 December�2014, the group had cash and cash equivalents of �802 million.

�

(2)�������������������������������� At 31 December�2014, 2,754,258,478 ordinary shares of 28 101/108�pence each were issued, all of which were fully paid, including shares issued, shares issued and held in employee share trusts and those held as treasury shares.

�

(3)�������������������������������� There have been no material changes to the performance guarantees or indemnities in respect of liabilities of third parties from those reported in Diageo�s Annual Report on Form�20-F for the year ended 30 June�2014.

�

(4)�������������������������������� At 31 December 2014, �256 million of the group�s net borrowings were secured on assets of the group.

�

(5)�������������������������������� Since 31 December�2014 no shares have been acquired by Diageo as part of the share buyback programs or to be held as treasury shares for hedging share scheme grants provided to employees.

�

(6)�������������������������������� Save as disclosed above there has been no material change since 31 December�2014 in the group�s net borrowings, performance guarantees, indemnities and capitalisation.

�

�

�

�

Diageo is the world�s leading premium drinks business and operates on an international scale selling all types of beverage alcohol. It is one of a small number of premium drinks companies that operate globally across spirits, beer and wine.

�

The following discussion is based on Diageo�s results for the six months ended 31 December�2014 compared with the six months ended 31 December�2013.

�

Unless otherwise stated in this section, percentage movements are organic movements. These movements and organic operating margin are before exceptional items. Commentary, unless otherwise stated, refers to organic movements. Share, unless otherwise stated, refers to value share. See �Definitions and reconciliations of non-GAAP measures to GAAP measures� for an explanation of organic movements on page 32.

�

REVISED SEGMENTAL INFORMATION FOR PRIOR REPORTING PERIODS

�

In the six months ended 31 December�2014 Diageo changed its internal reporting structure to reflect changes made to management responsibilities as announced on 30 July�2014. As a result of this change, Diageo reports the following geographical segments both for management reporting purposes and in the external financial statements: North America; Europe; Africa; Latin America and Caribbean; Asia Pacific and Corporate. As a consequence of these changes, comparative prior period figures have been restated. Restated segmental information for volume, sales, net sales, marketing spend and operating profit before exceptional items for prior periods with a reconciliation to previously reported figures is provided in �Definitions and reconciliations of non-GAAP measures to GAAP measures� on page�32.

�

�

Ivan Menezes, Chief Executive of Diageo, commenting on the six months ended 31 December�2014 said:

�

�We have improved our performance during the half and we have again shown: the strength of our brands, which is driving our share gains; our strong innovation capability, which has enabled us to access new growth opportunities, and our focus on cost.� We delivered the planned savings from our global efficiency programme together with procurement benefits in marketing spend which we have reinvested in our brands and we increased our investment in our routes to consumer� while again expanding our margins.

�

We have already taken action to improve the performance of those brands and markets that have not performed as well as we would expect. This contributed to our stronger second quarter performance and I expect to maintain this momentum through the year.

�

The half saw Diageo acquire control of USL, putting us in the position to create an iconic leader in spirits in an attractive market.� We have also reached agreement to acquire all of Don Julio, which will significantly strengthen our position in one of our fastest growing categories.

�

The quality of these results in a tough environment, with depletions ahead of shipments and improving cash flow, reinforce my confidence that Diageo can realise its full potential and deliver our performance ambition.�

�

The above comments were made by Ivan Menezes, Chief Executive of Diageo, in connection with the release of the Interim Announcement published on 29 January�2015.

�

�

OPERATING RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 2014 COMPARED WITH THE SIX MONTHS ENDED 31 DECEMBER 2013

�

Key highlights

�

������������������ Organic net sales in the half were broadly flat (-0.1%) with volume down 1.9%.� Performance improved in Q2

������������������ Continued strong performance of reserve brands, up 10%, was a key driver of positive overall price/mix

������������������ Marketing spend was in line with net sales, as effective spend benefitted from procurement efficiencies worth 3% of total marketing investment

������������������ Restructuring benefits drove operating margin improvement of 28bps with organic operating profit up 0.7%

������������������ Free cash flow was �699 million, up �373 million on the first half last year

������������������ Eps before exceptional items was 53.7 pence per share, down 8.9 pence per share driven mainly by negative exchange impacts and lower income from associates and joint ventures

