Form 6-K CREDIT SUISSE GROUP AG For: Mar 23

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

Form 6-K

______________

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

March 23, 2016

Commission File Number 001-15244

CREDIT SUISSE GROUP AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

______________

Commission File Number 001-33434

CREDIT SUISSE AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

______________

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

|

Form 20-F ☒

|

Form 40-F ☐

|

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Credit Suisse Strategy UpdateAccelerating the Restructuring Tidjane Thiam, Chief Executive OfficerTimothy O’Hara, Chief Executive Officer of Global Markets David Mathers, Chief Financial Officer LondonMarch 23, 2016

Disclaimer Cautionary statement regarding forward-looking statementsThis presentation contains forward-looking statements that involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements. A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in "Risk Factors" in our Annual Report on Form 20-F for the fiscal year ended December 31, 2014 and in "Cautionary statement regarding forward-looking information" in our fourth quarter earnings release 2015 filed with the US Securities and Exchange Commission, and in other public filings and press releases. We do not intend to update these forward-looking statements except as may be required by applicable law. We may not achieve the benefits of our strategic initiatives We may not achieve all of the expected benefits of our strategic initiatives. Factors beyond our control, including but not limited to the market and economic conditions, changes in laws, rules or regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives.Year to date financial information is subject to further reviewThe selected YTD 2016 financial information presented herein is preliminary and only reflects certain of our results for certain 2016 periods specified in this presentation. This data has not been evaluated, reviewed or audited by our independent registered public accounting firm. Accordingly, the YTD 2016 financial information contained in this presentation is inherently subject to change. This data should not be taken as a forecast or prediction of our results for 1Q16 as a whole or any other future periods. Statement regarding purpose and basis of presentationThis presentation contains certain historical information that has been re-segmented to approximate what our results under our new structure would have been, had it been in place from January 1, 2014. In addition, "Illustrative,“ “Ambition” and “Goal” presentations are not intended to be viewed as targets or projections, nor are they considered to be Key Performance Indicators. All such presentations are subject to a large number of inherent risks, assumptions and uncertainties, many of which are outside of our control. Accordingly, this information should not be relied on for any purpose. In preparing this presentation, management has made estimates and assumptions which affect the reported numbers. Actual results may differ. Figures throughout presentation may also be subject to rounding adjustments.Statement regarding non-GAAP financial measuresThis presentation also contains non-GAAP financial measures. Information needed to reconcile such non-GAAP financial measures to the most directly comparable measures under US GAAP can be found in this presentation, which is available on our website at credit-suisse.com.Statement regarding capital, liquidity and leverage As of January 1, 2013, Basel 3 was implemented in Switzerland along with the Swiss “Too Big to Fail” legislation and regulations thereunder. As of January 1, 2015, the Bank for International Settlements (BIS) leverage ratio framework, as issued by the Basel Committee on Banking Supervision (BCBS), was implemented in Switzerland by FINMA. Our related disclosures are in accordance with our interpretation of such requirements, including relevant assumptions. Changes in the interpretation of these requirements in Switzerland or in any of our assumptions or estimates could result in different numbers from those shown in this presentation. Capital and ratio numbers for periods prior to 2013 are based on estimates, which are calculated as if the Basel 3 framework had been in place in Switzerland during such periods. Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. Leverage amounts for 4Q14, which are presented in order to show meaningful comparative information, are based on estimates which are calculated as if the BIS leverage ratio framework had been implemented in Switzerland at such time. Beginning in 2015, the Swiss leverage ratio is calculated as Swiss total capital, divided by period-end leverage exposure. The look-through BIS tier 1 leverage ratio and CET1 leverage ratio are calculated as look-through BIS tier 1 capital and CET1 capital, respectively, divided by end-period leverage exposure.Cautionary statement regarding this presentationThis presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of Credit Suisse Group AG or Credit Suisse AG (together, the “Company”) in any jurisdiction or an inducement to enter into investment activity. No part of this document, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein. None of the Company or any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with the document. 2 March 23, 2016

3 March 23, 2016 Summary Our recent performance has further highlighted two key areas of challenge for Credit Suisse:Our fixed cost base and Our scale in Global Markets in the Americas and EuropeThis has translated into pressures on our capital position as demonstrated in a lower than expected CET1 ratio as reported at the end of 4Q15. A number of actions had been underway since October, to address these challenges. We had set ourselves:A gross cost saving target of CHF 3.5 bn by the end 2018A RWA target of USD 83-85 bn in Global Markets by end 2018 from USD 118 bn at 3Q15When we presented our 4Q15 results on February 4, we said that we would reassess our plans to (i) reduce our cost base and (ii) right size Global Markets. Since then, the market environment has remained unsupportive, with continued pressure in 1Q16. Like for the previous quarter, Global Markets will contribute a negative result in 1Q16, albeit at lower levels. We have now completed the reassessment of our plans and we are announcing today a step up in the pace of our restructuring with:An increase of our gross cost saving target from CHF 3.5 bn to CHF 4.3 bn with a CHF 1.7 bn gross cost savings target for 2016A new RWA target of USD 60 bn for Global Markets, approximately 30% below the previous targets

4 March 23, 2016 Accelerating the restructuring Group Costs Global Markets 2015 year endUSD 83 – 85 bn1USD 380 bn 2018CHF 3.5 bnCHF 2.0 bnCHF 18.5 – 19.0 bn CHF 4.3 bn> CHF 3.0 bn< CHF 18.0 bn Implement initiatives to drive cost savings of CHF 1.7 bn in 2016Reduce certain illiquid inventoriesOptimize Global Markets business portfolio with less volatile earningsTarget growth investments with CHF 1.0 bn of the CHF 1.5 bn announced being discretionaryDispose of assets and businesses of at least CHF 1.0 bn in 2016Partial IPO2 of Swiss UB3 planned for 2017 Targets announced at Investor Day 2018 targets(Today) USD 60 bnUSD 290 bn CHF 1.7 bnCHF 1.4 bnCHF 19.8 bn 2016 targets(Today) RWALeverage Gross cost savingsNet cost savingsOperating cost base 1 Compares to USD 118 bn in 3Q15. 2 Market conditions permitted. Any such IPO would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG. 3 More precisely, Credit Suisse (Schweiz) AG .

