Form 485BPOS VANGUARD CMT FUNDS

Tweet

Tweet Share

Share

| SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

| Form N-1A | ||

| REGISTRATION STATEMENT (NO. 333-111362) | ||

| UNDER THE SECURITIES ACT OF 1933 | [X] | |

| Pre-Effective Amendment No. | [ ] | |

| Post-Effective Amendment No. 21 | [X] | |

| and | ||

| REGISTRATION STATEMENT (NO. 811-21478) UNDER THE INVESTMENT COMPANY ACT | ||

| OF 1940 | ||

| Amendment No. 22 | [X] | |

| VANGUARD CMT FUNDS | ||

| (Exact Name of Registrant as Specified in Declaration of Trust) | ||

| P.O. Box 2600, Valley Forge, PA 19482 | ||

| (Address of Principal Executive Office) | ||

| Registrant’s Telephone Number (610) 669-1000 | ||

| Heidi Stam, Esquire | ||

| P.O. Box 876 | ||

| Valley Forge, PA 19482 | ||

| Approximate Date of Proposed Public Offering: | ||

| It is proposed that this filing will become effective (check appropriate box) | ||

| [ ] | immediately upon filing pursuant to paragraph (b) | |

| [X] | on August 12, 2016 pursuant to paragraph (b) | |

| [ ] | 60 days after filing pursuant to paragraph (a)(1) | |

| [ ] | on (date) pursuant to paragraph (a)(1) | |

| [ ] | 75 days after filing pursuant to paragraph (a)(2) | |

| [ ] | on (date) pursuant to paragraph (a)(2) of rule 485 | |

| If appropriate, check the following box: | ||

| [ ] | This post-effective amendment designates a new effective date for a | |

| previously filed post-effective amendment. | ||

![]()

| Vanguard Market Liquidity Fund |

| Prospectus |

| August 12, 2016 |

| Investor Shares |

| Vanguard Market Liquidity Fund |

| This prospectus contains financial data for the Fund through the fiscal period ended February 29, 2016. |

| The Securities and Exchange Commission (SEC) has not approved or disapproved these securities or |

| passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense. |

| Contents | |||

| Fund Summary | 1 | Financial Highlights | 19 |

| Investing in Money Market Funds | 6 | Investing With Vanguard | 21 |

| More on the Fund | 8 | Glossary of Investment Terms | 22 |

| The Fund and Vanguard | 15 | ||

| Investment Advisor | 15 | ||

| Dividends and Taxes | 16 | ||

| Share Price | 17 | ||

Fund Summary

Investment Objective

The Fund seeks to provide current income while maintaining liquidity.

Fees and Expenses

The following table describes the fees and expenses you may pay if you buy and hold shares of the Fund.

| Shareholder Fees | |

| (Fees paid directly from your investment) | |

| Sales Charge (Load) Imposed on Purchases | None |

| Purchase Fee | None |

| Sales Charge (Load) Imposed on Reinvested Dividends | None |

| Redemption Fee | None |

| Annual Fund Operating Expenses | |

| (Expenses that you pay each year as a percentage of the value of your investment) | |

| Management Fees | 0.005% |

| 12b-1 Distribution Fee | None |

| Other Expenses | None |

| Total Annual Fund Operating Expenses | 0.005% |

1

Example

The following example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. It illustrates the hypothetical expenses that you would incur over various periods if you invested $10,000 in the Fund’s shares. This example assumes that the Fund provides a return of 5% each year and that total annual fund operating expenses remain as stated in the preceding table. You would incur these hypothetical expenses whether or not you redeem your investment at the end of the given period. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years |

| $1 | $2 | $3 | $6 |

Principal Investment Policies

The Fund invests in high-quality, short-term money market instruments, including certificates of deposit, banker’s acceptances, commercial paper, Eurodollar and Yankee obligations, and other money market securities. To be considered high quality, a security must be determined by Vanguard to present minimal credit risk based in part on a consideration of maturity, portfolio diversification, portfolio liquidity, and credit quality. The Fund invests more than 25% of its assets in securities issued by companies in the financial services industry. The Fund maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less.

Principal Risks

Effective on or before October 14, 2016, the Fund, as an institutional money market fund, will be required to transition to a floating net asset value (NAV) as a result of the SEC’s money market fund reforms. The Fund is designed for investors with a low tolerance for risk; however, the Fund is subject to the following risks, which could affect the Fund’s performance:

• Income risk, which is the chance that the Fund’s income will decline because of falling interest rates. Because the Fund’s income is based on short-term interest rates—which can fluctuate significantly over short periods—income risk is expected to be high.

• Manager risk, which is the chance that poor security selection will cause the Fund to underperform relevant benchmarks or other funds with a similar investment objective.

• Credit risk, which is the chance that the issuer of a security will fail to pay interest or principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that security to decline. Credit risk should be

2

very low for the Fund because it invests primarily in securities that are considered to be of high quality.

• Industry concentration risk, which is the chance that there will be overall problems affecting a particular industry. Because the Fund invests more than 25% of its assets in securities issued by companies in the financial services industry, the Fund’s performance depends to a greater extent on the overall condition of that industry and is more susceptible to events affecting that industry.

A sale or exchange of Fund shares is a taxable event. This means that you may have a capital gain to report as income, or a capital loss to report as a deduction, when you complete your tax return.

You could lose money by investing in the Fund. Because the share price of the Fund will fluctuate, when you sell your shares they may be worth more or less than what you originally paid for them. The Fund may impose a fee upon sale of your shares or may temporarily suspend your ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you should not expect that the sponsor will provide financial support to the Fund at any time.

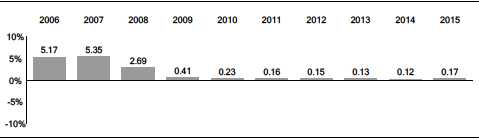

Annual Total Returns

The following bar chart and table are intended to help you understand the risks of investing in the Fund. The bar chart shows how the performance of the Fund has varied from one calendar year to another over the periods shown. The table shows how the average annual total returns of the Fund compare with those of a comparative benchmark, which has investment characteristics similar to those of the Fund. Returns for the Institutional Money Market Funds Average are derived from data provided by Lipper, a Thomson Reuters Company. Keep in mind that the Fund’s past performance does not indicate how the Fund will perform in the future. Updated performance information is available on our website at vanguard.com/performance or by calling Vanguard toll-free at 800-662-7447.

3

Annual Total Returns — Vanguard Market Liquidity Fund Investor Shares1

1 The year-to-date return as of the most recent calendar quarter, which ended on June 30, 2016, was 0.25%.

During the periods shown in the bar chart, the highest return for a calendar quarter was 1.36% (quarter ended December 31, 2006), and the lowest return for a quarter was 0.03% (quarter ended March 31, 2012).

| Average Annual Total Returns for Periods Ended December 31, 2015 | |||

| 1 Year | 5 Years | 10 Years | |

| Vanguard Market Liquidity Fund Investor Shares | 0.17% | 0.15% | 1.44% |

| Institutional Money Market Funds Average | 0.01% | 0.02% | 1.25% |

Investment Advisor

The Vanguard Group, Inc. (Vanguard)

Portfolio Manager

John C. Lanius, Portfolio Manager at Vanguard. He has managed the Fund since 2006.

4

Purchase and Sale of Fund Shares

The Fund has been established by Vanguard as a cash management vehicle for the Vanguard funds and certain trusts and accounts managed by Vanguard or its affiliates. The Fund is not available to other investors. Upon transition to a floating NAV on or before October 14, 2016, subscription orders in the Fund will only be able to be placed in dollars, while redemption orders can be placed in units or dollars.

Tax Information

The Fund’s distributions may be taxable as ordinary income or capital gain. If you are investing through a tax-deferred retirement account, such as an IRA, special tax rules apply.