������������������ Interim dividend up 9% to 21.5 pence per share

�

|

Key�performance�indicators |

� |

� |

� |

First� |

� |

First� |

� | |

|

Organic net sales growth |

� |

% |

� |

� |

� |

2 |

� | |

|

Organic operating margin improvement |

� |

basis points |

� |

28 |

� |

37 |

� | |

|

Earnings per share before exceptional items |

� |

pence |

� |

53.7 |

� |

62.6 |

� | |

|

Free cash flow |

� |

� |

� million |

� |

699 |

� |

326 |

� |

|

Return on average invested capital |

� |

% |

� |

13.9 |

� |

17.8 |

� | |

�

|

Other�financial�information |

� |

� |

� |

First�Half |

� |

First�Half |

� |

Organic� |

� |

Reported |

� | |

|

Volume |

� |

EUm |

� |

134.1 |

� |

84.3 |

� |

(2 |

) |

59 |

� | |

|

Net sales |

� |

� |

� million |

� |

5,900 |

� |

5,932 |

� |

� |

� |

(1 |

) |

|

Marketing spend |

� |

� |

� million |

� |

896 |

� |

903 |

� |

� |

� |

(1 |

) |

|

Operating profit before exceptional items (a) |

� |

� |

� million |

� |

1,839 |

� |

2,060 |

� |

1 |

� |

(11 |

) |

|

Operating profit (b) |

� |

� |

� million |

� |

1,668 |

� |

2,040 |

� |

� |

� |

(18 |

) |

|

Share of associates and joint ventures profit after tax |

� |

� |

� million |

� |

113 |

� |

181 |

� |

� |

� |

(38 |

) |

|

Net finance charges |

� |

� |

� million |

� |

239 |

� |

225 |

� |

� |

� |

6 |

� |

|

Reported tax rate |

� |

% |

� |

16.8 |

� |

18.2 |

� |

� |

� |

(8 |

) | |

|

Reported tax rate before exceptional items� |

� |

% |

� |

18.3 |

� |

19.4 |

� |

� |

� |

(6 |

) | |

|

Profit attributable to parent company�s shareholders |

� |

� |

� million |

� |

1,311 |

� |

1,599 |

� |

� |

� |

(18 |

) |

|

Basic earnings per share |

� |

pence |

� |

52.3 |

� |

63.8 |

� |

� |

� |

(18 |

) | |

|

Interim dividend per share |

� |

pence |

� |

21.5 |

� |

19.7 |

� |

� |

� |

9 |

� | |

�

(a)�������� Operating profit before exceptional items included attributable transaction and integration costs of �10 million in the six months ended 31 December�2013 in respect of business acquisitions.

(b)�������� Operating profit includes an exceptional charge of �171 million, an analysis for which is provided on page�16.

�

�

Key performance indicators

�

Net sales growth (� million)

�

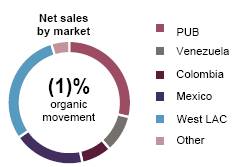

Reported net sales were flat. Adverse foreign exchange was offset by the full consolidation of USL. Growth in reserve brands and pricing in Venezuela offset volume decline

�

�

(a)�������� Impact of acquisitions and disposals on the first half F14 and the first half F15. See page�34 for further details.

�

Reported net sales were flat. Adverse foreign exchange was offset by the full consolidation of USL. Organic volume decline was largely driven by currency related market contraction in West LAC and South East Asia, a challenging environment in Venezuela and weakness in the standard price segment in North America. Positive price/mix was largely driven by the strong performance of reserve brands and price increases in Venezuela.

�

Operating margin improvement (%)

�

Cost savings delivered 28bps of organic margin improvement

�

�

The full consolidation of USL has rebased Diageo�s operating margin by 2pps. Adverse foreign exchange, primarily in respect of the Venezuelan bolivar, reduced reported margins while the organic increase in operating margin was 28bps driven by cost savings from the global efficiency programme.

�

�

Earnings per share before exceptional items (pence)

�

Eps before exceptionals impacted by adverse foreign exchange, decrease in associate profit and increase in finance charges

�

�

Eps fell 8.9 pence largely as a result of adverse foreign exchange movements, which reduced eps 8.4 pence.� Operating profit after tax and excluding foreign exchange movements had a positive impact on eps as a result of organic growth and the lower tax rate.� Lower income from associates and joint ventures and the increase in other finance charges, which largely reflects updated projections for dividends payable in respect of the Zacapa agreement, also had a negative impact on eps.