5 March 23, 2016 CHF 1.7 bn of gross cost savings in 2016 Note: Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses, restructuring costs and goodwill impairment taken in 4Q15, but including other costs to achieve savings. Headcount includes permanent FTEs, contractors, consultants and other contingent workers. Gross savings in CHF bn 2016 target Committed reduction to global headcount in 2016 Announced today As announcedFeb 4 Total 2016 commitment Additional headcount reduction based on acceleration of GM restructuring

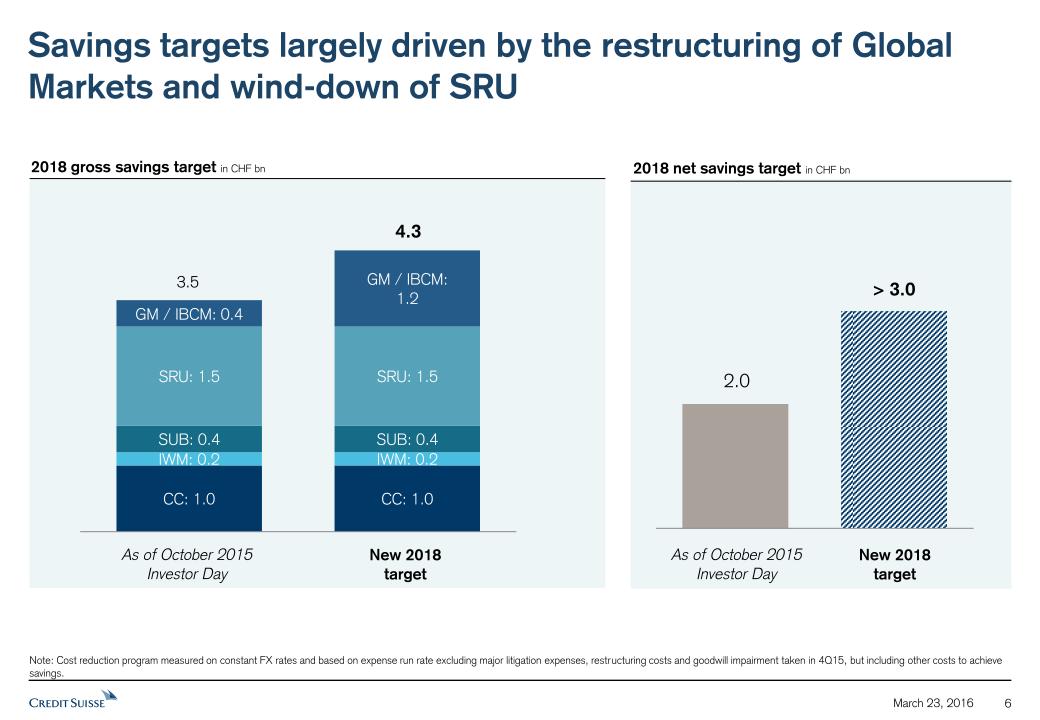

6 March 23, 2016 Savings targets largely driven by the restructuring of Global Markets and wind-down of SRU Note: Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses, restructuring costs and goodwill impairment taken in 4Q15, but including other costs to achieve savings. 2018 gross savings target in CHF bn 4.3 3.5 As of October 2015Investor Day New 2018 target As of October 2015Investor Day New 2018 target 2018 net savings target in CHF bn GM / IBCM: 0.4

7 March 23, 2016 Our new target cost base for 2018 is less than CHF 18 bn Note: Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses, restructuring costs and goodwill impairment taken in 4Q15, but including other costs to achieve savings. Target cost base in CHF bn Prior 2018Target 2016Target New 2018Target 19.8 18.5 – 19.0 <18.0 2015adjusted 21.2 o/w GM:CHF 6.3bn(USD 6.6bn) Group-wide strategic cost transformation in placeProgress on cost is supporting further acceleration of the program

8 March 23, 2016 Strategic analysis of Global Markets business portfolio – update since Investor Day Note: This slide presents financial information based on results under our old structure prior to our re-segmentation announcement on October 21, 2015.1 RoC calculated using income after tax, assuming tax rate of 30% and capital allocated on the highest of 10% Basel III risk-weighted assets or 3.5% end of 2014 leverage exposure. Analysis presented at Oct 2015 Investor Day

9 March 23, 2016 Global Markets performance deteriorated in 2015 with a disappointing 4Q15 and continued pressure in 1Q16 Reported pre-tax income in USD mn ‘Negative’ operational leverageAdverse market environment and depressed level of client activitySubstantial write-downs on legacy inventory in 4Q15GM bonuses lower by ~35% for 2015 1Q15 2Q15 3Q15 4Q151 1 Adjusted for goodwill impairment. 1Q16 Negative contribution continuing in 1Q16 albeit at lower levels

This resulted from outsized positions in activities not in line with the Global Markets strategy (1/2)… 10 March 23, 2016 US CLO Secondary exposures (market value) in USD mn

This resulted from outsized positions in activities not in line with the Global Markets strategy (2/2)… 11 March 23, 2016 Distressed Credit exposure (market value) in USD mn