Payments to Financial Intermediaries

The Fund and its investment advisor do not pay financial intermediaries for sales of Fund shares.

5

Investing in Money Market Funds

What is Money Market Reform?

In July 2014, the Securities and Exchange Commission (SEC) implemented a number of regulatory changes designed to enhance the stability and resilience of all money market funds. The reforms have created three categories of money market funds: • Retail money market funds, which may maintain a stable net asset value (NAV) but are subject to liquidity fees and redemption gates.

• Government money market funds, which may maintain a stable NAV but are not required to implement liquidity fees and redemption gates.

• Institutional money market funds, which are required to have a floating NAV and are subject to liquidity fees and redemption gates.

The board of trustees of Vanguard Market Liquidity Fund (the Board), in accordance with the best interest of the shareholders, approved a number of changes in response to the SEC’s 2014 amendments to the rules governing money market funds. The changes will become effective on or before October 14, 2016 (Compliance Date). Additional approvals are expected to be made, as needed, on or before the Compliance Date.

How Does This Affect Vanguard Money Market Funds?

The money market fund reforms adopted by the SEC in July 2014 will take effect during 2015 and 2016 on or before the Compliance Date. The reforms will impact money market funds differently depending on the types of investors permitted to invest in the fund and the types of securities in which the fund may invest.

Vanguard Market Liquidity Fund

Vanguard has designated Vanguard Market Liquidity Fund as an institutional money market fund.

Institutional money market funds are not limited to “natural persons” and may be held by institutional as well as retail investors. An institutional money market fund generally will no longer be permitted to use amortized cost or penny rounding methods to calculate NAV. Rather, an institutional money market fund will be required to transact at a market-based NAV calculated to four decimal places (i.e., at a floating NAV). If an institutional money market fund’s weekly liquid assets fall below a certain threshold, institutional money market funds are subject to fees and gates.

6

There are two types of liquidity fees: discretionary liquidity fees and default liquidity fees.

Discretionary liquidity fee. The Fund may impose a liquidity fee of up to 2% on all redemptions in the event that the Fund’s weekly liquid assets fall below 30% of its total assets if the Board determines that it is in the best interest of the Fund. Once the Fund has restored its weekly liquidity asset to 30% of total assets, any liquidity fee must be suspended.

Default liquidity fee. The Fund is required to impose a liquidity fee of 1% on all redemptions in the event that the Fund’s weekly liquid assets fall below 10% of its total assets unless the Fund’s Board determines that (1) the fee is not in the best interest of the Fund or (2) a lesser/higher fee (up to 2%) is in the best interest of the Fund.

In addition to, or in lieu of, the liquidity fee, the Fund is permitted to implement temporarily a redemption gate (i.e., suspend redemptions) if the Fund's weekly liquid assets fall below 30% of its total assets. The gate could remain in effect for no longer than 10 days in any 90-day period. Once the Fund has restored its weekly liquidity assets to 30% of total assets, the gate must be lifted.

The Fund is subject to money market fund reform regulatory risk, which is the chance that 2014 SEC reforms will affect the Fund's investment strategy, fees and expenses, portfolio, share liquidity, and return potential as the rules are implemented in 2015 and 2016.

7

More on the Fund

This prospectus describes the principal risks you would face as a Fund shareholder. It is important to keep in mind one of the main axioms of investing: generally, the higher the risk of losing money, the higher the potential reward. The reverse, also, is generally true: the lower the risk, the lower the potential reward. As you consider an investment in any mutual fund, you should take into account your personal tolerance for fluctuations in the securities markets. Look for this

symbol throughout the prospectus. It is used to mark detailed information about the more significant risks that you would confront as a Fund shareholder. To highlight terms and concepts important to mutual fund investors, we have provided Plain Talk® explanations along the way. Reading the prospectus will help you decide whether the Fund is the right investment for you. We suggest that you keep this prospectus for future reference.

symbol throughout the prospectus. It is used to mark detailed information about the more significant risks that you would confront as a Fund shareholder. To highlight terms and concepts important to mutual fund investors, we have provided Plain Talk® explanations along the way. Reading the prospectus will help you decide whether the Fund is the right investment for you. We suggest that you keep this prospectus for future reference.

Vanguard Market Liquidity Fund has been established by Vanguard as a cash management vehicle for the Vanguard funds and certain trusts and accounts managed by Vanguard or its affiliates. The Fund is not available to other investors. Vanguard reserves the right to change the availability of the Fund at any time without prior notice to shareholders. The Fund operates under an exemption issued by the SEC.

A Similar But Distinct Vanguard Fund

The Fund offered by this prospectus should not be confused with Vanguard Prime Money Market Fund, a separate Vanguard fund available only to retail investors that has a similar investment objective and similar policies but seeks to maintain a stable net asset value. The respective money market instruments held by the funds will differ. The funds’ holdings, combined with differences in the funds’ respective cash flows and expenses, are expected to produce different investment performances. Although Vanguard Market Liquidity Fund has lower expenses, investors should not expect this Fund necessarily to outperform Vanguard Prime Money Market Fund.

Vanguard Prime Money Market Fund offers its shares through a separate prospectus.

To obtain the prospectus for that fund, please call 800-662-7447.

| Plain Talk About Fund Expenses |

| All mutual funds have operating expenses. These expenses, which are deducted |

| from a fund’s gross income, are expressed as a percentage of the net assets of |

| the fund. Assuming that operating expenses remain as stated in the Fees and |

| Expenses section, Vanguard Market Liquidity Fund’s expense ratio would be |

| 0.005%, or $0.05 per $1,000 of average net assets. The average expense ratio |

| for institutional money market funds in 2015 was 0.18%, or $1.80 per $1,000 of |

| average net assets (derived from data provided by Lipper, a Thomson Reuters |

| Company, which reports on the mutual fund industry). |

8

| Plain Talk About Costs of Investing |

| Costs are an important consideration in choosing a mutual fund. That is because |

| you, as a shareholder, pay a proportionate share of the costs of operating a fund, |

| plus any transaction costs incurred when the fund buys or sells securities. These |

| costs can erode a substantial portion of the gross income or the capital |

| appreciation a fund achieves. Even seemingly small differences in expenses can, |

| over time, have a dramatic effect on a fund‘s performance. |

The following sections explain the principal investment policies that the Fund uses in pursuit of its objective. The Fund’s board of trustees, which oversees the Fund’s management, may change investment policies in the interest of shareholders without a shareholder vote, unless those policies are designated as fundamental. Note that the Fund’s investment objective is not fundamental and may be changed without a shareholder vote.

Market Exposure

The Fund’s principal policy is to invest in high-quality money market instruments. Also known as cash equivalent investments, these instruments are considered short-term (i.e., they usually mature in 397 days or less). The Fund maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less. The Fund invests more than 25% of its assets in securities issued by companies in the financial services industry.

| Plain Talk About Money Market Instruments |

| The term “money market instruments” refers to a variety of short-term, liquid |

| investments, usually with maturities of 397 days or less. Some common types |

| are U.S. Treasury bills and notes, which are securities issued by the U.S. |

| government; commercial paper, which is a promissory note issued by a large |

| company or a financial firm; banker’s acceptances, which are credit instruments |

| guaranteed by banks; and negotiable certificates of deposit, which are |

| promissory notes issued by banks in large denominations. Money market |

| securities can pay fixed, variable, or floating rates of interest. |

9

The Fund is subject to income risk, which is the chance that the Fund’s income will decline because of falling interest rates. A fund’s income declines when interest rates fall because the fund then must invest new cash flow and cash from maturing instruments in lower-yielding instruments. Because the Fund’s income is based on short-term interest rates—which can fluctuate significantly over short periods—income risk is expected to be high.