�

Basic eps was 52.3 pence (2013 � 63.8 pence), with exceptionals reducing eps by 1.4 pence (2013 � 1.2 pence favourable).

�

For movements in net finance charges see below:

�

|

Movement�in�net�finance�charges |

� |

� million |

� |

|

First Half F14 Reported |

� |

225 |

� |

|

Net interest charge |

� |

6 |

� |

|

Post employment charges |

� |

1 |

� |

|

Venezuela hyperinflation adjustment |

� |

(3 |

) |

|

Other finance charges |

� |

10 |

� |

|

First Half F15 Reported |

� |

239 |

� |

�

|

� |

� |

First�Half |

� |

First�Half� |

� |

|

Average monthly net borrowings (� million) |

� |

10,698 |

� |

9,160 |

� |

|

Effective interest rate |

� |

3.7% |

� |

4.1% |

� |

�

For the calculation of the effective interest rate, the net interest charge excludes fair value adjustments to derivative financial instruments and borrowings. Average monthly net borrowings include the impact of interest rate swaps that are no longer in a hedge relationship but excludes the market value adjustment for cross currency interest rate swaps.

�

The increase in average net borrowings was principally the result of the acquisition of the controlling interest in USL, completed on 2 July�2014, and the inclusion of USL�s net borrowings. The effective interest rate decreased in the six months ended 31 December 2014 principally as a results of lower interest rates on new debt issues.

�

�

Free cash flow (� million)

�

Positive working capital movement, lower interest and tax payments offset the impact of reduced operating profit and the full consolidation of USL on cash flow

�

�

(a)�������� Operating profit adjusted for non cash items including depreciation and amortisation.

(b)�������� Other movements includes dividends received from associates and joint ventures, movements in loans receivable and other investments, and payments in respect of the settlement of Thalidomide litigations.

�

The increase in free cash flow was primarily driven by the positive working capital movement, largely due to increases in creditor balances. Lower interest and tax payments are due to phasing. Contributions to pension plans were lower than the same period last year, largely driven by the one off payment made into the Irish pension scheme last year.

�

Return on average invested capital (ROIC) (a)

�

The investment in USL has rebased ROIC and adverse FX reduced ROIC in the period

�

�

(a)��� ROIC calculation excludes exceptional items

�

The full consolidation of USL reduced ROIC by 2.1pps. Foreign exchange movements which reduced operating profit, were partially offset by the impact of foreign exchange on invested capital.