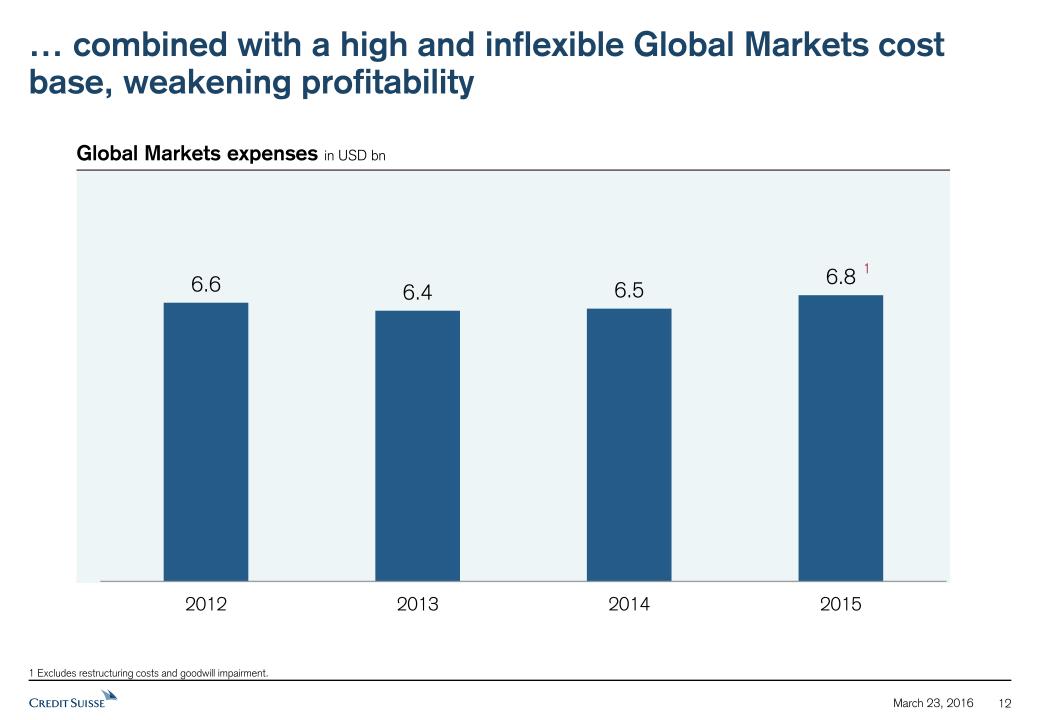

12 March 23, 2016 1 Excludes restructuring costs and goodwill impairment. Global Markets expenses in USD bn … combined with a high and inflexible Global Markets cost base, weakening profitability 1

This was compounded by challenging markets … 13 March 23, 2016 High Yield – spread to worst in bps March 22, 2016 809bps

… reduced client activity levels… 14 March 23, 2016 Source: Dealogic, March 17, 2016 YTD. Equity Capital Markets issuance volume in USD bn Leveraged Finance (HY) issuance volume in USD bn

…and external pressures 15 March 23, 2016 Central bank policiesLow liquidityHigh volatilityRegulatory change

We have taken immediate action and wound down outsized positions (1/2) 16 March 23, 2016 Distressed Credit Exposures (market value) in USD bn Gross write-downs 1Q16 YTD as of March 11: USD 99 mn as of March 11

We have taken immediate action and wound down outsized positions (2/2) 17 March 23, 2016 US CLO Secondary Exposures (market value) in USD bn Gross write-downs 1Q16 as of March 11: USD 64 mn as of March 11

18 March 23, 2016 Further write-downs expected in 1Q16, although at lower levels compared to 4Q15 Securitized Products (incl. CLO Secondary) Distressed Credit Corporate Bank2 Leveraged Finance Underwriting1 1 Reflects pre-IBCM JV. 2 Excludes MBPS.Note: Numbers not adding up due to rounding. (21)% (59)% (60)% Exposure reductionsas of March 11 633 346 Gross write-downs in USD mn

Low Connectivity 19 Decision matrix criteria Client Connectivity Corporates / Private Equity Connectivity Wealth Management Connectivity Core Institutional Clients High Utilization Low Quality Exit or RationalizeSubstantial reduction of illiquid inventoriesReduction in Securitized Products’ scaleRationalization of EMEA footprintConsolidation of derivative activities and platform rationalization Resource Usage Low Velocity of Capital Capital Intensity Funding Requirement Quality of Earnings Volatility of Earnings Counter-cyclical Performance Operating Leverage High Connectivity Low Resource Intensity Low Volatility, Strong Operating Leverage Invest or MaintainProducts directly supporting private banking, core institutional clients and corporates / private equityGlobally distinctive capabilities in Equities and CreditCross-asset solutions and electronic trading capabilities More fundamentally, we have taken a fresh look at our Global Markets’ business portfolio March 23, 2016

20 March 23, 2016 We are reconfiguring our Global Markets portfolio of businesses Equities Maintain / Invest Rationalize Exit Prime brokerageFlow Prime FinancingCash EquitiesEquity Capital Markets Credit Leveraged Finance Capital MarketsInvestment Grade Capital Markets Distressed CreditEuropean Securitized Products Trading Solutions US Rates Long-Term Illiquid Financing Flow Credit TradingUS Securitized Products Trading Global Asset FinanceSingle Name & Illiquid CDS Structured Eq DerivativesFlow Eq DerivativesCorporate Eq DerivativesConvertiblesStructured CreditFund-Linked ProductsEmerging Markets Financing 35%RWAreduction 16%RWAreduction Developed and Emerging Markets FX Trading (transfer to STS)