A low interest rate environment could adversely affect the Fund’s return. Low interest rates could prevent the Fund from providing a positive yield.

Security Selection

The Vanguard Group, Inc. (Vanguard), advisor to the Fund, selects high-quality money market instruments. The Fund focuses on securities of a particular class of issuer (the U.S. government, U.S. government agencies, or nongovernment issuers).

The Fund is subject to manager risk, which is the chance that poor security selection will cause the Fund to underperform relevant benchmarks or other funds with a similar investment objective.

| Plain Talk About Credit Quality |

| A money market instrument’s credit quality is an assessment of the issuer’s ability |

| to pay interest and, ultimately, to repay the principal. The lower the credit quality, |

| the greater the chance—in Vanguard’s opinion—that the issuer will default, or fail to |

| meet its payment obligations. Direct U.S. Treasury obligations, along with other |

| securities backed by the “full faith and credit” of the U.S. government, generally are |

| determined to have the highest credit quality. All things being equal, money market |

| instruments with greater credit risk offer higher yields. |

The Fund invests in high-quality, short-term money market instruments, including certificates of deposit, banker’s acceptances, commercial paper, and other money market securities. To be considered high quality, a security must be determined by Vanguard to present minimal credit risk based in part on a consideration of maturity, portfolio diversification, portfolio liquidity, and credit quality. The Fund also invests in short-term corporate, state, and municipal obligations that are considered high quality.

The Fund is subject to industry concentration risk, which is the chance that the Fund‘s performance will be significantly affected, for better or for worse, by developments in the financial services industry.

10

More than 25% of the Fund’s assets are invested in securities issued by companies in the financial services industry, such as U.S. and foreign banks, insurance companies, real estate-related companies (i.e., companies having at least 50% of their assets, revenues, or net income related to, or derived from, the real estate industry), securities firms, leasing companies, and other companies principally engaged in providing financial services to consumers and industry. These investments include, among others, bank obligations, high-quality asset-backed securities, and securities issued by the automobile finance industry. Changes in economic, regulatory, and political conditions that affect financial services companies could have a significant effect on the Fund. These conditions include changes in interest rates and defaults in payments by borrowers.

The Fund may also invest in Eurodollar and Yankee obligations, which include certificates of deposit issued in U.S. dollars by foreign banks and foreign branches of U.S. banks. Eurodollar and Yankee obligations have the same risks, such as income risk and credit risk, as those of U.S. money market instruments. Other risks of Eurodollar and Yankee obligations include the chance that a foreign government will not let U.S. dollar-denominated assets leave the country, the chance that the banks that issue Eurodollar obligations will not be subject to the same regulations as U.S. banks, and the chance that adverse political or economic developments will affect investments in a foreign country. Before the Fund’s advisor selects a Eurodollar or Yankee obligation, however, any foreign issuer undergoes the same credit-quality analysis and tests of financial strength as those for the issuers of domestic securities.

The Fund is subject, to a limited extent, to credit risk, which is the chance that the issuer of a security will fail to pay interest or principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that security to decline. Credit risk should be very low for the Fund because it invests primarily in securities that are considered to be of high quality.

11

| Plain Talk About U.S. Government-Sponsored Entities |

| A variety of U.S. government-sponsored entities (GSEs), such as the Federal |

| Home Loan Mortgage Corporation (FHLMC), the Federal National Mortgage |

| Association (FNMA), and the Federal Home Loan Banks (FHLBs), issue debt and |

| mortgage-backed securities. Although GSEs may be chartered or sponsored by |

| acts of Congress, they are not funded by congressional appropriations. In |

| September of 2008, the U.S. Treasury placed FNMA and FHLMC under |

| conservatorship and appointed the Federal Housing Finance Agency (FHFA) to |

| manage their daily operations. In addition, the U.S. Treasury entered into |

| purchase agreements with FNMA and FHLMC to provide them with capital in |

| exchange for senior preferred stock. Generally, their securities are neither issued |

| nor guaranteed by the U.S. Treasury and are not backed by the full faith and credit |

| of the U.S. government. In most cases, these securities are supported only by |

| the credit of the GSE, standing alone. In some cases, a GSE’s securities may be |

| supported by the ability of the GSE to borrow from the U.S. Treasury or may be |

| supported by the U.S. government in some other way. Securities issued by the |

| Government National Mortgage Association (GNMA), however, are backed by the |

| full faith and credit of the U.S. government. |

Overall, the Fund’s credit quality is considered to be very high. However, because the Fund invests a portion of its assets in money market securities issued by private companies, it is possible that one or more of these companies may experience financial difficulties and, as a result, may fail to pay interest to the Fund or fail to return the Fund’s principal when repayment is due. Bear in mind that although the Fund invests in high-quality money market instruments, the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other agency of the U.S. government.

The Fund reserves the right to invest in repurchase agreements, which are subject to specific risks.

| Plain Talk About Repurchase Agreements |

| Repurchase agreements are contracts in which a bank or securities dealer sells |

| government securities and agrees to repurchase the securities on a specific date |

| (normally the next business day) at a specific price. |

12

Repurchase agreements carry several risks. For instance, if the seller is unable to repurchase the securities as promised, the Fund may experience a loss when trying to sell the securities to another buyer. Also, if the seller becomes insolvent, a bankruptcy court may determine that the securities do not belong to the Fund and order that the securities be used to pay off the seller’s debts. The Fund‘s advisor believes that these risks can be controlled through careful security and counterparty selection and monitoring.

The Fund reserves the right to invest, to a limited extent, in adjustable-rate securities, which are a type of derivative.

An adjustable-rate security’s interest rate, as the name implies, is not set; instead, it fluctuates periodically. Generally, the security’s yield is based on a U.S. dollar-based interest-rate benchmark such as the federal funds rate, the 90-day U.S. Treasury bill rate, or the London Interbank Offered Rate (LIBOR). Adjustable-rate securities reset their yields on a periodic basis (e.g., daily, weekly, or quarterly) or upon a change in the benchmark interest rate. These yields are closely correlated to changes in money market interest rates.

The Fund will not use derivatives for speculation or for the purpose of leveraging (magnifying) investment returns.

| Plain Talk About Derivatives |

| A derivative is a financial contract whose value is based on the value of a financial |

| asset (such as a stock, a bond, or a currency), a money market benchmark (such |

| as U.S. Treasury bill rates or the federal funds effective rate), a physical asset |

| (such as gold, oil, or wheat), a market index (such as the Barclays U.S. Aggregate |

| Bond Index), or a reference rate (such as LIBOR). |

In addition, the Fund may invest up to 5% of its net assets in illiquid securities. Illiquid securities are securities that the Fund may not be able to sell within seven days in the ordinary course of business at approximately the price at which they are valued.

13

| Plain Talk About Weighted Average Maturity and Weighted Average Life |

| A money market fund will maintain a dollar-weighted average maturity (WAM) of 60 |

| days or less and a dollar-weighted average life (WAL) of 120 days or less. For |

| purposes of calculating a fund’s WAM, the maturity of certain longer-term |

| adjustable-rate securities held in the portfolio will generally be the period remaining |

| until the next interest rate adjustment. When calculating its WAL, the maturity for |

| these adjustable-rate securities will generally be the final maturity date—the date |

| on which principal is expected to be returned in full. Maintaining a WAL of 120 days |

| or less limits a fund’s ability to invest in longer-term adjustable-rate securities, |

| which are generally more sensitive to changes in interest rates, particularly in |

| volatile markets. |

Temporary Investment Measures

The Fund may temporarily depart from its normal investment policies and strategies—for instance, by allocating substantial assets to cash equivalent investments—in response to adverse or unusual market, economic, political, or other conditions. In doing so, the Fund may succeed in avoiding losses but may otherwise fail to achieve its investment objective.

| Plain Talk About Cash Equivalent Investments |

| For mutual funds that hold cash equivalent investments, “cash” does not mean |

| literally that the fund holds a stack of currency. Rather, cash refers to short-term, |

| interest-bearing securities that can easily and quickly be converted to currency. |

Frequent Trading or Market-Timing

Vanguard anticipates that shareholders will purchase and sell shares of money market funds frequently because these funds are designed to offer investors a liquid investment. For this reason, the board of trustees of the Fund has determined that it is not necessary to adopt policies and procedures designed to detect and deter frequent trading and market-timing in the money market fund shares. For information on frequent-trading limits of other Vanguard funds, please see the appropriate fund’s prospectus.