�

�

Additional financial information

�

Income statement

�

|

� |

� |

31�December |

� |

Exchange |

� |

Acquisitions |

� |

Organic |

� |

31�December |

� |

|

� |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

� million |

� |

|

Sales |

� |

8,014 |

� |

(637 |

) |

1,225 |

� |

122 |

� |

8,724 |

� |

|

Excise duties |

� |

(2,082 |

) |

149 |

� |

(762 |

) |

(129 |

) |

(2,824 |

) |

|

Net sales |

� |

5,932 |

� |

(488 |

) |

463 |

� |

(7 |

) |

5,900 |

� |

|

Cost of sales* |

� |

(2,184 |

) |

129 |

� |

(359 |

) |

(4 |

) |

(2,418 |

) |

|

Gross profit |

� |

3,748 |

� |

(359 |

) |

104 |

� |

(11 |

) |

3,482 |

� |

|

Marketing |

� |

(903 |

) |

43 |

� |

(35 |

) |

(1 |

) |

(896 |

) |

|

Other operating expenses* |

� |

(785 |

) |

48 |

� |

(35 |

) |

25 |

� |

(747 |

) |

|

Operating profit before exceptional items |

� |

2,060 |

� |

(268 |

) |

34 |

� |

13 |

� |

1,839 |

� |

|

Exceptional operating items (c) |

� |

(20 |

) |

� |

� |

� |

� |

� |

� |

(171 |

) |

|

Operating profit |

� |

2,040 |

� |

� |

� |

� |

� |

� |

� |

1,668 |

� |

|

Non-operating items (c) |

� |

138 |

� |

� |

� |

� |

� |

� |

� |

98 |

� |

|

Net finance charges |

� |

(225 |

) |

� |

� |

� |

� |

� |

� |

(239 |

) |

|

Share of after tax results of associates and joint ventures |

� |

181 |

� |

� |

� |

� |

� |

� |

� |

113 |

� |

|

Profit before taxation |

� |

2,134 |

� |

� |

� |

� |

� |

� |

� |

1,640 |

� |

|

Taxation |

� |

(388 |

) |

� |

� |

� |

� |

� |

� |

(276 |

) |

|

Profit from continuing operations |

� |

1,746 |

� |

� |

� |

� |

� |

� |

� |

1,364 |

� |

|

Discontinued operations (c) |

� |

(92 |

) |

� |

� |

� |

� |

� |

� |

� |

� |

|

Profit for the period |

� |

1,654 |

� |

� |

� |

� |

� |

� |

� |

1,364 |

� |

�

* before exceptional operating items

�

(a)�Exchange

�

The impact of movements in exchange rates on reported figures is principally in respect of the Venezuelan bolivar, the Russian rouble and the euro.

�

In March�2014, the Central Bank of Venezuela opened the Second Ancillary Foreign Currency Administration System (Sicad II) that allows private and public companies to trade foreign currency at a higher exchange rate than the official exchange rate. As a result, the group has applied Sicad II exchange rate to consolidate its Venezuelan operations for the year ended 30 June�2014 ($1 = VEF49.98; �1 = VEF85.47). Applying the consolidation rate of $1 = VEF49.99 (�1 = VEF77.98) at 31 December 2014 compared to the rate of $1�= VEF9 (�1 = VEF14.94) at 31 December 2013 reduced the net assets and cash and cash equivalents as at 31 December 2014 by �583 million and �404 million, respectively. The impact of applying the consolidation rate for the six months ended 31 December 2014 would have reduced the previously reported net sales and operating profit for the six months ended 31 December 2013 by �237�million and �183 million, respectively.

�

�

The effect of movements in exchange rates, associated finance charge movements and mark to market impact on interest expense on profit before exceptional items and taxation for the six months ended 31 December�2014 is set out in the table below.

�

|

� |

� |

� |

� |

Gains/ |

� |

|

� |

� |

� |

� |

(losses) |

� |

|

� |

� |

� |

� |

� million |

� |

|

Translation impact |

� |

� |

� |

(221 |

) |

|

Transaction impact |

� |

� |

� |

(47 |

) |

|

Operating profit before exceptional items |

� |

� |

� |

(268 |

) |

|

Net finance charges � translation impact |

� |

� |

� |

(1 |

) |

|

Mark to market impact of IAS 39 on interest expense |

� |

� |

� |

5 |

� |

|

Impact of IAS 21 and IAS 39 on net other finance charges |

� |

� |

� |

1 |

� |

|

Interest and other finance charges |

� |

� |

� |

5 |

� |

|

Associates � translation impact |

� |

� |

� |

(11 |

) |

|

Profit before exceptional items and taxation |

� |

� |

� |

(274 |

) |

�

|

� |

� |

Six�months�ended |

� |

Six�months�ended |

� |

|

� |

� |

31�December�2014 |

� |

31�December�2013 |

� |

|

Exchange rates |

� |

� |

� |

� |

� |

|

Translation �1 = |

� |

$1.61 |

� |

$1.60 |

� |

|

Transaction �1 = |

� |

$1.58 |

� |

$1.58 |

� |

|

Translation �1 = |

� |

�1.26 |

� |

�1.18 |

� |

|

Transaction �1 = |

� |

�1.24 |

� |

�1.23 |

� |

�

(b)�Acquisitions and disposals

�

The impact of acquisitions and disposals on the reported figures was primarily attributable to the acquisition of United Spirits Limited (USL).

�

(c)�Exceptional items

�

Exceptional operating charges of �171 million (2013 � �20 million) in the six months ended 31 December�2014 comprise:

�

������������������ �18 million (2013 � �nil) in respect of the Global efficiency programme announced in January�2014;

������������������ �11 million (2013 � �3 million) in respect of the Supply excellence restructuring programme;

������������������ a gain of �3 million (2013 � charge of �17 million) arising from a property sale in respect of the restructuring of the group�s supply operations; and

������������������ �145 million (2013 � �nil) representing an estimate of the income statement charge for the settlement cost of several related disputes with the Korean customs authorities regarding the transfer pricing methodology applicable to imported spirits. Payments to be made pursuant to settlement of these related disputes will be reduced by �88 million which was paid to the customs authorities prior to 30 June�2014, and was previously accounted for as a receivable from Korea customs.