… and reducing Global Markets capital usage 21 March 23, 2016 Leverage and RWA in USD bn 380 RWA Leverage 317 290

22 March 23, 2016 This will reduce volatility of earnings and improve the risk-adjusted performance of the Global Markets portfolio The reduction in risk exposure to illiquid assets in Securitized Products and Distressed Credit portfolio improves the overall risk profile in Global MarketsReduction in modelled Flight-to-Quality metrics and smaller business footprint translates into significantly lower potential Pre-Tax Income quarterly losses 1 Maximum Quarterly PTI loss based on Flight-to-Quality (“FTQ”) losses adjusted for management actions (position sale, hedging), net of fees, commissions, carry and client monetization income over fixed quarterly expenses. GM Volatility – Maximum quarterly PTI loss in stress scenario1 ~(50)% 2015 baseline De-risking Target

Global Markets will be smaller and more focused post restructuring 23 March 23, 2016 Equities Electronic Products Credit Solutions Client Coverage and Content Emerging Markets(Latin America, Eastern Europe, Middle East, Africa)

24 March 23, 2016 We will continue to build on our leading Equities capabilities… #1 share trader in the world1including access to key emerging markets EQ onshore presence Access to market Americas: Market access to: - 7 countries - 23 exchanges EMEA: Market access to: - 21 countries (plus 4 multi-country exchanges) - 33 exchanges APAC: Market access to: - 11 countries - 19 exchanges AMER APAC EMEA % of Daily Exchange Notional Executed by CS2 11.0% 10.7% 17.1% 1 Multiple sources including Bloomberg Rank, Greenwich, exchanges, reporting countries, Markit MSA. 2 Credit Suisse analysis based on 2015 Average Daily Notional.

25 March 23, 2016 … and Equity Capital Markets franchise Rank Bank Deal Value1 (USD bn) # of Deals % Share 1 JP Morgan 24.3 188 11.4 2 Credit Suisse 22.8 150 10.7 3 Morgan Stanley 20.7 152 9.7 4 Goldman Sachs Co. 20.6 148 9.7 5 Citi 19.4 159 9.1 6 Bank of America 17.9 171 8.4 7 Barclays 17.7 131 8.3 IFR Awards 2015: Credit Suisse IFR Americas Equity House of the Year 2015 US Equity Capital Markets Rankings Source: Dealogic US ECM league table. Dealogic standard criteria – apportioned credit to book runners. 1 Apportioned deal value.

DATE 26 Global Markets updateTimothy O’Hara, Chief Executive Officer of Global Markets Timothy O’HaraChief Executive Officer of Global Markets

Low Connectivity 27 Decision matrix criteria Client Connectivity Corporate / Private Equity Connectivity Wealth Management Connectivity Core Institutional Clients High Utilization Low Quality Exit or RationalizeSubstantial reduction of illiquid inventoriesReduction in Securitized Products’ scaleRationalization of EMEA footprintConsolidation of derivative activities and platform rationalization Resource Usage Low Velocity of Capital Capital Intensity Funding Requirement Quality of Earnings Volatility of Earnings Counter-cyclical Performance Operating Leverage High Connectivity Low Resource Intensity Low Volatility, Strong Operating Leverage Invest or MaintainProducts directly supporting private banking, core institutional clients and corporate / private equity clientsGlobally distinctive capabilities in Equities and CreditCross-asset solutions and electronic trading capabilities Portfolio assessment against our strategic aspirations Reinvest in products that meet our criteria, exit or refocus those that do not March 23, 2016

28 Global Markets remains critical to Credit Suisse’s strategy Equities Equity Capital MarketsElectronic and High-Touch Cash Trading Prime Services and Delta One Listed Derivatives and Clearing Electronic Products Credit Solutions Global Corporate Credit Origination and TradingUS Securitized Products Origination and Trading Global Asset Finance Cross-asset structured notes for HNWI and retail clients Select OTC derivative solutionsDerivative-linked lendingUS Rates Origination and trading of Equities, including Prime Services Origination and trading of Credit products Structured lending and selected derivative capabilities Client Coverage and Content Emerging Markets(Latin America, Eastern Europe, Middle East, Africa) Intended to create a business model with reduced risk profile and reduced earnings volatility. Supports a growing bias towards products that generate recurring revenuesAn immediate focus on complexity reduction and operating margin improvement. Execution will need to balance speed against exit costs. `HNWI = High Net Worth Individuals A client-centric investment bank built organically around the Group’s strong historic client franchises – private banking, core institutional clients and corporates March 23, 2016

A focused approach to core clients 29 Serving core client segments with products and services in which we excel Core Clients Wealth Management Core Institutional Corporate & Private Equity Delivering products and solutions to the Private BankIncreased focus on the provision of investment banking products to HNWI and UHNWIDevelopment of stronger internal distribution relationshipsSimpler organizational structure of product expertise Focused on Institutional ClientsIntensify focus on strategic clients to maximize wallet shareHolistic coverage via low-touch model Stronger alignment of cost and resource allocation with most profitable clientsLeaning into key account management to drive multi-asset revenues from core clientsLook to grow fee-driven businesses which also include products that generate recurring revenuesInvest and expand low-touch execution capabilities leveraging market leading AES brand Driving our Corporate and Private Equity RelationshipsContribute further to the development of the Group’s corporate and private equity franchiseGrowing focus on investment grade corporates Reiterate existing coverage strengths with high-yield clientsMaintain core coverage strengths with Leveraged Finance clients Wealth Management Core Institutional Corporate & Private Equity UHNWI = Ultra High Net Worth Individuals March 23, 2016