14

The Fund and Vanguard

The Vanguard Group is a family of more than 190 mutual funds holding assets of approximately $3.3 trillion. All of the funds that are members of The Vanguard Group (other than funds of funds) share in the expenses associated with administrative services and business operations, such as personnel, office space, and equipment. The Fund is not a member of The Vanguard Group but is administered by Vanguard and pays Vanguard a fee to provide management, advisory, marketing, accounting, transfer agency, and other services.

Investment Advisor

The Vanguard Group, Inc., P.O. Box 2600, Valley Forge, PA 19482, which began operations in 1975, serves as advisor to the Fund through its Fixed Income Group. As of June 30, 2016, Vanguard served as advisor for approximately $2.7 trillion in assets.

The Fund has two agreements with Vanguard.

Management and Distribution Agreement. Vanguard serves as the Fund’s advisor and provides a range of administrative services to the Fund under the terms of the Management and Distribution Agreement. As part of this agreement, the Fund pays Vanguard monthly on an at-cost basis.

Shareholder Services Agreement. Vanguard provides a range of transfer agency and shareholder services to the Fund under the terms of the Shareholder Services Agreement. As part of this agreement, the Fund pays Vanguard monthly on an at-cost basis.

For the fiscal year ended August 31, 2015, the amounts paid to Vanguard represented an effective annual rate of less than 0.01% of the Fund’s average net assets.

For a discussion of why the board of trustees approved the Fund’s investment advisory arrangement, see the most recent annual report to shareholders covering the fiscal year ended August 31.

The manager primarily responsible for the day-to-day management of the Fund is:

John C. Lanius, Portfolio Manager at Vanguard. He has been with Vanguard since 1996, has worked in investment management since 1997, has managed investment portfolios since 2004, and has managed the Fund since 2006. Education: B.A., Middlebury College.

The Statement of Additional Information provides information about the portfolio manager’s compensation, other accounts under management, and ownership of shares of the Fund.

15

Dividends and Taxes

Fund Distributions

The Fund distributes to shareholders virtually all of its net income (interest less expenses). The Fund may also realize capital gains from the sale of its holdings and distribute these gains (net of losses) to shareholders as capital gains distributions. As a money market fund, the Fund’s distributions are expected to consist primarily of income dividends. The Fund’s income dividends generally are declared daily and distributed monthly. In addition, the Fund may occasionally make a supplemental distribution at some other time during the year. You can receive your income distributions in cash, or you can have them automatically reinvested in more shares of the Fund.

Basic Tax Points

Vanguard will send you a statement each year showing the tax status of all of your distributions. In addition, investors in taxable accounts should be aware of the following basic federal income tax points:

• Distributions are taxable to you whether or not you reinvest these amounts in additional Fund shares.

• Distributions declared in December—if paid to you by the end of January—are taxable as if received in December.

• Any income dividend distribution or short-term capital gains distribution that you receive is taxable to you as ordinary income.

• Any distribution of net long-term capital gains is taxable to you as long-term capital gains, no matter how long you have owned shares in the Fund. Because of the short-term nature of the Fund’s holdings, the Fund generally does not expect to make distributions of net long-term capital gains.

• Because the Fund will transition to a floating NAV on or before October 14, 2016, a sale or exchange of Fund shares at or after that time may result in a capital gain or loss for you. This means that you may have a capital gain to report as income, or a capital loss to report as a deduction, when you complete your tax return. The Fund’s Statement of Additional Information contains more information regarding the different methods available to you for calculating this gain or loss.

Individuals, trusts, and estates whose income exceeds certain threshold amounts are subject to a 3.8% Medicare contribution tax on “net investment income.” Net investment income takes into account distributions paid by the Fund and capital gains from any sale or exchange of Fund shares.

16

Income dividends and capital gains distributions that you receive, as well as your gains or losses from any sale or exchange of fund shares, may be subject to state and local income taxes. Depending on your state’s rules, however, any dividends attributable to interest earned on direct obligations of the U.S. government may be exempt from state and local taxes. Vanguard will notify you each year how much, if any, of your dividends may qualify for this exemption.

This prospectus provides general tax information only. Please consult your tax advisor for detailed information about any tax consequences for you.

General Information

Backup withholding. By law, Vanguard must withhold 28% of any taxable distributions or redemptions from your account if you do not:

• Provide us with your correct taxpayer identification number.

• Certify that the taxpayer identification number is correct.

• Confirm that you are not subject to backup withholding.

Similarly, Vanguard must withhold taxes from your account if the IRS instructs us to do so.

Foreign investors. Vanguard funds offered for sale in the United States (Vanguard U.S. funds), including the Fund offered in this prospectus, are not widely available outside the United States. Non-U.S. investors should be aware that U.S. withholding and estate taxes and certain U.S. tax reporting requirements may apply to any investments in Vanguard U.S. funds. Foreign investors should visit the Non-U.S. Investors page on our website at vanguard.com for information on Vanguard’s non-U.S. products.

Invalid addresses. If an income dividend distribution or capital gains distribution check mailed to your address of record is returned as undeliverable, Vanguard will automatically reinvest the distribution and all future distributions until you provide us with a valid mailing address. Reinvestments will receive the net asset value calculated on the date of the reinvestment.

Share Price

Share price, also known as net asset value (NAV), is calculated each business day as of the close of regular trading on the New York Stock Exchange (NYSE), generally 4 p.m., Eastern time. The NAV per share is computed by dividing the total assets, minus liabilities, of the Fund by the number of Fund shares outstanding. On U.S. holidays or other days when the NYSE is closed, the NAV is not calculated, and the Fund does not sell or redeem shares.

17

Debt securities held by a Vanguard fund are valued based on information furnished by an independent pricing service or market quotations. Certain short-term debt instruments used to manage a fund’s cash may be valued at amortized cost when it approximates fair value. The values of any mutual fund shares held by a fund are based on the NAVs of the shares. The values of any ETF or closed-end fund shares held by a fund are based on the market value of the shares.

When a fund determines that pricing-service information or market quotations either are not readily available or do not accurately reflect the value of the security, the security is priced at its fair value (the amount that the owner might reasonably expect to receive upon the current sale of the security). A fund also may use fair-value pricing on bond market holidays when the fund is open for business (such as Columbus Day and Veterans Day).

Fair-value prices are determined by Vanguard according to procedures adopted by the board of trustees. When fair-value pricing is employed, the prices of securities used by a fund to calculate the NAV may differ from quoted or published prices for the same securities.

The NAV of Vanguard retail and government money market funds is expected to remain relatively stable. Instruments are purchased and managed with that goal in mind.

Vanguard fund share prices are published daily; share prices, along with money market fund yields, are available on our website at vanguard.com/prices.