�

In the second half of the year an exceptional operating charge of approximately �80 million is expected to be incurred primarily in respect of the Global efficiency and Supply excellence programmes.

�

Non-operating items in the six months ended 31 December�2014 include a gain of �103 million (2013 � gain of �140 million) following the acquisition of additional equity shares in USL which increased the group�s investment in USL from 25.02% to 54.78% excluding the 2.38% interest owned by the USL Benefit Trust (2013 � 10.04% to 25.02%). As a result of USL becoming a subsidiary of the group a gain is recognised on the difference between the book value of the 25.02% investment and the market value on the acquisition of the controlling stake on 2 July 2014. The gain includes a �79 million cumulative exchange loss recycled from other comprehensive income and �10 million of transaction costs.

�

Exceptional non-operating items comprise transaction costs of �5 million (2013 � �nil) in respect of the expected disposal of Bushmills.

�

Discontinued operations in the six months ended 31 December�2013 represent a charge after taxation of �92 million in respect of the settlement of the thalidomide litigation in Australia and New Zealand and anticipated future payments to thalidomide organisations.

�

Cash payments in the six months ended 31 December�2014 in respect of exceptional restructuring items and thalidomide were �62 million (2013 � �41 million) and �8 million (2013 � �2 million), respectively. Cash expenditure on exceptional restructuring items in the second half of the year is expected to be approximately �120 million.

�

(d)�Dividend

�

An interim dividend of 21.5 pence per share will be paid to holders of ordinary shares and ADRs on the register as of 27 February�2015. This represents an increase of 9% on last year�s interim dividend. The interim dividend will be paid to shareholders on 7 April�2015. Payment to US ADR holders will be made on 10 April�2015. A dividend reinvestment plan is available to holders of ordinary shares in respect of the interim dividend and the plan notice date is 12 March�2015.

�

�

Movement in net borrowings

�

|

� |

� |

2014 |

� |

2013 |

� |

|

� |

� |

� million |

� |

� million |

� |

|

Net borrowings at 30 June |

� |

(8,850 |

) |

(8,403 |

) |

|

Free cash flow (a) |

� |

699 |

� |

326 |

� |

|

Acquisition less sale of businesses (b) |

� |

(664 |

) |

(420 |

) |

|

Net purchase of own shares for share schemes (c) |

� |

(7 |

) |

(61 |

) |

|

Dividends paid to non-controlling interests |

� |

(34 |

) |

(61 |

) |

|

Purchase of shares of non-controlling interests (d) |

� |

� |

� |

(35 |

) |

|

Net movements in bonds (e) |

� |

(371 |

) |

(983 |

) |

|

Net movements in other borrowings (f) |

� |

1,316 |

� |

1,122 |

� |

|

Equity dividends paid |

� |

(801 |

) |

(735 |

) |

|

Net increase/(decrease) in cash and cash equivalents |

� |

138 |

� |

(847 |

) |

|

Net increase in bonds and other borrowings |

� |

(945 |

) |

(139 |

) |

|

Exchange differences (g) |

� |

(143 |

) |

337 |

� |

|

Borrowings acquired on acquisition of USL |

� |

(849 |

) |

� |

� |

|

Other non-cash items |

� |

(19 |

) |

(44 |

) |

|

Net borrowings at 31 December |

� |

(10,668 |

) |

(9,096 |

) |

�

(a)�See page�14 for the analysis of free cash flow.

�

(b)�On 2 July�2014 the group acquired an additional 26% investment in USL for INR 114.5 billion (�1,118 million). On 31 October�2014 the sale of the Whyte and Mackay Group by USL resulted in a net cash receipt of �395 million. In the six months ended 31 December�2013 cash payments primarily comprised �474 million in respect of the acquisition of a 18.74% investment in USL.

�

(c)�Net purchase of own shares comprised purchase of treasury shares for the future settlement of obligations under the employee share option schemes of �39 million (2013 � �116 million) less receipts from employees on the exercise of share options of �32 million (2013 � �55 million).