30 Cash Equities market share Prime Services leverage exposure optimization Source: Third Party Competitive Analysis RoA in bps Source: Credit Suisse Analysis; RoA (Returns on Assets) calculated using 5 quarter average leverage exposure +58% 2014 2015 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Global 3 3 3 3 3 3 3 3 AMER 2 2 3 2 3 3 3 3 EMEA 2 2 3 3 3 3 2 3 Product Strategies: Equities & Solutions Defend our market leading Prime and Cash franchises by reallocating leverage exposure into core Prime client base and investing in content and technology Equities Create a simplified cross-asset structured derivatives and lending offering for core CS clients Solutions Current state Solutions landscape: Macro Credit EMG Equities Prime Flow Derivatives Financing Flow Derivatives Structured Derivatives Structured Derivatives Structured Derivatives Financing Structured Derivatives Financing Financing Product Offering Op Model Flow Derivatives Market Making Utility Cross-Asset Structured Solutions Derivatives Financing Solutions Single Operating Model and Front-to-Back Infrastructure US Equity, Rates and FX Options and Convertibles Market Making Rates, FX, Equities, Credit & Fund-Linked Investment Products Structured lending against Equities, Credit and Fund Collateral Target state model: Risk Mgmt TradeMgmt March 23, 2016

31 Credit Products RWA evolution (in USD bn) Credit Products client footprint1 Product Strategies: Credit Sector Mix2 Divisional Client Overlap3: 40% Flow Trading Customer Financing Corporate Bank Distressed Trading Capital Markets (13)% (1) Based on 2015 & 2014 FY client revenue data; (2) Sector Mix: Real money includes Investment Managers, Insurance, Pensions, Government/Public, Sovereign Wealth Funds;(3) Divisional Client Overlap: APAC = APAC domiciled clients; IWM = Activity with IWM + Referrals; IBCM = Clients within IBCM that are also clients of GM Securitized Products client footprint1 Securitized Products RWA evolution (in USD bn) Sector Mix2 Divisional Client Overlap3: 41% Private Bank / Retail 1% US SP Trading EU SP Trading (41)% Global Asset Finance Right-size risk and capital profile, reduce revenue volatility while maintaining market-leading franchises 2015 Actuals 2015 Actuals March 23, 2016

VIX VDAX 32 1Q16 has been a challenging quarter Continued market uncertainty has slowed client activity Fund flow trends (in USD bn) Volatility metrics 2 yr Avg: 161Q16 QTD Avg: 22 2 yr Avg: 221Q16 QTD Avg: 29 Emerging Markets Funds3 YTD 2016 Commentary YTD’16, trading revenues have been disappointing and are expected to be down 40-45% compared to 1Q’15Credit Products and Securitized Products have been most affected with slower client activity and further mark-to-market losses. Emerging Markets has seen much lower levels of client activity as geopolitical nervousness and continued uncertainty about the Chinese economy has resulted in outflow of funds. Equities has been less affected with solid results in Cash Equities, Equity Derivatives and Prime Services, compared to prior year.Meanwhile, Macro results have improved benefitting from higher levels of market volatility. US High Yield Funds2 Global issuance volume1 (in USD bn) Institutional Loans High Yield Leveraged Finance Investment Grade (62)% (10)% Note: QTD ’15 is as of March 16, 2015; QTD ‘16 is as of March 16, 2016. Source: (1) Leveraged Finance: Credit Suisse US Credit Strategy (includes Americas and EMEA); Investment Grade: US IG Syndicate (US), Bondradar (EMEA) (2) EPFR (based on funds that report weekly data through to March 9th, 2016 and daily data from March 10th to March 15th, 2016); (3) Morningstar Asset Flows, includes equity and fixed income funds as of Jan 31, 2016 March 23, 2016

33 Improving the risk-adjusted performance of the portfolio GM Volatility – Quarterly Loss Maximum Quarterly Pre-Tax Income Loss in Stress Scenario4 ~(50)% Reduced Volatility (1) Return on regulatory capital is calculated using income after tax, reflects ‘worst of' return on RWA or leverage exposure; (2) As-reported by Credit Suisse (2011-2015), excludes goodwill and major litigation items, 2011-13 reported leverage exposure estimated based on 2014 Add-On; (4) Scenarios based on varying macro-economic assumptions; (4) Maximum Quarterly PTI loss based on flight-to-quality 5(“FTQ”) losses adjusted for management actions (position sale, hedging), net of fees, commissions, carry and client monetization income over fixed quarterly expenses; (5) A stress scenario defined as a position loss in an event of one-week of turbulent markets The restructured Global Markets’ business portfolio aims to generate returns on regulatory capital that are more stable through the cycleThe reduction in resources allocated to Securitized Products and Leveraged Finance affects two of Global Markets’ historically highest returning businesses. The reduction in risk exposure to illiquid assets in Securitized Products and Distressed Credit portfolios improves the overall risk profile in Global Markets.Reduction in modelled Flight-to-Quality5 metrics and smaller business footprint translates into significantly lower potential Pre-Tax Income quarterly losses GM evolution of returns RescaledFootprint Return on Regulatory Capital1 Historic Average2 2.7% 14.3% 10.2% Target Average3 Changes lead to more stable structural returns and higher quality of earnings March 23, 2016

2015 Year-End vs. Target (USD bn) RWA Leverage Exposure (30)% (22)% Further optimization of Global Markets reduces the division’s previous target RWA level by 30%, from USD 83-85bn to ~USD 60bn.Division-wide RWA reductions will be driven by inventory reductions in Securitized Products, Distressed Credit, CLO Secondary and other illiquid inventories. Global Market’s target for leverage exposure will be reduced a further 22%, from USD 370bn to ~USD 290bn.The primary drivers for leverage exposure reduction are reductions in Securitized Products and Illiquid or Long-Dated Customer Financing, partially offset by additional reinvestment in Prime Services. Reducing levels of resource consumption across Global Markets Changes will drive significant reductions in RWA and leverage exposure (1) As of October 21, 2015 1 1 34 Rationalization/ Realignment Rationalization/ Realignment (pre-inflation) March 23, 2016