18

Financial Highlights

The following financial highlights table is intended to help you understand the Fund’s financial performance for the periods shown, and certain information reflects financial results for a single Fund share. The total returns in the table represent the rate that an investor would have earned or lost each period on an investment in the Fund (assuming reinvestment of all distributions). The information for the six-month period ended February 29, 2016, has not been audited by an independent registered public accounting firm. The information for all periods in the table through August 31, 2015, has been obtained from the financial statements audited by PricewaterhouseCoopers LLP, an independent registered public accounting firm, whose report—along with the Fund’s financial statements—is included in the Fund’s most recent annual report to shareholders. You may obtain a free copy of the latest annual or semiannual report by contacting Vanguard by telephone or mail.

| Plain Talk About How to Read the Financial Highlights Table |

| The Fund began the fiscal period ended February 29, 2016, with a net asset value |

| (share price) of $1.00 per share. During the period, the Fund earned $0.002 per |

| share from investment income (interest). Shareholders received $0.002 per share |

| in the form of dividend distributions. |

| The earnings ($0.002 per share) minus the distributions ($0.002 per share) |

| resulted in a share price of $1.00 at the end of the period. For a shareholder who |

| reinvested the distributions in the purchase of more shares, the total return was |

| 0.15% for the period. |

| As of February 29, 2016, the Fund had approximately $42 billion in net assets. For |

| the period, its expense ratio was 0.005% ($0.05 per $1,000 of net assets), and its |

| net investment income amounted to 0.30% of its average net assets. |

19

| Market Liquidity Fund | ||||||

| Six Months | ||||||

| Ended | Year Ended August 31, | |||||

| For a Share Outstanding Throughout | February 29, | |||||

| Each Period | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 |

| Net Asset Value, Beginning of Period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Investment Operations | ||||||

| Net Investment Income | .002 | .001 | .001 | .001 | .001 | .002 |

| Net Realized and Unrealized Gain (Loss) | ||||||

| on Investments | — | — | — | — | — | — |

| Total from Investment Operations | .002 | .001 | .001 | .001 | .001 | .002 |

| Distributions | ||||||

| Dividends from Net Investment Income | (.002) | (.001) | (.001) | (.001) | (.001) | (.002) |

| Distributions from Realized Capital Gains | — | — | — | — | — | — |

| Total Distributions | (.002) | (.001) | (.001) | (.001) | (.001) | (.002) |

| Net Asset Value, End of Period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total Return | 0.15% | 0.13% | 0.12% | 0.15% | 0.14% | 0.20% |

| Ratios/Supplemental Data | ||||||

| Net Assets, End of Period (Millions) | $41,511 | $47,040 | $37,202 | $28,103 $32,648 | $27,384 | |

| Ratio of Total Expenses to Average | ||||||

| Net Assets | 0.005% | 0.005% | 0.005% | 0.005% | 0.005% | 0.005% |

| Ratio of Net Investment Income to | ||||||

| Average Net Assets | 0.30% | 0.13% | 0.12% | 0.15% | 0.14% | 0.19% |

| The expense ratio and net income ratio for the current period have been annualized. | ||||||

20

Investing With Vanguard

Vanguard Market Liquidity Fund has been established by Vanguard as a cash management vehicle for the Vanguard funds and certain trusts and accounts managed by Vanguard or its affiliates. The Fund is not available to other investors. Upon transition to a floating NAV on or before October 14, 2016, subscription orders in Vanguard Market Liquidity Fund will only be able to be placed in dollars, while redemption orders can be placed in units or dollars. Vanguard reserves the right to change the availability of Vanguard Market Liquidity Fund or offer additional funds at any time without prior notice to shareholders.

Purchases, redemptions, and exchanges of shares issued by Vanguard Market Liquidity Fund are conducted by Vanguard or its affiliates on behalf of the participating funds, trusts, and accounts based on a determination of the participant’s daily cash management requirements. There is no minimum amount required to open, to maintain, or to add to an existing account.

In all cases, transactions will be based on the Fund’s next-determined net asset value (NAV) after Vanguard receives the request (or, in the case of new contributions, the next-determined NAV after Vanguard receives the order). As long as this request is received before the close of regular trading on the New York Stock Exchange (generally 4 p.m., Eastern time), the investor will receive that business day’s NAV. This is known as the trade date. Transaction requests received after that time receive a trade date of the first business day following the date of receipt. The trade date may vary depending on the method of payment for the transaction.

Portfolio Holdings

Please consult the Fund’s Statement of Additional Information or our website for a description of the policies and procedures that govern disclosure of the Fund’s portfolio holdings.

| Additional Information | |||

| Inception | Vanguard | CUSIP | |

| Date | Fund Number | Number | |

| Market Liquidity Fund | 7/19/2004 | 1142 | 92202X209 |

21

Glossary of Investment Terms

Cash Equivalent Investments. Cash deposits, short-term bank deposits, and money market instruments that include U.S. Treasury bills and notes, bank certificates of deposit (CDs), repurchase agreements, commercial paper, and banker’s acceptances.

Dividend Distribution. Payment to mutual fund shareholders of income from interest or dividends generated by a fund’s investments.

Expense Ratio. A fund’s total annual operating expenses expressed as a percentage of the fund’s average net assets. The expense ratio includes management and administrative expenses, but it does not include the transaction costs of buying and selling portfolio securities.

Floating Net Asset Value (NAV). A share price that fluctuates in response to the current market-based value of the securities in a fund's underlying portfolio.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is generally measured from the inception date.

Money Market Instruments. Short-term, liquid investments (usually with a maturity of 397 days or less) that include U.S. Treasury bills and notes, bank certificates of deposit (CDs), repurchase agreements, commercial paper, and banker’s acceptances.

Mutual Fund. An investment company that pools the money of many people and invests it in a variety of securities in an effort to achieve a specific objective over time.

Principal. The face value of a debt instrument or the amount of money put into an investment.

Securities. Stocks, bonds, money market instruments, and other investments.

Stable Net Asset Value (NAV). A share price that maintains a consistent value (e.g., $1.00 or $100.00) using special pricing and valuation conventions.

Total Return. A percentage change, over a specified time period, in a mutual fund’s net asset value, assuming the reinvestment of all distributions of dividends and capital gains.

Volatility. The fluctuations in value of a mutual fund or other security. The greater a fund’s volatility, the wider the fluctuations in its returns.

Yield. Income (interest or dividends) earned by an investment, expressed as a percentage of the investment’s price.

22

This page intentionally left blank.

This page intentionally left blank.

This page intentionally left blank.

Institutional Division P.O. Box 2900 Valley Forge, PA 19482-2900

| Connect with Vanguard® > vanguard.com | |

| For More Information | If you are a client of Vanguard’s Institutional Division: |

| If you would like more information about Vanguard | The Vanguard Group |

| Market Liquidity Fund, the following documents are | Institutional Investor Information Department |

| available free upon request: | P.O. Box 2900 |

| Valley Forge, PA 19482-2900 | |

| Annual/Semiannual Reports to Shareholders | |

| Telephone: 888-809-8102; Text telephone for people | |

| Additional information about the Fund’s investments is | |

| with hearing impairment: 800-749-7273 | |

| available in the Fund’s annual and semiannual reports | |

| to shareholders. In the annual report, you will find a | If you are a current Vanguard shareholder and would |

| discussion of the market conditions and investment | like information about your account, account |

| policies that significantly affected the Fund’s | transactions, and/or account statements, please call: |

| performance during its last fiscal year. | |

| Client Services Department | |

| Statement of Additional Information (SAI) | Telephone: 800-662-2739; Text telephone for people |

| The SAI provides more detailed information about the Fund | with hearing impairment: 800-749-7273 |

| and is incorporated by reference into (and thus legally | |

| Information Provided by the Securities and | |

| a part of) this prospectus. | |

| Exchange Commission (SEC) | |

| To receive a free copy of the latest annual or semiannual | You can review and copy information about the Fund |

| report or the SAI, or to request additional information about | (including the SAI) at the SEC’s Public Reference Room |

| the Fund or other Vanguard funds, please visit | in Washington, DC. To find out more about this public |

| vanguard.com or contact us as follows: | service, call the SEC at 202-551-8090. Reports and |

| other information about the Fund are also available in | |

| If you are an individual investor: | |

| the EDGAR database on the SEC’s website at | |

| The Vanguard Group | |

| www.sec.gov, or you can receive copies of this | |

| Investor Information Department | |

| information, for a fee, by electronic request at the | |

| P.O. Box 2900 | |

| following email address: [email protected], or by | |

| Valley Forge, PA 19482-2900 | |

| writing the Public Reference Section, Securities and | |

| Telephone: 800-662-7447; Text telephone for people | |

| Exchange Commission, Washington, DC 20549-1520. | |

| with hearing impairment: 800-749-7273 | |

| Fund’s Investment Company Act file number: 811-21478 | |

© 2016 The Vanguard Group, Inc. All rights reserved. Vanguard Marketing Corporation, Distributor.