�

(d)�In the six months ended 31 December�2013 Diageo purchased the remaining 7% equity stake in Sichuan Chengdu Shuijingfang Group Co.,�Ltd.

�

(e)�In the six months ended 31 December�2014, the group repaid bonds of �1,000 million (�792 million) and issued bonds of �1,000 million (�791 million). In the comparable period, the group repaid bonds of �1,150 million (�983 million). A bond of �370 million acquired on the purchase of USL was repaid using the proceeds from the sale of the Whyte and Mackay Group.

�

(f)�Net movements in other borrowings are primarily in respect of the net drawdown of short term commercial paper which is used to finance day-to-day operations.

�

(g)�Exchange differences primarily arose on US dollar and euro denominated borrowings partially offset by the favourable change on foreign exchange swaps and forwards.

�

�

Movement in equity

�

|

� |

� |

2014 |

� |

2013 |

� |

|

� |

� |

� million |

� |

� million |

� |

|

Equity at 30 June |

� |

7,590 |

� |

8,088 |

� |

|

Profit for the period |

� |

1,364 |

� |

1,654 |

� |

|

Exchange adjustments (a) |

� |

266 |

� |

(770 |

) |

|

Net remeasurement of post employment plans |

� |

(341 |

) |

(89 |

) |

|

Exchange recycled to the income statement (b) |

� |

79 |

� |

� |

� |

|

Fair value movements on available-for-sale investments (b) |

� |

11 |

� |

(90 |

) |

|

Non-controlling interests acquired (b) |

� |

594 |

� |

� |

� |

|

Purchase of shares of non-controlling interests |

� |

� |

� |

(35 |

) |

|

Dividends to non-controlling interests |

� |

(34 |

) |

(61 |

) |

|

Dividends paid |

� |

(801 |

) |

(735 |

) |

|

Other reserve movements |

� |

(32 |

) |

76 |

� |

|

Equity at 31 December |

� |

8,696 |

� |

8,038 |

� |

�

(a)�Movement in the six months ended 31 December�2014 primarily arose on the US dollar, the euro, Brazilian real and the Indian rupee denominated net investments.

�

(b)�Following the change in accounting for USL from an associate to a subsidiary,�an exchange loss of �79 million has been recycled to the income statement in the six months ended 31 December�2014 and a 43.9% non-controlling interest has been recognised of �594 million. In the six months ended 31 December�2013 a gain of �85 million, in respect of USL, was recycled to the income statement reflecting the step up from available-for-sale investment to associate.

�

Post employment plans

�

The deficit in respect of post employment plans before taxation increased by �313 million from �475 million at 30 June�2014 to �788 million at 31 December�2014. The increase was primarily due to the reduction in returns from �AA� rated corporate bonds used to calculate the discount rates on the liabilities of the post employment plans (United Kingdom reduced from 4.2% to 3.5% and Ireland from 3% to 2.1%) partially offset by a reduction in long term inflation and an increase in the value of the assets held by the plans. Total cash contributions to the group�s post employment plans for the year ending 30 June�2015 are expected to be approximately �185 million.

�

Analysis by reporting segments

�

The organic movements for volume, net sales, marketing spend and operating profit before exceptional items by reporting segment for the six months ended 31 December�2014 were as follows:

�

|

� |

� |

Volume |

� |

Net�sales |

� |

Marketing�spend |

� |

Operating profit (a) |

� | ||||||||

|

Organic�growth�by�region |

� |

% |

� |

EUm |

� |

% |

� |

� million |

� |

% |

� |

� million |

� |

% |

� |

� million |

� |

|

North America |

� |

(2 |

) |

(0.6 |

) |

� |

� |

(1 |

) |

3 |

� |

8 |

� |

(1 |

) |

(7 |

) |

|

Europe |

� |

(1 |

) |

(0.2 |

) |

� |

� |

(4 |

) |

3 |

� |

6 |

� |

1 |

� |

3 |

� |

|

Africa |

� |

9 |

� |

1.1 |

� |

5 |

� |

38 |

� |

12 |

� |

9 |

� |

4 |

� |

7 |

� |

|

Latin America and Caribbean |

� |

(10 |

) |

(1.3 |

) |

(1 |

) |

(4 |

) |

3 |

� |

3 |

� |

7 |

� |

13 |

� |

|

Asia Pacific |

� |

(7 |

) |

(0.6 |

) |

(5 |

) |

(39 |

) |

(15 |

) |

(24 |

) |

(7 |

) |

(14 |

) |

|

Corporate |

� |

� |

� |

� |

� |

8 |

� |

3 |

� |

(20 |

) |

(1 |

) |

16 |

� |

11 |

� |

|

Diageo |

� |

(2 |

) |

(1.6 |

) |

� |

� |

(7 |

) |

� |

� |

1 |

� |

1 |

� |

13 |

� |

�

(a)�������� Before exceptional items.

�

�

North America

�

�Net sales in North America were in line with last year, given the slowdown in the US spirits market as a result of weaker pricing and our comparison against a strong first half last year. In our US Spirits and Wines business volume was down but continued strong performance of reserve brands was the main driver of 2.6 percentage points of price/mix.� Given our already premium price position in many categories, we have taken fewer price increases and engaged in more tactical promotional activities in the most competitive segments. Scotch shipments were down 9% against the prior period which benefitted from a number of innovations.� Depletions, however, were up for our scotch malts portfolio and Buchanan�s and both gained share, and Buchanan�s became the number two super premium scotch by value behind Johnnie Walker.� Our strength in innovation continues to be a key growth driver and C�roc Pineapple and Crown Royal Regal Apple contributed to overall growth in Diageo�s vodka and North American whiskey categories, up 6% and 3% respectively, while Captain Morgan gained share in rum driven by Captain Morgan White Rum.� Smirnoff saw improved consumer offtake driven by promotional activities and the new campaign and packaging, with the core brand gaining share.� Consumer demand for more authentic deluxe brands continued and our reserve brand business grew 10%, with strong performance from Don Julio and Bulleit which both outperformed their categories and gained share. In DGUSA net sales were broadly flat as ready to drink performance stabilised and the success of Guinness Blonde American Lager contributed to overall growth of the Guinness brand.� Diageo Canada has already seen some benefit from our new distribution system with net sales up 1%. Brand investment was up 3% focused on our innovation launches and Smirnoff.� Gross margin was negatively impacted by lower scotch shipments together with the one off impact on net sales from the change in the distribution system in Canada. This was only partially offset by lower overheads in the region and operating margin declined by 35 basis points.�

�

|

Key financials |

� |

First�Half |

� |

Exchange |

� |

Acquisitions |

� |

Organic |

� |

First�Half |

� |

Reported |

� |

|

Net sales |

� |

1,904 |

� |

(25 |

) |

(11 |

) |

(1 |

) |

1,867 |

� |

(2 |

) |

|

Marketing spend |

� |

293 |

� |

(4 |

) |

7 |

� |

8 |

� |

304 |

� |

4 |

� |

|

Operating profit before exceptional items |

� |

851 |

� |

(21 |

) |

(4 |

) |

(7 |

) |

819 |

� |

(4 |

) |

|

Exceptional items |

� |

(1 |

) |

� |

� |

� |

� |

� |

� |

(11 |

) |

� |

� |

|

Operating profit |

� |

850 |

� |

� |

� |

� |

� |

� |

� |

808 |

� |

(5 |

) |

�

|

� |

� |

Organic |

� |

Organic |

� |

Reported |

� |

|

� |

� |

volume |

� |

net�sales |

� |

net�sales |

� |

|

� |

� |

movement (a) |

� |

movement |

� |

movement |

� |

|

Markets and categories |

� |

% |

� |

% |

� |

% |

� |

|

North America |

� |

(2 |

) |

� |

� |

(2 |

) |

|

� |

� |

� |

� |

� |

� |

� |

� |

|

US Spirits and Wines |

� |

(3 |

) |

� |

� |

(1 |

) |

|

DGUSA |

� |

(2 |

) |

� |

� |

(1 |

) |

|

Canada |

� |

� |

� |

1 |

� |

(8 |

) |

|

� |

� |

� |

� |

� |

� |

� |

� |

|

Spirits (b) |

� |

(2 |

) |

� |

� |

(1 |

) |

|

Beer |

� |

(3 |

) |

(3 |

) |

(5 |

) |

|

Wine |

� |

2 |

� |

1 |

� |

1 |

� |

|

Ready to drink |

� |

(1 |

) |

1 |

� |

(12 |

) |

�

|

� |

� |

Organic |

� |

Organic |

� |

Reported |

� |

|

� |

� |

volume |

� |

net�sales |

� |

net�sales |

� |

|

� |

� |

movement (a) |

� |

movement |

� |

movement |

� |

|

Global giants and local stars (b) |

� |

% |

� |

% |

� |

% |

� |

|

Smirnoff |

� |

(5 |

) |

(7 |

) |

(8 |

) |

|

Crown Royal |

� |

� |

� |

(1 |

) |

(2 |

) |

|

Captain Morgan |

� |

(7 |

) |

(8 |

) |

(9 |

) |

|

Johnnie Walker |

� |

(4 |

) |

(14 |

) |

(15 |

) |

|

C�roc |

� |

27 |

� |

27 |

� |

26 |

� |

|

Ketel One vodka |

� |

(1 |

) |

(1 |

) |

(1 |

) |

|

Guinness |

� |

� |

� |

(1 |

) |

(3 |

) |

|

Baileys |

� |

(4 |

) |

(6 |

) |

(8 |

) |

|

Tanqueray |

� |

� |

� |

2 |

� |

1 |

� |

|

Don Julio |

� |

13 |

� |

21 |

� |

20 |

� |

|

Buchanan�s |

� |

30 |

� |

32 |

� |

31 |

� |

|

Bulleit |

� |

52 |

� |

59 |

� |

58 |

� |

�

|

(a) |

Organic equals reported movement for volume except for North America (3)%, US Spirits and Wines (4)%, spirits (3)% and ready to drink (17)% reflecting the termination of the transitional arrangements following the disposal of Jose Cuervo. |

|

(b) |

Spirits brands excluding ready to drink. |

�

|

|

|

�

�

|

� |

In US Spirits and Wines, which represents 82% of the net sales in the region, net sales were broadly flat, with 2.6pps of positive price/mix, driven by the double digit growth of reserve brands and innovation launches. Net sales in vodka grew 6% on the back of the successful launch of C�roc Pineapple which resulted in an overall net sales growth of 28% for the C�roc brand. High stock levels impacted Smirnoff net sales which were down 8%, however the relaunch of the brand with a new packaging and marketing campaign, coupled with targeted promotional activities have improved the core brand�s performance, which gained share. Captain Morgan net sales were down 9% as Captain Morgan Spiced Rum suffered from increasing competition in the spiced rum category and from lapping the launch of Captain Morgan White Rum last year, which performed well and gained share. Net sales in North American whiskey increased 3%, Bulleit continued to outperform the category with net sales up 58%, Crown Royal net sales declined 1%, with strong growth from the launch of Crown Royal Regal Apple offset by lapping the launch of Crown Royal XO in the same period last year. Johnnie Walker net sales were down 17% as it lapped the launch in the first half last year of super premium variants Johnnie Walker Platinum Label and Johnnie Walker Gold Label Reserve and the promotional activities and phasing of shipments in Johnnie Walker Black Label and Johnnie Walker Blue Label respectively. Buchanan�s net sales were up 33% as it continued to leverage its strong connection with the Hispanic community and it is now the second largest super premium scotch in value behind Johnnie Walker. Net sales of tequila were up 37%, driven by the continued success of Don Julio, with net sales up 21%, and the launches under Diageo�s ownership of the newly acquired Peligroso and DeLe�n brands. |

|

� |

DGUSA net sales were broadly flat, with volume down 2%. Guinness net sales were up 1%, driven by the successful launch of Guinness Blonde American Lager, but the core brand was still impacted by the decline in the on trade. Ready to drink net sales were up 2% as it benefitted from comparison against last year�s destocking in the pouches segment. |

|

� |

Net sales in Canada benefitted from the change in distribution system and increased 1%, with volume broadly flat. Growth in Johnnie Walker Black Label and reserve brands�partially offset the decline of Guinness, which was impacted by weakness in the on trade. |

|

� |

Marketing spend increased 3%, with the upweighted investment largely focused on supporting Smirnoff, with the new �Exclusively for Everybody� campaign, innovations such as C�roc Pineapple, Guinness Blonde American Lager, Crown Royal Regal Apple and Peligroso. |

�

�

Europe