2015 Year-End vs. Target Cost Reductions (USD bn) Operating costs to be reduced by a further USD 1.2bn as a result of the new divisional structure and the previously announced ongoing London Rightsizing initiative. Savings will be predominantly driven by: Reduction of front office headcount and further reduction in functions that support Global MarketsEfficiency programs including migrating Derivatives infrastructure onto a single, common platform across Solutions – a transformation of end-to-end processes and technology (~USD 0.2bn), and London rightsizing (~ USD 0.1bn)The estimated cost-to-achieve to achieve savings is forecast at USD 1.2bn, with ongoing target operating costs for Global Markets expected to be 20% lower than 2015 adjusted operating expenses. Cost-to-Achieve: USD ~1.2bn (20)% Improving operating leverage in Global Markets Business exits and recalibration allow significant cost reductions to be targeted 35 1 Business exits and realignments relate to operations transferred across reporting segments and discontinued operations. 1 March 23, 2016

Strategic Aspirations New Targets How do we get there? Global Markets critical to Credit Suisse’s strategy focused on IWM, corporate and core institutional clientsIntroducing clients to primary capital markets, providing market access and delivering vanilla and structured financing solutionsBalanced between risk appetite and management of earnings volatility, with a bias towards flow and financing and a reduced platform in complex products Optimization of business portfolio Exits largely focused on illiquid credit businessesRe-sizing and geographical rationalization of Securitized ProductsRationalization of EMEASelect investment for growthGrow Prime Services and Equities CashInvest and expand low-touch execution capabilities leveraging market leading AES brandCollaborate with IBCM and IWM to align with their priorities Execution on cost savingsImproving weak structural operating leverage Platform consolidation in Derivatives Further front-to-back simplification in de-emphasized businessesImportant to balance speed of execution against exit costs Leading Equities Franchise with high connectivity to rest of Global Markets offering Equities Credit Products Solutions Top Tier Credit and Securitized Products suite with leadership positions in Developed and Emerging Markets Cross-asset class Solutions Group providing derivative and financing solutions (1) Excludes goodwill, major litigation expenses and restructuring expenses; (2) As of October 21, 2015 Leverage Exposure Operating Costs(incl. variable compensation) (20)% RWA (30)% (24)% Global Markets’ post-restructuring strategy ~290 USD bn USD bn USD bn 1 ~83-85 2 2 36 March 23, 2016

DATE 37 Group cost and capital strategyDavid MathersChief Financial Officer

Reduced cost base underpins a more resilient business model 38 March 23, 2016 20.5 Reduced deferral rates Appreciation of USD vs. CHF Restructuring expenses Swiss holiday accrual Increased litigation provisions Others 2015excl. goodwill impairment 9M15annualized Restructuring expenses Major litigation expenses 2015adjusted 0.1 0.1 0.4 0.1 0.5 0.1 22.1 (0.4) (0.8) 2015 Total operating expenses development in CHF bn 0.3 Indirect taxes 2015 4Q15 21.2 20.9 0.3 Full-year impact of 4Q USD/CHF = 1.00

GM restructuring to result in increased cost savings 39 March 23, 2016 Overview of key savings initiatives CorporateCenter1 SharedServices Other Front Office and SRU Expenses 2018 Gross Cost Savings 1.0 0.9 1.6 4.3 Corp. CenterSubstantial completion of major programs including regulatory projects ServicesEfficiencies from workforce strategy and London right-sizing, etc. SRU & ExitsWind-down of SRU portfolio, business exits, and associated costs 1 2 3 Note: Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses, restructuring costs and goodwill impairment taken in 4Q15, but including other costs to achieve savings. 1 Includes rundown of realignment costs. Gross Cost Savings ~ 0.5 – 1.0 > 3.0 2018 NetCost Savings Reinvestment Additional savings from accelerated GM restructuring Sources of cost savings Investments to facilitate growth Reinvestment plan prioritized for relationship manager recruitment and growth priorities in APAC and IWM

40 March 23, 2016 Revised cost savings target will support a more resilient operating model Note: Cost reduction program measured on constant FX rates and based on expense run rate excluding major litigation expenses, restructuring costs and goodwill impairment taken in 4Q15, but including other costs to achieve savings. Cost program will achieve increased savings, particularly in fixed costs Target Gross Cost Savings in CHF bn Target Net Cost Savings in CHF bn Target Cost Base in CHF bn New 2018Target Prior 2018Target New 2018Target Prior 2018Target Prior 2018Target New 2016Target New 2018Target 4.3 3.5 > 3.0 2.0 19.8 18.5 – 19.0 < 18.0

Revised GM plan will involve additional restructuring costs, particularly in 2016 Restructuring cost guidance as of October 2015 Investor Day in CHF bn Revised guidance onrestructuring costs in CHF bn Business exits and reductions London initiative Workforce strategy Infrastructure efficiency programs 0.6 0.6 0.1 41 March 23, 2016 0.4 1.0 0.6

42 March 23, 2016 SRU on track to deliver CHF 1.5 bn of savings by 2018 Restructuring and major litigation expenses not shown for 1Q16E, 2015, 2016E and 2017E. Illustrative development ofdirect and indirect expenses in CHF mn Direct expenses Restructuring 255 Major Litigationexpenses Indirect expenses 642 153 176 466 ~300 2,347 ~150 ~450 1,050 Direct andindir. expenses Illustrative development ofRWA in CHF bn ~1,600 62 ~57-58 ~45 ~1,000 ~37 Continued progress of wind-down of our Strategic Resolution Unit Plan prior to Global Markets restructuring Operational risk Credit and market risk 19 43 ~(60)%excl. ops risk

43 March 23, 2016 Exit from PB US on track to deliver target cost savings Direct expenses1 in USD mn Sale of PB US expected to release cost savings of USD 0.5 bn in 20162016 exit costs expected to be ~USD 150 mn, split roughly 50/50 between wind-down and restructuring costsSale of the Private Banking businesses in Monaco and Gibraltar to J. Safra Sarasin signed 70 8 128 6 1 Excludes restructuring.

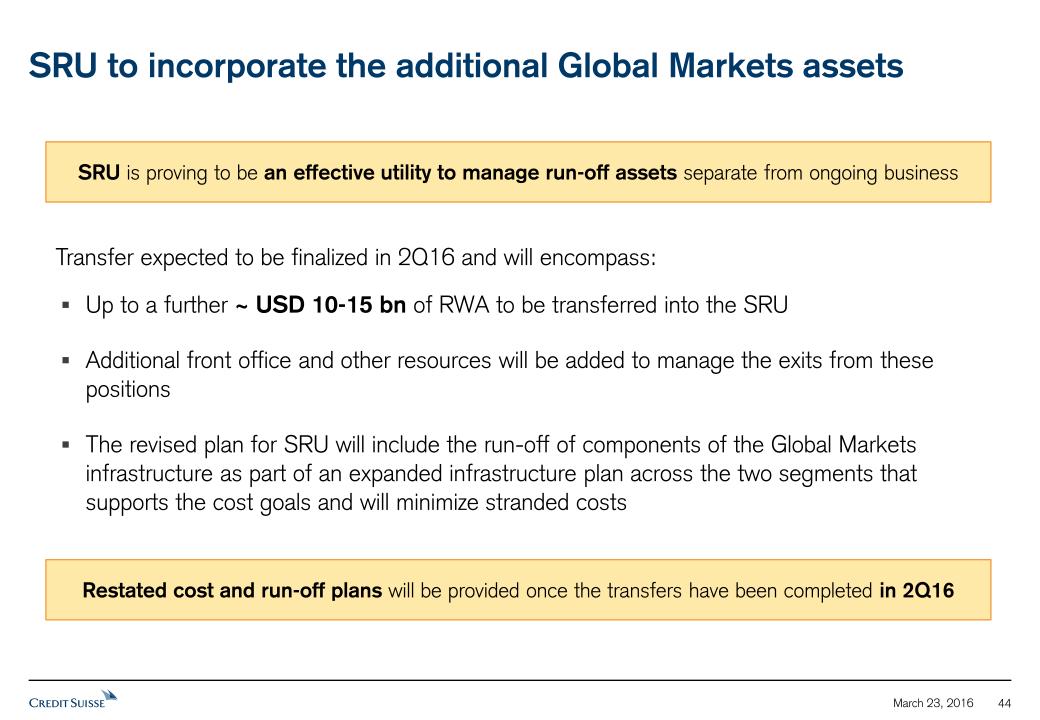

44 March 23, 2016 SRU to incorporate the additional Global Markets assets Transfer expected to be finalized in 2Q16 and will encompass:Up to a further ~ USD 10-15 bn of RWA to be transferred into the SRUAdditional front office and other resources will be added to manage the exits from these positionsThe revised plan for SRU will include the run-off of components of the Global Markets infrastructure as part of an expanded infrastructure plan across the two segments that supports the cost goals and will minimize stranded costs SRU is proving to be an effective utility to manage run-off assets separate from ongoing business Restated cost and run-off plans will be provided once the transfers have been completed in 2Q16

45 “Look-through” Basel III CET1 ratio 11.4% 4Q15 3Q15 10.2% 2Q15 10.3% 1Q15 10.0% Capital position substantially strengthened March 23, 2016

CET1 capital and ratio development in 4Q15 and through 2016 46 March 23, 2016 PTI = Pre-tax income. 1 Net of fees and taxes and including relating threshold impact for deferred tax assets. 2 Ratio based on 2015 year-end RWA. 3 Includes FX and the cash component of a dividend accrual, including relating threshold impact for deferred tax assets. Includes the assumption that 60% of the dividend is distributed in shares. Capital raise1 3Q15 CET1capital CET1 capital incl. capital raise Operating Free Capital Used excl. re-measurement Swiss pension Re-measurement Swiss pension Other3 4Q15 CET1capital 4Q15 capital generation in CHF bn 29.0 32.9 Increase in CET1 capital+ 3.9 35.4 CET1 ratio 10.2% 12.2%2 11.4% CET1 ratio 11-12% Maintain a CET1 ratio of 11-12% in 2016Subject to major litigation settlements 2016E

47 March 23, 2016 Measures to ensure delivery of our capital goals 1 Any such IPO would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG. CS Legal Entity Switzerland minority IPO1 On track for 2H17; expected capital impact of CHF 2 – 4 bn Business, real estate and other disposals / actions Potential scope to raise at least CHF 1 bn by end 2016 Global Markets wind-down Free up CHF 0.4 bn of capital by end 2017 Measures in place to strengthenour capital base Net cost savings Increased from CHF 2.0 bn to > CHF 3.0

2016: Expected to be the peak transformational year Costs Operating costs of CHF 19.8 bn in 2016, < CHF 18 bn by end of 2018SRU is a core component of this with expenses from the original portfolio expected to decline by ~ CHF 750 mn in 2016 and a further ~ CHF 600 mn in 2017The SRU utility will be further expanded in 2Q16 to support the Global Markets realignment, encompassing further GM infrastructure and developing an integrated plan with GM to minimize post run-off stranded costsRestructuring costs expected to peak in 2016 at CHF 1 bn before dropping to CHF 0.6 bn in 2017 Capital Plan Raise CHF 1 bn through disposals in 2016Improve capital generation through lower expensesIncrease capital in 2017 by CHF 2 – 4 bn through the minority IPO1 of our Credit Suisse Legal Entity Switzerland Dividend Policyas per Oct 21st, 2015 Recommendation of CHF 0.70 per share dividend with scrip option until we reach our capital target. In any event, we will not continue with scrip beyond 20172. We intend to move to 40% Operating Free Cash Generated (OFCG) payout as capital targets are met 48 March 23, 2016 1 Any such IPO would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG. 2 Until we reach our capital target however, we will recommend CHF 0.70 per share with a scrip alternative; we will discontinue the scrip once we have clarity on regulatory requirements and litigation risks. In any event, we will not continue with the scrip beyond 2017.

DATE 49 Accelerating the restructuringTidjane ThiamChief Executive Officer

Update: Asia Pacific 50 March 23, 2016 Diversified business platform with every country franchise profitable in 2015Continued NNA inflows (CHF 3.6 bn year-to-date) delivering stable growth and momentum to the Private BankStrong Investment Banking franchise, albeit impacted by lower client activity levels compared to 1Q15Stepping up pace in recruitment of Relationship ManagersIncreased product offerings and connectivity across Private Banking and Investment Banking businessesContinued focus on lending initiatives Number of relationship managers 470 +50 520 +70 590 610 - 625 For clarity: The NNA inflow figures referenced herein for Swiss UB, IWM and APAC refer to our current projections for the full 1Q16.

Update: Swiss Universal Bank 51 March 23, 2016 1 Advisory and discretionary mandates as percentage of total AuM, excluding AuM from the external asset manager (EAM) business. 2 Any such IPO would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG. Continued solid underlying NNA inflows (CHF 4.5 bn year-to-date)Progress on mandates penetration initiatives with an increase to 26% by end of 2015 to increase further in 2016Resilient pre-tax income performance expected in 1Q16Execution of measures to result in accelerated cost savingsOn track towards partial IPO2 of our Credit Suisse Legal Entity Switzerland: banking license submitted; expected to go live in 2H17 Mandates penetration1 16% 26% For clarity: The NNA inflow figures referenced herein for Swiss UB, IWM and APAC refer to our current projections for the full 1Q16.

Update: International Wealth Management 52 March 23, 2016 Focus on compliant business growth; joint venture with Palantir establishedRevenues on track to reach strong levels of 1Q15 for Private Banking, also reflecting strong net interest incomeContinued strong NNA inflows (CHF 7.1 bn year-to-date)Accelerated execution of cost savings measures in 2016 (CHF 200 mn p.a. expected)Implemented systematic coverage of strategic UHNW clientsSolid pipeline of new lending building up as we expand specialized and multi-collateral lending capabilities 520 Jan/Feb2015 480 Jan/Feb2016 Net Revenues in Private Banking in CHF mn For clarity: The NNA inflow figures referenced herein for Swiss UB, IWM and APAC refer to our current projections for the full 1Q16.

M&A and ECM at >50% of revenues by 2018, in USD bn(as presented at Investor Day) 53 March 23, 2016 Note: Excludes structured products; numbers not adding up due to rounding. IBCM continues to make progress against strategic objectives in challenging market conditions YTD M&A as a percent of total industry fees is at record levels for both the industry and CS, while CS YTD M&A revenues more than doubled YoYGrowing share with investment grade corporates which are accounting for a greater share of industry fees DCM Lev. Fin ECM M&A

54 March 23, 2016 1 Any such IPO would be subject to, among other things, all necessary approvals and would be intended to generate / raise additional capital for Credit Suisse AG or Credit Suisse (Schweiz) AG. 2 More precisely, Credit Suisse (Schweiz) AG. Stepping up the pace of our efforts to reduce our costs level and right size our Global Markets businessIncreased our net cost saving target for 2018 from CHF 2.0 bn to CHF 3.0 bnReducing the scale of our Global Markets footprint – Global Markets will be smaller, with more stable earnings and focused on our clients. Global Markets RWA at USD 60 bn and leverage exposure at USD 290 bn by end-2016 Maintain a strong capital position by (i) generating additional cost saving, (ii) reducing capital consumption in Global Markets, (iii) targeting our growth investments, (iv) disposing of assets and businesses for at least CHF 1 bnExecute a partial IPO1 of Swiss Universal Bank2 planned for 2017Post restructuring, be positioned to grow profitably and generate capital

DATE 55 Q&A

March 23, 2016

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrants have duly caused this report to be signed on their behalf by the undersigned, thereunto duly authorized.

|

CREDIT SUISSE GROUP AG and CREDIT SUISSE AG

|

||

|

(Registrants)

|

||

|

By:

|

/s/ Christian Schmid

|

|

|

Christian Schmid

|

||

|

Managing Director

|

||

| /s/ Claude Jehle | ||

| Claude Jehle | ||

| Date: March 23, 2016 | Director |

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- UBS (UBS) Said To Plan More Than 100 Job Cuts In Investment Bank - Bloomberg

- Barclays (BCS) Appoints Rafael Abati as Co-Head of Energy Transition EMEA

- Vistra Energy (VST) Announces Private Offerings of Senior Secured Notes and Senior Unsecured Notes

Create E-mail Alert Related Categories

SEC FilingsRelated Entities

Credit SuisseSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!