I 1142 082016

![]()

| Vanguard Municipal Cash Management Fund |

| Prospectus |

| August 12, 2016 |

| Investor Shares |

| Vanguard Municipal Cash Management Fund |

| This prospectus contains financial data for the Fund through the fiscal period ended February 29, 2016. |

| The Securities and Exchange Commission (SEC) has not approved or disapproved these securities or |

| passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense. |

| Contents | |||

| Fund Summary | 1 | Financial Highlights | 17 |

| Investing in Tax-Exempt Funds | 5 | Investing With Vanguard | 19 |

| Investing in Money Market Funds | 6 | Glossary of Investment Terms | 20 |

| More on the Fund | 8 | ||

| The Fund and Vanguard | 12 | ||

| Investment Advisor | 13 | ||

| Dividends and Taxes | 13 | ||

| Share Price | 16 | ||

Fund Summary

Investment Objective

The Fund seeks to provide current income that is exempt from federal personal income taxes, while maintaining liquidity.

Fees and Expenses

The following table describes the fees and expenses you may pay if you buy and hold shares of the Fund.

| Shareholder Fees | |

| (Fees paid directly from your investment) | |

| Sales Charge (Load) Imposed on Purchases | None |

| Purchase Fee | None |

| Sales Charge (Load) Imposed on Reinvested Dividends | None |

| Redemption Fee | None |

| Annual Fund Operating Expenses | |

| (Expenses that you pay each year as a percentage of the value of your investment) | |

| Management Fees | 0.01% |

| 12b-1 Distribution Fee | None |

| Other Expenses | None |

| Total Annual Fund Operating Expenses | 0.01% |

Example

The following example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. It illustrates the hypothetical expenses that you would incur over various periods if you invested $10,000 in the Fund’s shares. This example assumes that the Fund provides a return of 5% each year and that total annual fund operating expenses remain as stated in the preceding table. You would incur these hypothetical expenses whether or not you redeem your investment at the end of the given period. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years |

| $1 | $3 | $6 | $13 |

1

Principal Investment Policies

The Fund invests in a variety of high-quality, short-term municipal securities. To be considered high quality, a security must be determined by Vanguard to present minimal credit risk based in part on a consideration of maturity, portfolio diversification, portfolio liquidity, and credit quality. The Fund invests in securities with effective maturities of 397 days or less and maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less. As a matter of fundamental policy, the Fund will invest at least 80% of its assets in tax-exempt municipal bonds (including securities that may be subject to alternative minimum tax) under normal market conditions.

Principal Risks

Effective on or before October 14, 2016, the Fund, as an institutional money market fund, will be required to transition to a floating net asset value (NAV) as a result of the SEC’s money market fund reforms. The Fund is designed for investors with a low tolerance for risk; however, the Fund is subject to the following risks, which could affect the Fund’s performance:

• Income risk, which is the chance that the Fund’s income will decline because of falling interest rates. Because the Fund’s income is based on short-term interest rates—which can fluctuate significantly over short periods—income risk is expected to be high.

• Credit risk, which is the chance that the issuer of a security will fail to pay interest or principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that security to decline. Credit risk should be very low for the Fund because it invests primarily in securities that are considered to be of high quality.

• Manager risk, which is the chance that poor security selection will cause the Fund to underperform relevant benchmarks or other funds with a similar investment objective.

A sale or exchange of Fund shares is a taxable event. This means that you may have a capital gain to report as income, or a capital loss to report as a deduction, when you complete your tax return.

You could lose money by investing in the Fund. Because the share price of the Fund will fluctuate, when you sell your shares they may be worth more or less than what you originally paid for them. The Fund may impose a fee upon sale of your shares or may temporarily suspend your ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you

2

should not expect that the sponsor will provide financial support to the Fund at any time.

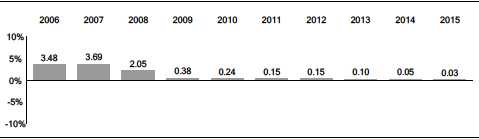

Annual Total Returns

The following bar chart and table are intended to help you understand the risks of investing in the Fund. The bar chart shows how the performance of the Fund has varied from one calendar year to another over the periods shown. The table shows how the average annual total returns of the Fund compare with those of a comparative benchmark, which has investment characteristics similar to those of the Fund. Returns for the Tax-Exempt Money Market Funds Average are derived from data provided by Lipper, a Thomson Reuters Company. Keep in mind that the Fund’s past performance does not indicate how the Fund will perform in the future. Updated performance information is available on our website at vanguard.com/performance or by calling Vanguard toll-free at 800-662-7447.

Annual Total Returns — Vanguard Municipal Cash Management Fund Investor Shares1

The year-to-date return as of the most recent calendar quarter, which ended on June 30, 2016, was 0.11%.

During the periods shown in the bar chart, the highest return for a calendar quarter was 0.94% (quarter ended June 30, 2007), and the lowest return for a quarter was 0.01% (quarter ended March 31, 2015).

| Average Annual Total Returns for Periods Ended December 31, 2015 | |||

| 1 Year | 5 Years | 10 Years | |

| Vanguard Municipal Cash Management Fund Investor Shares | 0.03% | 0.10% | 1.02% |

| Tax-Exempt Money Market Funds Average | 0.01% | 0.01% | 0.75% |

3

Investment Advisor

The Vanguard Group, Inc. (Vanguard)

Portfolio Manager

Justin A. Schwartz, CFA, Portfolio Manager at Vanguard. He has managed the Fund since 2010.

Purchase and Sale of Fund Shares

The Fund has been established by Vanguard as a cash management vehicle for the Vanguard funds and certain trusts and accounts managed by Vanguard or its affiliates. The Fund is not available to other investors. Upon transition to a floating NAV on or before October 14, 2016, subscription orders in the Fund will only be able to be placed in dollars, while redemption orders can be placed in units or dollars.

Tax Information

The Fund’s distributions may be taxable as ordinary income or capital gain. A majority of the income dividends that you receive from the Fund are expected to be exempt from federal income taxes. However, a portion of the Fund’s distributions may be subject to federal, state, or local income taxes or the federal alternative minimum tax.

Payments to Financial Intermediaries

The Fund and its investment advisor do not pay financial intermediaries for sales of Fund shares.

4

Investing in Tax-Exempt Funds

What Are Municipal Bond Funds?

Municipal bond funds invest primarily in interest-bearing securities issued by state and local governments and by other governmental authorities to support their needs or to finance public projects. A municipal bond—like a bond issued by a corporation or the U.S. government—obligates the issuer to pay the bondholder a fixed or variable amount of interest periodically and to repay the principal value of the bond on a specific maturity date. Unlike most other bonds, however, municipal bonds generally pay interest that is exempt from federal income taxes and, in some cases, from state and local taxes. For certain shareholders, the interest may be subject to the alternative minimum tax.

Taxable Versus Tax-Exempt Funds

Yields on tax-exempt bonds—such as some municipal bonds—are typically lower than those on taxable bonds, so investing in a tax-exempt fund makes sense only if you stand to save more in taxes than you would earn as additional income while invested in a taxable fund.

To determine whether a tax-exempt fund—such as Vanguard Municipal Cash Management Fund—makes sense for you, compute the tax-exempt fund’s taxable-equivalent yield. This figure enables you to take taxes into account when comparing your potential return on a tax-exempt fund with the potential return on a taxable fund.

To compute the taxable-equivalent yield, divide the tax-exempt fund’s yield by the difference between 100% and your federal tax bracket. For example, if you are in a 35% federal tax bracket, and assuming that you are considering a tax-exempt fund with a 5% yield, your taxable-equivalent yield would be 7.69% (5% divided by [100%–35%]).

In this example, you would choose the tax-exempt fund if its taxable-equivalent yield of 7.69% were greater than the yield of a similar, though taxable, investment.

Remember that we have used an assumed tax bracket in this example. Make sure to verify your actual tax bracket before calculating taxable-equivalent yields of your own.

There is no guarantee that all of a tax-exempt fund’s income from its municipal bonds will remain exempt from federal, state, or local income taxes. Income from municipal bonds held by a fund could be declared taxable, possibly with retroactive effect, because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service (IRS) or state or local tax authorities, or noncompliant conduct of a bond issuer.

5

Investing in Money Market Funds

What is Money Market Reform?

In July 2014, the Securities and Exchange Commission (SEC) implemented a number of regulatory changes designed to enhance the stability and resilience of all money market funds. The reforms have created three categories of money market funds:

• Retail money market funds, which may maintain a stable net asset value (NAV) but are subject to liquidity fees and redemption gates.

• Government money market funds, which may maintain a stable NAV but are not required to implement liquidity fees and redemption gates.

• Institutional money market funds, which are required to have a floating NAV and are subject to liquidity fees and redemption gates.

The board of trustees of Vanguard Municipal Cash Management Fund (the Board), in accordance with the best interest of the shareholders, approved a number of changes in response to the SEC’s 2014 amendments to the rules governing money market funds. The changes will become effective on or before October 14, 2016 (Compliance Date). Additional approvals are expected to be made, as needed, on or before the Compliance Date.

How Does This Affect Vanguard Money Market Funds?

The money market fund reforms adopted by the SEC in July 2014 will take effect during 2015 and 2016 on or before the Compliance Date. The reforms will impact money market funds differently depending on the types of investors permitted to invest in the fund and the types of securities in which the fund may invest.

Vanguard Municipal Cash Management Fund

Vanguard has designated Vanguard Municipal Cash Management Fund as a institutional money market fund.

Institutional money market funds are not limited to “natural persons” and may be held by institutional as well as retail investors. An institutional money market fund generally will no longer be permitted to use amortized cost or penny rounding methods to calculate NAV. Rather, an institutional money market fund will be required to transact at a market-based NAV calculated to four decimal places (i.e., at a floating NAV). If an institutional money market fund’s weekly liquid assets fall below a certain threshold, institutional money market funds are subject to fees and gates.

6

There are two types of liquidity fees: discretionary liquidity fees and default liquidity fees.

Discretionary liquidity fee. The Fund may impose a liquidity fee of up to 2% on all redemptions in the event that the Fund’s weekly liquid assets fall below 30% of its total assets if the Board determines that it is in the best interest of the Fund. Once the Fund has restored its weekly liquidity asset to 30% of total assets, any liquidity fee must be suspended.

Default liquidity fee. The Fund is required to impose a liquidity fee of 1% on all redemptions in the event that the Fund’s weekly liquid assets fall below 10% of its total assets unless the Fund’s Board determines that (1) the fee is not in the best interest of the Fund or (2) a lesser/higher fee (up to 2%) is in the best interest of the Fund.

In addition to, or in lieu of, the liquidity fee, the Fund is permitted to implement temporarily a redemption gate (i.e., suspend redemptions) if the Fund’s weekly liquid assets fall below 30% of its total assets. The gate could remain in effect for no longer than 10 days in any 90-day period. Once the Fund has restored its weekly liquidity assets to 30% of total assets, the gate must be lifted.

The Fund is subject to money market fund reform regulatory risk, which is the chance that 2014 SEC reforms will affect the Fund’s investment strategy, fees and expenses, portfolio, share liquidity, and return potential as the rules are implemented in 2015 and 2016.

7

More on the Fund

This prospectus describes the principal risks you would face as a Fund shareholder. It is important to keep in mind one of the main axioms of investing: generally, the higher the risk of losing money, the higher the potential reward. The reverse, also, is generally true: the lower the risk, the lower the potential reward. As you consider an investment in any mutual fund, you should take into account your personal tolerance for fluctuations in the securities markets. Look for this

symbol throughout the prospectus. It is used to mark detailed information about the more significant risks that you would confront as a Fund shareholder. To highlight terms and concepts important to mutual fund investors, we have provided Plain Talk® explanations along the way. Reading the prospectus will help you decide whether the Fund is the right investment for you. We suggest that you keep this prospectus for future reference.

symbol throughout the prospectus. It is used to mark detailed information about the more significant risks that you would confront as a Fund shareholder. To highlight terms and concepts important to mutual fund investors, we have provided Plain Talk® explanations along the way. Reading the prospectus will help you decide whether the Fund is the right investment for you. We suggest that you keep this prospectus for future reference.

Vanguard Municipal Cash Management Fund has been established by Vanguard as a cash management vehicle for the Vanguard funds and certain trusts and accounts managed by Vanguard or its affiliates. The Fund is not available to other investors. Vanguard reserves the right to change the availability of the Fund at any time without prior notice to shareholders. The Fund operates under an exemption issued by the SEC.

A Similar But Distinct Vanguard Fund

The Fund offered by this prospectus should not be confused with Vanguard Tax-Exempt Money Market Fund, a separate Vanguard fund available only to retail investors that has a similar investment objective and similar policies but seeks to maintain a stable net asset value. The respective municipal securities held by the funds will differ. The funds’ holdings, combined with differences in the funds’ respective cash flows and expenses, are expected to produce different investment performances. Although Vanguard Municipal Cash Management Fund has lower expenses, investors should not expect this Fund necessarily to outperform Vanguard Tax-Exempt Money Market Fund.

Vanguard Tax-Exempt Money Market Fund offers its shares through a separate prospectus. To obtain the prospectus for that fund, please call 800-662-7447.

| Plain Talk About Fund Expenses |

| All mutual funds have operating expenses. These expenses, which are deducted |

| from a fund’s gross income, are expressed as a percentage of the net assets of |

| the fund. Assuming that operating expenses remain as stated in the Fees and |

| Expenses section, Vanguard Municipal Cash Management Fund’s expense ratio |

| would be 0.01%, or $0.10 per $1,000 of average net assets. The average expense |

| ratio for tax-exempt money market funds in 2015 was 0.09%, or $0.90 per $1,000 |

| of average net assets (derived from data provided by Lipper, a Thomson Reuters |

| Company, which reports on the mutual fund industry). |

8

| Plain Talk About Costs of Investing |

| Costs are an important consideration in choosing a mutual fund. That is because |

| you, as a shareholder, pay a proportionate share of the costs of operating a fund, |

| plus any transaction costs incurred when the fund buys or sells securities. These |

| costs can erode a substantial portion of the gross income or the capital |

| appreciation a fund achieves. Even seemingly small differences in expenses can, |

| over time, have a dramatic effect on a fund‘s performance. |

The following sections explain the principal investment policies that the Fund uses in pursuit of its objective. The Fund’s board of trustees, which oversees the Fund’s management, may change investment policies in the interest of shareholders without a shareholder vote, unless those policies are designated as fundamental. Note that the Fund’s investment objective is not fundamental and may be changed without a shareholder vote.

Market Exposure

The Fund invests mainly in state and local municipal securities that provide tax-exempt income. As a result, it is subject to certain risks.

The Fund is subject to income risk, which is the chance that the Fund’s income will decline because of falling interest rates. A fund’s income declines when interest rates fall because the fund then must invest new cash flow and cash from maturing instruments in lower-yielding instruments. Because the Fund’s income is based on short-term interest rates—which can fluctuate significantly over short periods—income risk is expected to be high.

A low interest rate environment could adversely affect the Fund’s return. Low interest rates could prevent the Fund from providing a positive yield.

The Fund is subject to credit risk, which is the chance that the issuer of a security will fail to pay interest or principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that security to decline. Credit risk should be very low for the Fund because it invests primarily in securities that are considered to be of high quality.

The Fund tries to minimize credit risk by purchasing a wide selection of municipal securities. As a result, there is less chance that the Fund will be seriously affected by a particular bond issuer’s failure to pay either interest or principal.

9

| Plain Talk About Credit Quality |

| A money market instrument’s credit quality is an assessment of the issuer’s ability |

| to pay interest and, ultimately, to repay the principal. The lower the credit quality, |

| the greater the chance—in Vanguard’s opinion—that the issuer will default, or fail to |

| meet its payment obligations. Direct U.S. Treasury obligations, along with other |

| securities backed by the “full faith and credit” of the U.S. government, generally are |

| determined to have the highest credit quality. All things being equal, money market |

| instruments with greater credit risk offer higher yields. |

Up to 100% of the Fund’s assets may be invested in securities that are subject to the alternative minimum tax (AMT).

| Plain Talk About Alternative Minimum Tax |

| Certain tax-exempt bonds whose proceeds are used to fund private, for-profit |

| organizations may be considered “tax-preference items” for purposes of the |

| alternative minimum tax (AMT)—a special tax system designed to ensure that |

| individuals pay at least a certain level of federal taxes. Although AMT bond |

| income is exempt from federal income tax, taxpayers may have to pay AMT on |

| the income from bonds considered “tax-preference items.” |

Security Selection

The Vanguard Group, Inc. (Vanguard), advisor to the Fund, uses a top-down investment management approach to select a variety of high-quality, short-term municipal securities. This means that the advisor sets, and periodically adjusts, a duration target for the Fund based upon expectations about the direction of interest rates and other economic factors. The advisor then buys and sells securities to achieve the greatest relative value within the Fund’s targeted duration.

The Fund is subject to manager risk, which is the chance that poor security selection will cause the Fund to underperform relevant benchmarks or other funds with a similar investment objective.

The Fund invests in securities with effective maturities of 397 days or less and maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less.

10

| Plain Talk About Weighted Average Maturity and Weighted Average Life |

| A money market fund will maintain a dollar-weighted average maturity (WAM) of 60 |

| days or less and a dollar-weighted average life (WAL) of 120 days or less. For |

| purposes of calculating a fund’s WAM, the maturity of certain longer-term |

| adjustable-rate securities held in the portfolio will generally be the period remaining |

| until the next interest rate adjustment. When calculating its WAL, the maturity for |

| these adjustable-rate securities will generally be the final maturity date—the date |

| on which principal is expected to be returned in full. Maintaining a WAL of 120 days |

| or less limits a fund’s ability to invest in longer-term adjustable-rate securities, |

| which are generally more sensitive to changes in interest rates, particularly in |

| volatile markets. |

Other Investment Policies and Risks

In addition to investing in municipal securities, the Fund may make other kinds of investments to achieve its objective.

The Fund may purchase tax-exempt securities on a “when-issued” basis. When investing in “when-issued” securities, the Fund agrees to buy the securities at a certain price, even if the market price of the securities at the time of delivery is higher or lower than the agreed-upon purchase price.

The Fund may invest in derivatives. In general, investments in derivatives may involve risks different from, and possibly greater than, those of investments directly in the underlying securities or assets.

The Fund may invest in derivative securities that, in the advisor’s opinion, are consistent with the Fund’s objective of producing current tax-exempt income while maintaining liquidity. The Fund intends to use derivatives to increase diversification while maintaining its quality standards. There are many types of derivatives, including those in which the tax-exempt interest rate is determined by reference to an index or swap agreement or by some other formula.

In addition, the Fund may invest in tender option bond programs, a type of municipal bond derivative that allows the purchaser to receive a variable rate of tax-exempt income from a trust entity that holds long-term municipal bonds. Derivative securities are subject to certain structural risks that, in unexpected circumstances, could cause the Fund’s shareholders to lose money or receive taxable income.

11

| Plain Talk About Derivatives |

| A derivative is a financial contract whose value is based on the value of a financial |

| asset (such as a stock, a bond, or a currency), a money market benchmark (such |

| as U.S. Treasury bill rates or the federal funds effective rate), a physical asset |

| (such as gold, oil, or wheat), a market index (such as the Barclays U.S. Aggregate |

| Bond Index), or a reference rate (such as LIBOR). |

Temporary Investment Measures

The Fund may temporarily depart from its normal investment policies and strategies—for instance, by allocating substantial assets to cash equivalent investments, U.S. Treasury securities, or other taxable securities—in response to adverse or unusual market, economic, political, or other conditions. Such conditions could include a temporary decline in the availability of municipal money market obligations. By temporarily departing from its normal investment policies, the Fund may distribute income subject to federal personal income tax and may otherwise fail to achieve its investment objective.

| Plain Talk About Cash Equivalent Investments |

| For mutual funds that hold cash equivalent investments, “cash” does not mean |

| literally that the fund holds a stack of currency. Rather, cash refers to short-term, |

| interest-bearing securities that can easily and quickly be converted to currency. |

Frequent Trading or Market-Timing

Vanguard anticipates that shareholders will purchase and sell shares of money market funds frequently because these funds are designed to offer investors a liquid investment. For this reason, the board of trustees of the Fund has determined that it is not necessary to adopt policies and procedures designed to detect and deter frequent trading and market-timing in the money market fund shares. For information on frequent-trading limits of other Vanguard funds, please see the appropriate fund’s prospectus.

The Fund and Vanguard

The Vanguard Group is a family of more than 190 mutual funds holding assets of approximately $3.3 trillion. All of the funds that are members of The Vanguard Group (other than funds of funds) share in the expenses associated with administrative services and business operations, such as personnel, office space, and equipment. The Fund is not a member of The Vanguard Group but is administered by Vanguard

12

and pays Vanguard a fee to provide management, advisory, marketing, accounting, transfer agency, and other services.

Investment Advisor

The Vanguard Group, Inc., P.O. Box 2600, Valley Forge, PA 19482, which began operations in 1975, serves as advisor to the Fund through its Fixed Income Group. As of June 30, 2016, Vanguard served as advisor for approximately $2.7 trillion in assets.

The Fund has two agreements with Vanguard.

Management and Distribution Agreement. Vanguard serves as the Fund’s advisor and provides a range of administrative services to the Fund under the terms of the Management and Distribution Agreement. As part of this agreement, the Fund pays Vanguard monthly on an at-cost basis.

Shareholder Services Agreement. Vanguard provides a range of transfer agency and shareholder services to the Fund under the terms of the Shareholder Services Agreement. As part of this agreement, the Fund pays Vanguard monthly on an at-cost basis.

For the fiscal year ended August 31, 2015, the amounts paid to Vanguard represented an effective annual rate of less than 0.01% of the Fund’s average net assets.

For a discussion of why the board of trustees approved the Fund’s investment advisory arrangement, see the most recent annual report to shareholders covering the fiscal year ended August 31.

The manager primarily responsible for the day-to-day management of the Fund is: